Business Planning Lecture 11 Ch 18- 19 Payman Shafiee

Business Planning Lecture 11 Ch 18- 19 Payman Shafiee.

Dec 16, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Business PlanningLecture 11Ch 18- 19

Payman Shafiee

Evaluating strategic options

Evaluating and ultimately choosing the best strategic option is an art as much as it is a science and ultimately based on experience and instinct.

QUALITATIVE EVALUATION OF STRATEGIC CHOICEConsistencyValidityFeasibilityBusiness riskFlexibility

Accounting principles

ConsistencyStrategic alternatives must be consistent with

achieving the business’s vision, mission and goals.

ValidityThe assumptions behind the strategic options

must be valid. These assumptions may include the future business environment, the competition, customers and suppliers and how they will react to alternative strategies. i.e. A strategic option that involves lowering prices but does not recognise

the possibility that competitors may lower their prices may not be valid.

Accounting principles

FeasibilityA strategy may, in theory, be capable of delivering

the business’s vision, mission and goals, but in practice it must also be feasible. In other words, the business must have (or be capable of acquiring) the financing, resources, assets, experience, culture and skills to carry it out.

Business riskReturn on investment is related to risk, and all

strategic options carry some form of risk. They should also include ways of minimising the potential risk. The evaluation should aim to determine whether the residual risk of a strategic option is at a level commensurate with the anticipated return.

Accounting principles

FlexibilityIn today’s rapidly changing business world, a

strategy must have enough flexibility to work if circumstances change. If it can be broken down into a series of options that can be chosen, depending on circumstances, this is a considerable advantage.

EVALUATING THE BUSINESS DESIGN

The business design defines how the business makes profit. The design must be customer centric, focused on sustainable profitability and internally consistent.

the four strategic components of a business design:

Customer selection Value captureStrategic controlScope Slides by

Payman Shafiee

BUSINESS VALUATIONS

Providers of equity capital to a business want to see an increase in the value of their investment. The future value of the business’s equity under each strategic option should be calculated. This is done is by assessing the trade-off between the risks of a particular strategy and the anticipated returns.

Limitations: the underlying forecast on which it is based and the assumptions used in the chosen valuation technique

LIMITATIONS OF BUSINESS VALUATIONS

the underlying forecast on which it is based and the assumptions used in the chosen valuation technique.

Valuationsare based on cash flows, and what is included in

the cash flows will determine whether an enterprise or an equity value is calculated.

Enterprise value If the cash flows used are before the payment of interest

charges, they represent the monies that will ultimately flow to the providers of debt (via interest and principal repayments) and the providers of equity (via dividends). These cash flows represent the flow of cash to all providers of capital to the enterprise

LIMITATIONS OF BUSINESS VALUATIONS

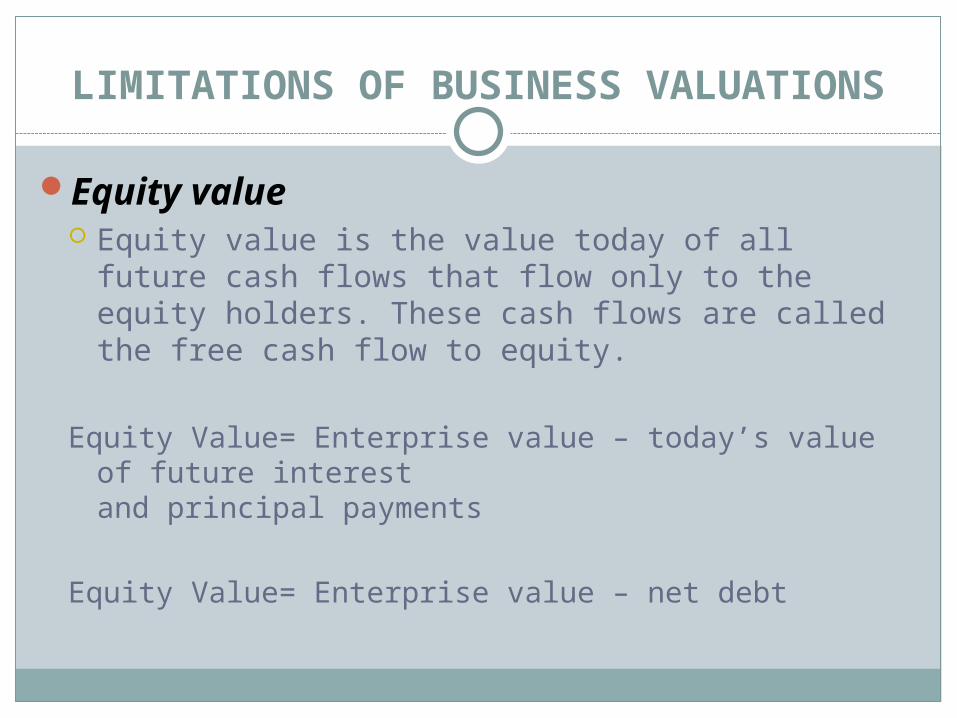

Equity value Equity value is the value today of all future cash

flows that flow only to the equity holders. These cash flows are called the free cash flow to equity.

Equity Value= Enterprise value – today’s value of future interest and principal payments

Equity Value= Enterprise value – net debt

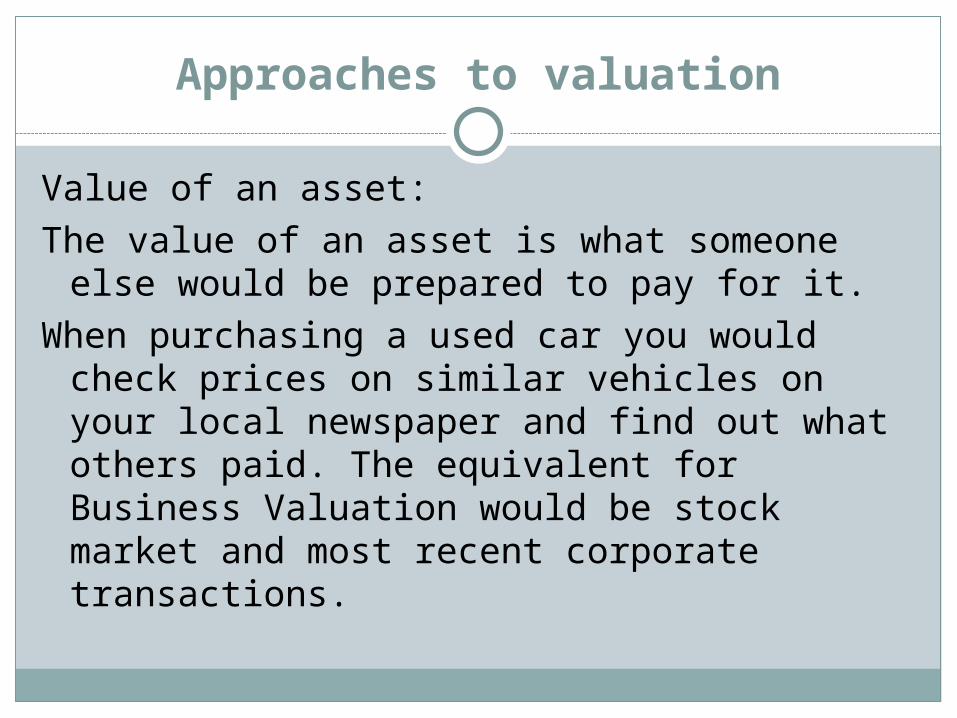

Approaches to valuation

Value of an asset: The value of an asset is what someone else

would be prepared to pay for it.When purchasing a used car you would check

prices on similar vehicles on your local newspaper and find out what others paid. The equivalent for Business Valuation would be stock market and most recent corporate transactions.

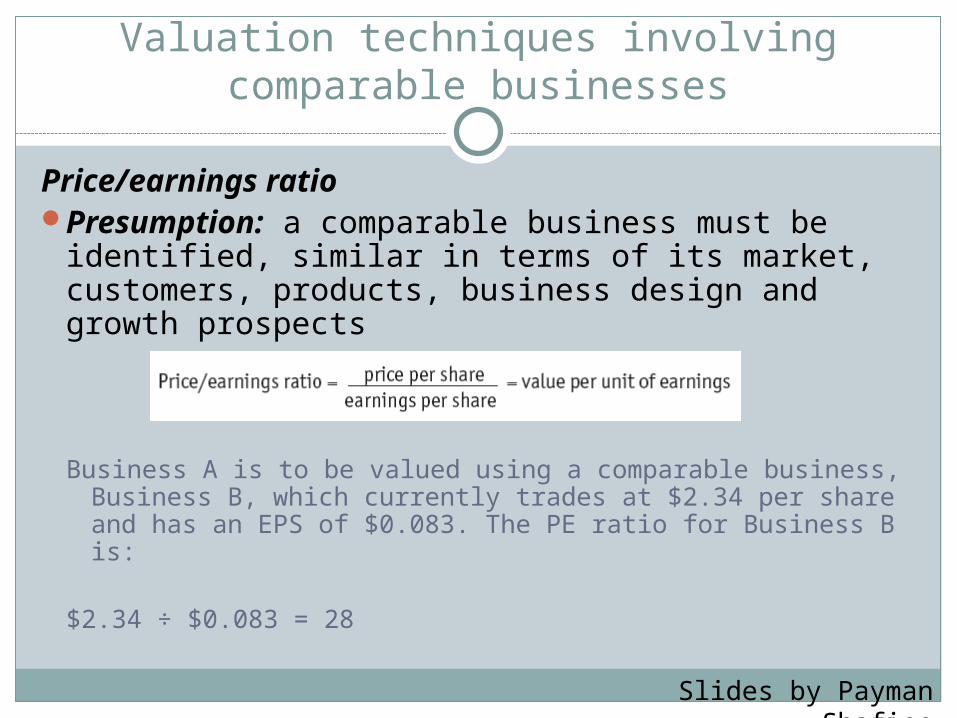

Valuation techniques involving comparable businesses

Price/earnings ratioPresumption: a comparable business must be

identified, similar in terms of its market, customers, products, business design and growth prospects

Business A is to be valued using a comparable business, Business B, which currently trades at $2.34 per share and has an EPS of $0.083. The PE ratio for Business B is:

$2.34 ÷ $0.083 = 28

Slides by Payman Shafiee

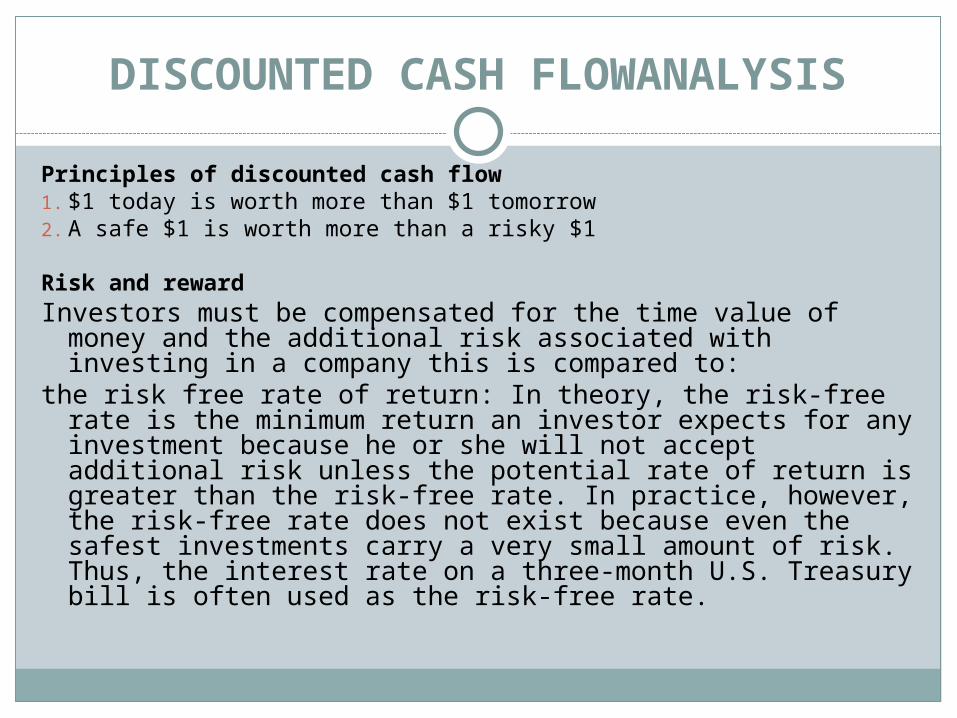

DISCOUNTED CASH FLOWANALYSIS

Principles of discounted cash flow1. $1 today is worth more than $1 tomorrow2. A safe $1 is worth more than a risky $1

Risk and rewardInvestors must be compensated for the time value of money

and the additional risk associated with investing in a company this is compared to:

the risk free rate of return: In theory, the risk-free rate is the minimum return an investor expects for any investment because he or she will not accept additional risk unless the potential rate of return is greater than the risk-free rate. In practice, however, the risk-free rate does not exist because even the safest investments carry a very small amount of risk. Thus, the interest rate on a three-month U.S. Treasury bill is often used as the risk-free rate.

the risk premium

Defined as the additional return to compensate for the extra risk associated with an investment. This is called the risk premium.

Funding issues

TYPES OF FINANCE: Debt and Equity Finance

Debt finance Debt finance can be obtained from a number of sources

but is often provided by a bank requires a business to pay an agreed, regular interest

charge The interest charges have to be paid irrespective of

the business’s performance Interest payments can be charged in the profit and

loss account and so can reduce a business’s tax liability

Funding issues

Equity finance The shareholders of a business (who can range from private

individuals to large institutions) provide equity finance Equity also includes any retained profits of the business Equity shares, unlike debt, represent ownership of a

business Unlike interest, dividends are paid after tax and are a

less tax efficient form of financing Shareholders right: In the event of liquidation,

shareholders only have a claim on what is left after all other creditors have been satisfied

the providers of equity take the highest risk of all finance providers

Slides by Payman Shafiee

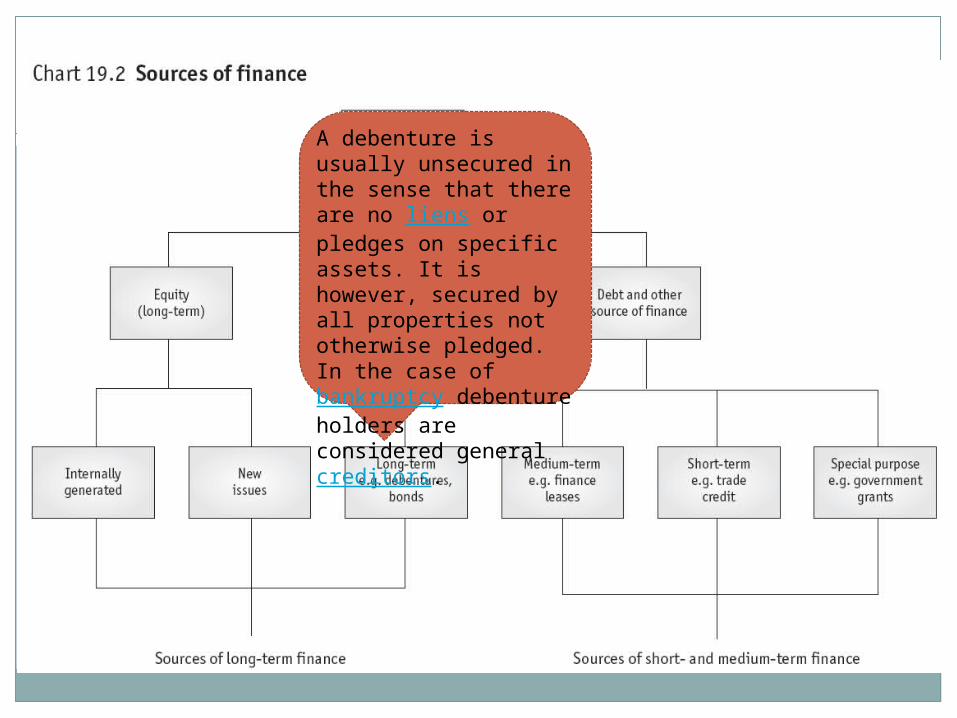

A debenture is usually unsecured in the sense that there are no liens or pledges on specific assets. It is however, secured by all properties not otherwise pledged. In the case of bankruptcy debenture holders are considered general creditors.

TERM OF DEBT

short, medium and long term definition can vary depending on the nature of the business

short term – up to 1 year; medium term – 1–10 years; long term – more than 10 years

Different forms of equity

An equity share represents a share of a business’s assets and also a share of any profits it generates. There are different classes of equity, each with different

rights that relate to dividends, voting and the return of capital in the event of liquidation Ordinary shares Preferred ordinary shares Non-voting shares

Slides by Payman Shafiee

Different forms of equity

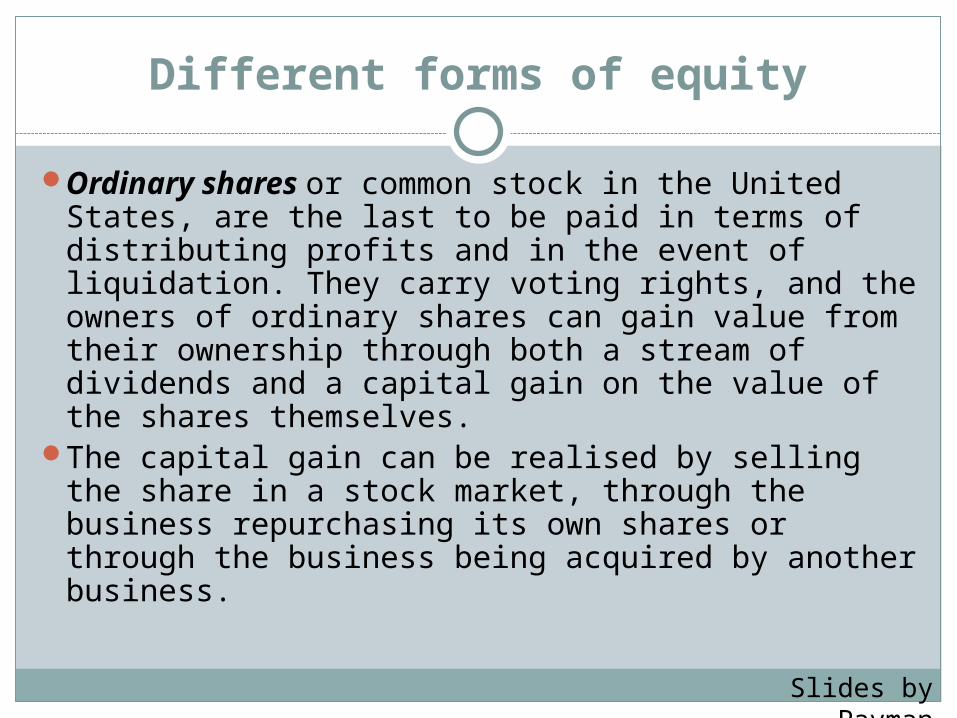

Ordinary shares or common stock in the United States, are the last to be paid in terms of distributing profits and in the event of liquidation. They carry voting rights, and the owners of ordinary shares can gain value from their ownership through both a stream of dividends and a capital gain on the value of the shares themselves.

The capital gain can be realised by selling the share in a stock market, through the business repurchasing its own shares or through the business being acquired by another business.

Slides by Payman Shafiee

Different forms of equity

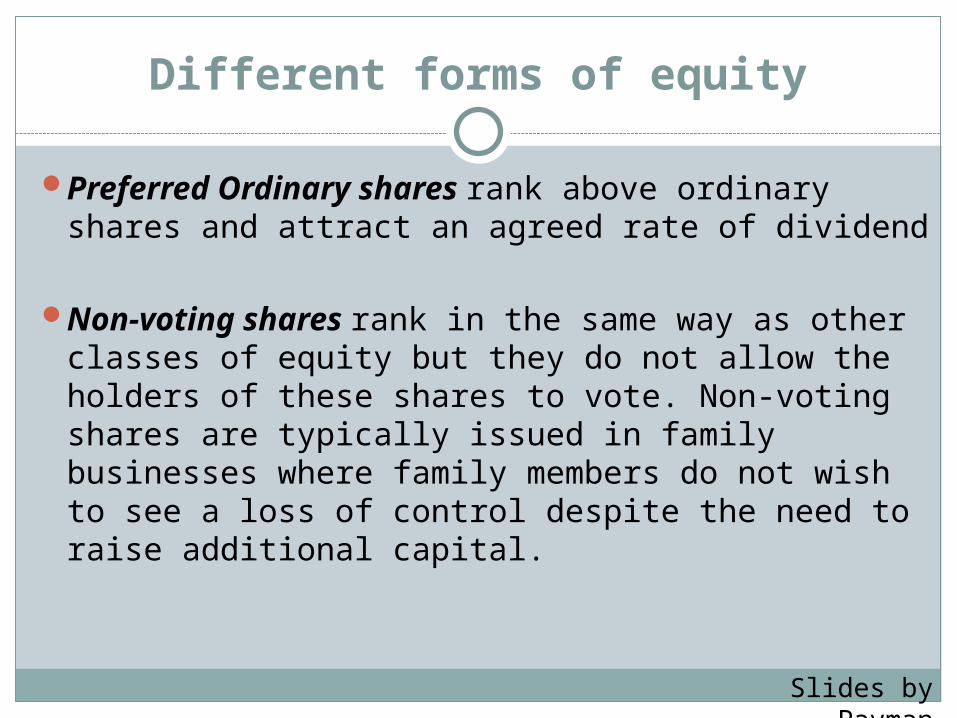

Preferred Ordinary shares rank above ordinary shares and attract an agreed rate of dividend

Non-voting shares rank in the same way as other classes of equity but they do not allow the holders of these shares to vote. Non-voting shares are typically issued in family businesses where family members do not wish to see a loss of control despite the need to raise additional capital.

Slides by Payman Shafiee

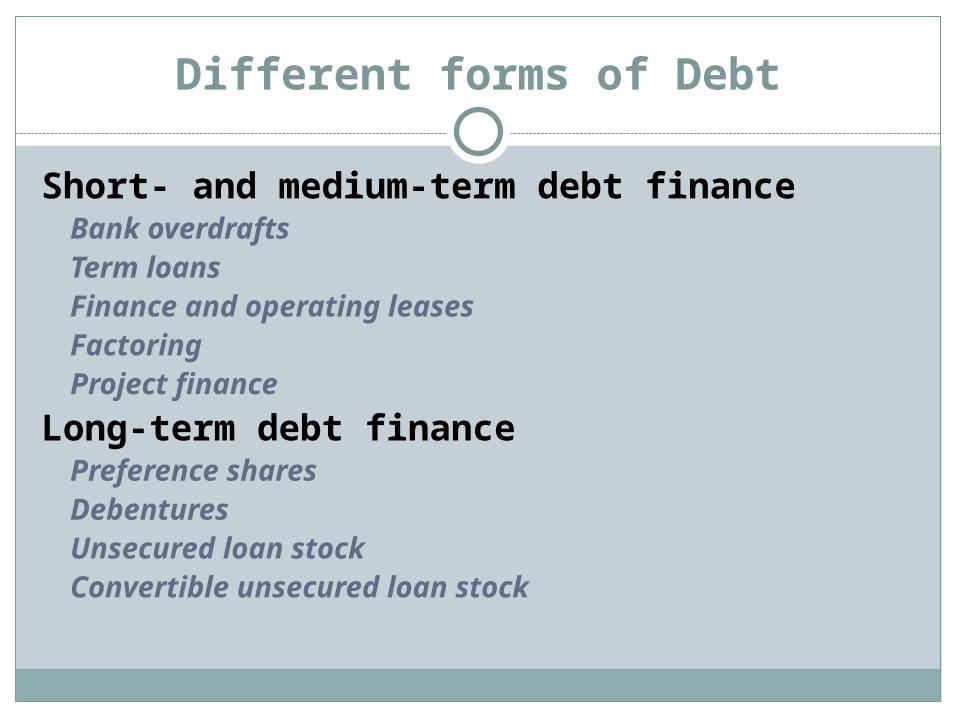

Different forms of Debt

Short- and medium-term debt financeBank overdraftsTerm loansFinance and operating leasesFactoringProject finance

Long-term debt financePreference sharesDebenturesUnsecured loan stockConvertible unsecured loan stock

Other features of debt instruments

Fixed and floating ratesRedeemable and irredeemableCoupon ratesDeep discounting

Deeply discounted loans have a low coupon rate at issue and are issued at prices considerably below par or the face value of the loan

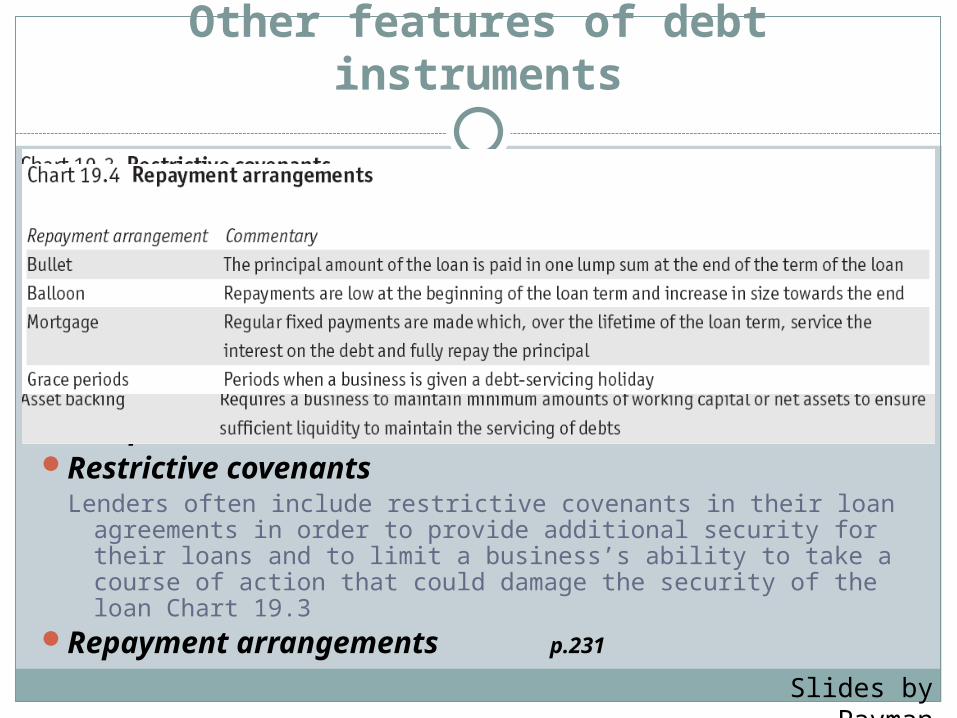

Call provisionsRestrictive covenants

Lenders often include restrictive covenants in their loan agreements in order to provide additional security for their loans and to limit a business’s ability to take a course of action that could damage the security of the loan Chart 19.3

Repayment arrangements p.231

Slides by Payman Shafiee

Related Documents