Business Optimism Index Kuwait Q1 2010 Presented by Dun & Bradstreet South Asia Middle East Ltd (D&B) Muthanna Investment Company (MIC)

Business Optimism Index Kuwait Q1 2010 Presented by Dun & Bradstreet South Asia Middle East Ltd (D&B) Muthanna Investment Company (MIC)

Dec 14, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Business Optimism Index Kuwait Q1 2010

Presented by Dun & Bradstreet South Asia Middle East Ltd (D&B) Muthanna Investment Company (MIC)

Business Optimism Index

• The D&B Business Optimism Index is recognized world over as an

indicator which ascertains the pulse of the business community

• Provides insight into the short-term outlook of businesses on sales,

profit growth, investment etc

• Provides analysis of major trends, outlook and issues concerning

businesses

• Sample of business units representing Kuwait’s economy was selected

• 500 business owners and senior executives across business units were

surveyed

• Survey conducted during December 2009 for the 1st quarter of 2010

• Respondents are asked questions about their expectations on relevant

business parameters

• Survey also captures respondent feedback on current business

conditions

Survey

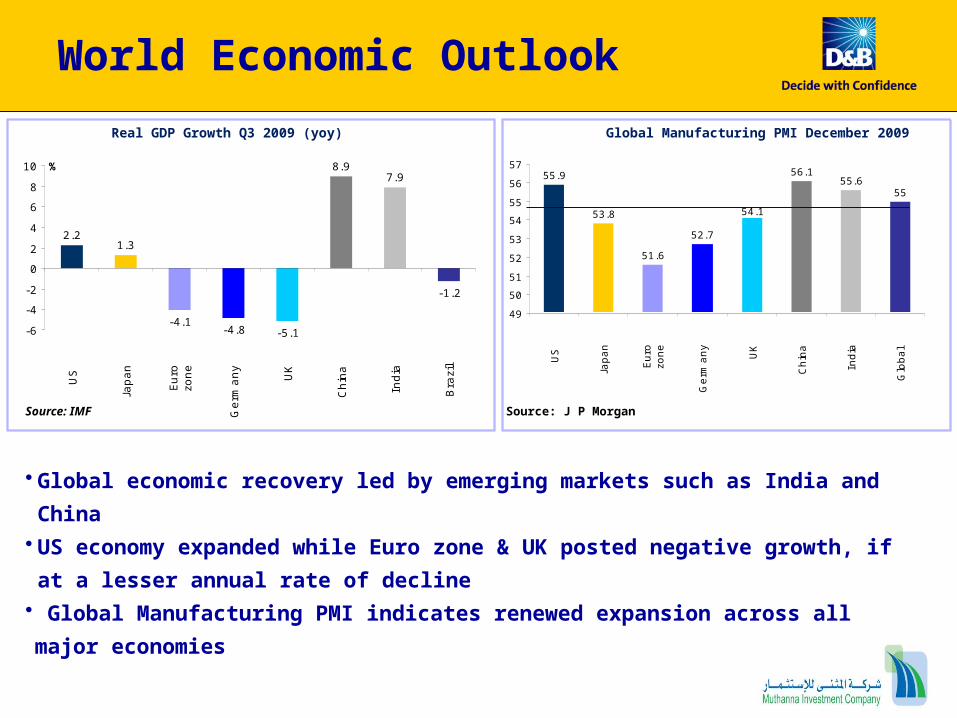

World Economic Outlook

• Global economic recovery led by emerging markets such as India and China• US economy expanded while Euro zone & UK posted negative growth, if at a lesser

annual rate of decline• Global Manufacturing PMI indicates renewed expansion across all major economies

Real GDP Growth Q3 2009 (yoy) Global Manufacturing PMI December 2009

2.21.3

-4.1-4.8 -5.1

8.97.9

-1.2

-6

-4

-2

0

2

4

6

8

10

US

Japan

Euro

zone

Germ

any

UK

Chin

a

India

Bra

zil

%55.9

53.8

51.6

52.7

56.155.6

55

54.1

49

50

51

52

53

54

55

56

57

US

Jap

an

Eu

rozo

ne

Ge

rma

ny

UK

Ch

ina

Ind

ia

Glo

ba

l

Source: IMF Source: J P Morgan

Kuwait’s economy

Source: IMF

• Kuwait’s GDP to register a growth rate of 3.2% after contracting by 1.6% in 2009; Non-oil GDP to grow at 4.1% in 2010

• Recovery in the oil prices has helped Kuwait post a budget surplus of US$ 22 bn for the first eight months of the fiscal year

Source: OPEC

2500

22762247 2254 2257 2274 2279

2100

2150

2200

2250

2300

2350

2400

2450

2500

2550

Q4 2008 Q1 2009 Q2 2009 Q3 2009 Sep-09 Oct-09 Nov-09

'000

bp

d

Crude oil production

GDP Outlook

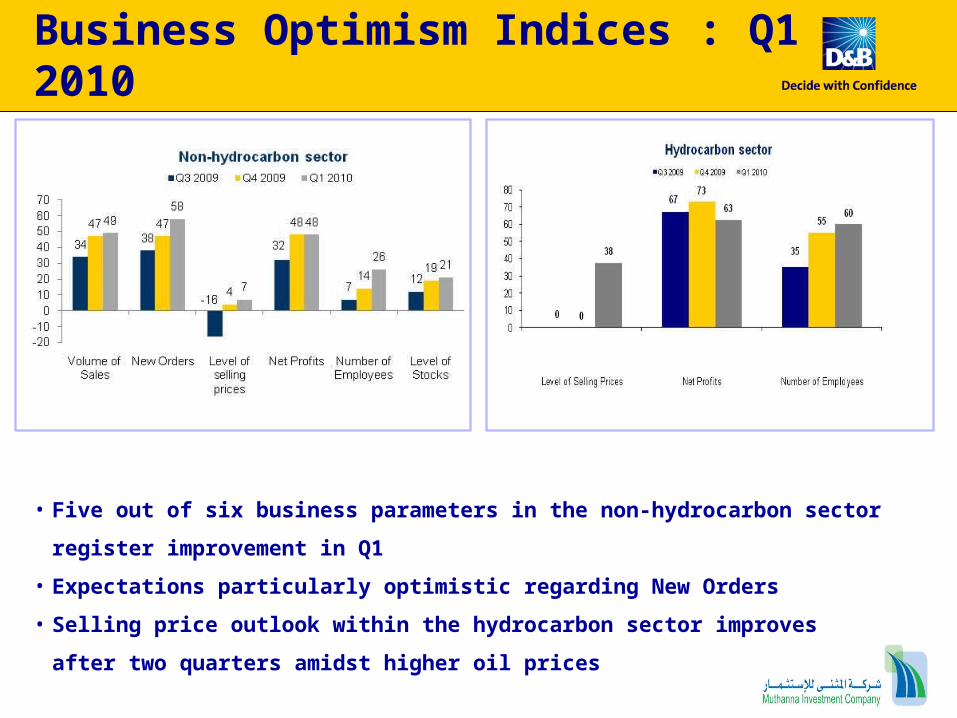

Business Optimism Indices : Q1 2010

• Five out of six business parameters in the non-hydrocarbon sector register

improvement in Q1

• Expectations particularly optimistic regarding New Orders

• Selling price outlook within the hydrocarbon sector improves after two quarters

amidst higher oil prices

Business Optimism Indices Trend

33

-23

3447

49

-30

-20

-10

0

10

20

30

40

50

60

Q1 2009 Q2 2009 Q3 2009 Q4 2009 Q1 2010

BO

I Ind

ex

Volume of Sales

40

-22

3847

58

-30

-20

-10

0

10

20

30

40

50

60

70

Q1 2009 Q2 2009 Q3 2009 Q4 2009 Q1 2010B

OI I

ndex

New Orders

7

-26

-16

47

-30

-25

-20

-15

-10

-5

0

5

10

Q1 2009 Q2 2009 Q3 2009 Q4 2009 Q1 2010

BO

I Ind

ex

Level of Selling Prices

35

-15

32

48

48

-20

-10

0

10

20

30

40

50

60

Q1 2009 Q2 2009 Q3 2009 Q4 2009 Q1 2010

BO

I Ind

ex

Net Profits

31

-7

7

14

26

-10

-5

0

5

10

15

20

25

30

35

Q1 2009 Q2 2009 Q3 2009 Q4 2009 Q1 2010

BO

I Ind

ex

Number of Employees

21

2

12

19

21

0

10

20

30

Q1 2009 Q2 2009 Q3 2009 Q4 2009 Q1 2010

BO

I Ind

ex

Level of Stock

3036

-27

30

-3

10

42 39

7

42

7

2935

55

12

3730

6

-30

-20

-10

0

10

20

30

40

50

60

Volume of Sales New Orders Level of Selling Prices

Net Profits Number of Employees

Level of Stock

Inde

x

Q3 2009 Q4 2009 Q1 2010

Se

p-0

8

Oc

t-0

8

No

v-0

8

De

c-0

8

Ja

n-0

9

Fe

b-0

9

Ma

r-0

9

Ap

r-0

9

Ma

y-0

9

Ju

n-0

9

Ju

l-0

9

Au

g-0

9

Se

p-0

9

Oc

t-0

9

No

v-0

9

De

c-0

9

30.0

35.0

40.0

45.0

50.0

55.0

44.7

41.0

36.5

33.2

35.0

35.8

37.3

41.8

45.346.9

50.0

53.1

53.0

54.4

53.7

55.0

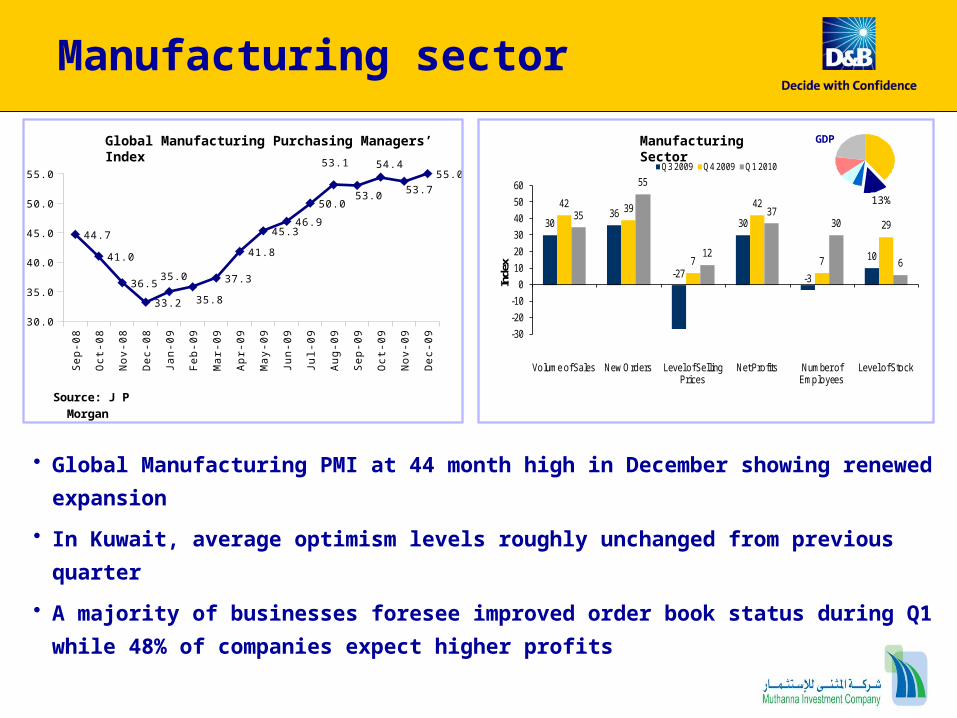

Source: J P Morgan

Manufacturing sector

• Global Manufacturing PMI at 44 month high in December showing renewed expansion

• In Kuwait, average optimism levels roughly unchanged from previous quarter

• A majority of businesses foresee improved order book status during Q1 while 48% of

companies expect higher profits

13%

Global Manufacturing Purchasing Managers’ Index Manufacturing Sector GDP

2722

-31

25

-235

47

36

8

47

16 18

4250

35

44 47 45

-40

-30

-20

-10

0

10

20

30

40

50

60

Volume of Sales New Orders Level of Selling Prices

Net Profits Number of Employees

Level of Stock

Inde

x

Q3 2009 Q4 2009 Q1 2010

• Global construction sector currently driven by infrastructure spending as commercial

property undergoes correction

• In Kuwait, optimism regarding New Orders, Level of Selling Prices, Number of

Employees and Level of Stock parameters improve substantially in Q1 2010

Construction sector

5%

GDPResidential construction outlook 2008-13Compound annual growth (%)

Construction Sector

26 28

-14

24

1522

4650

-27

46

05

43

53

-9

30

56

42

-40

-30

-20

-10

0

10

20

30

40

50

60

70

Volume of Sales New Orders Level of Selling Prices

Net Profits Number of Employees

Level of Stock

Ind

ex

Q3 2009 Q4 2009 Q1 2010

Trade, restaurants & hotels sector

• Global trade & hospitality sector is expected to pick up in 2010, but recovery will

be slow as consumers confidence remains weak

• In Kuwait, the sales and profitability outlook has weakened in Q1 2010 while order

book expectations and hiring plans have firmed

8%

GDPTrade, restaurants & hotels sector

2533

-10

22

12

51 53

13

51

20

60

73

2

59 60

-20

-10

0

10

20

30

40

50

60

70

80

Volume of Sales New Orders Level of Selling Prices

Net Profits Number of Employees

Ind

ex

Q3 2009 Q4 2009 Q1 2010 12%

• Global transport & communications sector expected to witness gradual recovery in 2010

• In Kuwait, expectations of higher sales lift profitability outlook

• Meanwhile, a surge in new orders is leading to increased hiring

Transport & communications sector

Transport & communications sector GDP

Finance, insurance, real estate & business services sector

• The Global Services PMI recovery has leveled out following extended recovery

• Kuwait’s service sector bullish about demand with increased optimism regarding

Volume of Sales and New Orders

23%GDP

Global Services Purchasing Managers' IndexFinance & Business Services

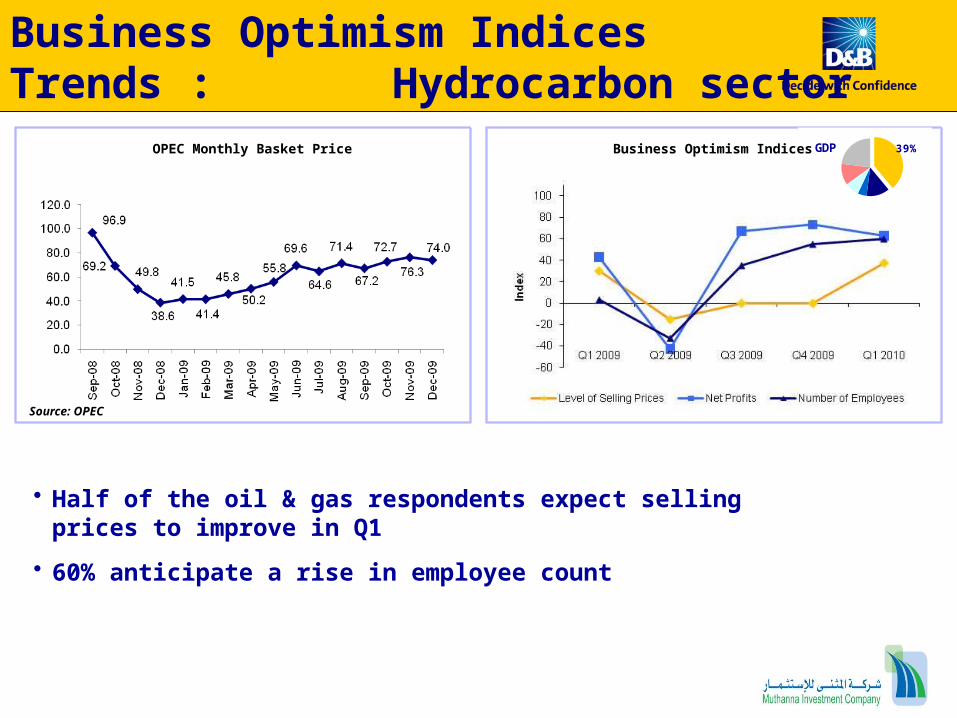

Business Optimism Indices Trends : Hydrocarbon sector

• Half of the oil & gas respondents expect selling prices to improve in Q1

• 60% anticipate a rise in employee count

GDP 39%

Source: OPEC

OPEC Monthly Basket Price Business Optimism Indices

Other Key Highlights

• Availability of finance and direct costs cited as leading

business concerns by the non-hydrocarbon sector

• 41% of the business units freeze investment outlays while

38% to invest in business expansion

• 45% of the business units in the non-hydrocarbon sector

expect borrowing conditions to remain unchanged

• Project delays identified as the chief concern by 69% of the

units in the hydrocarbon sector

Conclusion

• Business outlook for Q1 2010 improves across all sectors with

improved global economic condition

• Optimism in transport & communications sector stronger as

international trade outlook is expected to improve further in

2010

• Improving liquidity in the international financial markets lifts

optimism levels in Finance & business services sector

• Hydrocarbon sector optimistic on the back of strong oil prices

and improving demand conditions

THANK YOU

Related Documents