LGU Taxation and Revenue Practices DEPARTMENT OF FINANCE BUREAU OF LOCAL GOVERNMENT FINANCE

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

LGU Taxation and

Revenue Practices

DEPARTMENT OF FINANCE

BUREAU OF LOCAL GOVERNMENT FINANCE

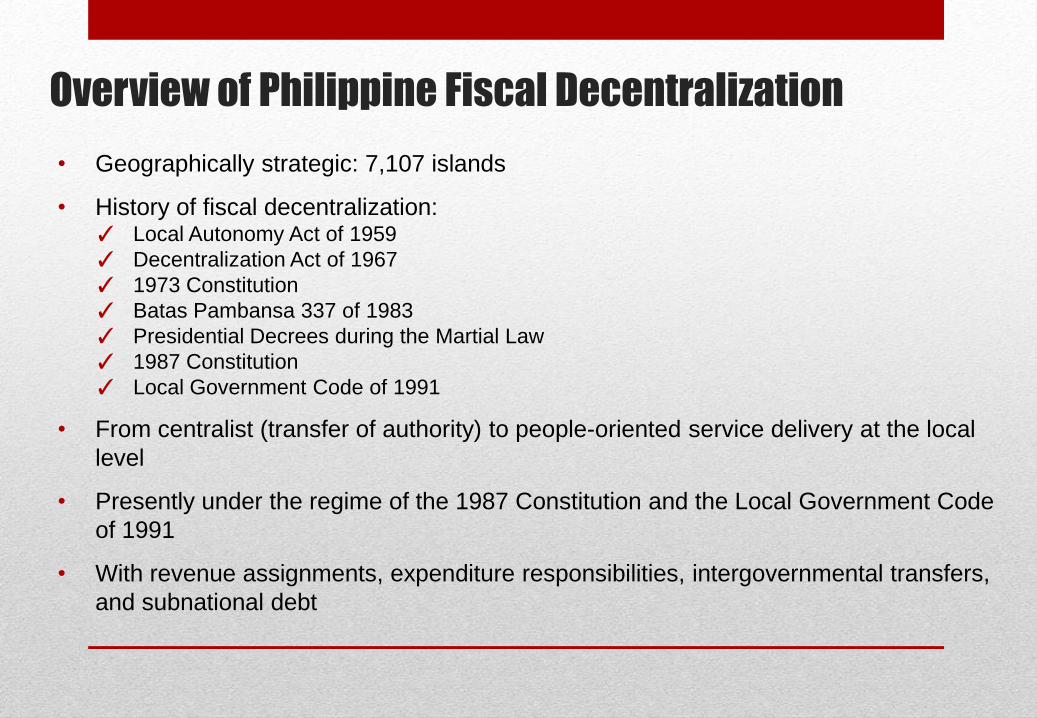

Overview of Philippine Fiscal Decentralization

• Geographically strategic: 7,107 islands

• History of fiscal decentralization: ✓ Local Autonomy Act of 1959

✓ Decentralization Act of 1967

✓ 1973 Constitution

✓ Batas Pambansa 337 of 1983

✓ Presidential Decrees during the Martial Law

✓ 1987 Constitution

✓ Local Government Code of 1991

• From centralist (transfer of authority) to people-oriented service delivery at the local

level

• Presently under the regime of the 1987 Constitution and the Local Government Code

of 1991

• With revenue assignments, expenditure responsibilities, intergovernmental transfers,

and subnational debt

Philippine Local Governments

Provinces (81)

Municipalities (1,489) Component Cities (105)

Barangays Barangays

Independent Cities (40) Highly Urbanized Cities (35)

Independent Component Cities (5)

Barangays

Total Number of Barangays: 42,028

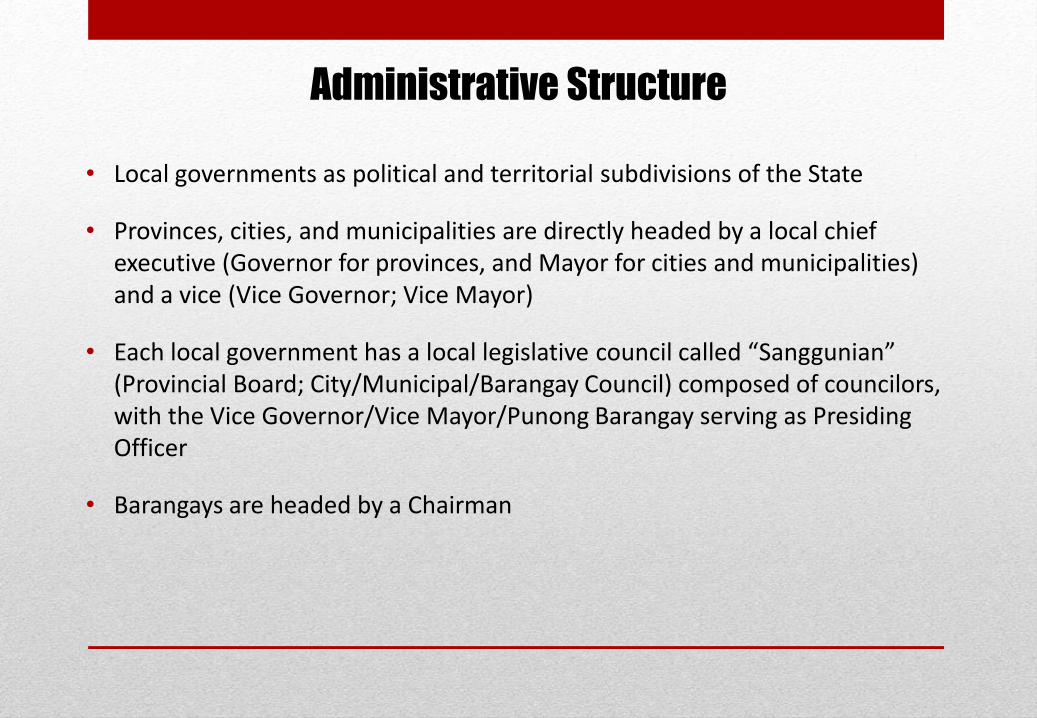

Administrative Structure

• Local governments as political and territorial subdivisions of the State

• Provinces, cities, and municipalities are directly headed by a local chief executive (Governor for provinces, and Mayor for cities and municipalities) and a vice (Vice Governor; Vice Mayor)

• Each local government has a local legislative council called “Sanggunian” (Provincial Board; City/Municipal/Barangay Council) composed of councilors, with the Vice Governor/Vice Mayor/Punong Barangay serving as Presiding Officer

• Barangays are headed by a Chairman

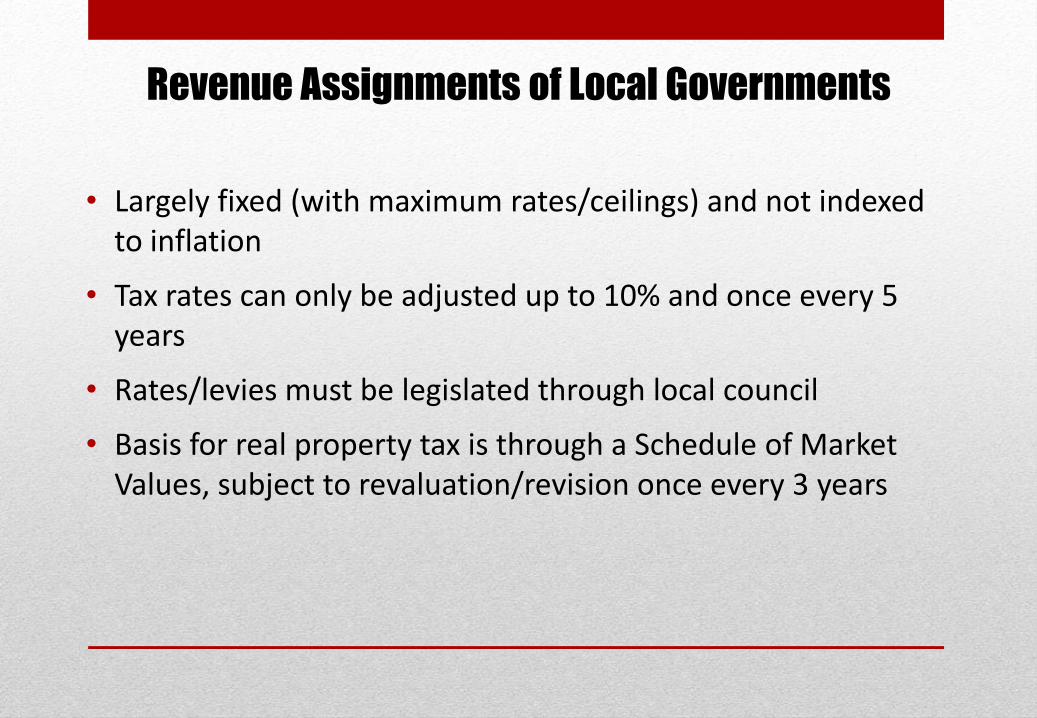

• Largely fixed (with maximum rates/ceilings) and not indexed to inflation

• Tax rates can only be adjusted up to 10% and once every 5 years

• Rates/levies must be legislated through local council

• Basis for real property tax is through a Schedule of Market Values, subject to revaluation/revision once every 3 years

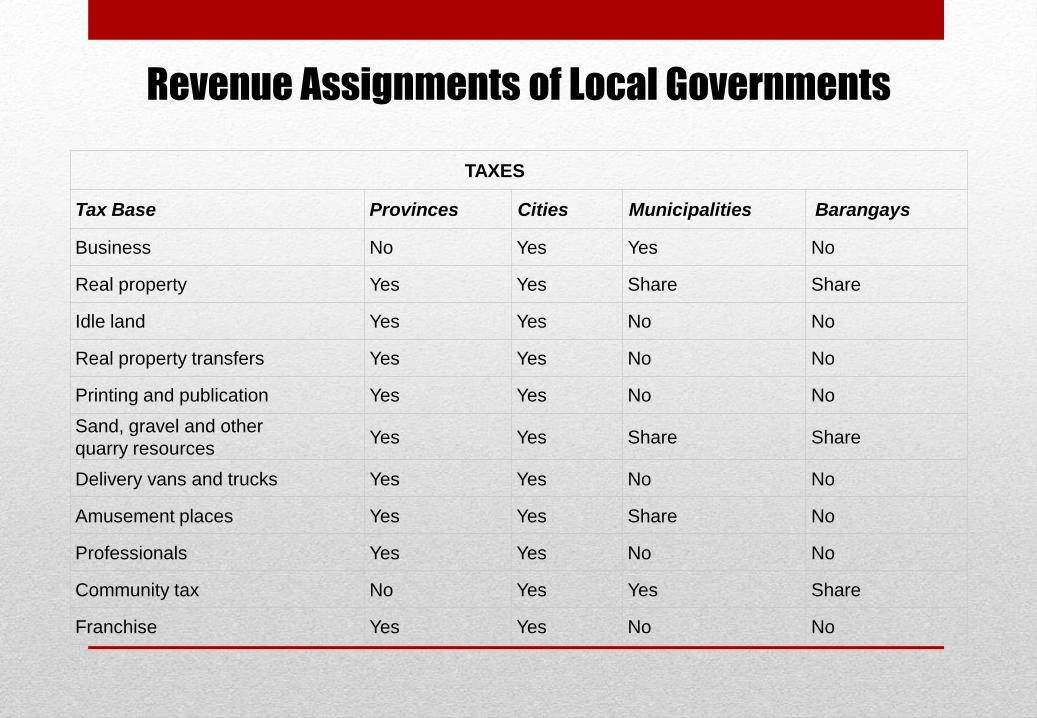

Revenue Assignments of Local Governments

Revenue Assignments of Local Governments

TAXES

Tax Base Provinces Cities Municipalities Barangays

Business No Yes Yes No

Real property Yes Yes Share Share

Idle land Yes Yes No No

Real property transfers Yes Yes No No

Printing and publication Yes Yes No No

Sand, gravel and other

quarry resources Yes Yes Share Share

Delivery vans and trucks Yes Yes No No

Amusement places Yes Yes Share No

Professionals Yes Yes No No

Community tax No Yes Yes Share

Franchise Yes Yes No No

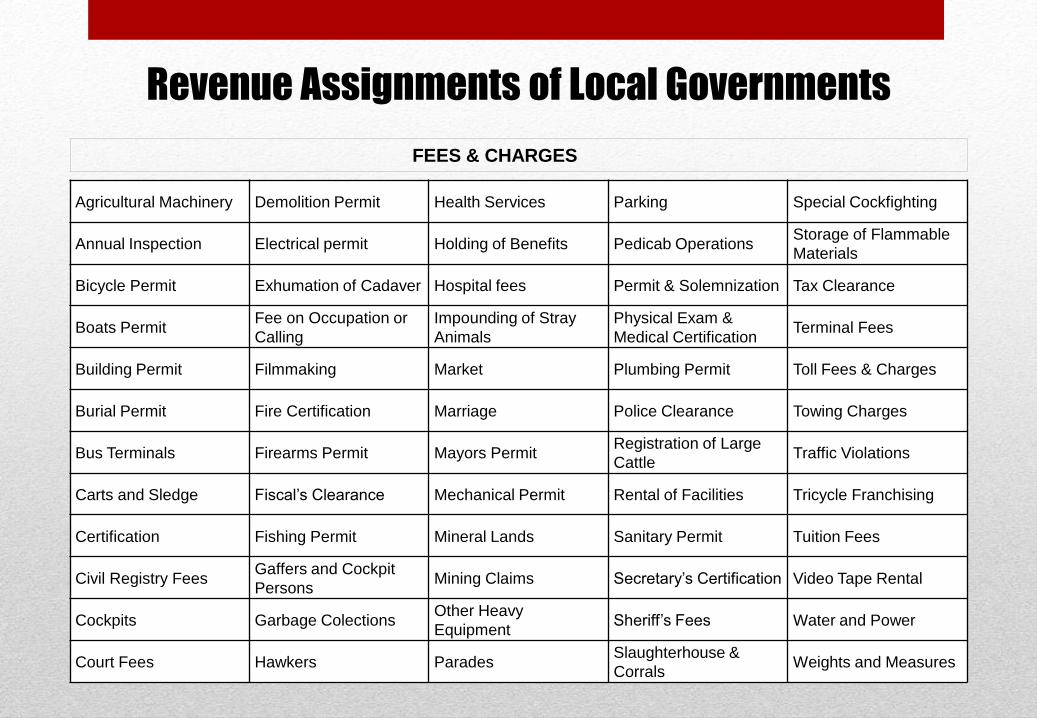

Revenue Assignments of Local Governments

FEES & CHARGES

Agricultural Machinery Demolition Permit Health Services Parking Special Cockfighting

Annual Inspection Electrical permit Holding of Benefits Pedicab Operations Storage of Flammable

Materials

Bicycle Permit Exhumation of Cadaver Hospital fees Permit & Solemnization Tax Clearance

Boats Permit Fee on Occupation or

Calling

Impounding of Stray

Animals

Physical Exam &

Medical Certification Terminal Fees

Building Permit Filmmaking Market Plumbing Permit Toll Fees & Charges

Burial Permit Fire Certification Marriage Police Clearance Towing Charges

Bus Terminals Firearms Permit Mayors Permit Registration of Large

Cattle Traffic Violations

Carts and Sledge Fiscal’s Clearance Mechanical Permit Rental of Facilities Tricycle Franchising

Certification Fishing Permit Mineral Lands Sanitary Permit Tuition Fees

Civil Registry Fees Gaffers and Cockpit

Persons Mining Claims Secretary’s Certification Video Tape Rental

Cockpits Garbage Colections Other Heavy

Equipment Sheriff’s Fees Water and Power

Court Fees Hawkers Parades Slaughterhouse &

Corrals Weights and Measures

Income Profile of Local

Government Units Provinces, Cities and Municipalities: 2009 - 2014

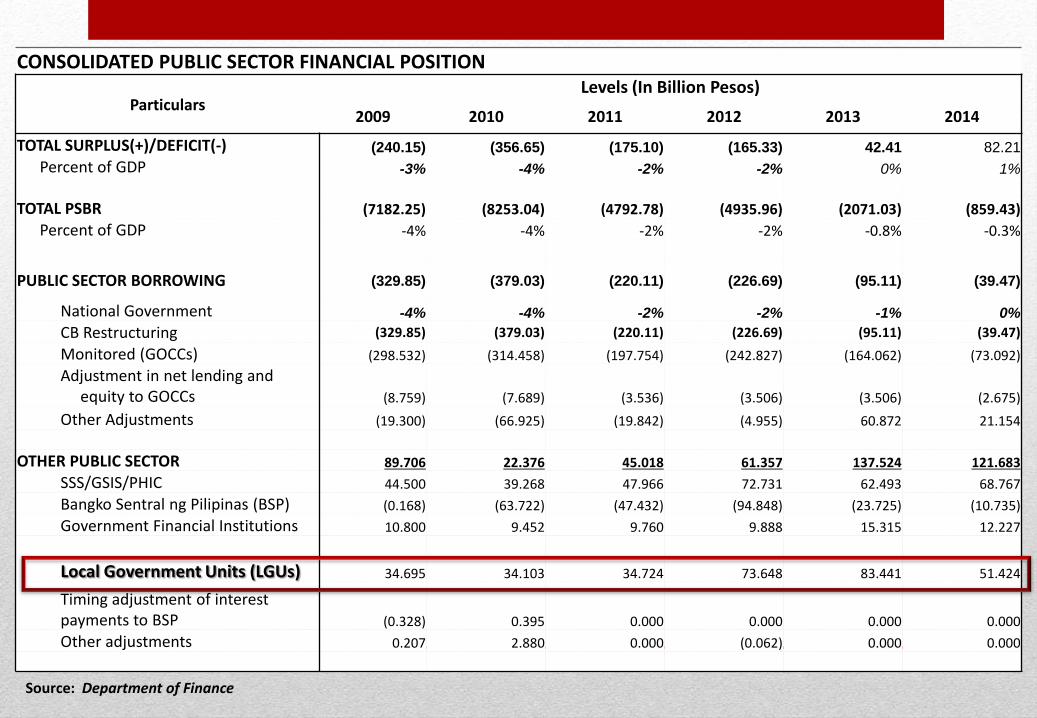

CONSOLIDATED PUBLIC SECTOR FINANCIAL POSITION

Particulars Levels (In Billion Pesos)

2009 2010 2011 2012 2013 2014

TOTAL SURPLUS(+)/DEFICIT(-) (240.15) (356.65) (175.10) (165.33) 42.41 82.21

Percent of GDP -3% -4% -2% -2% 0% 1%

TOTAL PSBR (7182.25) (8253.04) (4792.78) (4935.96) (2071.03) (859.43)

Percent of GDP -4% -4% -2% -2% -0.8% -0.3%

PUBLIC SECTOR BORROWING (329.85) (379.03) (220.11) (226.69) (95.11) (39.47)

National Government -4% -4% -2% -2% -1% 0%

CB Restructuring (329.85) (379.03) (220.11) (226.69) (95.11) (39.47)

Monitored (GOCCs) (298.532) (314.458) (197.754) (242.827) (164.062) (73.092)

Adjustment in net lending and equity to GOCCs (8.759) (7.689) (3.536) (3.506) (3.506) (2.675)

Other Adjustments (19.300) (66.925) (19.842) (4.955) 60.872 21.154

OTHER PUBLIC SECTOR 89.706 22.376 45.018 61.357 137.524 121.683

SSS/GSIS/PHIC 44.500 39.268 47.966 72.731 62.493 68.767

Bangko Sentral ng Pilipinas (BSP) (0.168) (63.722) (47.432) (94.848) (23.725) (10.735)

Government Financial Institutions 10.800 9.452 9.760 9.888 15.315 12.227

Local Government Units (LGUs) 34.695 34.103 34.724 73.648 83.441 51.424

Timing adjustment of interest payments to BSP (0.328) 0.395 0.000 0.000 0.000 0.000

Other adjustments 0.207 2.880 0.000 (0.062) 0.000 0.000

Source: Department of Finance

PARTICULARS 2009 2010 2011 2012 2013 2014 Average Amount in Million Pesos

Current Operating Income & Expenditures

Operating Income 311,011 336,613 366,093 367,912 389,558 429,429 366,769

Operating Expenditures 233,662 253,867 266,240 282,506 297,731 300,887 272,482

Net Operating Income/Loss 77,349 82,745 99,853 85,407 91,826 128,542 94,287

Non-Income Receipts & Non-Operating Expenditures

Non-Income Receipts 12,785 14,726 11,816 8,873 12,895 14,185 12,547

Non-Operating Expenditures 46,525 47,551 50,055 47,577 52,159 62,941 51,135

Net Increase/Decrease in Cash 43,608 49,921 61,614 46,703 52,562 79,785 55,699

Growth Rate

Current Operating Income & Expenditures

Income 8% 9% 0% 6% 10% 7%

Expenditures 9% 5% 6% 5% 1% 5%

Net Operating Income/Loss 7% 21% -14% 8% 40% 12%

Non-Income Receipts & Non-Operating Expenditures

Receipts 15% -20% -25% 45% 10% 5%

Expenditures 2% 5% -5% 10% 21% 7%

Growth rate of Net

Increase(Decrease) in Cash 14% 23% -24% 13% 52% 16%

Consolidated Statement of Receipts and Expenditures

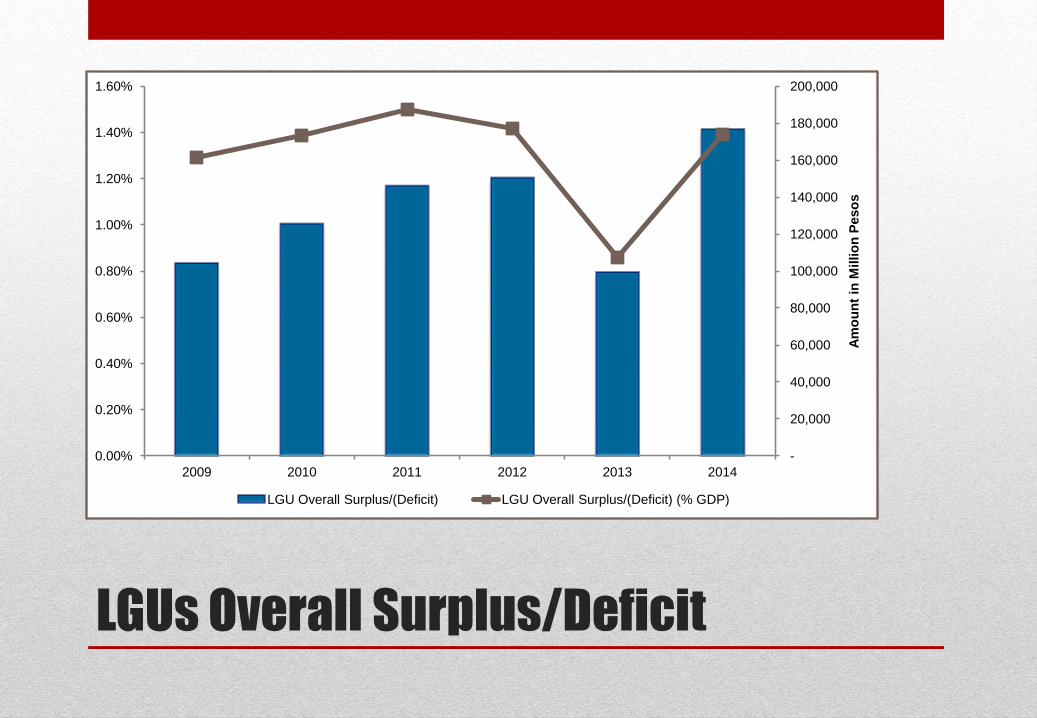

LGUs Overall Surplus/Deficit

0.00%

0.20%

0.40%

0.60%

0.80%

1.00%

1.20%

1.40%

1.60%

-

20,000

40,000

60,000

80,000

100,000

120,000

140,000

160,000

180,000

200,000

2009 2010 2011 2012 2013 2014

Am

ou

nt

in M

illio

n P

eso

s

LGU Overall Surplus/(Deficit) LGU Overall Surplus/(Deficit) (% GDP)

Net Operating Income(Loss): Growth Rate

-20%

-10%

0%

10%

20%

30%

40%

50%

0

50,000

100,000

150,000

200,000

250,000

300,000

350,000

400,000

450,000

2009 2010 2011 2012 2013 2014

Am

ou

nt in

Mill

ion

Pe

so

s

Operating Income Operating Expenditures Net Operating Income/Loss

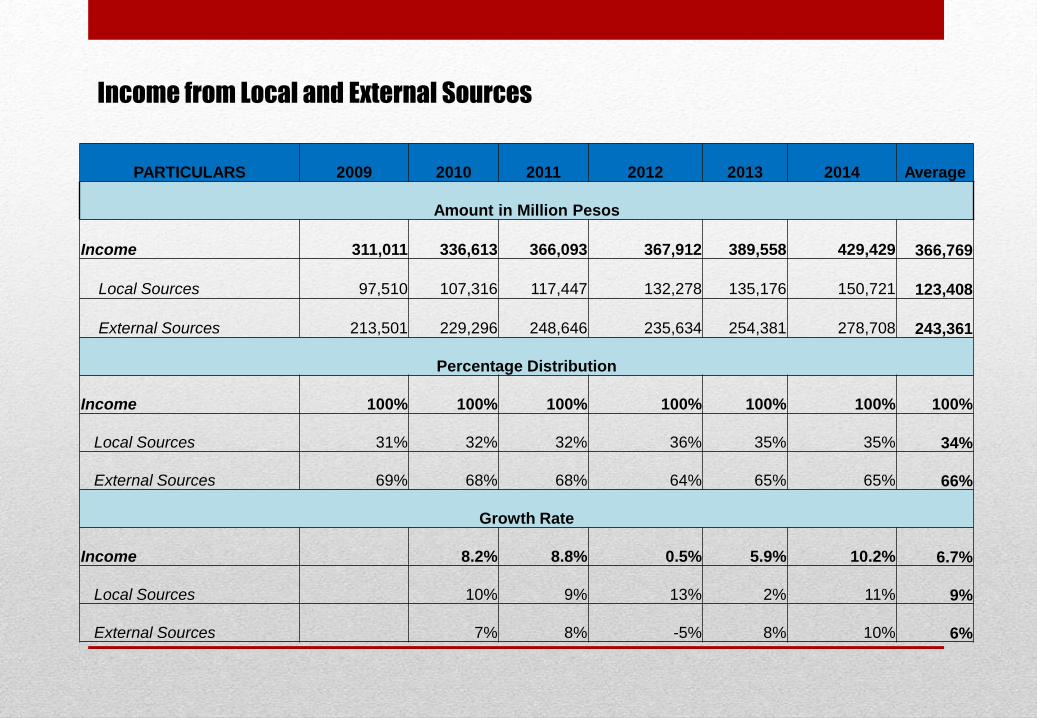

Income from Local and External Sources

PARTICULARS 2009 2010 2011 2012 2013 2014 Average

Amount in Million Pesos

Income

311,011

336,613

366,093

367,912

389,558

429,429

366,769

Local Sources

97,510

107,316

117,447

132,278

135,176

150,721

123,408

External Sources

213,501

229,296

248,646

235,634

254,381

278,708 243,361

Percentage Distribution

Income 100% 100% 100% 100% 100% 100% 100%

Local Sources 31% 32% 32% 36% 35% 35% 34%

External Sources 69% 68% 68% 64% 65% 65% 66%

Growth Rate

Income 8.2% 8.8% 0.5% 5.9% 10.2% 6.7%

Local Sources 10% 9% 13% 2% 11% 9%

External Sources 7% 8% -5% 8% 10% 6%

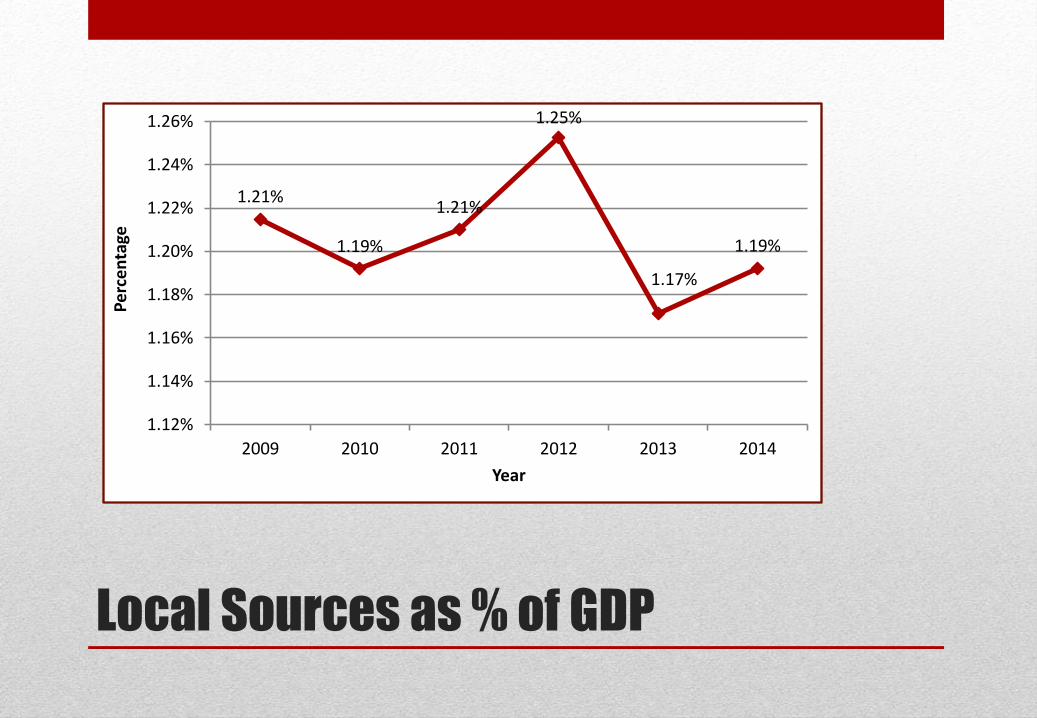

Local Sources as % of GDP

1.21%

1.19%

1.21%

1.25%

1.17%

1.19%

1.12%

1.14%

1.16%

1.18%

1.20%

1.22%

1.24%

1.26%

2009 2010 2011 2012 2013 2014

Pe

rce

nta

ge

Year

Local Sources vs. External Sources

Local Sources

34%

External Sources

66%

Local Sources vs. External Sources (Average Percentage Contribution)

2010 2011 2012 2013 2014

External Sources 7% 8% -5% 8% 10%

Local Sources 10% 9% 13% 2% 11%

-6%

-4%

-2%

0%

2%

4%

6%

8%

10%

12%

14%

Gro

wth

Rat

e

External Sources Local Sources

Growth Rate of Revenues from Local and External Sources

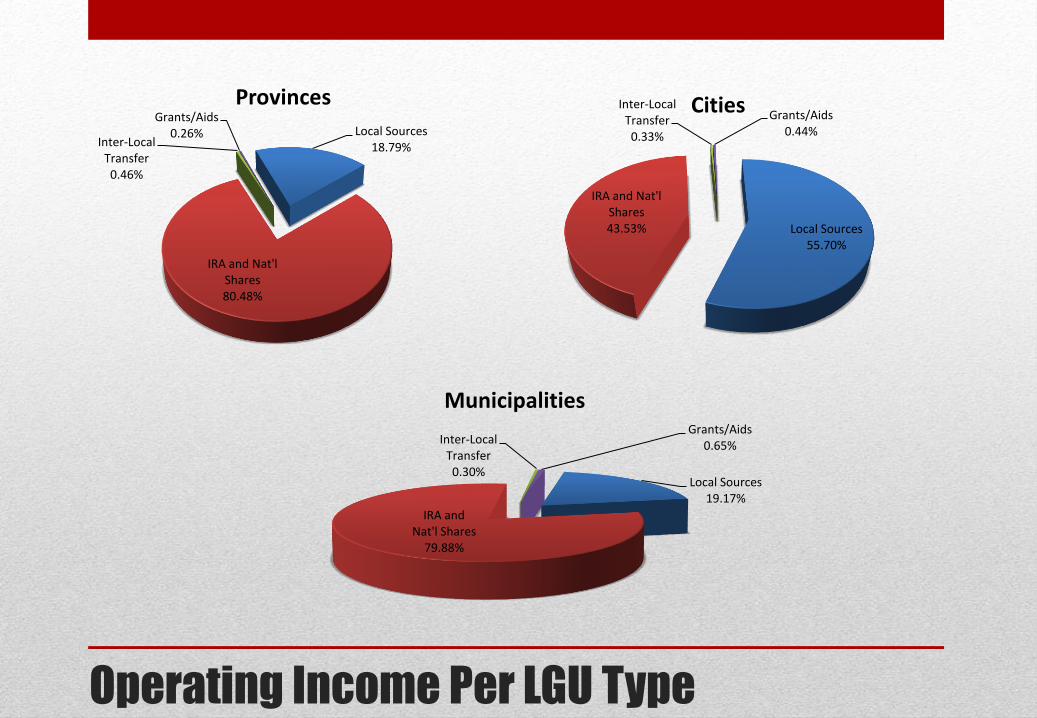

Operating Income Per LGU Type

Local Sources 18.79%

IRA and Nat'l Shares 80.48%

Inter-Local Transfer 0.46%

Grants/Aids 0.26%

Provinces

Local Sources 55.70%

IRA and Nat'l Shares 43.53%

Inter-Local Transfer 0.33%

Grants/Aids 0.44%

Cities

Local Sources 19.17%

IRA and Nat'l Shares

79.88%

Inter-Local Transfer 0.30%

Grants/Aids 0.65%

Municipalities

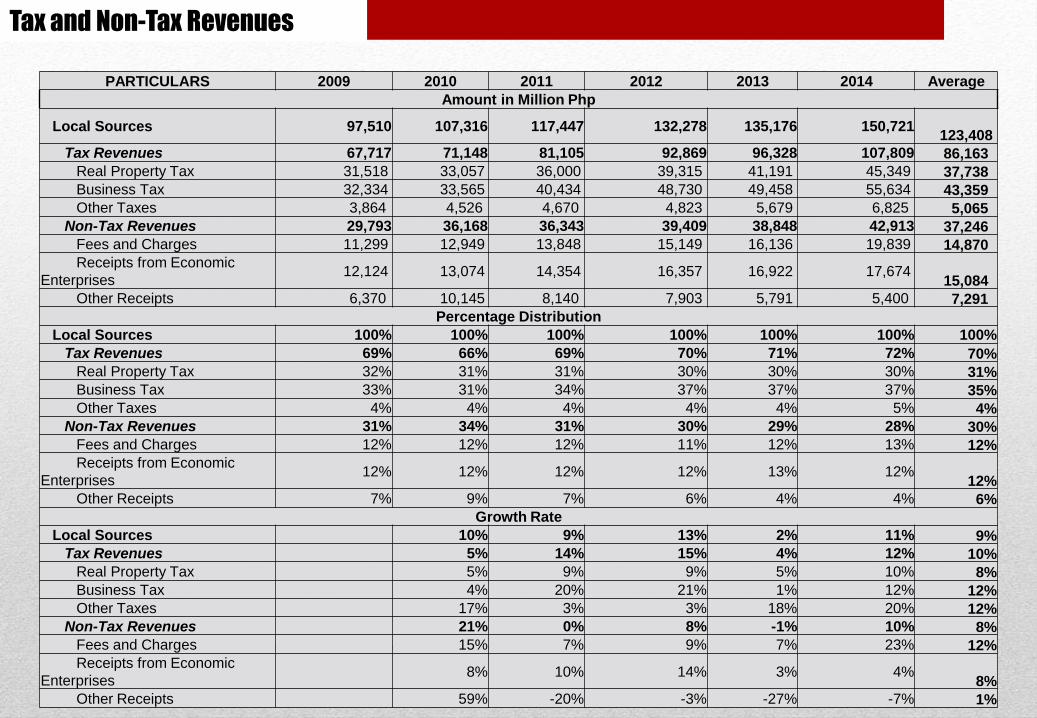

Tax and Non-Tax Revenues

PARTICULARS 2009 2010 2011 2012 2013 2014 Average

Amount in Million Php

Local Sources 97,510 107,316 117,447 132,278 135,176 150,721 123,408

Tax Revenues 67,717 71,148 81,105 92,869 96,328 107,809 86,163

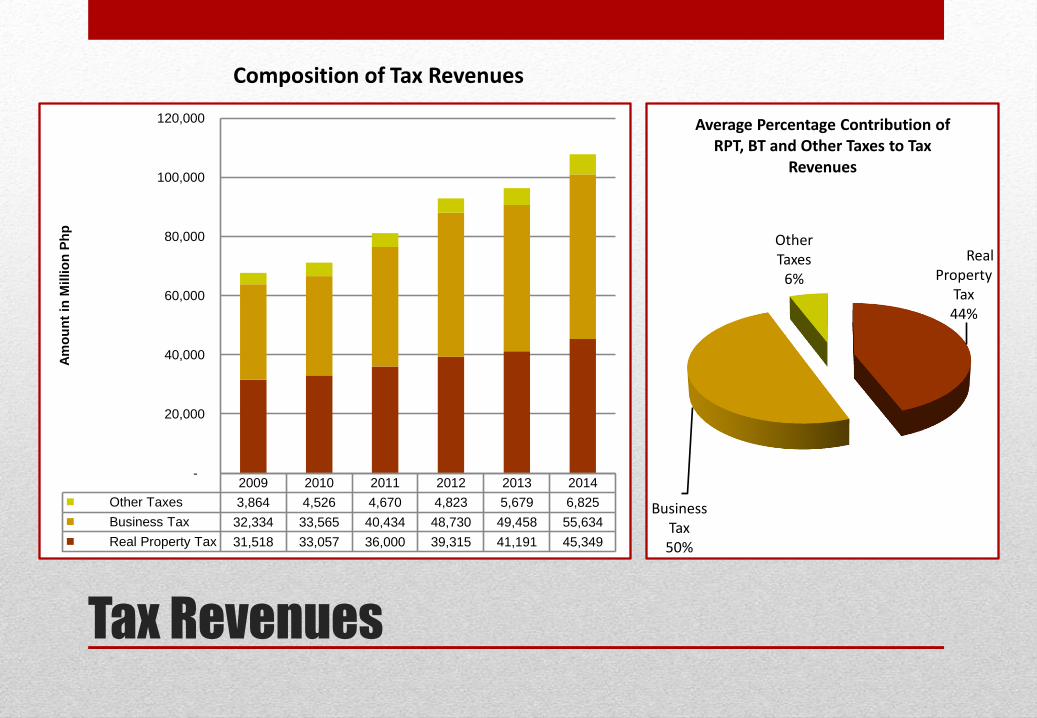

Real Property Tax 31,518 33,057 36,000 39,315 41,191 45,349 37,738

Business Tax 32,334 33,565 40,434 48,730 49,458 55,634 43,359

Other Taxes 3,864 4,526 4,670 4,823 5,679 6,825 5,065

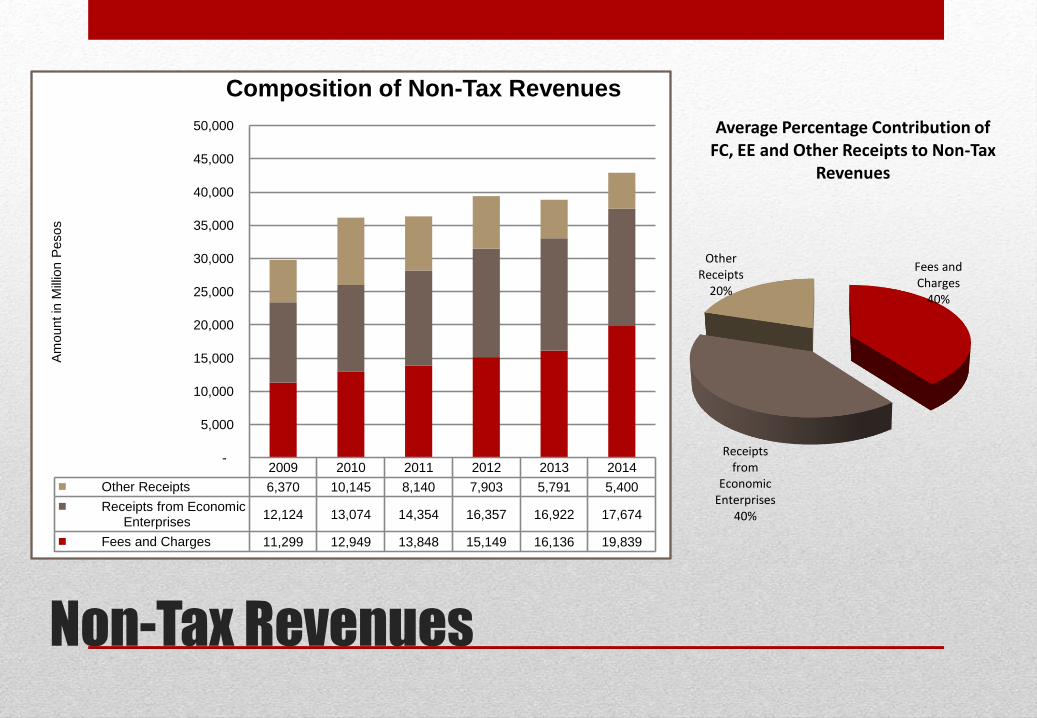

Non-Tax Revenues 29,793 36,168 36,343 39,409 38,848 42,913 37,246

Fees and Charges 11,299 12,949 13,848 15,149 16,136 19,839 14,870

Receipts from Economic

Enterprises 12,124 13,074 14,354 16,357 16,922 17,674

15,084

Other Receipts 6,370 10,145 8,140 7,903 5,791 5,400 7,291

Percentage Distribution

Local Sources 100% 100% 100% 100% 100% 100% 100%

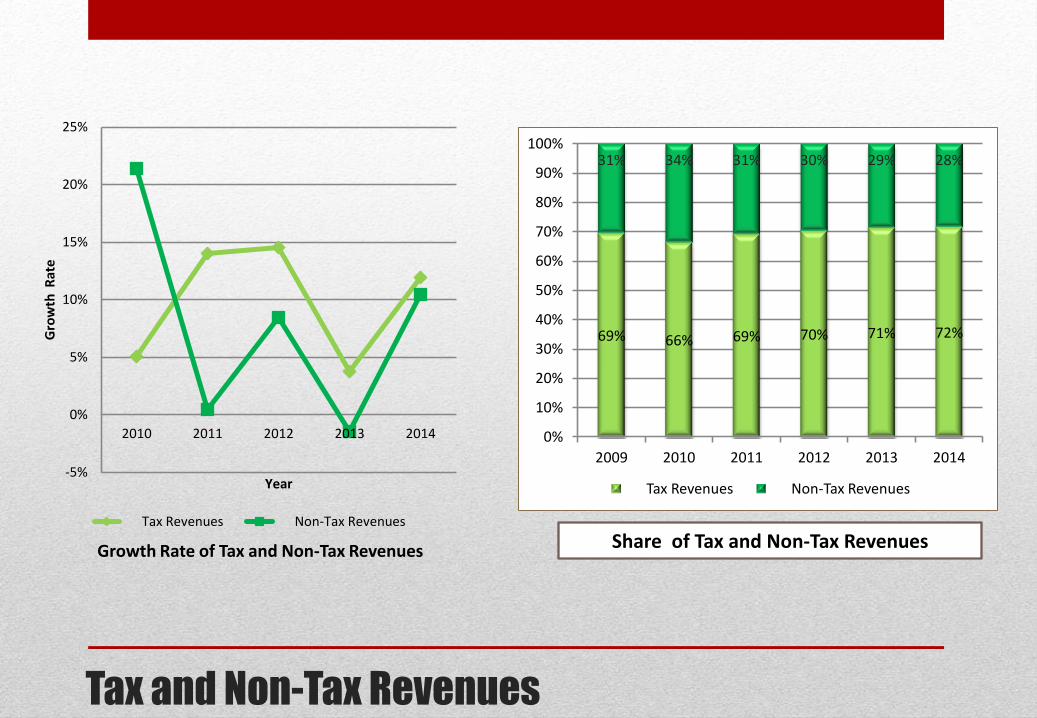

Tax Revenues 69% 66% 69% 70% 71% 72% 70%

Real Property Tax 32% 31% 31% 30% 30% 30% 31%

Business Tax 33% 31% 34% 37% 37% 37% 35%

Other Taxes 4% 4% 4% 4% 4% 5% 4%

Non-Tax Revenues 31% 34% 31% 30% 29% 28% 30%

Fees and Charges 12% 12% 12% 11% 12% 13% 12%

Receipts from Economic

Enterprises 12% 12% 12% 12% 13% 12%

12%

Other Receipts 7% 9% 7% 6% 4% 4% 6%

Growth Rate

Local Sources 10% 9% 13% 2% 11% 9%

Tax Revenues 5% 14% 15% 4% 12% 10%

Real Property Tax 5% 9% 9% 5% 10% 8%

Business Tax 4% 20% 21% 1% 12% 12%

Other Taxes 17% 3% 3% 18% 20% 12%

Non-Tax Revenues 21% 0% 8% -1% 10% 8%

Fees and Charges 15% 7% 9% 7% 23% 12%

Receipts from Economic

Enterprises 8% 10% 14% 3% 4%

8%

Other Receipts 59% -20% -3% -27% -7% 1%

Tax and Non-Tax Revenues

-5%

0%

5%

10%

15%

20%

25%

2010 2011 2012 2013 2014

Gro

wth

Rat

e

Year

Tax Revenues Non-Tax Revenues

69% 66% 69% 70% 71% 72%

31% 34% 31% 30% 29% 28%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2009 2010 2011 2012 2013 2014

Tax Revenues Non-Tax Revenues

Growth Rate of Tax and Non-Tax Revenues Share of Tax and Non-Tax Revenues

Tax Revenues

Real Property

Tax 44%

Business

Tax 50%

Other Taxes

6%

Average Percentage Contribution of RPT, BT and Other Taxes to Tax

Revenues

2009 2010 2011 2012 2013 2014

Other Taxes 3,864 4,526 4,670 4,823 5,679 6,825

Business Tax 32,334 33,565 40,434 48,730 49,458 55,634

Real Property Tax 31,518 33,057 36,000 39,315 41,191 45,349

-

20,000

40,000

60,000

80,000

100,000

120,000

Am

ou

nt

in M

illi

on

Ph

p

Composition of Tax Revenues

Non-Tax Revenues

Fees and Charges

40%

Receipts

from Economic

Enterprises 40%

Other Receipts

20%

Average Percentage Contribution of FC, EE and Other Receipts to Non-Tax

Revenues

2009 2010 2011 2012 2013 2014

Other Receipts 6,370 10,145 8,140 7,903 5,791 5,400

Receipts from Economic Enterprises

12,124 13,074 14,354 16,357 16,922 17,674

Fees and Charges 11,299 12,949 13,848 15,149 16,136 19,839

-

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

45,000

50,000

Am

ount in

Mill

ion P

esos

Composition of Non-Tax Revenues

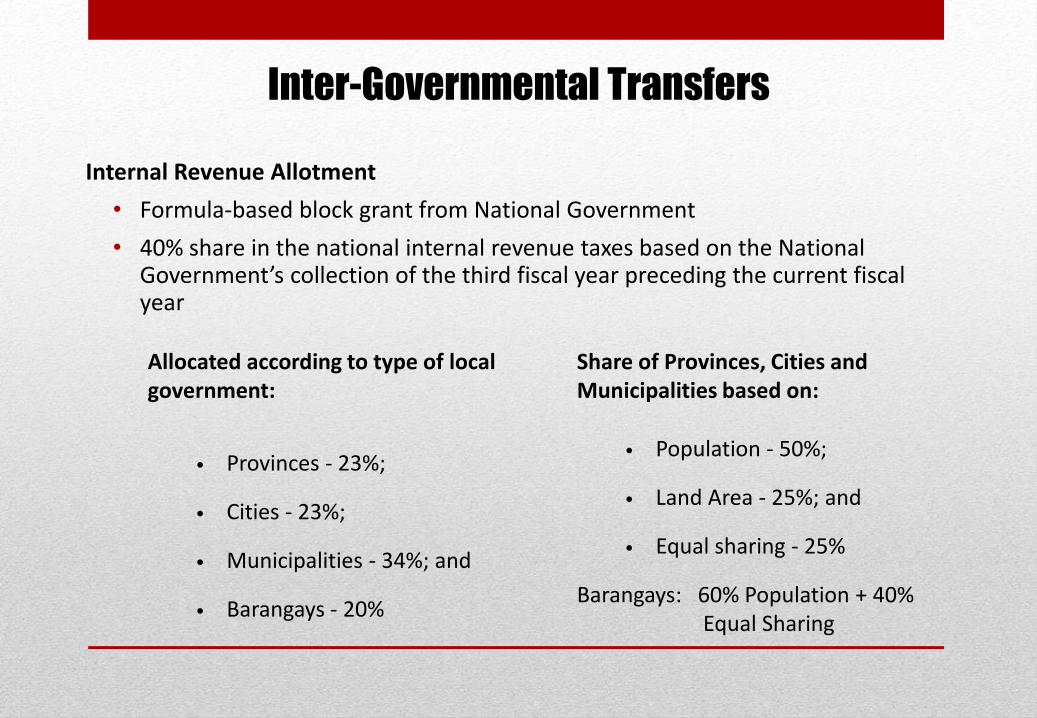

Internal Revenue Allotment

• Formula-based block grant from National Government

• 40% share in the national internal revenue taxes based on the National Government’s collection of the third fiscal year preceding the current fiscal year

Inter-Governmental Transfers

Allocated according to type of local government:

Share of Provinces, Cities and Municipalities based on:

• Provinces - 23%;

• Cities - 23%;

• Municipalities - 34%; and

• Barangays - 20%

• Population - 50%;

• Land Area - 25%; and

• Equal sharing - 25%

Barangays: 60% Population + 40% Equal Sharing

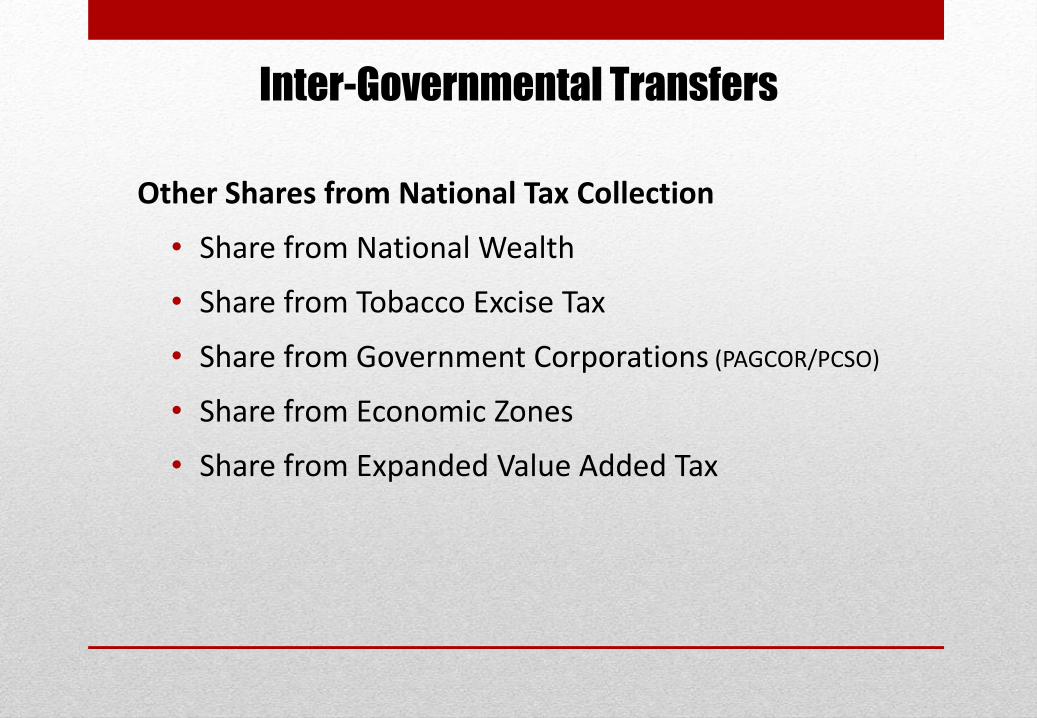

Other Shares from National Tax Collection

• Share from National Wealth

• Share from Tobacco Excise Tax

• Share from Government Corporations (PAGCOR/PCSO)

• Share from Economic Zones

• Share from Expanded Value Added Tax

Inter-Governmental Transfers

IRA and Other Shares from National Wealth

-

20,000.00

40,000.00

60,000.00

80,000.00

100,000.00

120,000.00

140,000.00

2009 2010 2011 2012 2013 2014

Am

ou

nt

in M

illi

on

Ph

p

Province

City

Municipality

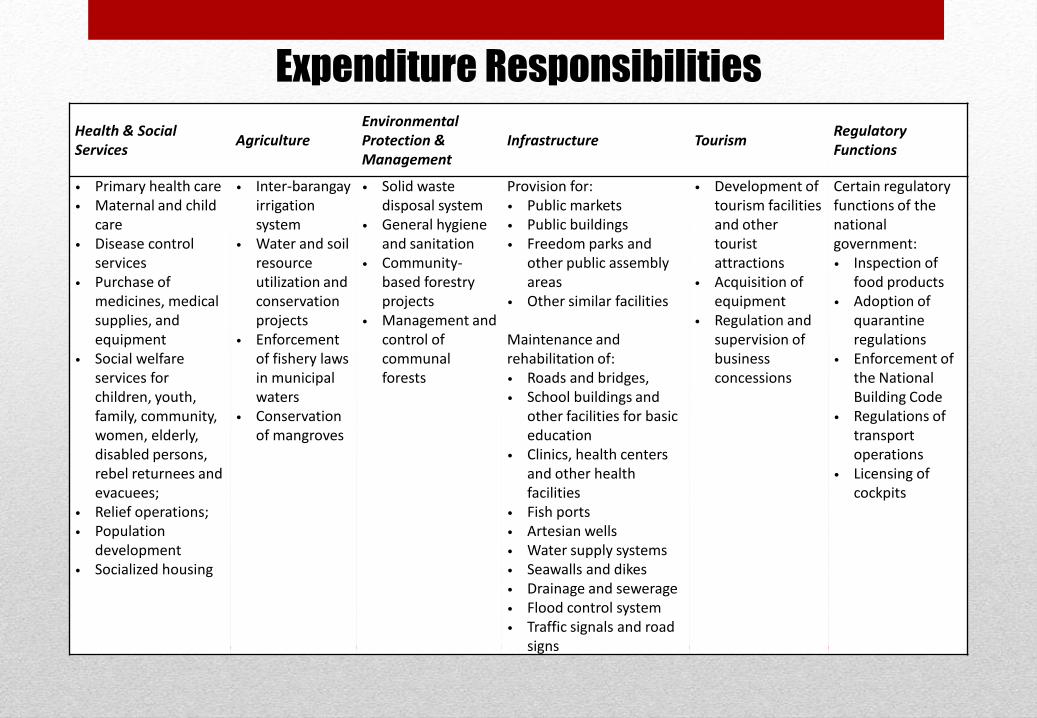

Expenditure Responsibilities

Health & Social Services

Agriculture Environmental Protection & Management

Infrastructure Tourism Regulatory Functions

• Primary health care • Maternal and child

care • Disease control

services • Purchase of

medicines, medical supplies, and equipment

• Social welfare services for children, youth, family, community, women, elderly, disabled persons, rebel returnees and evacuees;

• Relief operations; • Population

development • Socialized housing

• Inter-barangay irrigation system

• Water and soil resource utilization and conservation projects

• Enforcement of fishery laws in municipal waters

• Conservation of mangroves

• Solid waste disposal system

• General hygiene and sanitation

• Community-based forestry projects

• Management and control of communal forests

Provision for: • Public markets • Public buildings • Freedom parks and

other public assembly areas

• Other similar facilities Maintenance and rehabilitation of: • Roads and bridges, • School buildings and

other facilities for basic education

• Clinics, health centers and other health facilities

• Fish ports • Artesian wells • Water supply systems • Seawalls and dikes • Drainage and sewerage • Flood control system • Traffic signals and road

signs

• Development of tourism facilities and other tourist attractions

• Acquisition of equipment

• Regulation and supervision of business concessions

Certain regulatory functions of the national government: • Inspection of

food products • Adoption of

quarantine regulations

• Enforcement of the National Building Code

• Regulations of transport operations

• Licensing of cockpits

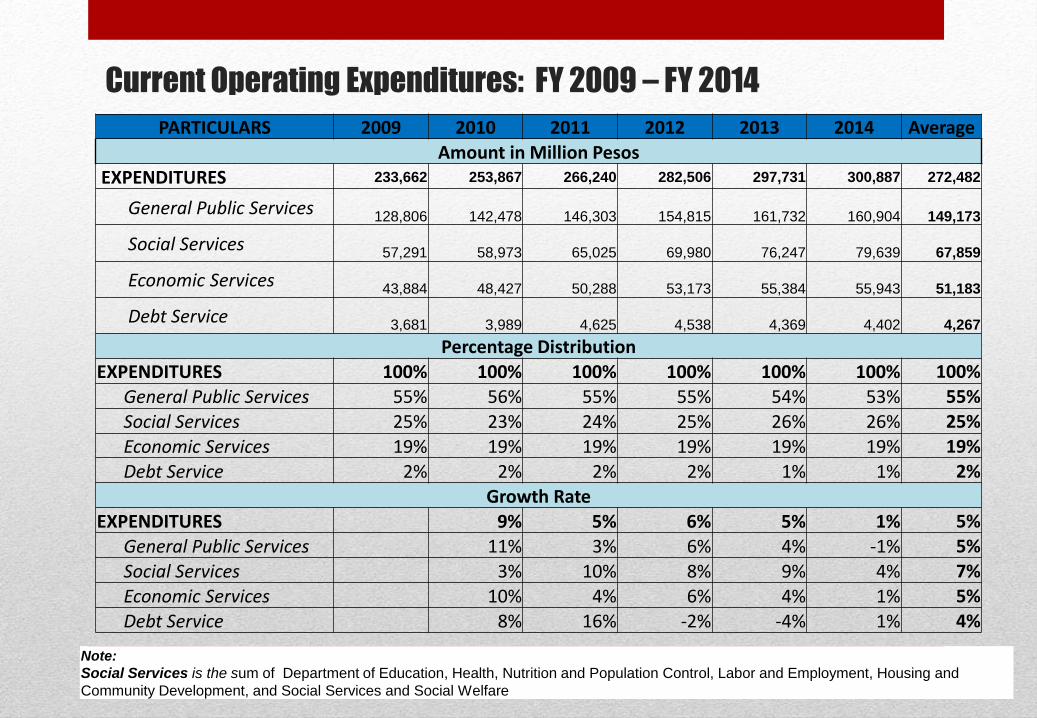

Current Operating Expenditures: FY 2009 – FY 2014

PARTICULARS 2009 2010 2011 2012 2013 2014 Average

Amount in Million Pesos EXPENDITURES 233,662 253,867 266,240 282,506 297,731 300,887 272,482

General Public Services

128,806 142,478 146,303

154,815 161,732

160,904 149,173

Social Services

57,291 58,973 65,025

69,980 76,247

79,639 67,859

Economic Services

43,884 48,427 50,288

53,173 55,384

55,943 51,183

Debt Service

3,681 3,989 4,625

4,538 4,369

4,402 4,267

Percentage Distribution

EXPENDITURES 100% 100% 100% 100% 100% 100% 100%

General Public Services 55% 56% 55% 55% 54% 53% 55%

Social Services 25% 23% 24% 25% 26% 26% 25%

Economic Services 19% 19% 19% 19% 19% 19% 19%

Debt Service 2% 2% 2% 2% 1% 1% 2%

Growth Rate EXPENDITURES 9% 5% 6% 5% 1% 5%

General Public Services 11% 3% 6% 4% -1% 5%

Social Services 3% 10% 8% 9% 4% 7%

Economic Services 10% 4% 6% 4% 1% 5%

Debt Service 8% 16% -2% -4% 1% 4%

Note:

Social Services is the sum of Department of Education, Health, Nutrition and Population Control, Labor and Employment, Housing and

Community Development, and Social Services and Social Welfare

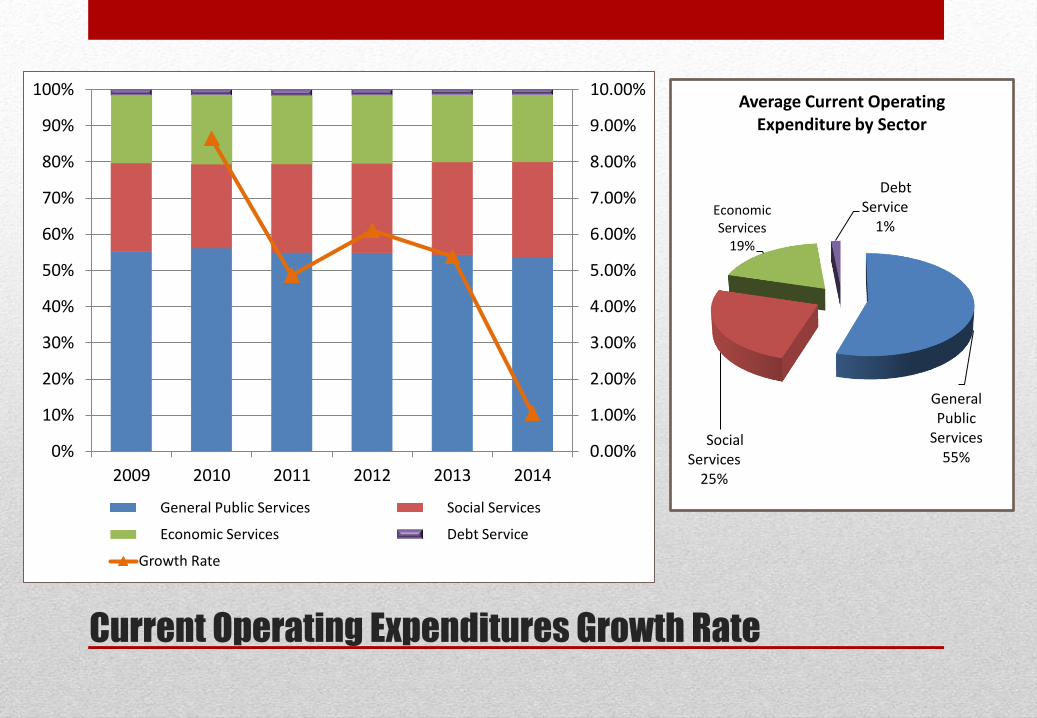

Current Operating Expenditures Growth Rate

0.00%

1.00%

2.00%

3.00%

4.00%

5.00%

6.00%

7.00%

8.00%

9.00%

10.00%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2009 2010 2011 2012 2013 2014

General Public Services Social Services

Economic Services Debt Service

Growth Rate

General Public

Services 55%

Social Services

25%

Economic Services

19%

Debt Service

1%

Average Current Operating Expenditure by Sector

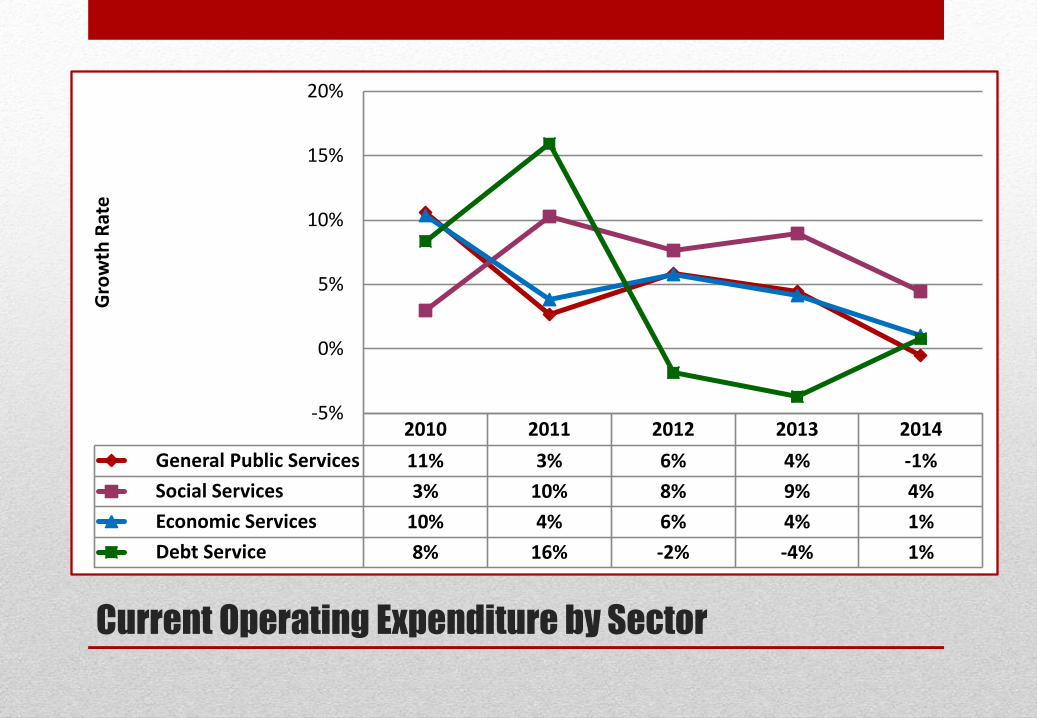

Current Operating Expenditure by Sector

2010 2011 2012 2013 2014

General Public Services 11% 3% 6% 4% -1%

Social Services 3% 10% 8% 9% 4%

Economic Services 10% 4% 6% 4% 1%

Debt Service 8% 16% -2% -4% 1%

-5%

0%

5%

10%

15%

20% G

row

th R

ate

• Any local government unit may create indebtedness, and avail of credit facilities to finance local infrastructure and other socio-economic development projects (based on the approved local development plan and public investment program)

• Forms of indebtedness/credit facilities: • Loans, deferred payment and other financial schemes • Bonds and other long-term securities • Inter-local government loans, grants, and subsidies. • Loans from funds secured by NG from foreign sources • Build-Operate-Transfer/Joint Ventures: financing, construction,

maintenance, operation, and management of infrastructure projects by the private sector

Sub-national Debt/Borrowing

• Statutory Limitations: the amount of appropriations for debt servicing shall not exceed 20% of the regular income of the local government unit concerned.

• Ex ante monitoring/regulations: DOF/BLGF certifies debts service ceiling and net borrowing capacity of LGUs; the Monetary Board issues opinion on the monetary and balance of payments implications for every proposed borrowing of local governments

• Policy preference to secure loans with government financial institutions

Sub-national Debt/Borrowing

LGU Borrowings

0.00%

0.10%

0.20%

0.30%

0.40%

0.50%

0.60%

0.70%

0.80%

0

10,000

20,000

30,000

40,000

50,000

60,000

70,000

80,000

2009 2010 2011 2012 2013 2014

Am

ou

nt

in M

illi

on

Ph

p

LGU Debt Service LGUs Loans Oustanding

LGU Debt Service (% of GDP) LGUs Loans Oustanding (% of GDP)

The Bureau of Local Government Finance

• Role of the BLGF

• Legal Basis & Mandate

• Clientele

• Organizational Structure

• Strategic Thrusts and Programs

• Special Projects

VISION:

The Bureau of Local Government Finance of the Department of Finance is the focal agency

and an authority in local finance that aims to be at the forefront of local economic growth

leading the way towards national development.

Role of the BLGF

• As an attached agency of the Department of Finance (DOF), the BLGF supports the DOF’s mandate to:

Supervise the revenue operations of all local government units; and

Monitor and support the implementation of policies and measures on local revenue administration;

• Provide technical assistance to local governments on local treasury and assessment operations, and overall revenue generation activities

• Assist in policy development and implementation to promote fiscal decentralization in the LGUs

• Assist the DOF in appointment and overall administrative supervision of local treasurers and in providing technical supervision to assessors in all local governments

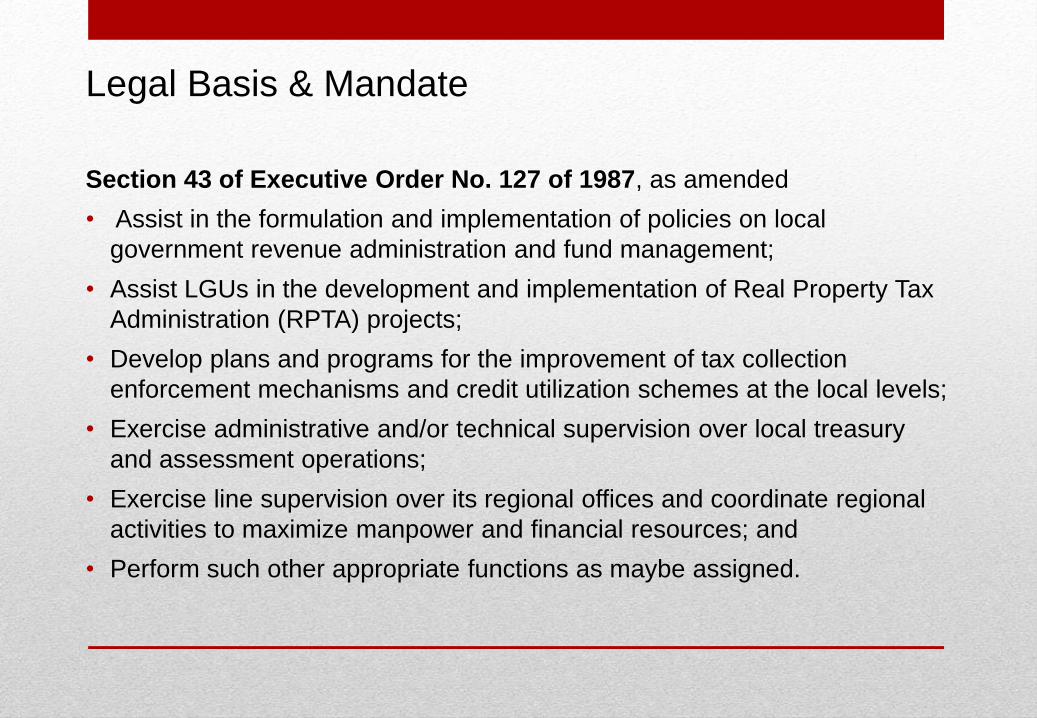

Legal Basis & Mandate

Section 43 of Executive Order No. 127 of 1987, as amended

• Assist in the formulation and implementation of policies on local

government revenue administration and fund management;

• Assist LGUs in the development and implementation of Real Property Tax

Administration (RPTA) projects;

• Develop plans and programs for the improvement of tax collection

enforcement mechanisms and credit utilization schemes at the local levels;

• Exercise administrative and/or technical supervision over local treasury

and assessment operations;

• Exercise line supervision over its regional offices and coordinate regional

activities to maximize manpower and financial resources; and

• Perform such other appropriate functions as maybe assigned.

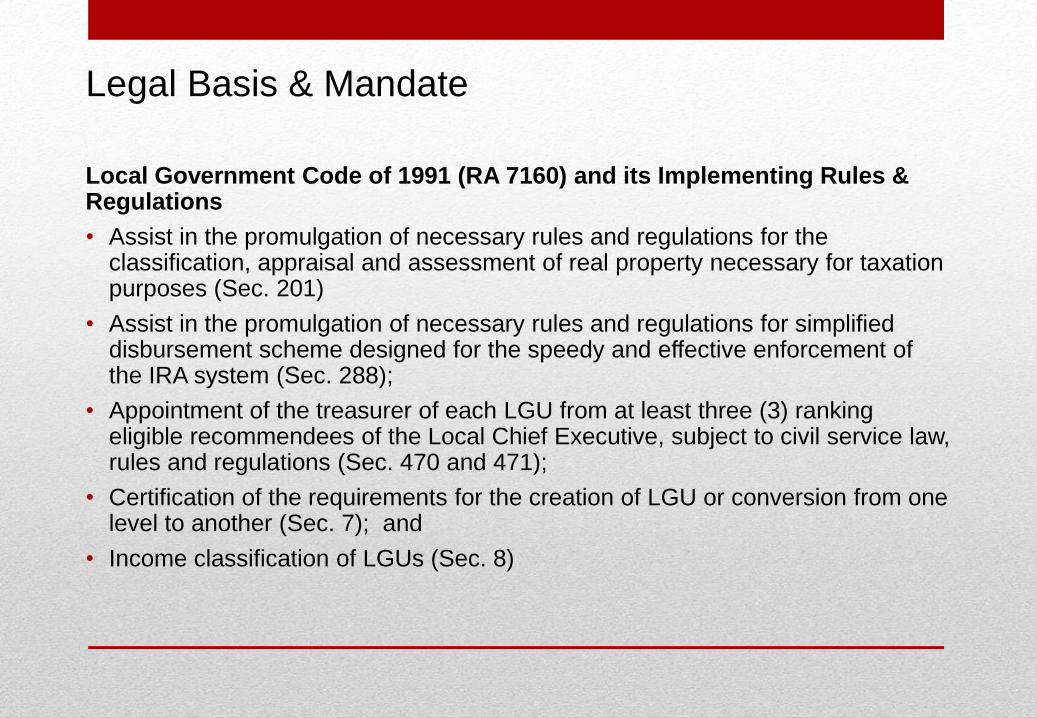

Legal Basis & Mandate

Local Government Code of 1991 (RA 7160) and its Implementing Rules & Regulations

• Assist in the promulgation of necessary rules and regulations for the classification, appraisal and assessment of real property necessary for taxation purposes (Sec. 201)

• Assist in the promulgation of necessary rules and regulations for simplified disbursement scheme designed for the speedy and effective enforcement of the IRA system (Sec. 288);

• Appointment of the treasurer of each LGU from at least three (3) ranking eligible recommendees of the Local Chief Executive, subject to civil service law, rules and regulations (Sec. 470 and 471);

• Certification of the requirements for the creation of LGU or conversion from one level to another (Sec. 7); and

• Income classification of LGUs (Sec. 8)

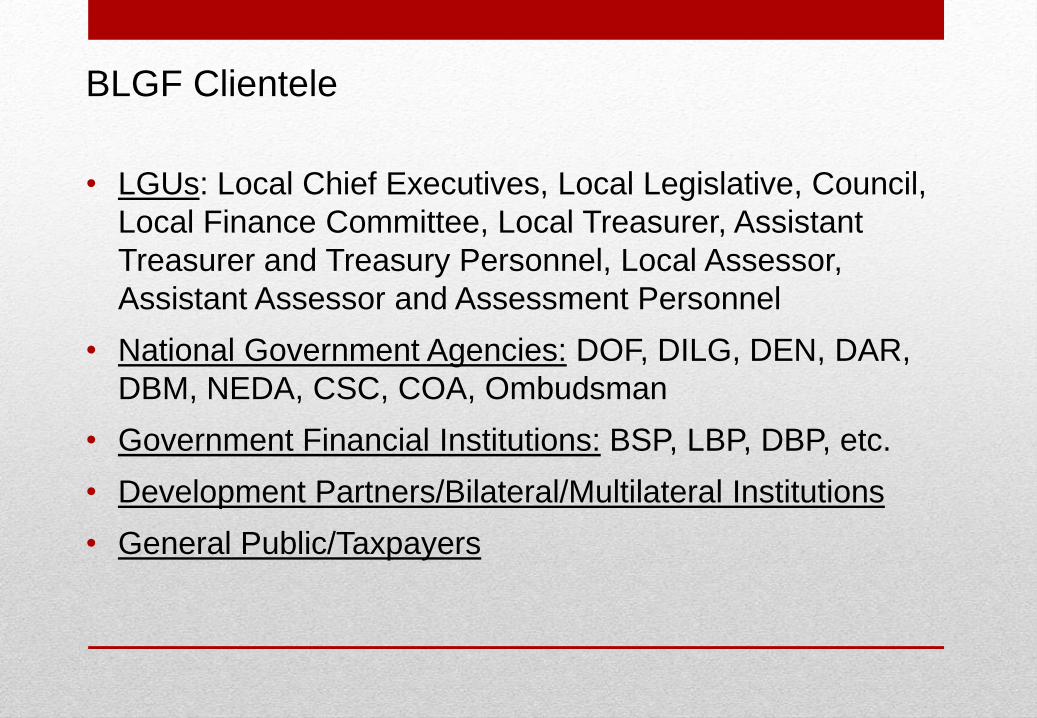

BLGF Clientele

• LGUs: Local Chief Executives, Local Legislative, Council,

Local Finance Committee, Local Treasurer, Assistant

Treasurer and Treasury Personnel, Local Assessor,

Assistant Assessor and Assessment Personnel

• National Government Agencies: DOF, DILG, DEN, DAR,

DBM, NEDA, CSC, COA, Ombudsman

• Government Financial Institutions: BSP, LBP, DBP, etc.

• Development Partners/Bilateral/Multilateral Institutions

• General Public/Taxpayers

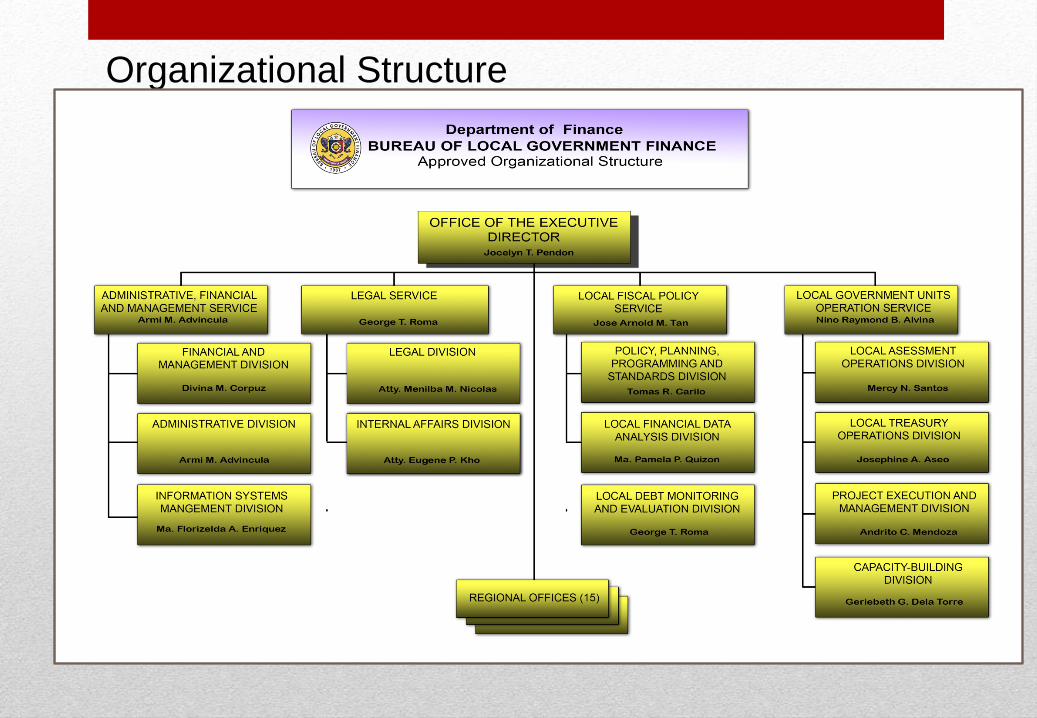

Organizational Structure

Special Projects

Local Government Finance and Development

Project (with MDFO)

Second Land Administration & Management

Project (with DENR, LRA)

LGU Public Financial Management (with DBM,

DILG, COA, NEDA)

Support to Local Government Revenue

Generation and Land Administration &

Management (with DENR)

LOGOFIND

EU PFM 2

ADB TA 7809

REGALA

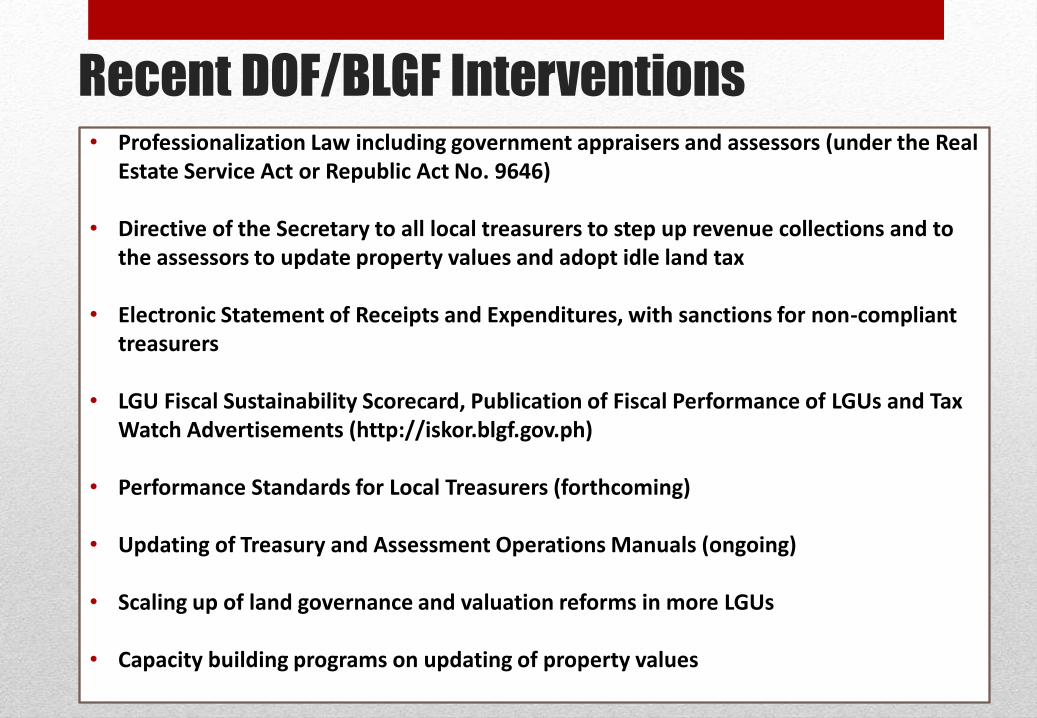

Recent DOF/BLGF Interventions • Professionalization Law including government appraisers and assessors (under the Real

Estate Service Act or Republic Act No. 9646)

• Directive of the Secretary to all local treasurers to step up revenue collections and to the assessors to update property values and adopt idle land tax

• Electronic Statement of Receipts and Expenditures, with sanctions for non-compliant treasurers

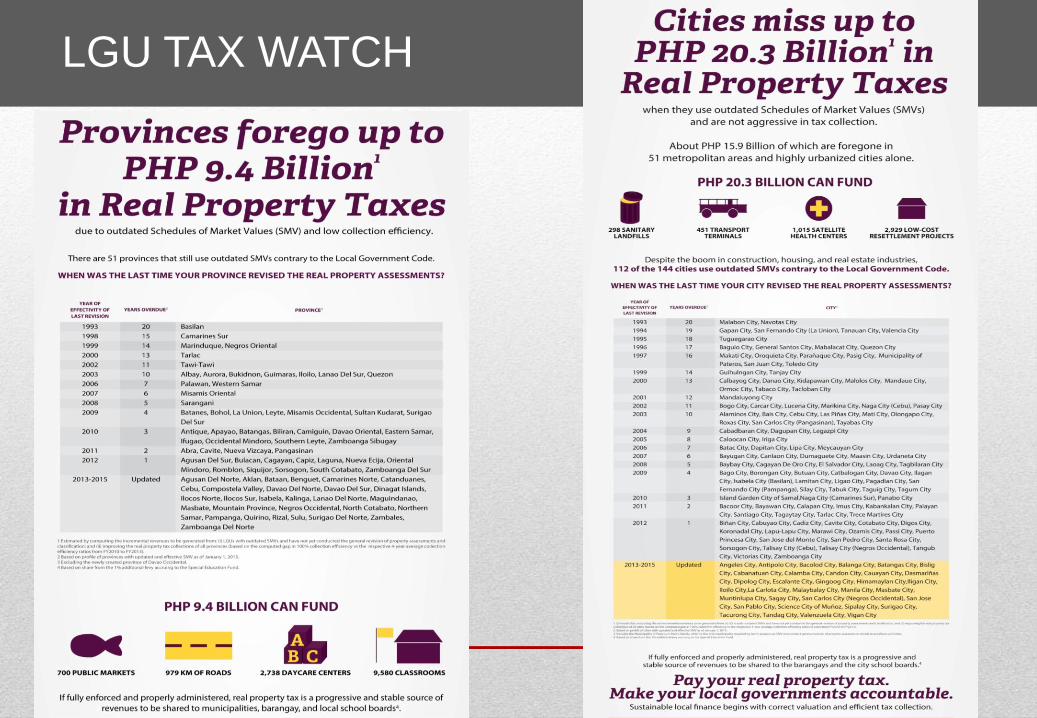

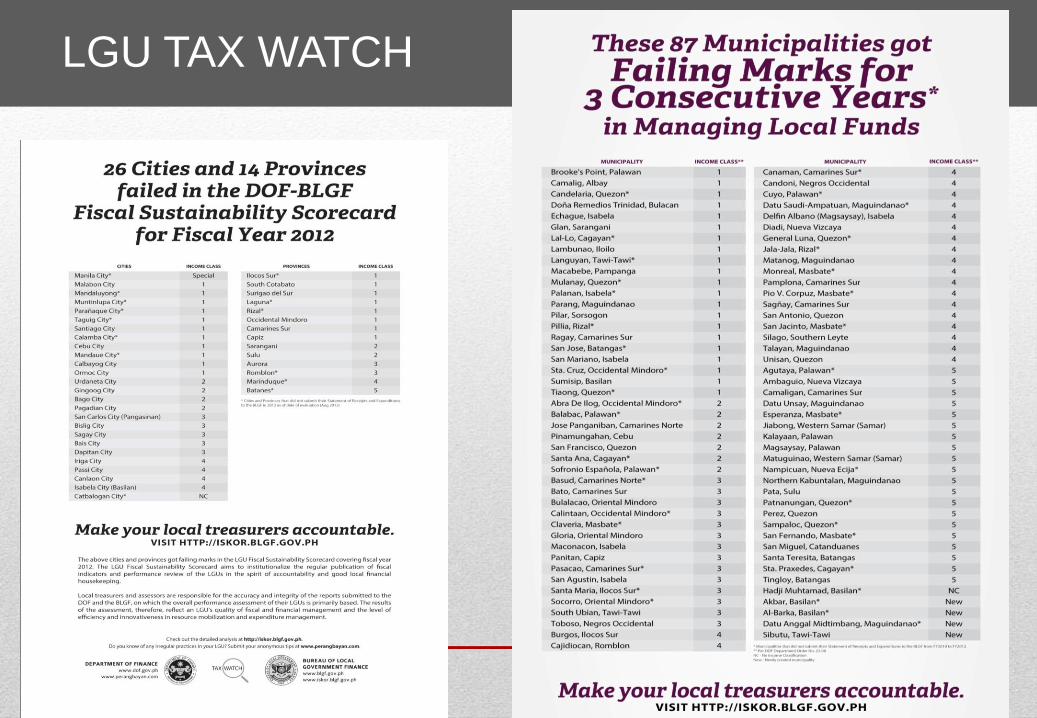

• LGU Fiscal Sustainability Scorecard, Publication of Fiscal Performance of LGUs and Tax Watch Advertisements (http://iskor.blgf.gov.ph)

• Performance Standards for Local Treasurers (forthcoming)

• Updating of Treasury and Assessment Operations Manuals (ongoing)

• Scaling up of land governance and valuation reforms in more LGUs

• Capacity building programs on updating of property values

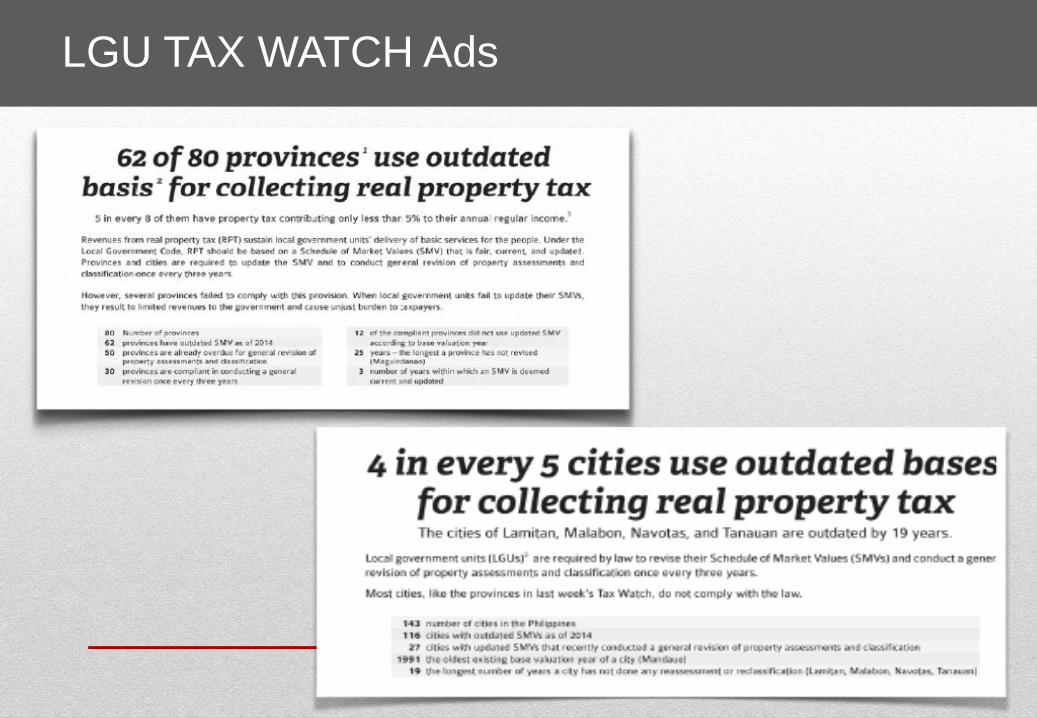

LGU TAX WATCH Ads

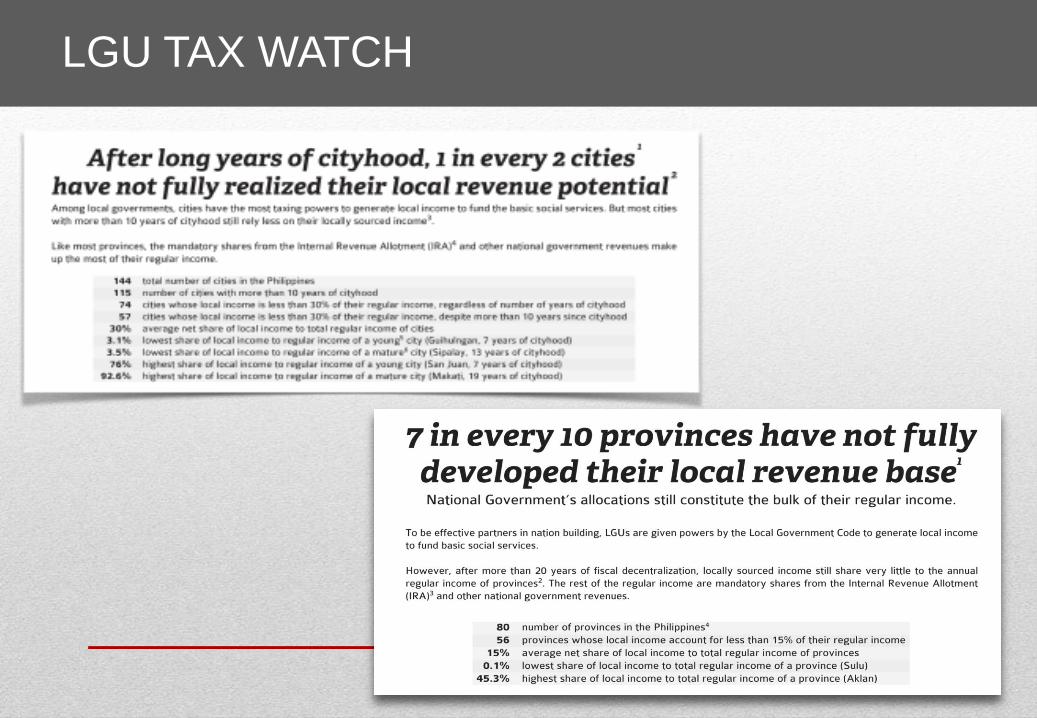

LGU TAX WATCH

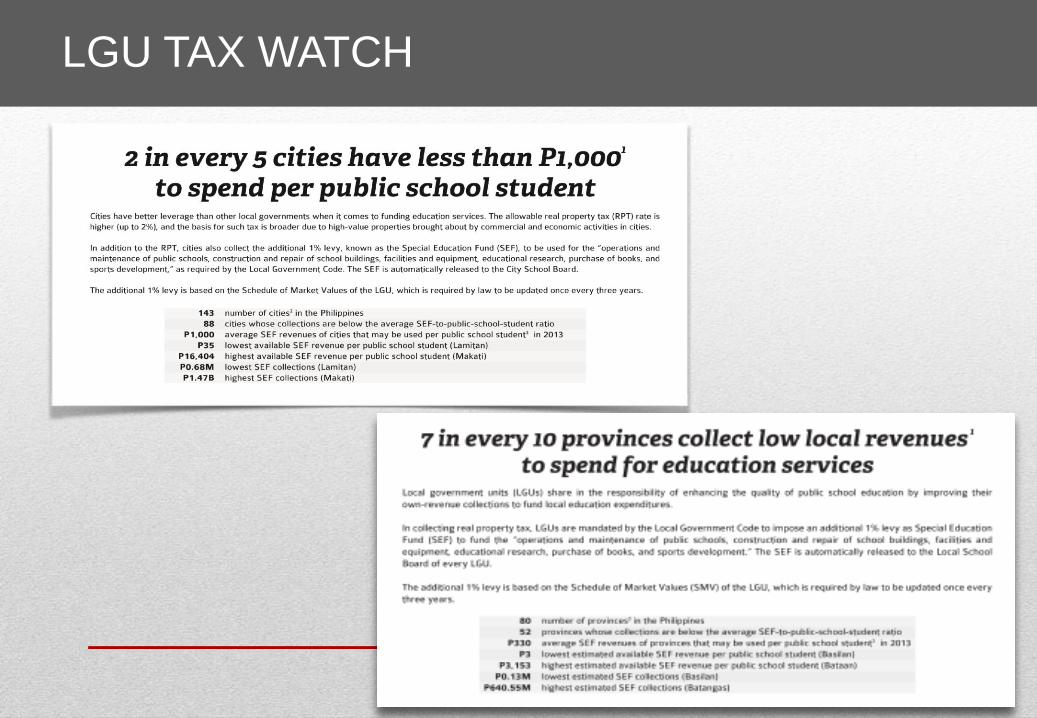

LGU TAX WATCH

LGU TAX WATCH

LGU TAX WATCH

LGU TAX WATCH

Moving forward

Review of the fiscal provisions of the 1991 Local Government Code: consider amendments on tax assignments and revenue mandates

Review current regulations on utilization of national transfers, local fiscal incentives, subnational borrowing, etc.

Prioritize the key legislation pending in Congress:

Valuation Reform Bill: recentralize the approval of property valuations

Income Classification Bill for the Secretary of Finance to set income brackets and to regularly reclassify local governments every 3 years

Bill increasing the income requirement for creation of cities from Php100M to Php250M (which may be increased every 3 years).

Continuous monitoring/technical assistance through oversight agencies: improve accountability and transparency, more capacity building for resource mobilization, harmonize PFM tools at the local levels, among others

Focus on rural areas/local governments with high poverty incidence

THANK YOU & MABUHAY!

Related Documents