Indonesia Infrastructure: Buy cement, transport Building blocks in place: positioning for multi-year growth in infra spending Robust macro story, coupled with fiscal budget deployment, to propel infrastructure spending and unlock pent-up growth. Government targeting to pass land acquisition law by 3Q11, enhancing investor-friendly stance. Positive leading indicators, with demand for cement and bulk cement up sharply in 1Q11. Supportive macro news and possibility of credit rating upgrade. Initiating on six toll road operators and cement, steel and construction companies. Forecasting 3-yr EBITDA CAGR of 16%. Key analysis in this anchor report includes: • Cement benefits most through multiplier effect. Bullish on toll roads, with new land law clearing way for development. Neutral on steel and construction on rising commodity prices and import competition. • BUY Semen Gresik (SMGR IJ - cement), Jasa Marga (JSMR IJ - transport) and Semen Cibinong (SMCB IJ - cement). NEUTRAL on Indocement (INTP IJ - cement), Krakatau Steel (KRAS IJ - steel) and Wijaya Karya (WIKA IJ - construction). EQUITY RESEARCH ANCHOR REPORT See Appendix A-1 for analyst certification and important disclosures. Analysts employed by non-US affiliates are not registered or qualified as research analysts with FINRA in the US. May 2, 2011 Research analysts Indonesia Basic Materials Wilianto Ie - PTNI [email protected] +62 21 2991 3341 Andy Lesmana - PTNI [email protected] +62 21 2991 3344

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Indonesia Infrastructure: Buy cement, transport

Building blocks in place: positioning for multi-year growth in infra spending

Robust macro story, coupled with fiscal budget deployment, to propel infrastructure spending and unlock pent-up growth.

Government targeting to pass land acquisition law by 3Q11, enhancing investor-friendly stance. Positive leading indicators, with demand for cement and bulk cement up sharply in 1Q11.

Supportive macro news and possibility of credit rating upgrade.

Initiating on six toll road operators and cement, steel and construction companies. Forecasting 3-yr EBITDA CAGR of 16%.

Key analysis in this anchor report includes:

• Cement benefits most through multiplier effect. Bullish on toll roads, with new land law clearing way for development. Neutral on steel and construction on rising commodity prices and import competition.

• BUY Semen Gresik (SMGR IJ - cement), Jasa Marga (JSMR IJ - transport) and Semen Cibinong (SMCB IJ - cement). NEUTRAL on Indocement (INTP IJ - cement), Krakatau Steel (KRAS IJ - steel) and Wijaya Karya (WIKA IJ - construction).

EQUITY RESEARCH

AN

CH

OR

RE

PO

RT

See Appendix A-1 for analyst certification and important disclosures. Analysts employed by non-US affiliates are not registered or qualified as research analysts with FINRA in the US.

May 2, 2011

Research analysts

Indonesia Basic Materials

Wilianto Ie - PTNI [email protected] +62 21 2991 3341

Andy Lesmana - PTNI [email protected] +62 21 2991 3344

Rating: See report end for details of Nomura’s rating system.

Indonesia Infrastructure

Basic Materials

EQUITY RESEARCH

Buy cement, transport

Building blocks in place: positioning for multi-year growth in infra spending

May 2, 2011

Action: Bullish on Indonesia infrastructure sector Indonesia's infrastructure development looks set to accelerate as the government gears up spending (the Ministry of Public Works budget is up 60% y-y and capital spending is up 43% y-y in 2011) and policies remain favourable for investors (eg, land acquisition bill and funding support). Leading indicators confirm a pickup in infra spending, with demand up 8% y-y for cement and 23% y-y for bulk cement in 1Q11.

Catalysts: Legislation of land law and macro-related newsflow Issue of the much-expected land acquisition law will be key to driving the infrastructure sector, in our view. Government and parliament target to pass the bill by 3Q11. Meanwhile, positive newsflow on the country's macroeconomy, including a possible credit rating upgrade to investment grade, should help to fuel further interest in the sector.

Sectors favoured: cement and transport We initiate coverage of the sector with Semen Gresik (largest cement player, with 20% y-y capacity expansion in 2012) and Jasa Marga (main toll road company, key beneficiary of land acquisition law) as our top picks. We also like Holcim (third-largest cement player, strong in bulk cement) and are NEUTRAL on Indocement (cement), Krakatau Steel (steel) and Wijaya Karya (construction).

Valuation We forecast three-year revenue and EBITDA CAGRs of 16% to 2013, driven by volume expansion. We value the infrastructure-related stocks using DCF methodology to capture three-year growth prospects.

Risks Higher production costs as a result of rising prices of commodities (iron ore, steel) and energy (mainly coal) are a key risk to the sector. The political environment, fiscal position, and external factors affecting the macro environment are also risks to the general sector.

Fig. 1: Summary of recommendations and valuations

Source: Nomura estimates

Anchor themes

Indonesia's economy looks set to take on a new growth trajectory. The robust macro story, coupled with fiscal budget deployment, should help propel investment spending in infrastructure, further unlocking growth potential.

Nomura vs consensus

Nomura's earnings forecasts for the aggregate sector are on average below consensus by 3-6% on EBITDA and 7% on net earnings.

Research analysts

Indonesia Basic Materials

Wilianto Ie - PTNI [email protected] +62 21 2991 3341

Andy Lesmana - PTNI [email protected] +62 21 2991 3344

Tgt Price % up /

Stocks Rec. (Rp/shr) downside PE 11F PE 12F EV / EBITDA 11F EV / EBITDA 12F

Gresik (SMGR IJ) Buy 11,700 23.8% 14.5 12.8 9.9 7.8

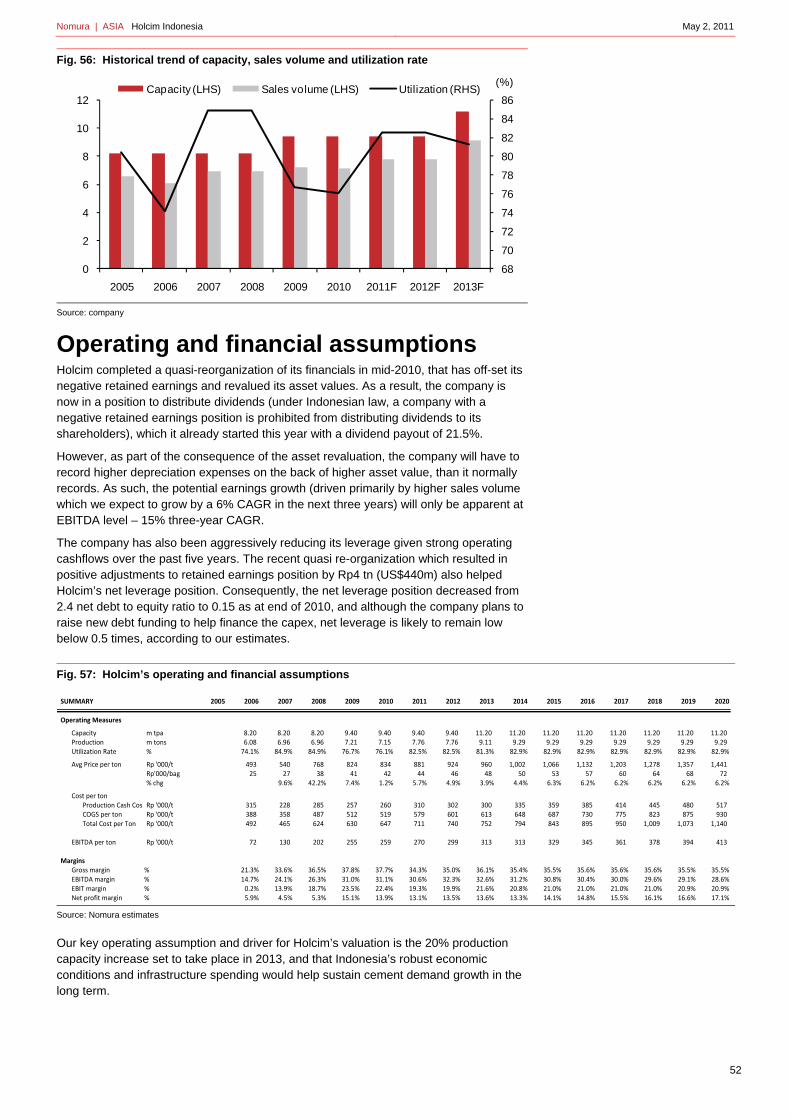

Holcim (SMCB IJ) Buy 2,700 18.7% 18 16.6 8 7.5

Indocement (INTP IJ) Neutral 17,200 0.6% 18 17.5 11.1 10.3

Jasa Marga (JSMR IJ) Buy 4,100 24.2% 11.5 9.2 10.7 9.9

Krakatau (KRAS IJ) Neutral 1,340 14.5% 12.6 9.5 9.5 7.6

Wijaya (WIKA IJ) Neutral 780 14.7% 11.7 11.8 5.2 5

Valuation at target price

See Appendix A-1 for analyst certification and important disclosures. Analysts employed by non US affiliates are not registered or qualified as research analysts with FINRA in the US.

Nomura | AEJ Indonesia Infrastructure May 2, 2011

2

Contents

3 Bullish on Indonesia infrastructure sector

4 Companies in brief

4 Why now?

5 Robust macroeconomic story

8 Nomura’s view on Indonesia’s macro outlook

9 Increasing government spending raises prospect of more infrastructure spending realisation

11 Investor-friendly regulatory framework

13 Risks

14 Cement: Bullish

14 Action: BUY Gresik and Holcim; NEUTRAL on Indocement

20 Company comparison

21 Transport: Bullish

21 Action: BUY Jasa Marga

23 Steel and construction: Neutral

26 Steel industry outlook

30 Semen Gresik

39 Indocement Tunggal Perkasa

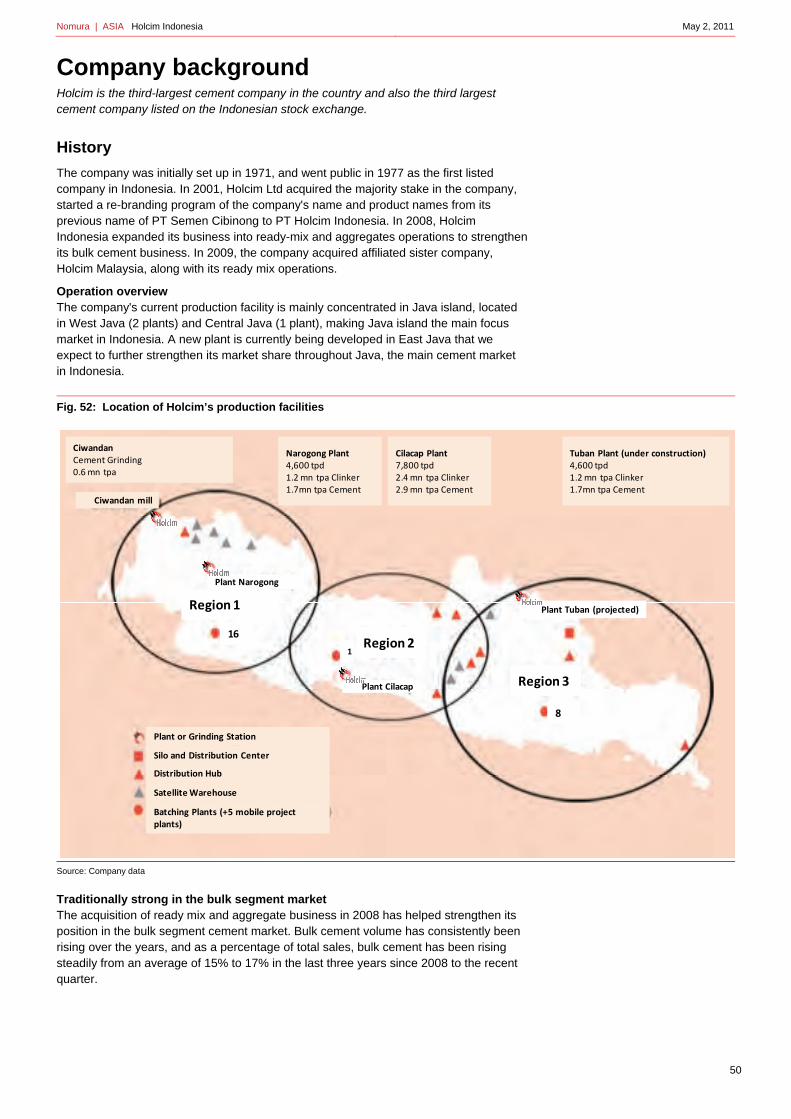

47 Holcim Indonesia

55 Jasa Marga

63 Krakatau Steel

71 Wijaya Karya

78 Appendix A-1

Nomura | AEJ Indonesia Infrastructure May 2, 2011

3

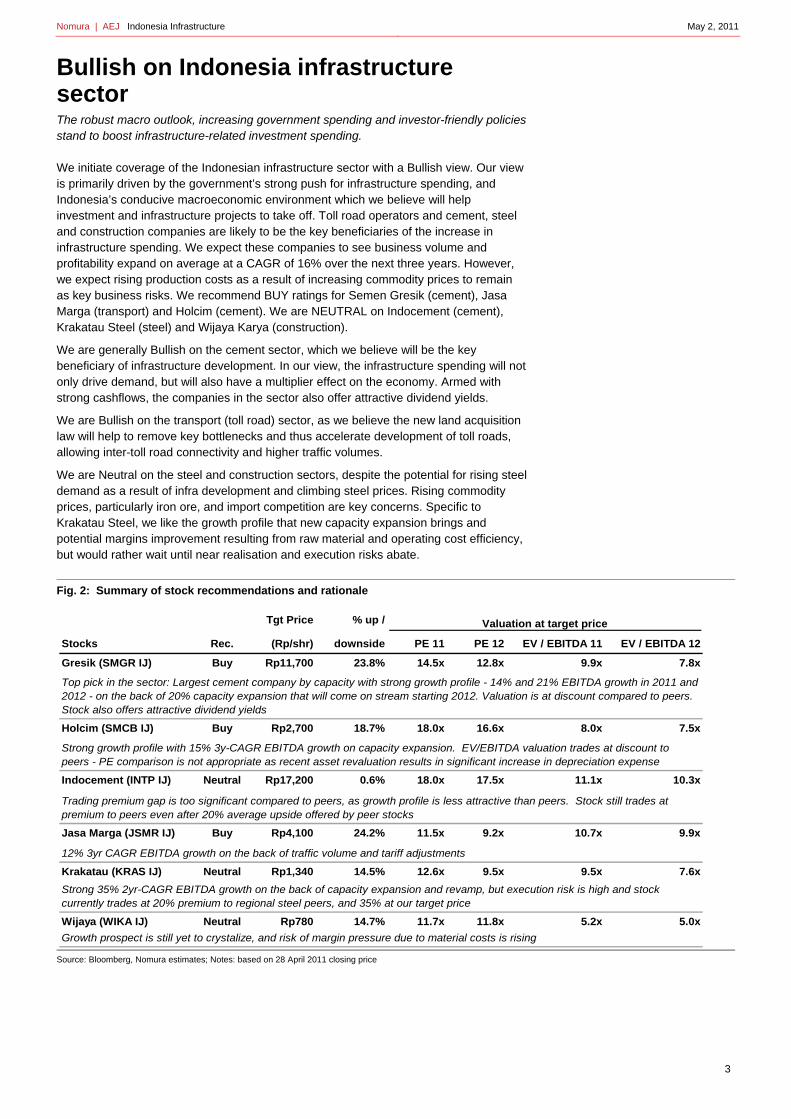

Bullish on Indonesia infrastructure sector The robust macro outlook, increasing government spending and investor-friendly policies stand to boost infrastructure-related investment spending.

We initiate coverage of the Indonesian infrastructure sector with a Bullish view. Our view is primarily driven by the government’s strong push for infrastructure spending, and Indonesia’s conducive macroeconomic environment which we believe will help investment and infrastructure projects to take off. Toll road operators and cement, steel and construction companies are likely to be the key beneficiaries of the increase in infrastructure spending. We expect these companies to see business volume and profitability expand on average at a CAGR of 16% over the next three years. However, we expect rising production costs as a result of increasing commodity prices to remain as key business risks. We recommend BUY ratings for Semen Gresik (cement), Jasa Marga (transport) and Holcim (cement). We are NEUTRAL on Indocement (cement), Krakatau Steel (steel) and Wijaya Karya (construction).

We are generally Bullish on the cement sector, which we believe will be the key beneficiary of infrastructure development. In our view, the infrastructure spending will not only drive demand, but will also have a multiplier effect on the economy. Armed with strong cashflows, the companies in the sector also offer attractive dividend yields.

We are Bullish on the transport (toll road) sector, as we believe the new land acquisition law will help to remove key bottlenecks and thus accelerate development of toll roads, allowing inter-toll road connectivity and higher traffic volumes.

We are Neutral on the steel and construction sectors, despite the potential for rising steel demand as a result of infra development and climbing steel prices. Rising commodity prices, particularly iron ore, and import competition are key concerns. Specific to Krakatau Steel, we like the growth profile that new capacity expansion brings and potential margins improvement resulting from raw material and operating cost efficiency, but would rather wait until near realisation and execution risks abate.

Fig. 2: Summary of stock recommendations and rationale

Source: Bloomberg, Nomura estimates; Notes: based on 28 April 2011 closing price

Tgt Price % up /

Stocks Rec. (Rp/shr) downside PE 11 PE 12 EV / EBITDA 11 EV / EBITDA 12

Gresik (SMGR IJ) Buy Rp11,700 23.8% 14.5x 12.8x 9.9x 7.8x

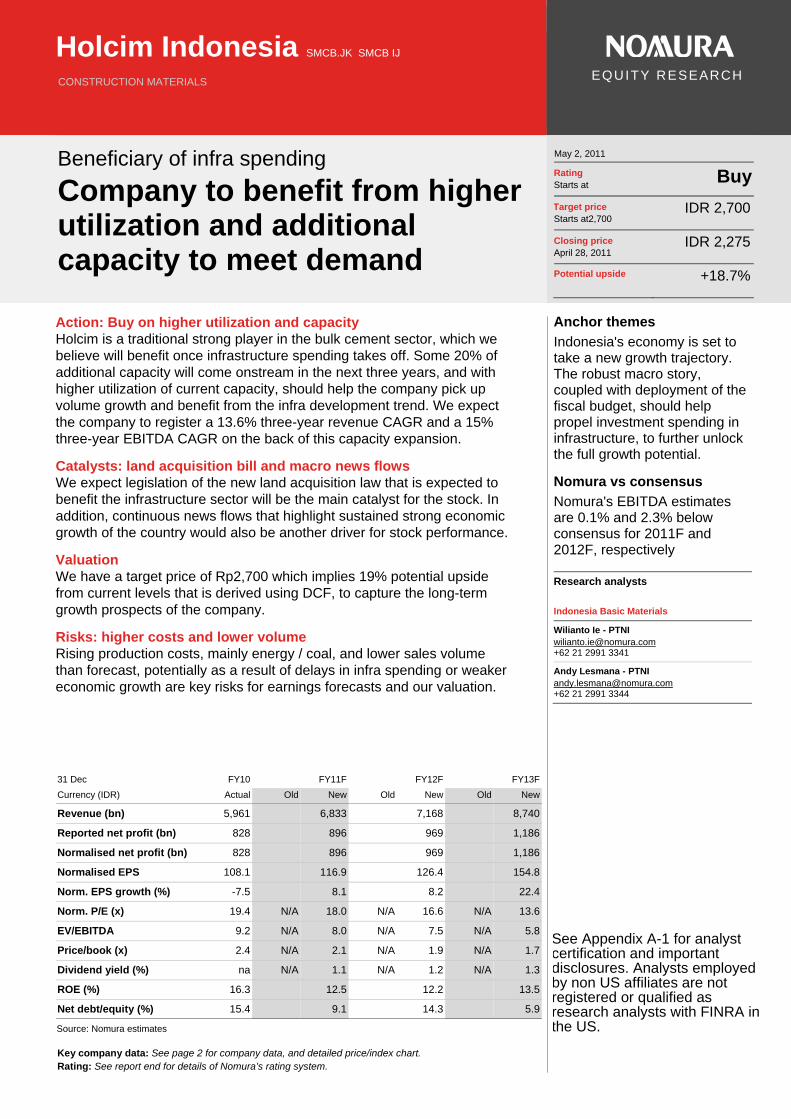

Holcim (SMCB IJ) Buy Rp2,700 18.7% 18.0x 16.6x 8.0x 7.5x

Indocement (INTP IJ) Neutral Rp17,200 0.6% 18.0x 17.5x 11.1x 10.3x

Jasa Marga (JSMR IJ) Buy Rp4,100 24.2% 11.5x 9.2x 10.7x 9.9x

Krakatau (KRAS IJ) Neutral Rp1,340 14.5% 12.6x 9.5x 9.5x 7.6x

Wijaya (WIKA IJ) Neutral Rp780 14.7% 11.7x 11.8x 5.2x 5.0x

Valuation at target price

Top pick in the sector: Largest cement company by capacity with strong growth profile - 14% and 21% EBITDA growth in 2011 and 2012 - on the back of 20% capacity expansion that will come on stream starting 2012. Valuation is at discount compared to peers. Stock also offers attractive dividend yields

Strong growth profile with 15% 3y-CAGR EBITDA growth on capacity expansion. EV/EBITDA valuation trades at discount to peers - PE comparison is not appropriate as recent asset revaluation results in significant increase in depreciation expense

Growth prospect is still yet to crystalize, and risk of margin pressure due to material costs is rising

Trading premium gap is too significant compared to peers, as growth profile is less attractive than peers. Stock still trades at premium to peers even after 20% average upside offered by peer stocks

12% 3yr CAGR EBITDA growth on the back of traffic volume and tariff adjustments

Strong 35% 2yr-CAGR EBITDA growth on the back of capacity expansion and revamp, but execution risk is high and stock currently trades at 20% premium to regional steel peers, and 35% at our target price

Nomura | AEJ Indonesia Infrastructure May 2, 2011

4

Companies in brief

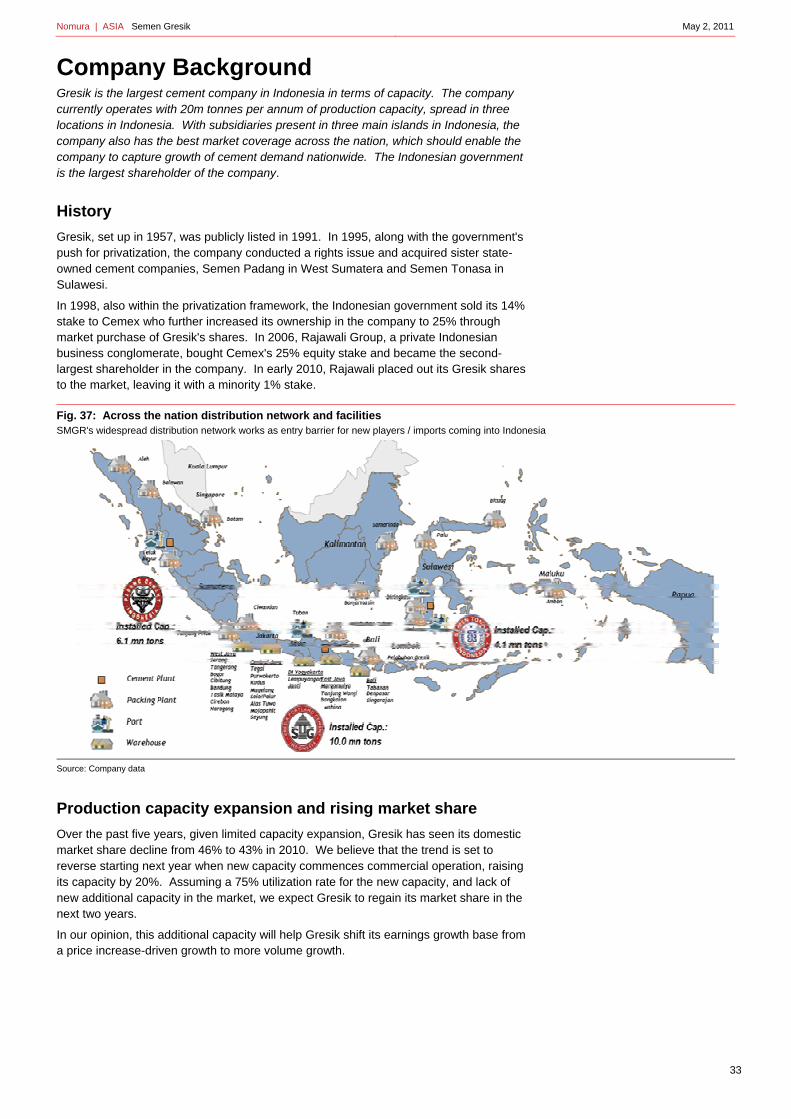

Semen Gresik (SMGR IJ, BUY) We believe Semen Gresik has the best market exposure across Indonesia, attributable to its spread of production capacity (West Sumatra, East Java and Sulawesi). As the largest cement producer in Indonesia, with 20mn tonnes capacity, Gresik has been losing market share over the past few years due to capacity constraints. However, with its planned new capacity, Gresik should start to regain market share.

Holcim Indonesia (SMCB IJ, BUY) Holcim Indonesia has a strong position in the bulk cement market, which we see as the key demand driver when infrastructure projects kick in. Holcim has a total domestic capacity of 8.7mn tonnes, of which only 62% is allocated for the domestic market (higher prices, higher profits), leaving enough capacity to fill in/benefit from strong growth in infrastructure demand (exports have lower prices and lower profitability).

Indocement (INTP IJ, NEUTRAL) Similar to Gresik, Indocement also has nationwide exposure in the areas of potential growth, and the company will also undertake capacity expansion in the next 2-3 years. However, the magnitude of the planned expansion is less than that at Gresik and Holcim, making its growth profile less attractive compared to its peers, while valuation remains rich. Thus, we initiate coverage with a NEUTRAL position on the stock.

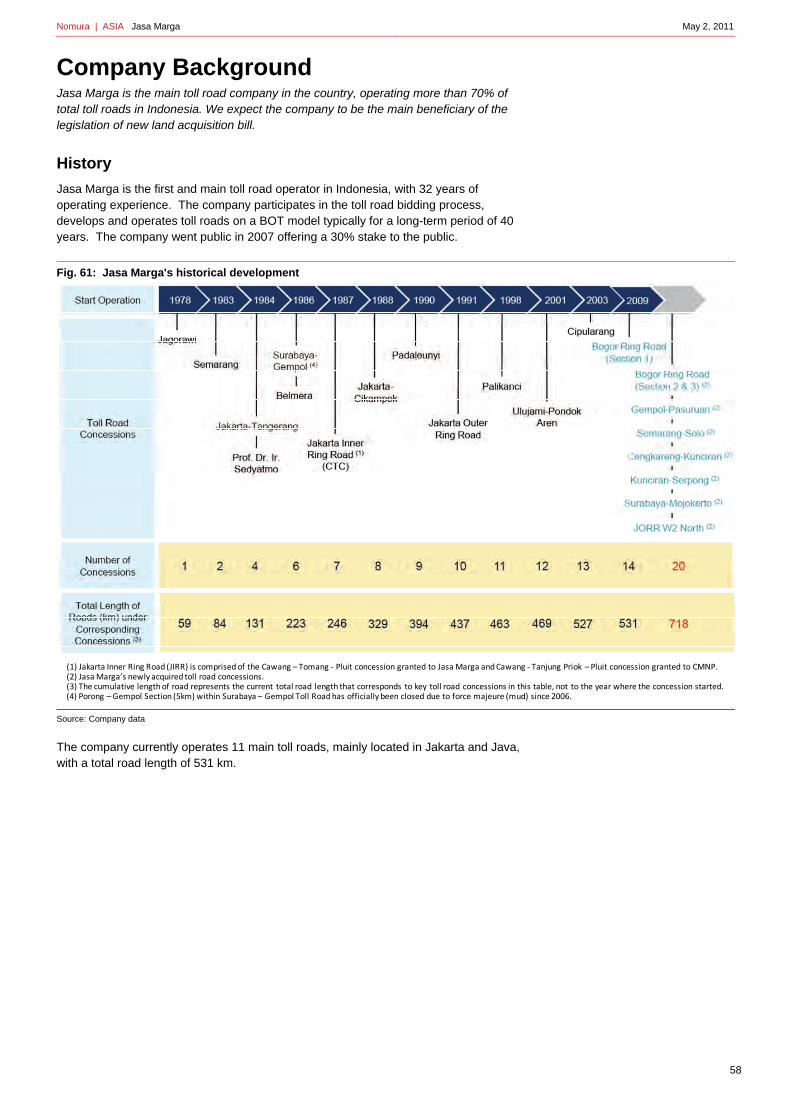

Jasa Marga (JSMR IJ, BUY) Jasa Marga is the main toll road operator in Indonesia, operating more than 70% of the toll roads (by length) and more than 80% of the toll road traffic (source: Jasa Marga). We believe it will be the main beneficiary of the upcoming new land acquisition law, which should help to accelerate ongoing toll road development, increase toll road connectivity and hence boost traffic volumes.

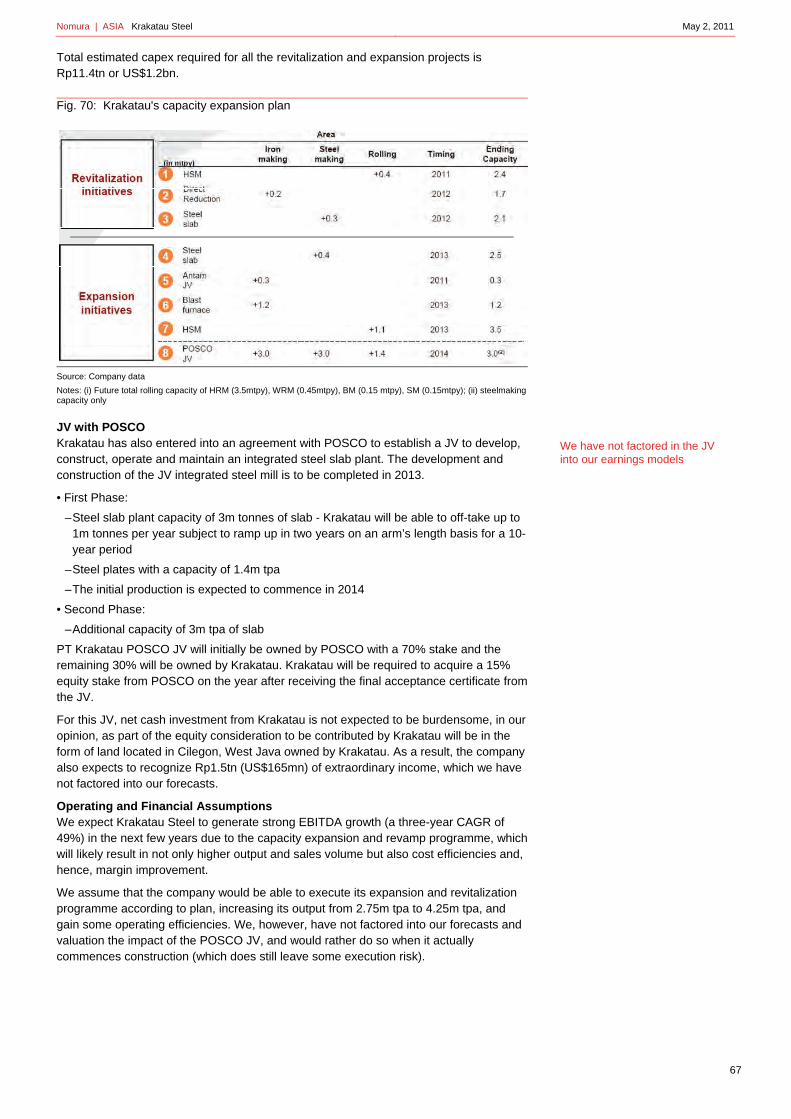

Krakatau Steel (KRAS IJ, NEUTRAL) Krakatau Steel is the largest integrated steel producer in Indonesia, and the company is revamping and expanding its production capacity. It plans to increase its production capacity from 2.8mn tpa currently to 4.25mn tpa by 2014. The company is adding blasting furnace production capacity that is more cost efficient than the current production facility (EAF-based) and this should help to reduce production costs by 5%.

Additional production capacity of 3mn tpa is also being developed under a joint venture with POSCO, whereby Krakatau will eventually have 45% equity interest. We expect the government to grant tax incentives in the form of a tax holiday and Krakatau to record Rp1.5tn of extraordinary gains from land sales to the JV.

Wijaya Karya (WIKA IJ, NEUTRAL) With market cap of less than US$500mn, Wijaya Karya is the largest and most liquid construction company listed on the Indonesia Stock Exchange. We expect the company to benefit from rising construction spending, particularly from construction spending promoted by the government.

Why now?

Admittedly, progress on infrastructure development in Indonesia has lagged expectations since the government launched the infrastructure development programme in 2005. Up until now, we believe it has relied heavily on private funding and has lacked the necessary regulatory framework required to attract investor interest and raise the feasibility of infrastructure projects. The country has also suffered from a number of external factors (2004 tsunami, 2005 fuel crisis and 2008 global credit crunch).

Notwithstanding, Indonesia has seen some minor progress in infrastructure development, adding some 135km of toll road length since 2005.

Moreover, we believe conditions have changed since 2005:

Nomura | AEJ Indonesia Infrastructure May 2, 2011

5

• Significantly improved macro story: economic growth has accelerated from 5.5% in 2005 to 6% in 2010; the credit rating has improved three notches from B+ in 2005 to BB+ in 2010 (S&P); and the long-term US-dollar government bond yield has declined from an average 12.5% in 2005 to a range of 7.5-8% in 2011.

• Stronger fiscal position: the revenue budget has more than doubled from Rp495tn or US$50bn in 2005 to Rp1,100tn or US$120bn in 2011, allowing the government to increase fund allocation for infrastructure spending.

• Sufficient regulatory framework in place: the regulatory framework now includes a bill on toll tariff increases and the establishment of a toll road authority.

In addition, government efforts to encourage state-owned companies to take part in driving infrastructure spending have been well received.

The incentives driving government efforts to boost infrastructure development are strong:

• Infrastructure development is a key ingredient for Indonesia to achieve its target 7% annual economic growth by 2014, when the next elections take place.

• Indonesia will host the Asia Pacific Economic Conference in Bali in 2013.

• Indonesia will host the SEA Games in Palembang, South Sumatera in 4Q11.

Fig. 3: Infrastructure progress despite challenges Some 135km of toll roads have been added since 2005

Source: Jasa Marga

Robust macroeconomic story

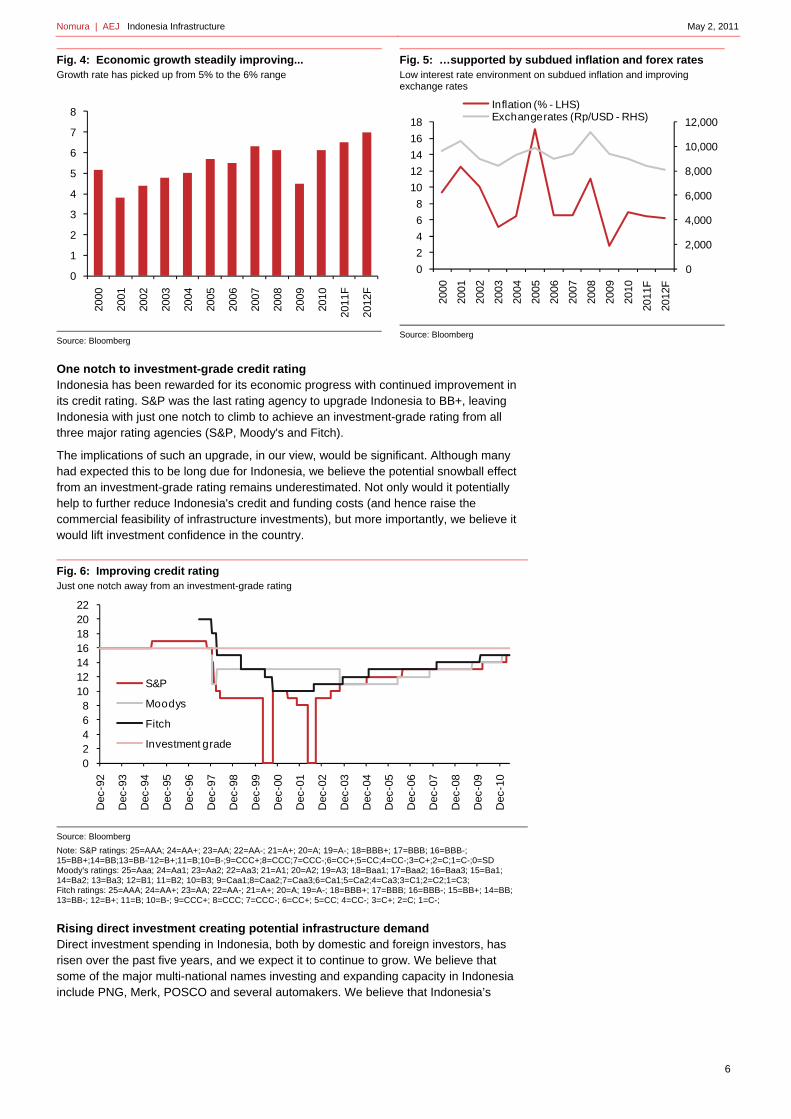

Central to our thesis of accelerating infrastructure spending is continued robust macroeconomic conditions in Indonesia. Economic growth has steadily picked up from an average of 5% pa in the first half of past decade to 6% in the past five years to 2010, and we expect the momentum to continue this year with the possibility of breaking the 7% mark. Subdued inflation, supported by stable and improving exchange rates, has resulted in a low interest rate environment.

400

500

600

700

800

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

(km)

Nomura | AEJ Indonesia Infrastructure May 2, 2011

6

Fig. 4: Economic growth steadily improving... Growth rate has picked up from 5% to the 6% range

Source: Bloomberg

Fig. 5: …supported by subdued inflation and forex rates Low interest rate environment on subdued inflation and improving exchange rates

Source: Bloomberg

One notch to investment-grade credit rating Indonesia has been rewarded for its economic progress with continued improvement in its credit rating. S&P was the last rating agency to upgrade Indonesia to BB+, leaving Indonesia with just one notch to climb to achieve an investment-grade rating from all three major rating agencies (S&P, Moody's and Fitch).

The implications of such an upgrade, in our view, would be significant. Although many had expected this to be long due for Indonesia, we believe the potential snowball effect from an investment-grade rating remains underestimated. Not only would it potentially help to further reduce Indonesia's credit and funding costs (and hence raise the commercial feasibility of infrastructure investments), but more importantly, we believe it would lift investment confidence in the country.

Fig. 6: Improving credit rating Just one notch away from an investment-grade rating

Source: Bloomberg

Note: S&P ratings: 25=AAA; 24=AA+; 23=AA; 22=AA-; 21=A+; 20=A; 19=A-; 18=BBB+; 17=BBB; 16=BBB-; 15=BB+;14=BB;13=BB-'12=B+;11=B;10=B-;9=CCC+;8=CCC;7=CCC-;6=CC+;5=CC;4=CC-;3=C+;2=C;1=C-;0=SD Moody's ratings: 25=Aaa; 24=Aa1; 23=Aa2; 22=Aa3; 21=A1; 20=A2; 19=A3; 18=Baa1; 17=Baa2; 16=Baa3; 15=Ba1; 14=Ba2; 13=Ba3; 12=B1; 11=B2; 10=B3; 9=Caa1;8=Caa2;7=Caa3;6=Ca1;5=Ca2;4=Ca3;3=C1;2=C2;1=C3; Fitch ratings: 25=AAA; 24=AA+; 23=AA; 22=AA-; 21=A+; 20=A; 19=A-; 18=BBB+; 17=BBB; 16=BBB-; 15=BB+; 14=BB; 13=BB-; 12=B+; 11=B; 10=B-; 9=CCC+; 8=CCC; 7=CCC-; 6=CC+; 5=CC; 4=CC-; 3=C+; 2=C; 1=C-;

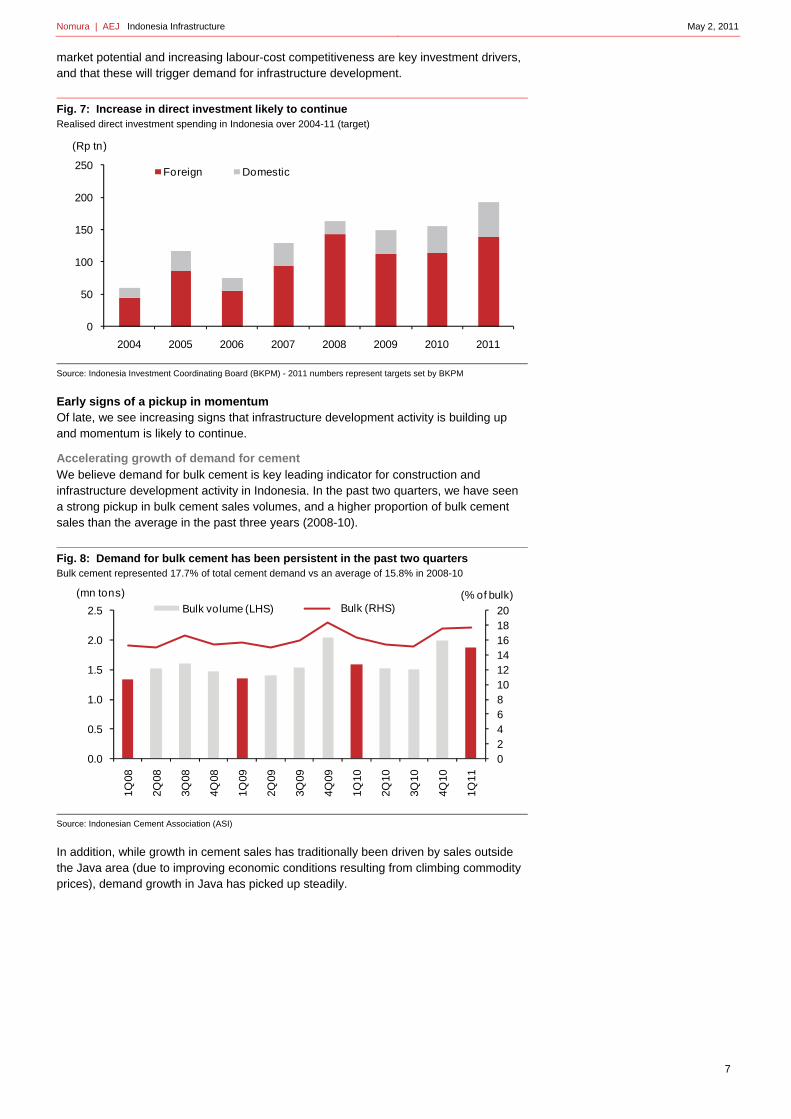

Rising direct investment creating potential infrastructure demand Direct investment spending in Indonesia, both by domestic and foreign investors, has risen over the past five years, and we expect it to continue to grow. We believe that some of the major multi-national names investing and expanding capacity in Indonesia include PNG, Merk, POSCO and several automakers. We believe that Indonesia’s

0

1

2

3

4

5

6

7

820

00

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

F

2012

F

0

2,000

4,000

6,000

8,000

10,000

12,000

0

2

4

6

8

10

12

14

16

18

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

F

2012

F

Inflation (% - LHS)Exchange rates (Rp/USD - RHS)

02468

10121416182022

Dec

-92

Dec

-93

Dec

-94

Dec

-95

Dec

-96

Dec

-97

Dec

-98

Dec

-99

Dec

-00

Dec

-01

Dec

-02

Dec

-03

Dec

-04

Dec

-05

Dec

-06

Dec

-07

Dec

-08

Dec

-09

Dec

-10

S&P

Moodys

Fitch

Investment grade

Nomura | AEJ Indonesia Infrastructure May 2, 2011

7

market potential and increasing labour-cost competitiveness are key investment drivers, and that these will trigger demand for infrastructure development.

Fig. 7: Increase in direct investment likely to continue Realised direct investment spending in Indonesia over 2004-11 (target)

Source: Indonesia Investment Coordinating Board (BKPM) - 2011 numbers represent targets set by BKPM

Early signs of a pickup in momentum Of late, we see increasing signs that infrastructure development activity is building up and momentum is likely to continue.

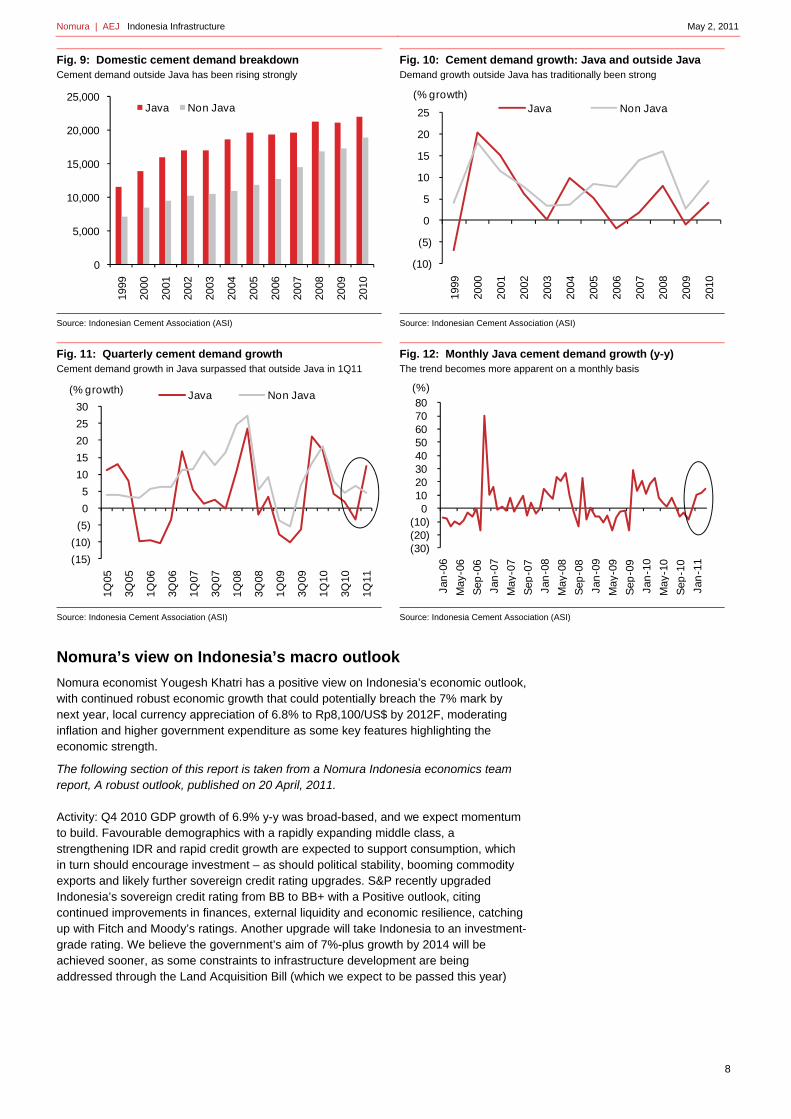

Accelerating growth of demand for cement We believe demand for bulk cement is key leading indicator for construction and infrastructure development activity in Indonesia. In the past two quarters, we have seen a strong pickup in bulk cement sales volumes, and a higher proportion of bulk cement sales than the average in the past three years (2008-10).

Fig. 8: Demand for bulk cement has been persistent in the past two quarters Bulk cement represented 17.7% of total cement demand vs an average of 15.8% in 2008-10

Source: Indonesian Cement Association (ASI)

In addition, while growth in cement sales has traditionally been driven by sales outside the Java area (due to improving economic conditions resulting from climbing commodity prices), demand growth in Java has picked up steadily.

0

50

100

150

200

250

2004 2005 2006 2007 2008 2009 2010 2011

(Rp tn)

Foreign Domestic

02468101214161820

0.0

0.5

1.0

1.5

2.0

2.5

1Q08

2Q08

3Q08

4Q08

1Q09

2Q09

3Q09

4Q09

1Q10

2Q10

3Q10

4Q10

1Q11

(% of bulk)(mn tons)

Bulk volume (LHS) Series2Bulk (RHS)

Nomura | AEJ Indonesia Infrastructure May 2, 2011

8

Fig. 9: Domestic cement demand breakdown Cement demand outside Java has been rising strongly

Source: Indonesian Cement Association (ASI)

Fig. 10: Cement demand growth: Java and outside Java Demand growth outside Java has traditionally been strong

Source: Indonesian Cement Association (ASI)

Fig. 11: Quarterly cement demand growth Cement demand growth in Java surpassed that outside Java in 1Q11

Source: Indonesia Cement Association (ASI)

Fig. 12: Monthly Java cement demand growth (y-y) The trend becomes more apparent on a monthly basis

Source: Indonesia Cement Association (ASI)

Nomura’s view on Indonesia’s macro outlook

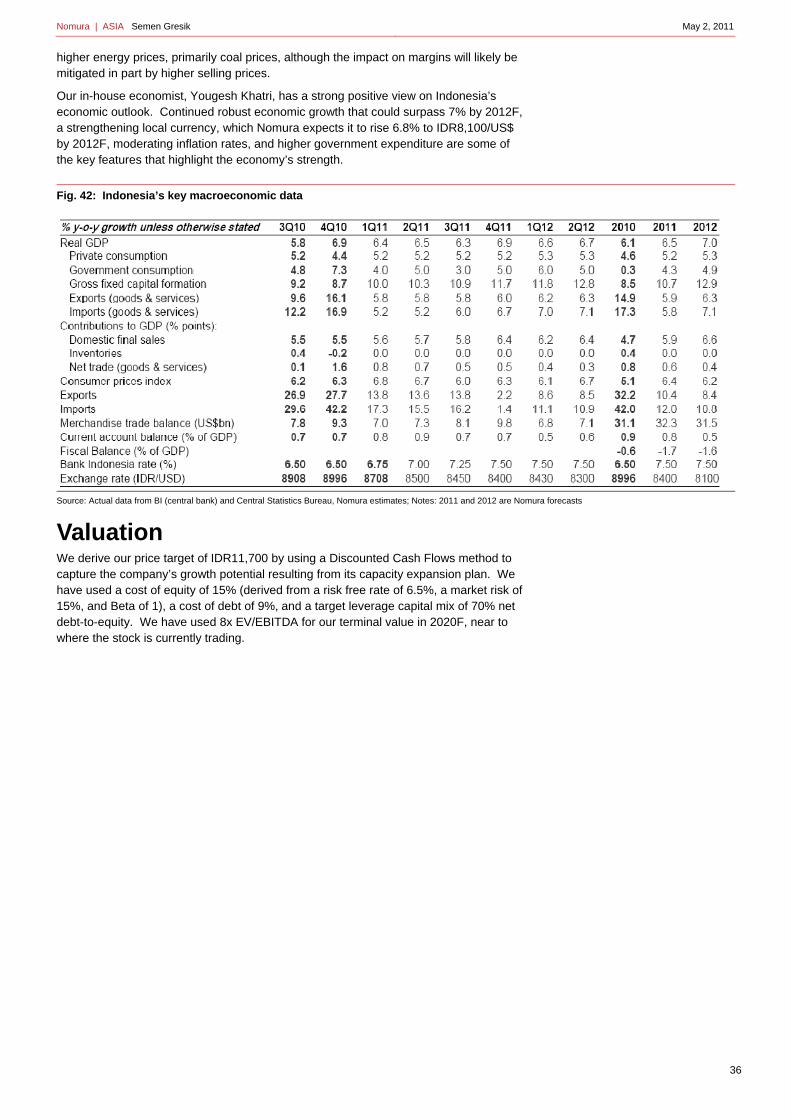

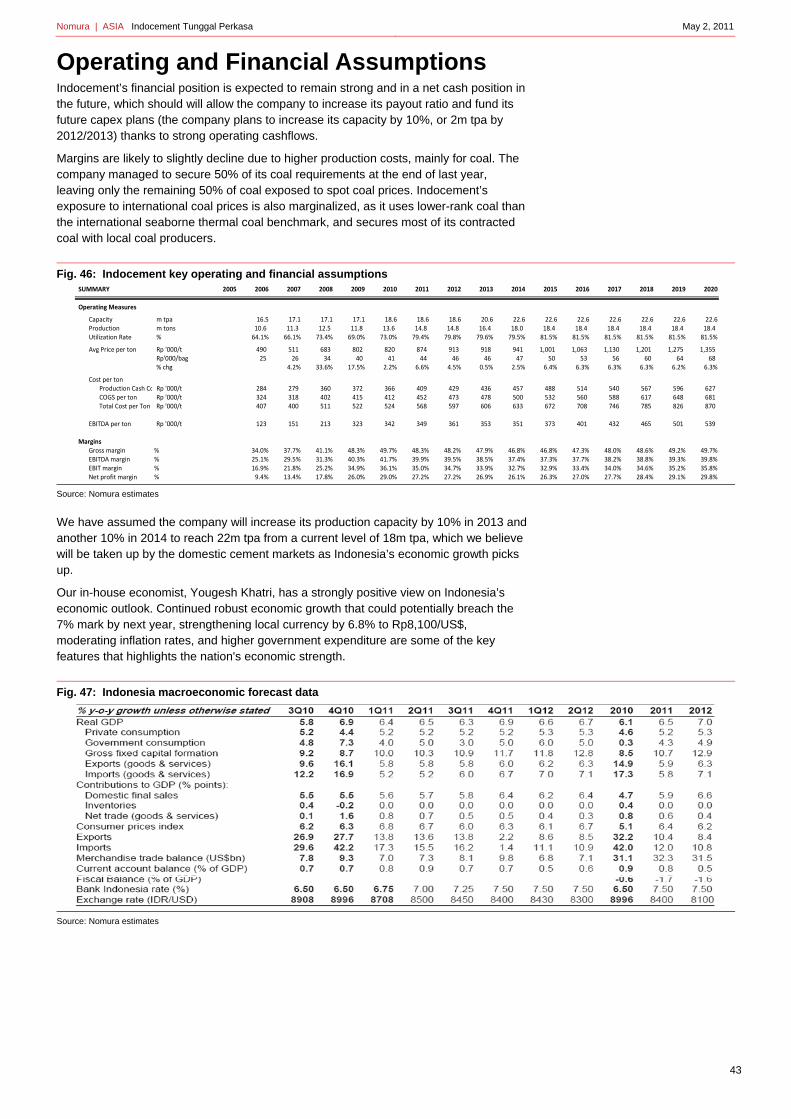

Nomura economist Yougesh Khatri has a positive view on Indonesia’s economic outlook, with continued robust economic growth that could potentially breach the 7% mark by next year, local currency appreciation of 6.8% to Rp8,100/US$ by 2012F, moderating inflation and higher government expenditure as some key features highlighting the economic strength.

The following section of this report is taken from a Nomura Indonesia economics team report, A robust outlook, published on 20 April, 2011.

Activity: Q4 2010 GDP growth of 6.9% y-y was broad-based, and we expect momentum to build. Favourable demographics with a rapidly expanding middle class, a strengthening IDR and rapid credit growth are expected to support consumption, which in turn should encourage investment – as should political stability, booming commodity exports and likely further sovereign credit rating upgrades. S&P recently upgraded Indonesia’s sovereign credit rating from BB to BB+ with a Positive outlook, citing continued improvements in finances, external liquidity and economic resilience, catching up with Fitch and Moody’s ratings. Another upgrade will take Indonesia to an investment-grade rating. We believe the government’s aim of 7%-plus growth by 2014 will be achieved sooner, as some constraints to infrastructure development are being addressed through the Land Acquisition Bill (which we expect to be passed this year)

0

5,000

10,000

15,000

20,000

25,000

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

Java Non Java

(10)

(5)

0

5

10

15

20

25

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

Java Non Java(% growth)

(15)

(10)

(5)

0

5

10

15

20

25

30

1Q05

3Q05

1Q06

3Q06

1Q07

3Q07

1Q08

3Q08

1Q09

3Q09

1Q10

3Q10

1Q11

Java Non Java(% growth)

(30)(20)(10)

0 10 20 30 40 50 60 70 80

Jan

-06

May

-06

Sep

-06

Jan

-07

May

-07

Se p

-07

Jan

-08

May

-08

Sep

-08

Jan

-09

May

-09

Se p

-09

Jan

-10

May

-10

Sep

-10

Jan

-11

(%)

Nomura | AEJ Indonesia Infrastructure May 2, 2011

9

and a planned step-up in public infrastructure investment. Stronger import growth and higher “income” outflows are expected to eventually lead to a current account deficit.

Inflation and monetary policy: Lower food prices brought down headline CPI inflation further in March to 6.7% y-y, from 6.8% y-y. Government deferral of the fuel subsidy measure pushes out the associated inflation impact. Bank Indonesia (BI) remained on hold in April as expected, but its policy statement remained hawkish – reaffirming the tightening bias and highlighting inflationary pressures from commodity prices and domestic demand. The IDR gains were flagged as part of BI’s policy to curb imported inflation. We expect one 25bp hike in each quarter this year, taking the policy rate to 7.50% by year-end. The path will depend critically on inflation and external developments. We also believe another reserve requirement rise on IDR deposits is possible (a second RR hike on FX deposits from 5% to 8% is scheduled for June). We expect capital inflows to trigger further non-market-based measures, such as the recently announced extension of the one-month holding period on SBI to six months, effective 13 May.

Fiscal policy: There is likely to be a fiscal tailwind this year with increases in infrastructure spending – the 2011 deficit target is 1.8% of GDP versus the 2010 outturn of 0.6% of GDP – together with government plans to raise expenditure realisation rates. The deferral of the plan to ban private cars from buying subsidised fuel from mid-2011 will add to already rising fuel-subsidy costs. The Ministry of Finance will likely propose a revised budget in mid-2011 with new macro assumptions including for oil prices (currently USD80/bbl) and the exchange rate.

Risks: Renewed global financial turmoil is a key external risk. Progress with infrastructure development and budgeted expenditure disbursements are key upside/downside risks to the outlook. International oil prices sustained at current or higher levels could trigger further administered fuel price increases and a stepped increase in inflation. The problems in Japan may affect Indonesia via trade, portfolio/direct investment flows, tourism and development aid.

Fig. 13: Summary of Indonesia key macroeconomic data and forecasts

Source: Nomura estimates

Increasing government spending raises prospect of more infrastructure spending realisation

We also believe that the infrastructure sector will benefit from higher government spending on infrastructure development. A strong fiscal position would allow the central government to budget more for infrastructure.

Indonesia’s current outstanding public debt sits at only 20% to GDP, and despite higher budget allocation for infrastructure spending, the current year estimates are running at a conservative budget deficit of 1.8% to GDP. Although the market already expects a rise

Nomura | AEJ Indonesia Infrastructure May 2, 2011

10

in the percentage of deficit, as a result of higher oil prices and the resulting higher subsidy, the government is still running with a budget surplus as of March 2011.

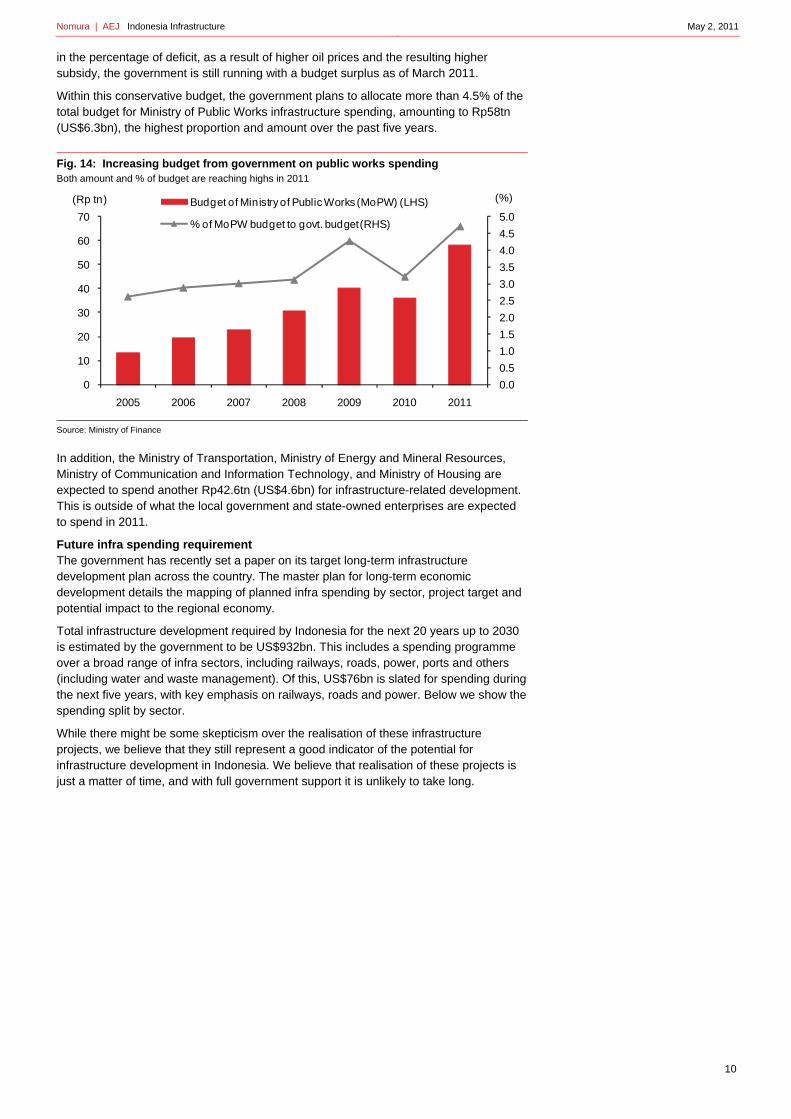

Within this conservative budget, the government plans to allocate more than 4.5% of the total budget for Ministry of Public Works infrastructure spending, amounting to Rp58tn (US$6.3bn), the highest proportion and amount over the past five years.

Fig. 14: Increasing budget from government on public works spending Both amount and % of budget are reaching highs in 2011

Source: Ministry of Finance

In addition, the Ministry of Transportation, Ministry of Energy and Mineral Resources, Ministry of Communication and Information Technology, and Ministry of Housing are expected to spend another Rp42.6tn (US$4.6bn) for infrastructure-related development. This is outside of what the local government and state-owned enterprises are expected to spend in 2011.

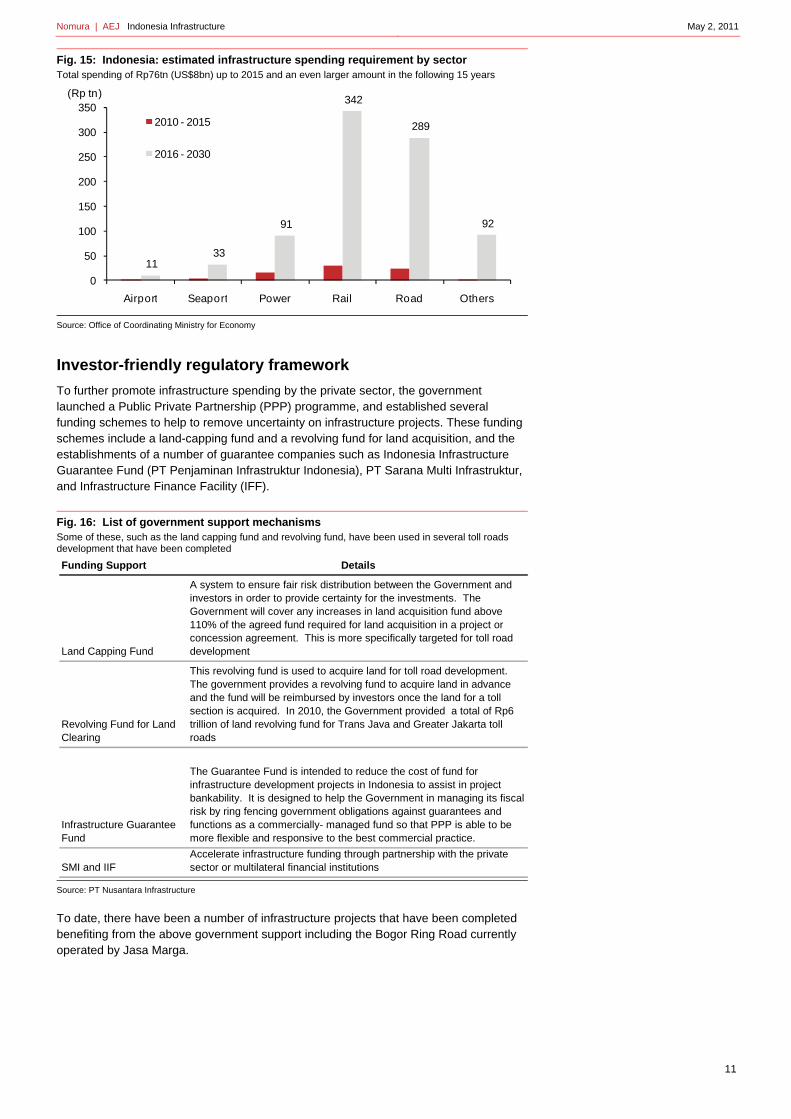

Future infra spending requirement The government has recently set a paper on its target long-term infrastructure development plan across the country. The master plan for long-term economic development details the mapping of planned infra spending by sector, project target and potential impact to the regional economy.

Total infrastructure development required by Indonesia for the next 20 years up to 2030 is estimated by the government to be US$932bn. This includes a spending programme over a broad range of infra sectors, including railways, roads, power, ports and others (including water and waste management). Of this, US$76bn is slated for spending during the next five years, with key emphasis on railways, roads and power. Below we show the spending split by sector.

While there might be some skepticism over the realisation of these infrastructure projects, we believe that they still represent a good indicator of the potential for infrastructure development in Indonesia. We believe that realisation of these projects is just a matter of time, and with full government support it is unlikely to take long.

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

5.0

0

10

20

30

40

50

60

70

2005 2006 2007 2008 2009 2010 2011

Budget of Ministry of Public Works (MoPW) (LHS)

% of MoPW budget to govt. budget (RHS)

(Rp tn) (%)

Nomura | AEJ Indonesia Infrastructure May 2, 2011

11

Fig. 15: Indonesia: estimated infrastructure spending requirement by sector Total spending of Rp76tn (US$8bn) up to 2015 and an even larger amount in the following 15 years

Source: Office of Coordinating Ministry for Economy

Investor-friendly regulatory framework

To further promote infrastructure spending by the private sector, the government launched a Public Private Partnership (PPP) programme, and established several funding schemes to help to remove uncertainty on infrastructure projects. These funding schemes include a land-capping fund and a revolving fund for land acquisition, and the establishments of a number of guarantee companies such as Indonesia Infrastructure Guarantee Fund (PT Penjaminan Infrastruktur Indonesia), PT Sarana Multi Infrastruktur, and Infrastructure Finance Facility (IFF).

Fig. 16: List of government support mechanisms Some of these, such as the land capping fund and revolving fund, have been used in several toll roads development that have been completed

Source: PT Nusantara Infrastructure

To date, there have been a number of infrastructure projects that have been completed benefiting from the above government support including the Bogor Ring Road currently operated by Jasa Marga.

11 33

91

342

289

92

0

50

100

150

200

250

300

350

Airport Seaport Power Rail Road Others

(Rp tn)

2010 - 2015

2016 - 2030

Funding Support Details

Land Capping Fund

A system to ensure fair risk distribution between the Government and investors in order to provide certainty for the investments. The Government will cover any increases in land acquisition fund above 110% of the agreed fund required for land acquisition in a project or concession agreement. This is more specifically targeted for toll road development

Revolving Fund for Land Clearing

This revolving fund is used to acquire land for toll road development. The government provides a revolving fund to acquire land in advance and the fund will be reimbursed by investors once the land for a toll section is acquired. In 2010, the Government provided a total of Rp6 trillion of land revolving fund for Trans Java and Greater Jakarta toll roads

Infrastructure Guarantee Fund

The Guarantee Fund is intended to reduce the cost of fund for infrastructure development projects in Indonesia to assist in project bankability. It is designed to help the Government in managing its fiscal risk by ring fencing government obligations against guarantees and functions as a commercially- managed fund so that PPP is able to be more flexible and responsive to the best commercial practice.

SMI and IIFAccelerate infrastructure funding through partnership with the private sector or multilateral financial institutions

Nomura | AEJ Indonesia Infrastructure May 2, 2011

12

Fig. 17: Overall public private partnership scheme Given a limited budget and a significant infrastructure spending requirement, the government is pushing for a public private partnership scheme

Source: PT Nusantara Infrastructure

Last stumbling block -- Land Acquisition Bill The Land Acquisition Bill to be passed by the parliament by the middle of this year will be important in driving infrastructure spending. With all the commercial funding support mechanisms well in place, the much-expected Land Acquisition Bill will be the last remaining stumbling block for infrastructure development to take off in a major way, in our view. It will help to provide a legal base for the government to enforce land acquisition for infrastructure development. We expect that the law will be passed by parliament scheduled in July or the early part of 3Q11.

Fig. 18: Scheduled parliament meetings and work program for Land Acquisition Bill Current target is to pass the land acquisition law at the plenary session meeting to be held in July 2011

Source: Parliament website

Activities / Progress

- Internal meeting – selection of head of Special Committee (Pansus)

- Establish work plan and work mechanics

- Meeting with government represented by relevant ministries (explanation by the Government)

- Meeting with Land Authority (BPN) and Ministry of Public Works

- Meeting with National Committee for Human Rights

- Meeting with technical experts, including experts of traditional law (hukum adat)

- Meeting with toll road authority (BPJT)

- Regional visits to Aceh, West Sumatera, Bali, Central Kalimantan and Papua

- Summary of meetings and visits

- Presentation to parliament members on summary of meetings and visits

- Compilation of issue inventory lists (Daftar Inventaris Masalah – DIM)

- Compile list of issues from parliament members by office of parliament secretary

- Delivers list of issues to the Government by office of secretary

- Meeting with Government to discuss list of issues

- Establish Working Committee

- Parliament overseas visits

- Working Committee internal meeting and meeting with Government

- Working Committee meeting continues

- Establish Drafting Team

- Meetings of Drafting Team

- Establish Synchronization Team

- Meetings of Synchronization Team of the draft Land Acquisition Law

- Reports by Drafting Team and Synchronization Team to Working Committee

- Report Meeting of Working Committee to the Parliament

- Plenary Session Meeting to Legislate the new Land Acquisition Law (July 15)

July

Timeline

February

March

April

May

June

Nomura | AEJ Indonesia Infrastructure May 2, 2011

13

Once the bill is passed, some additional implementing regulation will need to be issued for the law to become fully effective. However, given the strong support that we have seen so far for this law to be passed, we do not expect the issue of the implementing regulation to be prolonged.

However, in our view, the key caveat to successful implementation of the land acquisition bill will be the coordination amongst the various government institutions to implement the regulations.

Key features in the new land acquisition bill are:

• Land title/rights within public infrastructure corridor will automatically be cancelled.

• Public infrastructure includes: road, airport, seaport, power plant, power transmission grid, flood canal, and other infrastructure projects deemed important by the President of the Republic Indonesia.

• Compensation to landowners will be decided through appraisal by an independent committee that includes third-party appraisers, local governments, representatives of the local community and the Ministry of Public Works.

• Landowners that disagree with the compensation price can appeal to the courts and the court will have to decide within 30 days with no further appeal allowed. Regardless, the land title/rights will be cancelled immediately and the infrastructure projects can proceed.

The proposed land acquisition bill is being socialised to the people and has so far seen very little push-back from law makers and NGOs. The key issue raised is only the inclusion of the statement “... and other infrastructure projects deemed important by the President”, as this is seen as giving too much flexibility to the President.

Risks

Key risks to our thesis and view on infrastructure spending include Indonesia's macro conditions (lower growth, higher inflation and higher interest rates that will reduce return on infrastructure investment and hence investors' appetite in infrastructure), and government budget strains (either as a result of lower revenue collection, or higher spending in other sectors such as subsidies). Political factors could also be a risk, but we view it as very minimal.

Nomura | AEJ Indonesia Infrastructure May 2, 2011

14

Cement: Bullish We see the cement sector as the key beneficiary of Indonesia’s infrastructure story. Its use in a wide range building development should see the sector benefit from infrastructure spending itself, as well as the multiplier effect it brings for the economy.

Action: BUY Gresik and Holcim; NEUTRAL on Indocement

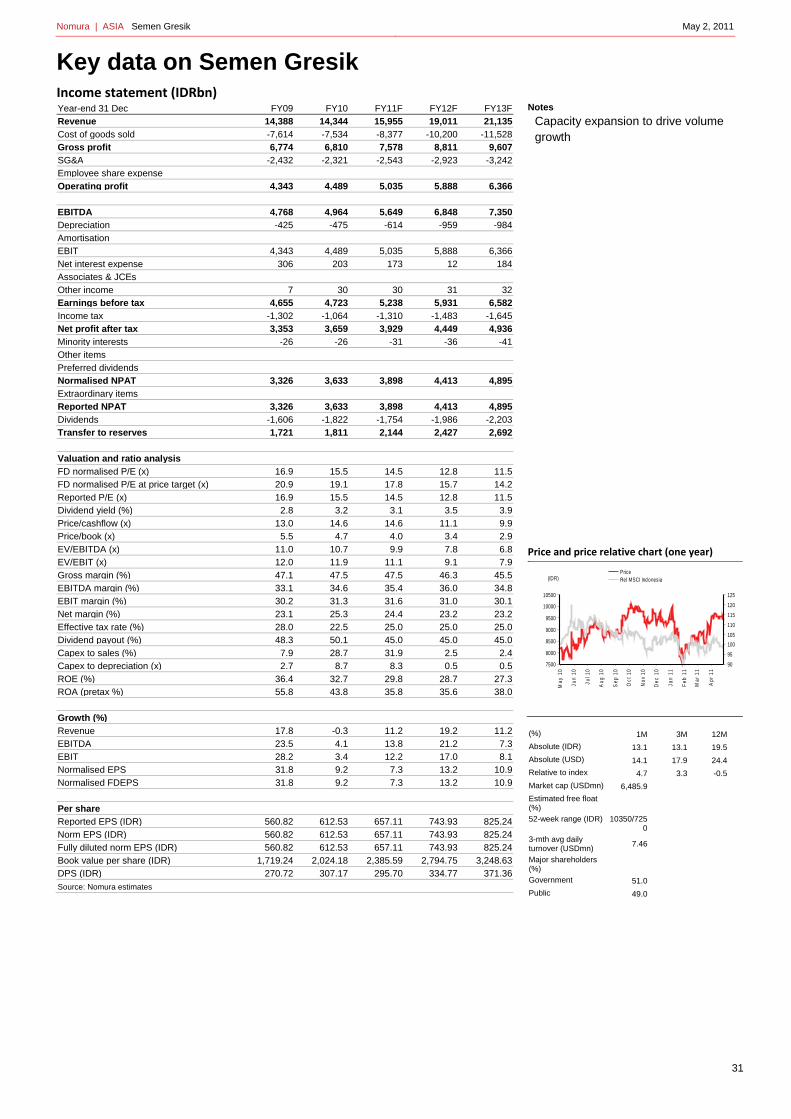

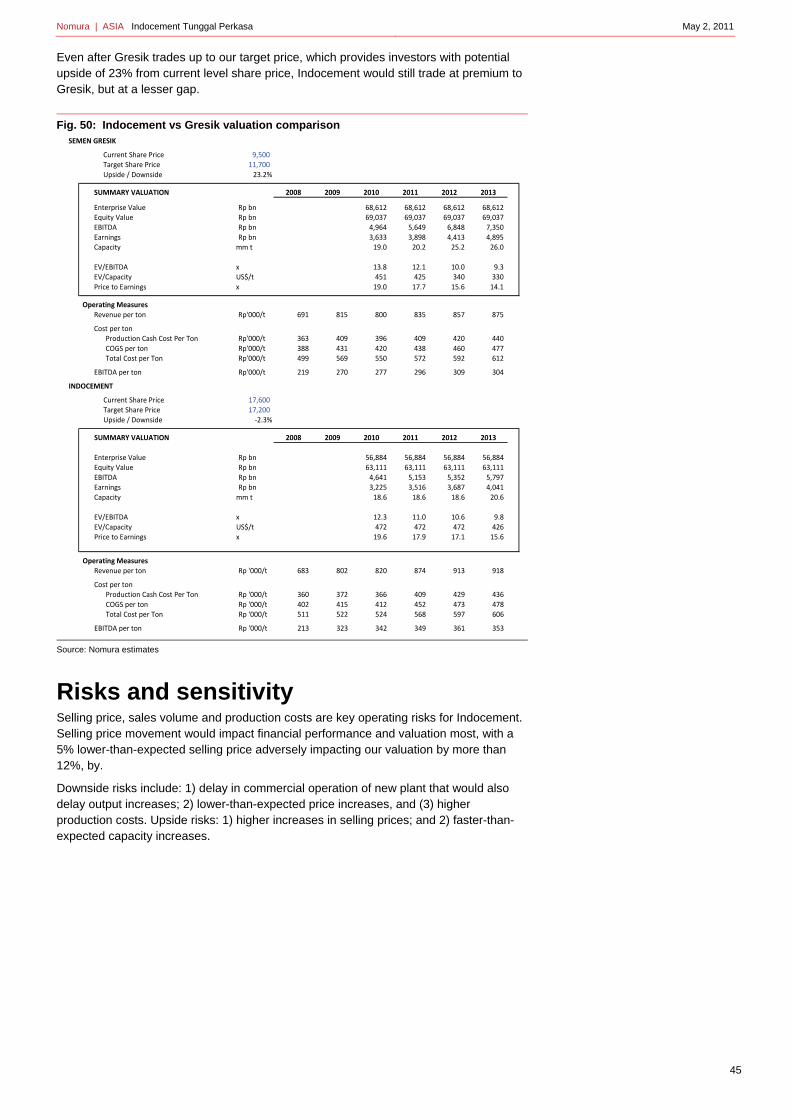

We initiate coverage of the Indonesian cement sector with BUY ratings on Semen Gresik (SMGR IJ) and Holcim Indonesia (SMCB IJ), and a NEUTRAL rating on Indocement (INTP IJ).

Investment thesis Our key investment thesis on the sector is volume growth driven by capacity expansion over the next five years and near-term selling price increase.

Volume growth on capacity expansion of 23% over next three years We expect the three listed cement companies to increase their capacity by a combined 23% from the current capacity of 46m tonnes to slightly more than 57mn tonnes.

Semen Gresik has the most aggressive expansion plan, which aims to increase capacity by almost 20% from the current level of 20mn tpa to 25mn tpa in 2012, with commercial operation to start in the early part of the year.

Holcim Indonesia is currently constructing its plant expansion in East Java that will see its operating capacity increase by 20% from the current 9mn tpa to 11mn tpa in 2013.

Some near-term price increase, albeit minimal We expect the cement companies to increase selling prices by about 5% this year after no price adjustments in 2010. Investigations of cartels last year by the anti-monopoly body were cited by cement companies as the main reason they did not adjust selling prices to reflect higher costs. We believe that the investigation issue has been resolved and the overhang has been removed such that there now appears to be some room for the cement players to catch-up with rising costs and adjust selling prices accordingly. While there is no assurance that there will be no more investigations, we view the possibility as minimal given cement price increases are likely to be rather limited in the next three years (+5% this year and +2.5% in the next two years).

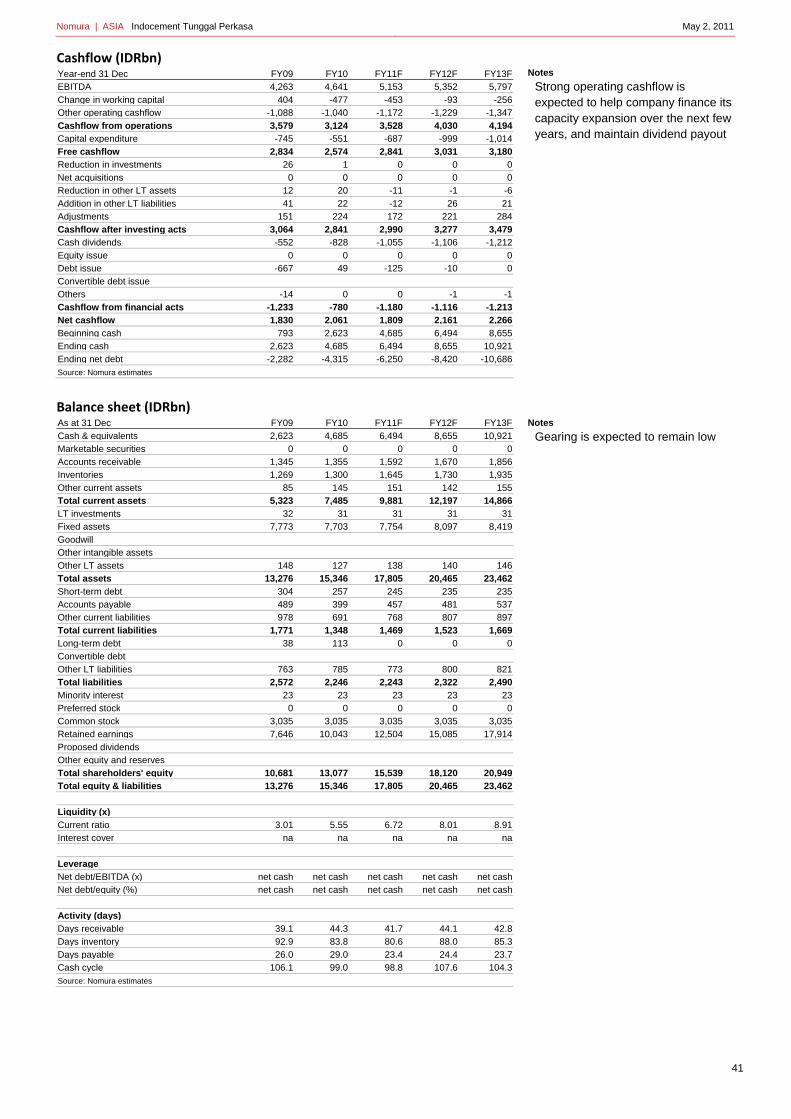

Dividend play Rising profitability and improving cashflows have allowed some cement companies to restructure their balance sheets, pay off debt and start to distribute dividends (Indocement, Holcim), while the financially stronger ones have consistently paid dividends at attractive payout ratios. Gresik has maintained a payout ratio of 45-50% for the past two years, while Indocement’s payout ratio stood at 30%. Holcim was the last company to restructure its balance sheet and started to pay out dividends this year at a 20% payout ratio.

Despite capex requirements for capacity expansion, we believe cement companies will continue to see strong operating cashflows, allowing them leverage to finance capex and remain as dividend plays.

Risks

Rising production costs Rising production costs have been cited by cement companies as the key operating risk this year, primarily those related to energy and coal in particular. In general, energy represents 50% of a cement company’s production costs and the majority of this is made up of coal.

Although some efficiency measures have been taken by replacing production facilities that allow lower-rank coal, and most coal supply contracts were secured at the end of last year, a further rise in coal prices could jeopardise profitability as some coal supply remains exposed to spot prices. We have assumed spot prices for coal of US$95/tonne for 5,000-5,500kcal quality, which is a 30% discount to the average seaborne thermal coal price of US$140/tonne (6,700kcal quality) assumed by our coal analysts.

Nomura | AEJ Indonesia Infrastructure May 2, 2011

15

Meanwhile, some cement companies that have secured their coal requirements through contract supply at prices below US$80, suggesting that the impact of coal price volatility may be rather limited and manageable.

Company recommendations

Semen Gresik (SMGR IJ, BUY) We believe Semen Gresik has the best market exposure across Indonesia, attributable to its spread of production capacity (West Sumatra, East Java and Sulawesi). As the largest cement producer in Indonesia with 20mn tonnes capacity, Gresik has been losing market share in the past few years due to capacity constraints. However, with its planned new capacity, Gresik should start to regain market share.

Holcim Indonesia (SMCB IJ, BUY) Holcim Indonesia has a strong position in the bulk cement market, which we see as the key demand driver when infrastructure projects kick in. Holcim has a total domestic capacity of 8.7mn tonnes, of which only 62% is allocated for the domestic market (higher prices, higher profits), leaving enough capacity to fill in/benefit from strong growth in infrastructure demand (exports have lower prices and lower profitability).

Indocement (INTP IJ, NEUTRAL) Similar to Gresik, Indocement also has nationwide exposure in the areas of potential growth, and the company will also undertake capacity expansion in the next 2-3 years. However, the magnitude of the planned expansion is less than that at Gresik and Holcim, making its growth profile less attractive compared to its peers, while valuation remains rich. Thus we initiate coverage with a NEUTRAL position on the stock.

Fig. 19: Cement: domestic demand trend

Source: Indonesian Cement Association (ASI), company data

0

2

4

6

8

10

12

1Q04

2Q04

3Q04

4Q04

1Q05

2Q05

3Q05

4Q05

1Q06

2Q06

3Q06

4Q06

1Q07

2Q07

3Q07

4Q07

1Q08

2Q08

3Q08

4Q08

1Q09

2Q09

3Q09

4Q09

1Q10

2Q10

3Q10

4Q10

1Q11

(mn tons) Domestic cement demand has been rising steadily at 8% pa over the past six years …

Nomura | AEJ Indonesia Infrastructure May 2, 2011

16

Fig. 20: Cement: industry capacity and utilisation rate trends

Source: Indonesian Cement Association (ASI), company data

Fig. 21: Cement: key players’ market share in domestic market

Source: Indonesian Cement Association (ASI), company data

Fig. 22: Cement: expected future capacity expansion to meet demand

Source: Company data, Nomura estimates

60

65

70

75

80

85

90

95

100

0

10

20

30

40

50

601Q

042Q

043Q

044Q

041Q

052Q

053Q

054Q

051Q

062Q

063Q

064Q

061Q

072Q

073Q

074Q

071Q

082Q

083Q

084Q

081Q

092Q

093Q

094Q

091Q

102Q

103Q

104Q

101Q

11

Capacity (LHS) Utilization (RHS)(mn tpa) (%)

9

10

11

12

13

14

15

16

17

18

15

20

25

30

35

40

45

50

55

60

2004 2005 2006 2007 2008 2009 2010 2011

SGG (LHS) INTP (LHS)

SMCB (RHS) Others (RHS)

(%)(%)

0

5

10

15

20

25

30

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Semen Gresik Group Indocement

Holcim Indonesia Others

… driving industry capacity utilisation to a peak, despite additional capacity coming on stream

Players that have lagged in increasing capacity are losing market share

Additional capacity coming on-stream will continue, mainly by the Big 3

Nomura | AEJ Indonesia Infrastructure May 2, 2011

17

Fig. 23: Estimated cement industry capacity and sales

Source: Indonesia Cement Association (ASI)

Our thesis of rising domestic demand for cement hinges upon a continued robust macro-economic situation in Indonesia. We would expect that the additional capacity will be absorbed by domestic demand growth (which is already growing strongly and cannibalizing export sales due to lack of capacity).

Annual domestic cement demand growth rate averaged at 7.5% over the past 10 years (6.2% 10-year CAGR), with the economy growing at an average of 5.2% between 2000 and 2010. Even during the global financial crisis in 2008-09, with Indonesia registering growth of only 4.5% in 2009, domestic cement demand continued to grow, albeit at a marginal 1%. But this is after the industry saw growth of 11.4% and 6.6% in 2008 and 2007, respectively. We assume average annual cement demand growth of 7.5% on the assumption that the economy will grow by an average 7% pa from 2012.

In the event of a major slowdown in the economy that results in an abrupt decline in cement growth, say to 1% in the next three years (with reference to the recent global crisis), we would expect utilisation to fall to 68%, a situation that we had back in 2000, even with all the capacity expansion still coming in.

In our view, the risk of such a dire economic situation is low, and we believe that cement will be relatively resilient. We already assume conservative price increases in the next three years of only 5% in 2011 and 2.5% in 2012 and 2013, compared to an average 10% price increase in the past 10 years in light of upcoming capacity addition.

Fig. 24: Bulk cement contribution to total sales volume

Source: Indonesian Cement Association

Million tons 2005 2006 2007 2008 2009 2010 2011F 2012F 2013F 2014F 2015F

Industry capacity 44.85 45.45 45.45 47.75 48.55 52.30 54.30 59.30 63.90 68.40 68.40

Domestic demand 31.48 32.06 34.18 38.09 38.35 40.82 43.84 47.19 50.81 54.72 58.54

Export sales 6.71 7.27 7.80 4.93 3.93 2.88 2.31 1.85 1.50 1.50 1.50

Total cement sales 38.19 39.32 41.98 43.02 42.28 43.70 46.15 49.04 52.31 56.22 60.04

Domestic demand to capacity 70.2% 70.5% 75.2% 79.8% 79.0% 78.1% 80.7% 79.6% 79.5% 80.0% 85.6%

Total Sales to capacity 85.1% 86.5% 92.4% 90.1% 87.1% 83.6% 85.0% 82.7% 81.9% 82.2% 87.8%

Domestic demand growth 6.4% 1.8% 6.6% 11.4% 0.7% 6.4% 7.4% 7.6% 7.7% 7.7% 7.0%

GDP growth 5.7% 5.5% 6.3% 6.1% 4.5% 6.1% 6.5% 7.0% 7.0% 6.8% 6.9%

10

12

14

16

18

20

22

24

26

28

30

1Q08

2Q08

3Q08

4Q08

1Q09

2Q09

3Q09

4Q09

1Q10

2Q10

3Q10

4Q10

1Q11

SGG INTP SMCB Others

(%) Bulk cement sales on the rise, resulting in a higher proportion of bulk cement sales

Nomura | AEJ Indonesia Infrastructure May 2, 2011

18

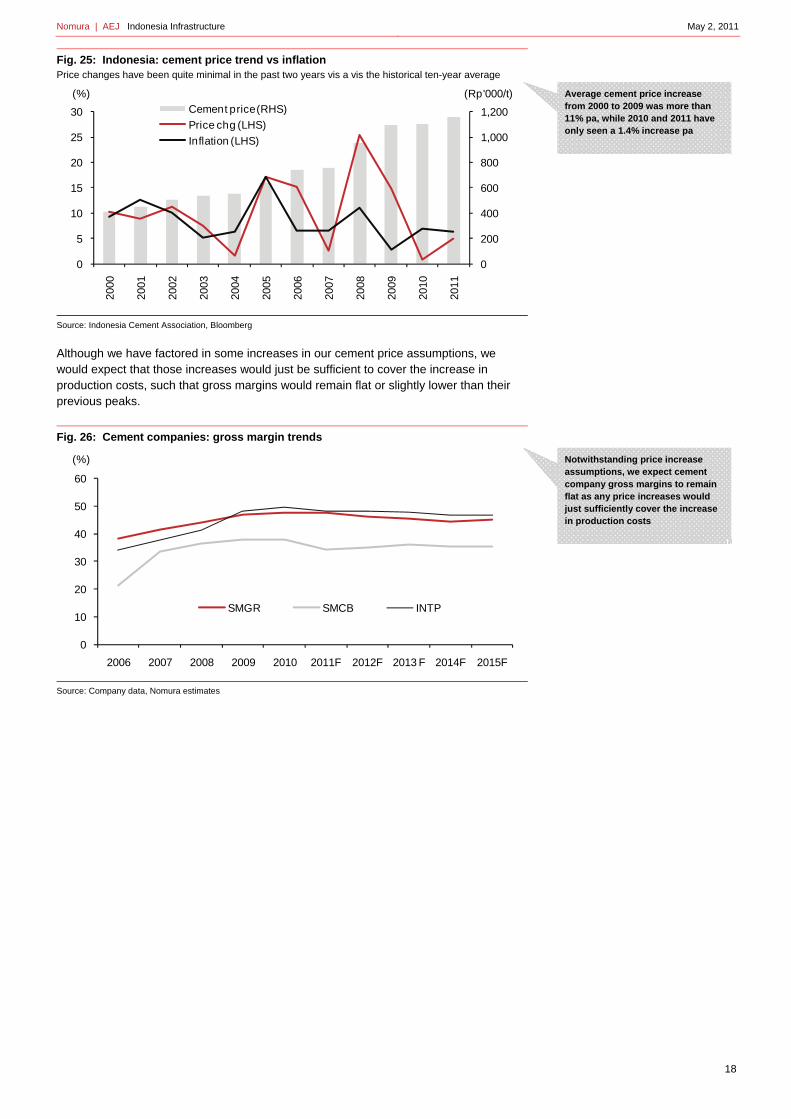

Fig. 25: Indonesia: cement price trend vs inflation Price changes have been quite minimal in the past two years vis a vis the historical ten-year average

Source: Indonesia Cement Association, Bloomberg

Although we have factored in some increases in our cement price assumptions, we would expect that those increases would just be sufficient to cover the increase in production costs, such that gross margins would remain flat or slightly lower than their previous peaks.

Fig. 26: Cement companies: gross margin trends

Source: Company data, Nomura estimates

0

200

400

600

800

1,000

1,200

0

5

10

15

20

25

3020

00

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

Cement price (RHS)

Price chg (LHS)

Inflation (LHS)

(%) (Rp'000/t)

0

10

20

30

40

50

60

2006 2007 2008 2009 2010 2011F 2012F 2013 F 2014F 2015F

SMGR SMCB INTP

(%)

Average cement price increase from 2000 to 2009 was more than 11% pa, while 2010 and 2011 have only seen a 1.4% increase pa

Notwithstanding price increase assumptions, we expect cement company gross margins to remain flat as any price increases would just sufficiently cover the increase in production costs

Nomura | AEJ Indonesia Infrastructure May 2, 2011

19

Fig. 27: Cement price increase was to reflect higher energy prices, primarily coal Cement prices in the past two years have yet to reflect substantially higher coal prices

Source: Indonesian Cement Association, Company data, Bloomberg

0

20

40

60

80

100

120

140

0

200

400

600

800

1,000

1,200

1,400

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

Cement price (LHS)

Coal price (RHS)

(Rp'000/t) (US$/t) Cement selling price is expected to play catch up with rising energy, coal prices

Nomura | AEJ Indonesia Infrastructure May 2, 2011

20

Company comparison

Fig. 28: Valuation comparison

Source: Company data, Nomura estimates

Notes: implied valuation at target price

SEMEN GRESIK

Current Share Price 9,450 Target Share Price 11,700 Upside / Downside 23.8%

SUMMARY VALUATION 2008 2009 2010 2011 2012 2013

Enterprise Value Rp bn 68,612 68,612 68,612 68,612 Equity Value Rp bn 69,037 69,037 69,037 69,037 EBITDA Rp bn 4,964 5,649 6,848 7,350 Earnings Rp bn 3,633 3,898 4,413 4,895 Capacity mm t 19.0 20.2 25.2 26.0

EV/EBITDA x 13.8 12.1 10.0 9.3 EV/Capacity US$/t 451 425 340 330 Price to Earnings x 19.0 17.7 15.6 14.1

Operating MeasuresRevenue per ton Rp'000/t 691 815 800 835 857 875

Cost per tonProduction Cash Cost Per Ton Rp'000/t 363 409 396 409 420 440 COGS per ton Rp'000/t 388 431 420 438 460 477 Total Cost per Ton Rp'000/t 499 569 550 572 592 612

EBITDA per ton Rp'000/t 219 270 277 296 309 304

INDOCEMENT

Current Share Price 17,100 Target Share Price 17,200 Upside / Downside 0.6%

SUMMARY VALUATION 2008 2009 2010 2011 2012 2013

Enterprise Value Rp bn 56,884 56,884 56,884 56,884 Equity Value Rp bn 63,111 63,111 63,111 63,111 EBITDA Rp bn 4,641 5,153 5,352 5,797 Earnings Rp bn 3,225 3,516 3,687 4,041 Capacity mm t 18.6 18.6 18.6 20.6

EV/EBITDA x 12.3 11.0 10.6 9.8 EV/Capacity US$/t 472 472 472 426 Price to Earnings x 19.6 17.9 17.1 15.6

Operating MeasuresRevenue per ton Rp '000/t 683 802 820 874 913 918

Cost per tonProduction Cash Cost Per Ton Rp '000/t 360 372 366 409 429 436 COGS per ton Rp '000/t 402 415 412 452 473 478 Total Cost per Ton Rp '000/t 511 522 524 568 597 606

EBITDA per ton Rp '000/t 213 323 342 349 361 353

HOLCIM INDONESIA

Current Share Price 2,275 Target Share Price 2,700 Upside / Downside 18.7%

SUMMARY VALUATION 2008 2009 2010 2011 2012 2013

Enterprise Value Rp bn 19,697 19,697 19,697 19,697 Equity Value Rp bn 20,618 20,618 20,618 20,618 EBITDA Rp bn 1,854 2,090 2,318 2,849 Earnings Rp bn 828 896 969 1,186 Capacity mm t 9.4 9.4 9.4 11.2

EV/EBITDA x 10.6 9.4 8.5 6.9 EV/Capacity US$/t 261 261 261 219 Price to Earnings x 24.9 23.0 21.3 17.4

Operating MeasuresRevenue per ton Rp '000/t 768 824 834 881 924 960

Cost per tonProduction Cash Cost Per Ton Rp '000/t 285 257 260 310 302 300 COGS per ton Rp '000/t 487 512 519 579 601 613 Total Cost per Ton Rp '000/t 624 630 647 711 740 752

EBITDA per ton Rp '000/t 202 255 259 270 299 313

Nomura | AEJ Indonesia Infrastructure May 2, 2011

21

Transport: Bullish Toll roads are the key focus of the government for infrastructure development, and thus the sector should benefit, in our view. We see more favourable regulations and development of more toll roads to increase connectivity (and car numbers) as key positives for the sector.

Action: BUY Jasa Marga

We initiate coverage of the transport sector (toll roads) with a BUY rating on Jasa Marga, Indonesia's main toll road operator.

Investment thesis

Land Acquisition Bill is the key catalyst We believe that the transport sector will be the main beneficiary of the new Land Acquisition Bill that will be passed by parliament this year. The benefit of being able to build more toll roads with the implementation of this law for the toll road operators and investors are threefold:

• It will allow acceleration in toll road development, adding project portfolio that will contribute traffic and cashflow (rather than just paper concessions), and potentially further re-investments in other toll roads by toll road operators.

• More toll road development will also help to unlock accelerated traffic growth potential that has been seized by capacity constraints. In the past 10 years, car sales growth hit an average 11% CAGR, while Jasa Marga's traffic volume recorded an average CAGR of 5%. We believe that the 5% CAGR is below the potential that Jasa Marga can achieve owing to the toll road capacity constraints (cars are avoiding some toll roads which are actually more jammed than normal roads), as such more toll roads should help to boost traffic growth.

• In addition, we expect that accelerating toll road development will increase toll road connections and thus lead to further traffic volume growth.

Strong growth in car sales Continued robust car sales growth will undoubtedly benefit toll road companies, provided that capacity constraints are reduced.

Risks Key risks to the toll road sector, in our view, include uncertainty over construction costs, primarily as a result of rising material costs, particularly as project development takes a few years to complete and commodity prices are volatile.

Fig. 29: Annual car sales (1997-2010) Annual car sales growth hit an average of 11% in the past 10 years, given economic growth

Source: Gaikindo, Nomura research

0

100,000

200,000

300,000

400,000

500,000

600,000

700,000

800,000

900,000

1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010

(Units) Car sales have grown by 11% pa over the past decade

Nomura | AEJ Indonesia Infrastructure May 2, 2011

22

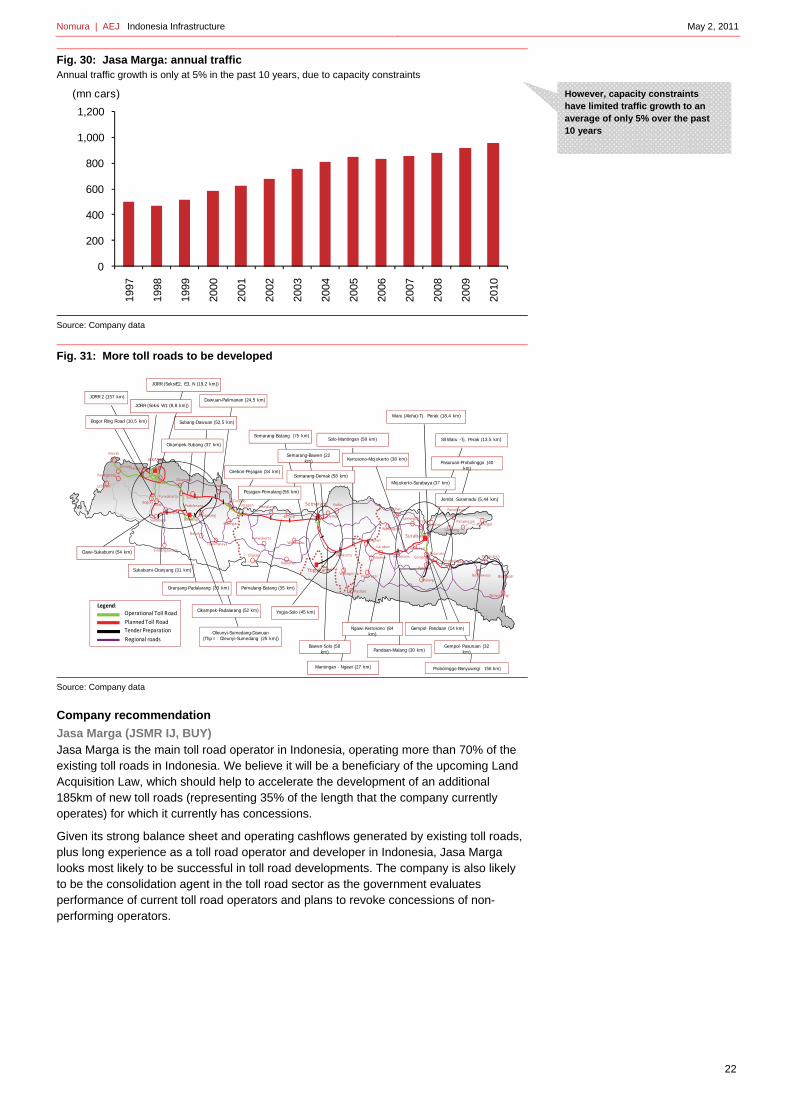

Fig. 30: Jasa Marga: annual traffic Annual traffic growth is only at 5% in the past 10 years, due to capacity constraints

Source: Company data

Fig. 31: More toll roads to be developed

Source: Company data

Company recommendation

Jasa Marga (JSMR IJ, BUY) Jasa Marga is the main toll road operator in Indonesia, operating more than 70% of the existing toll roads in Indonesia. We believe it will be a beneficiary of the upcoming Land Acquisition Law, which should help to accelerate the development of an additional 185km of new toll roads (representing 35% of the length that the company currently operates) for which it currently has concessions.

Given its strong balance sheet and operating cashflows generated by existing toll roads, plus long experience as a toll road operator and developer in Indonesia, Jasa Marga looks most likely to be successful in toll road developments. The company is also likely to be the consolidation agent in the toll road sector as the government evaluates performance of current toll road operators and plans to revoke concessions of non-performing operators.

0

200

400

600

800

1,000

1,200

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

(mn cars)

SurabayaSampang

BangkalanPamekasan

Pamekasan

Kalianget

Merak

Serang

Pandeglang

JAKARTA

Bogor

Bandung

BekasiCikampek

SumedangSukabumi

Cirebon

PemalangSemarang Kudus

Yogjakarta

Ngawi

Mojokerto

Malang

ProbolinggoPanarukan

Banyuwangi

Bondowoso Bajulmati

Gresik

Tuban

Bojonegoro

Lamongan

Caruban

Madiun Kertosono

Batang

PurwokertoWonosobo

Cilacap

Kebumen

Kuningan

Garut

Tasikmalaya

Sindangbarang

Dawuan

Subang

Pacitan

WonogiriPonorogo

Labuhan

Pejagan

Tangerang

Gempol

Gempol- Pandaan (14 km)

Probolinggo-Banyuwngi 156 km)

Gempol- Pasuruan (32 km)

Solo-Mantingan (58 km)

Kertosono-Mojokerto (38 km)

Pemalang-Batang (35 km)

Semarang-Batang (75 km)

Semarang-Bawen (22 km)

Semarang-Demak (58 km)Cirebon-Pejagan (34 km)

Pejagan-Pemalang (56 km)

Yogja-Solo (45 km)

Dawuan-Palimanan (24,5 km)

Subang-Dawuan (52,5 km)

Sukabumi-Ciranjang (31 km)

Cileunyi-Sumedang-Dawuan(Thp I : Cileunyi-Sumedang (25 km))

Cikampek-Padalarang (52 km)

Pandaan-Malang (30 km)

SS Waru -Tj. Perak (13,5 km)

Waru (Aloha)-Tj. Perak (18,4 km)

Pasuruan-Probolinggo (40 km)

Mojokerto-Surabaya (37 km)

JORR (SeksiE2, E3, N (19,2 km))

JORR 2 (157 km)

Ciawi-Sukabumi (54 km)

JORR (Seksi W1 (9,8 km))

Cikampek-Subang (37 km)

Bogor Ring Road (10,5 km)

Ciranjang-Padalarang (33 km)

Jembt. Suramadu (5,44 km)Purwakarta

Ciawi

Cianjur

Padalarang

Demak

Surakarta

Pandaan

Pasuruan

Mantingan - Ngawi (27 km)

Bawen-Solo (58 km)

Ngawi-Kertosono (84 km)

Operational Toll Road

Planned Toll Road

Regional roads

Legend:

Tender Preparation

However, capacity constraints have limited traffic growth to an average of only 5% over the past 10 years

Nomura | AEJ Indonesia Infrastructure May 2, 2011

23

Steel and construction: Neutral The steel and construction sectors are likely to see growing volumes with rising infrastructure spending and steel prices. However, increasing building material and raw material prices, coupled with import competition, have dampened sentiment.

Action: NEUTRAL on Krakatau and Wijaya We initiate coverage of the Indonesian steel and construction sectors with a NEUTRAL call on Krakatau Steel and Wijaya Karya.

Sector summary The construction sector will undoubtedly be one of the main beneficiaries of rising infrastructure spending, which should expand construction sector business volumes. Increasing government spending will particularly benefit the state-owned construction companies such as Wijaya Karya, which are the typical niche market for state construction works.

However, we believe that it may be too early to get into the sector as contract orders, particularly from the public sector, are back-end loaded and typically take longer to approve. In addition, we would also wait to see the impact of higher raw materials prices on construction margins. Contract values are typically locked in at the beginning of the contract. While contractors typically factor in some room for future raw material price increases, and contracts do provide some leeway for cost adjustments, significant increase in material costs could eventually erode margins.

Fig. 32: Historical and estimated construction spending nationwide and by government

Source: Association of Indonesian Construction Companies, Coordinating Ministry for Economy

Domestic steel demand has also been rising at an average 6.2% CAGR over the past 10 years, benefiting from economic expansion. Increasing property development activities, energy infrastructure spending and car sales are key drivers.

0

50

100

150

200

250

2008 2009 2010 2011F

(Rp tn)National Construction Spending

Government (Ministry of Public Works)

Nomura | AEJ Indonesia Infrastructure May 2, 2011

24

Fig. 33: Trend of domestic steel demand Indonesia domestic supply and imports 2000-09 (mn tonnes)

Source: Company data, CRU

However, much of the growth in demand has been driven by consumption of imported steel plates, primarily for the auto sector, which requires special types of steel and represents a niche market for imports. Import competition is also seen rising in other segments of steel markets aside from steel plates.

Fig. 34: Indonesia steel imports vs car sales Strong correlation between steel import volumes and domestic car sales

Source: Krakatau Steel, Nomura estimates

Given increasing import competition, we would prefer to wait to see if the local steel market can reap benefits from rising domestic steel demand. The threat from import competition stems not only from competitive steel products in the retail markets. Major infrastructure development funded by foreign funding, particularly bilateral cooperation and funding agreements, will experience some competition as these agreements will require use of materials from the origin country, including steel. We believe required use of local content for major infrastructure development would be beneficial for local players, and allow local players to ride the demand growth.

Our cautious stance on the steel sector is also built on concerns over the ability of the steel players to pass on higher raw materials costs (iron ore and pellets) in the face of competition from imported steel. The price-adjustment mechanism will be quite fluid. Krakatau Steel typically adjusts its steel selling price on a monthly basis. However, for steel market segments that face import competition, this sort of price adjustment could face some challenges.

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

9,000

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010

Domestic supply Imports

0

100

200

300

400

500

600

700

800

900

0

500

1,000

1,500

2,000

2,500

3,000

3,500

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

Imports Cars

Import steel ('000 t) Car sales ('000 units)

Nomura | AEJ Indonesia Infrastructure May 2, 2011

25

Risks Key risks for the sector are rising commodity prices that will increase production and construction costs. In addition, a rising interest rate would also be a risk for the construction sector as it would raise funding costs given that higher business volumes would require additional working capital funding.

Company recommendations

Krakatau Steel (KRAS IJ, NEUTRAL) Krakatau Steel is the largest integrated steel producer in Indonesia, and the company is revamping and expanding its production capacity. It plans to increase its production capacity from 2.8mn tpa currently to 4.25mn tpa by 2014. The company is adding blasting furnace production capacity that is more cost efficient than the current production facility (EAF-based) and this should help to reduce production costs by 5%.

Additional production capacity of 3mn tpa is also being developed under a joint venture with POSCO, whereby Krakatau will eventually have 45% equity interest. We expect the government to grant tax incentives in the form of a tax holiday and Krakatau to record Rp1.5tn of extraordinary gains from land sales to the JV.

New additional production capacity will start to contribute growth for Krakatau starting in 2012. Meanwhile, raw material costs (prices of iron ore and pellets) are rising. We recommend a NEUTRAL position on Krakatau, as we are cautious on the impact of rising materials costs and will continue to monitor the progress of expansion and revitalization programmes.

The stock is currently trading at premium to its regional peers. While such a premium may be attributable to the company’s strong growth profile over the next few years, our NETURAL stance highlights the execution risk of the company’s expansion plans that actually drives such growth. In addition, Krakatau just recently went public at the end of last year, so whether such premium valuation is justified and sustainable is yet to be seen. In any case, our valuation already assigns a higher premium than the current share price, thus in order for us to take a more optimistic view on the company, we need to see more concrete progress from the company’s expansion plans before we get any full conviction.

Wijaya Karya (WIKA IJ, NEUTRAL) With market cap of less than US$500mn, Wijaya Karya is the largest and most liquid construction company listed on the Indonesia Stock Exchange. We expect the company to benefit from rising construction spending, particularly from construction spending promoted by the government.

In addition, the company is also entering into investments and partnerships with sister state-owned companies Jasa Marga and PLN (the state electricity company) in a number of infrastructure projects, with the view that these investments will:

• support the construction business;

• help provide stability in future earnings; and

• diversify away from the more volatile construction business.

A strong balance sheet with a high level of cash (20% of total assets) has allowed companies such as Wijaya Karya to leverage on their balance sheets to win projects and selectively participate in the project ownership as investments.

However, we believe that the company's financial strength will be tested as business volume increases, requiring higher working capital funding. Coupled with rising raw material prices, we would remain cautious and recommend investors to sit on the sideline to monitor progress until it is clearer that the company can translate higher business volumes into much stronger earnings. NEUTRAL.

Nomura | AEJ Indonesia Infrastructure May 2, 2011

26

Steel industry outlook

The following section on the steel industry outlook is taken from the Nomura Global mining sector report, Buy the current correction, published on 7 February, 2011, and the Nomura European steel sector report, Solid 2Q discounted; market focused on 2H - Market waiting for a 2H margin collapse; we are more optimistic on 2H11 and 2012, published on 20 April, 2011.

Overview of steel sector

We expect steel prices to moderate ... Amid signs that steel prices have peaked for the near term, the market appears to have already priced in expectations of falling steel prices in the coming weeks and months. The share prices of ArcelorMittal (MT) and Kloeckner (KCO) tend to be correlated with spot steel prices, as investor sentiment towards these two companies rises and falls with spot steel prices (even if we believe that this approach does not capture the fundamental equity stories for these two stocks). Shares of both MT and KCO are down almost 15% since their recent peaks in February 2011. Against the backdrop of potential import pressure from Chinese steelmakers, falling scrap prices and a possible easing in the restocking that has played a part in driving steel prices upward in 1Q, it appears likely that steel prices in the US and Europe will moderate. In addition, our channel checks suggest that US and European steel customers are starting to take a wait-and-see attitude toward further orders. Overall, flat-rolled demand remains stronger than long-product demand, reflecting demand strength from automotive, capital goods and energy end markets vs. construction end markets.

... but steel prices should remain supported by elevated raw material costs Raw material costs remain elevated, with spot iron ore prices having rebounded to near peak levels, following a brief respite in March. At current levels, we believe that Chinese steel mills are barely profitable, implying steel prices there may have reached a floor, and we are encouraged by modest price increases in China that have been reported in recent weeks. The current iron ore spot price is in line with our 2Q house forecast price of $185/t. We expect iron ore prices to moderate slightly in 2H, to $170/t in 3Q and $160/t in 4Q; however, in the absence of meaningful supply coming to the market and continued steel production growth, we believe that iron ore markets will remain tight through 2012, where we forecast an iron ore price of $180/t. Similarly with coking coal, our house forecast is for prices to moderate slightly in 2H11 but remain elevated through 2012. We therefore see limited scope for a precipitous decline in steel prices, as steelmakers, particularly in China, cannot afford to bear much lower steel prices. Figs. 6 and 7 show how steel prices have tracked iron ore prices, suggesting limited downside risk to steel prices if iron ore prices remain elevated and steel demand remains adequate. Both iron ore and Chinese steel prices weakened in March, but the recent rebound in iron ore prices suggests Chinese steelmakers could need to raise prices to remain profitable, reducing the spread against (and easing the pressure on) US and European steel prices.

Chinese steel prices may have reached a floor We believe that Chinese steelmakers are barely profitable at current steel price levels due to elevated raw material cost pressure, and we note the $20–25/t increase in Chinese HRC steel prices in the last month. We believe that Chinese steel prices may have reached a near-term floor and may see a slight increase from current levels. We think a spread of greater than $150/t between US/EU and Chinese steel prices generally increases the threat of rising import volumes. Therefore, the current spread of $200– 250/t is likely to attract increased imports into the US and Europe. However, we believe that demand is not strong enough in the US or Europe where one could expect a flood of imports. It is our view, therefore, that European prices could moderate slightly in the near term, but that they will essentially remain supported by stable Chinese prices.

Steel prices will not collapse, but margins will come under pressure in 2H With elevated raw material costs likely to persist through 2011, underlying demand improving and inventories reasonable, we believe that steel prices will remain broadly supported at current levels, although we expect some moderation. However, high raw

Investor sentiment is low; the market is expecting steel prices to fall

We expect iron ore and coking coal markets to remain tight and prices to remain elevated through 2011, providing some cost-push support to steel prices

We see limited scope for Chinese prices to fall much further, given razor-thin margins and continued raw material cost pressure

2H11 will be weaker than 1H 2011, but not as bad 2H10

Nomura | AEJ Indonesia Infrastructure May 2, 2011

27

material costs will continue to pressure earnings and margins into 2H11. As a result, we expect modest margin compression in 2H for European steelmakers. Because raw material costs affect steelmakers’ P&L accounts with a lag, in our view high raw material prices in 1H will weigh on earnings into 2H. We believe that a typical seasonal downtick in shipment volumes and a likely softening of steel prices, in combination with higher input costs, will translate into a weaker 2H vs. 1H; however, we expect demand and inventories to hold up better than in 2H10. Confidence surrounding a global macroeconomic recovery is higher now than it was last year, while inventory levels remain low, suggesting the extreme destocking in 2H10 is unlikely to repeat. With end markets such as automotive, capital goods and mechanical engineering continuing to grow and signs of bottoming appearing in developed world construction markets, steelmakers should enjoy the benefits of higher utilisation rates in 2H11 (vs. 2H10). The risk of Japanese component supply disruptions to the automotive industry could certainly affect steel demand; however, early indications suggest that demand for automotive steel remains strong in Europe.

Fig. 35: Global steel supply and demand dynamics

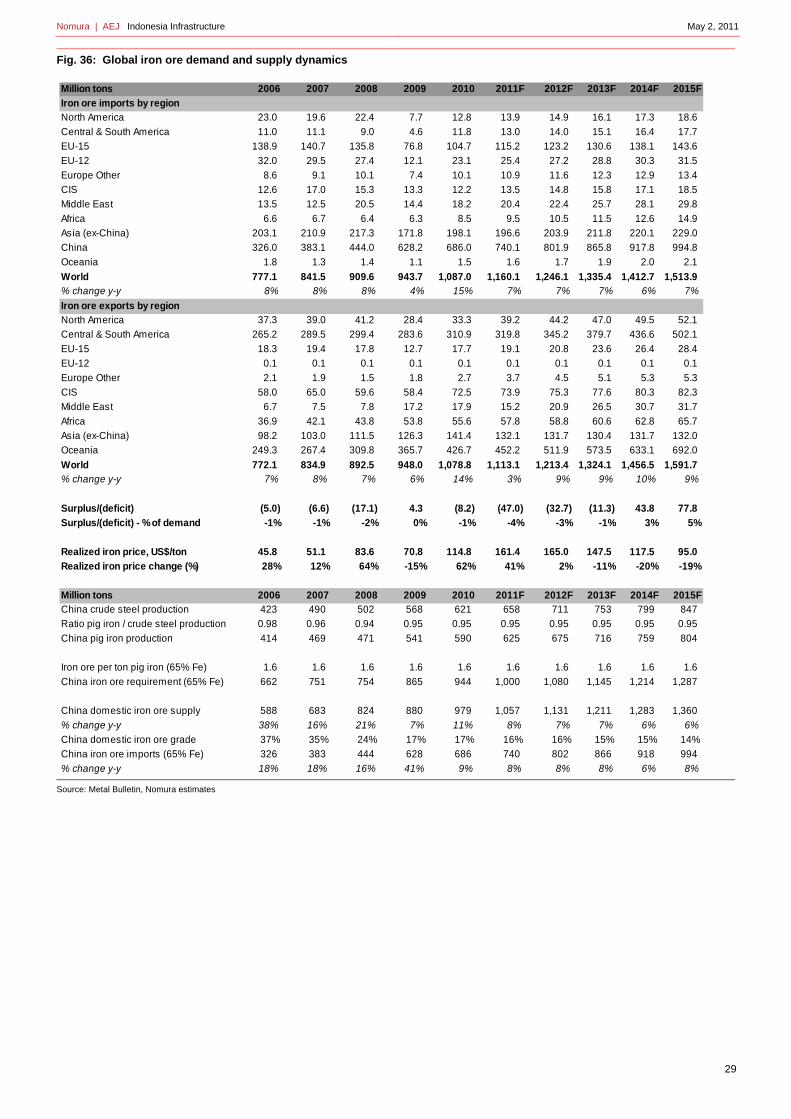

Source: Metal Bulletin, Nomura estimates

Million tons 2006 2007 2008 2009 2010 2011F 2012FCrude steel production (million tonnes)US 98.6 98.1 91.4 58.2 80.6 87.0 94.9 Other North America 33.2 34.5 33.2 24.2 31.2 34.3 35.7 North America 131.8 132.6 124.5 82.4 111.8 121.4 130.6 Brazil 30.9 33.8 33.7 26.5 32.8 36.1 39.0 Other Americas 14.4 14.5 13.6 11.3 11.0 12.1 13.1 Central & South America 45.3 48.2 47.4 37.8 43.8 48.2 52.0 EU-27 206.3 209.7 198.0 138.8 172.9 190.2 203.5 Europe-other 28.2 30.6 31.3 28.7 33.1 35.7 37.9 Russia 70.8 72.4 68.7 60.0 67.0 74.6 80.6 Other CIS 49.1 51.8 45.3 37.6 41.5 46.1 49.8 CIS 119.9 124.2 114.0 97.6 108.5 120.7 130.4 Middle East 15.4 16.0 16.0 17.7 19.6 22.0 24.1 Africa 18.8 18.8 16.7 15.2 17.5 19.6 21.6 China 422.7 489.9 500.3 573.6 626.7 685.0 739.8 India 50.8 53.1 58.4 62.8 66.8 70.8 77.9 Japan 116.2 120.2 118.7 87.5 109.6 111.9 112.8 Korea, South 48.5 51.5 53.6 48.6 58.6 62.3 68.6 Other Asia 38.0 47.2 18.4 32.4 36.2 39.8 43.0 Asia 676.2 761.9 749.5 804.9 897.9 969.8 1,042.0 Oceania 8.7 8.8 8.4 6.0 8.1 8.9 9.5

World 1,251.2 1,351.3 1,329.7 1,229.2 1,413.6 1,536.4 1,651.5 YoY change 9% 8% -2% -8% 15% 9% 7%

Million tons 2006 2007 2008 2009 2010F 2011F 2012FApparent steel consumption (million tonnes)North America 155.7 141.3 129.0 82.7 102.2 109.9 115.4 Brazil 18.5 22.1 24.0 18.5 22.8 25.1 27.3 Other Americas 17.9 19.8 20.3 15.1 18.4 20.2 21.9 Central & South America 36.4 41.9 44.3 33.6 41.2 45.3 49.2 EU-27 188.6 198.1 181.3 118.7 136.0 142.1 149.2 Europe-other 28.9 31.6 25.3 23.9 26.9 28.6 29.8 Russia 34.9 39.5 37.3 24.7 34.1 37.6 40.7 Ukraine 7.1 9.5 6.9 5.2 6.9 7.7 8.2 Other CIS 6.9 7.6 4.7 3.4 4.2 4.6 4.9 CIS 48.9 56.6 48.9 33.3 45.2 49.9 53.8 Middle East 34.9 40.3 43.1 40.6 44.5 49.0 52.9 Africa 22.9 25.1 26.2 28.7 30.6 33.7 36.4 China 361.3 408.3 425.7 542.4 574.4 606.0 654.5 India 46.1 52.1 53.0 55.3 63.6 69.0 75.9 Japan 77.3 79.6 76.4 53.2 58.7 61.9 62.2 Korea, South 50.2 55.4 58.9 45.4 50.6 54.0 59.4 Taiwan 19.8 20.2 16.7 11.3 13.2 14.5 15.5 Other Asia 55.4 55.6 69.7 50.2 56.0 61.6 65.9 Asia 610.1 671.3 700.5 757.8 816.5 867.0 933.5 Oceania 7.9 8.6 8.5 5.9 6.4 7.0 7.5

World 1,134.3 1,214.8 1,207.0 1,125.2 1,249.5 1,332.5 1,427.6 YoY change 9% 7% -1% -7% 11% 7% 7%

Nomura | AEJ Indonesia Infrastructure May 2, 2011

28

Overview of iron ore sector We believe iron ore supply is at least as tight as in 2008 when spot prices spiked to over USD200/tonne. We expect tight supply conditions to persist over the next three to five years as timelines for major new supply expansions in Brazil and Australia are subject to delays. We have further increased our medium-term estimates for iron ore price contracts from what we regard as already bullish levels. Thereafter, we see a large amount of new supply that is likely to return prices to equilibrium levels of around USD70/tonne (Australia FOB).

Under the quarterly pricing mechanism, a return to 2008 spot prices would equate to a realised price double that achieved in 2008. Vale's strategy to keep seaborne freight rates low by investing in its own fleet of bulk carriers also provides a benefit for the Australian miners without the additional capital cost.

Nomura | AEJ Indonesia Infrastructure May 2, 2011

29

Fig. 36: Global iron ore demand and supply dynamics

Source: Metal Bulletin, Nomura estimates

Million tons 2006 2007 2008 2009 2010 2011F 2012F 2013F 2014F 2015F

Iron ore imports by regionNorth America 23.0 19.6 22.4 7.7 12.8 13.9 14.9 16.1 17.3 18.6

Central & South America 11.0 11.1 9.0 4.6 11.8 13.0 14.0 15.1 16.4 17.7

EU-15 138.9 140.7 135.8 76.8 104.7 115.2 123.2 130.6 138.1 143.6

EU-12 32.0 29.5 27.4 12.1 23.1 25.4 27.2 28.8 30.3 31.5

Europe Other 8.6 9.1 10.1 7.4 10.1 10.9 11.6 12.3 12.9 13.4

CIS 12.6 17.0 15.3 13.3 12.2 13.5 14.8 15.8 17.1 18.5