AUGUST 2013 DUNDEE PRECIOUS METALS BUILDING A PREMIER, INTERMEDIATE, LOW-COST GOLD PRODUCER Proudly celebrating 30 years as a Toronto Stock Exchange listed company

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

AUGUST 2013

DUNDEE PRECIOUS METALS

BUILDING A PREMIER,

INTERMEDIATE, LOW-COST

GOLD PRODUCER

Proudly celebrating 30 years as a

Toronto Stock Exchange

listed company

2

FORWARD-LOOKING

STATEMENTS

This presentation contains “forward-looking information” or "forward-looking statements" that involve a number of risks and

uncertainties. Forward-looking information and forward-looking statements include, but are not limited to, statements with respect to

the future prices of gold and other metals, the estimation of mineral reserves and resources, the realization of mineral estimates, the

timing and amount of estimated future production and output, costs of production, capital expenditures, costs and timing of the

development of new deposits, success of exploration activities, permitting time lines, currency fluctuations, requirements for additional

capital, government regulation of mining operations, environmental risks, unanticipated reclamation expenses, title disputes or claims,

limitations on insurance coverage and timing and possible outcome of pending litigation. Often, but not always, forward-looking

statements can be identified by the use of words such as “plans”, “expects”, or “does not expect”, “is expected”, “budget”, “scheduled”,

“estimates”, “forecasts”, “intends”, “anticipates”, or “does not anticipate”, or “believes”, or variations of such words and phrases or state

that certain actions, events or results “may”, “could”, “would”, “might” or “will” be taken, occur or be achieved. Forward-looking

statements are based on the opinions and estimates of management as of the date such statements are made, and they involve

known and unknown risks, uncertainties and other factors which may cause the actual results, performance or achievements of the

Company to be materially different from any other future results, performance or achievements expressed or implied by the forward-

looking statements. Such factors include, among others: the actual results of current exploration activities; actual results of current

reclamation activities; conclusions of economic evaluations; changes in project parameters as plans continue to be refined; future

prices of gold; possible variations in ore grade or recovery rates; failure of plant, equipment or processes to operate as anticipated;

accidents, labour disputes and other risks of the mining industry; delays in obtaining governmental approvals or financing or in the

completion of development or construction activities, fluctuations in metal prices, as well as those risk factors discussed or referred to

in this news release under and in the Company’s annual information form under the heading "Risk Factors" and other documents filed

from time to time with the securities regulatory authorities in all provinces and territories of Canada and available at www.sedar.com.

Although the Company has attempted to identify important factors that could cause actual actions, events or results to differ materially

from those described in forward-looking statements, there may be other factors that cause actions, events or results not to be

anticipated, estimated or intended. There can be no assurance that forward-looking statements will prove to be accurate, as actual

results and future events could differ materially from those anticipated in such statements. Accordingly, readers are cautioned not to

place undue reliance on forward-looking statements.

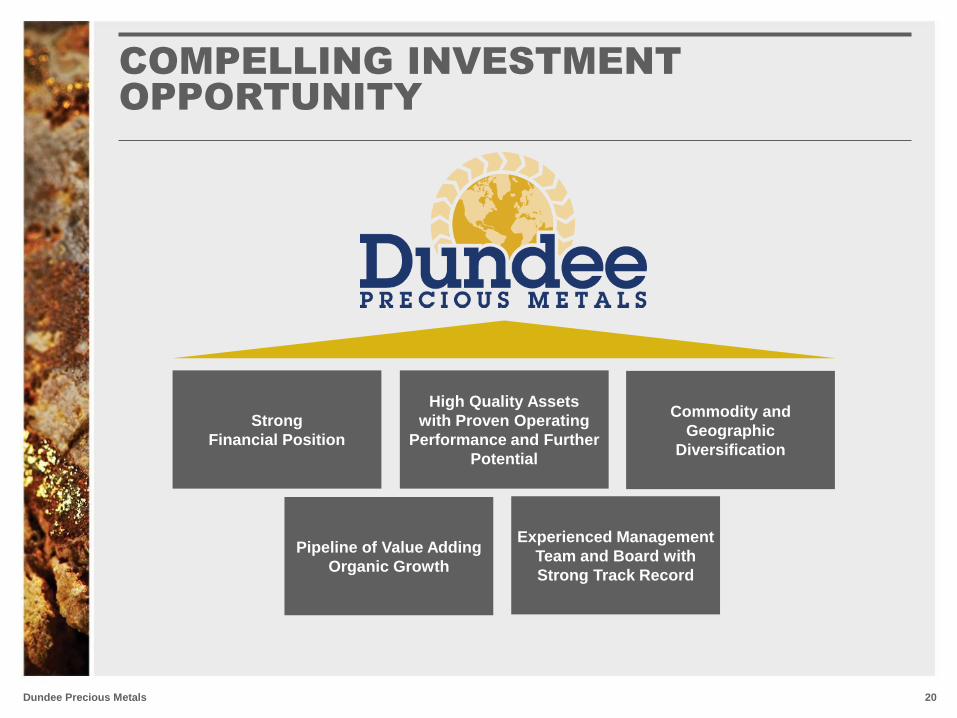

Dundee Precious Metals

Strong

Financial Position

Commodity and

Geographic

Diversification

High Quality Assets

with Proven Operating

Performance and Further

Potential

Experienced Management

Team and Board with

Strong Track Record

Pipeline of Value Adding

Organic Growth

INVESTMENT SUMMARY

3

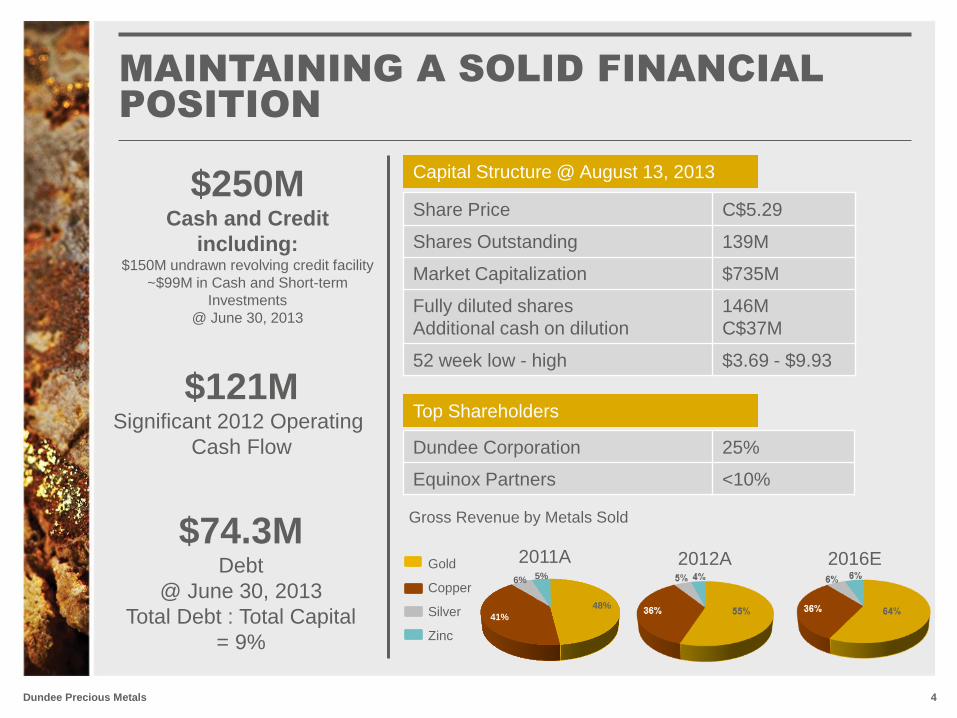

MAINTAINING A SOLID FINANCIAL

POSITION

4 Dundee Precious Metals

Share Price C$5.29

Shares Outstanding 139M

Market Capitalization $735M

Fully diluted shares

Additional cash on dilution

146M

C$37M

52 week low - high $3.69 - $9.93

Gross Revenue by Metals Sold

2011A 2012A 2016E Gold

Copper

Silver

Zinc

Dundee Corporation 25%

Equinox Partners <10%

$250M Cash and Credit

including: $150M undrawn revolving credit facility

~$99M in Cash and Short-term

Investments

@ June 30, 2013

$121M Significant 2012 Operating

Cash Flow

$74.3M Debt

@ June 30, 2013

Total Debt : Total Capital

= 9%

48%

41%

6% 5%

Capital Structure @ August 13, 2013

Top Shareholders

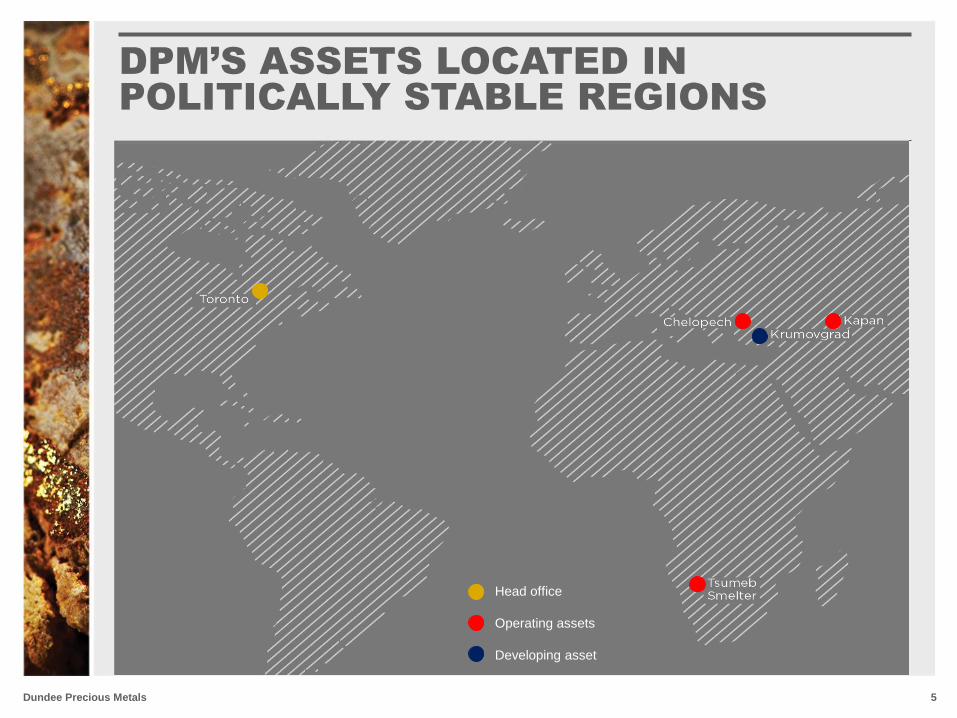

DPM’S ASSETS LOCATED IN

POLITICALLY STABLE REGIONS

5 Dundee Precious Metals

Head office

Operating assets

Developing asset

GOLD COMPOUND ANNUAL GROWTH

RATE OF 14%

6 Dundee Precious Metals

Consolidated Gold Production (oz 000’s) Consolidated Copper Production (lbs 000,000)

Copper production has increased 105% over four years Gold production has increased 70% over four years

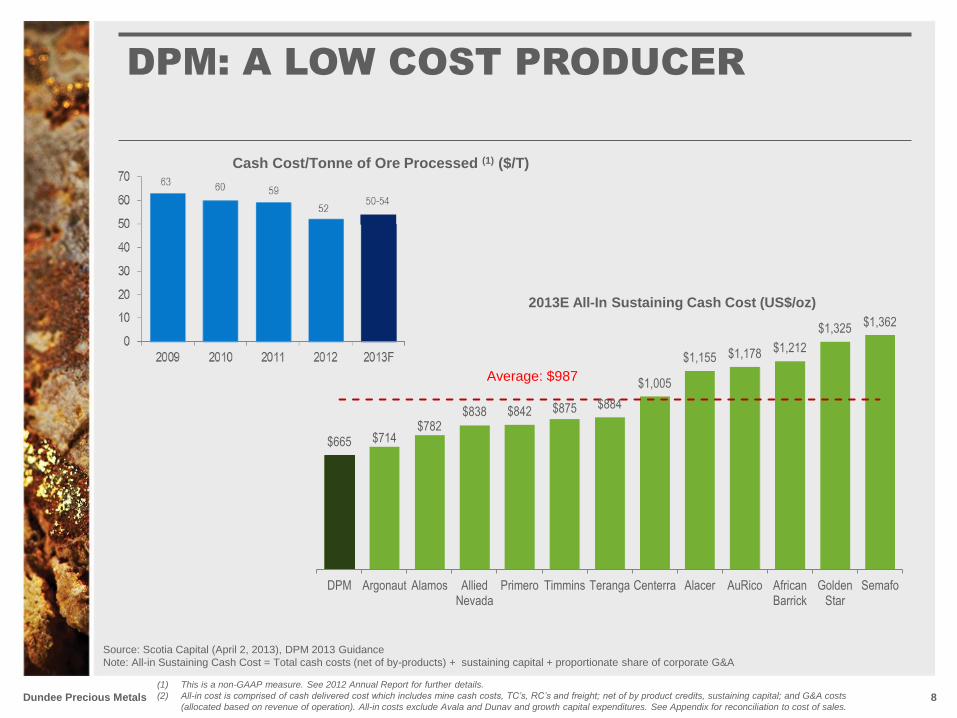

DECREASING CASH COSTS AND

INCREASING EBITDA

7 Dundee Precious Metals

Reduced cash cost per ounce of gold produced

78% over four years1

Consolidated Adjusted EBITDA increased

412% over four years2

($40)

$32 $45

$118 $125

2008 2009 2010 2011 2012

(1) Net of by-product credits

(2) Cdn $

8

Source: Scotia Capital (April 2, 2013), DPM 2013 Guidance

Note: All-in Sustaining Cash Cost = Total cash costs (net of by-products) + sustaining capital + proportionate share of corporate G&A

DPM: A LOW COST PRODUCER

Cash Cost/Tonne of Ore Processed (1) ($/T)

(1) This is a non-GAAP measure. See 2012 Annual Report for further details.

(2) All-in cost is comprised of cash delivered cost which includes mine cash costs, TC’s, RC’s and freight; net of by product credits, sustaining capital; and G&A costs

(allocated based on revenue of operation). All-in costs exclude Avala and Dunav and growth capital expenditures. See Appendix for reconciliation to cost of sales.

Dundee Precious Metals

$665 $714 $782

$838 $842 $875 $884

$1,005

$1,155 $1,178 $1,212

$1,325 $1,362

DPM Argonaut Alamos AlliedNevada

Primero Timmins Teranga Centerra Alacer AuRico AfricanBarrick

GoldenStar

Semafo

2013E All-In Sustaining Cash Cost (US$/oz)

Average: $987

CORPORATE VISION AND STRATEGY

9 Dundee Precious Metals

Building DPM into a premier, intermediate, low-cost gold producer

Optimize value of existing operating assets

Grow the business beyond existing operating assets

Sustain low quartile operating costs Conceptual

Illustration of

Krumovgrad

Gold Project

Tsumeb

Smelter,

Namibia

Exploration

at Kapan

Mine

Autoclave

fabricated for

the MPF to

be used for

Stage 2

Pyrite

Project at

Chelopech

• Increase mine production and extend LOMs

• Upgrade/expand smelter and establish long-term contracts

that provide a stable return

• Develop Krumovgrad gold project

• Establish deep pipeline of greenfield exploration

opportunities

• Complete acquisitions that offer accretive growth, diversity

and gold exposure, while maintaining a conservative

capital structure

Maintain a strong balance sheet with ample liquidity

Strategy

Vision

CHELOPECH MINE:

LOW COST, LONG LIFE PRODUCER

10 Dundee Precious Metals

Chelopech Optimization

Grade Ounces

Resources M&I

(at Dec.31, 2012)

Au (oz) 4.0 g/t 3.8M

Cu (lbs) 1.3% 825M

Reserves

(at Dec 31, 2012)

Au (oz) 3.6 g/t 2.5M

Cu (lbs) 1.1% Cu 519M

Estimated Mine Life @ expanded rate 10+ years

Continue to implement

cost/margin improvements

Operating at full capacity of two

million tonnes of ore per annum

Capitalize on lower cost / higher

recovery staged flotation reactor

technology

Perform targeted exploration to

replace depletion and increase

mineral resources / reserves

Install new pyrite concentrate

flotation circuit

Complete feasibility study on the

pyrite gold treatment project

Staged Flotation

Reactor at

Chelopech

Operations

Dundee Precious Metals

400,000 T pyrite concentrate produced (E)

Metals Potential Grades Est. Incremental Production Result

Au 6-7 g/t 75,000 - 90,000 oz

Ag 10 - 15 g/t 130,000 - 190,000 oz

Cu 0.5% - 0.7% 4.5M - 6.0M lbs

Cash cost per oz of gold (net of by-product credits) $615

Estimated capital costs $202M

NPV (5% discount rate) after tax(1) $141M

IRR after tax(1) 24%

Item Capex

Stage 1: Concentrator upgrade $23M

Stage 2: POX Facility

Phase 1 - start production 2017 $93M

Phase 2 - start production 2019 $87M (1) Assumes the following commodity prices after 2016: $1,250/oz Au, $25/oz Ag,

and $2.75/lb Cu

Project Highlights Project Stages

CHELOPECH MINE:

PYRITE PROJECT TO INCREASE RECOVERIES TO 90%

2013 Catalysts

Complete Stage 1

Concentrator Upgrade Q4 2013

Stage 2 POX

Facility Feasibility Study Q3 2013

11

Dundee Precious Metals 12 Dundee Precious Metals

Kapan Optimization

Complete final portion of drilling of

Shahumyan deposit to support

resource and potential expanded

operation

Complete studies to confirm optimal

mine plan based on new resource

Explore regional license to define

additional Mineral Resources

Continue operational improvements

and cost reductions

Product Cu & Zn concentrates

containing Au & Ag

Deposit Type Polymetallic vein deposit

(swarms)

Open Pit Resource Underway

Underground Resource Underway

KAPAN MINE:

POTENTIAL TO INCREASE SIZE AND EXTEND LIFE OF MINE

2012 Metals Production Grades

22,000 oz Au 1.56 g/t

2.5M lbs Cu 0.25%

15.4M lbs Zn 1.67%

450,000 oz Ag 32.20 g/t

Kapan Mine office

2013 Catalysts

Updated NI 43-101

Resource Estimate

Q3

2013

* Kapan operations were on care and maintenance as of November 2008; operations restarted April 2009.

Dundee Precious Metals

• One of the few smelters with

ability to process complex

concentrate

• Upgrades designed to meet

internationally accepted

environmental standards and

expand capacity to process

additional 3rd party

concentrate

• Lower per tonne operating

costs and more favourable

smelting terms are expected

to generate significantly higher

margins

Horne Smelter

Operated by Xstrata

Capacity: 825Kt of concentrate (total)

Note: Complex concentrate capacity limited

with little to no 3rd party capacity

Tsumeb Smelter

Operated by Dundee Precious Metals

Capacity: 240Kt-320Kt of complex concentrate

Operating Smelters

Closed Smelters

Other smelters that process various amounts of complex concentrates

La Oroya Smelter(1)

Operated by Doe Run

Kosaka Smelter

Shut down in Q1 2008San Luis de Potosi Smelter

Shut down in 2012

Note: Currently closed

Limited Global Smelting Capacity for Complex Concentrate

TSUMEB SMELTER:

A UNIQUE STRATEGIC ASSET

13

Dundee Precious Metals

DPM Ownership 100%

Location Namibia

Technology Ausmelt

Product Copper blister

bars

2012 concentrate throughput 159,356 tonnes

Emissions & dust capture upgrades $103M

Sulphuric acid capture plant (Q3 2014) $204M

Electric holding furnace (Q1 2016) ~$70M+

Asset Overview

TSUMEB SMELTER HAS POTENTIAL

TO POSITIVELY IMPACT EARNINGS C

om

ple

x C

on

Sm

elte

r C

ap

acity (

00

0’s

)

14

Tsumeb

Smelter

KRUMOVGRAD GOLD PROJECT:

LOW CASH COST OPERATION

15 Dundee Precious Metals

Proposed Mine Type Open Pit

Gold Recoveries 85%

Grade 3.4 g/t

Annual ore tonnage production 850,000 tpy

Annual Au production 74,000 ounces

Mine Life 9 years

Capital Costs to complete US$127M

Total cash cost per oz Au Eq $404

Conceptual

Illustration of

Krumovgrad

Gold Project

Secure final local approvals

required prior to proceeding with

ordering long lead items /

construction

Seek opportunities to increase

recoveries through use of SFR

technology

Update / finalize mine plan

Complete detailed engineering that

optimizes value of project

Evaluate other exploration

opportunities within existing

licenses and establish targeted drill

program

Based on Jan. 2012 DFS; Estimated recoveries, capital & operating costs in process of being updated.

Future Catalysts

Start Construction 2015

Start Production 2016

Dundee Precious Metals

• NI-43-101 resources include:

Bigar Hill initial Inferred Resource of 26.4 MT @

1.6 g/t Au for 1.4Moz

Korkan initial Inferred Resource of 20.1 MT @

1.5 g/t Au for 1.0 Moz

Kraku Pester initial Indicated resource of 6.3 MT

@ 1.3 g/t Au for 0.27 Mozs and Inferred

Resource of 2.2 MT @ 1.0 g/t Au for 0.07 Moz

• Total Inferred Resource of 48.7 MT @ 1.5 g/t Au for

2.5 Moz

• NI-43-101 inferred resources include:

Kiseljak Mineral Resource initial estimate 300

MT grading 0.27% Cu & 0.26 g/t Au for 1.8 Blbs

Cu and 2.5 Moz Au

• Bakrenjaca Au-Ag base metal epithermal system,

drilling intersected 11m @ 5.13 g/t Au, 346 g/t Ag and

1.19% Cu

DPM EXPLORATION UPDATE:

PARTIALLY-OWNED ENTITIES

Securities Shares

(m) % Held

Value

(C$M)

Sabina Gold & Silver

Special Warrants

Warrants (strike at C$1.07)

Total

18.5

10

5

9.9% 24

-

-

24

Avala Resources

Special Warrants

Warrants (strike at C$0.30)

Total

135

50

25

53%

8.8

-

-

8.8

Dunav Resources

Warrants (strike at C$0.42)

Total

56

27.5

46%

5.0

-

5.0

Total shares & securities ~ 37.8

Avala Resources Ltd. (TSX-V: AVZ) Equity Portfolio Overview as at August 13, 2013

Dunav Resources Ltd. (TSX-V: DNV)

16

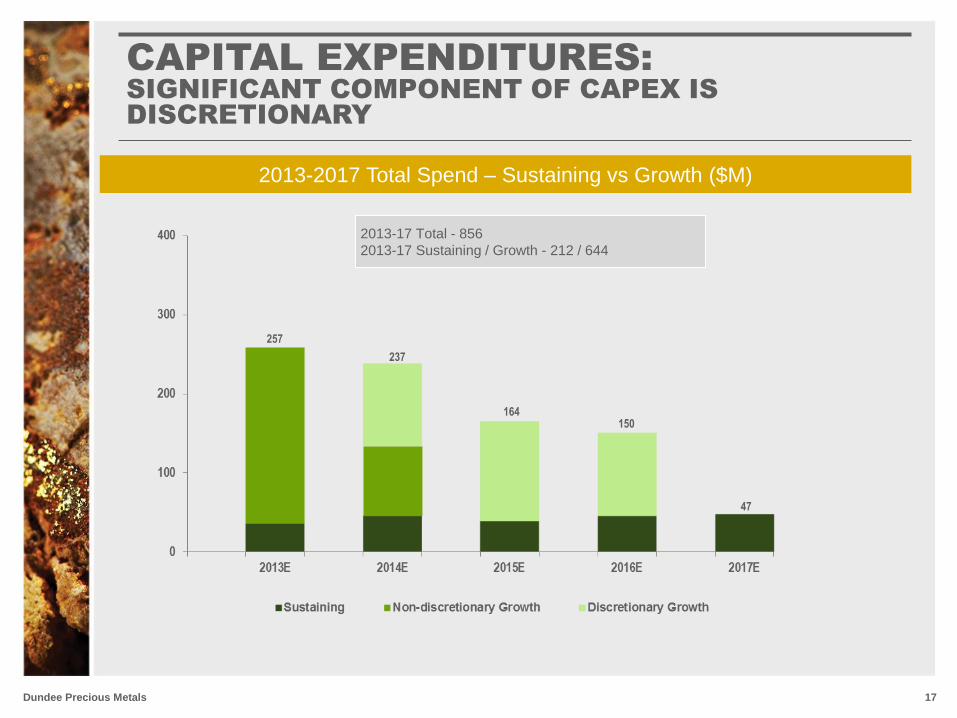

17 Dundee Precious Metals

2013-2017 Total Spend – Sustaining vs Growth ($M)

2013-17 Total - 856

2013-17 Sustaining / Growth - 212 / 644

257

237

164 150

47

CAPITAL EXPENDITURES:

SIGNIFICANT COMPONENT OF CAPEX IS

DISCRETIONARY

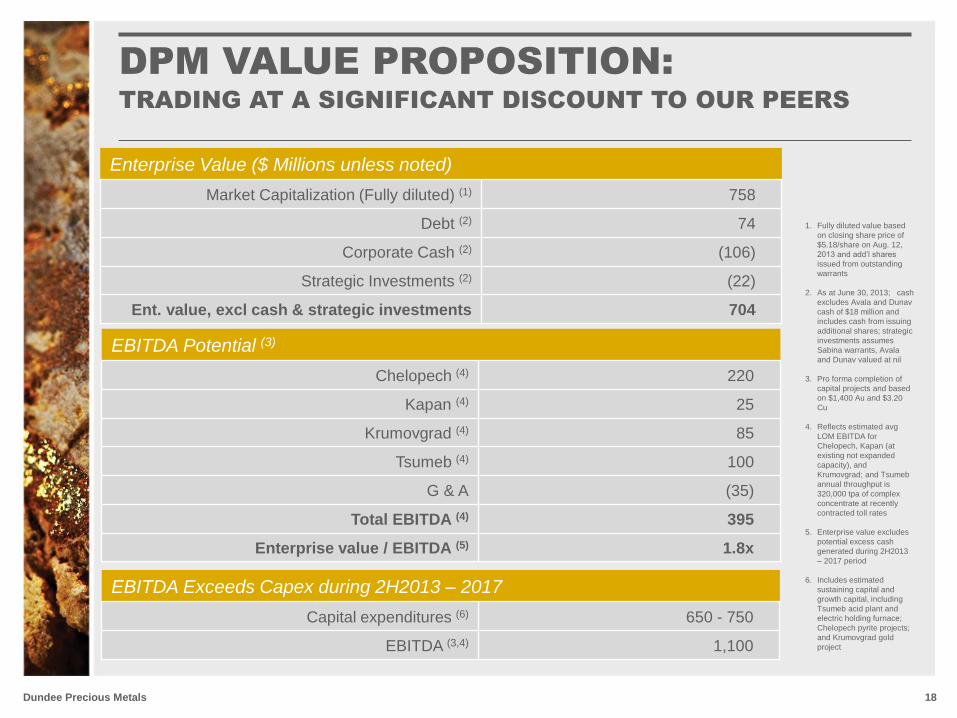

DPM VALUE PROPOSITION:

TRADING AT A SIGNIFICANT DISCOUNT TO OUR PEERS

18 Dundee Precious Metals

Enterprise Value ($ Millions unless noted)

Market Capitalization (Fully diluted) (1) 758

Debt (2) 74

Corporate Cash (2) (106)

Strategic Investments (2) (22)

Ent. value, excl cash & strategic investments 704

EBITDA Potential (3)

Chelopech (4) 220

Kapan (4) 25

Krumovgrad (4) 85

Tsumeb (4) 100

G & A (35)

Total EBITDA (4) 395

Enterprise value / EBITDA (5) 1.8x

1. Fully diluted value based

on closing share price of

$5.18/share on Aug. 12,

2013 and add’l shares

issued from outstanding

warrants

2. As at June 30, 2013; cash

excludes Avala and Dunav

cash of $18 million and

includes cash from issuing

additional shares; strategic

investments assumes

Sabina warrants, Avala

and Dunav valued at nil

3. Pro forma completion of

capital projects and based

on $1,400 Au and $3.20

Cu

4. Reflects estimated avg

LOM EBITDA for

Chelopech, Kapan (at

existing not expanded

capacity), and

Krumovgrad; and Tsumeb

annual throughput is

320,000 tpa of complex

concentrate at recently

contracted toll rates

5. Enterprise value excludes

potential excess cash

generated during 2H2013

– 2017 period

6. Includes estimated

sustaining capital and

growth capital, including

Tsumeb acid plant and

electric holding furnace;

Chelopech pyrite projects;

and Krumovgrad gold

project

EBITDA Exceeds Capex during 2H2013 – 2017

Capital expenditures (6) 650 - 750

EBITDA (3,4) 1,100

DPM FUTURE CATALYSTS

19 Dundee Precious Metals

Tsumeb

Ramps Up

to 100%

Capacity

Kapan Initial

Resource

Estimate

Chelopech

Pyrite Stage 2

Feasibility

Study

Q3 2013 Krumovgrad

Capital Cost

and Mine

Plan Update

Chelopech

Pyrite Stage 1

Construction

Complete

Tsumeb Acid

Plant

Commissioning

Krumovgrad

Construction

Begins

Krumovgrad

Begins

Production

Q4 2013

Q3 2014 2015 2016

Chelopech Mine

Dundee Precious Metals

Strong

Financial Position

Commodity and

Geographic

Diversification

High Quality Assets

with Proven Operating

Performance and Further

Potential

Experienced Management

Team and Board with

Strong Track Record

Pipeline of Value Adding

Organic Growth

COMPELLING INVESTMENT

OPPORTUNITY

20

DUNDEE PRECIOUS METALS

MANAGEMENT TEAM

21 Dundee Precious Metals

Rick Howes

President & Chief Executive Officer

David Rae Senior Vice President,

Operations

Adrian Goldstone Executive Vice President,

Sustainable

Business Development

Michael Dorfman Senior Vice President,

Corporate Development

Hume Kyle Executive Vice

President &

Chief Financial Officer

Lori Beak Senior Vice President,

Investor &

Regulatory Affairs &

Corporate Secretary

Hans Nolte Vice President & General

Manager, Tsumeb Smelter

Reuben Mills Vice President, Safety &

Asset Risk Management

Rob Taylor Vice President Projects

Jeremy Cooper Vice President,

Commercial Affairs

Simon Meik Vice President, Processing

Hratch Jabrayan Vice President & General

Manager,

Kapan Mine

Nikolay Hristov Vice President & General

Manager,

Chelopech Mine

Iliya Garkov Vice President & General

Manager, Krumovgrad

Gold Project

Richard Gosse Senior Vice

President,

Exploration

Jonathan Goodman

Executive Chairman

Paul Proulx Senior Vice President,

Corporate Services

dundeeprecious.com

One Adelaide Street East Suite 500

Toronto, Ontario M5C 2V9 T: 416 365-5191

Investor Relations T: 416 365-2851

TSX: DPM – Common Shares

DPM.WT.A – 2015 Warrants

Proudly celebrating 30 years as

a Toronto Stock Exchange listed

company

23

APPENDICES

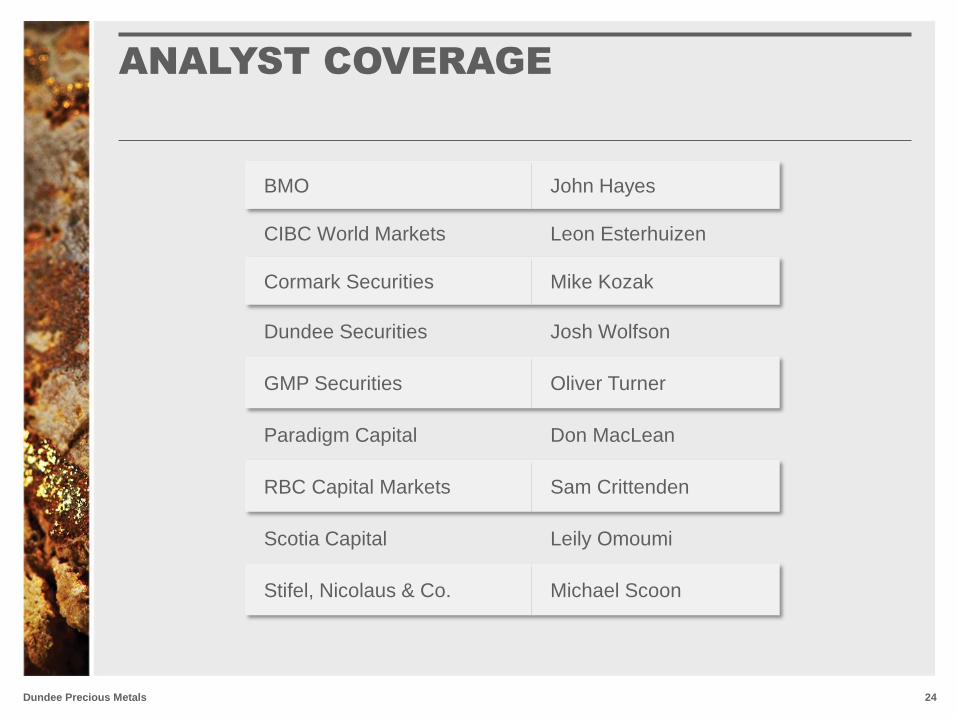

ANALYST COVERAGE

24 Dundee Precious Metals

BMO John Hayes

CIBC World Markets Leon Esterhuizen

Cormark Securities Mike Kozak

Dundee Securities Josh Wolfson

GMP Securities Oliver Turner

Paradigm Capital Don MacLean

RBC Capital Markets Sam Crittenden

Scotia Capital Leily Omoumi

Stifel, Nicolaus & Co. Michael Scoon

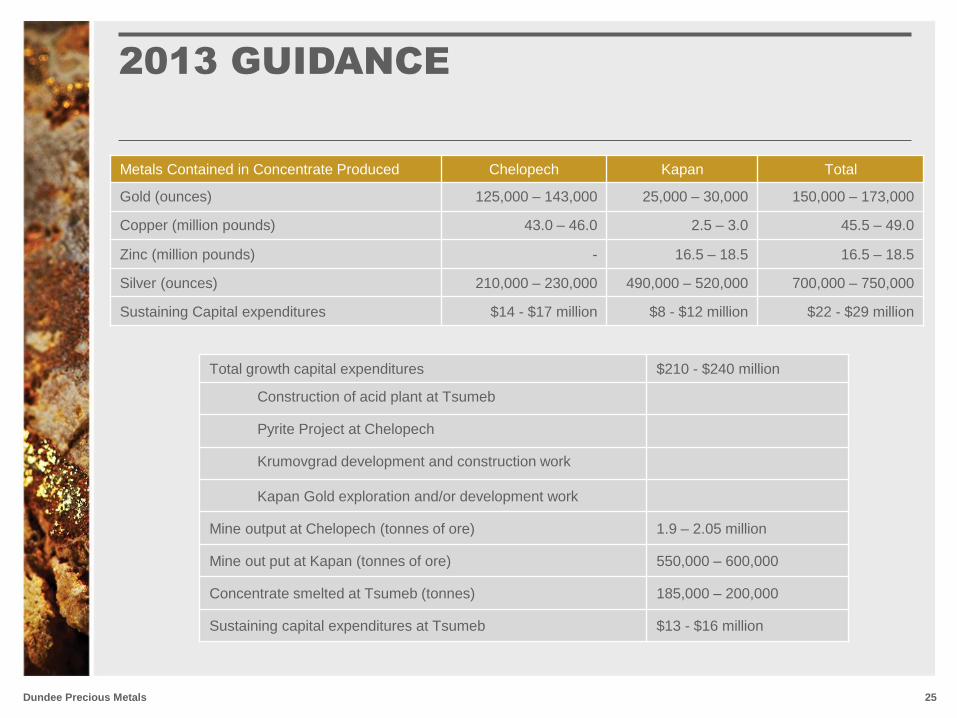

2013 GUIDANCE

25 Dundee Precious Metals

Metals Contained in Concentrate Produced Chelopech Kapan Total

Gold (ounces) 125,000 – 143,000 25,000 – 30,000 150,000 – 173,000

Copper (million pounds) 43.0 – 46.0 2.5 – 3.0 45.5 – 49.0

Zinc (million pounds) - 16.5 – 18.5 16.5 – 18.5

Silver (ounces) 210,000 – 230,000 490,000 – 520,000 700,000 – 750,000

Sustaining Capital expenditures $14 - $17 million $8 - $12 million $22 - $29 million

Total growth capital expenditures $210 - $240 million

Construction of acid plant at Tsumeb

Pyrite Project at Chelopech

Krumovgrad development and construction work

Kapan Gold exploration and/or development work

Mine output at Chelopech (tonnes of ore) 1.9 – 2.05 million

Mine out put at Kapan (tonnes of ore) 550,000 – 600,000

Concentrate smelted at Tsumeb (tonnes) 185,000 – 200,000

Sustaining capital expenditures at Tsumeb $13 - $16 million

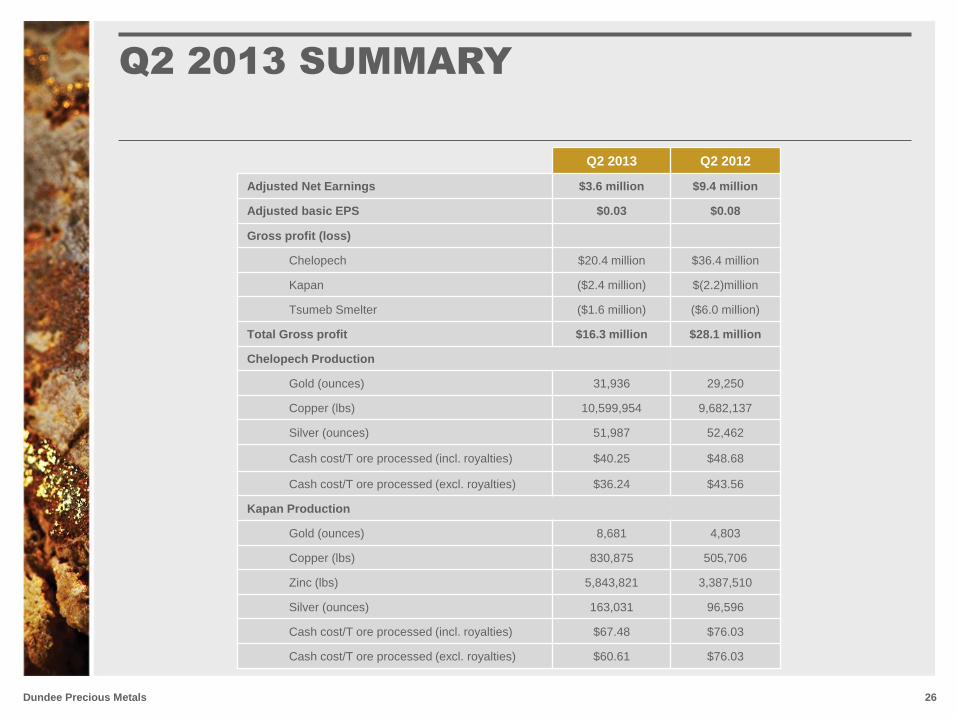

Q2 2013 SUMMARY

26 Dundee Precious Metals

Q2 2013 Q2 2012

Adjusted Net Earnings $3.6 million $9.4 million

Adjusted basic EPS $0.03 $0.08

Gross profit (loss)

Chelopech $20.4 million $36.4 million

Kapan ($2.4 million) $(2.2)million

Tsumeb Smelter ($1.6 million) ($6.0 million)

Total Gross profit $16.3 million $28.1 million

Chelopech Production

Gold (ounces) 31,936 29,250

Copper (lbs) 10,599,954 9,682,137

Silver (ounces) 51,987 52,462

Cash cost/T ore processed (incl. royalties) $40.25 $48.68

Cash cost/T ore processed (excl. royalties) $36.24 $43.56

Kapan Production

Gold (ounces) 8,681 4,803

Copper (lbs) 830,875 505,706

Zinc (lbs) 5,843,821 3,387,510

Silver (ounces) 163,031 96,596

Cash cost/T ore processed (incl. royalties) $67.48 $76.03

Cash cost/T ore processed (excl. royalties) $60.61 $76.03

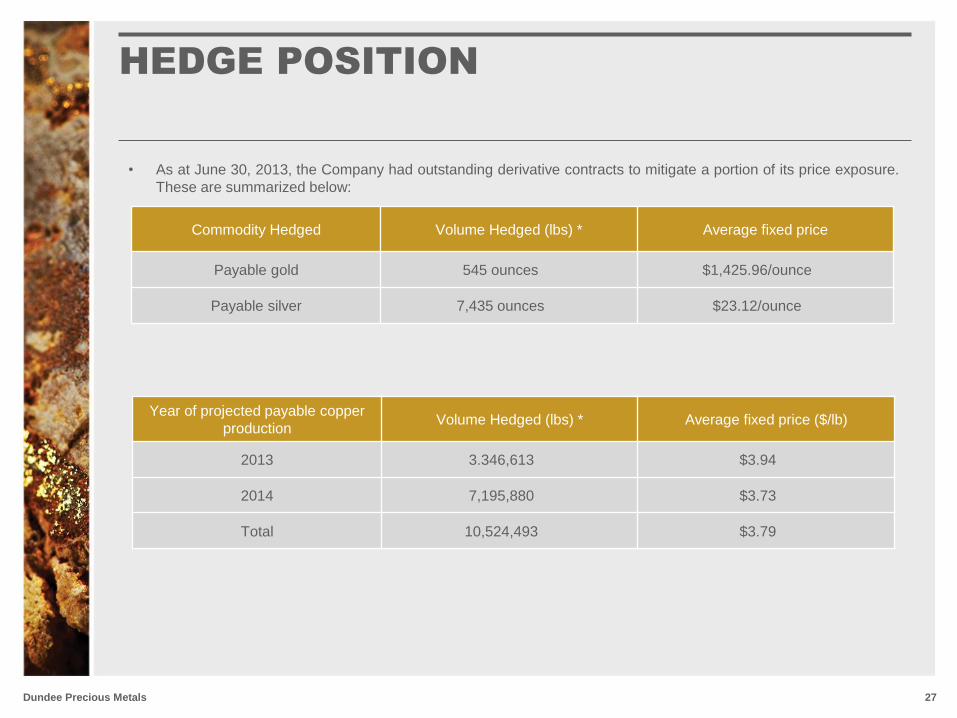

HEDGE POSITION

27 Dundee Precious Metals

Year of projected payable copper

production Volume Hedged (lbs) * Average fixed price ($/lb)

2013 3.346,613 $3.94

2014 7,195,880 $3.73

Total 10,524,493 $3.79

• As at June 30, 2013, the Company had outstanding derivative contracts to mitigate a portion of its price exposure.

These are summarized below:

Commodity Hedged Volume Hedged (lbs) * Average fixed price

Payable gold 545 ounces $1,425.96/ounce

Payable silver 7,435 ounces $23.12/ounce

CHELOPECH MINE:

UPDATED MINERAL RESERVES AND RESOURCES

28 Dundee Precious Metals

Chelopech Mineral Reserves – December 31, 2012

Category

Tonnes

(M)

Gold Copper Silver

Grade

(g/t)

Ounces

(M)

Grade

(%)

Pounds

(M)

Grade

(g/t) Ounces (M)

Proven 12.3 3.4 1.4 1.3 340 9.3 3.7

Probable 9.3 3.8 1.1 0.9 180 5.7 1.7

Total 21.6 3.6 2.5 1.1 519 7.7 5.4

Chelopech Mineral Resources – December 31, 2012

Category

Tonnes

(M)

Gold Copper Silver

Grade (g/t)

Ounces

(M)

Grade

(%)

Pounds

(M)

Grade

(g/t) Ounces (M)

Measured 15.1 4.0 2.0 1.5 490 10.3 5.0

Indicated 14.0 4.0 1.8 1.1 336 8.5 3.8

M&I 29.1 4.0 3.8 1.3 825 9.4 8.8

Inferred 9.3 2.9 0.9 0.9 182 10.6 3.2

1. The rounding of tonnage and grade figures has resulted in some columns showing relatively minor discrepancies in sum totals.

2. All Mineral Resources and Mineral Reserves Estimates have been determined and reported in accordance with NI 43-101 and the classification adopted by the CIM.

3. Chelopech Mineral Reserves are based on a gold equivalent cut-off of 4 g/t (Au g/t + 2.06xCu%) and a cut-off of USD 10 profit/tonne using NSR analysis, as of December 31, 2012. This information has been

prepared by Gordon Fellows who is a QP as defined in NI 43-101 and not independent of the Company.

4. Chelopech Mineral Resources are based on a gold equivalent cut-off 3 g/t (Au g/t + 2.06xCu%) and a greater than USD 0 profit/tonne test using NSR analysis, as of December 31, 2012. This information has

been prepared by Petya Kuzmanova and reviewed and approved by Julian Barnes. Julian Barnes is a QP as defined in NI 43-101 and not independent of the Company.

5. Mineral Reserves and Mineral Resources for Chelopech are based on long term metals prices of USD 1,250/oz Au, USD 2.75/lb Cu, USD 25/oz Ag.

6. Measured and Indicated Mineral Resources are inclusive of Proven and Probable Mineral Reserves.

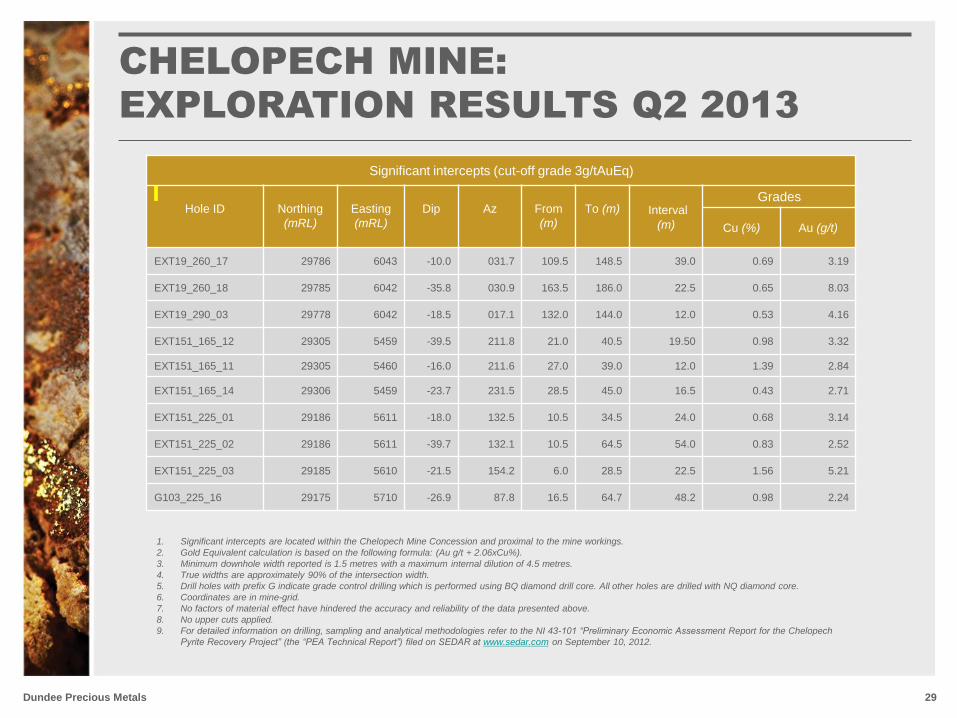

CHELOPECH MINE:

EXPLORATION RESULTS Q2 2013

29 Dundee Precious Metals

Significant intercepts (cut-off grade 3g/tAuEq)

Hole ID

Northing

(mRL)

Easting

(mRL)

Dip

Az

From

(m)

To (m) Interval

(m)

Grades

Cu (%) Au (g/t)

EXT19_260_17 29786 6043 -10.0 031.7 109.5 148.5 39.0 0.69 3.19

EXT19_260_18 29785 6042 -35.8 030.9 163.5 186.0 22.5 0.65 8.03

EXT19_290_03 29778 6042 -18.5 017.1 132.0 144.0 12.0 0.53 4.16

EXT151_165_12 29305 5459 -39.5 211.8 21.0 40.5 19.50 0.98 3.32

EXT151_165_11 29305 5460 -16.0 211.6 27.0 39.0 12.0 1.39 2.84

EXT151_165_14 29306 5459 -23.7 231.5 28.5 45.0 16.5 0.43 2.71

EXT151_225_01 29186 5611 -18.0 132.5 10.5 34.5 24.0 0.68 3.14

EXT151_225_02 29186 5611 -39.7 132.1 10.5 64.5 54.0 0.83 2.52

EXT151_225_03 29185 5610 -21.5 154.2 6.0 28.5 22.5 1.56 5.21

G103_225_16 29175 5710 -26.9 87.8 16.5 64.7 48.2 0.98 2.24

1. Significant intercepts are located within the Chelopech Mine Concession and proximal to the mine workings.

2. Gold Equivalent calculation is based on the following formula: (Au g/t + 2.06xCu%).

3. Minimum downhole width reported is 1.5 metres with a maximum internal dilution of 4.5 metres.

4. True widths are approximately 90% of the intersection width.

5. Drill holes with prefix G indicate grade control drilling which is performed using BQ diamond drill core. All other holes are drilled with NQ diamond core.

6. Coordinates are in mine-grid.

7. No factors of material effect have hindered the accuracy and reliability of the data presented above.

8. No upper cuts applied.

9. For detailed information on drilling, sampling and analytical methodologies refer to the NI 43-101 “Preliminary Economic Assessment Report for the Chelopech

Pyrite Recovery Project” (the “PEA Technical Report”) filed on SEDAR at www.sedar.com on September 10, 2012.

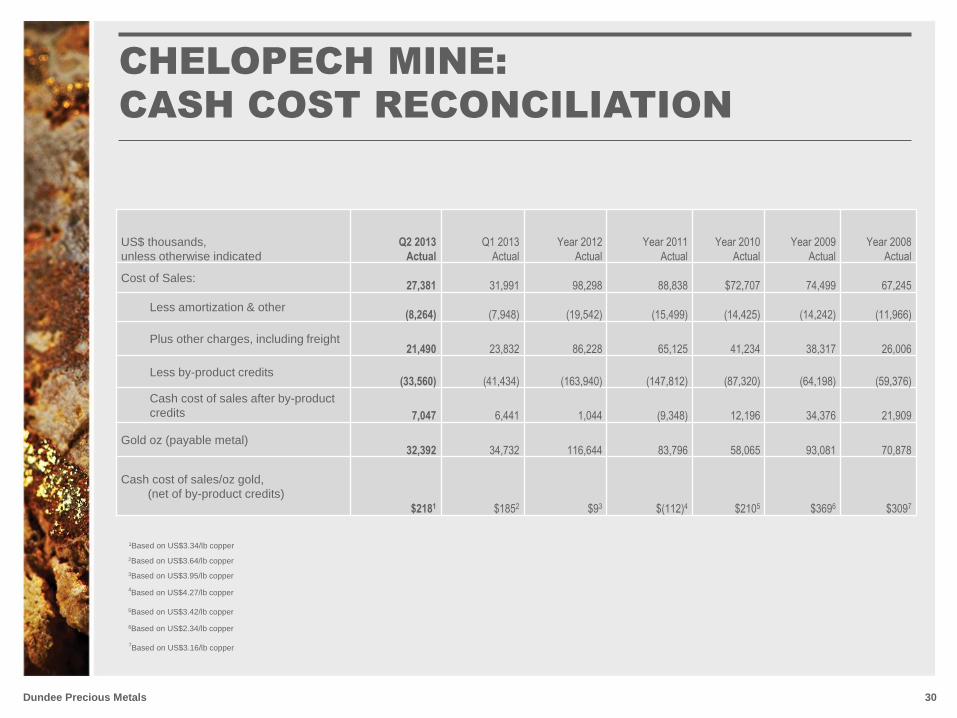

CHELOPECH MINE:

CASH COST RECONCILIATION

30 Dundee Precious Metals

US$ thousands,

unless otherwise indicated

Q2 2013

Actual

Q1 2013

Actual

Year 2012

Actual

Year 2011

Actual

Year 2010

Actual

Year 2009

Actual

Year 2008

Actual

Cost of Sales: 27,381 31,991 98,298 88,838 $72,707 74,499 67,245

Less amortization & other (8,264) (7,948) (19,542) (15,499) (14,425) (14,242) (11,966)

Plus other charges, including freight 21,490 23,832 86,228 65,125 41,234 38,317 26,006

Less by-product credits (33,560) (41,434) (163,940) (147,812) (87,320) (64,198) (59,376)

Cash cost of sales after by-product

credits 7,047 6,441 1,044 (9,348) 12,196 34,376 21,909

Gold oz (payable metal) 32,392 34,732 116,644 83,796 58,065 93,081 70,878

Cash cost of sales/oz gold,

(net of by-product credits)

$2181 $1852 $93 $(112)4 $2105 $3696 $3097

6Based on US$2.34/lb copper

7Based on US$3.16/lb copper

5Based on US$3.42/lb copper

4Based on US$4.27/lb copper

3Based on US$3.95/lb copper

2Based on US$3.64/lb copper

1Based on US$3.34/lb copper

CHELOPECH MINE:

CASH COST PER TONNE OF ORE RECONCILIATION

31 Dundee Precious Metals

1. Gold, copper and zinc are accounted for as co-products. Total cash costs are net of by-product silver revenue.

US$ thousands, unless otherwise indicated

For the periods indicated

Q2 2013

Actual

Q1

2013

Year 2012

Actual

Year 2011

Actual

Year 2010

Actual

Year 2009

Actual

Year 2008

Actual

Ore processed (mt) 501,134 513,360 1,819,687 1,353,733 1,000,781 980,928 900,563

Cost of sales 27,381 31,991 98,298 $ 88,838 $ 72,707 75,647 67,423

Add (deduct):

Depreciation, amortization & other non-cash

costs (8,264) (7,948) (19,542) (15,499) (14,425) (15,390) (11,966)

Change in concentrate inventory 1,054 (2,911) 4,535 862 (2,018) (419) (178)

Total cash cost of production 20,171 21,132 83,291 $ 74,201 $ 56,264 59,838 55,279

Cash cost per tonne of ore processed, including

royalties $40.25 $41.16 $ 45.77 $ 54.81 $ 56.22 $ 61.00 $ 61.38

Cash cost per tonne of ore processed, excluding

royalties $36.24 $36.55 $ 41.16 $ 49.99 $ 51.54 $ 55.23 $ 57.87

KAPAN MINE:

MINERAL RESOURCE ESTIMATE

32 Dundee Precious Metals

Cut off

(AuEq - g/t)

Tonnage

(Mt)

Gold Equiv.

(g/t)

Copper

(%)

Gold

(g/t)

Silver

(g/t)

Zinc

(%)

0.50 335.8 1.19 0.11 0.48 8.39 0.41

0.75 226.5 1.47 0.13 0.61 10.32 0.49

1.00 147.1 1.80 0.15 0.79 12.62 0.57

1.25 98.3 2.14 0.17 0.99 14.99 0.65

1.50 69.8 2.45 0.18 1.19 17.00 0.72

1.75 49.2 2.80 0.19 1.43 19.14 0.78

2.00 36.3 3.13 0.19 1.68 20.87 0.83

Shahumyan Deposit – September 2008

Inferred Mineral Resource – Ordinary Kriging Estimate

10mE x 10mN x 10mRL Block Size – 5m Capped Input Composite Data

AuEq US$ price assumptions: Cu $2.50/lb, Au $850/oz, Ag $16/oz and Zn $1.00/lb

KAPAN MINE:

EXPLORATION RESULTS Q2 2013

33 Dundee Precious Metals

Surface significant intercepts (SHDDR holes, cut-off grade 0.5 g/t AuEq) and underground significant intercepts (E holes, cut-off

grade 1.0g/t AuEq)

Hole ID Northing

(mRL)

Easting

(mRL)

RL

Dip

Azi

From

(m)

To

(m)

Interval

(m) & AuEQ

Au

(g/t)

Ag

(g/t)

Cu

(%)

Zn

(%)

E712DE039 4343207 8623972 712 -46.4 313.8 87.0 90.0 3m @ 19.67 11.11 187.2 1.81 3.37

E712DE040 4343207 8623972 712 -54.8 315.4 87.0 89.0 2m @ 60.32 47.47 343.9 2.65 2.94

E712DE044 4343208 8623974 714 -54.8 302.6 97.0 99.0 2m @ 28.07 19.06 161.0 1.72 5.42

E712DW015 4343183 8623801 714 -50.4 355.6 140.0 143.0 3m @ 7.46 4.59 18.4 1.49 0.07

SHDDR0557 4343577 8623580 916 -60.9 0.9 28.0 35.0 7m @ 6.22 1.54 78.7 0.59 3.89

SHDDR0560 4343572 8623579 916 -72.7 352.4 0.0 6.6 6.6m @ 4.93 2.87 39.3 0.30 1.45

SHDDR0560 4343572 8623579 916 -72.7 352.4 95.0 102.0 7m @ 5.11 1.19 54.2 0.36 4.09

SHDDR0560 4343572 8623579 916 -72.7 352.4 248.0 254.0 6m @ 4.88 1.82 64.5 0.75 1.07

SHDDR0561 4343636 8623531 927 -55.0 7.3 223.0 228.0 5m @ 6.58 3.50 43.2 0.50 2.53

SHDDR0562 4343540 8623470 929 -59.3 355.5 296.0 298.0 2m @ 23.72 17.52 130.4 0.17 6.05

SHDDR0563A 4343634 8623531 927 -63.2 6.8 239.0 244.0 5m @ 7.96 3.22 49.2 1.70 1.75

SHDDR0568 4343560 8623517 923 -62.3 8.1 142.0 157.0 15m @ 6.82 2.57 43.9 0.86 3.57

1. In situ gold equivalent (AuEq) grade based on the following long-term metal prices: $1,250 per ounce for gold, $25 per ounce for silver, $3.00 per pound for copper and $1.00 per

pound for zinc.

2. Holes with the prefix SHDDR are surface HQ diamond drilling, while E holes are underground drilling.

3. Significant intercepts for surface holes are located within the Central and Southern Zones while underground drilling is located within the Central Zone and Southern Zones of the

Shahumyan Deposit.

4. True widths are approximately 90% of the intersection width.

5. Minimum width reported is 2 metres and a maximum internal dilution of 2 metres.

6. All survey coordinates are transformed to AUSPOS.

7. No factors of material effect have hindered the accuracy and reliability of the data presented above.

8. No upper cuts have been applied.

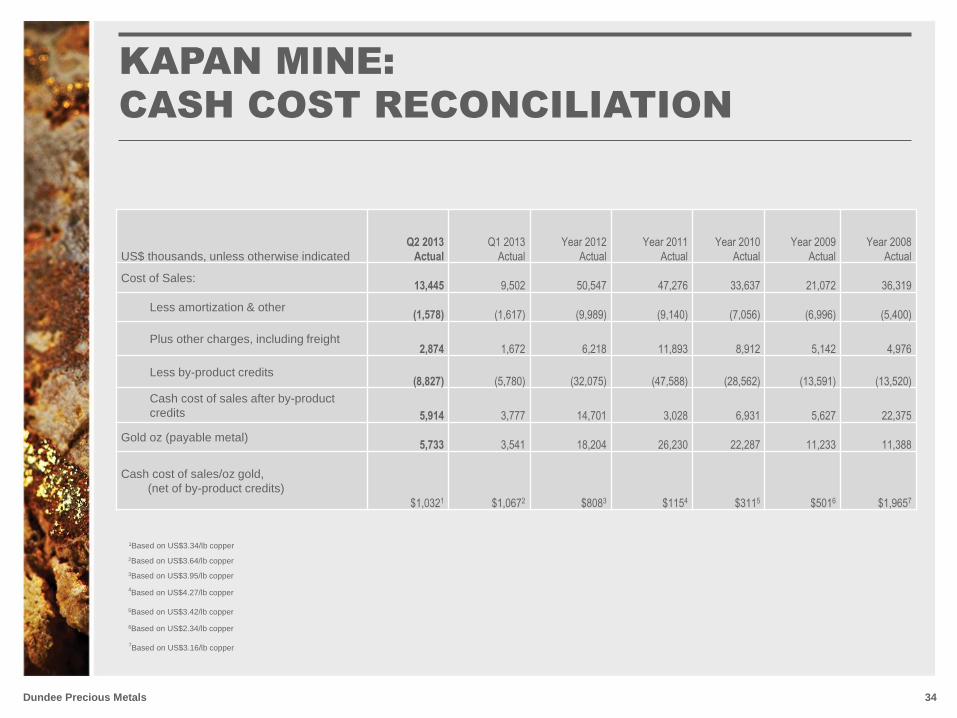

KAPAN MINE:

CASH COST RECONCILIATION

34 Dundee Precious Metals

US$ thousands, unless otherwise indicated

Q2 2013

Actual

Q1 2013

Actual

Year 2012

Actual

Year 2011

Actual

Year 2010

Actual

Year 2009

Actual

Year 2008

Actual

Cost of Sales: 13,445 9,502 50,547 47,276 33,637 21,072 36,319

Less amortization & other (1,578) (1,617) (9,989) (9,140) (7,056) (6,996) (5,400)

Plus other charges, including freight 2,874 1,672 6,218 11,893 8,912 5,142 4,976

Less by-product credits (8,827) (5,780) (32,075) (47,588) (28,562) (13,591) (13,520)

Cash cost of sales after by-product

credits 5,914 3,777 14,701 3,028 6,931 5,627 22,375

Gold oz (payable metal) 5,733 3,541 18,204 26,230 22,287 11,233 11,388

Cash cost of sales/oz gold,

(net of by-product credits)

$1,0321 $1,0672 $8083 $1154 $3115 $5016 $1,9657

6Based on US$2.34/lb copper

7Based on US$3.16/lb copper

5Based on US$3.42/lb copper

4Based on US$4.27/lb copper

3Based on US$3.95/lb copper

2Based on US$3.64/lb copper

1Based on US$3.34/lb copper

KAPAN MINE:

CASH COST PER TONNE OF ORE RECONCILIATION

35 Dundee Precious Metals

1. Gold, copper and zinc are accounted for as co-products. Total cash costs are net of by-product silver revenue.

US$ thousands, unless otherwise indicated

For the periods indicated

Q2 2013

Actual

Q1 2013

Actual

Year 2012

Actual

Year 2011

Actual

Year 2010

Actual

Year 2009

Actual

Year 2008

Actual

Ore processed (mt) 162,648 119,663 509,419 581,852 428,865 218,235 269,033

Cost of sales 13,445 9,502 50,547 $ 47,276 $ 33,637 $ 21,197 $ 36,319

Add (deduct):

Depreciation, amortization & other non-cash

costs (1,578) (1,617) (10,883) (9,140) (7,056) (4,047) (3,668)

Care and maintenance costs - - - - - (3,074) (1,732)

Change in concentrate inventory (892) 1,189 (718) 416 3,572 1,696 (1,485)

Total cash cost of production 7,263 9,074 38,946 $ 38,552 $ 30,153 $ 15,772 $ 29,434

Cash cost per tonne of ore processed

(royalties not applicable in 2009) $67.48 $75.83 $ 76.45 $ 66.26 $ 70.31 $ 72.27 $ 109.40

Cash cost per tonne of ore processed,

excluding royalties $60.61 $72.36 $ 69.10 $ 62.57 $ 66.33 $ 72.27 $ 109.40

KRUMOVGRAD GOLD PROJECT

36 Dundee Precious Metals

KRUMOVGRAD GOLD PROJECT

37 Dundee Precious Metals

Krumovgrad Mineral Reserves – December 31, 2011

Category

Tonnes

(M)

Gold Silver

Grade

(g/t)

Ounces

(M)

Grade

(g/t) Ounces (M)

Proven 2.94 4.70 0.44 2.54 0.24

Probable 4.30 2.44 0.34 1.52 0.21

Total 7.24 3.36 0.78 1.92 0.45

Krumovgrad Mineral Resources – December 31, 2011

Category

Tonnes

(M)

Gold Silver

Grade (g/t)

Ounces

(M)

Grade

(g/t) Ounces (M)

Measured 3.30 4.90 0.52 3.00 0.28

Indicated 4.69 2.50 0.38 2.00 0.24

M&I 7.99 3.50 0.90 2.00 0.51

Inferred 0.40 1.20 0.02 1.00 0.01

1. Rounding of tonnage and grade figures has resulted in some columns showing relatively minor discrepancies in sum totals.

2. All Mineral Resource Estimates have been determined and reported in accordance with NI 43-101 and the classification adopted by the CIM.

3. Krumovgrad Mineral Reserves and Resources are based on the Krumovgrad 2012 Technical Report using a variable economic cut-off grade and 0.5 g/t Au respectively.

4. All Mineral Reserves and Resources are based on long term metals prices of $1,250 Au, $3/lb Cu, $25/oz Ag and $1/lb Zn.

5. Measured and Indicated Mineral Resources are inclusive of Proven and Probable Reserves.

dundeeprecious.com

One Adelaide Street East Suite 500

Toronto, Ontario M5C 2V9 T: 416 365-5191

Investor Relations T: 416 365-2851

TSX: DPM – common shares

DPM.WT.A – 2015 Warrants

Proudly celebrating 30 years as

a Toronto Stock Exchange listed

company

Related Documents