Budgeting in Italy Jón Ragnar Blöndal Head of Budgeting and Public Expenditures Public Governance Directorate Organisation for Economic Cooperation and Development 36 th Annual Meeting of Senior Budget Officials Rome, 11 June 2015

Budgeting in Italy - Jon Blöndal, OECD

Aug 11, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Budgeting in Italy

Jón Ragnar Blöndal

Head of Budgeting and Public Expenditures

Public Governance Directorate

Organisation for Economic Cooperation and Development

36th Annual Meeting of Senior Budget Officials

Rome, 11 June 2015

Agenda

• Special Characteristics

• Annual Budget Cycle

• Conclusions and Recommendations

Special Characteristics

• “Budget” and “Stability Law”

• Role of Ministry of Economy and Finance

and Line Ministries

• Medium-Term Expenditure Framework

• Performance and Results

• Spending Reviews

• Responsibility for Economic Assumptions

– Parliamentary Budget Office

• Unpaid Commercial Invoices

“Budget” and “Stability Law”

• All appropriations must be in separate enabling legislation – Very limited exceptions

• Great distinction between “Budget” and “Stability Law”

• The “Budget” – A baseline of expenditures for current legislation

– Little political discussion; considered technical

• The “Stability Law” – All new expenditures require new laws or amendments to existing

legislation

– An omnibus law that enjoys “fast-track” treatment in parliament

– Focus of budget negotiations and parliamentary debate

• The two will be merged in 2017 – Implications

Role of Ministry of Economy and Finance and Line Ministries

• Ministry of Economy and Finance – Pre-eminent ministry within the Italian government – Ragioneria Generale della Stato – A high office of state, traces its origins to the very foundation of a

unified Italy

• Differs significantly from typical budget offices – 6,000 staff, focused on expenditure issues – Offices in each ministry for budget execution – “Bollino Blu”

• Line Ministries

– No central budget capacity – Diffuse and fragmented process in each ministry – Obstacle for ministry-wide internal prioritization, reallocation and

evaluation of programmes

Medium-Term Expenditure Framework

• A pioneer in macro-fiscal medium-term planning

• Links with annual budget process appear deficient – Out-year expenditure (growth) implications of current policy – Certain expenditures not included – Incorporating other expenditures not robust

• First phase of each annual budget process is a lengthy negotiating process for the baseline

• Reforms undertaken in 2015

Performance and Results

• A challenge as in many OECD countries

• Two “waves” of reform – 1997: Reduction of line items and “Preliminary Notes” – 2009: Missions (34) and Programmes (165 > 181)

• Abundance of performance information – Largely focused on administrative, not policy issues – Presentation not judged favorably by users

• Lack of performance culture – Near total focus in inputs

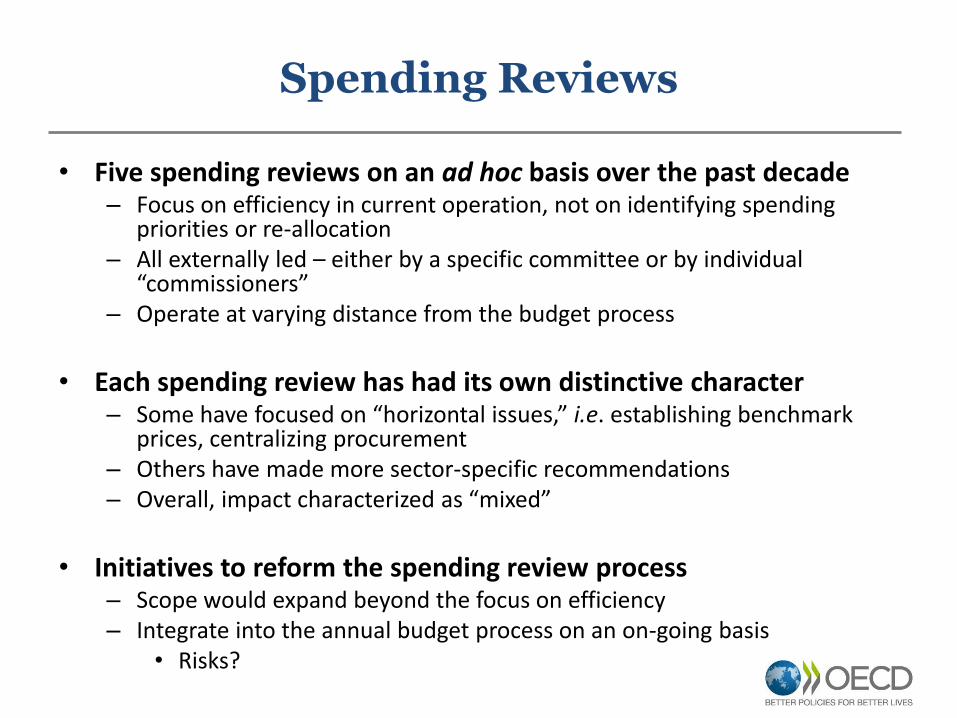

Spending Reviews

• Five spending reviews on an ad hoc basis over the past decade – Focus on efficiency in current operation, not on identifying spending

priorities or re-allocation – All externally led – either by a specific committee or by individual

“commissioners” – Operate at varying distance from the budget process

• Each spending review has had its own distinctive character

– Some have focused on “horizontal issues,” i.e. establishing benchmark prices, centralizing procurement

– Others have made more sector-specific recommendations – Overall, impact characterized as “mixed”

• Initiatives to reform the spending review process

– Scope would expand beyond the focus on efficiency – Integrate into the annual budget process on an on-going basis

• Risks?

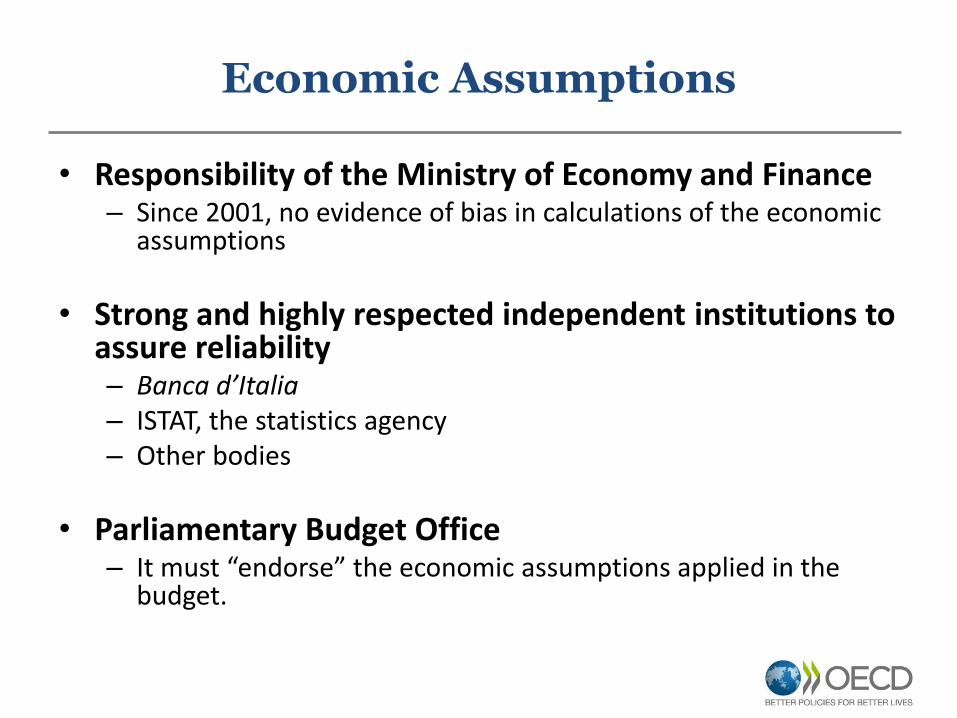

Economic Assumptions

• Responsibility of the Ministry of Economy and Finance – Since 2001, no evidence of bias in calculations of the economic

assumptions

• Strong and highly respected independent institutions to assure reliability – Banca d’Italia – ISTAT, the statistics agency – Other bodies

• Parliamentary Budget Office – It must “endorse” the economic assumptions applied in the

budget.

Unpaid Commercial Invoices

• Italy was once characterized by a large amount of such debt

– Did not count as “debt” for Eurostat purposes

• In 2014, the Banca d’Italia estimated this to be over 5% of GDP – half of which was overdue

– Based on a survey of government suppliers and was as such an overestimate.

• The government devoted significant funds to clear outstanding – and valid – invoices and put in place safeguards to prevent such behavior

Annual Budget Cycle

• Timeline has varied greatly in recent years with important milestones shifting significantly from one year to another

• Character of the budget formulation cycle depends

very much on each government

• Annual budget formulation cycle: – Phase I: Macro-Fiscal Policy Setting – Phase II: Baseline Updates (“The Budget”) – Phase III: Resource Allocation (“The Stability Law”)

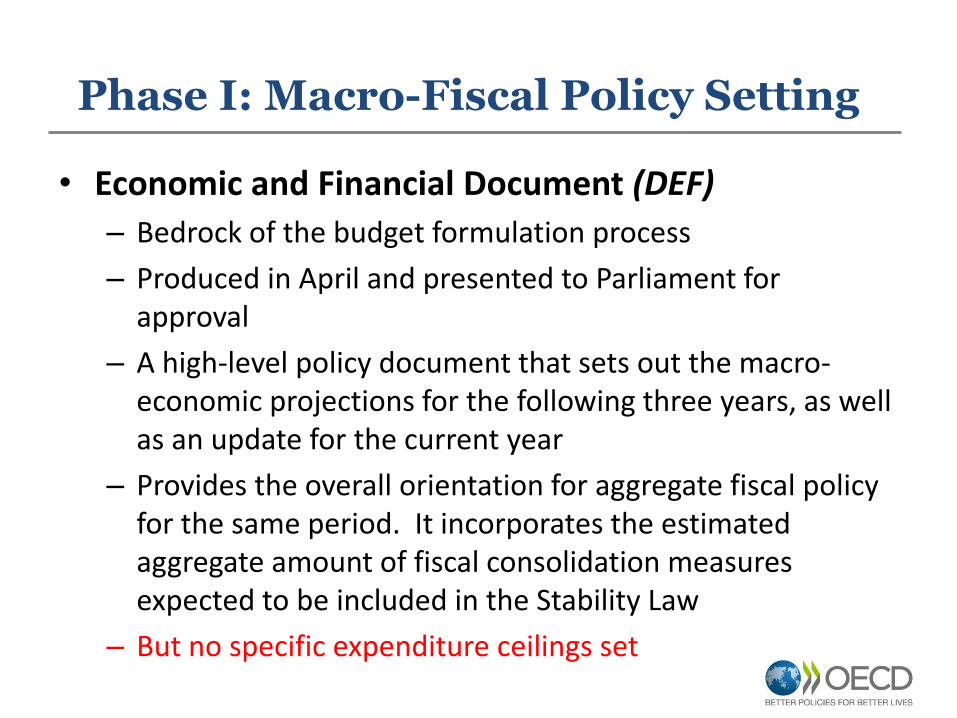

Phase I: Macro-Fiscal Policy Setting

• Economic and Financial Document (DEF)

– Bedrock of the budget formulation process

– Produced in April and presented to Parliament for approval

– A high-level policy document that sets out the macro-economic projections for the following three years, as well as an update for the current year

– Provides the overall orientation for aggregate fiscal policy for the same period. It incorporates the estimated aggregate amount of fiscal consolidation measures expected to be included in the Stability Law

– But no specific expenditure ceilings set

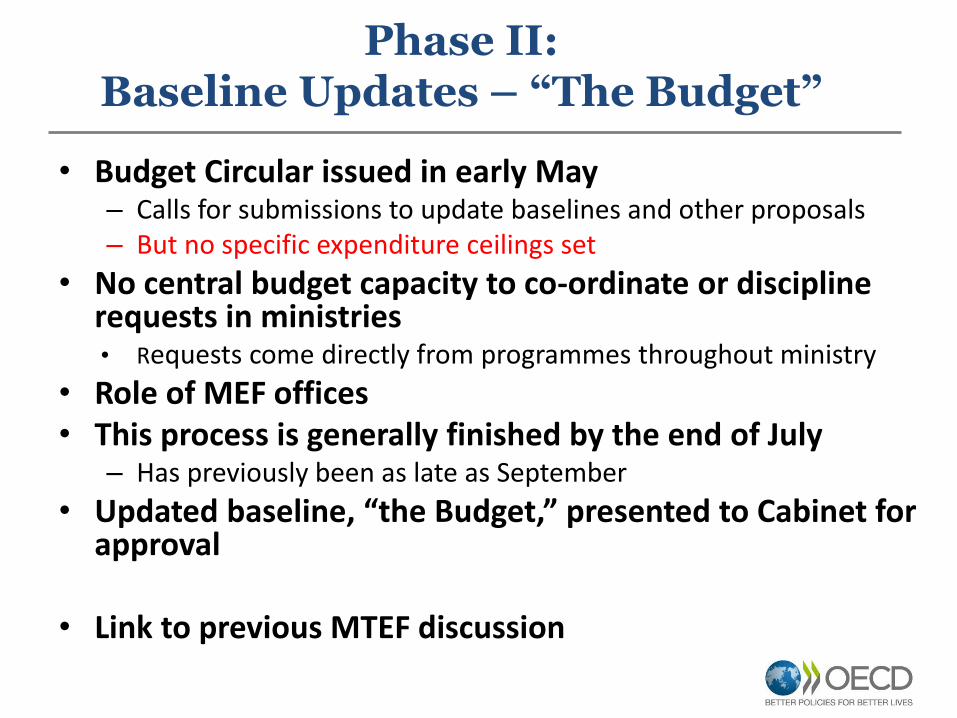

Phase II: Baseline Updates – “The Budget”

• Budget Circular issued in early May – Calls for submissions to update baselines and other proposals – But no specific expenditure ceilings set

• No central budget capacity to co-ordinate or discipline requests in ministries • Requests come directly from programmes throughout ministry

• Role of MEF offices • This process is generally finished by the end of July

– Has previously been as late as September

• Updated baseline, “the Budget,” presented to Cabinet for approval

• Link to previous MTEF discussion

Phase III: Resource Allocation – “The Stability Law”

• Normally “emerges” in July; climaxes in September. • Launched with formal meetings between the Ministry of Economy

and Finance and each line ministry at a high-level • Intensive but Informal Discussions

– Between Prime Minister and Minister of Economy and Finance – Between Minister of Economy and Finance and line ministers – Between respective staffs

• Updated Economic and Financial Document (DEF) available in mid-September – Basis for final decisions for the Stability Law.

• Decisions are taken quickly reflecting the informal discussions that have taken places during the previous months – Specific programmes – General savings targets

• The budget and Stability Law are then presented jointly to Parliament by 15 October. Will be merged in 2017.

Conclusions

• Italy is in the process of making significant reforms to its budget formulation process … – Merging of the budget and Stability Laws – A more robust MTEF process

• … Provides a basis for further reform of the budget formulation process

• Establish a central budget function in each line ministry – Full ownership by the respective ministry – Co-ordinate and streamline the work of line ministries; promote priority-setting and internal

re-allocations – Foster a greater focus on performance and results and be the basis for effective top-down

budgeting – Recasts the budget process and enhances strategic capacity to contribute to future spending

reviews – Continued role of MOFE offices

• Establish expenditure ceilings for each ministry at the beginning of the budget formulation process – Optimally, this could form part of the Economic and Financial Documentation (DEF) issued in

April, or with the Budget Circular issued in May. – This would be introduced with more binding timelines throughout the budget formulation

process.

Related Documents