COO Employee Council February 16, 2012 Budget Overview

Budget Overview

Feb 25, 2016

Budget Overview. COO Employee Council February 16, 2012. Budget Overview. Current Budget & Methodology New Internal Financial Model Capital Budget Questions. UVa’s 2011-12 Operating Budget (in millions). Academic Division$ 1,344.6 Medical Center $ 1,108.1 - PowerPoint PPT Presentation

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

COO Employee CouncilFebruary 16, 2012

Budget Overview

Budget Overview

• Current Budget & Methodology• New Internal Financial Model• Capital Budget• Questions

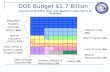

UVa’s 2011-12 Operating Budget(in millions)

Academic Division $ 1,344.6

Medical Center $ 1,108.1College at Wise $

34.3Total $ 2,487.0

Academic Division 54.0%

Medical Cen-ter

44.6%

Wise 1.4%

2011-12 Major Funding Sources Academic Division - $1.36 Billion

Tuition & Fees,32.6%

State Appropria-tions,9.5%Sponsored Programs,

24.0%

Auxiliary Revenues,

13.5%

Endowment Distribution,

10.4%

Expendable Gifts, 7.3%

Operating Balances1.2%

Sales & Other1.5%

2011-12 Major Spending AreasAcademic Division - $1.34 Billion

In-struction; 25.3%

Re-search & Pub-

lic Serv.

; 23.0%

Academic Support; 9.6%

Stu-dent Ser-

vices; 3.1%

General Ad-min, 5.1%

O&M, 8.2%

Fi-nancial Aid; 11.6%

Aux-il-

iaries;

14.1%

By Activity

Fac-ulty Com

p.31.3%

Staff Com

p. 21.9%

Wages 4.1%

GTA/GRA 2.1%

Other40.6%

By Expenditure Category

6

Current Budget Methodology

A Hybrid of Three Approaches:• Targeted Budgets• Sales and Services Budgets• Summary Budgets

7

Targeted Budgets• State general (SG), state restricted (SR), local general (LG), F&A

institutional (FI), endowment institutional (EI), and gift institutional (DI)

• University Budget Office (UBO) provides budget target and modifies it for salary increases, fringe benefit changes, addenda, and budget reductions

• Central covers costs for facilities and central administration

• Unit manages internal allocation of budget, hiring, carryforward, and operational decisions

• Central oversight is by UBO, managed on a year-to-date basis

• Required to be funded and budgeted in the Integrated System (IS)

8

Sales & Services Budgets• State sales and services (SS), state auxiliaries (SA), local sales and

services (LS), local auxiliaries (LA), and local other (LO)• Revenue-generating, self-supporting unit approach• Unit manages revenues and direct expenses (salary and fringe changes)• Cost for facilities and central administration responsibility varies:

– 100% facilities and indirect costs paid by auxiliaries– 100% facilities and 10% revenue tax assessed to self-sufficient– 10%-15% revenue tax assessed to some self-supporting units– No facilities or indirect costs assessed to other sales and services units

• Central oversight is by UBO; managed on a year-to-date basis

• Required to be funded and budgeted in the IS

9

Summary Budgets• Endowments (ER, EU, EF), gifts (DR, DU), F&A (FA), grants (G*, Z*),

and intellectual property (IP)

• Unit manages direct expenses (salary and fringe changes)

• Central covers cost of facilities and central administration, with the exception of grants (reimbursed by federal gov’t)

• Allocations and central oversight are by Comptroller’s Office, Gift Accounting, Sponsored Programs, and the VP for Research; managed on a project-to-date basis; not required to be funded and budgeted in the Integrated System

• Summary budgets are submitted to the UBO for purposes of developing a total budget, but they are not uploaded to the IS

Budget Overview

• Current Budget & Methodology• New Internal Financial Model• Capital Budget• Questions

11

Identified Concerns with Current Model• Historically based, with minimal re-alignment for activity

changes• Absence of incentives for innovation, creativity, and revenue

generation• Does not consider all available funds• Does not link resources and uses; inconsistent allocation of

revenue and expenses• Desire by deans for a more open decision-making process• Difficulty in developing multi-year budgets to align with

programmatic planning

12

Work to Date• Collected and reviewed data from peers; developed potential schematic and

identified possible methods of allocating revenues and central expenses

• Drafted a sources and uses report to represent operational cash flows by major revenue center

• Reviewed funding across units to consider a more consistent approach to record resource-sharing

• Developed a Statement of Purpose and preliminary timeline

• Identified Executive Co-Chairs and engaged senior administration in Steering Committee

• Conducted a needs analysis survey for financial reporting in academic and administrative units

• Completed preliminary groundwork to understand major revenue and service centers

• Launched a website: http://www.virginia.edu/resourcingthemission/

New Internal Financial ModelSteering Committee

Co-Chairs: John Simon, Michael Strine

Steering Committee Task Forces

Financial Reporting,

System Preparedness and Training

Communi-cation and

Change Management

Ensure that systems support new model and that people can make the most of new methodologies

• System architecture, assessment, and recommendations

• Reporting requirements

• Report development• Design, develop, and

test • Implementation Plan• Training plan /

schedule• Monitor operations

Ensure that University community is prepared for the new model and that change process is well managed

• Roles & Responsibilities

• Redesign budget process

• Communication• Change

management• Transition planning• Implementation

preparedness• Monitoring

outcomes

Develop methodologies for revenue flows and for incentivizing innovation and increased productivity

• Revenue attribution• Tuition allocation• Alternatives for other

funding (IFP, F&A, general funds, etc.)

• Build model• Incentives for

productivity• Incentives for

growing revenue and innovation

Develop methodologies for cost allocations, service levels and cost containment

• Cost Allocations• Categories for

expenditures• Level of costs for

central services• Benchmarking• Strategy for reserves• Build model• Incentives for

effective, efficient, quality service

• Incentives for stewardship of University resources

Ensure that policies support the new model and ongoing governance & stewardship of University mission and resources

• Inventory current policies

• Create/revise policies as necessary

• Monitor outcomes• Adjust model

and/or policies to ensure proper stewardship of University mission & resources

Revenue & Incentives

Cost and Service Level Architecture

Governance, Policy

Review and Oversight

James Hilton, Lead Bob Pianta, Lead Bob Bruner, Lead Paul Mahoney, Lead Kim Tanzer, Lead

High Level Task Force Timeline

Communication & Change Mgmt

Financial Reporting,

System Preparedness &

Training

Revenue & Incentives

Cost & Service Level

Architecture

Governance, Policy Review and Oversight

Jan-Feb-Mar Apr-May-Jun-Jul-Aug-Sept Oct 2012 - Jun 2013 FY2013-14Communication, Change Mgmt, &

Transition Planning

Education / Change Management / ImplementationMonitor & Adjust

System Architecture, Reporting Assessment / Re-quirements, & Training Plan

Short Term: System Architecture Changes & Report

Development

Test Train / Implement

Monitor & Adjust

Revenue Modeling:Revenue Attribution, Bench-marking, Tuition allocation,

Revenue IncentivesTest Train /

Implement

Current Policy Inventory Create / Revise Policies Approve Policies Train /

ImplementMonitor & Adjust

Cost Modeling:Cost allocations, Level of costs for services, Benchmarking, Strategy

for ReservesExpense Incentives

Long Term: System Architecture Changes & Report

Development

Monitor & Adjust

Input from Phase 11. Reconciled Actual

to Budget Data2. Design Principles DRAFT

Major Steering Committee Report Outs

Development

Implementation Monitor

Design Principles & Decision Mapping

15

Resources on Budget Model TransitionsWebsites of Peer Institutions• University of Florida – Responsibility Center Management, http://www.hr.ufl.edu/training/rcm/index.html• Indiana University – Responsibility Center Management, http://weathertop.bry.indiana.edu/mas/rcm/• University of Iowa – Task Force on Strategic Budgeting, http://provost.uiowa.edu/work/strategic-initiatives/tf-budget.htm• Iowa State University – Resource Management Model,

http://www.public.iastate.edu/~budgetmodel/overview/background.shtml• University of Michigan – University Budget Model, http://www.provost.umich.edu/budgeting/ub_model.pdf• University of New Hampshire – Responsibility Center Management, http://www.unh.edu/rcm/rcmmanual/manualtoc.htm• University of Pennsylvania – Responsibility Center Management, http://www.budget.upenn.edu/rcm/index.shtml• Ohio State, Resource – Centered Budgeting, http://www.rpia.ohio-state.edu/br/archive.html• Syracuse University – Responsibility Center Management, http://budplan.syr.edu/BudPlan/display.cfm?content_ID=%

23%28%28%2D%2C%0A

Books• Responsibility Center Budgeting – An Approach to Decentralized Management for Institutions of Higher

Education, by Edward Whalen. • Responsibility Center Management – Lessons from 25 years of Decentralized Management, by Jon C. Strauss and

John R. Curry

Articles• NACUBO Business Officer, April 2009: The Case for Decentralized Financial Management by Scott

Scarborough, at http://www.nacubo.org/Business_Officer_Magazine/Magazine_Archives/April_2009/The_Case_for_Decentralized_Financial__Management.html

Budget Overview

• Current Budget & Methodology• New Internal Financial Model• Capital Budget• Questions

Major Capital Projects ProgramCurrently Approved – by Status

(in 000s) (updated Jun 2011)

$0

$500,000

$1,000,000

$1,500,000

$2,000,000

$2,500,000

Academic Division Medical Center College at WiseTo be completed by 12/31/2011 Under Construction In Planning On Hold

$2,093,315

$461,304

$182,752

19

Major Capital Projects ProgramNear Term Proposed Through 2014 - By Funding

(in 000s) (updated Jun 2011)

$0

$100,000

$200,000

$300,000

$400,000

$500,000

$600,000

Academic Division Medical Center College at WiseState General Fund Debt Gifts Other NGF

$493,190

$25,460$51,400

21

Major Capital Projects Program Long Term Proposed (2015 - 2022) - By Funding

(in 000s) (updated Jun 2011)

$0

$250,000

$500,000

$750,000

$1,000,000

Academic Division Medical Center College at Wise

State General Fund Debt Gifts Other NGF

$935,216

$36,800None

Questions?

Types of Endowments True restricted endowment – written donor agreement

establishes original gift as an endowment and restrict how distribution can be spent

True unrestricted endowment - written donor agreement establishes original gift as an endowment but does not restrict spending

Quasi restricted endowment – funds are designated (or undesignated) as an endowment by the Board; written donor agreement establishes spending restrictions

Quasi unrestricted endowment - funds are designated (or undesignated) as an endowment by the Board; there are no spending restrictions

Size of the University’s Endowment(in millions)

$1,328 R&V’s Acad Div True Restricted Endow$ 6 R&V’s Acad Div True Unrestricted Endow$ 652 R&V’s Acad Div Quasi Restricted Endow$ 728 R&V’s Acad Div Quasi Unrestricted Endow$ 403 R&V’s Medical Center Endow$ 41 R&V’s Wise Endow$1,112 Affiliated foundations’ funds at UVIMCO$ 168 Other affiliated foundations’ funds$4,438

Distribution Policy• Spending policy has two objectives:

⁻ to provide reliable, predictable distributions to support programs

⁻ to preserve purchasing power of endowment principal to fund programs in perpetuity

⁻ Differing methods are employed; the Board revisits its approach every few years.

⁻ In general, goal is to spend between 4% and 6% of the market value.

Related Documents