Internal Audit & Risk delivering for 1 ANNEX A Internal Audit Report BUDGET MANAGEMENT – DEMAND LED BUDGETS Governance Opinion Adequacy of System Substantial Compliance Substantial Organisational Impact Minor

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Internal Audit & Risk delivering for

1

ANNEX A

Internal Audit Report

BUDGET MANAGEMENT – DEMAND LED BUDGETS

Governance Opinion

Adequacy of System Substantial

Compliance Substantial

Organisational Impact Minor

Internal Audit & Risk delivering for

2

Report Issued 31/05/2017

Follow Up due 30/11/2017

Audit Committee schedule 20/06/2017

Internal Audit & Risk delivering for

3

Executive Summary

1 Background

In February 2017, the Cabinet approved the Council’s Medium Term Financial Strategy and

Financial Sustainability Plan (FSP) and the full Council approved the 2017/18 Budget. The FSP is updated alongside the budget. It sets out the size of the financial challenge, our approach to sustainability and the anticipated impact as a result of changes. In summary,

the Council sought to address a financial gap of £58m from 2017/18 to 2020/21; including a gap of £19.0m in 2017/18.

The Council’s Revenue Budget reflects how the priorities of the Council, and underpinning annual Service Plans, can be delivered within the available level of resources. Total government funding is estimated at £76.9m for 2017/18, compared to £89.7m from 2016/17, a reduction of 14.3%

The 2017/18, Revenue Budget identified funding for ongoing pressures of £12.1m, with a further £17.8m of one-off being funded from identified one-off resources. These pressures

when combined with Government funding reductions, and additional council tax income, have led to the Council needing to identify £18.9m worth of budget reduction and income proposals.

Budget Managers are responsible to ensure that service areas work within the financial constraints of the approved budgets, and to support CLT in the ongoing generation of new

savings proposals for 2017/18 and beyond, which will ensure the Council is financially sustainable over the medium-term.

2 Audit Approach / Scope (including Volume / Value Indicators)

This audit is being completed as an ‘Added Value’ review for the Audit Committee. The

Control Objectives of this audit were to provide assurance to the Audit Committee that robust budget management arrangements exist within Milton Keynes Council, with particular emphasis and focus placed on demand led budgets. Including but not limited to:

• Documentation of the defined budget management arrangements in place within MKC including reporting requirements;

• Confirmation of the roles and responsibilities to support effective and robust budget

management activities; • Specific testing of a sample of demand led budgets to confirm ongoing effective budget

management activities.

It should be noted that this audit takes into consideration the findings and assurances obtained from the previous Budget Management audit completed in December 2016.

Internal Audit & Risk delivering for

4

Further, the scope of this audit has been restricted to Budget Management / Monitoring arrangements and does not comment on Budget Setting activities, as this will be subject to

a more detailed audit and delivered as part of the approved 2017/18 audit plan.

3 Internal Audit Opinion and Main Conclusions 3.1 AUDIT OPINION

Adequacy of System: Substantial

Compliance: Substantial

Organisational Impact: Moderate Minor 3.2 MAIN CONCLUSIONS

Budget Management Guidance and Instructions

Formal and well established budget management instructions, guidance and practices exist, to ensure effective budget activities are completed within MKC. These are contained within a number of corporate documents which are available via the Intranet and within the Constitution.

Budget Management Tool

Budget management / monthly forecasting are completed within MKC utilising the current SAP – Business Objects Planning (BPC). All Budget Managers are required to complete monthly forecasts using the Excel-based tool, for which there are separate modules for capital and revenue budgets. These monthly forecasts which are subject to

formal review by Finance are used to build the budget management report presented ultimately to Cabinet.

Budget Management Training

This audit has identified that formal training in the form of a full day training session entitled ‘Finance for Budget Managers’ ceased in June 2016. The reason for this being

the significant reduction in Budget Manager turn-over and the proposed implementation of the ERP Gold solution, replacing the current SAP ERP solution. This training has however been replaced by ad-hoc Budget Manager training which includes training on the use of the BPC forecasting tool. Additional guidance is also available via

the Finance pages on the Intranet.

Internal Audit & Risk delivering for

5

Reporting

A formal and defined budget management reporting timetable is in place, commencing with the completion of forecast updates by individual budget managers, leading to the production of the monthly budget management reports to the Corporate Leadership

Team (CLT) and then to Cabinet. This audit has confirmed that monthly reports were consistently presented to CLT and Cabinet however improvements to the clarity and consistency of detail of the reports could be improved.

There has been consistency throughout the 2016/17 with regards to the reporting of budgetary issues and concerns to CLT and Cabinet, with specific emphasis placed on demand led budget areas.

Demand Led Budgets

This audit has identified and confirmed that significant scrutiny and reporti ng is completed on service area budgets where sensitivities within demand are high and which can have significant impacts on budgets. As such, budgetary pressures in respect of a number of demand sensitive services, including temporary accommodation and

home to school transport have been consistently reported to Cabinet throughout the 2016/17 financial year.

In addition, an exercise is currently being completed to model ‘Demand and Pressures’

for seven key budget areas which are particularly sensitive to changes in demand. The objective of this activity is analyse the current 2017/18 budget against current assumptions, to assess demands and pressures and to recommend possible actions if

budget if the current budget is considered unrealistic.

3.3 KEY AGREED MANAGEMENT ACTIONS

Ensure consistency in reporting of financial implications to Cabinet to ensure effective and informed decisions can be made.

Internal Audit & Risk delivering for

6

DETAILED FINDINGS 4 Control objective: Formal budget management policies and guidance exist

and are fit-for-purpose. 4.1 Formal guidance regarding the corporate requirements and responsibilities to ensure

effective budget management arrangements exist within MKC, are outlined within several documents, including: Financial Regulations – Forming part of the Constitution and dated January 2015, these

regulations clearly articulate the financial governance standards and the responsibilities placed on Directors’ and Officers’ for effective budget management;

Finance Operational Guidance – updated in May 2017 and available via the MKC Intranet, this document outlines the tools available to support effective budget management and forecasting arrangements e.g. SAP-BPC and Business Reports. This

document also includes a link to a budget management training pack;

Financial procedure Rules – Further forming part of the Constitution, providing

additional clarification regarding the budget management and monitoring requi rements within MKC;

Budget Manager Guidance – dated May 2017 in draft format, but further published

within the Finance pages on the Intranet. This document provides additional clarity regarding the MKC defined budget management cycle and links back to the requirements highlighted within the documents above.

4.2 In addition to the above, all Directors, Heads of Service, Budget Managers and Project

Managers are required to sign an annual Budget Accountability Letter. This letter

confirms individual responsibil ities in relation to financial management and governance for 2017/18, as set out in the documents above and in individual job descriptions. In light of the challenging financial position and the need for continuing and improving effective

financial and commercial management in 2017/18, MKC concluded it essential for individual managers to formally confirm they have understood these responsibilities and will act in accordance with these requirements.

4.3 Significant formal guidance therefore exists within MKC to promote effective budget

management arrangements which are further supported by the need for budget managers to sign individual Budget Accountability Letters.

Internal Audit & Risk delivering for

7

Governance System Substantial

Compliance Substantial

5 Control Objective: Effective budget management arrangements are in

place.

Training

5.1 The Finance Operational Guidance states that ‘all new budget managers are expected to

attend training on using the BPC system. Your Finance team will ensure that this is

arranged and that you are given access to your budget codes’. In addition, links to Budget management training which includes reporting process flows and the BPC monitoring process are contained within the Finance Operational Guidance.

5.2 It has however been confirmed that formal whole day training sessions entitled ‘ Finance

for Budget Managers’ ceased in June 2016. The reason for this being that there had been

a significant reduction in Budget Manager churn, and in view of the impendi ng implementation of the ERP Gold solution. It has however been confirmed that training is now delivered on a one-to-one basis.

5.3 The Finance Intranet page includes a link entitled Budget Managers Training Videos,

however this returns an error message indicating that the content has been removed. It has also been confirmed that no finance or budget management raining is included on the

MKC e-learning portal.

Reporting Timetable

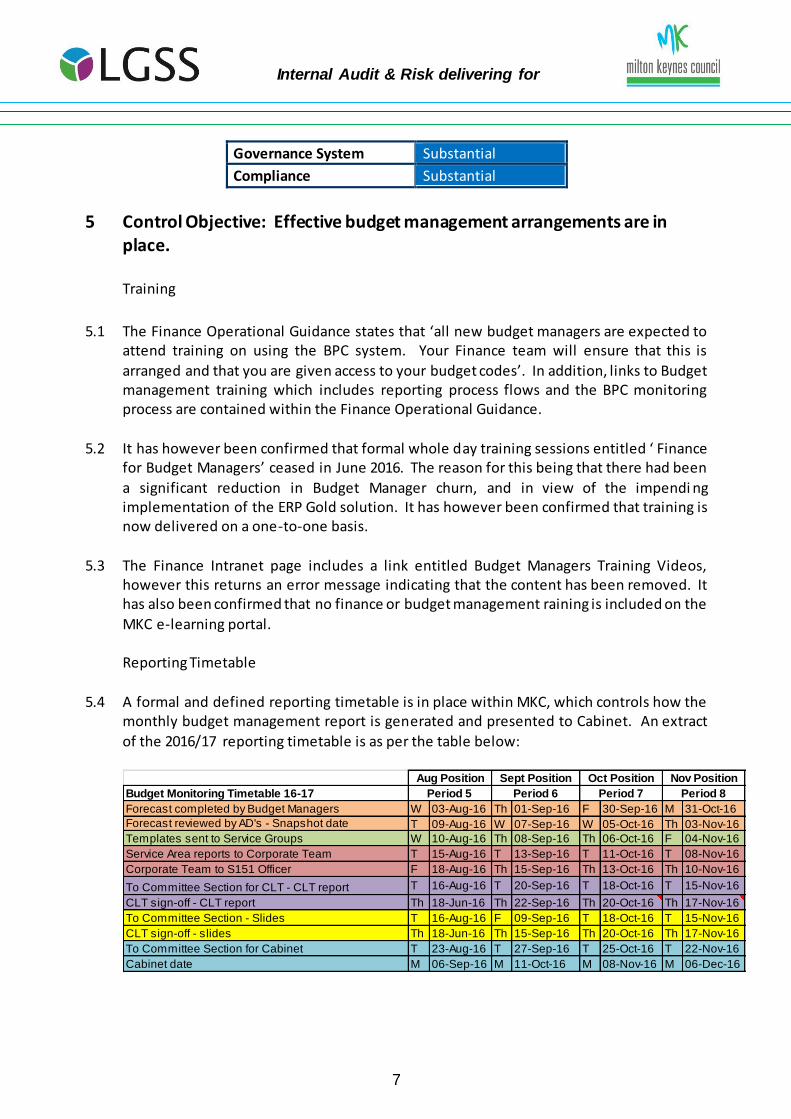

5.4 A formal and defined reporting timetable is in place within MKC, which controls how the

monthly budget management report is generated and presented to Cabinet. An extract

of the 2016/17 reporting timetable is as per the table below:

Budget Monitoring Timetable 16-17

Forecast completed by Budget Managers W 03-Aug-16 Th 01-Sep-16 F 30-Sep-16 M 31-Oct-16

Forecast reviewed by AD's - Snapshot date T 09-Aug-16 W 07-Sep-16 W 05-Oct-16 Th 03-Nov-16

Templates sent to Service Groups W 10-Aug-16 Th 08-Sep-16 Th 06-Oct-16 F 04-Nov-16

Service Area reports to Corporate Team T 15-Aug-16 T 13-Sep-16 T 11-Oct-16 T 08-Nov-16

Corporate Team to S151 Officer F 18-Aug-16 Th 15-Sep-16 Th 13-Oct-16 Th 10-Nov-16

To Committee Section for CLT - CLT report T 16-Aug-16 T 20-Sep-16 T 18-Oct-16 T 15-Nov-16

CLT sign-off - CLT report Th 18-Jun-16 Th 22-Sep-16 Th 20-Oct-16 Th 17-Nov-16

To Committee Section - Slides T 16-Aug-16 F 09-Sep-16 T 18-Oct-16 T 15-Nov-16

CLT sign-off - slides Th 18-Jun-16 Th 15-Sep-16 Th 20-Oct-16 Th 17-Nov-16

To Committee Section for Cabinet T 23-Aug-16 T 27-Sep-16 T 25-Oct-16 T 22-Nov-16

Cabinet date M 06-Sep-16 M 11-Oct-16 M 08-Nov-16 M 06-Dec-16

Period 7 Period 8

Nov Position

Period 5 Period 6

Aug Position Sept Position Oct Position

Internal Audit & Risk delivering for

8

5.5 As outlined within the table, a number of formal steps are taken which leads to the production of the monthly budget monitoring report to Cabinet. These steps include formal review of the consolidated forecast by the Section 151 Officer, prior to the production of the budget report which is presented to and reviewed by CLT and then by

Cabinet. This review has confirmed that throughout 2016/17, monthly budget management reports were presented to and reviewed by CLT and Cabinet.

Budget Areas of Concern Reported to Cabinet 5.6 This review has confirmed that regular revenue and capital budget management reports

were presented to Cabinet in accordance with the formal reporting timetable. The format and structure of the reports have generally been consistent, although it is recognised that minor changes to the report design were made to the March 2017 report.

The design of the report includes the fol lowing areas:

Executive Summary – providing a high-level forecast outturn position for the

General Fund, Housing Revenue Account (HRA), Dedicated Schools Grant (DSG) and Capital Programme;

Recommendations for decision by Cabinet; CLT View – highlighting the main areas of financial concern along with mitigations;

General fund revenue outturn; Significant movements and issues from the previous month; Significant overall revenue variances per directorate;

Progress against the delivery of budgets savings; DSG; and HRA including major underspends.

5.7 From the review of the budget management reports presented to Cabinet between

December 2016 and March 2017, the key areas of budgetary concern, consistently

reported related to the following areas:

Residual waste treatment facility; Temporary accommodation;

Home to school transport; Children’s social care; Car parking income;

Public health contracts; and Stantonbury Campus liability deficit.

5.8 With the exception of Car Parking Income, which was regularly reported as a risk to CLT but not reported to Cabinet as an issue in February 2017, the above issues have

Internal Audit & Risk delivering for

9

consistently been reported as the main budget areas of concern throughout the 2016/17 financial year.

5.9 It is noted that the financial issues highlighted towards the front of the report, appear to

be the priority issues and therefore the key issues of note for CLT’s attention. However, a review of the reports has identified occasions where a significant financial concern is

raised in one monthly report, but then is not highlighted in subsequent reports. This could suggest that the financial pressure has been successfully mitigated however this audit trail is not evident.

5.10 In addition, the clarity and consistency of reporting could be improved to ensure that the

financial consequences are accurately reflected for each area of concern, in order that

informed decisions can be made in respect of the recommendations made to Cabinet. It is recognised this is sometimes difficult to achieve whilst retaining the flexibili ty to properly represent the unique service issues.

5.11 It is further noted that revenue and capital budget management reports have been

presented to the Budget Scrutiny Committee during 2016/17.

Demand Led Budgets

5.12 In accordance with the defined reporting timetable, significant support is provided to

Budget Managers by the Finance team during the production of the monthly BPC forecasts. This support includes assisting with the production of the BPC, challenging forecasts, preparing reports for relevant Heads of Service and meeting with Heads of

Service prior to the production of the CLT / Cabinet reports.

5.13 In addition, in light of the complexities of demand led budgets and the impacts on budget

control, as exercise within Finance and service areas is currently being completed. The objective of this exercise is to undertake a detailed ‘Demand and Pressures’ review seven key budget areas, to analyse the current 2017/18 budget against current assumptions and

consider possible actions if the budget is considered unrealistic. The budget areas to be reviewed are:

Temporary accommodation;

Parking income; Home to school transport; Looked after children;

Adult social care; Contractual income; and Waste.

5.14 It is anticipated that this detailed exercise will be completed by the end of June 2017.

Internal Audit & Risk delivering for

10

Governance System Substantial

Compliance Substantial

Audit Committee Tracker Item AC31 – Budget Scrutiny Referral

5.15 Annex B attached to this report provides the Committee with a summary of the findings of the added value request in respect of the Budget Scrutiny referral in relation to the

2016/17 Waste Recycling budget savings. Specifically this related to the non-delivery of the £100k medium term budget saving in respect of the CRC contract.

5.16 In respect of the overall referral to the Chief Internal Auditor the initial analysis has

shown that the Waste proposal referred was supported by evidence that was sufficiently based on the best information available at the time. The specific concerns highlighted appear answered and further analysis is not considered necessary.

Internal Audit & Risk delivering for

11 6 June 2017

MANAGEMENT ACTION PLAN

The Agreed Actions are categorised on the following basis:

Essential - Action is imperative to ensure that the objectives for the area under review are met.

Important - Requires action to avoid exposure to significant risks in achieving objectives for the area under review.

Standard - Action recommended to enhance control or improve operational efficiency.

Ref. Issues & Risks

Agreed Action Management

Comments

Manager Responsible &

Target Date

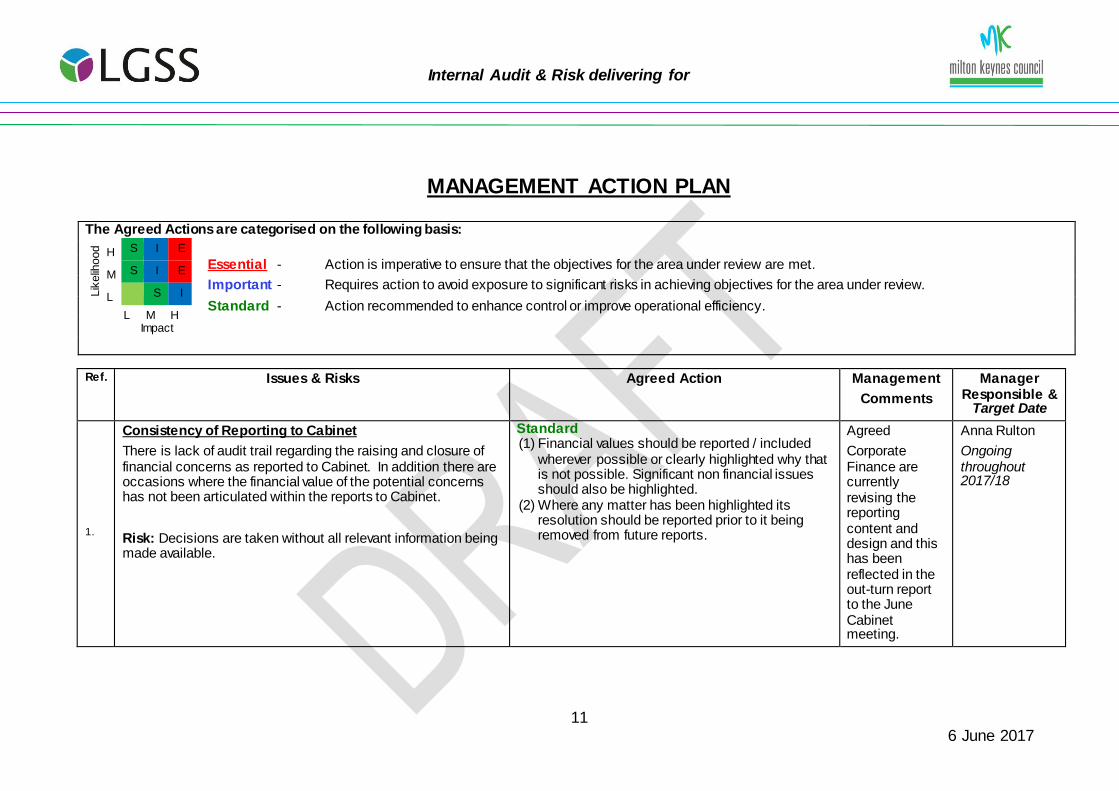

1.

Consistency of Reporting to Cabinet

There is lack of audit trail regarding the raising and closure of financial concerns as reported to Cabinet. In addition there are occasions where the financial value of the potential concerns has not been articulated within the reports to Cabinet.

Risk: Decisions are taken without all relevant information being made available.

Standard (1) Financial values should be reported / included

wherever possible or clearly highlighted why that is not possible. Significant non financial issues should also be highlighted.

(2) Where any matter has been highlighted its resolution should be reported prior to it being removed from future reports.

Agreed

Corporate Finance are currently revising the reporting content and design and this has been reflected in the out-turn report to the June Cabinet meeting.

Anna Rulton

Ongoing throughout 2017/18

Lik

elih

ood

H S I E

M S I E

L S I

L M H

Impact

Internal Audit & Risk delivering for

12

Appendix 1 – Glossary / Definitions There are three elements to consider when determining an assurance opinion as set out below. 1 Control Environment / System Assurance The adequacy of the control environment / system is perhaps the most important as this establishes the key controls and frequently systems ‘police/ enforce’ good control operated by individuals.

Assessed

Level Definitions

Substantial Substantial governance measures are in place that gives confidence the control

environment operates effectively.

Good Governance measures are in place with only minor control weaknesses that present low

risk to the control environment.

Satisfactory Systems operate to a moderate level with some control weaknesses that present a

medium risk to the control environment.

Limited There are significant control weaknesses that present a high risk to the control

environment.

No Assurance

There are fundamental control weaknesses that present an unacceptable level of risk to the control environment.

2 Compliance Assurance Strong systems of control should enforce compliance whilst ensuring ‘ease of use’. Strong systems can be abused / bypassed and therefore testing ascertains the extent to which the controls are being complied with in practice. Operational reality within testing accepts a level of variation from agreed controls where circumstances require.

Assessed Level

Definitions

Substantial Testing has proven that the control environment has operated as intended without

exception.

Good Testing has identified good compliance. Although some errors have been detected these

were exceptional and acceptable.

Satisfactory The control environment has mainly operated as intended although errors have been detected that should have been prevented / mitigated.

Limited The control environment has not operated as intended. Significant errors have been

detected and/or compliance levels unacceptable.

No Assurance

The control environment has fundamentally broken down and is open to significant error or abuse. The system of control is essentially absent.

Internal Audit & Risk delivering for

13

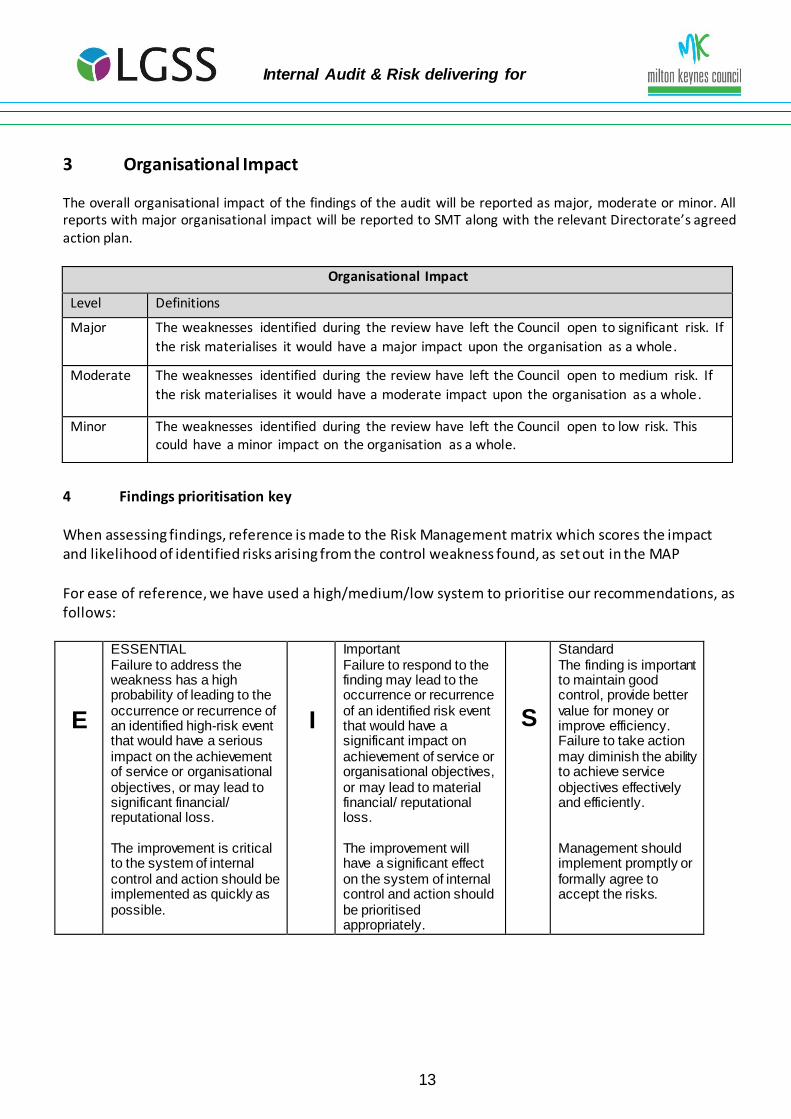

3 Organisational Impact

The overall organisational impact of the findings of the audit will be reported as major, moderate or minor. All reports with major organisational impact will be reported to SMT along with the relevant Directorate’s agreed action plan.

Organisational Impact

Level Definitions

Major

The weaknesses identified during the review have left the Council open to significant risk. If

the risk materialises it would have a major impact upon the organisation as a whole.

Moderate The weaknesses identified during the review have left the Council open to medium risk. If

the risk materialises it would have a moderate impact upon the organisation as a whole.

Minor The weaknesses identified during the review have left the Council open to low risk. This could have a minor impact on the organisation as a whole.

4 Findings prioritisation key When assessing findings, reference is made to the Risk Management matrix which scores the impact and likelihood of identified risks arising from the control weakness found, as set out in the MAP

For ease of reference, we have used a high/medium/low system to prioritise our recommendations, as follows:

E

ESSENTIAL Failure to address the weakness has a high probability of leading to the occurrence or recurrence of an identified high-risk event that would have a serious impact on the achievement of service or organisational objectives, or may lead to significant financial/ reputational loss. The improvement is critical to the system of internal control and action should be implemented as quickly as possible.

I

Important Failure to respond to the finding may lead to the occurrence or recurrence of an identified risk event that would have a significant impact on achievement of service or organisational objectives, or may lead to material financial/ reputational loss. The improvement will have a significant effect on the system of internal control and action should be prioritised appropriately.

S

Standard The finding is important to maintain good control, provide better value for money or improve efficiency. Failure to take action may diminish the ability to achieve service objectives effectively and efficiently. Management should implement promptly or formally agree to accept the risks.

Internal Audit & Risk delivering for

14

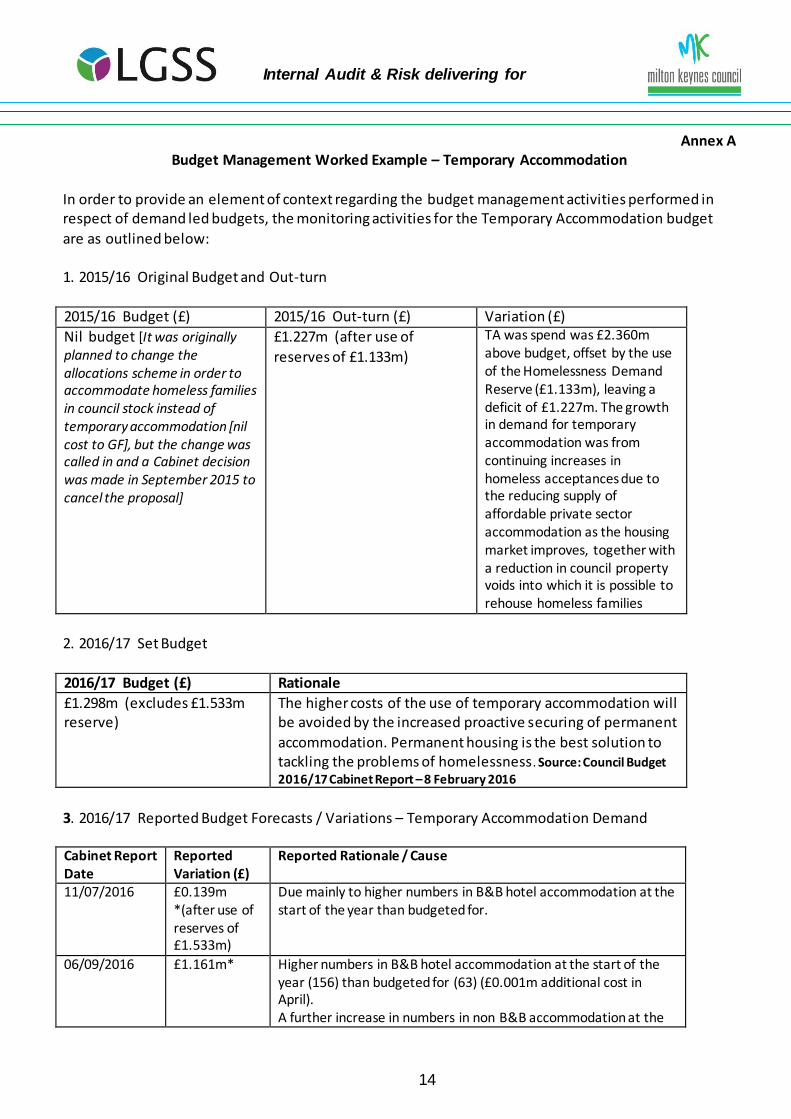

Annex A Budget Management Worked Example – Temporary Accommodation

In order to provide an element of context regarding the budget management activities performed in respect of demand led budgets, the monitoring activities for the Temporary Accommodation budget

are as outlined below: 1. 2015/16 Original Budget and Out-turn

2015/16 Budget (£) 2015/16 Out-turn (£) Variation (£)

Nil budget [It was originally planned to change the allocations scheme in order to accommodate homeless families in council stock instead of temporary accommodation [nil cost to GF], but the change was called in and a Cabinet decision was made in September 2015 to cancel the proposal]

£1.227m (after use of

reserves of £1.133m)

TA was spend was £2.360m above budget, offset by the use of the Homelessness Demand Reserve (£1.133m), leaving a deficit of £1.227m. The growth in demand for temporary accommodation was from continuing increases in homeless acceptances due to the reducing supply of affordable private sector accommodation as the housing market improves, together with a reduction in council property voids into which it is possible to rehouse homeless families

2. 2016/17 Set Budget

2016/17 Budget (£) Rationale

£1.298m (excludes £1.533m reserve)

The higher costs of the use of temporary accommodation will be avoided by the increased proactive securing of permanent

accommodation. Permanent housing is the best solution to tackling the problems of homelessness. Source: Council Budget 2016/17 Cabinet Report – 8 February 2016

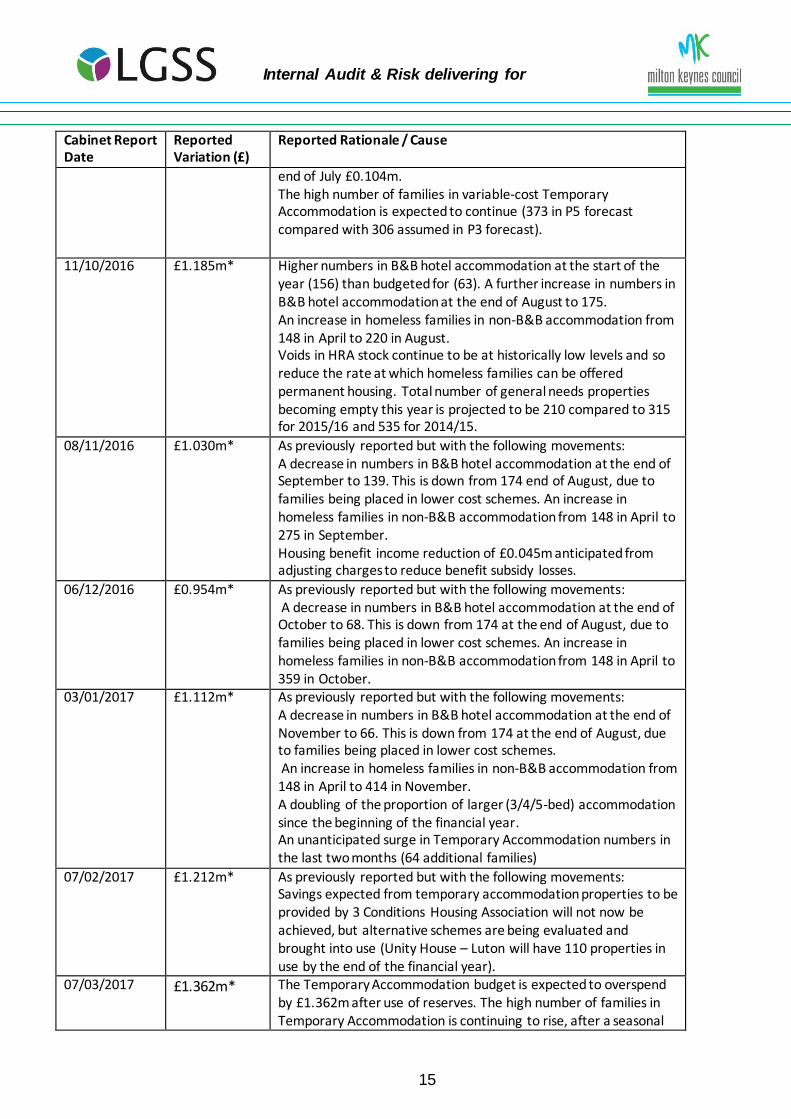

3. 2016/17 Reported Budget Forecasts / Variations – Temporary Accommodation Demand Cabinet Report Date

Reported Variation (£)

Reported Rationale / Cause

11/07/2016 £0.139m *(after use of reserves of £1.533m)

Due mainly to higher numbers in B&B hotel accommodation at the start of the year than budgeted for.

06/09/2016 £1.161m* Higher numbers in B&B hotel accommodation at the start of the year (156) than budgeted for (63) (£0.001m additional cost in April). A further increase in numbers in non B&B accommodation at the

Internal Audit & Risk delivering for

15

Cabinet Report Date

Reported Variation (£)

Reported Rationale / Cause

end of July £0.104m. The high number of families in variable-cost Temporary Accommodation is expected to continue (373 in P5 forecast compared with 306 assumed in P3 forecast).

11/10/2016 £1.185m* Higher numbers in B&B hotel accommodation at the start of the year (156) than budgeted for (63). A further increase in numbers in B&B hotel accommodation at the end of August to 175. An increase in homeless families in non-B&B accommodation from 148 in April to 220 in August. Voids in HRA stock continue to be at historically low levels and so reduce the rate at which homeless families can be offered permanent housing. Total number of general needs properties becoming empty this year is projected to be 210 compared to 315 for 2015/16 and 535 for 2014/15.

08/11/2016 £1.030m* As previously reported but with the following movements: A decrease in numbers in B&B hotel accommodation at the end of September to 139. This is down from 174 end of August, due to families being placed in lower cost schemes. An increase in homeless families in non-B&B accommodation from 148 in April to 275 in September. Housing benefit income reduction of £0.045m anticipated from adjusting charges to reduce benefit subsidy losses.

06/12/2016 £0.954m* As previously reported but with the following movements: A decrease in numbers in B&B hotel accommodation at the end of October to 68. This is down from 174 at the end of August, due to families being placed in lower cost schemes. An increase in homeless families in non-B&B accommodation from 148 in April to 359 in October.

03/01/2017 £1.112m* As previously reported but with the following movements: A decrease in numbers in B&B hotel accommodation at the end of November to 66. This is down from 174 at the end of August, due to families being placed in lower cost schemes. An increase in homeless families in non-B&B accommodation from 148 in April to 414 in November. A doubling of the proportion of larger (3/4/5-bed) accommodation since the beginning of the financial year. An unanticipated surge in Temporary Accommodation numbers in the last two months (64 additional families)

07/02/2017 £1.212m* As previously reported but with the following movements: Savings expected from temporary accommodation properties to be provided by 3 Conditions Housing Association will not now be achieved, but alternative schemes are being evaluated and brought into use (Unity House – Luton will have 110 properties in use by the end of the financial year).

07/03/2017 £1.362m* The Temporary Accommodation budget is expected to overspend by £1.362m after use of reserves. The high number of families in Temporary Accommodation is continuing to rise, after a seasonal

Internal Audit & Risk delivering for

16

Cabinet Report Date

Reported Variation (£)

Reported Rationale / Cause

hiatus in December, and is currently forecast to be a monthly average of 582 for March, an increase of 302 since April 2016 (for the variable cost accommodation types, i.e. excludes Ambassador House, Hostels and Women’s Refuges). The position continues to be closely monitored.

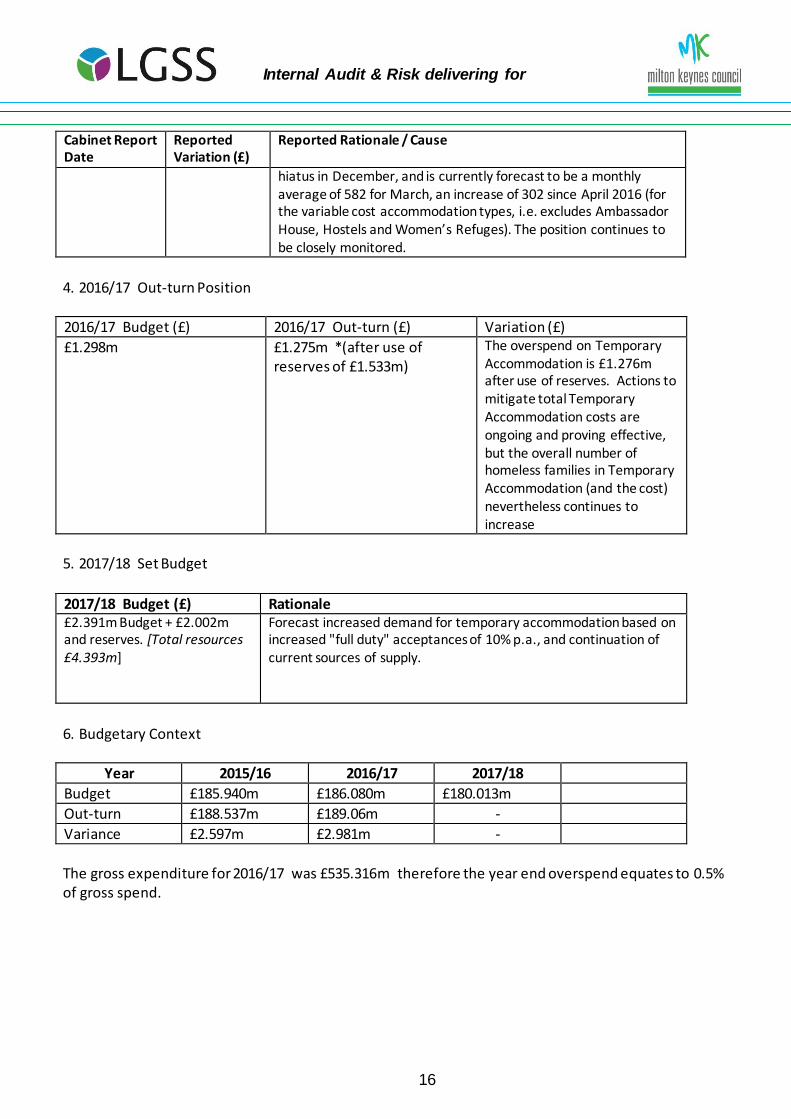

4. 2016/17 Out-turn Position

2016/17 Budget (£) 2016/17 Out-turn (£) Variation (£)

£1.298m £1.275m *(after use of reserves of £1.533m)

The overspend on Temporary Accommodation is £1.276m after use of reserves. Actions to mitigate total Temporary Accommodation costs are ongoing and proving effective, but the overall number of homeless families in Temporary Accommodation (and the cost) nevertheless continues to increase

5. 2017/18 Set Budget

2017/18 Budget (£) Rationale £2.391m Budget + £2.002m and reserves. [Total resources £4.393m]

Forecast increased demand for temporary accommodation based on increased "full duty" acceptances of 10% p.a., and continuation of current sources of supply.

6. Budgetary Context

Year 2015/16 2016/17 2017/18

Budget £185.940m £186.080m £180.013m

Out-turn £188.537m £189.06m -

Variance £2.597m £2.981m -

The gross expenditure for 2016/17 was £535.316m therefore the year end overspend equates to 0.5% of gross spend.

Internal Audit & Risk delivering for

17

Annex B Audit Committee – Decision Tracker Update

Item: AC31 – Budget Scrutiny Referral – Waste

Background Following the referral from the Budget Scrutiny Committee, the Chief Inte rnal Auditor was

requested to undertake an initial assessment of the concerns raised in respect of the unexpected fall in the sale of recyclable materials and its impact on the cost of the Community Recycling Centres, addressing why the figure included in the Council’s budget was so inaccurate. In particular:

a) Officer colleagues should have foreseen any large fluctuations in the market for

recyclable materials;

b) A fluctuation in the market for recyclable materials was the only reason for the savings

not being achieved;

c) Any budget factors were missed when preparing the Budget; and

d) There was an imposed budget saving which took no account of market conditions.

Approach

In order to obtain and understanding of the above concerns, the following actions have been undertaken:

Held discussions with Strategic Finance colleagues to obtain an understanding of the 16/17 budget setting / medium term budget savings process;

Obtained relevant background documentation to support the inclusion of the £100k medium term budget saving in respect of the CRC contract.

Held discussions with Waste Management colleagues to obtain an understanding of the methods for monitoring commodity pricing.

Key Findings

1. Within the final version of the Medium Term Budget Savings document, which was Annex

D to Item 10, presented to Cabinet on 8th February 2016, a one-off saving of £100k was

included in respect of “Savings arising from Community Recycling Centres contract re -let. (Saving reference S110).

2. The procurement process for the re-letting of the CRC contract commenced in 2014, on a competitive dialogue basis. In order to provide an element of context, a key high -level chronology relating to this procurement and the identification of the £100,000 medium term financial saving is as follows:

Internal Audit & Risk delivering for

18

Date Activity

1 July 2014 Report to Cabinet Procurement Committee seeking approval to commence the tender process to replace the

existing contract for the management and operation of the three Community Recycling Centres (CRC’s). Note: Financial comments within the report do not at this stage identify / quantify any financial savings likely to be

achieved through this procurement.

15 December 2014 Report to Cabinet Procurement Committee approving commencement to tender for the management and operation of the CRC’s. Procurement to be completed on a

competitive dialogue basis. Note: Financial comments within the report do not quantify a specific financial saving to be achieved from the

contract, there is however reference as to the expectation that the procurement would achieve greater value to the contract.

Jan – Dec 2015 Competitive dialogue with potential suppliers completed as per the approved procurement approach.

24 August 2015 Email from Head of Environment & Waste to Strategic

Finance identifying a number of budget saving proposals to be delivered from the Environmental and Waste Budgets. The potential CRC specific budget saving of £100k was

included on the basis of feedback received from one bidder during the competitive dialogue being completed. The assumption providing the basis for the saving was less

tonnage, a modelled reduction in opening hours and the introduction of a number of controls to reduce non-MKC resident waste, trade waste disguised as household waste.

This email also identified at this time that the recycling market had collapsed and the impacts of this had been included within the assumptions. Note: Finance have confirmed that the budget saving

proposal in respect of the CRC contract was not subject to additional scrutiny as the saving was indicative pending the outcome of the final tenders and based on an

estimated benefit, which had been supported by the Head of Service. .

14 December 2015 Draft 2016/17 Council Budget presented to Cabinet.

January 2016 Final Tenders received from 3 bidders for evaluation and modelling.

8 February 2016 Final Council Budget approved by Cabinet, including in Annex D the approved medium term budget savings. Saving

Ref S100 included in respect of the £100k CRC saving.

Internal Audit & Risk delivering for

19

Feb to May 2016 Bid evaluations completed resulting in a letter being sent to the three main bidders advising that none of the final tenders received were affordable. The letter advised that

the Council were therefore re-opening the procurement dialogue to explore ideas with bidders so that an affordable solution can be developed.

30 August 2016 Contract Procedure Rule Waiver approved to extend the existing the CRC contract to enable the current

procurement to be completed. It is anticipated that the award of contract will be

completed in April / May 2017 with mobilisation to be completed during July – September 2017.

Conclusion

In respect of the overall referral to the Chief Internal Auditor the initial analysis has shown that the Waste proposal referred was supported by evidence that was sufficiently based on the

best information available at the time. The specific concerns highlighted appear answered and further analysis is not considered necessary. In respect of the specific issues:

1. Officer colleagues should have foreseen any large fluctuations in the market for

recyclable materials;

2. A fluctuation in the market for recyclable materials was the only reason for the savings

not being achieved;

The £100k saving linked to the retendering of the CRC contract was identified in August 2015 as part of the budget setting process. At this time, the Waste service was aware

of the collapse of the recycling market and had reflected this within the proposal. The proposed saving was linked to the completion of the tendering process and through the introduction of a number of controls to reduce tonnage, non-MKC waste and trade waste abuse.

The proposed saving was further developed using modelling based on the competitive dialogue with one of the bidders, again in support of the controls proposed to be

introduced to reduce waste tonnage. It is therefore clear that the saving was / is to be delivered through the completion and

award of the CRC contract. As that procurement remains ongoing and will not be completed until September 2017, the 2016 budget saving cannot be delivered.

Due to the unaffordability of the final tenders received in January 2016, but not evaluated until after the Budget was set, the procurement was re-opened and dialogue

Internal Audit & Risk delivering for

20

on the final solution remains ongoing. Given the original timescales were within 2016 and derived from a procurement process it cannot be concluded that the market

fluctuations were the only reason for savings not being realised. Until this procurement is completed there remains the possibility / aspiration that the

budget saving could potentially be delivered, albeit late.

3. Any budget factors were missed when preparing the Budget;

The evidence shows that the savings were predicated on the procurement and as with any procurement until bids are opened, evaluated and accepted there are no guarantees. It is an accepted and prudent financial approach to estimate / apply a

savings target within a procurement process. In such cases it is important to clearly explain that dependency which evidence shows was reported within the budget process as part of the proposed budget savings report to Cabinet.

4. There was an imposed budget saving which took no account of market conditions.

The Council is under financial pressure and it must be a realistic understanding that budget savings are in some respects an external factor ‘imposed’ upon the Council and its services.

There is no indication that this was a budget saving imposed upon the service without any regard to service implications or deliverabil ity. Market factors were an element of

the proposal. Whilst some apportionment of targets will be a reality for Council services for some time MKC has a strong budget process that works with services to develop such choices

with clarity of the implications of those choices.

Potential Further Audit Work

1. The 2017 / 18 Internal Audit plan includes Budget Setting as a specific audit and

therefore the setting of budgets including demand led budgets will be subject to an

audit review.

2. It is proposed that during 2017/18 a detailed review of procurement activity within

MKC will be subject to audit, the scope of which is to be agreed however the efficiency and effectiveness of procurement strategies and approaches will be examined.

Internal Audit & Risk delivering for

21

Circulation Details:

Client

Issued to

CC

Date

Chief Internal Auditor

Lead Auditor

Status of report

Director of Resources

Corporate Director (Resources) Chief Executive Corporate Director Place

Corporate Director People Member with Finance Portfolio

External Audit ([email protected]

Link: http://www.milton-keynes.gov.uk/your-

council-and-elections/councillors-and-committees/cabinet-portfolios

07/06/2017

Duncan Wilkinson Steven Tinkler

Issued

Related Documents