Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

EY Ford Rhodes

BUDGET BRIEFING 2018

This Memorandum is correct to the best of our knowledge and belief at the time of going to the press. It is intended to provide only a general outline of the subjects covered. It should neither be regarded as comprehensive nor sufficient for making decisions, nor should it be used in place of professional advice. The Firm and Ernst & Young do not accept any responsibility for any loss arising from any action taken or not taken by anyone using this publication.

This Memorandum may be accessed on our website http://www.ey.com/pk

Budget Briefing

EY Ford Rhodes

This Memorandum has been prepared as a general guide for the benefit of our clients and is available to other interested

persons upon request. This should not be published in any manner without the Firm’s consent. This is not an exhaustive

treatise as it sets out interpretation of only the significant amendments proposed by the Finance Bill, 2018 (the Bill) in the

Income Tax Ordinance, 2001 (the Ordinance), the Sales Tax Act, 1990 (the ST Act), the Customs Act, 1969 (the Customs

Act) and the Federal Excise Act, 2005 (the FE Act) in a concise form sufficient enough to amplify the important aspects of the

changes proposed to be made. The Board means the Federal Board of Revenue, Government of Pakistan.

Changes of consequential, administrative, procedural or editorial in nature have either been excluded from these comments

or otherwise dealt with briefly.

The amendments proposed by the Bill after having been enacted as the Finance Act, 2018, shall, with or without

modification, become effective from the tax year 2018, unless otherwise indicated.

It is suggested that the text of the Bill and the relevant laws and notifications, where applicable, be referred to in considering

the interpretation of any provision. Since these are only general comments, no decision on any issue be taken without further

consideration and specific professional advice should be sought before any action is taken.

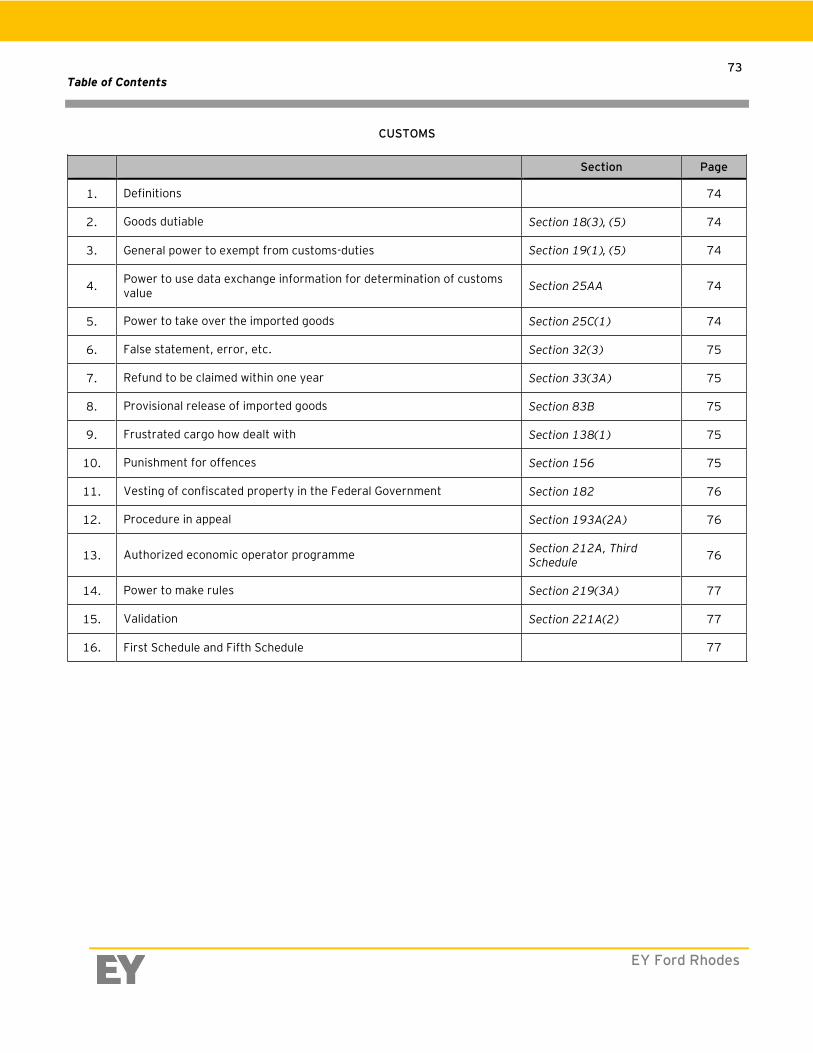

Contents Page

Highlights i – vii

Income Tax 1 – 50

Sales Tax 51 – 64

Islamabad Capital Territory 65

Federal Excise 66 – 72

Customs 73 - 79

KARACHI: 27 April 2018

Highlights

EY Ford Rhodes

i

Income Tax

The benefit available under non-recognition rules and valuations of assets received by way of a gift, is proposed to

be restricted to such gifts that are given to persons who are relatives.

Tax on issuance of bonus shares has been omitted.

Service of notice on an individual electronically, will also be treated as a valid mode of service of notice

Non-filers will not be allowed to purchase new and imported motor vehicles and immovable property.

Set-up of two new authorities i.e. the Directorate-General of Immovable Property and the Appellate Tribunal of

Immovable Property for regularizing and monitoring transactions of immovable property.

Super tax is proposed to be extended for a further period of three years up to the tax year 2020. However, the rate

of super tax would be reduced by 1% for each subsequent year up till 2020.

The eligible threshold of admissible investment in shares and premium on life insurance for claim of tax credit, is

proposed to be enhanced from Rs.1.5 million to Rs.2 million

Concealed foreign assets and foreign income can be taxed in the year of discovery, irrespective of the year of

acquisition under section 111 of the Ordinance

Explainable sources of foreign assets / expenditure may not be rejected by the Commissioner on the basis that the

source does not relate to the year of discovery of foreign assets / expenditure

Immunity from probe in respect of foreign currency remitted to Pakistan has been restricted to Rs.10 million in a tax

year

The tax collected by the Stock Exchange in Pakistan is being made adjustable against the final tax liability of the

members of the Stock Exchange or their customers, as the case may be.

The concept of ADRC has been re-vamped completely, in terms of constitution and its working.

Unabsorbed depreciation and amortization would be adjustable to the extent of 50% of business income and subject

to income thresholds.

Restrict of the time for passing an assessment order on a person who has been served with the notice to file a return

of income for the last ten years but fails to do so, within two years from the issuance date of such notice.

The Board withdraws demand for online access to banks’ central database with accompanying provisions.

The powers to amend the Second Schedule revert backed to the Federal Government

Mandatory requirement to distribute at least 40% dividend by listed companies to avoid tax on undistributed profits

is proposed to be reduced to 20%. The rate of tax on undistributed profits is also proposed to be reduced from 7.5%

to 5%.

The periods for availing tax credit under sections 65B, 65D and 65E are now proposed to be extended to 30 June

2021.

Highlights

EY Ford Rhodes

ii

Income derived by religious or charitable organizations from investment in deposits with microfinance banks also is

eligible for tax credit equal to the amount of tax on such income.

Requirement to file a foreign assets and income statement introduced for resident individuals subject to foreign

income thresholds.

The requirement of payment of 25% of the tax demand along with the appeal filed before the Commissioner

(Appeals) has been reduced to 10% of the tax demand.

Penalty for non-filing of statements under various provisions of the Ordinance is proposed to be rationalized.

The Appellate Tribunal cannot grant stay beyond the period of 180 days, notwithstanding that the appeal is pending

decision before it.

Civil suits are not maintainable in tax cases before the High Courts.

Tax paid at import stage deemed “minimum tax” for commercial importers.

Company being a member of an Association of Person is allowed to take credit of proportionate tax collected or

deducted on its behalf.

Appointment in special audit panels may include a foreign expert or specialist and an International Tax audit expert.

With certain exceptions, cases will now be selected for tax audits only once in 3 years.

Non filling a return of income within the due date will render the tax payer as a non-filer for the entire tax year and

limit the availability of brought forward losses.

Existing non-withholding tax limit on account of payment for goods and rendering of services has been enhanced

from existing Rs.25,000 and Rs.10,000 to Rs.75,000 and Rs.30,000 respectively.

Tax on sale of certain petroleum products will be collected at the prescribed rates and such tax will constitute final

tax.

The ambit of advance tax on purchase or transfer of immovable property has been broadened to include payments

made on installments.

The Bill proposes to provide additional powers to the Commissioner to examine the estimates of advance tax

submitted by the taxpayers and also seek supporting information regarding such estimates.

The concept of Controlled Foreign Company viz-a-viz its taxability in the hands of the resident person has been

introduced.

The concept of “dependent agents” has been proposed to be expanded to include agents who play the principal role

leading to the conclusion of contracts without material modification by the non-resident and who act exclusively or

almost exclusively on behalf of the non-resident.

Tax at the rate of 5% is proposed to be introduced on fee for offshore digital services paid by a resident person or

borne by a permanent establishment of a non-resident person.

Highlights

EY Ford Rhodes

iii

It is proposed that every banking company be required to collect adjustable advance tax at the rate of 1% (3% in case

of non-filers) from every credit card, debit card and prepaid card transaction completed with a person outside

Pakistan.

The Bill proposes that tax deducted on payments for services by a permanent establishment of a non-resident should

constitute a minimum tax.

The Bill seeks to expand the scope of Pakistan source business income derived by a non-resident person by including

import of goods, whether or not the title to the goods passes outside Pakistan, if the import is part of an overall

Engineering, Procurement, Construction and Commissioning (EPCC) arrangement irrespective of the fact that the

importer is the person, associate of the person or any other person.

The Bill seeks to introduce the concept of beneficial ownership by empowering the tax authorities to disregard an

entity or a corporate structure that does not have an economic or commercial substance or was created as part of

the tax avoidance scheme. Further, the Bill proposes that the benefits available under a Double Tax Treaty may also

be re-characterized by the tax authorities.

The Bill proposes to introduce a new section whereby disposal of assets outside Pakistan, by a non-resident, may

also be subject to tax in Pakistan if such assets derive their value from assets located in Pakistan.

The First Schedule

Part I

Income tax rates for individual (salaried and non-salaried) reduced and harmonized. Highest rate of tax being 15%.

The income tax rates for AOPs proposed to be rationalized by reducing the highest rate of tax to 30% from 35%.

The corporate tax rate is proposed to be reduced to 29% for tax year 2019 which will be reduced by 1% each year

upto the tax year 2023.

The rate of tax in respect of sale of securities remains unchanged.

Part III

Tax on dividend income derived by an individual from a Rental REIT Scheme is proposed to be reduced to 7.5%.

The withholding tax rates increased for non-filer corporate persons for supply of goods and execution of contracts.

Part IV

Advance tax on banking transactions otherwise than through cash reduced from 0.6% to 0.4%.

The Second Schedule

Part I

Certain charitable institutions have been included in the list of institutions whose income is exempt from tax.

Income from manufacturing activity of Modaraba no longer exempt from tax.

Highlights

EY Ford Rhodes

iv

Profits and gains derived by a refinery setup between 1st July 2018 and 30th June 2023 subject to fulfilment of

certain conditions.

Part III

New clauses are proposed to be inserted to provide reduction in the amount of tax payable by 50% on income

derived from film making by foreign film makers / resident companies.

Part IV

Public sector university whose income is exempt from tax under Clause (126) of part I of the Second Schedule to the

Ordinance is proposed to be exempted from the levy of minimum tax as well.

A new clause introduced to provide exemption from withholding tax on dividend paid to Transmission Line Project

under Transmission Line Policy 2015.

Clause (56B) deleted. The option to opt out FTR will no more be available to commercial importers

The Bill proposes to extend the levy of minimum tax under Section 113 of the Ordinance at the reduced rate of 0.5%

upto the tax year 2021.

It is proposed that no tax is to be collected on Imports of plant and machinery / construction material / armored and

security vehicle by certain motorway / CPEC projects on fulfillment of certain condition.

Inspection, certification, testing and training services are proposed to be inserted in the list of services specified in

the aforesaid clause. The period for application of Clause (94) is proposed to be extended to 30 June 2019.

The last date for furnishing an irrevocable undertaking for the tax year 2019 for the purpose of Clause (94) is

proposed to be extended to November 2018.

Section 7B of the Ordinance is proposed to be not applicable to profit on Bahbood Saving Certificates or Pensioner’s

Benefit Account subject to certain conditions.

Sales Tax

Rate of further tax is proposed to be increased from 2% to 3%.

The powers of the Federal Government to issue notifications under various sections of the Sales Tax Act, 1990 (the

ST Act) are sought to be restored which are presently vested with the Board.

Concept of appeal effect order has been proposed in the ST Act, whereby, the Commissioner or the Officer Inland

Revenue shall be required to issue the order within one year from the end of the financial year in which the appellate

order was served to the Commissioner or the Officer Inland Revenue.

Sales tax audit is proposed to be conducted only once in every three years.

Default surcharge is proposed to be fixed at 12% per annum. Presently it is KIBOR plus 3% per annum.

Highlights

EY Ford Rhodes

v

The concept of ADRC has been re-vamped completely, in terms of constitution and its working.

The requirement of payment of 25% of the tax demand along with the appeal filed before the Commissioner Inland

Revenue (Appeals) has been reduced to 10% of the tax demand.

The adjustment of input tax paid on import of scrap compressor is proposed to be restricted.

Exemption on import of parts by computer manufacturer certified by the Engineering Development Board is

proposed.

Exemption on import of plant and machinery is proposed to align with the provisions of the Special Economic Zone

Act, 2012.

Zero rating on stationery items is proposed to be restored.

Rate of further tax is proposed to be 1% on zero rated domestic supplies of finished goods covered under SRO 1125.

Adjustment of input tax on packing material is proposed to be allowed to five export oriented sectors covered under

SRO 1125.

Rate of sales tax is intended to be reduced from 7% to 12% on import of LNG by PSO and PLL and further supply of

RLNG to SNGPL by these companies.

Value addition tax of 3% on import of LNG is proposed to be waived off

Reduction in the rate of sales tax to 3% is proposed on all fertilizers.

Reduction in sales tax rate to 5% on supply of natural gas to fertilizer plants is proposed

Exemption of sales tax on import of LNG by fertilizer manufacturer for use as feedback stock.

Rate of sales tax on import and supply of finished articles of leather and textile sector is proposed to be increased to

9%, however, for branded outlets which are integrated with the online system of the Board is proposed at 6%.

Federal Excise Duty

The powers to issue notifications under various Sections of the FE Act reverted back to Federal Government

Appeal effect order proposed to be introduced within one year from the end of the financial year in which the order

is served

Default surcharge fixed at twelve percent per annum, present rate is KIBOR plus three percent per annum

The requirement of payment of 25% of the tax demand along with the appeal filed before the Commissioner

(Appeals) reduced to 10% of the tax demand

The concept of ADRC has been revamped completely in terms of constitution and its working

The powers of the Chief Commissioner and Commissioner to monitoring production, stock position, removal or sale

of goods and maintenance of records withdrawn

Highlights

EY Ford Rhodes

vi

Audit to be conducted once in every three years

The rate of FED on tobacco and cement increased

The following exemptions proposed:

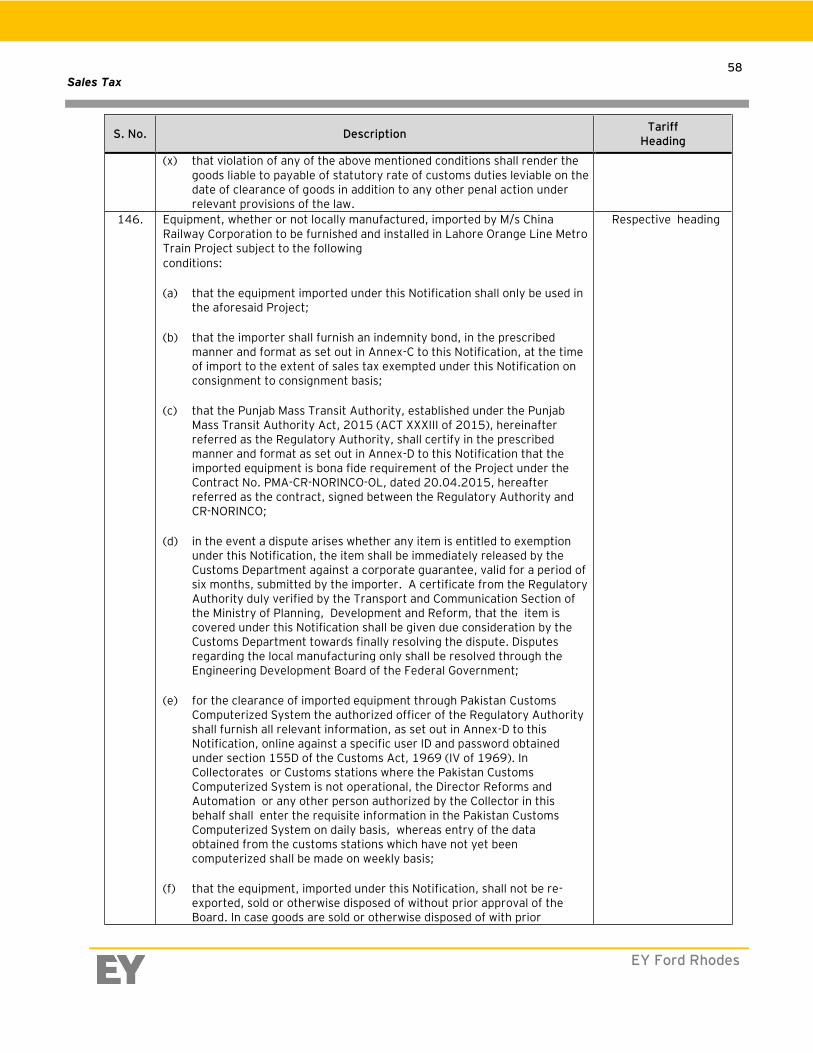

Equipment imported by M/s China Railway Corporation for Lahore Orange Line Metro Train Project

Construction materials and goods imported by China State Construction Engineering Corporation Limited for

Sukkur-Multan Motorway

Commission paid by the State Bank of Pakistan to National Bank or any other banking company, acting as

agents for handling banking services of federal and provincial governments

Customs

Additional customs duty is increased from 1% to 2% Customs duty is withdrawn on raw materials / inputs on 104 PCT headings and reduced on 28 PCT headings for

promotion of exports. Customs duty is reduced on aluminum foil for liquid food packaging industry, pre-fabricated structures for hotels,

input material for dairy sector, poultry sector, manufacturing of optical fibre cables, cinema industry, LED lights manufacturing, import of coal, and electric vehicles,

Fixed duty of US$ 5,000 is levied on import of vintage or classic cars/ jeeps. Duty is increased on import of rickshaw tyres, soya bean oil, aluminum auto parts scrap etc. New PCT codes introduced for radial tyres, CKD/SKD kits for home appliances, mobile phones, etc. Regulatory duty on non-essential and luxury items is to be reviewed. Collector (Appeals) is authorized to grant stay against recovery of duty/taxes for a maximum period of 30 days. Customs enforcement activities in the sea is extended up to 24 nautical miles.

Power of the Federal Government for any amendment in the customs law is restored. Currently, it is with the Board

after obtaining approval of the Federal Minister-in-charge. Legal coverage is provided for utilizing any data obtained under mutual assistance agreements for the purpose of

assessment and valuation. The power to take over imported goods is devolved from the Board to the Chief Collector. No proceedings can be initiated where the short paid duties, taxes or other charges is voluntarily paid.

Refund claim is to be decided within 180 days, subject to extension of further 90 days. Provisional release of confiscated imported goods will be possible on payment of duties and furnishing of bank

guarantee or pay order against monetary penalties involved thereof.

Highlights

EY Ford Rhodes

vii

Penalties introduced in case of non-compliance of electronic notices issued for requisition of documents Enhancement of penalties for pilferage, replacement enroute or in case transshipped goods failed to reach the port

of destination. Officer or person authorized by the Collector or Director can take and hold possession of confiscated goods. Authorized Economic Operator (AEO) program is introduced to meet the obligations of the Trade Facilitation

Agreement. Opportunity is to be provided to the public for offering comments before introducing any rules.

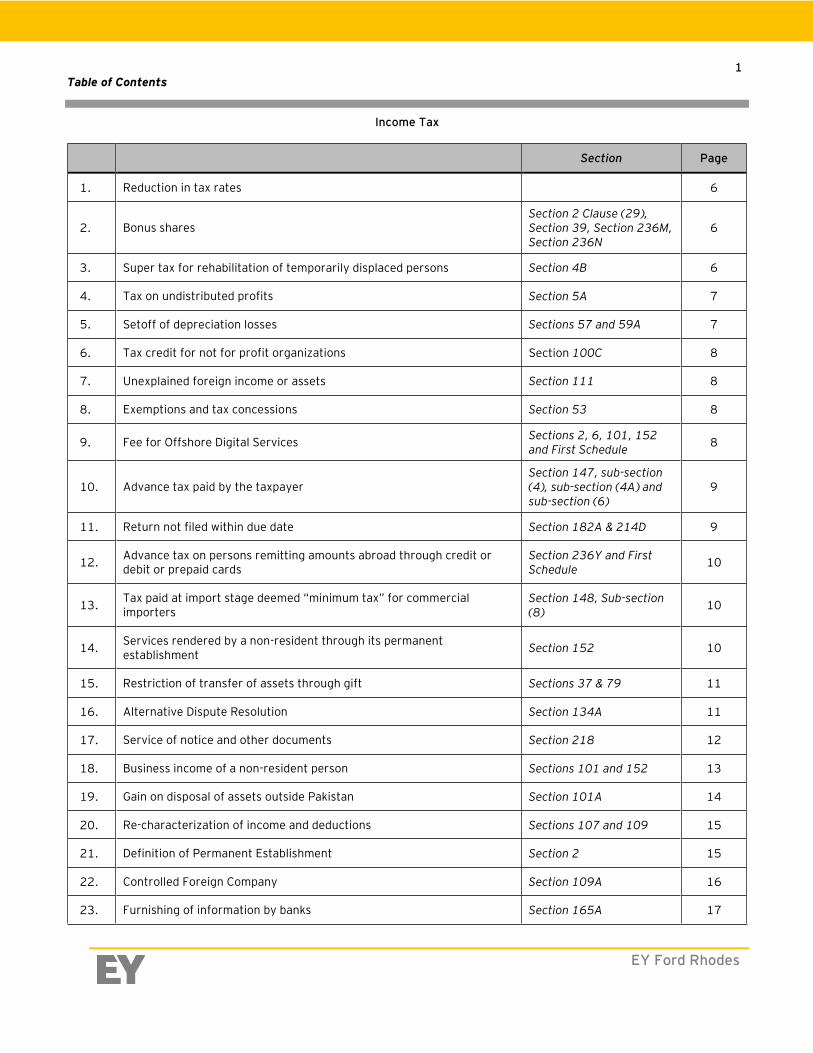

Table of Contents

EY Ford Rhodes

1

Income Tax

Section Page

1. Reduction in tax rates 6

2. Bonus shares Section 2 Clause (29), Section 39, Section 236M, Section 236N

6

3. Super tax for rehabilitation of temporarily displaced persons Section 4B 6

4. Tax on undistributed profits Section 5A 7

5. Setoff of depreciation losses Sections 57 and 59A 7

6. Tax credit for not for profit organizations Section 100C 8

7. Unexplained foreign income or assets Section 111 8

8. Exemptions and tax concessions Section 53 8

9. Fee for Offshore Digital Services Sections 2, 6, 101, 152 and First Schedule

8

10. Advance tax paid by the taxpayer Section 147, sub-section (4), sub-section (4A) and sub-section (6)

9

11. Return not filed within due date Section 182A & 214D 9

12. Advance tax on persons remitting amounts abroad through credit or debit or prepaid cards

Section 236Y and First Schedule

10

13. Tax paid at import stage deemed “minimum tax” for commercial importers

Section 148, Sub-section (8)

10

14. Services rendered by a non-resident through its permanent establishment

Section 152 10

15. Restriction of transfer of assets through gift Sections 37 & 79 11

16. Alternative Dispute Resolution Section 134A 11

17. Service of notice and other documents Section 218 12

18. Business income of a non-resident person Sections 101 and 152 13

19. Gain on disposal of assets outside Pakistan Section 101A 14

20. Re-characterization of income and deductions Sections 107 and 109 15

21. Definition of Permanent Establishment Section 2 15

22. Controlled Foreign Company Section 109A 16

23. Furnishing of information by banks Section 165A 17

Table of Contents

EY Ford Rhodes

2

Section Page

24. Restriction on purchase of certain assets Section 227C 18

25. Best judgment assessment Section 121 18

26. Tax credit for investment Section 65B 18

27. Tax credit for newly established industrial undertakings Section 65D 18

28. Tax credit for industrial undertakings established before the first day of July 2011

Section 65E 19

29. Foreign income and asset statements Section 116A 19

30. Return of income Sections 114 and 118 20

31. Recovery of tax Section 140 20

32. Penalties Section 182 20

33. Disclosure of information by public servant Section 216 20

34. Appeal to the Appellate Tribunal – stay of tax demand Section 131(5) 21

35. Bar of suits in Civil Courts Section 227 21

36. Transactions between associates Section 108 21

37. Claim of credit by a company being a member of an Association of Person

Section 168, Sub-section (2)

22

38. Appointment in special audit panel Section 177, Sub-section (11), Clause (d)

22

39. Selection of cases for audit Clause 105 Part IV of Second Schedule

23

40. Threshold limits for non-deduction of tax from payments of goods and services

Section 153 23

41. Tax on sale of certain petroleum products Section 236HA and Division XVA of Part IV of the First Schedule

23

42. Validation Section 241, Sub-section (2)

24

43. Advance tax on purchase or transfer of immovable property

Section 236K, sub-section (3) and Division XVIII of Part IV of the First Schedule

24

44. Directorate General of Immovable Property Section 230F 24

45. Tax credit for investment in shares and life insurance premium paid Section 62 25

46. Collection of tax by a Stock Exchange registered in Pakistan Section 233A 26

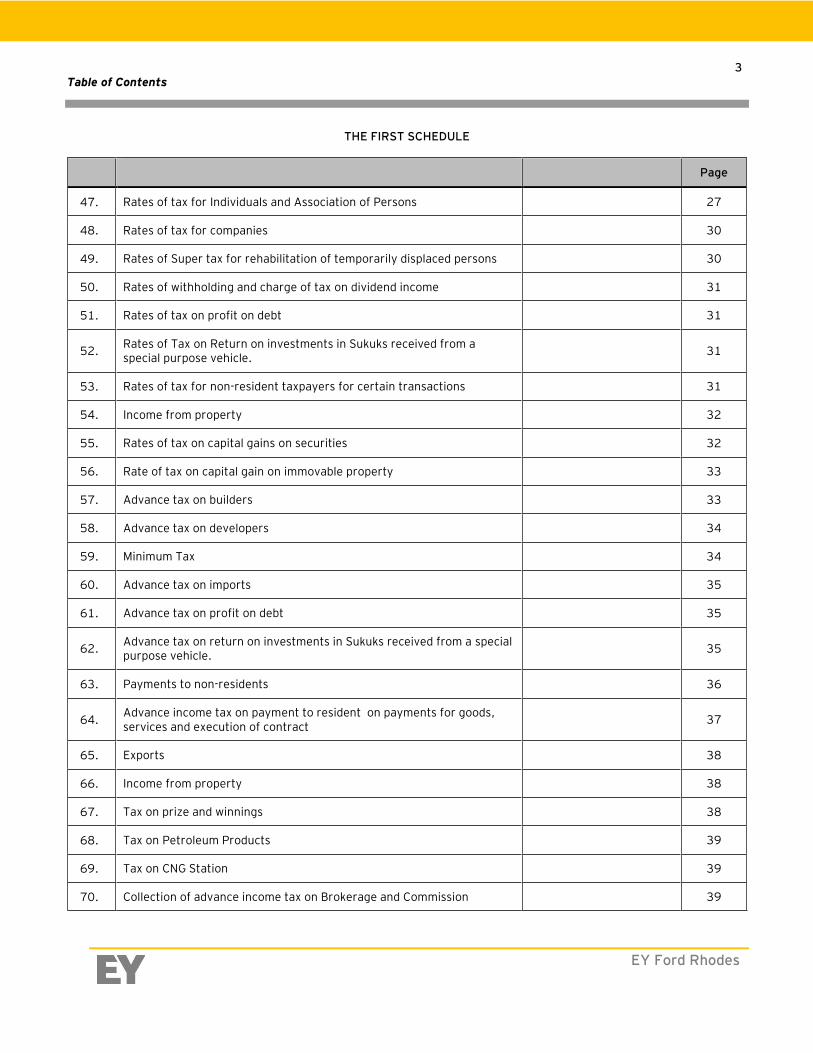

Table of Contents

EY Ford Rhodes

3

THE FIRST SCHEDULE

Page

47. Rates of tax for Individuals and Association of Persons 27

48. Rates of tax for companies 30

49. Rates of Super tax for rehabilitation of temporarily displaced persons 30

50. Rates of withholding and charge of tax on dividend income 31

51. Rates of tax on profit on debt 31

52. Rates of Tax on Return on investments in Sukuks received from a special purpose vehicle.

31

53. Rates of tax for non-resident taxpayers for certain transactions 31

54. Income from property 32

55. Rates of tax on capital gains on securities 32

56. Rate of tax on capital gain on immovable property 33

57. Advance tax on builders 33

58. Advance tax on developers 34

59. Minimum Tax 34

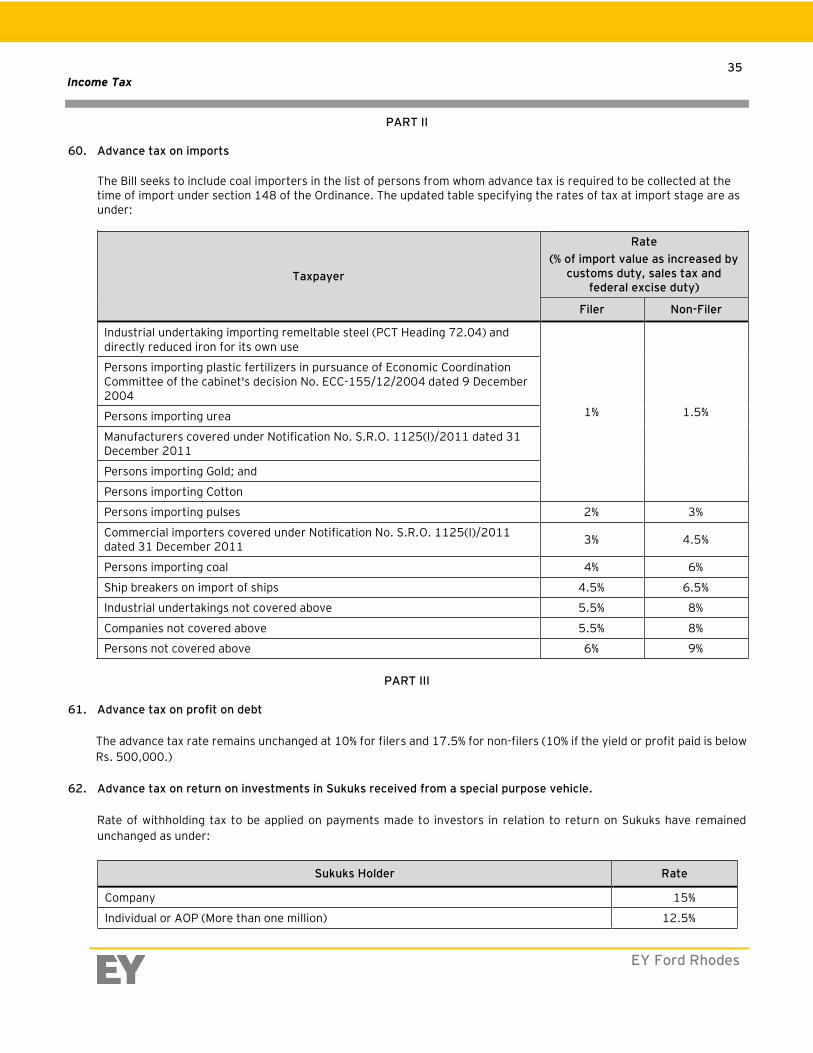

60. Advance tax on imports 35

61. Advance tax on profit on debt 35

62. Advance tax on return on investments in Sukuks received from a special purpose vehicle.

35

63. Payments to non-residents 36

64. Advance income tax on payment to resident on payments for goods, services and execution of contract

37

65. Exports 38

66. Income from property 38

67. Tax on prize and winnings 38

68. Tax on Petroleum Products 39

69. Tax on CNG Station 39

70. Collection of advance income tax on Brokerage and Commission 39

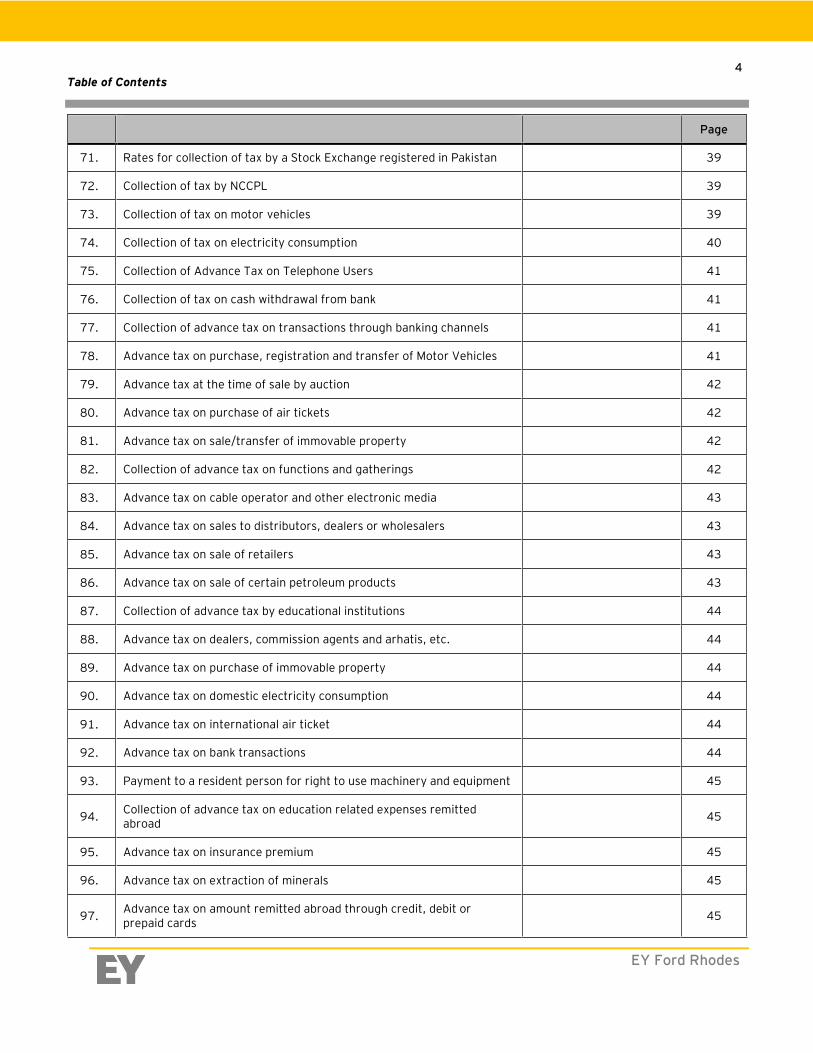

Table of Contents

EY Ford Rhodes

4

Page

71. Rates for collection of tax by a Stock Exchange registered in Pakistan 39

72. Collection of tax by NCCPL 39

73. Collection of tax on motor vehicles 39

74. Collection of tax on electricity consumption 40

75. Collection of Advance Tax on Telephone Users 41

76. Collection of tax on cash withdrawal from bank 41

77. Collection of advance tax on transactions through banking channels 41

78. Advance tax on purchase, registration and transfer of Motor Vehicles 41

79. Advance tax at the time of sale by auction 42

80. Advance tax on purchase of air tickets 42

81. Advance tax on sale/transfer of immovable property 42

82. Collection of advance tax on functions and gatherings 42

83. Advance tax on cable operator and other electronic media 43

84. Advance tax on sales to distributors, dealers or wholesalers 43

85. Advance tax on sale of retailers 43

86. Advance tax on sale of certain petroleum products 43

87. Collection of advance tax by educational institutions 44

88. Advance tax on dealers, commission agents and arhatis, etc. 44

89. Advance tax on purchase of immovable property 44

90. Advance tax on domestic electricity consumption 44

91. Advance tax on international air ticket 44

92. Advance tax on bank transactions 44

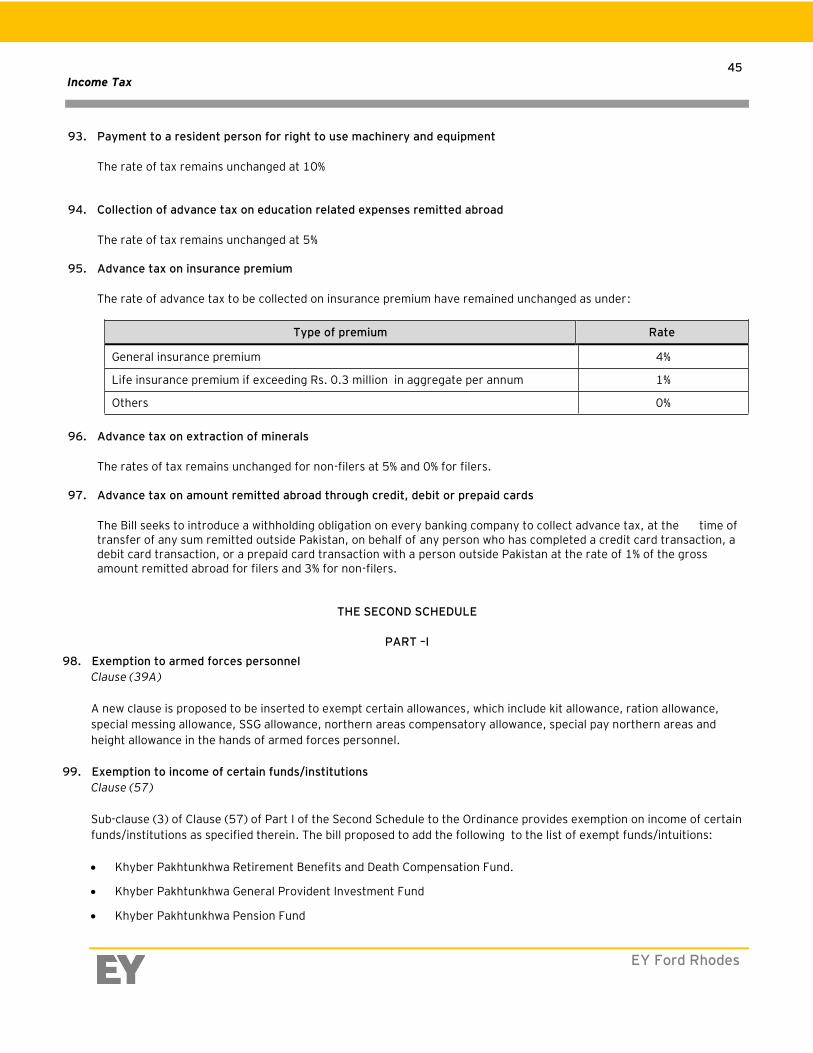

93. Payment to a resident person for right to use machinery and equipment 45

94. Collection of advance tax on education related expenses remitted abroad

45

95. Advance tax on insurance premium 45

96. Advance tax on extraction of minerals 45

97. Advance tax on amount remitted abroad through credit, debit or prepaid cards

45

Table of Contents

EY Ford Rhodes

5

THE SECOND SCHEDULE

Clause Page

98. Exemption to armed forces personnel 45

99. Exemption to income of certain funds/institutions 45

100. Exemption on donations 46

101. Exemption to income of certain charitable and other institutions Clause (66) 46

102. Exemption on profit on debt and gain on transfer of capital asset Clauses (90A & 110C) 47

103. Income of Modaraba (Clause 100) 47

104. Profit and gains derived from refinery operations Clause (126BA) 47

105. Reduce rate of tax on commercial contract Clause (24AA) 47

106. Incentive for film makers Clauses (7 & 8) 47

107. Exemption from provisions of Section 153 Clause (11E) 48

108. Exemption from provisions of Section 150 Clause (12A) 48

109. Exemption from provisions of Section 148 regarding withholding tax on imports

Clause (56) 48

110. Option to commercial importer Clause (56B) 48

111. Trading Houses Clause (57) 48

112. Exemption from collection of advance tax at import stage Clauses (60A), (60AA),

(60B) & (60C) 48

113. Institution deemed to be approved as NPO Clauses (63) 49

114. Minimum tax on services sector companies Clause (94) 49

115. Tax on profit on debt Clause (103) 49

116. Redundant Clauses of Second Schedule to the Ordinance 50

Income Tax

EY Ford Rhodes

6

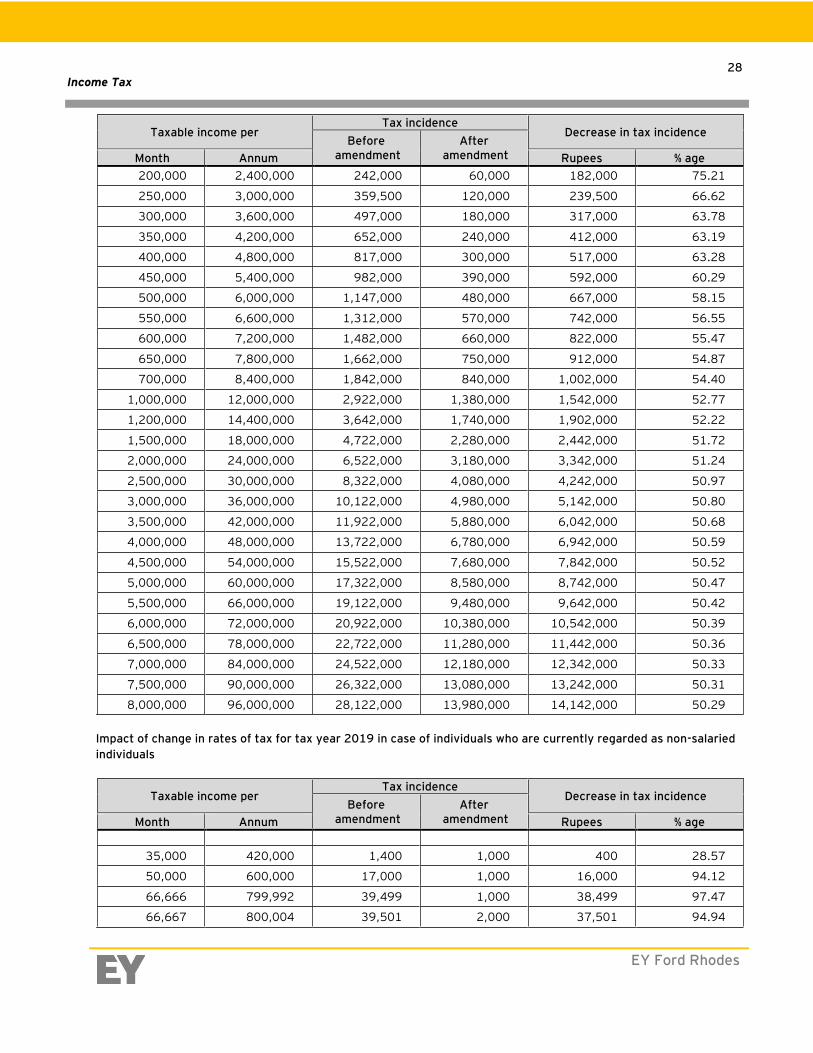

1. Reduction in tax rates

The Federal Government while announcing ‘Economic Reforms Package’, has provided substantial relief to salaried and

non-salaried individuals, whereby tax rates for individuals have been reduced with maximum applicable tax rate of 15%

on income in excess of Rs 4.8 million.

As per the Income Tax Amendment Ordinance, 2018, no tax was required to be paid by individuals deriving annual

income upto Rs.1,200,000. The Bill has however proposed that individuals deriving income from Rs.400,000 to

Rs.1,200,000 would be subject to tax of Rs.1000, and Rs.2,000 for income slabs ranging from Rs.400,000 to

Rs.800,000 and from Rs.800,000 to Rs.1,200,000 respectively

Similarly, the Bill also seeks to provide relief in tax rates for AOPs, which have also been reduced from the maximum

rate of 35% to 30%.

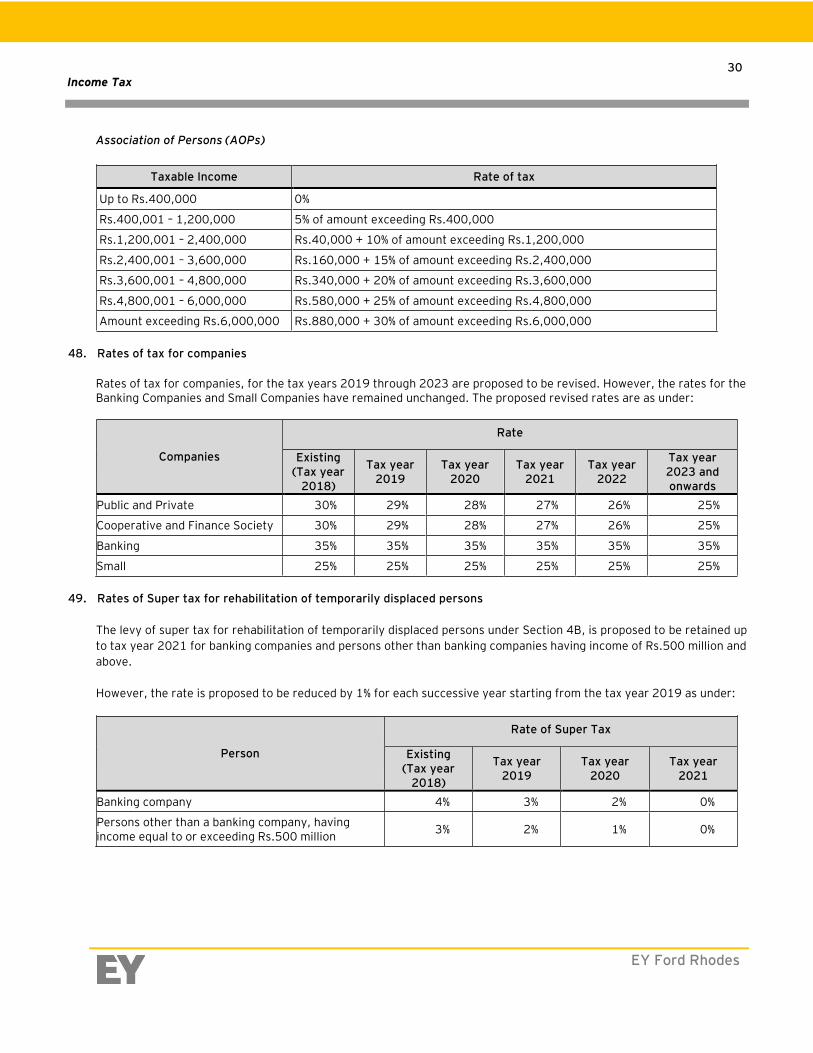

For companies, the tax rates have also been proposed to be reduced by 1% on yearly basis from present rate of 30% in

the tax year 2018 to the tax year 2023 in which the tax rate is proposed to be reduced to 25%.

2. Bonus shares

Section 2 Clause (29), Section 39, Section 236M, Section 236N

Under the scheme of taxation that has prevailed in Pakistan historically, the face value of bonus shares or the amount

of any bonus declared, issued or paid by a company to its shareholders (bonus shares) was excluded from the definition

of “income”. Non-taxability of bonus shares at the time of their issuance was based on the simple principle that the

shareholder does not derive any real income from the receipt of bonus shares and consequently income, if any, was

taxed as capital gain at the time when the bonus shares were actually disposed-off by the shareholders.

However, through Finance Act, 2014, bonus shares were declared as income of the recipient and corresponding

amendments were made in the Ordinance to tax receipt of bonus shares in the hands of the recipients. These tax

amendments were widely disliked. In reality, this measure did not generate tax as per the original estimates of the

Board, and at the same time the practice of issuance of bonus shares also declined substantially, hampering capital

accumulation, which is essential for expansion in the corporate sector.

After considerable persuasion by the capital market, business and professional forums, the Board has acceded to the

demands and it is now proposed that the taxation of bonus shares may be abolished. Consequently, several

amendments are proposed to withdraw the withholding of tax on issuance of bonus shares, treating the income from

bonus shares as other income, etc.

This is a much needed corrective measure, which will considerably promote capital formation and consolidation in the

corporate sector, simultaneously providing an impetus to the capital market.

3. Super tax for rehabilitation of temporarily displaced persons

Section 4B

The Finance Act, 2015, introduced a one-time super tax on all persons on all types of income, whether taxable under

the normal law or under the Final Tax Regime, in the tax year 2015. It was levied at 4% on banking companies and at 3%

on all other persons having taxable income of Rs.500 million or more. This levy was extended to the tax year 2017 by

the Finance Act, 2017. The Bill proposed to extend the application of Section 4B up to the tax year 2020. The Bill

further seeks to reduce the rate of super tax by one percent for each subsequent tax year, until tax year 2020.

The extension of super tax is not a surprise as the business quarters were anticipating it. However, most of the trade

and professional bodies had proposed to the government not to extend this levy any further. It seems that the constant

Income Tax

EY Ford Rhodes

7

increase in the tax collection targets by the Federal Government, coupled with the failure of the BOARD in broadening

the tax base, has left the Federal Government with little choice but to continue taking ad hoc measures like super tax, to

boost tax collection.

4. Tax on undistributed profits

Section 5A

The Finance Act, 2015, introduced taxation of undistributed reserves at the rate of 10%. Under this section tax was

imposed on a public company that derived profit for a tax year but did not distribute cash dividend equal to 40% of its

after tax profit or 50% of its paid-up capital, whichever is less, within six months of the end of the tax year, or which has

distributed a dividend to such an extent that its reserves remained in excess of 100% of its paid-up capital.

The Finance Act, 2017, revamped the taxation under the above section by changing undistributed reserves to

undistributed profits, and tax at 7.5% was imposed in case of non-distribution of 40% of after tax profits in the form of

cash dividend or bonus shares.

The Bill now seeks to reduce the tax rate from 7.5% to 5% in case the criterion as specified above is not met.

Furthermore, it is proposed that the condition of distribution of 40% of after tax profits may be reduced to 20%. The

distribution in this respect is to be made in cash as the option of bonus shares has been omitted, apparently due to the

withdrawal of taxation on bonus shares.

The Bill also seeks to omit the reference of this section from the provisions of section 8 of the Ordinance, which

contains general provisions regarding income falling under the final tax regime.

5. Setoff of depreciation losses

Sections 57 and 59A

The concept of adjustment of unabsorbed depreciation brought forward from previous years against income of the

current year, is an age-old concept. It was initially adopted in the Income Tax Act, 1922. It was then carried further

when the Income Tax Ordinance, 1979, was promulgated, repealing the Income Tax Act, 1922. When the Ordinance

was promulgated in the year 2003, this concept was pocketed by virtue of the provisions of sections 57 and 59A of the

Ordinance with minor amendments including taking the effect of amortization of intangibles and pre-commencement

expenditure. The concept dictates that in computing income from business, deduction on account of depreciation of

assets used in business (and amortization as above), if not completely absorbed by the profits and gains of business, the

unabsorbed depreciation and amortization is clubbed with the expense for the next year and so on until it is completely

utilized. In subsequent years, it becomes part of the depreciation and amortization deduction and after its adjustment, if

there is a loss computed, the same can be set off against income from any other head excluding gains from speculation

business. We have seen in a number of cases where unabsorbed depreciation and amortization are set off against

income from property (when Section 15 allowed such set off) and income falling under Section 39 of the Ordinance, i.e.

income from other sources.

The concept has also been tested in appeals a number of times and there is a plethora of case laws explaining the

application of the relevant provisions. Some of the cases that dealt with this issue are (i) Hon’ble High Court of Sindh

judgement in the case of Commissioner of Income Tax Vs. Karachi Electric Supply Corporation Ltd. (1985) 52 Tax 98,

(ii) judgment of the Supreme Court of India in the case of United Commercial Bank Ltd. Vs. CIT (1957) 32 ITR 688 and

(iii) judgment of full Bench of Bombay High Court in the case of B.M. Kamdar (1946) 14 ITR 10.

The Bill now intends to disturb this age-old concept by proposing amendments aiming to dislodge the allowability of such

adjustment. It is proposed that the adjustment of unabsorbed depreciation and amortization would be available against

income from business only and that too, to the extent of fifty percent of taxable income (after offsetting business

losses, if any) in a tax year. Where, however, the income from business in a tax year is less then Rs.10 million, the

unabsorbed depreciation and amortization would be set off without any limit i.e. to the extent of such income.

Income Tax

EY Ford Rhodes

8

The aim of the amendment per se seems nothing but to generate more tax collection by deferring the offset of losses,

which otherwise are available infinitely. However, the bigger loss is the inability to offset income from sources other

than business, against depreciation. As a result, despite losses the taxpayer will be forced to pay tax on such other

sources of income.

6. Tax credit for not for profit organizations

Section 100C

This section allows a tax credit equal to one hundred percent of the tax payable, including minimum tax and final taxes

to non-profit organizations, trusts and welfare institutions.

Currently tax credit is available on profit on debt derived from scheduled banks only. The Bill now proposes that the

same credit shall be extended to profit on debt derived from microfinance banks.

7. Unexplained foreign income or assets

Section 111

The Prime Minister announced an Economic Reforms package on 05 April 2018, which provided wide ranging measures

to solicit declaration of undeclared foreign as well as local assets and income. To compel persons to avail the tax

amnesty scheme, certain amendments were felt necessary in the Ordinance with respect to certain loop holes, which

were facilitating persons to remain out of the tax net without declaring their income and assets. For this purpose an

Ordinance, namely the Income Tax (Amendment) Ordinance, 2018, was promulgated, which inter-alia, introduced

amendments in section 111 of the Ordinance. These have now been made part of the Bill and are discussed in the

ensuing paragraphs.

8. Exemptions and tax concessions

Section 53

Before the Finance Act, 2017, the Federal Government was empowered to amend the Second Schedule in order to

provide or withdraw exemptions and tax concessions, or to provide conditions in respect thereof. Subsequently, through

the Finance Act, 2017, the Minister In-charge, pursuant to the approval of the Economic Coordination Committee of the

Cabinet, was empowered to make such amendments. However, the powers of the Minister on their own have been

challenged and there are decisions of the superior courts, which require the Federal Government to make such changes

in the law. The Bill now seeks to revert to the position prior to Finance Act, 2017 and surrender the powers back to the

Federal Government for making all such amendments in the Second Schedule.

9. Fee for Offshore Digital Services

Sections 2, 6, 101, 152 and First Schedule

With the advent of digitalization of businesses and e-commerce, taxpayers may derive income even from jurisdictions

where they are not physically present. This has led the tax authorities to question the right of a State to tax the

revenues derived by such taxpayers and the manner in which such tax may be collected. The existing provisions of the

Ordinance are also not equipped to deal with the rigors of e-commerce.

To address the above, the Bill proposes to introduce a concept of tax on fee for offshore digital services paid by a

resident person, or borne by a permanent establishment of a non-resident person. The term fee for offshore digital

services has been defined to mean any consideration for providing or rendering services by a non-resident person for

online advertising space, designing, creating, hosting or maintenance of websites, digital or cyber space for websites,

advertising, e-mails, online computing, blogs, online content and online data, providing any facility or service for

uploading, storing or distribution of digital content including digital text, digital audio or digital video, online collection

Income Tax

EY Ford Rhodes

9

or processing of data related to users in Pakistan, any facility for online sale of goods or services or any other online

facility. The tax rate on fee for off shore digital services is proposed to be 5% of the gross amount of such services.

The definition is quite extensive in nature and attempts to capture all e-commerce transactions that were previously not

covered by the Ordinance.

10. Advance tax paid by the taxpayer

Section 147, sub-section (4), sub-section (4A) and sub-section (6)

Section 147 deals with payment of advance tax by taxpayers on a quarterly basis. The Bill seeks to insert a proviso to

sub-section (4) in terms of which, while working out the advance tax liability for the quarter, in the case of a company or

AOP, if the tax payer fails to provide the turnover value for the said quarter, or the quantum of turnover is not known,

the advance tax liability in such case for the quarter is to be worked out by taking the value of turnover for the quarter

as being ¼th of 110% of the turnover of the latest tax year, for which a return has been filed.

Presently, under sub-section (4A) of section 147 of the Ordinance, the taxpayer is entitled to estimate the tax liability

for the relevant tax year at any time before the second instalment is due i.e. even before completion of the half year

after such estimation. This effectively requires payment of 50% of the estimated advance tax by the due date of the

second quarter of the relevant tax year. The remaining 50% is required to be paid in the third and fourth quarterly

instalments. Under the aforesaid sub-section, a taxpayer is not permitted to make a lower estimate of its income. The

Bill seeks to amend the aforesaid sub-section, whereby banking companies are proposed to be included within the ambit

of a taxpayer, with the result that the banking companies will be required to absolve their advance tax liability in

accordance with the provisions of sub-section (4A). However, banking companies under Rule 5(1) of the Seventh

Schedule and sub-section (4A) of section 147 have been specifically excluded. Since the Bill has not proposed any

amendment with regard to the provision of Rule 5 of the Seventh Schedule, therefore, in our opinion, the legal position

relating to the advance tax obligation of the banking company remains intact, as contained in Rule 5 of the Seventh

Schedule.

Moreover, the Bill seeks to amend the provision of sub-section (6), in terms of which a banking company is excluded for

the purpose of making its estimate under the aforesaid sub-section. However, under Rule 5(1) of the Seventh Schedule,

sub-section (6) of section 147 has been specifically excluded. The Bill also requires the taxpayer to provide the following

details to the Commissioner while working out the estimate of the amount of tax payable:

Turnover for the completed quarters of the relevant tax year;

Estimated turnover of the remaining quarters along with any valid reason for any decline in estimated turnover, if

any;

Documentary evidence of the estimated expenses or deductions which may result in lower payment of advance tax;

and

The computation of the estimated taxable income of the relevant tax year.

The Bill further seeks to empower the Commissioner to consider the rejection of the estimate, if the above information

is not made available by the taxpayer. In such a case, the advance tax liability is to be worked out on the basis of the

provisions of Sub-section (4).

11. Return not filed within due date

Section 182A & 214D

It would be recalled that Section 214D automatically selects a case for tax audit in case the return of income has not

been filed by the tax payer by the due date, or the extended due date, or the tax payable along with the return of

income has not been paid.

Income Tax

EY Ford Rhodes

10

Further, penalizing provisions were embedded under Section 182 whereby the non / late filing of the return of income

was subject to a penalty, at the prescribed rates.

Although the penal provisions have been retained, the bill proposes to omit Section 214D thereby relieving the tax

payer from selection of tax audit in case of non/ late filing of the return of income. However, in order to check on non /

late filing of tax return, the bill proposes to insert a new Section 182A, whereby it is proposed that if a taxpayer fails to

file the return of income within the due date or the extended due date, its name will not be included in the Active

Taxpayers List, and it will not be entitled to carry forward any loss for the year.

12. Advance tax on persons remitting amounts abroad through credit or debit or prepaid cards

Section 236Y and First Schedule

The Bill proposes to insert a new section wherein every banking company will now be required to collect adjustable

advance tax at the rate of 1% of the gross amount remitted abroad for filers and 3% in case of non-filers from every

credit card, debit card and prepaid card transaction with a person outside Pakistan.

Given the increasing trend of online transactions, the proposed advance tax is likely to have a positive impact on the

revenue collection. However, this increase in collection would come at the expense of an already administratively over-

burdened banking sector.

13. Tax paid at import stage deemed “minimum tax” for commercial importers

Section 148, Sub-section (8)

Presently tax required to be collected under this section on import of plastic raw material imported by an industrial

undertaking, falling under PCT headings 39.01 to 39.12, edible oils and packing material is treated as minimum tax. The

Bill proposes to amend the above sub-section whereby, in addition to the above mentioned goods, the tax required to be

collected on import of goods that are sold in the same condition as they were when imported is to be treated as

minimum tax. This is a substantive conceptual shift with respect to taxation of commercial importers being proposed to

be made in sub-section (8) of this section. Presently, commercial importers paying tax at the import stage are deemed

to have paid the same as “final tax”. The amendment now seeks to change the character of such tax payments from

“final tax” to “minimum tax”. Such commercial importers, pursuant to the proposed amendments will be required to file

a return of income instead of filing of statement in terms of section 115 of the Ordinance, and may be subject to

amendment of assessment/tax audit under section 177.

14. Services rendered by a non-resident through its permanent establishment

Section 152

Subject to certain exceptions, taxes withheld from resident service providers constituted a minimum tax pursuant to

section 153. Conversely, taxes withheld from a non-resident rendering services through its permanent establishment

was considered as an advance tax under section 152.

In order to provide a level playing field, the Bill proposes to amend section 152 with the effect that the taxes withheld

from payments to the permanent establishment of the non-resident service provider, would also now be regarded as a

minimum tax. However, the exception to such minimum taxation, as available to resident service providers under

section 153, would also mutatis mutandis apply to non-resident service providers.

The proposed amendment may be in conflict, in specific situations, with the taxation of non-resident service providers

who are from countries with whom Pakistan has signed Agreements for Avoidance of Double Taxation and Fiscal

Evasion, which overrides the domestic law .

Income Tax

EY Ford Rhodes

11

15. Restriction of transfer of assets through gift

Sections 37 & 79

Section 37 deals with taxation of capital gains on sale of assets. For the purpose of valuation of a capital asset, it is

inter-alia provided that where an asset becomes the property of a person under a gift, the fair market value of asset on

the date of its transfer shall be treated to be the cost of the asset.

Similarly, section 79 provides non-recognition rules which inter-alia provide that no gain or loss shall be taken to arise

on the disposal of an asset by reason of a gift.

The bill now seeks to restrict the gift to those which have been received from a relative. The term relative has been

defined in Section 85 of the Ordinance which deals with Associate. The definition of a relative in relation to an individual

is provided as under:

a) Ancestor, a descendant of any of the grand parent or an adopted child of the individual or of a spouse of the

individual;

or

b) A spouse of the individual or of any person specified in Clause (a).

It is understood that the aforesaid amendments are one of several anti-avoidance measures that are being introduced in

the law to check misuse of a legal provision to evade tax.

16. Alternative Dispute Resolution

Section 134A

The concept of Alternative Dispute Resolution (ADR) was introduced via the Finance Act, 2004 whereby a taxpayer may

bring any disputed matter, which is pending before an appellate authority before the Board by making an application.

For this purpose, the Board is required to constitute a Committee (ADRC) comprising an Officer of Inland Revenue (not

below the rank of a Commissioner) and two persons from a panel of Cost or Chartered Accountants, or Advocates or

Income Tax Practitioners being reputable taxpayers, before which the matter is to be placed for examination and

recommendations to the Board.

The ADRC shall undertake an examination of the issue and may make enquiry, obtain expert opinion and cause an audit

by any officer of Inland Revenue or any other person. Based on the findings, the ADRC shall make recommendations as

may be appropriate in the facts and circumstances of the case. The ADRC is required to be formed within the period of

sixty days of the making of an application by the taxpayer. The ADRC is then required to make its recommendations

within ninety days of its constitution. If the ADRC fails to make the recommendation within the above period of ninety

days, the Board is empowered to dissolve the ADRC and constitute a new ADRC, which is required to dispose of the

matter within a further period of ninety days. However, if the new ADRC fails to the resolve the dispute in the above

period, the matter shall be taken up by the appellate forum, where it is pending.

In case, the ADRC makes recommendation within the statutory period of ninety days, the Board is then required to pass

an order on the recommendations of the ADRC, as may be appropriate within ninety days of the receipt of ADRC’s

recommendations and if such an order is not passed, the recommendations would be treated to be an order passed by

the Board.

The most controversial provision was the powers of the Board either to reject the ADRC’s recommendations or to

accede to such recommendations, in the manner the Board deems appropriate. It was objected to on the basis that the

ADRC, which comprises of a senior officer of the Board and professionals/ reputable taxpayers, and which works on a

Income Tax

EY Ford Rhodes

12

pro-bono basis, does not have any say in the conclusion of the dispute. As a result, the process of ADR has not yielded

the desired results of reducing the pending litigation before the appellate authorities.

The Bill now proposes substantial changes in the entire process of constitution and working of ADRC. These are

discussed as under:

The ADRC members would be selected from a panel of retired Chartered Accountants or retired Advocates (the

term retired seems to be a mistake as no such condition is provided in ADRC mechanism prescribed for sales Tax

Act 1990 through this bill), and retired Judges of High Court besides an officer of Inland Revenue not below the

rank of a Commissioner.

The taxpayer invoking the powers of ADRC and the Board shall withdraw the appeals pending before the Appellate

Authority.

The ADRC shall not commence the proceedings unless the order of withdrawal by the Appellate Authority is

communicated to the Board. In the event the order of withdrawal is not communicated within seventy five days of

the appointment of the ADRC, the ADRC so appointed shall be dissolved.

The ADRC shall decide the dispute within one hundred and twenty days of its appointment excluding the period of

communicating the order of withdrawal.

The ADRC is now empowered to decide the matter, and such decision shall be binding on the aggrieved person as

well as on the Board.

If the ADRC fails to decide the matter within the period of one hundred and twenty days, the Board shall dissolve

the ADRC, inform the Appellate Authority (which passed the order of withdrawal of matter) and the matter would

be deemed to be pending before the Appellate Authority, which shall decide the matter as if the appeal was never

withdrawn. The Appellate Authority is required to decide the appeal within six months of the communication of the

order of dissolution of the ADRC.

The proposed amendments however, do not appear to achieve the objects with which the concept of ADR was

introduced. This is for the reason that the very concept of “Alternate” would fade away with the requirement to give

up the appellate process. Presently, the order passed by the Board on the recommendations of the ADRC is not

binding on the aggrieved person but on the Board officials. Such an order is to be presented before the Appellate

Authority, which is required to take into consideration while deciding the matter pending before it. This gives the

aggrieved person an option to evaluate the outcome of the ADR proceedings and decide whether to pursue the

appeal or not. However, since the appeal is now proposed to be withdrawn before the ADRC takes up the matter for

decision, the aggrieved person would not have this option. The law makers are therefore urged to make the order of

the ADRC binding on the Board and not on the aggrieved person.

17. Service of notice and other documents

Section 218

This section provides the manner in which a notice, or any other documents, are to be served on a taxpayer by the tax

authorities. It presently provides the following to be the acceptable manner in which a notice or other documents shall

be treated as properly served:

a) Personally served on the individual;

b) Sent by registered post or courier service to the registered office or address of the taxpayer; or

Income Tax

EY Ford Rhodes

13

c) Served on the person in the manner prescribed for service of Summons under the Code of Criminal Procedure,

1908.

The bill now seeks to amend this section to legitimize the procedure for service of notice, or any other documents,

which are sent electronically in the prescribed manner.

It may be noted that rules were formulated for service of notices through electronic medium, and practically the Board

was delivering notices and orders through its e-portal. Owing to the fact, however, that the main statute did not permit

service of notices electronically, notices and orders that were served through the e-portal of the Board were often

challenged in appeals.

Recently, the Board also acknowledged this shortcoming and directed its officers to ensure that along with electronic

service, the taxpayers were also sent hard copies of notices and orders through courier or post, in order to ensure

proper legal service. With this proposed amendment, however, the bill now seeks to rectify the shortcoming and enable

electronic servicing with full legal support.

18. Business income of a non-resident person

Sections 101 and 152

As in international tax, the Ordinance while defining the geographical source of income under section 101, recognizes

the force of attribution principle, whereby non-residents, in respect of their business income, are considered to derive

Pakistan source income if their income is attributable to the permanent establishment in Pakistan. The legislation also

recognized the limited force of attraction principle, whereby if the non-resident enters into same or similar activities or

sale of same or similar goods as that of the permanent establishment, such income is also regarded as Pakistan source.

Therefore, ordinarily, sales of goods made by non-residents outside Pakistan, fall outside the purview of Pakistan tax

even if the non-resident has a permanent establishment in Pakistan, which is engaged in the installation, erection and

commissioning into service of such goods. This principle was endorsed by the Honorable Appellate Tribunal Inland

Revenue in its judgment cited as (1999) 80 Tax 17(Trib.).

The Bill now proposes to undo the effect of this principle by inserting a new clause in Sub-section (3) of section 101,

under which Pakistan sourced income from business derived by a non-resident person, would include income on account

of import of goods, whether or not the title to the goods passes outside Pakistan, if the import is part of an overall

Engineering, Procurement, Construction and Commissioning (EPCC) arrangement, irrespective of the fact that the

importer is the person, associate of the person or any other person.

Keeping in view the proposed amendment in section 101(3), corresponding amendments have also been proposed in

Sub-section (7) of section 152, whereby a taxpayer would invariably now be required to obtain a tax exemption

certificate from the Commissioner, in case the taxpayer intends to make payments on account of such transactions

without deduction of tax.

Given that the government is focusing on expanding its economic horizon, including via C-PEC, in our view, such

amendments may have an adverse impact on the foreign investors. Additionally, it is practically witnessed that most of

the foreign contractors pass their tax burden on resident persons through tax gross-up clauses. Hence, the cost of

doing business for such resident persons would increase significantly due to the proposed amendments. Further, it

remains unclear what costs may be admissible to such a non-resident against such income.

Without prejudice to the above, it needs to be highlighted that the BEPS Action Plan 7 also recommends that Treaty

provisions are amended to ensure that PE formation is not avoided through artificial splitting of contracts to bypass any

timeframe requirements. While we may assume that the BEPS Action Plan 7 was a consideration in drafting the

suggested amendments, in our view however, the core essence of the Action Plan has not been correctly reflected.

Income Tax

EY Ford Rhodes

14

19. Gain on disposal of assets outside Pakistan

Section 101A

Section 101 of the Ordinance identifies the different circumstances under which a taxpayer is considered to derive

Pakistan source income. Under the said section, the indirect disposal of an asset in Pakistan generally does not

constitute Pakistan source income. The only exception to this rule is in relation to the gain arising from the disposal of

immovable property or shares in a company, the assets of which consist wholly or principally of immovable property,

including rights to explore for and exploit natural resources in Pakistan.

Historically, the Indian legislation also did not tax indirect disposals. However, after the Vodafone controversy, the

Indian Income Tax Act was amended to levy tax on the disposal of shares of foreign companies in circumstances where

such companies derived significant value from assets located in India.

The Bill seeks to introduce a similar concept of taxing indirect disposal of assets located in Pakistan by non-residents

through insertion of a new section 101A. The salient features of the proposed section are:

Gain from disposal of an asset located in Pakistan by a non-resident shall be Pakistan sourced income;

Where the asset is any share or interest in a non-resident company, it shall be treated to be located in Pakistan if it

derives its value, directly or indirectly, wholly or principally, from assets located in Pakistan and it represents 10

percent or more of the disposed share capital of the non-resident company;

The share or interest shall be treated to derive its value principally from the assets located in Pakistan, if the value

of such assets exceed one hundred million Rupees and represents at least fifty per cent of the value of all the assets

owned by the non-resident company;

Where the assets of the non-resident company are not wholly located in Pakistan, only income to the extent that is

reasonably attributable to such assets as are located in Pakistan, and is determined as may be prescribed, would be

taxable;

Where the assets in Pakistan are held through a resident company, such company shall be required to provide the

prescribed information to the Commissioner within 60 days of the transaction;

The buyer would be required to withhold tax at the rate of 15 percent of the gross amount of the consideration paid

to the non-resident;

Where the buyer has not withheld tax, the resident company is required to collect the requisite tax from the non-

resident seller;

The rate of tax to be withheld by the buyer or collected by the resident company shall be the higher of :

20% of the gain (i.e. fair market value less cost of acquisition of the asset); or

10% of the fair market value of the asset; and

Where the tax has been withheld by the buyer or collected by the resident company, no tax shall be payable by the

non-resident company in respect of the gain under the head “Income from Business” or “Capital Gains”.

Whilst the proposed insertion of the new section attempts to ensure that the revenue authorities receive a fair share of

tax on gains arising from the alienation of assets, whose underlying value is located in Pakistan, the proposed section

has not been drafted in a coherent manner. Issues like possible differences in interpretation, potential multiple taxation,

onerous compliance requirements and practical limitations on availability of information have not been considered,

which shall result in unnecessary litigation. Furthermore, there are ambiguities arising from the manner in which the

proposed section has been drafted.

Income Tax

EY Ford Rhodes

15

An example of the said anomalies is evident from the conflict in the rate at which the buyer is required to withhold tax

from the non-resident seller. As per one of the provisions, the buyer is required to withhold tax at 15% of the gross

consideration, whereas another provision requires the buyer to withhold the tax at the higher of 20% of the gain and

10% of the fair market value of the asset.

Overall, in our view, while the idea behind the proposed new section may be appreciated, it needs to be revisited and

redrafted rationally in order to address the key issues, which have not been duly considered.

20. Re-characterization of income and deductions

Sections 107 and 109

In light of the recommendations of the OECD Action Plans 5 and 6, relating to transparency and substance, and treaty

abuse, respectively, the Bill has proposed to amend the provisions of section 109 of the Ordinance by introducing the

concept of beneficial ownership and empowering the tax authorities to disregard an entity or a corporate structure, that

does not have an economic or commercial substance, or was created as part of a tax avoidance scheme.

Furthermore, while the Ordinance states that a tax avoidance scheme would include any transaction where the main

purpose is to reduce any person’s tax liability, the Bill now seeks to define the term reduction in tax liability. The

proposed definition states that such a term means the reduction, avoidance or deferral of tax, or the increase in a

refund of tax and includes a reduction, avoidance or deferral of tax that would have been payable under this Ordinance,

but are not payable due to a tax treaty for the avoidance of double taxation as referred to in section 107.

Moreover, an amendment in section 107 has also been proposed, whereby the benefits available under a double tax

treaty would be subject to section 109.

21. Definition of Permanent Establishment

Section 2

Currently, the definition of a permanent establishment, inter-alia, covers a dependent agent acting in Pakistan on behalf

of a non-resident person, if he has and habitually exercises an authority to conclude contracts on behalf of the non-

resident. The current definition in the Ordinance is narrower than the internationally accepted concept of a dependent

agent , which also encompasses persons who act exclusively on behalf of another person.

The Bill now seeks to align the local concept of a dependent agent with international practice, including BEPS Action

Plan 7, by expanding the definition. It is proposed that a dependent agent would include any person, who has and

habitually exercises an authority to conclude contracts on behalf of a non-resident person, or has and habitually plays

the principal role leading to the conclusion of contracts that are routinely concluded without material modification, and

these contracts are:

(a) in the name of the non-resident person; or

(b) for the transfer of the ownership of, or for the granting of the right to use property owned by that non-resident or

that the non-resident has the right to use; or

(c) for the provision of services by that person.

It may be appreciated that under the current definition, the concept of a dependent agent was confined only to dealing

in goods, and therefore, agents appointed in Pakistan vis-à-vis rendering of services and use of property were

interpreted to fall outside the purview of a dependent agency. However, it seems that the anomaly has now been

addressed by bringing such agents specifically within the scope of permanent establishment.

Income Tax

EY Ford Rhodes

16

The Bill also proposes to insert an explanation, whereby it is clarified that a dependent agent would include a person

acting exclusively, or almost exclusively, on behalf of the person of which it is an associate.

A new term of “cohesive business operation” has been inserted as part of the explanation, whereby an arrangement for

the supply of goods, installation, construction, assembly, commission, guarantees or supervisory activities, undertaken

or performed either by the person or the associates of the person, and a supply of goods including goods imported in

the name of the associate or any other person, whether or not the title to the goods passes outside Pakistan, has been

included.

22. Controlled Foreign Company

Section 109A

In line with BEPS Action Plan 3, the Bill seeks to introduce taxability of income derived by a Controlled Foreign Company

(CFC) by inserting a new section 109A of the Ordinance. The salient features of which are as follows:

A CFC is a corporate entity that is registered and conducts business in a different jurisdiction other than a

jurisdiction of a residency of the controlled owners.

The concept of CFC has been introduced in order to tax the income of a resident person by attributing its income in

CFC. It has been designed to limit artificial deferral of tax by using off-shore low taxed or exempt entities.

The definition of CFC proposed in the Bill is as follows:

(a) more than fifty percent of the capital or voting rights of the non-resident company are held, directly or

indirectly, by one or more persons resident in Pakistan or more than forty percent of the capital or voting

rights of the non-resident company are held, directly or indirectly, by a single resident person in Pakistan;

(b) tax paid, after taking into account any foreign tax credits available to the non-resident company, on the income

derived or accrued, during a foreign tax year, by the non-resident company to any tax authority outside

Pakistan is less than sixty percent of the tax payable on the said income under this Ordinance;

(c) the non-resident company does not derive active business income as defined under sub-section (3); and

(d) the shares of the company are not traded on any stock exchange recognized by law of the country or

jurisdiction of which the non-resident company is resident for tax purposes.

•The income to be offered for tax under CFC represents active income which accrues if:

(a) more than eighty percent of income of the company does not include income from dividend, interest, property,

capital gains, royalty, annuity payment, supply of goods or services to an associate, sale or licensing of

intangibles and management, holding or investment in securities and financial assets; and

(b) principally derives income under the head “Income from Business” in the country or jurisdiction, of which it is a

resident.

Taxable income of CFC is worked out by taking into account the provisions of the Ordinance on the assumption that

it is a resident tax payer.

Income Tax

EY Ford Rhodes

17

The income of CFC attributable to a Resident tax payer is computed as under:

A x (B/100)

Where -

A is the amount of income of a CFC under sub-section (2); and

B is the percentage of capital or voting rights, whichever is higher, held by the person, directly or indirectly,

in the CFC

•No income of the CFC will be attributable to a resident taxpayer if :

-capital or voting rights of the resident in such CFC are less than 10%; or

-the amount of income is less than Rs.10 million.

•In relation to working out the income of CFC, a concept of Foreign Tax Year has been introduced, which in relation

to a non-resident company, means any year or period of reporting for income tax purposes by such non-resident

company in its country or jurisdiction of residence, or if such company is not subject to income tax, any annual

period of financial reporting by such company.

•Income of a CFC in respect of the Foreign Tax Year shall be determined in the currency of that CFC. However, for

the purposes of determining the amount to be included in the income of any resident person during any tax year,

the same shall be converted into Pak Rupees at the applicable foreign exchange conversion rates, as notified by the

State Bank of Pakistan.

•Income attributable to CFC once taxed in Pakistan shall not be offered to tax upon its subsequent receipt in

Pakistan by a resident tax payer.

23. Furnishing of information by banks

Section 165A

The Finance Act, 2013, introduced a separate section requiring banking companies to furnish information about the

banking transactions of their customers, to the tax authorities. The law provides an overriding effect to the Protection

of Economic Reforms Act, 1992, the Banking Companies Ordinance, 1962, the Foreign Exchange Regulation Act, 1947,

and the regulations made under the State Bank of Pakistan Act, 1956. Apart from seeking particulars of deposits and

card transactions, the law requires details of loans written-off and certain other transactions. However, the most

contentious requirement was the provision of online access of the banks’ central database containing details of its

account holders and all transactions made in their accounts to the Board. This requirement in particular led to a lot of

controversy and the banks, due to their compulsion of maintaining secrecy of client data, were forced to approach the

courts for seeking a resolution of the matter. However, since 2013 to-date, the banking sector has neither provided the

requisite information nor access to the Board.

The Bill now seeks to omit the requirement of online access to the Board and instead required banks to provide

information about cash withdrawals by filers and non-filers in excess of Rs.1 million per month. It is further proposed

that the minimum threshold for providing details of deposits be enhanced from Rs.1 million to Rs.10 million per month.

Similarly, the limit of card transactions is also proposed to be enhanced to Rs.200,000 from the present prescribed limit

of Rs.100,000 per month.

Income Tax

EY Ford Rhodes

18

24. Restriction on purchase of certain assets

Section 227C

The bill seeks to introduce a new section, which provides that any person who is a non-filer will not be allowed to book,

register, purchase or transfer:

a) A new locally manufactured motor vehicle or an imported vehicle - applications for registration or purchase of such

motor vehicles will not be accepted by any vehicle registering authorities of the Excise and Taxation Department, or

a manufacturer of the motor vehicle unless the applicant, being a person, is a filer;

b) Immovable property - applications or requests for registering, recording or attesting the transfer of such

immovable properties shall not be accepted unless the applicant, being a person, is a filer.

This is a welcome step and will assist the Government in broadening the tax base.

25. Best judgment assessment

Section 121

The provisions of section 114 empower the Commissioner to issue a notice to any person who has not filed the return of

income in respect of one or more of the last five completed tax years. However, in cases where a person has not filed

any tax returns for the last five completed tax years, the Commissioner is empowered to issue a notice to such a person

for up to the last ten completed tax years.

Section 121 deals with powers of the Commissioner to pass a best judgment assessment in case where a person fails to

file a return in response to a notice issued by the tax authorities. The statute of limitation presently provided for any

action under this section, is that an assessment order can be passed within five years after the end of the tax year to

which it relates.

It is now proposed that in cases where the Commissioner uses his powers under section 114(5) and requires any person

to file tax returns upto ten years, then in such a case it is proposed that the time limit for passing an assessment order

would be within two years from the end of the tax year in which such notice was issued.

26. Tax credit for investment

Section 65B

Currently, corporate taxpayers investing any amount for purchase of plant and machinery for the purpose of extension,

expansion, balancing, modernization and replacement of plant and machinery already installed in the industrial

undertaking are entitled to a credit equal to 10% of the amount so invested, against the tax payable, subject to the

condition that the plant and machinery is purchased and installed at any time between 01 July 2010 to 30 June 2019.

The Bill now proposes to extend the date of installation to 30 June 2021.

27. Tax credit for newly established industrial undertakings

Section 65D

The Finance Act, 2011, introduced section 65D, which allows a tax credit equal to 100% of the amount of tax payable,

to a company set up after 01 July 2011 through a 100% equity investment. This is subject to the condition that the

company is incorporated and the industrial undertaking is set up between 01 July 2011 to 30 June 2016.

The Finance Act, 2016, extended the period to 30 Jun, 2019 and the above condition of equity financing of 100% was

relaxed to 70%, thereby allowing investment from debt financing upto 30%.

Income Tax

EY Ford Rhodes

19

The Bill now seeks to extend the availability of tax credit to companies set up until 30 June 2021.

28. Tax credit for industrial undertakings established before the first day of July 2011

Section 65E

In line with allowing a tax credit to a newly established industrial undertaking, Section 65E allows a similar tax credit to

industrial undertakings established prior to 01 July 2011, which invest through equity in new projects or balancing,

modernization, replacement, expansion or extension (BMREE) of the existing plant and machinery, subject to the

condition that plant and machinery is installed between 01 July 2011 to 30 June 2016.

The Finance Act, 2016, extended the period to 30 June 2019 and the above condition of equity financing of 100% was

relaxed to 70% thereby allowing investment from debt financing upto 30%.

The Bill now seeks to further extend the availability of tax credit to companies that install a new projector invest in

BMREE by 30 June 2021.

29. Foreign income and asset statements

Section 116A

In terms of Section 116 of the Ordinance, a resident individual is mandatorily required to file a Wealth Statement along

with the Return of Income for a tax year, declaring therein his total assets and liabilities (including assets held in others’

names) as on the 30th day of June preceding the due date for filing of the Return of Income. Although the Wealth

Statement was meant to declare all assets and liabilities including those held outside Pakistan, the declaration of foreign

assets had been debated in the past.

The new section 116A now requires resident persons, who have foreign income or foreign assets, to furnish a separate

statement namely “Foreign Income and Assets Statement” in addition to filing a Wealth Statement under section 116,

as discussed above. The minimum threshold of foreign assets and foreign income for filing of the ‘Foreign Income and

Assets Statement’ is as follows:

(a) Foreign income equal to or in excess of USD 10,000; and

(b) Foreign assets with a value of USD 100,000 or more.

The following particulars are to be incorporated in the ‘Foreign Income and Assets Statement’ to be filed by the person:

(a) Total foreign assets and liabilities as on the last day of the tax year;

(b) Any foreign assets transferred by the person to any other person during the tax year and the consideration for the

said transfer; and

(c) Complete particulars of foreign income, the expenditure incurred during the tax year and the expenditure wholly and