Presented by:

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Presented by:Presented by:

Presented by:

Looking Back at the last 50 Years and Forward Toward the Next 50

Rob StrandSenior Economist

American Bankers Association

Presented by:

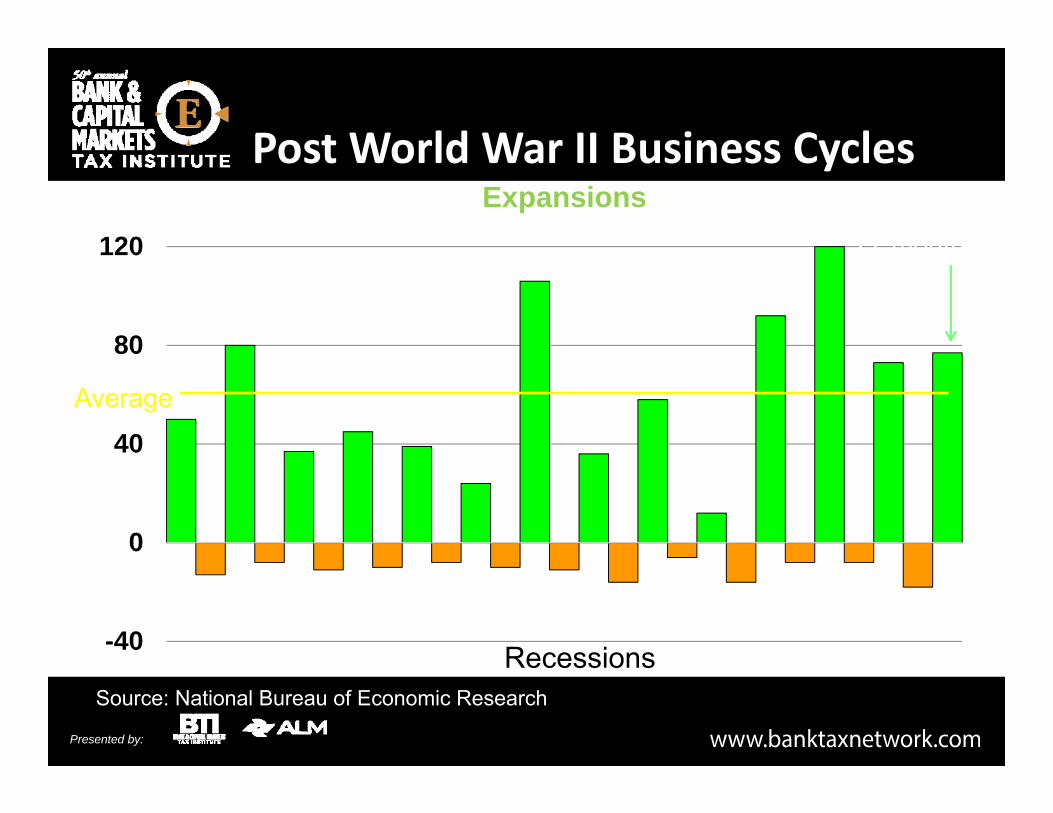

Source: National Bureau of Economic Research

-40

0

40

80

120

Post World War II Business CyclesMonths Expansions

Recessions

Current77 months

Average

Presented by:

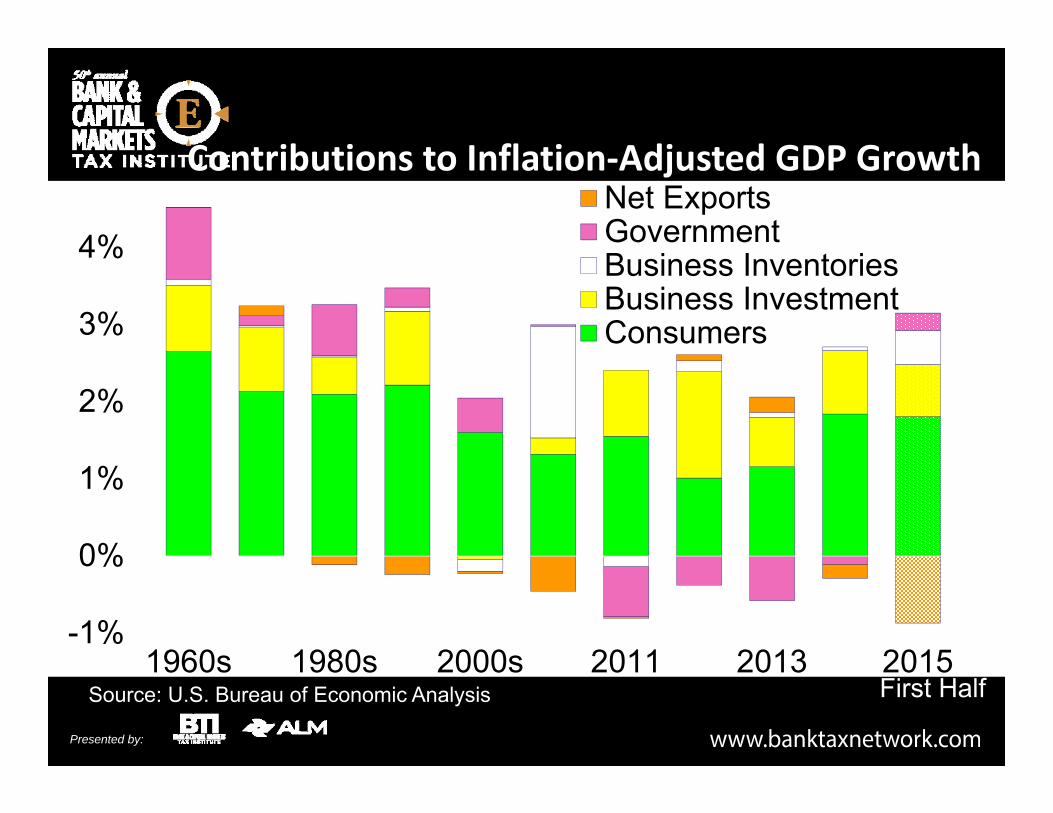

Source: U.S. Bureau of Economic Analysis

-1%

0%

1%

2%

3%

4%

1960s 1980s 2000s 2011 2013 2015

Net ExportsGovernmentBusiness InventoriesBusiness InvestmentConsumers

Contributions to Inflation‐Adjusted GDP Growth

First Half

Presented by:

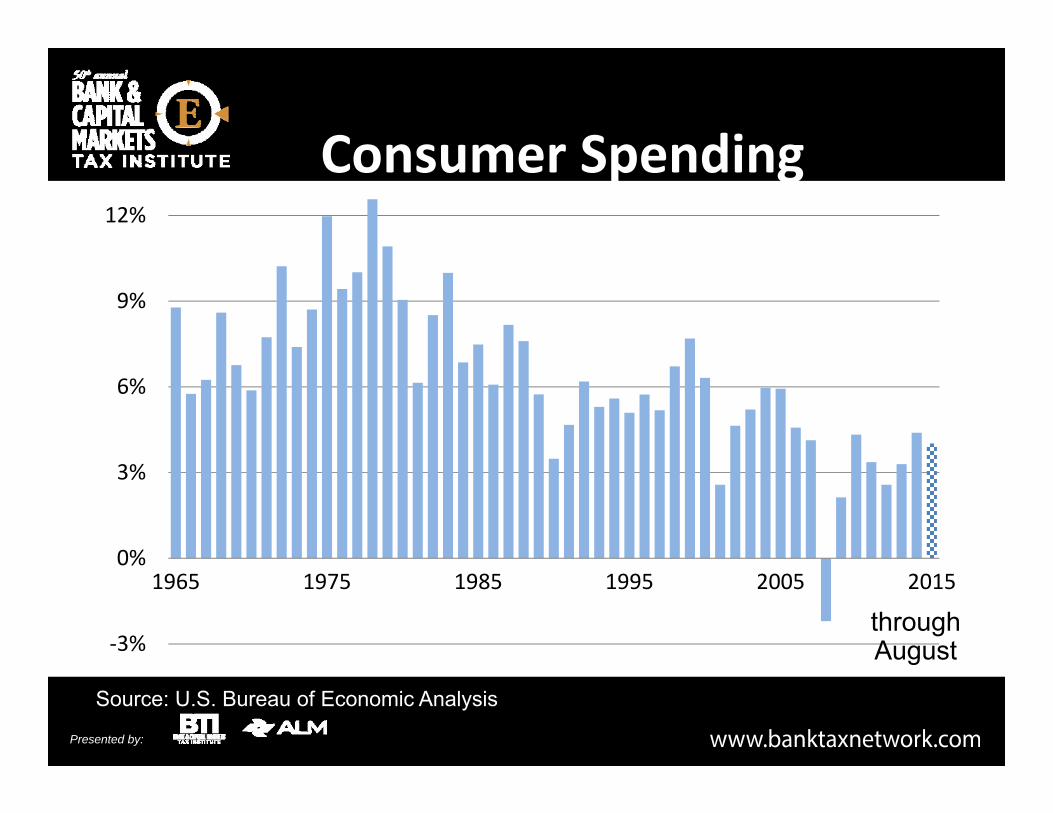

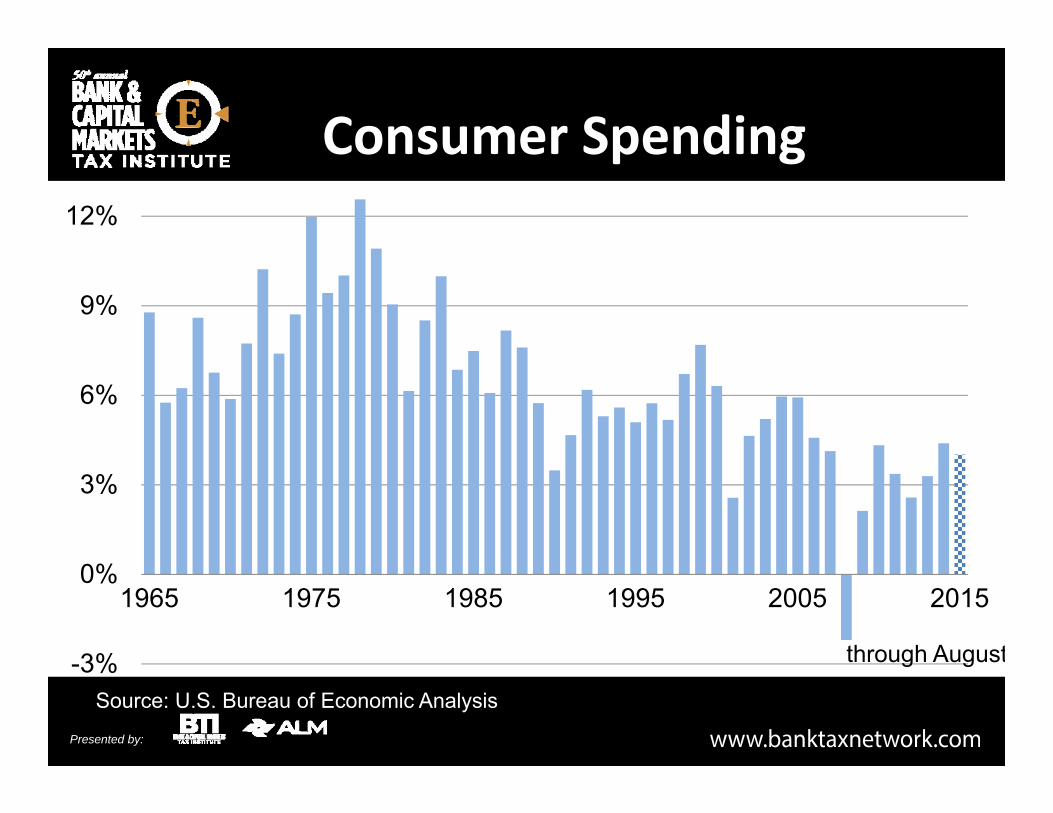

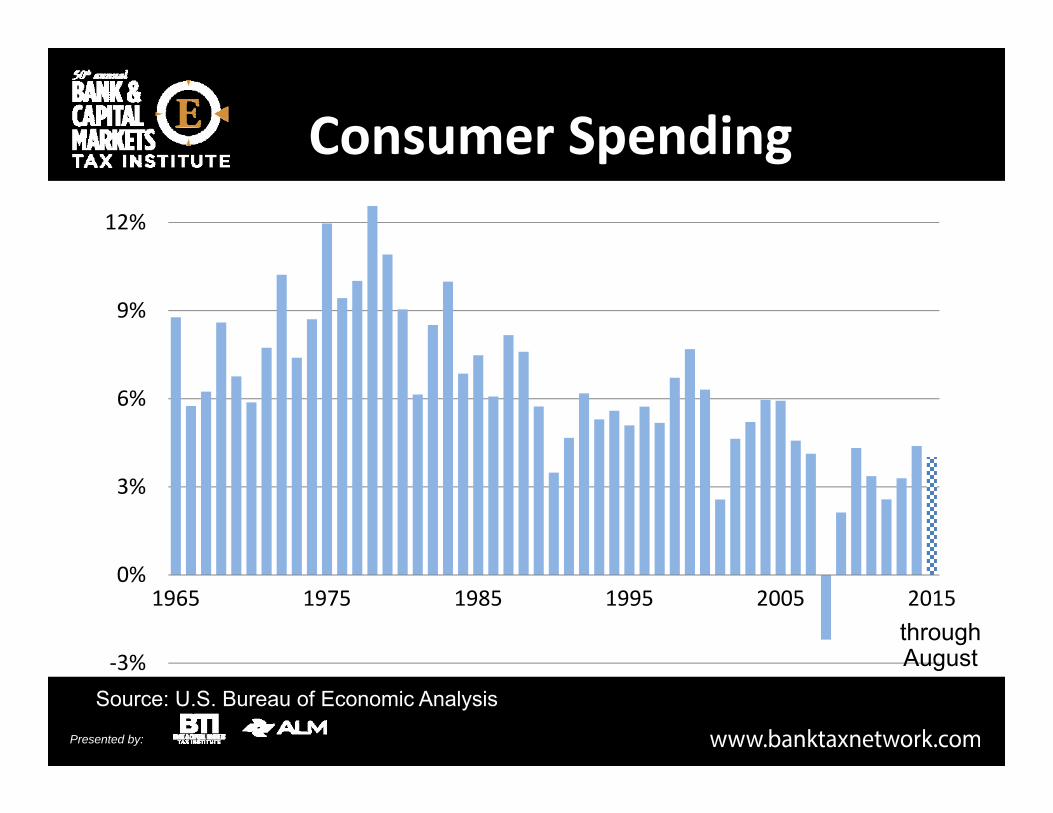

Consumer Spending

‐3%

0%

3%

6%

9%

12%

1965 1975 1985 1995 2005 2015

Source: U.S. Bureau of Economic Analysis

throughAugust

Annual Growth

Presented by:

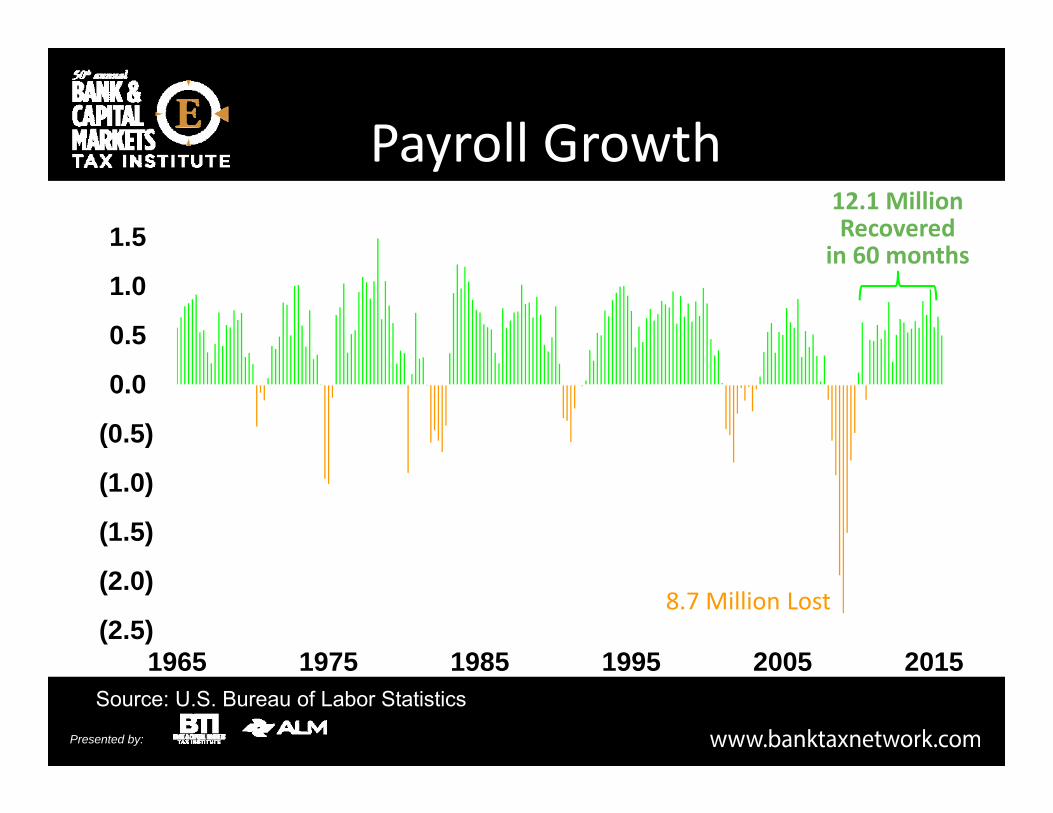

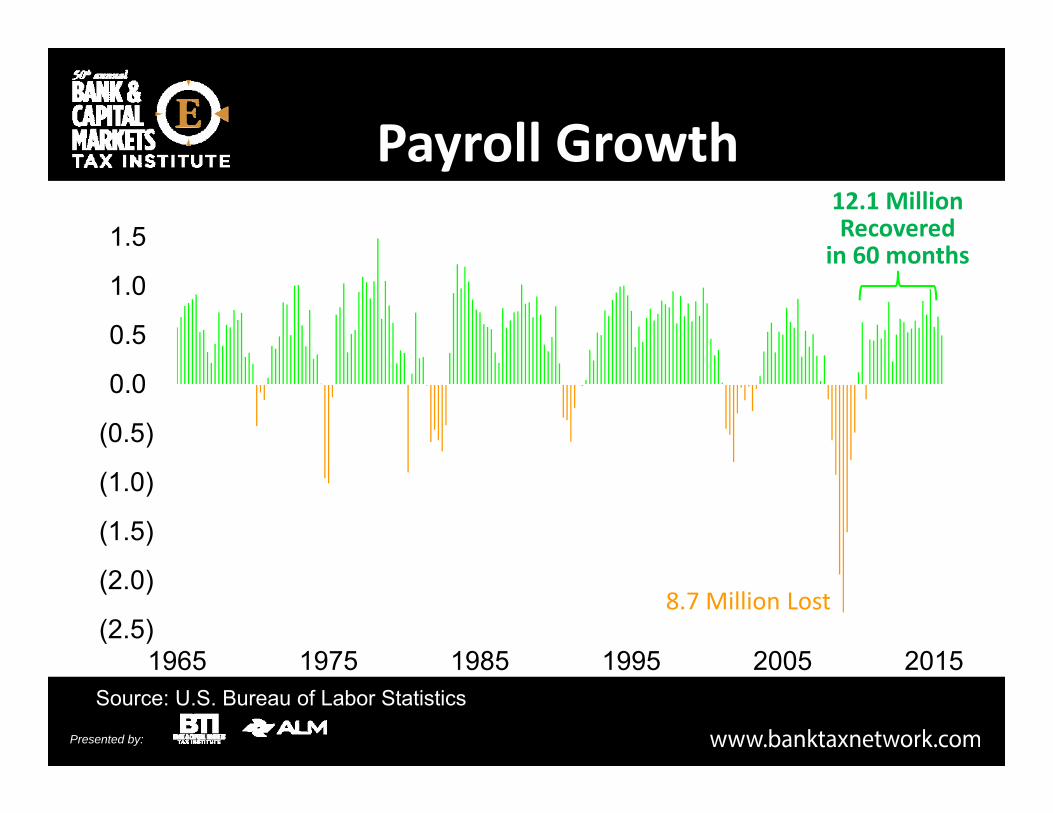

(2.5)

(2.0)

(1.5)

(1.0)

(0.5)

0.0

0.5

1.0

1.5

1965 1975 1985 1995 2005 2015Source: U.S. Bureau of Labor Statistics

8.7 Million Lost

12.1 Million Recovered

in 60 months

Payroll GrowthMillions Quarterly

Presented by:

0%

5%

10%

15%

1965 1975 1985 1995 2005 2015

Hun

dred

s

Source: U.S. Bureau of Labor Statistics

Underemployed

10.0%

5.1%Unemployed

Unemployment Rate

10.8%

Presented by:

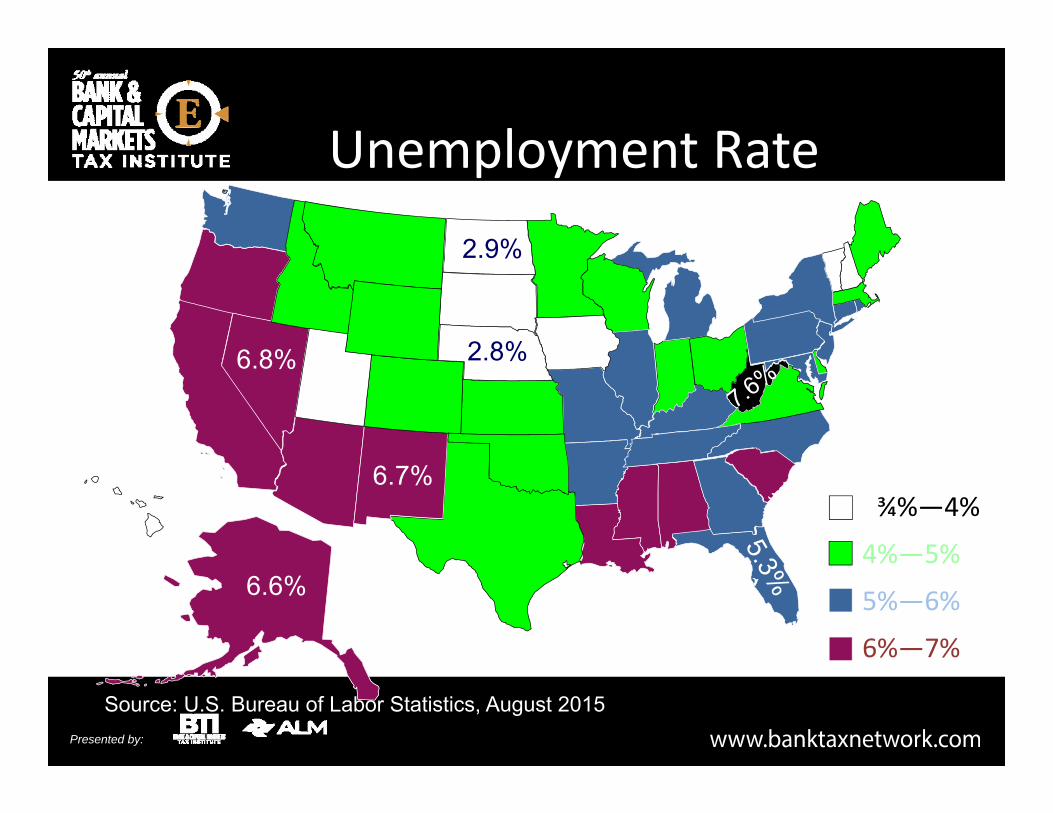

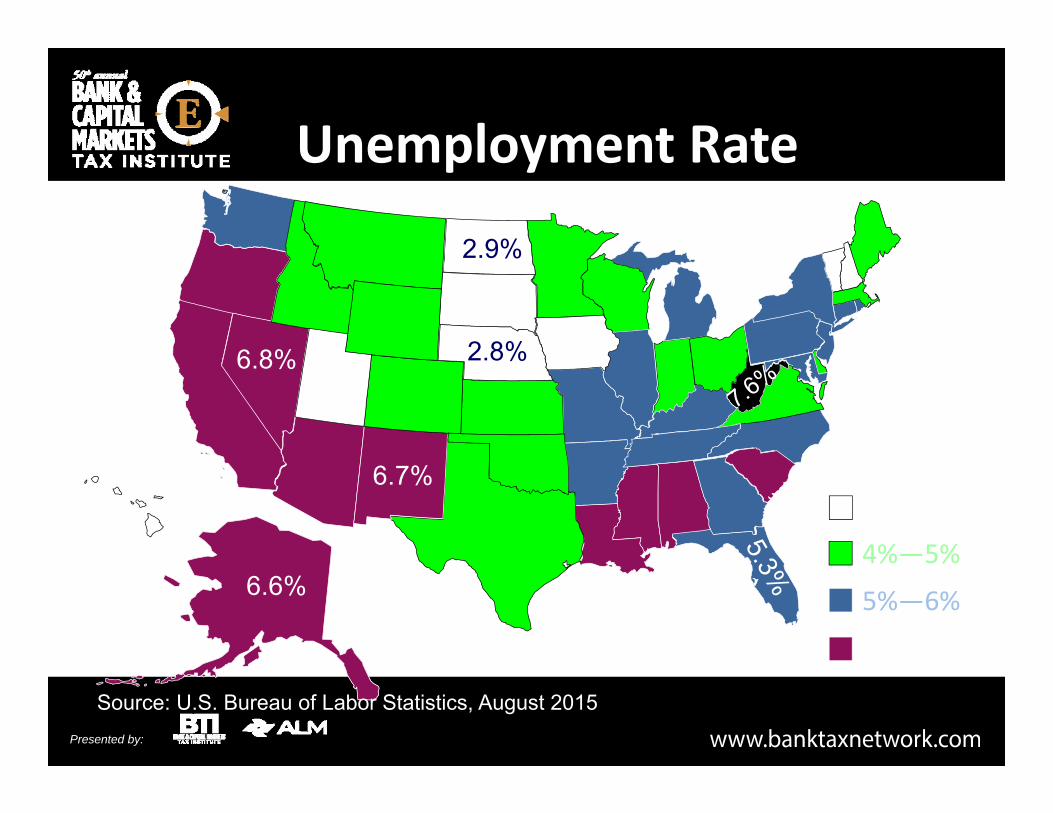

2¾%—4%

4%—5%

5%—6%

6%—7%

Unemployment Rate

Source: U.S. Bureau of Labor Statistics, August 2015

2.8%

2.9%

6.8%

6.7%

6.6%

Presented by:

11%

9%

9%

0.3%

-2%

-3%

-6%

-12%

-14%

-18%

Health Care

Bus. & Prof. Services

Leisure & Hospitality

Education

Trade & Transportation

Finance

Government

News & Entertainment

Manufacturing

Construction

Employment Change from Pre‐2011 Peak

Source: U.S. Bureau of Labor Statistics

Presented by:

Shifts in Employment Shares by Industry

GovernmentOther

TradeManufacturing

GovernmentOther

Trade

Manufacturing

1965 2015

Source: U.S. Bureau of Labor Statistics

Presented by:

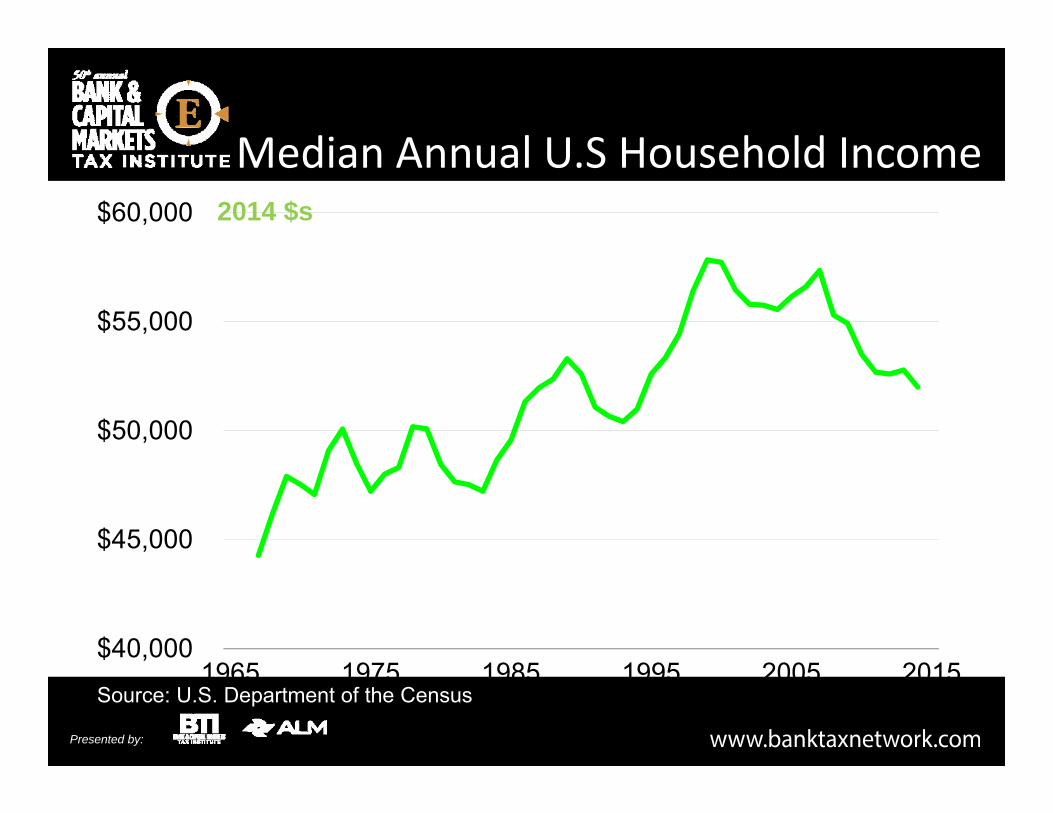

Median Annual U.S Household Income

$40,000

$45,000

$50,000

$55,000

$60,000

1965 1975 1985 1995 2005 2015Source: U.S. Department of the Census

2014 $s

Presented by:

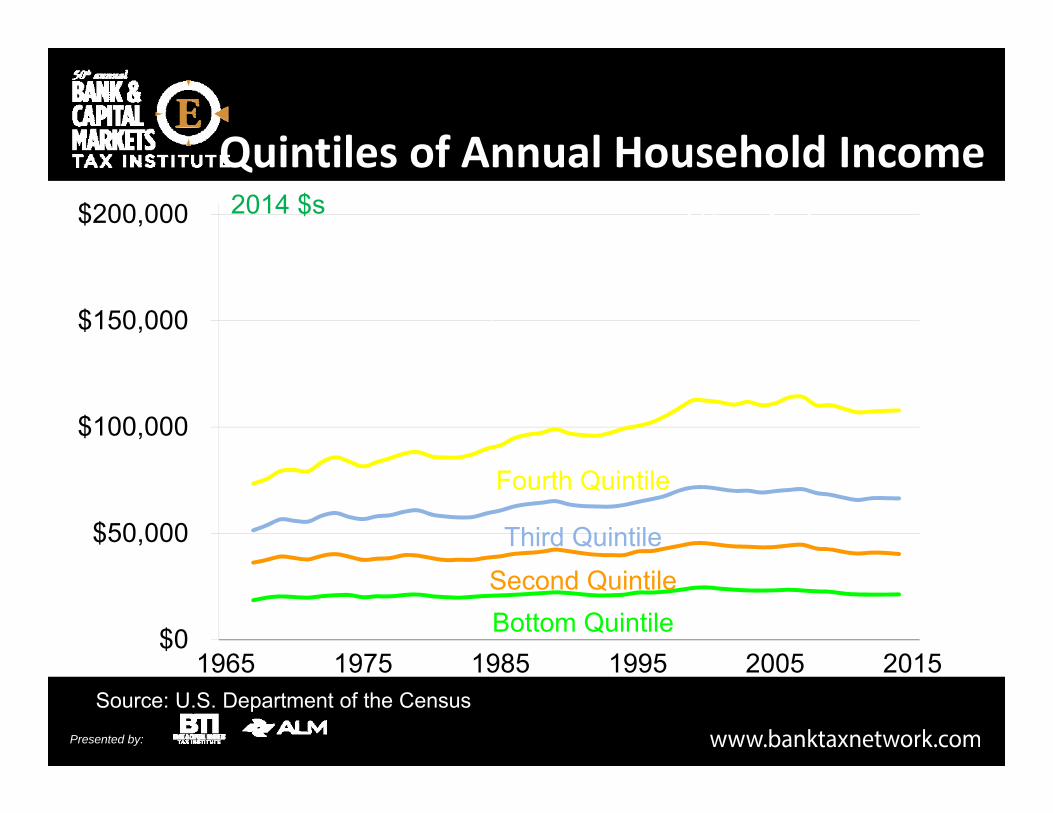

Quintiles of Annual Household Income

$0

$50,000

$100,000

$150,000

$200,000

1965 1975 1985 1995 2005 2015Source: U.S. Department of the Census

2014 $sTop 5 Percent

Top Quintile

Fourth Quintile

Third QuintileSecond QuintileBottom Quintile

Presented by:

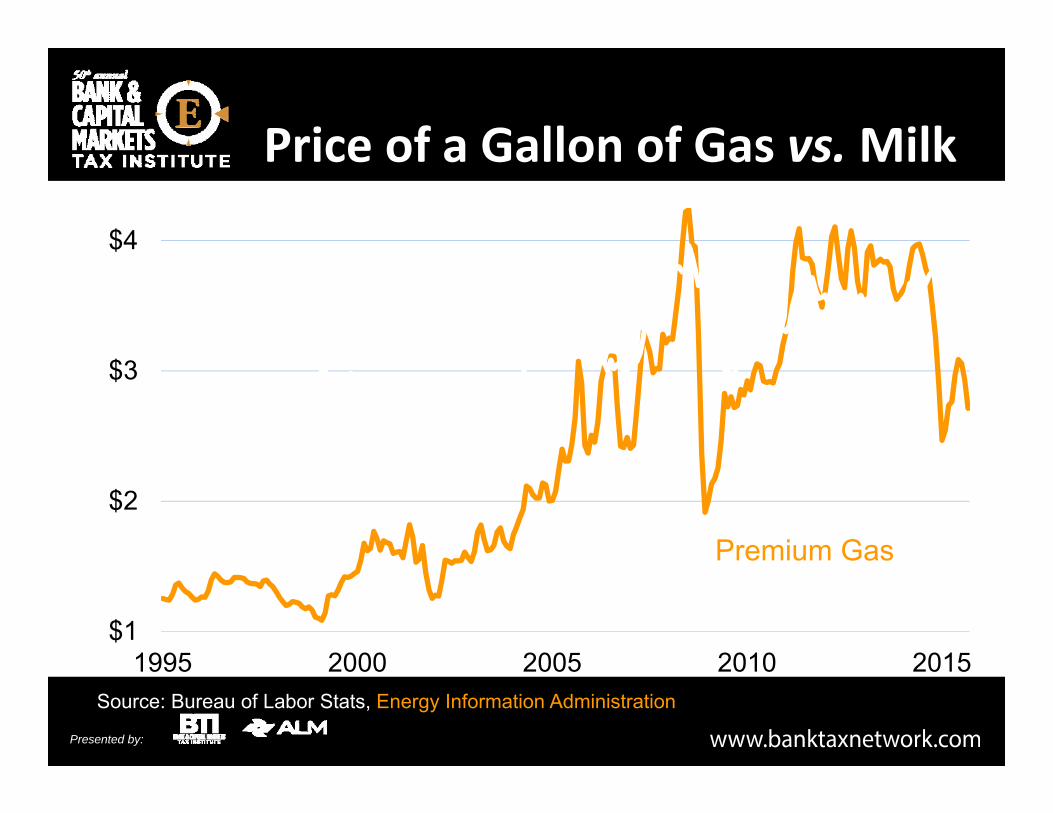

Price of a Gallon of Gas vs.Milk

$1

$2

$3

$4

1995 2000 2005 2010 2015

Premium Gas

Whole Milk

Source: Bureau of Labor Stats, Energy Information Administration

Presented by:

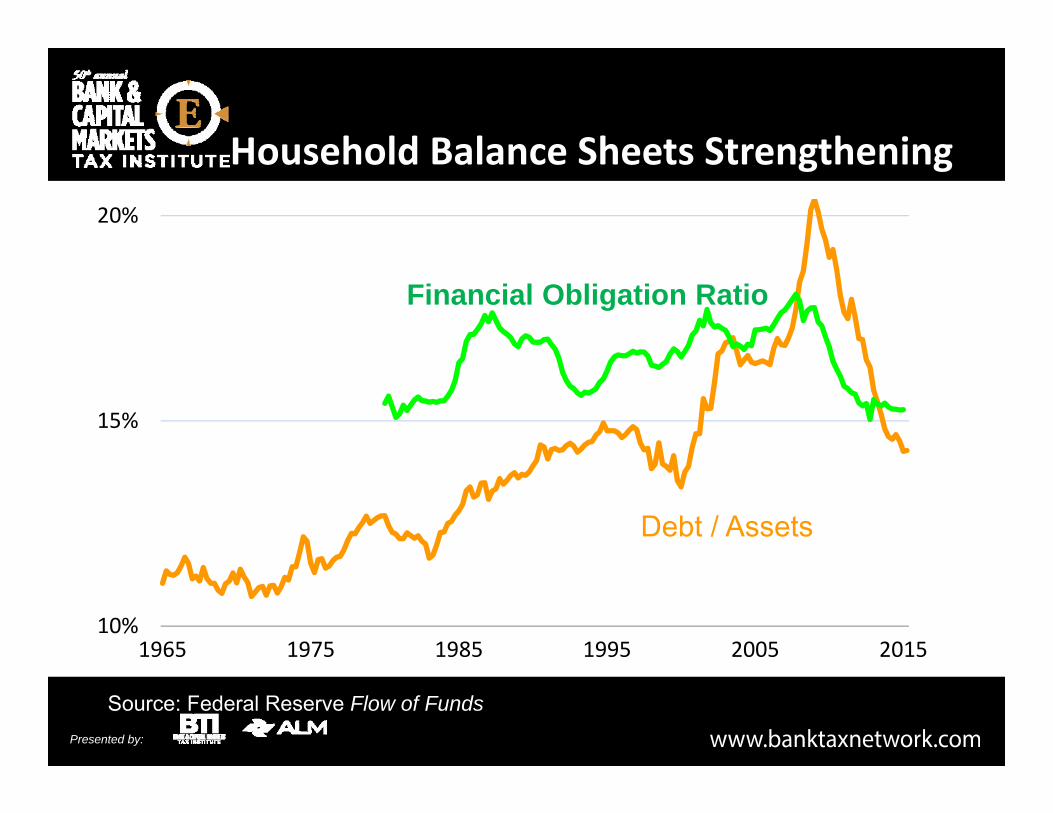

1965 1975 1985 1995 2005 201510%

15%

20%

Household Balance Sheets Strengthening

Source: Federal Reserve Flow of Funds

Debt / Assets

Financial Obligation Ratio

Presented by:

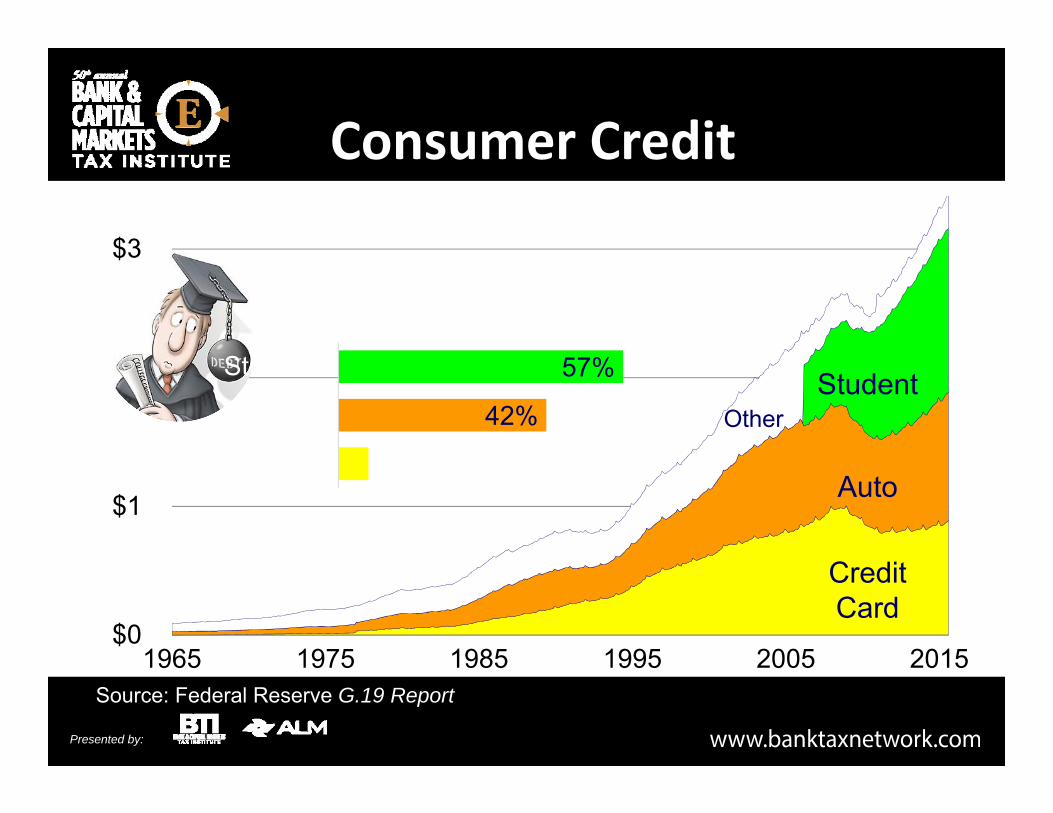

Consumer Credit

Source: Federal Reserve G.19 Report

$0

$1

$2

$3

1965 1975 1985 1995 2005 2015

CreditCard

Auto

StudentOther

6%

42%

57%

Credit Card

Auto

Student

Growth Since 2010 Trough

Trillions

Presented by:

2¾%—4%

4%—5%

5%—6%

6%—7%

Unemployment Rate

Source: U.S. Bureau of Labor Statistics, August 2015

2.8%

2.9%

6.8%

6.7%

6.6%

Presented by:

11%

9%

9%

0.3%

-2%

-3%

-6%

-12%

-14%

-18%

Health Care

Bus. & Prof. Services

Leisure & Hospitality

Education

Trade & Transportation

Finance

Government

News & Entertainment

Manufacturing

Construction

Employment Change from Pre‐2011 Peak

Source: U.S. Bureau of Labor Statistics

Presented by:

2¾%—4%

4%—5%

5%—6%

6%—7%

Unemployment Rate

Source: U.S. Bureau of Labor Statistics, August 2015

2.8%

2.9%

6.8%

6.7%

6.6%

Presented by:

0%

5%

10%

15%

1965 1975 1985 1995 2005 2015

Source: U.S. Bureau of Labor Statistics

Underemployed

10.0%

5.1%Unemployed

Unemployment Rate

10.8%

Presented by:

(2.5)

(2.0)

(1.5)

(1.0)

(0.5)

0.0

0.5

1.0

1.5

1965 1975 1985 1995 2005 2015Source: U.S. Bureau of Labor Statistics

8.7 Million Lost

12.1 Million Recovered

in 60 months

Payroll GrowthMillions Quarterly

Presented by:

Consumer Spending

-3%

0%

3%

6%

9%

12%

1965 1975 1985 1995 2005 2015

Source: U.S. Bureau of Economic Analysis

through August

Annual Growth

Presented by:

Consumer Spending

‐3%

0%

3%

6%

9%

12%

1965 1975 1985 1995 2005 2015

Source: U.S. Bureau of Economic Analysis

throughAugust

Annual Growth

Presented by:

Source: U.S. Bureau of Economic Analysis

-1%

0%

1%

2%

3%

4%

1960s 1980s 2000s 2011 2013 2015

Net ExportsGovernmentBusiness InventoriesBusiness InvestmentConsumers

Contributions to Inflation‐Adjusted GDP Growth

First Half

Presented by:

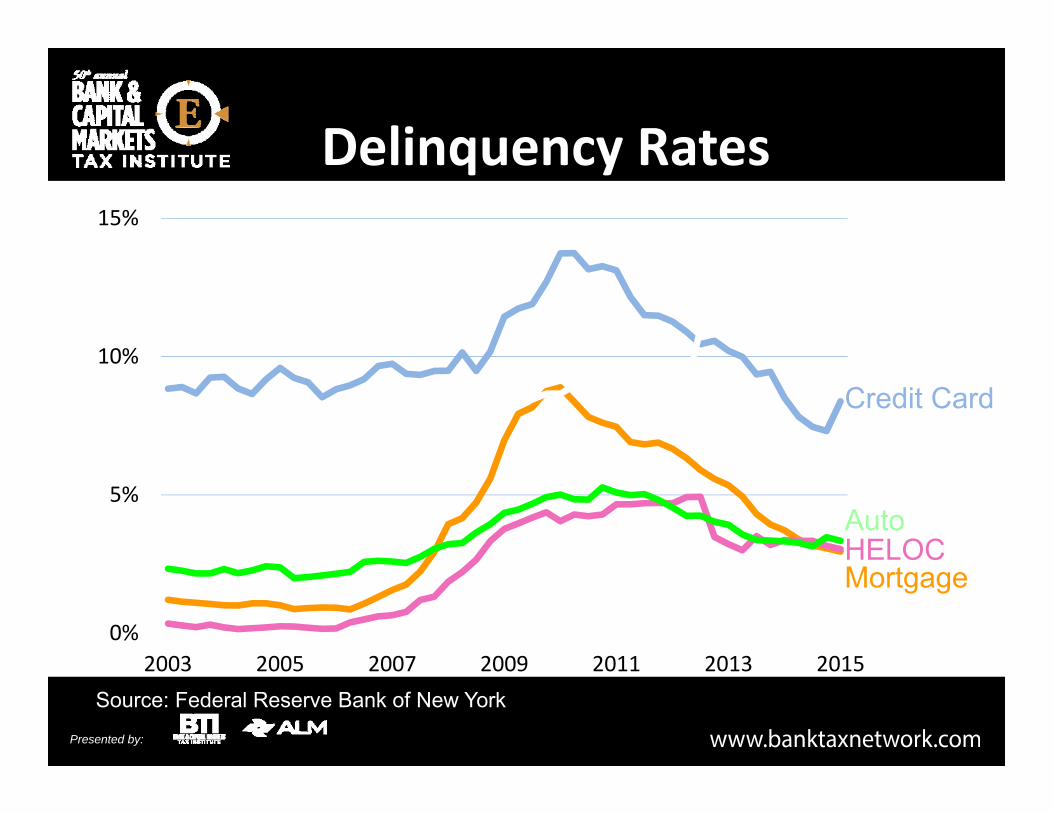

Delinquency Rates

0%

5%

10%

15%

2003 2005 2007 2009 2011 2013 2015Source: Federal Reserve Bank of New York

Mortgage

Credit Card

HELOCAuto

Student

Presented by:

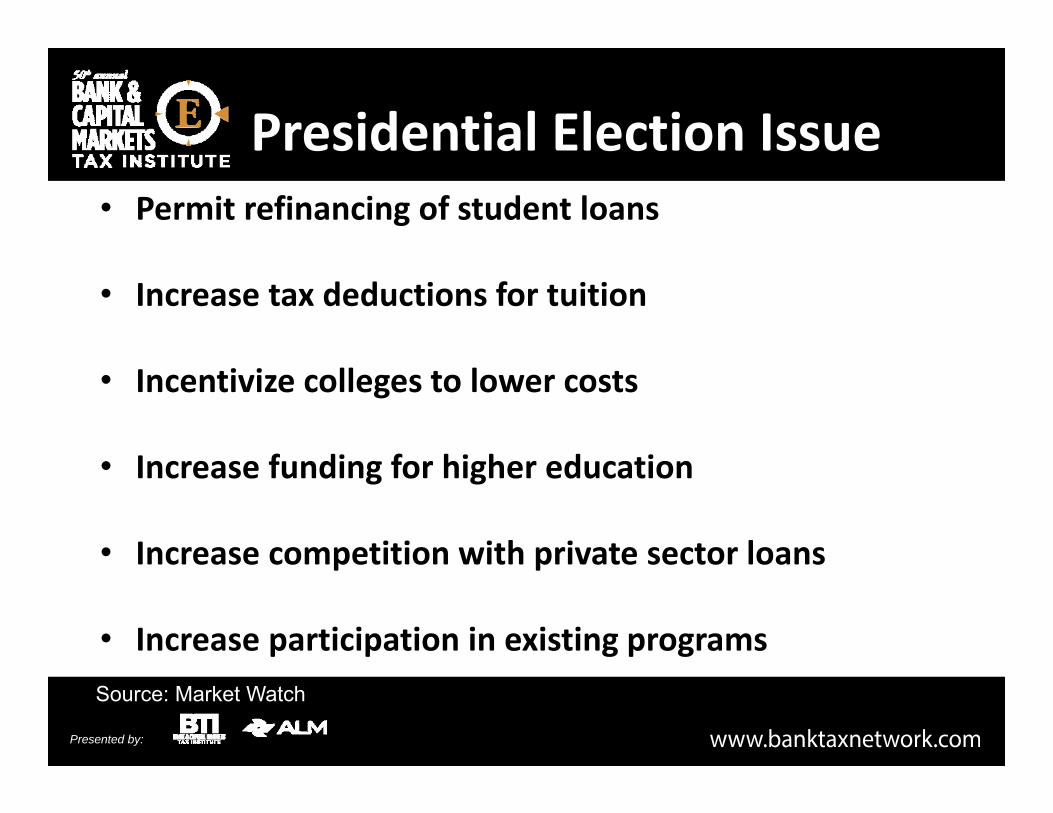

Presidential Election Issue• Permit refinancing of student loans

• Increase tax deductions for tuition

• Incentivize colleges to lower costs

• Increase funding for higher education

• Increase competition with private sector loans

• Increase participation in existing programsSource: Market Watch

Presented by:

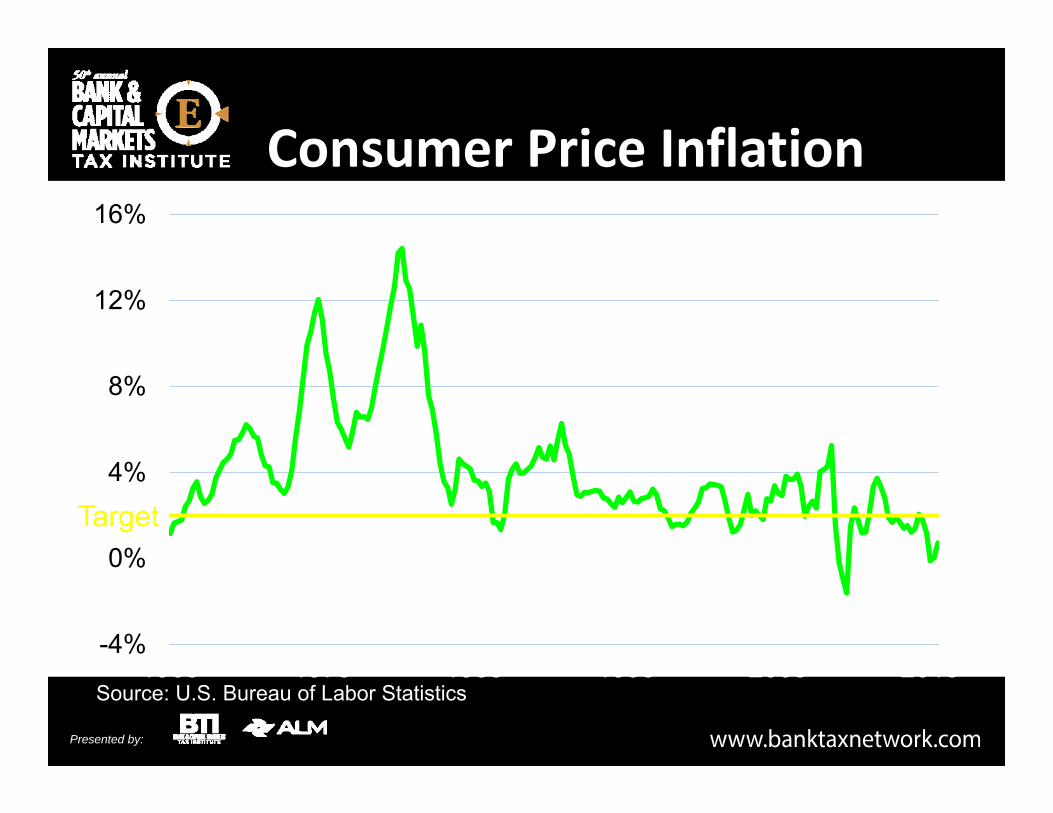

-4%

0%

4%

8%

12%

16%

1965 1975 1985 1995 2005 2015

Target

Source: U.S. Bureau of Labor Statistics

Consumer Price Inflation

Presented by:

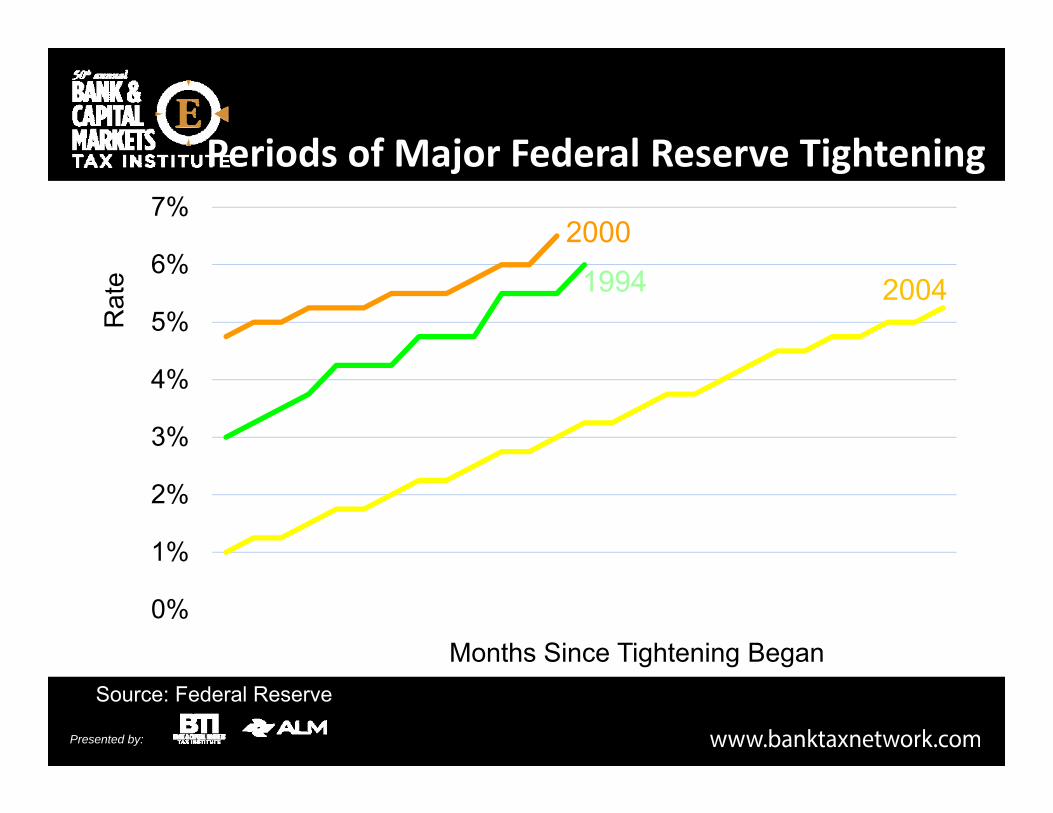

Periods of Major Federal Reserve Tightening

0%

1%

2%

3%

4%

5%

6%

7%

-1 1 3 5 7 9 11 13 15 17 19 21 23 25

Fed

Fund

s Ta

rget

Rat

e

Months Since Tightening Began

1994 2004

2000

Source: Federal Reserve

Presented by:

‐1%

0%

1%

2%

3%

4%

2014 2015 2016 2017 2018

FOMC

Federal Funds Rate Forecast (Year End)

Sources: Federal Reserve (Sept.), Chicago Mercantile Exchange

FF FuturesJuly

October

Presented by:

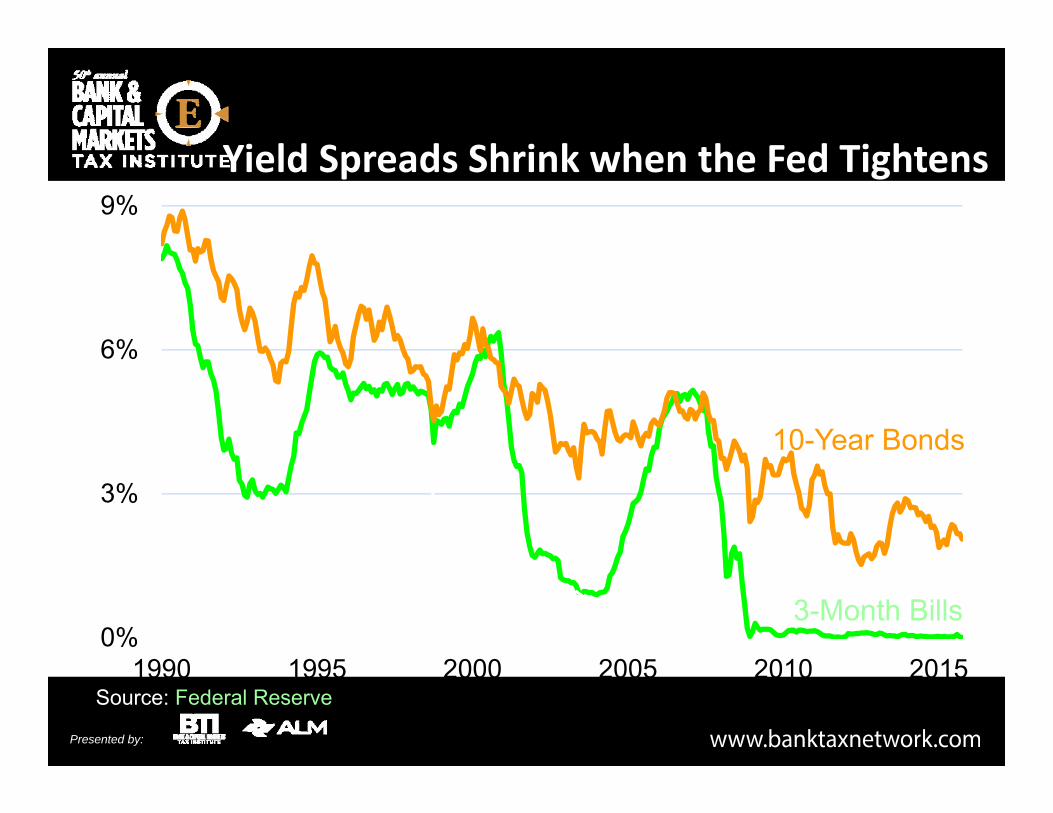

Yield Spreads Shrink when the Fed Tightens

0%

3%

6%

9%

1990 1995 2000 2005 2010 2015

Tightening Began

Source: Federal Reserve

10-Year Bonds

3-Month Bills

Presented by:

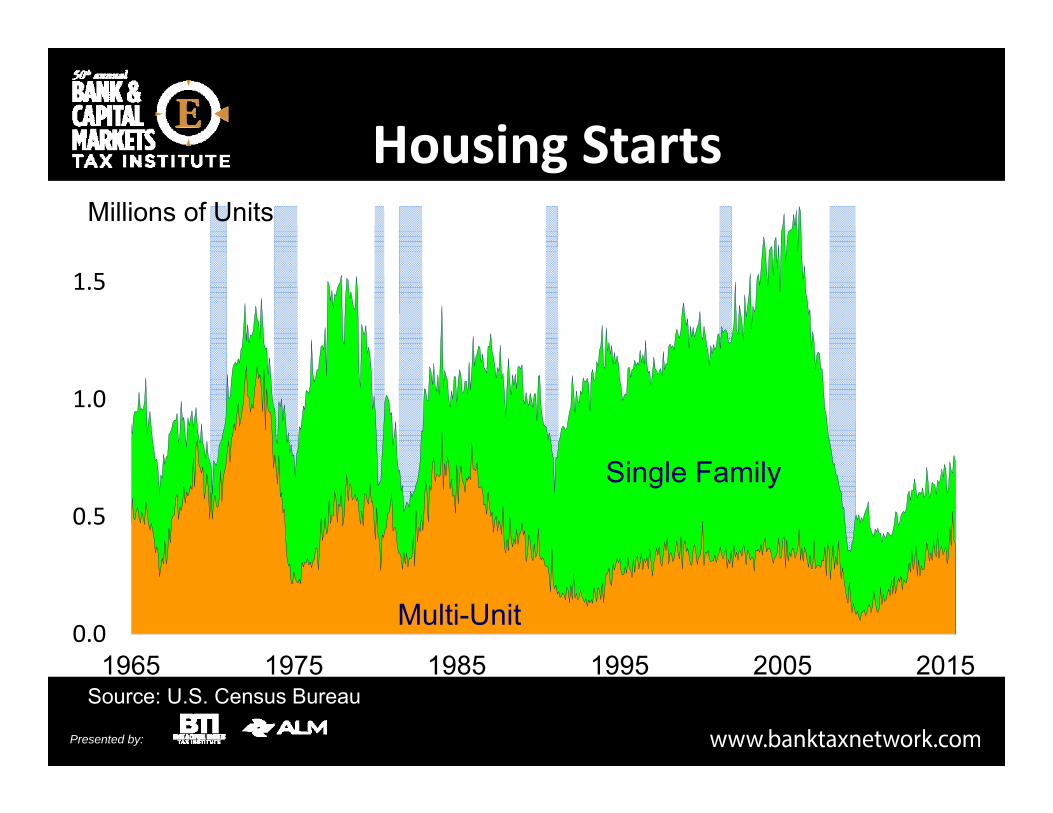

0.0

0.5

1.0

1.5

1965 1975 1985 1995 2005 2015

Housing Starts

Source: U.S. Census Bureau

Millions of Units

Single Family

Multi-Unit

Presented by:

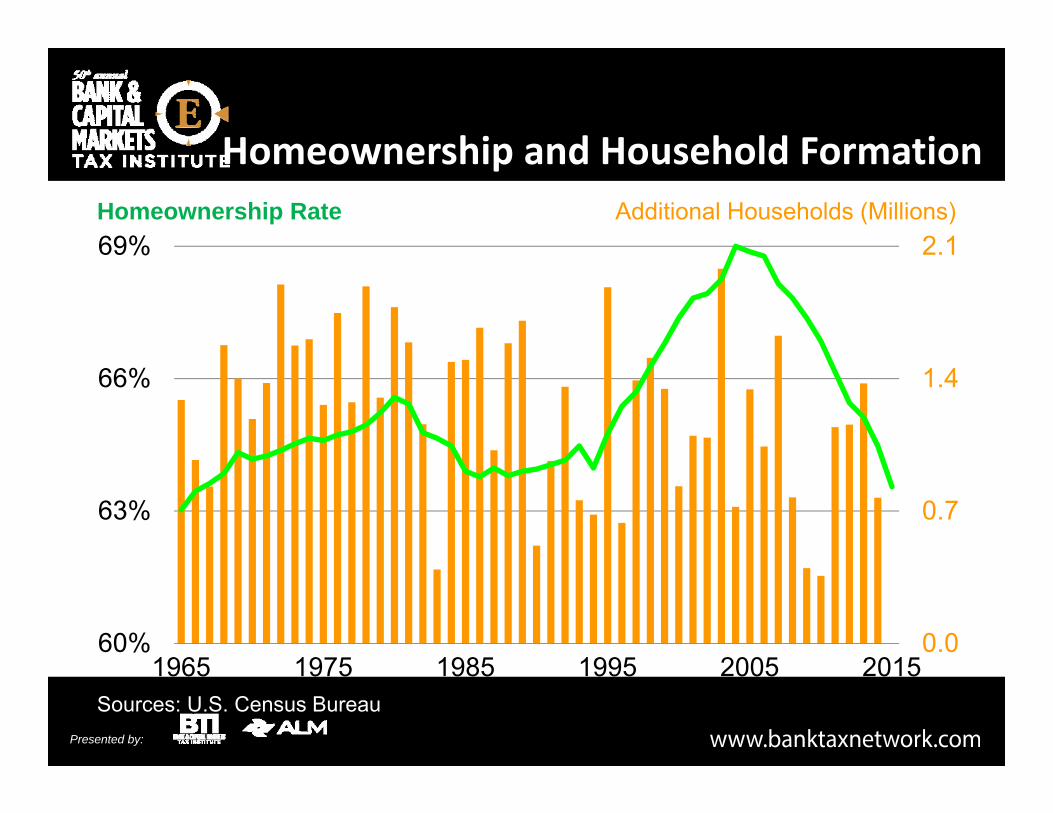

Homeownership and Household Formation

0.0

0.7

1.4

2.1

60%

63%

66%

69%

1965 1975 1985 1995 2005 2015Sources: U.S. Census Bureau

Additional Households (Millions)Homeownership Rate

Presented by:

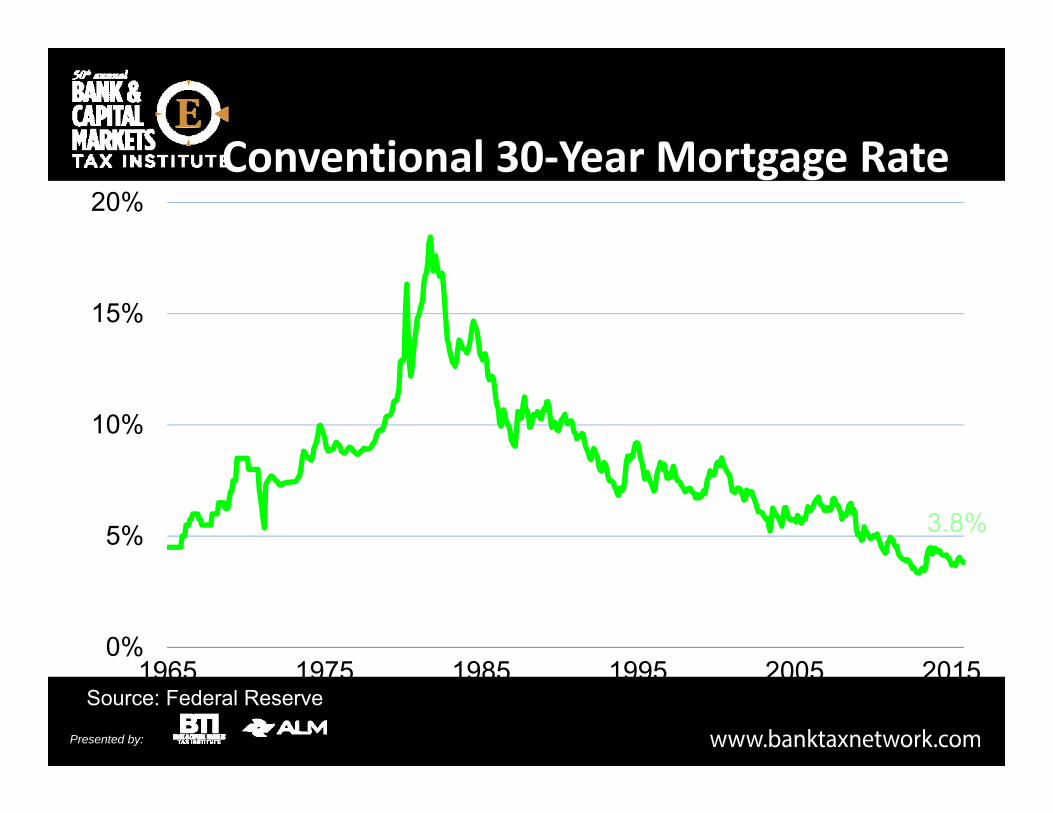

Conventional 30‐Year Mortgage Rate

0%

5%

10%

15%

20%

1965 1975 1985 1995 2005 2015Source: Federal Reserve

3.8%

Presented by:

Home Sales

0

3

6

9

2000 2005 2010 2015

Millions of UnitsSAAR

Sources: U.S. Census Bureau, National Association of Realtors

New Homes

Existing Homes

Presented by:

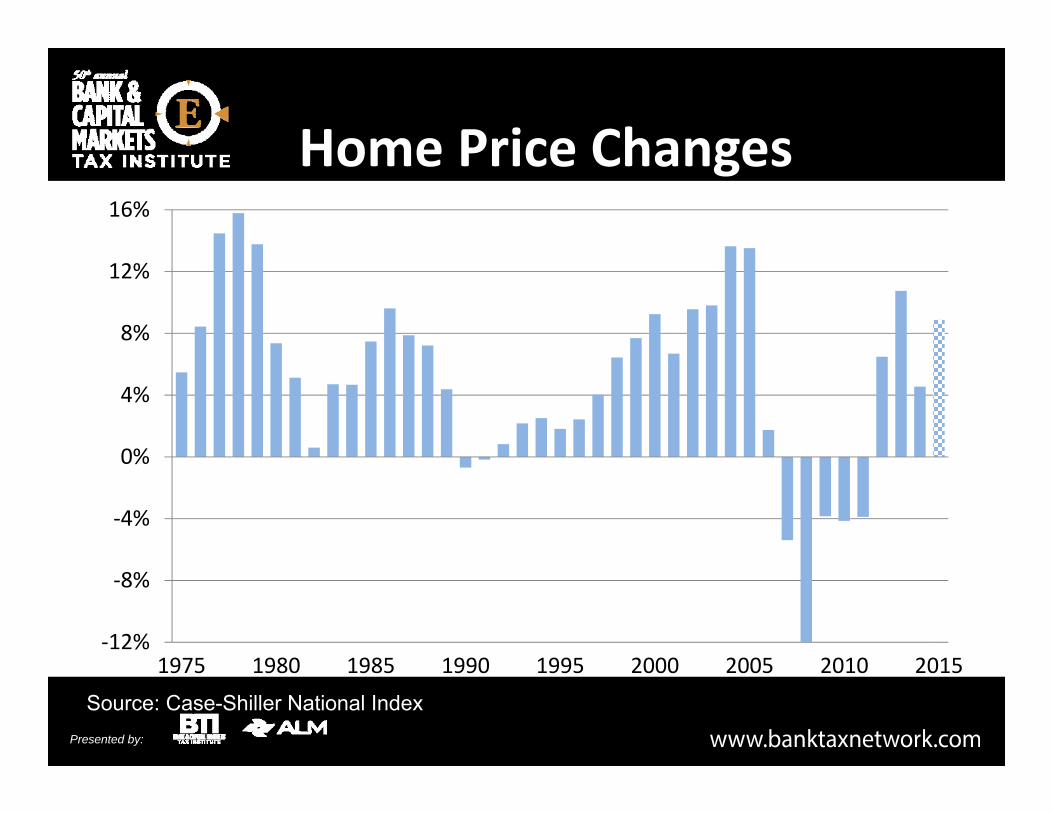

Home Price Changes

‐12%

‐8%

‐4%

0%

4%

8%

12%

16%

1975 1980 1985 1990 1995 2000 2005 2010 2015Source: Case-Shiller National Index

FirstHalf

Presented by:

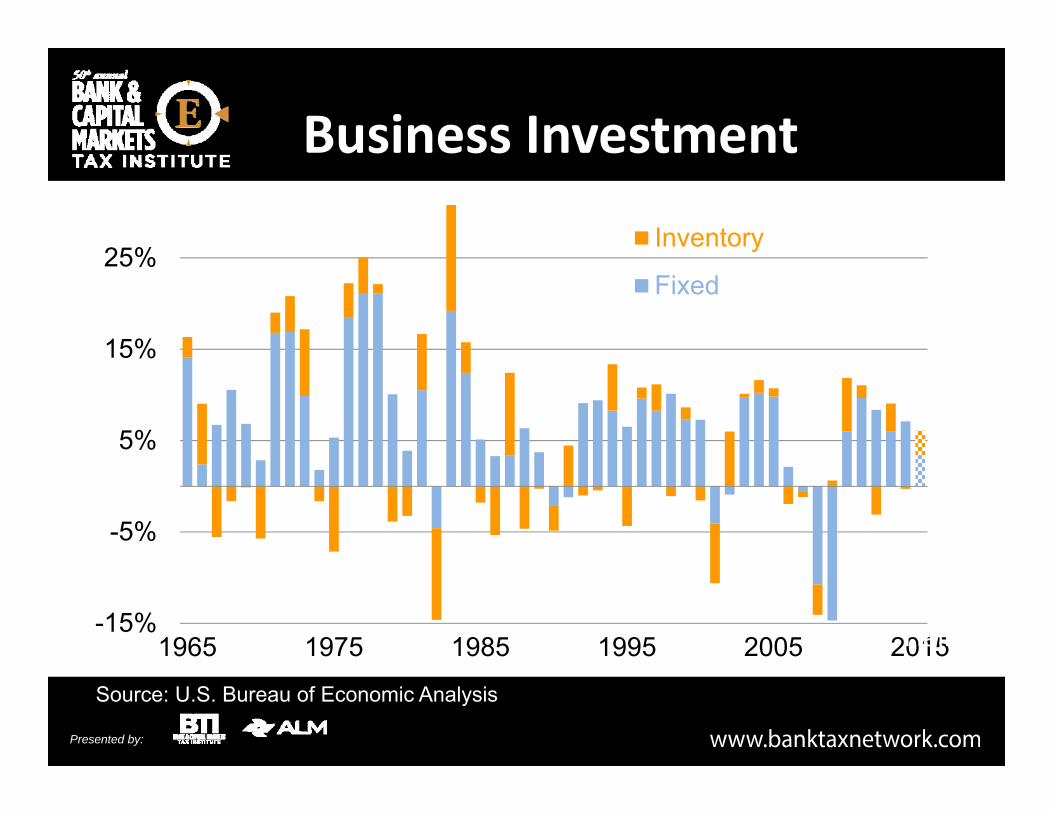

Business Investment

-15%

-5%

5%

15%

25%

1965 1975 1985 1995 2005 2015

Inventory

Fixed

Source: U.S. Bureau of Economic Analysis

FirstHalf

Presented by:

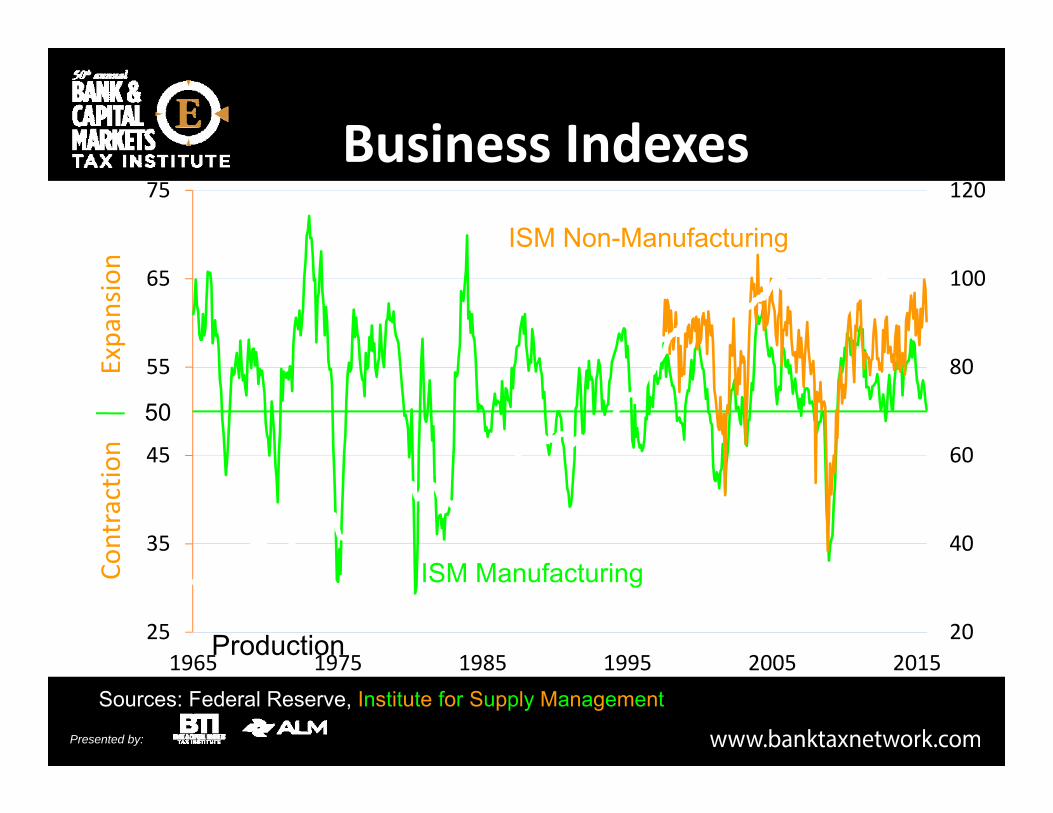

Business Indexes

20

40

60

80

100

120

25

35

45

55

65

75

1965 1975 1985 1995 2005 2015

Industrial Production

Contraction Expansion

ISM Manufacturing

Sources: Federal Reserve, Institute for Supply Management

ISM Non-Manufacturing

50

Presented by:

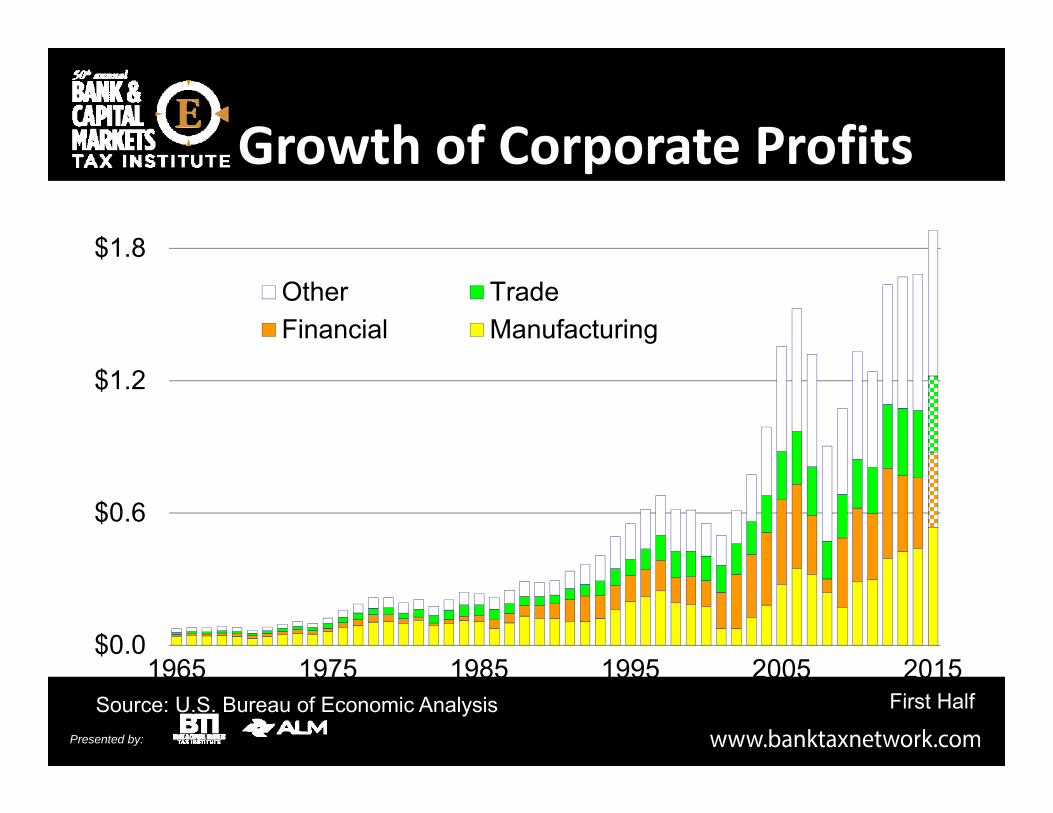

Growth of Corporate Profits

Source: U.S. Bureau of Economic Analysis

$0.0

$0.6

$1.2

$1.8

1965 1975 1985 1995 2005 2015

Other TradeFinancial Manufacturing

With inventory valuation and capital consumption adjustments, SAAR, $Trillions

First Half

Presented by:

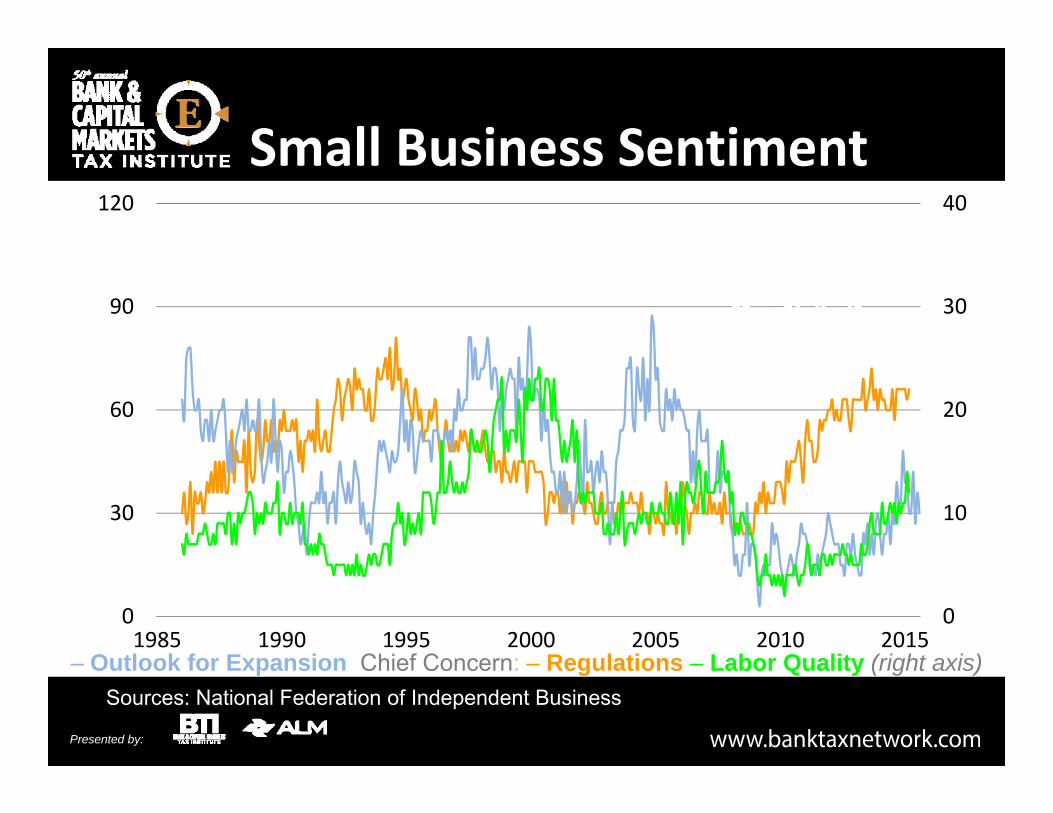

Small Business Sentiment

0

10

20

30

40

0

30

60

90

120

1985 1990 1995 2000 2005 2010 2015

Sources: National Federation of Independent Business

Index of Small Business Optimism (left axis)

– Outlook for Expansion Chief Concern: – Regulations – Labor Quality (right axis)

Presented by:

Labor Productivity Growth

-0.5%

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

1960s 1980s 2000s 2011 2013 2015Source: Bureau of Labor Statistics

FirstHalf

Presented by:

Commercial Real Estate

Source: Green Tree Advisors Commercial Property Price Index

0

30

60

90

120

1998 2000 2002 2004 2006 2008 2010 2012 2014

11.6% Annual Growth Since Mid-2009

Presented by:

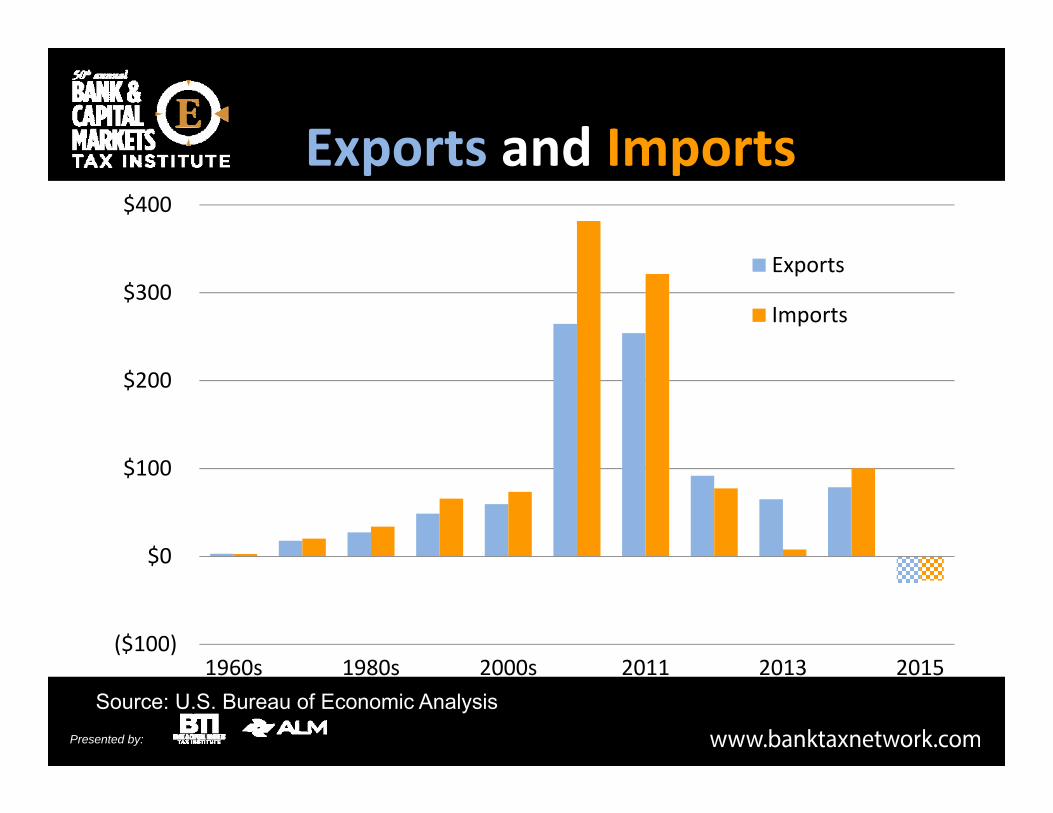

Exports and Imports

($100)

$0

$100

$200

$300

$400

1960s 1980s 2000s 2011 2013 2015

Exports

Imports

Source: U.S. Bureau of Economic Analysis

FirstHalf

Annual ChangeBillions of Dollars

Presented by:

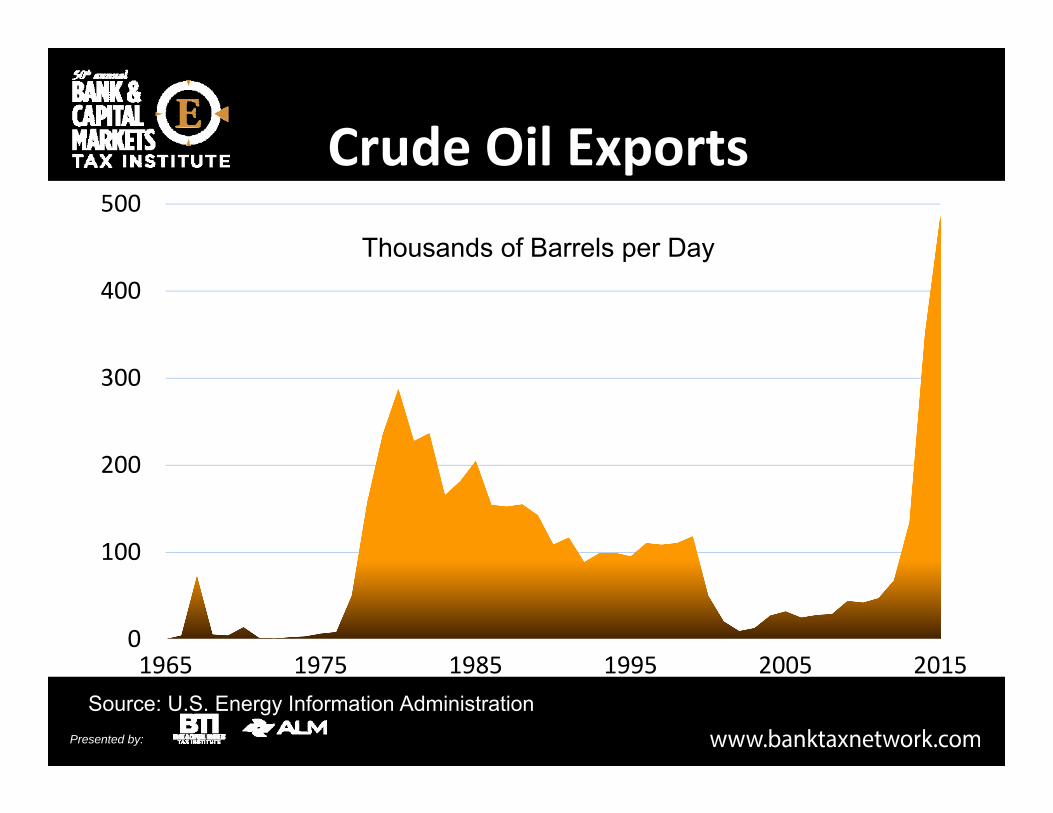

Crude Oil Exports

0

100

200

300

400

500

1965 1975 1985 1995 2005 2015Source: U.S. Energy Information Administration

Thousands of Barrels per Day

Presented by:

Major Currency Trade‐Weighted U.S. Dollar

60

90

120

150

1973 1979 1985 1991 1997 2003 2009 2015Source: Federal Reserve

1973=00

Presented by:

U.S. Exports$248

$172

$134

$82

$56

$33

$32

$19

European Union

Canada

Mexico

China

Japan

South Korea

Brazil

India

All other

U.K. Germ Fra IT

$466Source: U.S. Bureau of Economic Analysis

Billions of Dollars in the First Half of 2015

Presented by:

100

120

140

160

180

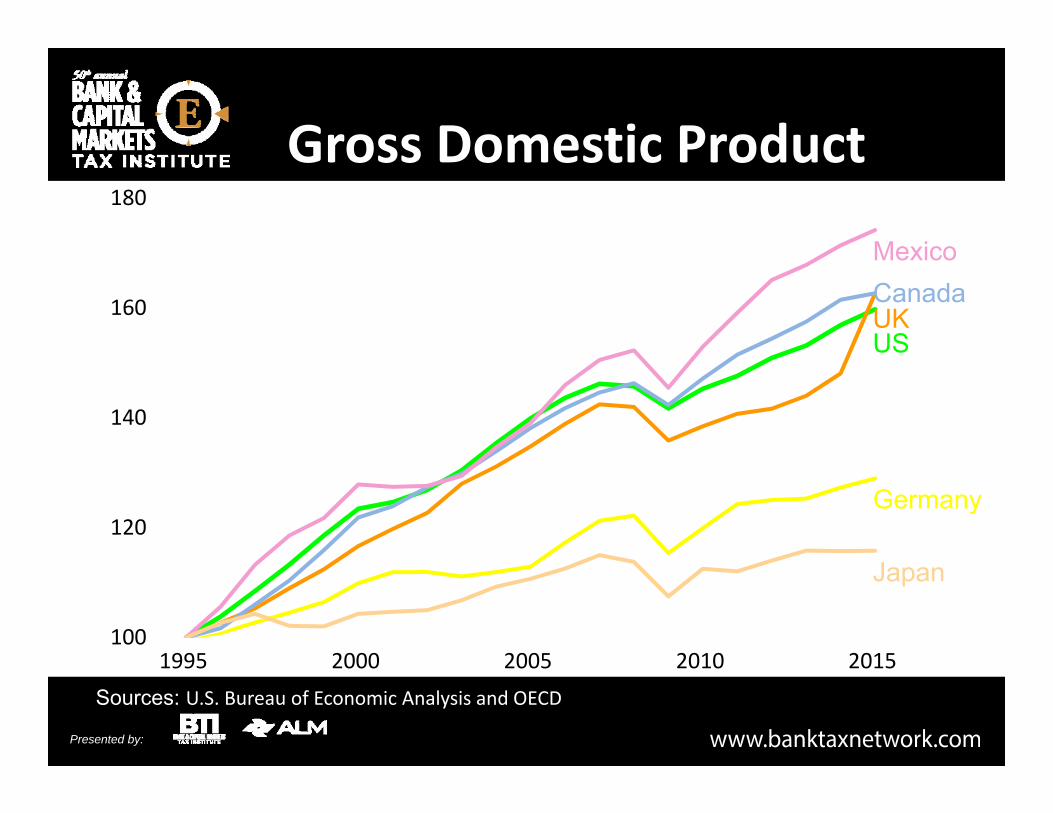

1995 2000 2005 2010 2015

Gross Domestic Product

Sources: U.S. Bureau of Economic Analysis and OECD

Index (1995=100)

US

France

Japan

CanadaMexico

UK

Germany

Presented by:

GDP Growth Slowing in Emerging Nations

0%

3%

6%

9%

12%

Brazil China India South Korea

1960s 1970s 1980s 1990s 2000s 2010s

Source: International Monetary Fund

Presented by:

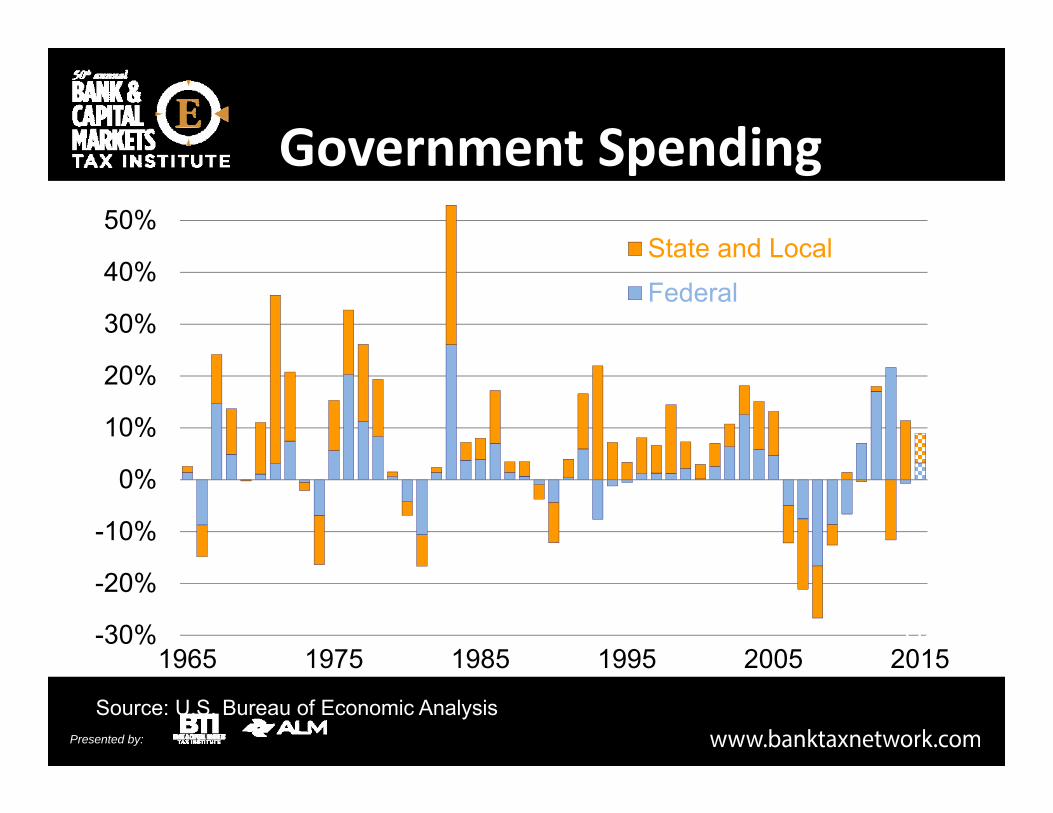

Government Spending

-30%

-20%

-10%

0%

10%

20%

30%

40%

50%

1965 1975 1985 1995 2005 2015

State and Local

Federal

Source: U.S. Bureau of Economic Analysis

FirstHalf

Growth Rate

Presented by:

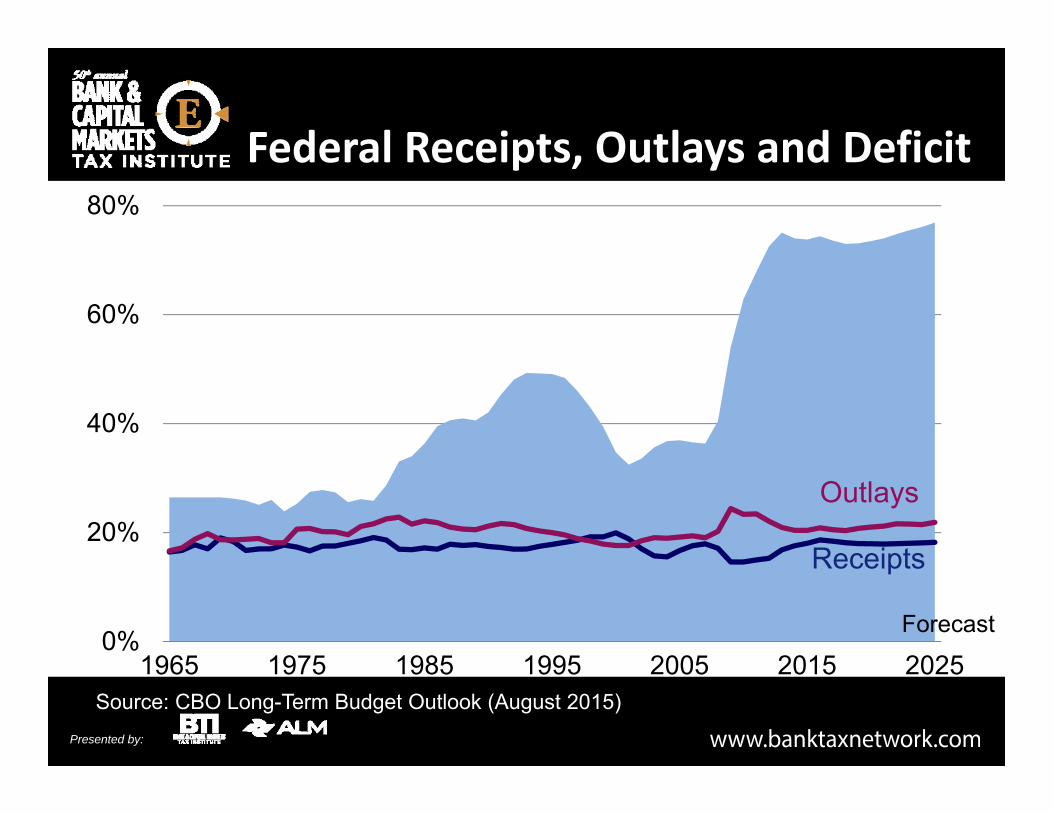

Federal Receipts, Outlays and Deficit

0%

20%

40%

60%

80%

1965 1975 1985 1995 2005 2015 2025

Receipts

Outlays

Forecast

Percent of GDP

Source: CBO Long-Term Budget Outlook (August 2015)

Presented by:

Long‐Term Structural ImbalanceThe long‐term fiscal problem cannot be solved by:

• a growing economy,

• eradicating fraud, waste and abuse,

• pulling U.S. troops out of the Middle East and cutting defense,

• restraining discretionary spending, and

• eliminating Congressional earmarks.

Source: U.S. Congressional Budget Office

Presented by:

Conclusion: Stress Points• Concentration of Income and Wealth• Fed Lift‐off and Interest Rates• Housing Recovery• Student Debt• Business Capital Formation• Foreign Economies• Government Finances

Presented by:

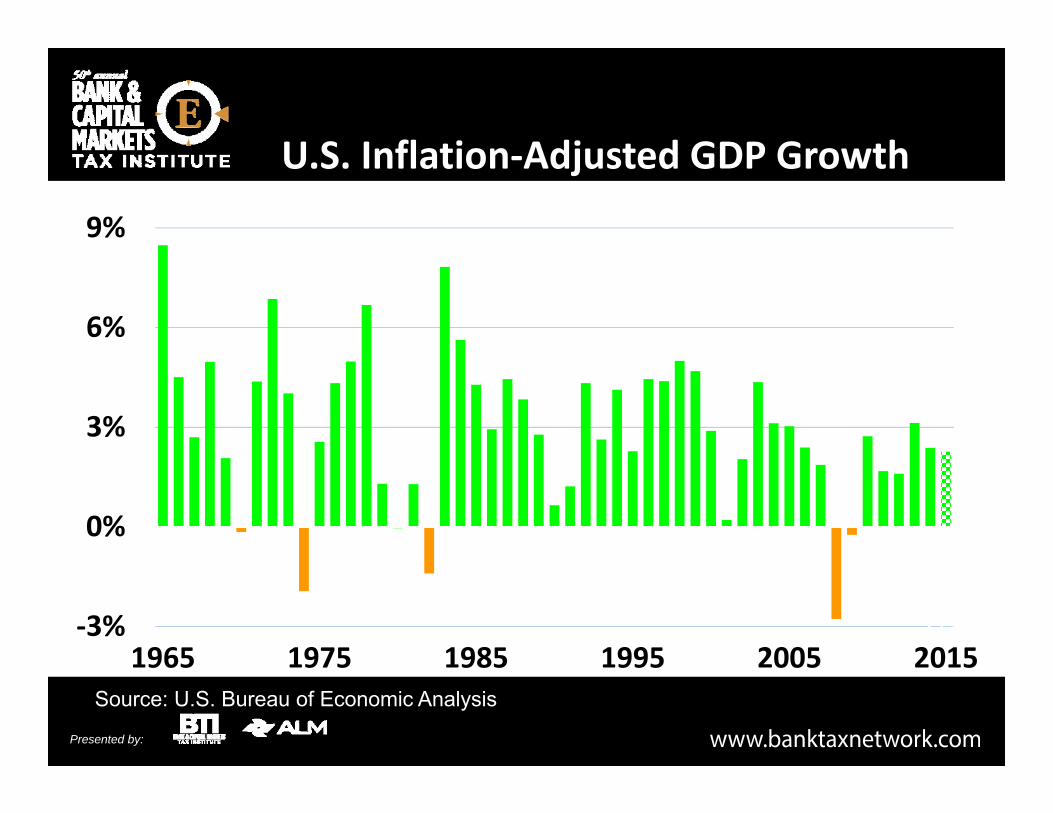

U.S. Inflation‐Adjusted GDP Growth

‐3%

0%

3%

6%

9%

1965 1975 1985 1995 2005 2015Source: U.S. Bureau of Economic Analysis

FirstHalf

Presented by:

0

500

1000

1500

2000

2005 2007 2009 2011 2013 2015

S&P 500 Index

Source: Standard & Poor’s

Up 164%in 6½ years

Presented by:

U.S. Traditional Advantages• Highly diverse economy

• Robust entrepreneurial culture

• Flexible capital and labor markets

→ Technological leader

→ Strong global competitor

Presented by:

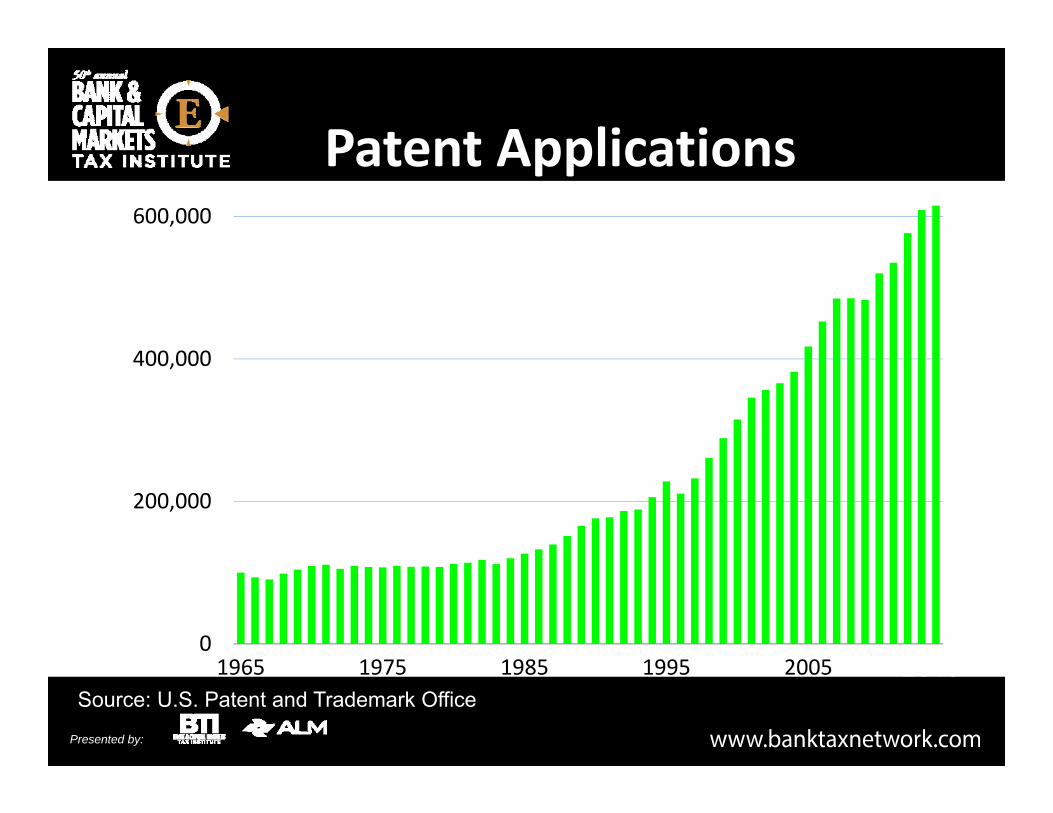

Patent Applications

0

200,000

400,000

600,000

1965 1975 1985 1995 2005Source: U.S. Patent and Trademark Office

2015

Presented by:

Related Documents