Broadband Study and Action Plan for CONNECT NW PA Supplemental Report Creating Optimum Networks n Expanding Connectivity to North west PA A Broadband Project of the Northwest Pennsylvania Regional Planning & Development Commission Submitted December 23, 2003 Spotts, Stevens and McCoy, Inc. 1047 North Park Road Reading, PA 19610-0307 Tel: 610.621.2000 Fax: 610.621.2001 www.ssmgroup.com Icon Broadband Technologies 6745 Bells Ferry Road Woodstock GA 30189 Tel: 770.592.9797 © Copyright Spotts, Stevens and McCoy, Incorporated 2003. Fax: 770.592.7363 All rights reserved www.iconbroadband.com

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Broadband Study and Action Plan for CONNECT NW PA

Supplemental Report

Creating Optimum Networks n Expanding Connectivity to Northwest PA

A Broadband Project of the Northwest Pennsylvania Regional

Planning & Development Commission

Submitted December 23, 2003

Spotts, Stevens and McCoy, Inc. 1047 North Park Road

Reading, PA 19610-0307 Tel: 610.621.2000 Fax: 610.621.2001

www.ssmgroup.com

Icon Broadband Technologies 6745 Bells Ferry Road Woodstock GA 30189

Tel: 770.592.9797 © Copyright Spotts, Stevens and McCoy, Incorporated 2003. Fax: 770.592.7363 All rights reserved www.iconbroadband.com

Northwest Pennsylvania Regional Planning & Development Commission CONNECT NW PA Broadband Supplemental Report - Preliminary Draft

Table of Contents Main Report-Overview for All Eight (8) Counties………………………………......Sections 1-8 Supplemental Report-Additional Case Studies and Data by County………............Sections 9-10

Section 9: Additional Case Studies.....................................................................................114

Case Studies Utilizing Various Types of Business Models............................................................. 114

Section 10: Additional Exhibits ............................................................................................126 Demographics Data for Pennsylvania and by County .................................................................... 126

Pennsylvania Data.............................................................................................................................................................126 County Data .......................................................................................................................................................................140 Clarion County ..................................................................................................................................................................142 Crawford County...............................................................................................................................................................150 Erie County ........................................................................................................................................................................158 Forest County.....................................................................................................................................................................166 Lawrence County..............................................................................................................................................................174 Mercer County...................................................................................................................................................................182 Venango County................................................................................................................................................................190 Warren County ..................................................................................................................................................................198

Economic Development Initiatives Data by County ...................................................................... 206 Clarion County ..................................................................................................................................................................206

Table 10-A: Clarion County Development Initiatives...............................................................................................207 Crawford County...............................................................................................................................................................208

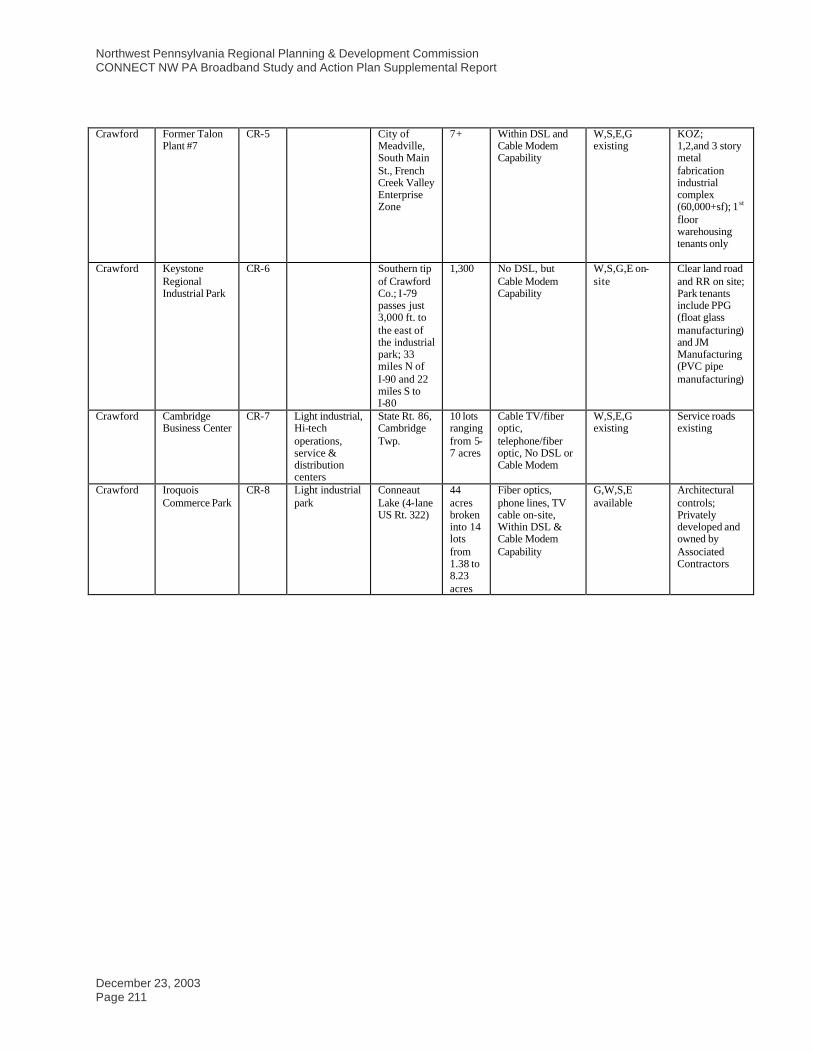

Table 10-B: Crawford County Development Initiatives ...........................................................................................210 Erie County ........................................................................................................................................................................212

Table 10-C: Erie County Development Initiatives....................................................................................................215 Figure 10-A: Erie County 2030 Transportation Plan-Highway Network...................................................................217 Figure 10-B: Erie County 2030 Transportation Plan-Erie Urban Area ......................................................................218 Figure 10-C: Erie County-Keystone Zones ................................................................................................................219 Figure 10-D: Erie County-Wide Enterprise Zone Program ........................................................................................220 Figure 10-E: Erie County Plans for Land Use & Community Facilities ....................................................................221 Figure 10-F: Erie County Composite Local Zoning Districts....................................................................................222

Forest County.....................................................................................................................................................................223 Table 10-D: Forest County Development Initiatives.................................................................................................226

Lawrence County..............................................................................................................................................................227 Table 10-E: Lawrence County Development Initiatives...........................................................................................228

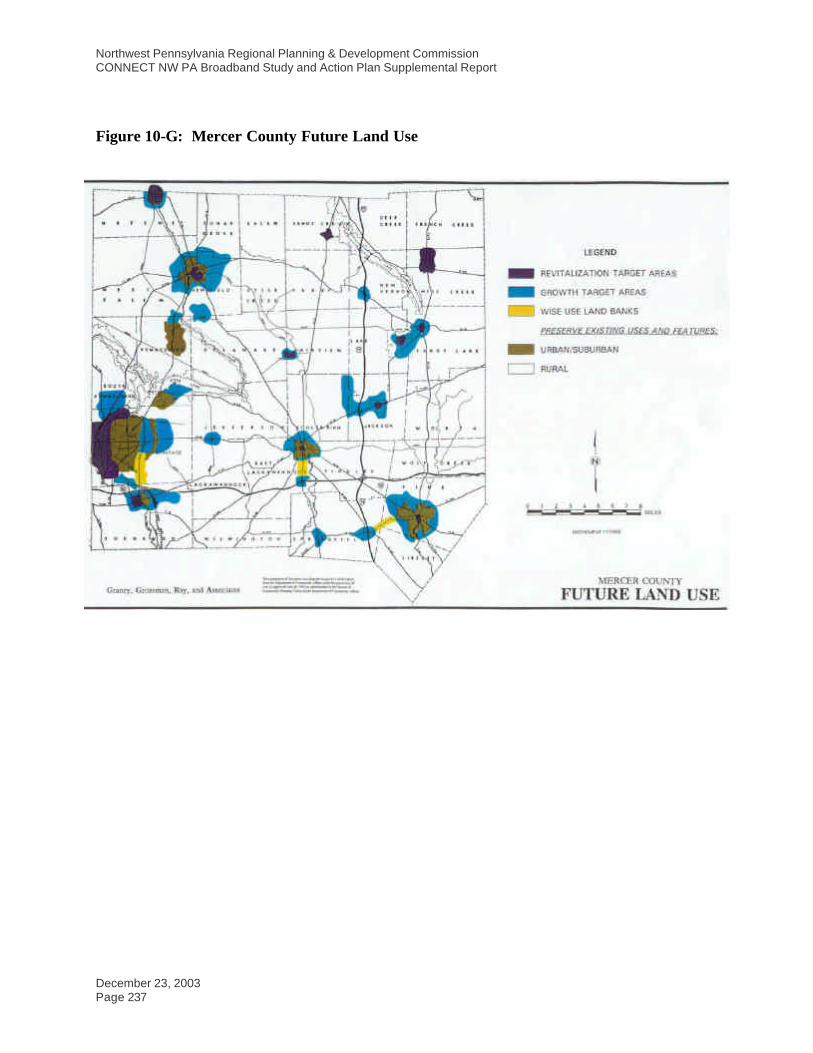

Mercer County...................................................................................................................................................................230 Table 10-F: Mercer County Development Initiatives ...............................................................................................235 Figure 10-G: Mercer County Future Land UseVenango County................................................................................237

Venango County.............................................................................................................................................................. 238 Table 10-G: Venango County Development Initiatives ............................................................................................239

Warren County ..................................................................................................................................................................240 Table 10-H: Warren County Development Initiatives...............................................................................................242

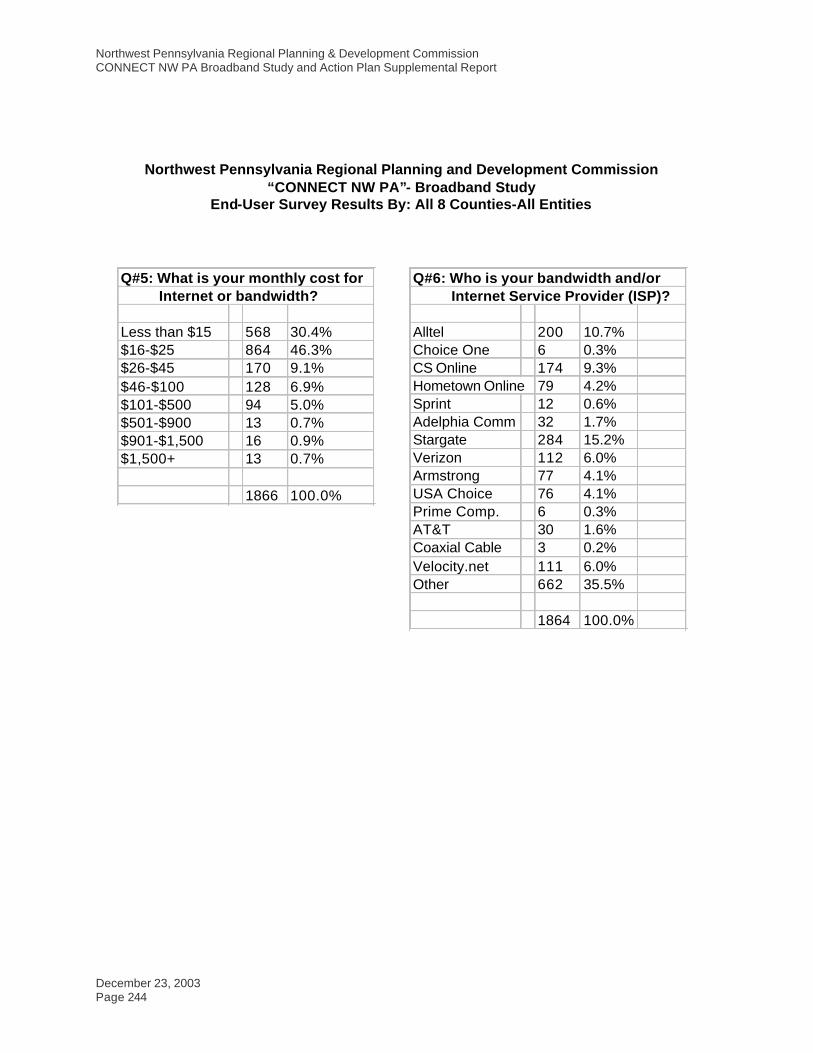

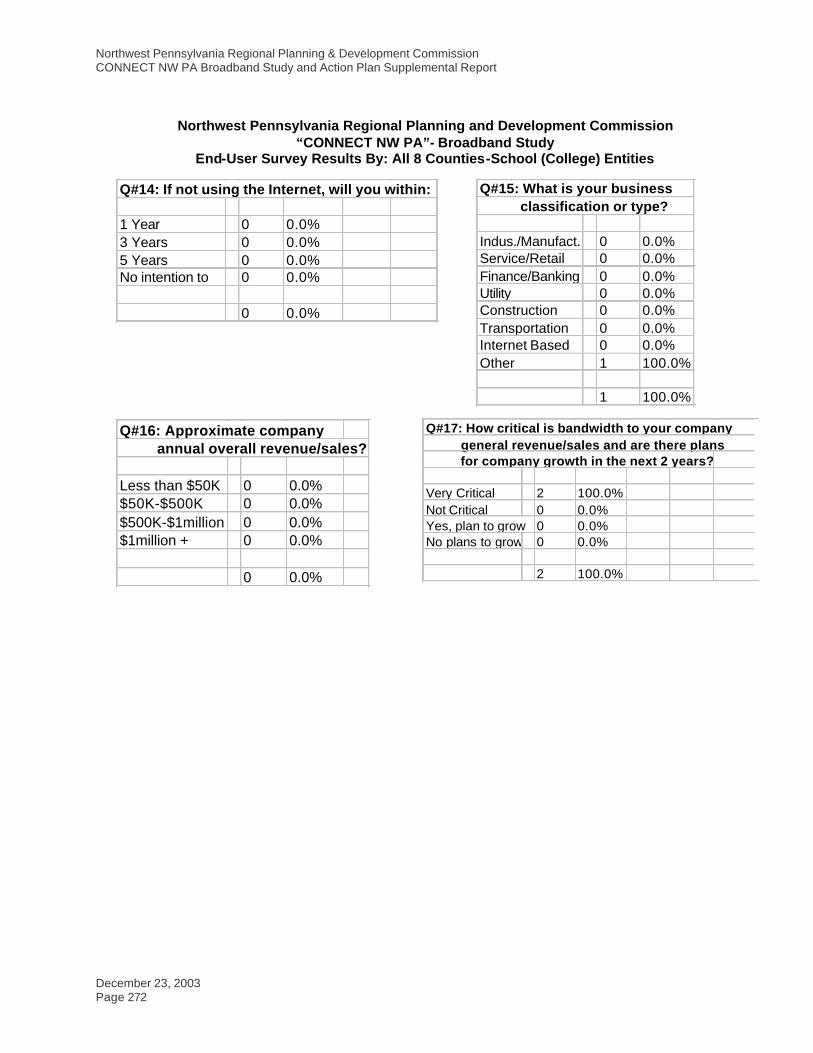

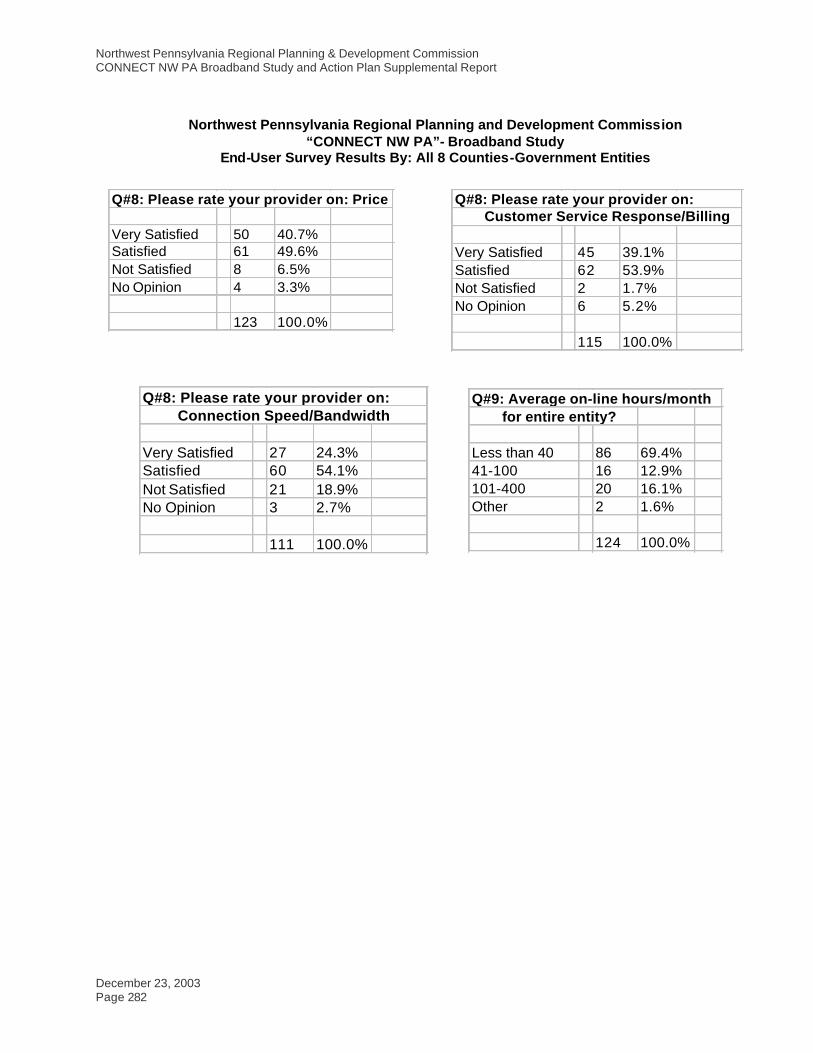

End-User Survey Response Data ................................................................................................. 243 Table 10-I: End-User Survey By: All 8 Counties – All Entities..............................................................................243 Table 10-J: End-User Survey By: All 8 Counties – Residential Entities .................................................................249 Table 10-K: End-User Survey By: All 8 Counties – Business Entities.....................................................................255 Table 10-L: End-User Survey By: All 8 Counties School (K-12) Entities ...............................................................261 Table 10-N: End-User Survey By: All 8 Counties Nonprofit Agency Entities.........................................................273 Table 10-O: End-User Survey By: All 8 Counties – Government Entities...............................................................279 Table 10-P: End-User Survey By: All 8 Counties – Health Care Facility Entities...................................................285 Table 10-Q: End-User Survey By: All 8 Counties – Other Entities.........................................................................291

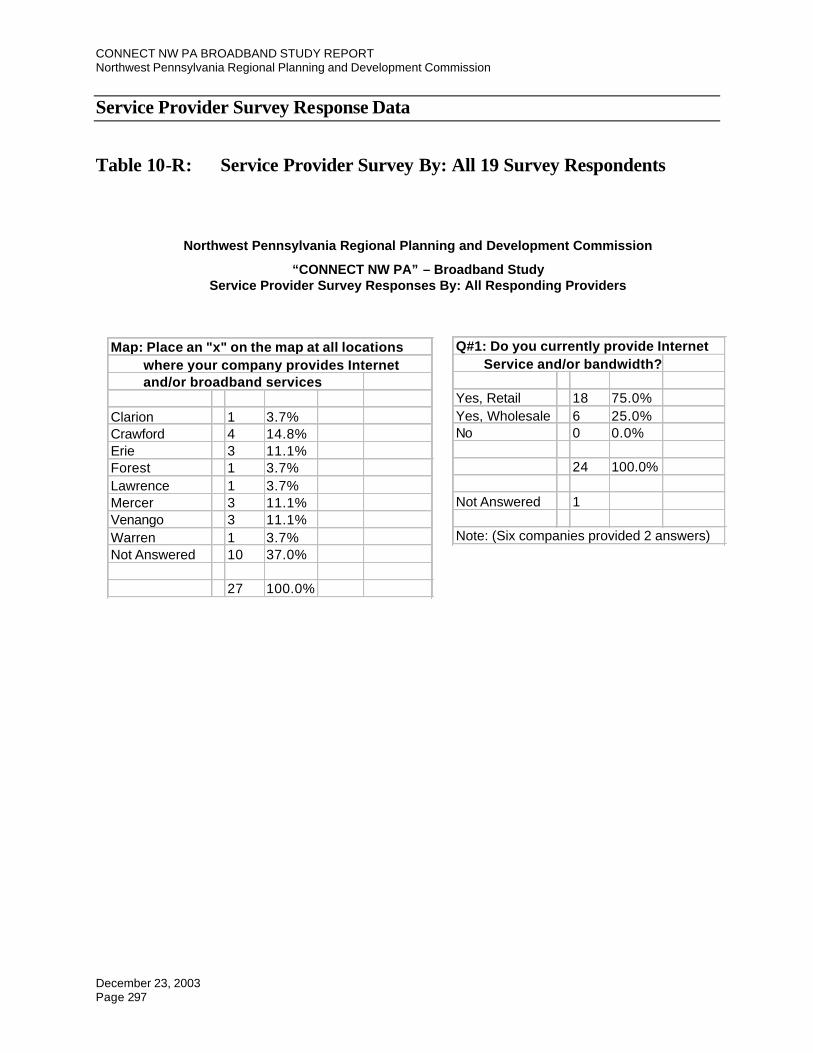

Service Provider Survey Response Data....................................................................................... 297 Table 10-R: Service Provider Survey By: All 19 Survey Respondents ...................................................................297

USGS Maps ............................................................................................................................... 307 Figures 2-E, 2-F, 2-G, and 2-H (Located at end of Supplemental Report)......................................................................307

Northwest Pennsylvania Regional Planning & Development Commission CONNECT NW PA Broadband Study and Action Plan Supplemental Report

December 23, 2003 Page 114

Section 9: Additional Case Studies

Case Studies Utilizing Various Types of Business Models

Big Sandy Telecommunications Center

Project Location: Pikeville, Kentucky Grant Recipient: Big Sandy Telecommuting Services, Inc./Pikeville College Total ARC Funding: $553,530 Total Matching Funds: $1,105,106

Prior to the ARC grant, very few businesses or residents in the Pikeville region had Internet access. In fact, there was no Internet service provider (ISP) in the region at the time the grant recipient applied for ARC funds. In addition to the lack of an ISP, most businesses and residents in Pikesville lacked access to training in the latest computer software programs. Given its isolated setting, there was also a desire to use the Internet and other forms of telecommunications technology, such as videoconferencing, to link schools, businesses, and community leaders with other communities in eastern Kentucky.

This project was primarily designed to provide a range of services to the businesses and residents of the five counties in the Big Sandy region of Kentucky. These included serving as an ISP, providing training and technical support in the use of the Internet and software, and building a telecommunications access site equipped with computers and videoconferencing equipment. Although the original ARC grant was designed to support a wide range of activities, much of the effort focused on establishing and maintaining the community's only ISP.

In serving as the region's first ISP, the project connected over 750 customers to the Internet. In addition, through the project’s training and telecommunications acquisitions, community businesses, educational institutions, and residents were exposed to new and emerging technologies. While this might have occurred without the ARC project, many felt that the ARC project accelerated this process. There are now 4-6 ISPs in the region, which are staffed or managed by people who received training or were exposed to the Internet through the project. In addition, the entire Big Sandy area was recently upgraded with a fiber optic backbone, which would not have been possible if not for the ARC grant and the resulting use of the Internet throughout the region.

Over the life of the ARC grant, over 700 people participated in classes on computer skills and applications. Because of the project, these professionals were able to take advantage of continuing education opportunities without leaving the community. People who attended BSTSI training are now employed in numerous businesses and educational institutions practicing the skills learned at BSTSI. Finally, the region has experienced increases in business productivity and job security, and several businesses had located in the region in part because they were able to find employees who had computer skills obtained through BSTSI.

Northwest Pennsylvania Regional Planning & Development Commission CONNECT NW PA Broadband Study and Action Plan Supplemental Report

December 23, 2003 Page 115

Medical and Government Internet Coalition Network (MAGICNET)

Project Location: Athens, Ohio Grant Recipient: Ohio University Total ARC Funding: $77,167 Total Matching Funds: $149,168

The primary goal of the Medical and Government Internet Coalition Network (MAGICnet) was to provide rural physicians and government officials access to "local services, state resources, and global connectivity" through the Internet. Toward this end, Ohio University’s College of Osteopathic Medicine (COM) and Institute for Local Government Administration and Rural Development (ILGARD) provided project participants with hardware, software, training, implementation assistance, and one year's worth of Internet access. COM and ILGARD also assisted local Internet service providers (ISPs) in expanding their service to underserved areas of southeast Ohio.

Project participants have taken advantage of the capacity-building opportunities made possible through the MAGICnet project. Sites have been able to institute computerized billing systems, saving time and money. Internet access has provided sites with access to a wealth of information, such as inter- library loan services for physicians and federal and state grant opportunities for government sites. Members of the community have received better service as a result. Physicians can access patient education materials online and print and disseminate them to their patients. Government officials can provide services in a timelier manner and can use technology to gain information, which makes their grant applications more competitive. The ISP situation has changed dramatically as well, with more competing ISPs and choices for service.

Recognizing the impact of technology, many sites have taken the initiative to upgrade their equipment and expand their vision of how they can use technology. As an example, some local governments have expressed an interest in learning Geographic Information Systems (GIS), which can be used for resource management and community planning and development.

N-Logue’s Rural Connectivity Model

Although among the top 10 largest networks in the world and the third largest among developing countries, India currently has only a teledensity of 2.5 per 100 persons (1). With development resources directed primarily towards the urban areas, rural populations conceal a strong latent demand for connectivity and communication access. Yet rough terrain, absent or decaying infrastructure, dispersed populations, and low per-capita incomes continue to ward off both public and private sector investment.

Business Model - Where others see obstacles, Indian start-up n-Logue Communications sees opportunity. N-Logue has created a for-profit business model to tap into this latent rural demand for connectivity. N-Logue was incubated by the Telecommunications and Computer Network (TeNet) Group of the Indian Institute of Technology in Madras as part of the institute's strategy for developing and disseminating innovative, affordable communication technologies to the rural

Northwest Pennsylvania Regional Planning & Development Commission CONNECT NW PA Broadband Study and Action Plan Supplemental Report

December 23, 2003 Page 116

poor of developing countries. N-Logue has fashioned a franchise-based business model that consists of three levels of interdependent networks. At the foundation- level, n-Logue forges and facilitates relationships among a wide-range of organizations—hardware and equipment providers, non-governmental organizations, content providers, and government—that enable and support the businesses of franchise owners. At the next level, n-Logue maintains a regional network of franchised Local Service Partners (LSP). The LSP works in tandem with n-Logue to set up an Access Center or node to which individual kiosk operators will be connected. At the highest level of the business model, local entrepreneurs are recruited by the LSP to establish village-level kiosk franchises that provide Internet and telephone access to the local population. Through the LSP, n-Logue offers low-priced "kiosk packages" consisting of a subscriber wall set (that connects the kiosk to the Access Center), a computer, printer and backup battery. The kiosks essentially function as combination rural Internet cafes and pay phone booths. While n-Logue provides kiosk owners with training, support, and technical assistance, local franchise owners themselves are responsible for developing additional product and service offerings (e.g., computer courses) and marketing strategies.

Infrastructure - N-Logue employs a unique, TeNet-designed Wireless Local Loop technology as the basis for its village- level communications package. This CorDECT technology consists of a fixed wireless local loop (WLL). CorDECT operates on the same principles as regular wireless technology with voice and data communication moving through radio frequency rather than wires. With WLL a fixed unit emits the originating signal. The CorDECT system provides voice, voice band FAX/DATA transfer and Internet connectivity at 35-70 Kbps to 1 Gbps when digitized. The subscriber wall set (WS-IP) can transmit both voice and data signals simultaneously to an access center, which must be located within a 25km line of sight distance. CorDECT technology effectively and inexpensively addresses the problems of distance and lack of infrastructure in rural areas. Installing a fixed wireless local loop does not require expensive digging, and the system consists of only 4 major components. Because the central base station/ direct interface unit (CBS/DIU) handles traffic from 200-1000 subscribers, it works ideally in small, dispersed markets and does not require the large subscriber base that traditional landline or cellular systems require for profitability. This low infrastructure investment, combined with low usage costs, makes the proposition affordable both for suppliers and customers in capital-constrained economies. Human Capacity - N-Logue offers training and business advisory services to its franchisees at the kiosk and LSP level. To find qualified kiosk operators, it has drawn from the large pool of graduates from India's many technical/computer institutes. It has been less successful in recruiting entrepreneurs at the LSP level, but recently has restructured and accelerated that process. N-Logue's own management consists of mature executives with extensive experience in the telecommunications sector and in sales, marketing, and business development for multinationals and blue chip Indian companies.

Northwest Pennsylvania Regional Planning & Development Commission CONNECT NW PA Broadband Study and Action Plan Supplemental Report

December 23, 2003 Page 117

Enterprise - The following factors enhance the sustainability of n-Logue's business model: « income generation at the local level « cost effective technology « decentralized organizational structure « local adaptability « local accountability

To implement its model, n-Logue has forged partnerships with an impressive network of organizations and entrepreneurs. To gain access to the long-haul telephone network and Internet backbone, n-Logue has negotiated relationships with BSNL, the former Department of Transportation monopoly, and Satyam Infoway, India's primary bandwidth provider. To facilitate entrepreneurs' access to capital, it has partnered with financial institutions such as the National Bank of Agriculture and Rural Development (NABARD) and Indian Bank. It has overcome the barrier of expensive hardware through its relationships with IIT incubated R&D and manufacturing companies and by obtaining volume discounts with suppliers. N-Logue's partnerships with entrepreneurs form the crux of its business. Local service providers (LSPs), who are usually established businesspeople or district governments, maintain access centers and recruit kiosk operators. LSPs provide training, business advisory services, and collect the revenues from the kiosk operators, which are then passed on to n-Logue. Kiosk operators develop and market their own business offerings. To date, most kiosk operators have generated the largest portions of their revenue from net-based services, computer education and job work.

Key Lessons - N-Logue's success in its pilot phase and the headway it has made towards resolving national and regional licensing and regulatory issues can be attributed to the strong relationships it established with influence makers, governments, other businesses and entrepreneurs. It has leveraged these relationships to overcome a host of obstacles ranging from capital constraints to expensive hardware to lack of relevant content. The company will need strong infusions of cash to meet its growth projections. Fortunately it has many of the other necessary inputs for growth in place. The enthusiastic response to the business opportunity of kiosk ownership and the innovation kiosk operators have demonstrated in developing their businesses have exceeded the most optimistic expectations of n-Logue managers. By developing a business that is locally adaptable and locally accountable, n-Logue has positioned itself to successfully tap into an enormous latent demand for connectivity in rural India.

Buffalo, Minnesota

Buffalo, Minnesota, a growing town of 12,000, decided to install a control and data acquisition system for its electric utility, so adding a few more strands of fiber for data transmission seemed an easy option for broadband connectivity for the community. However, demand suddenly

Northwest Pennsylvania Regional Planning & Development Commission CONNECT NW PA Broadband Study and Action Plan Supplemental Report

December 23, 2003 Page 118

increased from both residential and business users in the area. Since 90 percent of those in demand were not on the planned fiber route, and extending fiber to them was far too costly for the town to absorb, Buffalo decided to find another way to reach those demanding service.

Buffalo partnered with wireless equipment provider WaveRider Communications, Inc. and decided to become its own Internet Service Provider (ISP). The town is currently installing a non- line-of-sight (NLOS) broadband fixed wireless system that it hopes will reach about 1,700 homes and business, or about 60 percent of the available market.

Buffalo plans a two-phase rollout. The first phase is now complete and cost $180,000. This included the construction of three wireless towers. Residential users within one kilometer (five-eighths of a mile) of each tower pay $29.99 a month for 128 kilobits/ second for access. Business users can purchase speeds up to 256 kilobits/sec at a higher price. The second phase will require the construction of five more towers and will cost about $300,000. The town anticipates a four-year return on the total $480,000 investment.

Residential service started in late 2001. Over 125 customers had signed up by mid-January 2001, and two to three new subscribers sign up each day. According to Merton Auger, the city administrator, people looking to buy homes or set up businesses in Buffalo, just 26 miles from Minneapolis/St. Paul, are already asking if properties are located inside the high-speed Internet areas.

Grant County, Washington

The Grant County Public Utility District (GCPUD), a municipally owned public electric utility, has deployed a Fiber to the Home (FTTH) network in the city of Ephrata in Central Washington. The project, called ZIPP, includes a municipal fiber network and an all- fiber local access network. The utility deploys and operates the ZIPP fiber network, while independent service providers contract with the GCPUD to offer Internet access, voice, and video over the network.

In 1998, the utility began deploying a fiber network connecting the electric generating plants, power substations, and office buildings together for monitoring purposes. Once the utility points were connected, GCPUD decided to extend the network into a fiber ring and offer excess capacity to other businesses and organizations, including individual homes. The fiber ring was completed in 2000. The utility uses the network to offer advanced services such as automated metering and monitoring, and then leases the excess capacity to telecommunications service providers. In August of 2000, the utility started operating the network on a trial basis, serving 100 homes and 30 businesses. The FTTH network connects to the ZIPP municipal fiber ring and then connects through the Northwest Open Access Network (NoaNET) to a major Internet Point of Presence (PoP) located in the Westin building in Seattle.

The utility began deploying the network only to homes that had ordered the services. However, they decided to gradually deploy the network to all of the homes for a given stage of deployment since the fiber splicing and resealing process was so expensive. As of June 2000, network cabling was placed near 3,700 homes and businesses. The plan was to deploy the network to

Northwest Pennsylvania Regional Planning & Development Commission CONNECT NW PA Broadband Study and Action Plan Supplemental Report

December 23, 2003 Page 119

8,000 homes and businesses by the end of 2001 and complete coverage to all sites (approximately 40,000) in the next three to five years.

The project is financed by the utility’s capital budget. The first stage of the project has cost around $12 million and the total cost is estimated to be $130 million over the next three to five years. The utility estimates that it will pay $35 to 40 million of the total cost and that revenues will cover the rest of the costs. Equipment installed on a customer’s premises costs approximately $1,000 per subscriber, but consumers only pay the utility a one-time connection fee of $300 and an ongoing monthly fee of $40 to use the network. Subscribers choose their own service provider from four Internet Service Providers in the community. They provide symmetric broadband Internet access at 100 Mbps, with monthly fees ranging from $9 to $25 a month. A digital TV service with 120 channels and video-on-demand began on a trial basis in the summer of 2001.

Jacksonville, Florida

Jacksonville, Florida is a thriving community that boasts state-of-the-art fiber-optic connections in many of its downtown businesses, but the city wanted to find a way to get affordable broadband access to community centers in poor neighborhoods and economic development zones outside the downtown area. The city plans to conduct a pilot project over the next year that would create wireless zones across the region based on the 802.11b wireless local area network standard. Anyone within a defined Wireless Internet Zone (WIZ) created using 802.11b connections can access the Internet at speeds of up to 11 megabits/sec.

The city's first WIZ began operating in late 2001 as a technology proof-of-concept at Jacksonville Landing, a retail, restaurant and amusement center located on Jacksonville's downtown riverfront. Anyone with an appropriately equipped laptop or handheld computer can access the Internet within that zone, free of charge. As WIZ expands, the city may charge a small fee for access. WIZ will reach about 80 percent of the people in areas that want broadband services but cannot otherwise afford them. A WIZ can be installed for about an eighth of the price for a comparable wired solution.

Pocahontas, Iowa

Adopting the most appropriate (and sometimes innovative) technology can overcome many cost or deployment hurdles for rural areas. The most appropriate technology also takes into account demand factors, leading to higher take rates by consumers.

Pocahontas, Iowa, a community of approximately 2000 people, turned to a wireless system provider after being told that Qwest was not interested in providing broadband service. Rather than spending $4 million upgrading the town’s cable system for broadband, Pocahontas chose a multipoint microwave distribution system (MMDS) for an initial investment of only $32,000. The system is based on recently developed non- line-of-sight technology, which provides greater flexibility and quicker installation, but less bandwidth, than older line-of-sight systems. The

Northwest Pennsylvania Regional Planning & Development Commission CONNECT NW PA Broadband Study and Action Plan Supplemental Report

December 23, 2003 Page 120

system from Evertek Inc. provides MMDS technology in the 2.1 to 2.7 Ghz frequency range, allowing a single radio tower to cover a 35-mile radius.86 The city splits the monthly customer revenue with Evertek and expects to recoup their initial investment within three years.

Pocahontas is able to supply 512 Kbps downloads to customers for a $29.95 monthly fee. This is a broadband value proposition that seems to be hitting home with area residents. Around 20% of the town’s 900 households have signed up for the service, which has only been available since December of 2001. City Administrator Greg Fritz notes that the relatively low cost is the key to the system’s success. The lowest cost using a line-of-sight option would have been $45 per month for 128 Kbps service and $99 per month for businesses to receive 256 Kbps. Pocahontas charges the same price for business and residential and has 20% of the area businesses signed up as well. The 20% take rates for both residential and business customers are nearly double the national rate, which seems to confirm the importance of a broadband price point of approximately $30.

Stockholm, Sweden

The City of Stockholm believed broadband capacity would create an educated workforce, a prosperous economy, and an attractive lifestyle for its residents. In 1994, the city chartered a company called Stokab to build and manage a publicly owned, open-access fiber-optic network in the city that would provide dark fiber to telecommunications operators and other users at cost. Stockholm did not want multiple providers repetitively digging up its streets, so the city granted access to its ducts and tunnels. Stokab hung fiber-optic cable in the subways, and pulled it alongside steam and water pipes, electric cables, and sewer lines.

The City of Stockholm also realized it was cheaper and more practical for providers to lease Stokab fiber, than build their own networks. Stokab supplies dark fiber to carriers and resellers, who terminate and light their own fiber and supply all services above the fiber layer. Stokab is not involved in customer premises wiring. Any provider can use the network to deliver their services, allowing providers to customize their services for a specific customer. Customers of the Stokab network include telecom operators, Internet Service Providers, cable television networks, mobile telephone operators, municipalities, county councils, major banks, insurance companies, and the new media companies.

Under Swedish law, municipality-owned companies are operated to benefit the citizens and not to make a profit, so Stokab does not compete with the private sector. This increases competition among operators and thereby benefits business enterprise in the region. The users pay an access fee to use the network.

The Stokab fiber optic network began in the commercial districts of central Stockholm and the large industrial areas around Stockholm. In 1999, the network covered most of the central city and included public schools, libraries, district administrations, and industrial, office, and business centers in Stockholm. Based on the Stokab model, the Swedish Government is considering funding programs to assist municipalities in deploying open-access fiber infrastructure to every home, school, library, and business in the country. Sweden, working with the regional

Northwest Pennsylvania Regional Planning & Development Commission CONNECT NW PA Broadband Study and Action Plan Supplemental Report

December 23, 2003 Page 121

municipalities, has accepted responsibility for planning and coordination of a nationwide fiber optic network.

Northwest Pennsylvania Regional Planning & Development Commission CONNECT NW PA Broadband Study and Action Plan Supplemental Report

December 23, 2003 Page 122

Troy, New Hampshire The Troy Industrial Development Authority, seeking an innovative way to level the playing field, is creating a cooperative entity to provide broadband services. Subscribers would pay a town broadband entity, which would in turn pay a service provider. Since most providers don’t handle small business or residential users and Troy has a number of people who’d like higher bandwidth at more affordable prices, Troy officials are seeking to join Monadnock Connect as a town aggregate, not as an individual business. This project was in progress as of December 1, 2001, and attempts to serve all in the community. Digital Rivers

The Digital Rivers project in the Pittsburgh region is a comprehensive example of what can be done to gain an understanding of the market for broadband services.87 It focuses on the urban Pittsburgh area, but the demand analysis expands into surrounding rural counties. This project covers all the essentials for aligning broadband supply and demand factors. Broadband projects of this scope would serve greatly to enhance the broadband environment for any city. But short of replicating such a project, much can be applied to other areas from the Digital Rivers experience.

The major aspects of the project include the following:

« Status of local infrastructure « Area demographics « Cost analysis of various technologies and deployment « Survey of early adopters and unmet demand (county by county) « Analysis of current telecommunications environment, including the best practices of

others « Impediments to deployment « Implementation strategies « Pilot project

3 Rivers Connect (3rc) played a large role in the Digital Rivers project as well as the follow-up efforts based on the results of the project. 3rc, a non-profit organization, describes itself as a “project-oriented group (aiming) to provide broad, visionary leadership in the development of Western Pennsylvania’s information infrastructure.” One broadband deployment effort in Pittsburgh was implemented by 3rc, along with technology partner, Proxicast, LLC. Four different community improvement associations’ buildings were the first to be interconnected using Nokia Rooftop Wireless technology. Rooftop Wireless is a fixed wireless, mesh networking solution, which, in this case, delivers service speeds of 512 Kbps. The cost is approximately one-third of an equivalent speed DSL connection. The Digital River report points out that the Rooftop Wireless system is a competitive broadband technology for urban or suburban settings but is not suitable for areas where the number of houses per square mile is less than about 175. The ideal setting would be approximately 40 subscribers in a 1.5-mile radius. The Rooftop Wireless technology is one of several technological deployments considered by 3rc as they examine the various cost/performance tradeoffs for each community.

Northwest Pennsylvania Regional Planning & Development Commission CONNECT NW PA Broadband Study and Action Plan Supplemental Report

December 23, 2003 Page 123

The Digital Rivers project was a joint effort including state and local government, university and private resources. Carnegie Mellon University provided a great deal of expertise in cooperation with the Alleghany County Department of Economic Development, the Pennsylvania Technology Investment Authority and the Howard Heinz Endowment. An advisory group also included input from the Army National Guard, Pittsburgh Supercomputing Center and Redleaf Inc. Finally, there was a large group of stakeholders with direct interest in the region’s broadband capabilities. This included local and national companies, the City of Pittsburgh, and other interest groups. It takes an alignment of goals from all these groups in order to meet the broadband needs of communities.

Wireless Internet Zone

The Wireless Internet Zone in Jacksonville, Florida is one example of a project, which incorporates broadband access, computers, where needed, and training to maximize use of the technology. City officials and community activists are bringing wireless Internet connectivity to two low income neighborhoods. The recent emergence of low cost Wi-Fi wireless technology is making such broadband Internet deployments more feasible. The Internet zones cover two different community areas with wireless access. However, because Internet access cannot be accomplished without computers, they have also been made available to residents who need them through a combination of the Urban League, Humana and Florida’s Agency for Workforce Innovation. Awareness and education is also key; organizers stress the importance of getting the message out to local residents about what is now available. The larger goals for the project are to enhance literacy, workforce development, minority business development and voter education. The project is a joint effort by the City of Jacksonville, the Chamber of Commerce, the Urban League, BellSouth, and consulting firms, the Boardwalk Group, Connexsys, and the inc.well consulting group.

Thomasville, Georgia

Local efforts to aggregate organize and direct local demand can also accelerate the migration towards broadband adoption. Broadband efforts of regional municipalities can be combined in order to increase the scale of the operation. This provides more leverage in obtaining access to Internet backbone capacity and allows costs to be allocated more broadly. One example of this is occurring in rural Thomas County with a population of 43,000 in southern Georgia. Thomasville, the county seat, serves as the local cable head end and provides a broadband link to Camilla, Moultrie, and Cairo, Georgia. This broadband rollout was initiated through the Thomasville City Utility when the city could not talk anyone else into providing the service. Now that they are up and running, new competitors are starting to take the market more seriously, with the other local cable provider now upgrading its systems for broadband and a DSL competitor on the way.

Meanwhile, 50% to 60% of Thomasville’s residents have signed up for the new cable TV system and 47% of these customers have taken the cable modem service, called Rose.net. This works

Northwest Pennsylvania Regional Planning & Development Commission CONNECT NW PA Broadband Study and Action Plan Supplemental Report

December 23, 2003 Page 124

out to an overall broadband penetration for the city of almost 25%. The secrets of success in this case are likely to be found in price and customer service. Rose.net service for cable TV customers begins at $28.95 per month for 256 Kbps and climbs to $53.95 for 1 Mbps. Customers who subscribe to the cable modem service alone pay $43.95 for the 256 Kbps offering.

Dedicated customer service seems to be another factor for the higher take rate. Taking into account that most customers likely have limited technical expertise as well as patience, cable modems are installed by support staff for every customer, the technical support number is a local call and the wait is negligible. Moreover, the charges are incorporated on monthly utility bills in a precise, understandable manner.

“Hometown Utilicom”-Kutztown, Pennsylvania

The Borough of Kutztown with a population of over 5,000 is located approximately 50 miles northwest of Philadelphia between the cities of Reading and Allentown and adjacent to Kutztown University with an enrollment of over 8,000 students. In 2002, Kutztown completed construction of a broadband telecommunications infrastructure and facilities with fiber-optic cabling to the home/business (FTTH) capable of providing numerous voice, video, and data services. The borough was successful in building public-private service partnerships for the provisioning of services across the system. Just some of the services include traditional voice services, 10-100 Mbps Internet connectivity, security services, community intranet services and television programming from the municipal-owned headend. Some future anticipated services include state-of-the-art video and music offerings including both video and music-on-demand and interactive television and virtual private networking. These new voice, video and data services join the already existing borough electric energy supply and management services, water supply and treatment services, wastewater collection and treatment services and resource management (solid waste and recycling) services to provide one stop shopping, diverse billing and payment options and a value added services approach to the customer. This type of system was very complimentary to the municipal-owned electric system due to utility pole ownership, right-of-way assignments, bucket truck and other needed equipment being available, and technically competent staff for construction, service and maintenance, as well as marketing and billing services. Kutztown is also implementing an Automated Meter Reading (AMR) system for utilities. These new services will join the Borough’s existing Geographic Information System (GIS) and Supervisory Controlled and Data Acquisition (SCADA) systems in enhancing the development of Information Technologies (IT) of the Borough to better serve the propertie s and residents.

These services are marketed and billed under the registered service mark of “Hometown Utilicom”. Revenues stay within the community. Property owners and residents are not required to purchase any of the new services being offered, and the borough realizes that it must prove services are a benefit and competitive in cost to not only compete, but to justify municipal ownership of the system.

Northwest Pennsylvania Regional Planning & Development Commission CONNECT NW PA Broadband Study and Action Plan Supplemental Report

December 23, 2003 Page 125

A step-down star configuration passive optical network architecture was constructed to deliver converged voice, video and data services from the network operating center (NOC) or service control Point-of-Presence (POP) located in the municipal building to the customers’ premise. A fiber optics communication system was previously chosen for the utility’s SCADA system. The borough wanted to utilize future-proof technology to meet the high speed Internet and bandwidth demands and optical network solutions needed for additional services that will become available.

The borough has already discussed incorporating the Hometown Utilicom service industry with the Kutztown Main Street program, a downtown revitalization/reinvestment proposal. In addition, the borough is currently working on an economic development incentive initiative to attract commercial and industrial development along the Route 222 corridor to not only provide a basis for additional utility revenue, but to help relieve the growing school district tax burden on the constituents. The previously purchased Kutztown-Topton railroad spur by the borough may play a significant role in expanding services outside the Borough.

The borough felt that as a university host community, Kutztown’s needs to provide present and future adaptable technology to handle the needs of the information age is essential to remain attractive and viable to the students, as well as other residents who call Kutztown home.

Northwest Pennsylvania Regional Planning & Development Commission CONNECT NW PA Broadband Study and Action Plan Supplemental Report

December 23, 2003 Page 126

Section 10: Additional Exhibits

Demographics Data for Pennsylvania and by County

Pennsylvania Data

Main | Search | Feedback | FAQs | Glossary

Quick Tables Load Query | Save Query

DP-1. Profile of General Demographic Characteristics: 2000 Data Set: Census 2000 Summary File 1 (SF 1) 100-Percent Data Geographic Area: Pennsylvania NOTE: For information on confidentiality protection, nonsampling error, and definitions, see http://factfinder.census.gov/home/en/datanotes/expsf1u.htm.

Subject Number Percent

Total population 12,281,054 100.0

SEX AND AGE Male 5,929,663 48.3 Female 6,351,391 51.7

Under 5 years 727,804 5.9 5 to 9 years 827,945 6.7 10 to 14 years 863,849 7.0 15 to 19 years 850,986 6.9 20 to 24 years 746,086 6.1 25 to 34 years 1,560,486 12.7 35 to 44 years 1,948,076 15.9 45 to 54 years 1,705,032 13.9 55 to 59 years 619,969 5.0 60 to 64 years 511,656 4.2 65 to 74 years 969,272 7.9 75 to 84 years 712,326 5.8 85 years and over 237,567 1.9

Median age (years) 38.0 (X)

Northwest Pennsylvania Regional Planning & Development Commission CONNECT NW PA Broadband Study and Action Plan Supplemental Report

December 23, 2003 Page 127

Subject Number Percent

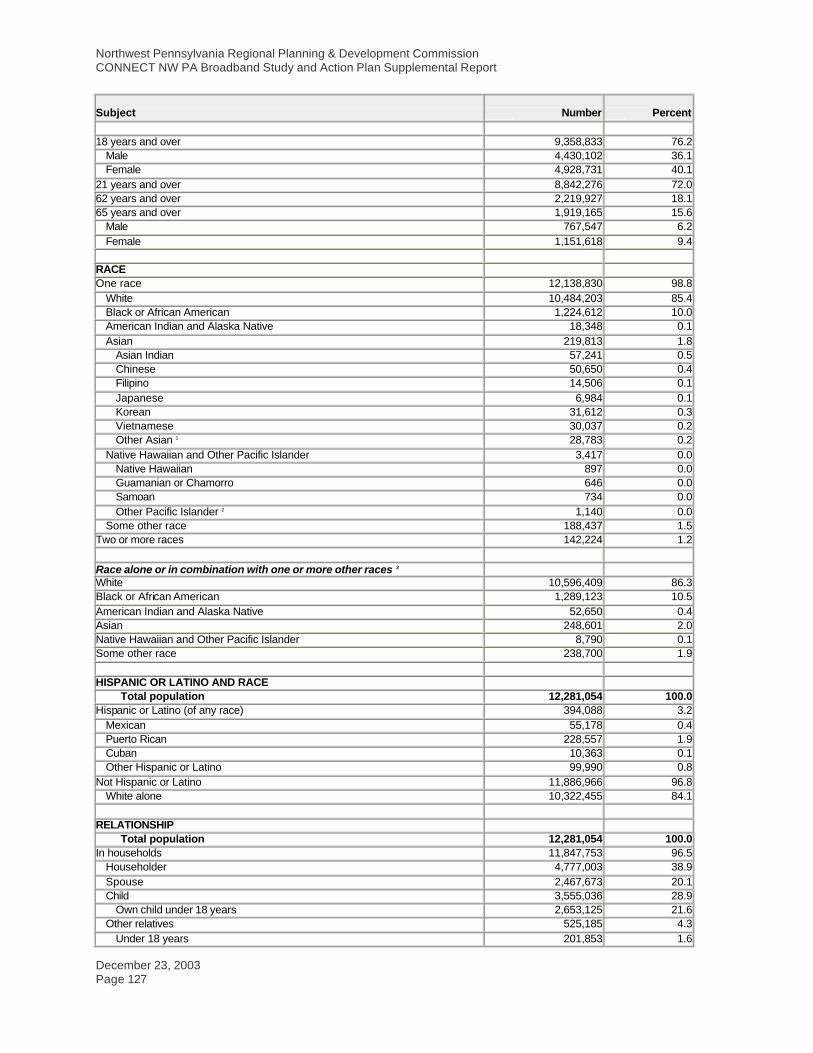

18 years and over 9,358,833 76.2

Male 4,430,102 36.1 Female 4,928,731 40.1

21 years and over 8,842,276 72.0 62 years and over 2,219,927 18.1 65 years and over 1,919,165 15.6

Male 767,547 6.2 Female 1,151,618 9.4

RACE One race 12,138,830 98.8

White 10,484,203 85.4 Black or African American 1,224,612 10.0 American Indian and Alaska Native 18,348 0.1 Asian 219,813 1.8

Asian Indian 57,241 0.5 Chinese 50,650 0.4 Filipino 14,506 0.1 Japanese 6,984 0.1 Korean 31,612 0.3 Vietnamese 30,037 0.2 Other Asian 1 28,783 0.2

Native Hawaiian and Other Pacific Islander 3,417 0.0 Native Hawaiian 897 0.0 Guamanian or Chamorro 646 0.0 Samoan 734 0.0 Other Pacific Islander 2 1,140 0.0

Some other race 188,437 1.5 Two or more races 142,224 1.2

Race alone or in combination with one or more other races 3 White 10,596,409 86.3 Black or African American 1,289,123 10.5 American Indian and Alaska Native 52,650 0.4 Asian 248,601 2.0 Native Hawaiian and Other Pacific Islander 8,790 0.1 Some other race 238,700 1.9

HISPANIC OR LATINO AND RACE

Total population 12,281,054 100.0 Hispanic or Latino (of any race) 394,088 3.2

Mexican 55,178 0.4 Puerto Rican 228,557 1.9 Cuban 10,363 0.1 Other Hispanic or Latino 99,990 0.8

Not Hispanic or Latino 11,886,966 96.8 White alone 10,322,455 84.1

RELATIONSHIP

Total population 12,281,054 100.0 In households 11,847,753 96.5

Householder 4,777,003 38.9 Spouse 2,467,673 20.1 Child 3,555,036 28.9

Own child under 18 years 2,653,125 21.6 Other relatives 525,185 4.3

Under 18 years 201,853 1.6

Northwest Pennsylvania Regional Planning & Development Commission CONNECT NW PA Broadband Study and Action Plan Supplemental Report

December 23, 2003 Page 128

Subject Number Percent

Nonrelatives 522,856 4.3 Unmarried partner 237,622 1.9

In group quarters 433,301 3.5 Institutionalized population 213,790 1.7 Noninstitutionalized population 219,511 1.8

HOUSEHOLDS BY TYPE

Total households 4,777,003 100.0 Family households (families) 3,208,388 67.2

With own children under 18 years 1,430,808 30.0 Married-couple family 2,467,673 51.7

With own children under 18 years 1,043,071 21.8 Female householder, no husband present 554,693 11.6

With own children under 18 years 298,021 6.2 Nonfamily households 1,568,615 32.8

Householder living alone 1,320,941 27.7 Householder 65 years and over 555,374 11.6

Households with individuals under 18 years 1,559,281 32.6 Households with individuals 65 years and over 1,328,237 27.8

Average household size 2.48 (X) Average family size 3.04 (X)

HOUSING OCCUPANCY

Total housing units 5,249,750 100.0 Occupied housing units 4,777,003 91.0 Vacant housing units 472,747 9.0

For seasonal, recreational, or occasional use 148,230 2.8

Homeowner vacanc y rate (percent) 1.6 (X) Rental vacancy rate (percent) 7.2 (X)

HOUSING TENURE

Occupied housing units 4,777,003 100.0 Owner-occupied housing units 3,406,337 71.3 Renter-occupied housing units 1,370,666 28.7

Average household size of owner-occupied unit 2.62 (X) Average household size of renter-occupied unit 2.12 (X)

Subject Number Percent (X) Not applicable 1 Other Asian alone, or two or more Asian categories. 2 Other Pacific Islander alone, or two or more Native Hawaiian and Other Pacific Islander categories. 3 In combination with one or more other races listed. The six numbers may add to more than the total population and the six percentages may add to more than 100 percent because individuals may report more than one race. Source: U.S. Census Bureau, Census 2000 Summary File 1, Matrices P1, P3, P4, P8, P9, P12, P13, P,17, P18, P19, P20, P23, P27, P28, P33, PCT5, PCT8, PCT11, PCT15, H1, H3, H4, H5, H11, and H12.

Northwest Pennsylvania Regional Planning & Development Commission CONNECT NW PA Broadband Study and Action Plan Supplemental Report

December 23, 2003 Page 129

Main | Search | Feedback | FAQs | Glossary

Quick Tables Load Query | Save Query

DP-2. Profile of Selected Social Characteristics: 2000 Data Set: Census 2000 Summary File 3 (SF 3) - Sample Data Geographic Area: Pennsylvania NOTE: Data based on a sample except in P3, P4, H3, and H4. For information on confidentiality protection, sampling error, nonsampling error, and definitions see http://factfinder.census.gov/home/en/datanotes/expsf3.htm.

Subject Number Percent

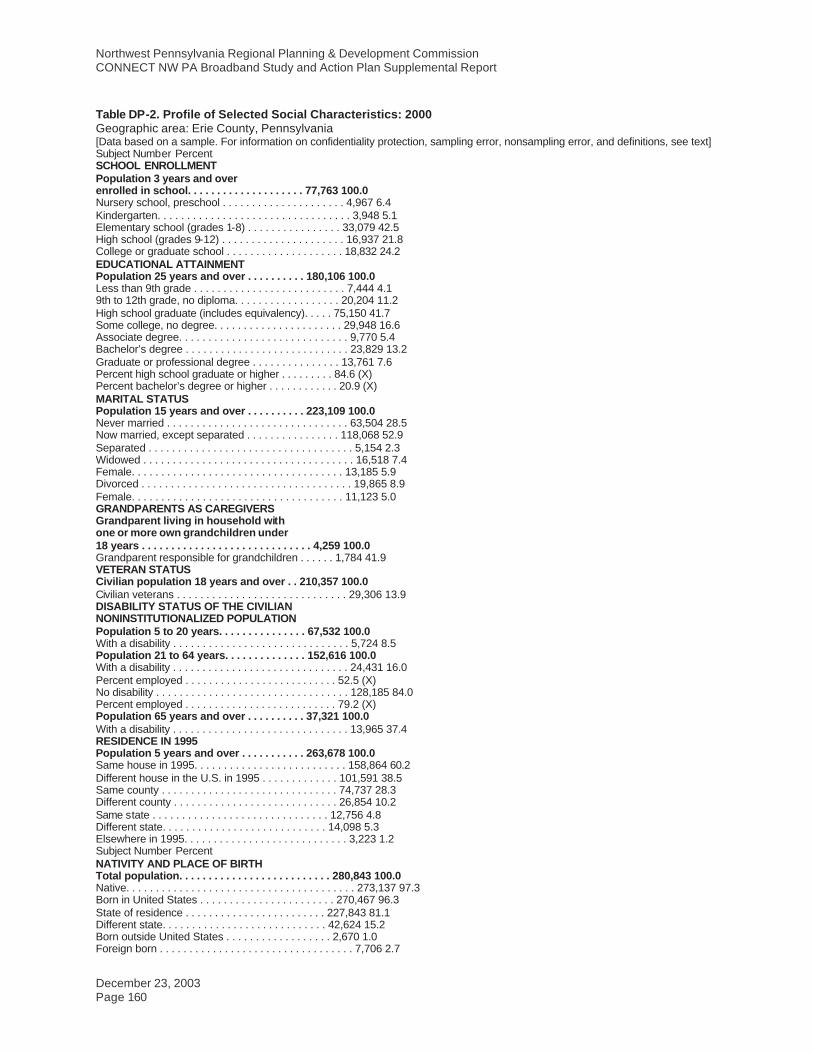

SCHOOL ENROLLMENT

Population 3 years and over enrolled in school 3,135,934 100.0 Nursery school, preschool 203,934 6.5 Kindergarten 159,146 5.1 Elementary school (grades 1-8) 1,379,671 44.0 High school (grades 9-12) 690,020 22.0 College or graduate school 703,163 22.4

EDUCATIONAL ATTAINMENT

Population 25 years and over 8,266,284 100.0 Less than 9th grade 452,069 5.5 9th to 12th grade, no diploma 1,044,036 12.6 High school graduate (includes equivalency) 3,150,013 38.1 Some college, no degree 1,284,731 15.5 Associate degree 487,804 5.9 Bachelor's degree 1,153,383 14.0 Graduate or professional degree 694,248 8.4

Percent high school graduate or higher 81.9 (X) Percent bachelor's degree or higher 22.4 (X)

MARITAL STATUS

Population 15 years and over 9,861,713 100.0 Never married 2,685,328 27.2 Now married, except separated 5,352,297 54.3 Separated 215,846 2.2 Widowed 808,903 8.2

Female 656,381 6.7

Northwest Pennsylvania Regional Planning & Development Commission CONNECT NW PA Broadband Study and Action Plan Supplemental Report

December 23, 2003 Page 130

Divorced 799,339 8.1

Female 456,801 4.6

GRANDPARENTS AS CAREGIVERS Grandparent living in household with one or more own grandchildren under 18 years 204,909 100.0

Grandparent responsible for grandchildren 80,423 39.2

VETERAN STATUS Civilian population 18 years and over 9,354,471 100.0

Civilian veterans 1,280,788 13.7

DISABILITY STATUS OF THE CIVILIAN NONINSTITUTIONALIZED POPULATION Population 5 to 20 years 2,689,895 100.0

With a disability 202,259 7.5

Population 21 to 64 years 6,837,268 100.0 With a disability 1,196,717 17.5

Percent employed 54.8 (X) No disability 5,640,551 82.5

Percent employed 78.3 (X)

Population 65 years and over 1,809,320 100.0 With a disability 712,795 39.4

RESIDENCE IN 1995

Population 5 years and over 11,555,538 100.0 Same house in 1995 7,333,591 63.5 Different house in the U.S. in 1995 4,056,716 35.1

Same county 2,513,167 21.7 Different county 1,543,549 13.4

Same state 874,796 7.6 Different state 668,753 5.8

Elsewhere in 1995 165,231 1.4

NATIVITY AND PLACE OF BIRTH Total population 12,281,054 100.0

Native 11,772,763 95.9 Born in United States 11,620,495 94.6

State of residence 9,544,251 77.7 Different state 2,076,244 16.9

Born outside United States 152,268 1.2 Foreign born 508,291 4.1

Entered 1990 to March 2000 209,123 1.7 Naturalized citizen 257,339 2.1 Not a citizen 250,952 2.0

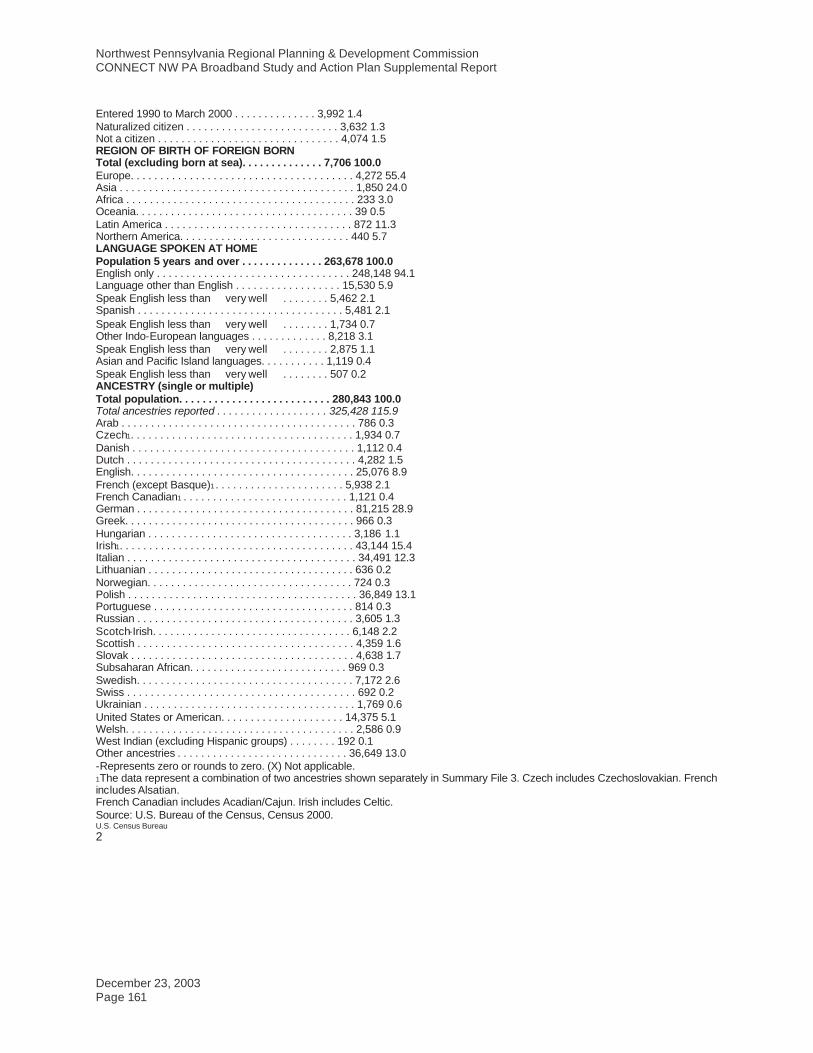

REGION OF BIRTH OF FOREIGN BORN

Total (excluding born at sea) 508,282 100.0 Europe 182,667 35.9 Asia 182,967 36.0 Africa 25,413 5.0 Oceania 2,178 0.4 Latin America 99,514 19.6 Northern America 15,543 3.1

LANGUAGE SPOKEN AT HOME

Population 5 years and over 11,555,538 100.0 English only 10,583,054 91.6 Language other than English 972,484 8.4

Northwest Pennsylvania Regional Planning & Development Commission CONNECT NW PA Broadband Study and Action Plan Supplemental Report

December 23, 2003 Page 131

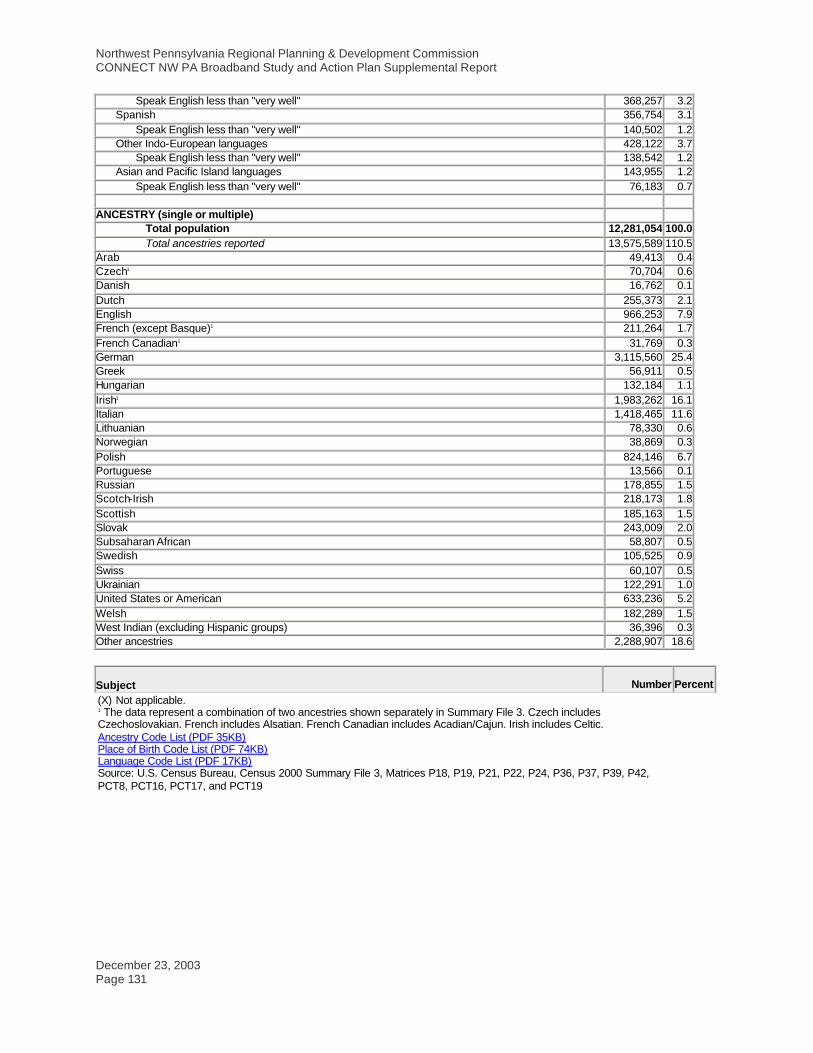

Speak English less than "very well" 368,257 3.2 Spanish 356,754 3.1

Speak English less than "very well" 140,502 1.2 Other Indo-European languages 428,122 3.7

Speak English less than "very well" 138,542 1.2 Asian and Pacific Island languages 143,955 1.2

Speak English less than "very well" 76,183 0.7

ANCESTRY (single or multiple) Total population 12,281,054 100.0 Total ancestries reported 13,575,589 110.5

Arab 49,413 0.4 Czech1 70,704 0.6 Danish 16,762 0.1 Dutch 255,373 2.1 English 966,253 7.9 French (except Basque)1 211,264 1.7 French Canadian1 31,769 0.3 German 3,115,560 25.4 Greek 56,911 0.5 Hungarian 132,184 1.1 Irish1 1,983,262 16.1 Italian 1,418,465 11.6 Lithuanian 78,330 0.6 Norwegian 38,869 0.3 Polish 824,146 6.7 Portuguese 13,566 0.1 Russian 178,855 1.5 Scotch-Irish 218,173 1.8 Scottish 185,163 1.5 Slovak 243,009 2.0 Subsaharan African 58,807 0.5 Swedish 105,525 0.9 Swiss 60,107 0.5 Ukrainian 122,291 1.0 United States or American 633,236 5.2 Welsh 182,289 1.5 West Indian (excluding Hispanic groups) 36,396 0.3 Other ancestries 2,288,907 18.6

Subject Number Percent (X) Not applicable. 1 The data represent a combination of two ancestries shown separately in Summary File 3. Czech includes Czechoslovakian. French includes Alsatian. French Canadian includes Acadian/Cajun. Irish includes Celtic. Ancestry Code List (PDF 35KB) Place of Birth Code List (PDF 74KB) Language Code List (PDF 17KB) Source: U.S. Census Bureau, Census 2000 Summary File 3, Matrices P18, P19, P21, P22, P24, P36, P37, P39, P42, PCT8, PCT16, PCT17, and PCT19

Northwest Pennsylvania Regional Planning & Development Commission CONNECT NW PA Broadband Study and Action Plan Supplemental Report

December 23, 2003 Page 132

Main | Search | Feedback | FAQs | Glossary

Quick Tables Load Query | Save Query

DP-3. Profile of Selected Economic Characteristics: 2000 Data Set: Census 2000 Summary File 3 (SF 3) - Sample Data Geographic Area: Pennsylvania NOTE: Data based on a sample except in P3, P4, H3, and H4. For information on confidentiality protection, sampling error, nonsampling error, and definitions see http://factfinder.census.gov/home/en/datanotes/expsf3.htm.

Subject Number Percent

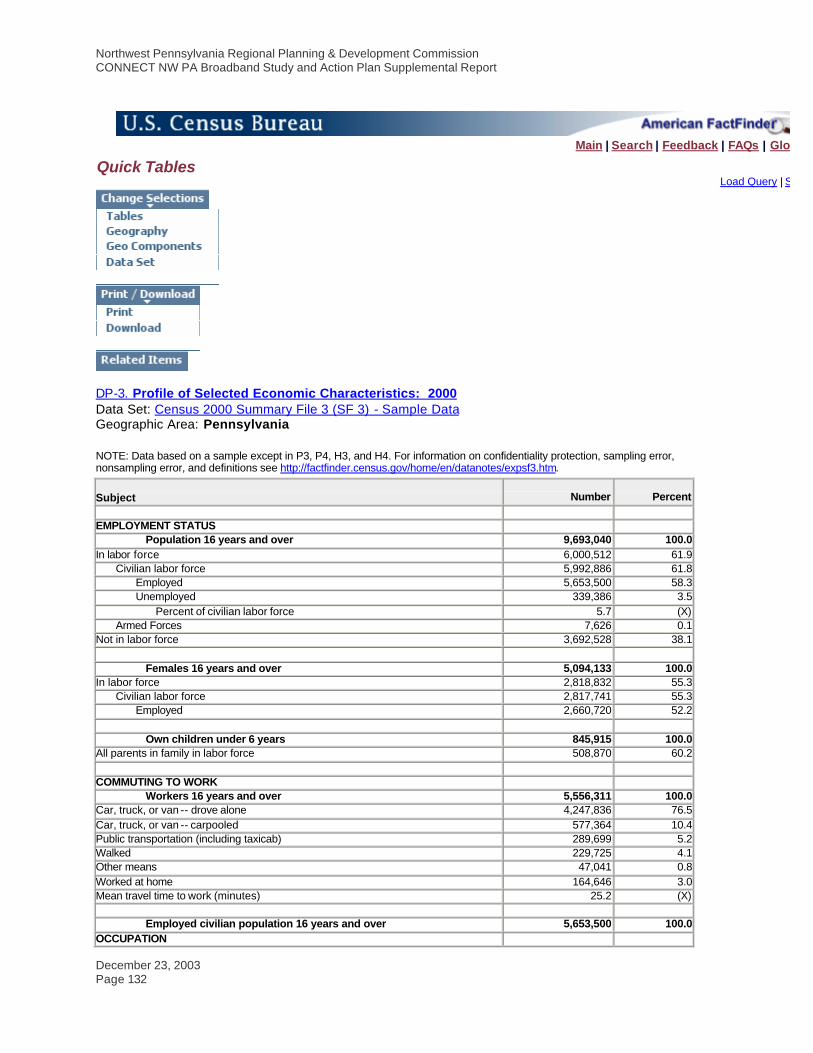

EMPLOYMENT STATUS

Population 16 years and over 9,693,040 100.0 In labor force 6,000,512 61.9

Civilian labor force 5,992,886 61.8 Employed 5,653,500 58.3 Unemployed 339,386 3.5

Percent of civilian labor force 5.7 (X) Armed Forces 7,626 0.1

Not in labor force 3,692,528 38.1

Females 16 years and over 5,094,133 100.0 In labor force 2,818,832 55.3

Civilian labor force 2,817,741 55.3 Employed 2,660,720 52.2

Own children under 6 years 845,915 100.0

All parents in family in labor force 508,870 60.2

COMMUTING TO WORK Workers 16 years and over 5,556,311 100.0

Car, truck, or van -- drove alone 4,247,836 76.5 Car, truck, or van -- carpooled 577,364 10.4 Public transportation (including taxicab) 289,699 5.2 Walked 229,725 4.1 Other means 47,041 0.8 Worked at home 164,646 3.0 Mean travel time to work (minutes) 25.2 (X)

Employed civilian population 16 years and over 5,653,500 100.0

OCCUPATION

Northwest Pennsylvania Regional Planning & Development Commission CONNECT NW PA Broadband Study and Action Plan Supplemental Report

December 23, 2003 Page 133

Subject Number Percent Management, professional, and related occupations 1,841,175 32.6 Service occupations 838,137 14.8 Sales and office occupations 1,525,131 27.0 Farming, fishing, and forestry occupations 26,722 0.5 Construction, extraction, and maintenance occupations 500,898 8.9 Production, transportation, and material moving occupations 921,437 16.3

INDUSTRY Agriculture, forestry, fishing and hunting, and mining 73,459 1.3 Construction 339,363 6.0 Manufacturing 906,398 16.0 Wholesale trade 201,084 3.6 Retail trade 684,179 12.1 Transportation and warehousing, and utilities 304,335 5.4 Information 148,841 2.6 Finance, insurance, real estate, and rental and leasing 372,148 6.6 Professional, scientific, management, administrative, and waste management services 478,937 8.5 Educational, health and social services 1,237,090 21.9 Arts, entertainment, recreation, accommodation and food services 397,871 7.0 Other services (except public administration) 274,028 4.8 Public administration 235,767 4.2

CLASS OF WORKER Private wage and salary workers 4,657,372 82.4 Government workers 639,088 11.3 Self-employed workers in own not incorporated business 339,631 6.0 Unpaid family workers 17,409 0.3

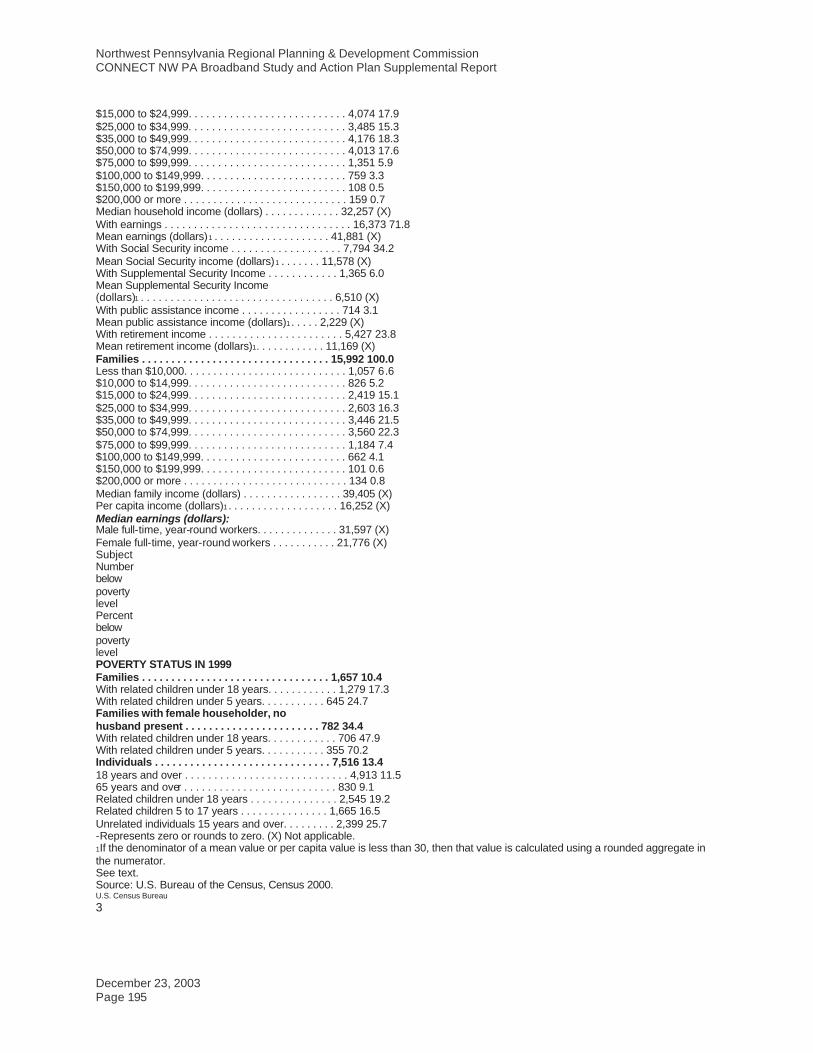

INCOME IN 1999

Households 4,779,186 100.0 Less than $10,000 465,860 9.7 $10,000 to $14,999 333,381 7.0 $15,000 to $24,999 657,266 13.8 $25,000 to $34,999 633,953 13.3 $35,000 to $49,999 809,165 16.9 $50,000 to $74,999 929,863 19.5 $75,000 to $99,999 457,480 9.6 $100,000 to $149,999 317,171 6.6 $150,000 to $199,999 84,173 1.8 $200,000 or more 90,874 1.9 Median household income (dollars) 40,106 (X)

With earnings 3,667,238 76.7

Mean earnings (dollars) 54,209 (X) With Social Security income 1,451,386 30.4

Mean Social Security income (dollars) 11,717 (X) With Supplemental Security Income 203,851 4.3

Mean Supplemental Security Income (dollars) 6,523 (X) With public assistance income 149,203 3.1

Mean public assistance income (dollars) 2,848 (X) With retirement income 940,184 19.7

Mean retirement income (dollars) 14,663 (X)

Families 3,225,707 100.0 Less than $10,000 167,090 5.2 $10,000 to $14,999 124,473 3.9 $15,000 to $24,999 352,867 10.9 $25,000 to $34,999 410,489 12.7

Northwest Pennsylvania Regional Planning & Development Commission CONNECT NW PA Broadband Study and Action Plan Supplemental Report

December 23, 2003 Page 134

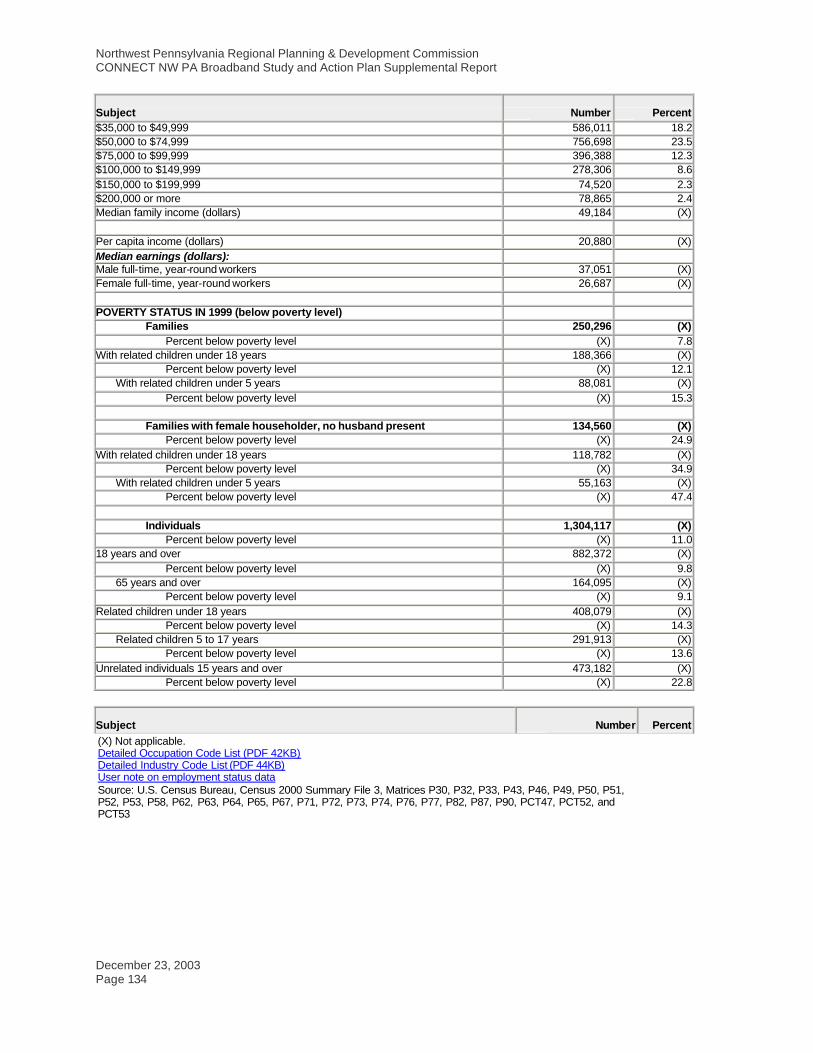

Subject Number Percent $35,000 to $49,999 586,011 18.2 $50,000 to $74,999 756,698 23.5 $75,000 to $99,999 396,388 12.3 $100,000 to $149,999 278,306 8.6 $150,000 to $199,999 74,520 2.3 $200,000 or more 78,865 2.4 Median family income (dollars) 49,184 (X)

Per capita income (dollars) 20,880 (X) Median earnings (dollars): Male full-time, year-round workers 37,051 (X) Female full-time, year-round workers 26,687 (X)

POVERTY STATUS IN 1999 (below poverty level)

Families 250,296 (X) Percent below poverty level (X) 7.8

With related children under 18 years 188,366 (X) Percent below poverty level (X) 12.1

With related children under 5 years 88,081 (X) Percent below poverty level (X) 15.3

Families with female householder, no husband present 134,560 (X)

Percent below poverty level (X) 24.9 With related children under 18 years 118,782 (X)

Percent below poverty level (X) 34.9 With related children under 5 years 55,163 (X)

Percent below poverty level (X) 47.4

Individuals 1,304,117 (X) Percent below poverty level (X) 11.0

18 years and over 882,372 (X) Percent below poverty level (X) 9.8

65 years and over 164,095 (X) Percent below poverty level (X) 9.1

Related children under 18 years 408,079 (X) Percent below poverty level (X) 14.3

Related children 5 to 17 years 291,913 (X) Percent below poverty level (X) 13.6

Unrelated individuals 15 years and over 473,182 (X) Percent below poverty level (X) 22.8

Subject Number Percent (X) Not applicable. Detailed Occupation Code List (PDF 42KB) Detailed Industry Code List (PDF 44KB) User note on employment status data Source: U.S. Census Bureau, Census 2000 Summary File 3, Matrices P30, P32, P33, P43, P46, P49, P50, P51, P52, P53, P58, P62, P63, P64, P65, P67, P71, P72, P73, P74, P76, P77, P82, P87, P90, PCT47, PCT52, and PCT53

Northwest Pennsylvania Regional Planning & Development Commission CONNECT NW PA Broadband Study and Action Plan Supplemental Report

December 23, 2003 Page 135

Main | Search | Feedback | FAQs | Glossary

Quick Tables

Load Query | Save Query

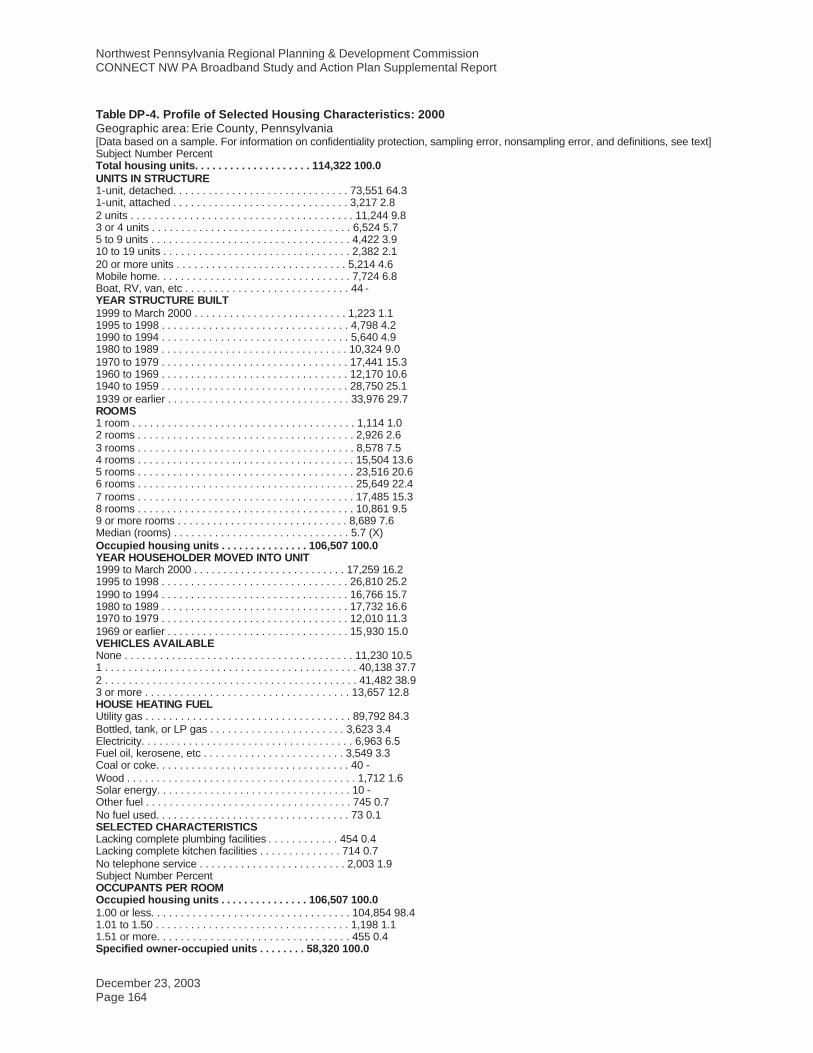

DP-4. Profile of Selected Housing Characteristics: 2000 Data Set: Census 2000 Summary File 3 (SF 3) - Sample Data Geographic Area: Pennsylvania NOTE: Data based on a sample except in P3, P4, H3, and H4. For information on confidentiality protection, sampling error, nonsampling error, and definitions see http://factfinder.census.gov/home/en/datanotes/expsf3.htm.

Subject Number Percent

Total housing units 5,249,750 100.0

UNITS IN STRUCTURE 1-unit, detached 2,935,248 55.9 1-unit, attached 940,396 17.9 2 units 273,798 5.2 3 or 4 units 241,745 4.6 5 to 9 units 179,909 3.4 10 to 19 units 131,691 2.5 20 or more units 283,714 5.4 Mobile home 258,551 4.9 Boat, RV, van, etc. 4,698 0.1

YEAR STRUCTURE BUILT 1999 to March 2000 66,916 1.3 1995 to 1998 212,916 4.1 1990 to 1994 266,445 5.1 1980 to 1989 531,986 10.1 1970 to 1979 709,768 13.5 1960 to 1969 595,897 11.4 1940 to 1959 1,275,149 24.3 1939 or earlier 1,590,673 30.3

ROOMS 1 room 62,654 1.2

Northwest Pennsylvania Regional Planning & Development Commission CONNECT NW PA Broadband Study and Action Plan Supplemental Report

December 23, 2003 Page 136

2 rooms 143,152 2.7 3 rooms 403,457 7.7 4 rooms 668,040 12.7 5 rooms 924,603 17.6 6 rooms 1,220,416 23.2 7 rooms 767,695 14.6 8 rooms 561,360 10.7 9 or more rooms 498,373 9.5 Median (rooms) 5.8 (X)

Occupied Housing Units 4,777,003 100.0

YEAR HOUSEHOLDER MOVED INTO UNIT 1999 to March 2000 696,279 14.6 1995 to 1998 1,139,483 23.9 1990 to 1994 734,248 15.4 1980 to 1989 821,152 17.2 1970 to 1979 575,344 12.0 1969 or earlier 810,497 17.0

VEHICLES AVAILABLE None 613,249 12.8 1 1,667,535 34.9 2 1,791,526 37.5 3 or more 704,693 14.8

HOUSE HEATING FUEL Utility gas 2,452,941 51.3 Bottled, tank, or LP gas 145,254 3.0 Electricity 786,648 16.5 Fuel oil, kerosene, etc. 1,217,155 25.5 Coal or coke 67,986 1.4 Wood 76,060 1.6 Solar energy 663 0.0 Other fuel 20,500 0.4 No fuel used 9,796 0.2

SELECTED CHARACTERISTICS Lacking complete plumbing facilities 24,450 0.5 Lacking complete kitchen facilities 25,831 0.5 No telephone service 65,680 1.4

OCCUPANTS PER ROOM

Occupied housing units 4,777,003 100.0 1.00 or less 4,685,858 98.1 1.01 to 1.50 60,627 1.3 1.51 or more 30,518 0.6

Specified owner-occupied units 2,889,484 100.0

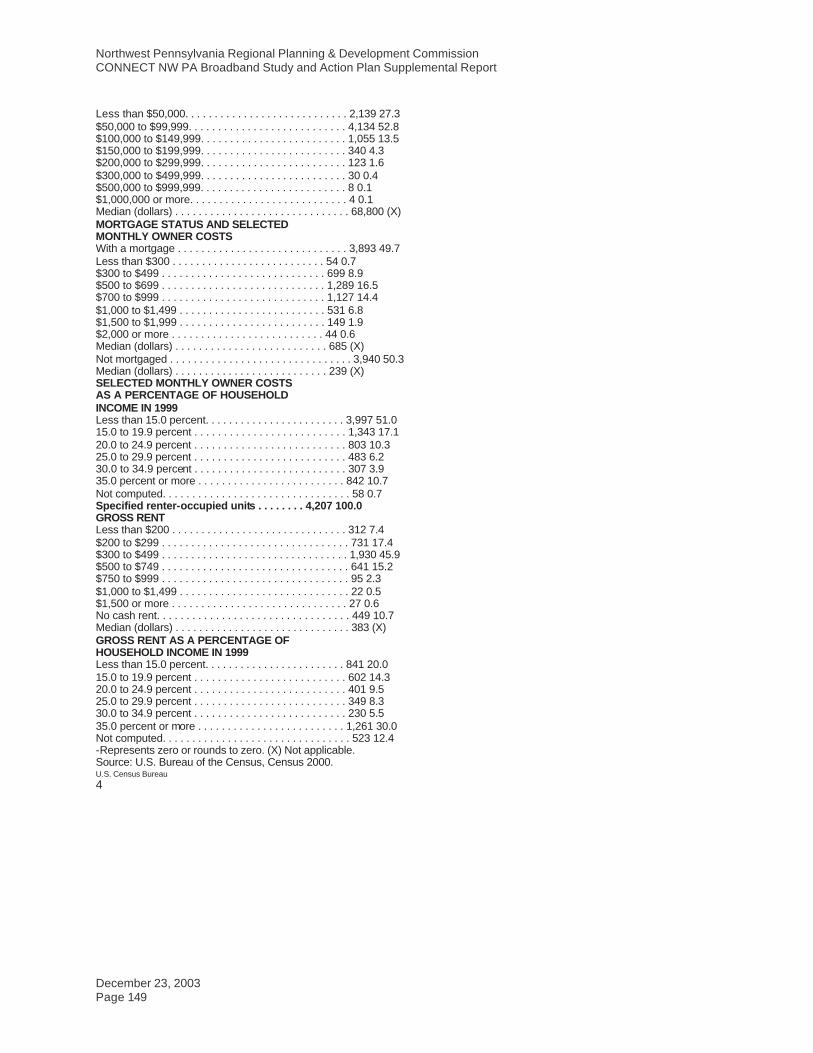

VALUE Less than $50,000 435,193 15.1 $50,000 to $99,999 1,079,698 37.4 $100,000 to $149,999 703,093 24.3 $150,000 to $199,999 344,172 11.9 $200,000 to $299,999 214,812 7.4 $300,000 to $499,999 84,425 2.9 $500,000 to $999,999 23,654 0.8 $1,000,000 or more 4,437 0.2 Median (dollars) 97,000 (X)

Northwest Pennsylvania Regional Planning & Development Commission CONNECT NW PA Broadband Study and Action Plan Supplemental Report

December 23, 2003 Page 137

MORTGAGE STATUS AND SELECTED MONTHLY OWNER COSTS With a mortgage 1,798,402 62.2

Less than $300 9,157 0.3 $300 to $499 108,720 3.8 $500 to $699 270,083 9.3 $700 to $999 498,003 17.2 $1,000 to $1,499 546,365 18.9 $1,500 to $1,999 220,493 7.6 $2,000 or more 145,581 5.0 Median (dollars) 1,010 (X)

Not mortgaged 1,091,082 37.8 Median (dollars) 318 (X)

SELECTED MONTHLY OWNER COSTS AS A PERCENTAGE OF HOUSEHOLD INCOME IN 1999

Less than 15 percent 1,091,368 37.8 15 to 19 percent 509,245 17.6 20 to 24 percent 399,694 13.8 25 to 29 percent 264,015 9.1 30 to 34 percent 164,558 5.7 35 percent or more 436,159 15.1 Not computed 24,445 0.8

Specified renter-occupied units 1,348,824 100.0

GROSS RENT Less than $200 85,346 6.3 $200 to $299 89,493 6.6 $300 to $499 389,144 28.9 $500 to $749 454,749 33.7 $750 to $999 167,064 12.4 $1,000 to $1,499 65,230 4.8 $1,500 or more 19,811 1.5 No cash rent 77,987 5.8 Median (dollars) 531 (X)

GROSS RENT AS A PERCENTAGE OF HOUSEHOLD INCOME IN 1999 Less than 15 percent 259,386 19.2 15 to 19 percent 193,612 14.4 20 to 24 percent 165,624 12.3 25 to 29 percent 139,877 10.4 30 to 34 percent 93,260 6.9 35 percent or more 386,384 28.6 Not computed 110,681 8.2

Subject Number Percent (X) Not applicable. Source: U.S. Census Bureau, Census 2000 Summary File 3, Matrices H1, H7, H20, H23, H24, H30, H34, H38, H40, H43, H44, H48, H51, H62, H63, H69, H74, H76, H90, H91, and H94

Northwest Pennsylvania Regional Planning & Development Commission CONNECT NW PA Broadband Study and Action Plan Supplemental Report

December 23, 2003 Page 138

Main | Search | Feedback | FAQs | Glossary

Quick Tables Load Query | Save Query

QT-H1. General Housing Characteristics: 2000 Data Set: Census 2000 Summary File 1 (SF 1) 100-Percent Data Geographic Area: Pennsylvania NOTE: For information on confidentiality protection, nonsampling error, and definitions, see http://factfinder.census.gov/home/en/datanotes/expsf1u.htm.

Subject

Number

Percent

OCCUPANCY STATUS

Total housing units 5,249,750 100.0 Occupied housing units 4,777,003 91.0 Vacant housing units 472,747 9.0

TENURE

Occupied housing units 4,777,003 100.0 Owner-occupied housing units 3,406,337 71.3 Renter-occupied housing units 1,370,666 28.7

VACANCY STATUS

Vacant housing units 472,747 100.0 For rent 105,585 22.3 For sale only 55,891 11.8 Rented or sold, not occupied 37,494 7.9 For seasonal, recreational, or occasional use 148,230 31.4 For migratory workers 386 0.1 Other vacant 125,161 26.5

RACE OF HOUSEHOLDER

Occupied housing units 4,777,003 100.0 One race 4,739,424 99.2

White 4,177,452 87.4 Black or African American 435,073 9.1 American Indian and Alaska Native 6,580 0.1 Asian 67,792 1.4 Native Hawaiian and Other Pacific Islander 873 0.0 Some other race 51,654 1.1

Two or more races 37,579 0.8

Northwest Pennsylvania Regional Planning & Development Commission CONNECT NW PA Broadband Study and Action Plan Supplemental Report

December 23, 2003 Page 139

Subject

Number

Percent

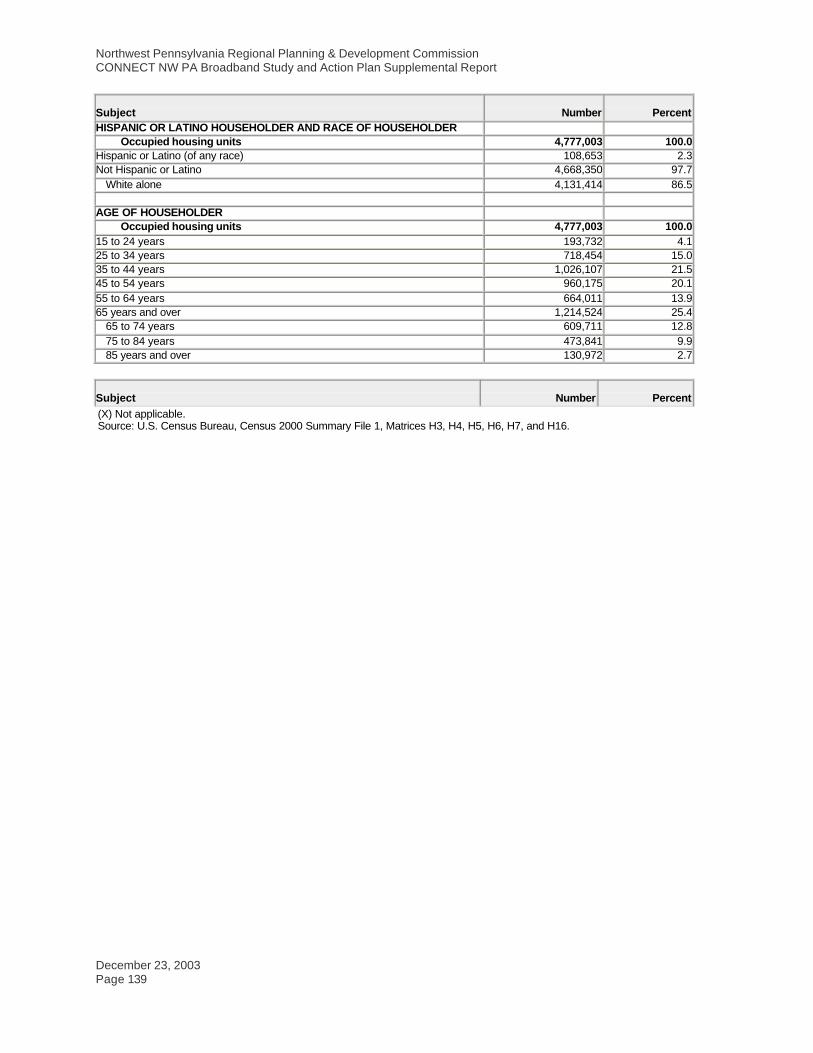

HISPANIC OR LATINO HOUSEHOLDER AND RACE OF HOUSEHOLDER Occupied housing units 4,777,003 100.0

Hispanic or Latino (of any race) 108,653 2.3 Not Hispanic or Latino 4,668,350 97.7

White alone 4,131,414 86.5

AGE OF HOUSEHOLDER Occupied housing units 4,777,003 100.0

15 to 24 years 193,732 4.1 25 to 34 years 718,454 15.0 35 to 44 years 1,026,107 21.5 45 to 54 years 960,175 20.1 55 to 64 years 664,011 13.9 65 years and over 1,214,524 25.4

65 to 74 years 609,711 12.8 75 to 84 years 473,841 9.9 85 years and over 130,972 2.7

Subject

Number

Percent

(X) Not applicable. Source: U.S. Census Bureau, Census 2000 Summary File 1, Matrices H3, H4, H5, H6, H7, and H16.

Northwest Pennsylvania Regional Planning & Development Commission CONNECT NW PA Broadband Study and Action Plan Supplemental Report

December 23, 2003 Page 140

County Data

Main | Search | Feedback | FAQs | Glossary

Geographic Comparison Table Load Query | Save Query

GCT-PH1. Population, Housing Units, Area, and Density: 2000 Data Set: Census 2000 Summary File 1 (SF 1) 100-Percent Data Geographic Area: Pennsylvania – County NOTE: For information on confidentiality protection, nonsampling error, and definitions, see http://factfinder.census.gov/home/en/datanotes/expsf1u.htm.

Area in square miles

Density per square mile of land area

Geographic area

Population

Housing

units

Total area

Water

area

Land area

Population

Housing

units Pennsylvania 12,281,054 5,249,750 46,055.24 1,238.63 44,816.61 274.0 117.1

COUNTY Adams County 91,292 35,831 521.52 1.51 520.01 175.6 68.9 Allegheny County 1,281,666 583,646 744.71 14.54 730.17 1,755.3 799.3 Armstrong County 72,392 32,387 664.44 10.51 653.93 110.7 49.5 Beaver County 181,412 77,765 443.90 9.69 434.21 417.8 179.1 Bedford County 49,984 23,529 1,017.40 2.89 1,014.51 49.3 23.2 Berks County 373,638 150,222 865.67 6.79 858.88 435.0 174.9 Blair County 129,144 55,061 527.11 1.31 525.80 245.6 104.7 Bradford County 62,761 28,664 1,161.03 10.37 1,150.67 54.5 24.9 Bucks County 597,635 225,498 622.11 14.74 607.38 984.0 371.3 Butler County 174,083 69,868 794.79 6.26 788.53 220.8 88.6 Cambria County 152,598 65,796 693.43 5.41 688.02 221.8 95.6 Cameron County 5,974 4,592 398.60 1.44 397.16 15.0 11.6 Carbon County 58,802 30,492 387.23 6.20 381.04 154.3 80.0 Centre County 135,758 53,161 1,111.85 4.32 1,107.53 122.6 48.0 Chester County 433,501 163,773 759.81 3.84 755.97 573.4 216.6 Clarion County 41,765 19,426 608.95 6.51 602.44 69.3 32.2 Clearfield County 83,382 37,855 1,153.80 6.49 1,147.32 72.7 33.0 Clinton County 37,914 18,166 898.09 7.23 890.87 42.6 20.4 Columbia County 64,151 27,733 489.79 4.24 485.55 132.1 57.1 Crawford County 90,366 42,416 1,037.74 25.01 1,012.72 89.2 41.9 Cumberland County 213,674 86,951 551.14 0.98 550.17 388.4 158.0 Dauphin County 251,798 111,133 557.53 32.24 525.29 479.4 211.6 Delaware County 550,864 216,978 190.74 6.53 184.21 2,990.4 1,177.9

Northwest Pennsylvania Regional Planning & Development Commission CONNECT NW PA Broadband Study and Action Plan Supplemental Report

December 23, 2003 Page 141

Area in square miles

Density per square mile of land area

Geographic area

Population

Housing

units

Total area

Water

area

Land area

Population

Housing

units Elk County 35,112 18,115 832.23 3.58 828.65 42.4 21.9 Erie County 280,843 114,322 1,558.40 756.46 801.95 350.2 142.6 Fayette County 148,644 66,490 798.00 7.86 790.14 188.1 84.1 Forest County 4,946 8,701 431.40 3.28 428.12 11.6 20.3 Franklin County 129,313 53,803 772.63 0.71 771.92 167.5 69.7 Fulton County 14,261 6,790 438.03 0.46 437.57 32.6 15.5 Greene County 40,672 16,678 577.95 2.09 575.86 70.6 29.0 Huntingdon County 45,586 21,058 889.03 14.98 874.05 52.2 24.1 Indiana County 89,605 37,250 834.29 5.02 829.27 108.1 44.9 Jefferson County 45,932 22,104 656.87 1.39 655.48 70.1 33.7 Juniata County 22,821 10,031 393.57 1.98 391.59 58.3 25.6 Lackawanna County 213,295 95,362 464.51 5.88 458.63 465.1 207.9 Lancaster County 470,658 179,990 983.81 34.75 949.06 495.9 189.7 Lawrence County 94,643 39,635 362.76 2.30 360.46 262.6 110.0 Lebanon County 120,327 49,320 362.60 0.74 361.86 332.5 136.3 Lehigh County 312,090 128,910 348.34 1.68 346.66 900.3 371.9 Luzerne County 319,250 144,686 907.13 16.32 890.81 358.4 162.4 Lycoming County 120,044 52,464 1,243.77 8.91 1,234.85 97.2 42.5 McKean County 45,936 21,644 984.17 2.60 981.57 46.8 22.1 Mercer County 120,293 49,859 682.57 10.76 671.82 179.1 74.2 Mifflin County 46,486 20,745 414.60 2.75 411.86 112.9 50.4 Monroe County 138,687 67,581 617.42 8.92 608.50 227.9 111.1 Montgomery County 750,097 297,434 487.45 4.33 483.12 1,552.6 615.7 Montour County 18,236 7,627 132.30 1.55 130.75 139.5 58.3 Northampton County 267,066 106,710 377.36 3.56 373.80 714.5 285.5 Northumberland County 94,556 43,164 477.38 17.47 459.91 205.6 93.9 Perry County 43,602 18,941 555.77 2.25 553.52 78.8 34.2 Philadelphia County 1,517,550 661,958 142.64 7.55 135.09 11,233.6 4,900.1 Pike County 46,302 34,681 566.64 19.83 546.81 84.7 63.4 Potter County 18,080 12,159 1,081.42 0.25 1,081.17 16.7 11.2 Schuylkill County 150,336 67,806 782.61 4.25 778.36 193.1 87.1 Snyder County 37,546 14,890 332.16 0.95 331.20 113.4 45.0 Somerset County 80,023 37,163 1,081.17 6.51 1,074.66 74.5 34.6 Sullivan County 6,556 6,017 452.35 2.41 449.94 14.6 13.4 Susquehanna County 42,238 21,829 832.40 9.54 822.86 51.3 26.5 Tioga County 41,373 19,893 1,137.30 3.58 1,133.73 36.5 17.5 Union County 41,624 14,684 317.12 0.39 316.73 131.4 46.4 Venango County 57,565 26,904 683.02 7.98 675.04 85.3 39.9 Warren County 43,863 23,058 897.81 14.36 883.45 49.6 26.1 Washington County 202,897 87,267 860.95 3.86 857.09 236.7 101.8 Wayne County 47,722 30,593 750.54 21.32 729.22 65.4 42.0 Westmoreland County 369,993 161,058 1,036.34 10.86 1,025.48 360.8 157.1 Wyoming County 28,080 12,713 404.79 7.59 397.20 70.7 32.0 York County 381,751 156,720 910.25 5.80 904.45 422.1 173.3

Area in square miles

Density per square mile of land area

Geographic area Population

Housing

units

Total area

Water

area

Land area Population

Housing

units (X) Not applicable Source: U.S. Census Bureau, Census 2000 Summary File 1

Northwest Pennsylvania Regional Planning & Development Commission CONNECT NW PA Broadband Study and Action Plan Supplemental Report

December 23, 2003 Page 142

Clarion County

U.S. Census Data

Table DP-1. Profile of General Demographic Characteristics: 2000 Geographic area: Clarion County, Pennsylvania [For information on confidentiality protection, nonsampling error, and definitions, see text] Subject Number Percent Total population. . . . . . . . . . . . . . . . . . . . . . . . . . 41,765 100.0 SEX AND AGE Male . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 20,162 48.3 Female. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 21,603 51.7 Under 5 years . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 2,267 5.4 5 to 9 years . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 2,500 6.0 10 to 14 years . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 2,669 6.4 15 to 19 years . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 3,798 9.1 20 to 24 years . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 4,221 10.1 25 to 34 years . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 4,765 11.4 35 to 44 years . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 5,748 13.8 45 to 54 years . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 5,386 12.9 55 to 59 years . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 2,124 5.1 60 to 64 years . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1,951 4.7 65 to 74 years . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 3,348 8.0 75 to 84 years . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 2,244 5.4 85 years and over . . . . . . . . . . . . . . . . . . . . . . . . . . . . 744 1.8 Median age (years) . . . . . . . . . . . . . . . . . . . . . . . . . . . 36.3 (X) 18 years and over . . . . . . . . . . . . . . . . . . . . . . . . . . . . 32,730 78.4 Male . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 15,543 37.2 Female. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 17,187 41.2 21 years and over . . . . . . . . . . . . . . . . . . . . . . . . . . . . 29,352 70.3 62 years and over . . . . . . . . . . . . . . . . . . . . . . . . . . . . 7,479 17.9 65 years and over . . . . . . . . . . . . . . . . . . . . . . . . . . . . 6,336 15.2 Male . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 2,691 6.4 Female. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 3,645 8.7 RACE One race . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 41,548 99.5 White . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 40,998 98.2 Black or African American . . . . . . . . . . . . . . . . . . . 329 0.8 American Indian and Alaska Native . . . . . . . . . . . 45 0.1 Asian . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 142 0.3 Asian Indian . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 35 0.1 Chinese . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 26 0.1 Filipino . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 20 - Japanese. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 7 - Korean. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 26 0.1 Vietnamese. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 9 - Other Asian 1 . . . . . . . . . . . . . . . . . . . . . . . . . . . . 19 - Native Hawaiian and Other Pacific Islander. . . . 2 - Native Hawaiian. . . . . . . . . . . . . . . . . . . . . . . . . . 2 - Guamanian or Chamorro . . . . . . . . . . . . . . . . . . - - Samoan. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . - - Other Pacific Islander 2 . . . . . . . . . . . . . . . . . . . - - Some other race . . . . . . . . . . . . . . . . . . . . . . . . . . . 32 0.1 Two or more races . . . . . . . . . . . . . . . . . . . . . . . . . . . 217 0.5 Race alone or in combination with one or more other races: 3

White . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 41,200 98.6 Black or African American . . . . . . . . . . . . . . . . . . . . . 396 0.9 American Indian and Alaska Native . . . . . . . . . . . . . 133 0.3 Asian . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 189 0.5 Native Hawaiian and Other Pacific Islander. . . . . . 9 - Some other race . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 62 0.1 Subject Number Percent HISPANIC OR LATINO AND RACE Total population. . . . . . . . . . . . . . . . . . . . . . . . . . 41,765 100.0 Hispanic or Latino (of any race) . . . . . . . . . . . . . . . . 172 0.4

Northwest Pennsylvania Regional Planning & Development Commission CONNECT NW PA Broadband Study and Action Plan Supplemental Report

December 23, 2003 Page 143