Brief Overview of International Financial Markets

Brief Overview of International Financial Markets.

Dec 26, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Brief Overview of International Financial Markets

Topics

• Basic functions/foundation• Key definitions• International payments system• Simple model of international finance• Currency swaps• Major international markets

Financial Market Functions

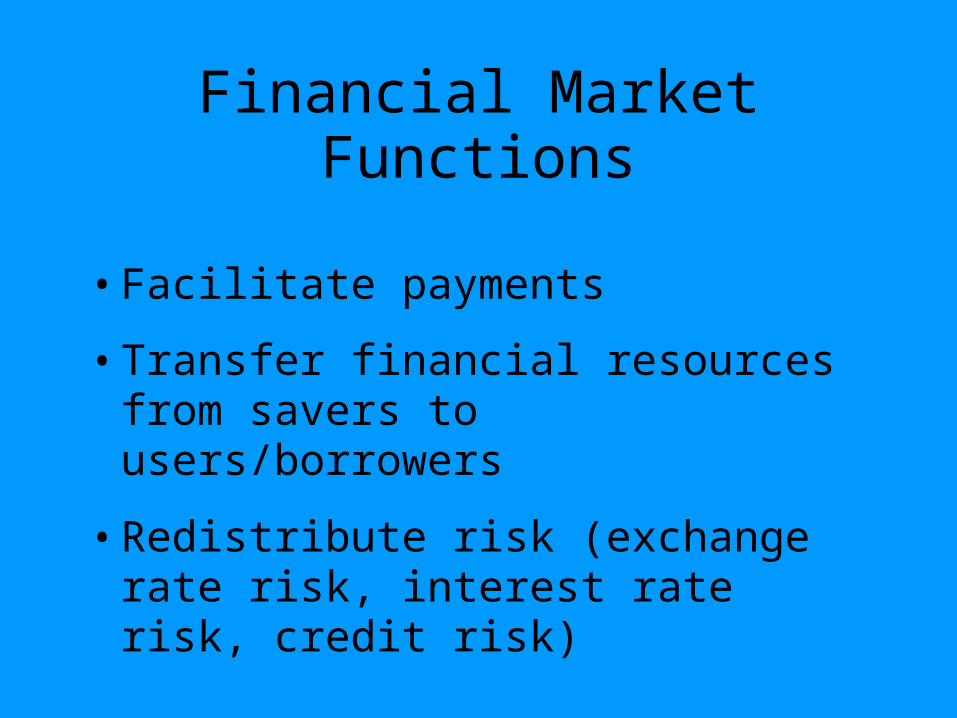

• Facilitate payments

• Transfer financial resources from savers to users/borrowers

• Redistribute risk (exchange rate risk, interest rate risk, credit risk)

Foundations of Strong Financial Markets

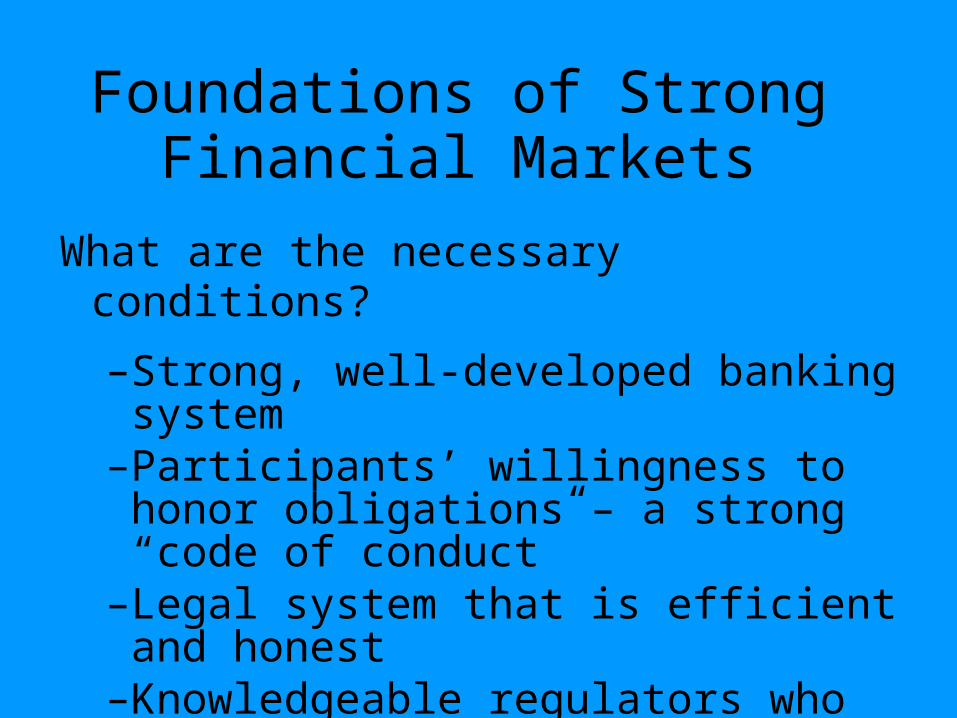

What are the necessary conditions?

–Strong, well-developed banking system–Participants’ willingness to honor

obligations – a strong “code of conduct”–Legal system that is efficient and honest–Knowledgeable regulators who

encourage innovation (up to a point)

Key Definitions• The Euro (€)• Eurocurrency markets – (not euros)• LIBOR

– “London Interbank Offer Rate” - short-term loans in Eurodollars

• Similar to fed funds rate – (not Discount rate)• Officially fixed once per day by large London

banks (British Bankers' Association)

• Euribor: interbank rate among EU banks• Financial derivatives

International Payments System

• Vital part of financial system infrastructure – the highway

• Nearly all significant international payments move via the banking system

• Depends upon banks keeping deposits with each other – “interbank deposits”

International Financial Markets

• Sectors

–Eurocurrency deposits/loans

–International bonds

–Foreign exchange

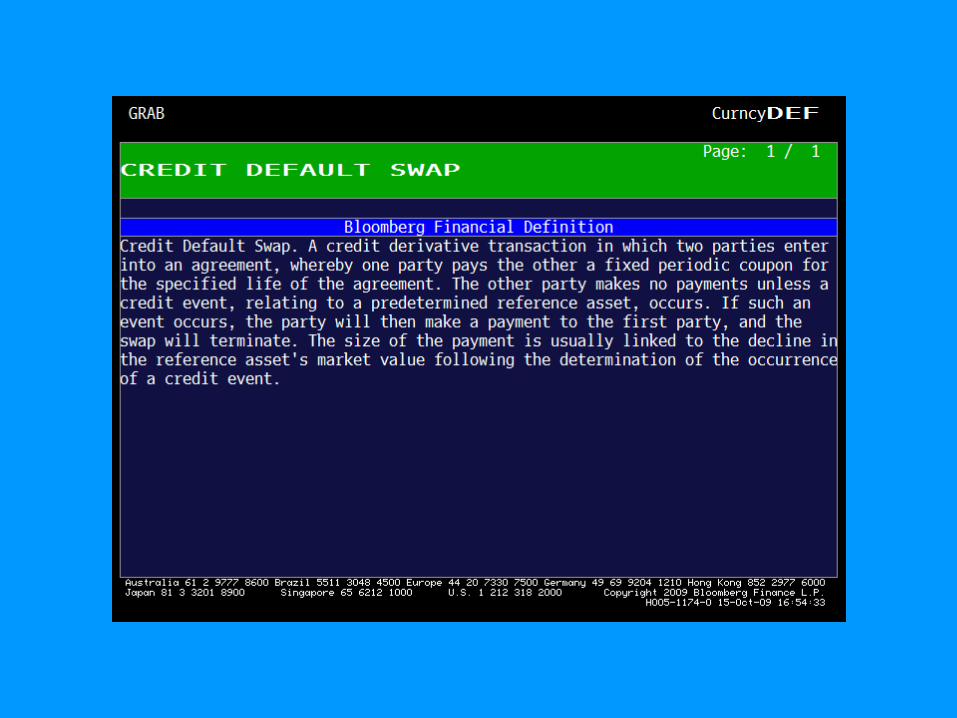

–Derivatives (currencies, interest rates, credit default swaps)

• Characteristics

–Wholesale

–Lightly regulated

–Continuous innovation

Eurocurrency Finance

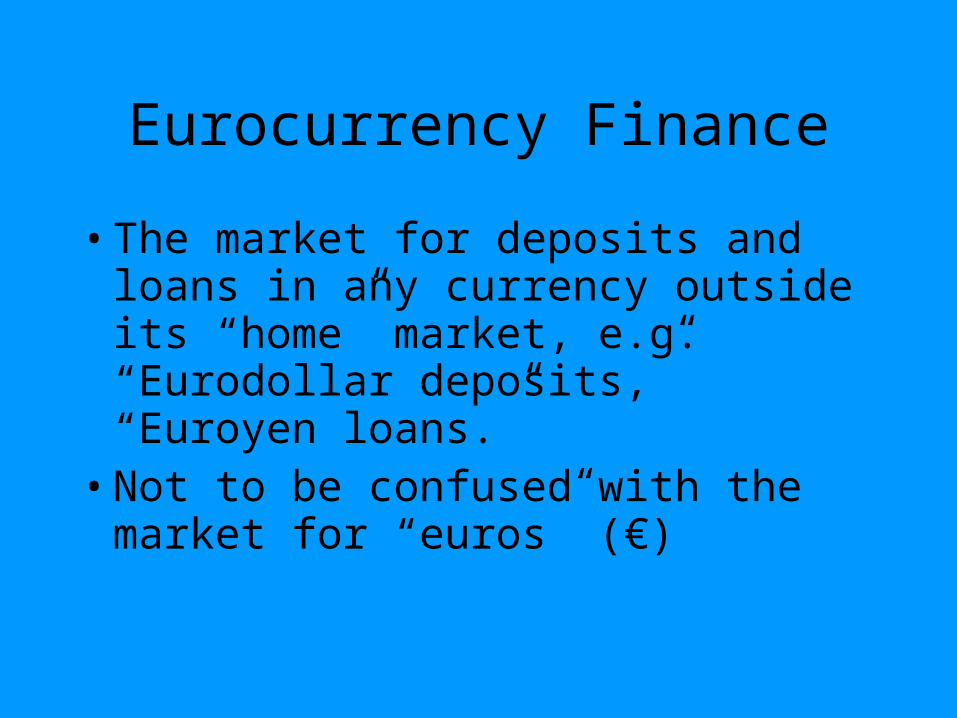

• The market for deposits and loans in any currency outside its “home” market, e.g. “Eurodollar deposits,” “Euroyen loans.”

• Not to be confused with the market for “euros” (€)

Eurocurrency Loan/Deposit Market

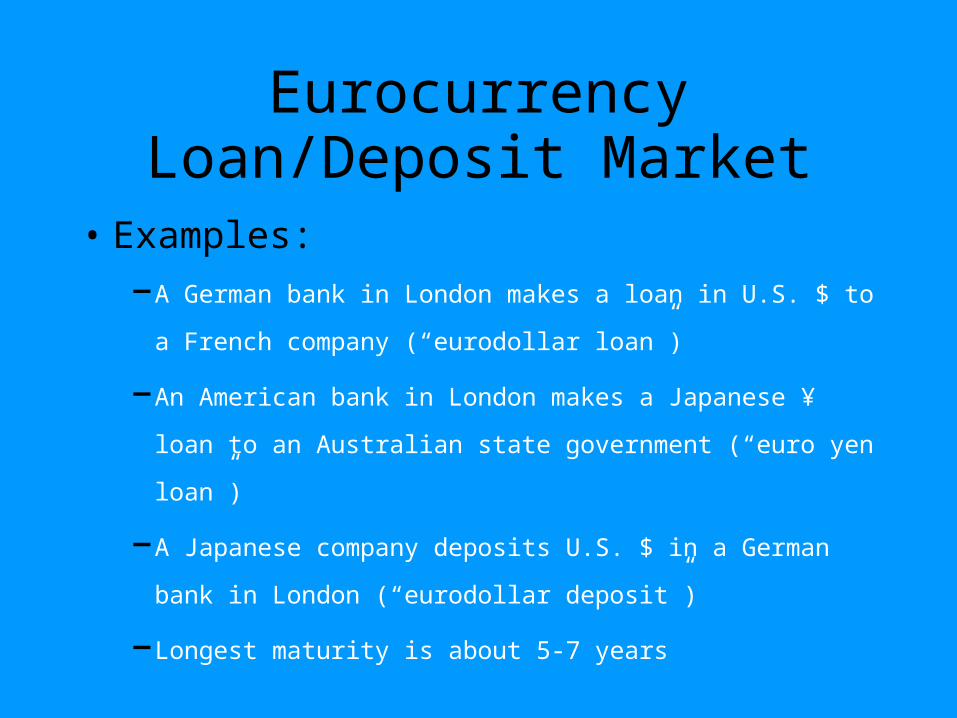

• Examples:

–A German bank in London makes a loan in U.S. $ to a French

company (“eurodollar loan”)

–An American bank in London makes a Japanese ¥ loan to an

Australian state government (“euro yen loan”)

–A Japanese company deposits U.S. $ in a German bank in

London (“eurodollar deposit”)

– Longest maturity is about 5-7 years

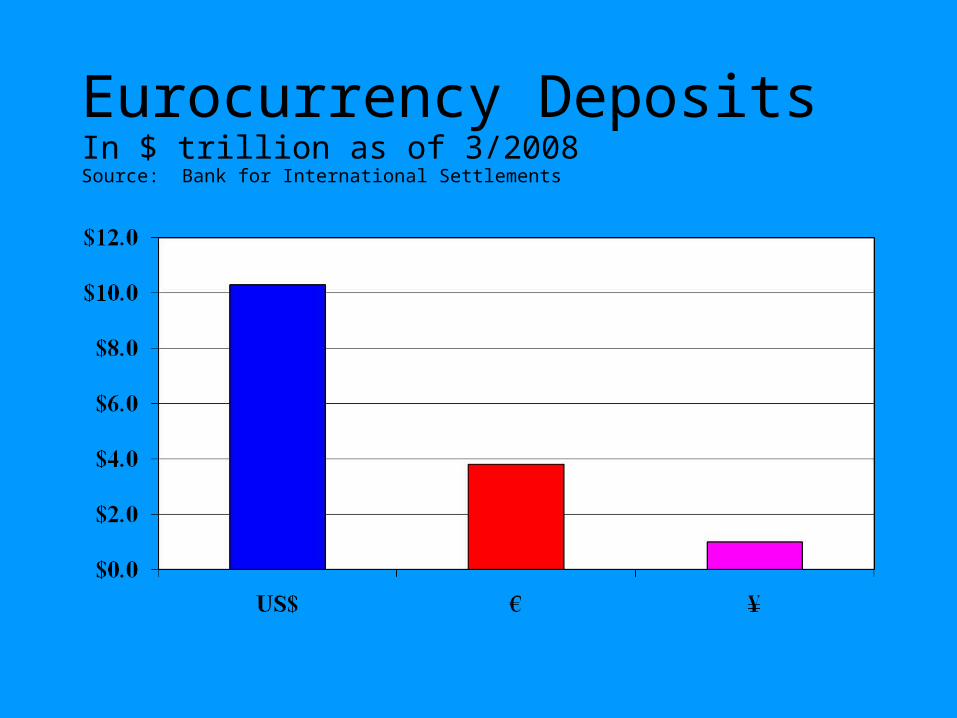

Eurocurrency DepositsIn $ trillion as of 3/2008Source: Bank for International Settlements

BIS Data on Cross-Border Liabilities

Why Most Financial Institutions are Fragile – Even in Good Times Leverage: High level of short-term debt

(liabilities) to equity (10:1 or greater)• Short-term liabilities often need to finance

longer term assets/investments (eg; loans)

• Value of many assets (loans, mortgages) subject to rapid devaluation

• Interbank deposits are a substantial share of large bank liabilities

Critical Aspect of the Financial Crisis of 2008

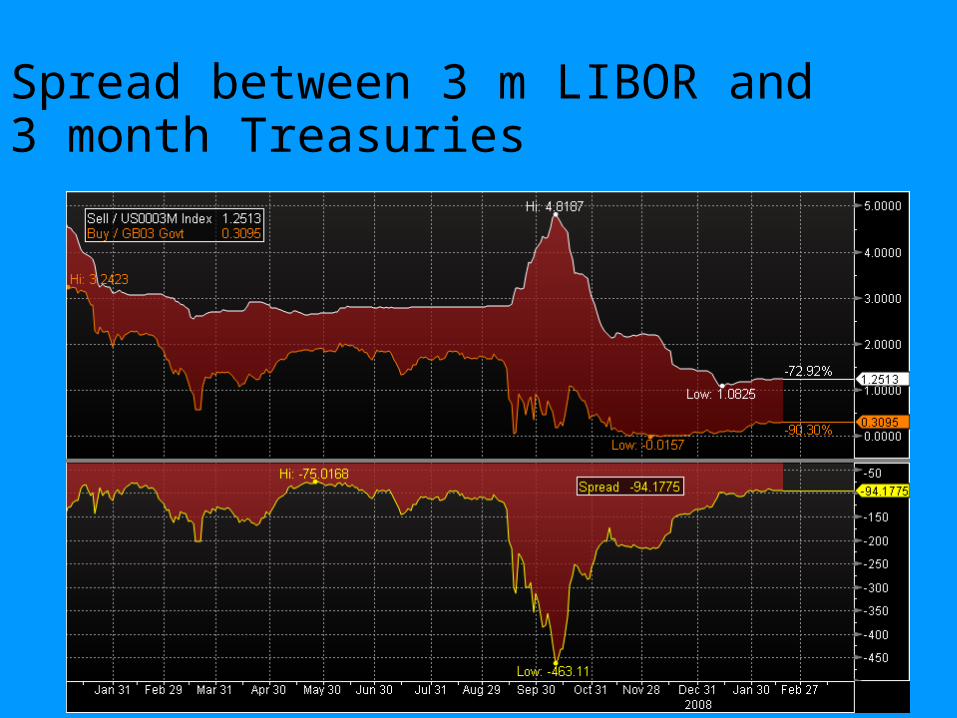

• Financial Markets responded to the credit crisis in 2008 by driving 3 month LIBOR rates up sharply while forcing rates on 3 month Treasury bills down dramatically by excess demand.

• Interest rate spread widened to over 400 basis points by October . . .

3 month LIBOR vs 3 month Treasuries

Spread between 3 month LIBORAnd 3 month Treasuries

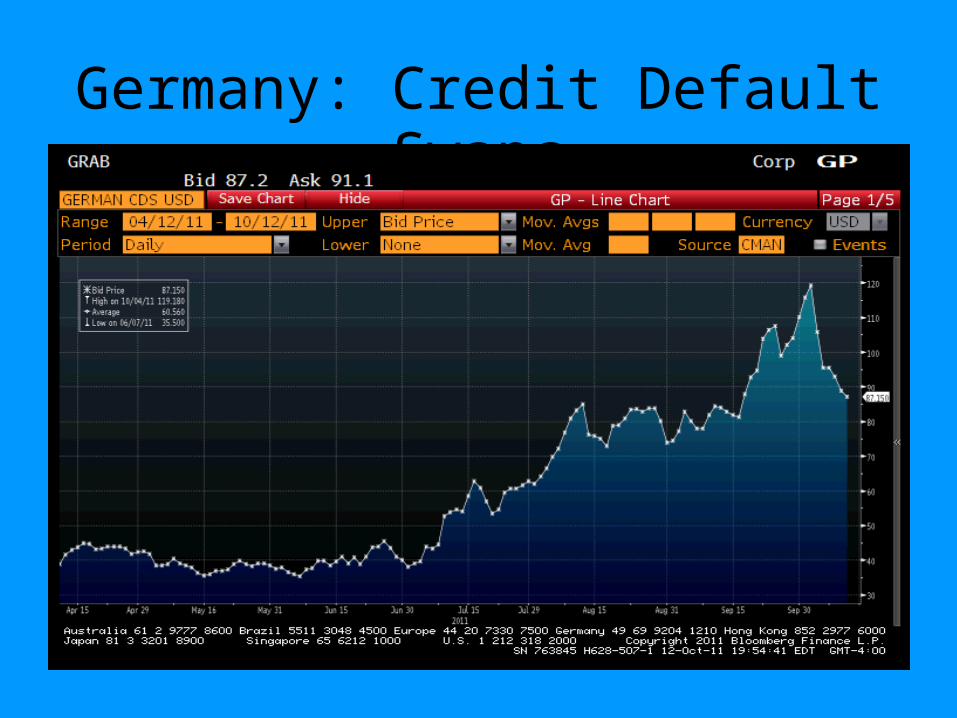

Another Example of the Financial Crisis of 2008

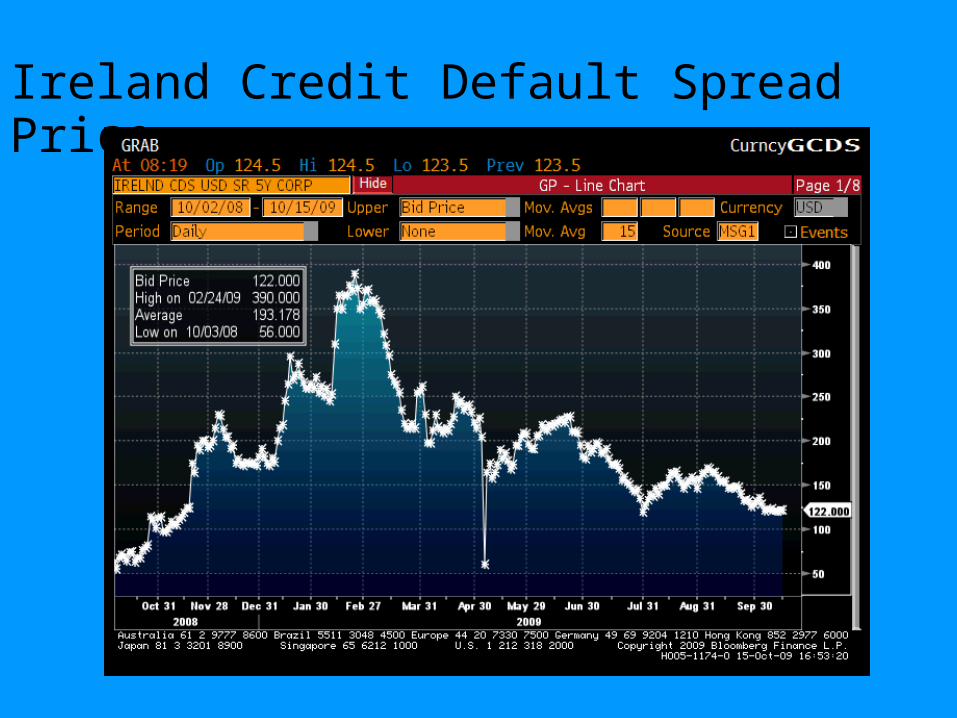

• Corporate and Sovereign Credit Default Swaps rose rapidly, especially for weaker economies.

Germany: Credit Default Swaps

Ireland: Credit Default Swaps

Greece: Credit Default Swaps

Credit Default Swaps Outstanding

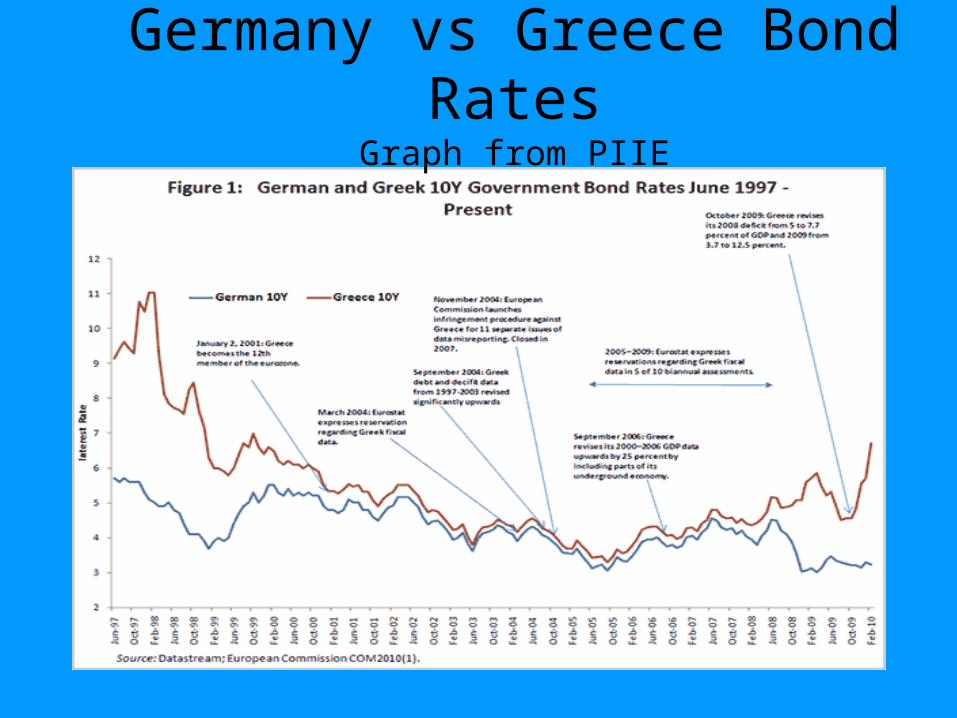

Germany vs Greece Bond Rates

Graph from PIIE

Greece vs Germany

International Interest Rates

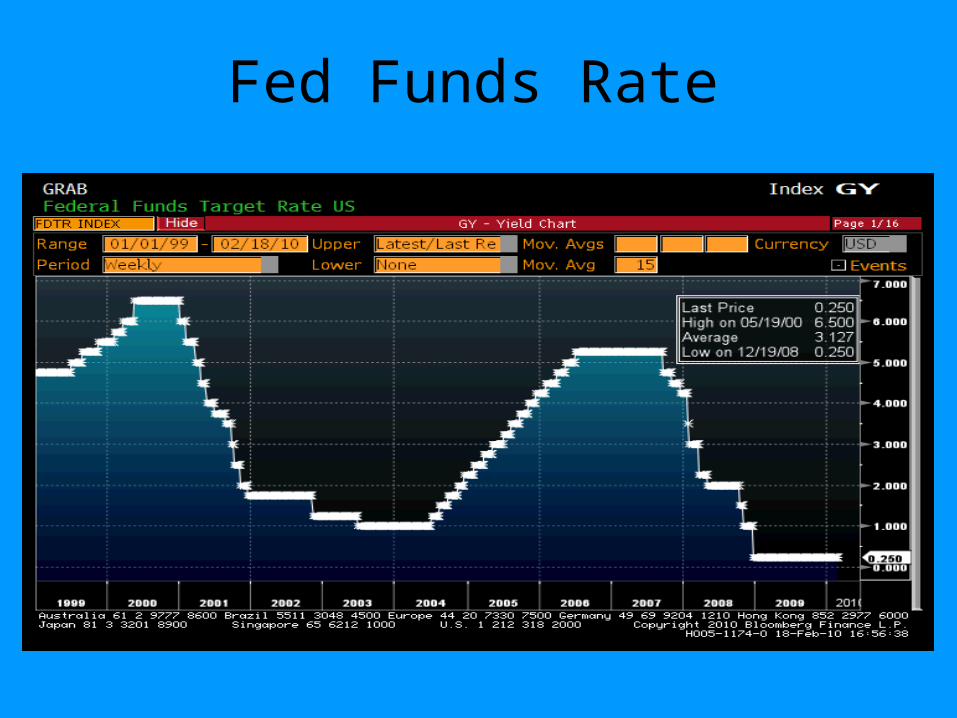

US Fed Funds Rate

Euro Official Rate

Clearing House for International Payments

(CHIPS)

• For US dollar payments between international banks – Created 1970

• Bank owned• About 46 member banks (30% US)• Based in New York City with Fed Bank of NY• Average daily activity

– 240,000 payments

– $1.2 trillion in value

• What if system breaks down?

HOW CHIPS WORKS

BARCLAYS BANK

CITIBANK

DEUTSCHE BANK

SUMITOMO Mitsui BANK

CHIPS

A

B

C

L

PNC

JI

H

G

F

ED

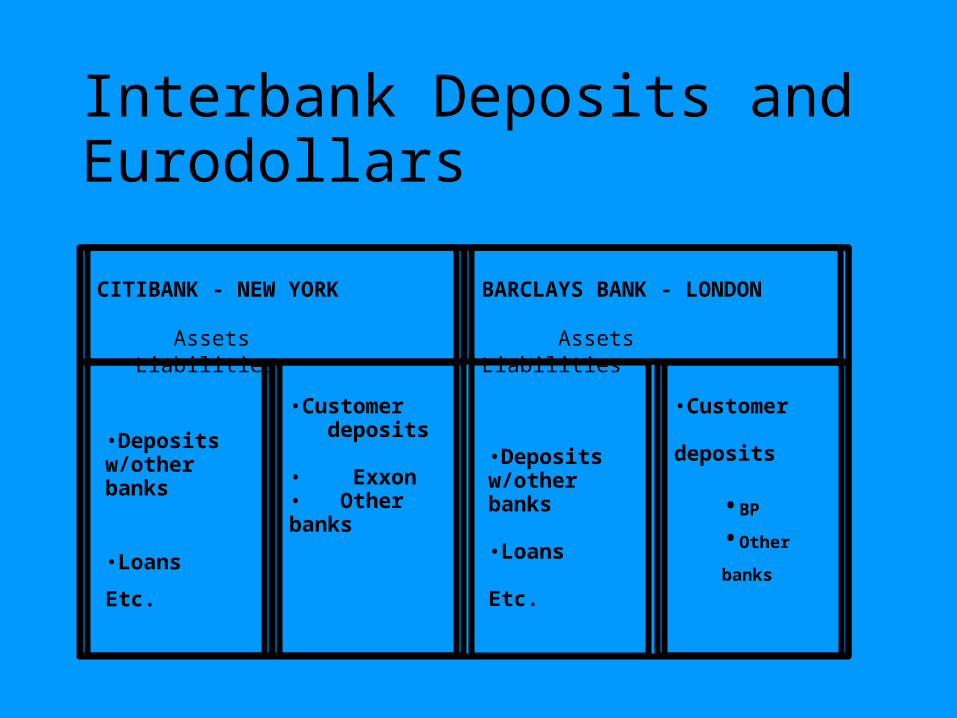

Interbank Deposits and Eurodollars

1. Exxon in NYC sends British Petroleum in London a $1 million check drawn on Citibank New York

2. BP deposits check with Barclays Bank, London3. Barclays Bank presents check to Citibank for

payment (via CHIPS)4. Citibank debits Exxon account and credits Barclays

account with Citibank

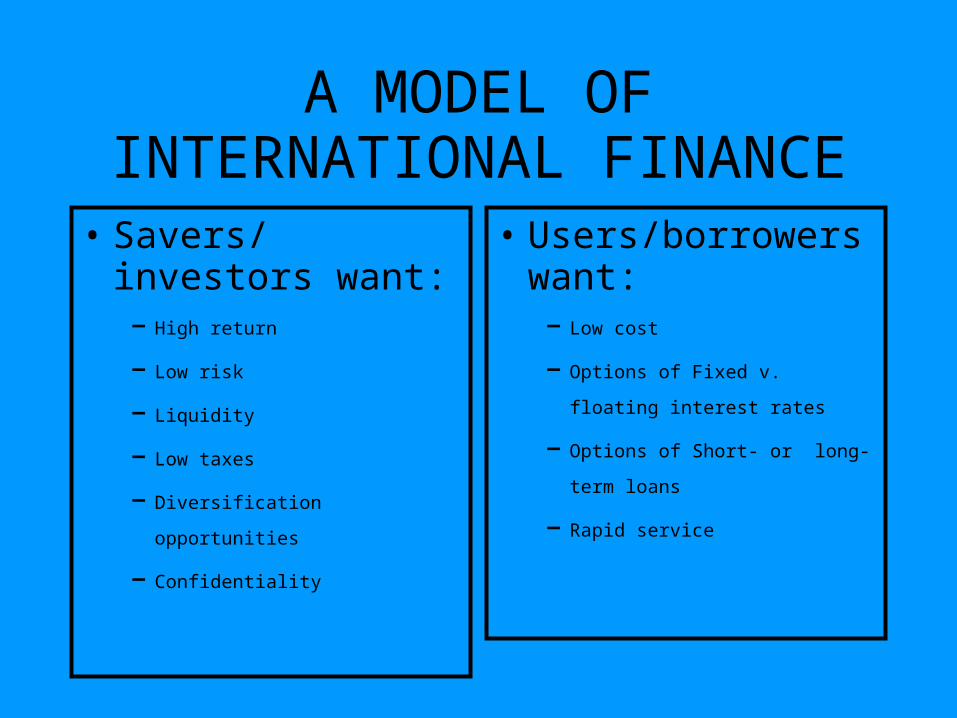

A Simple Model of International Finance

• Two countries• Four parties

– Savers/investors

– Users/borrowers

– Transactors/banks (middlemen)

– Authorities: i.e., Regulators/Government Agencies

A MODEL OF INTERNATIONAL FINANCE

• Savers/investors want:– High return

– Low risk

– Liquidity

– Low taxes

– Diversification opportunities

– Confidentiality

• Users/borrowers want:– Low cost

– Options of Fixed v. floating interest

rates

– Options of Short- or long-term loans

– Rapid service

A Simple Model of International Finance

• Transactors (banks) want:– High volume

– Wide spread (profit)

– Low taxes

– Stable political environment

• Authorities want:– Tax revenue

– Protect/help small customers

– Create jobs

– Reduce difficulties for monetary

policy

– Control

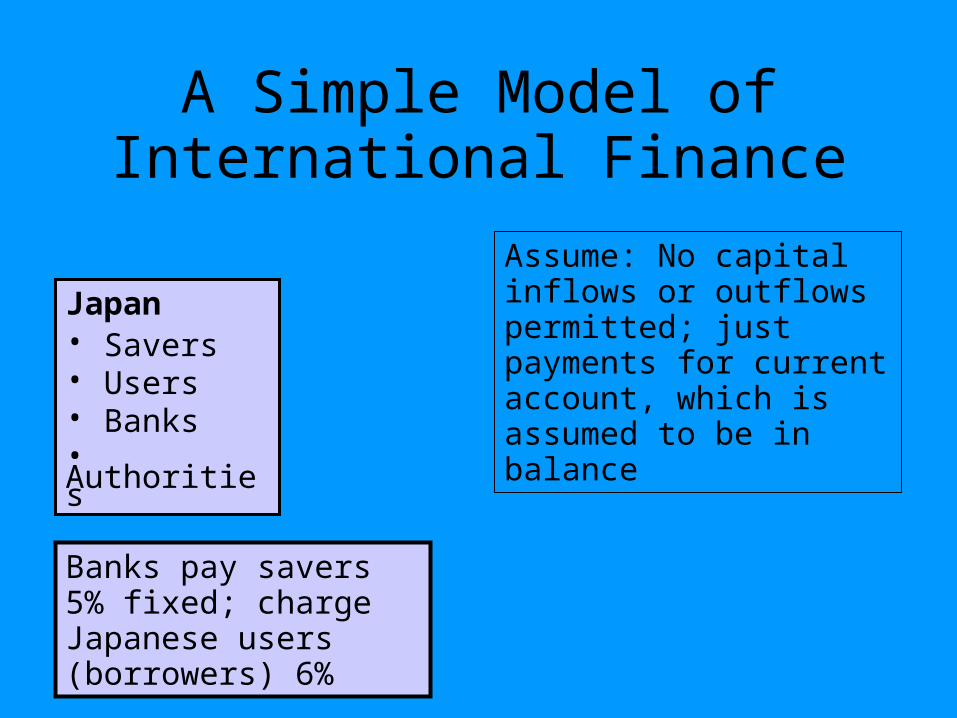

A Simple Model of International Finance

Japan• Savers• Users• Banks• Authorities

Banks pay savers 5% fixed; charge Japanese users (borrowers) 6%

Assume: No capital inflows or outflows permitted; just payments for current account, which is assumed to be in balance

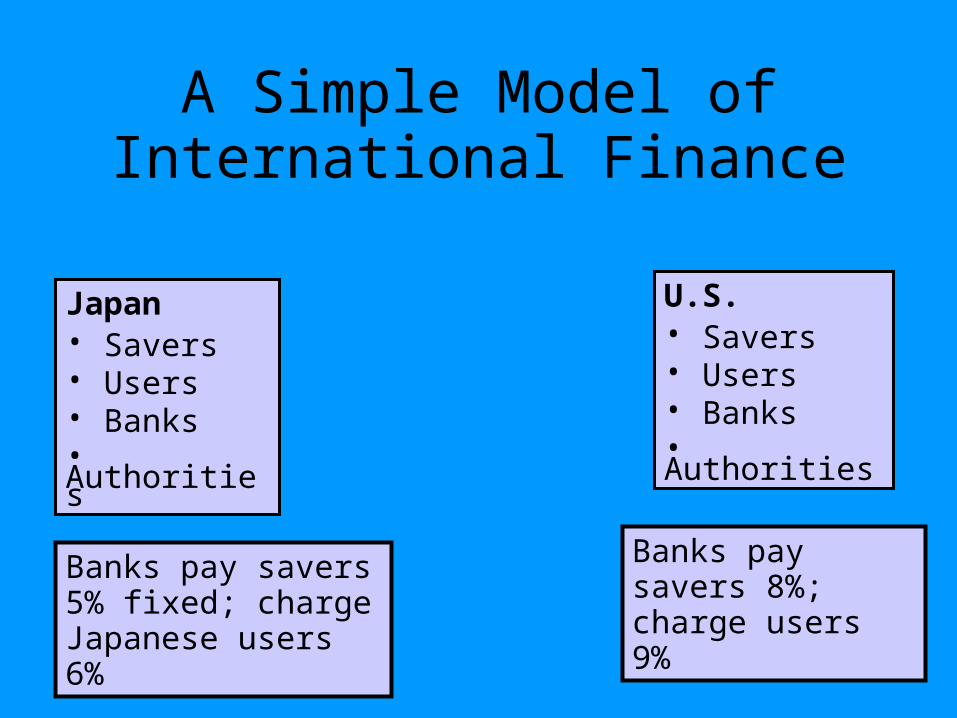

A Simple Model of International Finance

Japan• Savers• Users• Banks• Authorities

U.S.• Savers• Users• Banks• Authorities

Banks pay savers 5% fixed; charge Japanese users 6%

Banks pay savers 8%; charge users 9%

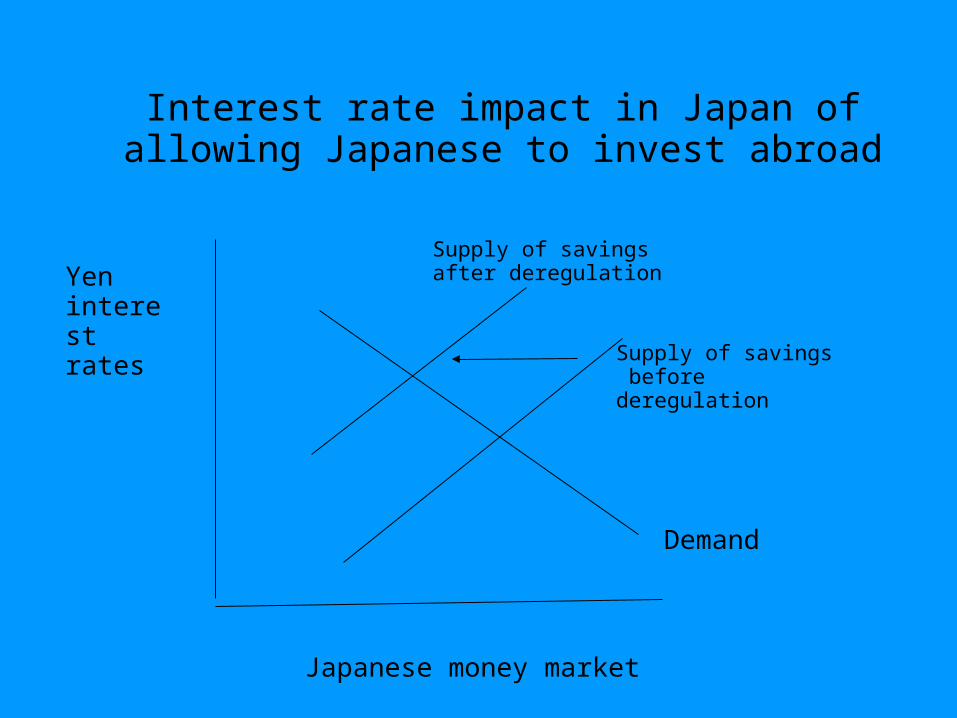

Impact of Relaxing Capital Controls

• Japan

–Savings flow from Japan to higher rates in U.S.

– Japanese banks increase savings rates to keep deposits at home

–Upward pressure on Japanese lending rates; Japanese users

pay more

– Japanese bankers lose business (unless they open branches in

the US)

– Japanese authorities concerned at outflow, exchange rate issues

Interest rate impact in Japan of allowing Japanese to invest abroad

Demand

Yen interest rates

Japanese money market

Supply of savings before deregulation

Supply of savings after deregulation

Affect on United States

• U.S.– Savings flow into the U.S.

– Downward pressure on U.S. interest rates

– U.S. users have lower borrowing costs

– U.S. banks have more business

– U.S. authorities pleased at lower interest rates, but exchange rate may be

under upward pressure, hurting exports

Interest rate impact in US Savings Market of allowing Japanese to invest abroad

Demand

US$ interest rates

US money market

Supply of savings after deregulation

Supply of savings before deregulation

General Implications

• Very difficult to liberalize “halfway;” • Once capital flows in any direction are

permitted, political pressures build up to liberalize completely

• Savers/investors want diversification by type of financial asset, as well as higher returns; international markets can help them achieve these goals

Further Implications

• Users/borrowers of capital want lower costs, new products, services that other countries may offer

• First openings can create substantial opportunities for arbitrage

Currency Swap Marketand Comparative Advantage

A very large and growing international market which permits companies, governments, and international financial institutions to reduce their borrowing costs and risks. Longer term up to 10 years.

A form of “financial engineering” that rests on the principle of “comparative advantage” in borrowing costs for each party involved in transaction.

Currency Swap Typically consists of an agreement between

two parties to exchange principal and fixed interest rate interest payments on a loan involving two currencies.

Differs from a forex swap (or FX swap) which is a more or less simultaneous purchase and sale of identical amounts of one currency for another with two different dates. Includes spot and forward transactions, often offsetting each other. Example is Central Bank Liquidity Swap

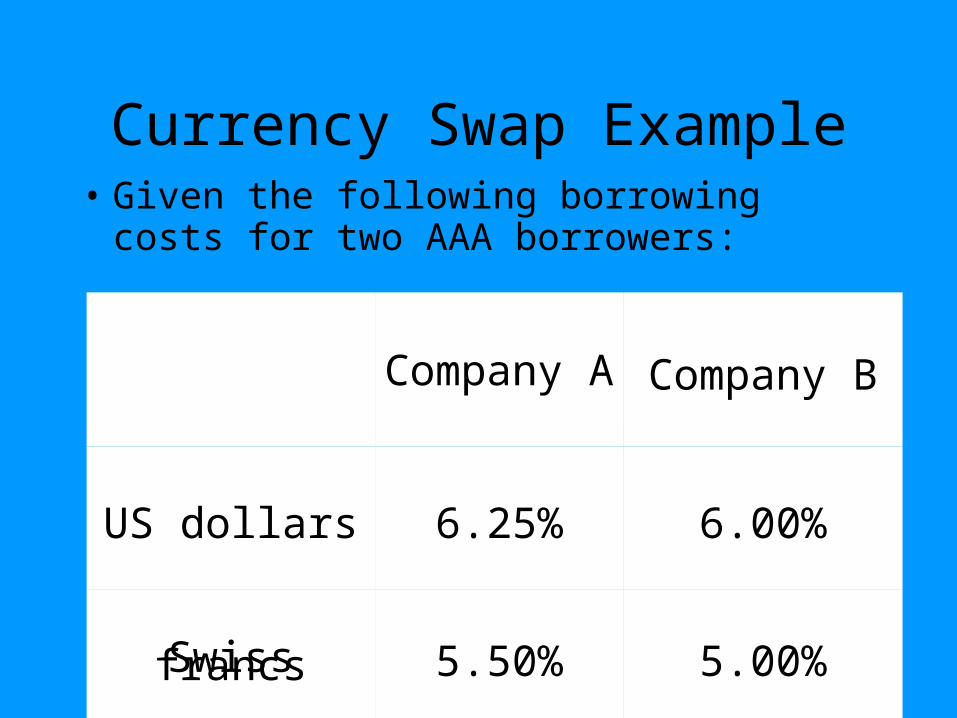

Currency Swap Example• Given the following borrowing costs for two

AAA borrowers:

Company A Company B

US dollars 6.25% 6.00%

Swiss francs 5.50% 5.00%

Currency Swap Example (cont.)

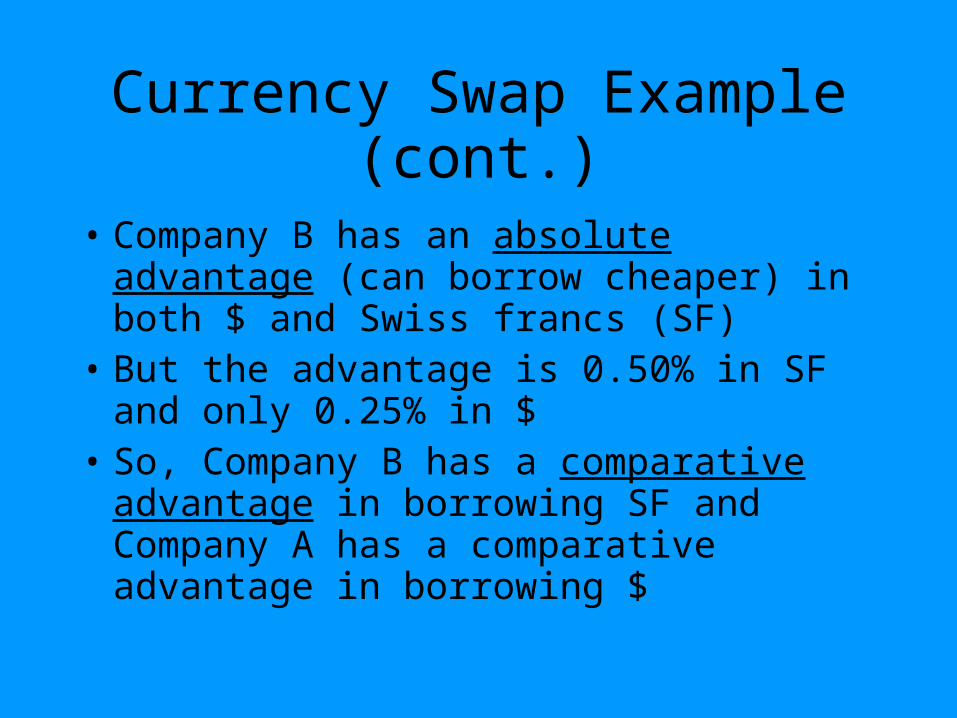

• Company B has an absolute advantage (can borrow cheaper) in both $ and Swiss francs (SF)

• But the advantage is 0.50% in SF and only 0.25% in $

• So, Company B has a comparative advantage in borrowing SF and Company A has a comparative advantage in borrowing $

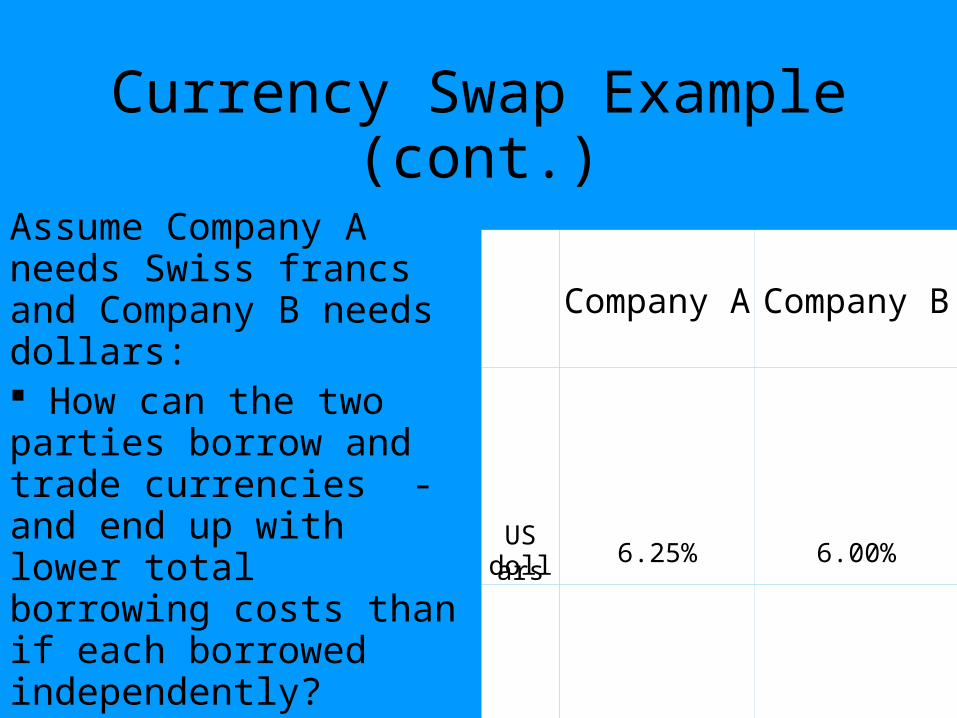

Currency Swap Example (cont.)

Assume Company A needs Swiss francs and Company B needs dollars: How can the two parties borrow and trade currencies - and end up with lower total borrowing costs than if each borrowed independently?

Company A Company B

US dollars

6.25% 6.00%

Swiss francs

5.50% 5.00%

Currency Swap Example (cont.)

Company A Company B

$ Market SF Market

$ at 6.25% SF at

5.00%

SF at 5.625%

$ at 6.50%

Currency Swap Example (cont.)Net Cost Calculation

Company A

$ borrowing 6.25%Less $ lending 6.50%

- 0.25%Plus SFr cost 5.625% Net Cost SF 5.375%w/o swap: 5.50%

Company B

SF borrowing 5.00%Less SFr lending 5.625%

- 0.625%Plus $ costs 6.50% Net Cost $ 5.875%w/o swap 6.00%

Why Does the Swap Work?

• Although both borrowers are rated AAA, the $ market and the SF market disagree about the relative attractiveness of buying their bonds

• Difference in New York is:6.25 – 6.00 = 0.25• Difference in Switzerland is:5.50 – 5.00 = 0.50

Swaps are a form of Arbitrage

Disagreement between $ and SF market about pricing risk open up opportunities to engage in transactions

If enough transactions are undertaken, interest rate differential of 0.25% will disappear

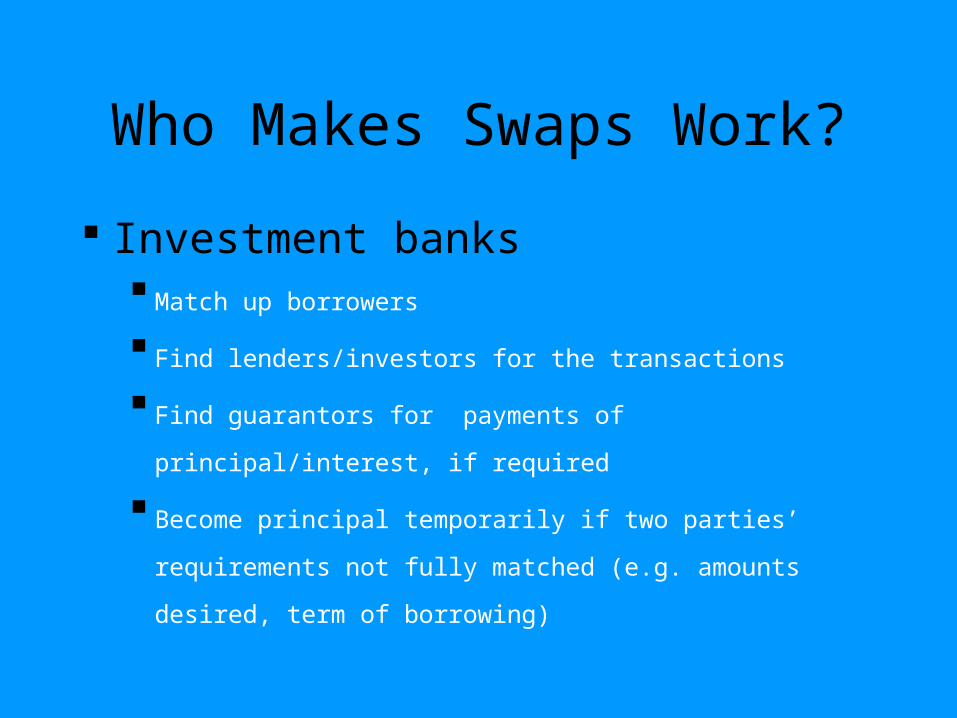

Who Makes Swaps Work?

Investment banks Match up borrowers

Find lenders/investors for the transactions

Find guarantors for payments of principal/interest, if required

Become principal temporarily if two parties’ requirements not fully

matched (e.g. amounts desired, term of borrowing)

Spread between 3 m LIBOR and 3 month Treasuries

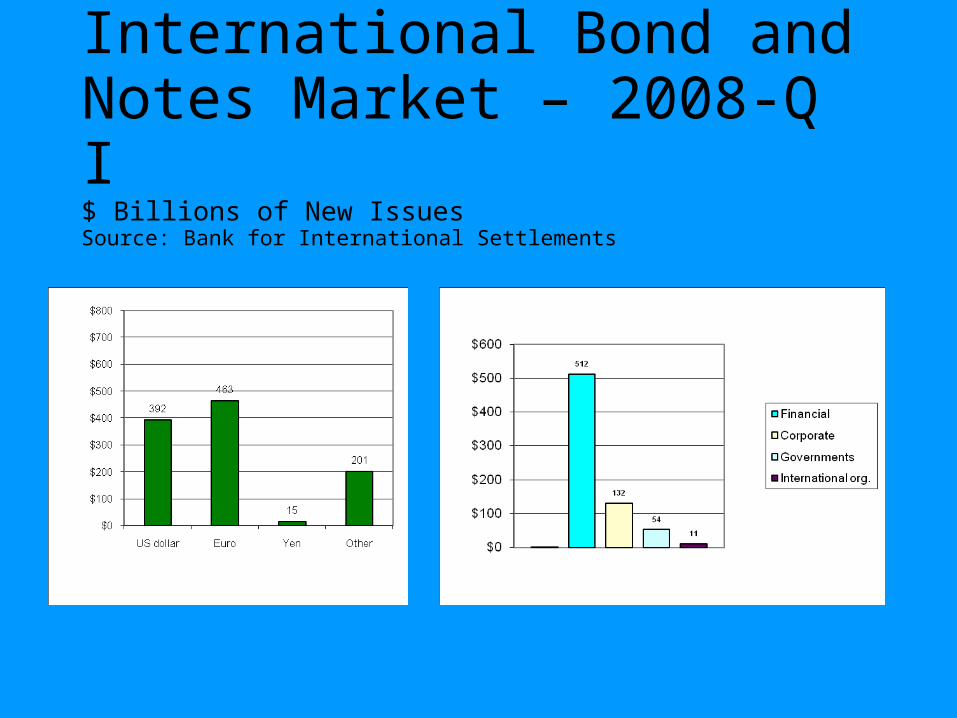

International Bond and Notes Market• Investors:

– Collective funds (mutual funds, hedge funds, etc.)

– Pension funds for employees in corporations and governments

– Banks

– Insurance companies

– Some individuals

• Markets

– “Over-the-counter”

International Bond and Notes Market – 2008-Q I$ Billions of New IssuesSource: Bank for International Settlements

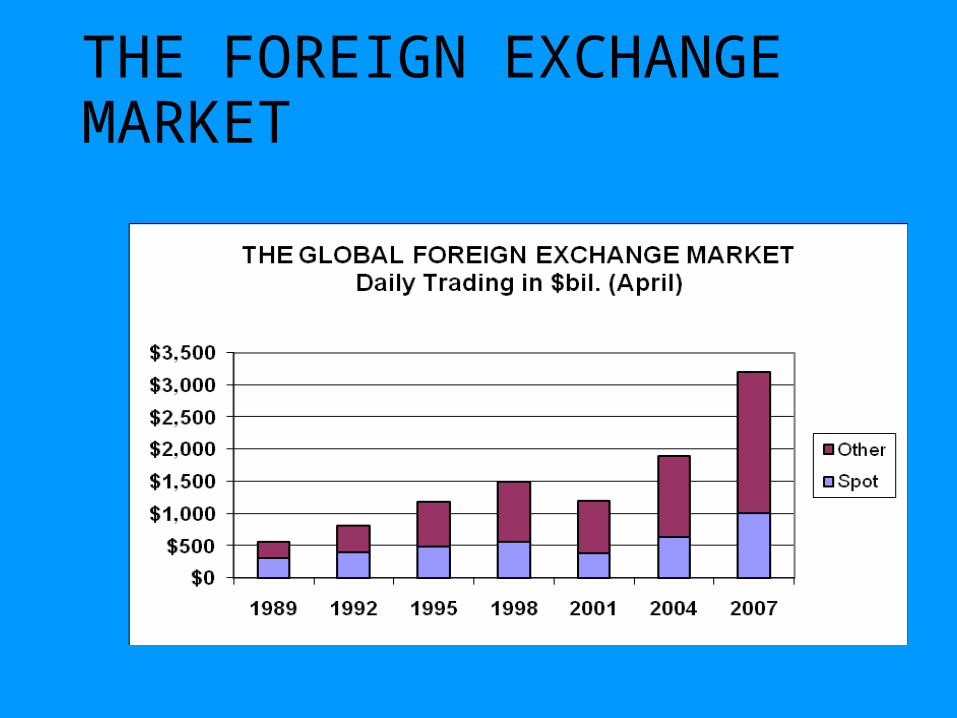

The Foreign Exchange Market

• Historically, an “informal dealer market” among large banks in the major financial centers

• The largest global financial market• Very decentralized – no centralized

regulation

MAJOR TRADING CENTERS% of Global MarketApril 2007

THE FOREIGN EXCHANGE MARKET

CHANGING STRUCTURE OF THE MARKET• Euro (€) has become important

currency, replacing German mark, Italian lira, etc.

• Investment-related v. trade related activity is increasing

• Impact of electronic trading on brokers• Corporate treasurers using more FX

options to implement hedging strategies

THE GLOBAL OTC DERIVATIVES MARKETDaily Turnover, $US billions

The J-Curve Effect

Japan Real GDP Y/Y

Japan CPI Y/y monthly

U.S. Real GDP (Y/Y)

Interbank Deposits and Eurodollars

CITIBANK - NEW YORK

Assets Liabilities

BARCLAYS BANK - LONDON

Assets Liabilities

•Customer deposits

• Exxon• Other banks

•Customer

deposits

•BP

•Other banks

•Deposits w/other banks

•Loans

Etc.

•Deposits w/other banks

•Loans

Etc.

Interbank Deposits and Eurodollars

CITIBANK - NEW YORK

BARCLAYS BANK - LONDON

$ DepositBarclays Bank-London + $500 $ DepositExxon - $500

Barclays $ DepositWith Citibank - New York + $500

$ Deposit British Petroleum +$500

Exxon sends British Petroleum US$

U.S. CPI (Y/Y)

Spread between 3 month LIBOR and 3 month Treasuries

Spread between 3 m LIBOR and 3 month Treasuries

Iceland Credit Default Spread Price

Ireland Credit Default Spread Price

Euro

Euro

Euro Interbank Offered Rate

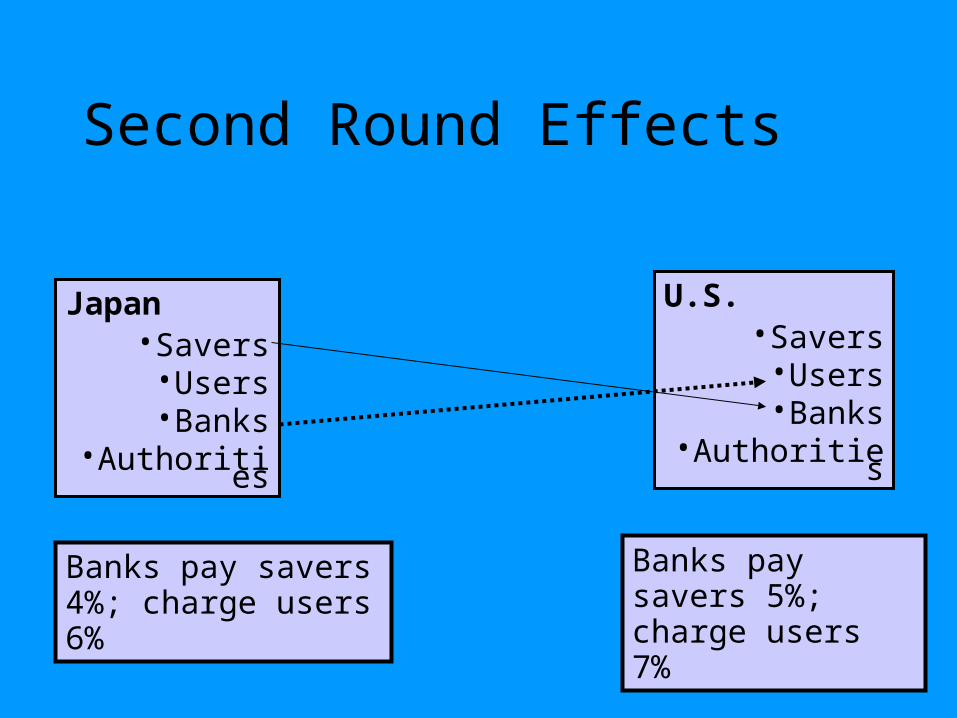

Second Round Effects

Japan•Savers•Users•Banks

•Authorities

U.S.•Savers•Users•Banks

•Authorities

Banks pay savers 4%; charge users 6%

Banks pay savers 5%; charge users 7%

Fed Funds Rate

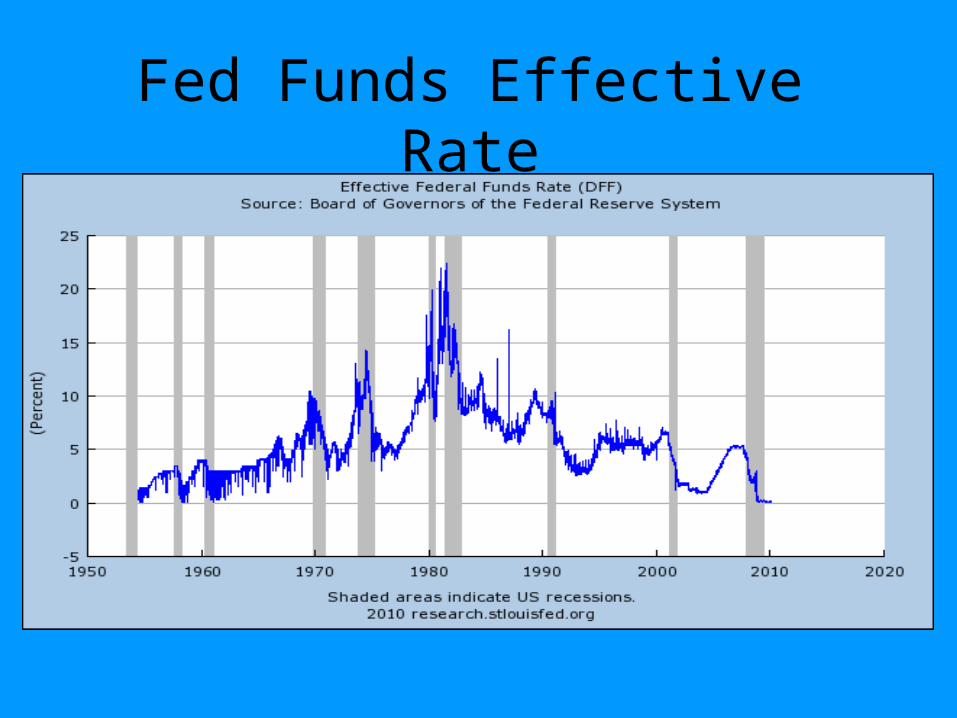

Fed Funds Effective Rate

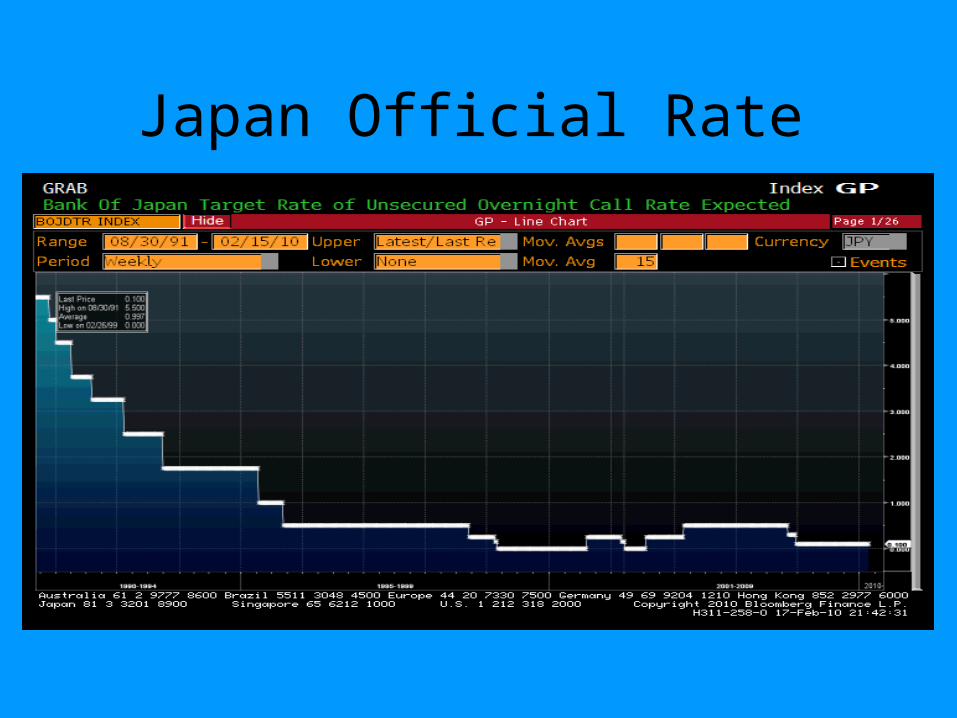

Japan Official Rate

Related Documents