David A. Rosenberg January 5, 2011 Chief Economist & Strategist Economic Commentary [email protected] + 1 416 681 8919 MARKET MUSINGS & DATA DECIPHERING Breakfast with Dave WHILE YOU WERE SLEEPING • What the bulls may be ignoring ... at their peril ... plus some ideas for 2011 • Fed less than impressed with the economic backdrop • Troubles with the profit forecasts • ADP surges! But is it for real? • Slowing trend in core capital expenditure orders ... this may throw a wrench into bullish business spending forecasts for 2011 • U.S. consumer finished the year in decent shape • While you were sleeping: wave of selling across Europe and Asia; U.S. dollar firming; euro slipping; commodity complex heading south; Aussie and Kiwi down; loonie declined from its lofty perch IN THIS ISSUE The markets have turned completely manic. After starting off the year on a very strong footing on virtually no net new information over the outlook, we see a wave of selling today across Europe and Asia (Asian equities were due for a breather — this was the first decline in eight days). Bonds have turned the corner and are back in rally mode . The U.S. dollar, predicta bly since it is still considered to be a less-cyclical and more-safe unit, is firming and is retesting the 100-day moving average (m.a.) after briefly breaking below the 50-day m.a. exactly 24 hours ago. Even though U.S. auto sales came i n a smidgen above expectations at 12.5 million units annualized in December (barely meeting replacement demand), the whispered numbers were far higher due to the huge discounting that had been going on to close the calendar year . And, the news from Reis that sho pping center vacancy rates jumped to 10.9% in Q4 from 10.6% a year ago served as a stark reminder that sorry, no, the American consumer is not really operating on all engines despite a better than expected holiday shopping season that was aided and abetted by what will likely turn out to be a temporary equity wealth effect that pulled down the savings rate for a brief time. Inflationist 's may love the fact that G.E. just announced a hefty price hike on appliances, but there are still other significant pockets of deflation, such as the fact that shopping mall rents are down 1.5% over the past year. The euro is slipping again as Eurozone refinancing challenges come back onto the front burner and People’s Bank of China officials are openly discussing their concerns surrounding China’s disturbing inflation backdrop — hinting at more policy tightening. As a result, the commod ity complex, as well as the resource - based currencies, is heading south (copper is down 1.4% today and oil is off the boil, though the damage to the economy has already been done as we explain below — also see Oil Price Enters Danger Zone on the front page of today’s FT); gold is hugging the 100-day m.a. line nicely a fter yesterday’s descent. The Aussie and Kiwi are down now for three days in a row and the loonie has declined from its lofty perch for the first time in ten sessions. As for credit, it remains to be seen whether we see some spread widening given the massive slate of new corporate issuance on tap for this quarter (see Bond Wave Strikes on Both Sides of the Atlantic on page 12 of th e FT). Pound for pound, we still prefer corporate bonds to equities, which would have been a very good call for 2010 by the way, and we would view any widening in spreads as a terrific buying opportunity. Please see important disclosures at the end of this document. Gluskin Sheff + Associates Inc. is one of Canada’s pre-eminent wealth management firms. Founded in 1984 and focused primarily on high net worth private clients, we are dedicated to meeting the needs of our clients by delivering strong, risk-adjusted returns together with the highest level of personalized client service. For more information or to subscribe to Gluskin Sheff economic reports, visit www.gluskinsheff.com

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

8/8/2019 Breakfast With Dave 010511

http://slidepdf.com/reader/full/breakfast-with-dave-010511 1/15

David A. Rosenberg January 5, 2011 Chief Economist & Strategist Economic [email protected]+ 1 416 681 8919

MARKET MUSINGS & DATA DECIPHERING

Breakfast with DaveWHILE YOU WERE SLEEPING

• What the bulls may beignoring ... at their peril ...plus some ideas for 2011

• Fed less than impressed

with the economicbackdrop

• Troubles with the profitforecasts

• ADP surges! But is it for

real?

• Slowing trend in corecapital expenditure orders... this may throw awrench into bullishbusiness spending forecasts for 2011

• U.S. consumer finished the year in decent shape

• While you were sleeping:wave of selling acrossEurope and Asia; U.S.dollar firming; euroslipping; commoditycomplex heading south;Aussie and Kiwi down;loonie declined from itslofty perch

IN THIS ISSUEThe markets have turned completely manic. After starting off the year on a very

strong footing on virtually no net new information over the outlook, we see a

wave of selling today across Europe and Asia (Asian equities were due for a

breather — this was the first decline in eight days). Bonds have turned the corner

and are back in rally mode. The U.S. dollar, predictably since it is still considered

to be a less-cyclical and more-safe unit, is firming and is retesting the 100-day

moving average (m.a.) after briefly breaking below the 50-day m.a. exactly 24

hours ago.

Even though U.S. auto sales came in a smidgen above expectations at 12.5

million units annualized in December (barely meeting replacement demand), the

whispered numbers were far higher due to the huge discounting that had been

going on to close the calendar year. And, the news from Reis that shopping

center vacancy rates jumped to 10.9% in Q4 from 10.6% a year ago served as a

stark reminder that sorry, no, the American consumer is not really operating on

all engines despite a better than expected holiday shopping season that was

aided and abetted by what will likely turn out to be a temporary equity wealth

effect that pulled down the savings rate for a brief time.

Inflationist's may love the fact that G.E. just announced a hefty price hike on

appliances, but there are still other significant pockets of deflation, such as the

fact that shopping mall rents are down 1.5% over the past year.

The euro is slipping again as Eurozone refinancing challenges come back onto

the front burner and People’s Bank of China officials are openly discussing their

concerns surrounding China’s disturbing inflation backdrop — hinting at more

policy tightening. As a result, the commodity complex, as well as the resource-

based currencies, is heading south (copper is down 1.4% today and oil is off the

boil, though the damage to the economy has already been done as we explain

below — also see Oil Price Enters Danger Zone on the front page of today’s FT);

gold is hugging the 100-day m.a. line nicely after yesterday’s descent. The

Aussie and Kiwi are down now for three days in a row and the loonie has

declined from its lofty perch for the first time in ten sessions.

As for credit, it remains to be seen whether we see some spread widening given the massive slate of new corporate issuance on tap for this quarter (see Bond

Wave Strikes on Both Sides of the Atlantic on page 12 of the FT). Pound for

pound, we still prefer corporate bonds to equities, which would have been a very

good call for 2010 by the way, and we would view any widening in spreads as a

terrific buying opportunity.

Please see important disclosures at the end of this document.

Gluskin Sheff + Associates Inc. is one of Canada’s pre-eminent wealth management firms. Founded in 1984 and focused primarily on high net worth private clients, we are dedicated to meeting the needs of our clients by delivering strong, risk-adjusted returns together with the highest

level of personalized client service. For more information or to subscribe to Gluskin Sheff economic reports,

visit www.gluskinsheff.com

8/8/2019 Breakfast With Dave 010511

http://slidepdf.com/reader/full/breakfast-with-dave-010511 2/15

January 5, 2011 – BREAKFAST WITH DAVE

Barrons.com ran an article yesterday quoting some obscure analyst criticizing

our macro economic and bond yield call for 2010, basically ridiculing us, calling

for a contraction in either Q3 or Q4 and for the yield on the U.S. 10-year note to

get as low as 2% or below. Here is the reality. The U.S. economy was clearly

sputtering by the spring and summer and we were calling for that early on as the

consensus was gazing at 5%+ fourth quarter growth in Q4 of 2009 and 3%+ in

the first quarter of 2010. Only when the long arm of the law — another round of

monetary and fiscal stimulus — was extended to give Mr. Market a nice lift did

the clouds part. That shows how fragile this recovery has been and remains —

just read the FOMC minutes to get a glimpse of the array of downside risks cited

(more on this below). While the 10-year yield did not finish the year at 2%, it

almost got there in the fall and nobody, except us, was calling for that a year

ago. So put that in your pipe and smoke it.

Only when the long arm of the

law — another round ofmonetary and fiscal stimulus —

was extended to give Mr.

Market a nice lift did the

clouds part

There is no doubt that we have had an incredible bear market rally on our

hands. But that is exactly what it is. As we noted yesterday, as per Bob Farrell,

even these spasms can go further than anyone thinks. But after a monstrous

80%-plus rally from the March 2009 lows (over such a short time frame, and the

most pronounced bounce since 1955) this market has become seriously

overextended in our view. Meanwhile, we have practically every market pundit

extrapolating the recent trend into the future because that is the easy thing to

do. But the Farrell’s and Walter Murphy’s of this world have become very

cautious and frankly, that is good enough for us. The fact that Laszlo Birinyi

published a report yesterday concluding that the S&P 500 will rally to 2,854

(what … no decimal place?) by September 4, 2013 (oh, only another 125% from

here) is perfect. Absolutely perfect.

Meanwhile, the masses only see the returns, they do not see the risks that arenearly invisible to the naked eye. But we see the risks. We assess them; we

measure them, and we benchmark the returns against them. I recall all too well

that 2003-07 bear market rally — yes, that is what it was. It was no 1949-1966

or 1982-2000 secular bull run. It was a classic bear market rally, and did last

five years. I was forever skeptical because what drove that bear market rally

was phony wealth generated by a non-productive asset called housing alongside

wide spread financial engineering, which triggered a wave of artificial paper

profits. I knew it would end in tears … sadly, I didn’t know exactly when. I was

constantly defensive in my investment recommendations at the time and there

was a huge price to be paid for being bearish when there is a bull on your

business card, trust me on that one.

We have been patient and will remain so, with an eye towards maximizing risk-adjusted returns, not merely gross nominal returns, which are the only ones that

get reported. Remember those returns only count if they aren’t ultimately

reversed by excessive greed. At the current time, we believe our clients are well

served by our equity strategies (minimal cyclical exposure and a focus on an

income equity-hard asset barbell); our long-short strategies (vital in controlling

risk in the portfolio and underscore our focus on capital preservation thematic)

and our fixed-income products (outside of commodities, deflation in the

Page 2 of 15

8/8/2019 Breakfast With Dave 010511

http://slidepdf.com/reader/full/breakfast-with-dave-010511 3/15

January 5, 2011 – BREAKFAST WITH DAVE

developed world remains the primary trend and is in such a backdrop that

“yield” makes perfect sense). Bear market rallies are not the

same as secular bull markets — the former are to be rented,

the latter are to be owned

How the Fed and the federal

government in the future

manage to redress their

pregnant balance sheetswithout creating a major

disturbance for the overall

economy is a legitimate

question

As investors discovered that the world wasn’t flat after all from late 2007

through to early 2009 as the roof caved in for most, who remembered that I was

just plain wrong in 2003 when the S&P 500 surged 26% or even in 2006 when

it rallied 13%. It is quite amazing that as the market rolled over, nobody

remembered how “wrongly bearish” I was during those years in the wilderness

when everyone believed in the wonders of financial market innovation and the

democratization of the housing market. I recall a senior portfolio manager in

Texas scolding me in 2005 about how his nanny just got a subprime mortgage

to buy her first home … let’s hope he didn’t co-sign).

It is an amazing commentary on human behaviour that I was forgiven for having

been more focused on bonds and gold during those go-go leveraged years of

2003-2007, and then treated like a hero after the financial system collapsed

under its own weight of dramatic excess. It goes to show that in the final

analysis, as much as it hurts, not to be involved in a speculative rally that sees

the market surge more than 80%, it is much much tougher to actually

experience a correction in the other direction. For the time being, it takes

extreme courage and resolve to not jump on the bandwagon (“don’t fight the

Fed”) and buy “the market” at current expensive pricing points.

As far as equities are concerned, make no mistake, we are in the throes of an

intense bear market rally, which is likely at the very late stage. Nobody will know

to get out at the peak and as we saw in late 2007 and into 2008, many of the

“longs” will be trapped. Bear market rallies are not the same as secular bull

markets — the former are to be rented, the latter are to be owned. Those

claiming to be adept market timers today that have been and are staying long

will be repeating the same mistake they made three-years ago.

This is not the 1949-66 secular bull market that was underpinned by troops

coming home and spurring on a baby-boom that would unleash years of

tremendously strong domestic demand growth. The demographics in the U.S.A.

are now downright poor — just look at the ratio of the working age population to

the total population. Nor is this the 1982-2000 secular bull market that saw the

central bank usher in years of disinflation (the current one is trying desperately

to create inflation!) and a wave of innovation that saw the mainframe, the

personal computer, the Internet, and then the smartphone, a boom in the

capital stock that enhanced structural productivity growth and led to sustained

gains in private sector economic activity, which by the end of that secular bullrun, allowed the government to actually start to record budgetary surpluses.

What is the major innovation today? The iPod? The iPad? Facebook? These

may be fun, but they don’t do much to promote the growth rate in the nation’s

capital stock or productivity.

What we have on our hands has been an economic revival and market bounce

back premised on unprecedented monetary and fiscal stimulus. How the Fed

Page 3 of 15

8/8/2019 Breakfast With Dave 010511

http://slidepdf.com/reader/full/breakfast-with-dave-010511 4/15

January 5, 2011 – BREAKFAST WITH DAVE

and the federal government in the future manage to redress their pregnant

balance sheets without creating a major disturbance for the overall economy is

a legitimate question and, sorry, does not deserve a double-digit market

multiple, in our view.

Don’t assume for a second

that Ben Bernanke has anymore rabbits in his hat or that

the new Congress is going to

fill anyone’s stockings with

more fiscal goodies towards

the end of the year

Maybe last quarter’s and next quarter’s GDP growth is relatively certain, but last

we saw, the stock market is a long-duration asset. If 2011 was a building block

for 2012, much like 1982 was for 1983, we would be impressed. But the

growth we will likely see in 2011 will be bought by the government and the Fed

at the expense of 2012 where there is likely going to be a huge air pocket, and

the presidential election of that year in the U.S. will likely be fought and won on

which party can successfully convince the voting public that the recession was

not its fault.

Just as the 2003-07 bear market rally was built on a shaky foundation of

unsustainable credit and house price appreciation, the current bear market rally

has been built on even shakier ground of surreal public sector intervention. This

may well have “saved the system” or “prevented a depression” back in the

opening months of 2009, as many like to believe; however, the reality (and even

former communist regimes figured this out a few decades ago) is that there is

no such thing as a free lunch.

The best buying opportunities for investors that actually do have a horizon that

lasts more than five months or even 15 months for that matter; investors that

are more focused on building wealth for the long-term as opposed to trying to

make recurring short-term trading profits, will happen when we see the payback

period. And this could happen sooner than you think. Don’t assume for a

second that Ben Bernanke has any more rabbits in his hat or that the new

Congress is going to fill anyone’s stockings with more fiscal goodies towards the

end of the year.

At least the editorial board at the Wall Street Journal get it. See page A14 of

today’s paper — The GOP Opportunity . To wit:

“John Boehner takes the Speakers gavel from Nancy Pelosi today, and the

transfer represents much more than a change in partisan control. It marks

perhaps the sharpest ideological shift in the House in 80 years, and it could set

the stage for a meaningful two-year debate over the role of the government and

the real sources of economic prosperity.”

As the chart below il lustrates, growth in the U.S. private sector capital stock has

actually turned negative for the first time since the post WWII era. This does not

bode well for future productivity gains, the U.S. economy’s non-inflationary

growth potential or consensus views that somehow a market multiple between

14x and 16x (depending on how it’s measured) is close to anything resembling

“fair-value”

Page 4 of 15

8/8/2019 Breakfast With Dave 010511

http://slidepdf.com/reader/full/breakfast-with-dave-010511 5/15

January 5, 2011 – BREAKFAST WITH DAVE

CHART 1: GROWTH IN PRIVATE SECTOR CAPITAL STOCKTURNS NEGATIVE

United States: Net Stock: Private Equipment & Software

(year-over-year percentage change)

05050505050505

Source: Bureau of Economic Anal sis /Haver Anal tics

25

20

15

10

5

0

-5

Source: Haver Analytics, Gluskin Sheff

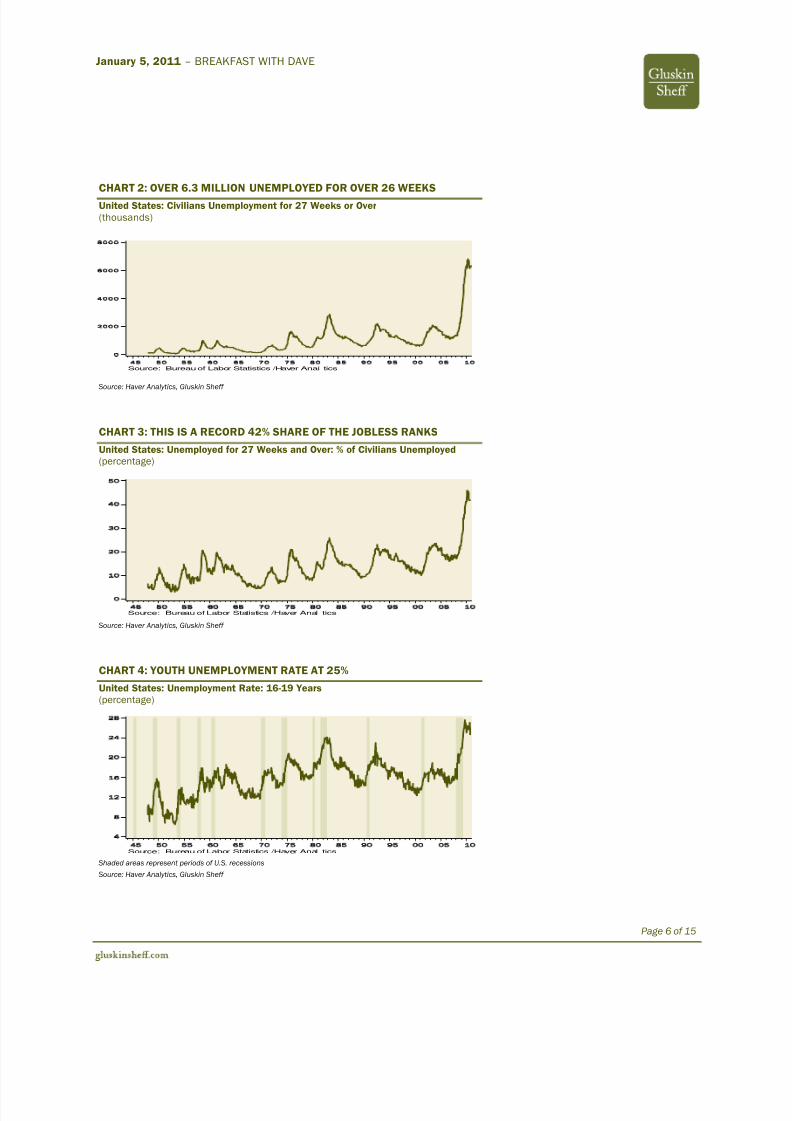

While today’s ADP number for December was surprisingly strong, the reality is

that U.S. labour market remains in a state of disarray. The labour force gaps are

huge if not unprecedented. Fully 6.3 million Americans have been actively

looking for a job with no success for at least six months — a record, both in

absolute and relative terms, to the size of the workforce. One cannot help but

contemplate the looming social issues that will be involved if youth

unemployment rates at 25% and adult male jobless rates at 10% are sustained.

Even the Fed did not offer much hope in yesterday’s minutes that the dramatic

excess capacity in the jobs market will be resolved in the coming year, even with

the last gasp attempt to stimulate the economy with monetary and fiscal

steroids. Again, this is a source of uncertainty that would ordinarily require a

lower fair-value P/E multiple than a higher one.

Page 5 of 15

8/8/2019 Breakfast With Dave 010511

http://slidepdf.com/reader/full/breakfast-with-dave-010511 6/15

January 5, 2011 – BREAKFAST WITH DAVE

CHART 2: OVER 6.3 MILLION UNEMPLOYED FOR OVER 26 WEEKS

United States: Civilians Unemployment for 27 Weeks or Over

(thousands)

105050505050505

Source: Bureau of Labor Statistics /Haver Anal tics

8000

6000

4000

2000

0

Source: Haver Analytics, Gluskin Sheff

CHART 3: THIS IS A RECORD 42% SHARE OF THE JOBLESS RANKS

United States: Unemployed for 27 Weeks and Over: % of Civilians Unemployed

(percentage)

105050505050505

Source: Bureau of Labor Statistics /Haver Anal tics

50

40

30

20

10

0

Source: Haver Analytics, Gluskin Sheff

CHART 4: YOUTH UNEMPLOYMENT RATE AT 25%

United States: Unemployment Rate: 16-19 Years

(percentage)

105050505050505

Source: Bureau of Labor Statistics /Haver Anal tics

28

24

20

16

12

8

4

Shaded areas represent periods of U.S. recessions

Source: Haver Analytics, Gluskin Sheff

Page 6 of 15

8/8/2019 Breakfast With Dave 010511

http://slidepdf.com/reader/full/breakfast-with-dave-010511 7/15

January 5, 2011 – BREAKFAST WITH DAVE

CHART 5: NEAR-10% UNEMPLOYMENT RATE FOR ADULT MALES

United States: Unemployment Rate: Men between 25-54 Years

(percentage)

105050505050505

Source: Bureau of Labor Statistics / Haver Anal tics

10

8

6

4

2

0

Shaded areas represent periods of U.S. recessions

Source: Haver Analytics, Gluskin Sheff

U.S. CONSUMER FINISHED THE YEAR IN DECENT SHAPE

The Redbook survey showed a 0.4% same-store sales gain to close out the year

and this resulted in 3.5% YoY pace which indeed was above target of a 3.2%

trend. According to the report, what helped the last week of 2010 were “post-

Christmas markdowns” and “clearance sales of seasonal inventory were

certainly a factor in post-Christmas buying”. There is no reason for deflationary

growth to be a negative for the fixed-income market but everywhere we look all

we see are bond bears.

SLOWING TREND IN CORE CAPEX ORDERS ... THIS MAY THROW A WRENCH

INTO BULLISH BUSINESS SPENDING FORECASTS FOR 2011

Yesterday’s manufacturing data tells me that we are off the boil as far as capital

spending growth is concerned and yet business spending is a key cornerstone

for the consensus regarding the 2011 macro outlook. Remember, capital

expenditure was up 15% last year, by far outpacing all other segments of U.S.

GDP (consumer spending was not even up 2% for the year as a whole, despite

the strong finish). Looking at the trend in new core capex orders, we are closing

the books in 2010 on a slowing path.

Yesterday’s manufacturing

data tells me that we are off

the boil as far as capital

spending growth is concerned

Over the past three months, core capex orders (capital goods orders excluding

defense and aircraft) have slowed to a 4.9% annual rate. Three-months ago,

this pace was running at 13.2% and six-months ago it was 39.3% at an annual

rate. This is actually the second softest trend since the recession ended in mid-

2009.

The second chart below is smoother and illustrates the six-month trend. In

November, it was running at an 8.9% annualized rate, which is okay as a stand-

alone print, but this masks the recent loss of momentum― this trend was north

of 20% both three- and six-months ago. And recall, we had the Fed embark on

QE2 and the investor-friendly election results prior to November. Also keep in

mind that over this three-month interval in which core order growth receded so

Page 7 of 15

8/8/2019 Breakfast With Dave 010511

http://slidepdf.com/reader/full/breakfast-with-dave-010511 8/15

January 5, 2011 – BREAKFAST WITH DAVE

sharply, the ISM orders index rang in near the 56 level. In other words, beware

of diffusion indices … they only tell you part of the story.

In terms of industry segments, fabricated metals, telecom equipment,

machinery and motor vehicles are now posting the sharpest slowing in order

books. By way of comparison, electrical equipment, computers, and steel are

exhibiting the best looking trends right now.

CHART 6: CAPEX ORDERS SLOWING

United States: Non-defense Capital Goods New Orders excluding Aircraft

(three-month percentage change annualized)

1098765432109

60

40

20

0

-20

-40

-60

Shaded areas represent periods of U.S. recessions

Source: Haver Analytics, Gluskin Sheff

CHART 7: THE SIX-MONTH TREND HAS SLOWED TO 8.9% FROM NORTH

OF 20% JUST A FEW MONTHS AGO

United States: Non-defense Capital Goods New Orders excluding Aircraft

(six-month percentage change annualized)

1098765432109

40

20

0

-20

-40

-60

Shaded areas represent periods of U.S. recessions

Source: Haver Analytics, Gluskin Sheff

Page 8 of 15

8/8/2019 Breakfast With Dave 010511

http://slidepdf.com/reader/full/breakfast-with-dave-010511 9/15

January 5, 2011 – BREAKFAST WITH DAVE

WHAT THE BULLS MAY BE IGNORING ... AT THEIR PERIL ... PLUS SOME

IDEAS FOR 2011 Obama just enhanced his

2012 re-election chances byappointing Daley as his chief

of staff

Nothing of course says that

the market can’t keep goingup over the near-term

The bullish case is pretty well established right now and there is no sense

repeating them but what may be ignored are these half-dozen risks:

1. How much of 2011 growth was borrowed from 2012 (the payroll tax cutand bonus depreciation allowance end in December 2011). This may bean issue heading into Q4.

2. Energy prices ― if oil breaks above $100 and gasoline prices approach$3.50/gallon then expect the consumer to sputter. Every penny at thepumps drains $1.5 billion out of household cash flow. At the moment, U.S.gas prices at the pumps are at $3.15/gallon, but consider that back inSeptember, it was closer to $2.70/gallon. This increase in energy prices ishardly the result of booming consumer demand, which we know from themonthly personal consumption expenditure data is down more than 2%from a year ago. This is nothing more than an exogenous negative shock,

which, at current levels, is approximately a $50-60 billion annualized drag from the U.S. household cashflow (basically absorbing half of the payroll

tax relief). If, as many experts predict, gas prices ultimately go to $4/gallon, then this would siphon another $100 billion into the gas tank. As for oil, the rule of thumb is that a 10% increase in prices shaves off 25 percentagepoints off GDP. This means that oil could be a near-one percentage pointhit to GDP growth.

3. The GOP-led House is pressing for $100 billion of spending cuts for thisyear. If enacted, and this could be part of a deal to resolve the debt ceiling issue looming this spring, could cause GDP estimates to be trimmed.

4. Obama just enhanced his 2012 re-election chances by appointing Daley ashis chief of staff. Either he is really going to move to the center, or he is

trying to cement the next election.

5. Everyone believes that a better employment picture will brighten the stockmarket’s prospects even more but in fact the opposite will happen asmargins get squeezed by rising labour costs. Remember what happened in1994. Be careful what you wish for.

6. I am hearing that the Fed is moving further away from entertaining thenotion of a QE3 program in the second half of the year. Something themarket will be grappling with in the second quarter, and I see that thesecond quarter may well offer up the best buying opportunity of the yearsince that is the quarter where the concern list will likely start to grow;lagged impact of China tightening shows through, big Europeanrefinancings, signs of no more QE, and the debt-ceiling issue hitting itspeak.

Nothing of course says that the market can’t keep going up over the near-term.

All I hear is about “not fighting the Fed” and “how great the economy is doing”

and maybe this will lure some fence-sitters into equities (as has already beenevident in the December fund-flow data). To be sure, the U.S. consumer has

surprised to the upside even with still-sluggish job market conditions, and the

stimulus impact will be most felt this quarter re: tax relief. But surely this is

already priced in. What may not be priced in is that much like 2010, the peak

rate of GDP growth for this year will be the quarter we are in right now (the peak

in 2010 was 3.7% in Q1). Until Bernanke uttered the words QE2 in late August,

the market was beginning to recognize the slowing pattern that was underway in

Page 9 of 15

8/8/2019 Breakfast With Dave 010511

http://slidepdf.com/reader/full/breakfast-with-dave-010511 10/15

January 5, 2011 – BREAKFAST WITH DAVE

the economy. If this pattern re-emerges this year, but the Fed no longer has the

willingness or ability to provide additional monetary stimulus, we could be in for

a great buying opportunity during the spring and summer months in particular.

Just as the onus was on the

double-dippers last summergiven the sentiment and

market action, the onus now is

clearly on the V-shaped

enthusiasts

To be sure, companies are still sitting on a hoard of cash but that is a better

guide for M&A and dividend payouts than for acceleration in capital spending,

which I see moderating this year as profit growth softens. Housing is going

nowhere. Ditto for commercial construction. The ISM index was decent but did

flag a slowing, if not termination, of the inventory cycle as well as a reduced

contribution to the economy from exports (this component is down two months

in a row). We also have escalating cuts at the state and local government levels

to contend with.

In a nutshell, just as the onus was on the double-dippers last summer given the

sentiment and market action, the onus now is clearly on the V-shaped

enthusiasts (by the way, they also dominated the landscape exactly a year ago

and were only proven to be correct after the tremendous monetary and fiscal

efforts to revive confidence and economic activity).

In terms of themes for 2011, we think that there are wide swaths of the fixed-

income market that offer good value at current pricing levels. Sentiment in

equities is overdone, but the barbell between hard assets and income-

generating securities still seems to have merit. REITs look expensive but some

of the fundamentals are beginning to show some improvement― office rents

and absorption firmed last quarter for the first time in nearly three years.

Volatility or the cost of insuring against a market correction is about as cheap as

it can be right now. Commodities are in a secular bull market but have moved a

tad too parabolic right now and speculative interest has picked up dramatically

of late ― with exploration budgets expanding sharply, the real play within the

space may be in oil and mining services.

The largest S&P 500 companies are sitting on 10% more cash than a year ago

at over $900 billion and that means more dividend payouts so the yield theme is

intact (255 companies raised their payouts last year compared to 157 in 2009).

With all this cash, M&A will be a major theme (up 12% last year to $895 billion

according to Dealogic), which in turn means that financials that have a high

concentration in the merger space may not be bad places to be. Stock

buybacks have risen now for five quarters in a row and that may also end up

being a source for the cash hoard going forward, and, as such could help

establish a firmer floor under the equity market. (However, do not mistake that

comment for my view that this market is overvalued, overbought andoverextended at the current time, but that we should be entertaining the notion

of becoming more constructive when corrective phases set in that serve up

more compelling valuation metrics. A 16x multiple is seen today as fair-value

but in fact before the tech bubble, such valuation occurred less than 30% of the

time so this is hardly the norm.)

Page 10 of 15

8/8/2019 Breakfast With Dave 010511

http://slidepdf.com/reader/full/breakfast-with-dave-010511 11/15

January 5, 2011 – BREAKFAST WITH DAVE

Please forgive us, but we

counted two “downside” risks

in the FOMC minutes. The

word “upside” was never

mentioned.

FED LESS THAN IMPRESSED WITH THE ECONOMIC BACKDROP

While most economists and strategists have literally been tripping over

themselves to declare the onset of a sustainable V-shaped economic expansion

ahead, the tone of the December FOMC minutes was rather dismissive of that

prospect ― even as it acknowledged that the incoming data have been decent

(in light of the very accommodative stance of monetary policy currently in place):

With the recent data on production and spending stronger, on balance, than the

staff anticipated at the time of the November FOMC meeting, the staff revised

up its projected increase in real GDP in the near term. However, the staff’s

outlook for real economic activity over the medium term was little changed, on

net, relative to the projection prepared for the November meeting. The staff

forecast incorporated the assumption that new fiscal actions, some of which

had not been anticipated in its previous forecast, were likely to boost the level of

real GDP in 2011 and 2012. But, compared with the November forecast, a

number of other conditioning assumptions were less favorable: House prices

and housing activity were likely to be lower, while interest rates, oil prices, and

the foreign exchange value of the dollar were projected to be higher, on

average, than previously assumed. As a result, although the staff projection

showed a higher level of real GDP, the average pace of growth over 2011 and

2012 was little changed from the November forecast, and the unemployment

rate was still projected to decline slowly.

Indicators of production and household spending had strengthened, and the

tone of the labor market was a little better on balance. The new fiscal package

was generally expected to support the pace of recovery next year. However, a

number of factors were seen as likely to continue restraining growth, including

the depressed housing market, employer’s continued reluctance to add topayrolls, and ongoing efforts by some households and businesses to delever.

Moreover, the recovery remained subject to some downside risks, such as the

possibility of a more extended period of weak activity and lower prices in the

housing sector and potential financial and economic spillovers if the banking

and sovereign debt problems in Europe were to worsen.

Others pointed to downside risks to growth. One common concern was that the

housing sector could weaken further in light of the considerable supply of

houses either on the market or likely to come to market. Another concern was

the ongoing deterioration in the fiscal position of U.S. states and localities,

which could lead to sharp cuts in spending and increases in taxes. In addition,

participants expressed concerns about a possible worsening of the banking and

financial strains in Europe, which could spill over to U.S. financial markets andinstitutions, and so to the broader U.S. economy.

Please forgive us, but we counted two “downside” risks in the minutes. The

word “upside” was never mentioned. How do you like that, Mr. Potter? For sure

that’s got to be worth a 20% four-month rally, no?

Page 11 of 15

8/8/2019 Breakfast With Dave 010511

http://slidepdf.com/reader/full/breakfast-with-dave-010511 12/15

January 5, 2011 – BREAKFAST WITH DAVE

Guess what did show up no fewer than ten times? The word ‘housing’ and it

wasn’t very complimentary. All of sudden, the sector that helped the most in

getting us into this mess is still the one that poses the single greatest cloud to

the outlook.

The sector that helped the

most in getting us into this

mess is still the one that poses

the single greatest cloud to

the outlookTROUBLES WITH THE PROFIT FORECASTS

The consensus now sees $96 for S&P 500 operating earnings for 2011 which

would be a 14% boost from what we saw in 2010. Let’s assume that two

percentage points of that come from stock buybacks. That’s fine. Companies

have the cash to do that. So call it 12% EPS growth delivered from the economy.

We know that the ex-U.S. economy is going to slow down this year so the adage

of 50% being derived outside of America is not going to be such a bullish story in

the coming twelve months. The markets have already discounted this, which is

why the U.S. stock market has so vastly outperformed the rest of the world of

late. America is home to dramatic fiscal and monetary ease while Europe is

busy tightening the former and emerging Asia busy tightening the latter. Only

the U.S. reserves the right to ease policy on both fronts but this really does little

more than mask the underlying structural weaknesses in housing, jobs and state

and local government finances that were so eloquently described in yesterday’s

FOMC minutes.

Here’s the rub. It is not possible that a 4% nominal GDP growth is going to

deliver 14% earnings growth at this stage of the profit cycle, with margins

already flirting near all-time highs. This is not the early or even the mid stages of

the profit cycle ― the V-shaped bounce off the lows puts it closer to the latter

stages. Mid at best. Now when we are coming out of recession and margins are

positioned to expand sharply even with a modest bounce in the economy, it is

not rare at all to see double-digit gains in corporate earnings. It’s called the“rubber band effect”. Indeed, we saw this in 1993 when 5% nominal GDP

growth translated into 29% EPS growth; in 2002 when 3.5% nominal GDP

growth coincided with 18.5% profit growth; and again in 2009 when in fact a

-1.7% growth rate gave way to a 15% profits rebound. But at this stage of the

cycle, history shows that it would take between 6% and 8% nominal GDP growth

to allow for a 14% earnings stream.

The consensus of economists, as bullish as it is, see 4% nominal GDP growth in

2011. The strategists see 14% profit growth net of buybacks. Either something

has to give ― or at the least the economists and strategists should spend more

time in the same room with each other.

ADP SURGES! BUT IS IT FOR REAL?The U.S. ADP private payroll number was a record +297k in December. Surreal.

The market was looking for +100k. We never had a number remotely this strong

during the last economic cycle — last time we were close was in February 2006

when real GDP growth was 5.4% at an annual rate. Even the most bullish

forecast for Q4 is 4%, consensus is at 2.5%, so either we have something on our

hands that is much stronger than that or productivity is starting to sag. Or… this

number is BS. Take your pick.

Page 12 of 15

8/8/2019 Breakfast With Dave 010511

http://slidepdf.com/reader/full/breakfast-with-dave-010511 13/15

January 5, 2011 – BREAKFAST WITH DAVE

Page 13 of 15

The huge gain was centered in services (+270k) and especially in small (+120k)

and mid-sized (+123k) companies. I am thinking that this must be retail

oriented towards the better than expected holiday shopping season (financial

services actually posted a 6k decline and this sector represents a non-trivial 8%

chunk of total private payrolls). Goods-producing jobs rose a more moderate

27k, helped by a 23k gain in manufacturing, which seemed at odds with ISM

employment which actually dipped to a nine-month low.

We have U.S. payroll data back to 1940. There have been 111 times when

private service sector payrolls were +200k or more in a given month. Of those,

only 11 took place with the financial sector shedding jobs. In other words, for

the nonfarm payroll report to match what we saw in ADP would be a 1-in-10

event.

8/8/2019 Breakfast With Dave 010511

http://slidepdf.com/reader/full/breakfast-with-dave-010511 14/15

January 5, 2011 – BREAKFAST WITH DAVE

Gluskin Sheff at a Glance

Gluskin Sheff + Associates Inc. is one of Canada’s pre-eminent wealth management firms.Founded in 1984 and focused primarily on high net worth private clients, we are dedicated to theprudent stewardship of our clients’ wealth through the delivery of strong, risk-adjustedinvestment returns together with the highest level of personalized client service. OVERVIEW

As of September 30, 2010, the Firmmanaged assets of $5.8 billion.

Gluskin Sheff became a publicly tradedcorporation on the Toronto Stock Exchange (symbol: GS) in May 2006 andremains 49% owned by its senior

management and employees. We havepublic company accountability andgovernance with a private company commitment to innovation and service.

Our investment interests are directly aligned with those of our clients, asGluskin Sheff’s management andemployees are collectively the largestclient of the Firm’s investment portfolios.

We offer a diverse platform of investmentstrategies (Canadian and U.S. equities,Alternative and Fixed Income) andinvestment styles (Value, Growth and

Income).1

The minimum investment required toestablish a client relationship with theFirm is $3 million.

PERFORMANCE

$1 million invested in our CanadianEquity Portfolio in 1991 (its inceptiondate) would have grown to $9.1 million

2

on September 30, 2010 versus $5.9 millionfor the S&P/TSX Total Return Indexover the same period.

$1 million usd invested in our U.S.Equity Portfolio in 1986 (its inceptiondate) would have grown to $11.8 millionusd

2on September 30, 2010 versus $9.6

million usd for the S&P 500 TotalReturn Index over the same period.

INVESTMENT STRATEGY & TEAM

We have strong and stable portfoliomanagement, research and client serviceteams. Aside from recent additions, ourPortfolio Managers have been with theFirm for a minimum of ten years and wehave attracted “best in class” talent at all

levels. Our performance results are thoseof the team in place.

Our investment interests are directlyaligned with those of our clients, as Gluskin

She ff ’s management and employees are collectively the largest client of the Firm’sinvestment portfolios.

$1 million invested in our

Canadian Equity Portfolio

in 1991 (its inception

date) would have grown to

$9.1 million2 on

September 30, 2010

versus $5.9 million for the

S&P/TSX Total Return

Index over the same

period.

We have a strong history of insightfulbottom-up security selection based onfundamental analysis.

For long equities, we look for companies with a history of long-term growth andstability, a proven track record,shareholder-minded management and ashare price below our estimate of intrinsic

value. We look for the opposite inequities that we sell short.

For corporate bonds, we look for issuers

with a margin of safety for the paymentof interest and principal, and yields whichare attractive relative to the assessedcredit risks involved.

We assemble concentrated portfolios -our top ten holdings typically representbetween 25% to 45% of a portfolio. In this

way, clients benefit from the ideas in which we have the highest conviction.

Our success has often been linked to ourlong history of investing in under-followed and under-appreciated smalland mid cap companies both in Canada

and the U.S.

PORTFOLIO CONSTRUCTION

In terms of asset mix and portfolioconstruction, we offer a unique marriagebetween our bottom-up security-specificfundamental analysis and our top-downmacroeconomic view.

For further information,

please contact

questions@gluskinshe ff .com

Notes:Unless otherwise noted, all values are in Canadian dollars.

Page 14 of 15

1. Not all investment strategies are available to non-Canadian investors. Please contact Gluskin Sheff for information specific to your situation.

2. Returns are based on the composite of segregated Value and U.S. Equity portfolios, as applicable, and are presented net of fees and expenses.

8/8/2019 Breakfast With Dave 010511

http://slidepdf.com/reader/full/breakfast-with-dave-010511 15/15

January 5, 2011 – BREAKFAST WITH DAVE

IMPORTANT DISCLOSURES

Copyright 2010 Gluskin Sheff + Associates Inc. (“Gluskin Sheff”). All rights

reserved. This report is prepared for the use of Gluskin Sheff clients andsubscribers to this report and may not be redistributed, retransmitted ordisclosed, in whole or in part, or in any form or manner, without the expresswritten consent of Gluskin Sheff. Gluskin Sheff reports are distributedsimultaneously to internal and client websites and other portals by GluskinSheff and are not publicly available materials. Any unauthorized use ordisclosure is prohibited.

Gluskin Sheff may own, buy, or sell, on behalf of its clients, securities of issuers that may be discussed in or impacted by this report. As a result,readers should be aware that Gluskin Sheff may have a conflict of interest

that could affect the objectivity of this report. This report should not beregarded by recipients as a substitute for the exercise of their own judgmentand readers are encouraged to seek independent, third-party research onany companies covered in or impacted by this report.

Individuals identified as economists do not function as research analystsunder U.S. law and reports prepared by them are not research reports underapplicable U.S. rules and regulations. Macroeconomic analysis isconsidered investment research for purposes of distribution in the U.K.

under the rules of the Financial Services Authority.

Neither the information nor any opinion expressed constitutes an offer or aninvitation to make an offer, to buy or sell any securities or other financialinstrument or any derivative related to such securities or instruments (e.g.,options, futures, warrants, and contracts for differences). This report is notintended to provide personal investment advice and it does not take intoaccount the specific investment objectives, financial situation and theparticular needs of any specific person. Investors should seek financialadvice regarding the appropriateness of investing in financial instrumentsand implementing investment strategies discussed or recommended in thisreport and should understand that statements regarding future prospectsmay not be realized. Any decision to purchase or subscribe for securities inany offering must be based solely on existing public information on suchsecurity or the information in the prospectus or other offering documentissued in connection with such offering, and not on this report.

Securities and other financial instruments discussed in this report, orrecommended by Gluskin Sheff, are not insured by the Federal DepositInsurance Corporation and are not deposits or other obligations of anyinsured depository institution. Investments in general and, derivatives, inparticular, involve numerous risks, including, among others, market risk,counterparty default risk and liquidity risk. No security, financial instrumentor derivative is suitable for all investors. In some cases, securities andother financial instruments may be difficult to value or sell and reliableinformation about the value or r isks related to the security or financialinstrument may be difficult to obtain. Investors should note that incomefrom such securities and other financial instruments, if any, may fluctuateand that price or value of such securities and instruments may rise or fall

and, in some cases, investors may lose their entire principal investment.

Past performance is not necessarily a guide to future performance. Levelsand basis for taxation may change.

Foreign currency rates of exchange may adversely affect the value, price orincome of any security or financial instrument mentioned in this report.Investors in such securities and instruments effectively assume currencyrisk.

Materials prepared by Gluskin Sheff research personnel are based on publicinformation. Facts and views presented in this material have not beenreviewed by, and may not reflect information known to, professionals inother business areas of Gluskin Sheff. To the extent this report discussesany legal proceeding or issues, it has not been prepared as nor is itintended to express any legal conclusion, opinion or advice. Investorsshould consult their own legal advisers as to issues of law relating to thesubject matter of this report. Gluskin Sheff research personnel’s knowledgeof legal proceedings in which any Gluskin Sheff entity and/or its directors,officers and employees may be plaintiffs, defendants, co—defendants orco—plaintiffs with or involving companies mentioned in this report is basedon public information. Facts and views presented in this material that relate

to any such proceedings have not been reviewed by, discussed with, andmay not reflect information known to, professionals in other business areasof Gluskin Sheff in connection with the legal proceedings or mattersrelevant to such proceedings.

Any information relating to the tax status of financial instruments discussedherein is not intended to provide tax advice or to be used by anyone toprovide tax advice. Investors are urged to seek tax advice based on theirparticular circumstances from an independent tax professional.

The information herein (other than disclosure information relating to GluskinSheff and its affiliates) was obtained from various sources and GluskinSheff does not guarantee its accuracy. This report may contain links to

third—party websites. Gluskin Sheff is not responsible for the content of any third—party website or any linked content contained in a third—party website.Content contained on such third—party websites is not part of this reportand is not incorporated by reference into this report. The inclusion of a linkin this report does not imply any endorsement by or any affiliation withGluskin Sheff.

All opinions, projections and estimates constitute the judgment of theauthor as of the date of the report and are subject to change without notice.Prices also are subject to change without notice. Gluskin Sheff is under noobligation to update this report and readers should therefore assume thatGluskin Sheff will not update any fact, circumstance or opinion contained in

this report.

Neither Gluskin Sheff nor any director, officer or employee of Gluskin Sheff accepts any liability whatsoever for any direct, indirect or consequentialdamages or losses arising from any use of this report or its contents.

Page 15 of 15

Related Documents