TEKST 84 TEKST 84 www.inventuremanagemen t.com Layout and design: Markedsavdelingen, Rio de Janeiro. www.markedsavdelingen-a s.no P h o t o s : S h u t t e r s t o c k

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

7/31/2019 Brazil How to Do Business in Brazil 2011

http://slidepdf.com/reader/full/brazil-how-to-do-business-in-brazil-2011 1/84

TEKST84 TEKST 84

www.inventuremanagement.com

Layout and design:Markedsavdelingen, Rio de Janeiro.

www.markedsavdelingen-as.no

P h o t o s : S h u t t er s t o ck

7/31/2019 Brazil How to Do Business in Brazil 2011

http://slidepdf.com/reader/full/brazil-how-to-do-business-in-brazil-2011 2/84

TEKST 1

e-Entr onsiderat on Page 8

s ag 56

T N S

A uide fo O , O ore

ri m ni s

nteri Br zil

B R A Z IL

2011 Edition

7/31/2019 Brazil How to Do Business in Brazil 2011

http://slidepdf.com/reader/full/brazil-how-to-do-business-in-brazil-2011 3/84

2

WELCOME

TO BRAZIL!

Area

Brazil is South America’s largest country, about 22 timeslarger than Norway, and in fact larger than continentalUSA. Brazil shares a border with 10 other South American countries and stretches over 3 time zones.

Rio de Janeiro

Brasilia

Sao Paulo

Amazonas

Parana

Macae

7/31/2019 Brazil How to Do Business in Brazil 2011

http://slidepdf.com/reader/full/brazil-how-to-do-business-in-brazil-2011 4/84

3

www.howtodobusinessinbrazil.com

The Portuguese

discovered Brazil in 1500.Brazil remained a Portu-guese colony until 1822, when independency wasdeclared.

Brazil has the world’s eighth largest economy,

and one of the fastest growing. Projected growthfor 2011 is around 5%. Half of Latin America’s totalGDP is generated in Brazil.

Brazil has a spectacular na-

ture. The Amazonas basin ishome to both the world’s larg-est rain forest and the world’slargest river. Brazil has morethan 5,000 km of coast lineforming an almost continuousstretch of white sand beaches.The Pantanal wetland area is

globally unique for its animaland plant diversity, and theIguaçu waterfalls are larger than the Niagara Falls.

Social development. Over the last5 years, more than 25 million Brazil-ians have been lifted out of poverty,and crime rates are dropping in thelargest cities.

Population. Brazil’s population is almost 200million. The rich Southeastern region is themost populous, dominated by people of Euro-pean descent. The poorer Northeastern regionis a mix of people with European, African andindigenous roots. The vast Western, Cen-tral and Northern regions are relatively thinlypopulated.

The carnival of

Brazil is worldfamous, butrepresents justa small part ofthe country’sexceptionally

rich cultural life.

Brazil is a republic, with a president whois directly elected for a 4 year term. Thepresident is both the Head of State and theHead of the Government, and has extensivepowers. Dilma Rousseff, elected in 2010, isBrazil’s first female president.

Voting is mandatory in Brazil for allliterate citizens aged between 18 and 70.

The most important cities are Brasilia (the capital),Rio de Janeiro (the oil&gascapital) and Sao Paulo (thecommercial engine). SaoPaulo (picture) has morethan 20 million inhabitants.

Football is what most people associate withBrazil. The five time world champion will hostthe football World Cup in 2014 as well as theSummer Olympics in 2016, and will see massiveinvestments in infrastructure.

Export. Brazil is the world’s biggest coffeeexporter. But evenlarger export articlesare soy beans,steel, petroleum andchicken products.

Brazil has discovered enormous

offshore oil reserves. This is theengine in Brazil’s current economicboom, and has generated a strongand growing demand of all kinds ofproducts and services related to theoil sector, as well as reviving the Bra-zilian maritime industry. Over the nextfive years, a total investment of more

than USD 300 billion is expected inareas where Norwegian suppliers inmany cases are world leading. Thecenter for the oil activity is Rio de Janeiro, with nearby Macae as animportant hub.

Lusoimages / Shutterstock.com

7/31/2019 Brazil How to Do Business in Brazil 2011

http://slidepdf.com/reader/full/brazil-how-to-do-business-in-brazil-2011 5/84

This is the second edition of the “How to Do Business in Brazil” guide, developed for INTSOK,Innovation Norway and the Norwegian General Consulate in Rio de Janeiro.

The report is written by Inventure Management in Rio de Janeiro, and is an expanded, updatedand completely revised version of the first edition.

Inventure Management is an establishment partner for oil, offshore and maritime companiesentering and expanding in the Brazilian market.

Rio de Janeiro, August 2011

INTRODUCTION

4

www.howtodobusinessinbrazil.com

Layout and design:Markedsavdelingen, Rio de Janeiro.

7/31/2019 Brazil How to Do Business in Brazil 2011

http://slidepdf.com/reader/full/brazil-how-to-do-business-in-brazil-2011 6/84

The aim of this guide is to give a structured overview of the various issues and challengesforeign companies face when establishing themselves in the Brazilian market.

The content is divided into 3 sequential phases: 1) Pre-entry considerations, 2) Start-up phaseand 3) Running operations. Most of the issues covered in the start-up phase are of course alsorelevant for the operational phase, but are covered here to emphasize the importance of estab-

lishing solid systems and procedures from the very beginning.

Content overview:

HOW TO USE

THIS GUIDE

PART 1:

PRE-ENTRY

CONSIDERATIONS

PART 2:

START-UP

PHASE

PART 3:

RUNNING

OPERATIONS

Risks

Defining a Brazil Entry

Strategy

Market Overview

The Need for Production

in Brazil

Available sources of

Financing and Support

Company Establishment

Visa

HR, Brazilian Employees

Expat Management

Paying Taxes

Accounting

Legal Issues - Contracts

Petrobras Supplier

Certification

Business Culture

Import

Local Content

Corporate Social

Responsibility

5

www.howtodobusinessinbrazil.com

All USD and NOK figures in this guide are based on BRL (Brazilian Real) values, at the exchange rates of 1 August 2011:1 USD = 1.6 BRL.1 BRL = 3.5 NOK.

7/31/2019 Brazil How to Do Business in Brazil 2011

http://slidepdf.com/reader/full/brazil-how-to-do-business-in-brazil-2011 7/84

PART 2: START-UP PHASE 26

Introduction 28Company Establishment 29

Deciding on Company Type 29Establishment Process 30Corporate Capital Needs 30

Visa Requirements 31Overview 31Is it Necessary to Apply for a Visa for Regular Business Trips to Brazil?

32

Obtaining a Visa 32

HR, Brazilian Employees 33Overview 33

Salaries and Employee Costs 33Managing the Employees 34Terminating a Contrac 35 Alternatives to Hiring 35

Expat Management 36Salaries and Employee Costs 36Practical Tips for New Expats in Brazil 37

Paying Taxes 39Corporate Taxes 39Tax on Dividends 42Tax on Capital Gains 42Tax Implications if Invoicing from Abroad 42Individual Income Tax for Expats 42Tax Deduction Programs 43

Accounting 44Brazilian Accounting and Financial Terminology 44 Audits 45

Legal Issues 46Introduction 46Legal Assistance 47Contract Issues 47Property Law 47

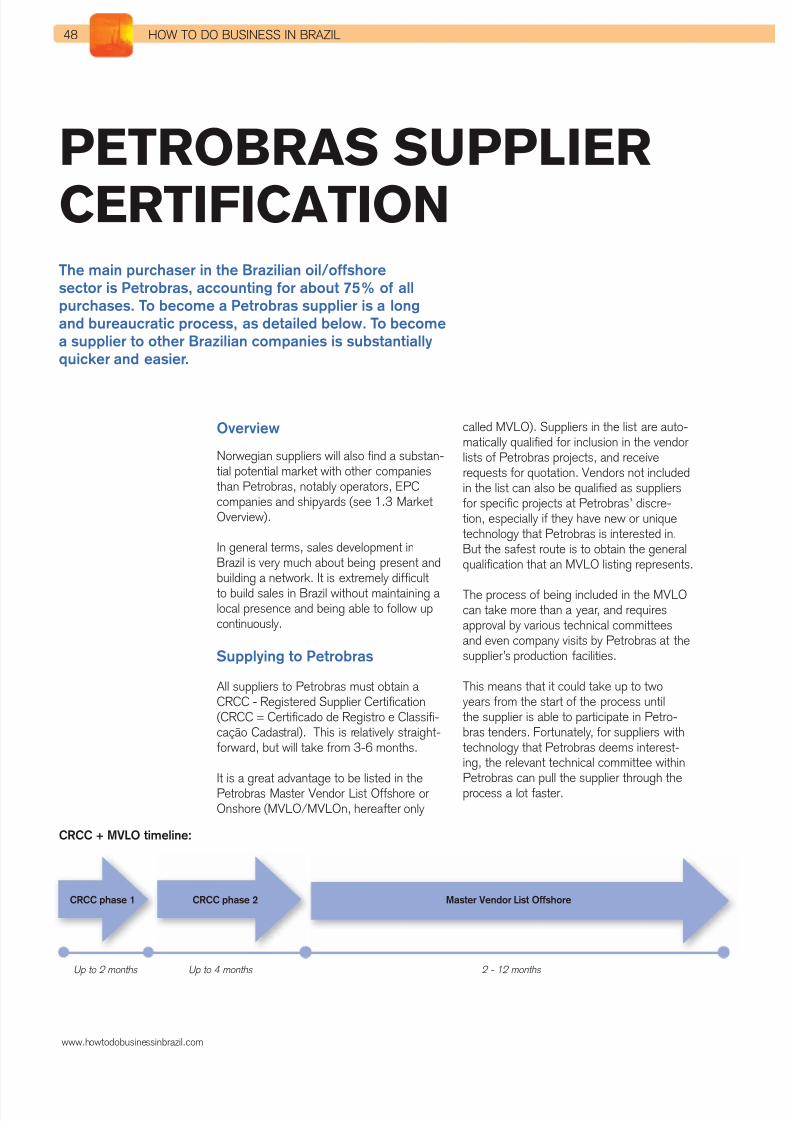

Petrobras Supplier Certification 48Overview 48

Supplying to Petrobras 48Business Culture in Brazil 52

Overview 52Typical Issues 52Global Cultural Types 54

Introduction 4

How to Use this Guide 6

PART 1: PRE-ENTRY CONSIDERATIONS 8

Introduction 10Risks 11

Corruption and Transparency 11Running Operations 11

Defining a Brazil Entry Strategy 12Market Research 12Business Setup 12

Market Overview – The Brazilian Oil, Offshore

and Maritime Market

14

Introduction 14The Pre Salt Opportunity 14The Main Players 16

Summary of Petrobras Business Plan 18OGX 22The Shipbuilding Market 23

The Need for Production in Brazil 24

Available Sources of Financing and Support 25Innovation Norway 25INTSOK 25GIEK – Garanti-Instituttet for Eksport-Kreditt 25Nopef – the Nordic Project Fund (“Nordisk Eksportfond”)

25

CONTENTS

6

www.howtodobusinessinbrazil.com

7/31/2019 Brazil How to Do Business in Brazil 2011

http://slidepdf.com/reader/full/brazil-how-to-do-business-in-brazil-2011 8/84

PART 3: RUNNING OPERATIONS 56

Introduction 58Import 59

Overview 59Import License 59Import Taxes for Goods 60 Authorities Involved in the Import Process 60Special Customs Regimes 61REPETRO 61

Local Content 63Introduction 63Local Content Levels 64Local Content Implications for Operators 66Local Content Implications for Suppliers 66

Regulations 68

Corporate Social Responsibility 69CSR Impact in Brazil 69Tax Benefits for Donors 69Existing Norwegian-Brazilian Projects 69

APPENDICES 70

Appendix 1: Useful Contacts 72

Appendix 2:

Labor Law 74

Appendix 3:

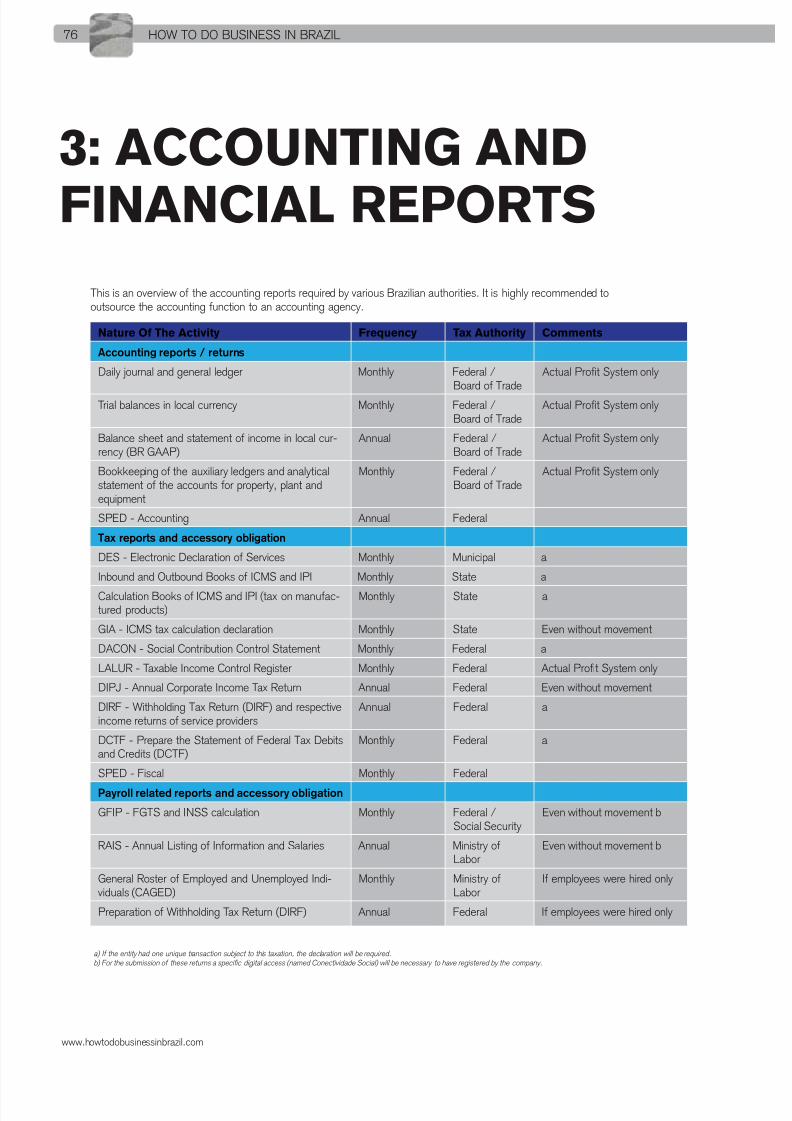

Accounting and Financial Reports 76

Appendix 4:

Differences Between “Limited Liability” and “Corporation” Company Types

77

Appendix 5:

Framework and Stakeholders 78

Appendix 6:

Brazilian Shipyards 82

7

www.howtodobusinessinbrazil.com

7/31/2019 Brazil How to Do Business in Brazil 2011

http://slidepdf.com/reader/full/brazil-how-to-do-business-in-brazil-2011 9/84

TEKST88

CONTENTS PRE-ENTRY CONSIDERATIONS:

10 Introduction

11 Risks

12 Defining a Brazil Entry Strategy

14 Market Overview

24 The Need for Production in Brazil

25 Available Sources of Financing and Support

7/31/2019 Brazil How to Do Business in Brazil 2011

http://slidepdf.com/reader/full/brazil-how-to-do-business-in-brazil-2011 10/84

9

7/31/2019 Brazil How to Do Business in Brazil 2011

http://slidepdf.com/reader/full/brazil-how-to-do-business-in-brazil-2011 11/84

HOW TO DO BUSINESS IN BRAZIL10

Companies considering a Brazilian marketentry are strongly advised to invest sufficienttime in market analysis and strategy prepara-tion.

A crucial success factor is the willingnessand ability to dedicate sufficient resourcesto the Brazil entry, in terms of both moneyand personnel. It is likely that some of your key staff will have to divert their focus fromother markets to Brazil over a significant timeperiod.

It is important to remember that frameworkconditions and premises are different from what you are used to. Norwegians tend toconnect well with Brazilians at a personallevel, making it difficult to realize that thebusiness cultures actually are very different. A lot more patience and continuous follow-up is necessary in Brazil than in Norway, inorder to build enough trust to do business.Without this trust, activities will developslowly or not at all.

INTRODUCTION

The Brazilian bureaucracy can be stifling.The World Bank’s 2011 “Ease of doingBusiness” index places Brazil as one of themost difficult places in the world to do busi-ness – ranked as number 127 out of 187economies tracked by the institution. Thescore for 2011 is worse than for 2010, indi-cating a development in the wrong direction.

There are many sources of information andadvice. INTSOK and Innovation Norway areexcellent sources for initial market informa-

tion and analysis. Further and more special-ized strategic advice may also be necessaryin this phase.

Brazil offers vast opportunities in the oil, offshore and maritime

industries. At the same time, it is a complex and challenging

market to enter, with many aspects not obvious to Norwegian

companies.

www.howtodobusinessinbrazil.com

Ease of doing business in Brazil.

7/31/2019 Brazil How to Do Business in Brazil 2011

http://slidepdf.com/reader/full/brazil-how-to-do-business-in-brazil-2011 12/84

PART 1: PRE-ENTRY CONSIDERATIONS 11

RISKSDoing business in Brazil exposes a company to other types of risks than in

Norway. The most commonly mentioned issue is corruption, but there are also

other risks related to business operations. They are all manageable, but should

by no means be ignored.

www.howtodobusinessinbrazil.com

Corruption and Transparency

Corrupt practices can be found at all levelsof public administration in Brazil. But corrup-tion is not endemic in the sense that bribes would be necessary in order to conductbusiness. It is perfectly possible to run acompany in Brazil without paying any bribes whatsoever. In fact, paying a bribe would inmany cases create more problems than it ismeant to solve.

A common way of trying to solicit a bribe isto “create a problem to sell a solution”. Pub-lic processes are complex, and it is not un-common for a foreign company to discover that it has made a wrong turn or skipped astep in a procedure, only to realize that thisis not easily reversible. When stuck, it can betempting to buy a “quick solution” to resolvethe problem, which could be both costly andrisky, and of course in direct conflict withethical standards of doing business.

Public procurement is also an area suscep-tible to corruption. This is sometimes in theform of technical specifications favoring aspecific supplier in a tender process, but canalso be related to payments in order to obtaincontracts/concessions or licences/permits.

Risk Mitigation

The most important way of avoiding corrup-tion is to pay close attention to all detailedsteps and requirements when dealing with au-thorities. If all procedures have been followed,there simply doesn’t exist a “problem” where

you can buy a “solution”. This also goes for customs clearance of imported goods – anyminor discrepancy, for example in the shippingdocuments, can stall a shipment, and retrievalcan be costly and time consuming.

Be very aware of middlemen or agents offer-ing shortcuts for an extra fee. It is commonto use middlemen (“despachantes”) to deal with the practical issues of the bureaucracyon your behalf, but any shortcut for an extrafee is inadvisable. This also goes for regis-trations with Petrobras, authority permits etc.It is not necessary and can be very costly.

Fostering an anti-corruption mindset in thecompany and compliance of anti-corruptionstandards are very important measures, and

a clear management responsibility.

Running Operations

Apart from corrupt practices, running a com-pany in Brazil also poses a number of risksrelated to operational activities. This includestaxation, import, immigration, compliance with regulatory requirements, legal disputesand security issues.

Risk Mitigation

Regarding operational risks, we have in-cluded the main risks and mitigation strate-gies in the relevant chapters throughout thisguide. But a general advice to minimize riskis to do proper background checks of allbusiness counterparts. This important secu-rity measure is commonly skipped by foreigncompanies.

Doing a proper background check in Brazilis complex and involves getting documentsfrom around 15 different public offices andentities. In many cases the publicly available

information is not enough, and cooperation with the investigated company’s accountantis necessary.

7/31/2019 Brazil How to Do Business in Brazil 2011

http://slidepdf.com/reader/full/brazil-how-to-do-business-in-brazil-2011 13/84

HOW TO DO BUSINESS IN BRAZIL12

www.howtodobusinessinbrazil.com

Market Research

In general, the market opportunities for oil/offshore/maritime related goods andservices are excellent in Brazil. But it is ofutmost importance to invest in proper marketresearch for your specific product. Marketand regulatory issues specific to Brazil oftendictate a different strategic angle than what would seem obvious in other markets.

A surprising number of companies, includingNorwegian ones, enter the Brazilian market without detailed market analysis. This oftenresults in unnecessary time and money spentrealigning operations to the market realities.

The minimum a company should know aboutthe market for their specific product/serviceincludes:

Current and projected total demand Main purchasers, competitors and their

relationships Most likely potential customers, current

and future opportunities Potential market share Market and regulatory obstacles Supply chain dynamics Macro issues affecting the product/

service Entry costs

Business set-up

The ideal setup for an individual company will of course vary, and a thorough pre-entryanalysis is indispensable.

Such research should be adapted in line withthe main available setup options:1. Serving the Brazilian market from

Norway2. Selling through a Brazilian agent/repre-

sentative3. Establishing a Brazilian entity

a) Establishing a fully owned subsidiaryb) Establishing a joint venture with aBrazilian companyc) Acquiring an existing Brazilian company

Experience shows that many foreign com-panies underestimate the need to investsufficient time in defining the Brazil strategy.Each case is different, and it is not possibleto cover any company’s specific considera-tions in a general guide. Two fundamentalquestions when considering a market entryin Brazil are:

1. What is the market potential for

my product in Brazil? (See MarketResearch.)

2. What is the best business setup?

(See Business Setup)

DEFINING A BRAZIL

ENTRY STRATEGYThe Brazil entry strategy should depend on careful

and detailed analysis of the market potential,

possible partners, supply chain positioning, needed

investments, and a range of other financial and

strategic considerations.

7/31/2019 Brazil How to Do Business in Brazil 2011

http://slidepdf.com/reader/full/brazil-how-to-do-business-in-brazil-2011 14/84

PART 1: PRE-ENTRY CONSIDERATIONS 13

www.howtodobusinessinbrazil.com

1. Serving the Brazilian Market from

Norway

It is possible to serve the Brazilian marketfrom Norway, but in practice, it is very dif-

ficult to successfully develop sales in Brazil without a continuous physical presence.Even frequent visits to Brazil will generallynot be sufficient to pick up opportunities,maintain and build relations with customers,or handle the necessary on-the-ground co-ordination. In addition, invoicing from outsideof Brazil generally adds up to 25% in extrataxes (see chapter 2.6 Paying Taxes). Fur-thermore, the main purchaser in the Brazilianmarket, Petrobras, demands that all its certi-fied suppliers for supplies to Brazil also must

have a legal representative in Brazil.

Some suppliers with unique and strategicallycritical technology, however, might be able toserve the Brazilian market from Norway, atleast for a period of time.

2. Selling through a Brazilian Agent/

Representative

A number of Norwegian companies com-mercialize their products (and in some casesalso services) through a Brazilian agent or representative. This can work out well for suppliers that manage to become an impor-tant part of the portfolio of a focused andefficient agent.

Advantages: Low investment costs The agent already has an established

industry network, can follow up on op-portunities and is familiar with Brazilianregulations, requirements and businesspractices.

Disadvantages: Many agents carry a (too) high number

of representations, limiting the attentionthey are able to give to your products/services.

Coordination and reporting issues. Invoicing from outside of Brazil generally

adds at least 25% in extra taxes (seechapter 2.6 Paying Taxes)

3. Establishing an Entity in Brazil

Establishing own operations in Brazil isincreasingly becoming a business necessity,for various reasons: A continuous presence is necessary

to maintain and develop client relation-ships. An agent might not be able togive enough attention to your company.

Increased political pressure for localcontent (a part of the product must beproduced in Brazil) makes it an advan-tage, and in some cases a requirement,for foreign suppliers to have productionor assembly functions in Brazil.

Invoicing from Brazil saves at least 25%in taxes levied on invoices from abroad

(see chapter 2.6 Paying Taxes). In order to qualify most goods/services

for the Petrobras Master Vendor List,a legally established local presence isnecessary.

The main establishment options are:a) Establishing a fully owned subsidiary(most common)b) Establishing a joint venture with a Braziliancompanyc) Acquiring an existing Brazilian company.

The main focus of this guide is option a)Establishing a fully owned subsidiary. This isthe most common entry form for Norwegiancompanies in Brazil.

The contents of the guide are also valid for options b) and c), but these options poseadditional sets of challenges, and shouldalways be based on a solid due diligenceprocess. The increased attention neededfor coordination and control should not beunderestimated. Because of the managerial

and cultural challenges involved, it is neces-sary to put in place specialized transitionmanagement until operations and proce-dures are aligned.

Foreign companies are often offered to buyan existing, sleeping company in order to getstarted more quickly. However, the bureau-cracy around necessary alterations of bylawsand registrations generally makes this justas time consuming and costly as starting anew company from scratch. In practice, this

normally saves neither time nor money, andcan add potential risks.

...issues specific

to Brazil often

dictate a differ-

ent strategic

angle than what

would seem

obvious.

7/31/2019 Brazil How to Do Business in Brazil 2011

http://slidepdf.com/reader/full/brazil-how-to-do-business-in-brazil-2011 15/84

HOW TO DO BUSINESS IN BRAZIL14

www.howtodobusinessinbrazil.com

For companies entering Brazil, detailed mar-

ket research will be necessary to determinethe entry strategy. Both INTSOK and Innova-tion Norway, as well as specialized firms, canassist with this kind of research to create anunderstanding of the market potential for agiven product or service.

The end clients in the Brazilian oil andoffshore market are the E&P operators andasset owners, with Petrobras being the mostimportant one by far. From a macro perspec-tive, the Petrobras Business Plan is the key

driver for market opportunities. But sincethe oil and gas exploration monopoly wasabandoned in 1997, other E&P operatorshave also positioned themselves in the Bra-zilian market and are becoming increasinglyimportant.

Rig- and ship owners, engineering compa-nies, ship yards and other main contractorssupporting the operators also represent ex-cellent opportunities for Norwegian technol-ogy and services.

This market overview lists the main playersand drivers in the Brazilian oil/offshore andmaritime/shipbuilding markets, with twocompanies examined in more detail: Petrobras, as the key driver of opportu-

nities and pivotal for all oil and offshoreactivity in Brazil.

OGX, the largest fully private Brazil-ian oil company, with very aggressiveexpansion plans.

MARKET OVERVIEW– THE BRAZILIAN OIL, OFFSHOREAND MARITIME MARKET

The overall growth outlook for the Brazilian market is impressive,

creating vast opportunities in the oil, offshore and maritime

industries.

The Pre Salt Opportunity

Brazil has discovered gigantic potential oilreserves off the coast of South-East Brazil,in an area referred to as the Pre-Salt Area.The potential of this area is a key driver ofthe current oil investment boom in Brazil.

It is important to remember, however, thateven without the Pre-Salt Area, Brazil hasan oil output equal to that of Norway, setto double over the next 10 years. The mainpart of the growth forecasted in Petrobras’

business plan will come from already provenresources outside the Pre-Salt Area. Thevast Pre-Salt opportunities, which may welldwarf existing production, will come on topof this.

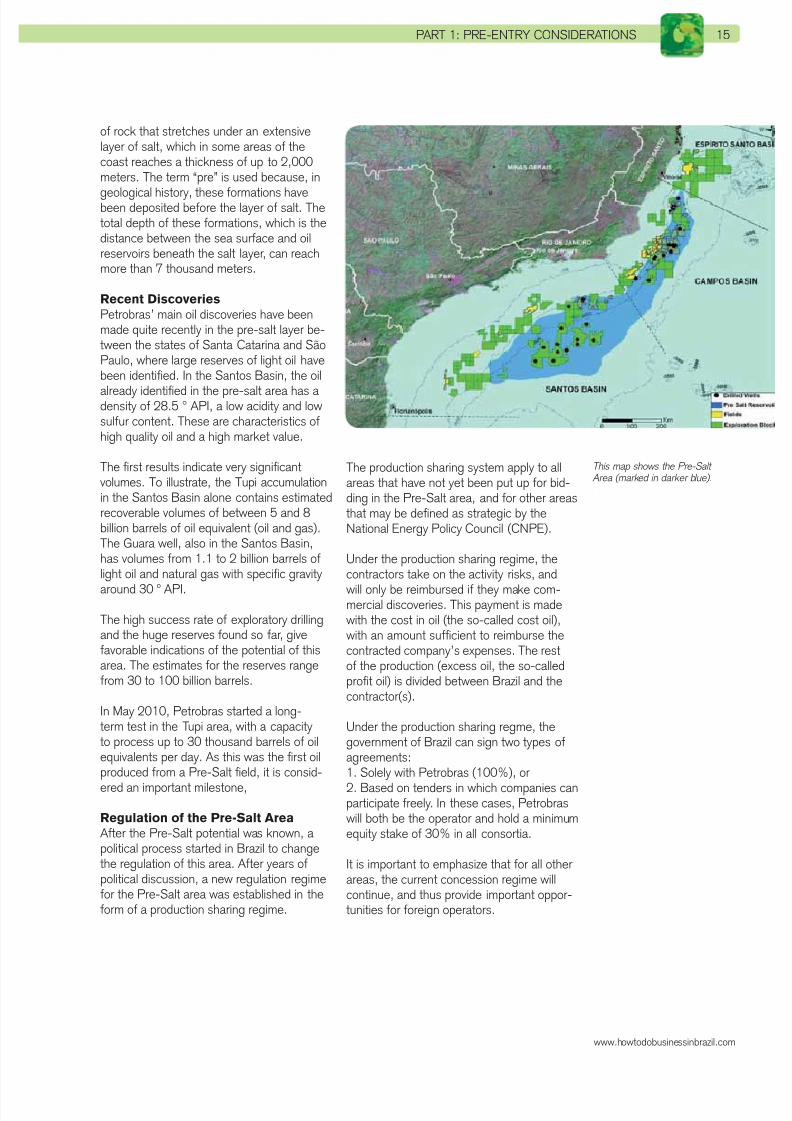

Geological Formation

The Pre-Salt layer is a geological formationon the continental shelves off the coast of Africa and Brazil, holding vast reserves of oil.It is called pre-salt because it forms a range

Structure of thePre-Salt area.

7/31/2019 Brazil How to Do Business in Brazil 2011

http://slidepdf.com/reader/full/brazil-how-to-do-business-in-brazil-2011 16/84

PART 1: PRE-ENTRY CONSIDERATIONS 15

www.howtodobusinessinbrazil.com

of rock that stretches under an extensivelayer of salt, which in some areas of thecoast reaches a thickness of up to 2,000meters. The term “pre” is used because, in

geological history, these formations havebeen deposited before the layer of salt. Thetotal depth of these formations, which is thedistance between the sea surface and oilreservoirs beneath the salt layer, can reachmore than 7 thousand meters.

Recent Discoveries

Petrobras’ main oil discoveries have beenmade quite recently in the pre-salt layer be-tween the states of Santa Catarina and SãoPaulo, where large reserves of light oil have

been identified. In the Santos Basin, the oilalready identified in the pre-salt area has adensity of 28.5 ° API, a low acidity and lowsulfur content. These are characteristics ofhigh quality oil and a high market value.

The first results indicate very significantvolumes. To illustrate, the Tupi accumulationin the Santos Basin alone contains estimatedrecoverable volumes of between 5 and 8billion barrels of oil equivalent (oil and gas).The Guara well, also in the Santos Basin,has volumes from 1.1 to 2 billion barrels oflight oil and natural gas with specific gravityaround 30 º API.

The high success rate of exploratory drillingand the huge reserves found so far, givefavorable indications of the potential of thisarea. The estimates for the reserves rangefrom 30 to 100 billion barrels.

In May 2010, Petrobras started a long-term test in the Tupi area, with a capacityto process up to 30 thousand barrels of oil

equivalents per day. As this was the first oilproduced from a Pre-Salt field, it is consid-ered an important milestone,

Regulation of the Pre-Salt Area

After the Pre-Salt potential was known, apolitical process started in Brazil to changethe regulation of this area. After years ofpolitical discussion, a new regulation regimefor the Pre-Salt area was established in theform of a production sharing regime.

The production sharing system apply to allareas that have not yet been put up for bid-ding in the Pre-Salt area, and for other areasthat may be defined as strategic by theNational Energy Policy Council (CNPE).

Under the production sharing regime, thecontractors take on the activity risks, and will only be reimbursed if they make com-mercial discoveries. This payment is made with the cost in oil (the so-called cost oil), with an amount sufficient to reimburse thecontracted company’s expenses. The restof the production (excess oil, the so-calledprofit oil) is divided between Brazil and thecontractor(s).

Under the production sharing regme, thegovernment of Brazil can sign two types of

agreements:1. Solely with Petrobras (100%), or 2. Based on tenders in which companies canparticipate freely. In these cases, Petrobras will both be the operator and hold a minimumequity stake of 30% in all consortia.

It is important to emphasize that for all other areas, the current concession regime willcontinue, and thus provide important oppor-tunities for foreign operators.

This map shows the Pre-Salt Area (marked in darker blue).

7/31/2019 Brazil How to Do Business in Brazil 2011

http://slidepdf.com/reader/full/brazil-how-to-do-business-in-brazil-2011 17/84

HOW TO DO BUSINESS IN BRAZIL16

www.howtodobusinessinbrazil.com

The Main Players

Operators

Petrobras is by far the largest oil pro-ducer in Brazil. Statoil is on its way tobecoming number two, when the Statoiloperated Peregrino field reaches itsplanned production of 100 000 barrelsper day in 2012.

OperatorPetroleum

(BPD)

Petrobras 1,881,455

Shell Brasil 75,235

Chevron Frade 67,825Empresa Devon (BP) 22,840

Sonangol Starfish 987

Statoil Brasil 885

Petrosynergy 602

Alvorada 558

UP Petroleo Brasil 351

Partex Brasil 278

Petrogal Brasil 217

UTC Engenharia 194

Recôncavo E&P 192

W. Petroleo 162

Severo Villares 26

Cheim 26

Norberto Odebrecht 18

Silver Marlin 15

Koch Petroleo 9

Egesa 7

Gran Tierra 6

Genesis 2000 6Vipetro 5

Panergy 3

Allpetro 0.2

Total 2,051,093

7/31/2019 Brazil How to Do Business in Brazil 2011

http://slidepdf.com/reader/full/brazil-how-to-do-business-in-brazil-2011 18/84

PART 1: PRE-ENTRY CONSIDERATIONS 17

www.howtodobusinessinbrazil.com

Important Organizations and Government Entities

For further descriptions of the listed entities, see Appendix 5: Frameworkand Stakeholders. (a) The National Energy Policy (CNPE)(b) The National Petroleum Agency (ANP)(c) Ministry of Mines and Energy (MME)(d) The Brazilian Institute of Environment and Natural Resources

- (IBAMA) and the National Environment Council (CONAMA)(e) National Agency of Waterway Transportation (ANTAQ)(f) Brazilian Navy (NAVY)(g) Directorate of Ports and Coasts (DPC)(h) Brazilian Institute of Oil, Gas and Biofuels (IBP)(i) National Organization of the Petroleum Industry (ONIP)

Brazil

State of Rio de Janeiro

Important EPC Companies and

Shipyards

An overview of the major EPC (Engineering,Procurement and Construction) companies

and shipyards in Brazil, all of them possiblecustomers for Norwegian oil, offshore andmaritime suppliers:

See also Appendix 6: Shipyards.

7/31/2019 Brazil How to Do Business in Brazil 2011

http://slidepdf.com/reader/full/brazil-how-to-do-business-in-brazil-2011 19/84

0

1000

2000

3000

4000

5000

6000

7000

020201591101020092008

HOW TO DO BUSINESS IN BRAZIL18

www.howtodobusinessinbrazil.com

Summary of Petrobras

Business Plan

The Petrobras business plan is updatedannually, and the market has recentlyseen a steady growth in planned invest-ments of more than 10% per annum.

The current plan, for 2011-2015, fore-sees investments at about the same levelas the 2010-2014 plan, with projectedinvestments over the next five yearsstipulated at USD 224.7 billion.

The main change from the last plan isthe increased investment in E&P, up

from 53% to 57%. This represents anincrease of USD 8.7 billion, with E&Pinvestments totaling USD 127.5 billion.

These investments will drive a stronggrowth in Petrobras’ output of oil andgas over the next 10 years. Most of theproduction growth will come from alreadyproven reserves. Getting resources, bothcapital and human, to achieve these am-bitious goals is the bottleneck for Brazilat the moment. The need for qualified

professionals is a growing concern inthis respect. In 10 years’ time Petrobrasexpects to have a production of over 6million barrels of oil equivalents per day.

With this growth, Petrobras is expected toovertake companies like ExxonMobil, BP, Shelland Chevron. And as a comparison, while the

Business Segment

Brazil and Abroad

as Production - Brazil

il Production - Brazil

as Prosuction - International

il Production - International

Brazilian oil output in June 2011 is roughlyequal to that of Norway, within the next 10years it will probably be double.

orporate

iofuels

istribution

etrochemicals

&E

ownstream

P

Corporate 1%

Biofuels 2%

Downstream 1%

Petrochemicals 2%

Natural gas, energy, gaschemicals 6%

RTC (refining, transportation,commercialization) 31%

E&P 57%

Total USD 224.7 billion

International

Brazil

International 5%

Brazil 95%

Total USD 224.7 billion

Gas Production - International

Oil Production - International

Gas Production - Brazil

Oil Production - Brazil

Pre-Salt Transfer of Rights

2,386 2,516 2,5752,772

+ 10 Post-SaltProjects

+ 8 Pre-SaltProjects

+ 1 Transfer of Rights

3,993

6,418

Petrobras Investments 2011-2015

Estimated production growth in Brazil

´ 0 0 0

b o e / d a y

4. 9 % p. Y.

Added CapacityOil2,300,000 bpd

+ 35 Systems

3 , 0

7 0

543

131,148

845

4 , 9

1 0

Accomplishment of 30 EWTs from2011 to 2015: 13 in the Pre-Salt, 7 inthe Transfer of Rights Area and 10 inthe Post-Salt.

Pre-Salt participation in the totalproduction will enchance from thecurrent 2% to 18% in 2015 and40.5% in 2020.

7/31/2019 Brazil How to Do Business in Brazil 2011

http://slidepdf.com/reader/full/brazil-how-to-do-business-in-brazil-2011 20/84

PART 1: PRE-ENTRY CONSIDERATIONS 19

www.howtodobusinessinbrazil.com

Petrobras Headquartersin Rio de Janeiro.

The world’s major oil producers

6000

5500

5000

4500

4000

3500

3000

2500

2000

1500

1000

500

2 0 0 0

2 0 0 1

2 0 0 2

2 0 0 3

2 0 0 4

2 0 0 5

2 0 0 6

2 0 0 7

2 0 0 8

2 0 0 9

2 0 1 0

2 0 1 1

2 0 1 2

2 0 1 3

2 0 1 4

2 0 1 5

2 0 1 6

2 0 1 7

2 0 1 8

2 0 1 9

2 0 2 0

Source: PFC Energy and Company reports

t h o u s a n d

b o e / d

Petrobras:3.9 MM boe/d in 2014and 6.4 MM boe/d in 2020

ExxonMobil:Production growth rate ~3-4%in 2010; ~2-3% p.y. up to 2013

BP:Production growthrate~1-2% p.y. up to 2015

Shell:~3.5 MM boe/d in 2012and ~3.7 MM boe/d in 2014

Chevron:Production growth rate ~1%p.y. between 2010-2014 and4.5% p.y.between 2014-2017

7/31/2019 Brazil How to Do Business in Brazil 2011

http://slidepdf.com/reader/full/brazil-how-to-do-business-in-brazil-2011 21/84

HOW TO DO BUSINESS IN BRAZIL20

www.howtodobusinessinbrazil.com

In a country where the oil, offshore andmaritime industries must compete fiercely with other sectors of the economy for scarceengineering resources, and where in addition

Critical Resources

Current

situation

Delivery Plan (to be contracted)

Accumulated Value

By 2013 By 2015 By 2020

Drilling Rigs Water Depth Above 2.000 m 5 26 31 53

Supply and Special Vessel 254 465 491 504

Production Platforms SS eFPSO 41 53 63 84

Others (Jacket and TLWP) 79 81 83 85

Supply Vessel

26 Rigs Contracted,

28 More to Be Built

by 2020, Totalling 54:

Until 2013:

13 rigs contracted before

2008 and 1 rig relocatedfrom international opera-

tions; + 12 new rigs con-

tracted in 2008, through

international bidding.

2013-2020:

Bidding in process, to

contract 28 rigs to be built

in Brazil.

Drilling Rigs

Productio Platform (FPSO)

Petrobras construction needs

the local industry is rarely competitive on theinternational market, Petrobras and Brazilare facing a huge challenge.

7/31/2019 Brazil How to Do Business in Brazil 2011

http://slidepdf.com/reader/full/brazil-how-to-do-business-in-brazil-2011 22/84

PART 1: PRE-ENTRY CONSIDERATIONS 21

www.howtodobusinessinbrazil.com

But in order to build and en-sure the smooth operations ofso many offshore rigs and ves-sels, there is a huge need for

sub-suppliers of products andservices of all categories. Andlocal industry is not expectedto be able to fulfill all theseneeds. See the graphs on thispage for a demand overviewfor the Brazilian offshore sector until 2015.

At the same time, the need(and opportunity) to build astrong local supplier industryis increasing, and this hasbecome a key political issue inBrazil. The politicians intend touse this unique opportunity todevelop the local industry, andhave implemented both regula-tions and incentives to increasethe local content in the Brazil-ian oil, gas and offshore indus-try (for more details, see nextpage and the Local Contentchapter on page 63).

CUBEAUTO Chart

S(ChartType:ColumnStacked

;Legend:Custom;GridLinesX:off;GridLinesY:off;LegendX:0;LegendY:0;Palette :Default;PaletteText:off;AxisTitleY:{u};LegendCols:1;LegendRows:3)

F(INTSOK Geographical Market:Brazil;On-Offshore:Offshore;INTSOK Category:Field Development)

C(INTSOK Market Definition)

R(Year:2005-2015)

V(EP Expenditure:USD million)

CUBEAUTO Chart

S(ChartType:ColumnStacked ;Legend:Custom;GridLinesX:off;GridLinesY:off;LegendX:0;LegendY:0;Palette :Default;PaletteText:off;AxisTitleY:{u};LegendCols:1;LegendRows:3)

F(INTSOK Geographical Market:Brazil;On-Offshore:Offshore;INTSOK Category:Subsea)

C(INTSOK Market Definition)

R(Year:2005-2015)

V(EP Expenditure:USD million)

CUBEAUTO Chart

S(ChartType:ColumnStacked ;Legend:Custom;GridLinesX:off;GridLinesY:off;LegendX:0;LegendY:0;Palette :Default;PaletteText:off;AxisTitleY:{u};LegendCols:1;LegendRows:3)

F(INTSOK Geographical Market:Brazil;On-Offshore:Offshore;INTSOK Category:Well)

C(INTSOK Market Definition)

R(Year:2005-2015)

V(EP Expenditure:USD million)

CUBEAUTO Chart

S(ChartType:ColumnStacked ;Legend:Custom;GridLinesX:off;GridLinesY:off;LegendX:0;LegendY:0;Palette :Default;PaletteText:off;AxisTitleY:{u};MaxValue:10000)

F(INTSOK Geographical Market:Brazil;On-Offshore:Offshore;INTSOK Category:Operations)

C(INTSOK Market Definition)

R(Year:2005-2015)

V(EP Expenditure:USD million)

Demand overview, the Brazilian offshore sector (source: INTSOK)

Field Development

Offshore Field Development Market by Definition – Brazil

Subsea

Subsea Market by Definition – Brazil

Well

Offshore Well Market by Definition – Brazil

Operations

Offshore Operations Market by Definition – Brazil

7/31/2019 Brazil How to Do Business in Brazil 2011

http://slidepdf.com/reader/full/brazil-how-to-do-business-in-brazil-2011 23/84

HOW TO DO BUSINESS IN BRAZIL22

www.howtodobusinessinbrazil.com

OGX

Besides Petrobras, the most active E &P company in Brazil right now is OGX, aBrazilian company owned by Eike Batista,Brazil’s richest person. OGX is the larg-est fully private Brazilian oil company. Their license portfolio has been growing fast, andthe company is now entering a new phase with initial production. Their ambition level isextremely high: over 1 million barrels within10 years, as shown in the below chart.

To achieve their ambitious growth targets,OGX will also require a high number ofoffshore assets. Demand for new FPSOsfor example is expected to reach 60 unitsfor Petrobras and OGX alone. It is alsoassumed that around 50% of the world’sdeep-water fleet for both FPSOs and rigs will be in Brazil over the next few years.

This of course represents many opportunitiesfor service suppliers to this segment, an area where the offering from local suppliers still ismodest and the market immature.

OGX equipment demand and production targets

1,380

730

20

CAGR 70 %

OGX Production Targets - kboepd

2011E 2015E 2019E

Base Case of 48 Offshore E & P Units Equivalent toUS$ 30 bn

ahead of schedule

st FPSO already contracted with OSX for a periodof 20 years, at an average day rate of US$ 263,000

Expected Demand of Offshore Equipment (2011 - 2019)Number of Units

FPSO

TLWP

WHP

Total

19

5

24

48

Source: OGX

Delivery Timeline

2011E 2012E 2013E 2014E 2015E 2016E 2017E 2018E 2019E

1 1 1 4 5 32 1 1

1 1

4

7

11

13

6

4

13

1

2

1

5

1

6

6

2

2

Source: OGX

7/31/2019 Brazil How to Do Business in Brazil 2011

http://slidepdf.com/reader/full/brazil-how-to-do-business-in-brazil-2011 24/84

PART 1: PRE-ENTRY CONSIDERATIONS 23

www.howtodobusinessinbrazil.com

The Shipbuilding Market

Benefitting from both the growingneed for rigs and ships, and thecontinued tightening of the gov-ernment’s local content initiative,the Brazilian ship building industryare currently being rebuilt and the whole sector re-energized. Manyshipyards that were flourishing inthe “golden eighties” but almostinactive in the nineties, are nowincreasing their production andpositioning themselves for theincreased demand.

See Appendix 6 Brazilian Ship-yards for an overview of the mainshipyards and their current activitylevels.

At the same time, the Braziliangovernment and Petrobras aregiving incentives to new shipyardsto be built from scratch, filling upthe order books for these so-called“Virtual Shipyards”. The most suc-cessful one so far is the Atlantico

Sul shipyard just south of Recife,already with an order book of 22tankers before the shipyard haseven been completed. Recently Atlantico Sul was also awardedthe contract to build the first 7 in atotal package of 28 drillships to beconstructed in Brazil over the nextdecade.

Still, the Brazilian shipbuildingindustry is not competitive inter-nationally, even if 10 years have

passed since the market started toimprove. This is due to various fac-tors, including lack of investments,lack of qualified labor, powerfullabor unions and a very strong localcurrency.

Without the demand brought on bylocal content we would not haveseen the level of shipbuilding andrelated activities that are takingplace in Brazil today.

Many shipyards are

now increasing their

production andpositioning

themselves for the

increased demand.

7/31/2019 Brazil How to Do Business in Brazil 2011

http://slidepdf.com/reader/full/brazil-how-to-do-business-in-brazil-2011 25/84

HOW TO DO BUSINESS IN BRAZIL24

The overall minimum percentage of localcontent in a product or service is defined bythe government, and this has implicationsfor foreign suppliers entering the Brazilian

market. Being able to meet local contentquotas may in many cases be a necessity,and in other cases contribute to a competi-tive advantage.

A very brief summary of the system: Companies that win a concession to

operate an oil field must commit to anoverall local content level, on averagearound 60%, depending on product andapplication.

The local content commitment is passedon to suppliers. Percentages vary for

different types of equipment and ser-vices, but the overall local content quotamust be met.

Each level of suppliers and sub-suppli-ers must prove their local content levelthrough certificates issued by an author-ized local content certification company.

At least 10% of the product value mustbe added in Brazil for the local contentto be registered. on top of that, all valueadded in Brazil, including assembly,testing and even the sales margin can

contribute to increase the official localcontent level.

THE NEED FOR

PRODUCTION IN BRAZIL

The local content debate is heated in Brazil,and local content is a reality that all com-panies must take into consideration when

evaluating their chances in the Brazilianmarket.

For some foreign companies, with uniqueproducts, it would be possible to do businessdirectly from abroad without local content,at least in the first stages of market entry.For most companies, however, it will be anecessity to create sufficient local content toensure competiveness in the long run. Thegovernment’s stated goal is that by 2020,90% of all production should take place in

Brazil.

For more details, see Local Content, page63.

There is increasing political pressure in Brazil for as much as possible of

the production for the oil and offshore industry to be done in Brazil.

www.howtodobusinessinbrazil.com

“Everything that can be

done in Brazil, shall bedone in Brazil.”

- Former Brazilian

president Lula

7/31/2019 Brazil How to Do Business in Brazil 2011

http://slidepdf.com/reader/full/brazil-how-to-do-business-in-brazil-2011 26/84

PART 1: PRE-ENTRY CONSIDERATIONS 25

Innovation Norway

Innovation Norway’s International Growth

Program provides local assistance and coun-seling for establishing a company in foreignmarkets.

Services: Market consulting Practical assistance Networks with local knowledge

The companies pay 50% of InnovationNorway’s hourly costs; the remaining 50% iscovered by public funds through the Interna-

tional Growth Program.

More information:http://www2-invanor.no1.asap-asp.net/Tjenester/Programmer/Internasjonal-vekst-programmet/- (only in Norwegian)

INTSOK

INTSOK - Norwegian Oil and Gas Partners- was established by the Norwegian oil and

gas industry and the Norwegian Govern-ment. INTSOK is an effective vehicle for promoting the Norwegian offshore industry’scapabilities to key clients in the Brazilianmarket, as well as providing market informa-tion to its partners.

Services: Market entry services to INTSOK

partners free of charge at a maximumof 5 days per year per market

Market entry project for Brazil Client seminars, workshops, network

meetings, strategic advice.

More information: www.intsok.com

AVAILABLE SOURCES OF

FINANCING AND SUPPORTCompanies preparing to expand internationally should be aware of the

financing opportunities available to Norwegian companies.

www.howtodobusinessinbrazil.com

GIEK – Garanti-Instituttet for

Eksport-Kreditt

Safe export: GIEK guarantees for Norwe-gian companies’ export credits on behalf ofThe Norwegian Government. With assis-tance from GIEK, exporters can offer creditor finance without bearing the entire riskthemselves. GIEK secures competitive termsfor the industry and promotes the export ofNorwegian goods and services and invest-ment abroad.

Services: GIEK offers guarantees for buyer and

supplier credit, pre-shipment, bid bondsand tenders, investments, building loansand letters of credit.

Credit insurance.

More information: http://www.giek.no/produkter/en

Nopef – the Nordic Project Fund

(“Nordisk Eksportfond”)

Nopef can finance up to 40% of the ap-

proved feasibility study costs in connection with international business set up, in theform of a loan that can be fully or partiallyconverted into a grant pending final projectreport approval.

A company is eligible for Nopef loans if thecompany: has fewer than 250 employees and a

turnover less than 50 MEUR. is operational in the Nordic countries. has experience in the same business

area as the project.

More information: http://www.nopef.com/pages/eng/financing.php

7/31/2019 Brazil How to Do Business in Brazil 2011

http://slidepdf.com/reader/full/brazil-how-to-do-business-in-brazil-2011 27/84

26

CONTENTS START-UP PHASE:

28 Introduction

29 Company Establishment

31 Visa Requirements

33 HR, Brazilian Employees

36 Expat Management

39 Paying Taxes

44 Accounting

46 Legal Issues

48 Petrobras Supplier Certification

52 Business Culture in Brazil

7/31/2019 Brazil How to Do Business in Brazil 2011

http://slidepdf.com/reader/full/brazil-how-to-do-business-in-brazil-2011 28/84

27

7/31/2019 Brazil How to Do Business in Brazil 2011

http://slidepdf.com/reader/full/brazil-how-to-do-business-in-brazil-2011 29/84

HOW TO DO BUSINESS IN BRAZIL28

www.howtodobusinessinbrazil.com

All administrative and operational systemsneed to be established and adjusted, thecompany needs to start paying taxes, reportto the authorities, hire and manage employ-ees, and relate to the local legal framework. At the same time, the company must buildsales and get certified as a supplier to keycustomers.

Experience shows that a common mistakeis underestimating the administrative andlegal complexity of Brazil. In many cases,

a foreign expat in a Country Manager rolecan end up spending a lot of time trying to

The first 12-24 months is the critical start-up phase where many

foreign companies get consumed by bureaucracy and complex

administrative requirements.

resolve administrative issues rather thanfocusing on the market development. Thisis especially true if proper attention has notbeen given to planning and organization dur-ing the initial phases of a new Brazilian com-pany’s life. Adding to the challenges is thefact that it is not always immediately noticed when an unfortunate or even illegal admin-istrative decision has been taken. Resultingproblems may compound, and could derailthe company’s development due to the costand time involved in restructuring systems

and updating registrations with necessaryauthorities.

7/31/2019 Brazil How to Do Business in Brazil 2011

http://slidepdf.com/reader/full/brazil-how-to-do-business-in-brazil-2011 30/84

PART 2: START-UP PHASE 29

COMPANY

ESTABLISHMENT

www.howtodobusinessinbrazil.com

Setting up a company in Brazil can be a long

and time-consuming process. It involves anumber of steps which all need to be carriedout in the right order and with a great atten-tion to detail. Short-cuts are inadvisable, asthis is very likely to halt the whole processand create additional delays.

When the process is well managed how-ever, and foreign investors are aware of thenecessary documentation and legal require-ments, things can run relatively smoothly.

The most common way for

foreign companies to establish a

presence in Brazil is to set up a

Brazilian subsidiary.

Deciding on Company Type

Brazilian law allows for several types ofcorporate entities. Most foreign investors optfor theLimitada (Limited Liability Company- “Sociedade Limitada”). In some cases theS.A. (Joint Stock Company - “Sociedade Anônima”) is to be preferred.

Limitada (Ltda.)

The flexible decision making mechanisms,reduced bureaucracy, no audit requirements,greater confidentiality and lower operatingcosts makes this a very attractive option for small and medium sized companies. Further,there are no mandatory auditing require-ments for limitadas.

S.A.

The freely transferrable shares, more formaldecision-making process and easier accessto external financing makes this a better choice for larger companies with a morediversified shareholding. An S.A. must beaudited once a year.

For more details on these company types,see Appendix 4: Differences between Limi-tada and S.A.

3 to 4 months

is a realistic

time frame

to get a

company fully

operational.

7/31/2019 Brazil How to Do Business in Brazil 2011

http://slidepdf.com/reader/full/brazil-how-to-do-business-in-brazil-2011 31/84

HOW TO DO BUSINESS IN BRAZIL30

www.howtodobusinessinbrazil.com

Establishment Process

This is a brief overview of the process of es-tablishing a company in Brazil. Each step hasits own procedures and sub-steps, whichdepend on the specifics of the company.

Initial Preparations

1. Select a company name and checkavailability

2. Select an qualified attorney-in-fact torepresent each of the foreign partners,and prepare power of attorney(s)

3. Register the foreign partners with theBrazilian Central Bank

4. Apply for a notarised Norwegian certifi-

cate of incorporation5. The power of attorney and certificates

of incorporation must be authenticatedby a Norwegian public notary (“NotariusPublicus”), consularized (verified) by theBrazilian embassy in Oslo and translatedinto Portuguese by a certified translator in Brazil

6. Register the foreign partners with theBrazilian Central Bank and get the busi-ness registration number.

Legally Incorporating the Company7. Draft the company’s articles of associa-tion (“Contrato Social”) and establishthe company by public deed (Limitada)or in a general meeting of incorporation(Corporation).

8. The newly formed company can thenregister its corporate acts with the localBoard of Trade (“Junta Comercial”) inorder to obtain a company registrationnumber (“NIRE”).

9. Register for federal and state taxes, re-ceive a company tax number (“CNPJ”).

10. By completing this process, the com-pany will also be automatically registered with the National Institute of SocialSecurity (“INSS”).

11. The company will now be automaticallyregistered with the government savingsbank for social security purposes, “CaixaEconomica Federal (CEF)”, with anaccount in the Federal UnemploymentFund (“FGTS”).

12. Depending on the area of activity, thecompany might need to apply for a spe-

cific environmental or sanitary licencebefore obtaining the CNPJ.

Receiving the CNPJ marks the start of thecompany as an independent legal entity and allows it to sign contracts. However, it can still not employ people or invoice customers.

A few further steps are required to make thecompany fully operational.

Getting the Company Operational

13. Open a Brazilian bank account14. Register the paid foreign share capital

with the Central Bank15. Register the company with municipal tax

authorities16. Apply for permission to issue invoices,17. Register employees with the National

Institute of Social Security (“INSS”)

18. Register employees in the company’saccount with the Federal UnemploymentFund (“FGTS”)

19. Notify the Ministry of Labor of employ-ees

20. Register with the Patronal Union andthe Employee Union

21. Apply to the municipality for an opera-tions permit (“Alvará”).

Time Frame

When the whole process is well managedand no specific problems occur, each of thethree phases will take around 30 days. Ex-perience shows however that it rarely takesless than 4 months to get a company fullyoperational. A lot of time is often lost in thepreparation phase, and poor communicationand coordination are factors that often causedelays.

Corporate Capital Needs

There are generally no minimum corporatecapital requirements in Brazil, except for afew specific sectors.The optimal amount willtherefore depend on variables such as thetype of activity, planned investments, work-ing capital requirements, expected opera-tional cash flow and risk profile. The amountof planned imports may also be a factor asimport licences are linked to an evaluation ofcompanies’ perceived financial solidity.

Although there is no specific requirementregarding the optimal amount of corporatecapital, at least R$ 150.000 is recommend-

ed for service providers and significantlymore for industrial players depending on thenature of their activity.

7/31/2019 Brazil How to Do Business in Brazil 2011

http://slidepdf.com/reader/full/brazil-how-to-do-business-in-brazil-2011 32/84

PART 2: START-UP PHASE 31

ISA REQUIREMENTS

www.howtodobusinessinbrazil.com

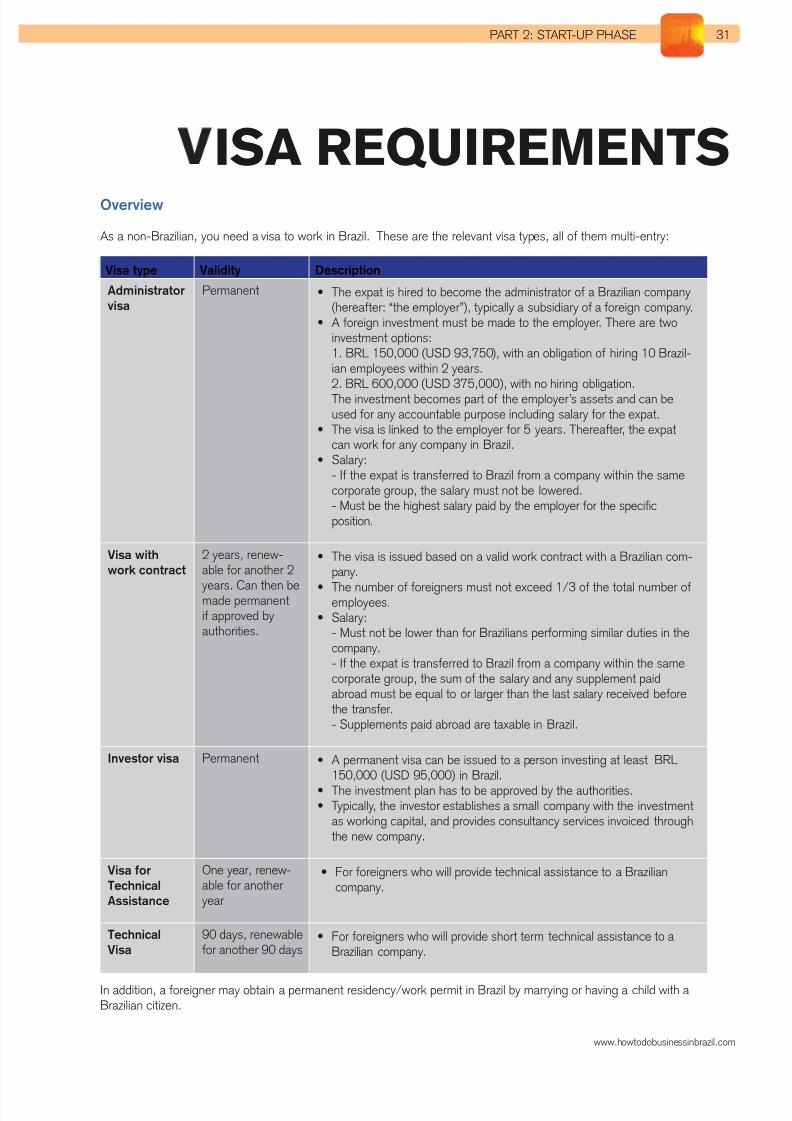

Overview

As a non-Brazilian, you need a visa to work in Brazil. These are the relevant visa types, all of them multi-entry:

Visa type Validity Description

Administrator

visa

Permanent The expat is hired to become the administrator of a Brazilian company(hereafter: “the employer”), typically a subsidiary of a foreign company.

A foreign investment must be made to the employer. There are twoinvestment options:1. BRL 150,000 (USD 93,750), with an obligation of hiring 10 Brazil-ian employees within 2 years.2. BRL 600,000 (USD 375,000), with no hiring obligation.The investment becomes part of the employer’s assets and can beused for any accountable purpose including salary for the expat.

The visa is linked to the employer for 5 years. Thereafter, the expatcan work for any company in Brazil.

Salary:- If the expat is transferred to Brazil from a company within the samecorporate group, the salary must not be lowered.- Must be the highest salary paid by the employer for the specificposition.

Visa with

work contract

2 years, renew-

able for another 2years. Can then bemade permanentif approved byauthorities.

The visa is issued based on a valid work contract with a Brazilian com-pany.

The number of foreigners must not exceed 1/3 of the total number ofemployees.

Salary:- Must not be lower than for Brazilians performing similar duties in thecompany.- If the expat is transferred to Brazil from a company within the samecorporate group, the sum of the salary and any supplement paidabroad must be equal to or larger than the last salary received beforethe transfer.- Supplements paid abroad are taxable in Brazil.

Investor visa Permanent A permanent visa can be issued to a person investing at least BRL150,000 (USD 95,000) in Brazil.

The investment plan has to be approved by the authorities. Typically, the investor establishes a small company with the investment

as working capital, and provides consultancy services invoiced throughthe new company.

Visa for

Technical

Assistance

One year, renew-able for another year

For foreigners who will provide technical assistance to a Braziliancompany.

Technical

Visa

90 days, renewablefor another 90 days

For foreigners who will provide short term technical assistance to aBrazilian company.

In addition, a foreigner may obtain a permanent residency/work permit in Brazil by marrying or having a child with aBrazilian citizen.

7/31/2019 Brazil How to Do Business in Brazil 2011

http://slidepdf.com/reader/full/brazil-how-to-do-business-in-brazil-2011 33/84

HOW TO DO BUSINESS IN BRAZIL32

www.howtodobusinessinbrazil.com

Is it Necessary to Apply for a Visa

for Regular Business Trips to

Brazil?

Norwegians automatically receive a 3month visitor’s visa on arrival in Brazil. Themaximum allowed stay is an accumulated6 months per 12 month period. Businessmeetings can be conducted during this time,but the visa is not intended for work activitiessuch as rendering services to clients. Also,you are not allowed to embark on offshoreinstallations with only a visitor’s visa.

IMPORTANT: On arrival in Brazil, all foreigners need to specify the pur- pose of the visit on the arrival form. If you don’t have a specific work visa, select “Business” and NOT “Work”.If “Work” is indicated and there is no

work visa in your passport, you are likely to be refused entry and put on a flight out of Brazil at your own expense. This actually happens quite frequently.

Obtaining a Visa

The visa process involves a substantialamount of forms and attestations, as well asextensive interaction with relevant authori-ties. It is highly recommended to let a spe-cialized company handle the visa process.

How Long Does it Take?

The Ministry of Labor processes a work visain 30-60 days after all the correct docu-mentation has been submitted, but becauseof the other work involved (see below), arealistic time frame is 3-4 months for the

whole process.

How Much Does it Cost?

A specialized company will charge aroundUSD 2,000 per visa for the visa types listedin this chapter, except for the 90 Day Tech-nical Visa which should cost around USD700. In addition, consular processing feesamount to around USD 500.

Brief Overview of the Visa Process

1. Necessary forms and attestationsmust be filled in according to therequirements, which vary betweenthe different visa types. Non-Braziliandocuments generally include have tobe notarized at a public notary officein the country of origin, and then veri-fied at the Brazilian Embassy in thesame country.

2. All documents are sent to Brazil, where they have to be translated toPortuguese by a state authorizedtranslator.

3. Visa documents are submitted to theMinistry of Labor, which has a pro-cessing time of around 2 months.

4. If the application is successful, thevisa will be sent to any Braziliandiplomatic station outside of Brazil,at your choice, where the visa willbe available for 180 days. The visacan not be collected in Brazil. Whencollecting the visa, it is necessary topresent an English official transcript

of your criminal record no older than90 days, issued by the police of your home country.

5. When the visa has been collected, thevisa holder must travel to Brazil within90 days.

6. Within 30 days after arrival in Brazil,the visa holder must report to thefederal police (“Policia Federal”) for registration.

7. For permanent visa holders, the Poli-cia Federal will issue an ID card withthe RNE (National Registry of For-eigners) number. This takes another 6months. In the meantime, a stampedpaper slip called “Protocolo” with aphoto of the visa holder is issued asa temporary proof of the visa status.The Protocolo or RNE card must bepresented together with the passport when entering Brazil.

7/31/2019 Brazil How to Do Business in Brazil 2011

http://slidepdf.com/reader/full/brazil-how-to-do-business-in-brazil-2011 34/84

PART 2: START-UP PHASE 33

www.howtodobusinessinbrazil.com

As the company grows, there will inevitably be a need for employing

and managing Brazilian staff. Brazilian labor laws provide a detailed

and rigid framework for the management of employees.

Overview

Brazilian employees enjoy very good pro-tection by the laws. It is not uncommon for former employees to sue their ex-employer,especially if unlawful demission can beclaimed. This type of cases can be time-consuming, and the verdict almost always is

in the former employee’s favor. Therefore,special care has to be taken 1) when evalu-ating candidates to hire, and 2) to make surethat all labor regulations are strictly adheredto, to avoid grounds for lawsuits.

Salaries and Employee Costs

Basic administrative staff is less costly inBrazil than in Norway. Specialized person-nel like engineers and managers will matchor even exceed Norwegian salary levels,especially if the employee is proficient inEnglish (less than 10% of the population

speaks English.) The social costs levied bythe government for each employee amountto approximately 80% of the gross salary.Considering other common benefits, includ-ing meal tickets, transportation allowancesand private pension plans the total cost of anemployee is around 2x the gross salary.

Below is an overview of typical salary rangesfor some professions in Brazil. The figuresare gross salaries. To find the cost of em-ployment, each figure has to be multiplied by

2 (approximately) to find the total cost to thecompany.

HR, BRAZILIAN

EMPLOYEES

7/31/2019 Brazil How to Do Business in Brazil 2011

http://slidepdf.com/reader/full/brazil-how-to-do-business-in-brazil-2011 35/84

HOW TO DO BUSINESS IN BRAZIL34

www.howtodobusinessinbrazil.com

Non-mandatory, but common benefits(cost pr. month pr. employee): Health and dental insurance: USD 150

- 500. Life insurance: USD 35 - 70. Private pension plan: 4% - 8% of salary. Lunch: USD 250 - 650.

Managing the Employees

See “Appendix 2: Labor Law” for more de-tails on HR regulations. Some highlights: Work hours: Maximum 8 hours per day

and 44 hours per week. Entitlements: Christmas bonus (equal

to one month’s salary), vacation bonus(equal to 1/3 of one month’s salary).

Vacation: 22 work days after each12-month working period. No vacationentitlement during the first 12 months ofemployment.

Maternity leave: 120 days, extendableto 180. Paternity leave: 5 days.

Minimum salary: BRL 580 (ca USD380) pr month, adjusted annually.

Position Comment Required Min.

Experience

Monthly Salary

(USD)

Receptionist A receptionist is only expected to answer thephone and receive visitors, and has a low de-gree of autonomy.

None 650 - 1,100

Executive

Secretary

Experience shows that many start-ups need anexecutive secretary rather than just a recep-tionist. An executive secretary writes letters,memos, takes care of reservations and travelitineraries etc, in addition to receptionist tasks.This is normally a person with some level ofhigher education.

1-2 years 1,900 - 2,500

Sales Assistant 2 years Ca 4,000

Financial Manager 5-10 years Ca 6,500Sales Manager 5-10 years Ca 7,500

General Manager 10-15 years 12,000 - 15,000

Engineer For offshore work, up to 88% is added to thefixed salary, depending on the salary regimechosen. It is advisable to consult with a com-pany with specific offshore payroll knowledgebefore deciding on the salary regime.

Recent universitygraduate

3,500 - 5,000

1-5 years 3,500 - 7,500(incl. offshoresupplement)

5-10 years 7,500 - 11,000(incl. offshore

supplement)

Engineer

with oil/gas

management

experience

Project manager role 5 years Ca 9,500

Branch manager role 10 years Ca 14,000

15 years Ca 17,000 -19,000

...the total cost of an employee is

around 2x the gross salary.

Salary ranges for some Brazilian employee categories.

7/31/2019 Brazil How to Do Business in Brazil 2011

http://slidepdf.com/reader/full/brazil-how-to-do-business-in-brazil-2011 36/84

PART 2: START-UP PHASE 35

www.howtodobusinessinbrazil.com

Terminating a Contract

Individual agreements may be terminatedupon lapse of the determined period or bynotice from either Company or the em-ployee.

In the event of termination, the employee isentitled to receive (a) the balance of his or her pay, (b) the corresponding payment for vacations not taken, and (c) a proportionalamount of the Christmas bonus equivalent to

the number of months he or she has workedduring the calendar year.

In the event fixed-term agreements areterminated without cause, the terminatingparty must pay damages in the amount offorty percent (40%) of the compensationestablished for the remaining term of theagreement. In the case of contracts with anindefinite term, the terminating party mustgive prior notice of at least thirty (30) days.

The employee who registers as a candidate

for a position of union leader or representa-tive may not be dismissed as of the date ofsaid registration until one year after termina-tion of the term of office, even if electedas alternate, unless the employee commitsa serious fault under the terms of the law.Other employees who have attained a tem-porary employment stability set forth either by law or by collective bargaining agreement,such as expectant mothers and employeesthat have been away from work due to workaccident, may not be dismissed either.

Alternatives to Hiring

Independent Individual Service

Providers

Many mid to high level managers in small/medium sized companies prefer to invoicefor their time as independent service provid-ers, rather than being an employee of thecompany. In practice, this setup is flexibleand easy to manage. The manager generally works full time for the company, and invoicesthrough his/her own small service company.

Benefits: For the hiring company: no social costs

on top of the salary, easy to manage.

For the manager: lower tax, more flex-ibility.

Drawbacks: For the hiring company: Higher risk,

as the manager may in some casesretroactively claim de facto employeestatus and benefits based on tasks and work hours.

For the manager: Lower job security,loss of social benefits and pension/health plans available to regular employ-

ees.

Outsourcing of Functions

Some functions, like accounting services,are commonly outsourced to individual com-panies. But it can also be very worthwhileto consider outsourcing administrative andback-office functions like payroll, HR, finan-cial and tax management. In this case it isnecessary to be able to follow up and evalu-ate the quality of the outsourced services, which can vary considerably.

Benefits: Do not have to build in-house capacity. Frees up time for managing operational

issues. Leaner organization.

Drawbacks: Quality may vary considerably between

suppliers, so a thorough backgroundcheck is necessary.

Higher probability of communication andcoordination problems.

7/31/2019 Brazil How to Do Business in Brazil 2011

http://slidepdf.com/reader/full/brazil-how-to-do-business-in-brazil-2011 37/84

HOW TO DO BUSINESS IN BRAZIL36

www.howtodobusinessinbrazil.com

Salaries and Employee Costs

Based on benefit policy and the expat’s fam-ily situation, the total annual cost per expatnormally is in the USD 350,000 - 700,000(NOK 2 - 4 million) range. It is customary tocover all living expenses in the expat’s salarypackage.

Housing costs are calculated for a familyliving in the Ipanema/Leblon area in Rio de Janeiro, which receives the great majority offoreign expats in Rio. Nearby, recommend-able neighborhoods will have slightly lower housing costs.

EXPAT MANAGEMENT

Cost Items Comment Annual Cost

(NOK)

Salary It is common to offer a full Norwegian salary with anadditional 50% to compensate for being expatriated.Social cost is 80% of the salary.

1.5 - 2.5 million

Car/Benefits 100,000

Family Re-

lated Costs

Income compen-sation for spouse

It is customary to compensate for the lost incomeof the spouse, as a spouse is generally only grantedresidency and not a work visa. The Norwegian Ministryof Foreign Affairs (MFA) suggests an additional NOK 210,000 for the accompanying spouse.

210,000

Living expensesper child

Rate suggested by the Norwegian MFA 56,000

Tuition per child Rate suggested by the Norwegian MFA 130,000

Home travel 2 trips per year for the family 50,000

Housing

Costs

(Ipanema/

Leblon)

Apartment hotel 1-2 bedrooms, not luxury, small kitchen and cleaningincluded: ca NOK 30,000 - 35,000 per month

360,000-420,000

Apartment 3-4 bedrooms, Decent standard, reasonable location:NOK 35,000 - 40,000 per month

420,000 -480,000

3-4 bedrooms, OK standard, better located: NOK 40,000 - 50,000 per month

480,000 -600,000

3-4 bedrooms, recently renovated, new, good location(typical executive apartment): NOK 60,000 - 70,000per month

720,000 -840,000

Gas, electricity,internet

Ca NOK 2,000 per month 24,000

Expat costs

7/31/2019 Brazil How to Do Business in Brazil 2011

http://slidepdf.com/reader/full/brazil-how-to-do-business-in-brazil-2011 38/84

PART 2: START-UP PHASE 37

www.howtodobusinessinbrazil.com

Practical Tips for New Expats

in Brazil

Social Security Number and

Identification

The Brazilian equivalent of a social securitynumber is in fact two numbers, both of themnecessary in order to live and work in Brazil,see table below:

ID Needed For Comment How To Get It Cost Time Frame

CPF

(Registry

of

Persons)

Almost all transactionsand official purposes.

Required for anyone with a formal connec-tion to Brazil, also for non-residents.

The process is initiatedat a post office or inany filial of Banco doBrasil, and requires afollow-up visit to themunicipal tax authori-ties.

AboutBRL 15.

About 2 weeks.

RNE

(National

Registry

of For-

eigners)

Activities only availableto residents, such assigning of contracts,public health services

etc.

The official BrazilianID card for foreigners, which proves Brazil-ian residency. Issued

to foreigners with aqualifying visa.

The RNE number isissued by the federalpolice when the visais presented to them

after arrival. (See 2.3Visa Requirements.)

Includedin costof visa.

Issuance ofRNE number:10 days.The physical

ID card: 6months.

Visa for Spouse and Children

An expat’s spouse and children are includedin the expat’s visa. The spouse generallygets a residence permit only, and is NOT

allowed to work in Brazil.

Finding an Apartment

Apartment prices are high in Brazil (seeExpat Management, previous page.) Find-ing a good apartment is time consuming,and could easily take a month or two. Thegeneral standard is lower than in Norway, which often makes it necessary to see a lotof apartments to find a nice one.

In Rio de Janeiro, virtually all expats are living

in the Zona Sul area, with the great major-ity in the Ipanema or Leblon neighborhoods.There are many real estate agents in ZonaSul which can assist in finding an apart-ment. The website www.zap.com.br andthe Sunday edition of the Globo newspaper have comprehensive listings of apartmentsfor rent.

In São Paulo, good areas include Jardinsand adjacent neighborhoods, as well as Mo-rumbi and a few other areas. The São Paulotraffic is congested, so it is generally a goodidea to live close to the office.

Standard rental contract length in Brazil is36 months, with the possibility of moving outafter 12 months without extra costs. Movingout before 12 months generally incurs a fineof up to 3 months’ rent.

...the total annual

cost per expat

is normally NOK

2-4 million.

Social Security Number and Identification

7/31/2019 Brazil How to Do Business in Brazil 2011

http://slidepdf.com/reader/full/brazil-how-to-do-business-in-brazil-2011 39/84

HOW TO DO BUSINESS IN BRAZIL38

www.howtodobusinessinbrazil.com

Security

It is easy to get a negative impression ofthe security situation in Brazil through newsreports. But in general, working and living in

Rio de Janeiro or São Paulo is unproblem-atic, as long as some basic common senseprecautions are taken, such as avoiding poor areas at night. The security situation in Riode Janeiro has in fact improved a lot over thepast few years.

Opening a Bank Account

Opening a Brazilian bank account in generalrequires residency status, as well as proof ofphysical residence (such as a gas bill in your name). Recommended banks for foreigners

include Itau and Bradesco, or internationalbanks such as Citibank.

Signing Contracts

All contract signing usually requires that your signature is verified and countersigned bya public notary office. Your signature needsto be registered at the public notary officebeforehand.

The Norwegian driving

licence is valid in Brazil

for resident Norwegians.

Vaccines, Health Services,

Insurance

There is no requirement for specificvaccines for travellers to Brazil, but the

Hepatitis A vaccine is recommended bythe Norwegian Institute of Public Health(Folkehelseinstituttet, www.fhi.no).

Most expats buy private medical insur-ance in the form of a health plan (“planode saude”, usually included in the salarypackage). The cost is normally in the USD150-500 range, depending on benefits.

Certificate and Driving

Traffic in Brazilian cities can be dense, but

otherwise not too difficult to navigate for aNorwegian driver. The Norwegian drivinglicence is valid in Brazil for resident Norwe-gians. It is advisable to also carry an author-ized translation in Portuguese of the drivinglicence, to make possible encounters withthe traffic police easier. Barring languageproblems, encounters with the police do notrepresent a problem for expats in Brazil.

7/31/2019 Brazil How to Do Business in Brazil 2011

http://slidepdf.com/reader/full/brazil-how-to-do-business-in-brazil-2011 40/84

PART 2: START-UP PHASE 39

www.howtodobusinessinbrazil.com

PAYING TAXESBrazil has one of the world’s most complex tax

systems. In the World Bank’s annual “Ease of

Doing Business” index, Brazil’s 2011 ranking for

“Paying Taxes” is number 152 out of 187 tracked

economies.

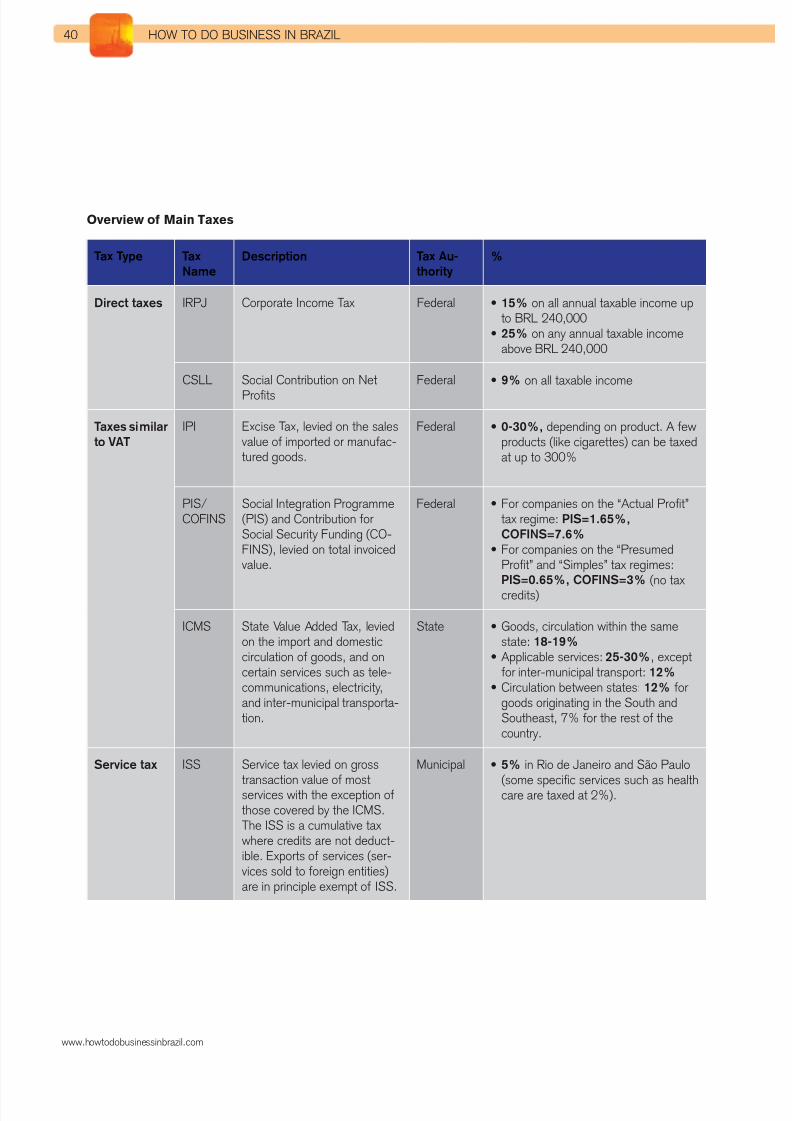

Corporate Taxes

Corporate taxes levied on a Brazilian

company are:

Direct taxes:

Around 34% of income for most busi-nesses, but the calculation of taxableincome depends on the tax regime (seebelow).

VAT:

There is no uniform Value Added Tax(VAT) in Brazil, but rather a range of in-direct taxes, depending on the nature of

the product or service. These taxes arelevied when purchasing, creating a taxcredit which is deductible when resellingthe product/service.

Service tax:

Levied on services not covered by theVAT type taxes. Generally 5% of invoicevalue. Does not create tax credit.

Other taxes:

A whole range of taxes, including socialcosts for employees, property taxes,vehicle taxes, credit operation tax, etcetc. Not treated in detail in this guide.

7/31/2019 Brazil How to Do Business in Brazil 2011

http://slidepdf.com/reader/full/brazil-how-to-do-business-in-brazil-2011 41/84

HOW TO DO BUSINESS IN BRAZIL40

www.howtodobusinessinbrazil.com

Tax Type Tax

Name

Description Tax Au-

thority

%

Direct taxes IRPJ Corporate Income Tax Federal 15% on all annual taxable income upto BRL 240,000

25% on any annual taxable incomeabove BRL 240,000

CSLL Social Contribution on NetProfits

Federal 9% on all taxable income

Taxes similar

to VAT

IPI Excise Tax, levied on the salesvalue of imported or manufac-tured goods.

Federal 0-30%, depending on product. A fewproducts (like cigarettes) can be taxedat up to 300%

PIS/COFINS

Social Integration Programme(PIS) and Contribution for Social Security Funding (CO-FINS), levied on total invoiced

value.

Federal For companies on the “Actual Profit”tax regime: PIS=1.65%,

COFINS=7.6%

For companies on the “Presumed

Profit” and “Simples” tax regimes:PIS=0.65%, COFINS=3% (no taxcredits)

ICMS State Value Added Tax, leviedon the import and domesticcirculation of goods, and oncertain services such as tele-communications, electricity,and inter-municipal transporta-tion.