BOUNTY HUNTERS & THE ILLINOIS FALSE CLAIMS ACT – IF YOU CHARGE FOR SHIPPING, YOU MAY BE NEXT Taxpayers’ Federation of Illinois Illinois State & Local Tax Conference September 20, 2012 Catherine A. Battin McDermott Will & Emery LLP [email protected] David J. Kupiec Kupiec & Martin, LLC [email protected] m

BOUNTY HUNTERS & THE ILLINOIS FALSE CLAIMS ACT – IF YOU CHARGE FOR SHIPPING, YOU MAY BE NEXT Taxpayers’ Federation of Illinois Illinois State & Local Tax.

Dec 15, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

BOUNTY HUNTERS & THE ILLINOIS FALSE CLAIMS ACT – IF YOU CHARGE

FOR SHIPPING, YOU MAY BE NEXT

Taxpayers’ Federation of IllinoisIllinois State & Local Tax Conference

September 20, 2012

Catherine A. BattinMcDermott Will & Emery [email protected]

David J. KupiecKupiec & Martin, [email protected]

2

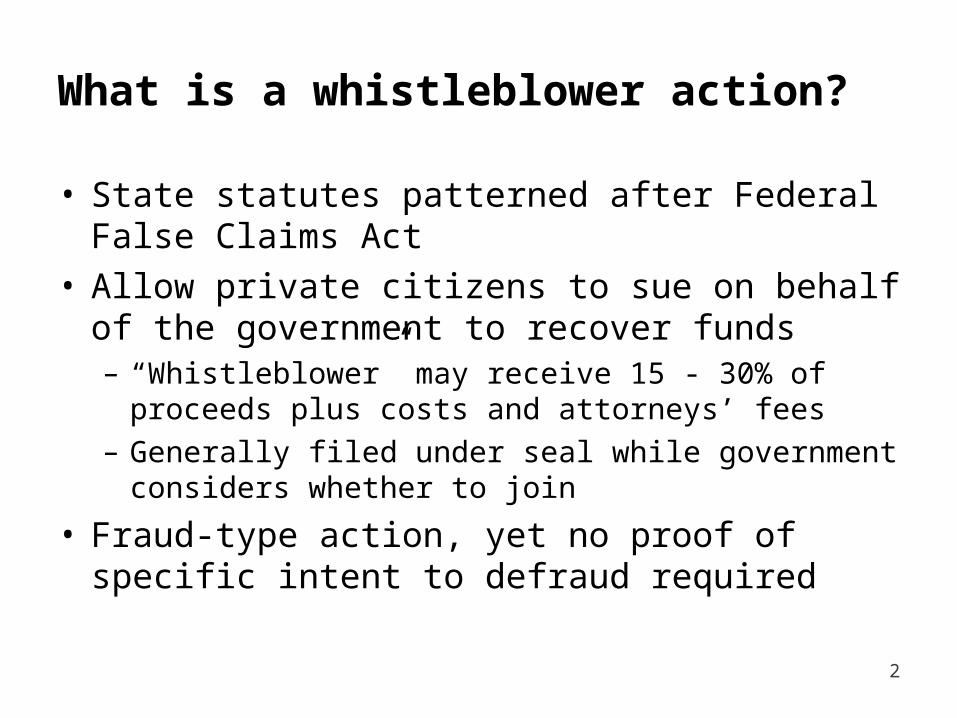

What is a whistleblower action?

• State statutes patterned after Federal False Claims Act

• Allow private citizens to sue on behalf of the government to recover funds – “Whistleblower” may receive 15 - 30% of proceeds

plus costs and attorneys’ fees– Generally filed under seal while government

considers whether to join

• Fraud-type action, yet no proof of specific intent to defraud required

3

Who are the players?

• Relator– Private party initiating the suit

• Real party in interest– Governmental entity

• Defendant(s)– Purported violator(s)

4

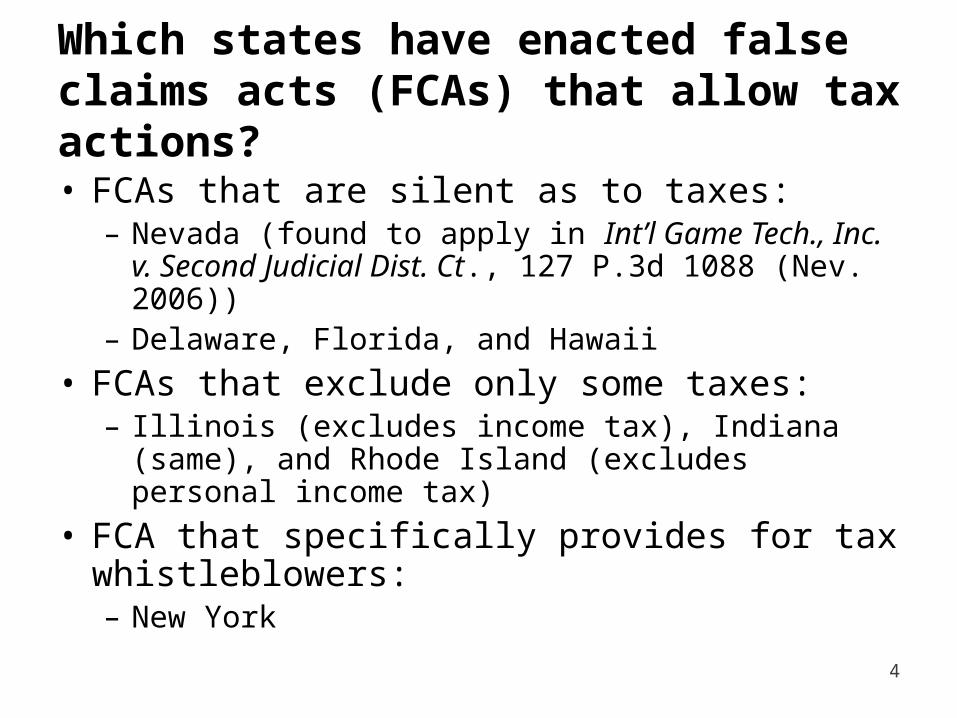

Which states have enacted false claims acts (FCAs) that allow tax actions?

• FCAs that are silent as to taxes:– Nevada (found to apply in Int’l Game Tech., Inc. v.

Second Judicial Dist. Ct., 127 P.3d 1088 (Nev. 2006))– Delaware, Florida, and Hawaii

• FCAs that exclude only some taxes:– Illinois (excludes income tax), Indiana (same), and

Rhode Island (excludes personal income tax)

• FCA that specifically provides for tax whistleblowers:– New York

5

What does NY’s FCA provide?

• First state FCA to specifically target taxes• Similar to US FCA and other state FCAs:

– Three times the damages, plus expenses, costs, and attorneys’ fees

– Up to 30% of the recovery to the Relator• Differences from US FCA:

– “Original source” requirement not jurisdictional– As applied to taxes - medium and large taxpayers only:

• Annual income or sales exceed $1,000,000 and • Complaint alleges damages in excess of $350,000

– NY Attorney General must coordinate with the NY Department of Taxation & Finance

6

Where have FCA cases alleging tax issues been filed?

• FCA sales/use tax actions:– Illinois (over 200 cases)– Nevada (approx. 12 cases)– Tennessee (approx. 20 cases brought prior to the

statute’s amendment to preclude tax claims)

• NY FCA action related to sales tax base

7

What are the elements of a state FCA claim?

• 2 common kinds of FCA actions: – Traditional false claims actions– Reverse false claims actions

• Elements of a reverse false claims action:– Defendant knowingly made or used a false statement;– Material to an obligation to pay money due to the

government; or– Knowingly conceals or knowingly and improperly

avoids or decreases an obligation to pay money to the government; and

– Proper whistleblower (i.e., action may not be based on publicly available information unless Relator is “original source” of the information)

8

What are the typical damages?

• Three times the unpaid tax liability, penalties and interest

• Per occurrence civil penalties (up to $11,000 per false claim in Illinois)

• Reasonable attorneys’ fees/costs of Relator and the State

9

How have Internet sales become state FCA cases?

• Relator purchases goods online• Relator collects evidence concerning seller’s tax collection practice

– Web pages or catalogs indicating states where seller collects and remits tax on goods sold or, in newest litigation, on shipping/handling charges

– Documents related to the sale showing no collection of tax• Relator collects “evidence” to support a tax collection obligation,

often using investigators (e.g., if a nexus issue, examines direct physical presence, physical presence of affiliate, and presence of agent or representative)

• Relator files whistleblower case under seal and the state decides whether to intervene in the case

10

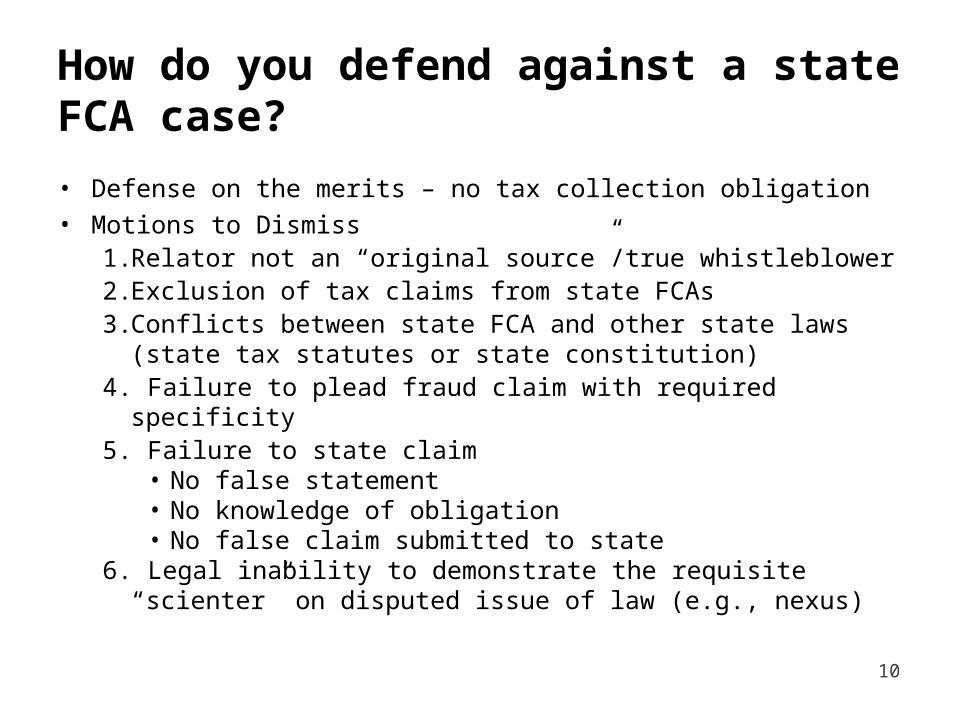

How do you defend against a state FCA case?

• Defense on the merits – no tax collection obligation• Motions to Dismiss

1. Relator not an “original source”/true whistleblower2. Exclusion of tax claims from state FCAs3. Conflicts between state FCA and other state laws (state tax

statutes or state constitution)4. Failure to plead fraud claim with required specificity5. Failure to state claim

• No false statement• No knowledge of obligation• No false claim submitted to state

6. Legal inability to demonstrate the requisite “scienter” on disputed issue of law (e.g., nexus)

11

What has happened historically with state tax FCA cases?

• Tennessee– Dismissed by order of Chancery Court (12/1/03)– Statute amended to exclude tax matters– Failure to state a claim – no submission of alleged false

statement to state, no falsity, no knowledge• Nevada

– Supreme Court of Nevada dismissed cases (127 P.3d 1088 (2006))

– Nevada AG established good cause for dismissal based on its view that tax matters are best left to DOR

12

What is the procedural status of whistleblower actions? • Illinois Round One (Tax on Economic Goods)

– Multiple trips to Illinois Appellate Court; one trip to Illinois Supreme Court– App. Ct.:

• Invoices/tax returns truthfully showing that no tax was collected are not false statements unless there is scienter

• State’s prosecutorial discretion to dismiss upheld absent evidence of fraud

– Trial Court:• Public disclosure requires specific identification of actual defendant• Scienter grounds expected to be determined on motions to dismiss

(Fall 2012)– Settlements/Dismissals:

• Some approved over Relator’s objections in contested settlement hearings

• Some consensual settlements• Some dismissals under the State’s prosecutorial discretion

13

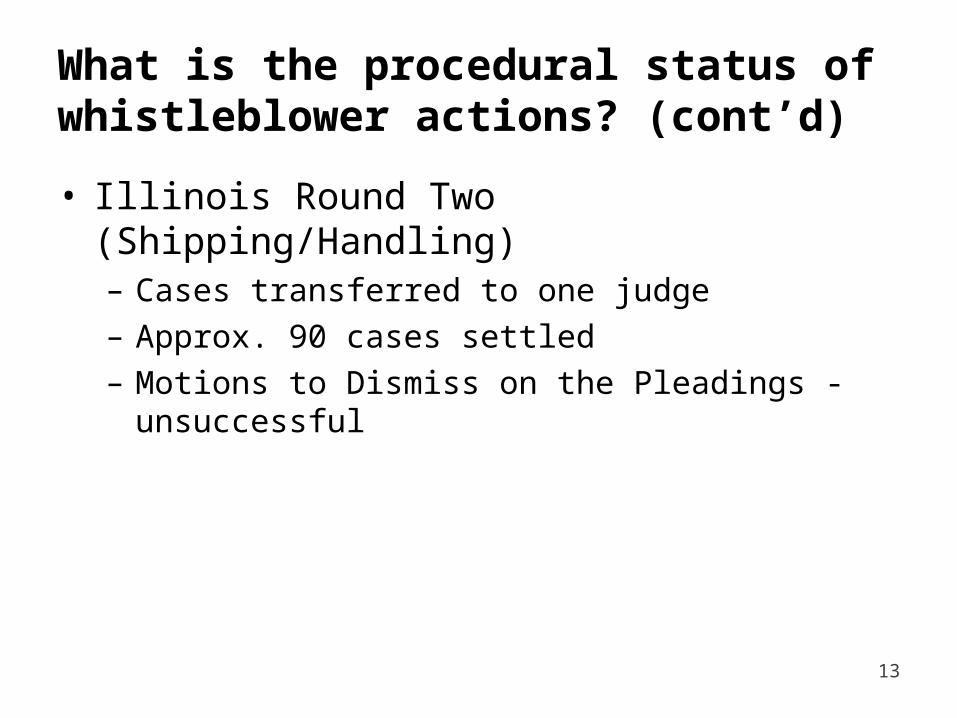

What is the procedural status of whistleblower actions? (cont’d)

• Illinois Round Two (Shipping/Handling)– Cases transferred to one judge– Approx. 90 cases settled– Motions to Dismiss on the Pleadings - unsuccessful

14

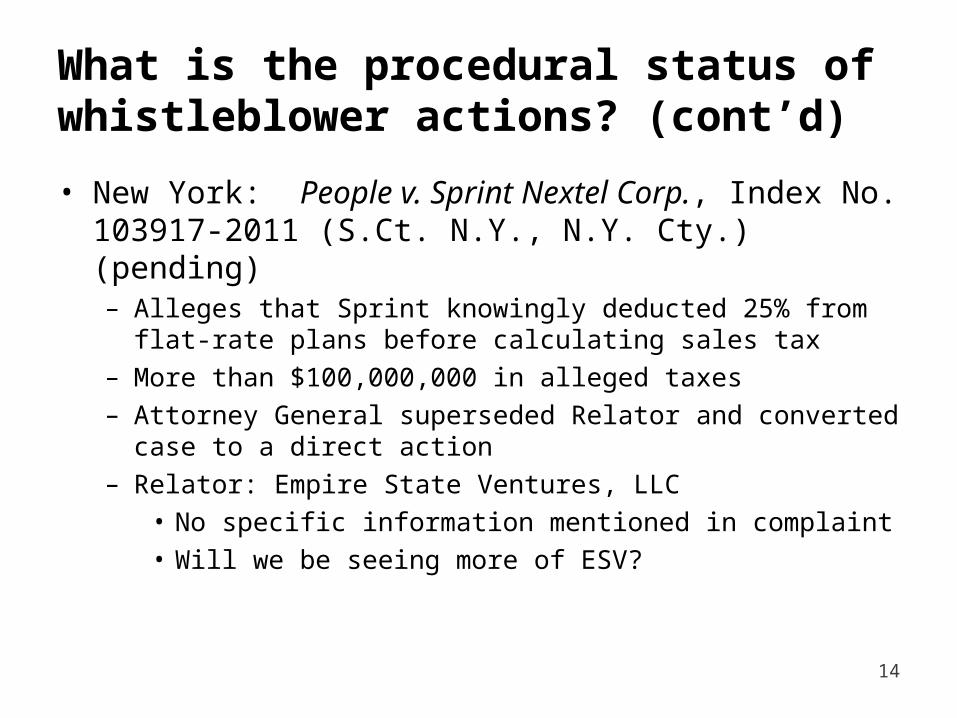

What is the procedural status of whistleblower actions? (cont’d)

• New York: People v. Sprint Nextel Corp., Index No. 103917-2011 (S.Ct. N.Y., N.Y. Cty.) (pending)– Alleges that Sprint knowingly deducted 25% from flat-rate plans

before calculating sales tax– More than $100,000,000 in alleged taxes– Attorney General superseded Relator and converted case to a

direct action– Relator: Empire State Ventures, LLC

• No specific information mentioned in complaint• Will we be seeing more of ESV?

15

How can you minimize your chances of being sued or prevailing, if sued?

• Lobby for express exclusion of all tax matters• Prudent nexus tax planning

– Separate corporate entities for Internet/catalog operations– Written policy prohibiting in-store returns from Internet/catalog

sales– Separate gift-certificates/gift cards for Internet and retail stores– No in-store advertising for Internet/catalog retailers– Strict separation of inventory– No in-store referrals of customer to website/catalog– Caution with in-state drop shippers

• Update research on state tax nuances and change practices accordingly– State taxes on shipping/handling charges– Rates to be charged

Illinois Supreme Court Opinion

Kean v. Wal Mart • Plaintiff purchased item online and claimed violations of

Consumer Fraud and Deceptive Business Practices Act• Supreme Court held that due to absence of delivery

choice at time of purchase, Regulation required that shipping charges were part of taxable purchase price

• Opinion filed on November 19, 2009

16

Public Act 97-0978New Law

Signed by Governor with effective date of August 17, 2012

Amends Provisions of Section 4 of the Illinois False Claims Act

Amendments include:“The court shall dismiss an action or claim under this Section, unless opposed by the State, if substantially the same allegations or transactions as alleged in the action or claim were publicly disclosed:”

17

Department of Revenue’s Proposed Regulatory Changes

• On May 25, 2012, the Department Proposed Amendments to Regulation Sections 130.410, 130.415 & 140.301

• Amendments Would Subject Shipping and Handling Charges to Illinois Sales Tax

• Proposed Effective Date – October 1, 2012

18

Illinois House Revenue Committee Hearing

• July 26, 2012 Public Hearing in Chicago

• Testimony By:– Department of Revenue– Attorney General’s Office– Taxpayer Organizations– Taxpayers & Attorneys

19

Department’s Hearing On Proposed

Regulations

• August 21, 2012 Public Hearing in Springfield

• Testimony Opposing Proposed Regs

• Testimony Supporting Proposed Regs

• Effective Date – Not October 1, 2012

• Next Steps

20

Questions

21

Disclaimers

CIRCULAR 230 DISCLOSURE - To comply with Treasury Department regulations, we inform you that, unless otherwise expressly indicated, any tax advice contained in this communication (including any attachments) is not intended or written to be used, and cannot be used, for the purpose of (1) avoiding penalties that may be imposed under the Internal Revenue Code or any other applicable tax law, or (2) promoting, marketing or recommending to another party any transaction, arrangement or other matter.

22

Related Documents