Bond Prices Zero-coupon bonds : promise a single future payment, e.g., a U.S. Treasury Bill. Fixed payment loans , e.g., conventional mortgages. Coupon Bonds : make periodic interest payments and repay the principal at maturity, e.g., U.S. Treasury Bonds and most corporate bonds. Consols : make periodic interest payments forever, never repaying the principal that was borrowed, e.g., British consols.

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

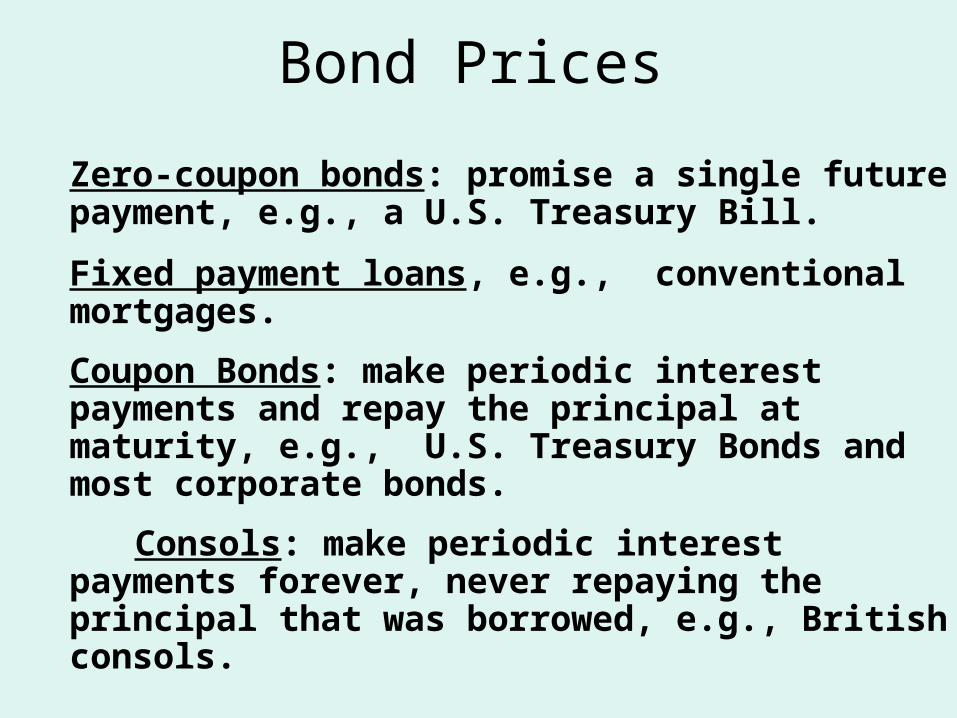

Bond Prices

Zero-coupon bonds: promise a single future payment, e.g., a U.S. Treasury Bill.

Fixed payment loans, e.g., conventional mortgages.

Coupon Bonds: make periodic interest payments and repay the principal at maturity, e.g., U.S. Treasury Bonds and most corporate bonds.

Consols: make periodic interest payments forever, never repaying the principal that was borrowed, e.g., British consols.

Bond Prices

Zero-Coupon Bonds or Discount Bonds

Price of a $100 face value zero-coupon bond

Where i = interest rate

n = time until the payment is made

ni)1(

100$

Bond Prices Zero-Coupon Bonds or Discount Bonds

Examples. Assume i=4%

Price of a One-Year Treasury Bill.

Price of a Six-Month Treasury Bill

06.98$)04.01(

1002/1

Bond PricesFixed Payment Loans

Value of a Fixed Payment Loan =

ni

ntFixedPayme

i

ntFixedPayme

i

ntFixedPayme

)1()1()1( 2

Bond PricesCoupon Bond

nnCB i

FaceValue

i

entCouponPaym

i

entCouponPaym

i

entCouponPaymP

)1()1(......

)1()1( 21

Bond PricesConsols

i

PaymentCoupon Yearly PConsol

Bond YieldsYield to Maturity

Price of One-Year 5 percent Coupon Bond =

The value of i that solves this equation is the yield to maturity

)1(

100$

)1(

5$

ii

Bond YieldsYield To Maturity

• If the price of the bond is $100, then the yield to maturity equals the coupon rate.

• Since the price rises as the yield falls, when the price is above $100, the yield to maturity must be below the coupon rate.

– If you pay more than the face value for a bond, you are earning less than the coupon rate.

Bond Yields

Paid Price

Payment CouponYearly YieldCurrent

Bond Yields Relationship Between a Bond’s Price and

Its Coupon Rate, Current Yield and Yield to Maturity

Bond Price < Face Value Coupon Rate < Current Yield < Yield to

Maturity

Bond Price = Face Value Coupon Rate = Current Yield = Yield to

Maturity

Bond Price > Face Value Coupon Rate > Current Yield > Yield to

Maturity

Bond YieldsHolding Period Return:

the return to holding a bond and selling it before maturity.

The holding period return can differ from the yield to maturity when you do not hold the bond to maturity.

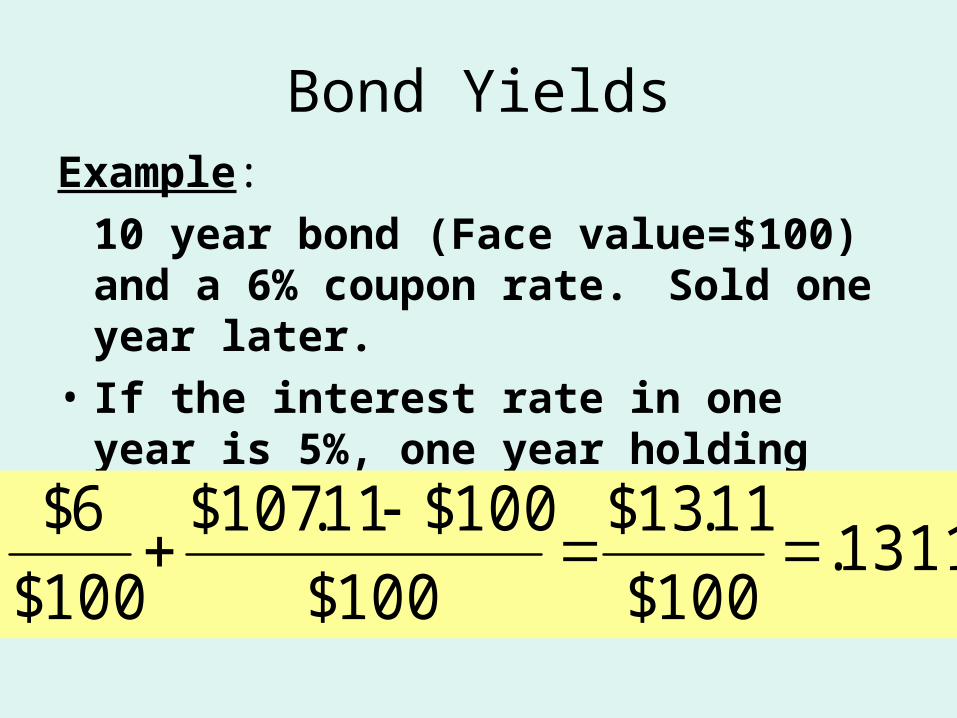

Bond YieldsExample:

10 year bond (Face value=$100) and a 6% coupon rate. Sold one year later.

• If the interest rate in one year is 5%, one year holding period return =

1311.100$

11.13$

100$

100$11.107$

100$

6$

Bond YieldsIf the interest rate in one year is 7%

One year holding Period return =

or -.52%

0052.100$

52$.

100$

100$48.93$

100$

6$

Bond Market and Interest Rates

One Year Zero-coupon (discount) Bond.

P

Pi or

iP

100$

1

100$

Bond Market and Interest Rates

Bond Market and Interest Rates

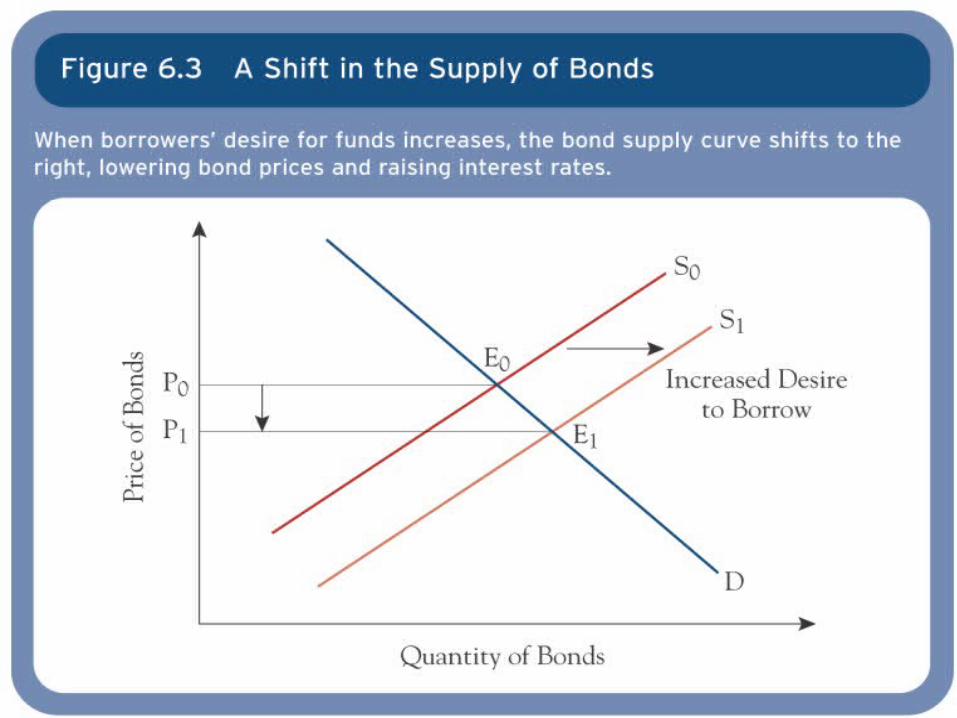

Factors that shift Bond Supply

• An increase in the government’s borrowing increases the quantity of bonds outstanding, shifting the bond supply curve to the right.

• As business conditions improve, the bond supply curve shifts to the right.

• An increase in expected inflation shifts the bond supply curve to the right.

Bond Market and Interest Rates

Factors that Shift Bond Demand to Right

• An increases in wealth.

• A fall in expected inflation.

• If the return on bonds rises relative to the return on alternative investments, the demand for bonds increases.

• If a bond becomes less risky relative to alternative investments, the demand for the bond increases.

• When a bond becomes more liquid relative to alternatives, the demand for the bond increases.

Bond Market and Interest Rates

Bonds and Risk

Sources of Bond Risk

• Default Risk

• Inflation Risk

• Interest-Rate Risk

Related Documents