| 1 Excise and Customs – key issues SERIVE TAX REGULATIONS C h a l l e n g e U s

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

| 1Excise and Customs – key issuesSERIVE TAX REGULATIONSC h a l l e n g e U s

All

rig

hts

reserv

ed

Excise and Customs – key issues | 2

8th Interactive workshop on

SUCCESSFUL EPC CONTRACTING IN INDIA

KEY EXCISE AND CUSTOMS DUTY ISSUES

Sujit Ghosh | Partner | BMR Legal

November 30, 2010 | Hotel ITC Grand | Mumbai

Insert picture from stock here

Excise and Customs – key issues | 3

DISCLAIMER

This presentation provides general information existing as at the

time of preparation. The presentation is meant for general

guidance and no responsibility for loss arising to any person acting

or refraining from acting as a result of any material contained in this

publication will be accepted by BMR Advisors. It is recommended

that professional advice be taken based on the specific facts and

circumstances. This presentation does not substitute the need to

refer to the original pronouncements

All

rig

hts

reserv

ed

Excise and Customs – key issues | 4

CUSTOM DUTY

CONCESSIONS -

PROJECT IMPORT

SCHEME

All

rig

hts

reserv

ed

Excise and Customs – key issues | 5

PROJECT IMPORT SCHEME

To facilitate setting up of/ substantial expansion of a unit of

industrial, infrastructure and other projects

A project falls qualifies as „substantial expansion‟ if the installed

capacity is increased by not less than 25 %

Seeks to achieve simplification of assessment by levy of a flat rate of duty

Imports classified under tariff heading 9801 of the Customs Tariff

Duty concessions can be availed by the

Project owner or Contractors

All

rig

hts

reserv

ed

Excise and Customs – key issues | 6

PROJECT NOT COVERED UNDER THE SCHEME

Project imports scheme is not available to the following class of

projects:

Hotels;

Hospitals;

Photographic studios;

Photographic film processing laboratories;

Photocopying studios;

Laundries; and

Garages and workshops

The benefit is also not available to a single or composite machine

All

rig

hts

reserv

ed

Excise and Customs – key issues | 7

KEY STEPS

Project Finalization &

Refund of Deposit

(Customs)

Classification of

Imported goods &

Clearance (Customs)

Plant Site Verification &

Installation Certificate

(Central Excise)

Letter of Recommendation

(Sponsoring Authority)

Project Registration

(Customs)

All

rig

hts

reserv

ed

Excise and Customs – key issues | 8

PROJECT IMPORT

SCHEME –

AUXILIARY

EQUIPMENT

All

rig

hts

reserv

ed

Excise and Customs – key issues | 9

PROJECT IMPORTS

Initial set-up or substantial expansion of following projects eligible

for project import and linked concessions:

Industrial plant

Power

Mining

Irrigation

Oil and gas exploration

Others

Eligible imports

All items of machinery (required for above) including prime movers,

instruments, apparatus, appliances, control gear, transmission

equipment, auxiliary equipment, equipment required for research and

development, equipment for testing and quality control, components,

raw materials for the manufacture of above items and spare parts not

exceeding 10% of the value of the goods specified above

All

rig

hts

reserv

ed

Excise and Customs – key issues | 10

AUXILIARY EQUIPMENT

No statutory definition/ criterion exists for ‗auxiliary equipment

Legal meaning of the term ‗auxiliary‘

“aiding or supporting, subsidiary” – Black‘s law dictionary

“giving additional help; supplemental or subsidiary; an item not directly a

part of a specific component or system but required for its functional

operation” - Words and Phrases of Excise and Customs by S.B. Sarkar

“one that aids or helps; an assistant; a confederate

Assisting or supporting” – Advanced Law Lexicon

All

rig

hts

reserv

ed

Excise and Customs – key issues | 11

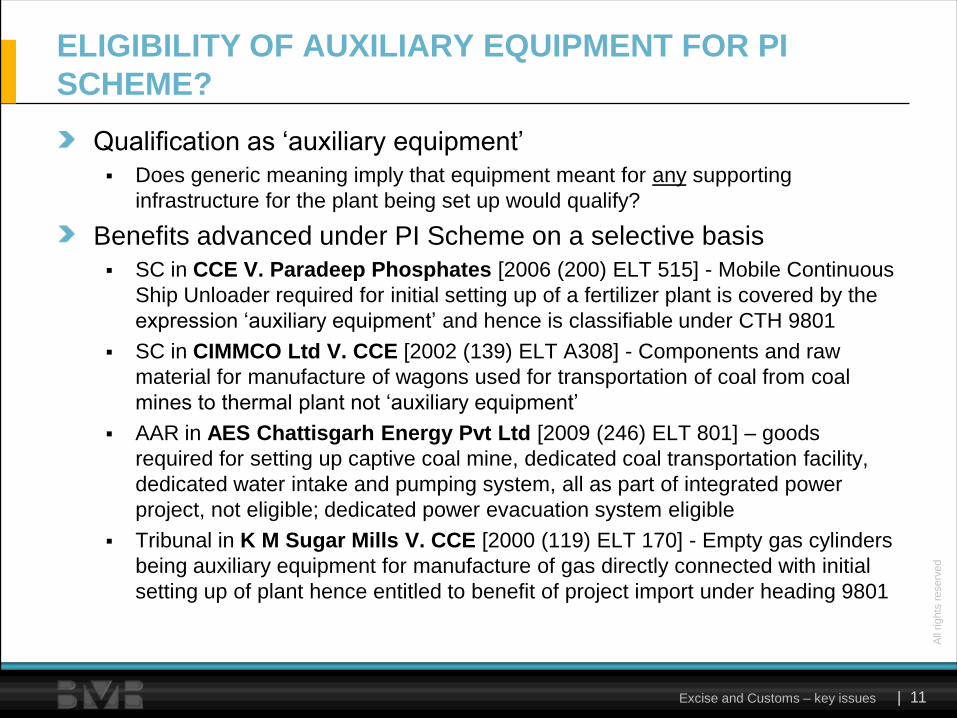

ELIGIBILITY OF AUXILIARY EQUIPMENT FOR PI

SCHEME?

Qualification as ‗auxiliary equipment‘

Does generic meaning imply that equipment meant for any supporting

infrastructure for the plant being set up would qualify?

Benefits advanced under PI Scheme on a selective basis

SC in CCE V. Paradeep Phosphates [2006 (200) ELT 515] - Mobile Continuous

Ship Unloader required for initial setting up of a fertilizer plant is covered by the

expression ‗auxiliary equipment‘ and hence is classifiable under CTH 9801

SC in CIMMCO Ltd V. CCE [2002 (139) ELT A308] - Components and raw

material for manufacture of wagons used for transportation of coal from coal

mines to thermal plant not ‗auxiliary equipment‘

AAR in AES Chattisgarh Energy Pvt Ltd [2009 (246) ELT 801] – goods

required for setting up captive coal mine, dedicated coal transportation facility,

dedicated water intake and pumping system, all as part of integrated power

project, not eligible; dedicated power evacuation system eligible

Tribunal in K M Sugar Mills V. CCE [2000 (119) ELT 170] - Empty gas cylinders

being auxiliary equipment for manufacture of gas directly connected with initial

setting up of plant hence entitled to benefit of project import under heading 9801

All

rig

hts

reserv

ed

Excise and Customs – key issues | 12

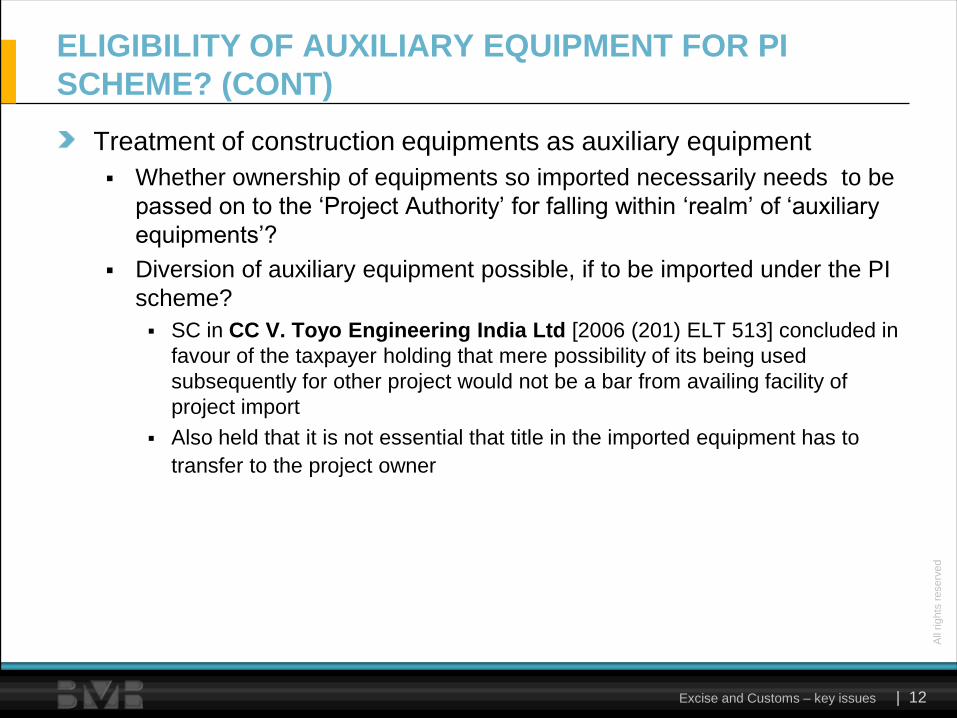

ELIGIBILITY OF AUXILIARY EQUIPMENT FOR PI

SCHEME? (CONT)

Treatment of construction equipments as auxiliary equipment

Whether ownership of equipments so imported necessarily needs to be

passed on to the ‗Project Authority‘ for falling within ‗realm‘ of ‗auxiliary

equipments‘?

Diversion of auxiliary equipment possible, if to be imported under the PI

scheme?

SC in CC V. Toyo Engineering India Ltd [2006 (201) ELT 513] concluded in

favour of the taxpayer holding that mere possibility of its being used

subsequently for other project would not be a bar from availing facility of

project import

Also held that it is not essential that title in the imported equipment has to

transfer to the project owner

All

rig

hts

reserv

ed

Excise and Customs – key issues | 13

RELEVANCE IN PROJECT PLANNING

Shifting focus, beyond machinery/ equipments that actually form part

of the plant/ main plant, for PI benefits

Larger relevance for rail, road, bridge projects

Contractor‘s ability to import high end equipment in India at

concessional rate of duty and servicing multiple projects thereafter

Given varying positions, prior or advance ruling may

be sought in complicated cases, for upfront clarity

All

rig

hts

reserv

ed

Excise and Customs – key issues | 14

BENEFIT OF

PROJECT IMPORTS

FOR CIVIL

MATERIALS

All

rig

hts

reserv

ed

Excise and Customs – key issues | 15

PROJECT IMPORTS FOR CIVIL MATERIALS

Projects like mega power projects, drinking water supply

projects, coal mining projects and fertilizer projects entitled to

customs duty exemption/concession

Covers all items of machinery including

Prime movers, instruments, apparatus and appliances,

Control gear and transmission equipment,

Auxiliary equipment (including those required for R & D testing

and quality control)

All components (whether finished or not) or raw materials for the

manufacture of the aforesaid items and their components

required for setting up & substantial expansion of the project

All

rig

hts

reserv

ed

Excise and Customs – key issues | 16

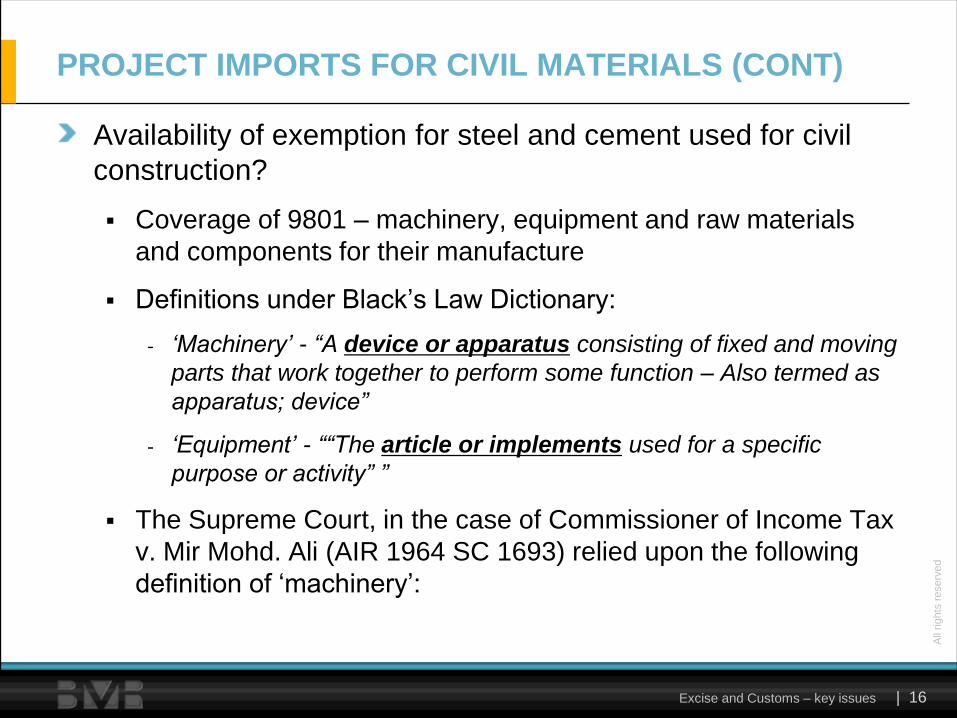

Availability of exemption for steel and cement used for civil

construction?

Coverage of 9801 – machinery, equipment and raw materials

and components for their manufacture

Definitions under Black‘s Law Dictionary:

- „Machinery‟ - “A device or apparatus consisting of fixed and moving

parts that work together to perform some function – Also termed as

apparatus; device”

- „Equipment‟ - ““The article or implements used for a specific

purpose or activity” ”

The Supreme Court, in the case of Commissioner of Income Tax

v. Mir Mohd. Ali (AIR 1964 SC 1693) relied upon the following

definition of ‗machinery‘:

PROJECT IMPORTS FOR CIVIL MATERIALS (CONT)

All

rig

hts

reserv

ed

Excise and Customs – key issues | 17

―The word „machinery‟ when used in ordinary language prima facie,

means some mechanical contrivances which by themselves or in

combination with one or more other mechanical contrivances, by the

combined movement and interdependent operation of their

respective parts generate power, or evoke, modify, apply or direct

natural forces with the object in each case of effecting so definite or

specific a result”

Civil material like cement and steel may not qualify as machinery

or equipments

The phrase - ‗Components or raw material‘ also used in 9801

Components or raw material qualify only when the same is used

in the manufacture of machinery and equipments – not

applicable for Cement and Steel to be used for civil construction

Thus, customs duty exemption/concessions may not be

available for Cement and Steel to be used for civil construction

PROJECT IMPORTS FOR CIVIL MATERIALS (CONT)

All

rig

hts

reserv

ed

Excise and Customs – key issues | 18

Pertinent to note how this issue manifests itself under Excise

for Mega and Ultra-Mega Power Projects (―UMPPs‖)

Excise exemption for a Mega and Ultra Mega Power Project is

subject to customs duty exemption

As discussed, customs duty exemption doubtful for steel and

cement for civil works

Accordingly, even excise exemption for steel and cement for civil

works jeopardized

It is pertinent to note that for UMPPs, format of certification from

Chief Engineer in the Central Electricity Authority specifically

includes Cement and Steel for civil works – greater clarity

required

PROJECT IMPORTS FOR CIVIL MATERIALS (CONT)

All

rig

hts

reserv

ed

Excise and Customs – key issues | 19

Possible to say that a civil structure is an integral part of plant and

therefore eligible for PI benefits?

What if sponsoring authority approves essentiality of civil materials for

completion of the respective plant?

Though not in context of civil materials, SC in CCE V. Paradeep

Phosphates [2006 (200) ELT 515] approved the principle that once goods

approved as essential requirement for completion of the plant by the

sponsoring ministry, the PI benefits would be available

Eligibility for importing micro-silica (sand), under the PI Scheme, for construction

of spillway structure of the dam – prima facie merits seen in the case and matter

remanded de novo – Tehri Hydo Development Corpn Ltd V. CCE [ 2007 (212)

ELT 366]

Test of functionality to be proved - SC in CIT V. Taj Mahal Hotel [1971 (82) ITR

44] – reasonable level of complexity

Difficulty in importing civil materials against advance licence also, as

arguably not used in manufacture of goods

PROJECT IMPORTS FOR CIVIL MATERIALS (CONT)

All

rig

hts

reserv

ed

Excise and Customs – key issues | 20

RECENT

EXTENSION OF

CONCESSIONS –

BROWNFIELD

EXPANSION OF

MEGA POWER

PROJECTS

All

rig

hts

reserv

ed

Excise and Customs – key issues | 21

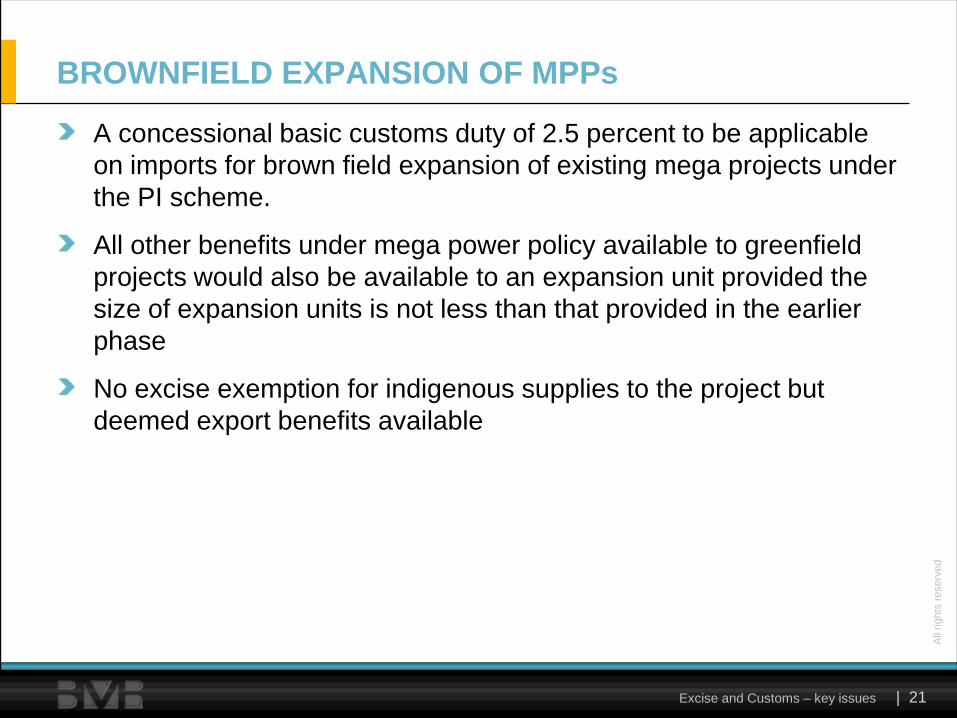

BROWNFIELD EXPANSION OF MPPs

A concessional basic customs duty of 2.5 percent to be applicable

on imports for brown field expansion of existing mega projects under

the PI scheme.

All other benefits under mega power policy available to greenfield

projects would also be available to an expansion unit provided the

size of expansion units is not less than that provided in the earlier

phase

No excise exemption for indigenous supplies to the project but

deemed export benefits available

All

rig

hts

reserv

ed

Excise and Customs – key issues | 22

The expression ‗brown-field expansion‘ not defined either through

the Mega Power Policy or under the customs law resulting in lack of

clarity on following issues:

What qualifies as expansion? Essential for the new facility to be dependent

on existing capacity or can it be a standalone unit and still qualify as a

brown-field expansion?

Mere co-location sufficient? Very commonly seen since due to availability of

large tracts of land

As per MPP, size of expansion units not to be less than the size of existing

units. PI Scheme also states that project will qualify as expansion only if

capacity enhancement more than 25 percent – both conditions to be

fulfilled?

Treatment of brown-field project of 1000 MW or more ?

BROWNFIELD EXPANSION – ISSUES

All

rig

hts

reserv

ed

Excise and Customs – key issues | 23

DEEMED EXPORTS

Concept & Benefits

All

rig

hts

reserv

ed

Excise and Customs – key issues | 24

‗Deemed Exports‘

goods supplied do not leave the country; and

goods must be manufactured in India

payment received either in INR or in free foreign exchange

‗Deemed Exports‘ eligible for certain export related facilities

and benefits

Ten categories of supply of goods by main /sub- contractors

which qualify as ‗Deemed Exports‘

(a) Supply of goods against Advance Authorization

(b) Supply of goods to EOUs/ STPs/ EHTPs/ BTPs

(c) Supply of capital goods to holder of EPCG Authorization

DEEMED EXPORTS – CONCEPT

All

rig

hts

reserv

ed

Excise and Customs – key issues | 25

(d) Supply of goods to projects financed by multilateral or bilateral

agencies/ funds – typically covers infrastructural projects

(e) Supply of capital goods, … to fertilizer plants

(f) Supply of goods to any project or purpose in respect of which

the MOF, by a notification , permits import of such goods at zero

customs duty – covers mega power projects and UMPPs

(g) Supply of goods to power projects and refineries not covered by

above category – covers non-mega power and MPP

expansion projects

(h) Supply of marine freight containers by 100% EOUs

(i) Supply to projects funded by UN Agencies

(j) Supply of goods to Nuclear Power Projects through competitive

bidding as opposed to ICB

DEEMED EXPORTS – CONCEPT (CONT)

All

rig

hts

reserv

ed

Excise and Customs – key issues | 26

Essential for the goods supplied to be manufactured in India

Benefits of deemed exports under paras (d), (e), (f) and (g)

only if the supply is made under procedure of ICB

Exception for Mega Power Projects

Following lines added

―However, in regard to mega power projects, the requirement of

ICB would not be mandatory, if the requisite quantum of power

has been tied up through tariff based competitive bidding or if

the project has been awarded through tariff based competitive

bidding”

Deemed exports governed by chapters 8 of the Foreign

Trade Policy (―FTP‖) and the corresponding Handbook of

Procedures (―HoP‖)

DEEMED EXPORTS – CONCEPT (CONT)

All

rig

hts

reserv

ed

Excise and Customs – key issues | 27

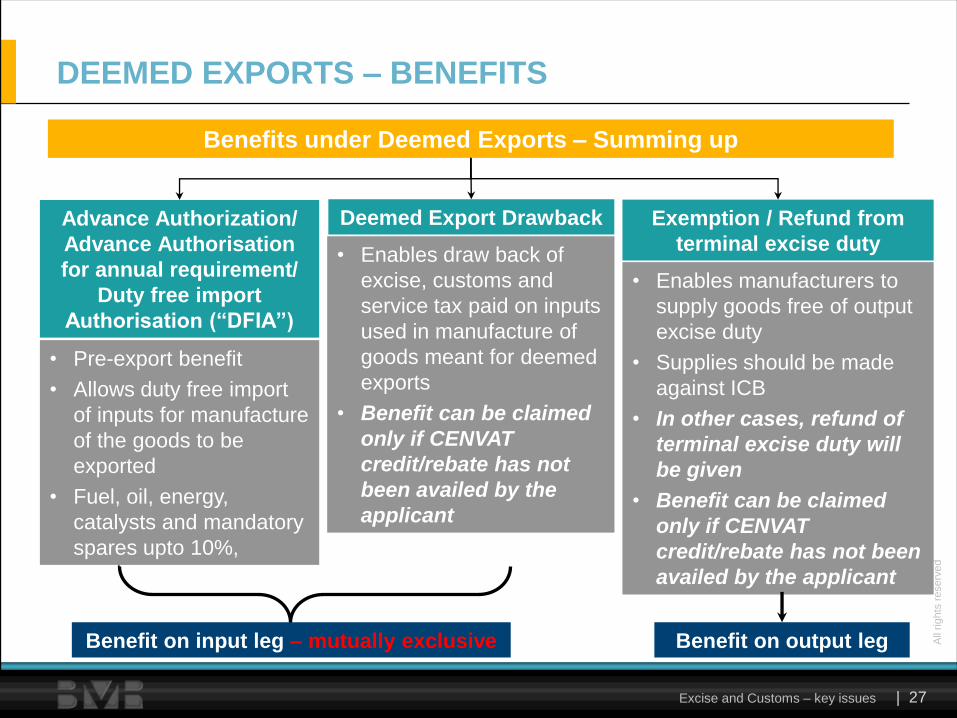

DEEMED EXPORTS – BENEFITS

Advance Authorization/

Advance Authorisation

for annual requirement/

Duty free import

Authorisation (“DFIA”)

Deemed Export Drawback Exemption / Refund from

terminal excise duty

Benefits under Deemed Exports – Summing up

• Pre-export benefit

• Allows duty free import

of inputs for manufacture

of the goods to be

exported

• Fuel, oil, energy,

catalysts and mandatory

spares upto 10%,

• Enables draw back of

excise, customs and

service tax paid on inputs

used in manufacture of

goods meant for deemed

exports

• Benefit can be claimed

only if CENVAT

credit/rebate has not

been availed by the

applicant

• Enables manufacturers to

supply goods free of output

excise duty

• Supplies should be made

against ICB

• In other cases, refund of

terminal excise duty will

be given

• Benefit can be claimed

only if CENVAT

credit/rebate has not been

availed by the applicant

Benefit on output legBenefit on input leg – mutually exclusive

All

rig

hts

reserv

ed

Excise and Customs – key issues | 28

Thus, for deemed exports, the OEM can claim benefits on both input

as well as output side

The above benefits are available to the OEM as well as his sub-

contractors subject to conditions under para 8.6.2 of the FTP as

under:

being mentioned specifically as a sub-contractor (either initially or

subsequently) in the contract between project owner and the EPC

contactor;

the sub-contractor ships the goods directly to the project site; and

Project authority certificate and payment certificate is issued by

project owner to the main contractor and by the main contractor to

the sub-contractor

Thus the deemed export benefits can flow down through the

supply chain and proper planning through out the supply chain

would significantly reduce the costs of the project

DEEMED EXPORTS BENEFITS TO SUB – CONTRACTOR

All

rig

hts

reserv

ed

Excise and Customs – key issues | 29

HC in Dee Development Engineers Ltd V. UOI [2010-TIOL-491-

HC], was appraising the issue to extending benefits to sub-contractor

for goods supplied to a project funded by notified agencies

Facts

The eligible project awarded supply contract to M/s Thermax

Babcock & Wilcox Ltd, Pune and issued necessary certificate in its

favour so as to enable availment of duty benefits

Thermax Babcock & Wilcox Ltd in turn sub-contracted part of

supplies to the Assessee

Assessee supplied the goods directly to the project site under excise

exemption on grounds that valid certificate in favour of Thermax

Babcock & Wilcox Ltd existed at material times, who has placed

supply orders on the Assessee

DEEMED EXPORTS BENEFITS TO SUB – CONTRACTOR

(CONT)

All

rig

hts

reserv

ed

Excise and Customs – key issues | 30

Revenue‟s case

Exemption benefits extends to only those parties in whose favour a

valid certificate has been issued and not otherwise

HC Decision

The court held that:

“as no certificate was issued by the Project Implementing Authority approved

by the Government of India in favour of the assessee, therefore, it

(assessee) cannot claim exemption from duty on the basis of certificate

(Annexure A2) issued in favour of the supplier M/s Thermax Babcock &

Wilcox Limited, Pune”

Comments

Evidently, the denial of benefits by the court were preceded by lack

of planning in the whole arrangement

DEEMED EXPORTS BENEFITS TO SUB – CONTRACTOR

(CONT)

All

rig

hts

reserv

ed

Excise and Customs – key issues | 31

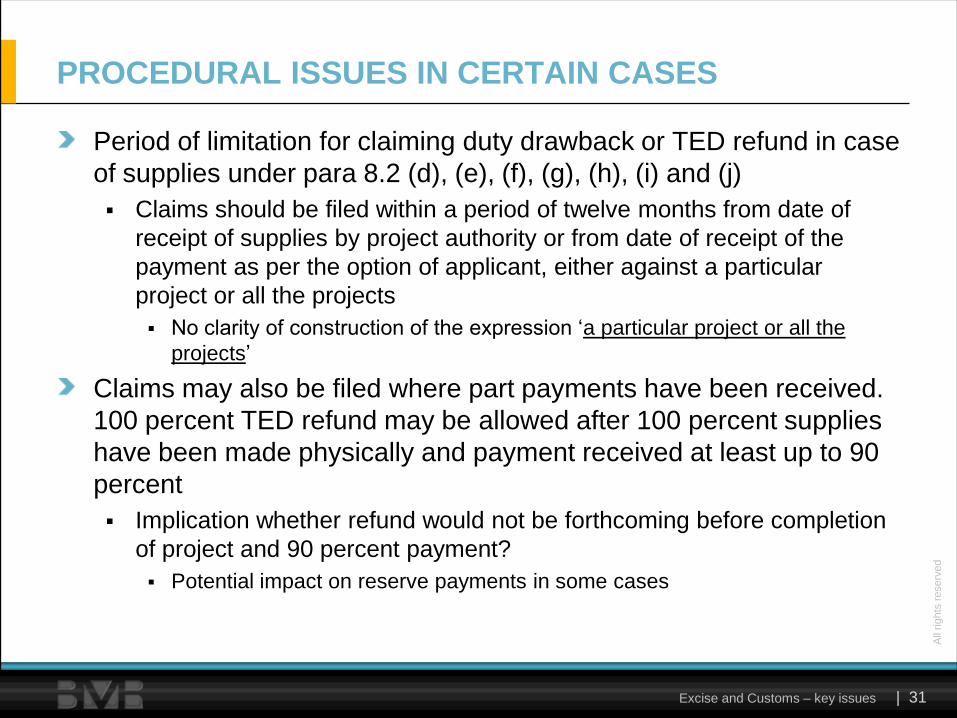

PROCEDURAL ISSUES IN CERTAIN CASES

Period of limitation for claiming duty drawback or TED refund in case

of supplies under para 8.2 (d), (e), (f), (g), (h), (i) and (j)

Claims should be filed within a period of twelve months from date of

receipt of supplies by project authority or from date of receipt of the

payment as per the option of applicant, either against a particular

project or all the projects

No clarity of construction of the expression ‗a particular project or all the

projects‘

Claims may also be filed where part payments have been received.

100 percent TED refund may be allowed after 100 percent supplies

have been made physically and payment received at least up to 90

percent

Implication whether refund would not be forthcoming before completion

of project and 90 percent payment?

Potential impact on reserve payments in some cases

All

rig

hts

reserv

ed

Excise and Customs – key issues | 32

ICB AND LINKED

EXCISE DUTY

BENEFITS

All

rig

hts

reserv

ed

Excise and Customs – key issues | 33

CONTROVERSIES SURROUNDING ICB

Many projects brought into existence through EPC contracts have no output excise/ service tax liability – like power projects

Hence, excise duty on the procurement side becomes a cost

Notification 6/ 2006 – CE, vide entry 91, provides for an exemption from excise duty to ―goods supplied against International Competitive Bidding (ICB)‖

Above exemption subject to Customs Duty exemption

The phrase ―goods supplied under ICB‖ however is not defined – ie ICB to be undertaken at what stage – IPP or Concession/ EPC/ OEM? – reasonable clarity that at IPP\EPC\PPA level should suffice

Resultant ambiguities best exemplified by power projects till recently – issue resolved for Mega Power projects vide introduction of entry 91B in Budget 2010?

―Goods supplied to mega power projects from which the supply of power has been tied up through tariff based competitive bidding or a mega power project awarded to a developer on the basis of such bidding‖

All

rig

hts

reserv

ed

Excise and Customs – key issues | 34

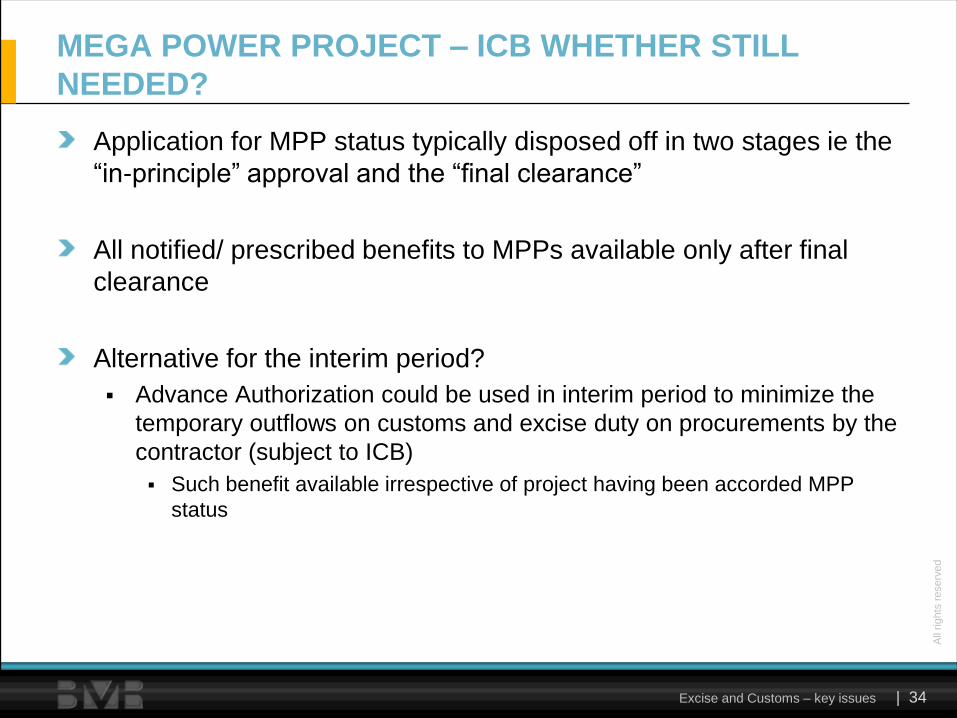

MEGA POWER PROJECT – ICB WHETHER STILL

NEEDED?

Application for MPP status typically disposed off in two stages ie the

―in-principle‖ approval and the ―final clearance‖

All notified/ prescribed benefits to MPPs available only after final

clearance

Alternative for the interim period?

Advance Authorization could be used in interim period to minimize the

temporary outflows on customs and excise duty on procurements by the

contractor (subject to ICB)

Such benefit available irrespective of project having been accorded MPP

status

All

rig

hts

reserv

ed

Excise and Customs – key issues | 35

Key conditions (amongst others) for grant of the Mega Power Project status? Either project should have been awarded on basis of competitive bidding; or

supply of power has been tied up through tariff based competitive bidding

Hence most times, ICB may not be critical

Exceptions to above – State Utilities Typically the IPP or the project award stage does not arise as generation utility of

the state responsible to undertake the project

As per the Tariff Policy, state utilities need not tie up sale of power on a competitive bidding basis

Given the above, a state utility may undertake a project without following both the attendant conditions – fate of deemed export benefits (especially excise duty exemption)? If ICB followed to award the EPC contract, for corresponding supplies/ works,

benefits will still be available

MEGA POWER PROJECT – ICB WHETHER STILL NEEDED?

(CONT)

All

rig

hts

reserv

ed

Excise and Customs – key issues | 36

DEEMED EXPORTS

- OTHER ISSUES

All

rig

hts

reserv

ed

Excise and Customs – key issues | 37

DEEMED V. PHYSICAL EXPORTS – CENVAT

IMPLICATIONS

Reasonable degree of debate on whether deemed export supplies

trigger restrictive implications under Rule 6 of the Cenvat Credit

Rules, 2004 (Credit Rules) in hands of the local manufacturer-

supplier

Ie cenvatability of corresponding input credits (excise duty/ service tax)

in such cases?

The Revenue contentions

Distinction between physical and deemed exports

Benefits (by way of cenvat credit) advanced in case of physical exports

cannot be made available to deemed exports

All

rig

hts

reserv

ed

Excise and Customs – key issues | 38

DEEMED V. PHYSICAL EXPORTS – CENVAT

IMPLICATIONS (CONT)

Recent Development

Credit Rule 6(6) amended to include the following:

all goods which are exempt from the duties of customs leviable under the

First Schedule to the Customs Tariff Act, 1975 (51 of 1975) and the

additional duty leviable under sub-section (1) of section 3 of the said

Customs Tariff Act when imported into India and are supplied, —

(a) against International Competitive Bidding; or

(b) to a power project from which power supply has been tied up through

tariff based competitive bidding; or

(c) to a power project awarded to a developer through tariff based

competitive bidding,

in terms of notification No. 6/2006-Central Excise

Implication

Legislative intent to provided tax benefits to deemed exports ratified

Welcome amendment – amicable resolution of the dispute!!

All

rig

hts

reserv

ed

Excise and Customs – key issues | 39

Para 8.3 (c) of FTP provides as under:

“Exemption from terminal excise duty where supplies are made against ICB.

In other cases, refund of terminal excise duty will be given”

“In other cases” – connotation?

Cases in which ICB has not been followed; and / or

Cases in which no central excise exemption notification (for eg supply to

Advance Authorization or EPCG authorization holder)

Doctrine of unjust enrichment applicable [Sahakari Khand Udyog

Mandal Ltd vs CCE, 2005 - TIOL- 48 – SC – LB]

duty payments to be reflected as ‗Receivables‘; and

Ability to satisfactorily prove that the amounts being claimed as refund

have not been passed on to the ultimate consumers

TED EXEMPTION OR REFUND?

All

rig

hts

reserv

ed

Excise and Customs – key issues | 40

Refund of Excise duty technically unavailable for non-mega power

projects – unlike mega power projects and UMPPs

Para 8.4.4 (iv) reads as under:

“Supply of Capital goods and spares upto 10% of FOR value of capital goods to

power projects in terms of paragraph 8.2(g) shall be entitled for deemed export

benefits ….. Supplier shall be eligible for benefits listed in paragraph 8.3(a) and (b) of

FTP, whichever is applicable.

However, supply of goods required for setting up of any mega power projects

…., shall be eligible for deemed exports benefits as mentioned in paragraph

8.3(a), (b) and (c) of FTP, whichever is applicable

Further, supply of goods required for the expansion of existing mega power

project ….. shall also be eligible for deemed export benefits as mentioned in

paragraph 8.3 ( a), (b) and (c) of FTP, whichever is applicable.,….”

Attempts at refund still made basis paragraph 8.4.4 (i) of FTP read

with 8.3.1 (iv) of the HOP – interpretative issue

TED EXEMPTION OR REFUND? (CONT)

All

rig

hts

reserv

ed

Excise and Customs – key issues | 41

Paragraph 8.4.4 (i) of FTP

“In respect of supplies made under paragraphs 8.2(d), (f) and (g) of FTP, supplier

shall be entitled to benefits listed in paragraphs 8.3(a), (b) and (c), whichever is applicable”

Thus as per the above paragraph, all the deemed export benefits will be available for supplies to mega as well as non-mega power plants – contradiction with Para 8.4.4 (iv)

Paragraph 8.3.1 (iv) of HOP

In respect of supplies under categories mentioned in paragraphs 8.2(d), (e), (f), (g),(h), (i) and (j) of FTP, claim may be filed either on the basis of proof of supplies effected or payment received……100% TED refund may be allowed after 100% supplies have been made physically and payment received at least upto 90%.

However, paragraph 8.4.4 (iv) being more specific to power projects appears to be the more appropriate paragraph – in which paragraph excise exemption / refund is not available for non-mega power projects

TED EXEMPTION OR REFUND? (CONT)

All

rig

hts

reserv

ed

Excise and Customs – key issues | 42

Nil input and output indirect tax cost for a deemed exporter who is

eligible for all three deemed export benefits

Viz. advance authorization or deemed export drawback on the input side

and excise duty exemption or refund on the output side)

For those ineligible for excise duty exemption or refund on the output

side, output excise duty becomes a cost

‗Manufacture‘ in India – key requirement for deemed export benefits

‗Manufacture‘ under FTP wider than under Central Excise laws

Certain activities may amount to ‗Manufacture‘ under FTP (and enjoy

deemed export benefits) but not amount to ‗Manufacture of excisable

goods‘ under Central Excise laws (and not suffer Excise duty)

ONSITE ACTIVITIES – „MANUFACTURE‟?

All

rig

hts

reserv

ed

Excise and Customs – key issues | 43

‗Manufacture‘ under FTP:

“Manufacture” means to make, produce, fabricate, assemble, process or

bring into existence, by hand or by machine, a new product having a

distinctive name, character or use and shall include processes such as

refrigeration, re-packing, polishing, labelling, Re-conditioning repair,

remaking, refurbishing, testing, calibration, re-engineering. Manufacture, for

the purpose of FTP, shall also include agriculture, aquaculture, animal

husbandry, floriculture, horticulture, pisciculture, poultry, sericulture,

viticulture and mining”

Bringing into existence immoveable property through onsite

fabrication or assembly = ‗manufacture‘ under FTP?

Circular F. No. Misc.8/AM-2001/DBK Cell, dated December 5, 2000

issued by the Directorate General of Foreign Trade (―DGFT‖) -

pertinent

ONSITE ACTIVITIES – „MANUFACTURE‟? (CONT)

All

rig

hts

reserv

ed

Excise and Customs – key issues | 44

The circular: relevant excerpt

“It is noted that it is not possible for a single contractor to manufacture

himself all the items required for completion of such projects and hence

certain items…have necessarily to be procured from other sources. These

items are often directly supplied to the project for assembly, commissioning,

erection, testing etc at site. It is, therefore, clarified that for all such directly

supplied items whether imported or indigenous as are used in the project,

the condition of „manufacture in India‟, a pre-requisite for grant of deemed

export benefits, is satisfied in view of the fact that the aforesaid activities

being undertaken at the project site constitute „manufacture‟…”

Bringing into existence a project (a power project, for example) or

part thereof constitutes ‗manufacture‘ under FTP?

If yes, handing over the project to owner = deemed export?

ONSITE ACTIVITIES – „MANUFACTURE‟? (CONT)

All

rig

hts

reserv

ed

Excise and Customs – key issues | 45

If yes, entitled for deemed export benefits on the input side and no

excise duty on the output side?

May be explored by those ineligible for excise duty exemption or

refund on the output side

Technical issues:

All deemed export categories require ‗supply of goods‘

Such interpretation will equalize indirect tax benefits for mega and non-

mega power projects – against policy framework

ONSITE ACTIVITIES – „MANUFACTURE‟? (CONT)

All

rig

hts

reserv

ed

Excise and Customs – key issues | 46

As discussed earlier, for those ineligible for excise duty exemption or

refund on the output side, output excise duty becomes a cost

Broad definition of ‗Manufacture‘ under FTP:

“Manufacture” means to make, produce, fabricate, assemble, process or

bring into existence, by hand or by machine, a new product having a

distinctive name, character or use and shall include processes such as

refrigeration, re-packing, polishing, labelling, Re-conditioning repair, remaking,

refurbishing, testing, calibration, re-engineering. Manufacture, for the purpose

of FTP, shall also include agriculture, aquaculture, animal husbandry,

floriculture, horticulture, pisciculture, poultry, sericulture, viticulture and

mining”

Minor processing may amount to ‗Manufacture‘ under FTP but not

under Central Excise laws

MINOR PROCESSING – „MANUFACTURE‟?

All

rig

hts

reserv

ed

Excise and Customs – key issues | 47

Importing equipments and polishing or labeling or repacking them

constitutes ‗manufacture‘ under FTP?

If yes, supply of such polished/ labeled/ repacked equipments to

owner = deemed export?

If yes, entitled for deemed export benefits on the input side and no

excise duty on the output side?

May be explored by those ineligible for excise duty exemption or

refund on the output side

Technical issues:

‗manufacture‘ = new, marketable product/good must emerge

Such interpretation will equalize indirect tax benefits for mega and non-

mega power projects – against policy framework

MINOR PROCESSING – „MANUFACTURE‟? (CONT)

All

rig

hts

reserv

ed

Excise and Customs – key issues | 48

PROJECT IMPORTS

& DEEMED EXPORT

BENEFITS TO

POWER PROJECTS

All

rig

hts

reserv

ed

Excise and Customs – key issues | 49

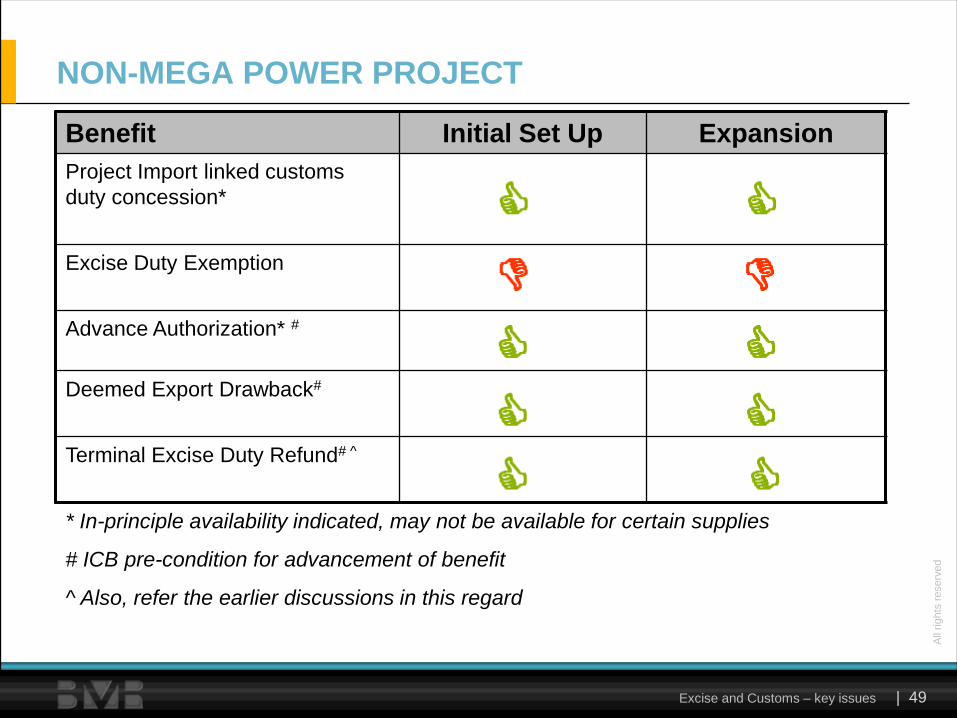

NON-MEGA POWER PROJECT

Benefit Initial Set Up Expansion

Project Import linked customs

duty concession*

Excise Duty Exemption

Advance Authorization* #

Deemed Export Drawback#

Terminal Excise Duty Refund# ^

* In-principle availability indicated, may not be available for certain supplies

# ICB pre-condition for advancement of benefit

^ Also, refer the earlier discussions in this regard

All

rig

hts

reserv

ed

Excise and Customs – key issues | 50

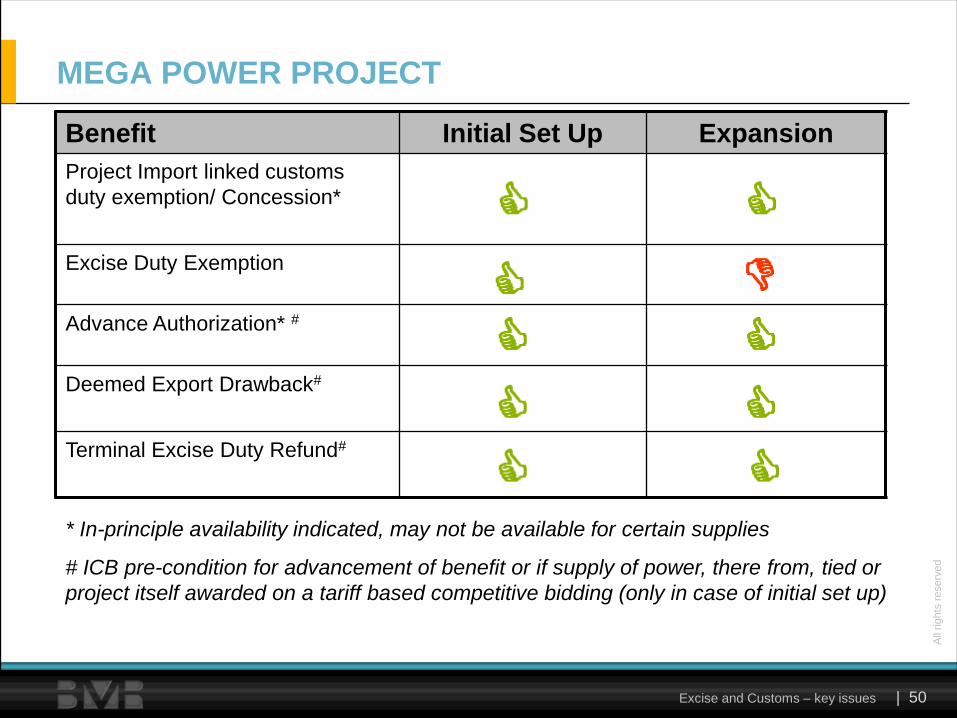

MEGA POWER PROJECT

Benefit Initial Set Up Expansion

Project Import linked customs

duty exemption/ Concession*

Excise Duty Exemption

Advance Authorization* #

Deemed Export Drawback#

Terminal Excise Duty Refund#

* In-principle availability indicated, may not be available for certain supplies

# ICB pre-condition for advancement of benefit or if supply of power, there from, tied or

project itself awarded on a tariff based competitive bidding (only in case of initial set up)

All

rig

hts

reserv

ed

Excise and Customs – key issues | 51

ULTRA MEGA POWER PROJECT

Benefit Initial Set Up Expansion

Project Import linked customs

duty exemption/ Concession*

Excise Duty Exemption^

Advance Authorization* #

Deemed Export Drawback#

Terminal Excise Duty Refund#

* In-principle availability indicated, may not be available for certain supplies

^ If supply of power tied, there from, through a tariff based competitive bidding

# ICB pre-condition for advancement of benefit or supply of power tied, there from,

through a tariff based competitive bidding (only in case of initial set up)

All

rig

hts

reserv

ed

Excise and Customs – key issues | 52C h a l l e n g e U s

All

rig

hts

reserv

ed

Excise and Customs – key issues | 53

ANNEXURES

All

rig

hts

reserv

ed

Excise and Customs – key issues | 54

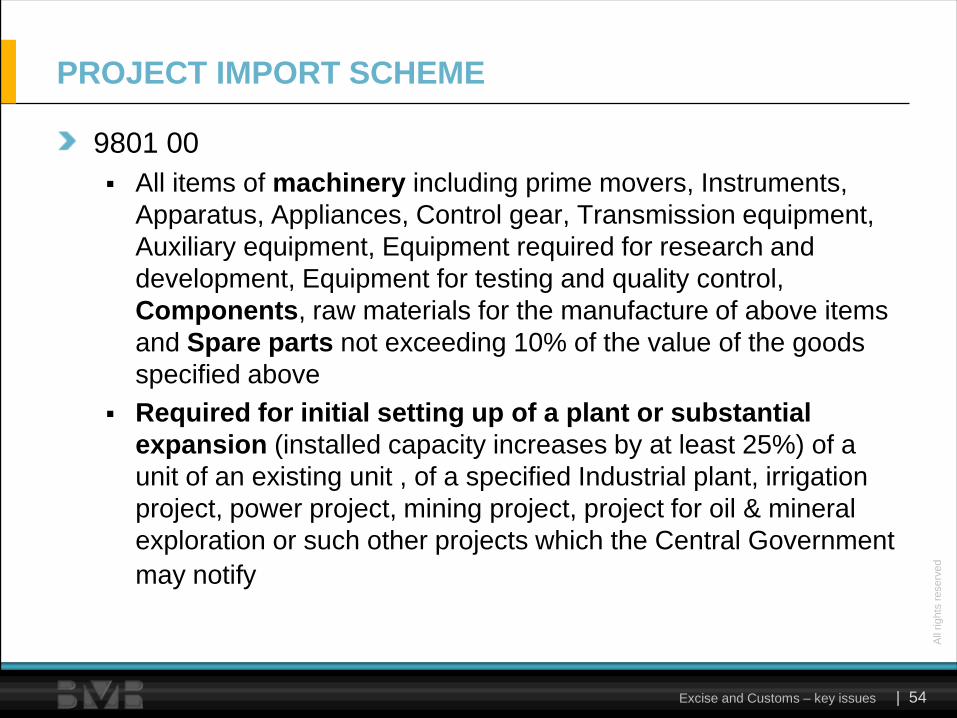

PROJECT IMPORT SCHEME

9801 00

All items of machinery including prime movers, Instruments,

Apparatus, Appliances, Control gear, Transmission equipment,

Auxiliary equipment, Equipment required for research and

development, Equipment for testing and quality control,

Components, raw materials for the manufacture of above items

and Spare parts not exceeding 10% of the value of the goods

specified above

Required for initial setting up of a plant or substantial

expansion (installed capacity increases by at least 25%) of a

unit of an existing unit , of a specified Industrial plant, irrigation

project, power project, mining project, project for oil & mineral

exploration or such other projects which the Central Government

may notify

All

rig

hts

reserv

ed

Excise and Customs – key issues | 55

--- Machinery :

9801 00 11 ---- For industrial plant project

9801 00 12 ---- For irrigation plant

9801 00 13 ---- For power project

9801 00 14 ---- For mining project

9801 00 15 ---- Project for exploration of oil or other minerals

9801 00 19 ---- For other projects

9801 00 20 --- Components (whether or not finished or not) or

raw materials for the manufacture of aforesaid

items required for the initial setting up of a unit or

the substantial expansion of a unit

9801 00 30 --- Spare parts and other raw materials (including

semi-finished materials or consumable stores for

the maintenance of plant or project

CUSTOMS TARIFF CLASSIFICATION

All

rig

hts

reserv

ed

Excise and Customs – key issues | 56C h a l l e n g e U s

Related Documents