The Discounted Cash Flow Valuation Method

BlueBookAcademy.com - Value companies using Discounted Cash Flow Valuation

Aug 14, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

The Discounted Cash Flow Valuation Method

•Steps involved to build a DCF model from scratch

• Pros and Cons of the DCF valuation technique

• Best Practices in Model Building

Learning Outcomes

Discounted Cash Flow (DCF) valuation is a tool for estimating the value of a company or its shares.

In summary: the expected value of an asset is the present value of the forecast cash flows of an asset, using a discount rate adjusted to reflect the risk.

Introduction

Steps to Build a DCF Model

1. Historical Performance

3. Calculate Terminal Value

4. Discount using Cost of Capital

2. Forecasting

5. Value the Company

Discounted Cash Flow Model

Years 0 1 2 3 4 5 5Financial Year (Dec. 31-Dec-14 31-Dec-15 31-Dec-16 31-Dec-17 31-Dec-18 31-Dec-19 Terminal PeriodTotal Turnover 5,505 6,590 8,133 9,632 11,155 12,661growth (%) 19.7% 23.4% 18.4% 15.8% 13.5%

EBIT 403 969 1,191 1,545 2,092 2,925margin (%) 7.3% 14.7% 14.6% 16.0% 18.8% 23.1%

Depreciation & Amortisation

54.0 62.4 119.3 174.1 226.9 278.5

Tax @ 23.6% (95.2) (229.0) (281.4) (365.2) (494.4) (691.3)Capital Expenditure 144.5 191.1 235.9 279.3 323.5 367.2Capex/Sales (%) -2.6% -2.9% -2.9% -2.9% -2.9% -2.9%

Change in Working Capital

0.0 (340.3) 491.5 471.7 471.7 453.4Working Capital / Sales (%)

0.0% 5.2% -6.0% -4.9% -4.2% -3.6%

Free Cash Flow 217 271 1284 1546 1972 2598 2598

Discount Factor 0.91 0.83 0.76 0.69 0.63 0.63

Terminal Value 39,628

Present Value 247 1,066 1,170 1,359 1,632 24,884Enterprise Value 30,357Net Debt -213.6Market 30,571No. Shares (m) 61.7 Share Price ($) 495.5

Discounted Cash Flow Model

AssumptionsTax rate 24%WACC (see calc below) 9.6%Terminal Growth Rate 3.0%

WACCCost of Equity (CAPM)Risk Free Rate 1.79%Market Risk Premium 8.21%Equity Beta 0.97

Cost of Equity 9.8%

Cost of Debt kd 5.38%kd (1-t) 4.11%

WACC CalculationMarket Value of Equity ($m)

26,800Market Value of Debt 900

WACC 9.6%

Weighted Average Cost of Capital Calculation

Discounting Formula

Forecast Cash Flow

Discount Rate

Expected cash flows to be generated in future years

Discount rate (%) reflects the risk and uncertainty of cash flows

Higher discount rate —> Higher uncertainty

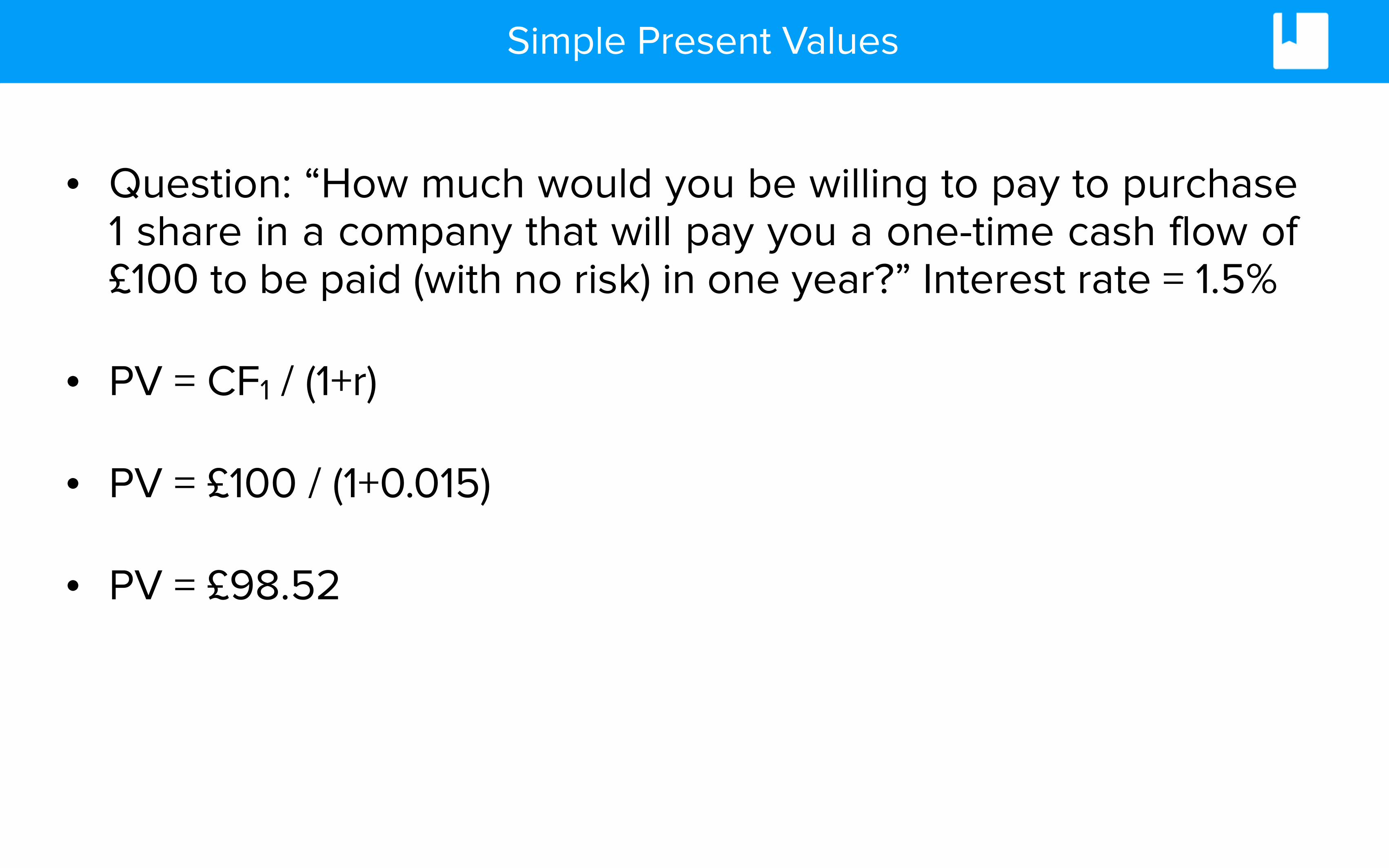

Simple Present Values

• Question: “How much would you be willing to pay to purchase 1 share in a company that will pay you a one-time cash flow of £100 to be paid (with no risk) in one year?” Interest rate = 1.5%

• PV = CF1 / (1+r)

• PV = £100 / (1+0.015)

• PV = £98.52

• The valuation of a company requires discounting the future ‘free’ cash flows to the present.

• ‘r’ indicates the appropriate cost of capital.

Valuation Using Free Cash Flows

• Free cash flow is the amount of cash that a company has left over after it has paid all of its expenses, including capital expenditures.

• Free cash flow is expressed as:

• Cash flow from operations - Capital Expenditures

• Free cash flow to the firm is the cash available to all investors, both equity and debt holders.

Valuation Using Free Cash Flows

• Free cash flow generated by assets:

– Free Cash Flow = EBIT x (1 - Tax Rate)

» + Depreciation + Amortisation

» +/– Change in Operating Working Capital

» – Capital expenditure

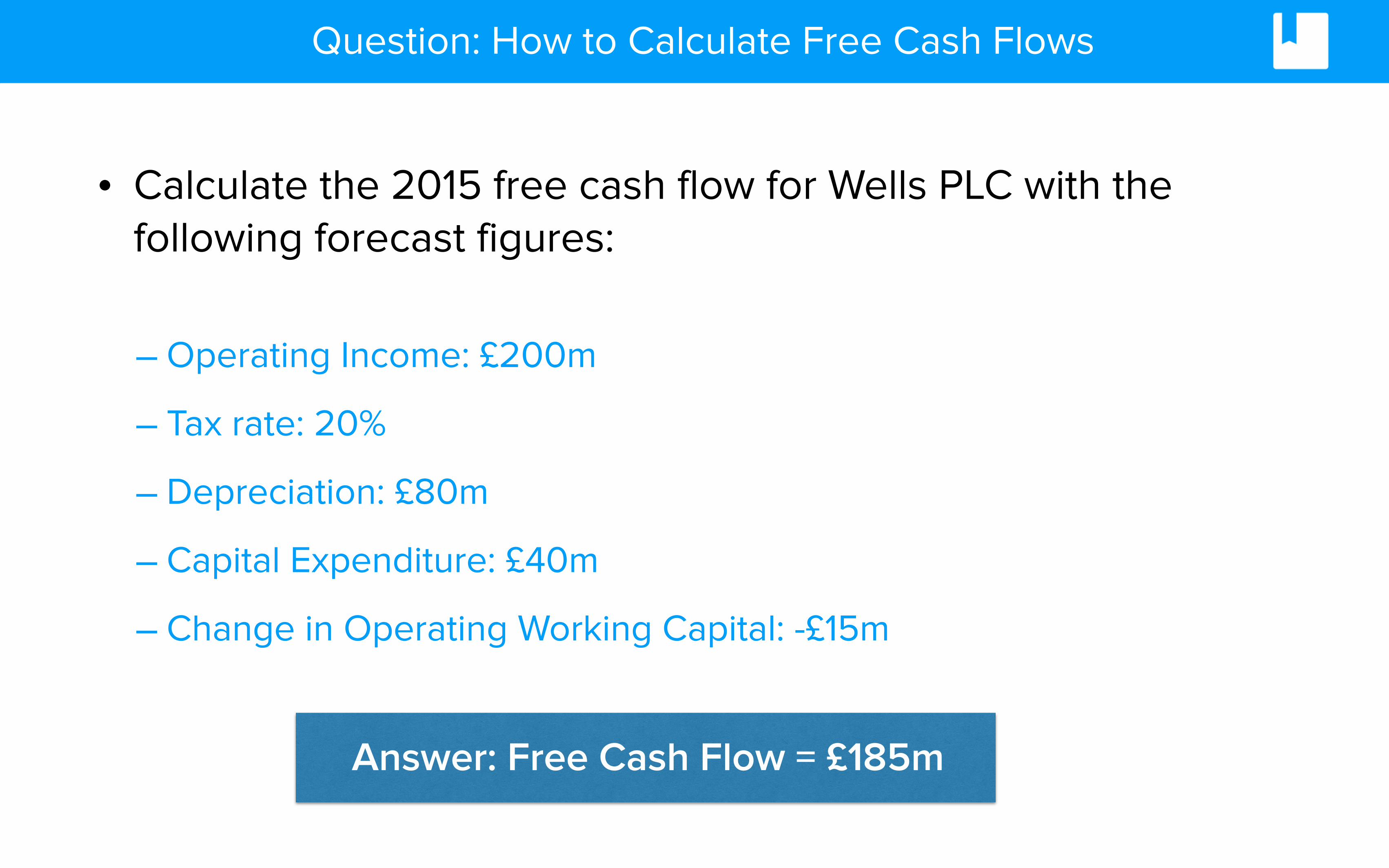

How to Calculate Free Cash Flows

• Calculate the 2015 free cash flow for Wells PLC with the following forecast figures:

– Operating Income: £200m

– Tax rate: 20%

– Depreciation: £80m

– Capital Expenditure: £40m

– Change in Operating Working Capital: -£15m

Question: How to Calculate Free Cash Flows

Answer: Free Cash Flow = £185m

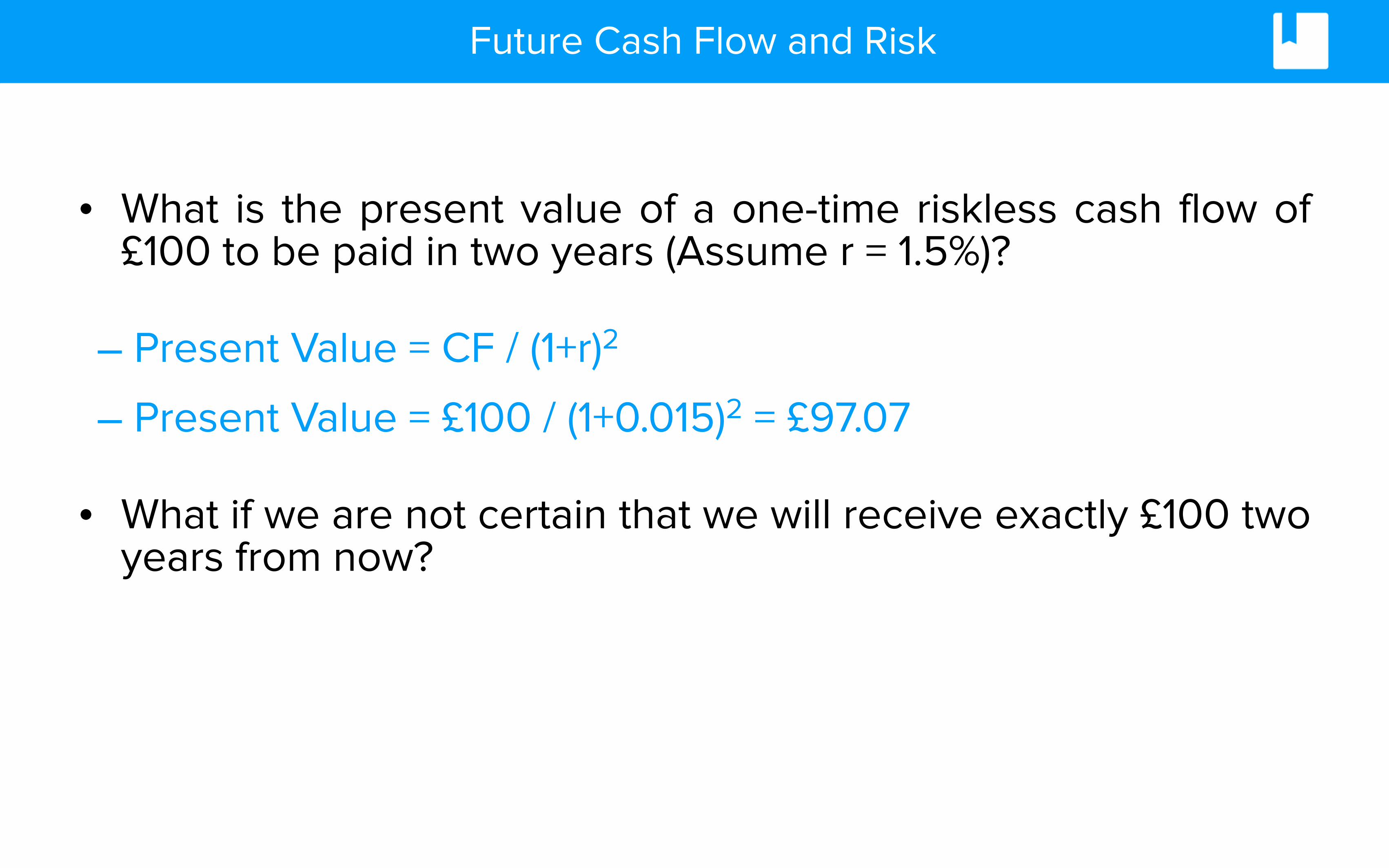

Future Cash Flow and Risk

• What is the present value of a one-time riskless cash flow of £100 to be paid in two years (Assume r = 1.5%)?

– Present Value = CF / (1+r)2

– Present Value = £100 / (1+0.015)2 = £97.07

• What if we are not certain that we will receive exactly £100 two years from now?

Present Value of What Value? Equity or Enterprise?

1. Equity valuation:

– Forecast free cash flows available to equity holders. – Discount expected cash flows by the cost of equity capital.

2. Enterprise valuation:

– Forecast cash flows available to all providers of capital (debt and equity). – Discount expected cash flows by weighted average cost of (debt and

equity) capital. – Calculate equity value by subtracting value of debt.

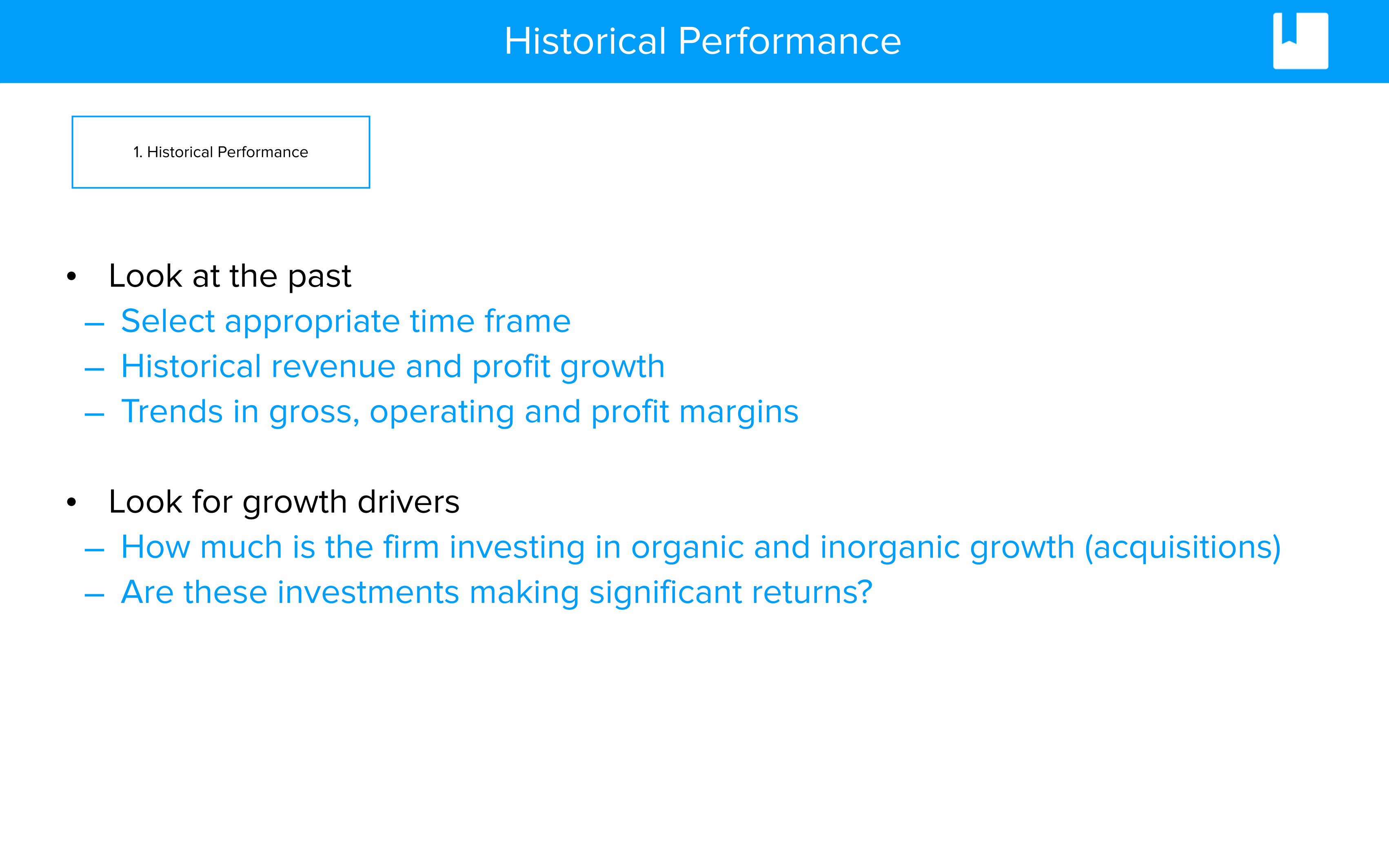

Historical Performance

• Look at the past – Select appropriate time frame – Historical revenue and profit growth – Trends in gross, operating and profit margins

• Look for growth drivers – How much is the firm investing in organic and inorganic growth (acquisitions) – Are these investments making significant returns?

1. Historical Performance

Forecasting Performance

• The value of a business comes from two periods: – Explicit forecast period

– Terminal value

• To develop forecasts, read industry reports, assess macroeconomic indicators to determine (i) market demand (ii) investment required to meet that demand and (iii) its related operating costs.

• Explicit forecast period reflects the time horizon that company can maintain return on investment from its projects in excess of required return.

2. Forecasting

Multiple Cash Flows

• What if the firm will generate many cash flows at different times in the future?

• PV = CF1 / (1+r) + CF2 / (1+r)2 + CF3 / (1+r)3 + …

• Example: Calculate the present value of three $10 cash flows paid at end of year 1, year 2 and year 3. Assume a discount rate of 10%.

• PV = 10 / (1.10) + 10 / (1.10)2 + 10 / (1.10)3

• PV = 9.09 + 8.26 + 7.51 = $24.86

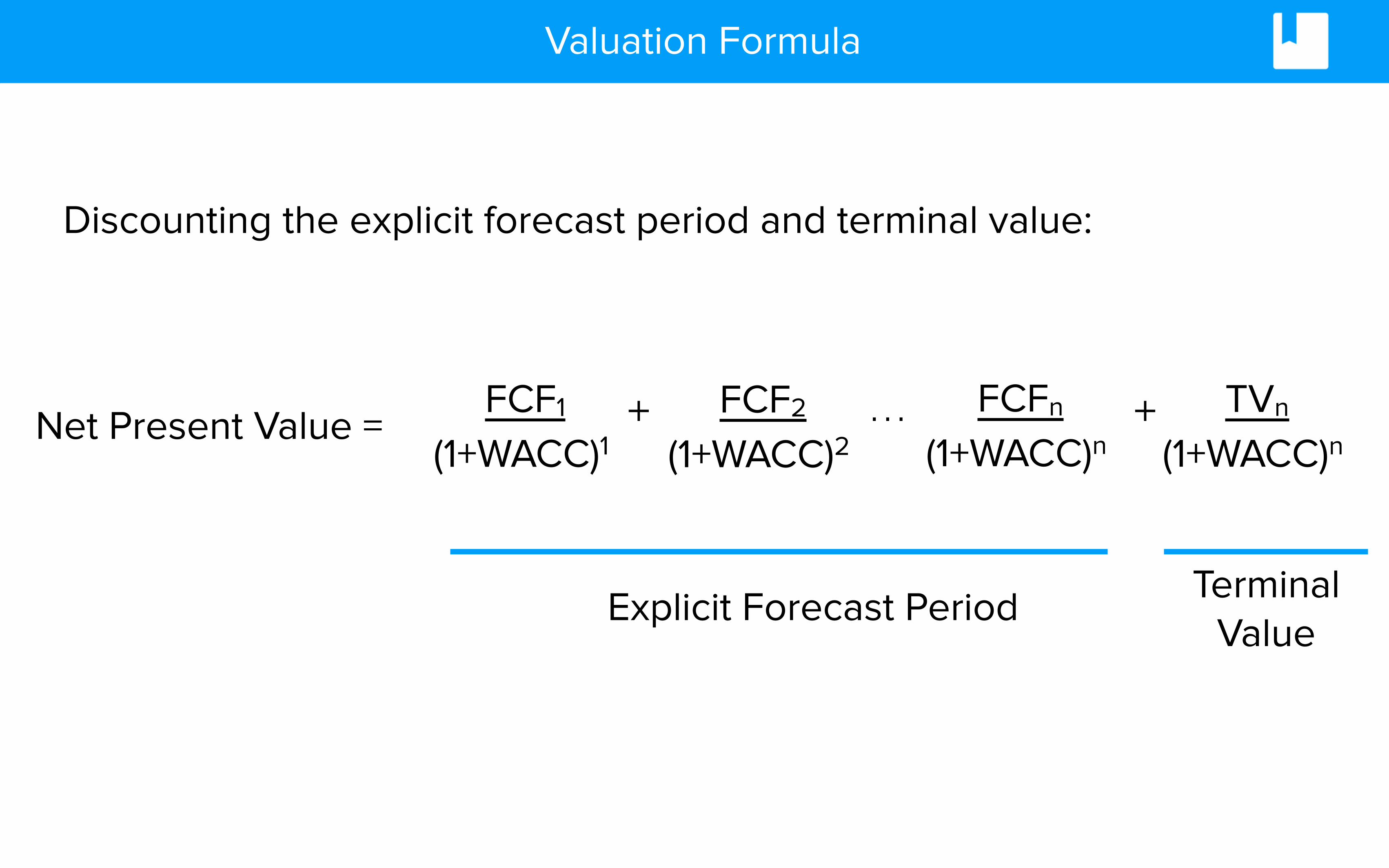

Valuation Formula

Discounting the explicit forecast period and terminal value:

Net Present Value = FCF1

(1+WACC)1FCF2

(1+WACC)2FCFn

(1+WACC)nTVn

(1+WACC)n+ … +

Explicit Forecast Period Terminal Value

Perpetuity

• What if we received £10 a year forever?

• PV = CF1 / (1+r) + CF2 / (1+r)2 + CF3 / (1+r)3+…

• Formula for a perpetuity: PV = CF / r

• Used for calculating terminal values

Example: Value of Growing Perpetuity

Example:

• Calculate the present value of a cash flow stream that starts at £10 one year from today, and then grows at a rate of 5% per year thereafter. Assume a discount rate of 12%.

– PV = CF / (r-g)

– PV = 10 / (0.12-0.05)

– PV = £142.86

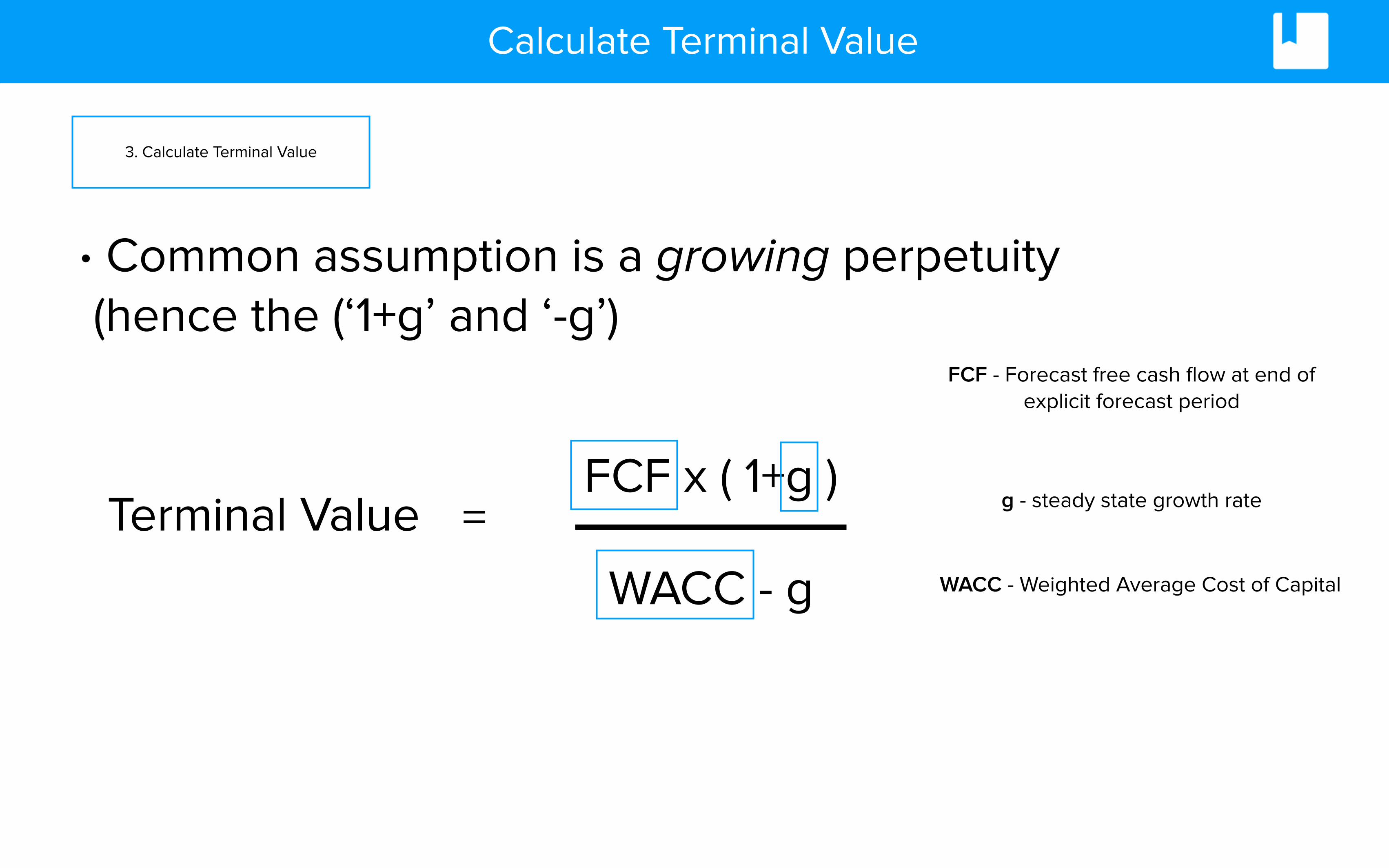

Calculate Terminal Value

3. Calculate Terminal Value

FCF x ( 1+g )

WACC - gTerminal Value =

• Common assumption is a growing perpetuity (hence the (‘1+g’ and ‘-g’)

FCF - Forecast free cash flow at end of explicit forecast period

g - steady state growth rate

WACC - Weighted Average Cost of Capital

Calculate Terminal Value

3. Calculate Terminal Value

• Why (1+g)? - we need to discount cash flows which come in at the end of the year, not the beginning

• How do we determine ‘g’? • Normally above inflation. • Lower than the explicit forecast period. • Cannot exceed its return on equity in the long term.

Analysing ‘r’ - The Cost of Capital

• The cost of capital of a firm is also known as the ‘Weighted Average Cost of Capital’ or WACC.

• As we know, a company has two sources of funds:

1. Equity

2. Debt

• WACC is the weighted average of the costs of these two sources of capital.

4. Discount using Cost of Capital

Analysing ‘r’ - The Cost of Capital

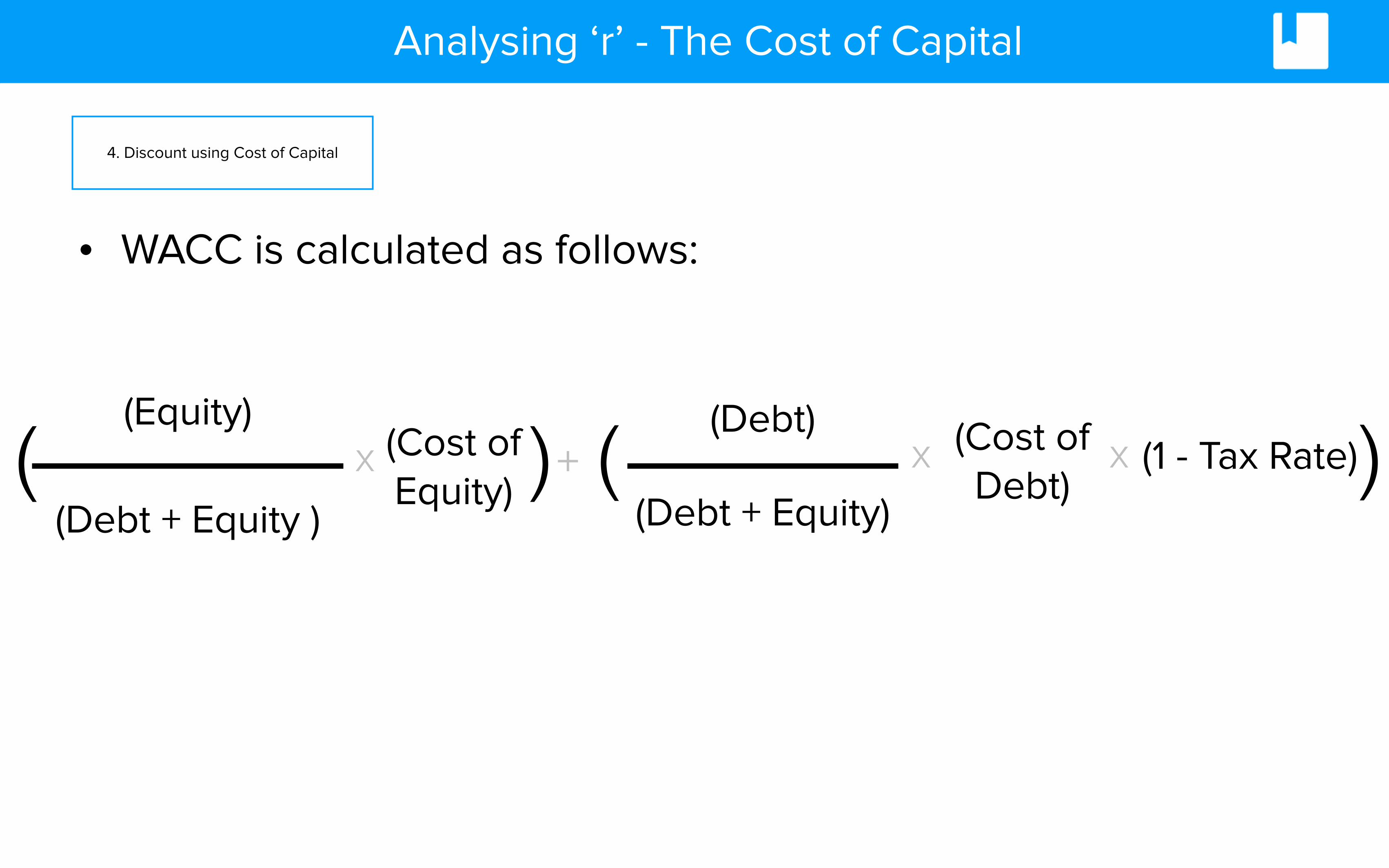

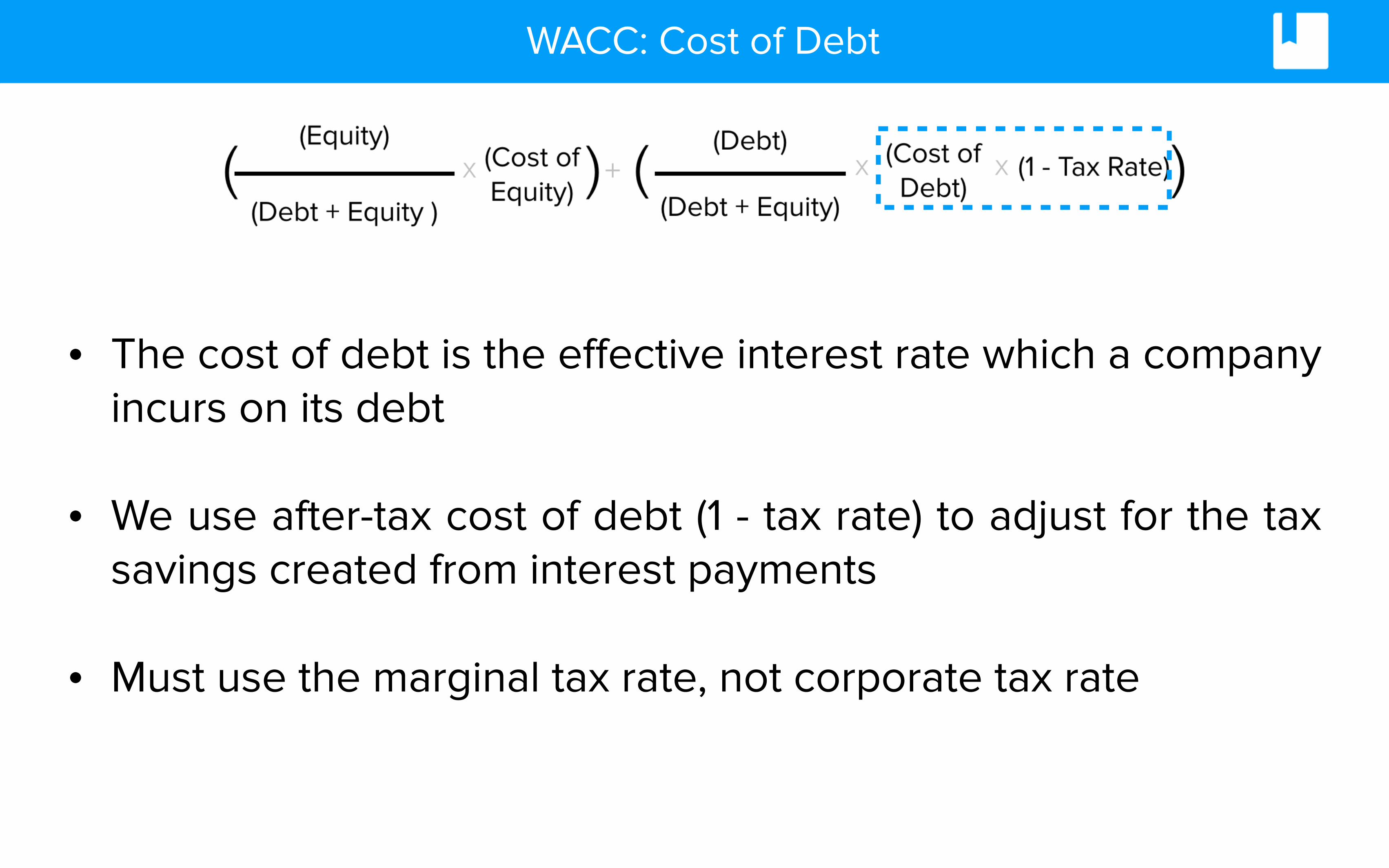

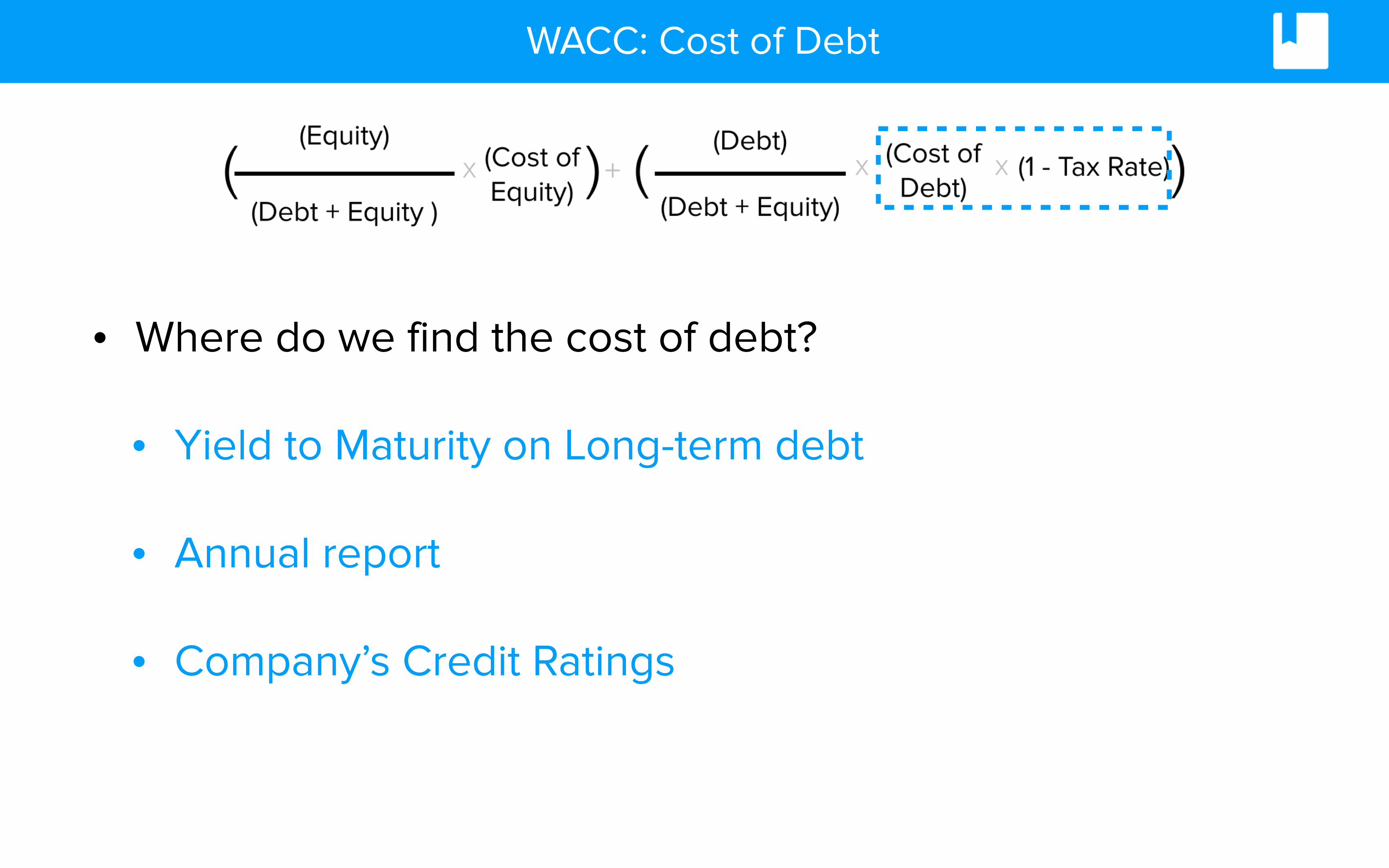

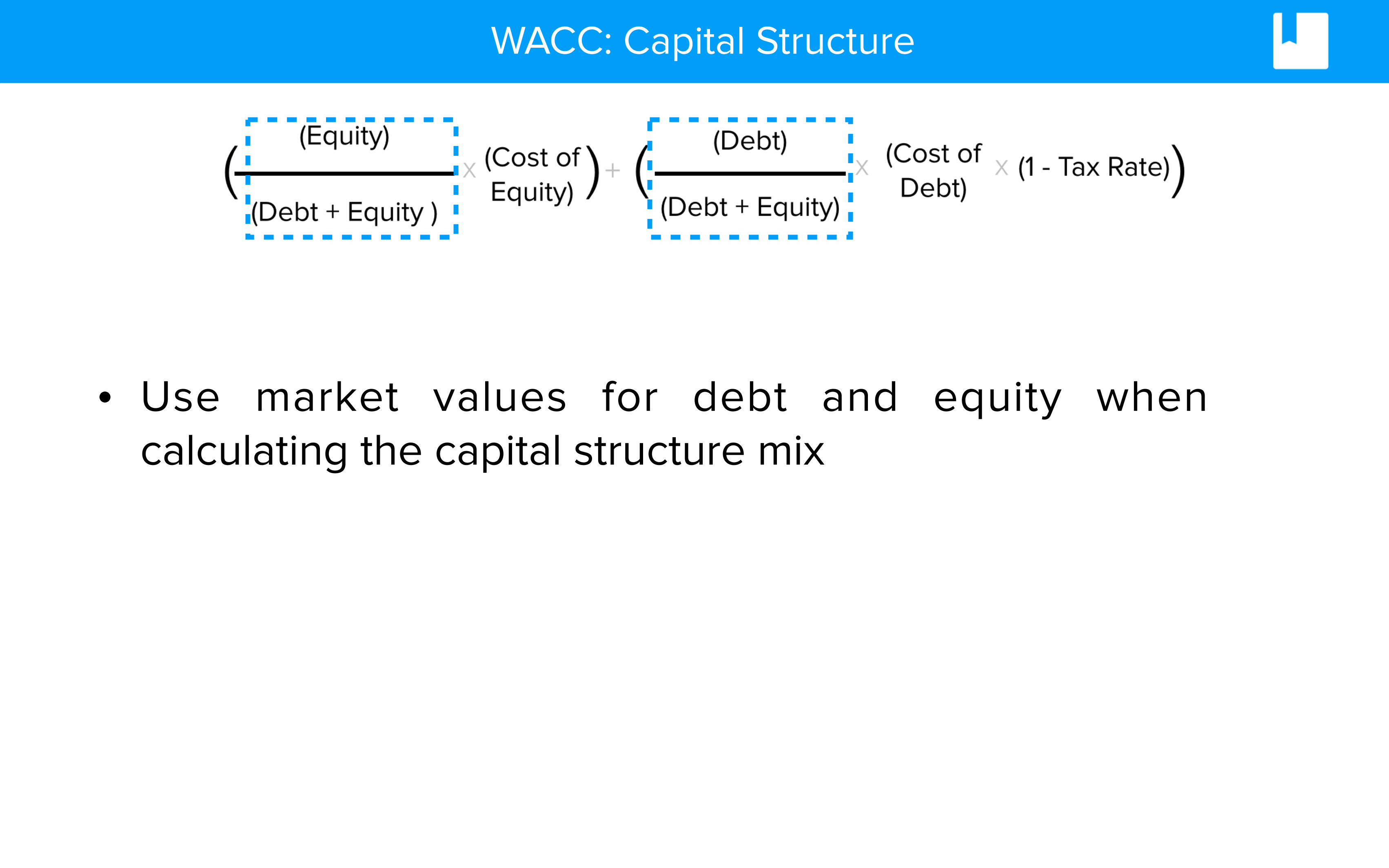

• WACC is calculated as follows:

(Cost of Debt)

x(Debt)

(Debt + Equity)+ (

(Equity)

(Debt + Equity )( (Cost of

Equity) x ) (1 - Tax Rate)x )

4. Discount using Cost of Capital

Calculating Cost of Equity using CAPM

• Two key applications of the Capital Asset Pricing Model (CAPM):

1. Measures and quantifies risk – One stock is riskier than another if it has a higher Beta.

2. Valuation – Used to measure cost of capital when finding the discount

rate

Cost of Equity

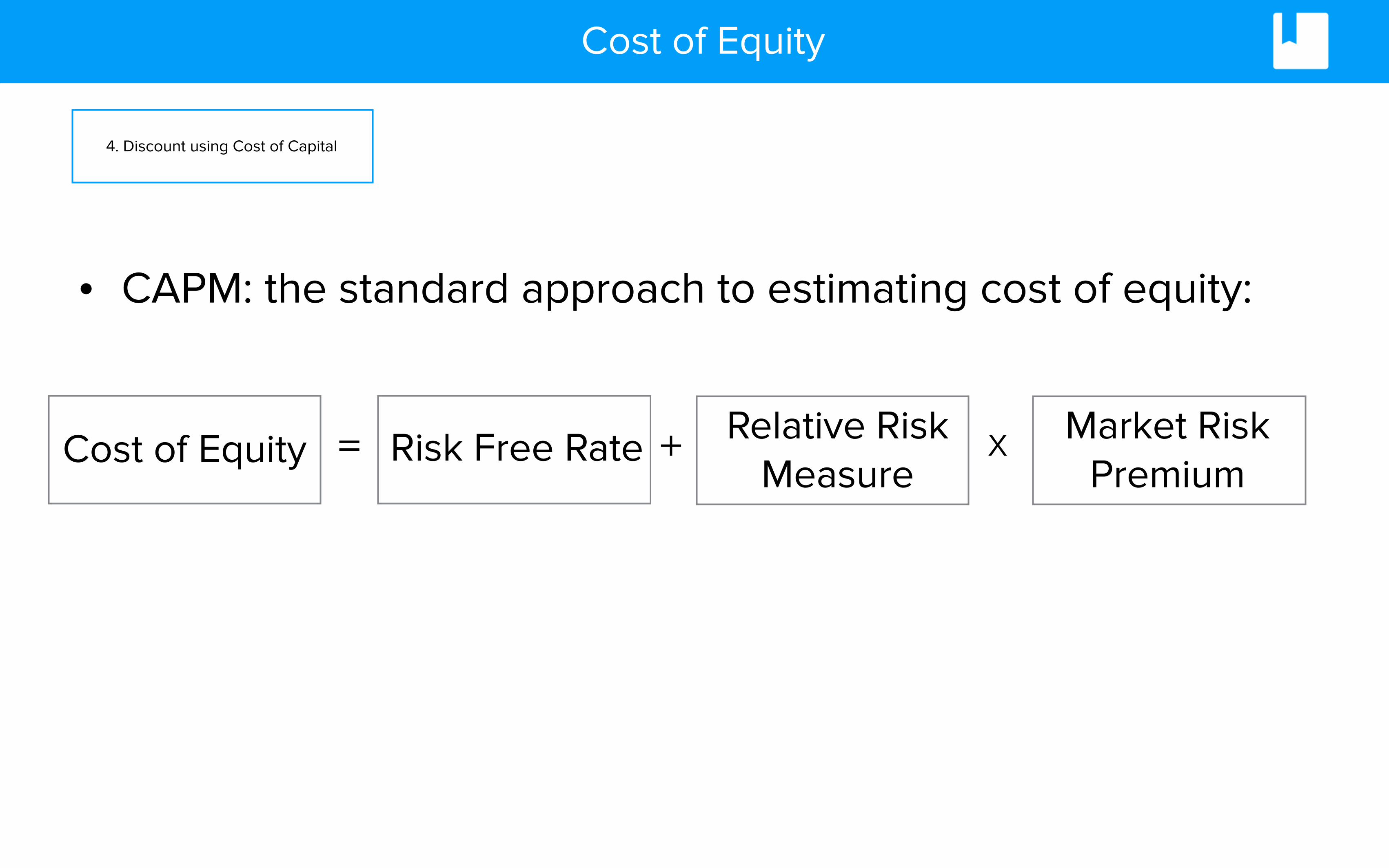

• CAPM: the standard approach to estimating cost of equity:

=Cost of Equity Risk Free Rate + Relative Risk Measure

x Market Risk Premium

4. Discount using Cost of Capital

Cost of Equity

• The return on any investment with such low risk that the risk is considered to not exist.

• Usually the yield on a 10-year government bond.

=Cost of Equity Risk Free Rate + Relative Risk Measure

x Market Risk Premium

Cost of Equity

• Market risk premium is the average return on the market minus the risk free rate

• Investors need to be compensated for the additional risk of investing in stocks

=Cost of Equity Risk Free Rate + Relative Risk Measure

x Market Risk Premium

Cost of Equity

• Known as ‘Beta’ - Measures the volatility of a company’s stock price to changes in the broader market

• Beta = 1 indicates the stock price moves in line with the market

• Beta > 1 Stock price is more volatile than the market

=Cost of Equity Risk Free Rate + Relative Risk Measure

x Market Risk Premium

Cost of Equity

Question

What does Beta = 0 indicate?

WACC: Cost of Equity

• In the real world:

– Government security rates are used as risk free rates

– Historical risk premiums are used for the risk premium

– Betas are estimated by regressing stock returns against market returns

4. Discount using Cost of Capital

WACC: Cost of Debt

• The cost of debt is the effective interest rate which a company incurs on its debt

• We use after-tax cost of debt (1 - tax rate) to adjust for the tax savings created from interest payments

• Must use the marginal tax rate, not corporate tax rate

WACC: Cost of Debt

• Where do we find the cost of debt?

• Yield to Maturity on Long-term debt

• Annual report

• Company’s Credit Ratings

WACC: Capital Structure

• Use market values for debt and equity when calculating the capital structure mix

WACC

AssumptionsTax rate 24%WACC (see calc below) 9.6%Terminal Growth Rate 3.0%

WACCCost of Equity (CAPM)Risk Free Rate 1.79%Market Risk Premium 8.21%Equity Beta 0.97

Cost of Equity 9.8%

Cost of Debt kd 5.38%kd (1-t) 4.11%

WACC CalculationMarket Value of Equity ($m)

26,800Market Value of Debt 900

WACC 9.6%

Weighted Average Cost of Capital Calculation

4. Discount using Cost of Capital

6 Steps to Build a DCF

1. Calculate a free cash flow:

2. Discounting a single cash flow: – PV = CF1 / (1+r)

3. Discounting a single cash flow in “n” years from now: – PV = CFn / (1+r)n

4. Multiple cash flows in future: – PV = CF1 / (1+r) + CF2 / (1+r)2 + CF3 / (1+r)3 + …

5. Growing Perpetuity: – PV = CF / (r-g) (1st CF at end of year 1, then grow at g)

6. Deduct Net Debt from Enterprise Value to calculate Equity Value: – Enterprise Value - Net Debt = Equity Value

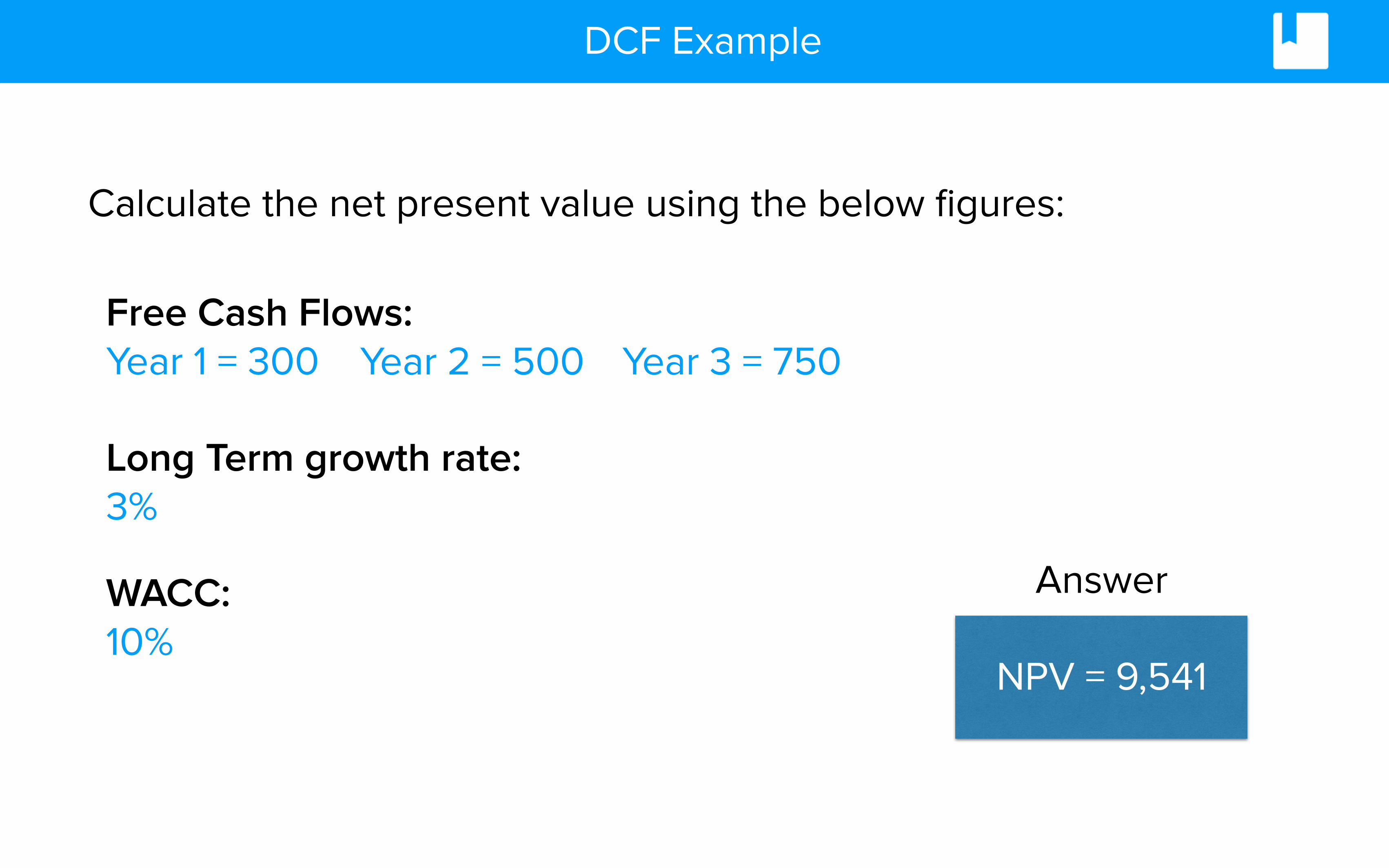

DCF Example

Calculate the net present value using the below figures:

Free Cash Flows: Year 1 = 300 Year 3 = 750Year 2 = 500

Long Term growth rate: 3%

WACC: 10%

NPV = 9,541

Answer

Discounted Cash Flow Model

Years 0 1 2 3 4 5 5Financial Year (Dec. Year end) 31-Dec-14 31-Dec-15 31-Dec-16 31-Dec-17 31-Dec-18 31-Dec-19 Terminal PeriodTotal Turnover 5,505 6,590 8,133 9,632 11,155 12,661growth (%) 19.7% 23.4% 18.4% 15.8% 13.5%

EBIT 403 969 1,191 1,545 2,092 2,925margin (%) 7.3% 14.7% 14.6% 16.0% 18.8% 23.1%

Depreciation & Amortisation 54.0 62.4 119.3 174.1 226.9 278.5

Tax @ 23.6% (95.2) (229.0) (281.4) (365.2) (494.4) (691.3)Capital Expenditure 144.5 191.1 235.9 279.3 323.5 367.2Capex/Sales (%) -2.6% -2.9% -2.9% -2.9% -2.9% -2.9%

Change in Working Capital 0.0 (340.3) 491.5 471.7 471.7 453.4Working Capital / Sales (%) 0.0% 5.2% -6.0% -4.9% -4.2% -3.6%

Free Cash Flow 217 271 1284 1546 1972 2598 2598

Discount Factor 0.91 0.83 0.76 0.69 0.63 0.63

Terminal Value 39,628

Present Value 247 1,066 1,170 1,359 1,632 24,884Enterprise Value (m) 30,357Net Debt -213.6Market Capitalisation ($m) 30,571No. Shares (m) 61.7 Share Price ($) 495.5

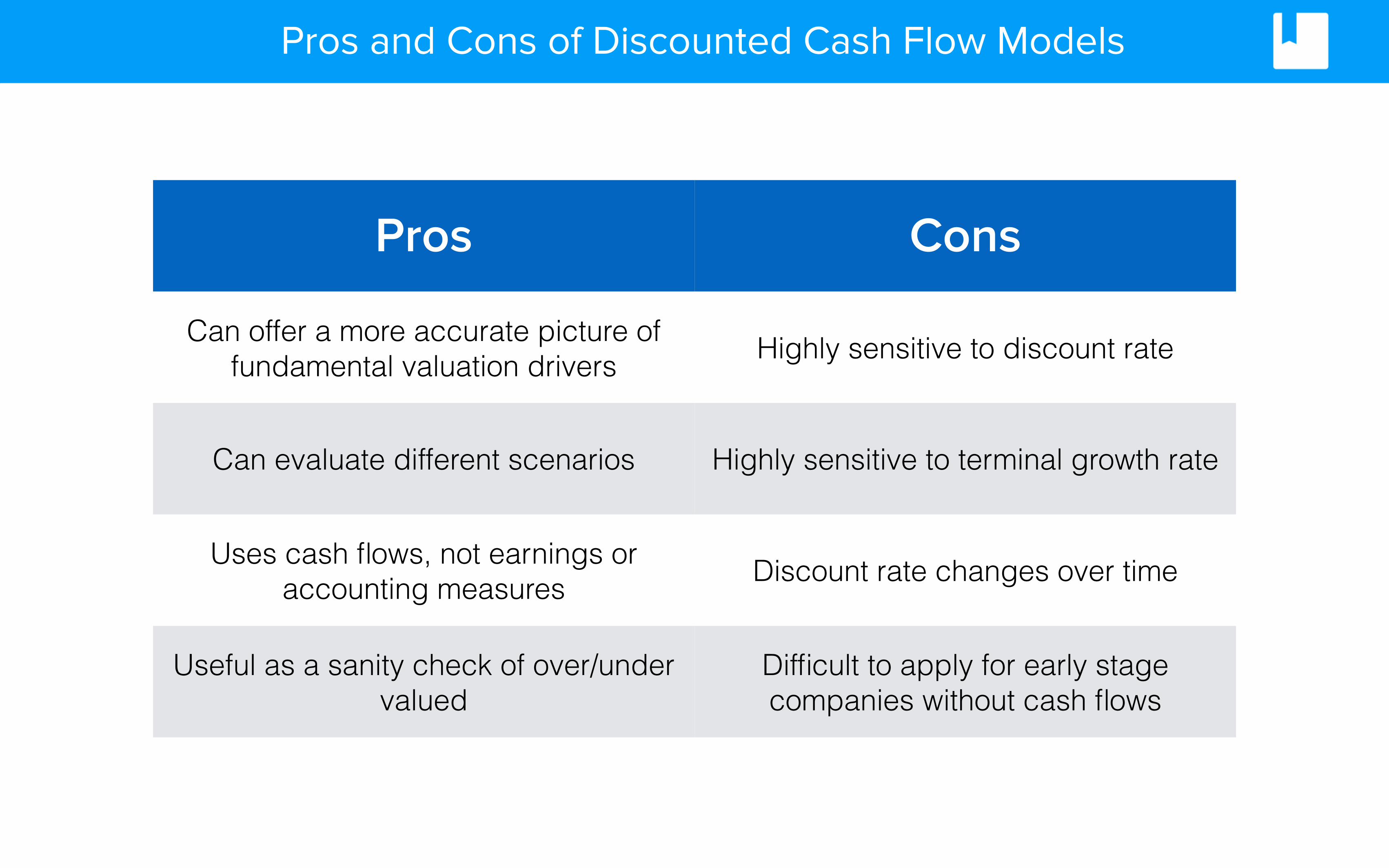

Pros and Cons of Discounted Cash Flow Models

Pros Cons

Can offer a more accurate picture of fundamental valuation drivers Highly sensitive to discount rate

Can evaluate different scenarios Highly sensitive to terminal growth rate

Uses cash flows, not earnings or accounting measures Discount rate changes over time

Useful as a sanity check of over/under valued

Difficult to apply for early stage companies without cash flows

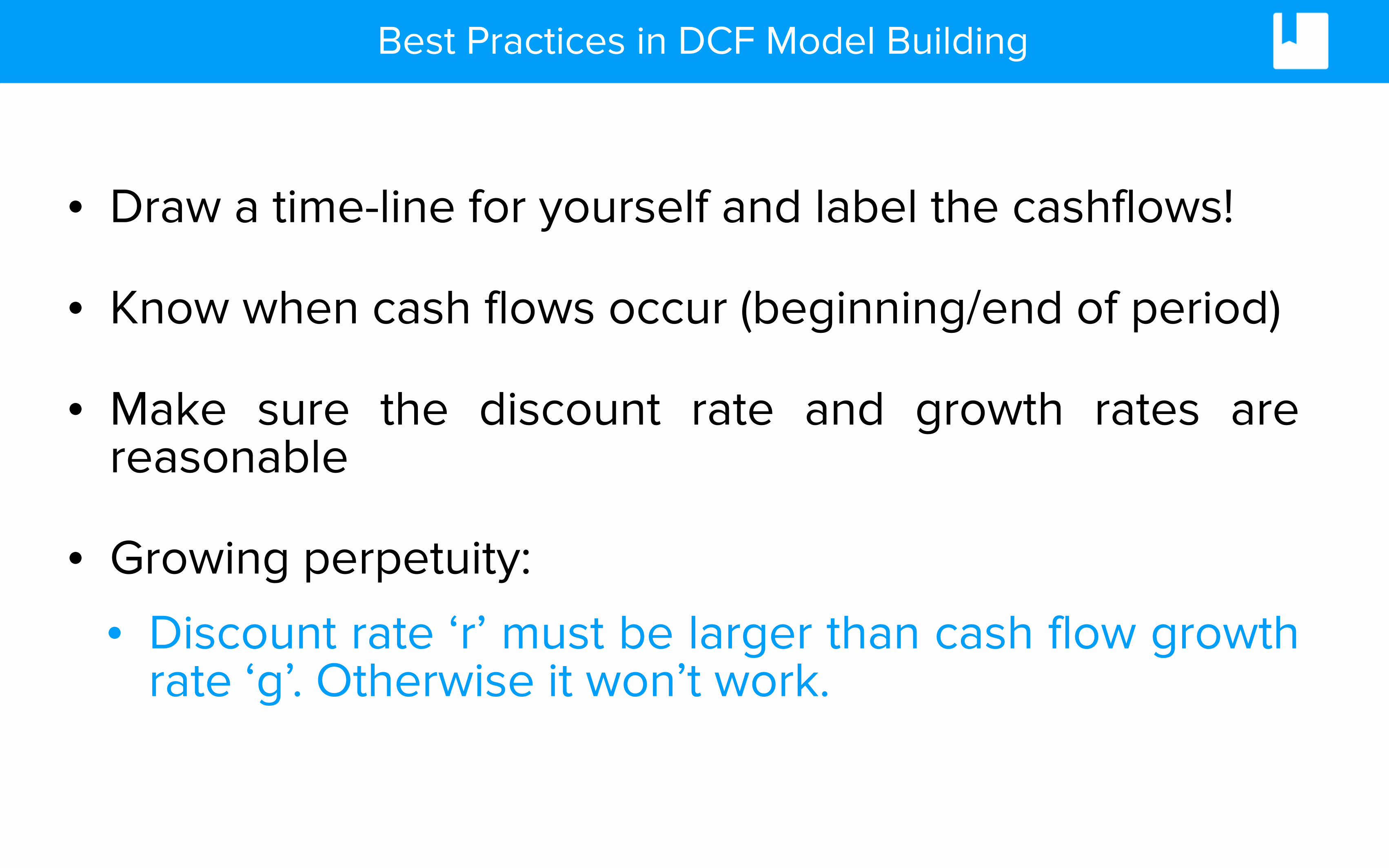

Best Practices in DCF Model Building

• Draw a time-line for yourself and label the cashflows!

• Know when cash flows occur (beginning/end of period)

• Make sure the discount rate and growth rates are reasonable

• Growing perpetuity:

• Discount rate ‘r’ must be larger than cash flow growth rate ‘g’. Otherwise it won’t work.

Recap

• Steps to build a Discounted cash flow model

• Determining the explicit forecast period

• Calculating the terminal value

• How to calculate the discount rate

• Value a company using a DCF Model

Related Documents