BLUE PAPER March 2017 Investing in the Era of Reflation

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

BLUE PAPERMarch 2017

Investing in the Era of Reflation

1

2

3

4

5

Source: Pioneer Investments, data as of February 28, 2017.

Source: Pioneer Investments, data as of February 28, 2017.

Inflation Drivers Inflation Forecasts for 2017 (%)

Risks to our Forecasts

UK

2.8

0.8

2.4

1.2

1.8

0.3

-0.3

0.6

US

EUROZONE

JAPAN

INVESTING IN THE ERA OF REFLATION

Tight Labour Market in the US

Positive Commodity Outlook

Loose Fiscal Policies

Service Sector Inflation

Weaker Globalization

Wage inflation is starting to pick-up in the US. Repatriation of US business and infrastructure spending could put additional pressure on job market.

“Investors should be aware of the new inflation narrative in order to build portfolios that are resilient to this new market scenario.”

2016 2017

Firming global demand should support commodity prices. Oil and metals are set to outperform agricultural commodities. Oil prices are expected to be 60 USD per barrel by the end of 2017.

Deregulation, personal income and corporate tax cuts and infrastructure spending will be the drivers of fiscal expansion in the US. Looser policies also expected in Japan and the Eurozone.

Demographic trends and broad-based economic recovery should sustain service sector inflation, especially in housing and health-care components.

The possible rise of protectionist measures and populism will likely mark an inflection point for globalization, that in the last 20 years has driven a fall in prices and wages.

Trump Disappointment

Trade WarInvestment

Squeeze

Protectionism Weak PolicyImplementationFed Policy

Mistake

-75-55-35-15

5254565

IND

EX

Source: Bloomberg, Citi, data as February 15, 2017.

Source: Pioneer Investments forecast horizon December 17and elaborations on S&P Capital IQ data as of February 15, 2017.

Fixed Income

Inflation Surprise Index Trend Potential Inflation Beneficiaries

Asset Classes AssessmentEU Earnings Per Share Growth (YoY) F

7.2% 8.4%Government Bonds

Equities

Commodities

Credit

European Equities

US Equities

Multi-Asset

INVESTING OPPORTUNITIES

Important Information

Unless otherwise stated, all information contained in this document is from Pioneer Investments and is as of February 15, 2017. The views expressed regarding market and economic trends are those of the author and not necessarily Pioneer Investments, and are subject to change at any time based on market and other conditions and there can be no assurances that countries, markets or sectors will perform as expected. These views should not be relied upon as investment advice, as securities recommendations, or as an indication of trading on behalf of any Pioneer Investments product. There is no guarantee that market forecasts discussed will be realized or that these trends will continue. Investments involve certain risks, including political and currency risks. Investment return and principal value may go down as well as up and could result in the loss of all capital invested. This material does not constitute an offer to buy or a solicitation to sell any units of any investment fund or any services. Pioneer Investments is a trading name of the Pioneer Global Asset Management S.p.A. group of companies.

Date of First Use: March 1, 2017. Infographic tool by Financial Communication team.

Inflation-linked and short duration bonds could support fixed income portfolios in periods of higher inflation.

Materials Financials Industrials

A reflation scenario is positive for European value stocks and earnings growth. Single name selection is crucial to identify the companies that combine value and quality.

Oct 16 Feb 17

A modest increase in inflation driven by a rise in real GDP growth could benefit US equity markets, especially cyclical sectors such as materials, industrials and financials.

In a phase of asset reflation the favourite asset classes have historically been global equities, credit and commodities. Real assets can offer interesting inflation protection opportunities.

BLUE PAPER │ Investing in the Era of Reflation March 2017

4

Inflation: Five Factors to Watch in 2017 and BeyondAfter years of global disinflation in developed markets, inflation pressures seem to finally be building up. Deflation fears, which dominated in Japan and the Eurozone during the last three years, started to dissolve at the end of 2016, as promises of a wide expansionary push in the US nurtured expectations of a step up in global inflation.As you can see in the chart below, inflation dynamics are finally creeping upward across the main Developed Markets (DM).

In our 2017 outlook, inflationary forces appear to be quite strong especially in the US, where positive cyclical momentum is being enhanced by Trump’s expansionary fiscal programme, and in the UK, where currency depreciation is impacting import prices of goods and services. In the Eurozone and Japan, inflation levels should remain below Central Banks’ targets in 2017. However, the turnaround in price dynamics is quite evident even here, thanks to the base effects kicking in.

Putting these trends into perspective, we do not foresee a new phase of structurally high global inflation – such as the one that characterised the 80s and 90s – because some deflationary forces remain active at a global level. However, we believe that 2017 will mark a period of discontinuity in the DM inflation outlook, following the lowflation environment that has dominated since the Great Financial Crisis.

For this reason, we believe that investors should be aware of this new narrative in order to build portfolios that are suitably resilient. In the next few pages, we will analyse the five main drivers investors should pay attention to in 2017 and beyond, as well as offering perspectives on dealing with rising inflation trends across fixed income, equity and multi asset.

Driver # 1. Tight US Labour MarketOne of the main medium-term inflationary triggers we see in the US is related to the tightening of labour markets. Historically, a negative relationship between wage growth and unemployment has prevailed – this is the famous Phillips curve,

We believe that 2017 will mark a period of discontinuity in the DM inflation outlook.

Investors should be aware of the new inflation narrative in order to build portfolios that are suitably resilient.

Wage inflation is starting to pick-up in the US.

Monica Defend Head of Global Asset Allocation Research

This material reflects the opinions of the above author at the time of writing.

Figure 1. Pioneer Investments’ Inflation 2017 Forecast 3.0 2.5 2.0 1.5 1.0 0.5 0.0-0.5

Japan Eurozone US UK

2016 2017Source: Pioneer Investments, February 28, 2017.

%

BLUE PAPER │ Investing in the Era of Reflation March 2017

5

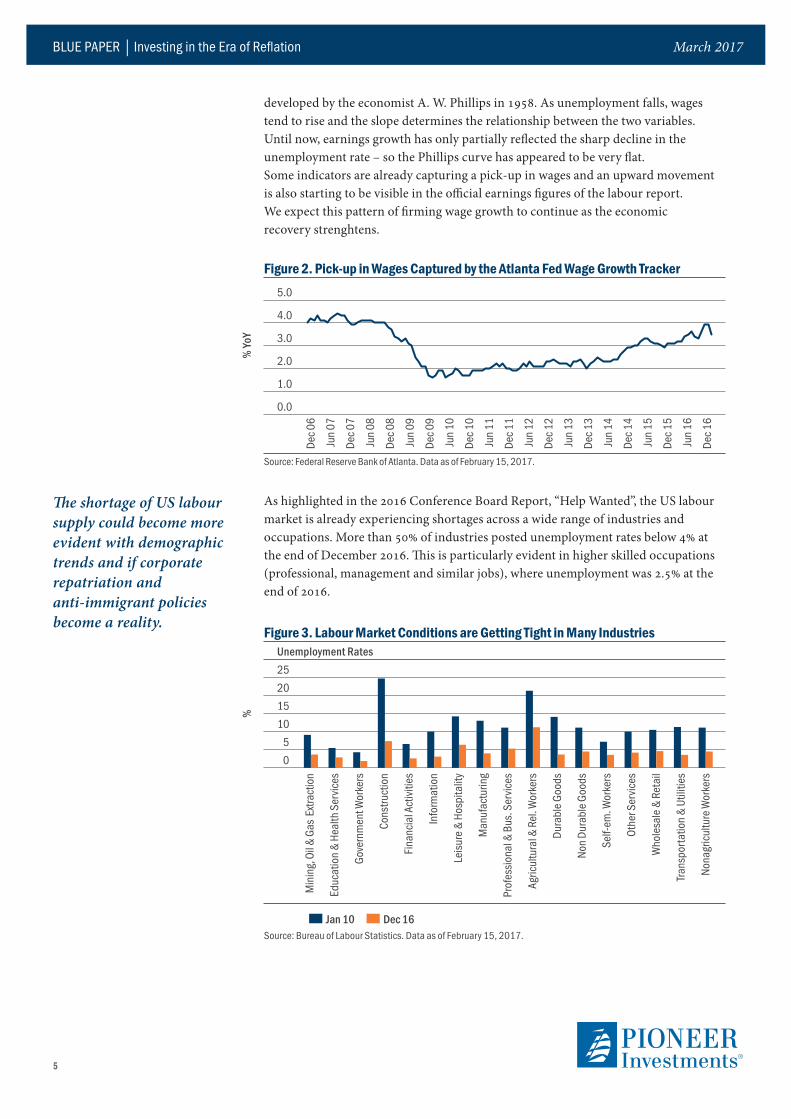

developed by the economist A. W. Phillips in 1958. As unemployment falls, wages tend to rise and the slope determines the relationship between the two variables. Until now, earnings growth has only partially reflected the sharp decline in the unemployment rate – so the Phillips curve has appeared to be very flat. Some indicators are already capturing a pick-up in wages and an upward movement is also starting to be visible in the official earnings figures of the labour report. We expect this pattern of firming wage growth to continue as the economic recovery strenghtens.

As highlighted in the 2016 Conference Board Report, “Help Wanted”, the US labour market is already experiencing shortages across a wide range of industries and occupations. More than 50% of industries posted unemployment rates below 4% at the end of December 2016. This is particularly evident in higher skilled occupations (professional, management and similar jobs), where unemployment was 2.5% at the end of 2016.

The shortage of US labour supply could become more evident with demographic trends and if corporate repatriation and anti-immigrant policies become a reality.

Figure 2. Pick-up in Wages Captured by the Atlanta Fed Wage Growth Tracker5.0

4.0

3.0

2.0

1.0

0.0

Source: Federal Reserve Bank of Atlanta. Data as of February 15, 2017.

% Yo

Y

Dec 0

6

Jun 0

7

Dec 0

7

Jun 0

8

Dec 0

8

Jun 0

9

Dec 0

9

Jun 1

0

Dec 1

0

Jun 1

1

Dec 1

1

Jun 1

2

Dec 1

2

Jun 1

3

Dec 1

3

Jun 1

4

Dec 1

4

Jun 1

5

Dec 1

5

Jun 1

6

Dec 1

6

Figure 3. Labour Market Conditions are Getting Tight in Many IndustriesUnemployment Rates25201510 5 0

Jan 10 Dec 16Source: Bureau of Labour Statistics. Data as of February 15, 2017.

Mining, Oil &

Gas Extraction

Education &

Health Services

Gove

rnm

ent W

orke

rs

Construction

Financial Activities

Info

rmat

ion

Leisu

re & Hospitality

Man

ufac

turin

g

Professio

nal & Bus. Services

Agricultural & Rel. W

orkers

Durable G

oods

Non D

urable Goods

Self-em

. Workers

Othe

r Ser

vices

Wholesale & Retail

Transporta

tion &

Utilities

Nonagricu

lture Workers

%

BLUE PAPER │ Investing in the Era of Reflation March 2017

6

The repatriation of US business and focus on infrastructure spending, as promised by President Trump, are forces that could potentially put additional pressure on the US labour market and on wages. Trends that will likely be exacerbated by demographic factors (retirement of baby boomers) and restrictive policies on immigration.

We believe that the evolution of wage inflation will be particularly important in 2017 in determining Fed policy and the velocity of interest rate adjustments.

The Fed could be forced to act more quickly and aggressively than expected.

In the last twenty years, there has been a strong relationship between unit labour cost increases and the Fed fund rates, which weakened in the aftermath of the Great Financial Crisis. Now that economic conditions are normalising and wage inflation is picking up, we expect the Fed to be more willing to stop the economy from overheating, with the risk that the market will start to reprice a more aggressive Fed policy in the coming months.

Driver # 2. Rising Commodity and Oil Prices The rise in oil prices is producing a strong base effect in energy inflation; inflation forecasts are on the rise not only in the US, but also in other areas which are at a different stage of the economic cycle, notably in the Eurozone and Japan. We expect the current uptrend in oil prices to continue as the world is currently experiencing a small supply shock – triggered by the production cuts agreed between OPEC and non-OPEC producers. On the demand side, a sound economic outlook for developed markets is consistent with a rising demand for oil that should keep it well supported in 2017. Our forecast for oil prices is for 60 USD per barrel at the end of 2017, with a limited risk of a spike towards 70/80 USD per barrel. The significant potential of US onshore oil production should provide a cap to avoid oil prices overshooting.

We expect other commodity prices to remain supported by firmer global demand, should the Chinese recovery stay on track, with oil and metals set to outperform agricultural commodities. This trend is also consistent with the strong broad-based rebound in the manufacturing sector, as illustrated by the chart below.

We expect the current uptrend in oil prices to continue as the world is currently experiencing a small supply shock and increasing demand.

Figure 4. Fed Fund Rates and Unit Labour Costs16

12

8

4

0

-41997 2002 2007 2012 2017

Business Sector: Unit Labour Cost (LS) Fed Fund Target Rate (RS)Source: Pioneer Investments, BLS. Data as of February 15, 2017.

% C

hang

e, 1

6 Qu

arte

rs 8%

6%

4%

2%

0%

BLUE PAPER │ Investing in the Era of Reflation March 2017

7

We observe that the pass-through of commodity price increases to factory inflation has generally been mild, although quite widespread.

Producer price inflation is becoming a widespread phenomenon, generating further pressure on consumer inflation.

The movement is appreciably global and it is upwardly-oriented in many countries, across different areas. In China, for example, higher input costs have squeezed manufacturers and are generating inflation in the industrial sector, creating another potential force for price increases. The rise of commodity prices, combined with strong currency depreciation, is also creating significant cost-side pressures in the UK.

Driver # 3. Loose Fiscal Policy Transmission channels through which fiscal policy affects the economy are multiple and complex.According to neoclassical economic theory, fiscal stimulus shifts aggregate demand higher as public expenditure is a ‘demand’ component; if fiscal stimulus is implemented via tax cuts, which increase disposable income, the shift of aggregate demand comes from an increase in consumption. Rising aggregate demand implies a more rapid rate of growth for employment (wage pressures) and GDP. Prices go up and inflation will be higher, the closer the economy is to full employment. In this framework, interest rates will tend to rise to balance savings and investments.

Figure 5. US Manufacturing PMI and Industrial Metals180

160

140

120

100

80

ISM Manufacturing PMI SA (RS) BBG Industrial Metals (LS)Source: Bloomberg. Data as of February 15, 2017.

Jan 1

3

Apr 13

Jul 13

Oct 1

3

Jan 1

4

Apr 14

Jul 14

Oct 1

4

Jan 1

5

Apr 15

Jul 15

Oct 1

5

Jan 1

6

Apr 16

Jul 16

Oct 1

6

Jan 1

7

57555351494745

Figure 6. Producer Prices (YoY) 12%

8%

4%

0%

-4%

-8%

-12%

China UK US Eurozone JapanSource: Bloomberg, data as of February 15, 2017.

Jan-11

Apr-1

1Jul-11

Oct-1

1Jan-12

Apr-1

2Jul-12

Oct-1

2Jan-13

Apr-1

3Jul-13

Oct-1

3Jan-14

Apr-1

4Jul-14

Oct-1

4Jan-15

Apr-1

5Jul-15

Oct-1

5Jan-16

Apr-1

6Jul-16

Oct-1

6Jan-17

BLUE PAPER │ Investing in the Era of Reflation March 2017

8

But higher interest rates discourage private investment (the crowding out effect of public expenditure).

When considering open economies with flexible exchange rate regimes, fiscal policy could also have an impact on currencies. Capital inflows driven by higher interest rates could put pressure on the currency and have an effect on a country’s competitiveness.

Whatever effect prevails, and whatever the size of the fiscal multipliers, depends on the propensity to consume and on corporates’ propensity to invest in the growth creation potential of public projects. Having the necessary fiscal space will be crucial for an economy willing to adopt expansive fiscal policy, in order to avoid unpleasant unsustainability issues regarding public debt.

In our macroeconomic outlook we have pointed out that in 2017 we will likely see a shift from monetary to fiscal expansion, albeit varying across different countries. The area where fiscal policy will likely be most active will be the US.

At this point, it is difficult to sketch the possible impact of Trumponomics; Trump’s set of priorities point to rising infrastructure investment, cutting corporate taxes and personal income taxes, more forcefully protecting domestic production and deregulating the economy.

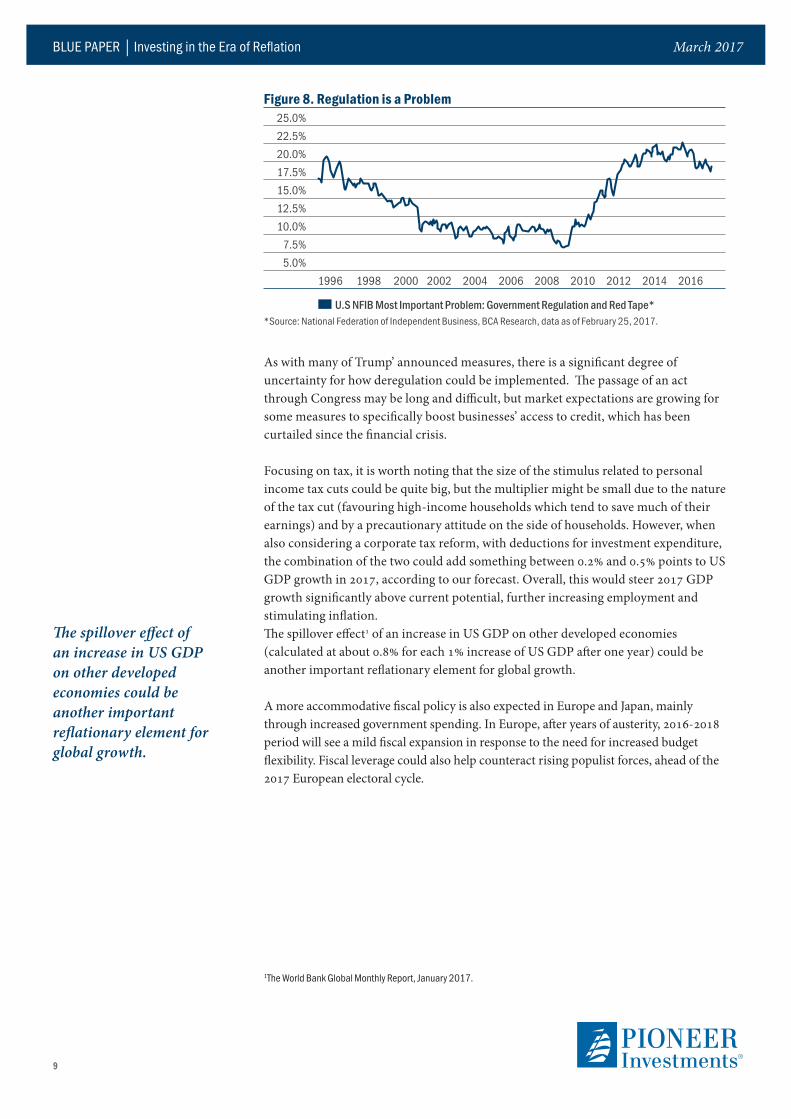

Deregulation is, in theory, a powerful growth-enhancing tool. According to NFIB (National Federation of Independent Business) research, small business owners rank unreasonable government regulation as their second most important problem, after taxes.

Fiscal stimulus can have a significant impact on US GDP potential growth, and be inflationary through consumption growth.

Figure 7. Main Implications of Fiscal Expansion on the Economy

Earnings improvement Higher inflation

Higher business and household spending Higher employment

Stronger economic growth Higher fiscal deficit

Fiscal Expansion

Source: Pioneer Investments, for illustrative purpose only, data as of February 15, 2017.

BLUE PAPER │ Investing in the Era of Reflation March 2017

9

As with many of Trump’ announced measures, there is a significant degree of uncertainty for how deregulation could be implemented. The passage of an act through Congress may be long and difficult, but market expectations are growing for some measures to specifically boost businesses’ access to credit, which has been curtailed since the financial crisis.

Focusing on tax, it is worth noting that the size of the stimulus related to personal income tax cuts could be quite big, but the multiplier might be small due to the nature of the tax cut (favouring high-income households which tend to save much of their earnings) and by a precautionary attitude on the side of households. However, when also considering a corporate tax reform, with deductions for investment expenditure, the combination of the two could add something between 0.2% and 0.5% points to US GDP growth in 2017, according to our forecast. Overall, this would steer 2017 GDP growth significantly above current potential, further increasing employment and stimulating inflation.The spillover effect1 of an increase in US GDP on other developed economies (calculated at about 0.8% for each 1% increase of US GDP after one year) could be another important reflationary element for global growth.

A more accommodative fiscal policy is also expected in Europe and Japan, mainly through increased government spending. In Europe, after years of austerity, 2016-2018 period will see a mild fiscal expansion in response to the need for increased budget flexibility. Fiscal leverage could also help counteract rising populist forces, ahead of the 2017 European electoral cycle.

1The World Bank Global Monthly Report, January 2017.

The spillover effect of an increase in US GDP on other developed economies could be another important reflationary element for global growth.

Figure 8. Regulation is a Problem25.0%22.5%20.0%17.5%15.0%12.5%10.0% 7.5% 5.0%

1996 1998 2000 2002 2004 2006 2008 2010 2012 2014 2016

U.S NFIB Most Important Problem: Government Regulation and Red Tape**Source: National Federation of Independent Business, BCA Research, data as of February 25, 2017.

BLUE PAPER │ Investing in the Era of Reflation March 2017

10

In Japan, the game changer for fiscal policy has been, in our view, the second Supplementary Budget approved in October 2016 of more than JPY 3 trillion, targeting small and medium enterprises, infrastructure investments and enhanced welfare services. We believe all of these fiscal measures will have a positive effect on global growth and inflation in the coming months.

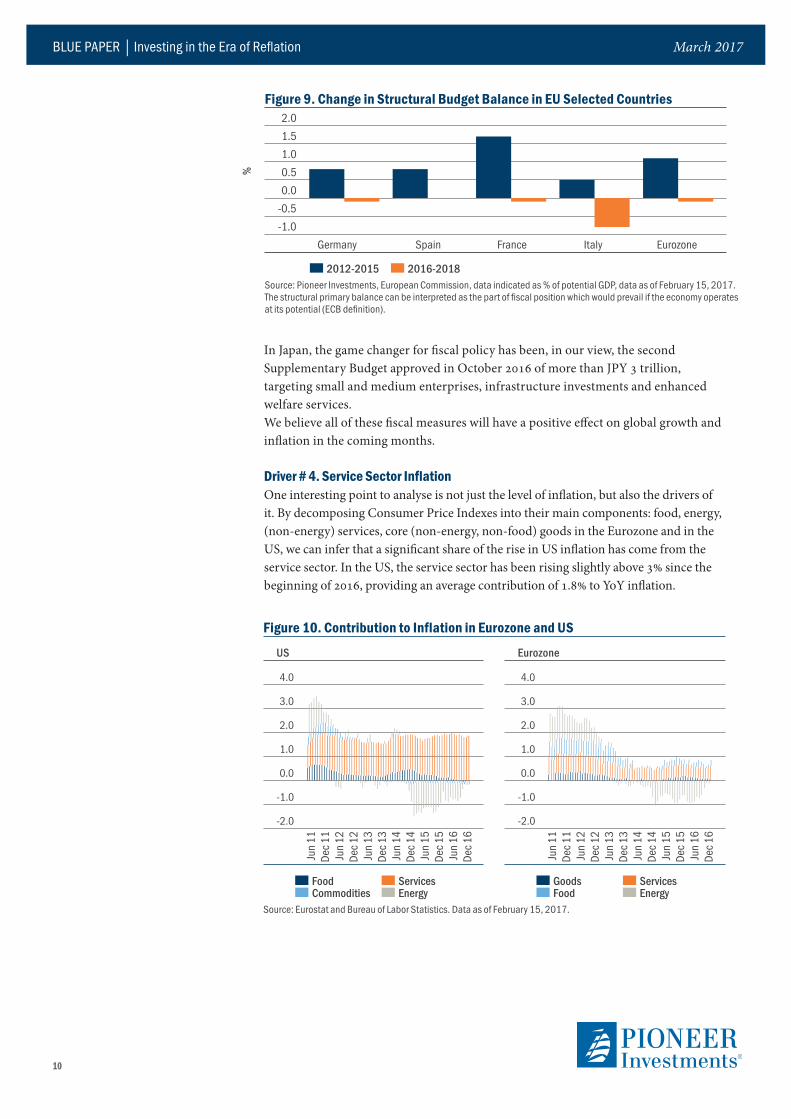

Driver # 4. Service Sector Inflation One interesting point to analyse is not just the level of inflation, but also the drivers of it. By decomposing Consumer Price Indexes into their main components: food, energy, (non-energy) services, core (non-energy, non-food) goods in the Eurozone and in the US, we can infer that a significant share of the rise in US inflation has come from the service sector. In the US, the service sector has been rising slightly above 3% since the beginning of 2016, providing an average contribution of 1.8% to YoY inflation.

Figure 9. Change in Structural Budget Balance in EU Selected Countries 2.0 1.5 1.0 0.5 0.0-0.5-1.0

Germany Spain France Italy Eurozone

2012-2015 2016-2018Source: Pioneer Investments, European Commission, data indicated as % of potential GDP, data as of February 15, 2017. The structural primary balance can be interpreted as the part of fiscal position which would prevail if the economy operates at its potential (ECB definition).

Figure 10. Contribution to Inflation in Eurozone and US

Source: Eurostat and Bureau of Labor Statistics. Data as of February 15, 2017.

4.0

3.0

2.0

1.0

0.0

-1.0

-2.0

Food Services Commodities Energy

4.0

3.0

2.0

1.0

0.0

-1.0

-2.0

Goods Services Food Energy

Jun 1

1Dec 1

1Jun 1

2Dec 1

2Jun 1

3Dec 1

3Jun 1

4Dec 1

4Jun 1

5Dec 1

5Jun 1

6Dec 1

6

Jun 1

1Dec 1

1Jun 1

2Dec 1

2Jun 1

3Dec 1

3Jun 1

4Dec 1

4Jun 1

5Dec 1

5Jun 1

6Dec 1

6

EurozoneUS

%

BLUE PAPER │ Investing in the Era of Reflation March 2017

11

Similarly, in the Eurozone the only non-marginal source of inflation in 2015-2016 has been the service sector, with a relatively stable contribution to overall inflation of around 0.5%. It is interesting to note that inflation in the service sector is mainly an indicator of domestic conditions and is less influenced by external factors, such as commodity/energy prices, so by nature, it’s a relatively stable component of CPI.Within the US service sector, a good portion of the rise in inflation has been due to increases in medical care costs and in housing rental costs, both of which have risen at a higher pace than general inflation and this is expected to be sustained in the next few years.

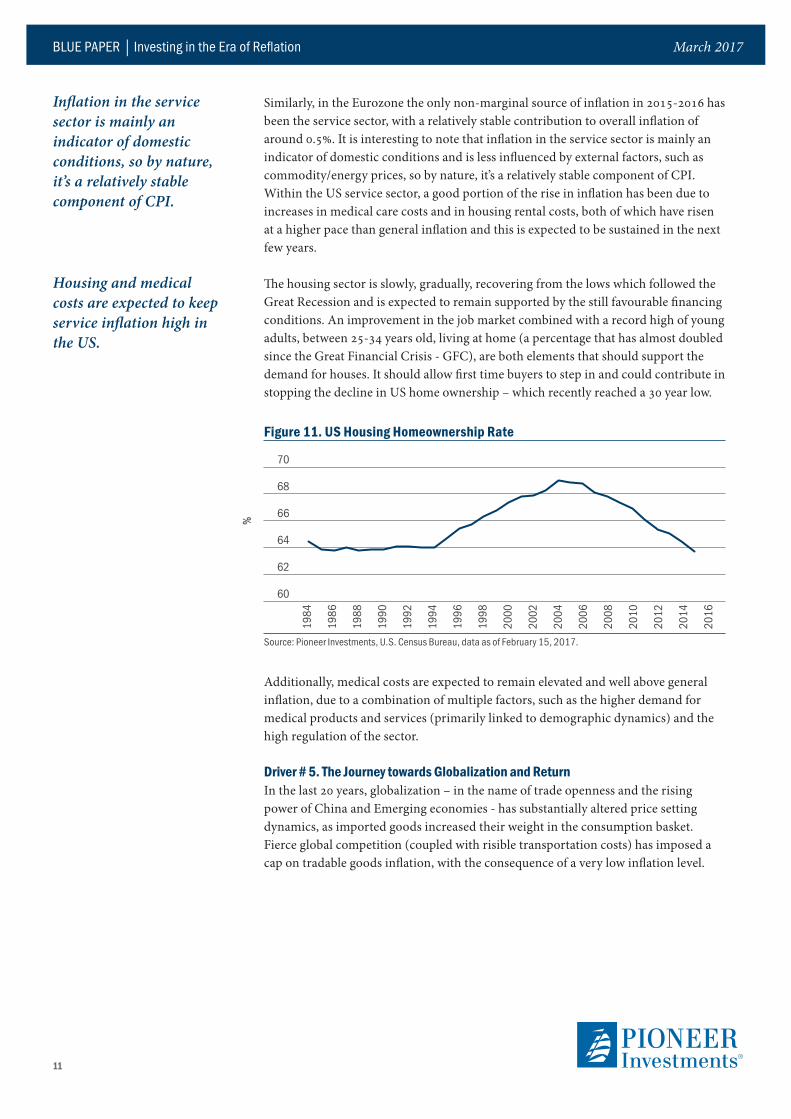

The housing sector is slowly, gradually, recovering from the lows which followed the Great Recession and is expected to remain supported by the still favourable financing conditions. An improvement in the job market combined with a record high of young adults, between 25-34 years old, living at home (a percentage that has almost doubled since the Great Financial Crisis - GFC), are both elements that should support the demand for houses. It should allow first time buyers to step in and could contribute in stopping the decline in US home ownership – which recently reached a 30 year low.

Inflation in the service sector is mainly an indicator of domestic conditions, so by nature, it’s a relatively stable component of CPI.

Housing and medical costs are expected to keep service inflation high in the US.

Additionally, medical costs are expected to remain elevated and well above general inflation, due to a combination of multiple factors, such as the higher demand for medical products and services (primarily linked to demographic dynamics) and the high regulation of the sector.

Driver # 5. The Journey towards Globalization and ReturnIn the last 20 years, globalization – in the name of trade openness and the rising power of China and Emerging economies - has substantially altered price setting dynamics, as imported goods increased their weight in the consumption basket. Fierce global competition (coupled with risible transportation costs) has imposed a cap on tradable goods inflation, with the consequence of a very low inflation level.

Figure 11. US Housing Homeownership Rate

70

68

66

64

62

60

Source: Pioneer Investments, U.S. Census Bureau, data as of February 15, 2017.

1984

1986

1988

1990

1992

1994

1996

1998

2000

2002

2004

2006

2008

2010

2012

2014

2016

%

BLUE PAPER │ Investing in the Era of Reflation March 2017

12

An increased labour integration across countries has also altered wage growth dynamics: companies have access to a much wider and cheaper labour force in order to produce exportable goods and services. The globalization of the labour force has probably contributed to the reduction of bargaining power in setting wages by unions and workers in advanced countries, therefore lowering domestic inflation rates.

However, in our view, there is reason to believe that the peak of globalization is behind us. We are already seeing a fall in the value of global trade in the last three years, accompanied by a rise in the number of trade restrictive measures.

In our view, pick of globalization is behind us, as new nationalist forces emerge almost everywhere.

In the US, Trump’s future trade policies could potentially introduce tariffs, or other kinds of protectionist measures, which could push inflation levels up. Trump’s campaign also fiercely addressed popular concerns regarding the risks of wage competition and job displacement, pledging policies to increasingly manage borders in order to limit labour market integration and to help preserve workers’ bargaining power. The rise of populist/nationalist parties in the Eurozone and the Brexit outcome are all forces that, in our view, will push for protectionism and a domestic focus and will pose a limit to further globalization.

Risks to the Reflation Scenario: What Could go Wrong? As highlighted in the previous pages, our central case is a reflation scenario for the global economy. However, we acknowledge the journey from lowlowflation to reflation will not be risk-free. Equilibrium is still fragile: it’s important that the negative effects of protectionism and rising rates do not displace the benefits of a gradually recovering commodity cycle and healthy wage inflation.

On the fiscal side, Trump’s future policies are still very uncertain; while a clear protectionist agenda has emerged in his first weeks as President, few details have been released about his expansion projects. It is difficult to assess how productive the increased public spending will be and what the impact on GDP of fiscal reforms will be in the medium to long-term.

Equilibrium is still fragile: it’s important that the potential negatives of protectionism and rising rates do not displace the benefits of a gradually recovering commodity cycle and healthy wage inflation.

Figure 12. Global Trade and the Number of Trade Restrictive Measures

Source: Pioneer Investments, WT, CPB World Trade Monitor. Data as at February 15, 2017.

Number of Trade Restrictive Measures

2500

2000

1500

1000

500

0

Mid October Mid October 2010 2016

Global Trade

130

110

90

70

50

30

World Exports World - Value (USD)

2000

2002

2004

2006

2008

2010

2012

2014

2016

Leve

l (20

10 =

100

)

BLUE PAPER │ Investing in the Era of Reflation March 2017

13

Many offsetting components will be at work following any protectionist measures, ranging from possible retaliation policies by damaged commercial partners, to the loss of competitiveness due to a stronger US Dollar.

A radical shift towards protectionism could depress world trade and negatively impacting global growth.

The potential effect of corporate tax cuts could be marginal as many companies are already sitting on hordes of cash and effective tax rates are below statutory levels. US companies could also see their margins eroded by higher labour costs and by higher input costs if their pricing power is not strong enough. Higher interest rates could crowd out any private productive investments and increased mortgage rates could hurt the housing sector recovery.

On the monetary policy side, we have argued for a period of time that its effectiveness is rapidly fading, yet we are convinced that reflationary policies will only succeed if Central Banks manage to prevent economies from overheating (especially in the US) while not incurring any policy mistakes. The gradual approach of the Federal Reserve, as well as the efforts of the European Central Bank and Bank of Japan to achieve medium-term inflation and growth will be crucial in allowing a smooth transition out of the lowlow terrain.

Reflationary policy will succeed if Central Banks will manage to prevent economies from overheating (especially in US) without incurring in policy mistakes.

BLUE PAPER │ Investing in the Era of Reflation March 2017

14

Investing Opportunities in a Reflationary WorldIn the new reflation narrative, it will be crucial, in our view, for investors to diversify their portfolios with asset classes able to benefit from rising inflation.

In periods of inflation surprises, traditional assets may underperform while real assets, inflation-linked bonds and some selective equity sectors have the potential to outperform. In the analysis displayed in Figure 13 we have measured the annual returns of different US-based traditional asset classes and real asset investments in periods of US inflation surprises. These periods have been identified as years when the realized inflation (as measured by the Bureau of Labor Statistics year-on-year change in US consumer prices CPI) has exceeded the inflation expectations forecast the previous year (as measured by the University of Michigan Change In Prices During the Next Year: Median Value).

We believe that investors should be prepared to deal with the new inflation scenario by choosing an active and selective approach in fixed income equity and multi-asset.

As shown in the graph, during periods of inflation surprises real asset-backed investments exhibited the strongest performance on average, outperforming their long-term average (as shown in the bubbles at the bottom of the graph). On the other hand, traditional asset classes such as government bonds, credit, high yield and the overall US equity index tended to underperform compared to their historical average. However within equity, some commodity-driven sectors delivered very good performance.

We believe that in the upcoming reflation scenario, new opportunities are opening for investors with an active and selective approach.

Figure 13. Asset Classes Performances in Periods of Unexpected Inflation35%

30%

25%

20%

15%

10%

5%

0%

Source: Bloomberg. Analysis on monthly data from March 31, 1997 to December 31, 2016. Periods of Inflation Surprise are defined as periods when the University of Michigan Survey of 1-Year Ahead Median Inflation Expectations is lower compared to the actual year-over-year CPI inflation rates reported 12 months later. US Equity = S&P500, US Govt Bond= J.P Morgan GBI US, US IG Credit = Barclays US Aggregate Credit, US HY = Barclays US Corporate High Yield, TIPS =BofA Merrill Lynch US Inflation Linked Treasury, REITS = FTSE EPRA/NAREIT US Index , US Agricultural Equity = S&P500 Agricultural Products Index, N.A.S Nat. Res. Equities = S&P North American Natural Resources Sector, US Energy Equity = S&P500 Energy Index, Commodities = S&P GCSI Commodity Index. All indexes are total return in USD unhedged. Analysis on monthly data. Data represents past performance, which is no guarantee of future results.

TRADITIONAL INVESTMENTS

REAL ASSET BACKED INVESTMENTS

Aver

age 1

Year

Ret

urn i

n Per

iods

of

Infla

tion S

urpr

ise

Diffe

renc

e vs

Aver

age o

n Al

l Per

iods

-1.2% -0.1% -1.2% -1.8% +2.3% +1.5% +6.2% +13.1% +11.2% +24.8%

US IG Credit

US Govt Bonds

US HY

US Eq

uity

US TIPS

US REITS

US Agricu

lt. Eq

uity

N.A.

Nat

.Res

. Equ

ity

US En

ergy Eq

uity

Commodities

BLUE PAPER │ Investing in the Era of Reflation March 2017

15

Fixed Income: Inflation Linked Bonds and Short Duration to Protect Portfolios1. Inflation has traditionally been bond investors’ big enemy. Is this still the case? Nominal rates were seen as being more attractive when investors were worrying about deflation and a stronger downturn in growth. Now, that the economic scenario is improving, we do not expect a sharp pick-up in inflation, especially in Europe where there are only few signs of domestically-generated inflation. However, with interest rates so low, even a small pick-up in inflation would easily push bond returns into negative territory. That said, after years of deflation concerns, a tame inflation environment would be welcome, it would generate steeper yield curves and create more incentive for long-term investments.

2. What is the role for Central Banks’ policy in the next twelve months?We are at a point where Central Banks are gradually stepping back from being the potential growth/inflation engine and they are now leaving room for Governments to step in. By acknowledging the reduced effectiveness of marginal increases to the monetary base and the economic costs experience of negative interest rates, we think that Central Banks have averted what was a major concern for us over the last few years: the supremacy of their policies. With fiscal policies becoming simulative in most developed markets, notably Trump’s pledge for a strong fiscal boost, we expect a more favourable and balanced macro policy framework which could bring a gradual normalization of the yield curves.

3. What segments of fixed income are expected to outperform in a rising inflation environment? In a rising inflation environment, we believe it is worth considering inflation linked bonds versus corresponding nominal bonds in order to avoid duration risk. For this year, we believe that investors should consider short duration bonds in their portfolios. In the US, we see more space for the medium part of the curve to cheapen, as investors could start to incorporate expectations for further rate hikes once the next one materializes. In the Eurozone, we expect some steepening of yield curves, as higher inflation expectations will be gradually be incorporated in long-term yields. That said, political risk (mainly linked to French elections) and news flow will probably continue to dominate in the next few months, altering the shape of yield curves.

4. Can inflation linked bonds be considered a global opportunity for 2017? How much of the higher inflation expectations is already priced in the market? When we look at valuations, the market is still very conservative for near-term inflation projections. Short dated inflation break-evens2 in the Eurozone offer cheap protection to further inflation upside, in our view. The market is not pricing in a return to 2% inflation for the next 30 years, underlining a full “Japanification”3 of the Eurozone term structure.

2Breakeven inflation is the difference between the nominal yield on a fixed-rate investment and the real yield on an inflation-linked investment of similar maturity and credit quality.3A long period of sluggish growth and low inflation as in Japan’s experience.

We are at a point where Central Banks are gradually stepping back from being the potential growth/inflation engine and they are leaving room for Governments to step in.

We still see value in inflation linked bonds. For this year, we believe that investors should consider short duration bonds in their portfolios.

Cosimo Marasciulo Head of Fixed Income, Europe

This material reflects the opinions of the above author at the time of writing.

BLUE PAPER │ Investing in the Era of Reflation March 2017

16

If we plot the European Inflation Swap Curve – which considers the inflation priced in by the swap market for each maturity – we observe a wide gap for short and medium-term maturities between what is priced in and the ECB’s target. We think there is value in this segment.

We also see opportunities in inflation break-evens in the US. We have already seen some domestic drivers for price increases; this could push inflation above 2%, which is currently the level of inflation discounted by the market for the next 10 years.

Figure 14. EU Break Even Inflation Swap Curve Versus the ECB Inflation Target2.4

2.2

2.0

1.8

1.6

1.4

1.2

1.0

0.8

0.6

0.4

0.2

0.0

ECB Inflation Target Break-Even Inflation Swap CurveSource: Bloomberg, data as March 2, 2017.

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25 26 27 28 29 30

Infla

tion (

%)

Time to Maturity (Years)

BLUE PAPER │ Investing in the Era of Reflation March 2017

17

US Equities: Selective with Mild Inflation 1. Inflation expectations have increased in the US: how do you expect US equity to perform in a reflation scenario? Which sector could benefit?It depends on how much inflation increases and the causes of this. A modest increase in inflation, driven by an increase in real GDP growth, could benefit equity markets, especially cyclical sectors such as materials, industrials and financials. A significant increase in inflation, however, would likely cause the Fed to become more aggressive in raising interest rates. This could cause economic growth to slow and put pressure on equities. In addition, inflation driven by increased trade protectionism would not be viewed positively, as the increase in inflation would be accompanied by lower real spending, slower growth, reduced earnings and valuations.

2. Equities and yields: do you believe rising interest rates could hurt equities through increased borrowing costs or could they support the equity market by being a way to increase corporate pricing power? Higher interest rates increases the cost of capital for both debt and equity. However, some sectors, such as financials, should benefit from higher interest rates as net interest margins widen. In addition, the extent to which higher interest rates are a function of higher GDP growth, earnings may grow faster, benefitting equities. Since the election, both interest rates and equities have increased.

The strong positive correlation4 between equities and bonds which characterized the Quantitative Easing era already seems to be weakening.

Since the election, both interest rates and equities have increased. Whether this relationship holds for all of 2017 depends in part on the magnitude of rate increases going forward.

4The degree of association between two or more variables; in finance, it is the degree to which assets or asset class prices have moved in relation to one another. Correlation is expressed by a correlation coefficient that ranges from -1 (never move together) through 0 (absolutely independent) to 1 (always move together).

Andrew AchesonPortfolio Manager US Equities, Senior Vice President

This material reflects the opinions of the above author at the time of writing.

A modest increase in inflation driven by an increase in real GDP growth could benefit equity markets, especially cyclical sectors such as materials, industrials and financials.

Figure 15. Equities can Sustain Higher Interest Rates

500

450

400

350

300

250

Global Aggregate Bond Index (LHS) 3Y Rolling Correlation Bonds Equity (RHS)Source: Bloomberg, data as of February 15, 2017.

Glob

al A

ggre

gate

Bon

d In

dex

3Y Rolling Correlation

0.80

0.60

0.40

0.20

-

-0.20

-0.40

-0.60

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

BLUE PAPER │ Investing in the Era of Reflation March 2017

18

3. What will the drivers for US equity be, now that the positive election implications seem to be price-in? Interest rates, earnings growth and valuations are the three biggest drivers of equity performance. There are a number of risk factors that are also likely to affect performance, however, most notably public policy related to taxes, healthcare, and trade could be an influence. The equity market may be forward looking, but it is important to also consider that it is rarely patient. Disappointment in the speed of policy change could be reflected in near-term weakness. 4. How do you think US equities would react to rising protectionism? Which sectors could be the winners and the losers? Trade barriers could benefit companies that produce and sell goods and services in the US, such as domestically-focused consumer companies. However, trade barriers would likely hurt US exporters as well as US companies that source goods and services from other countries, such as IT outsourcing firms. Overall, trade barriers would likely have a negative impact on the global economy and global equities. For this reason, we think a radical change in US trade policy is unlikely, though in an era of policy uncertainty it is very important to consider that this could occur.

Disappointment in the speed of policy change could be reflected in near-term weakness.

BLUE PAPER │ Investing in the Era of Reflation March 2017

19

European Equities: Value with Quality1. Do you believe European Equity will be a beneficiary of a reflationary environment?As a general statement – yes. Under normal circumstances investors could expect rising inflation and rising (US) bond yields would be supportive of European equities and we do believe this market climate will provide support to European risk assets this year. The financial sector (Banks, Insurance and Diversified Financials) and commodity-related sectors are typically the most positively impacted by rising inflation, the opposite happens for Healthcare and Utilities.That said, the landscape is far from simple. Investors should closely monitor how global growth is converted into better European earnings, as this will be the key driver of European equities going forward. The market is undeniably fairly valued at this point and, without clear earnings growth to act as a catalyst, will likely move sideways at best. This is particularly relevant given the number of political events on the horizon in Europe this year. The market needs the support of fundamental drivers for investors to look through the political noise and allow for upside. The good news is that we are already beginning to witness this trend with pleasing 2016 Q4 earnings releases to date. Interestingly, although positive earnings per share revisions in Europe are clearly exceeding those of the US, the European market continues to lag the US. If this confirmation of earnings growth continues through 2017, we may experience some closure of this gap. Even so, we believe consensus expectations for earnings growth in Europe this year are a little too high, at around 16%. We prefer to be more conservative. Our house view is that the Eurozone will experience +8.4% EPS growth while Pan-European markets will be a little higher at +9.5%. This improved number is caused by the positive impact from the fall in the British Pound for international companies listed in the UK. If our forecasts prove correct, the market may perform in line with earnings growth.

2. What about value investing? Do you believe that the outperformance of value areas of the market will continue?The European value index has underperformed the growth index and, since August 2016, showed a strong relationship with US 10 Y bond yield. As GDP growth and bond yields continue to move higher, value areas of the market may again experience better performance in 2017, particularly if the positive support mentioned above translates into earnings growth.

Diego FranzinHead of Equity - Europe Executive Vice President

This material reflects the opinions of the above author at the time of writing.

Although positive earnings per share revisions in Europe are clearly exceeding those of the US, the European market continues to lag the US. We may experience some closure of this gap in 2017 if earnings momentum continues.

Figure 16. MSCI Europe Value and Growth Ratio vs 10 Year Treasury Bond Yield

1.2

1.1

1.0

0.9

0.82012 2013 2014 2015 2016 2017

US 10Y Yield (RS) Ratio Value vs Growth (LS)Source: Bloomberg, data as of February 15, 2017.

Ratio

3.5

3.0

2.5

2.0

1.5

1.0

%

BLUE PAPER │ Investing in the Era of Reflation March 2017

20

That said, we believe investors will need to be savvy going forward to capture upside value areas offered by the market and will need to put the fundamentals of these companies under greater scrutiny. One of the risks to “value” investing is that investors are just looking at the “price” of the asset and not paying due consideration to the actual “value” of that company. Sometimes companies are considered “value” for a reason, because their business model is broken. We believe the approach should be to identify viable companies and only invest when the price represents a cushion to what the actual “value” of the company should be. In our view, the “sweet spot” in 2017 will involve identifying those companies which offer significant upside (value) but who can also demonstrate the ability to deliver earningsgrowth. This is more likely to be on a stock specific basis than focusing on one particular sector.

3. How do you believe investors should approach investing in European Equity in 2017? During 2016, our key message was for having a “balanced” approach and although our stance has become more constructive, we remain of that view today. We acknowledge that value areas of the market appear more attractive, but caution that uncertainty is still high. Investors should therefore continue to seek quality and reliability during times of market stress. We believe it will continue to be important to find a balance between “quality at the right value” and “value with a certain level of quality”. We expect a further rotation into equity is likely in the global reflation scenario, but believe investors will look for evidence of earnings growth to support this. As has been the case in 2016, investors should participate in these trends through single stocks rather than on a sector or style bias. A good example, in our view, is the financial sector. This should be a clear beneficiary of a more supportive backdrop and yield curve steepening. But in this case it will also be important to focus on those companies with financial strength and stability that will be able to capture the trend and convert it to higher profitability. Again quality stock selection should prevail.

4. What are the risks for European investors in 2017?Our one concern remains the political agenda (in Europe and, more recently, further afield). While investors can overlook this for a certain amount of time, it leaves the market vulnerable to external shocks. Given the magnitude of the rally we have experienced in the last 2 months (post Trump’s election), we should expect a pause or slight pullback before the acceleration continues. As we have experienced nearly every year since the Global Financial Crisis, periods of drawdown should be expected and investors should be prepared to absorb these periods of volatility and accumulate equity positions for the long term at more attractive prices.

We expect a further rotation into equity is likely in the global reflation scenario, but believe investors will look for evidence of earnings growth to support this. Quality stock selection should prevail.

BLUE PAPER │ Investing in the Era of Reflation March 2017

21

Multi-Asset: Focus on Real Assets and Diversification1. From a Multi-Asset perspective, where do you see value in a reflation scenario?According to our models, we are currently experiencing a period of asset reflation with possible elements of a late cycle scenario. Here the favourite asset classes have historically been global equities, credit and commodities. In the current environment, we need to consider whether the long bull market, induced by Central Banks’ unconventional policies, has distorted market valuations.

We think credit still offers some opportunities in relative terms, especially on higher yielding securities. The asset class remains supported by the ongoing search for income and, in the Eurozone, by the ECB’s bond purchasing programme. However, we are aware that valuations look expensive in a possible reflationary scenario characterized by higher interest rates, the over-crowded investment grade segment in particular. Within HY, energy and materials look less vulnerable than one year ago thanks to the commodity recovery.

We are cautiously positive on EM bonds, with a preference for hard currency debt, while being wary of possible pressures on EM currencies from the strong US dollar. In the short term, however, headwinds to the asset class are strong because of the Fed’s effort to cool down mounting inflation pressures making the Dollar Trade Weighted Index stronger.On the equity side, we have a positive view on a cyclical earnings recovery, favouring US and Japan and with a constructive view on European Equity. On EMs, we prefer a country specific approach, favouring countries like India that less vulnerable to external threats.

Francesco SandriniHead of Multi Asset Securities Solutions

This material reflects the opinions of the above author at the time of writing.

We are currently experiencing a period of asset reflation with possible elements of a late cycle scenario. Here the favourite asset classes have historically been global equities, credit and commodities.

Figure 17. Earnings Per Share Growth (YoY) Forecasts, Horizon Dec’179%8%7%6%5%4%3%2%1%0%

US Eurozone Japan Emerging Markets

Q3 16 Feb-17Source. Pioneer Investments forecast and elaborations on S&P Capital IQ data as of February 15, 2017.

BLUE PAPER │ Investing in the Era of Reflation March 2017

22

Sector-wise, the reflationary environment should be supportive for financials: the steepening of curves supports the return on equity. Less litigation, expanding credit and a peak in the regulation wave could also boost the return of equity and, on the other side, less uncertainty would lower the cost of equity. We tend to prefer cyclical sectors - energy, materials, financials - while maintaining a cautious stance on interest rate sensitive sectors, such as utilities, telecoms, staples and real estate.

2. As mentioned above, your base scenario for 2017 is constructive on commodities. Which assets could be favoured in this context?Most commodity fundamentals have improved and prices for some commodities are already anticipating widening deficits in supply demand dynamics. Global demand for energy and industrial metals should remain supported by the fiscal expansionary plans in EM and DM economies alike.

A boost for infrastructure spending in the US and in EMs - LATAM especially - should support demand for metals. Zinc inventories are already declining, while Global demand for Copper and Nickel is rising. We are more cautious on Global Crude Oil as the market has discounted the productions cut agreed by OPEC (1.2mln barrel/d) and major Non-OPEC producers and we don’t foresee a strong upside from current levels. In a context of a stable/positive commodity outlook, opportunities could be found in EM commodity currencies, which our internal quantitative models suggest are attractive in terms of valuation - such as the Russia Ruble and the Chilean Peso.

3. How can multi-asset investors deal with changing inflation expectations? In periods of inflation surprises, real assets can offer interesting inflation protection opportunities. Here we can include inflation-linked bonds, which offer good diversification5 and inflation protection; commodities or specific instruments such as MLPs – Master Limited Partnerships, which benefit from more stable oil and gas prices and infrastructure spending. Despite their historical outperformance in periods of inflation surprises, we prefer to stay cautious on REITs because the search for income induced by abundant Central Bank liquidity has led their valuation at historically high levels.

We monitor gold as this can be used as a “tactical hedge”, as well as an additional source of diversification. This is an asset which will likely rebound in potential periods of declining real interest rates – for example if markets become impatient and frustrated at not seeing the fruits of reflation.

5Diversification does not guarantee a profit or protect against a loss.

Global demand for energy and industrial metals should remain supported by the fiscal expansionary plans in EM and in DM economies alike.

BLUE PAPER │ Investing in the Era of Reflation March 2017

23

Important InformationThe MSCI information may only be used for your internal use, may not be reproduced or redisseminated in any form and may not be used as a basis for or a component of any financial instruments or products or indices. None of the MSCI information is intended to constitute investment advice or a recommendation to make (or refrain from making) any kind of investment decision and may not be relied on as such. Historical data and analysis should not be taken as an indication or guarantee of any future performance analysis, forecast or prediction. The MSCI information is provided on an “as is” basis and the user of this information assumes the entire risk of any use made of this information. MSCI, each of its affiliates and each other person involved in or related to compiling, computing or creating any MSCI information (collectively, the “MSCI Parties”) expressly disclaims all warranties (including, without limitation, any warranties of originality, accuracy, completeness, timeliness, non-infringement, merchantability and fitness for a particular purpose) with respect to this information. Without limiting any of the foregoing, in no event shall any MSCI Party have any liability for any direct, indirect, special, incidental, punitive, consequential (including, without limitation, lost profits) or any other damages. (www.mscibarra.com).

Unless otherwise stated, all information contained in this document is from Pioneer Investments and is as of February 15, 2017.

The views expressed regarding market and economic trends are those of the author and not necessarily Pioneer Investments, and are subject to change at any time based on market and other conditions and there can be no assurances that countries, markets or sectors will perform as expected. These views should not be relied upon as investment advice, as securities recommendations, or as an indication of trading on behalf of any Pioneer Investment product. There is no guarantee that market forecasts discussed will be realized or that these trends will continue. Investments involve certain risks, including political and currency risks. Investment return and principal value may go down as well as up and could result in the loss of all capital invested.

This material does not constitute an offer to buy or a solicitation to sell any units of any investment fund or any service.

All investments involve risks. You should consider your financial needs, goals, and risk tolerance before making any investment decisions.

Pioneer Investments is a trading name of the Pioneer Global Asset Management S.p.A. group of companies.

Date of First Use: March 6, 2017.

Follow us on:

www.pioneerinvestments.com

DISCOVER OUR INVESTMENT VIEW

Claudia BertinoHead of Financial Communication, Global Strategy and Marketing

Laura FiorotFinancial Communication Specialist,Global Strategy and Marketing

Giuseppina Marinotti Financial Communication Specialist, Global Strategy & Marketing

EDITORIAL TEAM

INSIGHT

Spotlight on Global Asset Classes

Global Asset Allocation ResearchFebruary 2017

1

Since the beginning of the year, three main themes have emerged, which may have an impact on asset allocation. The first is the strong momentum in economic data, in developed markets (DMs), confirming that reflation policies are working - not just as potential, but that they are already penetrating the real economies. In the US, businesses have continued to create jobs at a slow but steady pace and wage inflation is finally materializing. In Euroland, even with help from rising energy prices, inflation has surprised on the upside and progress in the labour market is taking place. A second theme to consider is the increased uncertainty of Trumponomics. The pledged fiscal boost and infrastructure expenditure package have not been released or even outlined yet. Fiscal reform could be moved towards the end of the year, with effects visible only in 2018. Much of the President’s attention has been dedicated to US borders and protectionism. We will monitor future political developments to assess if Trumponomics will be as powerful as the markets have started to price in. Lastly, European political risk: France’s elections are perceived as a high risk factor, as a Le Pen victory would put the Euro and Euroland at risk. This is a low probability event, but, after the sequence of unexpected outcomes in 2016, markets are already exhibiting nervousness, for example through higher government bond spreads or higher Credit Default Swaps on the European investment grade market. In this setting, we think investors should seek to exploit growth opportunities through US and Japanese equities. European equities are also attractive

in this environment, but Brexit and the outcome of the elections in France constitute an element of uncertainty and so we are more cautious here. In fixed income, we think yield curves will tend to steepen to incorporate a higher inflation premium at the long end. We are still constructive on inflation-linked bonds in the US and in Euroland. Credit valuations in DMs are expensive (especially in the high quality segment) but are expected to outperform sovereign bonds. Because of the still present headwinds in the global economy, and because financial markets have raised the bar and disappointment risk is higher, we believe that broadening sources of diversification and incorporating efficient hedging strategies will continue to be crucial to try to protect investors’ assets.

MULTI-ASSET THEMES MULTI-ASSET THEMES Actionable Investment Ideas

February 2017Improving MomentumWith reflationary policies at work, developed markets are experiencing a broad-based pick-up in economic activity and more solid inflation dynamics. Central Bank divergences persist as economies find themselves in different phases of the cycle.

Complacency RiskWith higher expectations, there is more room for disappointment. Trump’s fiscal reforms could be delayed, his protectionist policies could damage the global economy. We therefore like riding the reflationary wave with a strong focus on hedging (gold and US dollar).

Equity Likes Fiscal BoostExpectations for further fiscal stimulus, especially in the US but also in Japan and (less so) in the Eurozone, support investors’ rotation from government bonds to equities, especially in DMs. In EMs, selection remains paramount in equity and fixed income.

DMs: Developed Markets; EMs: Emerging Markets.A credit default swap (CDS) is a financial swap agreement that the seller of the CDS will compensate the buyer in the event of a loan default or other credit event.Diversification does not guarantee a profit or protect against a loss.

There are increasing signs that reflation policies are working and that they are already penetrating the real economy.

Source: Pioneer Investments, Bloomberg, Markit, February 21, 2017. Levels above 50 indicate expansion of the manufacturing sector.

Sound Business Confidence

Playing Economic Acceleration

4648505254565860

US Man. PMI UK Man. PMIEurozone Man. PMI Japan Man. PMI

Leve

l

REF-1046

Related Documents