April 2016 Market Commentary 02 Commodity Performance BCOM 08 Roll Select 09 Historical 10 Contribution to Return & Weights 11 Commodity Volatility Realized 12 Implied 13 Historical Realized 14 Commodity Correlation Composites 15 Singles 16 US CPI Indices 17 Country CPI 18 Country GDP 19 Commitment of Traders Report Monthly Notional Change & Correlation 20 Historical Net Positions 21 Commodity Inventories & Sales Monthly Change & Correlation 23 Historical Levels 24 Commodity ETP Flows 26 Term Structures 27 Research Dashboards (BI) 29 Bloomberg Cheat Sheet 30 Contact us: <Help> <Help> on the Bloomberg Professional service 1-212-617-5020 [email protected] TABLES & CHARTS (BCOM) BLOOMBERG COMMODITY INDEX

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

April 2016Market Commentary 02Commodity Performance BCOM 08 Roll Select 09 Historical 10Contribution to Return & Weights 11Commodity Volatility Realized 12 Implied 13 Historical Realized 14Commodity Correlation Composites 15 Singles 16 US CPI Indices 17 Country CPI 18 Country GDP 19Commitment of Traders Report Monthly Notional Change & Correlation 20 Historical Net Positions 21Commodity Inventories & Sales Monthly Change & Correlation 23 Historical Levels 24Commodity ETP Flows 26Term Structures 27Research Dashboards (BI) 29Bloomberg Cheat Sheet 30

Contact us:<Help> <Help> on the Bloomberg Professional [email protected]

TABLES & CHARTS(BCOM)BLOOMBERG COMMODITY INDEX

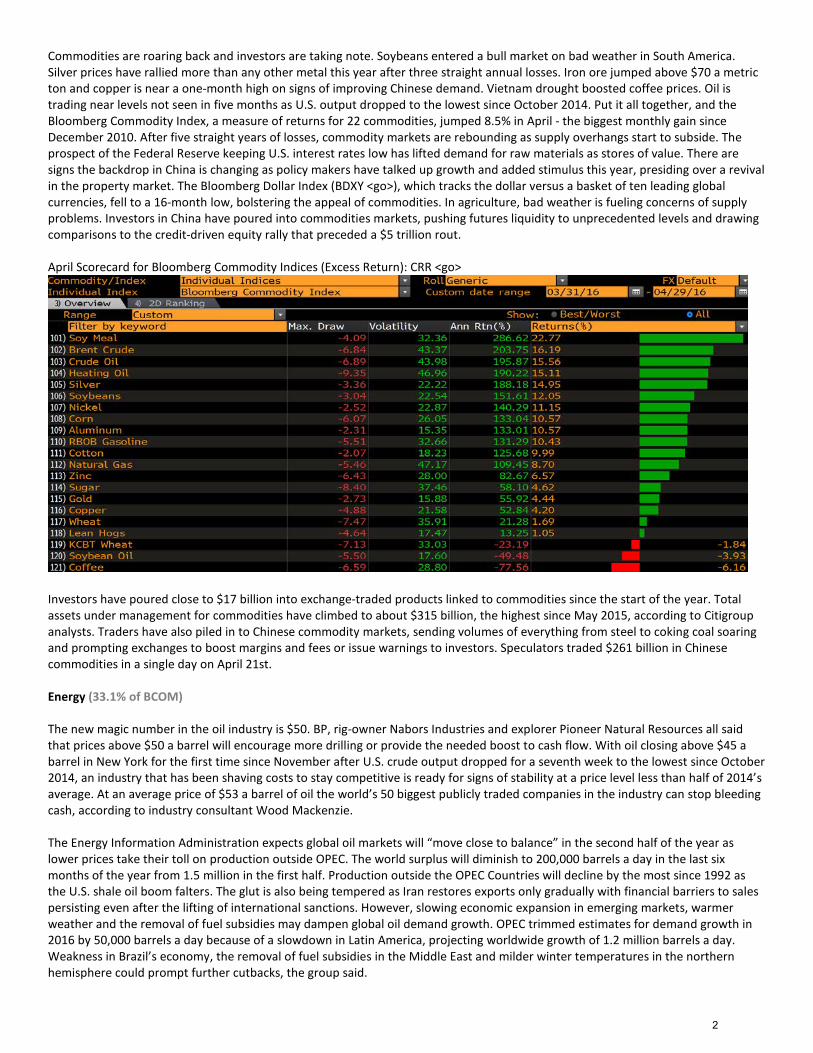

Commodities are roaring back and investors are taking note. Soybeans entered a bull market on bad weather in South America. Silver prices have rallied more than any other metal this year after three straight annual losses. Iron ore jumped above $70 a metric ton and copper is near a one-month high on signs of improving Chinese demand. Vietnam drought boosted coffee prices. Oil is trading near levels not seen in five months as U.S. output dropped to the lowest since October 2014. Put it all together, and the Bloomberg Commodity Index, a measure of returns for 22 commodities, jumped 8.5% in April - the biggest monthly gain since December 2010. After five straight years of losses, commodity markets are rebounding as supply overhangs start to subside. The prospect of the Federal Reserve keeping U.S. interest rates low has lifted demand for raw materials as stores of value. There are signs the backdrop in China is changing as policy makers have talked up growth and added stimulus this year, presiding over a revival in the property market. The Bloomberg Dollar Index (BDXY <go>), which tracks the dollar versus a basket of ten leading global currencies, fell to a 16-month low, bolstering the appeal of commodities. In agriculture, bad weather is fueling concerns of supply problems. Investors in China have poured into commodities markets, pushing futures liquidity to unprecedented levels and drawing comparisons to the credit-driven equity rally that preceded a $5 trillion rout.

April Scorecard for Bloomberg Commodity Indices (Excess Return): CRR <go>

Investors have poured close to $17 billion into exchange-traded products linked to commodities since the start of the year. Total assets under management for commodities have climbed to about $315 billion, the highest since May 2015, according to Citigroup analysts. Traders have also piled in to Chinese commodity markets, sending volumes of everything from steel to coking coal soaring and prompting exchanges to boost margins and fees or issue warnings to investors. Speculators traded $261 billion in Chinese commodities in a single day on April 21st.

Energy (33.1% of BCOM)

The new magic number in the oil industry is $50. BP, rig-owner Nabors Industries and explorer Pioneer Natural Resources all said that prices above $50 a barrel will encourage more drilling or provide the needed boost to cash flow. With oil closing above $45 a barrel in New York for the first time since November after U.S. crude output dropped for a seventh week to the lowest since October 2014, an industry that has been shaving costs to stay competitive is ready for signs of stability at a price level less than half of 2014’s average. At an average price of $53 a barrel of oil the world’s 50 biggest publicly traded companies in the industry can stop bleeding cash, according to industry consultant Wood Mackenzie.

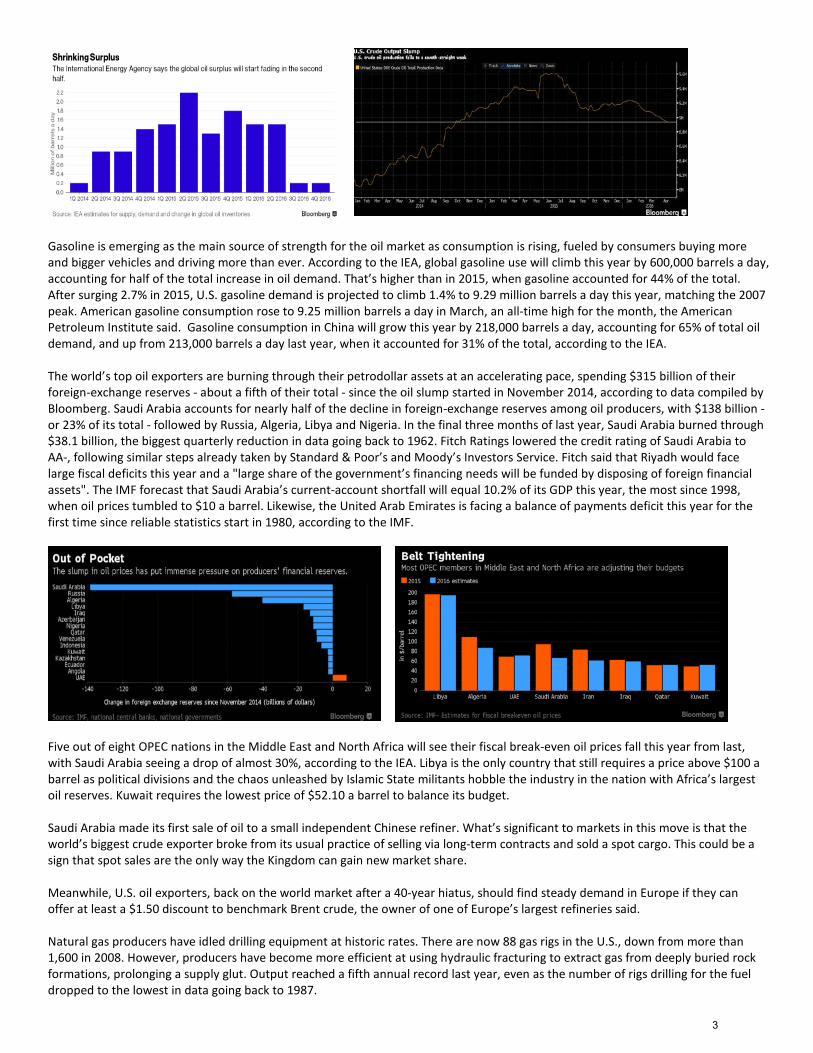

The Energy Information Administration expects global oil markets will “move close to balance” in the second half of the year as lower prices take their toll on production outside OPEC. The world surplus will diminish to 200,000 barrels a day in the last six months of the year from 1.5 million in the first half. Production outside the OPEC Countries will decline by the most since 1992 as the U.S. shale oil boom falters. The glut is also being tempered as Iran restores exports only gradually with financial barriers to sales persisting even after the lifting of international sanctions. However, slowing economic expansion in emerging markets, warmer weather and the removal of fuel subsidies may dampen global oil demand growth. OPEC trimmed estimates for demand growth in 2016 by 50,000 barrels a day because of a slowdown in Latin America, projecting worldwide growth of 1.2 million barrels a day. Weakness in Brazil’s economy, the removal of fuel subsidies in the Middle East and milder winter temperatures in the northern hemisphere could prompt further cutbacks, the group said.

2

Gasoline is emerging as the main source of strength for the oil market as consumption is rising, fueled by consumers buying more and bigger vehicles and driving more than ever. According to the IEA, global gasoline use will climb this year by 600,000 barrels a day, accounting for half of the total increase in oil demand. That’s higher than in 2015, when gasoline accounted for 44% of the total. After surging 2.7% in 2015, U.S. gasoline demand is projected to climb 1.4% to 9.29 million barrels a day this year, matching the 2007 peak. American gasoline consumption rose to 9.25 million barrels a day in March, an all-time high for the month, the American Petroleum Institute said. Gasoline consumption in China will grow this year by 218,000 barrels a day, accounting for 65% of total oil demand, and up from 213,000 barrels a day last year, when it accounted for 31% of the total, according to the IEA.

The world’s top oil exporters are burning through their petrodollar assets at an accelerating pace, spending $315 billion of their foreign-exchange reserves - about a fifth of their total - since the oil slump started in November 2014, according to data compiled by Bloomberg. Saudi Arabia accounts for nearly half of the decline in foreign-exchange reserves among oil producers, with $138 billion - or 23% of its total - followed by Russia, Algeria, Libya and Nigeria. In the final three months of last year, Saudi Arabia burned through $38.1 billion, the biggest quarterly reduction in data going back to 1962. Fitch Ratings lowered the credit rating of Saudi Arabia to AA-, following similar steps already taken by Standard & Poor’s and Moody’s Investors Service. Fitch said that Riyadh would face large fiscal deficits this year and a "large share of the government’s financing needs will be funded by disposing of foreign financial assets". The IMF forecast that Saudi Arabia’s current-account shortfall will equal 10.2% of its GDP this year, the most since 1998, when oil prices tumbled to $10 a barrel. Likewise, the United Arab Emirates is facing a balance of payments deficit this year for the first time since reliable statistics start in 1980, according to the IMF.

Five out of eight OPEC nations in the Middle East and North Africa will see their fiscal break-even oil prices fall this year from last, with Saudi Arabia seeing a drop of almost 30%, according to the IEA. Libya is the only country that still requires a price above $100 a barrel as political divisions and the chaos unleashed by Islamic State militants hobble the industry in the nation with Africa’s largest oil reserves. Kuwait requires the lowest price of $52.10 a barrel to balance its budget.

Saudi Arabia made its first sale of oil to a small independent Chinese refiner. What’s significant to markets in this move is that the world’s biggest crude exporter broke from its usual practice of selling via long-term contracts and sold a spot cargo. This could be a sign that spot sales are the only way the Kingdom can gain new market share.

Meanwhile, U.S. oil exporters, back on the world market after a 40-year hiatus, should find steady demand in Europe if they can offer at least a $1.50 discount to benchmark Brent crude, the owner of one of Europe’s largest refineries said.

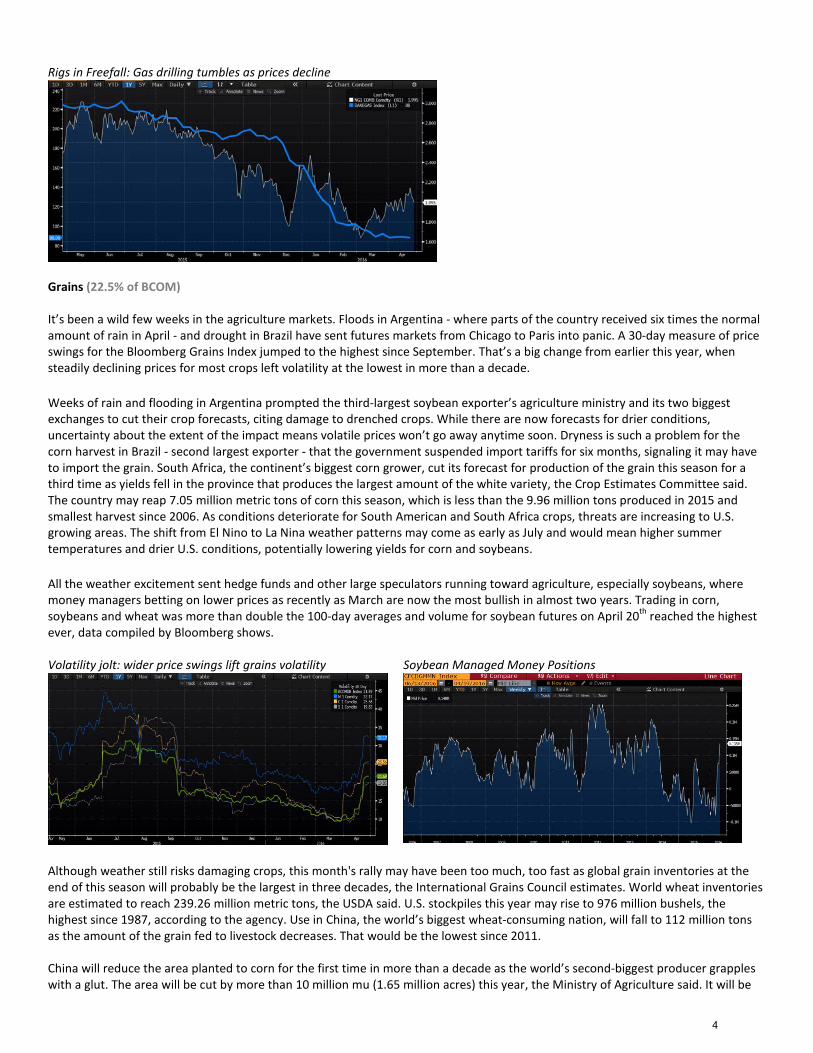

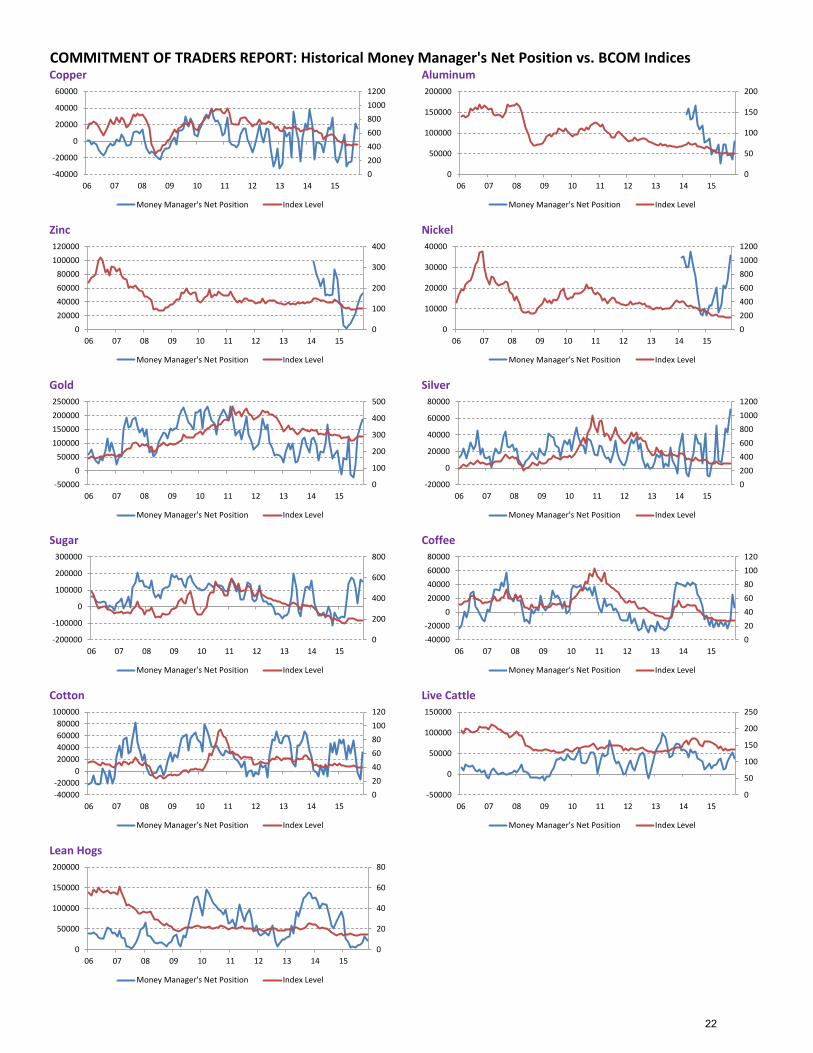

Natural gas producers have idled drilling equipment at historic rates. There are now 88 gas rigs in the U.S., down from more than 1,600 in 2008. However, producers have become more efficient at using hydraulic fracturing to extract gas from deeply buried rock formations, prolonging a supply glut. Output reached a fifth annual record last year, even as the number of rigs drilling for the fuel dropped to the lowest in data going back to 1987.

3

Rigs in Freefall: Gas drilling tumbles as prices decline

Grains (22.5% of BCOM)

It’s been a wild few weeks in the agriculture markets. Floods in Argentina - where parts of the country received six times the normal amount of rain in April - and drought in Brazil have sent futures markets from Chicago to Paris into panic. A 30-day measure of price swings for the Bloomberg Grains Index jumped to the highest since September. That’s a big change from earlier this year, when steadily declining prices for most crops left volatility at the lowest in more than a decade.

Weeks of rain and flooding in Argentina prompted the third-largest soybean exporter’s agriculture ministry and its two biggest exchanges to cut their crop forecasts, citing damage to drenched crops. While there are now forecasts for drier conditions, uncertainty about the extent of the impact means volatile prices won’t go away anytime soon. Dryness is such a problem for the corn harvest in Brazil - second largest exporter - that the government suspended import tariffs for six months, signaling it may have to import the grain. South Africa, the continent’s biggest corn grower, cut its forecast for production of the grain this season for a third time as yields fell in the province that produces the largest amount of the white variety, the Crop Estimates Committee said. The country may reap 7.05 million metric tons of corn this season, which is less than the 9.96 million tons produced in 2015 and smallest harvest since 2006. As conditions deteriorate for South American and South Africa crops, threats are increasing to U.S. growing areas. The shift from El Nino to La Nina weather patterns may come as early as July and would mean higher summer temperatures and drier U.S. conditions, potentially lowering yields for corn and soybeans.

All the weather excitement sent hedge funds and other large speculators running toward agriculture, especially soybeans, where money managers betting on lower prices as recently as March are now the most bullish in almost two years. Trading in corn, soybeans and wheat was more than double the 100-day averages and volume for soybean futures on April 20th reached the highest ever, data compiled by Bloomberg shows.

Volatility jolt: wider price swings lift grains volatility Soybean Managed Money Positions

Although weather still risks damaging crops, this month's rally may have been too much, too fast as global grain inventories at the end of this season will probably be the largest in three decades, the International Grains Council estimates. World wheat inventories are estimated to reach 239.26 million metric tons, the USDA said. U.S. stockpiles this year may rise to 976 million bushels, the highest since 1987, according to the agency. Use in China, the world’s biggest wheat-consuming nation, will fall to 112 million tons as the amount of the grain fed to livestock decreases. That would be the lowest since 2011.

China will reduce the area planted to corn for the first time in more than a decade as the world’s second-biggest producer grapples with a glut. The area will be cut by more than 10 million mu (1.65 million acres) this year, the Ministry of Agriculture said. It will be

4

the first decline since 2003-04, according to USDA data. It’s part of a plan to reduce planting by 8.2 million acres by 2020, the ministry said. That’s about 8.7% of the 2015-16 area, USDA data show. China is grappling with a corn glut after the government began subsidizing output in 2008, acquiring grain at above-market prices to protect farm incomes and spurring growers to plant more. The country is also ending its state corn stockpiling program, replacing it with other subsidizes to make it more market based. According to USDA estimates, China's corn stockpiles are forecast at 109.5 million tons at the end of the 2015-16 season, more than double the reserves held in the U.S. and more than half of world inventories.

Industrial Metals (16.5% of BCOM)

Raw materials used in property and manufacturing in China have rallied as a rebound in construction coincided with low inventories after weaker production at the start of the year.

Aluminum's Boom: Trading spike in Shanghai Shanghai Futures Exchange Copper Deliverable Stocks

Futures traders in China have flocked to metals, sending aluminum prices to around a 10-month high on the Shanghai Futures Exchange after volume more than quadrupled. That echoes the performance of steel reinforcement bar, where prices rose 20% in four days as trading ballooned. While strong demand and tight supplies in the first quarter drove up aluminum futures, the risk is that aluminum smelters in China - which supply more than half the world’s metal - are restarting idled plants after a price rally, according to the industry group that brokered an agreement in December to curb capacity. As much as half of Chinese smelter capacity is profitable at current prices, the deputy chairman of the China Nonferrous Metals Industry Association said, adding the restarts weren’t a breach of the December accord because the pact allowed for flexibility in production.

Copper stockpiles monitored by the Shanghai Futures Exchange fell from a record, coinciding with a rise in inventories tracked by the London Metal Exchange, a sign flows to China may be reversing. Stockpiles in sheds followed by the LME in Asia rose 8% to 72,675 tons, the most in tonnage terms since January. In March, the average gap between the spot price for copper in China and the cash contract on the LME was the smallest since 2008, a sign that exports from the top user were becoming more attractive. The increase in LME warehouses in Asia is almost certainly the consequence of shipments from China - the world’s biggest copper consumer - which imported 328,604 tons of refined metal in February and exported 10,767 tons.

A quarter of the world’s nickel miners are churning out stainless steel at a loss in the hope that competitors will shut first, according to research firm IHS Inc. The price of nickel slumped 30% in the past year, the worst performance among major metals traded on the LME, as slowing demand helps feed a global glut. Stockpiles on the LME are up fivefold since 2011. IHS estimates that 70% of producers globally are losing money on an operating-cost basis. Of those, 40% are diversified companies that won’t be hurt by the nickel losses, 5% to 10% get government subsidies or some other form of support, while about a quarter of the industry is becoming price-sensitive. With an average price forecast of $8,927 a ton this year and about 90% of production profitable at $15,000, a sudden shutdown in supply is required to rebalance the industry. Many producers are vertically integrated and use their own nickel to make stainless steel. Most loss-making nickel is from companies producing the lower-grade pig iron variety, which requires more energy. Following Indonesia’s 2014 ore-export ban - the world’s biggest producer of mined nickel in 2013 - the Philippines production increased 30% to 410,789 tons, or 20% of global mined production, according to the World Bureau of Metal Statistics.

Precious Metals (16.1% of BCOM)

The first quarter’s best-performing metal has run out of juice. Gold’s barely changed this month, flipping between gains and losses, after surging 16% in the first quarter, the biggest such advance in three decades. Cash flowing into exchange-traded funds backed by the metal has hit the buffers after pouring in at the fastest pace in seven years in the first three months. However, money managers continued to increase their wagers on a price rally to the highest since 2012, taking their optimism to a level last seen before a three-year bear market started. Federal Reserve officials are cautious about raising U.S. interest rates amid persistent risks facing

5

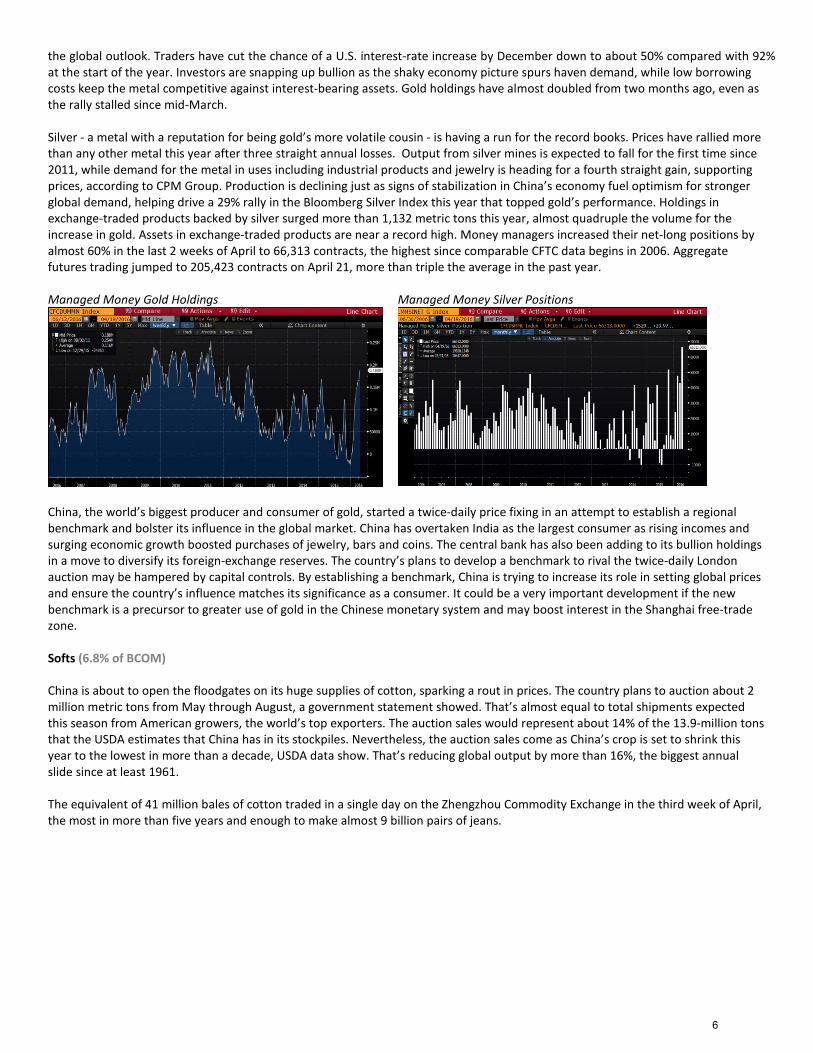

the global outlook. Traders have cut the chance of a U.S. interest-rate increase by December down to about 50% compared with 92% at the start of the year. Investors are snapping up bullion as the shaky economy picture spurs haven demand, while low borrowing costs keep the metal competitive against interest-bearing assets. Gold holdings have almost doubled from two months ago, even as the rally stalled since mid-March.

Silver - a metal with a reputation for being gold’s more volatile cousin - is having a run for the record books. Prices have rallied more than any other metal this year after three straight annual losses. Output from silver mines is expected to fall for the first time since 2011, while demand for the metal in uses including industrial products and jewelry is heading for a fourth straight gain, supporting prices, according to CPM Group. Production is declining just as signs of stabilization in China’s economy fuel optimism for stronger global demand, helping drive a 29% rally in the Bloomberg Silver Index this year that topped gold’s performance. Holdings in exchange-traded products backed by silver surged more than 1,132 metric tons this year, almost quadruple the volume for the increase in gold. Assets in exchange-traded products are near a record high. Money managers increased their net-long positions by almost 60% in the last 2 weeks of April to 66,313 contracts, the highest since comparable CFTC data begins in 2006. Aggregate futures trading jumped to 205,423 contracts on April 21, more than triple the average in the past year.

Managed Money Gold Holdings Managed Money Silver Positions

China, the world’s biggest producer and consumer of gold, started a twice-daily price fixing in an attempt to establish a regional benchmark and bolster its influence in the global market. China has overtaken India as the largest consumer as rising incomes and surging economic growth boosted purchases of jewelry, bars and coins. The central bank has also been adding to its bullion holdings in a move to diversify its foreign-exchange reserves. The country’s plans to develop a benchmark to rival the twice-daily London auction may be hampered by capital controls. By establishing a benchmark, China is trying to increase its role in setting global prices and ensure the country’s influence matches its significance as a consumer. It could be a very important development if the new benchmark is a precursor to greater use of gold in the Chinese monetary system and may boost interest in the Shanghai free-trade zone.

Softs (6.8% of BCOM)

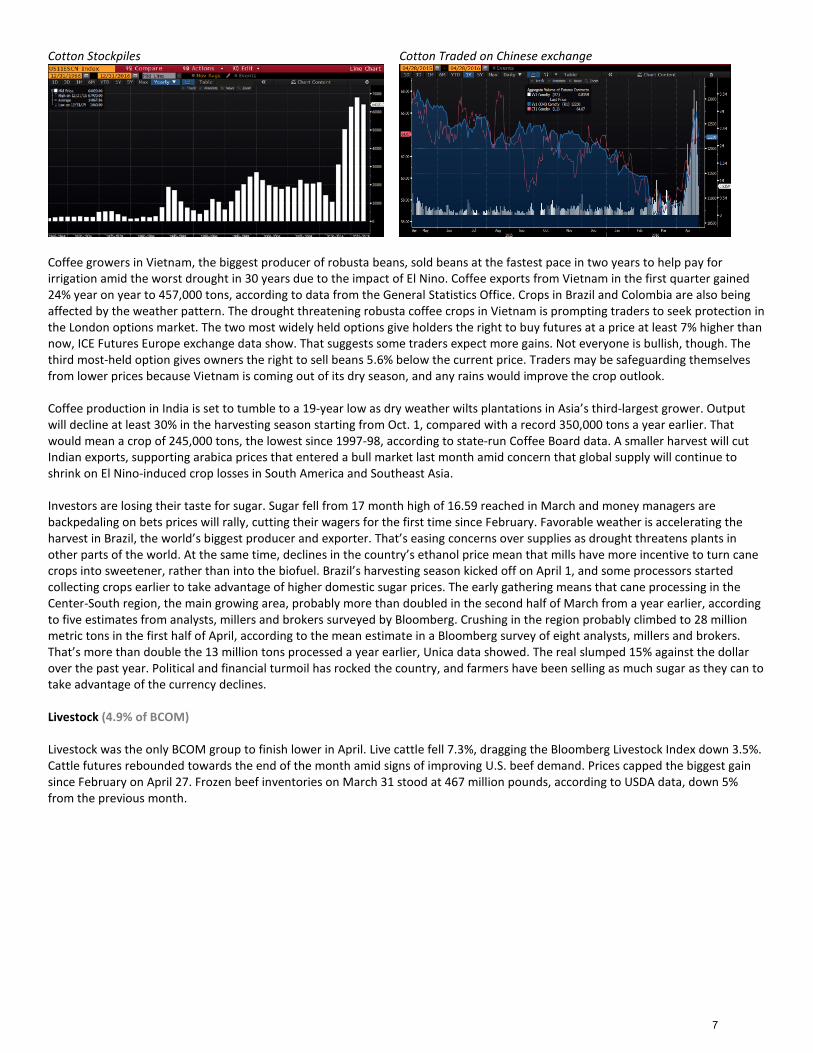

China is about to open the floodgates on its huge supplies of cotton, sparking a rout in prices. The country plans to auction about 2 million metric tons from May through August, a government statement showed. That’s almost equal to total shipments expected this season from American growers, the world’s top exporters. The auction sales would represent about 14% of the 13.9-million tons that the USDA estimates that China has in its stockpiles. Nevertheless, the auction sales come as China’s crop is set to shrink this year to the lowest in more than a decade, USDA data show. That’s reducing global output by more than 16%, the biggest annual slide since at least 1961.

The equivalent of 41 million bales of cotton traded in a single day on the Zhengzhou Commodity Exchange in the third week of April, the most in more than five years and enough to make almost 9 billion pairs of jeans.

6

Cotton Stockpiles Cotton Traded on Chinese exchange

Coffee growers in Vietnam, the biggest producer of robusta beans, sold beans at the fastest pace in two years to help pay for irrigation amid the worst drought in 30 years due to the impact of El Nino. Coffee exports from Vietnam in the first quarter gained 24% year on year to 457,000 tons, according to data from the General Statistics Office. Crops in Brazil and Colombia are also being affected by the weather pattern. The drought threatening robusta coffee crops in Vietnam is prompting traders to seek protection in the London options market. The two most widely held options give holders the right to buy futures at a price at least 7% higher than now, ICE Futures Europe exchange data show. That suggests some traders expect more gains. Not everyone is bullish, though. The third most-held option gives owners the right to sell beans 5.6% below the current price. Traders may be safeguarding themselves from lower prices because Vietnam is coming out of its dry season, and any rains would improve the crop outlook.

Coffee production in India is set to tumble to a 19-year low as dry weather wilts plantations in Asia’s third-largest grower. Output will decline at least 30% in the harvesting season starting from Oct. 1, compared with a record 350,000 tons a year earlier. That would mean a crop of 245,000 tons, the lowest since 1997-98, according to state-run Coffee Board data. A smaller harvest will cut Indian exports, supporting arabica prices that entered a bull market last month amid concern that global supply will continue to shrink on El Nino-induced crop losses in South America and Southeast Asia.

Investors are losing their taste for sugar. Sugar fell from 17 month high of 16.59 reached in March and money managers are backpedaling on bets prices will rally, cutting their wagers for the first time since February. Favorable weather is accelerating the harvest in Brazil, the world’s biggest producer and exporter. That’s easing concerns over supplies as drought threatens plants in other parts of the world. At the same time, declines in the country’s ethanol price mean that mills have more incentive to turn cane crops into sweetener, rather than into the biofuel. Brazil’s harvesting season kicked off on April 1, and some processors started collecting crops earlier to take advantage of higher domestic sugar prices. The early gathering means that cane processing in the Center-South region, the main growing area, probably more than doubled in the second half of March from a year earlier, according to five estimates from analysts, millers and brokers surveyed by Bloomberg. Crushing in the region probably climbed to 28 million metric tons in the first half of April, according to the mean estimate in a Bloomberg survey of eight analysts, millers and brokers. That’s more than double the 13 million tons processed a year earlier, Unica data showed. The real slumped 15% against the dollar over the past year. Political and financial turmoil has rocked the country, and farmers have been selling as much sugar as they can to take advantage of the currency declines.

Livestock (4.9% of BCOM)

Livestock was the only BCOM group to finish lower in April. Live cattle fell 7.3%, dragging the Bloomberg Livestock Index down 3.5%. Cattle futures rebounded towards the end of the month amid signs of improving U.S. beef demand. Prices capped the biggest gain since February on April 27. Frozen beef inventories on March 31 stood at 467 million pounds, according to USDA data, down 5% from the previous month.

7

Composite Indices* Click hyperlinks to open in Bloomberg

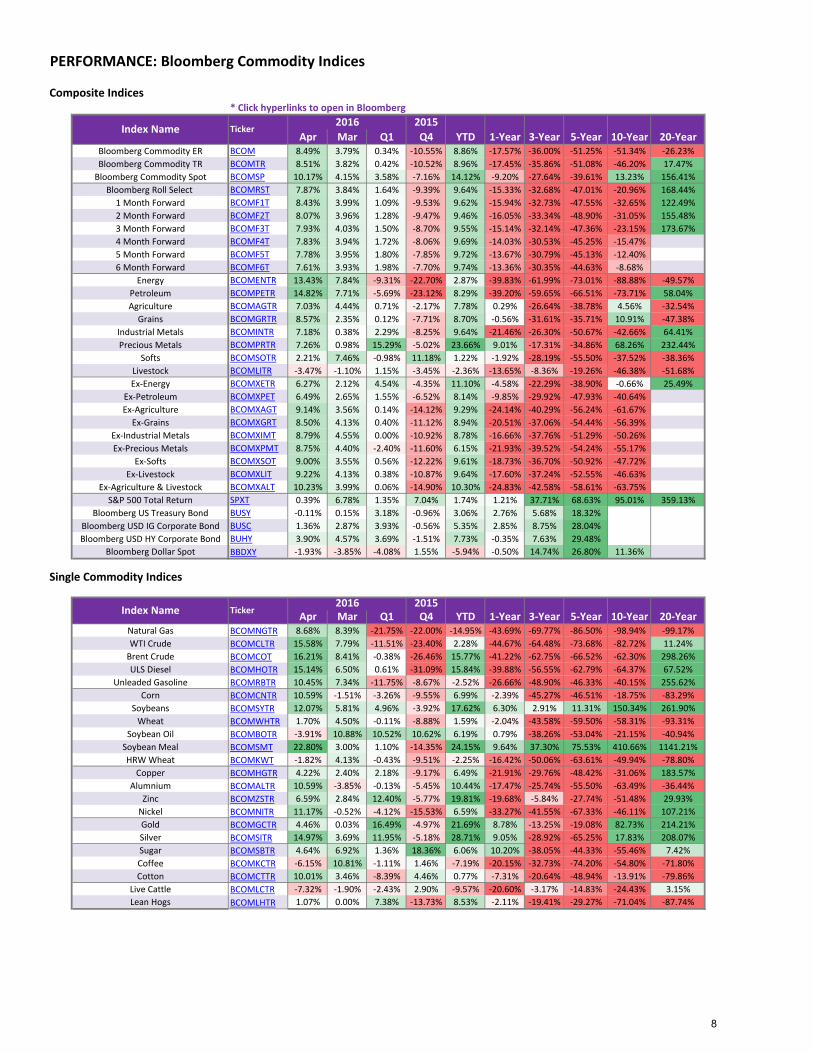

2015Apr Mar Q1 Q4 YTD 1-Year 3-Year 5-Year 10-Year 20-Year

Bloomberg Commodity ER BCOM 8.49% 3.79% 0.34% -10.55% 8.86% -17.57% -36.00% -51.25% -51.34% -26.23%Bloomberg Commodity TR BCOMTR 8.51% 3.82% 0.42% -10.52% 8.96% -17.45% -35.86% -51.08% -46.20% 17.47%

Bloomberg Commodity Spot BCOMSP 10.17% 4.15% 3.58% -7.16% 14.12% -9.20% -27.64% -39.61% 13.23% 156.41%Bloomberg Roll Select BCOMRST 7.87% 3.84% 1.64% -9.39% 9.64% -15.33% -32.68% -47.01% -20.96% 168.44%

1 Month Forward BCOMF1T 8.43% 3.99% 1.09% -9.53% 9.62% -15.94% -32.73% -47.55% -32.65% 122.49% 2 Month Forward BCOMF2T 8.07% 3.96% 1.28% -9.47% 9.46% -16.05% -33.34% -48.90% -31.05% 155.48% 3 Month Forward BCOMF3T 7.93% 4.03% 1.50% -8.70% 9.55% -15.14% -32.14% -47.36% -23.15% 173.67% 4 Month Forward BCOMF4T 7.83% 3.94% 1.72% -8.06% 9.69% -14.03% -30.53% -45.25% -15.47% 5 Month Forward BCOMF5T 7.78% 3.95% 1.80% -7.85% 9.72% -13.67% -30.79% -45.13% -12.40% 6 Month Forward BCOMF6T 7.61% 3.93% 1.98% -7.70% 9.74% -13.36% -30.35% -44.63% -8.68%

Energy BCOMENTR 13.43% 7.84% -9.31% -22.70% 2.87% -39.83% -61.99% -73.01% -88.88% -49.57%Petroleum BCOMPETR 14.82% 7.71% -5.69% -23.12% 8.29% -39.20% -59.65% -66.51% -73.71% 58.04%Agriculture BCOMAGTR 7.03% 4.44% 0.71% -2.17% 7.78% 0.29% -26.64% -38.78% 4.56% -32.54%

Grains BCOMGRTR 8.57% 2.35% 0.12% -7.71% 8.70% -0.56% -31.61% -35.71% 10.91% -47.38%Industrial Metals BCOMINTR 7.18% 0.38% 2.29% -8.25% 9.64% -21.46% -26.30% -50.67% -42.66% 64.41%Precious Metals BCOMPRTR 7.26% 0.98% 15.29% -5.02% 23.66% 9.01% -17.31% -34.86% 68.26% 232.44%

Softs BCOMSOTR 2.21% 7.46% -0.98% 11.18% 1.22% -1.92% -28.19% -55.50% -37.52% -38.36%Livestock BCOMLITR -3.47% -1.10% 1.15% -3.45% -2.36% -13.65% -8.36% -19.26% -46.38% -51.68%Ex-Energy BCOMXETR 6.27% 2.12% 4.54% -4.35% 11.10% -4.58% -22.29% -38.90% -0.66% 25.49%

Ex-Petroleum BCOMXPET 6.49% 2.65% 1.55% -6.52% 8.14% -9.85% -29.92% -47.93% -40.64%Ex-Agriculture BCOMXAGT 9.14% 3.56% 0.14% -14.12% 9.29% -24.14% -40.29% -56.24% -61.67%

Ex-Grains BCOMXGRT 8.50% 4.13% 0.40% -11.12% 8.94% -20.51% -37.06% -54.44% -56.39%Ex-Industrial Metals BCOMXIMT 8.79% 4.55% 0.00% -10.92% 8.78% -16.66% -37.76% -51.29% -50.26%Ex-Precious Metals BCOMXPMT 8.75% 4.40% -2.40% -11.60% 6.15% -21.93% -39.52% -54.24% -55.17%

Ex-Softs BCOMXSOT 9.00% 3.55% 0.56% -12.22% 9.61% -18.73% -36.70% -50.92% -47.72%Ex-Livestock BCOMXLIT 9.22% 4.13% 0.38% -10.87% 9.64% -17.60% -37.24% -52.55% -46.63%

Ex-Agriculture & Livestock BCOMXALT 10.23% 3.99% 0.06% -14.90% 10.30% -24.83% -42.58% -58.61% -63.75%S&P 500 Total Return SPXT 0.39% 6.78% 1.35% 7.04% 1.74% 1.21% 37.71% 68.63% 95.01% 359.13%

Bloomberg US Treasury Bond BUSY -0.11% 0.15% 3.18% -0.96% 3.06% 2.76% 5.68% 18.32%Bloomberg USD IG Corporate Bond BUSC 1.36% 2.87% 3.93% -0.56% 5.35% 2.85% 8.75% 28.04%Bloomberg USD HY Corporate Bond BUHY 3.90% 4.57% 3.69% -1.51% 7.73% -0.35% 7.63% 29.48%

Bloomberg Dollar Spot BBDXY -1.93% -3.85% -4.08% 1.55% -5.94% -0.50% 14.74% 26.80% 11.36%

Single Commodity Indices

2015Apr Mar Q1 Q4 YTD 1-Year 3-Year 5-Year 10-Year 20-Year

Natural Gas BCOMNGTR 8.68% 8.39% -21.75% -22.00% -14.95% -43.69% -69.77% -86.50% -98.94% -99.17%WTI Crude BCOMCLTR 15.58% 7.79% -11.51% -23.40% 2.28% -44.67% -64.48% -73.68% -82.72% 11.24%

Brent Crude BCOMCOT 16.21% 8.41% -0.38% -26.46% 15.77% -41.22% -62.75% -66.52% -62.30% 298.26%ULS Diesel BCOMHOTR 15.14% 6.50% 0.61% -31.09% 15.84% -39.88% -56.55% -62.79% -64.37% 67.52%

Unleaded Gasoline BCOMRBTR 10.45% 7.34% -11.75% -8.67% -2.52% -26.66% -48.90% -46.33% -40.15% 255.62%Corn BCOMCNTR 10.59% -1.51% -3.26% -9.55% 6.99% -2.39% -45.27% -46.51% -18.75% -83.29%

Soybeans BCOMSYTR 12.07% 5.81% 4.96% -3.92% 17.62% 6.30% 2.91% 11.31% 150.34% 261.90%Wheat BCOMWHTR 1.70% 4.50% -0.11% -8.88% 1.59% -2.04% -43.58% -59.50% -58.31% -93.31%

Soybean Oil BCOMBOTR -3.91% 10.88% 10.52% 10.62% 6.19% 0.79% -38.26% -53.04% -21.15% -40.94%Soybean Meal BCOMSMT 22.80% 3.00% 1.10% -14.35% 24.15% 9.64% 37.30% 75.53% 410.66% 1141.21%HRW Wheat BCOMKWT -1.82% 4.13% -0.43% -9.51% -2.25% -16.42% -50.06% -63.61% -49.94% -78.80%

Copper BCOMHGTR 4.22% 2.40% 2.18% -9.17% 6.49% -21.91% -29.76% -48.42% -31.06% 183.57%Alumnium BCOMALTR 10.59% -3.85% -0.13% -5.45% 10.44% -17.47% -25.74% -55.50% -63.49% -36.44%

Zinc BCOMZSTR 6.59% 2.84% 12.40% -5.77% 19.81% -19.68% -5.84% -27.74% -51.48% 29.93%Nickel BCOMNITR 11.17% -0.52% -4.12% -15.53% 6.59% -33.27% -41.55% -67.33% -46.11% 107.21%Gold BCOMGCTR 4.46% 0.03% 16.49% -4.97% 21.69% 8.78% -13.25% -19.08% 82.73% 214.21%Silver BCOMSITR 14.97% 3.69% 11.95% -5.18% 28.71% 9.05% -28.92% -65.25% 17.83% 208.07%Sugar BCOMSBTR 4.64% 6.92% 1.36% 18.36% 6.06% 10.20% -38.05% -44.33% -55.46% 7.42%Coffee BCOMKCTR -6.15% 10.81% -1.11% 1.46% -7.19% -20.15% -32.73% -74.20% -54.80% -71.80%Cotton BCOMCTTR 10.01% 3.46% -8.39% 4.46% 0.77% -7.31% -20.64% -48.94% -13.91% -79.86%

Live Cattle BCOMLCTR -7.32% -1.90% -2.43% 2.90% -9.57% -20.60% -3.17% -14.83% -24.43% 3.15%Lean Hogs BCOMLHTR 1.07% 0.00% 7.38% -13.73% 8.53% -2.11% -19.41% -29.27% -71.04% -87.74%

Index Name Ticker

Index Name Ticker

PERFORMANCE: Bloomberg Commodity Indices

2016

2016

8

Composite Roll Select Indices * Click hyperlinks to open in Bloomberg

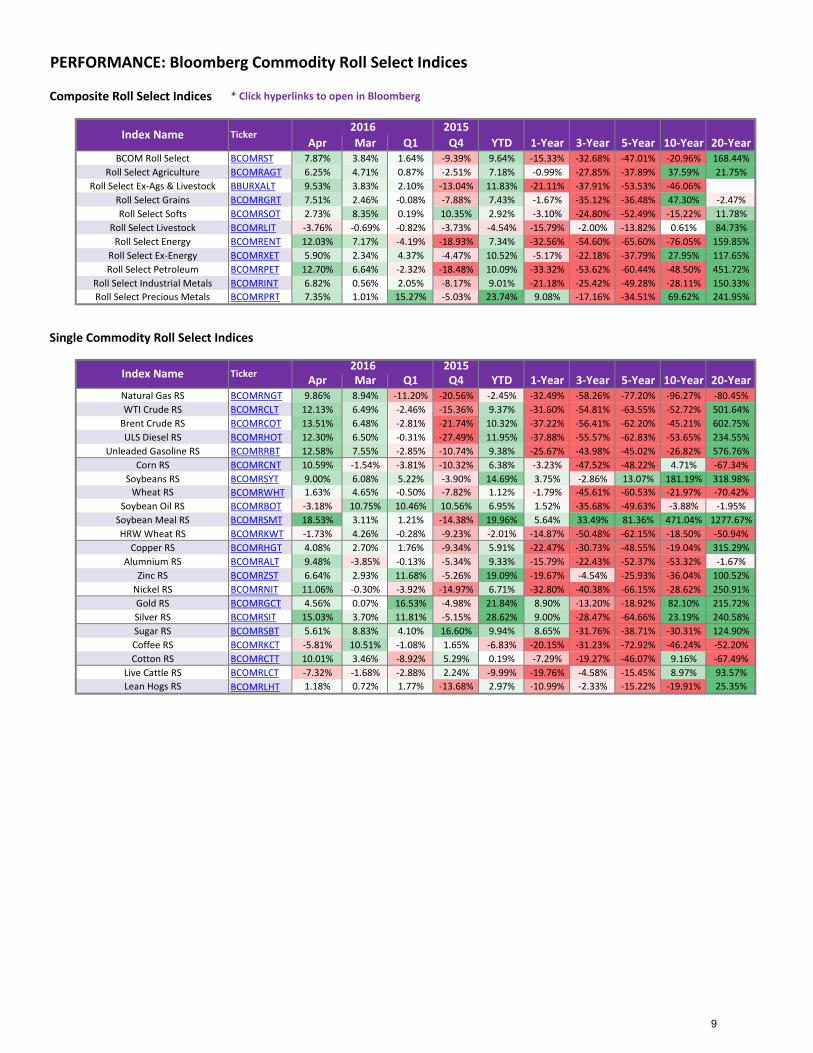

2015Apr Mar Q1 Q4 YTD 1-Year 3-Year 5-Year 10-Year 20-Year

BCOM Roll Select BCOMRST 7.87% 3.84% 1.64% -9.39% 9.64% -15.33% -32.68% -47.01% -20.96% 168.44%Roll Select Agriculture BCOMRAGT 6.25% 4.71% 0.87% -2.51% 7.18% -0.99% -27.85% -37.89% 37.59% 21.75%

Roll Select Ex-Ags & Livestock BBURXALT 9.53% 3.83% 2.10% -13.04% 11.83% -21.11% -37.91% -53.53% -46.06%Roll Select Grains BCOMRGRT 7.51% 2.46% -0.08% -7.88% 7.43% -1.67% -35.12% -36.48% 47.30% -2.47%Roll Select Softs BCOMRSOT 2.73% 8.35% 0.19% 10.35% 2.92% -3.10% -24.80% -52.49% -15.22% 11.78%

Roll Select Livestock BCOMRLIT -3.76% -0.69% -0.82% -3.73% -4.54% -15.79% -2.00% -13.82% 0.61% 84.73%Roll Select Energy BCOMRENT 12.03% 7.17% -4.19% -18.93% 7.34% -32.56% -54.60% -65.60% -76.05% 159.85%

Roll Select Ex-Energy BCOMRXET 5.90% 2.34% 4.37% -4.47% 10.52% -5.17% -22.18% -37.79% 27.95% 117.65%Roll Select Petroleum BCOMRPET 12.70% 6.64% -2.32% -18.48% 10.09% -33.32% -53.62% -60.44% -48.50% 451.72%

Roll Select Industrial Metals BCOMRINT 6.82% 0.56% 2.05% -8.17% 9.01% -21.18% -25.42% -49.28% -28.11% 150.33%Roll Select Precious Metals BCOMRPRT 7.35% 1.01% 15.27% -5.03% 23.74% 9.08% -17.16% -34.51% 69.62% 241.95%

Single Commodity Roll Select Indices

2015Apr Mar Q1 Q4 YTD 1-Year 3-Year 5-Year 10-Year 20-Year

Natural Gas RS BCOMRNGT 9.86% 8.94% -11.20% -20.56% -2.45% -32.49% -58.26% -77.20% -96.27% -80.45%WTI Crude RS BCOMRCLT 12.13% 6.49% -2.46% -15.36% 9.37% -31.60% -54.81% -63.55% -52.72% 501.64%

Brent Crude RS BCOMRCOT 13.51% 6.48% -2.81% -21.74% 10.32% -37.22% -56.41% -62.20% -45.21% 602.75%ULS Diesel RS BCOMRHOT 12.30% 6.50% -0.31% -27.49% 11.95% -37.88% -55.57% -62.83% -53.65% 234.55%

Unleaded Gasoline RS BCOMRRBT 12.58% 7.55% -2.85% -10.74% 9.38% -25.67% -43.98% -45.02% -26.82% 576.76%Corn RS BCOMRCNT 10.59% -1.54% -3.81% -10.32% 6.38% -3.23% -47.52% -48.22% 4.71% -67.34%

Soybeans RS BCOMRSYT 9.00% 6.08% 5.22% -3.90% 14.69% 3.75% -2.86% 13.07% 181.19% 318.98%Wheat RS BCOMRWHT 1.63% 4.65% -0.50% -7.82% 1.12% -1.79% -45.61% -60.53% -21.97% -70.42%

Soybean Oil RS BCOMRBOT -3.18% 10.75% 10.46% 10.56% 6.95% 1.52% -35.68% -49.63% -3.88% -1.95%Soybean Meal RS BCOMRSMT 18.53% 3.11% 1.21% -14.38% 19.96% 5.64% 33.49% 81.36% 471.04% 1277.67%HRW Wheat RS BCOMRKWT -1.73% 4.26% -0.28% -9.23% -2.01% -14.87% -50.48% -62.15% -18.50% -50.94%

Copper RS BCOMRHGT 4.08% 2.70% 1.76% -9.34% 5.91% -22.47% -30.73% -48.55% -19.04% 315.29%Alumnium RS BCOMRALT 9.48% -3.85% -0.13% -5.34% 9.33% -15.79% -22.43% -52.37% -53.32% -1.67%

Zinc RS BCOMRZST 6.64% 2.93% 11.68% -5.26% 19.09% -19.67% -4.54% -25.93% -36.04% 100.52%Nickel RS BCOMRNIT 11.06% -0.30% -3.92% -14.97% 6.71% -32.80% -40.38% -66.15% -28.62% 250.91%Gold RS BCOMRGCT 4.56% 0.07% 16.53% -4.98% 21.84% 8.90% -13.20% -18.92% 82.10% 215.72%Silver RS BCOMRSIT 15.03% 3.70% 11.81% -5.15% 28.62% 9.00% -28.47% -64.66% 23.19% 240.58%Sugar RS BCOMRSBT 5.61% 8.83% 4.10% 16.60% 9.94% 8.65% -31.76% -38.71% -30.31% 124.90%Coffee RS BCOMRKCT -5.81% 10.51% -1.08% 1.65% -6.83% -20.15% -31.23% -72.92% -46.24% -52.20%Cotton RS BCOMRCTT 10.01% 3.46% -8.92% 5.29% 0.19% -7.29% -19.27% -46.07% 9.16% -67.49%

Live Cattle RS BCOMRLCT -7.32% -1.68% -2.88% 2.24% -9.99% -19.76% -4.58% -15.45% 8.97% 93.57%Lean Hogs RS BCOMRLHT 1.18% 0.72% 1.77% -13.68% 2.97% -10.99% -2.33% -15.22% -19.91% 25.35%

PERFORMANCE: Bloomberg Commodity Roll Select Indices

Index Name Ticker

Index Name Ticker

2016

2016

9

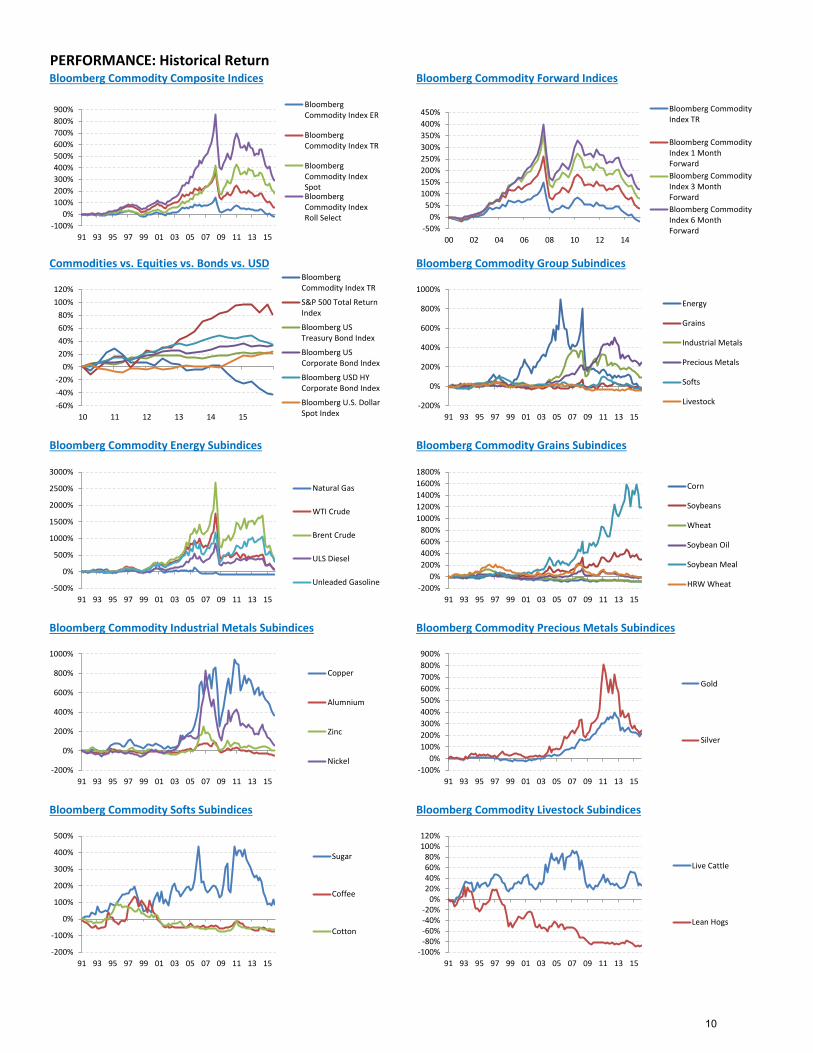

PERFORMANCE: Historical ReturnBloomberg Commodity Composite Indices

Commodities vs. Equities vs. Bonds vs. USD

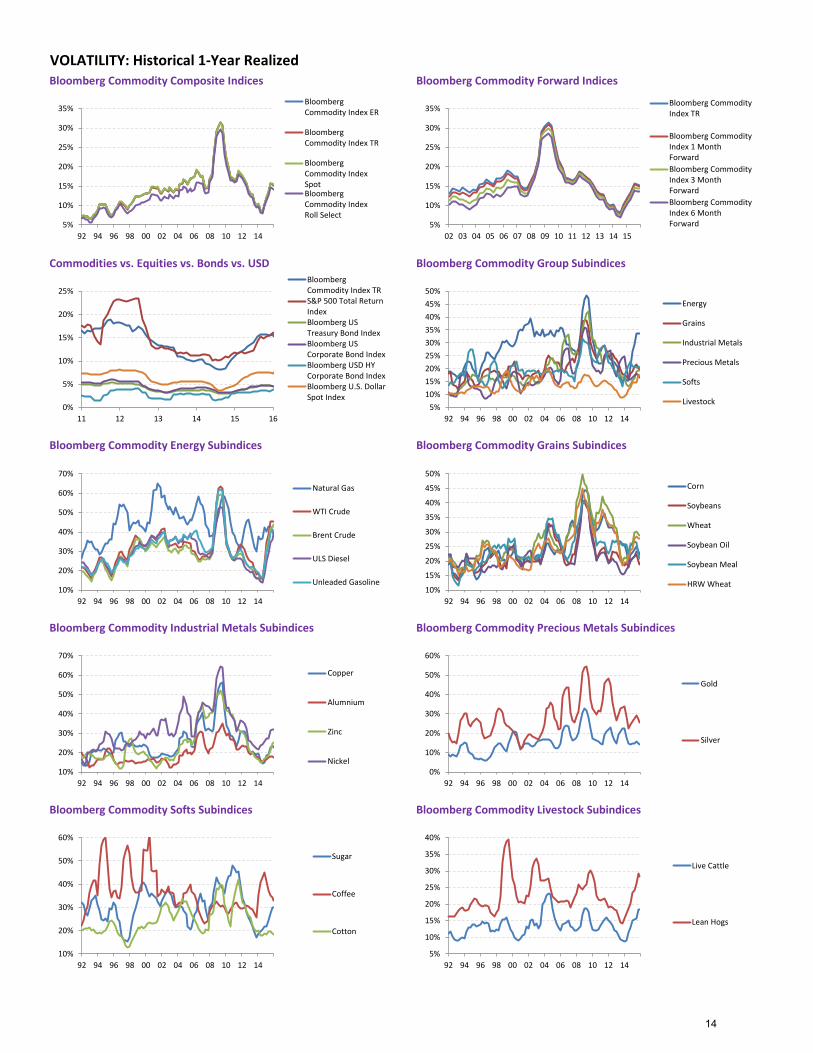

Bloomberg Commodity Energy Subindices

Bloomberg Commodity Forward Indices

Bloomberg Commodity Group Subindices

Bloomberg Commodity Grains Subindices

Bloomberg Commodity Industrial Metals Subindices Bloomberg Commodity Precious Metals Subindices

Bloomberg Commodity Softs Subindices Bloomberg Commodity Livestock Subindices

-100%0%

100%200%300%400%500%600%700%800%900%

91 93 95 97 99 01 03 05 07 09 11 13 15

BloombergCommodity Index ER

BloombergCommodity Index TR

BloombergCommodity IndexSpotBloombergCommodity IndexRoll Select

-50%0%

50%100%150%200%250%300%350%400%450%

00 02 04 06 08 10 12 14

Bloomberg CommodityIndex TR

Bloomberg CommodityIndex 1 MonthForwardBloomberg CommodityIndex 3 MonthForwardBloomberg CommodityIndex 6 MonthForward

-60%-40%-20%

0%20%40%60%80%

100%120%

10 11 12 13 14 15

BloombergCommodity Index TR

S&P 500 Total ReturnIndex

Bloomberg USTreasury Bond Index

Bloomberg USCorporate Bond Index

Bloomberg USD HYCorporate Bond Index

Bloomberg U.S. DollarSpot Index

-200%

0%

200%

400%

600%

800%

1000%

91 93 95 97 99 01 03 05 07 09 11 13 15

Energy

Grains

Industrial Metals

Precious Metals

Softs

Livestock

-500%

0%

500%

1000%

1500%

2000%

2500%

3000%

91 93 95 97 99 01 03 05 07 09 11 13 15

Natural Gas

WTI Crude

Brent Crude

ULS Diesel

Unleaded Gasoline-200%

0%200%400%600%800%

1000%1200%1400%1600%1800%

91 93 95 97 99 01 03 05 07 09 11 13 15

Corn

Soybeans

Wheat

Soybean Oil

Soybean Meal

HRW Wheat

-200%

0%

200%

400%

600%

800%

1000%

91 93 95 97 99 01 03 05 07 09 11 13 15

Copper

Alumnium

Zinc

Nickel-100%

0%100%200%300%400%500%600%700%800%900%

91 93 95 97 99 01 03 05 07 09 11 13 15

Gold

Silver

-200%

-100%

0%

100%

200%

300%

400%

500%

91 93 95 97 99 01 03 05 07 09 11 13 15

Sugar

Coffee

Cotton

-100%-80%-60%-40%-20%

0%20%40%60%80%

100%120%

91 93 95 97 99 01 03 05 07 09 11 13 15

Live Cattle

Lean Hogs

10

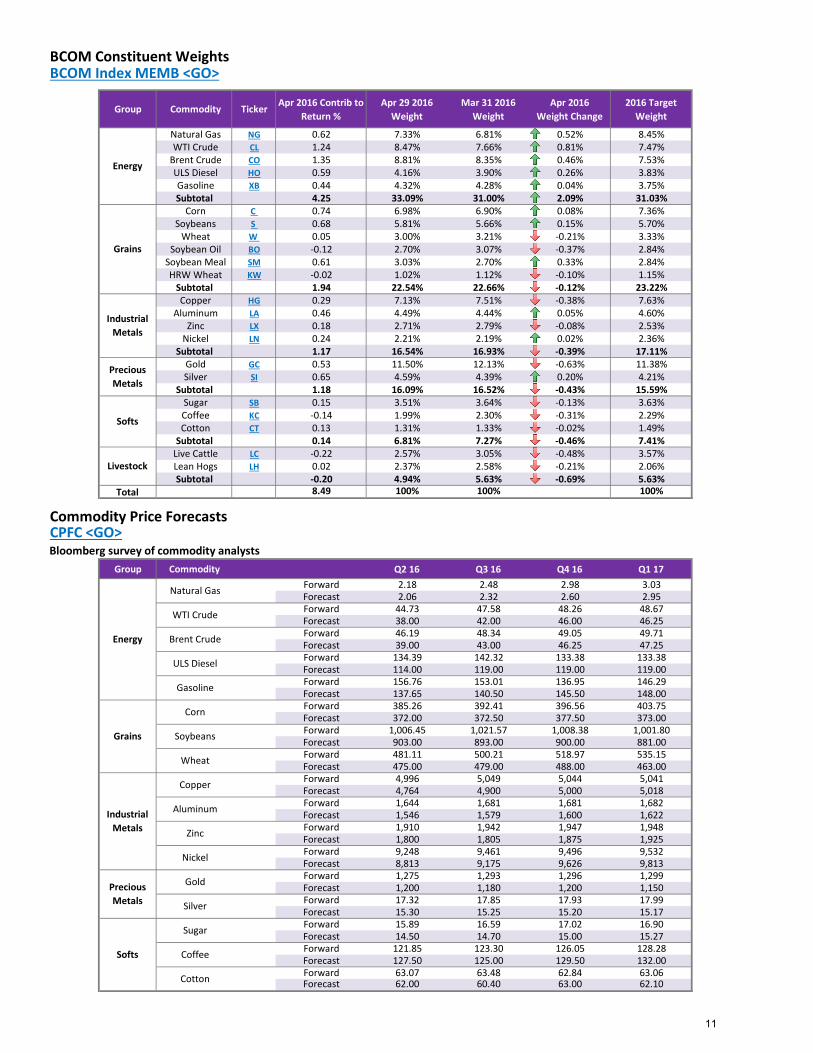

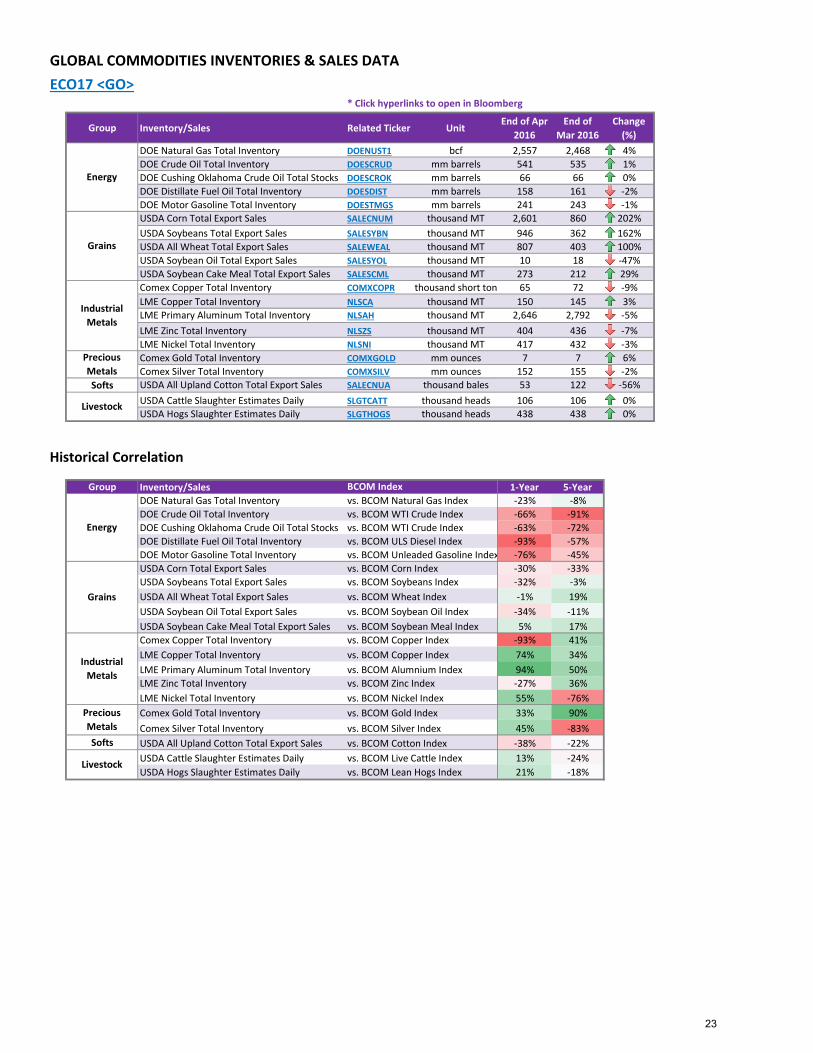

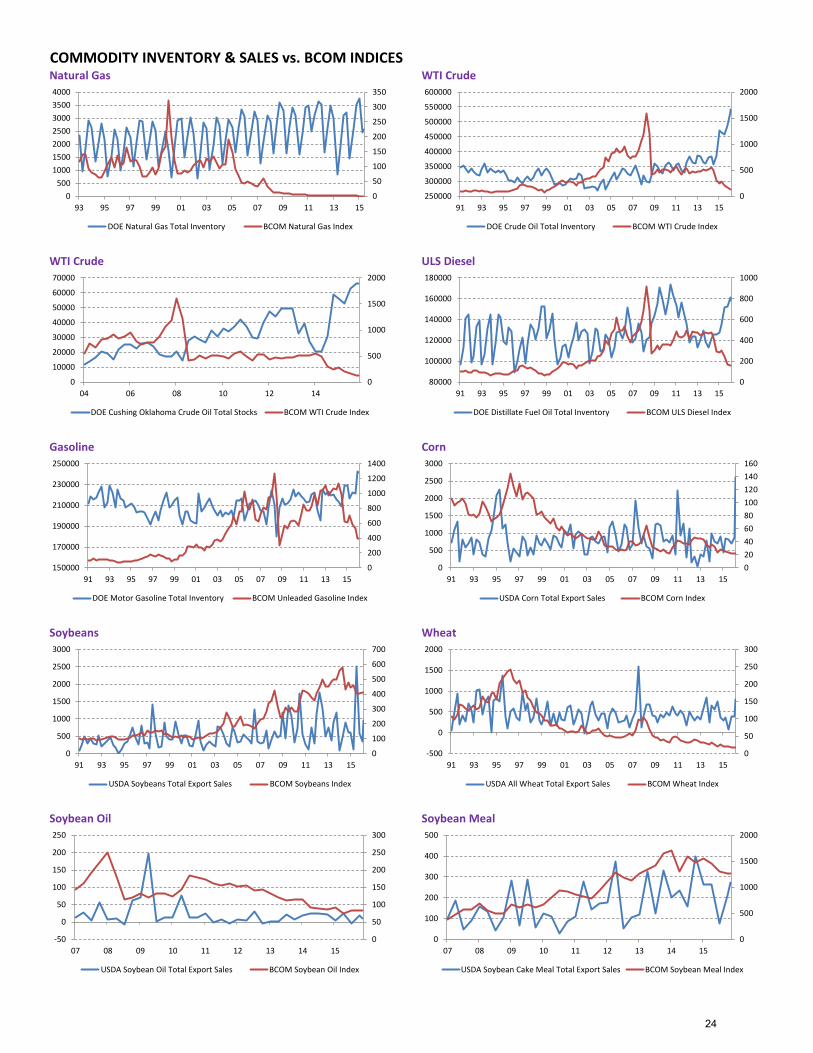

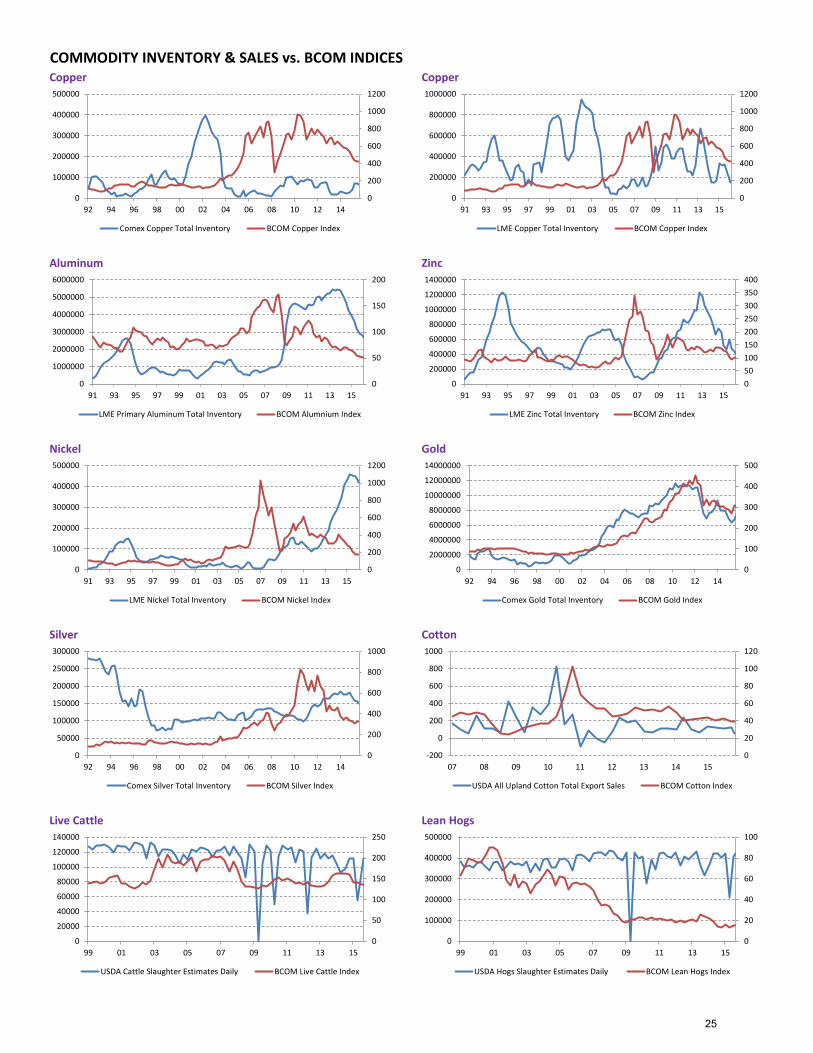

BCOM Constituent Weights BCOM Index MEMB <GO>

Group Commodity Ticker Apr 2016 Contrib to Return %

Apr 29 2016 Weight

Mar 31 2016 Weight

Apr 2016 Weight Change

2016 Target Weight

Natural Gas NG 0.62 7.33% 6.81% 0.52% 8.45% WTI Crude CL 1.24 8.47% 7.66% 0.81% 7.47%

Brent Crude CO 1.35 8.81% 8.35% 0.46% 7.53% ULS Diesel HO 0.59 4.16% 3.90% 0.26% 3.83% Gasoline XB 0.44 4.32% 4.28% 0.04% 3.75%Subtotal 4.25 33.09% 31.00% 2.09% 31.03%

Corn C 0.74 6.98% 6.90% 0.08% 7.36% Soybeans S 0.68 5.81% 5.66% 0.15% 5.70%

Wheat W 0.05 3.00% 3.21% -0.21% 3.33% Soybean Oil BO -0.12 2.70% 3.07% -0.37% 2.84%

Soybean Meal SM 0.61 3.03% 2.70% 0.33% 2.84% HRW Wheat KW -0.02 1.02% 1.12% -0.10% 1.15%

Subtotal 1.94 22.54% 22.66% -0.12% 23.22% Copper HG 0.29 7.13% 7.51% -0.38% 7.63%

Aluminum LA 0.46 4.49% 4.44% 0.05% 4.60% Zinc LX 0.18 2.71% 2.79% -0.08% 2.53%

Nickel LN 0.24 2.21% 2.19% 0.02% 2.36%Subtotal 1.17 16.54% 16.93% -0.39% 17.11%

Gold GC 0.53 11.50% 12.13% -0.63% 11.38% Silver SI 0.65 4.59% 4.39% 0.20% 4.21%

Subtotal 1.18 16.09% 16.52% -0.43% 15.59% Sugar SB 0.15 3.51% 3.64% -0.13% 3.63% Coffee KC -0.14 1.99% 2.30% -0.31% 2.29% Cotton CT 0.13 1.31% 1.33% -0.02% 1.49%

Subtotal 0.14 6.81% 7.27% -0.46% 7.41% Live Cattle LC -0.22 2.57% 3.05% -0.48% 3.57% Lean Hogs LH 0.02 2.37% 2.58% -0.21% 2.06%

Subtotal -0.20 4.94% 5.63% -0.69% 5.63%Total 8.49 100% 100% 100%

Commodity Price ForecastsCPFC <GO>

Group Commodity Q2 16 Q3 16 Q4 16 Q1 17Forward 2.18 2.48 2.98 3.03Forecast 2.06 2.32 2.60 2.95Forward 44.73 47.58 48.26 48.67Forecast 38.00 42.00 46.00 46.25Forward 46.19 48.34 49.05 49.71Forecast 39.00 43.00 46.25 47.25Forward 134.39 142.32 133.38 133.38Forecast 114.00 119.00 119.00 119.00Forward 156.76 153.01 136.95 146.29Forecast 137.65 140.50 145.50 148.00Forward 385.26 392.41 396.56 403.75Forecast 372.00 372.50 377.50 373.00Forward 1,006.45 1,021.57 1,008.38 1,001.80Forecast 903.00 893.00 900.00 881.00Forward 481.11 500.21 518.97 535.15Forecast 475.00 479.00 488.00 463.00Forward 4,996 5,049 5,044 5,041Forecast 4,764 4,900 5,000 5,018Forward 1,644 1,681 1,681 1,682Forecast 1,546 1,579 1,600 1,622Forward 1,910 1,942 1,947 1,948Forecast 1,800 1,805 1,875 1,925Forward 9,248 9,461 9,496 9,532Forecast 8,813 9,175 9,626 9,813Forward 1,275 1,293 1,296 1,299Forecast 1,200 1,180 1,200 1,150Forward 17.32 17.85 17.93 17.99Forecast 15.30 15.25 15.20 15.17Forward 15.89 16.59 17.02 16.90Forecast 14.50 14.70 15.00 15.27Forward 121.85 123.30 126.05 128.28Forecast 127.50 125.00 129.50 132.00Forward 63.07 63.48 62.84 63.06Forecast 62.00 60.40 63.00 62.10

Energy

Livestock

Softs

Precious Metals

Industrial Metals

Grains

Coffee

Cotton

Zinc

Nickel

Gold

Silver

Sugar

Softs

Bloomberg survey of commodity analysts

Energy

Grains

Industrial Metals

Precious Metals

Natural Gas

WTI Crude

Brent Crude

ULS Diesel

Gasoline

Corn

Soybeans

Wheat

Copper

Aluminum

11

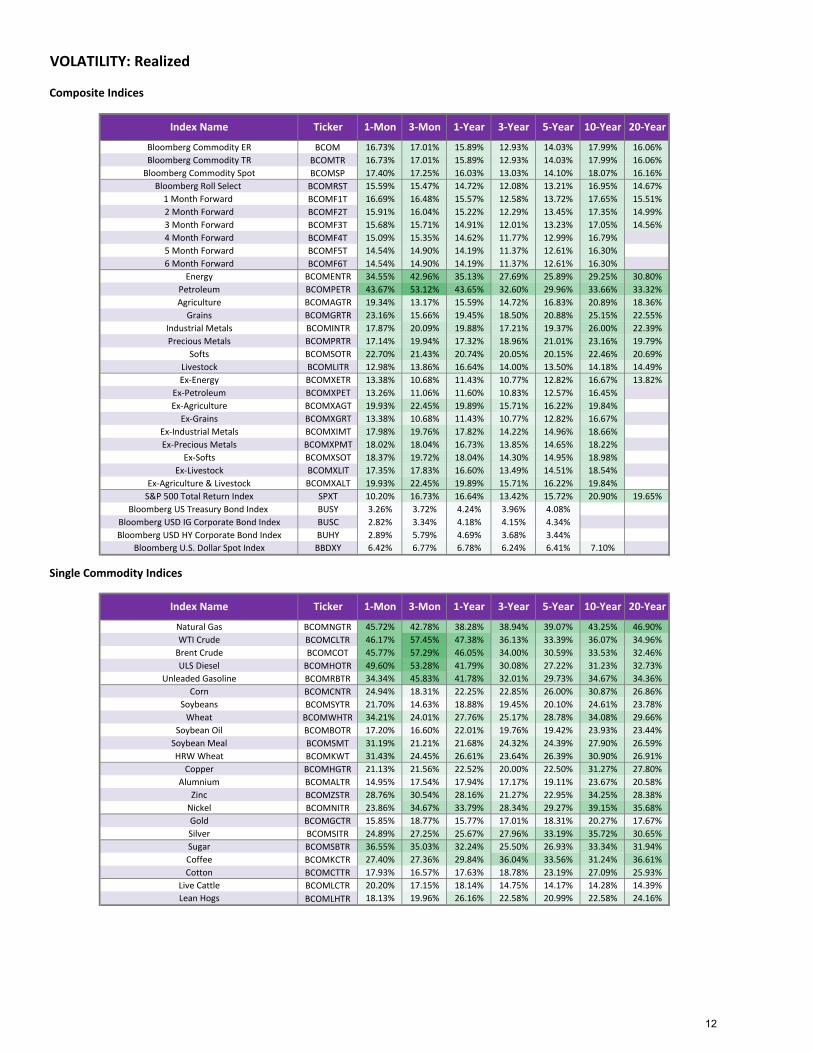

Composite Indices

Bloomberg Commodity ER BCOM 16.73% 17.01% 15.89% 12.93% 14.03% 17.99% 16.06%Bloomberg Commodity TR BCOMTR 16.73% 17.01% 15.89% 12.93% 14.03% 17.99% 16.06%

Bloomberg Commodity Spot BCOMSP 17.40% 17.25% 16.03% 13.03% 14.10% 18.07% 16.16%Bloomberg Roll Select BCOMRST 15.59% 15.47% 14.72% 12.08% 13.21% 16.95% 14.67%

1 Month Forward BCOMF1T 16.69% 16.48% 15.57% 12.58% 13.72% 17.65% 15.51% 2 Month Forward BCOMF2T 15.91% 16.04% 15.22% 12.29% 13.45% 17.35% 14.99% 3 Month Forward BCOMF3T 15.68% 15.71% 14.91% 12.01% 13.23% 17.05% 14.56% 4 Month Forward BCOMF4T 15.09% 15.35% 14.62% 11.77% 12.99% 16.79% 5 Month Forward BCOMF5T 14.54% 14.90% 14.19% 11.37% 12.61% 16.30% 6 Month Forward BCOMF6T 14.54% 14.90% 14.19% 11.37% 12.61% 16.30%

Energy BCOMENTR 34.55% 42.96% 35.13% 27.69% 25.89% 29.25% 30.80%Petroleum BCOMPETR 43.67% 53.12% 43.65% 32.60% 29.96% 33.66% 33.32%Agriculture BCOMAGTR 19.34% 13.17% 15.59% 14.72% 16.83% 20.89% 18.36%

Grains BCOMGRTR 23.16% 15.66% 19.45% 18.50% 20.88% 25.15% 22.55%Industrial Metals BCOMINTR 17.87% 20.09% 19.88% 17.21% 19.37% 26.00% 22.39%Precious Metals BCOMPRTR 17.14% 19.94% 17.32% 18.96% 21.01% 23.16% 19.79%

Softs BCOMSOTR 22.70% 21.43% 20.74% 20.05% 20.15% 22.46% 20.69%Livestock BCOMLITR 12.98% 13.86% 16.64% 14.00% 13.50% 14.18% 14.49%Ex-Energy BCOMXETR 13.38% 10.68% 11.43% 10.77% 12.82% 16.67% 13.82%

Ex-Petroleum BCOMXPET 13.26% 11.06% 11.60% 10.83% 12.57% 16.45%Ex-Agriculture BCOMXAGT 19.93% 22.45% 19.89% 15.71% 16.22% 19.84%

Ex-Grains BCOMXGRT 13.38% 10.68% 11.43% 10.77% 12.82% 16.67%Ex-Industrial Metals BCOMXIMT 17.98% 19.76% 17.82% 14.22% 14.96% 18.66%Ex-Precious Metals BCOMXPMT 18.02% 18.04% 16.73% 13.85% 14.65% 18.22%

Ex-Softs BCOMXSOT 18.37% 19.72% 18.04% 14.30% 14.95% 18.98%Ex-Livestock BCOMXLIT 17.35% 17.83% 16.60% 13.49% 14.51% 18.54%

Ex-Agriculture & Livestock BCOMXALT 19.93% 22.45% 19.89% 15.71% 16.22% 19.84%S&P 500 Total Return Index SPXT 10.20% 16.73% 16.64% 13.42% 15.72% 20.90% 19.65%

Bloomberg US Treasury Bond Index BUSY 3.26% 3.72% 4.24% 3.96% 4.08%Bloomberg USD IG Corporate Bond Index BUSC 2.82% 3.34% 4.18% 4.15% 4.34%Bloomberg USD HY Corporate Bond Index BUHY 2.89% 5.79% 4.69% 3.68% 3.44%

Bloomberg U.S. Dollar Spot Index BBDXY 6.42% 6.77% 6.78% 6.24% 6.41% 7.10%

Single Commodity Indices

Natural Gas BCOMNGTR 45.72% 42.78% 38.28% 38.94% 39.07% 43.25% 46.90%WTI Crude BCOMCLTR 46.17% 57.45% 47.38% 36.13% 33.39% 36.07% 34.96%

Brent Crude BCOMCOT 45.77% 57.29% 46.05% 34.00% 30.59% 33.53% 32.46%ULS Diesel BCOMHOTR 49.60% 53.28% 41.79% 30.08% 27.22% 31.23% 32.73%

Unleaded Gasoline BCOMRBTR 34.34% 45.83% 41.78% 32.01% 29.73% 34.67% 34.36%Corn BCOMCNTR 24.94% 18.31% 22.25% 22.85% 26.00% 30.87% 26.86%

Soybeans BCOMSYTR 21.70% 14.63% 18.88% 19.45% 20.10% 24.61% 23.78%Wheat BCOMWHTR 34.21% 24.01% 27.76% 25.17% 28.78% 34.08% 29.66%

Soybean Oil BCOMBOTR 17.20% 16.60% 22.01% 19.76% 19.42% 23.93% 23.44%Soybean Meal BCOMSMT 31.19% 21.21% 21.68% 24.32% 24.39% 27.90% 26.59%HRW Wheat BCOMKWT 31.43% 24.45% 26.61% 23.64% 26.39% 30.90% 26.91%

Copper BCOMHGTR 21.13% 21.56% 22.52% 20.00% 22.50% 31.27% 27.80%Alumnium BCOMALTR 14.95% 17.54% 17.94% 17.17% 19.11% 23.67% 20.58%

Zinc BCOMZSTR 28.76% 30.54% 28.16% 21.27% 22.95% 34.25% 28.38%Nickel BCOMNITR 23.86% 34.67% 33.79% 28.34% 29.27% 39.15% 35.68%Gold BCOMGCTR 15.85% 18.77% 15.77% 17.01% 18.31% 20.27% 17.67%Silver BCOMSITR 24.89% 27.25% 25.67% 27.96% 33.19% 35.72% 30.65%Sugar BCOMSBTR 36.55% 35.03% 32.24% 25.50% 26.93% 33.34% 31.94%Coffee BCOMKCTR 27.40% 27.36% 29.84% 36.04% 33.56% 31.24% 36.61%Cotton BCOMCTTR 17.93% 16.57% 17.63% 18.78% 23.19% 27.09% 25.93%

Live Cattle BCOMLCTR 20.20% 17.15% 18.14% 14.75% 14.17% 14.28% 14.39%Lean Hogs BCOMLHTR 18.13% 19.96% 26.16% 22.58% 20.99% 22.58% 24.16%

VOLATILITY: Realized

Index Name Ticker

Index Name Ticker

3-Mon 1-Year 3-Year1-Mon

1-Mon 3-Mon 1-Year 3-Year 5-Year 10-Year

5-Year 10-Year 20-Year

20-Year

12

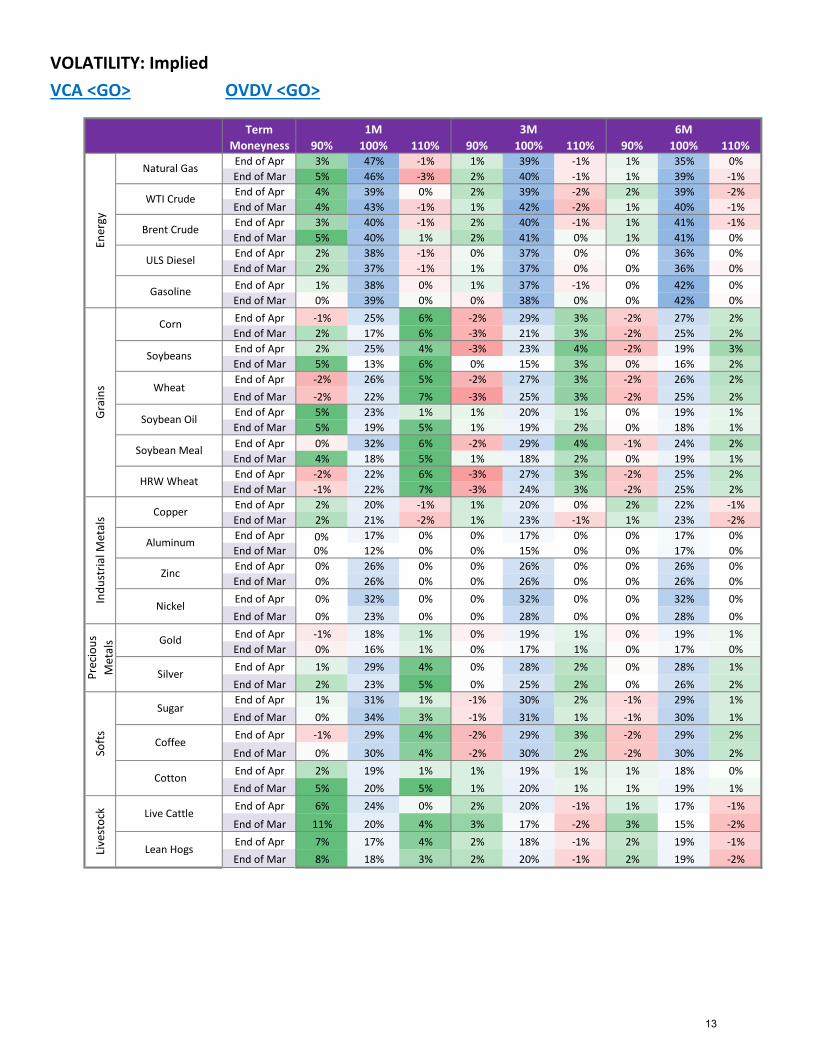

VOLATILITY: ImpliedVCA <GO> OVDV <GO>

TermMoneyness 90% 100% 110% 90% 100% 110% 90% 100% 110%End of Apr 3% 47% -1% 1% 39% -1% 1% 35% 0%End of Mar 5% 46% -3% 2% 40% -1% 1% 39% -1%End of Apr 4% 39% 0% 2% 39% -2% 2% 39% -2%End of Mar 4% 43% -1% 1% 42% -2% 1% 40% -1%End of Apr 3% 40% -1% 2% 40% -1% 1% 41% -1%End of Mar 5% 40% 1% 2% 41% 0% 1% 41% 0%End of Apr 2% 38% -1% 0% 37% 0% 0% 36% 0%End of Mar 2% 37% -1% 1% 37% 0% 0% 36% 0%End of Apr 1% 38% 0% 1% 37% -1% 0% 42% 0%End of Mar 0% 39% 0% 0% 38% 0% 0% 42% 0%End of Apr -1% 25% 6% -2% 29% 3% -2% 27% 2%End of Mar 2% 17% 6% -3% 21% 3% -2% 25% 2%End of Apr 2% 25% 4% -3% 23% 4% -2% 19% 3%End of Mar 5% 13% 6% 0% 15% 3% 0% 16% 2%End of Apr -2% 26% 5% -2% 27% 3% -2% 26% 2%End of Mar -2% 22% 7% -3% 25% 3% -2% 25% 2%End of Apr 5% 23% 1% 1% 20% 1% 0% 19% 1%End of Mar 5% 19% 5% 1% 19% 2% 0% 18% 1%End of Apr 0% 32% 6% -2% 29% 4% -1% 24% 2%End of Mar 4% 18% 5% 1% 18% 2% 0% 19% 1%End of Apr -2% 22% 6% -3% 27% 3% -2% 25% 2%End of Mar -1% 22% 7% -3% 24% 3% -2% 25% 2%End of Apr 2% 20% -1% 1% 20% 0% 2% 22% -1%End of Mar 2% 21% -2% 1% 23% -1% 1% 23% -2%End of Apr 0% 17% 0% 0% 17% 0% 0% 17% 0%End of Mar 0% 12% 0% 0% 15% 0% 0% 17% 0%End of Apr 0% 26% 0% 0% 26% 0% 0% 26% 0%End of Mar 0% 26% 0% 0% 26% 0% 0% 26% 0%End of Apr 0% 32% 0% 0% 32% 0% 0% 32% 0%End of Mar 0% 23% 0% 0% 28% 0% 0% 28% 0%End of Apr -1% 18% 1% 0% 19% 1% 0% 19% 1%End of Mar 0% 16% 1% 0% 17% 1% 0% 17% 0%End of Apr 1% 29% 4% 0% 28% 2% 0% 28% 1%End of Mar 2% 23% 5% 0% 25% 2% 0% 26% 2%End of Apr 1% 31% 1% -1% 30% 2% -1% 29% 1%End of Mar 0% 34% 3% -1% 31% 1% -1% 30% 1%End of Apr -1% 29% 4% -2% 29% 3% -2% 29% 2%End of Mar 0% 30% 4% -2% 30% 2% -2% 30% 2%End of Apr 2% 19% 1% 1% 19% 1% 1% 18% 0%End of Mar 5% 20% 5% 1% 20% 1% 1% 19% 1%End of Apr 6% 24% 0% 2% 20% -1% 1% 17% -1%End of Mar 11% 20% 4% 3% 17% -2% 3% 15% -2%End of Apr 7% 17% 4% 2% 18% -1% 2% 19% -1%End of Mar 8% 18% 3% 2% 20% -1% 2% 19% -2%

3M 6M

Corn

Soybeans

Wheat

1M

Live

stoc

k Live Cattle

Lean Hogs

Gra

ins

Prec

ious

M

etal

s Gold

Silver

Soft

s

Sugar

Coffee

Cotton

Soybean Oil

Soybean Meal

HRW Wheat

Indu

stria

l Met

als Copper

Aluminum

Zinc

Nickel

Ener

gy

Natural Gas

WTI Crude

Brent Crude

ULS Diesel

Gasoline

13

Bloomberg Commodity Energy Subindices Bloomberg Commodity Grains Subindices

VOLATILITY: Historical 1-Year RealizedBloomberg Commodity Composite Indices Bloomberg Commodity Forward Indices

Commodities vs. Equities vs. Bonds vs. USD Bloomberg Commodity Group Subindices

Bloomberg Commodity Industrial Metals Subindices Bloomberg Commodity Precious Metals Subindices

Bloomberg Commodity Softs Subindices Bloomberg Commodity Livestock Subindices

5%

10%

15%

20%

25%

30%

35%

92 94 96 98 00 02 04 06 08 10 12 14

BloombergCommodity Index ER

BloombergCommodity Index TR

BloombergCommodity IndexSpotBloombergCommodity IndexRoll Select

5%

10%

15%

20%

25%

30%

35%

02 03 04 05 06 07 08 09 10 11 12 13 14 15

Bloomberg CommodityIndex TR

Bloomberg CommodityIndex 1 MonthForwardBloomberg CommodityIndex 3 MonthForwardBloomberg CommodityIndex 6 MonthForward

0%

5%

10%

15%

20%

25%

11 12 13 14 15 16

BloombergCommodity Index TRS&P 500 Total ReturnIndexBloomberg USTreasury Bond IndexBloomberg USCorporate Bond IndexBloomberg USD HYCorporate Bond IndexBloomberg U.S. DollarSpot Index

5%10%15%20%25%30%35%40%45%50%

92 94 96 98 00 02 04 06 08 10 12 14

Energy

Grains

Industrial Metals

Precious Metals

Softs

Livestock

10%

20%

30%

40%

50%

60%

70%

92 94 96 98 00 02 04 06 08 10 12 14

Natural Gas

WTI Crude

Brent Crude

ULS Diesel

Unleaded Gasoline10%

15%

20%

25%

30%

35%

40%

45%

50%

92 94 96 98 00 02 04 06 08 10 12 14

Corn

Soybeans

Wheat

Soybean Oil

Soybean Meal

HRW Wheat

10%

20%

30%

40%

50%

60%

70%

92 94 96 98 00 02 04 06 08 10 12 14

Copper

Alumnium

Zinc

Nickel0%

10%

20%

30%

40%

50%

60%

92 94 96 98 00 02 04 06 08 10 12 14

Gold

Silver

10%

20%

30%

40%

50%

60%

92 94 96 98 00 02 04 06 08 10 12 14

Sugar

Coffee

Cotton

5%

10%

15%

20%

25%

30%

35%

40%

92 94 96 98 00 02 04 06 08 10 12 14

Live Cattle

Lean Hogs

14

Bloo

mbe

rg

Com

mod

ity

Roll

Sele

ct

1 M

onth

Fo

rwar

d

3 M

onth

Fo

rwar

d

6 M

onth

Fo

rwar

d

Ener

gy

Petr

oleu

m

Agric

ultu

re

Gra

ins

Indu

stria

l M

etal

s

Prec

ious

M

etal

s

Soft

s

Live

stoc

k

Ex-E

nerg

y

Ex-A

gs &

Li

vest

ock

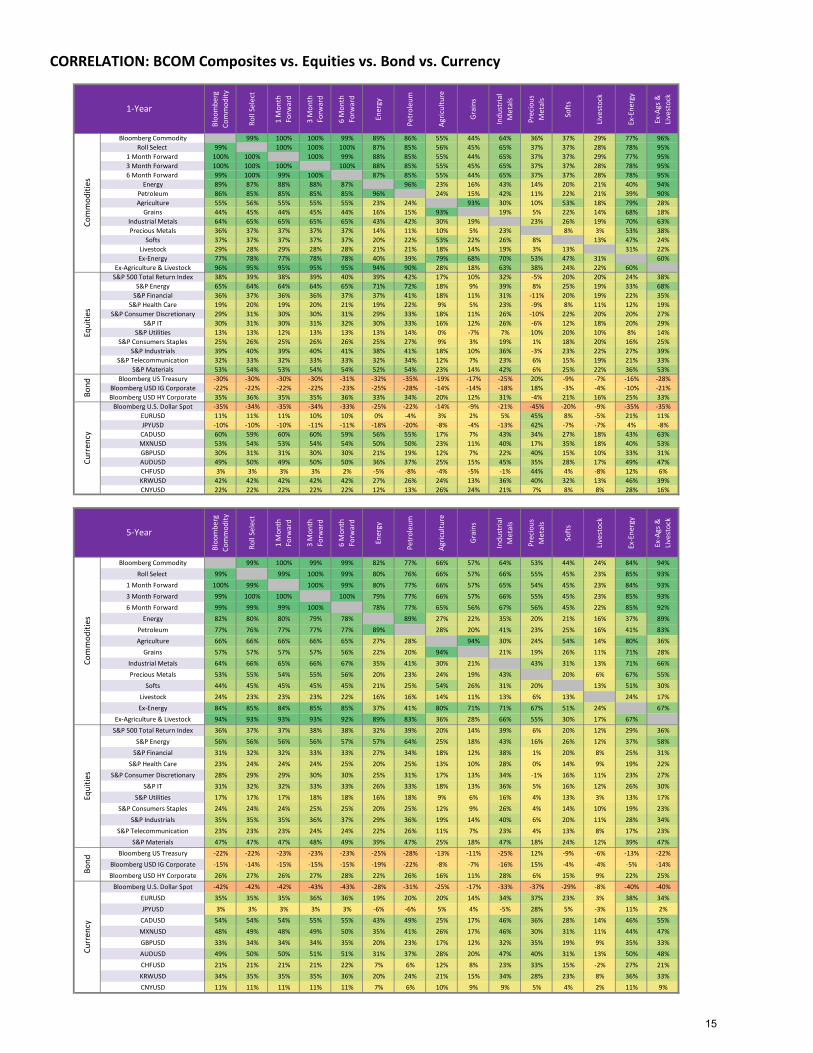

Bloomberg Commodity 99% 100% 100% 99% 89% 86% 55% 44% 64% 36% 37% 29% 77% 96%Roll Select 99% 100% 100% 100% 87% 85% 56% 45% 65% 37% 37% 28% 78% 95%

1 Month Forward 100% 100% 100% 99% 88% 85% 55% 44% 65% 37% 37% 29% 77% 95%3 Month Forward 100% 100% 100% 100% 88% 85% 55% 45% 65% 37% 37% 28% 78% 95%6 Month Forward 99% 100% 99% 100% 87% 85% 55% 44% 65% 37% 37% 28% 78% 95%

Energy 89% 87% 88% 88% 87% 96% 23% 16% 43% 14% 20% 21% 40% 94%Petroleum 86% 85% 85% 85% 85% 96% 24% 15% 42% 11% 22% 21% 39% 90%Agriculture 55% 56% 55% 55% 55% 23% 24% 93% 30% 10% 53% 18% 79% 28%

Grains 44% 45% 44% 45% 44% 16% 15% 93% 19% 5% 22% 14% 68% 18%Industrial Metals 64% 65% 65% 65% 65% 43% 42% 30% 19% 23% 26% 19% 70% 63%Precious Metals 36% 37% 37% 37% 37% 14% 11% 10% 5% 23% 8% 3% 53% 38%

Softs 37% 37% 37% 37% 37% 20% 22% 53% 22% 26% 8% 13% 47% 24%Livestock 29% 28% 29% 28% 28% 21% 21% 18% 14% 19% 3% 13% 31% 22%Ex-Energy 77% 78% 77% 78% 78% 40% 39% 79% 68% 70% 53% 47% 31% 60%

Ex-Agriculture & Livestock 96% 95% 95% 95% 95% 94% 90% 28% 18% 63% 38% 24% 22% 60%S&P 500 Total Return Index 38% 39% 38% 39% 40% 39% 42% 17% 10% 32% -5% 20% 20% 24% 38%

S&P Energy 65% 64% 64% 64% 65% 71% 72% 18% 9% 39% 8% 25% 19% 33% 68%S&P Financial 36% 37% 36% 36% 37% 37% 41% 18% 11% 31% -11% 20% 19% 22% 35%

S&P Health Care 19% 20% 19% 20% 21% 19% 22% 9% 5% 23% -9% 8% 11% 12% 19%S&P Consumer Discretionary 29% 31% 30% 30% 31% 29% 33% 18% 11% 26% -10% 22% 20% 20% 27%

S&P IT 30% 31% 30% 31% 32% 30% 33% 16% 12% 26% -6% 12% 18% 20% 29%S&P Utilities 13% 13% 12% 13% 13% 13% 14% 0% -7% 7% 10% 20% 10% 8% 14%

S&P Consumers Staples 25% 26% 25% 26% 26% 25% 27% 9% 3% 19% 1% 18% 20% 16% 25%S&P Industrials 39% 40% 39% 40% 41% 38% 41% 18% 10% 36% -3% 23% 22% 27% 39%

S&P Telecommunication 32% 33% 32% 33% 33% 32% 34% 12% 7% 23% 6% 15% 19% 21% 33%S&P Materials 53% 54% 53% 54% 54% 52% 54% 23% 14% 42% 6% 25% 22% 36% 53%

Bloomberg US Treasury -30% -30% -30% -30% -31% -32% -35% -19% -17% -25% 20% -9% -7% -16% -28%Bloomberg USD IG Corporate -22% -22% -22% -22% -23% -25% -28% -14% -14% -18% 18% -3% -4% -10% -21%Bloomberg USD HY Corporate 35% 36% 35% 35% 36% 33% 34% 20% 12% 31% -4% 21% 16% 25% 33%

Bloomberg U.S. Dollar Spot -35% -34% -35% -34% -33% -25% -22% -14% -9% -21% -45% -20% -9% -35% -35%EURUSD 11% 11% 11% 10% 10% 0% -4% 3% 2% 5% 45% 8% -5% 21% 11%JPYUSD -10% -10% -10% -11% -11% -18% -20% -8% -4% -13% 42% -7% -7% 4% -8%CADUSD 60% 59% 60% 60% 59% 56% 55% 17% 7% 43% 34% 27% 18% 43% 63%MXNUSD 53% 54% 53% 54% 54% 50% 50% 23% 11% 40% 17% 35% 18% 40% 53%GBPUSD 30% 31% 31% 30% 30% 21% 19% 12% 7% 22% 40% 15% 10% 33% 31%AUDUSD 49% 50% 49% 50% 50% 36% 37% 25% 15% 45% 35% 28% 17% 49% 47%CHFUSD 3% 3% 3% 3% 2% -5% -8% -4% -5% -1% 44% 4% -8% 12% 6%KRWUSD 42% 42% 42% 42% 42% 27% 26% 24% 13% 36% 40% 32% 13% 46% 39%CNYUSD 22% 22% 22% 22% 22% 12% 13% 26% 24% 21% 7% 8% 8% 28% 16%

Bloo

mbe

rg

Com

mod

ity

Roll

Sele

ct

1 M

onth

Fo

rwar

d

3 M

onth

Fo

rwar

d

6 M

onth

Fo

rwar

d

Ener

gy

Petr

oleu

m

Agric

ultu

re

Gra

ins

Indu

stria

l M

etal

s

Prec

ious

M

etal

s

Soft

s

Live

stoc

k

Ex-E

nerg

y

Ex-A

gs &

Li

vest

ock

Bloomberg Commodity 99% 100% 99% 99% 82% 77% 66% 57% 64% 53% 44% 24% 84% 94%Roll Select 99% 99% 100% 99% 80% 76% 66% 57% 66% 55% 45% 23% 85% 93%

1 Month Forward 100% 99% 100% 99% 80% 77% 66% 57% 65% 54% 45% 23% 84% 93%3 Month Forward 99% 100% 100% 100% 79% 77% 66% 57% 66% 55% 45% 23% 85% 93%6 Month Forward 99% 99% 99% 100% 78% 77% 65% 56% 67% 56% 45% 22% 85% 92%

Energy 82% 80% 80% 79% 78% 89% 27% 22% 35% 20% 21% 16% 37% 89%Petroleum 77% 76% 77% 77% 77% 89% 28% 20% 41% 23% 25% 16% 41% 83%Agriculture 66% 66% 66% 66% 65% 27% 28% 94% 30% 24% 54% 14% 80% 36%

Grains 57% 57% 57% 57% 56% 22% 20% 94% 21% 19% 26% 11% 71% 28%Industrial Metals 64% 66% 65% 66% 67% 35% 41% 30% 21% 43% 31% 13% 71% 66%Precious Metals 53% 55% 54% 55% 56% 20% 23% 24% 19% 43% 20% 6% 67% 55%

Softs 44% 45% 45% 45% 45% 21% 25% 54% 26% 31% 20% 13% 51% 30%Livestock 24% 23% 23% 23% 22% 16% 16% 14% 11% 13% 6% 13% 24% 17%Ex-Energy 84% 85% 84% 85% 85% 37% 41% 80% 71% 71% 67% 51% 24% 67%

Ex-Agriculture & Livestock 94% 93% 93% 93% 92% 89% 83% 36% 28% 66% 55% 30% 17% 67%S&P 500 Total Return Index 36% 37% 37% 38% 38% 32% 39% 20% 14% 39% 6% 20% 12% 29% 36%

S&P Energy 56% 56% 56% 56% 57% 57% 64% 25% 18% 43% 16% 26% 12% 37% 58%S&P Financial 31% 32% 32% 33% 33% 27% 34% 18% 12% 38% 1% 20% 8% 25% 31%

S&P Health Care 23% 24% 24% 24% 25% 20% 25% 13% 10% 28% 0% 14% 9% 19% 22%S&P Consumer Discretionary 28% 29% 29% 30% 30% 25% 31% 17% 13% 34% -1% 16% 11% 23% 27%

S&P IT 31% 32% 32% 33% 33% 26% 33% 18% 13% 36% 5% 16% 12% 26% 30%S&P Utilities 17% 17% 17% 18% 18% 16% 18% 9% 6% 16% 4% 13% 3% 13% 17%

S&P Consumers Staples 24% 24% 24% 25% 25% 20% 25% 12% 9% 26% 4% 14% 10% 19% 23%S&P Industrials 35% 35% 35% 36% 37% 29% 36% 19% 14% 40% 6% 20% 11% 28% 34%

S&P Telecommunication 23% 23% 23% 24% 24% 22% 26% 11% 7% 23% 4% 13% 8% 17% 23%S&P Materials 47% 47% 47% 48% 49% 39% 47% 25% 18% 47% 18% 24% 12% 39% 47%

Bloomberg US Treasury -22% -22% -23% -23% -23% -25% -28% -13% -11% -25% 12% -9% -6% -13% -22%Bloomberg USD IG Corporate -15% -14% -15% -15% -15% -19% -22% -8% -7% -16% 15% -4% -4% -5% -14%Bloomberg USD HY Corporate 26% 27% 26% 27% 28% 22% 26% 16% 11% 28% 6% 15% 9% 22% 25%

Bloomberg U.S. Dollar Spot -42% -42% -42% -43% -43% -28% -31% -25% -17% -33% -37% -29% -8% -40% -40%EURUSD 35% 35% 35% 36% 36% 19% 20% 20% 14% 34% 37% 23% 3% 38% 34%JPYUSD 3% 3% 3% 3% 3% -6% -6% 5% 4% -5% 28% 5% -3% 11% 2%CADUSD 54% 54% 54% 55% 55% 43% 49% 25% 17% 46% 36% 28% 14% 46% 55%MXNUSD 48% 49% 48% 49% 50% 35% 41% 26% 17% 46% 30% 31% 11% 44% 47%GBPUSD 33% 34% 34% 34% 35% 20% 23% 17% 12% 32% 35% 19% 9% 35% 33%AUDUSD 49% 50% 50% 51% 51% 31% 37% 28% 20% 47% 40% 31% 13% 50% 48%CHFUSD 21% 21% 21% 21% 22% 7% 6% 12% 8% 23% 33% 15% -2% 27% 21%KRWUSD 34% 35% 35% 35% 36% 20% 24% 21% 15% 34% 28% 23% 8% 36% 33%CNYUSD 11% 11% 11% 11% 11% 7% 6% 10% 9% 9% 5% 4% 2% 11% 9%

Bond

Curr

ency

Bond

CORRELATION: BCOM Composites vs. Equities vs. Bond vs. Currency Cu

rren

cyCo

mm

oditi

esEq

uitie

s

5-Year

1-Year

Com

mod

ities

Equi

ties

15

Nat

ural

Gas

WTI

Cru

de

Bren

t Cru

de

ULS

Die

sel

Unl

eade

d G

asol

ine

Corn

Soyb

eans

Whe

at

Soyb

ean

Oil

Soyb

ean

Mea

l

HRW

Whe

at

Copp

er

Alum

nium

Zinc

Nic

kel

Gol

d

Silv

er

Suga

r

Coffe

e

Cott

on

Live

Cat

tle

Lean

Hog

s

Natural Gas 17% 17% 16% 11% 5% 4% 7% 12% 0% 5% 16% 15% 11% 12% 13% 13% -2% 0% 1% 5% 7%WTI Crude 17% 97% 93% 83% 14% 21% 4% 36% 8% 7% 43% 31% 24% 37% 2% 23% 13% 29% 15% 19% 15%

Brent Crude 17% 97% 96% 86% 15% 20% 4% 35% 8% 8% 42% 30% 24% 36% 1% 22% 9% 29% 16% 17% 13%ULS Diesel 16% 93% 96% 82% 16% 22% 6% 33% 10% 9% 40% 30% 23% 32% 5% 24% 9% 27% 15% 16% 16%

Unleaded Gasoline 11% 83% 86% 82% 11% 16% 2% 32% 5% 6% 39% 28% 20% 28% 2% 20% 4% 20% 18% 11% 11%Corn 5% 14% 15% 16% 11% 67% 68% 34% 60% 65% 15% 9% 6% 14% -3% 5% 12% 18% 15% 8% 12%

Soybeans 4% 21% 20% 22% 16% 67% 45% 56% 87% 43% 31% 25% 22% 29% 3% 24% 8% 32% 25% 16% 12%Wheat 7% 4% 4% 6% 2% 68% 45% 21% 41% 95% 9% 0% 0% 2% 5% 7% 7% 22% 17% 5% 5%

Soybean Oil 12% 36% 35% 33% 32% 34% 56% 21% 18% 19% 37% 33% 28% 31% 10% 33% 3% 35% 28% 23% 12%Soybean Meal 0% 8% 8% 10% 5% 60% 87% 41% 18% 38% 22% 16% 16% 17% 1% 14% 6% 20% 16% 6% 7%HRW Wheat 5% 7% 8% 9% 6% 65% 43% 95% 19% 38% 10% 0% -1% 4% 3% 5% 6% 18% 14% 6% 7%

Copper 16% 43% 42% 40% 39% 15% 31% 9% 37% 22% 10% 60% 65% 67% 12% 36% 16% 26% 23% 16% 16%Alumnium 15% 31% 30% 30% 28% 9% 25% 0% 33% 16% 0% 60% 62% 55% 8% 26% 6% 16% 22% 13% 13%

Zinc 11% 24% 24% 23% 20% 6% 22% 0% 28% 16% -1% 65% 62% 53% 21% 32% 10% 19% 15% 7% 11%Nickel 12% 37% 36% 32% 28% 14% 29% 2% 31% 17% 4% 67% 55% 53% 5% 26% 10% 20% 23% 5% 5%Gold 13% 2% 1% 5% 2% -3% 3% 5% 10% 1% 3% 12% 8% 21% 5% 77% 1% 2% 2% -3% 3%Silver 13% 23% 22% 24% 20% 5% 24% 7% 33% 14% 5% 36% 26% 32% 26% 77% 10% 19% 15% 7% 4%Sugar -2% 13% 9% 9% 4% 12% 8% 7% 3% 6% 6% 16% 6% 10% 10% 1% 10% 23% 6% 5% 10%Coffee 0% 29% 29% 27% 20% 18% 32% 22% 35% 20% 18% 26% 16% 19% 20% 2% 19% 23% 18% 10% 8%Cotton 1% 15% 16% 15% 18% 15% 25% 17% 28% 16% 14% 23% 22% 15% 23% 2% 15% 6% 18% 6% 4%

Live Cattle 5% 19% 17% 16% 11% 8% 16% 5% 23% 6% 6% 16% 13% 7% 5% -3% 7% 5% 10% 6% 26%Lean Hogs 7% 15% 13% 16% 11% 12% 12% 5% 12% 7% 7% 16% 13% 11% 5% 3% 4% 10% 8% 4% 26%

S&P 500 Total Return Index 3% 42% 43% 40% 36% 10% 15% 1% 21% 5% 4% 31% 22% 21% 33% -13% 9% 7% 27% 18% 24% 6%S&P Energy 18% 73% 71% 70% 61% 9% 14% 1% 28% 0% 7% 39% 29% 23% 36% -1% 22% 13% 28% 17% 20% 9%

S&P Financial 3% 41% 41% 39% 34% 11% 17% 1% 19% 7% 4% 29% 22% 20% 34% -20% 6% 7% 28% 18% 24% 3%S&P Health Care -2% 22% 23% 22% 18% 5% 11% -2% 13% 4% -1% 20% 19% 16% 24% -14% 2% 0% 14% 12% 14% 1%

S&P Consumer Discretionary -3% 33% 34% 32% 28% 11% 14% 3% 16% 6% 5% 25% 18% 16% 27% -16% 3% 10% 27% 17% 22% 9%S&P IT 0% 33% 34% 31% 30% 11% 15% 4% 21% 6% 7% 25% 16% 20% 28% -12% 5% 0% 24% 13% 23% 4%

S&P Utilities 2% 14% 15% 15% 10% -6% -4% -6% 1% -9% -7% 10% -3% 6% 7% 8% 14% 10% 22% 16% 14% 1%S&P Consumers Staples 6% 26% 28% 26% 21% 4% 7% -3% 12% -1% -1% 20% 10% 13% 21% -4% 10% 8% 20% 19% 25% 5%

S&P Industrials 5% 41% 41% 38% 35% 10% 14% 2% 18% 5% 5% 37% 21% 24% 34% -12% 13% 11% 28% 14% 25% 8%S&P Telecommunication 5% 33% 36% 34% 27% 8% 9% 1% 14% -1% 3% 24% 14% 15% 22% 0% 15% 2% 25% 21% 24% 4%

S&P Materials 11% 54% 54% 51% 45% 13% 20% 3% 27% 8% 6% 43% 29% 28% 37% -4% 22% 11% 32% 18% 24% 9%Bloomberg US Treasury 1% -37% -35% -33% -28% -16% -20% -8% -16% -17% -9% -28% -20% -8% -24% 26% 7% 0% -21% -9% -9% -1%

Bloomberg USD IG Corporate 3% -30% -28% -26% -21% -14% -13% -8% -11% -12% -7% -21% -15% -2% -18% 21% 10% 4% -14% -4% -4% -3%Bloomberg USD HY Corporate 7% 34% 36% 34% 25% 9% 19% 5% 14% 17% 7% 29% 25% 24% 24% -12% 11% 11% 24% 15% 23% -1%

Bloomberg U.S. Dollar Spot -16% -24% -20% -22% -16% -6% -5% -14% -7% -3% -10% -24% -11% -17% -9% -45% -39% -10% -21% -15% -1% -13%EURUSD 12% -2% -5% -2% -6% -1% -4% 10% 1% -5% 7% 9% -1% 5% -3% 48% 33% 3% 6% 13% -10% 3%JPYUSD 0% -20% -21% -18% -16% -3% -13% 6% -21% -3% 4% -11% -9% -6% -19% 51% 19% -1% -10% -10% -15% 6%CADUSD 20% 56% 54% 53% 43% 3% 11% 5% 24% 2% 5% 40% 33% 35% 34% 27% 42% 15% 30% 15% 15% 11%MXNUSD 13% 52% 50% 48% 41% 7% 18% 5% 22% 11% 5% 39% 27% 31% 35% 9% 30% 23% 34% 11% 18% 10%GBPUSD 12% 22% 16% 16% 14% 4% 8% 8% 10% 5% 3% 25% 13% 18% 10% 38% 39% 6% 17% 14% 10% 6%AUDUSD 8% 37% 36% 36% 32% 10% 21% 9% 28% 13% 7% 44% 30% 41% 30% 28% 42% 14% 36% 13% 17% 9%CHFUSD 6% -5% -9% -7% -10% -6% -12% 6% 0% -13% 4% 1% -4% 3% -8% 48% 30% 4% -1% 8% -14% 2%KRWUSD 11% 28% 25% 25% 21% 10% 16% 9% 20% 12% 6% 35% 22% 34% 26% 33% 47% 23% 29% 10% 11% 9%CNYUSD 2% 16% 13% 13% 3% 22% 26% 15% 19% 25% 13% 20% 13% 19% 18% 3% 11% 2% 16% 3% 7% 4%

Nat

ural

Gas

WTI

Cru

de

Bren

t Cru

de

ULS

Die

sel

Unl

eade

d G

asol

ine

Corn

Soyb

eans

Whe

at

Soyb

ean

Oil

Soyb

ean

Mea

l

HRW

Whe

at

Copp

er

Alum

nium

Zinc

Nic

kel

Gol

d

Silv

er

Suga

r

Coffe

e

Cott

on

Live

Cat

tle

Lean

Hog

s

Natural Gas 15% 14% 14% 12% 12% 5% 9% 8% 4% 10% 2% 6% 1% 2% 1% 4% 3% 3% 0% 4% 5%WTI Crude 15% 93% 88% 82% 17% 22% 13% 36% 13% 14% 42% 34% 30% 31% 18% 30% 19% 19% 21% 16% 12%

Brent Crude 14% 93% 96% 89% 16% 21% 12% 34% 12% 14% 38% 29% 27% 28% 15% 28% 16% 17% 20% 14% 10%ULS Diesel 14% 88% 96% 85% 16% 22% 12% 34% 14% 14% 36% 28% 26% 27% 16% 28% 16% 17% 20% 13% 11%

Unleaded Gasoline 12% 82% 89% 85% 14% 19% 11% 33% 10% 13% 34% 28% 24% 25% 16% 28% 12% 13% 19% 12% 8%Corn 12% 17% 16% 16% 14% 61% 70% 41% 54% 65% 15% 13% 10% 15% 12% 18% 18% 13% 17% 11% 6%

Soybeans 5% 22% 21% 22% 19% 61% 47% 65% 91% 45% 25% 21% 20% 19% 16% 24% 18% 14% 19% 10% 5%Wheat 9% 13% 12% 12% 11% 70% 47% 34% 41% 94% 14% 11% 10% 13% 13% 16% 18% 16% 19% 9% 2%

Soybean Oil 8% 36% 34% 34% 33% 41% 65% 34% 37% 32% 31% 28% 29% 25% 21% 31% 15% 19% 24% 15% 7%Soybean Meal 4% 13% 12% 14% 10% 54% 91% 41% 37% 39% 17% 14% 13% 11% 11% 17% 15% 8% 12% 5% 2%HRW Wheat 10% 14% 14% 14% 13% 65% 45% 94% 32% 39% 14% 10% 9% 13% 11% 15% 16% 14% 18% 9% 3%

Copper 2% 42% 38% 36% 34% 15% 25% 14% 31% 17% 14% 66% 71% 60% 36% 50% 21% 20% 23% 12% 10%Alumnium 6% 34% 29% 28% 28% 13% 21% 11% 28% 14% 10% 66% 69% 56% 30% 40% 18% 15% 19% 9% 8%

Zinc 1% 30% 27% 26% 24% 10% 20% 10% 29% 13% 9% 71% 69% 57% 30% 40% 20% 17% 16% 8% 8%Nickel 2% 31% 28% 27% 25% 15% 19% 13% 25% 11% 13% 60% 56% 57% 21% 31% 21% 15% 23% 7% 6%Gold 1% 18% 15% 16% 16% 12% 16% 13% 21% 11% 11% 36% 30% 30% 21% 82% 10% 14% 10% 4% 2%Silver 4% 30% 28% 28% 28% 18% 24% 16% 31% 17% 15% 50% 40% 40% 31% 82% 16% 20% 16% 8% 4%Sugar 3% 19% 16% 16% 12% 18% 18% 18% 15% 15% 16% 21% 18% 20% 21% 10% 16% 24% 15% 9% 9%Coffee 3% 19% 17% 17% 13% 13% 14% 16% 19% 8% 14% 20% 15% 17% 15% 14% 20% 24% 11% 6% 7%Cotton 0% 21% 20% 20% 19% 17% 19% 19% 24% 12% 18% 23% 19% 16% 23% 10% 16% 15% 11% 8% 4%

Live Cattle 4% 16% 14% 13% 12% 11% 10% 9% 15% 5% 9% 12% 9% 8% 7% 4% 8% 9% 6% 8% 31%Lean Hogs 5% 12% 10% 11% 8% 6% 5% 2% 7% 2% 3% 10% 8% 8% 6% 2% 4% 9% 7% 4% 31%

S&P 500 Total Return Index 1% 39% 37% 35% 33% 11% 17% 10% 22% 10% 12% 40% 30% 30% 29% 1% 14% 15% 12% 21% 13% 5%S&P Energy 13% 64% 61% 59% 54% 15% 19% 13% 28% 10% 16% 43% 33% 32% 31% 10% 24% 20% 16% 22% 13% 7%

S&P Financial 0% 34% 32% 30% 28% 8% 15% 9% 20% 9% 11% 38% 28% 28% 28% -4% 11% 15% 12% 20% 10% 3%S&P Health Care -1% 25% 24% 22% 20% 7% 12% 6% 15% 8% 7% 28% 23% 22% 21% -3% 7% 9% 8% 16% 11% 4%

S&P Consumer Discretionary -2% 31% 30% 28% 27% 10% 14% 10% 18% 9% 11% 35% 26% 25% 27% -5% 7% 12% 9% 18% 13% 4%S&P IT -2% 33% 32% 30% 29% 10% 16% 8% 21% 9% 10% 35% 28% 28% 27% 1% 12% 11% 10% 19% 14% 5%

S&P Utilities 3% 19% 17% 15% 14% 4% 5% 6% 8% 2% 8% 18% 10% 12% 10% 3% 6% 12% 5% 15% 6% 0%S&P Consumers Staples 1% 25% 24% 23% 20% 7% 10% 6% 14% 5% 8% 27% 19% 19% 20% 1% 9% 11% 6% 17% 11% 5%

S&P Industrials 0% 37% 34% 31% 31% 10% 17% 9% 21% 11% 12% 41% 30% 31% 29% 1% 14% 15% 11% 19% 11% 5%S&P Telecommunication 1% 25% 25% 24% 22% 6% 8% 6% 11% 4% 7% 24% 18% 18% 16% 1% 8% 10% 7% 15% 10% 3%

S&P Materials 3% 47% 44% 42% 40% 15% 19% 13% 26% 12% 15% 47% 36% 36% 33% 12% 25% 18% 15% 22% 14% 6%Bloomberg US Treasury -4% -29% -27% -25% -24% -7% -13% -7% -16% -8% -9% -27% -20% -16% -17% 17% 1% -5% -7% -10% -5% -5%

Bloomberg USD IG Corporate -3% -23% -21% -19% -18% -4% -8% -5% -11% -4% -6% -18% -13% -10% -10% 19% 6% -2% -3% -5% -3% -4%Bloomberg USD HY Corporate 1% 25% 27% 26% 20% 9% 15% 5% 17% 12% 6% 27% 22% 23% 21% 1% 12% 10% 10% 14% 11% 3%

Bloomberg U.S. Dollar Spot -7% -32% -29% -28% -25% -13% -17% -16% -18% -13% -16% -34% -27% -25% -20% -36% -34% -19% -21% -22% -5% -8%EURUSD 6% 22% 17% 18% 16% 9% 13% 15% 16% 9% 15% 34% 29% 25% 21% 36% 35% 14% 16% 20% -1% 6%JPYUSD -2% -6% -7% -6% -4% 5% 1% 5% -7% 5% 4% -5% -3% -4% -7% 32% 18% 3% 6% 0% -4% -1%CADUSD 6% 49% 47% 45% 40% 11% 21% 12% 29% 14% 13% 45% 36% 37% 33% 32% 38% 17% 23% 22% 11% 11%MXNUSD 4% 42% 39% 37% 35% 12% 21% 12% 25% 14% 13% 45% 37% 36% 34% 26% 33% 22% 21% 24% 10% 7%GBPUSD 3% 25% 21% 20% 18% 7% 14% 11% 16% 10% 11% 32% 26% 24% 20% 33% 33% 11% 15% 16% 8% 6%AUDUSD 2% 37% 35% 34% 31% 13% 24% 15% 28% 18% 16% 46% 35% 40% 33% 37% 41% 21% 24% 24% 11% 10%CHFUSD 3% 8% 5% 5% 5% 6% 4% 10% 10% 2% 10% 23% 21% 16% 14% 35% 28% 13% 8% 11% -6% 3%KRWUSD 2% 25% 22% 22% 20% 10% 17% 12% 21% 14% 11% 33% 26% 30% 26% 26% 29% 14% 18% 18% 6% 7%CNYUSD 3% 7% 7% 7% 3% 8% 8% 7% 9% 5% 8% 8% 7% 7% 11% 4% 5% -1% 8% 4% 3% 1%

Curr

ency

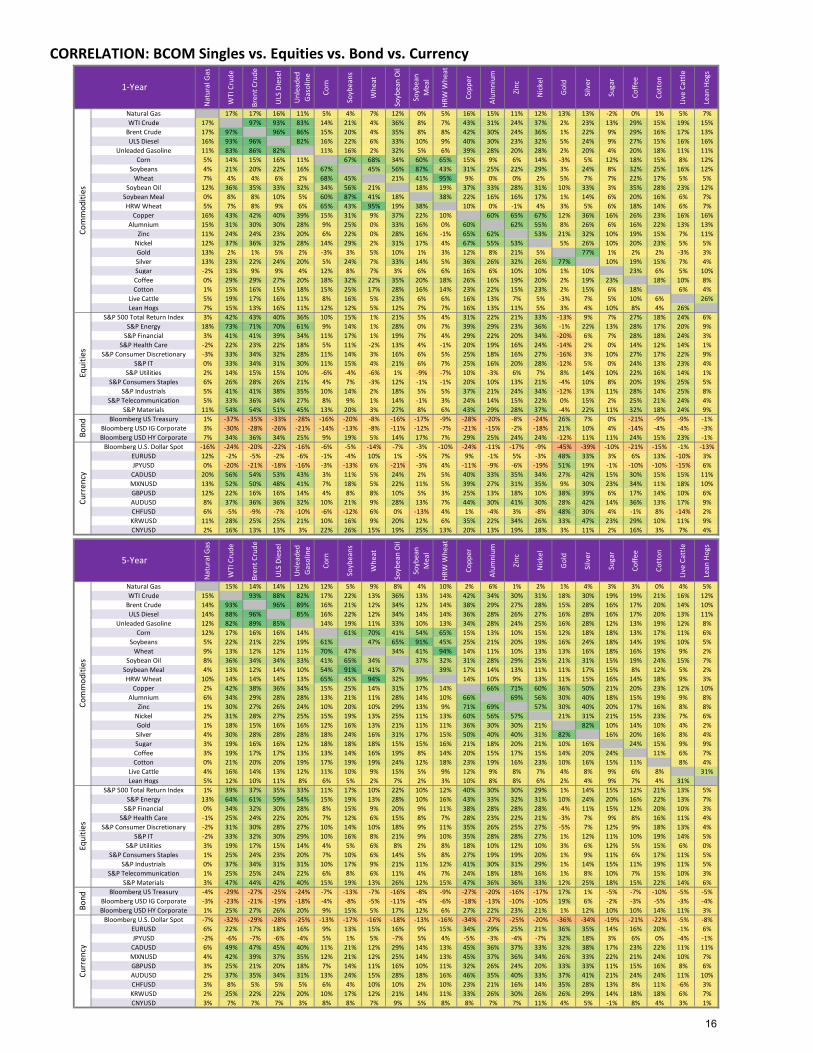

CORRELATION: BCOM Singles vs. Equities vs. Bond vs. Currency

5-Year

Com

mod

ities

Equi

ties

Bond

1-YearCo

mm

oditi

esEq

uitie

sBo

ndCu

rren

cy

16

All i

tem

s

Core

Food

Food

at h

ome

Food

aw

ay fr

om

hom

e

Ener

gy

Ener

gy

Com

mod

ities

Fuel

Oil

Mot

or F

uel

Ener

gy se

rvic

es

Elec

tric

ity

Util

ity g

as se

rvic

e

Com

mod

ities

less

fo

od a

nd e

nerg

y

Serv

ices

less

en

ergy

serv

ices

Shel

ter

Med

ical

car

e

Tran

spor

tatio

n

Bloomberg Commodity 60% -14% 18% 18% 4% 63% 60% 65% 60% 23% 3% 35% -10% -8% -21% 5% 14%Energy 64% -22% 12% 14% -4% 74% 74% 75% 73% 20% 4% 29% -3% -25% -28% -6% -4%

Petroleum 71% -12% 8% 9% -4% 78% 78% 80% 78% 5% 3% 5% 1% -14% -30% -1% 5%Agriculture 18% -10% 9% 9% 5% 19% 16% 11% 17% 13% -11% 34% -25% 8% -5% 9% 25%

Grains 10% -8% 7% 6% 6% 10% 8% 3% 9% 8% -15% 30% -20% 7% -7% 14% 18%Industrial Metals 40% 6% -1% 0% -5% 39% 37% 44% 37% -3% 4% -7% -1% 11% 2% 8% 15%Precious Metals 30% 13% 32% 30% 21% 20% 13% 28% 13% 17% 14% 14% 15% 6% -11% 17% 9%

Softs 21% -14% 18% 17% 9% 23% 20% 17% 21% 24% 6% 32% -28% 6% 2% -5% 30%Livestock 18% 2% 18% 17% 9% 18% 15% 13% 15% 20% 1% 34% -1% 6% -2% 17% 8%

Natural Gas 10% -26% 18% 20% -3% 17% 15% 12% 15% 38% 4% 59% -9% -28% -4% -13% -15%WTI Crude 65% -12% 8% 9% -1% 72% 73% 73% 72% 7% 5% 7% -2% -11% -28% 3% 5%

Brent Crude 72% -12% 12% 14% -4% 78% 78% 83% 78% 7% 5% 6% 7% -18% -34% -5% 5%ULS Diesel 69% -17% 15% 16% 1% 76% 75% 85% 74% 8% 6% 7% 3% -22% -32% -7% 3%

Unleaded Gasoline 80% -4% 9% 11% -5% 85% 86% 79% 86% -2% -2% 1% 7% -8% -26% -6% 13%Corn 12% -7% 15% 14% 10% 10% 7% 7% 8% 9% -15% 31% -12% 1% -13% 13% 18%

Soybeans 18% -4% -4% -3% -6% 19% 17% 11% 18% 5% -9% 19% -19% 12% -3% 13% 20%Wheat -4% -12% 0% -2% 8% -2% -3% -13% -2% 5% -20% 31% -30% 9% 0% 10% 11%

Soybean Oil 25% 9% -13% -13% -3% 23% 21% 12% 21% 1% -13% 15% -6% 19% -1% 0% 31%Soybean Meal 13% -9% 4% 5% -4% 16% 15% 11% 15% 4% -6% 14% -24% 8% 0% 11% 14%HRW Wheat 7% -12% 9% 7% 10% 8% 5% -1% 6% 18% -11% 42% -21% 3% -11% 9% 13%

Copper 39% 10% -11% -11% -5% 39% 39% 48% 39% -6% 5% -14% 3% 12% 2% 11% 11%Alumnium 37% -5% 10% 9% 6% 35% 33% 33% 33% -10% -7% -7% 1% -7% -3% 0% 5%

Zinc 27% 9% -11% -9% -15% 26% 24% 34% 24% 2% 11% -8% -3% 15% 8% 9% 16%Nickel 30% 3% 21% 24% -5% 28% 25% 32% 25% 14% 10% 14% -12% 17% 2% 6% 23%Gold 22% 18% 32% 29% 24% 11% 5% 21% 5% 16% 11% 16% 20% 8% -9% 18% 9%Silver 40% 4% 28% 27% 14% 32% 25% 37% 25% 17% 17% 10% 5% 2% -13% 13% 9%Sugar 2% 6% -5% -6% 4% 4% 5% 1% 5% 4% 2% 4% -8% 16% 4% 3% 29%Coffee 21% -15% 39% 38% 17% 20% 14% 12% 15% 39% 12% 50% -20% -4% 5% -9% 7%Cotton 21% -25% 0% 3% -10% 25% 23% 29% 23% 6% -3% 13% -32% -2% -5% -5% 21%

Live Cattle 24% -9% 11% 11% 5% 26% 26% 27% 25% 12% 11% 8% -6% -4% -2% 11% 3%Lean Hogs 8% 10% 19% 18% 8% 5% 2% -2% 2% 22% -6% 43% 5% 11% -2% 15% 8%

S&P 500 Total Return Index 25% -41% -30% -27% -24% 40% 40% 36% 40% 5% 9% -1% -31% -27% -13% -12% -17%Bloomberg US Treasury -34% 12% 31% 27% 31% -42% -44% -35% -44% 11% 8% 8% 27% -10% -12% 8% -8%

Bloomberg USD IG Corporate -4% -10% 17% 14% 22% -4% -7% 6% -7% 17% 11% 16% 17% -28% -21% -9% -16%Bloomberg USD HY Corporate 38% -25% -12% -11% -7% 49% 50% 58% 50% 8% 3% 10% -1% -29% -30% -18% -11%

Bloomberg U.S. Dollar Spot -52% -2% -16% -16% -6% -50% -46% -46% -46% -15% -7% -19% -10% 6% 20% 9% -12%

All i

tem

s

Core

Food

Food

at h

ome

Food

aw

ay fr

om

hom

e

Ener

gy

Ener

gy

Com

mod

ities

Fuel

Oil

Mot

or F

uel

Ener

gy se

rvic

es

Elec

tric

ity

Util

ity g

as se

rvic

e

Com

mod

ities

less

fo

od a

nd e

nerg

y

Serv

ices

less

en

ergy

serv

ices

Shel

ter

Med

ical

car

e

Tran

spor

tatio

n

Bloomberg Commodity 68% 5% 5% 8% -12% 69% 67% 66% 66% 31% -1% 41% 1% 8% 0% 8% 19%Energy 68% 0% 11% 14% -9% 72% 70% 69% 68% 38% 0% 48% -1% 4% -2% 2% 14%

Petroleum 72% 4% 10% 12% -7% 75% 76% 72% 75% 23% 2% 29% 2% 6% -2% 4% 17%Agriculture 29% 7% -1% 0% -7% 27% 26% 24% 26% 5% -3% 10% 1% 9% 6% 8% 15%

Grains 23% 7% 2% 2% -2% 20% 20% 19% 20% 2% -3% 6% -1% 10% 9% 8% 10%Industrial Metals 43% 6% -10% -7% -14% 44% 44% 43% 44% 11% 1% 14% 4% 5% -1% 8% 10%Precious Metals 30% 5% 0% 0% 0% 28% 26% 27% 25% 11% 7% 10% 4% 4% -6% 14% 15%

Softs 26% 3% -7% -4% -13% 28% 27% 21% 27% 11% -2% 15% 4% 0% -5% 4% 19%Livestock 15% -3% 17% 21% -9% 13% 10% 9% 10% 16% 8% 17% -12% 8% 5% 9% 3%

Natural Gas 36% -6% 9% 14% -12% 39% 33% 37% 32% 47% -5% 61% -3% -3% -3% -7% 3%WTI Crude 67% 5% 11% 13% -5% 70% 71% 68% 70% 22% 4% 27% 1% 8% 0% 7% 17%

Brent Crude 70% 5% 10% 13% -7% 72% 74% 70% 73% 19% 3% 23% 4% 6% -1% 4% 16%ULS Diesel 69% 1% 13% 15% -4% 72% 72% 77% 71% 27% 3% 33% 2% 2% -6% 1% 18%

Unleaded Gasoline 79% 3% 4% 8% -11% 82% 84% 67% 83% 21% -2% 28% 5% 2% -5% 0% 15%Corn 22% 5% 5% 6% -2% 19% 18% 19% 18% 4% -4% 10% 3% 4% 4% 1% 8%

Soybeans 22% 7% -2% -1% -8% 20% 20% 20% 20% 1% 1% 2% -1% 11% 8% 7% 15%Wheat 15% 6% 0% -2% 5% 13% 14% 9% 14% 1% -5% 5% -5% 11% 11% 14% 3%

Soybean Oil 30% 14% -3% -2% -6% 25% 24% 23% 24% 4% -3% 8% 4% 16% 11% 10% 16%Soybean Meal 17% 3% 1% 2% -6% 16% 17% 16% 17% 1% 6% -1% -2% 6% 4% 4% 13%HRW Wheat 22% 7% -1% -2% 3% 21% 21% 16% 21% 7% -1% 11% 0% 8% 8% 15% 2%

Copper 43% 9% -12% -11% -11% 43% 44% 41% 43% 9% 0% 10% 9% 5% -4% 9% 13%Alumnium 41% 4% 0% 3% -9% 41% 40% 44% 39% 19% 3% 23% 1% 5% 3% 3% 8%

Zinc 24% 6% -20% -18% -15% 26% 27% 22% 27% 1% 0% 1% 8% 2% 0% 2% 2%Nickel 32% -4% -4% 0% -18% 36% 37% 31% 37% 4% -2% 8% -10% 3% -3% 11% 8%Gold 27% 3% 5% 4% 5% 25% 23% 25% 23% 12% 10% 9% 3% 5% -6% 13% 15%Silver 29% 5% -7% -5% -7% 27% 25% 27% 25% 9% 2% 10% 6% 2% -5% 12% 12%Sugar 18% 7% -8% -7% -5% 18% 16% 12% 16% 11% 4% 13% 12% 0% -5% 4% 14%Coffee 13% 5% 0% 3% -8% 13% 13% 8% 13% 3% 1% 6% 3% -1% 1% -4% 4%Cotton 27% -8% -5% -2% -18% 30% 30% 32% 29% 8% -6% 12% 0% -8% -11% 1% 18%

Live Cattle 21% -6% 20% 23% -9% 19% 17% 12% 17% 15% 11% 13% -15% 8% 8% 9% 2%Lean Hogs 5% -3% 11% 13% -6% 3% 0% 3% 0% 12% 4% 14% -8% 3% -1% 7% 3%

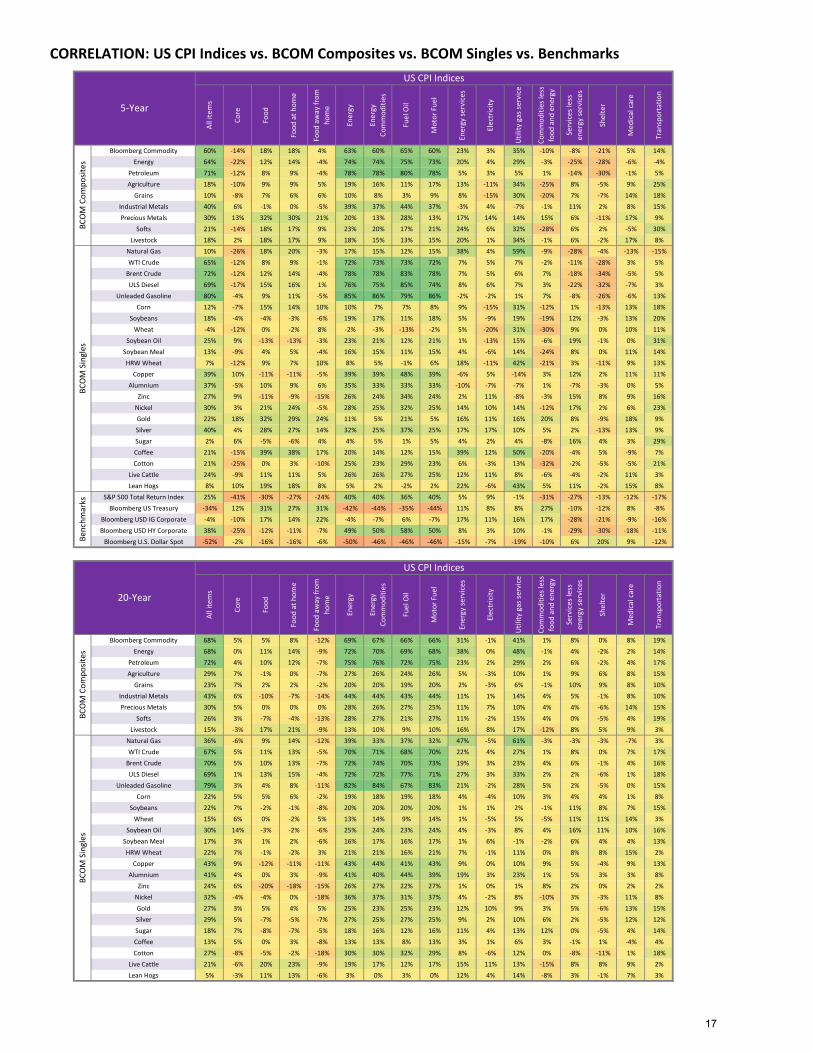

CORRELATION: US CPI Indices vs. BCOM Composites vs. BCOM Singles vs. Benchmarks

20-Year

US CPI Indices

BCO

M C

ompo

sites

BCO

M S

ingl

esUS CPI Indices

5-Year

BCO

M C

ompo

sites

BCO

M S

ingl

esBe

nchm

arks

17

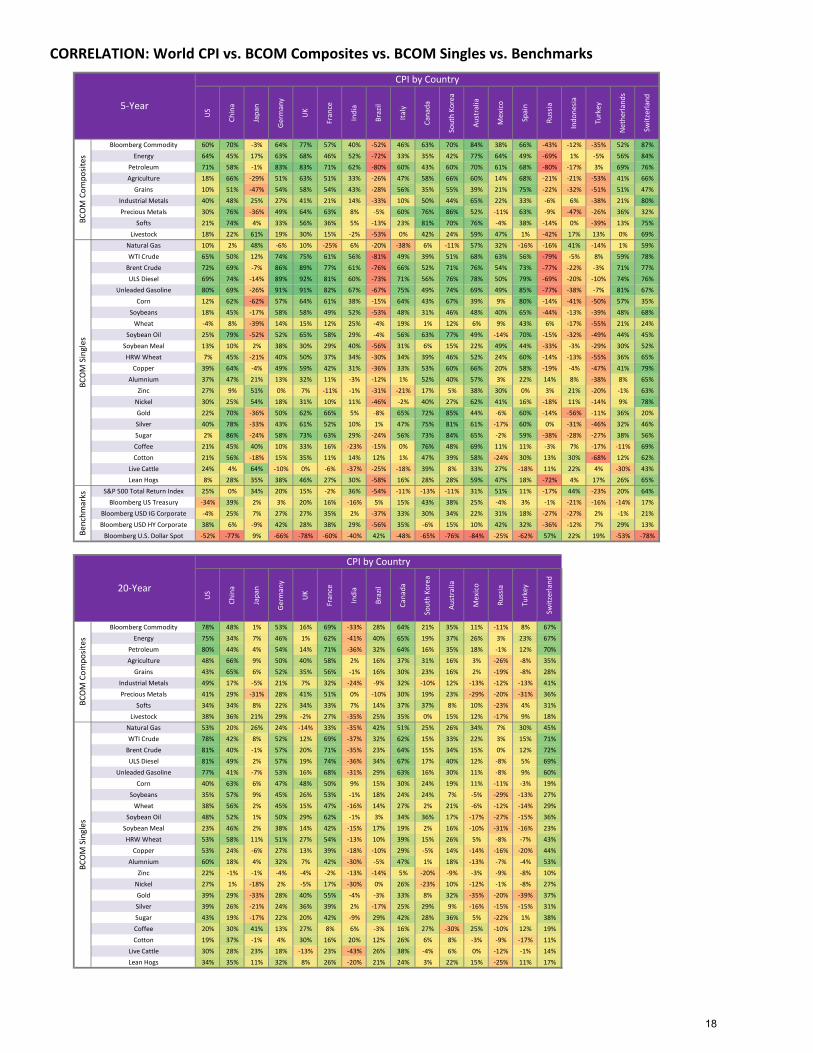

CORRELATION: World CPI vs. BCOM Composites vs. BCOM Singles vs. Benchmarks

US

Chin

a

Japa

n

Ger

man

y

UK

Fran

ce

Indi

a

Braz

il

Italy

Cana

da

Sout

h Ko

rea

Aust

ralia

Mex

ico

Spai

n

Russ

ia

Indo

nesi

a

Turk

ey

Net

herla

nds

Switz

erla

nd

Bloomberg Commodity 60% 70% -3% 64% 77% 57% 40% -52% 46% 63% 70% 84% 38% 66% -43% -12% -35% 52% 87%Energy 64% 45% 17% 63% 68% 46% 52% -72% 33% 35% 42% 77% 64% 49% -69% 1% -5% 56% 84%

Petroleum 71% 58% -1% 83% 83% 71% 62% -80% 60% 43% 60% 70% 61% 68% -80% -17% 3% 69% 76%Agriculture 18% 66% -29% 51% 63% 51% 33% -26% 47% 58% 66% 60% 14% 68% -21% -21% -53% 41% 66%

Grains 10% 51% -47% 54% 58% 54% 43% -28% 56% 35% 55% 39% 21% 75% -22% -32% -51% 51% 47%Industrial Metals 40% 48% 25% 27% 41% 21% 14% -33% 10% 50% 44% 65% 22% 33% -6% 6% -38% 21% 80%Precious Metals 30% 76% -36% 49% 64% 63% 8% -5% 60% 76% 86% 52% -11% 63% -9% -47% -26% 36% 32%

Softs 21% 74% 4% 33% 56% 36% 5% -13% 23% 81% 70% 76% -4% 38% -14% 0% -39% 13% 75%Livestock 18% 22% 61% 19% 30% 15% -2% -53% 0% 42% 24% 59% 47% 1% -42% 17% 13% 0% 69%

Natural Gas 10% 2% 48% -6% 10% -25% 6% -20% -38% 6% -11% 57% 32% -16% -16% 41% -14% 1% 59%WTI Crude 65% 50% 12% 74% 75% 61% 56% -81% 49% 39% 51% 68% 63% 56% -79% -5% 8% 59% 78%

Brent Crude 72% 69% -7% 86% 89% 77% 61% -76% 66% 52% 71% 76% 54% 73% -77% -22% -3% 71% 77%ULS Diesel 69% 74% -14% 89% 92% 81% 60% -73% 71% 56% 76% 78% 50% 79% -69% -20% -10% 74% 76%

Unleaded Gasoline 80% 69% -26% 91% 91% 82% 67% -67% 75% 49% 74% 69% 49% 85% -77% -38% -7% 81% 67%Corn 12% 62% -62% 57% 64% 61% 38% -15% 64% 43% 67% 39% 9% 80% -14% -41% -50% 57% 35%

Soybeans 18% 45% -17% 58% 58% 49% 52% -53% 48% 31% 46% 48% 40% 65% -44% -13% -39% 48% 68%Wheat -4% 8% -39% 14% 15% 12% 25% -4% 19% 1% 12% 6% 9% 43% 6% -17% -55% 21% 24%

Soybean Oil 25% 79% -52% 52% 65% 58% 29% -4% 56% 63% 77% 49% -14% 70% -15% -32% -49% 44% 45%Soybean Meal 13% 10% 2% 38% 30% 29% 40% -56% 31% 6% 15% 22% 49% 44% -33% -3% -29% 30% 52%HRW Wheat 7% 45% -21% 40% 50% 37% 34% -30% 34% 39% 46% 52% 24% 60% -14% -13% -55% 36% 65%

Copper 39% 64% -4% 49% 59% 42% 31% -36% 33% 53% 60% 66% 20% 58% -19% -4% -47% 41% 79%Alumnium 37% 47% 21% 13% 32% 11% -3% -12% 1% 52% 40% 57% 3% 22% 14% 8% -38% 8% 65%

Zinc 27% 9% 51% 0% 7% -11% -1% -31% -21% 17% 5% 38% 30% 0% 3% 21% -20% -1% 63%Nickel 30% 25% 54% 18% 31% 10% 11% -46% -2% 40% 27% 62% 41% 16% -18% 11% -14% 9% 78%Gold 22% 70% -36% 50% 62% 66% 5% -8% 65% 72% 85% 44% -6% 60% -14% -56% -11% 36% 20%Silver 40% 78% -33% 43% 61% 52% 10% 1% 47% 75% 81% 61% -17% 60% 0% -31% -46% 32% 46%Sugar 2% 86% -24% 58% 73% 63% 29% -24% 56% 73% 84% 65% -2% 59% -38% -28% -27% 38% 56%Coffee 21% 45% 40% 10% 33% 16% -23% -15% 0% 76% 48% 69% 11% 11% -3% 7% -17% -11% 69%Cotton 21% 56% -18% 15% 35% 11% 14% 12% 1% 47% 39% 58% -24% 30% 13% 30% -68% 12% 62%

Live Cattle 24% 4% 64% -10% 0% -6% -37% -25% -18% 39% 8% 33% 27% -18% 11% 22% 4% -30% 43%Lean Hogs 8% 28% 35% 38% 46% 27% 30% -58% 16% 28% 28% 59% 47% 18% -72% 4% 17% 26% 65%

S&P 500 Total Return Index 25% 0% 34% 20% 15% -2% 36% -54% -11% -13% -11% 31% 51% 11% -17% 44% -23% 20% 64%Bloomberg US Treasury -34% 39% 2% 3% 20% 16% -16% 5% 15% 43% 38% 25% -4% 3% -1% -21% -16% -14% 17%

Bloomberg USD IG Corporate -4% 25% 7% 27% 27% 35% 2% -37% 33% 30% 34% 22% 31% 18% -27% -27% 2% -1% 21%Bloomberg USD HY Corporate 38% 6% -9% 42% 28% 38% 29% -56% 35% -6% 15% 10% 42% 32% -36% -12% 7% 29% 13%

Bloomberg U.S. Dollar Spot -52% -77% 9% -66% -78% -60% -40% 42% -48% -65% -76% -84% -25% -62% 57% 22% 19% -53% -78%

US

Chin

a

Japa

n

Ger

man

y

UK

Fran

ce

Indi

a

Braz

il

Cana

da

Sout

h Ko

rea

Aust

ralia

Mex

ico

Russ

ia

Turk

ey

Switz

erla

nd

Bloomberg Commodity 78% 48% 1% 53% 16% 69% -33% 28% 64% 21% 35% 11% -11% 8% 67%Energy 75% 34% 7% 46% 1% 62% -41% 40% 65% 19% 37% 26% 3% 23% 67%

Petroleum 80% 44% 4% 54% 14% 71% -36% 32% 64% 16% 35% 18% -1% 12% 70%Agriculture 48% 66% 9% 50% 40% 58% 2% 16% 37% 31% 16% 3% -26% -8% 35%

Grains 43% 65% 6% 52% 35% 56% -1% 16% 30% 23% 16% 2% -19% -8% 28%Industrial Metals 49% 17% -5% 21% 7% 32% -24% -9% 32% -10% 12% -13% -12% -13% 41%Precious Metals 41% 29% -31% 28% 41% 51% 0% -10% 30% 19% 23% -29% -20% -31% 36%

Softs 34% 34% 8% 22% 34% 33% 7% 14% 37% 37% 8% 10% -23% 4% 31%Livestock 38% 36% 21% 29% -2% 27% -35% 25% 35% 0% 15% 12% -17% 9% 18%

Natural Gas 53% 20% 26% 24% -14% 33% -35% 42% 51% 25% 26% 34% 7% 30% 45%WTI Crude 78% 42% 8% 52% 12% 69% -37% 32% 62% 15% 33% 22% 3% 15% 71%

Brent Crude 81% 40% -1% 57% 20% 71% -35% 23% 64% 15% 34% 15% 0% 12% 72%ULS Diesel 81% 49% 2% 57% 19% 74% -36% 34% 67% 17% 40% 12% -8% 5% 69%

Unleaded Gasoline 77% 41% -7% 53% 16% 68% -31% 29% 63% 16% 30% 11% -8% 9% 60%Corn 40% 63% 6% 47% 48% 50% 9% 15% 30% 24% 19% 11% -11% -3% 19%

Soybeans 35% 57% 9% 45% 26% 53% -1% 18% 24% 24% 7% -5% -29% -13% 27%Wheat 38% 56% 2% 45% 15% 47% -16% 14% 27% 2% 21% -6% -12% -14% 29%

Soybean Oil 48% 52% 1% 50% 29% 62% -1% 3% 34% 36% 17% -17% -27% -15% 36%Soybean Meal 23% 46% 2% 38% 14% 42% -15% 17% 19% 2% 16% -10% -31% -16% 23%HRW Wheat 53% 58% 11% 51% 27% 54% -13% 10% 39% 15% 26% 5% -8% -7% 43%

Copper 53% 24% -6% 27% 13% 39% -18% -10% 29% -5% 14% -14% -16% -20% 44%Alumnium 60% 18% 4% 32% 7% 42% -30% -5% 47% 1% 18% -13% -7% -4% 53%

Zinc 22% -1% -1% -4% -4% -2% -13% -14% 5% -20% -9% -3% -9% -8% 10%Nickel 27% 1% -18% 2% -5% 17% -30% 0% 26% -23% 10% -12% -1% -8% 27%Gold 39% 29% -33% 28% 40% 55% -4% -3% 33% 8% 32% -35% -20% -39% 37%Silver 39% 26% -21% 24% 36% 39% 2% -17% 25% 29% 9% -16% -15% -15% 31%Sugar 43% 19% -17% 22% 20% 42% -9% 29% 42% 28% 36% 5% -22% 1% 38%Coffee 20% 30% 41% 13% 27% 8% 6% -3% 16% 27% -30% 25% -10% 12% 19%Cotton 19% 37% -1% 4% 30% 16% 20% 12% 26% 6% 8% -3% -9% -17% 11%

Live Cattle 30% 28% 23% 18% -13% 23% -43% 26% 38% -4% 6% 0% -12% -1% 14%Lean Hogs 34% 35% 11% 32% 8% 26% -20% 21% 24% 3% 22% 15% -25% 11% 17%

BCO

M C

ompo

sites

BCO

M S

ingl

es

5-Year

CPI by CountryBC

OM

Com

posit

esBC

OM

Sin

gles

Benc

hmar

ks

20-Year

CPI by Country

18

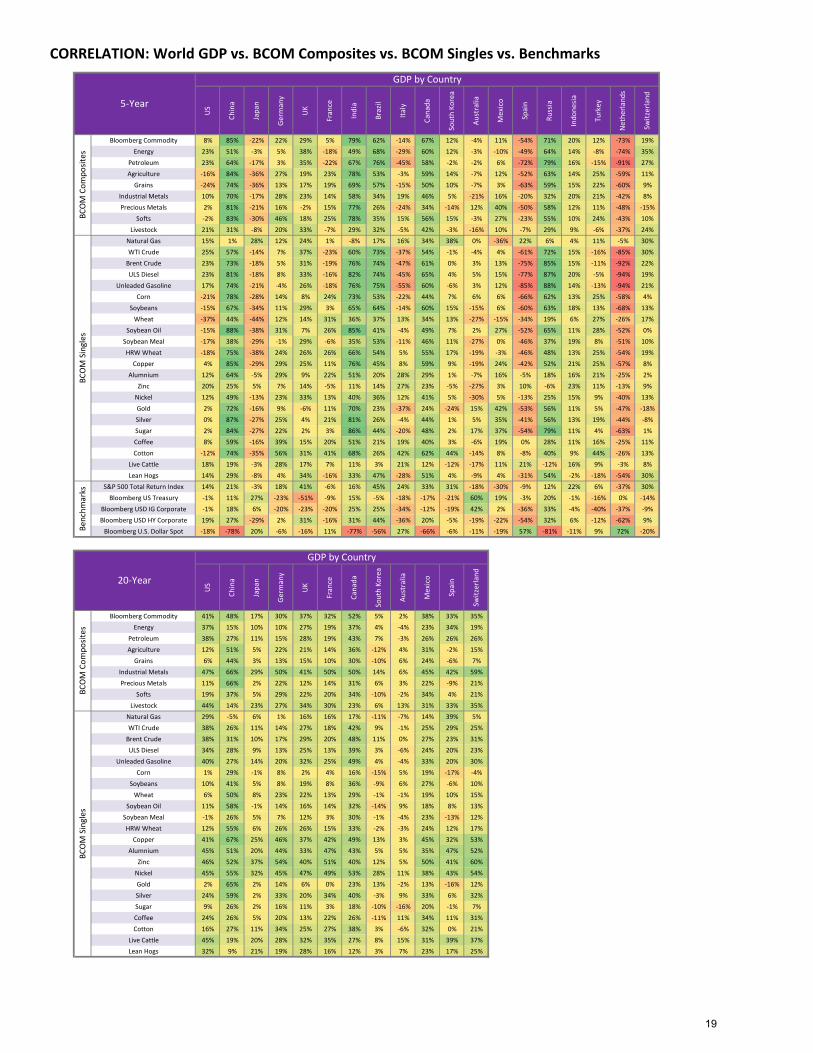

CORRELATION: World GDP vs. BCOM Composites vs. BCOM Singles vs. Benchmarks

US

Chin

a

Japa

n

Ger

man

y

UK

Fran

ce

Indi

a

Braz

il

Italy

Cana

da

Sout

h Ko

rea

Aust

ralia

Mex

ico

Spai

n

Russ

ia

Indo

nesi

a

Turk

ey

Net

herla

nds

Switz

erla

nd

Bloomberg Commodity 8% 85% -22% 22% 29% 5% 79% 62% -14% 67% 12% -4% 11% -54% 71% 20% 12% -73% 19%Energy 23% 51% -3% 5% 38% -18% 49% 68% -29% 60% 12% -3% -10% -49% 64% 14% -8% -74% 35%

Petroleum 23% 64% -17% 3% 35% -22% 67% 76% -45% 58% -2% -2% 6% -72% 79% 16% -15% -91% 27%Agriculture -16% 84% -36% 27% 19% 23% 78% 53% -3% 59% 14% -7% 12% -52% 63% 14% 25% -59% 11%