400 W. Wilson Bridge Road, Suite 200, Worthington, OH, 43085 614-846-0146 [email protected] PAMELA GOODFELLOW CONSUMER INSIGHTS DIRECTOR, BIGINSIGHT™ MARIANNE BICKLE, PH.D. DIRECTOR, CENTER FOR RETAILING UNIVERSITY OF SOUTH CAROLINA The BIG Call March 2012

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

400 W. Wilson Bridge Road, Suite 200, Worthington, OH, 43085 614-846-0146 [email protected]

PAM E L A G O O D F E L L O W C O N S U M E R I N S I G H T S D I R E C T O R , B I G I N S I G H T ™

M AR I A N N E B I C K L E , P H . D .

D I R E C T O R , C E N T E R F O R R E TAI L I N G U N I V E R S I T Y O F S O U T H C AR O L I N A

The BIG Call March 2012

© 2012, Prosper®

Marianne Bickle, Ph.D.

Chair and Director for the Center for Retailing, University of South Carolina Author:

• Fashion Marketing (published by Fairchild Books) • The Changing American Consumer (in cooperation with the Prosper Foundation)

Regular contributor on the Forbes Prosper Now Blog Has published and presented in excess of 90 peer referred

papers in relation to cross-channel shopping, e-commerce, and student learning paradigms of retailing.

On the Board of Directors on a privately owned fashion company and is a regular retail contributing expert for news corporations.

Fostered international relationships in France, Italy, Korea, and the United Kingdom.

Earned a Ph.D. in Family Ecology, a master’s degree in clothing and textiles and holds a B.S. in retailing of clothing and textiles.

© 2012, Prosper®

March 2012 Consumer Survey

Disclaimer: BIGinsight™ is a trademark of Prosper Business Development Corp. Services are delivered by Prosper and/or a Prosper affiliated company (“Prosper”). Prosper makes no warranties, either expressed or implied, concerning: data gathered or obtained from any source; the present or future methodology employed in producing the statistics; or the data and estimates represent only the opinion of Prosper and reliance thereon and use thereof shall be at the user’s own risk.

This report is derived from the following studies:

• BIGinsight™ Monthly Consumer Survey, March 2012 (N = 9242, respondents surveyed 3/6 – 3/13/12)

• BIGinsight™ Monthly Consumer Survey Trends, March 2007 – March 2012

March 2012 Results • Consumer Confidence • Practical Purchasing • Financial Forecast • Gas Price Impact • 90 Day Outlook: Future Purchase Plans

The Changing American Consumer • A Special Look at Fast Food Trends

© 2012, Prosper®

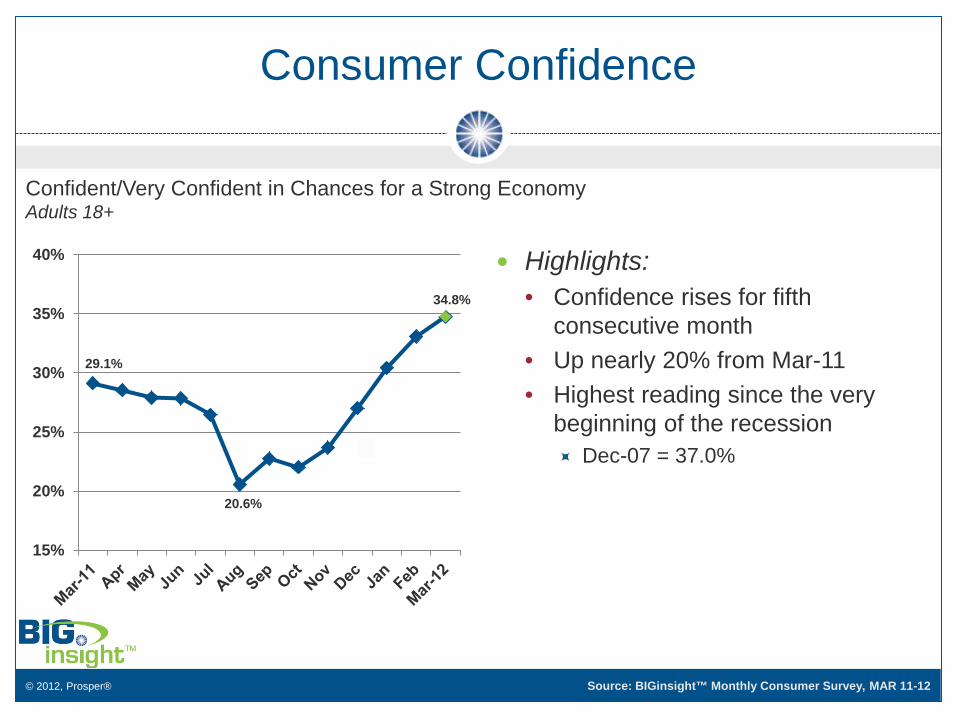

Confident/Very Confident in Chances for a Strong Economy Adults 18+

Consumer Confidence

Source: BIGinsight™ Monthly Consumer Survey, MAR 11-12

Highlights: • Confidence rises for fifth

consecutive month • Up nearly 20% from Mar-11 • Highest reading since the very

beginning of the recession Dec-07 = 37.0%

29.1%

20.6%

34.8%

15%

20%

25%

30%

35%

40%

© 2012, Prosper®

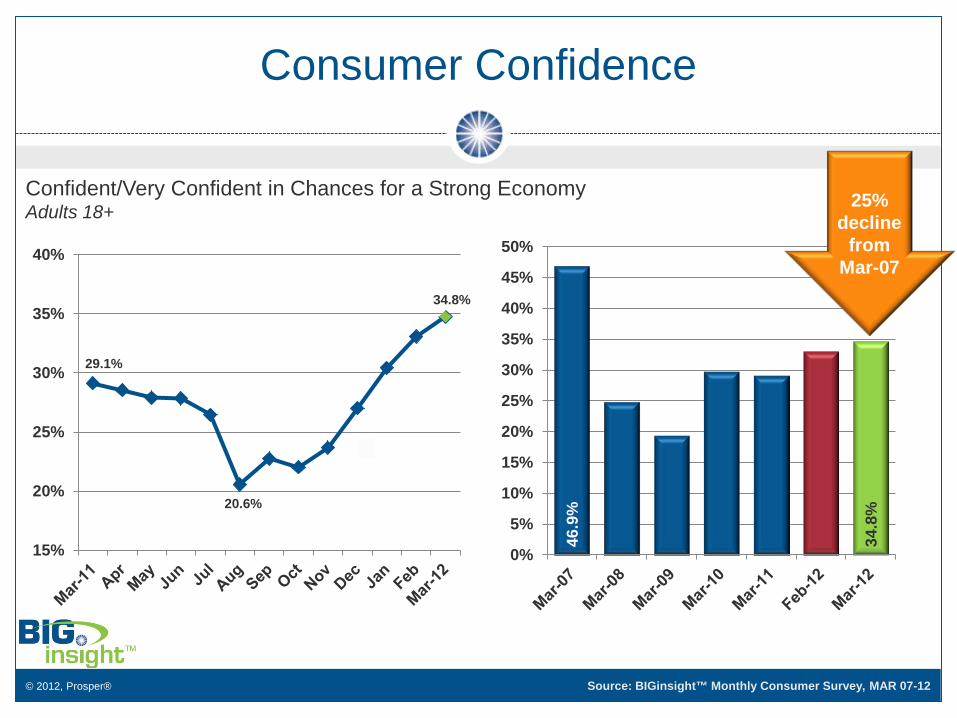

Confident/Very Confident in Chances for a Strong Economy Adults 18+

Consumer Confidence

Source: BIGinsight™ Monthly Consumer Survey, MAR 07-12

29.1%

20.6%

34.8%

15%

20%

25%

30%

35%

40%

46.9

%

34.8

%

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

50%

25%

decline from

Mar-07

© 2012, Prosper® Source: BIGinsight™ Monthly Consumer Survey, MAR 11-12

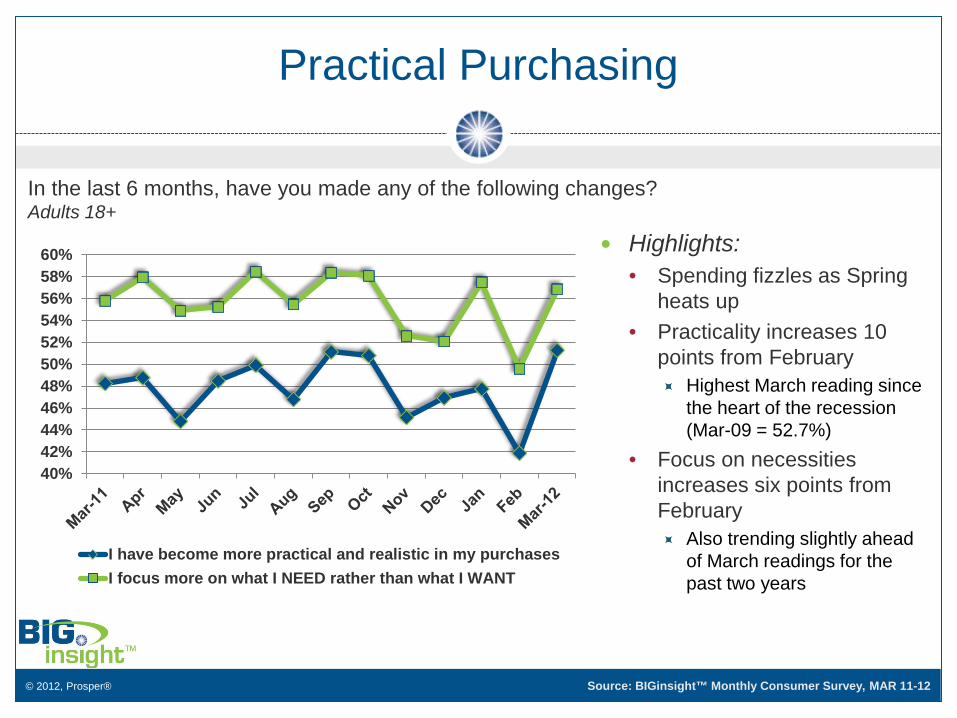

Practical Purchasing

In the last 6 months, have you made any of the following changes? Adults 18+

Highlights: • Spending fizzles as Spring

heats up • Practicality increases 10

points from February Highest March reading since

the heart of the recession (Mar-09 = 52.7%)

• Focus on necessities increases six points from February Also trending slightly ahead

of March readings for the past two years

40%42%44%46%48%50%52%54%56%58%60%

I have become more practical and realistic in my purchasesI focus more on what I NEED rather than what I WANT

© 2012, Prosper® Source: BIGinsight™ Monthly Consumer Survey, MAR 11-12

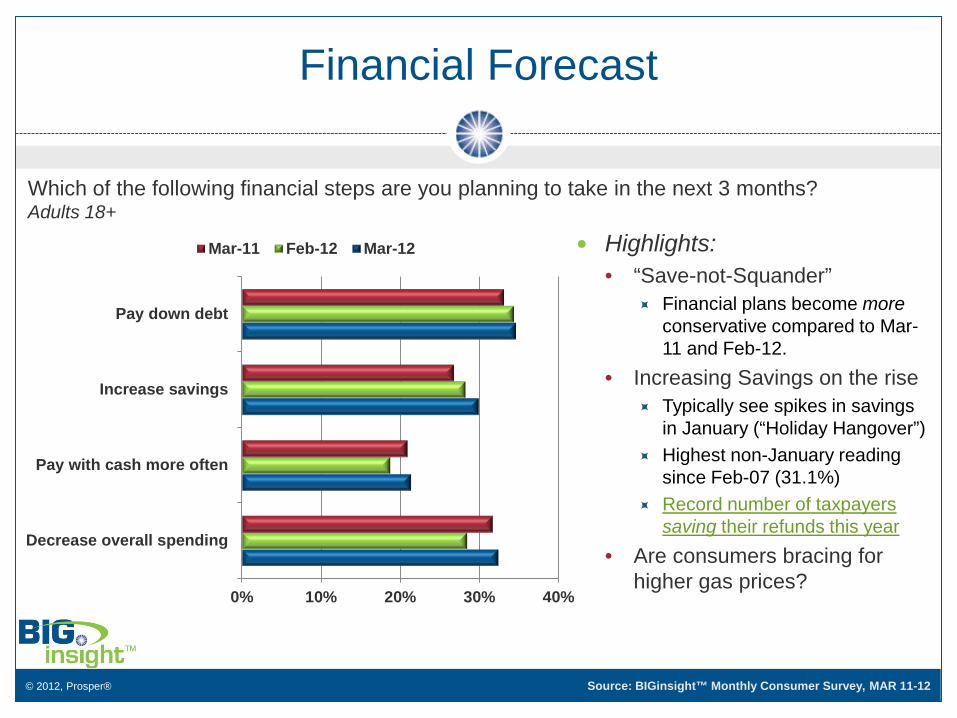

Financial Forecast

Which of the following financial steps are you planning to take in the next 3 months? Adults 18+

Highlights: • “Save-not-Squander”

Financial plans become more conservative compared to Mar-11 and Feb-12.

• Increasing Savings on the rise Typically see spikes in savings

in January (“Holiday Hangover”) Highest non-January reading

since Feb-07 (31.1%) Record number of taxpayers

saving their refunds this year • Are consumers bracing for

higher gas prices? 0% 10% 20% 30% 40%

Pay down debt

Increase savings

Pay with cash more often

Decrease overall spending

Mar-11 Feb-12 Mar-12

© 2012, Prosper® Source: BIGinsight™ Monthly Consumer Survey, MAR-12

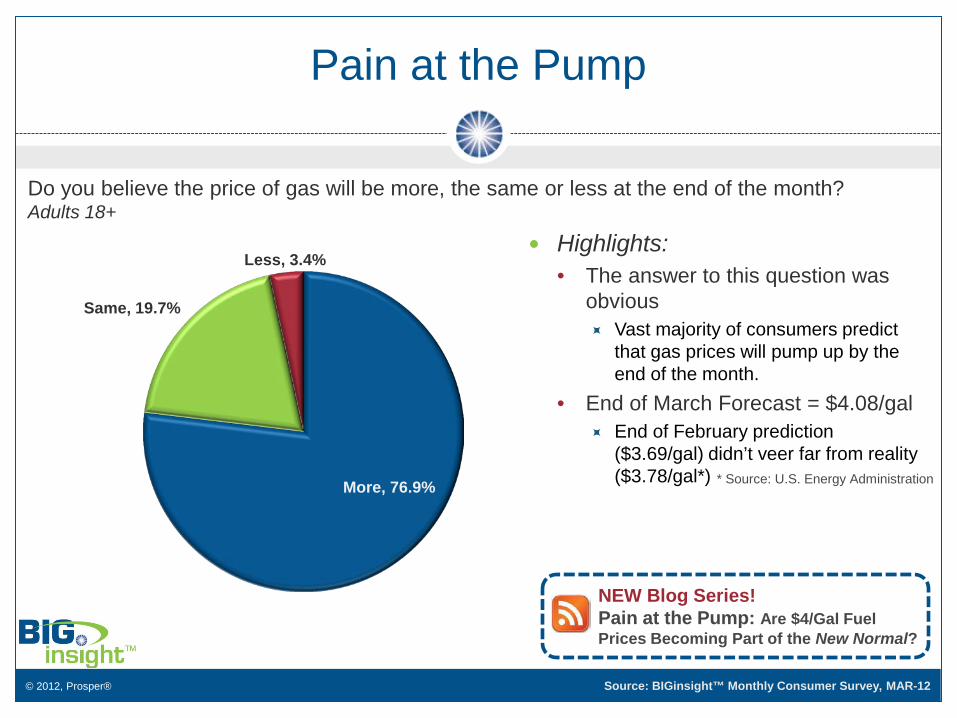

Pain at the Pump

Do you believe the price of gas will be more, the same or less at the end of the month? Adults 18+

Highlights: • The answer to this question was

obvious Vast majority of consumers predict

that gas prices will pump up by the end of the month.

• End of March Forecast = $4.08/gal End of February prediction

($3.69/gal) didn’t veer far from reality ($3.78/gal*) More, 76.9%

Same, 19.7%

Less, 3.4%

* Source: U.S. Energy Administration

NEW Blog Series! Pain at the Pump: Are $4/Gal Fuel Prices Becoming Part of the New Normal?

© 2012, Prosper® Source: BIGinsight™ Monthly Consumer Survey, MAR-12

Pain at the Pump

How have fluctuating gas prices impacted your spending? by Yearly Household Income

Highlights: • Under $50K wage earners are more

affected by prices at the pump, but $50K+ consumers aren’t immune to impact. <$50K: 81% $50K+: 73% Adults 18+: 77%

• Driving less is most popular way to defray fuel expenses Dining Out, Vacation Travel also

prime cutbacks

0% 20% 40% 60%

Delayed major purchase

Reduced dining out

Decreased vacation/travel

I will be driving less

Spending less on groceries

Spending less on clothing

Less than $50K $50K or More

NEW Blog Series! Pain at the Pump: Are $4/Gal Fuel Prices Becoming Part of the New Normal?

© 2012, Prosper®

Category: Feb-12 Mar-11 Mar-10 Category: Feb-12 Mar-11 Mar-10

Children’s up up up Toys/Games up up up

Women’s Dress up up up CDs/DVDs/Videos/Books down up up

Women’s Casual up up up Electronics up up up

Men’s Dress up up up Groceries up up up

Men’s Casual up up up Home Improvement down up up

Shoes up up up Lawn & Garden up up up

HBC flat up up Home Furniture down up up

Dining Out down up up Home Décor flat up up

Sporting Goods up up up Linens/Bedding/Draperies down up up

Retail Merchandise Categories - 90 Day Outlook (Mar-12 compared to Feb-12, Mar-11, and Mar-10)

Note: “Up,” Down,” “Flat” refers to the direction of the Diffusion Index compared to the previous month (Feb-12) or years (Mar-11, Mar-10). Diffusion Index = % Spending More - % Spending Less.

BIG Forward Look: 90 Day Spending

Source: BIGinsight™ Monthly Consumer Survey, MAR 10-12

Over the next 90 days (March, April and May), do you plan on spending more, the same or less on the following items than you would normally spend at this time of the year? Adults 18+

© 2012, Prosper®

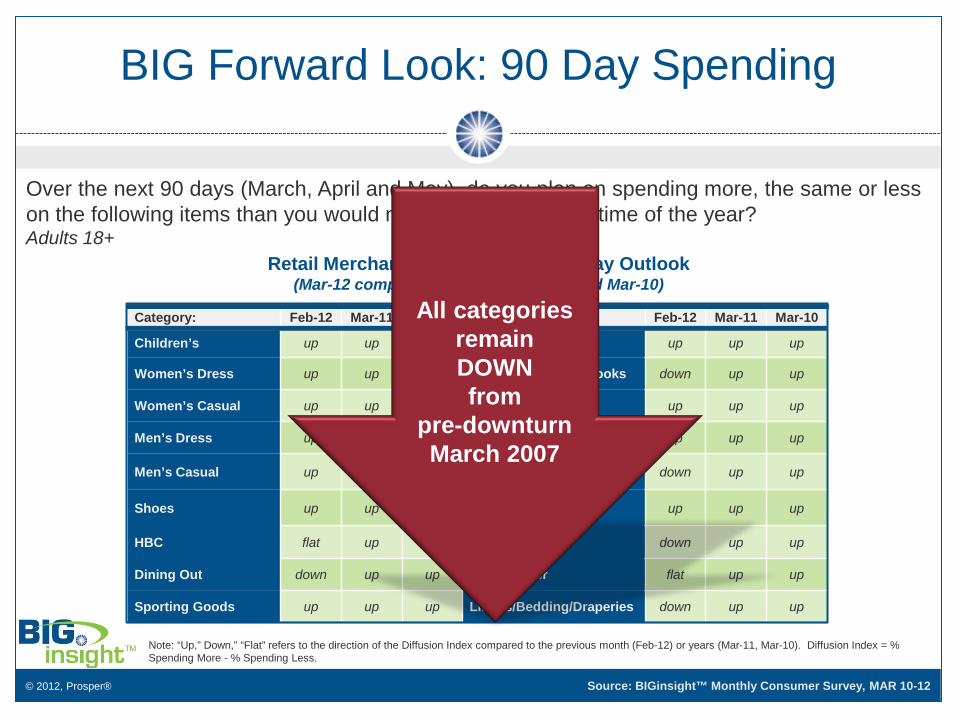

Category: Feb-12 Mar-11 Mar-10 Category: Feb-12 Mar-11 Mar-10

Children’s up up up Toys/Games up up up

Women’s Dress up up up CDs/DVDs/Videos/Books down up up

Women’s Casual up up up Electronics up up up

Men’s Dress up up up Groceries up up up

Men’s Casual up up up Home Improvement down up up

Shoes up up up Lawn & Garden up up up

HBC flat up up Home Furniture down up up

Dining Out down up up Home Décor flat up up

Sporting Goods up up up Linens/Bedding/Draperies down up up

Retail Merchandise Categories - 90 Day Outlook (Mar-12 compared to Feb-12, Mar-11, and Mar-10)

Note: “Up,” Down,” “Flat” refers to the direction of the Diffusion Index compared to the previous month (Feb-12) or years (Mar-11, Mar-10). Diffusion Index = % Spending More - % Spending Less.

BIG Forward Look: 90 Day Spending

Source: BIGinsight™ Monthly Consumer Survey, MAR 10-12

Over the next 90 days (March, April and May), do you plan on spending more, the same or less on the following items than you would normally spend at this time of the year? Adults 18+

All categories remain DOWN from

pre-downturn March 2007

© 2012, Prosper®

National Trend

Increase in consumers’ weight Centers for Disease Control and Prevention:

• 34% of adults 20 years+ are obese • 68% of consumers are classified as overweight

© 2012, Prosper®

Battle of the sexes: Who is the fast food junky?

Feb 2012 survey of consumers who frequently eat fast food • 52.7% men • 47.3% women

These consumers patronized

fast food restaurants four or more times per week

New insights reveal consumers patterns are changing since 2005 (Source: The Changing American Consumer)

40.0%

45.0%

50.0%

55.0%

Male Female

Frequent Fast Food Restaurants Four or More Times per Month

Source: BIGinsight™ Monthly Consumer Survey, FEB-12

© 2012, Prosper®

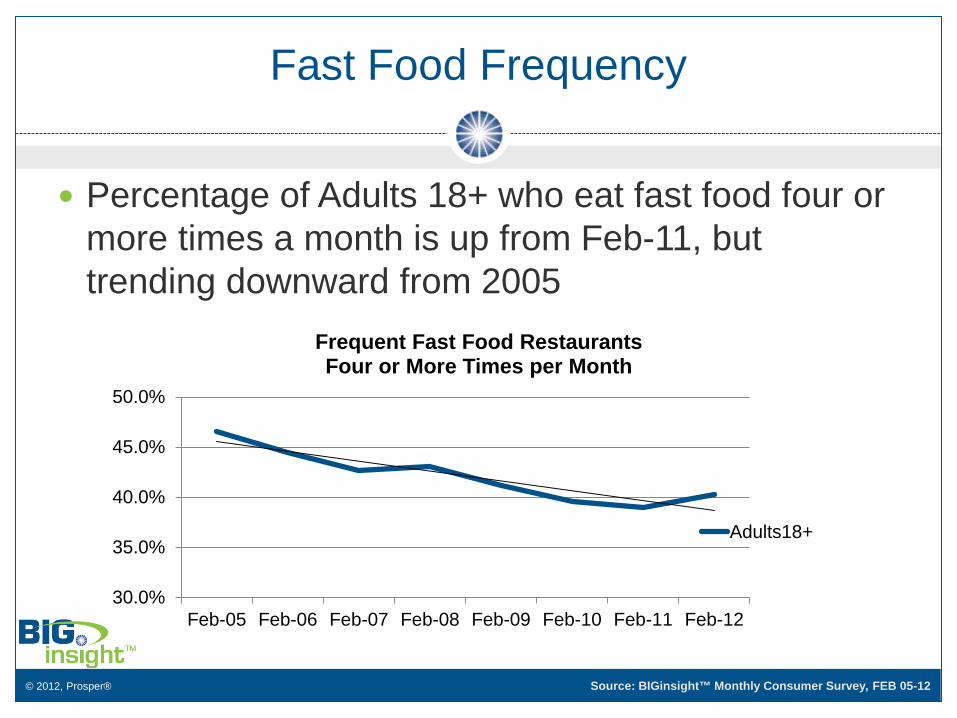

Fast Food Frequency

Percentage of Adults 18+ who eat fast food four or more times a month is up from Feb-11, but trending downward from 2005

30.0%

35.0%

40.0%

45.0%

50.0%

Feb-05 Feb-06 Feb-07 Feb-08 Feb-09 Feb-10 Feb-11 Feb-12

Frequent Fast Food Restaurants Four or More Times per Month

Adults18+

Source: BIGinsight™ Monthly Consumer Survey, FEB 05-12

© 2012, Prosper®

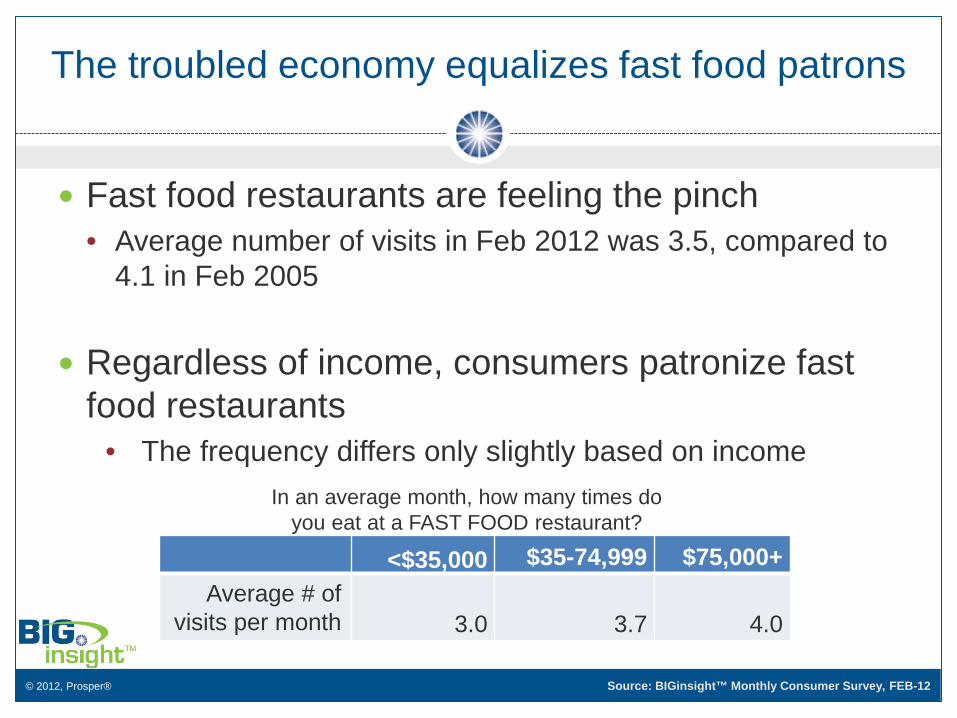

The troubled economy equalizes fast food patrons

Fast food restaurants are feeling the pinch • Average number of visits in Feb 2012 was 3.5, compared to

4.1 in Feb 2005

Regardless of income, consumers patronize fast food restaurants

• The frequency differs only slightly based on income

<$35,000 $35-74,999 $75,000+

Average # of visits per month 3.0 3.7 4.0

In an average month, how many times do you eat at a FAST FOOD restaurant?

Source: BIGinsight™ Monthly Consumer Survey, FEB-12

© 2012, Prosper®

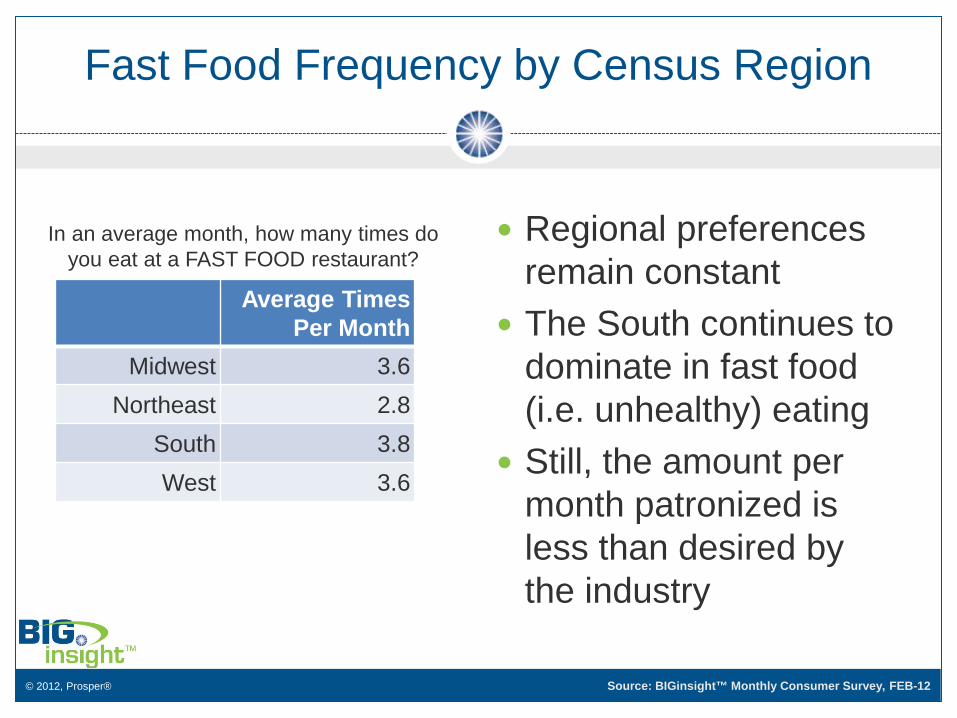

Regional preferences remain constant

The South continues to dominate in fast food (i.e. unhealthy) eating

Still, the amount per month patronized is less than desired by the industry

Average Times Per Month

Midwest 3.6 Northeast 2.8

South 3.8 West 3.6

Fast Food Frequency by Census Region

In an average month, how many times do you eat at a FAST FOOD restaurant?

Source: BIGinsight™ Monthly Consumer Survey, FEB-12

© 2012, Prosper®

Preferred Fast Food Restaurant

Men Women McDonald’s 24.2% 28.1%

Wendy’s 7.6% 8.1% Burger King 7.9% 5.1%

Subway 7.8% 7.2% Taco Bell 5.7% 4.9%

Arby’s 1.8% 1.9%

McDonald’s continues to dominate the market

However: • Changing frequency of

patronage will place challenges on McDonald’s and its competitors

• New strategies and brand images may be required for the long term

At what FAST FOOD Restaurant do you eat at most often?

Source: BIGinsight™ Monthly Consumer Survey, FEB-12

© 2012, Prosper®

Top Reasons for Patronizing Fast Food Restaurants

Issues traditionally thought of with a restaurant (i.e. healthy food, cleanliness) are not as important

Regardless of income, consumers eat at fast food restaurants because of: • Price • Convenience

© 2012, Prosper®

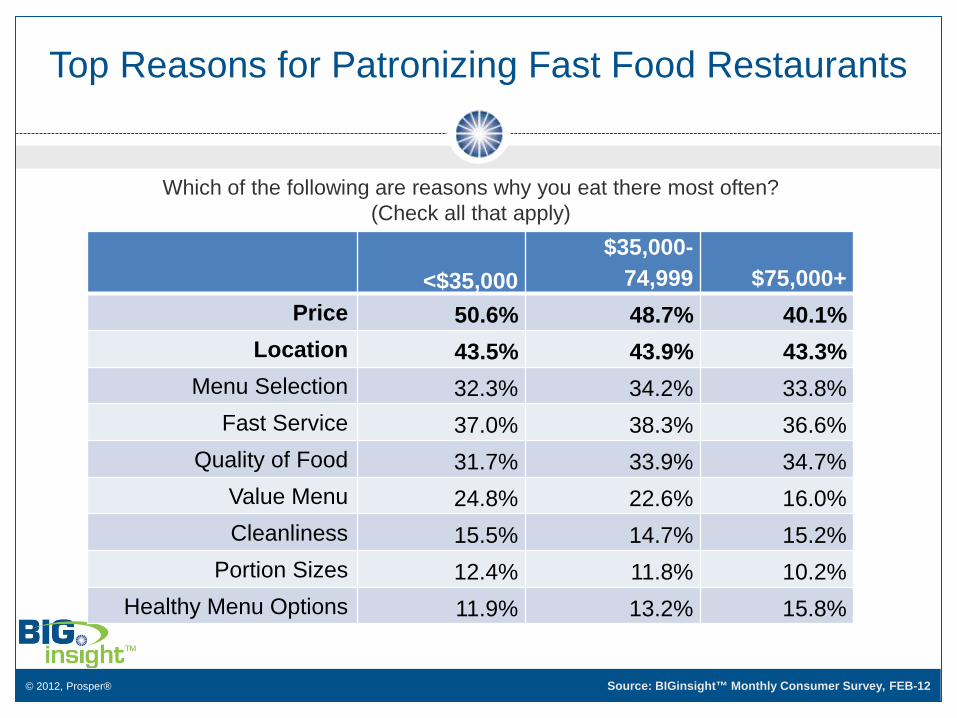

Top Reasons for Patronizing Fast Food Restaurants

<$35,000 $35,000-

74,999 $75,000+ Price 50.6% 48.7% 40.1%

Location 43.5% 43.9% 43.3% Menu Selection 32.3% 34.2% 33.8%

Fast Service 37.0% 38.3% 36.6% Quality of Food 31.7% 33.9% 34.7%

Value Menu 24.8% 22.6% 16.0% Cleanliness 15.5% 14.7% 15.2%

Portion Sizes 12.4% 11.8% 10.2% Healthy Menu Options 11.9% 13.2% 15.8%

Which of the following are reasons why you eat there most often? (Check all that apply)

Source: BIGinsight™ Monthly Consumer Survey, FEB-12

© 2012, Prosper®

Snapshot

Fast food industry is experiencing changes in sales volume

Attributes desired are not typical of “eat in”

restaurants

Consumers’ income does not play as big of a role as it may originally have

© 2012, Prosper®

For More About Americans and Their Fast Food

McDonald’s, Taco Bell and Wendy’s Customers Most Unhappy with Their Health view Fast food frequenters’ wellbeing tied to personal behavior

rather than drive-thru of choice

The Changing American Consumer

Identifies consumer trends regarding the Fast Food Industry (Chapter 6: Make Mine Large)

© 2012, Prosper®

The Changing American Consumer

Some of the consumer trends identified in The Changing American Consumer include: Personal Finance | Chapter 1: America, Land of Plenty? Home Ownership | Chapter 3: Building the American Castle Auto Market |Chapter 4: Consumers’ Love Affair with Autos Online Shopping | Chapter 8: Shopping in Your Boxers, Briefs

or Bathrobe

Every chapter includes top five lessons learned

© 2012, Prosper®

The Changing American Consumer

American consumers’ real beliefs, attitudes and behavior revealed by unique methods and analytical software from BIGinsight™

Consumer confidence and purchasing intentions based on focus, in-depth analysis

A comparison of high-earners and regular consumers – with surprising results!

Trends to help businesses target their markets better in the coming decade

Consumers’ attitudes towards: credit, debt mortgages, buying cars and houses, choosing cell phones, fast food and store brand goods, big box retailers, online and TV shopping, social networking, and politics.

American consumers’ long-term economic hopes and fears

Vital Insights for American Businesses!

© 2012, Prosper®

The Changing American Consumer

American consumers’ real beliefs, attitudes and behavior revealed by unique methods and analytical software from BIGinsight™

Consumer confidence and purchasing intentions based on focus, in-depth analysis

A comparison of high-earners and regular consumers – with surprising results!

Trends to help businesses target their markets better in the coming decade

Consumers’ attitudes towards: credit, debt mortgages, buying cars and houses, choosing cell phones, fast food and store brand goods, big box retailers, online and TV shopping, social networking, and politics.

American consumers’ long-term economic hopes and fears

Vital Insights for American Businesses!

For more information or to purchase, please visit:

www.ChangingConsumer.com/info

Kindle edition coming soon!

© 2012, Prosper®

BIG

Con

sum

er

Blo

g FYU: Shoes view

Generation Gap: Confidence Defined view

Is Pinterest Your New Obsession? view

It’s Me and Jamie Oliver Against the World view

Generation Gap: Yuck, It’s Tax Season view

State Superlatives: Dreamiest Destination, Finest Fare, Best Bet for a “Rerun” + more view

UPCOMING: The Award for Best Portrayal of an Ideal Model Family Goes to… view

“Fair is Fair” but is Square…well…Square? view

© 2012, Prosper®

Con

tact

400 W. Wilson Bridge Road Suite 200 Worthington, OH 43085 Ph: 614-846-0146 [email protected]

Dr. Marianne Bickle Center for Retailing, University of South Carolina [email protected] Forbes Prosper Now Blog

for complimentary insights, visit: www.BIGinsight.com

Related Documents