Beyond portals, content and mobile entertainment Mobile service evolution in the Baltics Sarunas Chomentauskas, BITE group [email protected]

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Beyond portals, content and mobile entertainment

Mobile service evolution in the Baltics

Sarunas Chomentauskas, BITE [email protected]

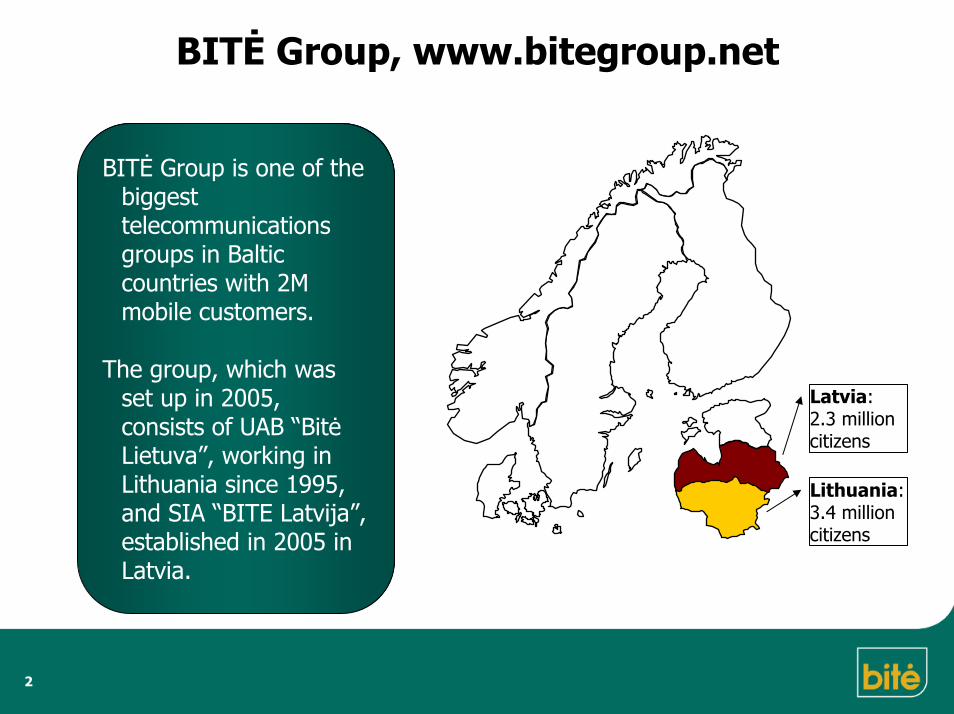

BITĖ Group, www.bitegroup.net

2

BITĖ Group is one of the biggest telecommunicationsgroups in Baltic countries with 2M mobile customers.

The group, which was set up in 2005, consists of UAB “BitėLietuva”, working in Lithuania since 1995, and SIA “BITE Latvija”, established in 2005 in Latvia.

Latvia: 2.3 million citizens

Lithuania: 3.4 million citizens

3

Looking back at 2006

4

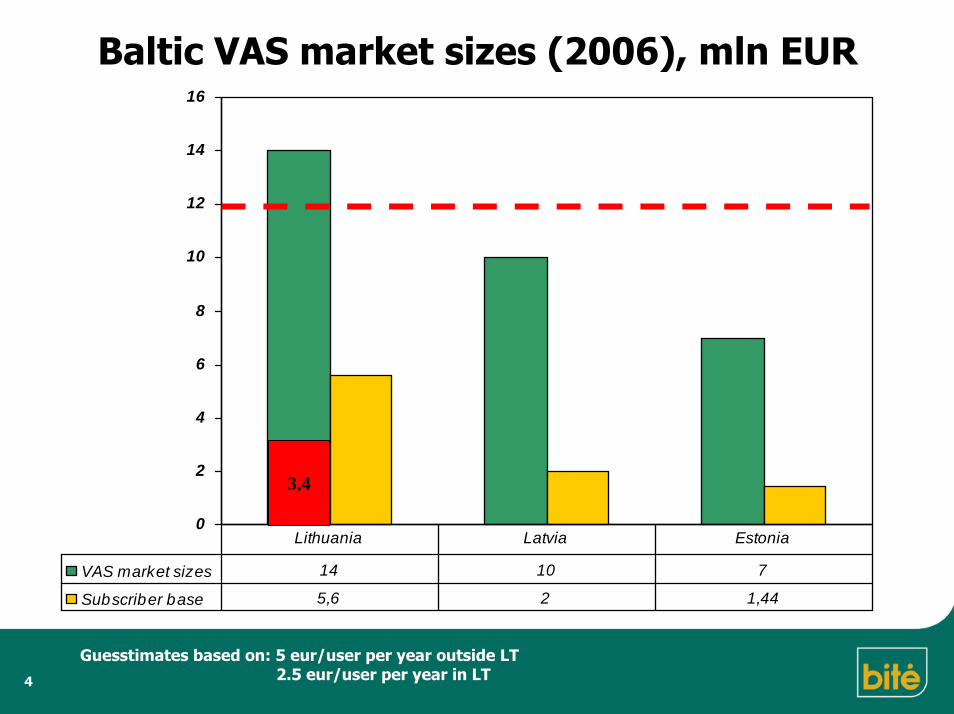

Baltic VAS market sizes (2006), mln EUR

0

2

4

6

8

10

12

14

16

VAS market sizes 14 10 7

Subscriber base 5,6 2 1,44

Lithuania Latvia Estonia

3,4

Guesstimates based on: 5 eur/user per year outside LT2.5 eur/user per year in LT

- Lt

1.000.000 Lt

2.000.000 Lt

3.000.000 Lt

4.000.000 Lt

5.000.000 Lt

6.000.000 Lt

7.000.000 Lt

8.000.000 Lt

9.000.000 Lt

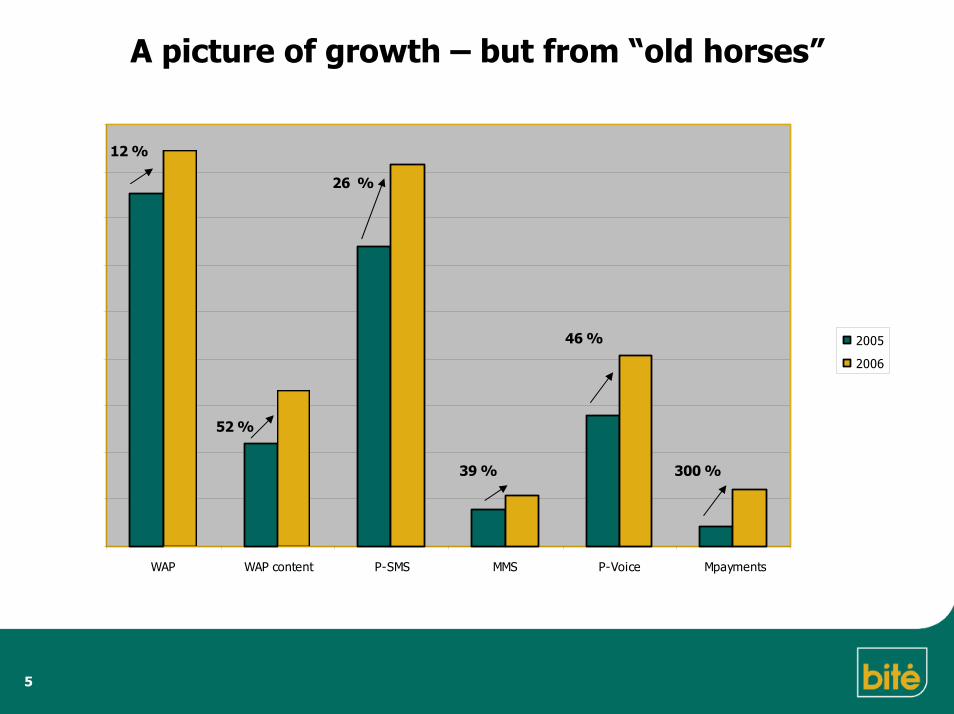

WAP WAP content P-SMS MMS P-Voice Mpayments

2005

2006

12 %

52 %

26 %

39 %

46 %

300 %

A picture of growth – but from “old horses”

5

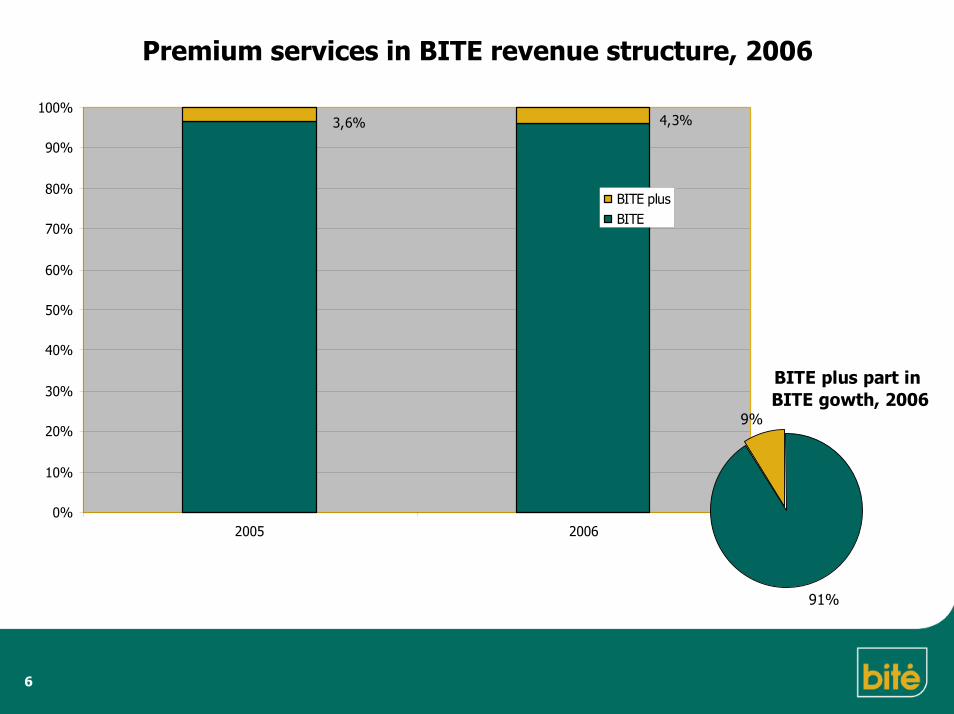

Premium services in BITE revenue structure, 2006

6

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2005 2006

BITE plusBITE

3,6% 4,3%

BITE plus part in BITE gowth, 2006

91%

9%

7

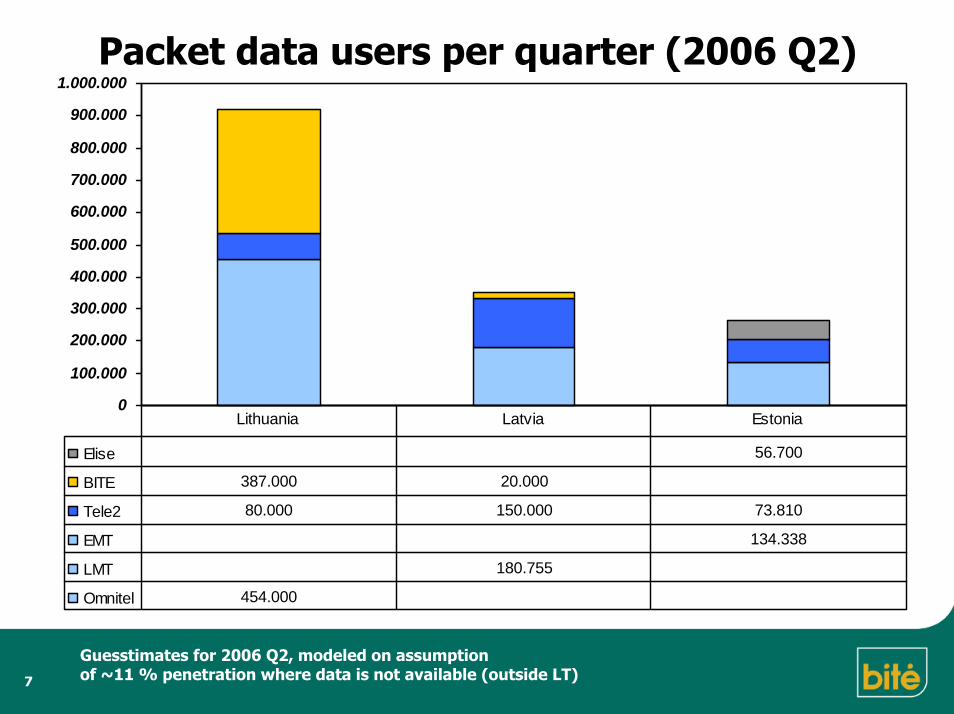

Packet data users per quarter (2006 Q2)

0

100.000

200.000

300.000

400.000

500.000

600.000

700.000

800.000

900.000

1.000.000

Elise 56.700

BITE 387.000 20.000

Tele2 80.000 150.000 73.810

EMT 134.338

LMT 180.755

Omnitel 454.000

Lithuania Latvia Estonia

Guesstimates for 2006 Q2, modeled on assumptionof ~11 % penetration where data is not available (outside LT)

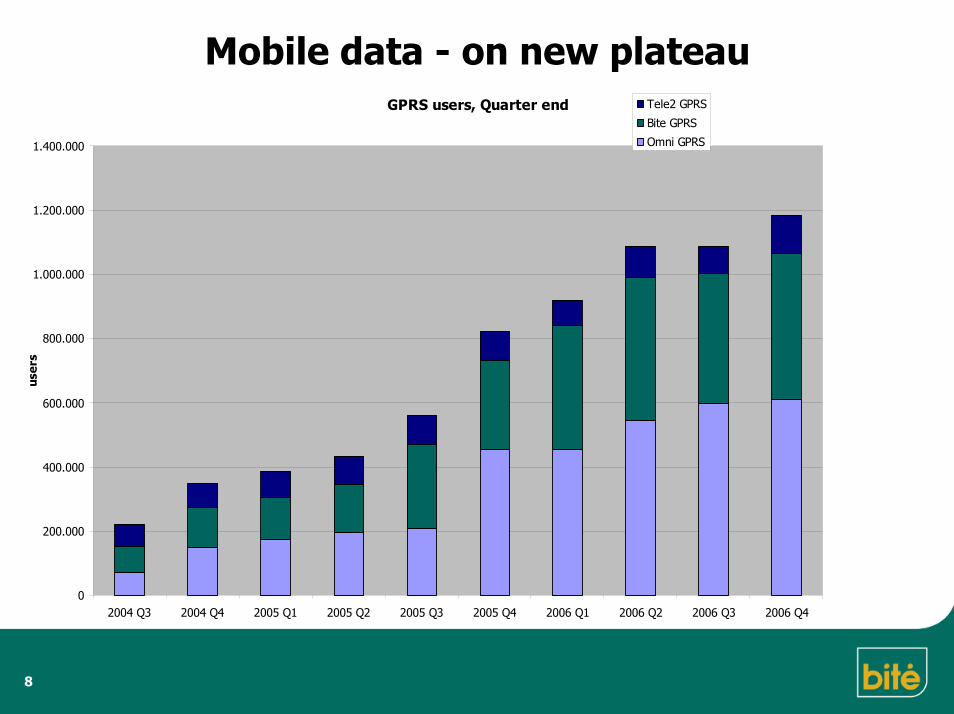

Mobile data - on new plateau

8

GPRS users, Quarter end

0

200.000

400.000

600.000

800.000

1.000.000

1.200.000

1.400.000

2004 Q3 2004 Q4 2005 Q1 2005 Q2 2005 Q3 2005 Q4 2006 Q1 2006 Q2 2006 Q3 2006 Q4

user

s

Tele2 GPRS

Bite GPRS

Omni GPRS

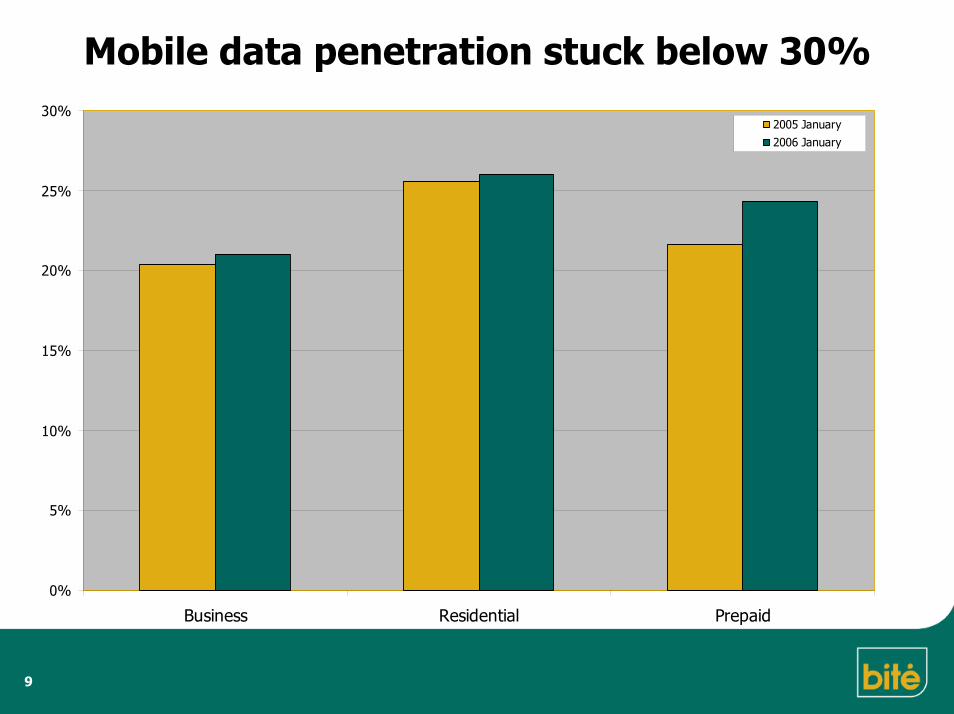

Mobile data penetration stuck below 30%

9

0%

5%

10%

15%

20%

25%

30%

Business Residential Prepaid

2005 January2006 January

10

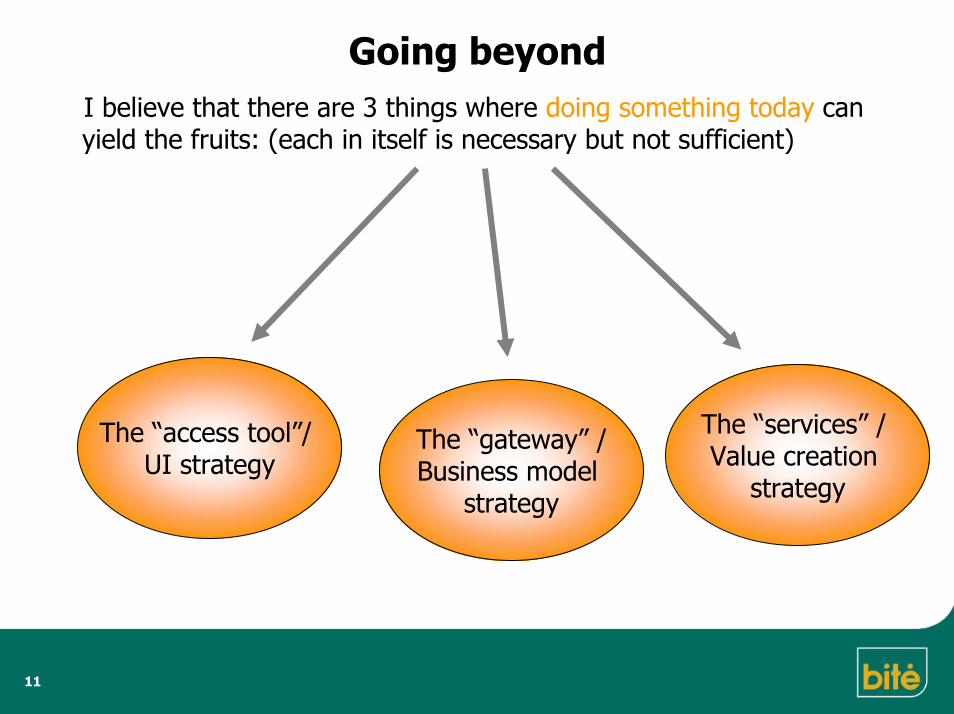

Going beyond: where to?

Going beyondI believe that there are 3 things where doing something today can yield the fruits: (each in itself is necessary but not sufficient)

The “access tool”/ UI strategy

The “services” / Value creation

strategy

The “gateway” /Business model

strategy

11

12

Service=Software

Independent consumption enabler in mobile context.

Accessory/helper in context with other media.

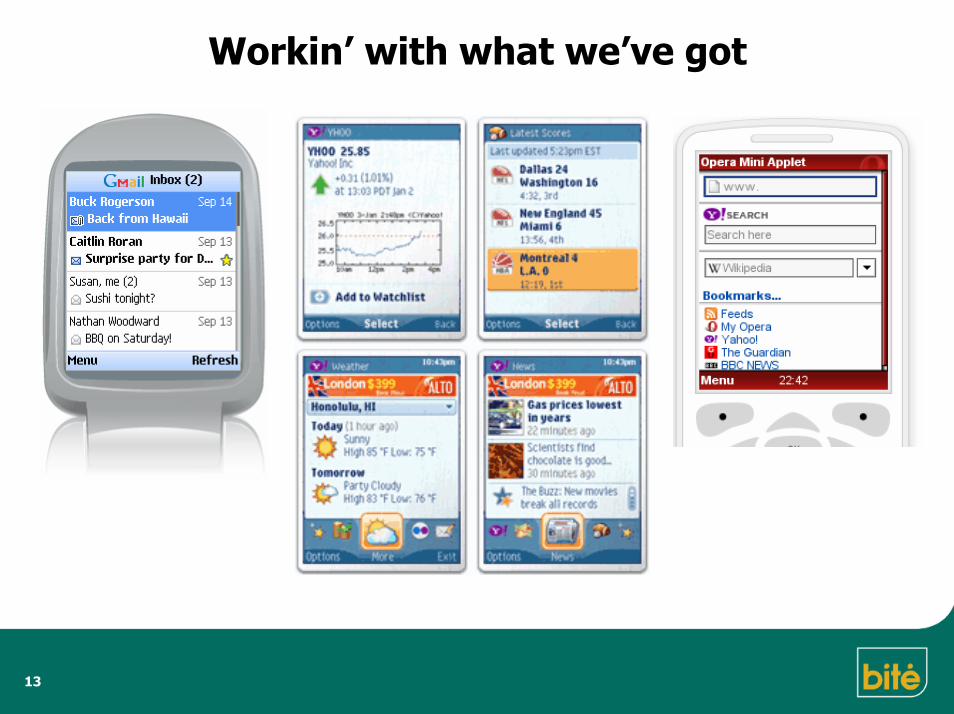

Workin’ with what we’ve got

13

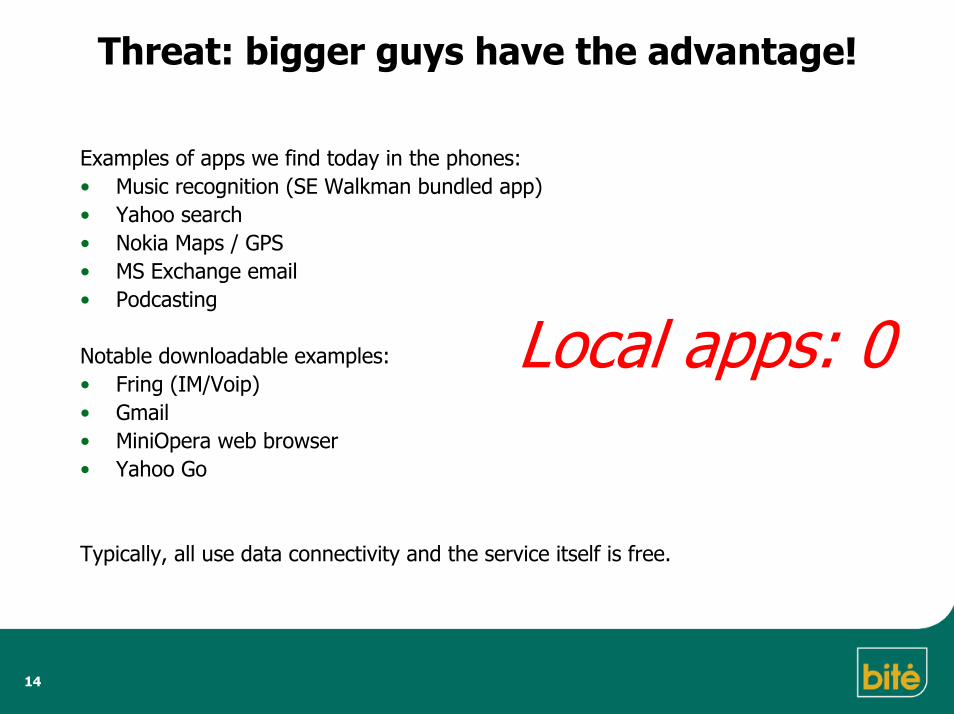

Threat: bigger guys have the advantage!

Examples of apps we find today in the phones: • Music recognition (SE Walkman bundled app)• Yahoo search • Nokia Maps / GPS • MS Exchange email• Podcasting

Notable downloadable examples: • Fring (IM/Voip)• Gmail • MiniOpera web browser• Yahoo Go

Typically, all use data connectivity and the service itself is free.

Local apps: 0

14

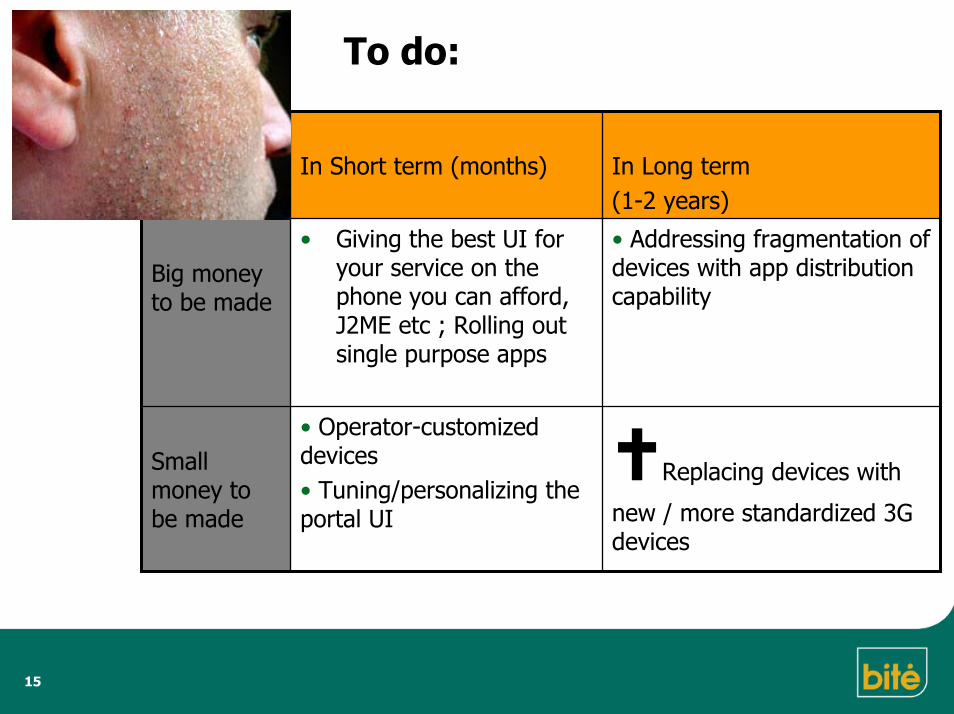

In Short term (months) In Long term(1-2 years)

Big moneyto be made

• Giving the best UI for your service on the phone you can afford, J2ME etc ; Rolling out single purpose apps

• Addressing fragmentation of devices with app distribution capability

Small money to be made

• Operator-customized devices • Tuning/personalizing the portal UI

Replacing devices with

new / more standardized 3G devices

To do:

15

16

Evolving the business models

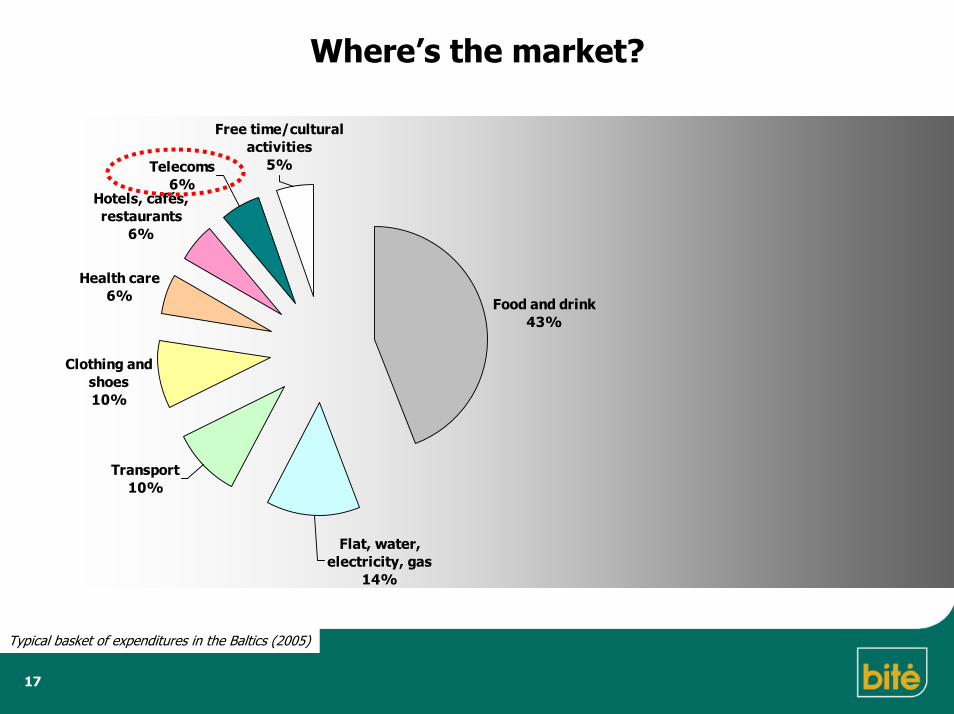

Where’s the market?

Food and drink43%

Clothing and shoes10%

Health care6%

Hotels, cafés, restaurants

6%

Free time/cultural activities

5%

Transport10%

Flat, water, electricity, gas

14%

Telecoms6%

17

Typical basket of expenditures in the Baltics (2005)

18

Telco=Gateway

•By definition, a “gate” to partners

•All parties win/win

•SPs, propose a fair model, please!

Case in point: Mobile TV• Up and running for 1 year now• 20 channels streamed live• Crappy business model – media companies capable only of cable channel approach.

19

-1.000,00 EUR

0,00 EUR

1.000,00 EUR

2.000,00 EUR

3.000,00 EUR

4.000,00 EUR

5.000,00 EUR

6.000,00 EUR

1 2 3 4 5 6

Total LT+LVCosts

Net

Case in point: Mobile Advertising

Letting the free content flourish

… Admobi mobile advertising network for the whole country.

… First commercial ads by mobile service providers.

… ~ 20 mobile sites has connected to the network.

20

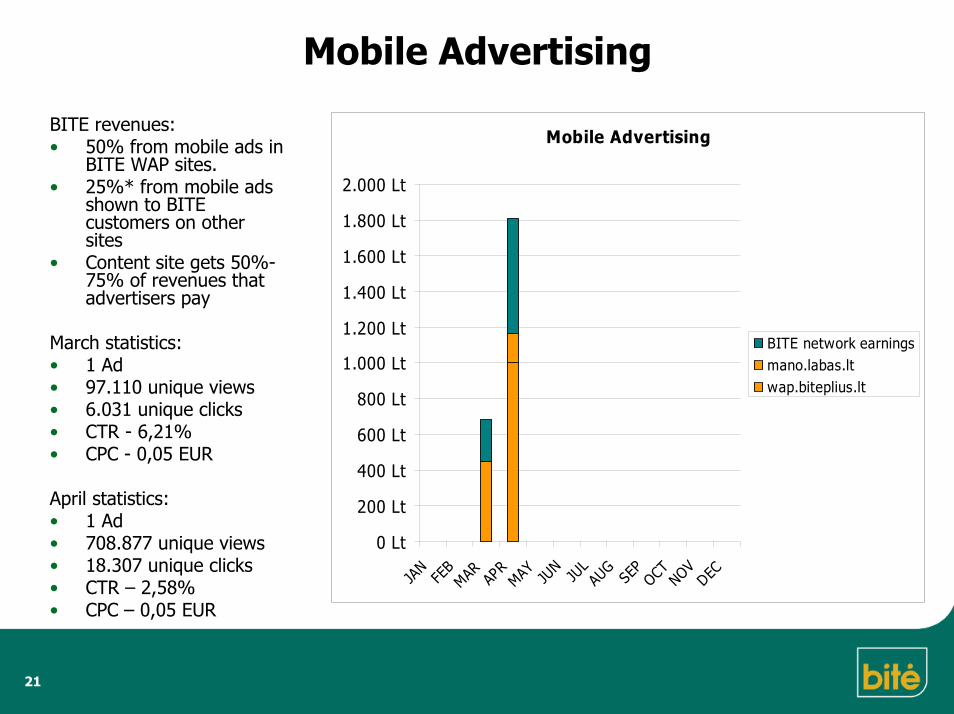

Mobile Advertising

21

BITE revenues:• 50% from mobile ads in

BITE WAP sites.• 25%* from mobile ads

shown to BITE customers on other sites

• Content site gets 50%-75% of revenues that advertisers pay

March statistics:• 1 Ad • 97.110 unique views• 6.031 unique clicks• CTR - 6,21% • CPC - 0,05 EUR

April statistics:• 1 Ad• 708.877 unique views• 18.307 unique clicks• CTR – 2,58%• CPC – 0,05 EUR

Mobile Advertising

0 Lt

200 Lt

400 Lt

600 Lt

800 Lt

1.000 Lt

1.200 Lt

1.400 Lt

1.600 Lt

1.800 Lt

2.000 Lt

JAN

FEB

MAR APR

MAY JUN

JUL

AUG

SEP

OCT NOVDEC

BITE network earningsmano.labas.ltwap.biteplius.lt

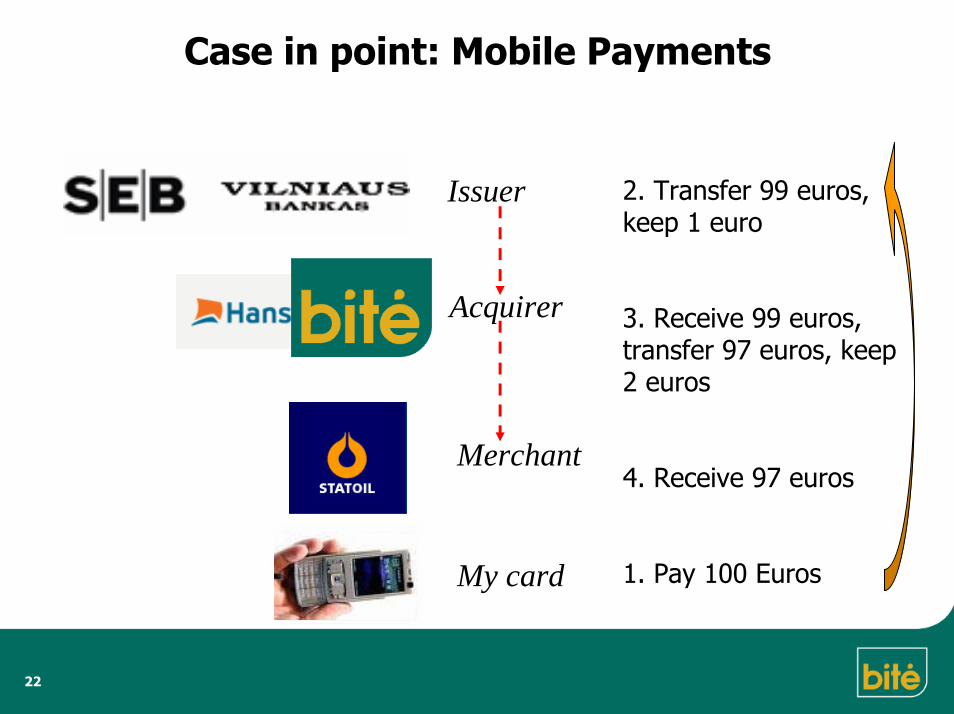

Case in point: Mobile Payments

2. Transfer 99 euros, keep 1 euro

3. Receive 99 euros, transfer 97 euros, keep 2 euros

4. Receive 97 euros

1. Pay 100 Euros

22

Issuer

Merchant

My card

Acquirer

23

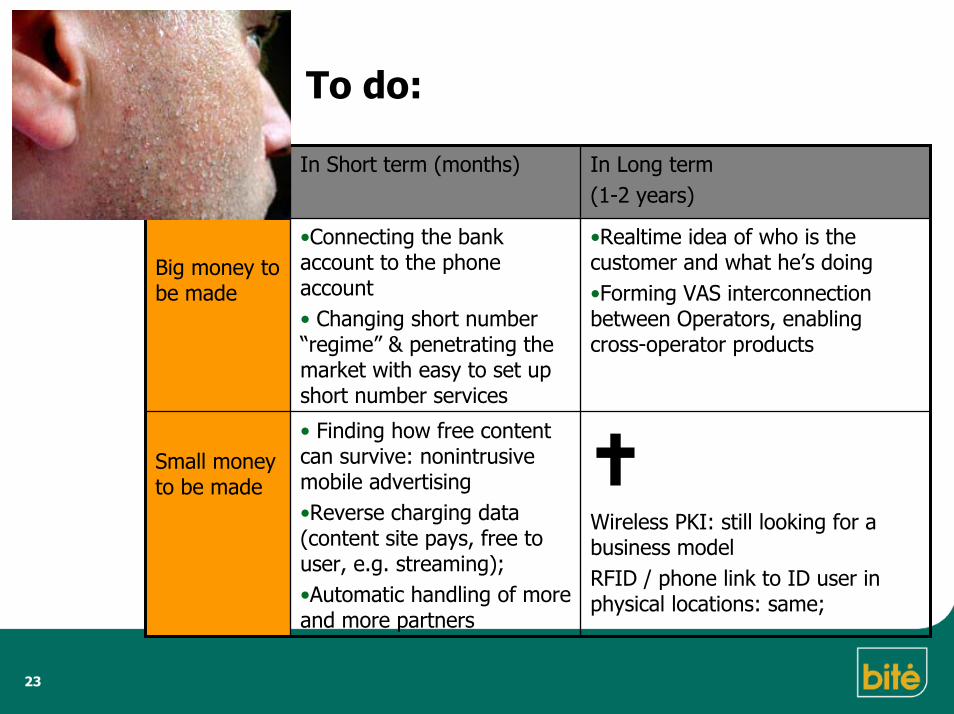

To do:

In Short term (months) In Long term(1-2 years)

Big money to be made

•Connecting the bank account to the phone account• Changing short number “regime” & penetrating the market with easy to set up short number services

•Realtime idea of who is the customer and what he’s doing•Forming VAS interconnection between Operators, enabling cross-operator products

Small moneyto be made

• Finding how free content can survive: nonintrusive mobile advertising•Reverse charging data (content site pays, free to user, e.g. streaming); •Automatic handling of more and more partners

Wireless PKI: still looking for a business modelRFID / phone link to ID user in physical locations: same;

24

Services:relevance, please

25

“If there’s nothing veryspecial about your work…

you won’t get noticed, and that means

you won’t get paid much, either” —Tom Peters

26

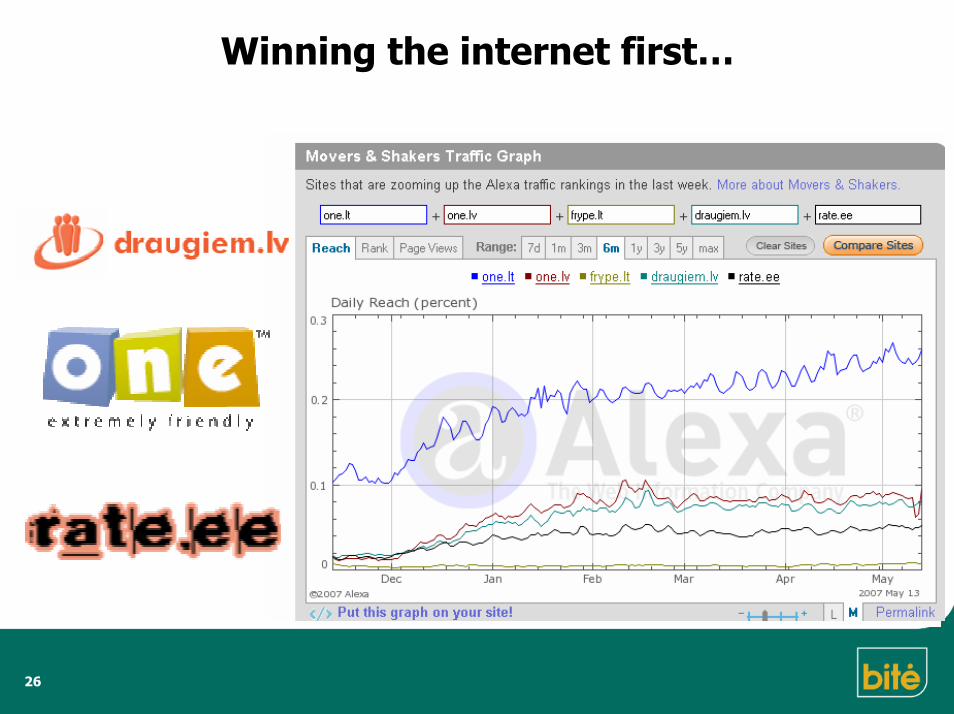

Winning the internet first…

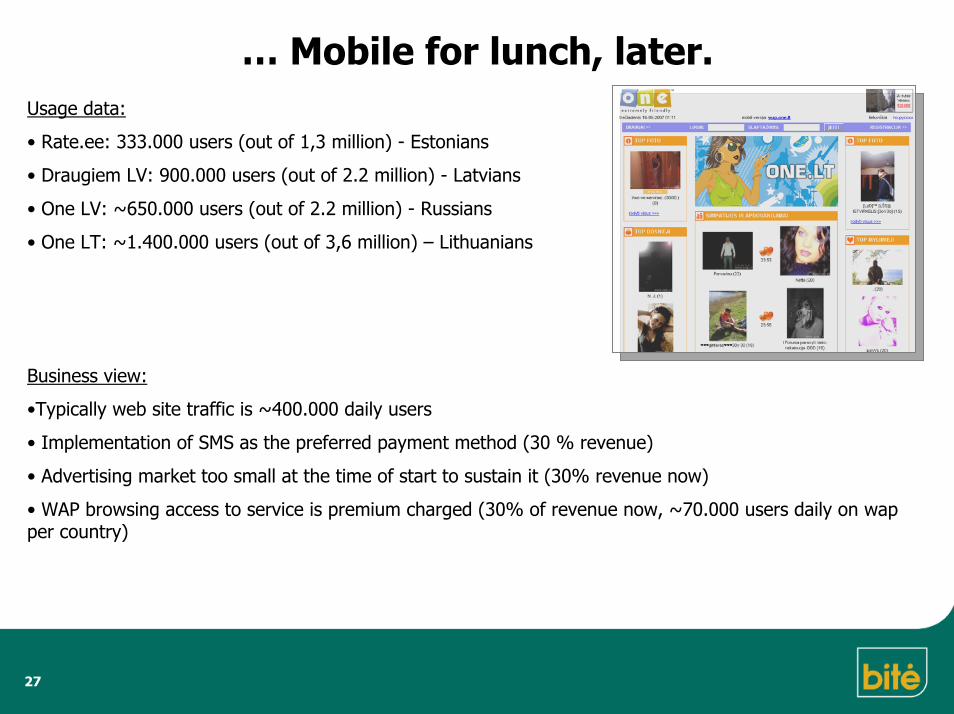

… Mobile for lunch, later. Usage data:

• Rate.ee: 333.000 users (out of 1,3 million) - Estonians

• Draugiem LV: 900.000 users (out of 2.2 million) - Latvians

• One LV: ~650.000 users (out of 2.2 million) - Russians

• One LT: ~1.400.000 users (out of 3,6 million) – Lithuanians

Business view:

•Typically web site traffic is ~400.000 daily users

• Implementation of SMS as the preferred payment method (30 % revenue)

• Advertising market too small at the time of start to sustain it (30% revenue now)

• WAP browsing access to service is premium charged (30% of revenue now, ~70.000 users daily on wap per country)

27

Ticking off the other checkboxes

• Some notable examples can be summarized in few sentences:Mobile news: competition drives premium sites to go free, waiting for the advertising revenuesMobile sports: subscription based fan clubs thrive, but growth perspectives lowMobile TV: weak consumption, problematic marginMobile music: sales of truetones weak, very poor margin

• Some have more success:Mobile games: strong sales, good marginFotobazaar: there’s really a lot of photos out thereMobile gambling: getting the format rightMobile parking: success where done right (20% Vilnius, ~70% in Tallin, 0% in Riga)

28

To do:

In Short term (months) In Long term(1-2 years)

Big money to be made

Reach to millions. Monetize later or as you go along if possible.Super-relevant for the age group/segment. Can’t live without it.

Adressing the segments: women, middle agedMoving out of of “air”into real problem areas, replacing cash

Small moneyto be made

Mobile gamesMobile musicM-payments

Mobile TV

Instant messagingLBS, etc

29

Thank you!Sarunas Chomentauskas, Head of mobile internet / BITE [email protected]

You will find the full copy of this presentation available for download.

Get more info on the “BITE plus” partnership progam and start working with us now! Visit

http://partner.biteplius.lt/

30

Related Documents