November 2020 BEYOND MODERN PORTFOLIO THEORY: EXPECTED UTILITY MAXIMISATION Investors persistently attempt to beat the market using different approaches to portfolio construction. One of the most conventional methods is the Markowitz (1952) Modern Portfolio Theory, which has been widely used since its introduction in the 1950s. The underlying assumptions of this method have been proven to be unrealistic over time. In this article, we explore the utility-based approach, which addresses the well-known pitfalls of Modern Portfolio Theory. This article is focused on comparison of the strengths and weaknesses of these two frameworks, along with their applications in portfolio construc- tion. UTILITY THEORY The general idea of Utility theory lies in the possibility of depicting the pref- erences of an individual by a utility function. The concept of rationality implies that the utility function of an individual must satisfy the von Neu- mann & Morgenstern (1953) axioms, implying transitivity and complete- ness of the individual’s preferences. For the purposes of analysing the be- haviour of a rational individual making investment decisions, it is assumed that an increased consumption of a good leads to higher utility, leading to a positive incline. Another assumption is the decreasing marginal utility, which gives the utility function a concave appearance. The meaning of this is that an extra unit of wealth increases the utility less when the wealth is bigger. Utility functions may differ considerably and should be selected based on the specific use case. In finance, it is common to choose the family of con- stant risk aversion utility functions. This implies that the investor keeps the same disinclination towards the risk over a period of time. For de- tailed information about properties and usages of the utility function, see Eeckhoudt et al. (2005). By making some further fundamental assumptions, e.g. making it possible to consistently rank the utility of all goods, it can be shown that the optimal portfolio preferred by all investors under uncertainty is represented by the portfolio that maximizes their expected utility. Beyond Modern Portfolio Theory: Expected Utility Maximisation 1

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

November 2020

BEYOND MODERN PORTFOLIOTHEORY: EXPECTED UTILITYMAXIMISATION

Investors persistently attempt to beat themarket using different approachesto portfolio construction. One of the most conventional methods is theMarkowitz (1952) Modern Portfolio Theory, which has been widely usedsince its introduction in the 1950s. The underlying assumptions of thismethod have been proven to be unrealistic over time. In this article, weexplore the utility-based approach, which addresses the well-known pitfallsof Modern Portfolio Theory.

This article is focused on comparison of the strengths and weaknesses ofthese two frameworks, along with their applications in portfolio construc-tion.

UTILITY THEORY

The general idea of Utility theory lies in the possibility of depicting the pref-erences of an individual by a utility function. The concept of rationalityimplies that the utility function of an individual must satisfy the von Neu-mann & Morgenstern (1953) axioms, implying transitivity and complete-ness of the individual’s preferences. For the purposes of analysing the be-haviour of a rational individual making investment decisions, it is assumedthat an increased consumption of a good leads to higher utility, leading toa positive incline. Another assumption is the decreasing marginal utility,which gives the utility function a concave appearance. The meaning of thisis that an extra unit of wealth increases the utility less when the wealth isbigger.

Utility functions may differ considerably and should be selected based onthe specific use case. In finance, it is common to choose the family of con-stant risk aversion utility functions. This implies that the investor keepsthe same disinclination towards the risk over a period of time. For de-tailed information about properties and usages of the utility function, seeEeckhoudt et al. (2005).

By making some further fundamental assumptions, e.g. making it possibleto consistently rank the utility of all goods, it can be shown that the optimalportfolio preferred by all investors under uncertainty is represented by theportfolio that maximizes their expected utility.

Beyond Modern Portfolio Theory: Expected Utility Maximisation 1

November 2020

MODERN PORTFOLIO THEORY

Modern portfolio theory (MPT) is a utility-maximizing framework devisedby Nobel laureate Markowitz (1952). In this framework, the risk is quan-tified by the variance and the returns are assumed to follow a multivariatenormal distribution. If this assumption holds, the ranking of all portfolios isdetermined by solely their mean and variances. This means that the port-folio with the highest utility is given by Mean-Variance optimization, i.e.maximisation of the expected return for a given variance, or alternatively,minimisation of variance for a given mean return.

PITFALLS OF MODERN PORTFOLIO THEORY

Despite its popularity, MPT has received considerable critique. Mainly,the criticism concerns the unrealistic assumptions regardingmarket move-ments, in particular the assumption that the returns are normally dis-tributed. Numerous studies have shown that a multivariate normal distri-bution can not adequately capture the behaviour of financial time series;returns have been shown to have larger tails with excess kurtosis and sig-nificant skewness, as both correlations and volatility increase in turbulenttimes. As MPT considers only the first two moments, the method com-pletely disregards these properties. Consequently, MPT often producessuboptimal portfolios that do not maximize the investors’ utility. In ad-dition, as tail risks are overlooked, MPT fails to capture the complete riskof the portfolio and the predictions can potentially show large deviationsrelative to actual observed outcomes.

MODERN PORTFOLIO THEORY VS. UTILITY THEORY

To compare the two methods, we first examine their common traits. TheMPT is actually a simplified version of the Utility theory. In fact, the Mean-Variance approximation is a second-order Taylor expansion of a utilityfunction around the mean portfolio return. While MPT only incorporatesthe two first moments, Utility theory takes all moments into account. Con-sequently, Mean-Variance optimization is only equivalent to the maximumexpected utility if the following is true:

1. All asset returns are multivariate normally distributed 1.

2. The utility function is quadratic.

1More specifically, this applies to elliptic distributions.

Beyond Modern Portfolio Theory: Expected Utility Maximisation 2

November 2020

A quadratic utility function has two considerable drawbacks; it implies anincreasing level of absolute risk aversion along with an existence of a maxi-mum value for the utility, meaning that the expected utility decreases withconsumption of a good after this point.

As discussed above, the assumption of normally distributed returns hasbeen contradicted by empirical studies. If this assumption is removed,however, the optimal MPT portfolio would no longer maximize the ex-pected utility as the mean and variance are no longer sufficient to ade-quately represent the return distribution. There has been several attemptsto address this problem. For instance, by using a different risk measure,e.g. Value-at-Risk or Expected Shortfall, the issue with the incomplete riskpicture can be slightly amended. However, a new problem arises; the sug-gested risk measures still don’t take all the distributional properties of theportfolio value into account. When the risk measures are rewritten intodecision rules, the resulting utility functions will contain plateaus and non-continuous derivatives. Consequently, as the utility function is no longerconcave and this means the investor may have to pay to take on more risk.

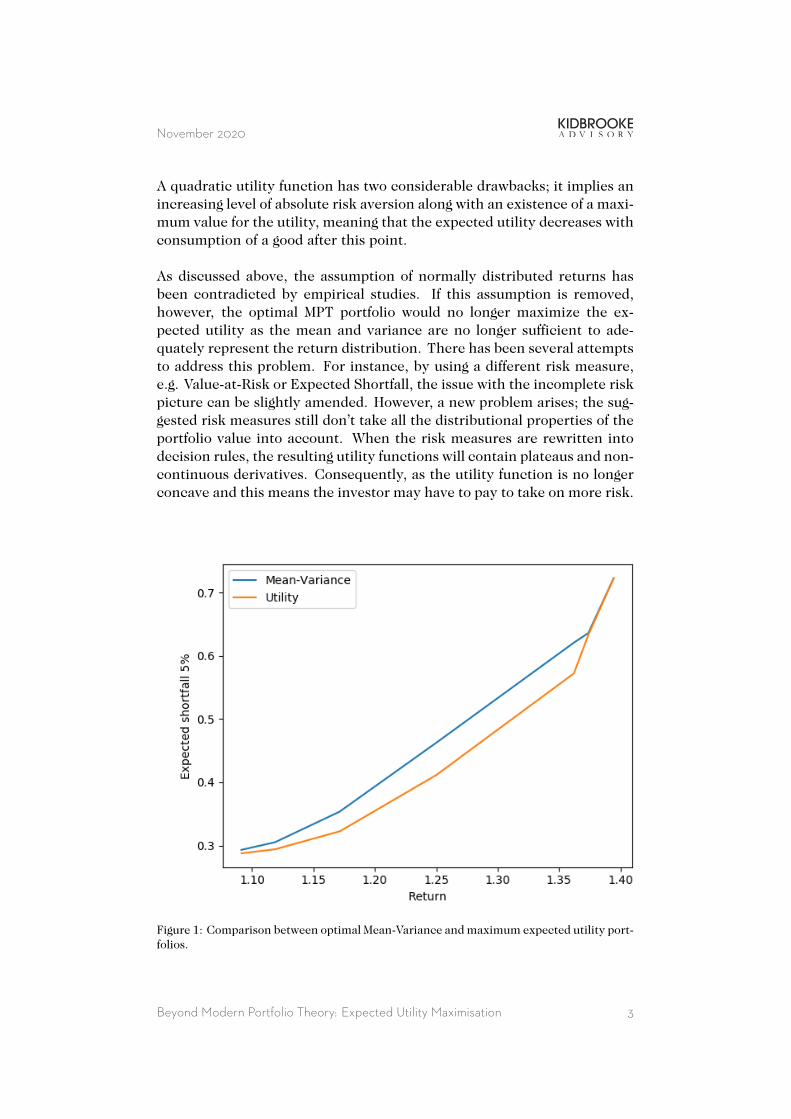

Figure 1: Comparison between optimal Mean-Variance andmaximum expected utility port-folios.

Beyond Modern Portfolio Theory: Expected Utility Maximisation 3

November 2020

To demonstrate the differences between the optimal portfolios obtainedby two frameworks, consider Figure 1. The plot displays the 5% ExpectedShortfall for each return level of optimal Mean-Variance and maximum ex-pected utility portfolios, with an asset universe consisting of an emergingmarket equity index, a global government bond index and a global equityindex. It is clear that expected utility maximisation results in more effi-cient portfolios, i.e., providing the same return for a lower related tail-risk.

FURTHER REMARKS ON UTILITY THEORY

After discussing the advantages over MPT, it is important to note that Util-ity theory has a number of limitations. One of the most prominent flawsis the so called Allais paradox, implying that maximizing the expected util-ity leads to contradictions regarding the utility function. This, and othercontradictions, arise mainly for very small investments in regard to thetotal wealth of the investor, or for comparisons between alternatives thatare difficult to relate to. However, as long as the investment constitutes asignificant part of the total wealth, the expected utility maximization willnot be influenced by these problems.

Empirical studies have shown that the utility function derived for a ratio-nal, risk-averse investor has a poor fit for a actual consumer behaviour. Theexplanation for this is that investors have been shown to act irrationally attimes. This set the base for Prospect theory, which is briefly introduced inthe subsequent section. However, it should be noted that this result is inno way a limitation; as will be further discussed below, an irrational andrisk-loving investment strategy is never a good idea.

PROSPECT THEORY

As a branch of Utility theory, Prospect theory is used to describe the wayconsumers make decisions under uncertainty. As previously mentioned,investors are known to act irrationally at times. Prospect theory aims tocapture this by assigning a new shape to the utility function, in which a lossaversion parameter is present in addition to the risk aversion parameter.This gives the function a convex shape up until a certain reference pointis reached (e.g. a savings goal), implying that the investor actually paysfor risk up until this point. Findings within cognitive psychology implythat consumers actually display this irrational behaviour, as all means aredeployed to reach, for instance, their savings goal.

As previously mentioned, while Prospect theory more accurately portrays

Beyond Modern Portfolio Theory: Expected Utility Maximisation 4

November 2020

the behaviour of an investor, one should refrain from using it as an invest-ment strategy. This would result in a risk-loving approach where the in-vestor pays for risk, which is obviously never a good strategy. For a deeperaccount on Prospect theory and its applications, see Kahneman & Tversky(1979).

Beyond Modern Portfolio Theory: Expected Utility Maximisation 5

November 2020

BibliographyEeckhoudt, L., Gollier, C., & Schlesinger, H. 2005. Economic and FinancialDecisions under Risk. Princeton University Press, Princeton.

Kahneman, D., & Tversky, A. 1979. Prospect Theory: An analysis of Deci-sion Making under Risk. Econometrica. 47 (2), 263–291.

Markowitz, H.M. 1952. Portfolio Selection. Journal of Finance. 7 (1), 77–91.

von Neumann, J., & Morgenstern, O. 1953. Theory of Games and EconomicBehavior. Princeton University Press.

Beyond Modern Portfolio Theory: Expected Utility Maximisation 6

November 2020

CONTACT USDo you want to know more about Kidbrooke Advisory?Please contact us for more information.

a. Kidbrooke Advisory ABEngelbrektsgatan 7SE-114 32 StockholmSweden

FREDRIK DAVÉUSManaging Partner+46(0)761 170 [email protected]

EDVARD SJÖGRENPartner+46(0)733 182 [email protected]

Beyond Modern Portfolio Theory: Expected Utility Maximisation 7

November 2020

DISCLAIMERCopyright 2020 Kidbrooke Advisory AB; All rights reserved. Reproduction in whole or in part is pro-hibited except by prior written permission of Kidbrooke Advisory AB registered in Sweden. The infor-mation in this document is believed to be correct but cannot be guaranteed. All opinions and estimatesincluded in this document constitute our judgement as of the date included and are subject of changewithout notice. Any opinions expressed do not constitute any form of advice (including legal, tax,and or investment advice). This document is intended for information purposes only and is not in-tended as an offer or recommendation to buy or sell securities. Kidbrooke Advisory AB excludes allliability howsoever arising (other than liability which may not otherwise be limited or excluded underapplicable law) to any party for any loss resulting from any action taken as a result of the informationprovided in this document. The Kidbrooke Advisory AB, its clients and officers may have a positionor engage in transactions in any of the securities mentioned.

Beyond Modern Portfolio Theory: Expected Utility Maximisation 8

Related Documents