Beyond connectivity Can telecom operators offer new services to business customers?

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Beyond connectivityCan telecom operators offer new services to business customers?

Telecommunications operators are facing the challenges of growth, convergence, business transformation, technological change and regulatory pressures in increasingly difficult economic conditions. Operators choose Ernst & Young because they value our industry-based approach to addressing their assurance, tax, transaction and advisory needs. They know that they have much to gain from our clear understanding of the opportunities, complexities and commercial realities of the telecommunications industry — wherever in the world they’re operating. What gives us this understanding is our Global Telecommunications Center. Operating from Paris, Cologne, Johannesburg, Riyadh, Delhi, Beijing, and San Antonio, the Center brings together people and ideas from across the world, to help our clients address the challenges of today — and tomorrow. Our clients benefit from our insights on key trends and emerging issues. These may relate to the economic downturn, next-generation services, infrastructure sharing, outsourcing, revenue assurance, operational efficiency, regulations, future growth markets or mergers and acquisitions. We help our clients react to trends in a way that improves the financial performance of their business. Learn more about our approaches and services by visiting our website: www.ey.com/telecommunications

About Ernst & Young’s Global Telecommunications Center

About the survey

The quantitative findings presented in this report are based on an online survey conducted by the Economist Intelligence Unit (EIU) in November 2009. Ernst & Young commissioned the EIU to conduct the survey and write this report. A total of 365 senior procurement and IT executives from a broad range of industries participated in the survey, of whom 50% were C-suite or above. Roughly 33% were based in Europe, 36% in North and Latin America, 27% in the Asia-Pacific region and the remaining 4% coming from the Middle East and Africa. Participants also represented

a wide cross-section of company sizes, with 58% having annual revenue of over US$5m, and 20% with revenue of over US$5b per year. In addition to the online survey, nine executives were interviewed on the record for this report. We would like to thank everyone who participated in the research for their valuable contributions.

The Economist Intelligence Unit interviewed a small number of executives in the course of their research. We wish to thank the following people for their valuable contribution:

Beyond connectivity

Dr Martin Elspermann COO of ASIC Allianz Managed Operations and Services SE

Wim de Bruyn COO and CIO Standard Bank International

Walter Curd CIO Maxim

Kingsley Poultan Head of Corporate Infrastructure Services Standard Bank International

Philip Parker Chair Professor of Management Science INSEAD

Keith Willetts CEO and Chairman TM Forum

Philip Hawker Manager Communication Networks & Infrastructure British Airways

Mike Russell Group IS Director Atkins

Written in cooperation with:

Cont

ents

6Executivesummary

10Mixed messages from business customers Good news and bad news

28Conclusion

26

22Playing to strengths Networks, unified communications and partnerships

Smaller companies — an untapped market

14

21

Moving beyond core services Challenges ahead

Customer loyalty — looks can be deceiving

Beyond connectivity

5

Vincent de La Bachelerie Global Telecommunications Leader, Ernst & Young

Here at Ernst & Young‘s Global Telecommunications Center, we hear from telecommunications operators across the world about their challenges in delivering services to business, or enterprise, customers. Many of our clients face enormous fundamental challenges right now from intense competition across many areas of their business. This is no exception.

One of the main conclusions in our Power of the pipe study last year, was that there appeared to be a significant revenue opportunity for operators in addressing the needs of their enterprise customers, but that there were very few examples of that being done successfully.

We decided to seek first-hand evidence from the people that matter: the buyers.

The conclusions perhaps won't surprise everyone. Many of our clients still have some way to go to overcome scepticism about the services they can provide,

especially if they aim to position themselves beyond the core network. I'm proud to see that our study offers our clients some clear indications for how they can improve their success in this area.

Our thanks to the Economist Intelligence Unit for their research. And our thanks also to the executives who kindly agreed to be quoted in our report. This report has depended on the generous time and insight of those who make major procurement decisions every day. Finally, our thanks go to the 365 professionals who took time to respond to our survey.

Foreword

Vincent de La Bachelerie

Beyond connectivity

6

Executive summary

1.

7

Beyond connectivity

Getting accurate answers to this question is vitally important for telcos that wish to generate incremental revenue from enterprises, as well as attract and retain business customers. With a clearer understanding of their customers’ perceptions, telcos will be in a better position to shape more effective strategies for targeting enterprises.

What do enterprises really think about their telecoms service providers?

8

Beyond connectivity

Not all telcos are starting from the same point. Some have global network footprints, while others have only regional or national reach. Some telcos have both fixed-line and mobile operations, and others run either a fixed-line or a mobile network. Despite this diversity, a survey conducted by the Economist Intelligence Unit in November 2009 revealed large areas of agreement among respondents (representing large and smaller companies, various industry sectors and based in different geographical regions) about what they see as telcos’ main strengths and weaknesses. The overall message is remarkably uniform: telcos are doing a reasonably good job at providing core connectivity services, but there is still much scepticism that they can deliver “non-core” services.

But it’s not all doom and gloom for telcos looking to broaden their service portfolio beyond the so-called dumb pipe. Enterprises haven’t ruled out telcos playing a more expansive role, but, as this report argues, to move successfully into non-core service areas, telcos will have to emphasize more of their network strengths, explore further strategic partnerships with IT vendors and heed warnings from enterprises about their shortcomings.

Telcos are doing a reasonably good job at providing core connectivity services, but there is still much scepticism that they can deliver “non-core” services.

9

Beyond connectivity

Here are the key findings from the report.

• Telcos face a tough challenge convincing enterprise customers they can be trusted providers of additional services beyond voice and data. If telcos want to win customers over, they would be better served by showing agreater understanding of individual business requirements, and to tailor their service propositions accordingly, rather than to promote a wide range of services that enterprises don’t need or want.

• Network expertise is the telco trump card. Enterprises hold their telcos in high regard for the delivery of real-time services over

IP networks, such as video and audio conferencing. Telcos are therefore well placed to play a much more prominent role within the enterprise as demand increases for unified communications, the mobile internet and Voice over internet protocol (VoIP).

• Telcos cannot assume, however, that providing a good basic connectivity service will automatically lead to greater enterprise enthusiasm for their additional services.

There is no strong correlation between offering a reliable core service and the propensity of enterprises to take on additional services from their telecoms service provider.

• Telcos can extend their capabilities through partnerships and acquisitions. By being more open to partnerships with IT providers and systems integrators, telcos

can strengthen their position in the ICT market. Acquisitions, too, can lead to greater credibility in key areas where they lack capability.

• Customers have a broadly positive view of the telco in areas of legacy expertise. Many enterprise customers are wholly satisified with the telecoms service they

currently receive. Although connectivity services are subject to ongoing pricing pressure, mobile voice and data are increasing spending priorities for many organizations.

• Smaller companies are more sceptical. The survey shows that smaller companies have more doubts than larger companies

about telcos’ ability to deliver offerings in non-core areas, such as cloud computing, Software as a service (SaaS) and unified communications.

Good news and bad news

2.

10

Mixed messages from business customers

11

Beyond connectivity

Telcos face a challenge in convincing enterprises they can be trusted providers of additional services beyond network connectivity and a few closely-related network tasks. While many business customers appear happy to let their telecoms service providers manage network security and network installation, there are high levels of resistance to letting telcos do more, particularly if it involves handling their data assets.

12

Beyond connectivity

First, the bad newsNearly half of survey respondents say they would not consider using their telecoms service provider for data backup and retrieval. Telcos’ data centers and managed hosting services are viewed with even less enthusiasm. Neither are telcos seen as natural choices by enterprises for the relatively new and growing markets of SaaS and cloud computing.

Which of the following services would you NOT consider obtaining from your telecoms service provider (as opposed to IT or other service providers)?

Enterprises have also warned telcos that they shouldn’t take for granted that enterprises will continue using them for core telecoms services. In fact, 66% of survey respondents say it doesn’t make any difference from whom they buy telco services, as long as those companies, acting as resellers, can deliver comparable quality.

Although telecoms spending by enterprises is holding up fairly well in the economic downturn, with 75% of survey respondents saying their companies’ telecoms budget will either remain the same or grow “somewhat” during the next two years, purse strings are not going to be loosened dramatically any time soon. Add in the fact that the survey respondents make it abundantly clear that price and reliability are by far their top two considerations when weighing up the performance of their current telecoms service provider, telcos can expect no let up from business customers trying to get more value for their money (with the veiled threat they will go elsewhere for their core telecoms services if they are not satisfied on price).

What are the three most important criteria for evaluating the performance of your current telecoms service provider?

0 10 20 30 40 50 60

62%

51%

37%

29%

50%

50%

32%

49%

44%

46%

33%

45%

70

SaaS

Cloud computing

Network security

Data backup and retrieval

Percentage

Domain and web hosting

Data centers (managed hosting)

Governance and compliance

Business consulting

Conferencing (web, video, audio)

Network installation and maintenance

IT help desk

Customer call centers

Source: EIU

0 10 20 30 40 50 60 70 80 90 100

Transparency of billing

Personalized/customizedoffering

Privacy/securitycredentials

Other

Corporate social responsibilitycredentials (e.g., low

carbon footprint)

Scalability

Range of productsand services

Geographical coverage

Quality of support

Price

Reliability of service 83%

78%

30%

27%

25%

13%

10%

9%

5%

2%

2%

Percentage

Source: EIU

13

Beyond connectivity

The high regard that enterprises have for telcos’ ability to provide real-time services might call into question the sincerity of survey respondents who claim it doesn’t make any difference to them where they buy telecoms services. After all, it would be easier to resolve network performance issues with the telco directly rather than with a reseller, and there isn’t much survey evidence of enterprise customers actually deserting their telecoms service providers (see Customer loyalty — looks can be deceiving, page 21). While enterprises are clearly warning telcos that they should not be complacent, their apparent open-mindedness towards resellers might partly be explained by a wish to keep telcos on their toes (and to lower their prices), particularly by those requiring service level assurances on network performance.

The survey also gives encouragement to telcos wishing to play a more prominent role in “non-core” areas. Although half of respondents say they would not consider their telco for business consulting — a service far removed from their core expertise — more than 40% are either currently paying for business consulting from their telecoms service provider or would consider doing so. Progress of this sort shows it is not beyond telcos’ capability to reinvent themselves in the eyes of many enterprise customers.

Now the good newsDespite some misgivings from customers, telcos have made progress in convincing enterprises that they are capable of delivering non-core services. For example, survey respondents appear to value telcos’ ability to deliver real-time IP-based services, such as video and audio conferencing.

Which of the following services are you currently buying or would consider buying in the next 12 months from your telecoms service provider (as opposed to IT or other service providers)?

0 10 20 30 40 50 60 70

12% 15%

25% 13%

19% 20%

25% 21%

29% 18%

22% 21%

15% 23%

18% 20%

36% 17%

39% 26%

40% 23%

41% 20%

SaaS

Cloud computing

Network security

Data backup and retrieval

Domain and web hosting

Data centers (managed hosting)

Governance and compliance

Business consulting

Conferencing (web, video, audio)

Network installation and maintenance

IT help desk

Customer call centers

Currently buying

Would consider buying inthe next 12 months

PercentageSource: EIU

Challenges ahead

Moving beyond core services

3.

14

15

Beyond connectivity

A surprise survey finding, perhaps, is that there is no strong correlation between offering a reliable core service and the propensity of enterprises to take on additional services from their telecoms service provider. The 36% of respondents who see no current drawbacks with their current service are on the whole no more willing to buy non-core services than the overall sample.

16

Beyond connectivity

Moreover, the 17% of respondents who “agree strongly” that their telco has a clear menu of services (assuming that clarity is related to the “core connectivity” services on offer) are also, on the whole, no more likely to buy (or consider buying) non-core services than those who don’t hold companies views on service menu clarity. A similar picture emerges when comparing the service-buying intentions of those who agree that telcos’ SLAs make it easy to evaluate performance with those that neither agree nor disagree on this matter.

Working hard on getting the basics right for core services will only take telcos so far, it seems, in persuading enterprise customers to take on additional services. Customer satisfaction does not necessarily lead to successful upselling.

Which of the following services are you currently buying or would you consider buying in the next 12 months from your telecoms service provider (as opposed to IT or other service providers)? (Whole sample compared with those who see no drawback with their current telecoms service.)

Telcos might take heart from the 36% of respondents who say they are perfectly happy with their telco service, but it isn’t necessarily a sign of complete success. If the satisfied customers are typically buying only simple network connectivity at ever cheaper prices, the result is not so impressive from the telcos’ perspective.

47%

61%

42%

45%

37%

63%

38%

38%

65%

53%

39%

26%

48 %

60 %

30 %

43 %

35 %

60 %

36 %

35 %

56 %

53 %

37%

18 %

No drawbacks to current telecoms serviceWhole sample

0 10 20 30 40 50 60 70

SaaS

Cloud computing

Network security

Data backup and retrieval

Domain and web hosting

Data centers (managed hosting)

Governance and compliance

Business consulting

Conferencing (web, video, audio)

Network installation and maintenance

IT help desk

Customer call centers

Percentage

Source: EIU

17

Beyond connectivity

What is the main drawback of your current telecoms service?

Tread carefully, sales teamSurvey respondents have delivered a clear statement to telcos, with more than half agreeing that “telecoms service providers should stick to their core business instead of trying to be all things to all people.” Respondents could be recalling how telcos over-reached in the past with ambitious “one-stop shop” promises, or simply they are still not convinced that telecoms service providers are thinking through their non-core service propositions carefully enough.

“Advanced services, such as SaaS and hosting, appear to be useful but are not always well thought out from telcos,” says Kingsley Poulton, Head of Corporate Infrastructure Services at Standard Bank International. “They can appear as another offering [by the telco] to provide an alternative income stream rather than a properly integrated service.”

Thoughtless over-pitching can also damage telcos’ ability to retain customers for more basic services. “I’m much more interested in talking to someone who wants to sell me a reliable, cost-effective network than someone constantly looking over my shoulder to see if there’s a chance to host my data center,” says Phil Hawker, Manager of Communication Networks and Infrastructure at British Airways.

Telcos should also think carefully about where to expend their service delivery efforts. One of the services most highly valued by enterprises, data backup and retrieval, is also one they are least willing to hand over to their telecoms service provider, so it might make sense to prioritize marketing efforts elsewhere. The survey suggests that SaaS and cloud computing could be more promising areas, for example, because customers see them as valuable and are more willing to hand over their management to telcos.

0 10 20 30 40 50 60 70 80 90 100

There are no drawbacks to my current telecoms service

Percentage

Other

Incompatible standards

Weak data privacy

Inadequate security

International coverage for your organization

Insufficient quality of service

Too much complexity

High cost 21%

13%

11%

8%

3%

3%

1%

3%

36%

Source: EIUNote: Due to rounding, percentages do not add up to 100%

18

Beyond connectivity

Comparing the services rated “valuable” or “highly valuable” by respondents with willingness to buy the service from telcos (as opposed to IT or other service provider).

The survey revealed some industry differences. Financial services companies and enterprises in the IT and technology sector value business consulting far more than manufacturing companies. Manufacturing companies, on the other hand, are more enthusiastic than financial services companies about buying SaaS from telecoms service providers. Telcos that successfully sell non-core services will be sensitive to these kinds of nuances. To deliver a more targeted sales proposition, telcos that have traditionally focused on core services will most likely have to retrain sales teams and account managers — or perhaps even partner with outside consulting professionals — if they are to make a more sophisticated and successful play for the enterprise segment.

Integrated operators are well placed, but they need to up their gameSurvey respondents are ambivalent about the importance of having one supplier for fixed and mobile services. Those who are enthusiastic about opting for one supplier are matched by just as many who do not see it as important. It might be that many “integrated” operators, which run both mobile and fixed networks, are finding it difficult to coordinate their fixed and mobile businesses to the extent where they can offer a compelling converged service.

SaaS

Cloud computing

Network security

Data backup and retrieval

Domain and web hosting

Data centers (managed hosting)

Governance and compliance

Business consulting

Conferencing (web, video, audio)

Network installation and maintenance

IT help desk

Customer call centers

Services rated “highly valuable” by respondentsCurrently buying or would consider buying in the next 12 months from a teleco

47 %

61 %

42 %

45 %

37 %

63 %

38 %

38 %

65 %

53 %

39 %

26 %

72 %

58%

49%

36%

26%

77%

49%

31%

48%

58%

44%

28%

Percentage

0 10 20 30 40 50 60 70 80

Source: EIU

19

Beyond connectivity

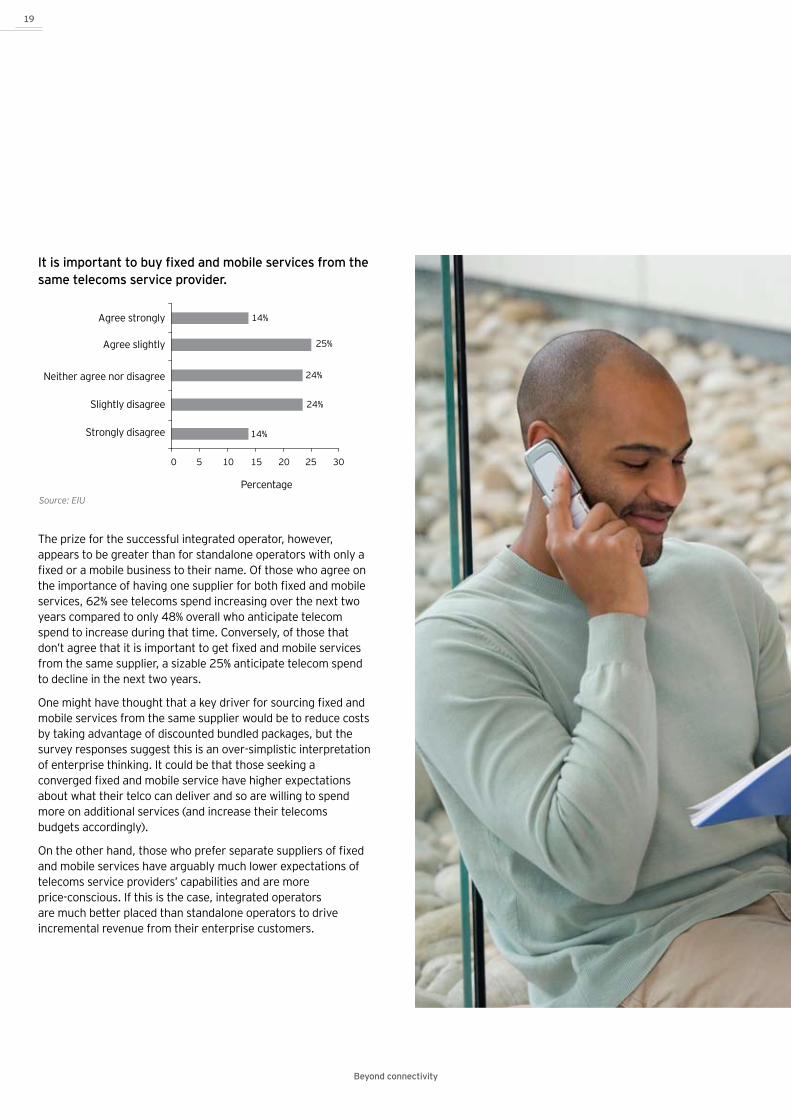

It is important to buy fixed and mobile services from the same telecoms service provider.

The prize for the successful integrated operator, however, appears to be greater than for standalone operators with only a fixed or a mobile business to their name. Of those who agree on the importance of having one supplier for both fixed and mobile services, 62% see telecoms spend increasing over the next two years compared to only 48% overall who anticipate telecom spend to increase during that time. Conversely, of those that don’t agree that it is important to get fixed and mobile services from the same supplier, a sizable 25% anticipate telecom spend to decline in the next two years.

One might have thought that a key driver for sourcing fixed and mobile services from the same supplier would be to reduce costs by taking advantage of discounted bundled packages, but the survey responses suggest this is an over-simplistic interpretation of enterprise thinking. It could be that those seeking a converged fixed and mobile service have higher expectations about what their telco can deliver and so are willing to spend more on additional services (and increase their telecoms budgets accordingly).

On the other hand, those who prefer separate suppliers of fixed and mobile services have arguably much lower expectations of telecoms service providers’ capabilities and are more price-conscious. If this is the case, integrated operators are much better placed than standalone operators to drive incremental revenue from their enterprise customers.

0 5 10 15 20 25

14%

25%

24%

24%

14%

30

Strongly disagree

Percentage

Slightly disagree

Neither agree nor disagree

Agree slightly

Agree strongly

Source: EIU

20

Beyond connectivity

Mike Russell, Group IS Director at Atkins, an engineering and design consultancy with over 200 offices around the world, argues that those with a fixed-line heritage have the advantage. He believes that customers who want a single supplier are more likely to choose a fixed-line operator that has added mobile, rather than the other way around. “Mobile service providers have yet to be convincing about their capacity to manage fixed networks,” he says. “At the same time, fixed services vendors have a well-established service provisioning capability. Conservatism might lead people to hang on to what they know.”

Show us you careEnterprises have long criticised telcos for their poor customer support, and the survey shows it remains a weakness. Customer call centers top the list of services that enterprise customers would not consider handing over to their telecoms service provider, followed by IT help desks (see bar chart, page 18). Enterprises may be thinking that if telcos can’t look after them as well as they would like, why trust them with their own customers?

“A good quality customer experience, where the provider really shows that they know about and care about the customer, is lacking across the [telecoms] sector pretty much everywhere,” adds Keith Willetts, CEO and Chairman of the TM Forum, a telecoms industry association.

Customer care problems appear to be more pronounced at smaller companies where telcos have typically not exerted much effort, perceiving higher-margin opportunities among higher-spending multinational companies (see Smaller companies: an untapped market, page 26). But even among the higher-spending accounts, customer care problems still persist.

“Our experience with our fixed communications vendor is that while they are competent and professional, they do need regular management to keep them on track and responding well,” says Russell. He also complains of long lead-in times promised by telcos to provision core services, which need to be “arm-wrestled down.” “This can take a lot of project management effort,” adds Russell.

In their pursuit of selling more advanced services, telcos would be well advised not take their eye off basic customer care issues — and not just when it comes to dealing with enterprises directly. “The major telcos have a unique problem in that many of the people making purchasing decisions for enterprise services and initiatives will have direct experience of the telco’s consumer products in their personal life, and that experience may have been variable at best,” warns Hawker.

21

Customer loyalty — looks can be deceiving Only 10% of the survey respondents say they have changed telecoms providers in the last year, with most opting to keep with the same telco for at least two years, and probably much longer than that. 20% of survey respondents say they don’t ever recall a change in their telecoms service provider. What explains customers’ apparent willingness to stay with what they know?

Given that 33% of survey respondents say there are no drawbacks to their current telecoms service (and of this group, 30% have no memory of changing their telecoms service providers) it might be tempting to conclude that telcos and enterprises are generally happy with each other. This, however, would be misleading.

One contributing factor to “customer loyalty” could be the difficulty of changing providers, but it isn’t the full explanation. For most survey respondents (60%), the difficulties that may be associated with switching providers are not seen as big stumbling blocks to making a move. Enterprises have also become much sharper in their dealings with their telecoms service providers (as Russell asserts) by inserting escape clauses into long-term contracts if they become uncompetitive.

The most likely reason why enterprises say they are happy with their provider is because they have been successful in squeezing out ever more favorable deals on a regular basis. A sign that enterprises are keeping telco providers on their toes is that over 33% of survey respondents say their companies put their telecoms contracts up for tender “on a needs basis,” while the majority of the remainder typically put their telecoms contracts up for tender every two or three years. Despite the high frequency of contract tenders, however, there appears no rush to switch providers, which suggests that many enterprises are getting what they want when contracts come up for renewal — cheaper, reliable core services — and electing to stay with them as a result.

Ovum, a telecoms research company, provides further evidence. It projects a 14.5% compound annual growth rate (CAGR) for the number of managed IP/MPLS VPN connections between 2008 and 2014. Revenue from these connections, however, is expected to grow at half that rate during the same time period. In the relationship between the telecoms service provider and the enterprise customer, enterprises appear to have the upper hand.

21

Beyond connectivity

Networks, unified communications and partnerships

Playing to strengths

4.

22

23

Beyond connectivity

Network know-howEnterprises value telcos’ network expertise. “The criteria in our RFP process are very challenging,” says Dr. Martin Elspermann, COO of ASIC, the European IT infrastructure services provider of Allianz, an international insurance and financial services company. “And experience shows that incumbent operators mostly fulfill the RFP demands.”

24

Beyond connectivity

Wim de Bruyn, COO and CIO of Standard Bank International, is equally fulsome in his praise of telcos’ network know-how. “Due to fast developments in technology, the level of expertise for telecommunications market is critical,” he says. “With this in mind, specialized telecoms providers are still the preferred route.”

In particular, most enterprises look to telecoms providers when it comes to the delivery of real-time IP-based services, such as video and audio conferencing. 66% of survey respondents say they are either currently buying or would consider buying conferencing services from their telecoms service providers. Large companies, with annual revenues in excess of US$5b, have even more enthusiasm. Sixty-six percent of this group already purchase voice and video conferencing services from their telcoms, with another 17% saying they would consider doing so. High take-up of telcos’ conferencing services by multinational companies suggests that telecoms service providers are capable of offering these services on a large scale, which would also set them apart from most resellers.

Incorporating real-time IP-based voice and video into SaaS or unified communications propositions — which IT suppliers or in-house IT departments might find difficult to implement — may be one way, that telcos (along with IT partners) can bring innovative service propositions to the attention of enterprise customers and generate incremental revenue.

VoIP is another area of opportunity. Although there are still pockets of resistance — 17% of respondents say they don’t use VoIP and have no plans to — nearly 33% of survey respondents say they will have replaced their traditional fixed-line service within two years, joining the existing 15% who have already made the change. The time for VoIP may have finally arrived and many enterprises appear to be embarking on a significant network transformation. Telcos should be well placed to help enterprises manage this transformation if they want to be seen as the IP experts.

Tougher economic conditions have also encouraged enterprises to invest more in virtual collaboration tools. It’s a trend that should favor telcos as it plays to their strengths in the delivery of real-time IP-based services.

How has the downturn affected the take-up of the following services?

Workforces are increasingly on the move, reflected in enterprises’ shifting spending priorities from fixed to mobile. Larger companies are putting more emphasis, in particular, on the mobile internet, with 61% giving a higher priority to mobile internet spending (compared with 41% of smaller companies). It’s likely that many smaller companies view the mobile internet as a luxury item, while larger companies can take advantage of economies of scale and clearer productivity benefits.

20%

0 10 20 30 40 50 60 70 80 90 100

Significantly increased

Slightly reduced

Slightly increased

Significantly reduced

The downturn hasn’t affected use

Don’t use this service

Unified communications (i.e., unifiedplatform for voice, messaging, video,

collaboration, etc.)

Video conferencing

Percentage

VoIP

5%

1%

11% 23%

25%

13% 25% 35% 19%4%4%

39% 8% 3%

38% 6% 20%

Source: EIUNote: Due to rounding, percentages do not add up to 100%

The time for VoIP may have finally arrived and many enterprises appear to be embarking on a significant network transformation.

25

Beyond connectivity

Please indicate whether you expect to give the following services higher or lower spending priority in the next two years, compared to what you currently spend.

The growing use of smartphones also means IT departments are facing much bigger network security and device management challenges, which creates other potential opportunities for telcos. As trusted providers of network security — and in partnership with device management software vendors — telcos could offer to either manage this increased complexity on enterprises’ behalf, or give enterprises the tools to do it themselves, perhaps on an SaaS basis. “I feel that in the future we can expect to see more control of the ‘outfield’ network being offered to the enterprise by the operator and by the device manufacturer to ensure devices, users and data are kept safe from harm’s way,” says a senior executive for an ebilling specialist.

Sharing the ICT proposition through partnershipsAlthough broadening the service portfolio beyond basic network connectivity appears to be the aim of many telecoms service providers, the majority of enterprise customers don’t yet appear to see their telco in a more far-reaching role. Only 25% of survey respondents feel that is important that their telecoms service provider offers a broad range of product and services.

The message from many enterprises seems to be that they want their telecoms service providers to remain specialized and focus on their historical expertise — the network. With those views in mind, telcos might be better served by partnering with IT providers that can deliver the wider range of services that enterprises require. Partnership opportunities in SaaS, unified communications and mobile device management look like particularly promising areas.

Moreover, enterprises are increasingly allocating telecoms spend as part of their overall IT budget, which implies a closer coordination between IT and telecoms procurement. Nearly 60% of survey respondents include the telecoms budget in their overall IT budget. The trend of combining budgets should provide a greater opportunity for telcos — and their partners — to sell packaged ICT services.

0 10

2%

13% 53%

20 30 40 50 60 70 80 90 100

Other privatenetworks

Other services

Virtual privatenetworks (VPNs)

Mobile internetaccess

Fixed internetaccess

Mobiletelephone

Fixed linetelephone

2%

2%1%

1%

1%

1%

0%

26% 3% 4%

4%9%

5%

12%

7% 28%

13%

14% 45% 8% 30%

47% 13% 3% 23%

41% 9% 14%

33% 37% 12% 6%

28% 52% 11% 3%

38% 39% 10%

A lot higher spendingpriority compared to now

Somewhat higher spendingpriority compared to now

The same spending priority

Somewhat lower spendingpriority compared to now

A lot lower spendingpriority compared to now

Don’t know

PercentageSource: EIU

The growing use of smartphones also means IT departments are facing much bigger network security and device management challenges, which creates other potential opportunities for telcos.

26

Survey respondents from smaller companies show more scepticism than their larger counterparts toward accepting non-core services from telcos. Smaller companies (with annual revenues below US$500m) also see less intrinsic value in non-core services than larger ones (annual revenues above US$5b). For example, more than 40% of survey respondents from larger enterprises see value in cloud computing, as opposed to less than 20% of survey respondents from smaller companies. Likewise, over 40% of survey respondents from larger companies see value in SaaS, but less than 30% of survey respondents have similar feelings among smaller enterprises.

Comparing larger companies ($5b+ annual revenue) with smaller companies (below $500m in annual revenue): To what extent do you value the following services? (Percentage of those answering 4 or 5 on a 5-point scale, where 5 is “highly valuable” and 1 is “not valuable at all.”)

One might have thought that smaller companies would have seen more readily the cost and productivity benefits from SaaS and cloud computing. Perhaps a reason why many do not is because neither telcos nor software companies have managed to adequately sell the benefits, or have failed to make them attractive to companies with smaller budgets.

Telcos have an advantage, however, in that they already have a billing relationship with many smaller companies for basic connectivity services, and there may be an opportunity to sell additional and generic services, courtesy of SaaS and cloud computing, as long as these services scale easily. These additional services could also be used to promote telcos’ core service proposition to smaller companies by bundling, say, a CRM SaaS product with broadband access. Mutually beneficial partnerships with IT vendors could be one way to achieve this. By partnering with telcos, for example, SaaS vendors would get a ready-made sales channel to many more (smaller) businesses that otherwise would be too expensive to reach directly; telcos would get the opportunity to broaden their service portfolio and increase revenue.

Of course, this all sounds much easier than it is in practice. Executing on service delivery, where “cloud” services are synchronised with on-premise equipment, remains a significant challenge — both at smaller and large companies.

Smaller companies — an untapped market

26

0 10 20 30 40 50 60 70 80

SaaSCloud computingNetwork security

Data backup and retrievalDomain and web hosting

Data centers (managed hosting)

Governance and complianceBusiness consulting

Conferencing (web, video, audio)Network installation and maintenance

IT help deskCustomer call centers

Larger firmsSmaller firms

65%

41%

28%

18%

70%

37%

26%37%

52%

37%

20%

76%

57%57%

56%

42%

43%

76%53%

44%

64%

58%45%

32%

PercentageSource: EIU

Beyond connectivity

Telcos have an advantage, in that they already have a billing relationship with many smaller companies for basic connectivity services.

27

Beyond connectivity

The overwhelming good news for telcos is that enterprises highly value their network expertise. This makes it hard to imagine that telecoms service providers will be relegated by large swathes of enterprise customers to a sub-contractor network role (despite their threats to do so), especially if those customers require stringent SLAs on network performance.

28

Beyond connectivity

ConclusionThe depth of telcos’ expertise on WAN optimization, managed IP/MPLS VPN services and application performance management also means telcos are in a strong position to fend off incursions by non-traditional telecoms service providers into their core territory. They also have a solid basis from which to make a successful push on core-adjacent and non-core services.

Yet telcos looking to make company strides beyond their core service propositions are going to find it difficult. Enterprise customers are highly sceptical that telecoms companies can deliver a wide range of services beyond the dumb pipe, but it doesn’t mean the sceptics can’t be won over. Telcos can make progress by integrating their non-core services more clearly into their product offering and by addressing the individual requirements of their business customers.

Network know-how is the telco’s trump card, but they must play it wisely. That means partnering with established IT vendors, which should enable them to move more swiftly and more effectively into newer service areas, such as SaaS and cloud computing. Partnerships could also bolster telcos’ presence in other service areas, such as unified communications. Telcos can’t do everything, as the survey respondents make clear, but they can leverage their network strengths to better advantage. Enterprises have sent out a clear warning to telcos that they must not repeat past mistakes of trying to be all things to all people.

Given that 72% of survey respondents say that telecoms spend over the last two years has either remained roughly equivalent or increased in relation to IT spend, it is not unreasonable to conclude that most enterprises recognize that maintaining a high-performance network, allied with software infrastructure investment, is vital to increasing business productivity. This recognition should give telcos a head start in gaining a stronger foothold in the market for non-core and more IT-centric services. Even so, telcos can’t afford to be complacent.

30

Beyond connectivity

Global Telecommunications Center contacts

Vincent de La BachelerieGlobal Telecommunications Leadertel: +33 1 4693 6205

email: [email protected]

Marc ChayaGlobal Telecommunications Markets Leader

tel: +33 1 4693 8515email: [email protected]

Jonathan DharmapalanGlobal Telecommunications Centertel: +1 415 994 6947email: [email protected]

Holger ForstGlobal Telecommunications Center — Colognetel: +49 221 2779 20171

email: [email protected]

Steve LoGlobal Telecommunications Center — Beijing

tel: +86 10 5815 2837 email: [email protected]

Prashant SinghalGlobal Telecommunications Center — Delhi

tel: +91 124 464 4000 email: [email protected]

Julia LamberthGlobal Telecommunications Center — Johannesburgtel: +27 11 772 3385email: [email protected]

Serge ThiemeleGlobal Telecommunications Center — Johannesburgtel: +225 2030 6050

email: [email protected]

Wasim KhanGlobal Telecommunications Center — Riyadh

tel: +9662 667 1040email: [email protected]

Mike StoltzGlobal Telecommunications Center — San Antonio

tel: +1 210 242 7205email: [email protected]

Ernst & Young

Assurance | Tax | Transactions | Advisory

About Ernst & YoungErnst & Young is a global leader in assurance, tax, transaction and advisory services. Worldwide, our 144,000 people are united by our shared values and an unwavering commitment to quality. We make a difference by helping our people, our clients and our wider communities achieve their potential.

Ernst & Young refers to the global organization of member firms of Ernst & Young Global Limited, each of which is a separate legal entity. Ernst & Young Global Limited, a UK company limited by guarantee, does not provide services to clients. For more information about our organization, please visit www.ey.com.

© 2010 EYGM Limited. All Rights Reserved.

EYG no. EF0081

This publication contains information in summary form and is therefore intended for general guidance only. It is not intended to be a substitute for detailed research or the exercise of professional judgment. Neither EYGM Limited nor any other member of the global Ernst & Young organization can accept any responsibility for loss occasioned to any person acting or refraining from action as a result of any material in this publication. On any specific matter, reference should be made to the appropriate advisor.

Related Documents