Beyond Borders Global biotechnology report 2008 Vancouver, Canada 29 October 2008

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Beyond BordersGlobal biotechnology report 2008Vancouver, Canada

29 October 2008

Headlines: the big picture

Beyond Borders3

Strong growth in 2007

Record dealsBooming financings Improved profitability

All-time high, led by mega-mergers

VC sets new record of US$7.4 billion

US publicly traded industry’s net loss reaches record low

Beyond Borders4

Emerging challenges

Safety concernsRegulatory challenges

emergePublic equity markets

cool late in year

Several new black box warnings

Lowest FDA NME approvals in 25 years

CMS, NICE decisions

Credit crunch drives flight to safety

Beyond Borders5

A challenging landscape in 2008

Credit crisis, global recession fears drive risk-averse public investors

Companies focus on efficiency, survival

VC, alliances, M&A remain strong

Market cap decline,

IPO drought, debt offerings down

Restructuring, bankruptcies up

Activity on par with recent years

Beyond Borders6

Reinventing drug development

Pharma’s patent productivity challenges drive change

Short-term: cost cutting, stock buybacks, late-stage acquisitions

Long-term: platform deals, restructuring R&D (smaller teams, networked, more autonomous)

Americas overview: the road lengthens

Beyond Borders8

US financial performance

0

2

4

6

2006 2007

Net loss (US$b) -95%

0

10

20

30

2006 2007

R&D expense (US$b) +6%

010203040506070

2006 2007

Revenues (US$b) +11%

0

50

100

150

2006 2007

Employees (000) +3%

Beyond Borders9

Behind the numbers: acquisitions and black box warnings

19%

11%

14%

0%

5%

10%

15%

20%

2006 2007 2007 adjusted

Gro

wth

rat

e

Acquisitions and black box warnings dented revenue growth in 2007

Source: Ernst & Young

Beyond Borders10

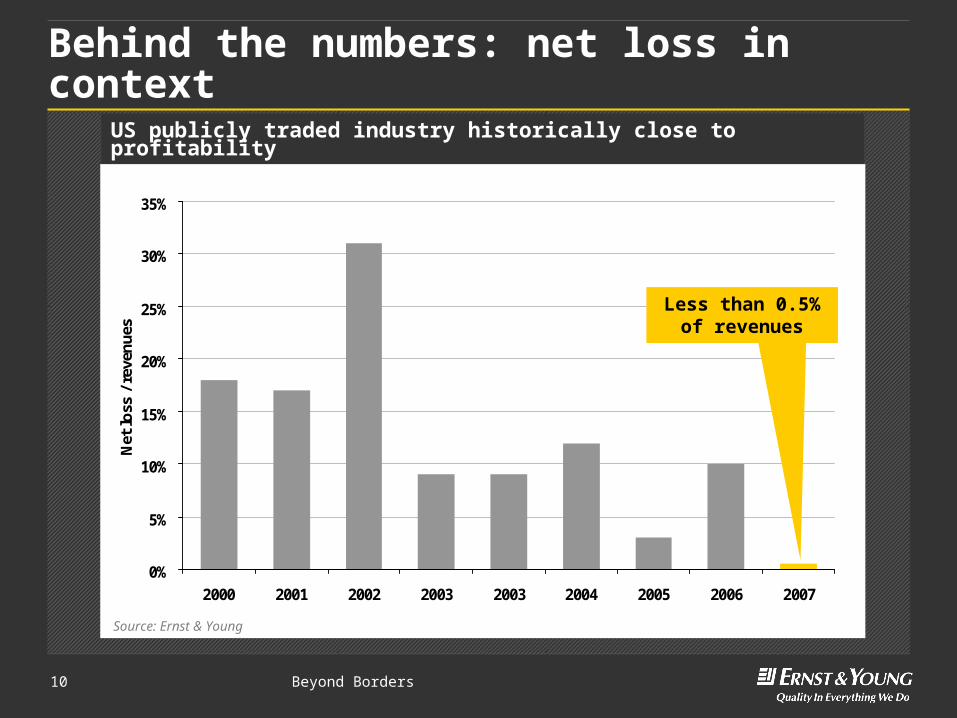

Behind the numbers: net loss in context

0%

5%

10%

15%

20%

25%

30%

35%

2000 2001 2002 2003 2003 2004 2005 2006 2007

Net

lo

ss /

rev

enu

es

US publicly traded industry historically close to profitability

Source: Ernst & Young

Less than 0.5% of revenues

Beyond Borders11

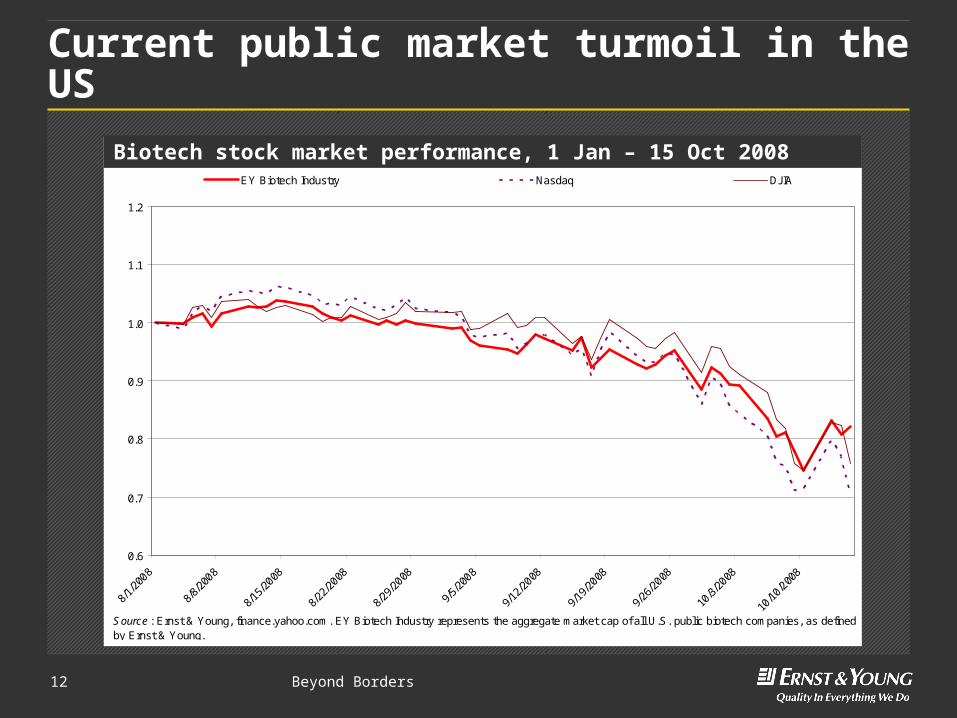

Current public market turmoil in the US

Biotech stock market performance, 2007

0.6

0.7

0.8

0.9

1.0

1.1

1.2

1/3/

2007

1/17

/200

7

1/31

/200

7

2/14

/200

7

2/28

/200

7

3/14

/200

7

3/28

/200

7

4/11

/200

7

4/25

/200

7

5/9/

2007

5/23

/200

7

6/6/

2007

6/20

/200

7

7/4/

2007

7/18

/200

7

8/1/

2007

8/15

/200

7

8/29

/200

7

9/12

/200

7

9/26

/200

7

10/1

0/20

07

10/2

4/20

07

11/7

/200

7

11/2

1/20

07

12/5

/200

7

12/1

9/20

07

EY Biotech Industry Nasdaq DJIA

Source : Ernst & Young, finance.yahoo.com. EY Biotech Industry represents the aggregate market cap of all U.S. public biotech companies, as defined by Ernst & Young.

Beyond Borders12

Current public market turmoil in the US

Biotech stock market performance, 1 Jan – 15 Oct 2008

0.6

0.7

0.8

0.9

1.0

1.1

1.2

8/1/

2008

8/8/

2008

8/15

/2008

8/22

/2008

8/29

/2008

9/5/

2008

9/12

/2008

9/19

/2008

9/26

/2008

10/3/

2008

10/10

/200

8

EY Biotech Industry Nasdaq DJIA

Source : Ernst & Young, finance.yahoo.com. EY Biotech Industry represents the aggregate market cap of all U.S. public biotech companies, as defined by Ernst & Young.

Beyond Borders13

US financing

0

5

10

15

20

25

30

35

1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008H1

US

$b

Venture IPO Follow-on Other

US financing reaches second-highest total on record

Source: Ernst & Young, BioCentury, BioWorld and VentureOne

Beyond Borders14

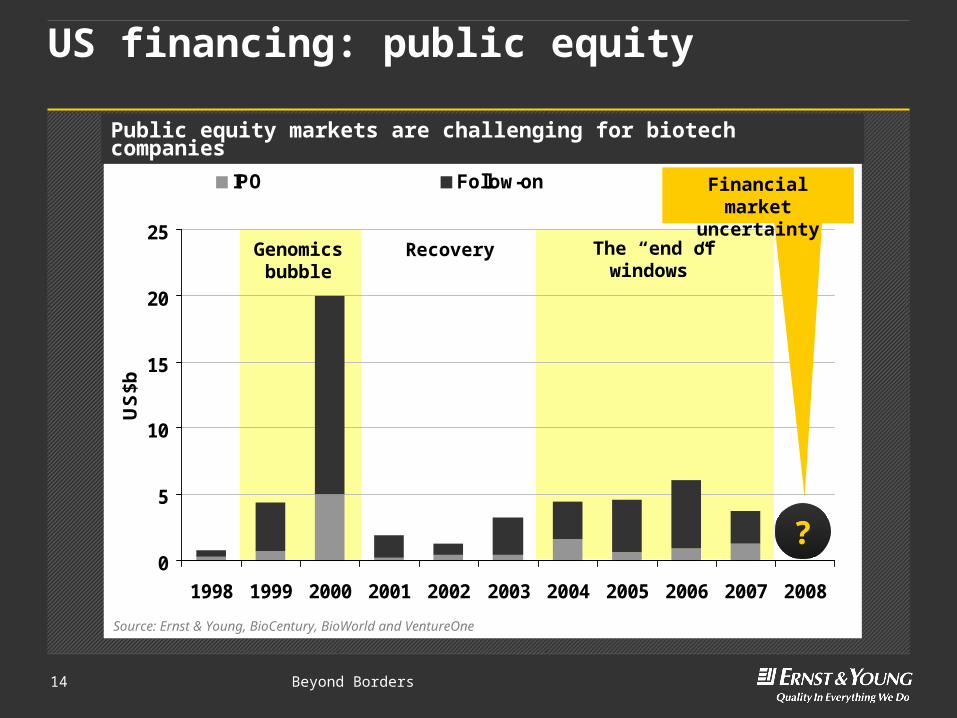

US financing: public equity

0

5

10

15

20

25

1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008

US

$b

IPO Follow-on

Public equity markets are challenging for biotech companies

Source: Ernst & Young, BioCentury, BioWorld and VentureOne

?

Genomics bubble

Recovery The “end of windows”

Financial market uncertainty

Beyond Borders15

US financing: regional distribution

Capital raised by leading US regions in 2007

Beyond Borders16

US deals: mergers and acquisitions

0

5

10

15

20

25

30

35

1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 H1

US

$b

Pharma-biotech mega deals Pharma-biotech Biotech-biotech Biotech-biotech mega deals

Source: Ernst & Young, BioWorld, Recombinant Capital and Windhover

Beyond Borders17

US deals: mergers and acquisitions adjusted for mega deals

0

5

10

15

20

25

30

35

1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 H1

US

$b

Pharma-biotech Biotech-biotech

Source: Ernst & Young, BioWorld, Recombinant Capital and Windhover

Beyond Borders18

US deals: alliances

0

5

10

15

20

25

30

1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 H1

US

$b

Pharma-biotech Biotech-biotech

Source: Ernst & Young, BioWorld, Recombinant Capital and Windhover

Beyond Borders19

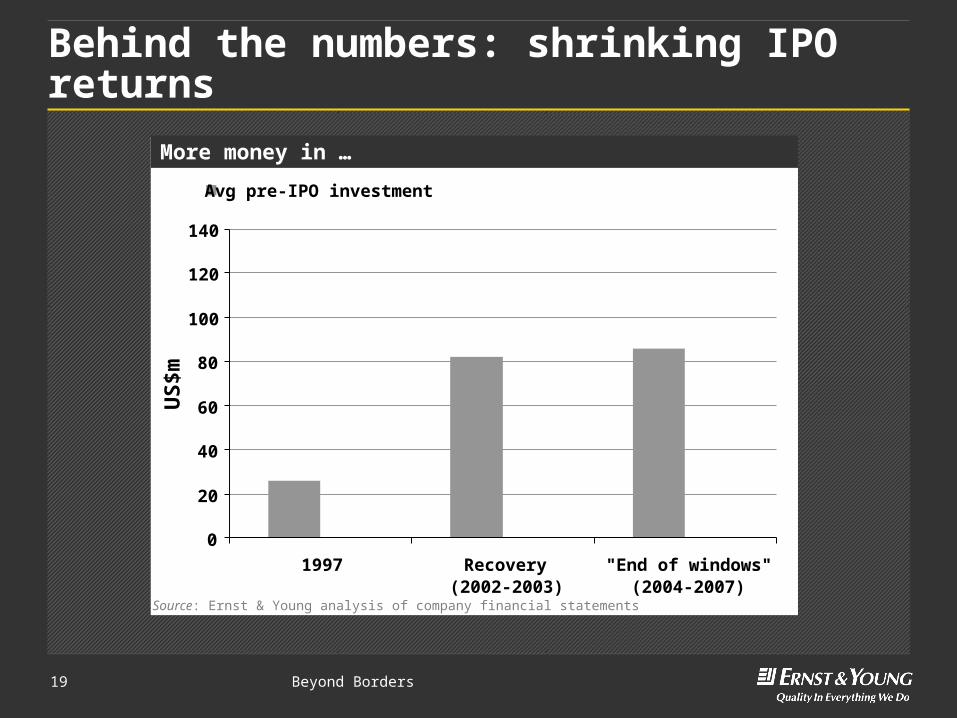

Behind the numbers: shrinking IPO returns

More money in …

Source: Ernst & Young analysis of company financial statements

0

20

40

60

80

100

120

140

1997 Recovery(2002-2003)

"End of windows"(2004-2007)

US

$mAvg pre-IPO investment

Beyond Borders20

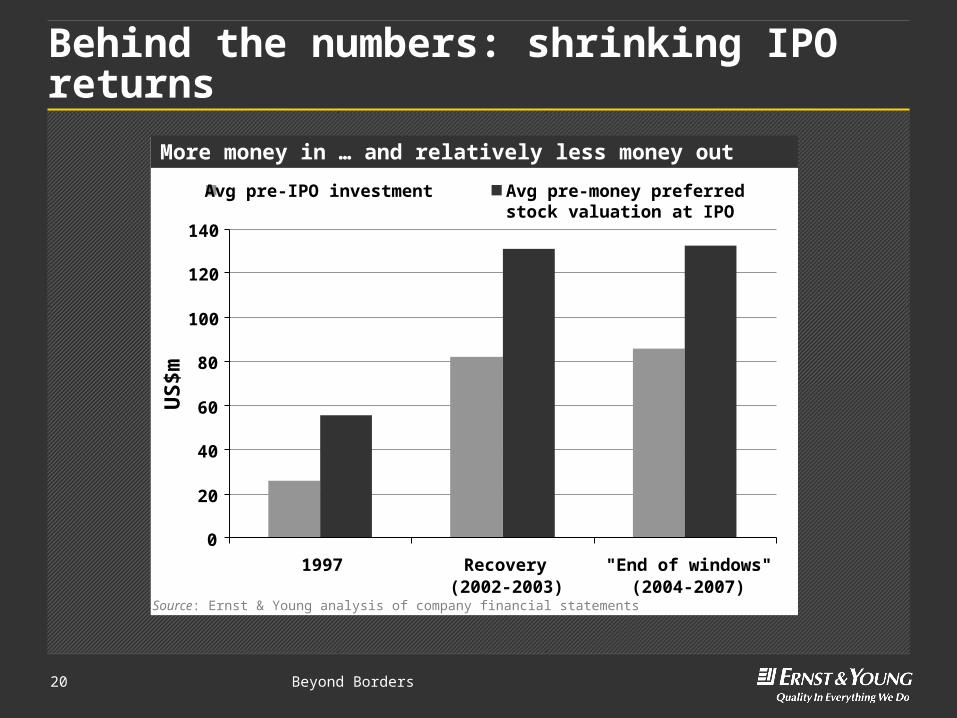

Behind the numbers: shrinking IPO returns

More money in … and relatively less money out

Source: Ernst & Young analysis of company financial statements

0

20

40

60

80

100

120

140

1997 Recovery(2002-2003)

"End of windows"(2004-2007)

US

$mAvg pre-IPO investment Avg pre-money preferred stock

valuation at IPO

Beyond Borders21

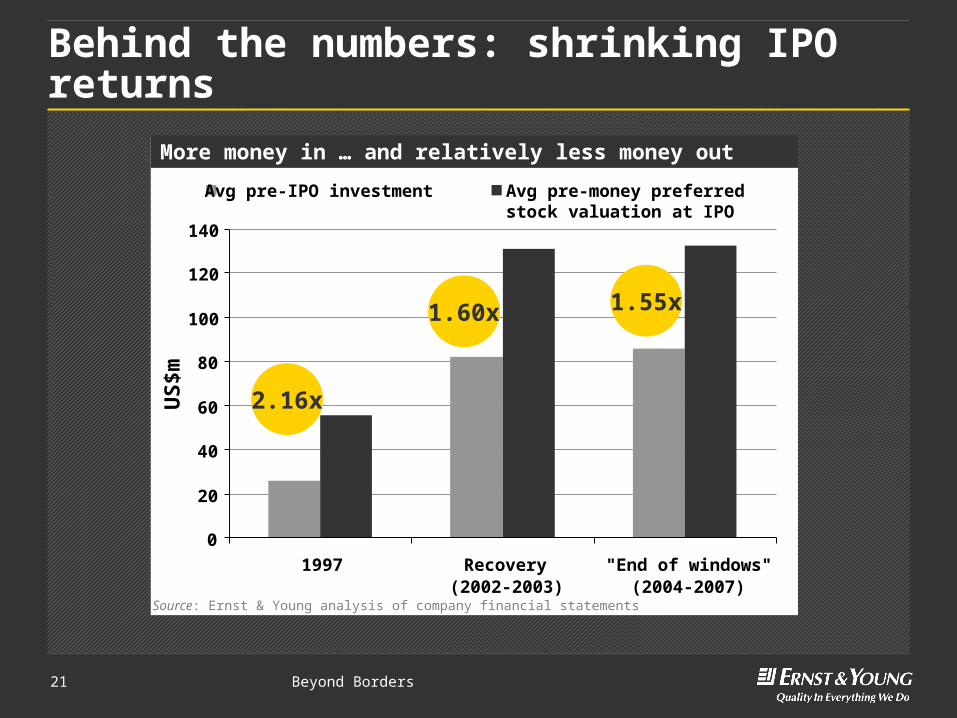

Behind the numbers: shrinking IPO returns

More money in … and relatively less money out

Source: Ernst & Young analysis of company financial statements

0

20

40

60

80

100

120

140

1997 Recovery(2002-2003)

"End of windows"(2004-2007)

US

$mAvg pre-IPO investment Avg pre-money preferred stock

valuation at IPO

2.16x

1.60x 1.55x

Beyond Borders22

Behind the numbers: the valuation gap

Company Acquirer Value (US$ million)

Agensys Astellas 537

Adnexus BMS 505

Rinat Pfizer 478

Domantis GSK 454

Illypsa Amgen 420

Glycofi Merck 400

Avidia Amgen 380

Illumigen Cubist 341

Alantos Amgen 300

Average value of “IPO-ready” company acquisitions: $425 millionAverage pre-money IPO valuation: $150-160 million

Selected acquisitions of private “IPO ready” companies, 2006-2007

Source: Ernst & Young

Beyond Borders23

US financing: creative financingsSymphony Capital

NewCo

►Inlicenses IP►Funds clinical development IP

Funding clinical

development

Symphony Capital

$$

Portfolio Company

►Retains right to acquire IP

►Conducts clinical developmt

License to IP

$

IP

Future option to re-acquire IP at pre-negotiated premium

Shares / warrants

RRD International

Clinical development assistance (optional)

Source: Ernst & Young

Beyond Borders24

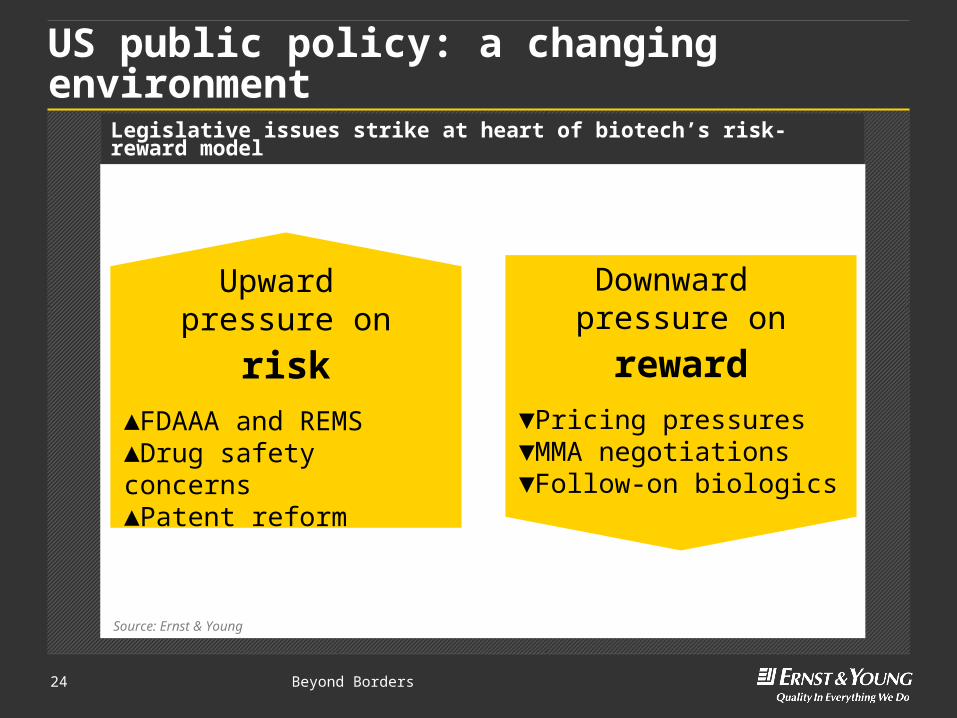

US public policy: a changing environment

Legislative issues strike at heart of biotech’s risk-reward model

Upward pressure on

risk▲FDAAA and REMS ▲Drug safety concerns▲Patent reform

Downward pressure on

reward▼Pricing pressures ▼MMA negotiations▼Follow-on biologics

Source: Ernst & Young

Beyond Borders25

Canadian overview: sustainability?

Beyond Borders26

Canadian financial performance – Public Companies

Revenues (US$ B)

0.5

1.01.52.02.5

2006 2007

R&D Expense (US$ B)

0.2.4.6.8

1.0

2006 2007

+12%+1%

Employees (000)

2.5

5.0

7.5

10.0

2006 2007

+ 2% Net Loss (US$ B)

.2

.4

.6

.8

2006 2007

+ 21%

Beyond Borders27

Canadian financing

0.0

0.2

0.4

0.6

0.8

1.0

1.2

1.4

1.6

1.8

2.0

2000 2001 2002 2003 2004 2005 2006 2007

US

$b

Venture IPOs Follow-on Other

Source: Ernst & Young, BioCentury, BioWorld and VentureOne

Beyond Borders28

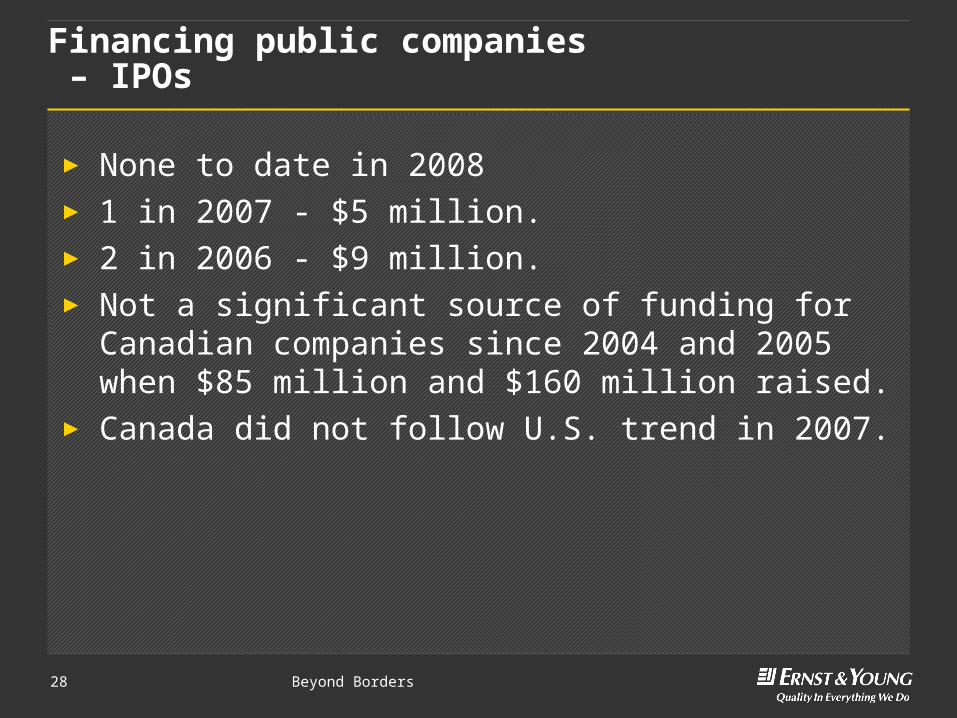

Financing public companies – IPOs

► None to date in 2008► 1 in 2007 - $5 million.► 2 in 2006 - $9 million.► Not a significant source of funding for Canadian

companies since 2004 and 2005 when $85 million and $160 million raised.

► Canada did not follow U.S. trend in 2007.

Beyond Borders29

Canadian financing by province

0

50

100

150

200

250

300

350

400

Quebec British Columbia Ontario Alberta Other

Public companies Private companies

Canadian census 2007

Source: Ernst & Young

Beyond Borders30

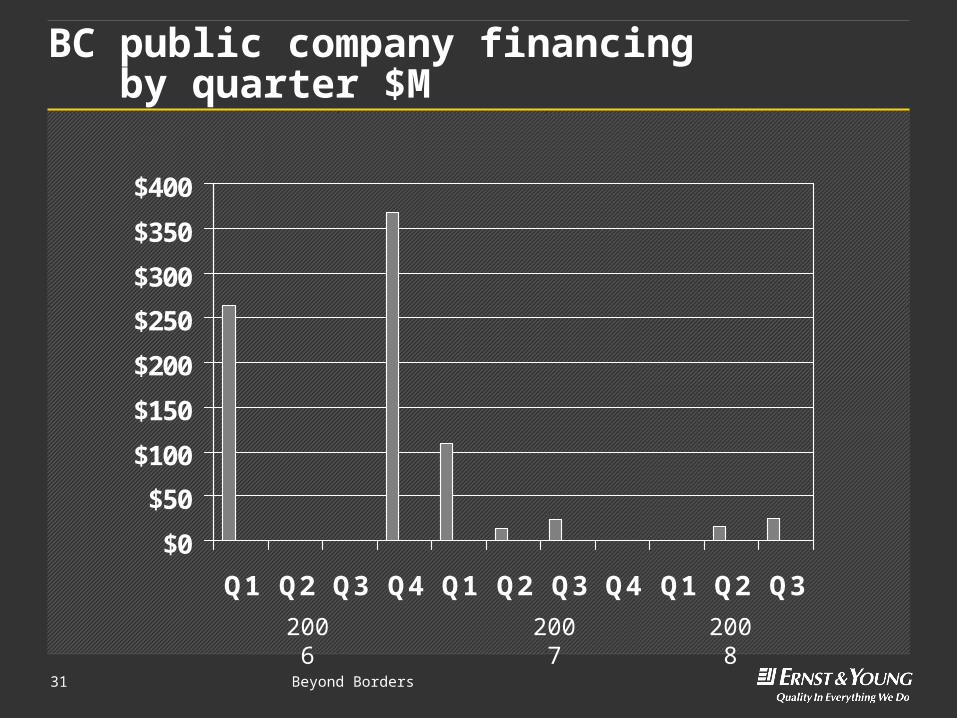

Canadian public company financing by quarter $M

2006 2007 2008

493

248

87

770

352

190

87 7921 27 39

0

100

200

300

400

500

600

700

800

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3

Beyond Borders31

BC public company financing by quarter $M

$0

$50

$100

$150

$200

$250

$300

$350

$400

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3

2006 2007 2008

Beyond Borders32

VC funding – Canada $M

2006 2007 2008

$57

$81

$19

$61

$174

$33

$96

$50

$20

$46

$125

$0$20$40$60$80

$100$120$140$160$180$200

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3

Beyond Borders33

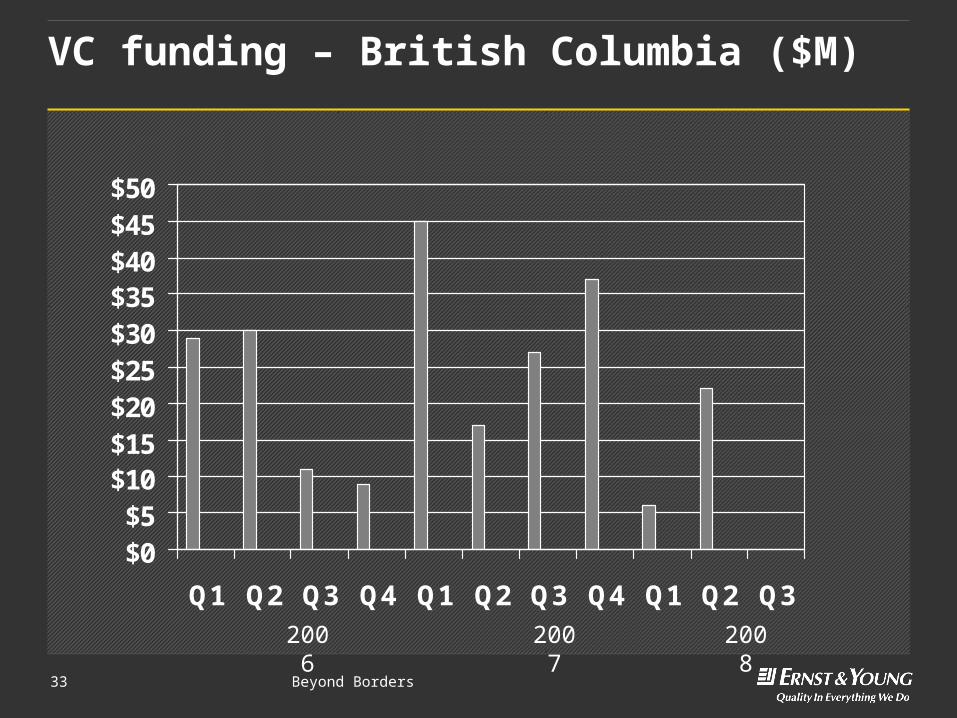

VC funding – British Columbia ($M)

$0$5

$10$15$20$25$30$35$40$45$50

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3

2006 2007 2008

Beyond Borders34

Number of VC financings and average value

$7.50

$11.40

$2.50

$4.90$6.10

$0.00

$2.00

$4.00

$6.00

$8.00

$10.00

$12.00

2004 2005 2006 2007 2008 TODATE

110

55 42

47

Avg. $USM

17

Beyond Borders35

Canadian financial performance

Market Capitalization (US$ B)

17.442

12.909

8.867

13.837 13.68513.219 12.934

10.844

8.500

8

9

10

11

12

13

14

15

16

17

2000 2001 2002 2003 2004 2005 2006 2007 2008MidYear

Beyond Borders36

Ernst & Young’s survival index for Canadian public companies – 2007

30%

23%

8%

40%

Less than 1 year of cash

Between 1 and 2 years ofcashBetween 2 and 3 years ofcashMore than 4 years of cash

Beyond Borders37

Canadian private biotech companies

0

50

100

150

200

250

300

350

400

2006 2007

Total

Ontario

Québec

BC

Beyond Borders38

Number of companies

0

20

40

60

80

100

120

140

Nu

mb

er o

f co

mp

anie

s

Public companies Private companies

Canadian census 2007

Source: Ernst & Young

Beyond Borders39

Canadian financing by leading clusters

Capital raised by leading Canadian biotech clusters in 2007

Beyond Borders40

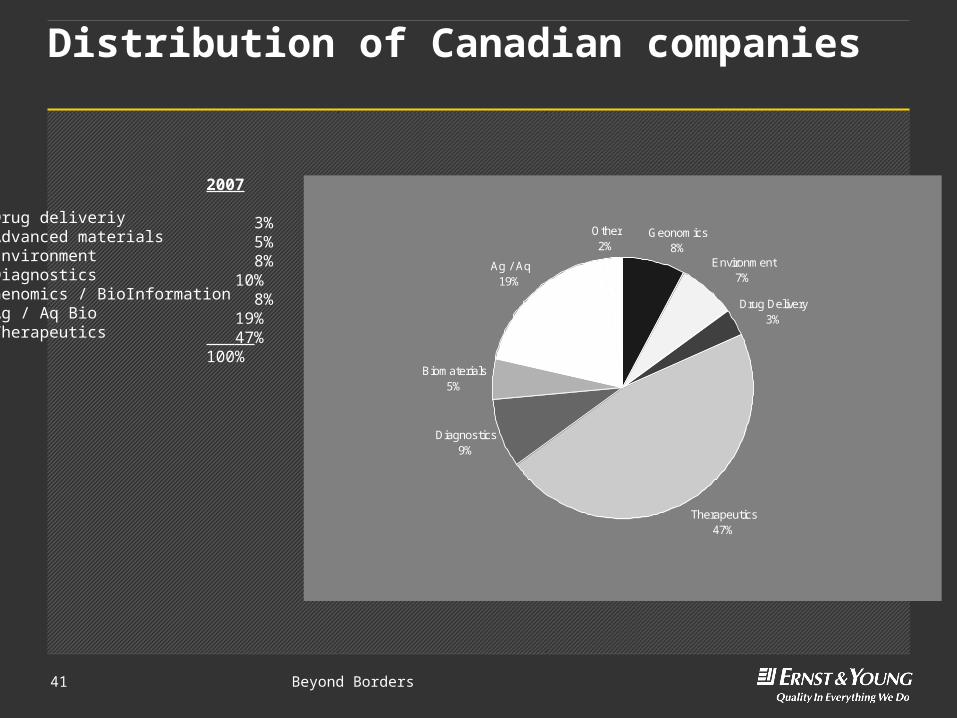

Distribution of Canadian companies

Geonomics8%

Environment7%

Drug Delivery3%

Therapeutics47%

Diagnostics9%

Biomaterials5%

Ag / Aq19%

Other2%

Drug deliveriyAdvanced materialsEnvironmentDiagnosticsGenomics / BioInformationAg / Aq BioTherapeutics

2004

3% 4% 6% 6% 9% 15% 57%100%

Beyond Borders41

Distribution of Canadian companies

Geonomics8%

Environment7%

Drug Delivery3%

Therapeutics47%

Diagnostics9%

Biomaterials5%

Ag / Aq19%

Other2%

Drug deliveriyAdvanced materialsEnvironmentDiagnosticsGenomics / BioInformationAg / Aq BioTherapeutics

2007

3% 5% 8% 10% 8% 19% 47%100%

Beyond Borders42

Major Canadian Transactions in 2008

► Axcan Pharma acquired by TPG Capital - $1.3 billion

► Aspreva Pharmaceutical acquired by Galencia Group - US$900 million.

► Draxis Health Inc. acquired by Jubilant Organosys - $255M

► Arius Research Inc. acquired by Roche - $191 million

Beyond Borders43

BC Transactions in 2008

► Tekmira Pharmaceuticals Corporation and Protiva Biotherapeutics Inc. (share deal worth approx. $32M per Tekmira Q2 FS)

► OncoGenex Technologies Inc. reverse takeover of Sonus Pharmaceuticals, Inc. (share exchange deal worth about US$11M per Sonus proxy)

► Medigen Biotechnology Corporation planned reverse takeover of Pacgen Biopharmaceuticals Corporation (per Pacgen October 24 press release)

► Angiotech?

Beyond Borders44

European overview: growing strengths

Beyond Borders45

European financial performance

0.00.20.40.60.81.01.21.4

2006 2007

Net loss (€ b) 108%

0

1

2

3

4

2006 2007

R&D expense (€ b) +7%

0

2

4

6

8

10

12

2006 2007

Revenues (€b) -6%

0

20

40

60

2006 2007

Employees (000) +6%

Beyond Borders46

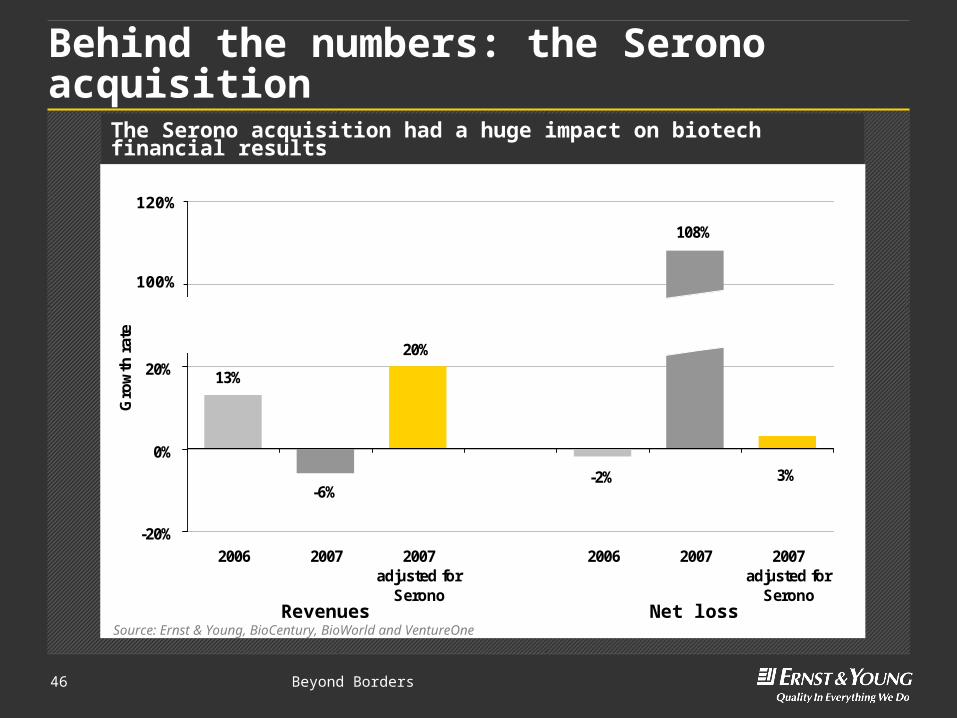

Behind the numbers: the Serono acquisition

3%

108%

-2%

20%

-6%

13%

-20%

0%

20%

40%

60%

2006 2007 2007adjusted for

Serono

2006 2007 2007adjusted for

Serono

Gro

wth

rat

e

The Serono acquisition had a huge impact on biotech financial results

Source: Ernst & Young, BioCentury, BioWorld and VentureOneRevenues Net loss

100%

120%

Beyond Borders47

European financing: IPOs

0

100

200

300

400

500

600

700

800

900

2001 2002 2003 2004 2005 2006 2007 2008 H1

€m

Source: Ernst & Young, BioCentury, BioWorld, VentureOne and company news (through NewsAnalyzer)

Beyond Borders48

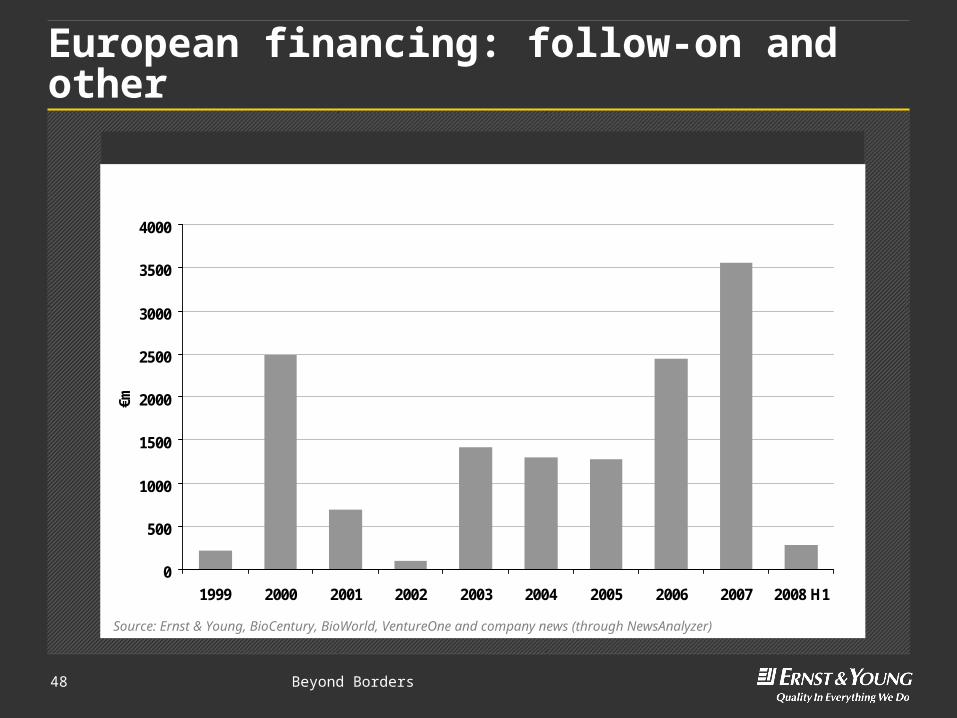

European financing: follow-on and other

0

500

1000

1500

2000

2500

3000

3500

4000

1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 H1

€m

Source: Ernst & Young, BioCentury, BioWorld, VentureOne and company news (through NewsAnalyzer)

Beyond Borders49

European financing: regional distribution

Capital raised by major European countries in 2007

Beyond Borders50

European deals: mergers and acquisitions

0

2

4

6

8

10

12

14

16

2005 2006 2007 2008 H1

€b

Biotech-biotech Pharma-biotech Pharma-biotech mega deals

Source: Ernst & Young, Windhover, BioWorld, Recombinant Capital and company news (through Newsanalyzer)

Beyond Borders51

European deals: alliances

0

2

4

6

8

10

12

2005 2006 2007 2008 H1

€b

Biotech-biotech Pharma-biotech

Source: Ernst & Young, Windhover, BioWorld, Recombinant Capital and company news (through Newsanalyzer)

Beyond Borders52

European pipeline by phase

0

100

200

300

400

500

600

700

800

Preclinical Phase I Phase II Phase IIINu

mb

er o

f p

rod

uct

can

did

ates

in s

tud

ies

2006 2007

European pipeline shows strong growth, particularly in Phase II

Source: Ernst & Young and company websites

Outlook: the year ahead

Beyond Borders54

Rules of the road

Look for Rules of the road

Deals ► Increasing urgency around big pharma pipeline issues

► Stiff competition for biotech assets► High valuations, more negotiating

power for biotechs

“Bargaining power matters”► Dual-tracking preserves options

for private companies ► Creative deal structures can retain

flexibility, capture greater share of value

Financing ► Sustained strength in venture investments

► Challenging public equity markets► New, creative financing options► Restructuring

“Stay lean, mean and focused”► Capital efficiency for leaner times► Alternative sources of capital

Products & regulatory

► Increased safety scrutiny, including post-marketing

► Higher bar from payors, pay-for-performance

► Continued focus on sales/mktg.

“Show me the value”► Articulate value props early in

R&D► New reimbursement / pricing

approaches

Source: Ernst & Young

Long-term outlook:reinnovation and reinvention

Beyond Borders56

Is a pattern emerging?

Big pharma companies announce layoffs, restructuringsStock buybacksSafety concerns take bite out of product sales

Velcade gives NICE an unprecedented money-back guarantee

FDA NME approvals fall to lowest level in

over 25 years more pricing

pressuresemerging

Product safety incidents in the

rising China market

Big pharma’s search for pipeline productivity propels a booming deal environment

Biotech companies retain more

rights in deals

The mega deal… is back

π?

8%

Government negotiation of drug prices under MMA returns to public policy debate

FIPNETs

Creative deal structures

►

►

►

►

►►M&A R

EMS

FDAAA ►

$►

€►

¥ ►

£

R&D

►

??? ? ?►re-in

Beyond Borders57

Reinvention

Big pharma companies announce layoffs, restructuringsStock buybacksSafety concerns take bite out of product sales

Velcade gives NICE an unprecedented money-back guarantee

FDA NME approvals fall to lowest level in

over 25 years more pricing

pressuresemerging

Product safety incidents in the

rising China market

Big pharma’s search for pipeline productivity propels a booming deal environment

Biotech companies retain more

rights in deals

The mega deal… is back

π?

8%

Government negotiation of drug prices under MMA returns to public policy debate

FIPNETs

Creative deal structures

►

►

►

►

►►M&A R

EMS

FDAAA ►

$►

€►

¥ ►

£

R&D

►

??? ? ?►

The drug industry is being reinvented by three sweeping trends:

►R&D productivity►Personalized medicine

►Globalization

re-inre-in

Beyond Borders58

These drivers will fundamentally change the business of drug development

► Approaches to research and development► Business models► The value chain► Deal structures► Balance of power between biotech and big pharma► Partnerships between western companies and

companies in emerging markets

Big pharma companies announce layoffs, restructuringsStock buybacksSafety concerns take bite out of product sales

Velcade gives NICE an unprecedented money-back guarantee

FDA NME approvals fall to lowest level in

over 25 years more pricing

pressuresemerging

Product safety incidents in the

rising China market

Big pharma’s search for pipeline productivity propels a booming deal environment

Biotech companies retain more

rights in deals

The mega deal…is back

π?

8%

Government negotiation of drug prices under MMA returns to public policy debate

FIPNETs

Creative deal structures

►

►

►

►

►►M&A R

EMS

FDAAA ►

$►

€►

¥►

£

R&D

►

??? ? ?►

Big pharma companies announce layoffs, restructuringsStock buybacksSafety concerns take bite out of product sales

Velcade gives NICE an unprecedented money-back guarantee

FDA NME approvals fall to lowest level in

over 25 years more pricing

pressuresemerging

Product safety incidents in the

rising China market

Product safety incidents in the

rising China market

Big pharma’s search for pipeline productivity propels a booming deal environment

Biotech companies retain more

rights in deals

The mega deal…is back

π?

8%

Government negotiation of drug prices under MMA returns to public policy debate

Government negotiation of drug prices under MMA returns to public policy debate

FIPNETs

Creative deal structures

►

►

►

►

►►M&A R

EMS

FDAAA ►

$►

€►

¥►

£

R&D

►

??? ? ???? ? ?

►

The first driver of reinvention:R&D productivity

Beyond Borders60

The problem: patent expirations

0

5

10

15

20

25

2007 2008 2009 2010 2011 2012

US

$b

Projected sales losses from patent expirations to reach US$67b by 2012

Source: Sanford C. Bernstein & Co.

Beyond Borders61

Big companies need sustainable solutions

Buying pipeline assets

►High prices lower upside potential

►Limited reserves of cash

Cutting costs

►Short-term gains

Boosting EPS►Short-term gains►Limited reserves of cash

Companies need

sustainable solutions to fix the real problem:low R&D

productivity

Source: Ernst & Young

Beyond Borders62

The inertia of size

Small companies Conduct and performance Large companies Conduct and performance

Stru

cture

► Small ► Individuals have more control over outcomes

► Large ► Poor sense of ownership

► Flexible ► Encourages creativity and collegiality

► Rigid ► Centralized, bureaucratic processes

► Risk-aversion over time

► Cash-starved ► Driven to raise capital► Lean operations,

sometimes cut corners

► Strong cash flow ► Not as “hungry” or driven to succeed

Incen

tives

► Stock-based compensation is a strong incentive

► Direct financial tie to performance

► Stock-based compensation is not meaningful

► Less tied to outcomes► Less passion

► Private investors with longer horizons

► Less focused on short-term financial performance

► Public investors demanding quarterly results

► More sensitive to short-term impact of long-term decisions

Structure and incentives drive conduct and performance

Source: Ernst & Young

Beyond Borders63

Emulating biotech

Creating small, autonomous R&D units

Emulate

Large monolithic big pharma company

Preserving entities after acquisitions

Adopting networked structures

Pay-for-performance tied to small-team milestones

culture

of

small

biotech

companiesSource: Ernst & Young

Big pharma companies announce layoffs, restructuringsStock buybacksSafety concerns take bite out of product sales

Velcade gives NICE an unprecedented money-back guarantee

FDA NME approvals fall to lowest level in

over 25 years more pricing

pressuresemerging

Product safety incidents in the

rising China market

Big pharma’s search for pipeline productivity propels a booming deal environment

Biotech companies retain more

rights in deals

The mega deal…is back

π?

8%

Government negotiation of drug prices under MMA returns to public policy debate

FIPNETs

Creative deal structures

►

►

►

►

►►M&A R

EMS

FDAAA ►

$►

€►

¥►

£

R&D

►

??? ? ?►

Big pharma companies announce layoffs, restructuringsStock buybacksSafety concerns take bite out of product sales

Velcade gives NICE an unprecedented money-back guarantee

FDA NME approvals fall to lowest level in

over 25 years more pricing

pressuresemerging

Product safety incidents in the

rising China market

Product safety incidents in the

rising China market

Big pharma’s search for pipeline productivity propels a booming deal environment

Biotech companies retain more

rights in deals

The mega deal…is back

π?

8%

Government negotiation of drug prices under MMA returns to public policy debate

Government negotiation of drug prices under MMA returns to public policy debate

FIPNETs

Creative deal structures

►

►

►

►

►►M&A R

EMS

FDAAA ►

$►

€►

¥►

£

R&D

►

??? ? ???? ? ?

►

The second driver of reinvention:Personalized medicine

Beyond Borders65

Personalized medicine: why now?

Safety concerns

►Targeted approaches►Less misdiagnosis,

fewer adverse events

Pricing pressures

►Smaller clinical trials►Cheaper drug development

R&D productivity

►More efficient identification and development of drug targets

Move from efficacy to efficiency

in drug development

and healthcare

delivery

Source: Ernst & Young

Beyond Borders66

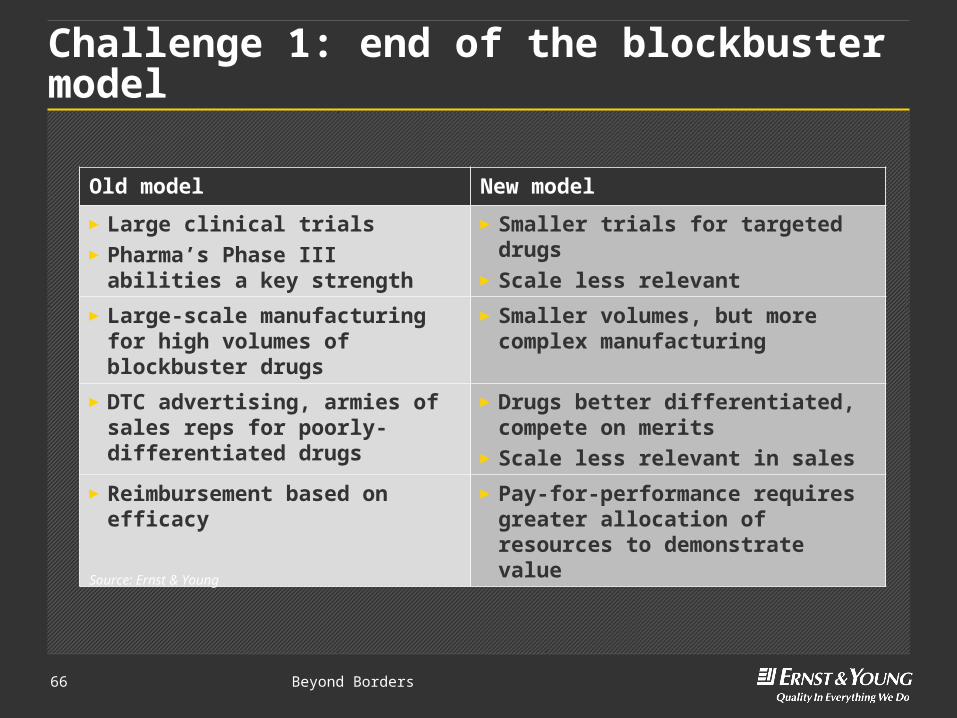

Challenge 1: end of the blockbuster model

Old model New model

►Large clinical trials►Pharma’s Phase III abilities a key

strength

►Smaller trials for targeted drugs►Scale less relevant

►Large-scale manufacturing for high volumes of blockbuster drugs

►Smaller volumes, but more complex manufacturing

►DTC advertising, armies of sales reps for poorly-differentiated drugs

►Drugs better differentiated, compete on merits

►Scale less relevant in sales

►Reimbursement based on efficacy ►Pay-for-performance requires greater allocation of resources to demonstrate value

Source: Ernst & Young

Beyond Borders67

Challenge 2: making the numbers work

Source: Ernst & Young

►Targeted therapeutics for more efficient treatment of disease

►More efficient drug development with smaller, cheaper clinical trials

Rx

►Diagnostics for more efficient:

►Prediction►Diagnosis►Dosing►Monitoring

►Lower healthcare costs from new efficiencies

Dx 3x

►Incentives and metrics to support the economics and ROI for investors:

►Better pricing for diagnostics

►Reimbursement based on value

►Measures across healthcare system

Big pharma companies announce layoffs, restructuringsStock buybacksSafety concerns take bite out of product sales

Velcade gives NICE an unprecedented money-back guarantee

FDA NME approvals fall to lowest level in

over 25 years more pricing

pressuresemerging

Product safety incidents in the

rising China market

Big pharma’s search for pipeline productivity propels a booming deal environment

Biotech companies retain more

rights in deals

The mega deal…is back

π?

8%

Government negotiation of drug prices under MMA returns to public policy debate

FIPNETs

Creative deal structures

►

►

►

►

►►M&A R

EMS

FDAAA ►

$►

€►

¥►

£

R&D

►

??? ? ?►

Big pharma companies announce layoffs, restructuringsStock buybacksSafety concerns take bite out of product sales

Velcade gives NICE an unprecedented money-back guarantee

FDA NME approvals fall to lowest level in

over 25 years more pricing

pressuresemerging

Product safety incidents in the

rising China market

Product safety incidents in the

rising China market

Big pharma’s search for pipeline productivity propels a booming deal environment

Biotech companies retain more

rights in deals

The mega deal…is back

π?

8%

Government negotiation of drug prices under MMA returns to public policy debate

Government negotiation of drug prices under MMA returns to public policy debate

FIPNETs

Creative deal structures

►

►

►

►

►►M&A R

EMS

FDAAA ►

$►

€►

¥►

£

R&D

►

??? ? ???? ? ?

►

The third driver of reinvention:Globalization

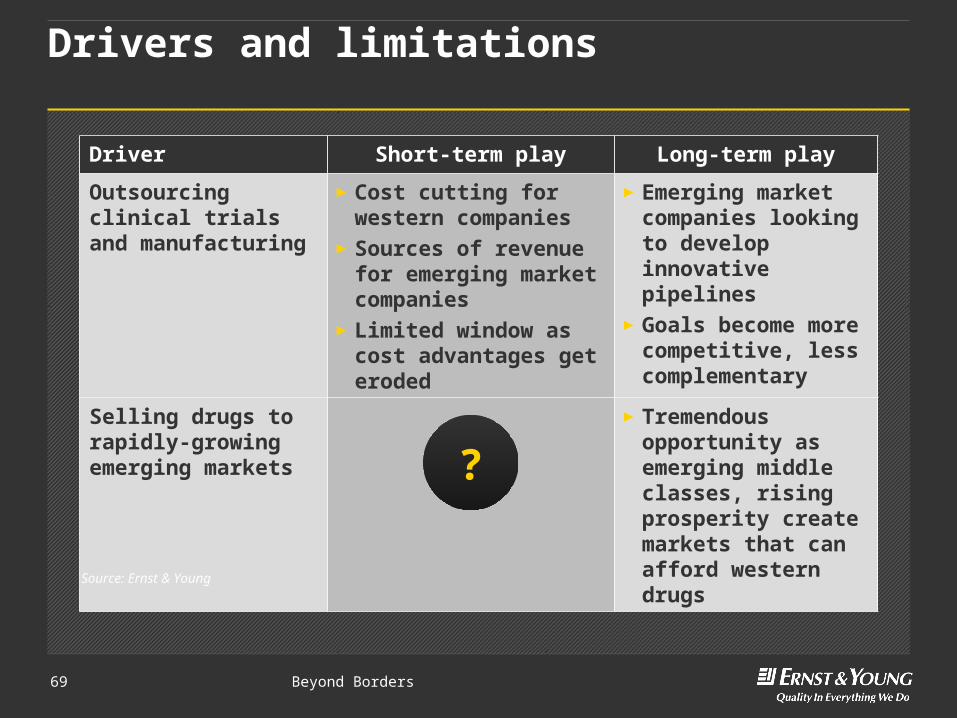

Beyond Borders69

Drivers and limitations

Driver Short-term play Long-term play

Outsourcing clinical trials and manufacturing

►Cost cutting for western companies

►Sources of revenue for emerging market companies

►Limited window as cost advantages get eroded

►Emerging market companies looking to develop innovative pipelines

►Goals become more competitive, less complementary

Selling drugs to rapidly-growing emerging markets

►Tremendous opportunity as emerging middle classes, rising prosperity create markets that can afford western drugs

Source: Ernst & Young

?

Beyond Borders70

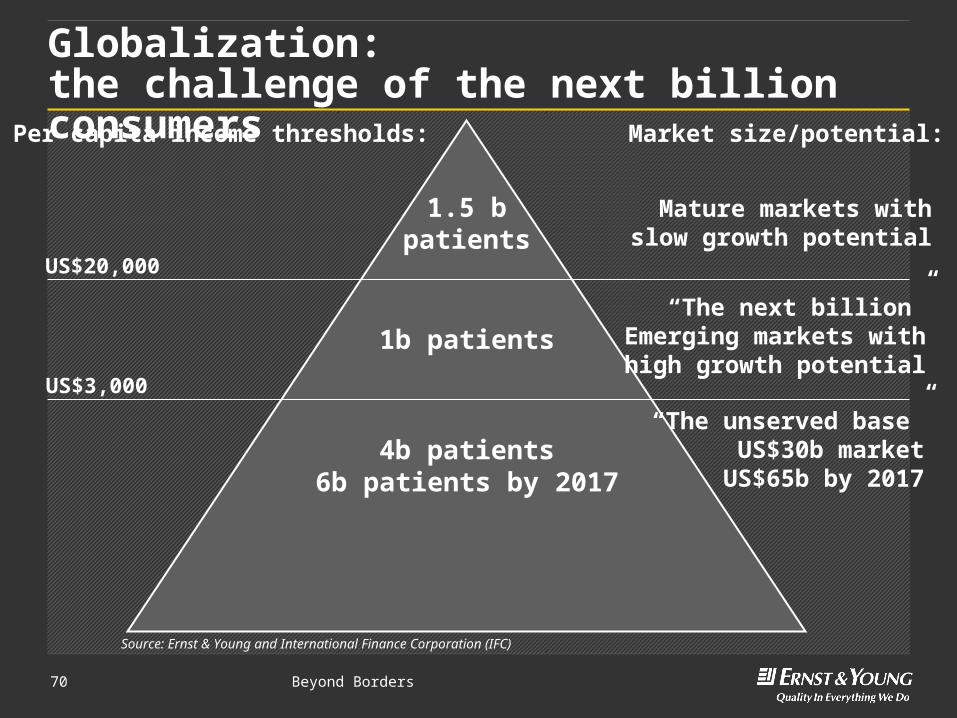

Globalization:the challenge of the next billion consumers

Source: Ernst & Young and International Finance Corporation (IFC)

US$20,000

US$3,000

“The unserved base”US$30b market

US$65b by 20174b patients

6b patients by 2017

1b patients

1.5 bpatients

Mature markets withslow growth potential

Per-capita income thresholds: Market size/potential:

“The next billion”Emerging markets with

high growth potential

Big pharma companies announce layoffs, restructuringsStock buybacksSafety concerns take bite out of product sales

Velcade gives NICE an unprecedented money-back guarantee

FDA NME approvals fall to lowest level in

over 25 years more pricing

pressuresemerging

Product safety incidents in the

rising China market

Big pharma’s search for pipeline productivity propels a booming deal environment

Biotech companies retain more

rights in deals

The mega deal…is back

π?

8%

Government negotiation of drug prices under MMA returns to public policy debate

FIPNETs

Creative deal structures

►

►

►

►

►►M&A R

EMS

FDAAA ►

$►

€►

¥►

£

R&D

►

??? ? ?►

Big pharma companies announce layoffs, restructuringsStock buybacksSafety concerns take bite out of product sales

Velcade gives NICE an unprecedented money-back guarantee

FDA NME approvals fall to lowest level in

over 25 years more pricing

pressuresemerging

Product safety incidents in the

rising China market

Product safety incidents in the

rising China market

Big pharma’s search for pipeline productivity propels a booming deal environment

Biotech companies retain more

rights in deals

The mega deal…is back

π?

8%

Government negotiation of drug prices under MMA returns to public policy debate

Government negotiation of drug prices under MMA returns to public policy debate

FIPNETs

Creative deal structures

►

►

►

►

►►M&A R

EMS

FDAAA ►

$►

€►

¥►

£

R&D

►

??? ? ???? ? ?

►

The shape of the future

Beyond Borders72

Changing business models

Personalized medicine changes the nature of competition

Source: Ernst & Young

Present state

Beyond Borders73

Changing business models

Personalized medicine changes the nature of competition

Source: Ernst & Young

Future state

Beyond Borders74

Changing business models

Personalized medicine redistributes value in the value chain

Source: Ernst & Young

Research

Research

Early development

Early developmentLate development

Late developmentManufacturing

Manufacturing

Sales and marketing

Sales and marketing

0%

20%

40%

60%

80%

100%

Current state Future state - personalized medicine

Value accrues to innovation

Beyond Borders75

The need for new models

R&D

Source: Ernst & Young

Operations

Capital formation & efficiency

Deals

Pharma

►Boost productivity

Biotech

►Remain innovative

►Adapt to smaller scale►Variabilize fixed costs►Tap networks

►Value chain specialization / non-FIPCO models

►Efficient allocation & deployment of capital

►Access capital with less dilution

►Minimize burn rate

►Portfolio approach►Manage risk

►Retain control & rights►Higher share of value

Beyond Borders76

Opportunities for companies

Biotechs gaining

more bargaining

power

More flexibility

Greater share of value

produced

Source: Ernst & Young

Pharma’s imperative to fix R&D product-

ivity

Greater rights retention

Minimize P&L impact of

investments

Creative deals

Accept more risk to increase

potential upside

Acquire culture, not just

pipeline

Biotech Pharma

Beyond Borders77

Models of the future

Source: Ernst & Young

►Leaner FIPCOs: less infrastructure required

►Value-chain specialization

►Becoming FIPCOs less imperative with higher royalties, co-promotion rights

Biotech

►Some successfully reinvent R&D

►New Models: ►More risk

accepting in R&D

►Leaner sales►More networked

Pharma 1 Pharma 2

►For those that don’t succeed at reinvention:

►Core strengths are lower-margin

►Competition from emerging markets

►De facto CROs or CMOs?

Beyond Borders84

Thank you

Stay tuned:

ey.com/biotech

ey.com/beyondborders

Reinnovate. Reinvent. You in?

Related Documents