Belarus and the IMF JVI Course - Financial Programming and Policies Raubichi, January 25, 2017 Bas B. Bakker Senior Regional Resident Representative for Central and Eastern Europe

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Belarus and the IMF

JVI Course - Financial Programming and Policies

Raubichi, January 25, 2017

Bas B. Bakker

Senior Regional Resident Representative

for Central and Eastern Europe

Three phases in Belarus macro

performance since independence:

Post independence contraction (1992-1995)

Boom years (1995-2009)

Slow growth and recession (2010-201x)

2

Sharp decline in GDP in the early

transition

3

30

40

50

60

70

80

90

100

110

t t+1 t+2 t+3 t+4 t+5 t+6

Real GDP per capita, PPP-adjusted

(t=100)

POLCZESVK

BGRROM

EST

BLR

RUS

LVA

UKR

MDA

LTU

t=1991 for former soviet republics (solid lines)

t=1989 for other countries (dashed lines)

UKR

75

100

125

150

175

200

225

250

275

300

1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008

ROM

1995-2008: rapid growth

4

Real GDP per capita, PPP-adjusted

(1995=100)

POL

CZE

SVK

BGR

EST

BLR

RUS

LVA

MDA

-10

-5

0

5

10

15

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Since 2009, growth has slowed sharply

5

Real GDP growth

(2-year moving average, percent)

Belarus

Russia

CE4SEE EU

Baltics

Seen over entire 1990-2016 period,

growth in Belarus has not been bad…

6

-40

-20

0

20

40

60

80

100

120

140

160

0 5,000 10,000 15,000 20,000 25,000

GDP per capita, PPP-adjusted, 1990

GD

P p

er

cap

ita

gro

wth

, 1990-2

014

(perc

en

t)

GDP per capita growth, 1990-2014

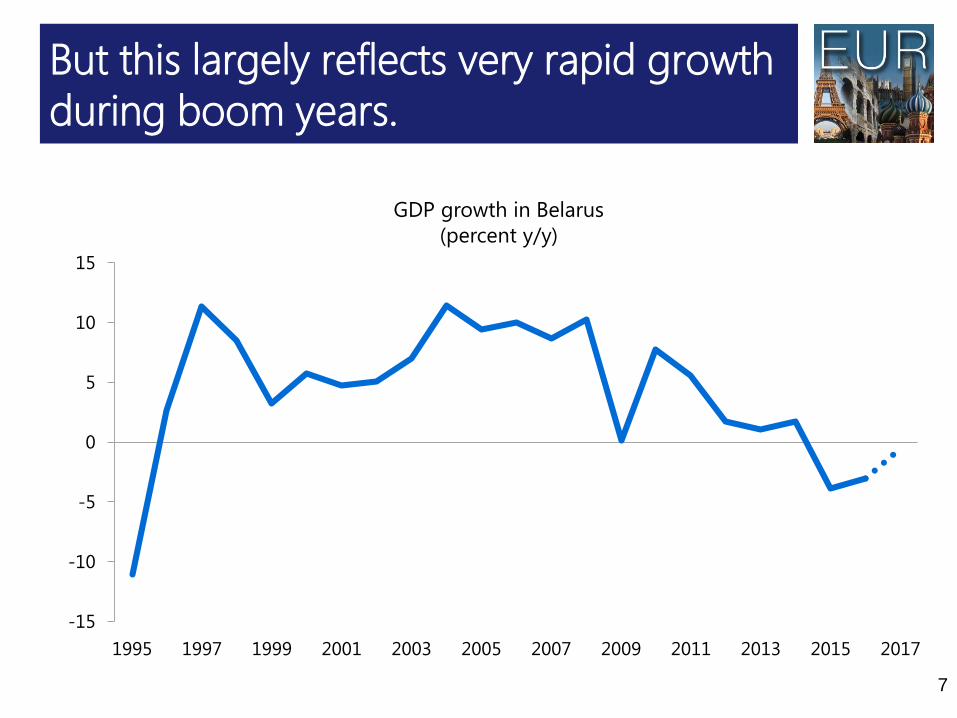

But this largely reflects very rapid growth

during boom years.

7

-15

-10

-5

0

5

10

15

1995 1997 1999 2001 2003 2005 2007 2009 2011 2013 2015 2017

GDP growth in Belarus

(percent y/y)

Why has economic performance

deteriorated?

Is it due to external reasons (including

recession in Russia and Ukraine)?

Or were there also internal reasons? Was the

growth model unsustainable?

Which reforms could help to restore growth?

How can the IMF help?

8

External Reasons for the

Growth slowdown

9

-8

-6

-4

-2

0

2

4

6

8

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

External factors have certainly played a role in the

slowdown: Belarus export markets have done poorly

10

Export market growth

(percent, y/y)

Note: export market growth is weighted average of Belarus’ trading partners real GDP growth, covering over 95 percent of

exports.

5-year moving average

Global growth has been fairly stable in recent

years…

11

Global GDP growth

(percent)

-1

0

1

2

3

4

5

6

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

-4

-2

0

2

4

6

8

10

12

14

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

But growth in emerging markets has slowed—

particularly outside China and India

12

GDP growth

(percent)

Advanced economies

China and India

Other EMs

Within CESEE, there were significant

differences in growth….

13

-10

-8

-6

-4

-2

0

2

4

6

8

10

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

As CIS was in recession, and the rest of

CESEE was growing quite strongly

14

PPP weighted real GDP growth

(percent)

CIS

Other CESEE

-16

-14

-12

-10

-8

-6

-4

-2

0

Ukraine Belarus Russia

Russia and Ukraine suffered from shocks, and

Belarus from spillovers.

Collapse of commodity prices

Sudden stop in capital flows to Russia, result of sanctions on Russia

Conflict in Ukraine

15

Change in GDP

(percent)

Between

2013-15

Between

2013-16

Exchange rate flexibility was unavoidable

given the limited buffers…

16

20

30

40

50

60

70

80

90

100

110

120

20 30 40 50 60 70 80 90 100 110

RUS

UKRBLR

2013

2014 2014

2014

2015

2015

2015

2016

2016

2016

Foreign reserves and XR depreciation

(6-month moving averages)

USD exchange rate (index, H1’2013=100)

Fo

reig

n r

ese

rves

(USD

in

dex,

H1’2

013=

100)

Depreciation

Reserv

es d

raw

dow

n

-5

0

5

10

15

20

25

30

2004 2006 2008 2010 2012 2014 2016

…but increased inflation and reduced real

wages

17

CPI Inflation in European CIS

(percent, weighted average)

max

min

0

250

500

750

1000

Q1'2010 Q1'2012 Q1'2014 Q1'2016

RUS

UKR

BLR

USD 500 line

Average monthly wages

(USD)

-20

-15

-10

-5

0

5

10

15

20

2005 2007 2009 2011 2013 2015

Ukraine and Russia are now recovering (helped

by rising oil prices)

18

-100

-75

-50

-25

0

25

50

75

100

-20

-15

-10

-5

0

5

10

15

20

2005 2007 2009 2011 2013 2015

RUS

Oil prices

(right axis)

Real GDP growth in Russia, other CIS countries and changes in oil prices

(percent, y/y)

UKR

RUS

BLR

-12

-9

-6

-3

0

3

Demand Supply

-12

-9

-6

-3

0

3

Demand Supply

Statistical

discrepancy

-12

-9

-6

-3

0

3

Demand Supply

No signs of recovery yet in Belarus; recession

driven by sharp drop in domestic demand

19

Belarus Russia Ukraine

Domestic

demand

Exports

GDP

growth

Demand and supply components: contribution to GDP in 2016

(percent)

Imports

Forecast for 2017: Non-CIS similar as 2016;

pick-up in CIS; Belarus still in recession

20

-3

-2

-1

0

1

2

3

4

5

6

BLR RUS SVN HRV HUN EST UKR CZE BGR SRB LTU MDA BIH SVK UVK POL LVA MKD MNE ALB ROM

2016

2017

GDP growth

(percent)

Note: CIS countries in red.

Internal Causes for

Growth Slowdown

21

Belarus growth model was unsustainable

Growth was increasingly driven by

unsustainable investment /domestic demand

boom

This led to BOP crises

Productivity (TFP) declined, offsetting the

impact of the larger capital stock

22

15

20

25

30

35

40

45

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Investment to GDP ratio increased

sharply in the 2000s

23

Investment rates

(percent of GDP)

Belarus

SEE non-EU

SEE EU

BalticsCE5

20

25

30

35

40

45

2000 2002 2004 2006 2008 2010 2012 2014 2016

As domestic saving was not sufficient…

24

Investment

Saving

Investment and saving rates

(percent of GDP)

…the current account deficit increased sharply…

25

Current Account Balance

(percent of GDP)

-16

-14

-12

-10

-8

-6

-4

-2

0

2

2000 2002 2004 2006 2008 2010 2012 2014 2016

…and would have been even higher

without support from Russia.

26

Wages increased strongly

27

Average monthly wages in USD

0

100

200

300

400

500

600

700

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

USD 500 line

0

10

20

30

40

50

60

70

80

90

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

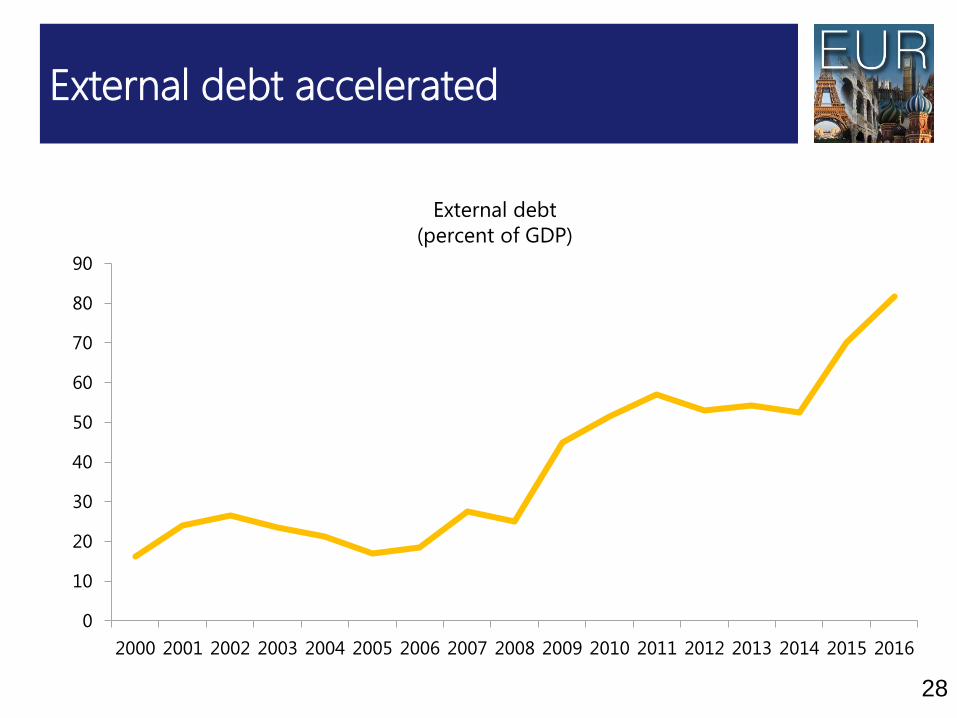

External debt accelerated

28

External debt

(percent of GDP)

0

10

20

30

40

50

60

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

As did public debt.

29

General government debt

(percent of GDP)

-12

-7

-2

3

8

13

18

-40

-30

-20

-10

0

10

20

30

40

50

60

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

The result was several BOP crises

30

Official reserves , rhs

(percent of GDP)

BYR/USD exchange rate

(monthly changes, percent)

Changes in exchange rate and official reserves

Reigniting growth

31

40

50

60

70

80

90

100

Jan-13 Jul-13 Jan-14 Jul-14 Jan-15 Jul-15 Jan-16 Jul-16

Exchange rate has now stabilized

32

BYR/USD

(Jan-2013=100)

Floating of BYR

Dep

reci

ati

on

How can growth be reignited?

33

-15

-10

-5

0

5

10

15

1995 1997 1999 2001 2003 2005 2007 2009 2011 2013 2015 2017

GDP growth in Belarus

(percent y/y)

Not by generating another investment

boom

Without improving exports, investment boom

would increase the current account deficit and

lead to another BOP crisis

We cannot count on a return to past higher

growth rates in Belarus’s key trading partner

Russia

Nor the same level of favorable energy import

pricing.

34

-3

0

3

6

9

12

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Without meaningful SOE restructuring,

investment alone will not improve productivity

and exports

35

Contributions to GDP growth

(2-year moving average, percentage points)

GDP growth

Capital

TFP

Labor

Increasing efficiency rather than

increasing inputs

Instead, growth will to a much larger extent need

to come from increasing efficiency rather than

increasing inputs.

Indeed, what sets Belarus apart from other

countries, is not low investment or low

employment, but, rather low productivity.

36

Investment in Belarus is quite high

37

0

5

10

15

20

25

30

35

UKR BIH SVN SRB HRV POL LTU BGR HUN LVA RUS EST MDA SVK ROM CZE MNE BLR KOS ALB

Investment to GDP ratio, 2016

0

10

20

30

40

50

60

70

80

90

0 10 20 30 40 50 60 70 80 90 100

What sets Belarus from other countries is low

productivity

38

Em

plo

ym

en

t ra

te

(perc

en

t o

f w

ork

ing

ag

e p

op

.)

Labor productivity

(PPP adjusted 2014 USD, thousands)

Labor productivity and utilization, 2015

Flags size reflects GDP per capita in 2015 (PPP-adjusted).

Economic efficiency may be hampered by the too

limited role of the price mechanism in allocating

resources

39

Examples:

Absent hard financial constraint, many

state-owned enterprises are loss

making

Household energy prices are below

cost-recovery levels

Losses of SOEs create macro problem

They have to be compensated by

Higher fiscal expenditures

Or by cheap credit (directed lending)

While current policies have protected

employment in inefficient SOEs, this comes at

the cost of seeding the sows of the next crisis.

40

Simply stopping transfers may create a

banking sector problem

SOEs need to be restructured

IMF providing TA on how to do this

Strong social safety net needed to cushion

adverse impact on unemployment

Growth-enhancing policies, such as lending

programs for privately-owned SME may help

The World Bank is working on a loan/project to

support SME lending.

41

Setting heating tariffs at cost-recovery levels and reducing cross-

subsidization means lower subsidies and more incentive to use

more energy-efficient technologies

42Source: IMF Staff Report, September 2016. Methodology for calculating cost-

recovery in Belarus has since changed.

Belarus needs to catch-up with transition

43

0

1

2

3

4

1989 1999 2009 1989 1999 20091989 1999 20091989 1999 2009 1989 1999 2009

Large scale

privatization

Small scale

privatization

Governance and

restructuring

Price

liberalization

Trade and

forex system

Competition

policy

Belarus

Baltics

SEE EU CE4*

*CE4 includes Hungary, Poland, Slovakia and Slovenia.

1989 1999 2009

EBRD transition indicators

Lessons from Early Transition

In the early 1990s economists had strong

disagreements about whether transition should

be gradual or more rapid

In the end, some countries (Czech, Poland,

Baltics) opted for rapid; others (CIS, Bulgaria)

for more gradual

44

What were the results?

Rapid liberalizers had a much shallower

recession—as well as strong long-term

growth

So waiting with liberalization did not

moderate the pain—it exacerbated it.

45

Postponing reforms can be costly

Reforms can certainly be painful in the short

run, but not transforming the inefficient

economy can have even larger costs

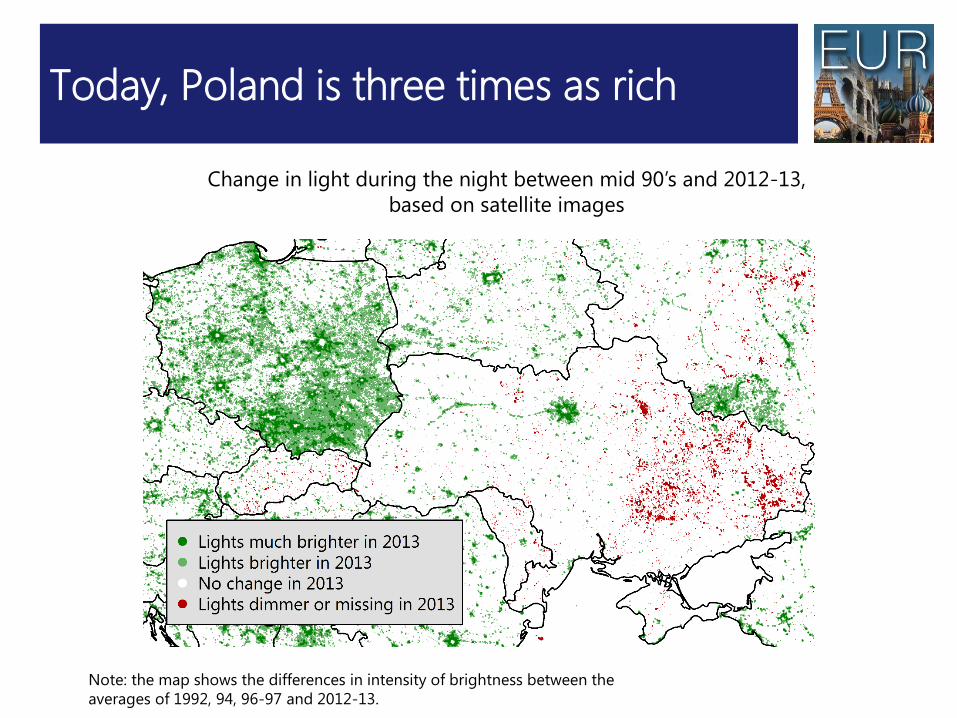

Example: in 1989 Poland and Ukraine were

equally poor. Poland pursued transition

reforms quickly, as opposed to Ukraine.

46

Today, Poland is three times as rich

Change in light during the night between mid 90’s and 2012-13,

based on satellite images

Note: the map shows the differences in intensity of brightness between the

averages of 1992, 94, 96-97 and 2012-13.

Belarus and the IMF

48

Belarus has had several IMF Programs

since independence

49

0.0

0.5

1.0

1.5

2.0

2.5

1993 1995 1997 1999 2001 2003 2005 2007 2009 2011 2013 2015

IMF arrangements with Belarus and credit outstanding

(SDR billion)

Systemic Transformation Facility

Standby Arrangement

Standby Arrangement

Systemic Transformation Facility

Many promised reforms not

implemented

Many of the structural reforms pledged in STF

have still not be done.

SOE Reform

Utility Reform

50

Last program in 2009/10

Achieved temporary stability, but

Macro-adjustment was not durable

Directed lending increased sharply during

program

Shortly after program ended, policies were

loosened

BOP crises followed

Few structural reforms

51

Belarus and IMF have talking on and off for

past two years about possible new program

Goal is to reach agreement on 3 year EFF

program

Macro-adjustment to reduce vulnerabilities

Structural reforms to reignite growth (and

further reduce vulnerabilities)

52

More contentious elements of program

Pace and depth of SOE Reform

Raise cost recovery for utilities

Adequacy of Social Safety Nets

53

Experience in other countries suggests

“ownership” is important

Programs are most successful if governments

implement reforms because they believe in

them—not because they feel they have to

Examples of successful IMF programs with

ownership

Korea

Ireland

Latvia

54

IMF does not impose reforms

The IMF is a strong supporter, not just of growth, but of inclusive growth.

That is why we advocate reforms that will support economic growth, with targeted support for those in need.

We cannot and do not want to impose reforms.

But we can help countries that want to reform.

We hope that we will be able to help Belarus to reform.

55

Conclusions

Belarus has had rapid growth

But growth model no longer sustainable

Reforms and more market mechanism needed

To fix macro problems

To fix micro problems

Waiting with reforms may exacerbate pain—

not lessen it.

56

Thank you

Related Documents