Beer Institute Research Washington, DC Draft Beer Industry Update, 2012 Lester Jones Chief Economist Beer Institute, Washington, DC

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

8/17/2019 Beer Industry Draft Beer Update - 2012

http://slidepdf.com/reader/full/beer-industry-draft-beer-update-2012 1/17

Beer Institute Research

Washington, DC

Draft Beer Industry Update, 2012

Lester Jones

Chief Economist

Beer Institute, Washington, DC

8/17/2019 Beer Industry Draft Beer Update - 2012

http://slidepdf.com/reader/full/beer-industry-draft-beer-update-2012 2/17

The

brewing

industry

is

a

dynamic

part

of

the

U.S.

economy

with

$246.5

billion

in

economic

output

or

1.6%

of

US

GDP.

• Bottom up approach – counting establishments and jobs

• Industry directly or indirectly employ 2 million Americans

• Employees earn $79 billion in wages and benefits

• Every state and virtually every community in the country contributes to the

brewing industry in some way

The

Beer

Industry

generates

over

$49

billion

in

taxes

each

year.

• The industry and their employees pay $39 billion in direct business and

personal taxes at federal, state and local levels (Implan estimates)

• The consumption of beer generates $10.2 billion in taxes including $3.7 billion

in federal excise taxes, $1.7 billion in state excise taxes and another $6.5 billion

in sales and other related state taxes. (BI Estimates)

• $49 billion ‐‐ over 40% of the retail value of beer is paid in taxes

BEER

SERVES

AMERICA,

2012

Source: Beer Institute, 2013

8/17/2019 Beer Industry Draft Beer Update - 2012

http://slidepdf.com/reader/full/beer-industry-draft-beer-update-2012 3/17

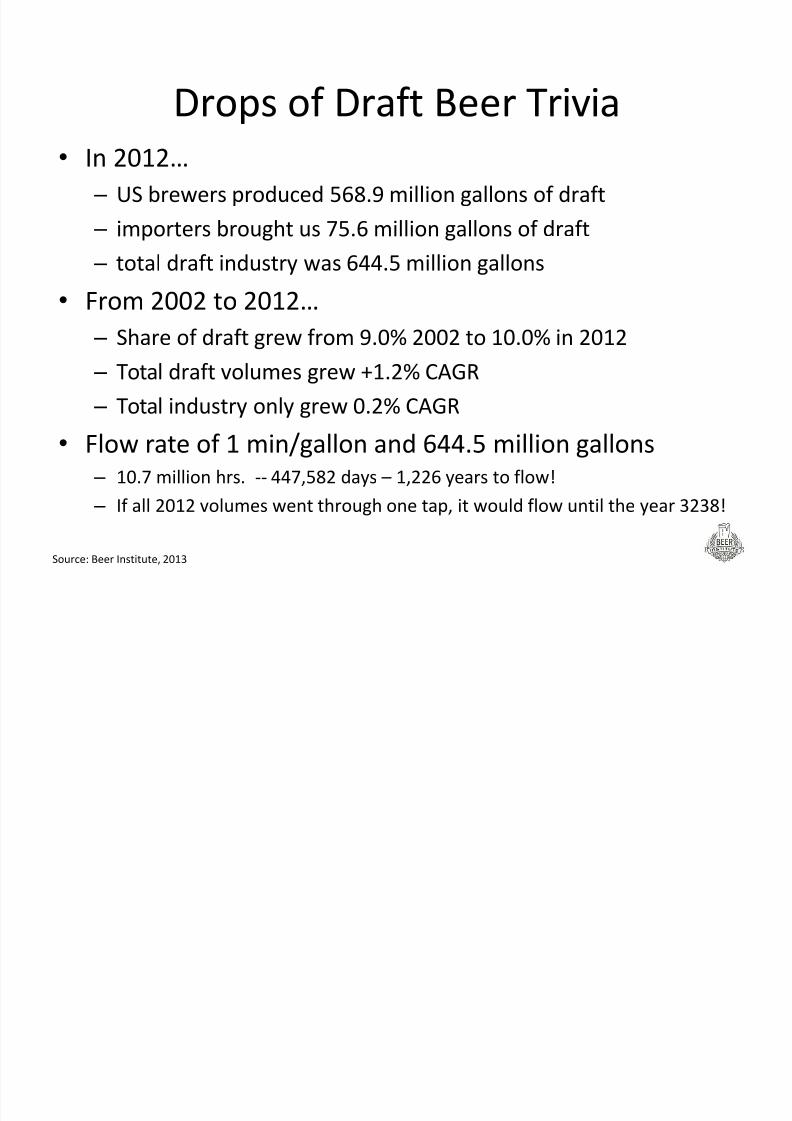

Drops of

Draft

Beer

Trivia

• In 2012…

– US brewers produced 568.9 million gallons of draft

– importers brought us 75.6 million gallons of draft

– total draft industry was 644.5 million gallons

• From 2002 to 2012…

– Share of draft grew from 9.0% 2002 to 10.0% in 2012

– Total draft volumes grew +1.2% CAGR

– Total industry only grew 0.2% CAGR

• Flow rate of 1 min/gallon and 644.5 million gallons – 10.7 million hrs. ‐‐ 447,582 days – 1,226 years to flow!

– If all 2012 volumes went through one tap, it would flow until the year 3238!

Source: Beer Institute, 2013

8/17/2019 Beer Industry Draft Beer Update - 2012

http://slidepdf.com/reader/full/beer-industry-draft-beer-update-2012 4/17

Per Capita Consumption of Malt Beverages

United States

1980

to

2012(total

gallons/total

population)

18.0

19.0

20.0

21.0

22.0

23.0

24.0

25.0

1 9 8 0

1 9 8 1

1 9 8 2

1 9 8 3

1 9 8 4

1 9 8 5

1 9 8 6

1 9 8 7

1 9 8 8

1 9 8 9

1 9 9 0

1 9 9 1

1 9 9 2

1 9 9 3

1 9 9 4

1 9 9 5

1 9 9 6

1 9 9 7

1 9 9 8

1 9 9 9

2 0 0 0

2 0 0 1

2 0 0 2

2 0 0 3

2 0 0 4

2 0 0 5

2 0 0 6

2 0 0 7

2 0 0 8

2 0 0 9

2 0 1 0

2 0 1 1

2 0 1 2

1. 24.6 in 1981 to 20.5 in 2012

2. Demographics (baby boomer‐millenniums )

3. Increased alcohol beverage competition

4. Increased non‐alcohol beverage competition

5. Policy Changes (21 LDA and .08 BAC)

6. Economic (YM25‐34) 4 million out of work

Source: Beer Institute, 2013

8/17/2019 Beer Industry Draft Beer Update - 2012

http://slidepdf.com/reader/full/beer-industry-draft-beer-update-2012 5/17

Annual Draft Beer Statistics2002 – 2012 (31 gallon barrels)

Year

Total

DomesticSupply

Total

ImportSupply

Total

IndustrySupply

DomesticDraft

ImportDraft

Total

IndustryDraft

Domestic

DraftShare

Import

DraftShare

Total

DraftShare

2002 180,400 23,079 203,479 16,542 1,746 18,288 9.2% 7.6% 9.0%

2003 179,400 23,519 202,919 16,944 1,903 18,847 9.4% 8.1% 9.3%

2004 181,254 23,850 205,104 17,162 1,799 18,961 9.5% 7.5% 9.2%

2005 179,645 25,566 205,210 17,106 2,101 19,207 9.5% 8.2% 9.4%

2006 180,500 29,294 209,794 17,425 2,194 19,619 9.7% 7.5% 9.4%

2007 182,687 29,695 212,382 17,602 2,450 20,052 9.6% 8.2% 9.4%

2008 184,571 28,700 213,271 17,670 2,577 20,247 9.6% 9.0% 9.5%

2009 183,218 25,881 209,100 17,845 2,106 19,952 9.7% 8.1% 9.5%

2010 181,148 27,142 208,290 18,204 2,211 20,414 10.0% 8.1% 9.8%

2011 178,030 27,338 205,368 18,327 2,407 20,733 10.3% 8.8% 10.1%

2012 180,061 27,713 207,774 18,352 2,439 20,791 10.2% 8.8% 10.0%

Source: Beer Institute, 2013

8/17/2019 Beer Industry Draft Beer Update - 2012

http://slidepdf.com/reader/full/beer-industry-draft-beer-update-2012 6/17

0

50

100

150

200

1 9 5 0

1 9 5 2

1 9 5 4

1 9 5 6

1 9 5 8

1 9 6 0

1 9 6 2

1 9 6 4

1 9 6 6

1 9 6 8

1 9 7 0

1 9 7 2

1 9 7 4

1 9 7 6

1 9 7 8

1 9 8 0

1 9 8 2

1 9 8 4

1 9 8 6

1 9 8 8

1 9 9 0

1 9 9 2

1 9 9 4

1 9 9 6

1 9 9 8

2 0 0 0

2 0 0 2

2 0 0 4

2 0 0 6

2 0 0 8

2 0 1 0

2 0 1 2

M i l l i o n s o

f B a r r e l s

US Malt Beverages, National Package Mix1950 to 2012

CAN VOLUME BOTTLES VOLUME REFILL VOLUME DRAUGHT VOLUME

Source: Beer Institute, 2013

8/17/2019 Beer Industry Draft Beer Update - 2012

http://slidepdf.com/reader/full/beer-industry-draft-beer-update-2012 7/17

Draft Beer Share of Market

1950‐2012

0

5

10

15

20

25

30

1 9 5 0

1 9 5 3

1 9 5 6

1 9 5 9

1 9 6 2

1 9 6 5

1 9 6 8

1 9 7 1

1 9 7 4

1 9 7 7

1 9 8 0

1 9 8 3

1 9 8 6

1 9 8 9

1 9 9 2

1 9 9 5

1 9 9 8

2 0 0 1

2 0 0 4

2 0 0 7

2 0 1 0

P e r c e n t a g e S h a r e o f m a r k e t

The good old days of tavern and pub culture are long gone. Big TVs, packaged beer and

move to the suburbs shifted consumption away from bars and taverns and into homes.

Source: Beer Institute, 2013

8/17/2019 Beer Industry Draft Beer Update - 2012

http://slidepdf.com/reader/full/beer-industry-draft-beer-update-2012 8/17

Total Draft Gallons

1950 t0

2012

0

100

200

300

400500

600

700

800

900

1 9 5 0

1 9 5 3

1 9 5 6

1 9 5 9

1 9 6 2

1 9 6 5

1 9 6 8

1 9 7 1

1 9 7 4

1 9 7 7

1 9 8 0

1 9 8 3

1 9 8 6

1 9 8 9

1 9 9 2

1 9 9 5

1 9 9 8

2 0 0 1

2 0 0 4

2 0 0 7

2 0 1 0

M i l l i o n s

Source: Beer Institute, 2013

8/17/2019 Beer Industry Draft Beer Update - 2012

http://slidepdf.com/reader/full/beer-industry-draft-beer-update-2012 9/17

Per Capita Consumption of Draft Beer

1950 ‐

2012

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.04.5

5.0

1 9 5 0

1 9 5 3

1 9 5 6

1 9 5 9

1 9 6 2

1 9 6 5

1 9 6 8

1 9 7 1

1 9 7 4

1 9 7 7

1 9 8 0

1 9 8 3

1 9 8 6

1 9 8 9

1 9 9 2

1 9 9 5

1 9 9 8

2 0 0 1

2 0 0 4

2 0 0 7

2 0 1 0

G a l l o n s p e r P e r s o n

Source: Beer Institute, 2013

8/17/2019 Beer Industry Draft Beer Update - 2012

http://slidepdf.com/reader/full/beer-industry-draft-beer-update-2012 10/17

Growing US Draft Share

2002 ‐

2012

7.0%

7.5%

8.0%

8.5%

9.0%

9.5%

10.0%

10.5%

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

Imports Domestic Total

Holding steady at 10 share in 2012.

Source: Beer Institute, TTB and US Dept. of Commerce 2013.

8/17/2019 Beer Industry Draft Beer Update - 2012

http://slidepdf.com/reader/full/beer-industry-draft-beer-update-2012 11/17

Source: TTB and Beer Institute, 2013

12% < share

2012

Draft

Share

of

Market

9%< share < 12%

0%< share <9%

US Average 10% in 2012

5.1

billion

16oz

Servings

8/17/2019 Beer Industry Draft Beer Update - 2012

http://slidepdf.com/reader/full/beer-industry-draft-beer-update-2012 12/17

Draft Beer Growth 2010 to 2012Domestic and Import volume growth

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

8.0%

9.0%

10.0%

2010 2011 2012

Domestic Imports TotalSource: TTB, Commerce Dept and Beer Institute, 2013

8/17/2019 Beer Industry Draft Beer Update - 2012

http://slidepdf.com/reader/full/beer-industry-draft-beer-update-2012 13/17

2012 Imported

Draft

Beer

Country 2012 Volume Share

Cumulative

Share Change Growth

Belgium 630,174 26% 26% 38,284 6.5%

Ireland 476,698 20% 45% (19,339) ‐3.9%

Mexico 448,811 18% 64% 100,950 29.0%

Canada 271,058 11% 75% (72,781) ‐21.2%

Germany 196,585

8% 83% (6,945) ‐

3.4%United Kingdom 160,819 7% 90% (9,486) ‐5.6%

Netherlands 154,213 6% 96% 286 0.2%

Italy 51,996 2% 98% 8,972 20.9%

Czech Republic 15,154

1% 99% 425

2.9%

Denmark 9,376 0% 99% 371 4.1%

All Others 23,666 1% 100% 31,962 1.3%

Total 2,438,550 100% 31,962 1.3%

Source: Commerce Dept. and Beer Institute, 2013

8/17/2019 Beer Industry Draft Beer Update - 2012

http://slidepdf.com/reader/full/beer-industry-draft-beer-update-2012 14/17

Source: TTB and Beer Institute, 2013

Growth 2.4% to 16%

Draft

Volume

Growth,

2012

Growth 0% to +2.3%

Growth -10% to 0% US Average +0.3%

8/17/2019 Beer Industry Draft Beer Update - 2012

http://slidepdf.com/reader/full/beer-industry-draft-beer-update-2012 15/17

2012

Top

10

Largest

Draft

States

Top

10

Largest

States

have

54%

of

US

Volume

Source: Beer Institute, 2013

State

2012 Draft

Volume

Draft

Share

Cumulative

Share

Change in Draft

Volumes

California 2,119,550 9.6% 10% 1.9%

Florida 1,501,510 11.7% 18% 2.4%Pennsylvania 1,453,924 16.6% 25% -1.8%

Texas 1,394,250 7.0% 31% 2.3%

New York 1,113,584 10.6% 37% 0.5%

Illinois 860,979 9.9% 41% -0.1%

Colorado 720,105 19.4% 44% -0.6%

Wisconsin 691,046 14.2% 48% -1.7%

Ohio 652,348 8.1% 51% -2.0%

Michigan 630,241 10.1% 54% -2.7%

Top 10 States 11,137,537 10.5% 54% 0.3%Others 9,474,653 9.5% 46% 0.4%

Total US 19,985,467 10.0% 100% 0.3%

8/17/2019 Beer Industry Draft Beer Update - 2012

http://slidepdf.com/reader/full/beer-industry-draft-beer-update-2012 16/17

On vs.

Off

Premise

• 576,000 establishments that sell beer in US in 2012

– 355,000 On

Premise

Accounts

in

the

US

– Includes bars, taverns, restaurants, concessions and

military bars

• Total US

beer

business

is

worth

$104

billion

dollars

at

retail in 2012

– Off premise has 80% of volumes but only 45% of

dollars

– On premise has 20% of volumes but 55% of retail

dollars

8/17/2019 Beer Industry Draft Beer Update - 2012

http://slidepdf.com/reader/full/beer-industry-draft-beer-update-2012 17/17

Thank You

Lester Jones

Chief Economist

Beer Institute, Washington, DC

Related Documents