3/20/22 2/14/201 0 controlling Course: BBA Subject: Principles of Management Unit: IV

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Apr 15, 20232/14/201

0

controlling

Course: BBASubject: Principles of Management

Unit: IV

Apr 15, 2023 2

TopicsThe Control Function: Planning and

Controlling – Importance of Controlling – Levels of Controlling, Control Process - Requirements for Effective Controls.

Control Techniques: Major Control Systems – Financial Control: Financial Statements; Ratio Analysis – Budgetary Control: Responsibility Centers; Uses of Responsibility Centers – Quality Control – Inventory Control.

Apr 15, 2023 3

controlling

• Definition:Acc. To Koontz: “Managerial control implies the measurement of accomplishment against the standard and the correction of deviations to assure attainment of objective according to plans. “

Apr 15, 2023 4

controlling

against

Measurement of accomplishment (performance)Ex. 80 cards sold

StandardEx. 100 cards

Deviation (gap)Ex. 20 cards

Corrective measuresEx. -Giving proper training - Facilities of mobile & petrol - incentives

So that performance can be achieved acc. To plan

1

Apr 15, 2023 5

2. Control process

1. Establishment of standards

2. Collecting data about actual performance

3. Comparing performance with standards

4. Taking corrective steps

Apr 15, 2023 6

1. Establishment of standards / targets:

- Criteria to measure the performance

Ex. Selling / producing 1000 units

- Types:

(A) Physical standard:

- not expressed in financial terms

- to measure: materials consumed, labor hours, output of the factory

- quantity : production per man-hour, units produced in a day

- quality : hardness of steel, durability of cloth

(B) Cost Standard:

- expressed in monetary terms

- ex. Cost per unit of output, wages/ unit of output, expense / manhour

Apr 15, 2023 7

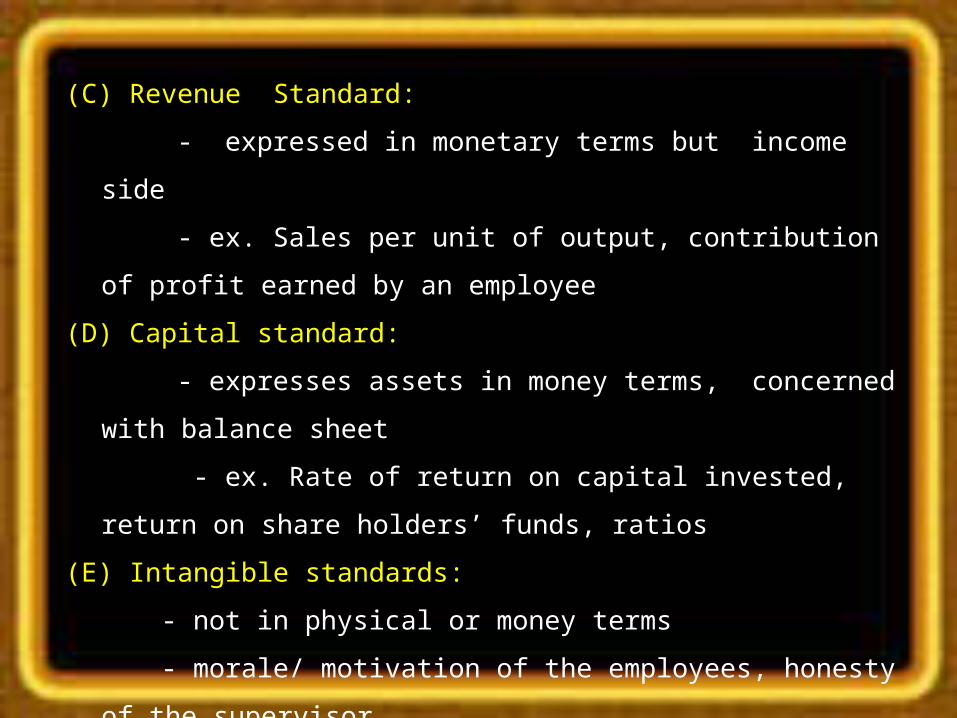

(C) Revenue Standard:

- expressed in monetary terms but income side

- ex. Sales per unit of output, contribution of profit earned by an

employee

(D) Capital standard:

- expresses assets in money terms, concerned with balance sheet

- ex. Rate of return on capital invested, return on share holders’ funds,

ratios

(E) Intangible standards:

- not in physical or money terms

- morale/ motivation of the employees, honesty of the supervisor

Apr 15, 2023 8

2. Collecting data about actual performance - what is done?

- ways to find performance

(A) Personal observation:

- visit of the manager on the sight

- most suitable for intangible results i.e, morale of the employees , response of

buyers

- accuracy is absent

- delay in D.M.

- creates distrust in the empl.

Apr 15, 2023 9

(B) Oral reports:

- orally taking info at the end of the day

- in the group meeting

- ex. Nu. Of units sold, nu. Of customers. visited

- increases relations with employees

- queries can be solved directly

(C) Written reports:

- detailed info.

- preserved for a record

- routine reports (monthly, weekly, daily) – special reports

- charts & table

Apr 15, 2023 10

3. Comparing actual performance

- comparison of actual data of performance with the

standard

- if its according to target – no problem

- if its not acc. to target

- finding the deviation (gap) if any

- ex. Actual performance is 200 laptops sold against target of

300 laptops – Deviation : 100 laptops

Apr 15, 2023 11

4. Taking corrective steps Controlling incomplete without corrective steps

If performance is not acc. to standard – corrective measures need to be taken

Corrective actions involve restructuring organizational set up, training to

employees or reassignment of duties

Should be with future reference

Cost – benefit analysis

Ex. If selling is less than standard :-- corrective steps may be:

- changing advertising copy

- training/ incentives to sales force

- increase frequency of adds.

- improve quality of product

Apr 15, 2023 12

3. Control Techniques

- Ratio Analysis - Budgetary control - Zero Based Budgeting(ZBB) - PERT - CPM

Apr 15, 2023 13

Ratio Analysis:

- Only financial statements (P&L acc., Balance sheet) are of little use for

investors, creditors etc.

- But its relationship provides useful hint for financial health and ability of

business to make profit

- “ Relation between two related items of financial statement is known as

Ratio”

- Ex. Banker used current ratio to know the capacity of repaying the loan

- Gross profit ratio, net profit ratio indicates the profitability

- Current ratio, liquid ratio shows the liquidity of the business

Apr 15, 2023 14

(A) Types of Ratio:

1. Gross Profit Ratio:

Gross Profit 100

Sales

2. Expense Ratio:

Expenses 100

Sales3. Current Ratio: Current Assets 100

Current Liabilities

4. Debt- Equity Ratio:

Outside Liabilities 100

Shareholders’ funds

- Operation ratio, Net Profit Ratio, Stock Turnover Ratio, Quick Ratio etc..

Apr 15, 2023 15

- Budgetary control :

- Budget: numerical statement expressing the plans , policies, and goals of

org for fix period in future.

- Budgetary control: acc. To G.Terry: “B.C. is a process of finding out what

is being done and comparing actual results with the prepared budget data

to find the difference and taking corrective steps”

- Types of Budget where B.C. is necessary:

- Operating Budget: sales budget, production budget, raw material budget,

labor budget, overhead budget

- Financial Budget: cash budget, capital budget, Projected balance sheet

Control systems and techniques

2

Managerial Levels and Control Systems

Level of Management

Type of Control

Top level management

Financial control

Middle level management

Budgetary control

Quality control

Lower level management

Inventory control

1.Financial controlsBalance sheetRatio analysisBudget controls: Zero-Base Budgeting

2.Human Resource Controls

3.Marketing Controls

Market research Test marketing

4.Quality Control

5.Inventory Control•ABC analysis

•EOQ

•PERT/CPM

Thank You

Apr 15, 2023 21

Reference1. https://lh4.ggpht.com/dpjWNEP-

MFaPQW0hg1wfJOxHa0H0U38h90cKUaIdqBGm9nRTuy-Lxf33keqDBSYqLRsB7g=s115

2. https://lh5.ggpht.com/S0o_cwtxKxcz6afa-dVPoEsI8W4oSoyNPnjD1AgfhUVLW__ZAvGGOnkB-ey9TWoAdT4EsA=s131

Related Documents