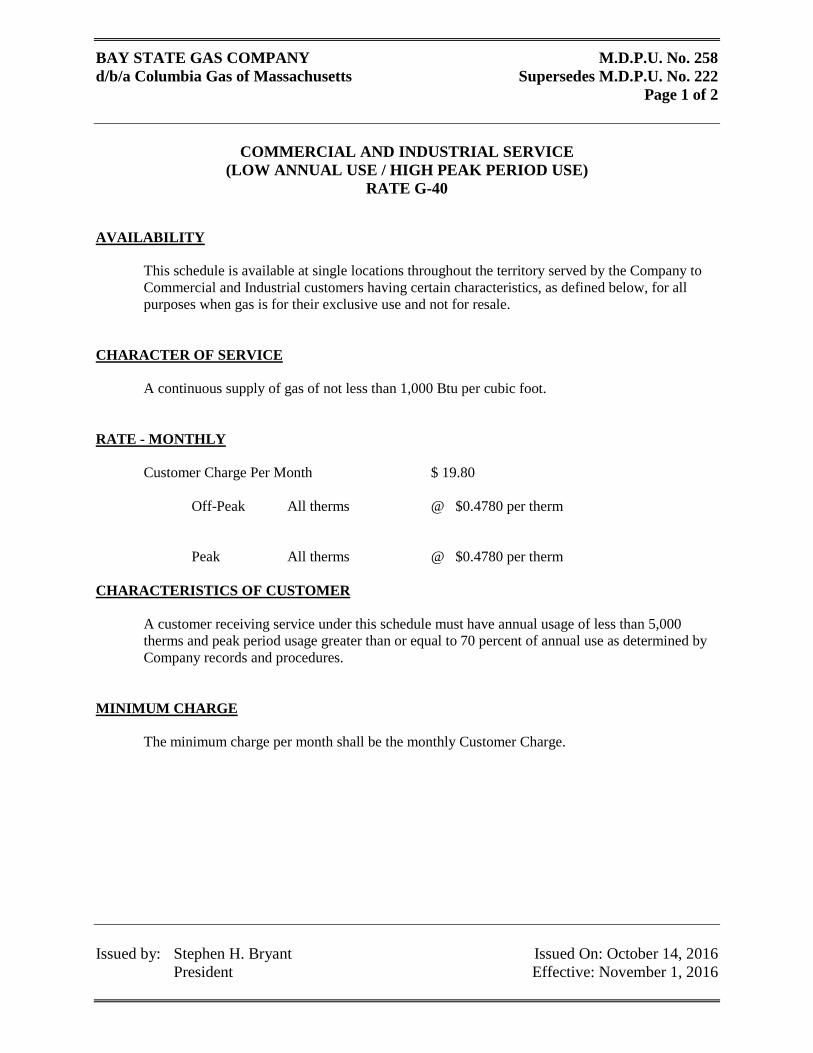

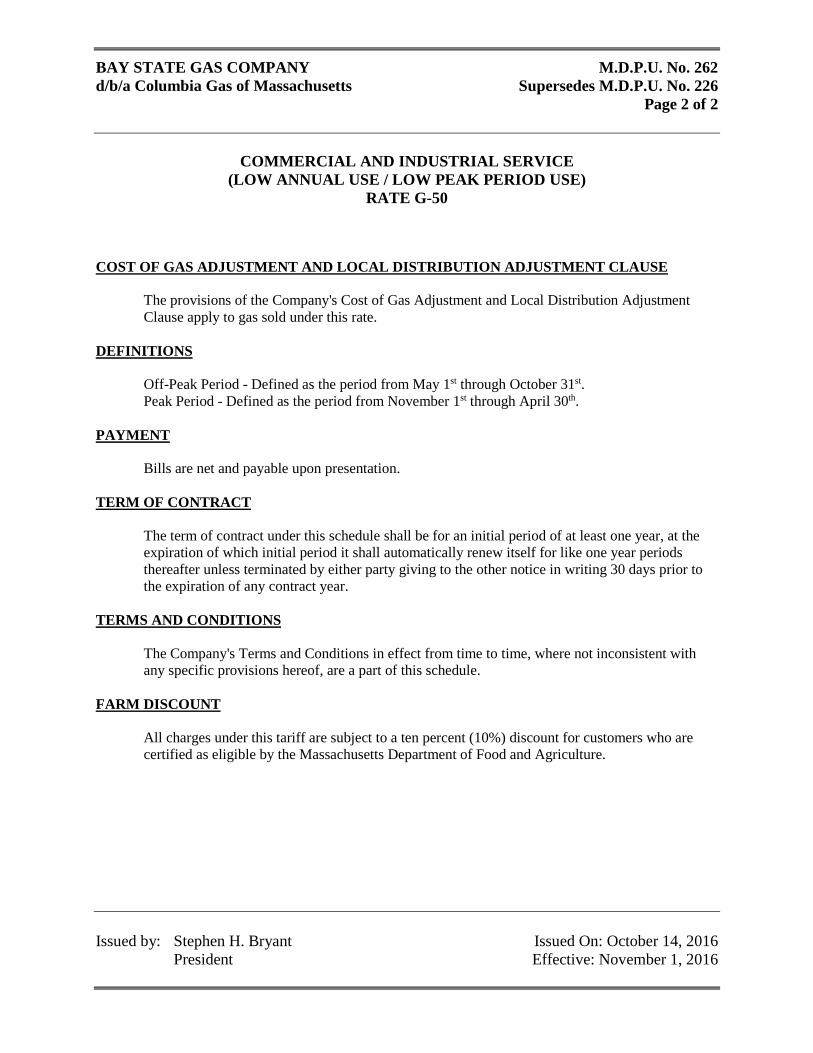

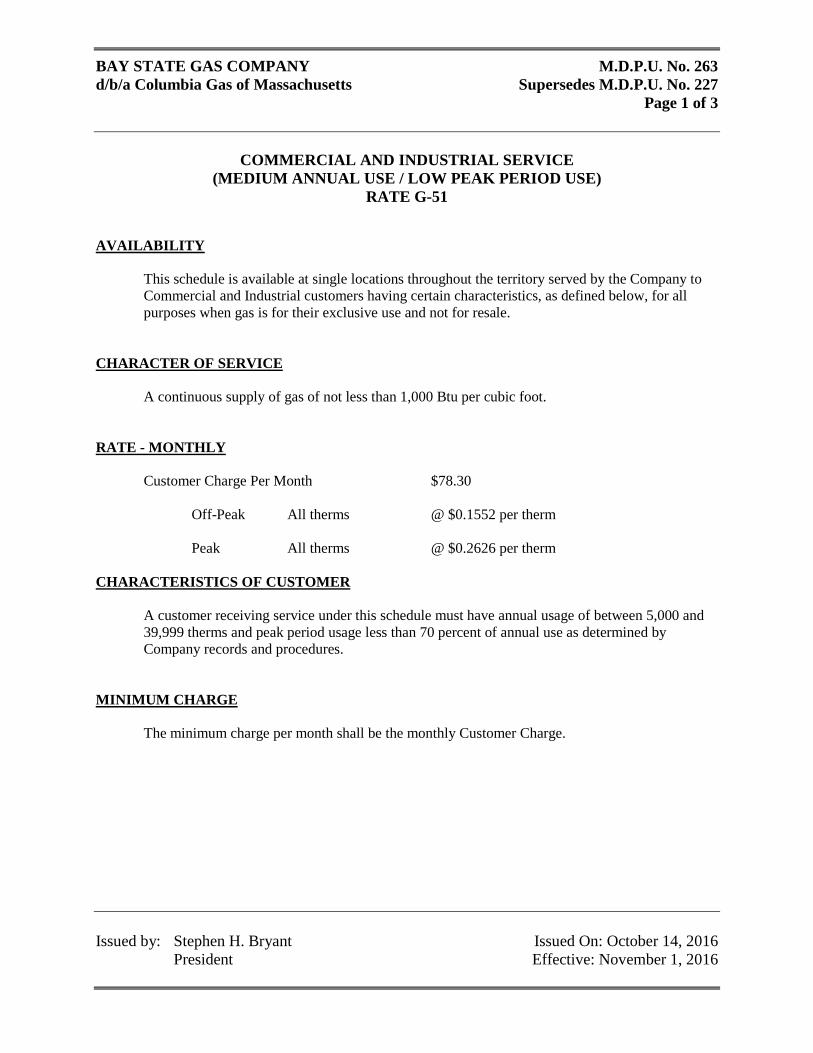

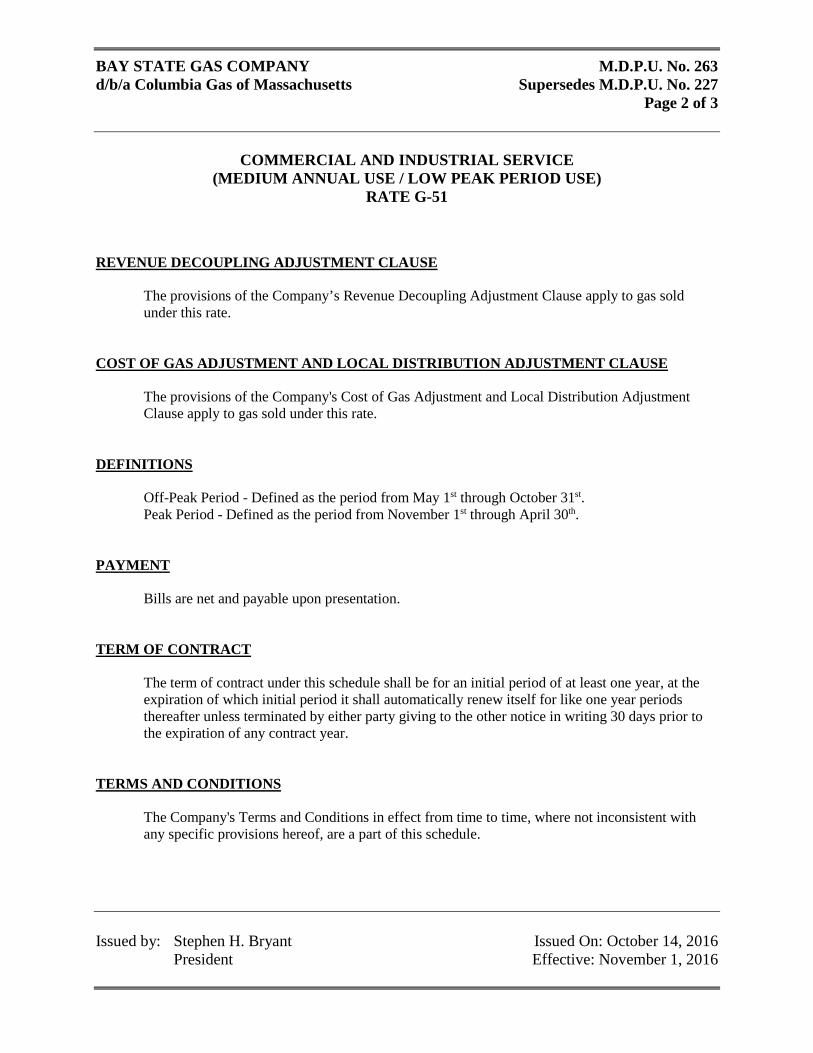

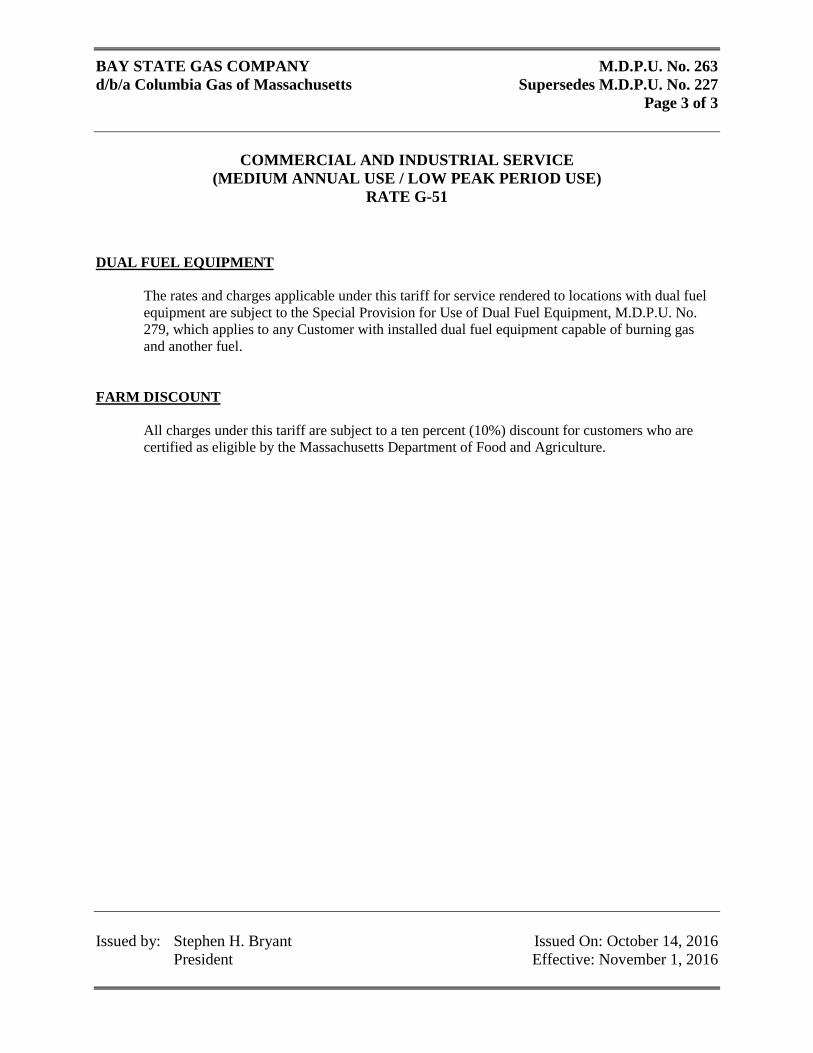

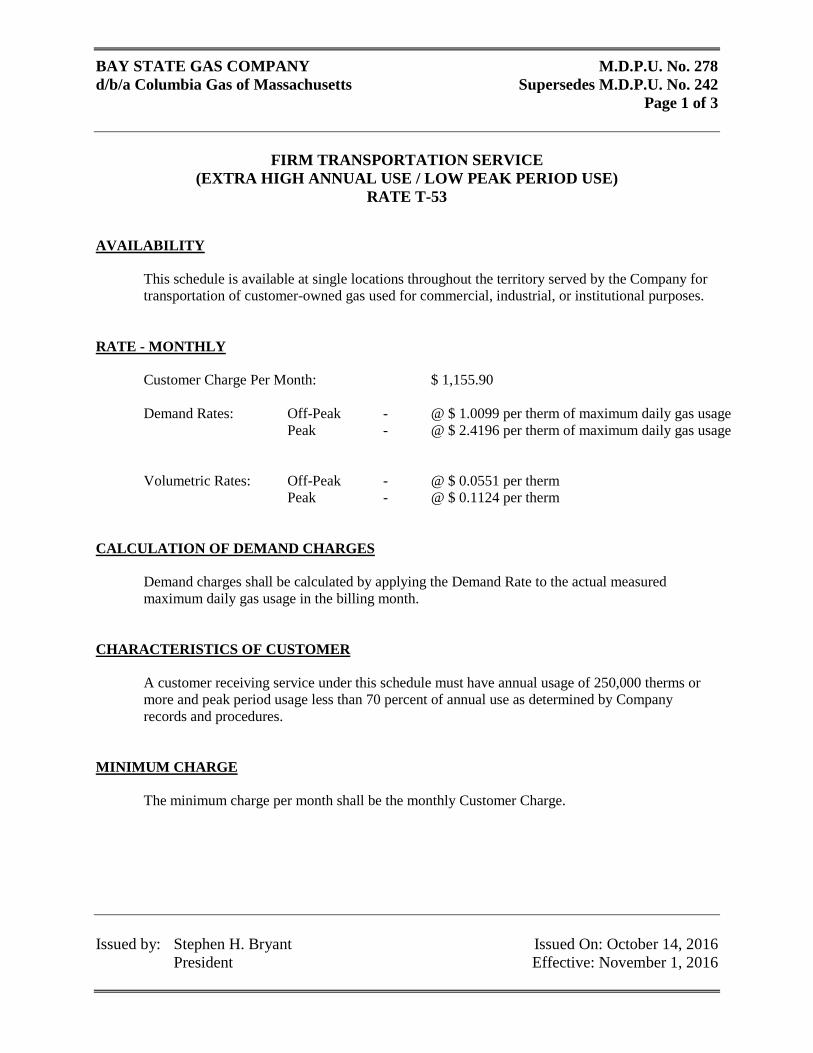

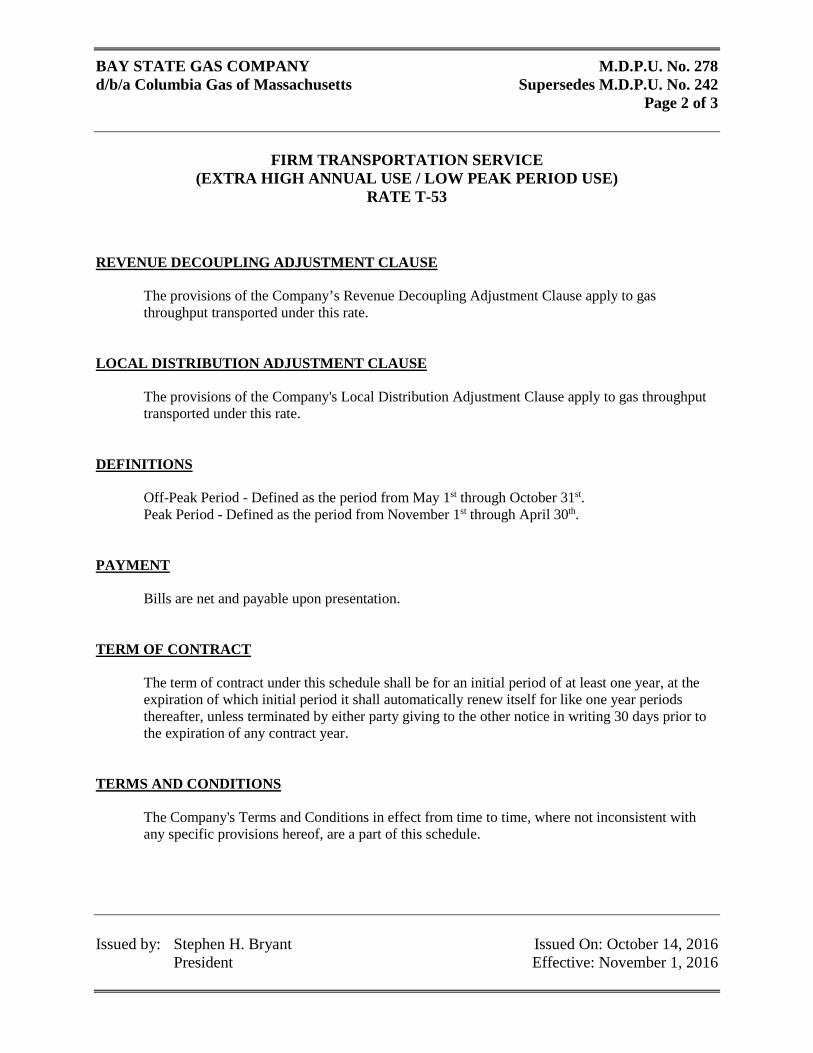

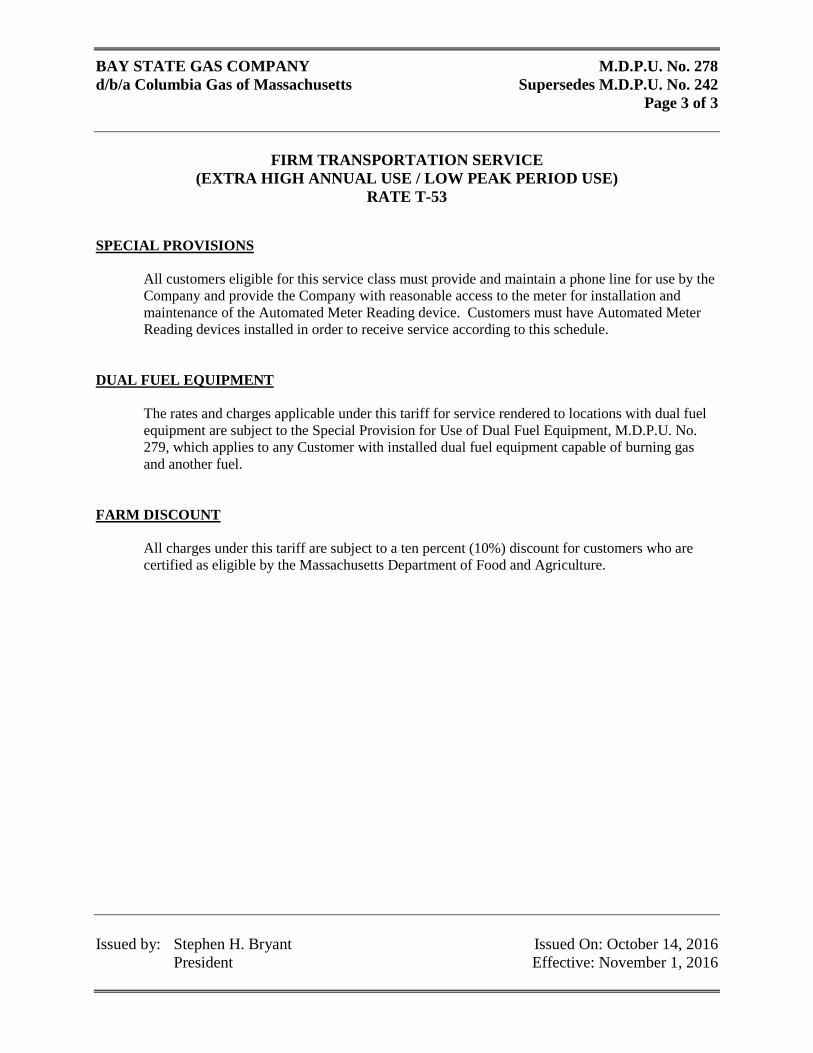

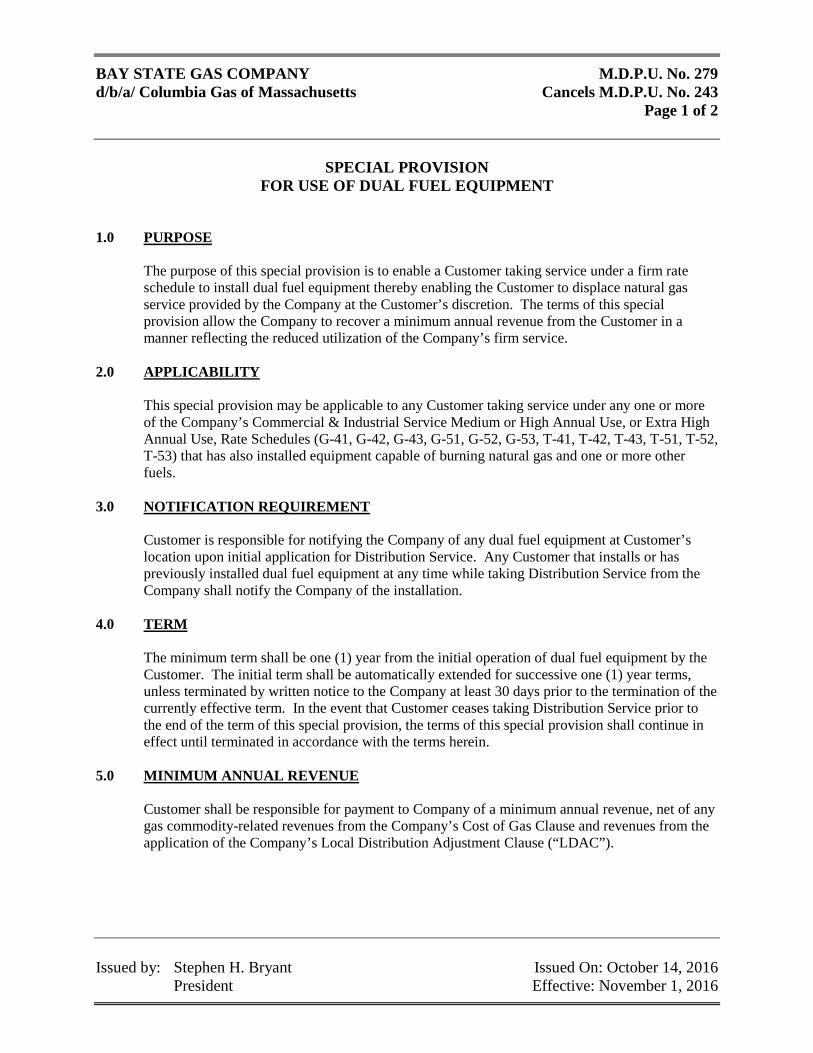

GAS COMPANIES The Commonwealth of Massachusetts RETURN OF THE BAY STATE GAS COMPANY d/b/a COLUMBIA GAS OF MASSACHUSETTS TO THE DEPARTMENT OF PUBLIC UTILITIES OF MASSACHUSETTS FOR THE YEAR ENDED DECEMBER 31, 2017

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

GAS COMPANIES

The Commonwealth of Massachusetts

RETURN

OF THE

BAY STATE GAS COMPANY d/b/a COLUMBIA GAS OF MASSACHUSETTS

TO THE

DEPARTMENT OF PUBLIC UTILITIES

OF MASSACHUSETTS

FOR THE YEAR ENDED DECEMBER 31,

2017

THIS PAGE INTENTIONALLY LEFT BLANK

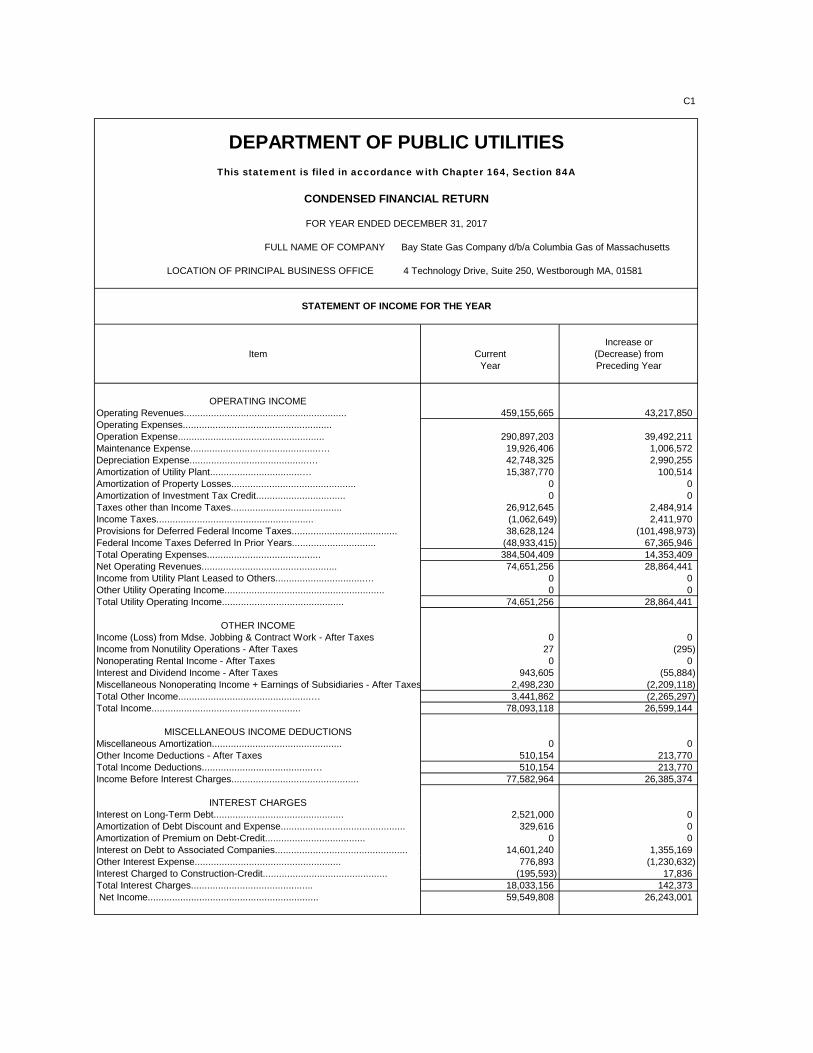

C1

DEPARTMENT OF PUBLIC UTILITIESThis statement is filed in accordance with Chapter 164, Section 84A

CONDENSED FINANCIAL RETURN

FOR YEAR ENDED DECEMBER 31, 2017

FULL NAME OF COMPANY Bay State Gas Company d/b/a Columbia Gas of Massachusetts

LOCATION OF PRINCIPAL BUSINESS OFFICE 4 Technology Drive, Suite 250, Westborough MA, 01581

STATEMENT OF INCOME FOR THE YEAR

Increase orItem Current (Decrease) from

Year Preceding Year

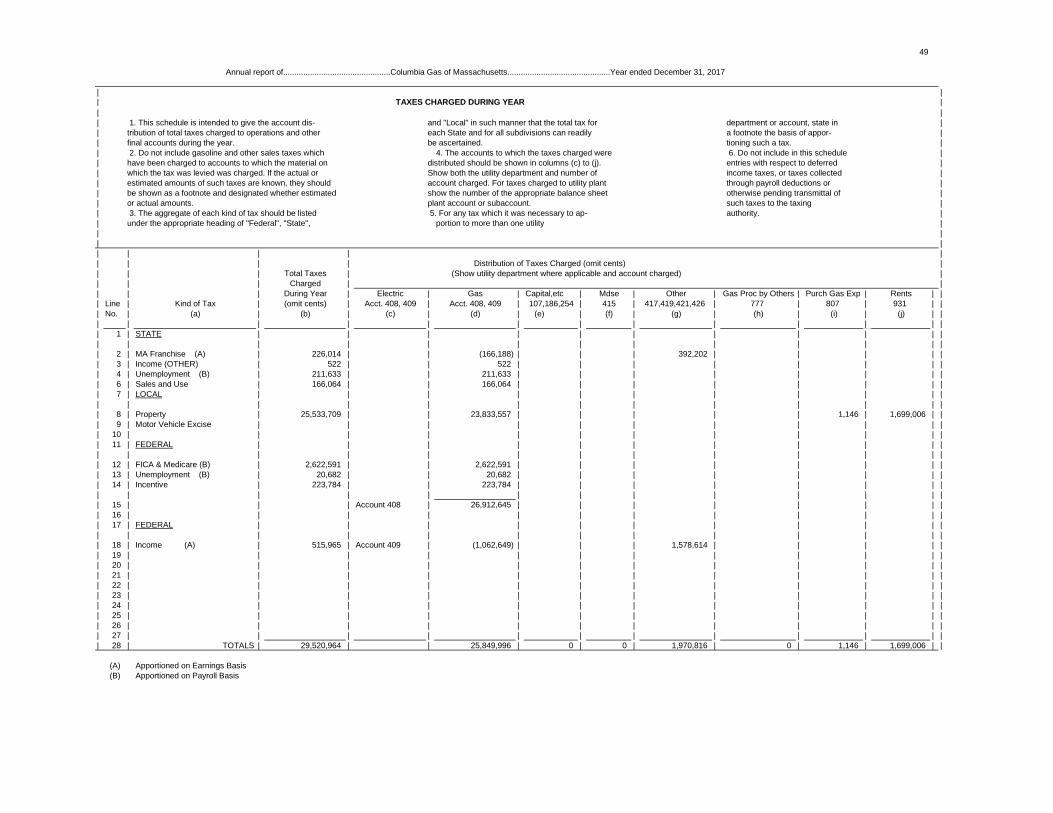

OPERATING INCOMEOperating Revenues............................................................ 459,155,665 43,217,850Operating Expenses.......................................................Operation Expense...................................................... 290,897,203 39,492,211Maintenance Expense................................................… 19,926,406 1,006,572Depreciation Expense............................................… 42,748,325 2,990,255Amortization of Utility Plant..................................… 15,387,770 100,514Amortization of Property Losses.............................................. 0 0Amortization of Investment Tax Credit................................. 0 0Taxes other than Income Taxes......................................... 26,912,645 2,484,914Income Taxes.......................................................... (1,062,649) 2,411,970Provisions for Deferred Federal Income Taxes....................................... 38,628,124 (101,498,973)Federal Income Taxes Deferred In Prior Years............................... (48,933,415) 67,365,946Total Operating Expenses.......................................... 384,504,409 14,353,409Net Operating Revenues.................................................. 74,651,256 28,864,441Income from Utility Plant Leased to Others.................................… 0 0Other Utility Operating Income........................................................... 0 0Total Utility Operating Income............................................. 74,651,256 28,864,441

OTHER INCOMEIncome (Loss) from Mdse. Jobbing & Contract Work - After Taxes 0 0Income from Nonutility Operations - After Taxes 27 (295)Nonoperating Rental Income - After Taxes 0 0Interest and Dividend Income - After Taxes 943,605 (55,884)Miscellaneous Nonoperating Income + Earnings of Subsidiaries - After Taxes 2,498,230 (2,209,118)Total Other Income.................................................… 3,441,862 (2,265,297)Total Income....................................................... 78,093,118 26,599,144

MISCELLANEOUS INCOME DEDUCTIONSMiscellaneous Amortization................................................ 0 0Other Income Deductions - After Taxes 510,154 213,770Total Income Deductions.........................................… 510,154 213,770Income Before Interest Charges............................................... 77,582,964 26,385,374

INTEREST CHARGESInterest on Long-Term Debt................................................ 2,521,000 0Amortization of Debt Discount and Expense.............................................. 329,616 0Amortization of Premium on Debt-Credit..................................... 0 0Interest on Debt to Associated Companies................................................. 14,601,240 1,355,169Other Interest Expense...................................................... 776,893 (1,230,632)Interest Charged to Construction-Credit.............................................. (195,593) 17,836Total Interest Charges............................................. 18,033,156 142,373 Net Income............................................................... 59,549,808 26,243,001

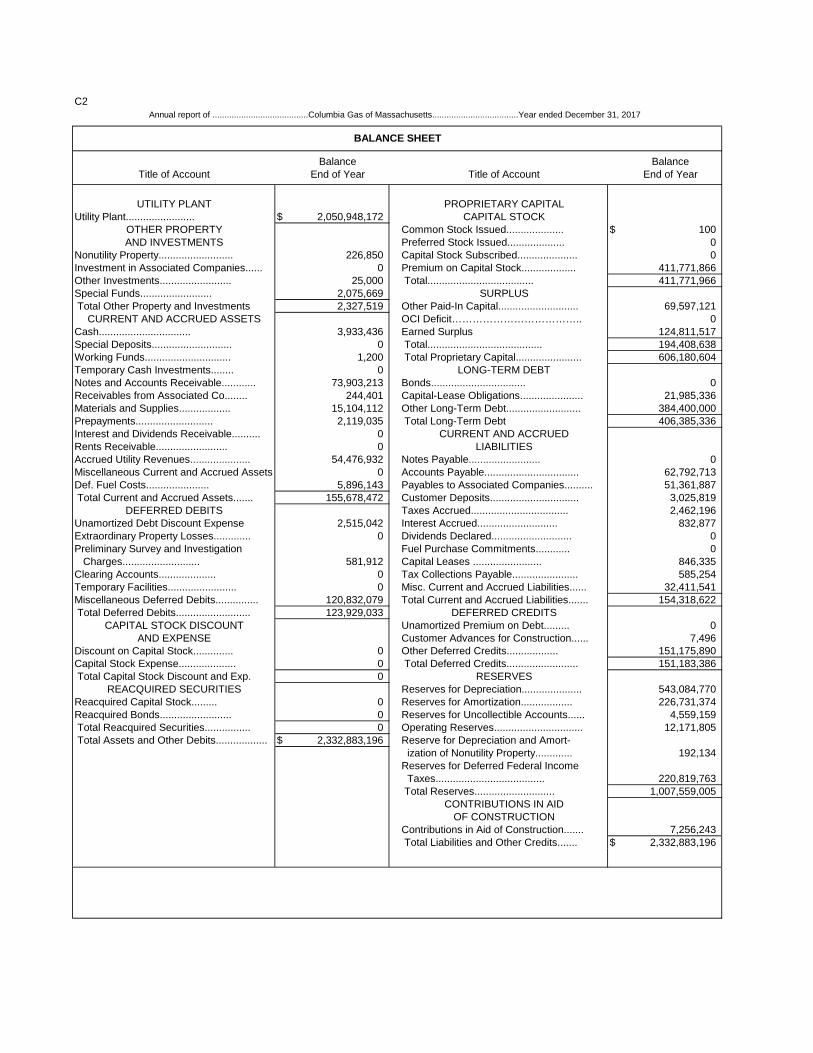

C2Annual report of ........................................Columbia Gas of Massachusetts....................................Year ended December 31, 2017

BALANCE SHEET

Balance BalanceTitle of Account End of Year Title of Account End of Year

UTILITY PLANT PROPRIETARY CAPITALUtility Plant........................ $ 2,050,948,172 CAPITAL STOCK

OTHER PROPERTY Common Stock Issued.................... $ 100AND INVESTMENTS Preferred Stock Issued.................... 0

Nonutility Property.......................... 226,850 Capital Stock Subscribed..................... 0Investment in Associated Companies...... 0 Premium on Capital Stock................... 411,771,866Other Investments......................... 25,000 Total..................................... 411,771,966Special Funds......................... 2,075,669 SURPLUS Total Other Property and Investments 2,327,519 Other Paid-In Capital............................ 69,597,121

CURRENT AND ACCRUED ASSETS OCI Deficit……………………………….. 0Cash................................ 3,933,436 Earned Surplus 124,811,517Special Deposits............................ 0 Total........................................ 194,408,638Working Funds.............................. 1,200 Total Proprietary Capital....................... 606,180,604Temporary Cash Investments........ 0 LONG-TERM DEBTNotes and Accounts Receivable............ 73,903,213 Bonds................................. 0Receivables from Associated Co........ 244,401 Capital-Lease Obligations...................... 21,985,336Materials and Supplies.................. 15,104,112 Other Long-Term Debt.......................... 384,400,000Prepayments........................... 2,119,035 Total Long-Term Debt 406,385,336Interest and Dividends Receivable.......... 0 CURRENT AND ACCRUEDRents Receivable......................... 0 LIABILITIESAccrued Utility Revenues..................... 54,476,932 Notes Payable......................... 0Miscellaneous Current and Accrued Assets 0 Accounts Payable................................. 62,792,713Def. Fuel Costs...................... 5,896,143 Payables to Associated Companies.......... 51,361,887 Total Current and Accrued Assets....... 155,678,472 Customer Deposits............................... 3,025,819

DEFERRED DEBITS Taxes Accrued.................................. 2,462,196Unamortized Debt Discount Expense 2,515,042 Interest Accrued............................ 832,877Extraordinary Property Losses............. 0 Dividends Declared............................ 0Preliminary Survey and Investigation Fuel Purchase Commitments............ 0 Charges........................... 581,912 Capital Leases ........................ 846,335Clearing Accounts.................... 0 Tax Collections Payable....................... 585,254Temporary Facilities........................ 0 Misc. Current and Accrued Liabilities...... 32,411,541Miscellaneous Deferred Debits............... 120,832,079 Total Current and Accrued Liabilities....... 154,318,622 Total Deferred Debits.......................... 123,929,033 DEFERRED CREDITS

CAPITAL STOCK DISCOUNT Unamortized Premium on Debt......... 0AND EXPENSE Customer Advances for Construction...... 7,496

Discount on Capital Stock.............. 0 Other Deferred Credits.................. 151,175,890Capital Stock Expense.................... 0 Total Deferred Credits......................... 151,183,386 Total Capital Stock Discount and Exp. 0 RESERVES

REACQUIRED SECURITIES Reserves for Depreciation..................... 543,084,770Reacquired Capital Stock......... 0 Reserves for Amortization.................. 226,731,374Reacquired Bonds......................... 0 Reserves for Uncollectible Accounts...... 4,559,159 Total Reacquired Securities................ 0 Operating Reserves............................... 12,171,805 Total Assets and Other Debits.................. $ 2,332,883,196 Reserve for Depreciation and Amort-

ization of Nonutility Property............. 192,134Reserves for Deferred Federal Income Taxes...................................... 220,819,763 Total Reserves............................ 1,007,559,005

CONTRIBUTIONS IN AIDOF CONSTRUCTION

Contributions in Aid of Construction....... 7,256,243 Total Liabilities and Other Credits....... $ 2,332,883,196

C3 Annual report of ........................................Columbia Gas of Massachusetts....................................Year ended December 31, 2017

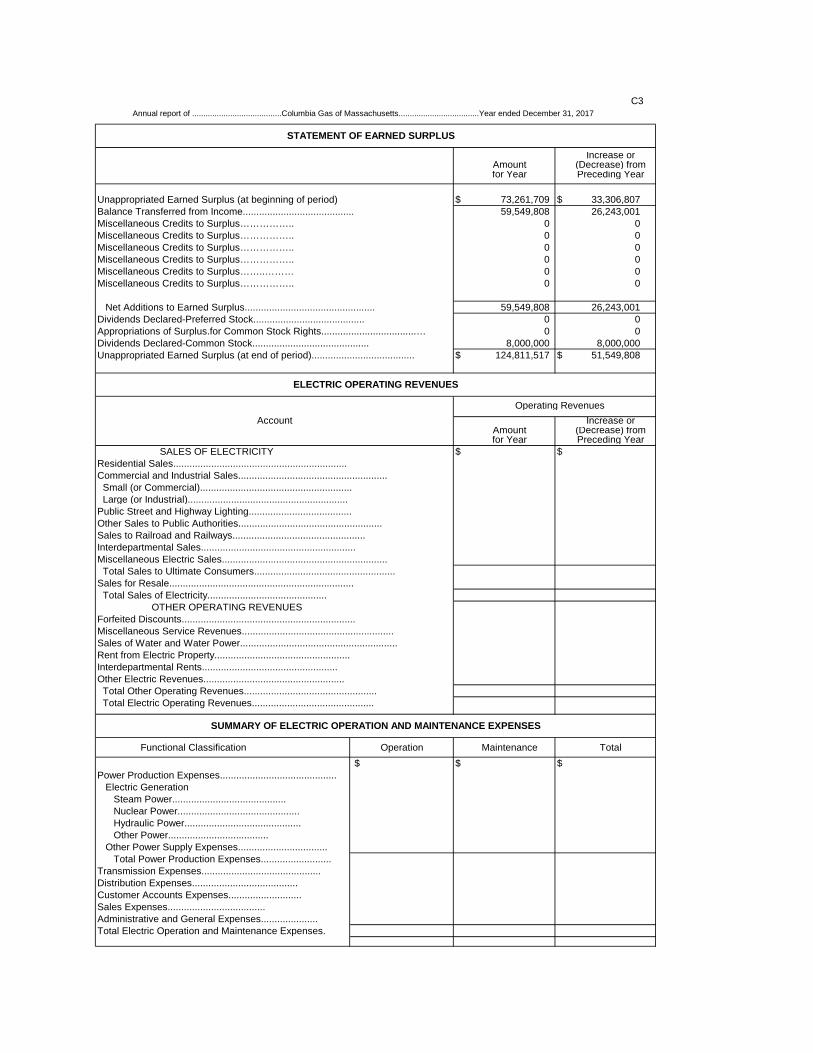

STATEMENT OF EARNED SURPLUS

Increase orAmount (Decrease) fromfor Year Preceding Year

Unappropriated Earned Surplus (at beginning of period) $ 73,261,709 $ 33,306,807Balance Transferred from Income......................................... 59,549,808 26,243,001Miscellaneous Credits to Surplus…………….. 0 0Miscellaneous Credits to Surplus…………….. 0 0Miscellaneous Credits to Surplus…………….. 0 0Miscellaneous Credits to Surplus…………….. 0 0Miscellaneous Credits to Surplus……..……… 0 0Miscellaneous Credits to Surplus…………….. 0 0

Net Additions to Earned Surplus................................................ 59,549,808 26,243,001Dividends Declared-Preferred Stock......................................... 0 0Appropriations of Surplus.for Common Stock Rights...................................… 0 0Dividends Declared-Common Stock........................................... 8,000,000 8,000,000Unappropriated Earned Surplus (at end of period)...................................... $ 124,811,517 $ 51,549,808

ELECTRIC OPERATING REVENUES

Operating RevenuesAccount Increase or

Amount (Decrease) fromfor Year Preceding Year

SALES OF ELECTRICITY $ $Residential Sales................................................................Commercial and Industrial Sales....................................................... Small (or Commercial)........................................................ Large (or Industrial)...........................................................Public Street and Highway Lighting......................................Other Sales to Public Authorities.....................................................Sales to Railroad and Railways.................................................Interdepartmental Sales.........................................................Miscellaneous Electric Sales............................................................. Total Sales to Ultimate Consumers.................................................... Sales for Resale.................................................................... Total Sales of Electricity............................................ OTHER OPERATING REVENUESForfeited Discounts................................................................Miscellaneous Service Revenues........................................................Sales of Water and Water Power..........................................................Rent from Electric Property..................................................Interdepartmental Rents..................................................Other Electric Revenues.................................................... Total Other Operating Revenues................................................. Total Electric Operating Revenues.............................................

SUMMARY OF ELECTRIC OPERATION AND MAINTENANCE EXPENSES

Functional Classification Operation Maintenance Total $ $ $

Power Production Expenses........................................... Electric Generation Steam Power.......................................... Nuclear Power............................................. Hydraulic Power........................................... Other Power..................................... Other Power Supply Expenses................................. Total Power Production Expenses.......................... Transmission Expenses............................................ Distribution Expenses....................................... Customer Accounts Expenses........................... Sales Expenses.................................... Administrative and General Expenses..................... Total Electric Operation and Maintenance Expenses.

C4 Annual report of .................... Columbia Gas of Massachusetts ................. Year ended December 31, 2017

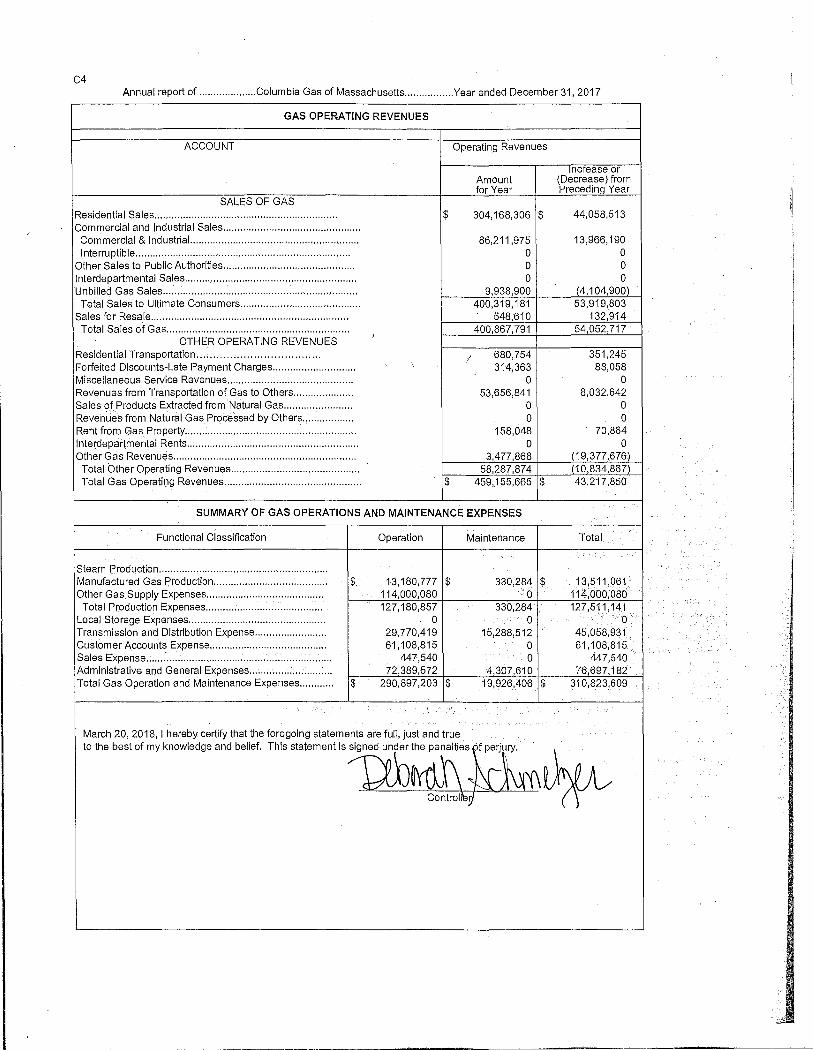

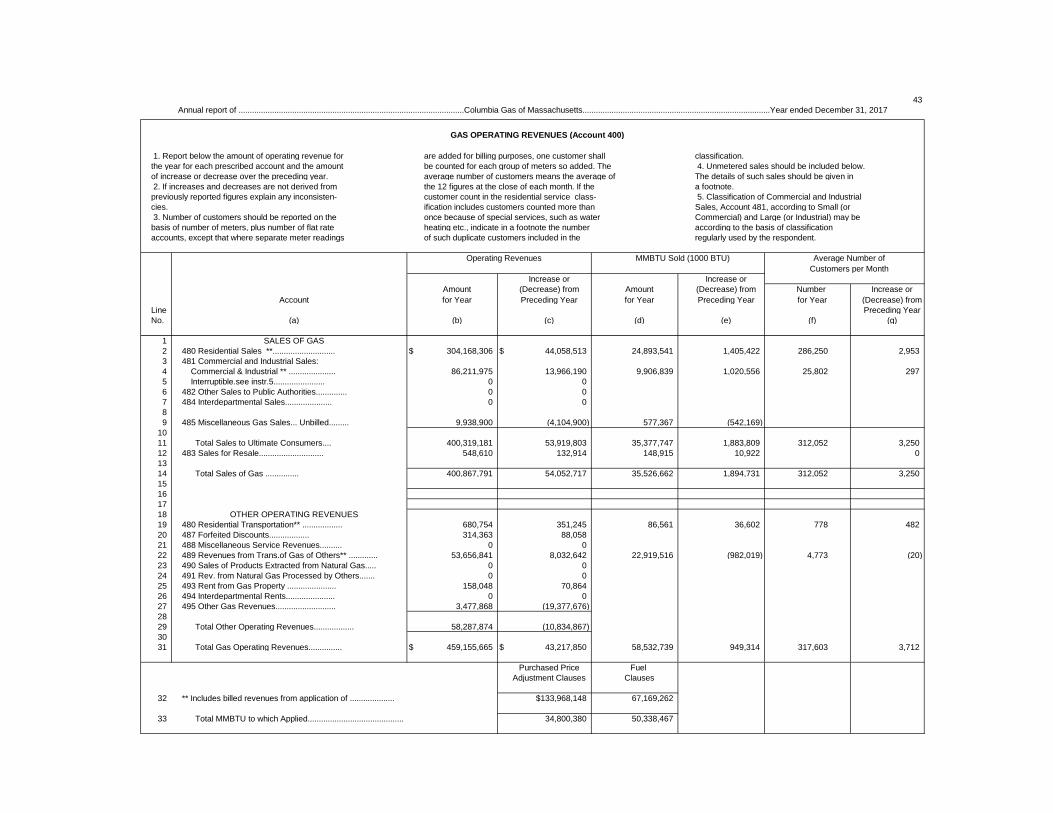

GAS OPERATING REVENUES

ACCOUNT Operating Revenues

increase or Amount (Decrease) from for Year Preceding Year

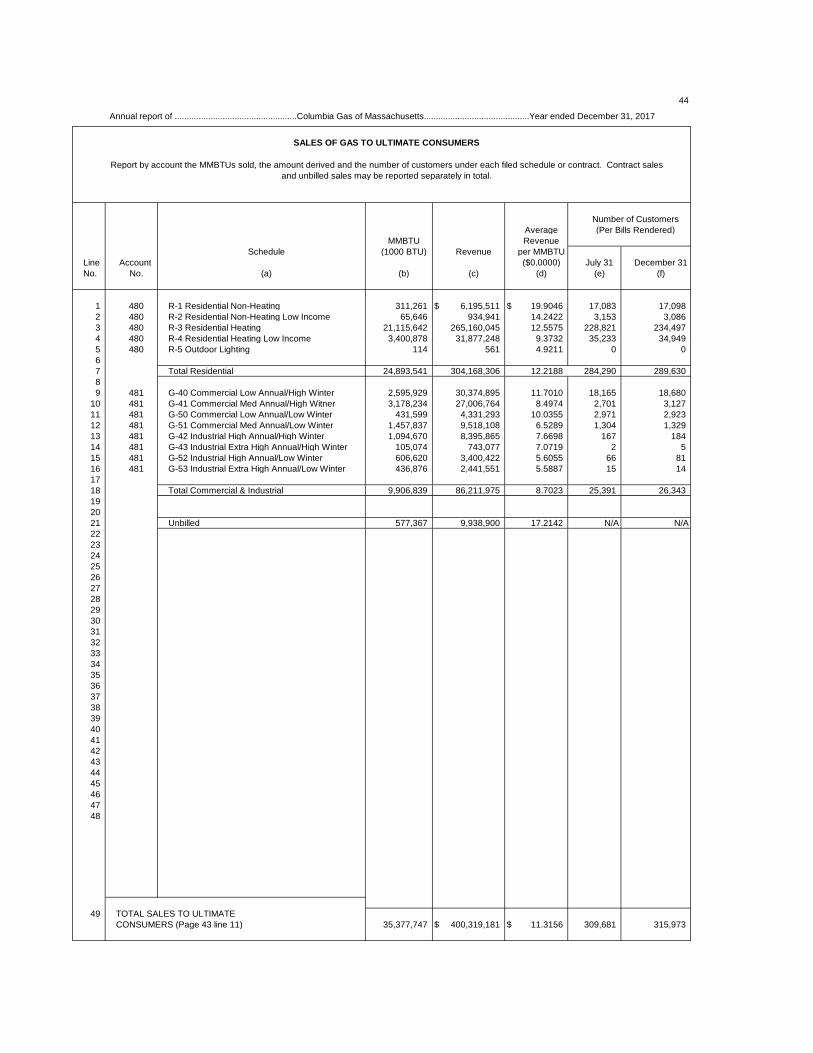

SALES OF GAS Residential Sales ................................................................ $ 304,168,306 $ 44,058,513 Commercial and Industrial Sales ................................................

Commercial & Industrial... ........................................................ 86,211,975 13,966,190 Interruptible ..... , ..................................................................... 0 0

Other Sales to Public Authorities .............................................. 0 0 Interdepartmental S_ales ............................................................ 0 0 Unbilled Gas Sales .................................................................... 9,938,900 (4,104,900)

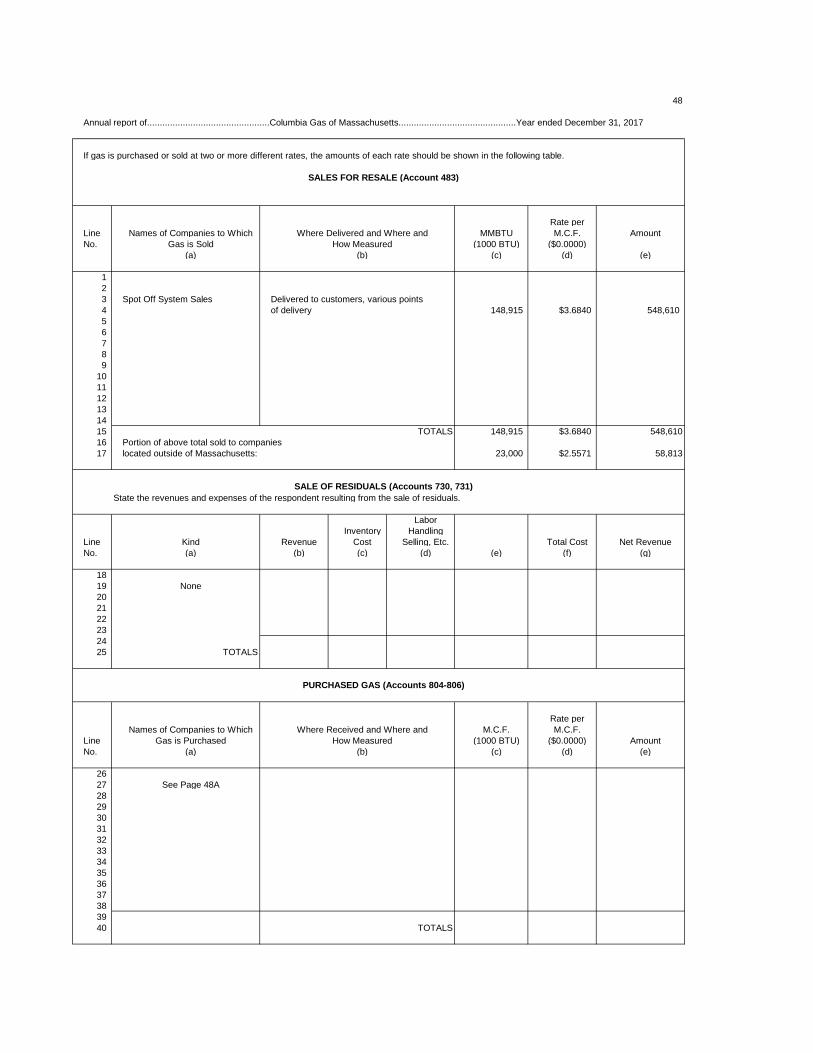

Total Sales to Ultimate Consumers .......................................... 400,319,181 53,919,803 Sales for Resale ..................................................................... 548,610 132,914

Total Sales of Gas ................................................................ 400,867,791 54,052,717 OTHER OPERATING REVENUES ·'

Residential Transportation ........... , ...................... , .. I 680,754 351,245 Forfeited Discounts-Late Payment Charges ............................. 314,363 88,058 Miscellaneous SeNice Revenues ............................................ 0 0 Revenues from Transportation of Gas to Others ..................... 53,656,841 8,032,642 Sales of Products Extracted from Natural Gas ........................ 0 0 Revenues from Natural Gas Processed by Others .................. 0 0 Rent from Gas Property ................. , .......................................... 158,048 70,864 lnterdepar\mental Rents ............................................................ 0 0 Other Gas Revenues ................................................................ 3,477,868 (19,377,676)

Total Other Operating Revenues ............................................. 58,287,874 (10,834,867) Total Gas Operating Revenues ................................................ $ 459,155,665 $ 43,217,850

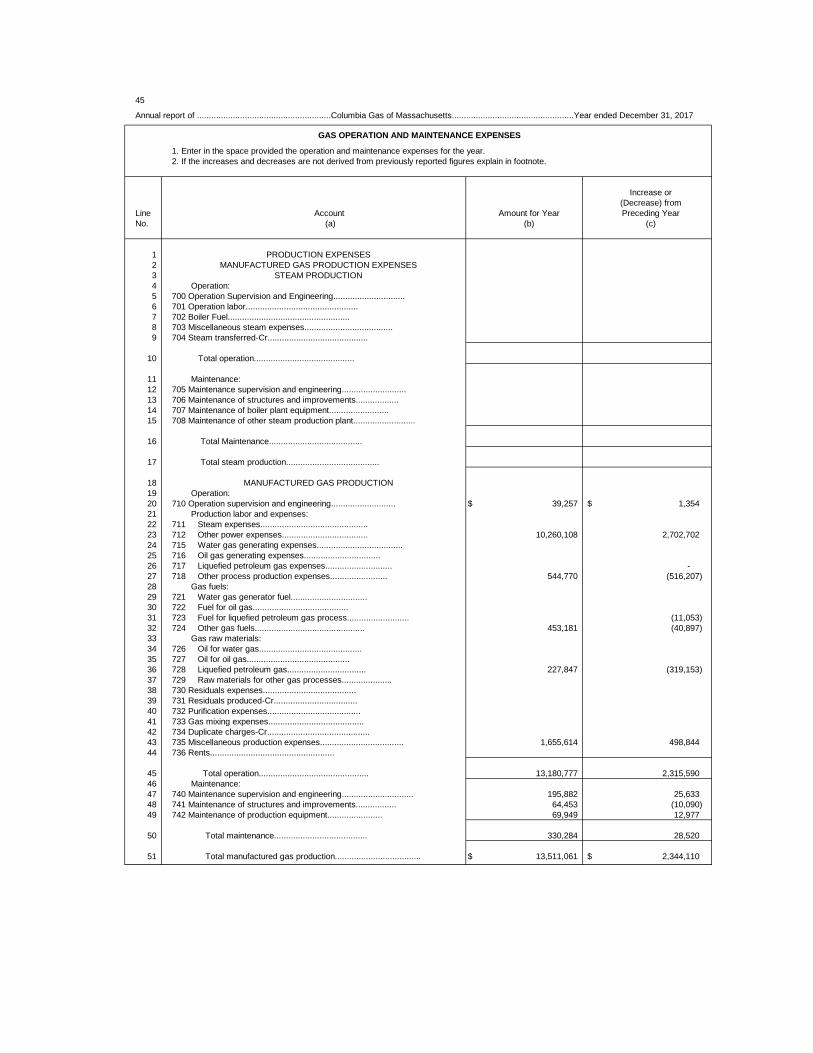

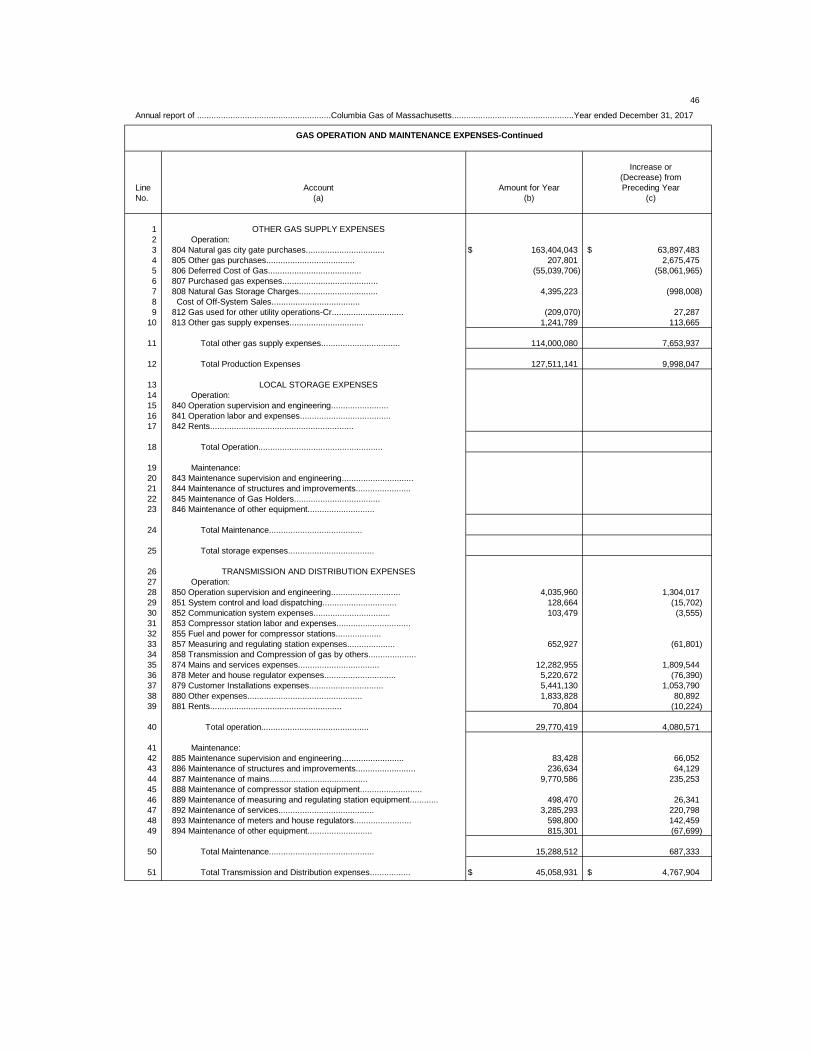

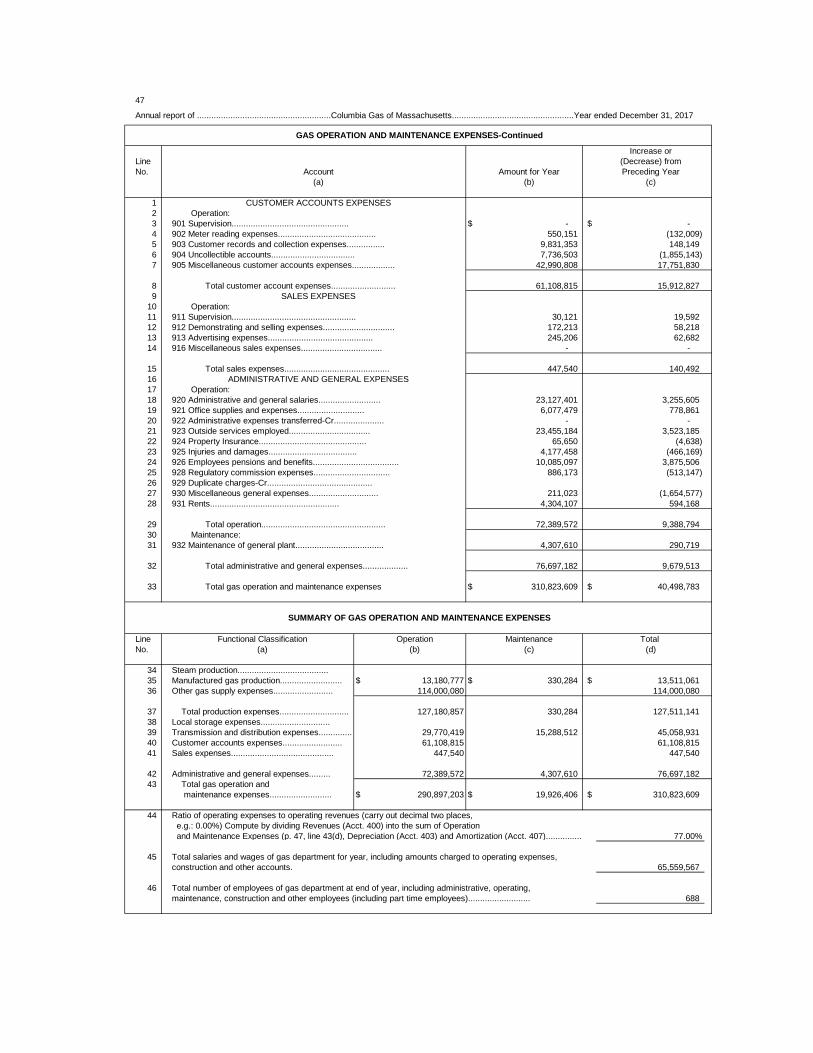

SUMMARY OF GAS OPERATIONS AND MAINTENANCE EXPENSES

Functional Classification Operation Maintenance Total

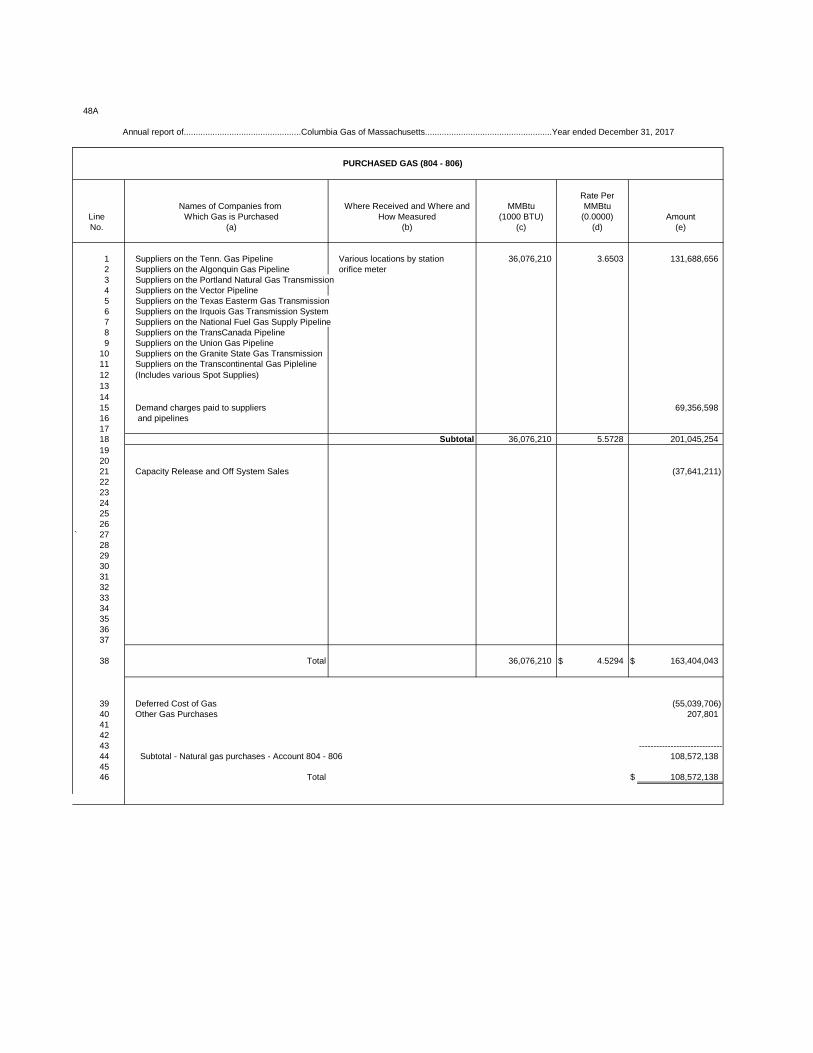

Steam Production ........................................................... Manufactured Gas Production ..................................... , .. $ 13,180,777 $ 330,284 $ 13,511,061 Other Gas Supply Expenses ......................................... 114,000,080 0 114:000,oso

Total Production Expenses ......................................... 127,180,857 330,284 127,511,141 Local Storage Expenses ................................................ 0 0 0 Transmission and Distribution Expense ......................... 29,770,419 15,288,512 45,058,931 Customer Accounts Expense ......................................... 61,108,815 0 61,108,815 Sales Expense ................................................................. 447,540 0 447,540 Administrative and General Expenses ............................. 72,389,572 4,307,610 76,697,182 Total Gas Operation and Maintenance Expenses ............ $ 290,897,203 $ 19,926,406 $ 310,823,609

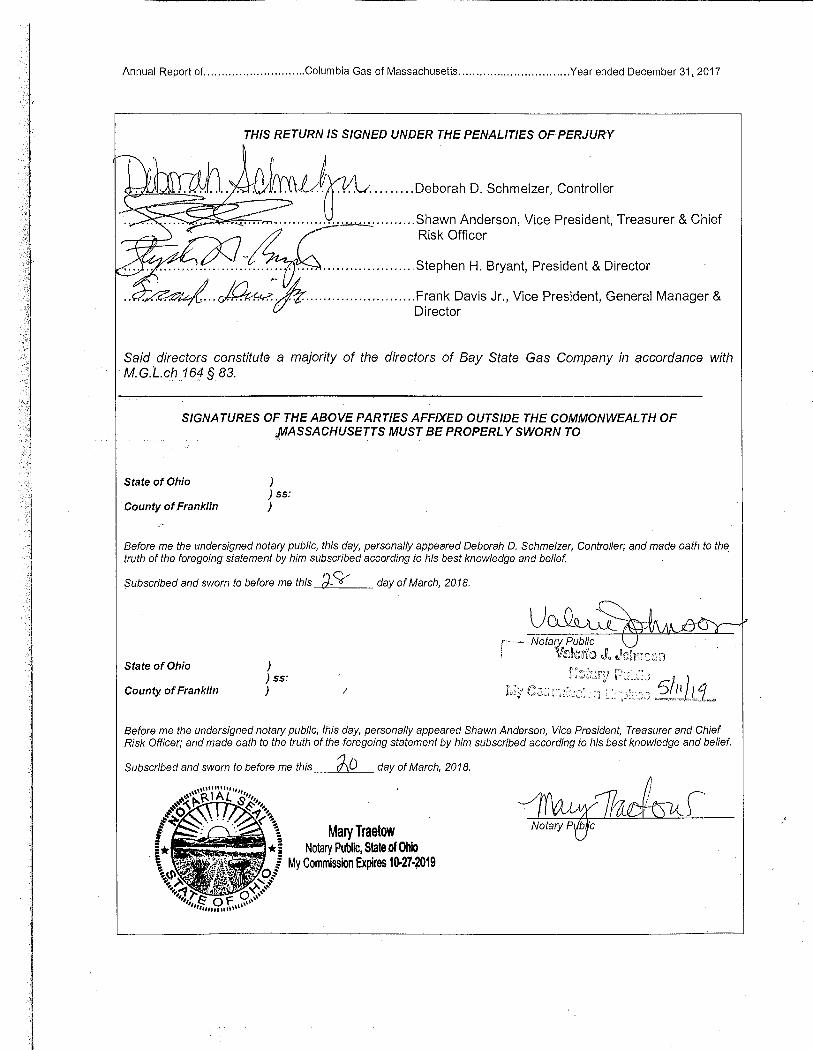

March 20, 2018, I hereby certify that the foregoing statements are full, just and true to the best of my knowledge and belief.

This srat,meot Is 15£~\\s,~k~ Controlrer

Name of Company D/B/A

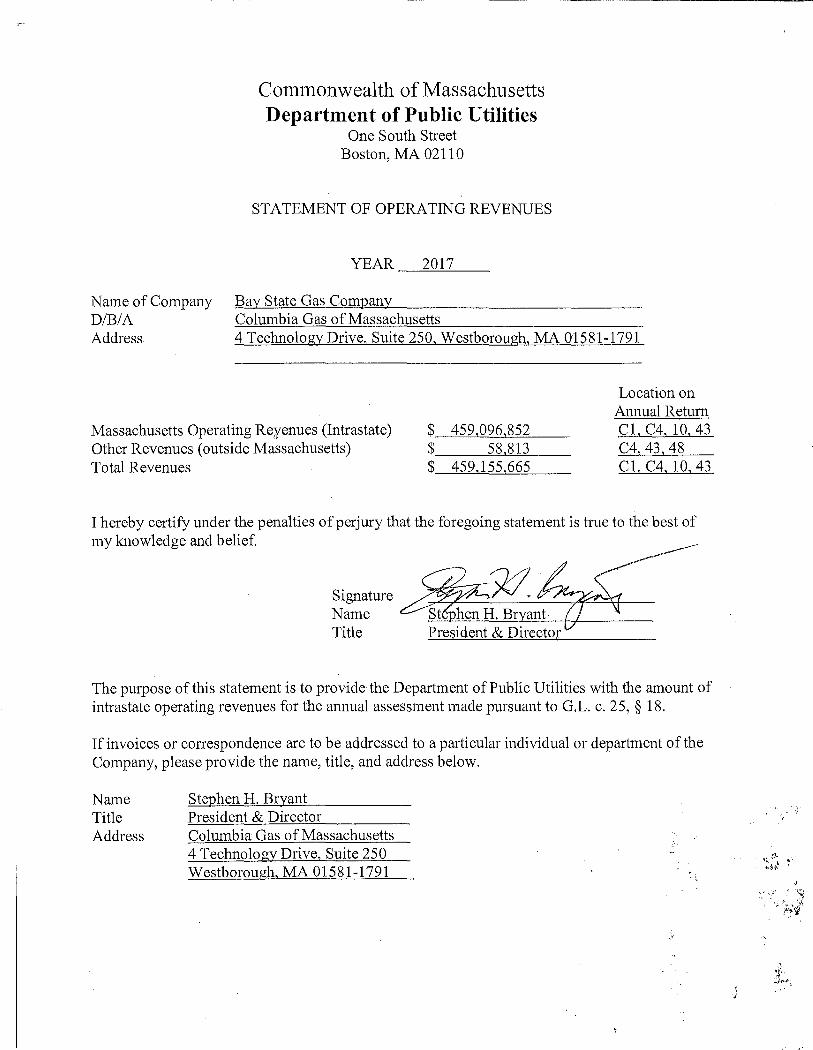

Commonwealth of Massachusetts Department of Public Utilities

One South Street Boston, MA 02110

STATEMENT OF OPERATING REVENUES

YEAR 2017

Bay State Gas Company Columbia Gas of Massachusetts

Address 4 Technology Drive, Suite 250, Westborough, MA 01581-1791

Massachusetts Operating Reyenues (Intrastate) Other Revenues ( outside Massachusetts) Total Revenues

$ 459,096,852 $ 58 813 $ 459,155,665

Location on Annual Return Cl, C4, 10, 43 C4 43 48 Cl, C4, 10, 43

I hereby certify under the penalties of perjury that the foregoing statement is trne to the best of my knowledge and belief.

Signature Name Title

The purpose of this statement is to provide the Department of Public Utilities with the amount of intrastate operating revenues for the annual assessment made pursuant to G.L. c. 25, § 18.

If invoices or correspondence are to be addressed to a particular individual or department of the Company, please provide the name, title, and address below.

Name Title Address

Stephen H. Bryant President & Director Columbia Gas of Massachusetts 4 Technology Drive, Suite 250 Westborough, MA 01581-1791

j

::\'.;i

THIS PAGE INTENTIONALLY LEFT BLANK[NEXT PAGE IS R2]

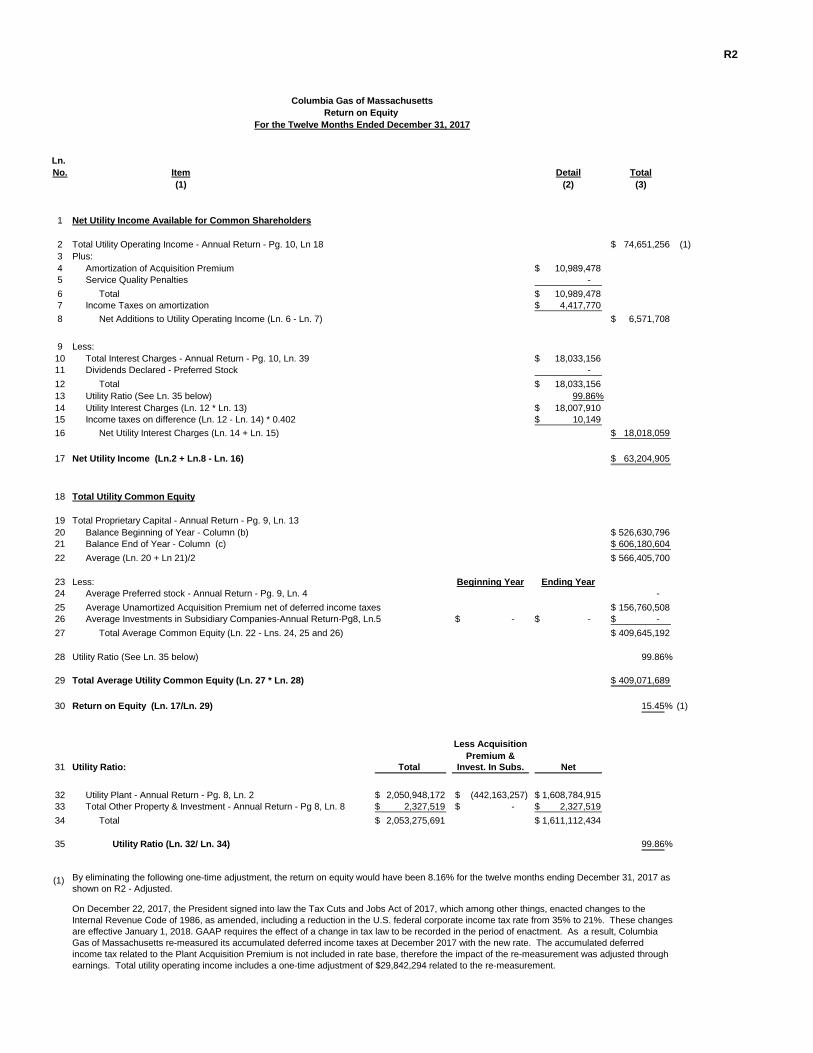

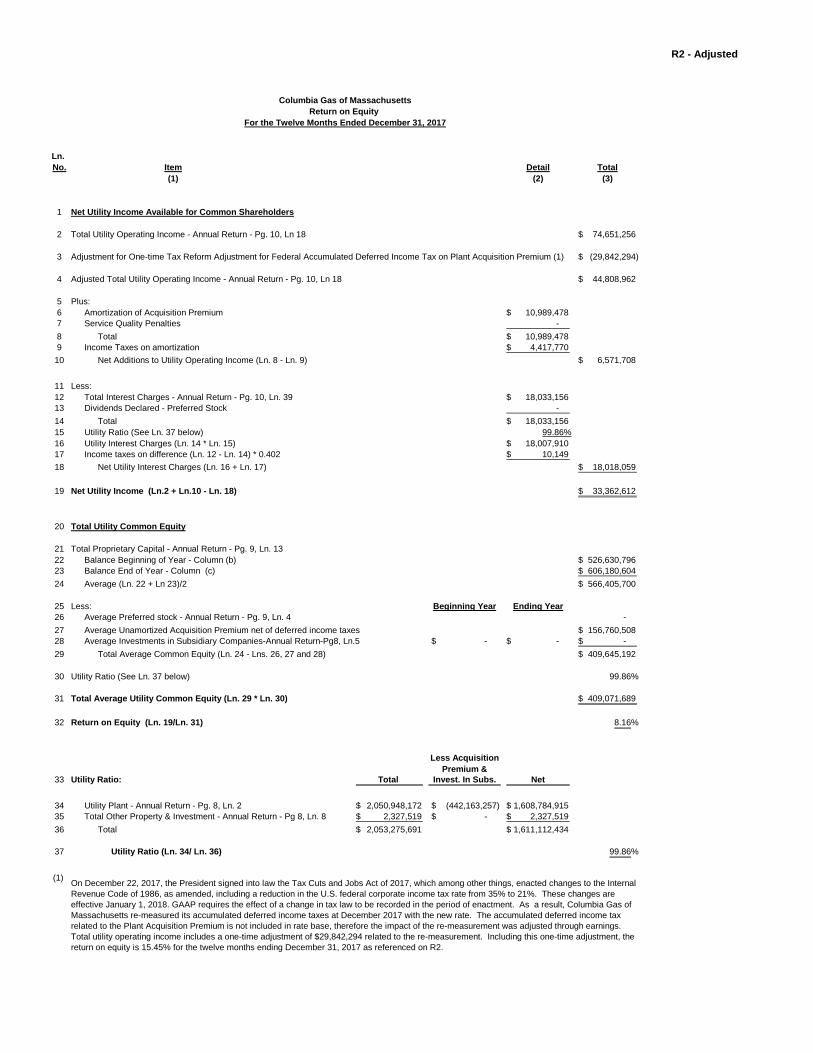

R2

Ln. No. Detail Total

(2) (3)

1 Net Utility Income Available for Common Shareholders

2 Total Utility Operating Income - Annual Return - Pg. 10, Ln 18 74,651,256$ (1)3 Plus:4 Amortization of Acquisition Premium 10,989,478$ 5 Service Quality Penalties - 6 Total 10,989,478$ 7 Income Taxes on amortization 4,417,770$ 8 Net Additions to Utility Operating Income (Ln. 6 - Ln. 7) 6,571,708$

9 Less:10 Total Interest Charges - Annual Return - Pg. 10, Ln. 39 18,033,156$ 11 Dividends Declared - Preferred Stock - 12 Total 18,033,156$ 13 Utility Ratio (See Ln. 35 below) 99.86%14 Utility Interest Charges (Ln. 12 * Ln. 13) 18,007,910$ 15 Income taxes on difference (Ln. 12 - Ln. 14) * 0.402 10,149$ 16 Net Utility Interest Charges (Ln. 14 + Ln. 15) 18,018,059$

17 Net Utility Income (Ln.2 + Ln.8 - Ln. 16) 63,204,905$

18 Total Utility Common Equity

19 Total Proprietary Capital - Annual Return - Pg. 9, Ln. 1320 Balance Beginning of Year - Column (b) 526,630,796$ 21 Balance End of Year - Column (c) 606,180,604$ 22 Average (Ln. 20 + Ln 21)/2 566,405,700$

23 Less: Beginning Year Ending Year24 Average Preferred stock - Annual Return - Pg. 9, Ln. 4 - 25 Average Unamortized Acquisition Premium net of deferred income taxes 156,760,508$ 26 Average Investments in Subsidiary Companies-Annual Return-Pg8, Ln.5 -$ -$ -$ 27 Total Average Common Equity (Ln. 22 - Lns. 24, 25 and 26) 409,645,192$

28 Utility Ratio (See Ln. 35 below) 99.86%

29 Total Average Utility Common Equity (Ln. 27 * Ln. 28) 409,071,689$

30 Return on Equity (Ln. 17/Ln. 29) 15.45% (1)

Less AcquisitionPremium &

31 Utility Ratio: Total Invest. In Subs. Net

32 Utility Plant - Annual Return - Pg. 8, Ln. 2 2,050,948,172$ (442,163,257)$ 1,608,784,915$ 33 Total Other Property & Investment - Annual Return - Pg 8, Ln. 8 2,327,519$ -$ 2,327,519$ 34 Total 2,053,275,691$ 1,611,112,434$

35 Utility Ratio (Ln. 32/ Ln. 34) 99.86%

(1)

On December 22, 2017, the President signed into law the Tax Cuts and Jobs Act of 2017, which among other things, enacted changes to the Internal Revenue Code of 1986, as amended, including a reduction in the U.S. federal corporate income tax rate from 35% to 21%. These changes are effective January 1, 2018. GAAP requires the effect of a change in tax law to be recorded in the period of enactment. As a result, Columbia Gas of Massachusetts re-measured its accumulated deferred income taxes at December 2017 with the new rate. The accumulated deferred income tax related to the Plant Acquisition Premium is not included in rate base, therefore the impact of the re-measurement was adjusted through earnings. Total utility operating income includes a one-time adjustment of $29,842,294 related to the re-measurement.

Columbia Gas of MassachusettsReturn on Equity

For the Twelve Months Ended December 31, 2017

Item(1)

By eliminating the following one-time adjustment, the return on equity would have been 8.16% for the twelve months ending December 31, 2017 as shown on R2 - Adjusted.

R2 - Adjusted

Ln. No. Detail Total

(2) (3)

1 Net Utility Income Available for Common Shareholders

2 Total Utility Operating Income - Annual Return - Pg. 10, Ln 18 74,651,256$

3 Adjustment for One-time Tax Reform Adjustment for Federal Accumulated Deferred Income Tax on Plant Acquisition Premium (1) (29,842,294)$

4 Adjusted Total Utility Operating Income - Annual Return - Pg. 10, Ln 18 44,808,962$

5 Plus:6 Amortization of Acquisition Premium 10,989,478$ 7 Service Quality Penalties - 8 Total 10,989,478$ 9 Income Taxes on amortization 4,417,770$ 10 Net Additions to Utility Operating Income (Ln. 8 - Ln. 9) 6,571,708$

11 Less:12 Total Interest Charges - Annual Return - Pg. 10, Ln. 39 18,033,156$ 13 Dividends Declared - Preferred Stock - 14 Total 18,033,156$ 15 Utility Ratio (See Ln. 37 below) 99.86%16 Utility Interest Charges (Ln. 14 * Ln. 15) 18,007,910$ 17 Income taxes on difference (Ln. 12 - Ln. 14) * 0.402 10,149$ 18 Net Utility Interest Charges (Ln. 16 + Ln. 17) 18,018,059$

19 Net Utility Income (Ln.2 + Ln.10 - Ln. 18) 33,362,612$

20 Total Utility Common Equity

21 Total Proprietary Capital - Annual Return - Pg. 9, Ln. 1322 Balance Beginning of Year - Column (b) 526,630,796$ 23 Balance End of Year - Column (c) 606,180,604$ 24 Average (Ln. 22 + Ln 23)/2 566,405,700$

25 Less: Beginning Year Ending Year26 Average Preferred stock - Annual Return - Pg. 9, Ln. 4 - 27 Average Unamortized Acquisition Premium net of deferred income taxes 156,760,508$ 28 Average Investments in Subsidiary Companies-Annual Return-Pg8, Ln.5 -$ -$ -$ 29 Total Average Common Equity (Ln. 24 - Lns. 26, 27 and 28) 409,645,192$

30 Utility Ratio (See Ln. 37 below) 99.86%

31 Total Average Utility Common Equity (Ln. 29 * Ln. 30) 409,071,689$

32 Return on Equity (Ln. 19/Ln. 31) 8.16%

Less AcquisitionPremium &

33 Utility Ratio: Total Invest. In Subs. Net

34 Utility Plant - Annual Return - Pg. 8, Ln. 2 2,050,948,172$ (442,163,257)$ 1,608,784,915$ 35 Total Other Property & Investment - Annual Return - Pg 8, Ln. 8 2,327,519$ -$ 2,327,519$ 36 Total 2,053,275,691$ 1,611,112,434$

37 Utility Ratio (Ln. 34/ Ln. 36) 99.86%

(1) On December 22, 2017, the President signed into law the Tax Cuts and Jobs Act of 2017, which among other things, enacted changes to the Internal Revenue Code of 1986, as amended, including a reduction in the U.S. federal corporate income tax rate from 35% to 21%. These changes are effective January 1, 2018. GAAP requires the effect of a change in tax law to be recorded in the period of enactment. As a result, Columbia Gas of Massachusetts re-measured its accumulated deferred income taxes at December 2017 with the new rate. The accumulated deferred income tax related to the Plant Acquisition Premium is not included in rate base, therefore the impact of the re-measurement was adjusted through earnings. Total utility operating income includes a one-time adjustment of $29,842,294 related to the re-measurement. Including this one-time adjustment, the return on equity is 15.45% for the twelve months ending December 31, 2017 as referenced on R2.

Columbia Gas of MassachusettsReturn on Equity

For the Twelve Months Ended December 31, 2017

Item(1)

2

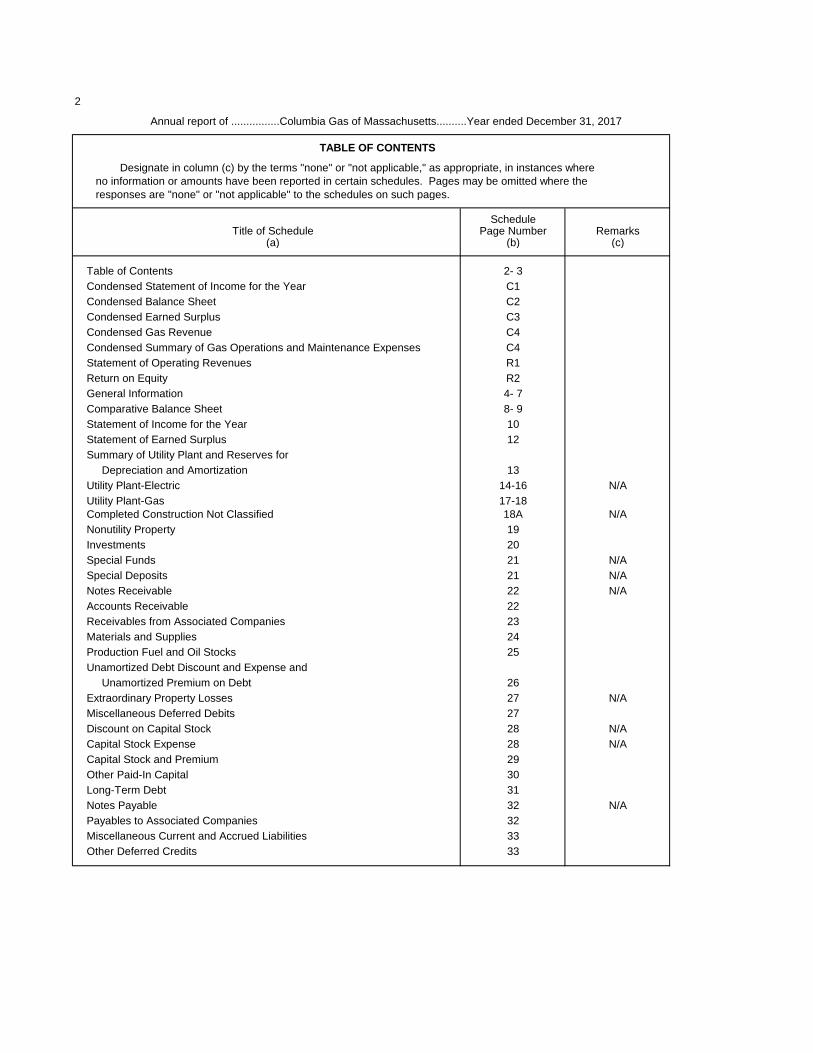

Annual report of ................Columbia Gas of Massachusetts..........Year ended December 31, 2017

TABLE OF CONTENTS

Designate in column (c) by the terms "none" or "not applicable," as appropriate, in instances where no information or amounts have been reported in certain schedules. Pages may be omitted where the responses are "none" or "not applicable" to the schedules on such pages.

ScheduleTitle of Schedule Page Number Remarks

(a) (b) (c)

Table of Contents 2- 3Condensed Statement of Income for the Year C1Condensed Balance Sheet C2Condensed Earned Surplus C3Condensed Gas Revenue C4Condensed Summary of Gas Operations and Maintenance Expenses C4Statement of Operating Revenues R1Return on Equity R2General Information 4- 7Comparative Balance Sheet 8- 9Statement of Income for the Year 10Statement of Earned Surplus 12Summary of Utility Plant and Reserves for Depreciation and Amortization 13Utility Plant-Electric 14-16 N/AUtility Plant-Gas 17-18Completed Construction Not Classified 18A N/ANonutility Property 19Investments 20Special Funds 21 N/ASpecial Deposits 21 N/ANotes Receivable 22 N/AAccounts Receivable 22Receivables from Associated Companies 23Materials and Supplies 24Production Fuel and Oil Stocks 25Unamortized Debt Discount and Expense and Unamortized Premium on Debt 26Extraordinary Property Losses 27 N/AMiscellaneous Deferred Debits 27Discount on Capital Stock 28 N/ACapital Stock Expense 28 N/ACapital Stock and Premium 29Other Paid-In Capital 30Long-Term Debt 31Notes Payable 32 N/APayables to Associated Companies 32Miscellaneous Current and Accrued Liabilities 33Other Deferred Credits 33

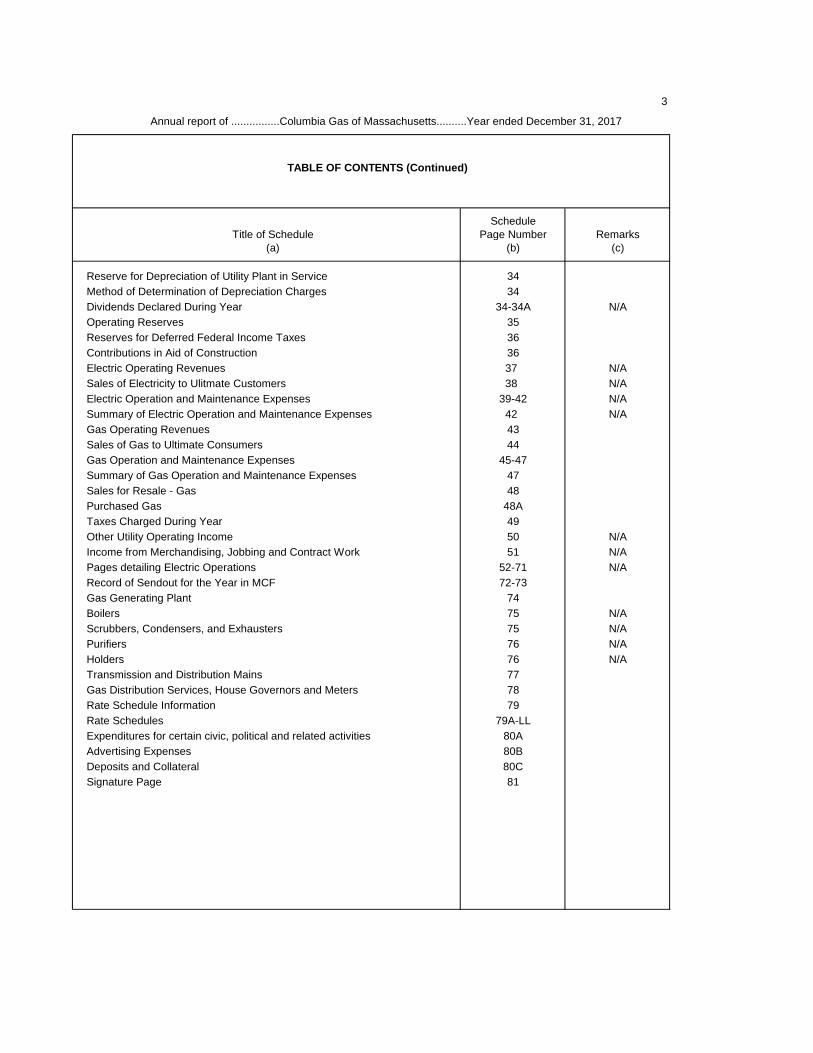

3

Annual report of ................Columbia Gas of Massachusetts..........Year ended December 31, 2017

TABLE OF CONTENTS (Continued)

ScheduleTitle of Schedule Page Number Remarks

(a) (b) (c)

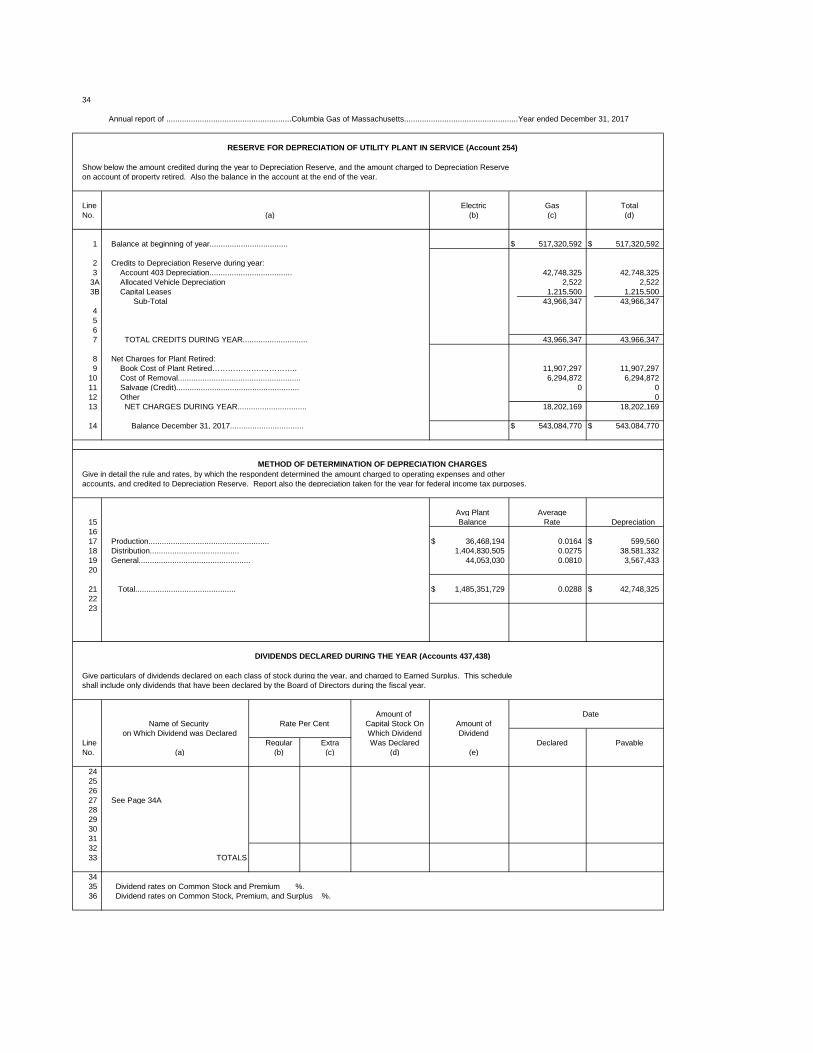

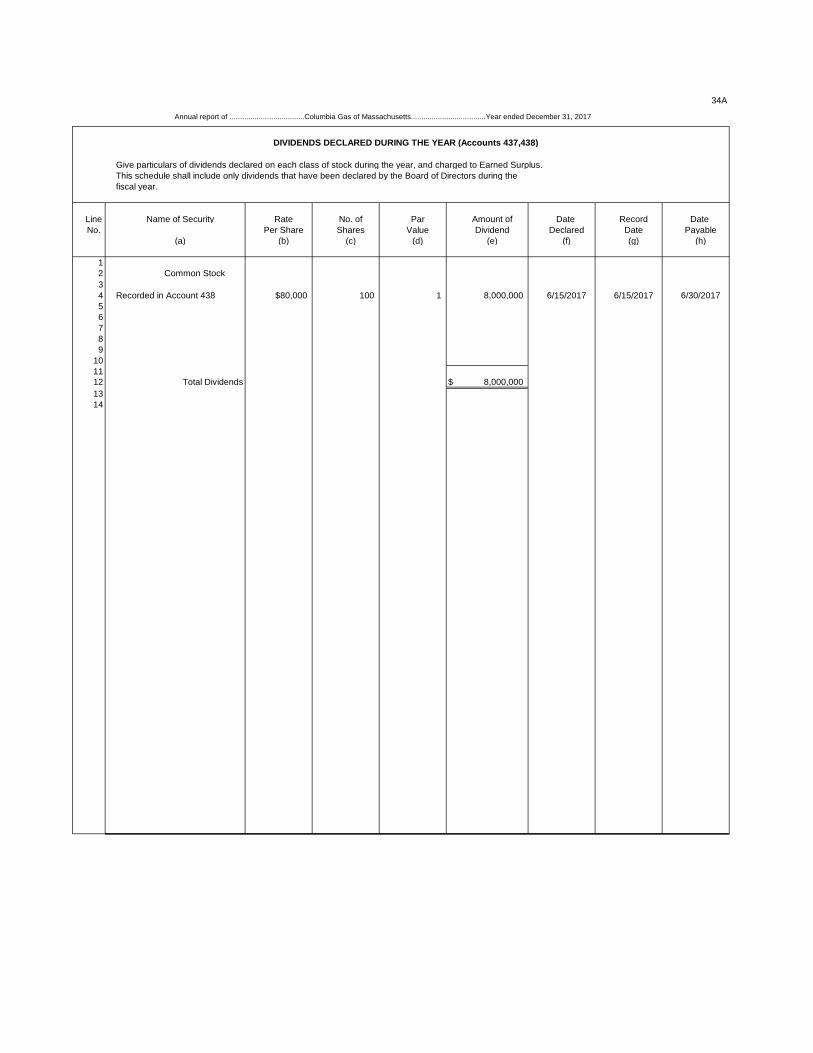

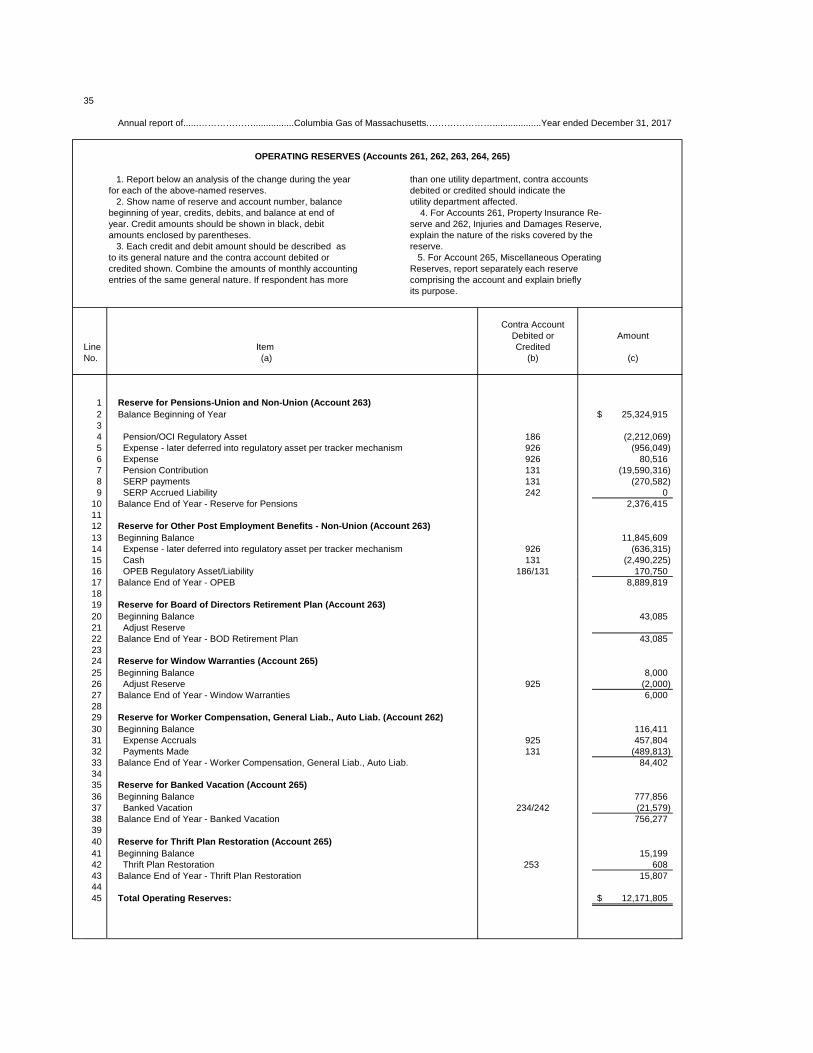

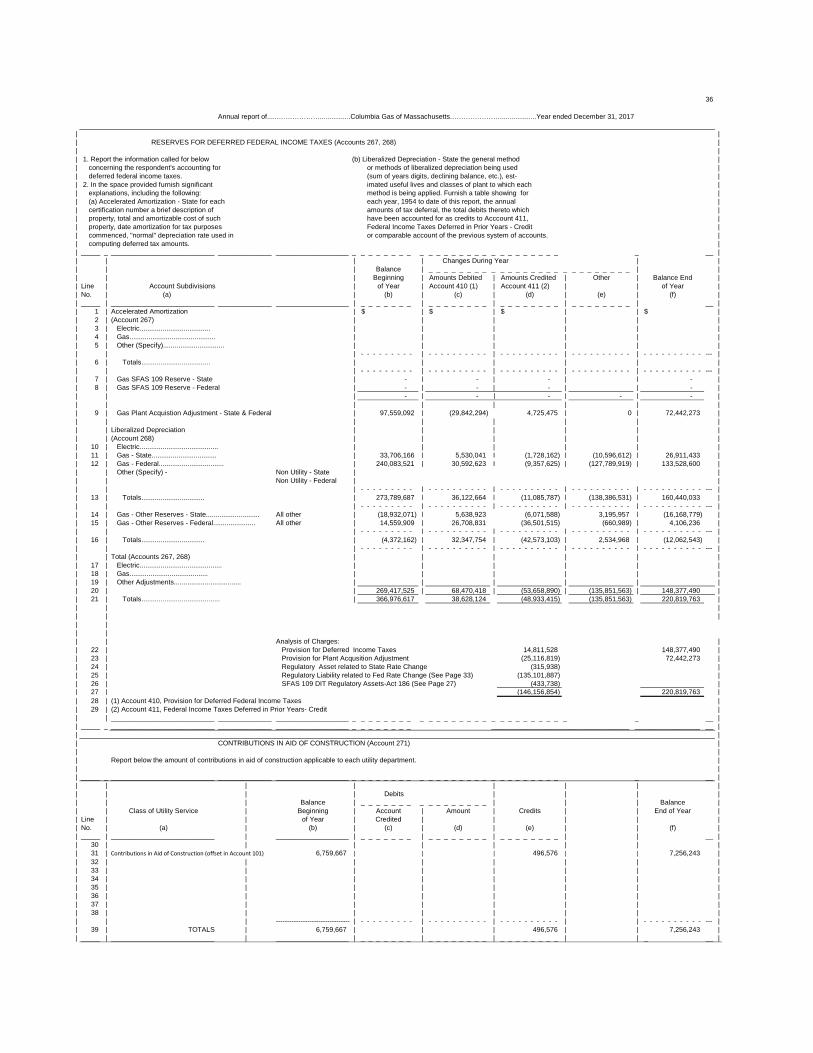

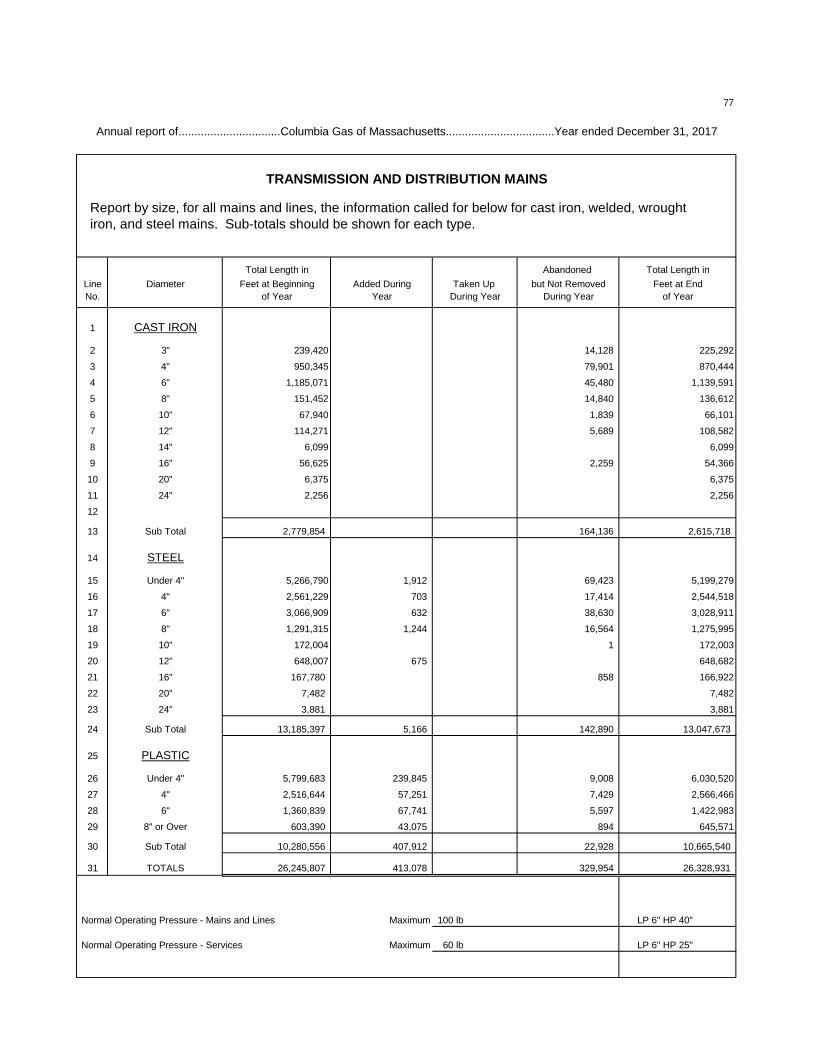

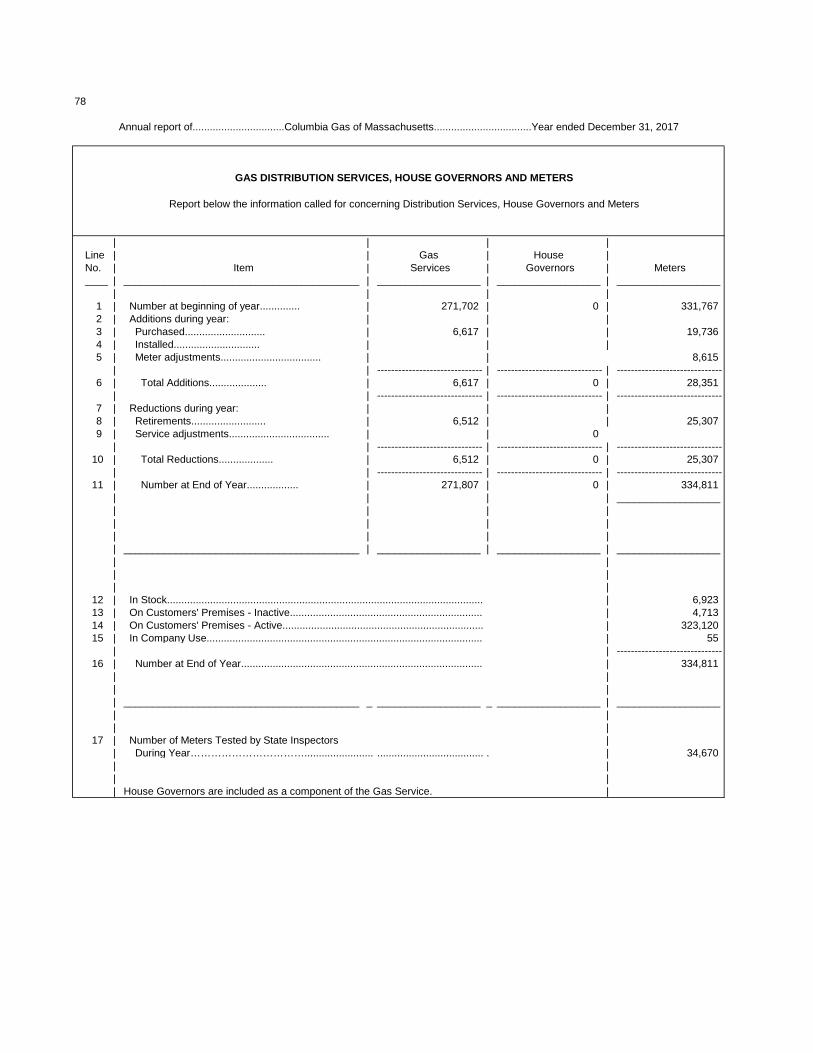

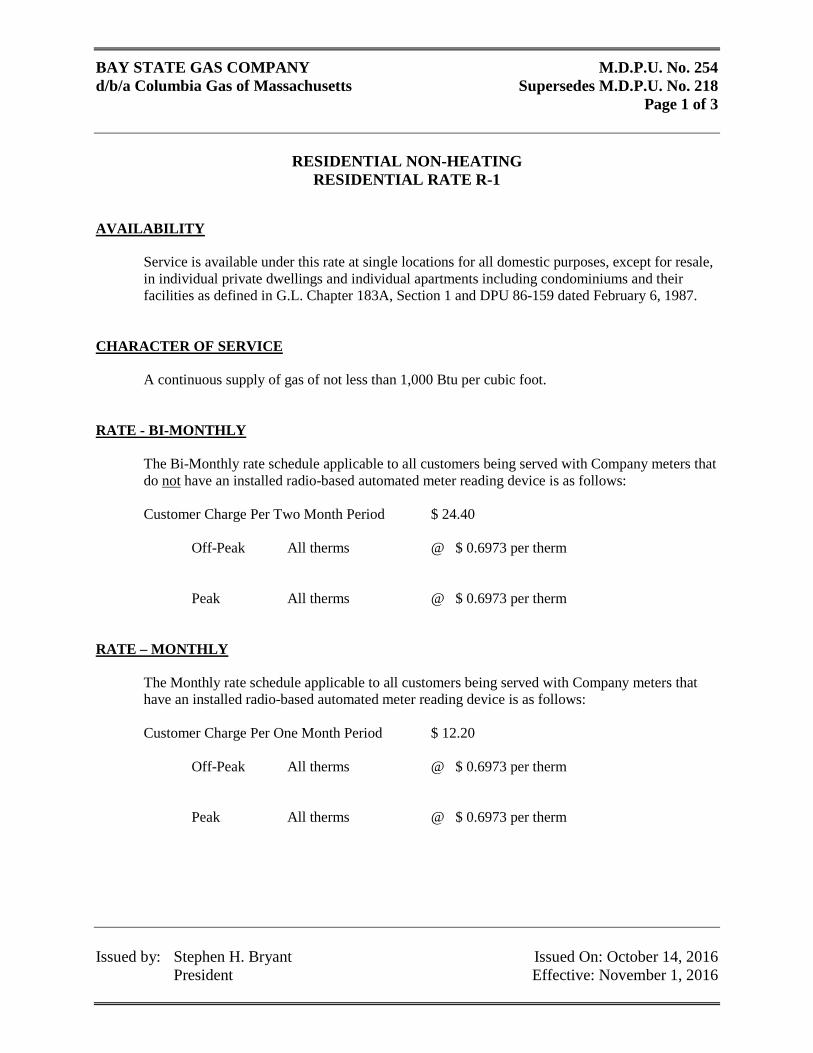

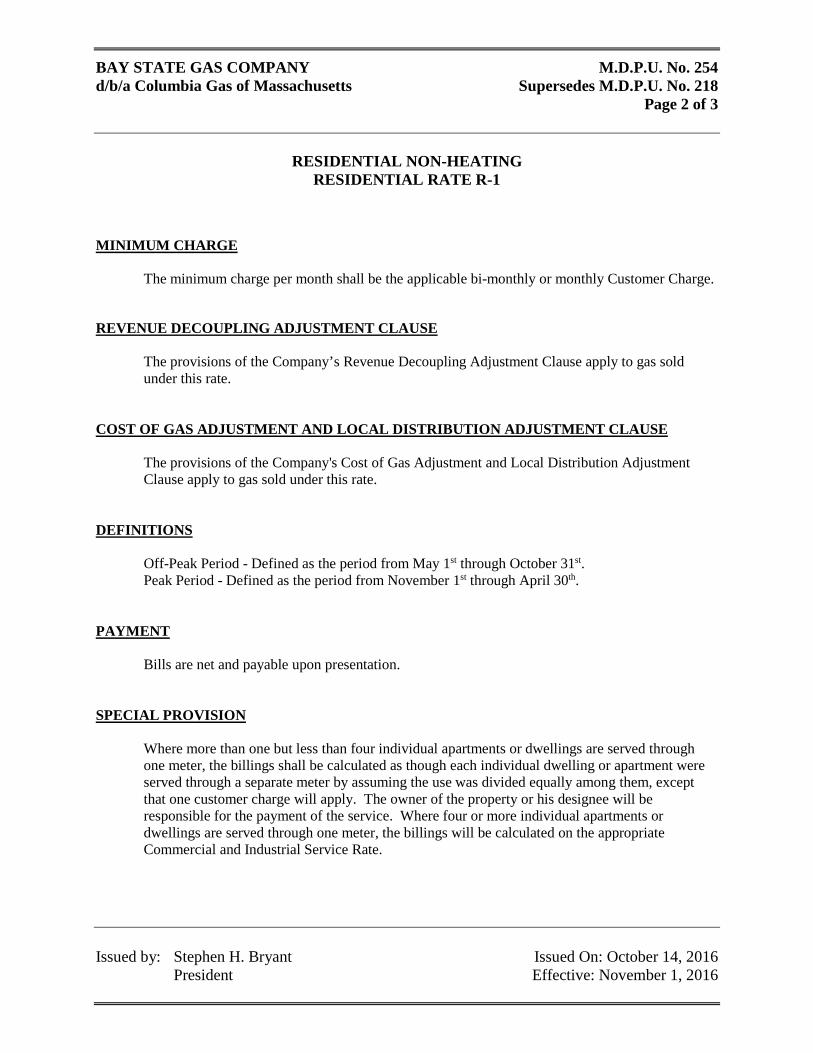

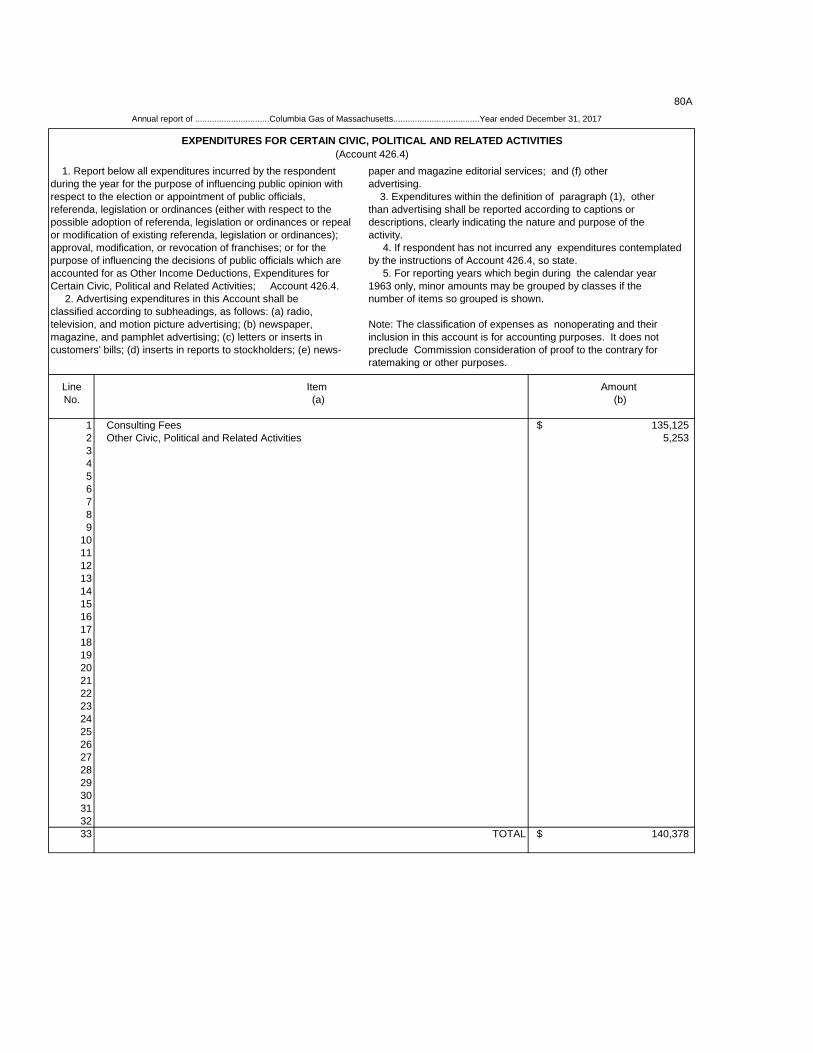

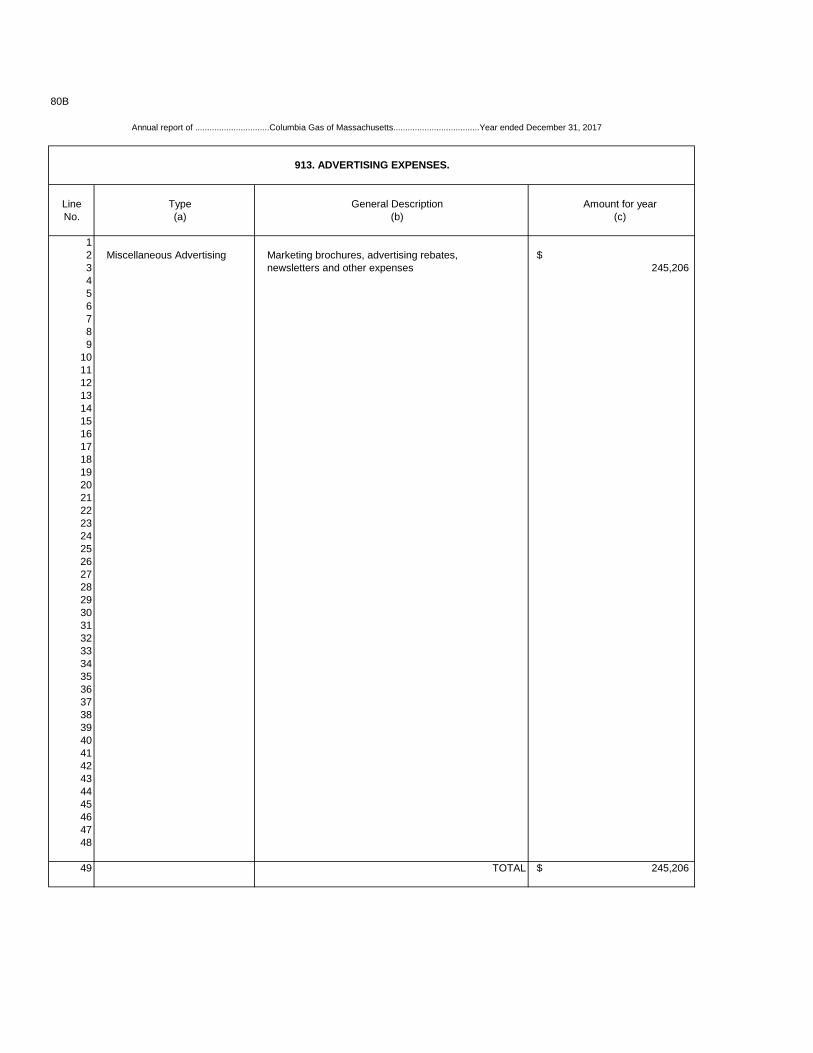

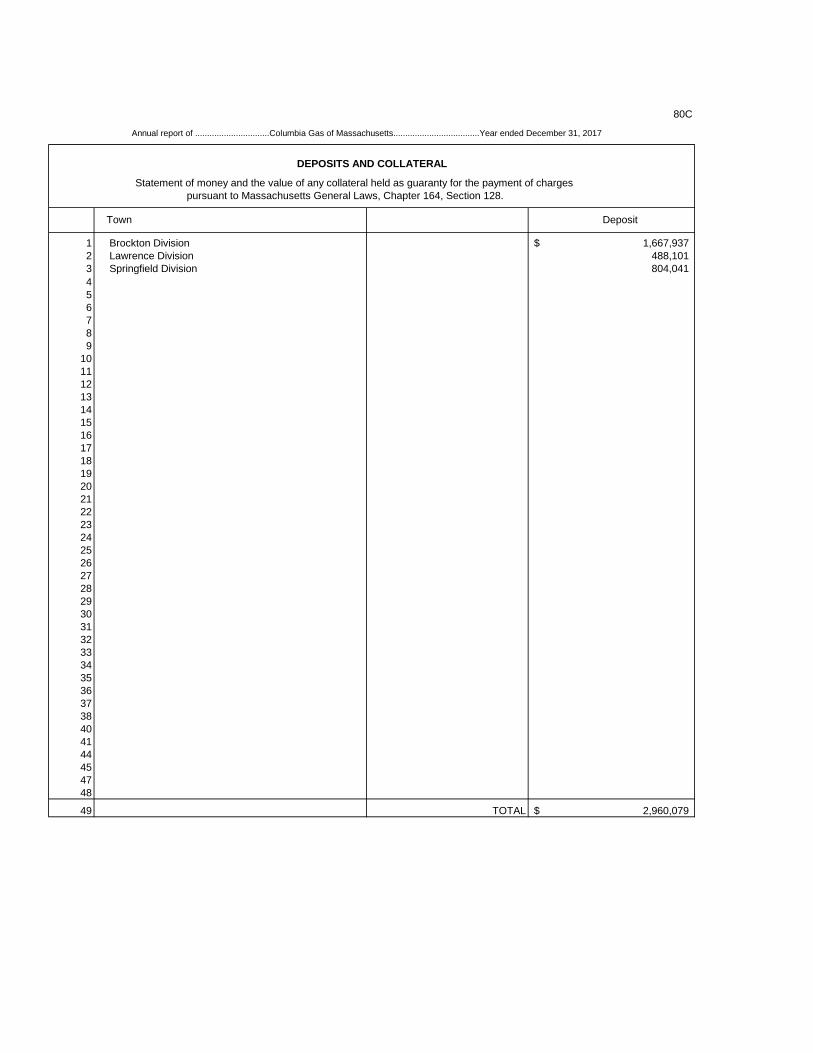

Reserve for Depreciation of Utility Plant in Service 34Method of Determination of Depreciation Charges 34Dividends Declared During Year 34-34A N/AOperating Reserves 35Reserves for Deferred Federal Income Taxes 36Contributions in Aid of Construction 36Electric Operating Revenues 37 N/ASales of Electricity to Ulitmate Customers 38 N/AElectric Operation and Maintenance Expenses 39-42 N/ASummary of Electric Operation and Maintenance Expenses 42 N/AGas Operating Revenues 43Sales of Gas to Ultimate Consumers 44Gas Operation and Maintenance Expenses 45-47Summary of Gas Operation and Maintenance Expenses 47Sales for Resale - Gas 48Purchased Gas 48ATaxes Charged During Year 49Other Utility Operating Income 50 N/AIncome from Merchandising, Jobbing and Contract Work 51 N/APages detailing Electric Operations 52-71 N/ARecord of Sendout for the Year in MCF 72-73Gas Generating Plant 74Boilers 75 N/AScrubbers, Condensers, and Exhausters 75 N/APurifiers 76 N/AHolders 76 N/ATransmission and Distribution Mains 77Gas Distribution Services, House Governors and Meters 78Rate Schedule Information 79Rate Schedules 79A-LLExpenditures for certain civic, political and related activities 80AAdvertising Expenses 80BDeposits and Collateral 80CSignature Page 81

4

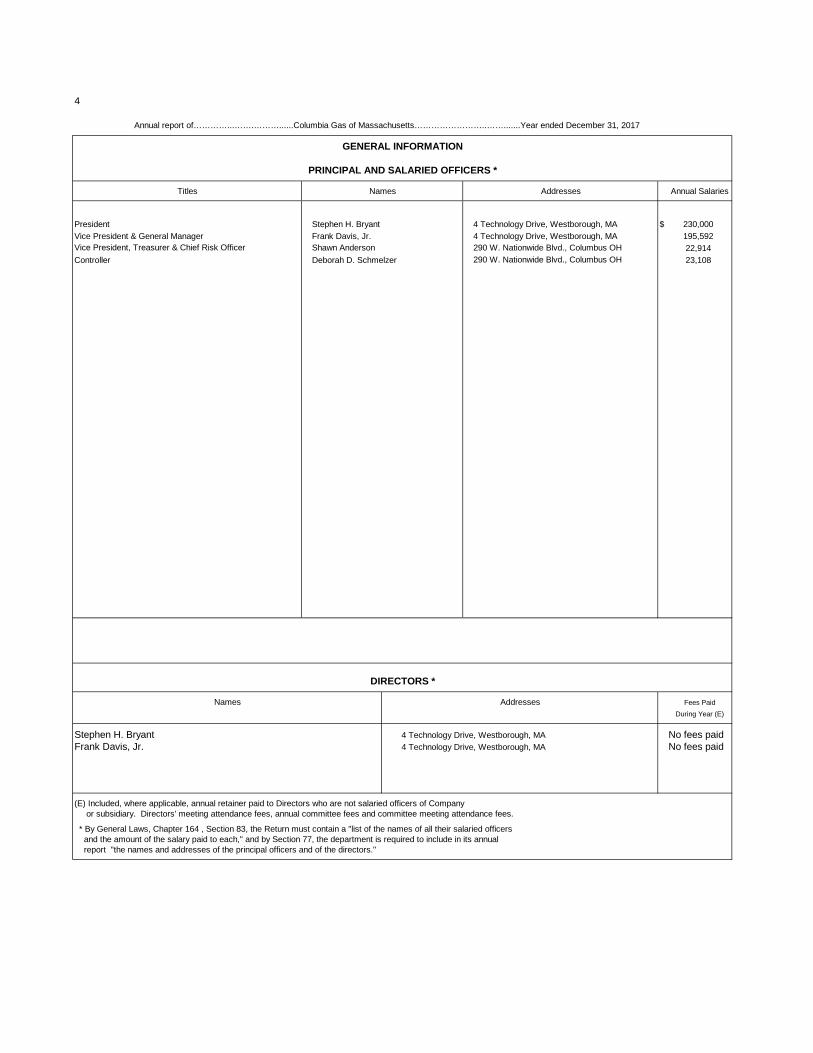

Annual report of…………...…….………......Columbia Gas of Massachusetts……………………..…….......Year ended December 31, 2017

GENERAL INFORMATION

PRINCIPAL AND SALARIED OFFICERS *

Titles Names Addresses Annual Salaries

President Stephen H. Bryant 4 Technology Drive, Westborough, MA $ 230,000Vice President & General Manager Frank Davis, Jr. 4 Technology Drive, Westborough, MA 195,592Vice President, Treasurer & Chief Risk Officer Shawn Anderson 290 W. Nationwide Blvd., Columbus OH 22,914Controller Deborah D. Schmelzer 290 W. Nationwide Blvd., Columbus OH 23,108

DIRECTORS *

Names Addresses Fees PaidDuring Year (E)

Stephen H. Bryant 4 Technology Drive, Westborough, MA No fees paidFrank Davis, Jr. 4 Technology Drive, Westborough, MA No fees paid

(E) Included, where applicable, annual retainer paid to Directors who are not salaried officers of Company or subsidiary. Directors' meeting attendance fees, annual committee fees and committee meeting attendance fees.

* By General Laws, Chapter 164 , Section 83, the Return must contain a "list of the names of all their salaried officers and the amount of the salary paid to each," and by Section 77, the department is required to include in its annual report "the names and addresses of the principal officers and of the directors."

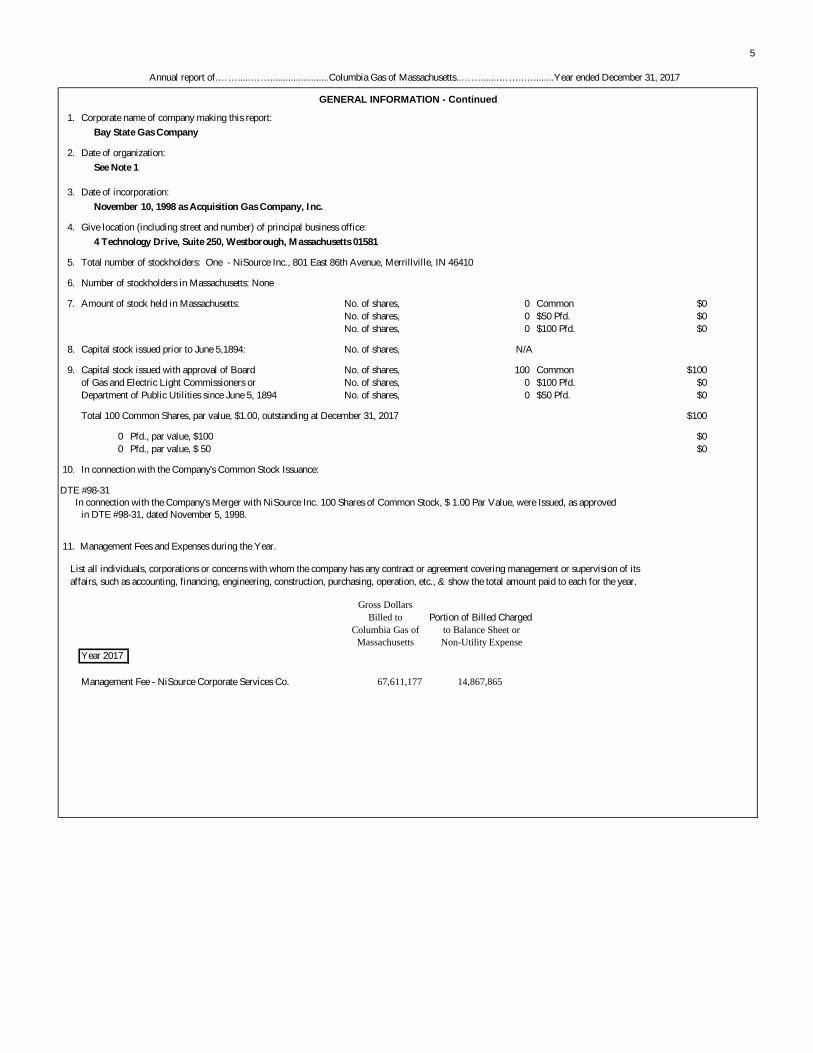

5

Annual report of.…….....…….......................Columbia Gas of Massachusetts..…….......……..…........Year ended December 31, 2017

GENERAL INFORMATION - Continued

1. Corporate name of company making this report: Bay State Gas Company

2. Date of organization: See Note 1

3. Date of incorporation: November 10, 1998 as Acquisition Gas Company, Inc.

4. Give location (including street and number) of principal business office: 4 Technology Drive, Suite 250, Westborough, Massachusetts 01581

5. Total number of stockholders: One - NiSource Inc., 801 East 86th Avenue, Merrillville, IN 46410

6. Number of stockholders in Massachusetts: None

7. Amount of stock held in Massachusetts: No. of shares, 0 Common $0No. of shares, 0 $50 Pfd. $0No. of shares, 0 $100 Pfd. $0

8. Capital stock issued prior to June 5,1894: No. of shares, N/A

9. Capital stock issued with approval of Board No. of shares, 100 Common $100of Gas and Electric Light Commissioners or No. of shares, 0 $100 Pfd. $0Department of Public Utilities since June 5, 1894 No. of shares, 0 $50 Pfd. $0

Total 100 Common Shares, par value, $1.00, outstanding at December 31, 2017 $100

0 Pfd., par value, $100 $00 Pfd., par value, $ 50 $0

10. In connection with the Company's Common Stock Issuance:

DTE #98-31 In connection with the Company's Merger with NiSource Inc. 100 Shares of Common Stock, $ 1.00 Par Value, were Issued, as approved

in DTE #98-31, dated November 5, 1998.

11. Management Fees and Expenses during the Year.

List all individuals, corporations or concerns with whom the company has any contract or agreement covering management or supervision of its affairs, such as accounting, financing, engineering, construction, purchasing, operation, etc., & show the total amount paid to each for the year.

Gross DollarsBilled to Portion of Billed Charged

Columbia Gas of to Balance Sheet orMassachusetts Non-Utility Expense

Year 2017

Management Fee - NiSource Corporate Services Co. 67,611,177 14,867,865

6

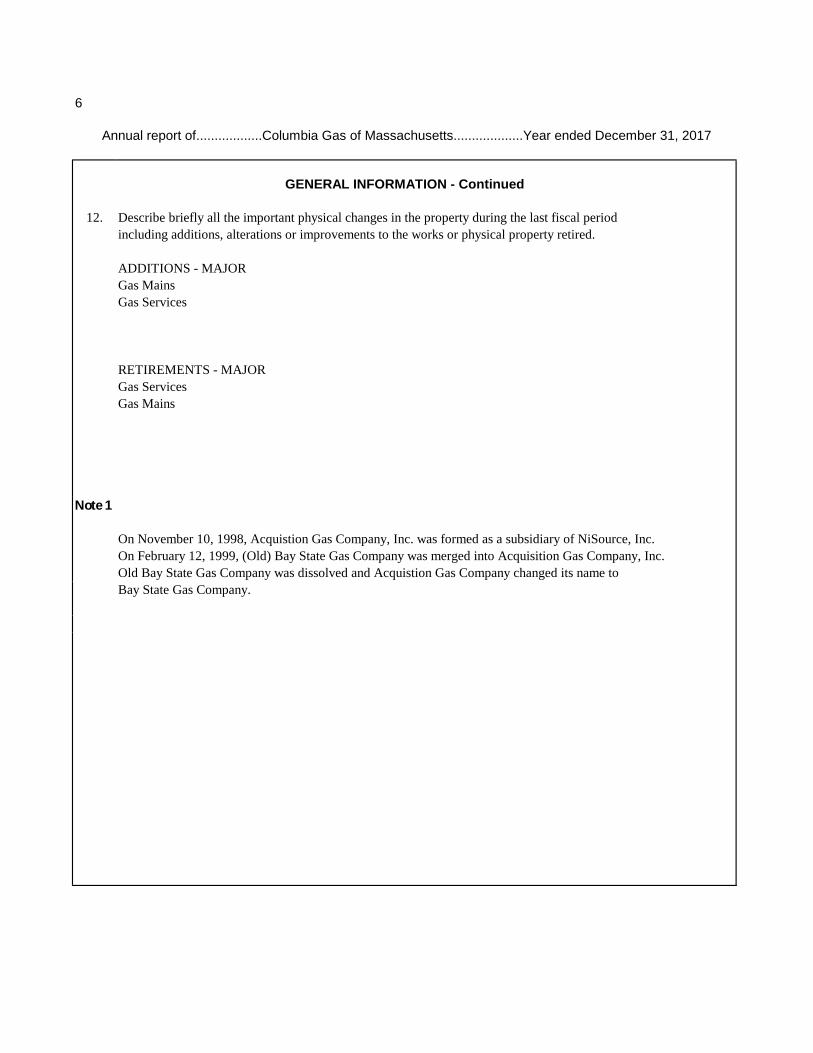

GENERAL INFORMATION - Continued

12. Describe briefly all the important physical changes in the property during the last fiscal periodincluding additions, alterations or improvements to the works or physical property retired.

ADDITIONS - MAJORGas MainsGas Services

RETIREMENTS - MAJORGas ServicesGas Mains

Note 1

On November 10, 1998, Acquistion Gas Company, Inc. was formed as a subsidiary of NiSource, Inc.On February 12, 1999, (Old) Bay State Gas Company was merged into Acquisition Gas Company, Inc.Old Bay State Gas Company was dissolved and Acquistion Gas Company changed its name toBay State Gas Company.

Annual report of..................Columbia Gas of Massachusetts...................Year ended December 31, 2017

7

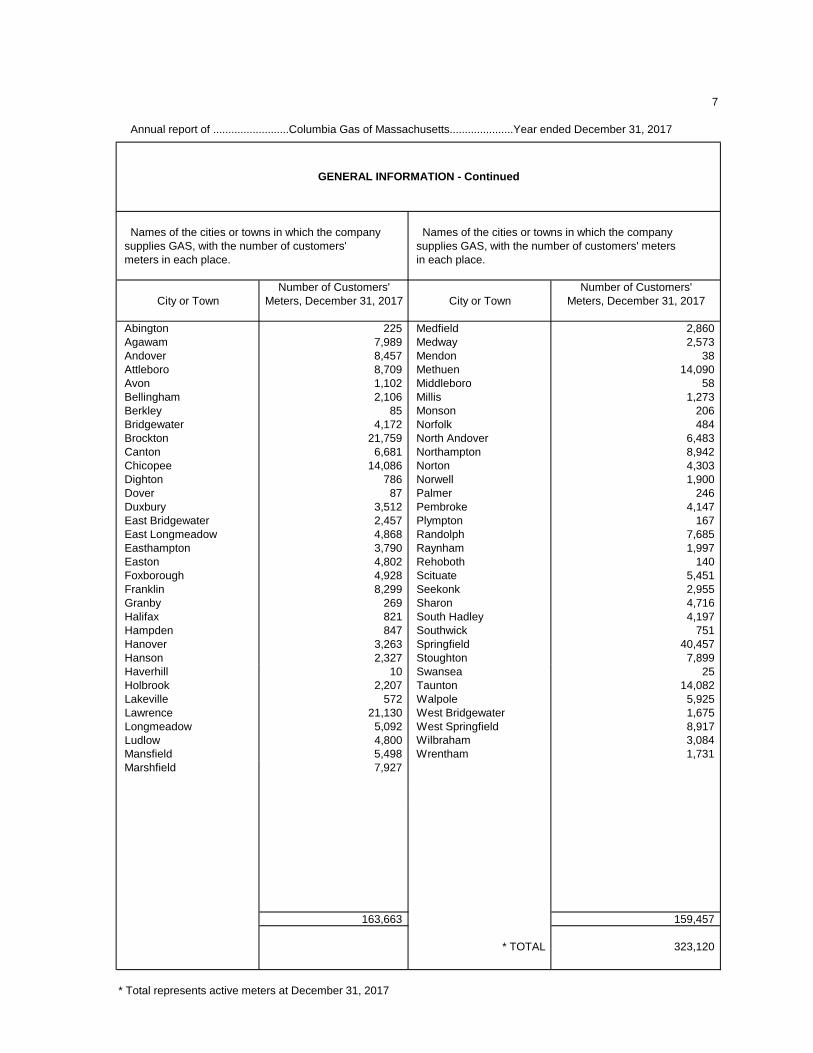

Annual report of .........................Columbia Gas of Massachusetts.....................Year ended December 31, 2017

GENERAL INFORMATION - Continued

Names of the cities or towns in which the company Names of the cities or towns in which the company supplies GAS, with the number of customers' supplies GAS, with the number of customers' meters meters in each place. in each place.

Number of Customers' Number of Customers'City or Town Meters, December 31, 2017 City or Town Meters, December 31, 2017

Abington 225 Medfield 2,860 Agawam 7,989 Medway 2,573 Andover 8,457 Mendon 38 Attleboro 8,709 Methuen 14,090 Avon 1,102 Middleboro 58 Bellingham 2,106 Millis 1,273 Berkley 85 Monson 206 Bridgewater 4,172 Norfolk 484 Brockton 21,759 North Andover 6,483 Canton 6,681 Northampton 8,942 Chicopee 14,086 Norton 4,303 Dighton 786 Norwell 1,900 Dover 87 Palmer 246 Duxbury 3,512 Pembroke 4,147 East Bridgewater 2,457 Plympton 167 East Longmeadow 4,868 Randolph 7,685 Easthampton 3,790 Raynham 1,997 Easton 4,802 Rehoboth 140 Foxborough 4,928 Scituate 5,451 Franklin 8,299 Seekonk 2,955 Granby 269 Sharon 4,716 Halifax 821 South Hadley 4,197 Hampden 847 Southwick 751 Hanover 3,263 Springfield 40,457 Hanson 2,327 Stoughton 7,899 Haverhill 10 Swansea 25 Holbrook 2,207 Taunton 14,082 Lakeville 572 Walpole 5,925 Lawrence 21,130 West Bridgewater 1,675 Longmeadow 5,092 West Springfield 8,917 Ludlow 4,800 Wilbraham 3,084 Mansfield 5,498 Wrentham 1,731 Marshfield 7,927

163,663 159,457

* TOTAL 323,120

* Total represents active meters at December 31, 2017

8

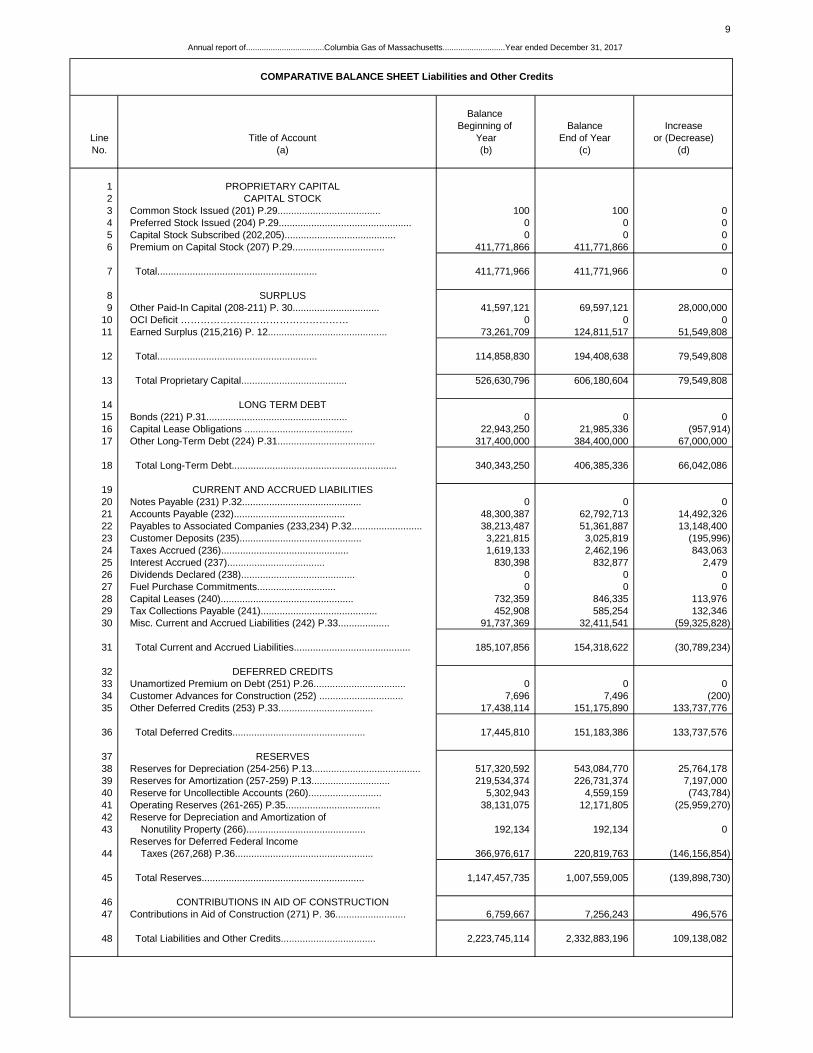

Annual report of............................................Columbia Gas of Massachusetts............................................Year ended December 31, 2017

COMPARATIVE BALANCE SHEET Assets and Other Debits

BalanceBeginning of Balance End Increase

Line Title of Account Year of Year or (Decrease)No. (a) (b) (c) (d)

1 UTILITY PLANT2 Utility Plant (101-107) P.13 ................................. 1,943,128,983 2,050,948,172 107,819,189

3 OTHER PROPERTY AND INVESTMENTS4 Nonutility Property (121) P.19............................................ 226,850 226,850 05 Investment in Associated Companies (123) P.20.......................... 0 0 06 Other Investments (124) P.20.................................................... 25,000 25,000 07 Special Funds (125,126,127,128) P.21...................................... 0 2,075,669 2,075,669

8 Total Other Property and Investments...................................... 251,850 2,327,519 2,075,669

9 CURRENT AND ACCRUED ASSETS10 Cash (131)................................................................ 3,820,299 3,933,436 113,13711 Special Deposits (132,133,134) P.21..................................... 0 0 012 Working Funds (135)....................................................... 1,200 1,200 013 Temporary Cash Investments (136) P.20...................................... 0 0 014 Notes and Accounts Receivable (141,142,143) P.22........................ 77,025,320 73,903,213 (3,122,107)15 Receivables from Assoc. Companies (145,146) P.23......................... 247,239 244,401 (2,838)16 Materials and Supplies (151-159,163) P.24.............................. 14,791,567 15,104,112 312,54517 Prepayments (165)................................................... 2,104,366 2,119,035 14,66918 Interest and Dividends Receivable (171)........................................ 0 0 019 Rents Receivable (172)..................................................... 0 0 020 Accrued Utility Revenues (173).......................................... 43,688,875 54,476,932 10,788,05721 Miscellaneous Current and Accrued Assets (174) 0 0 022 Def. Fuel Costs (175)............................................ 0 5,896,143 5,896,143

23 Total Current and Accrued Assets........................................ 141,678,866 155,678,472 13,999,606

24 DEFERRED DEBITS25 Unamortized Debt Discount and Expense (181) P.26..................... 2,780,230 2,515,042 (265,188)26 Extraordinary Property Losses (182) P.27............................... 0 0 027 Preliminary Survey and Investigation Charges (183).................... 882,387 581,912 (300,475)28 Clearing Accounts (184).................................................. 0 0 029 Temporary Facilities (185).......................................... 0 0 030 Miscellaneous Deferred Debits (186)...P.27........................ 135,022,798 120,832,079 (14,190,719)

31 Total Deferred Debits..................................................... 138,685,415 123,929,033 (14,756,382)

32 CAPITAL STOCK DISCOUNT AND EXPENSE33 Discount on Capital Stock (191) P.28....................................... 0 0 034 Capital Stock Expense (192) P.28......................................... 0 0 0

35 Total Capital Stock Discount and Expense......................... 0 0 0

36 REACQUIRED SECURITIES37 Reacquired Capital Stock (196)....................................... 0 0 038 Reacquired Bonds (197)............................................... 0 0 0

39 Total Reacquired Securities.............................................. 0 0 0

40 Total Assets and Other Debits..................................... 2,223,745,114 2,332,883,196 109,138,082

9

Annual report of...................................Columbia Gas of Massachusetts............................Year ended December 31, 2017

COMPARATIVE BALANCE SHEET Liabilities and Other Credits

Balance Beginning of Balance Increase

Line Title of Account Year End of Year or (Decrease)No. (a) (b) (c) (d)

1 PROPRIETARY CAPITAL2 CAPITAL STOCK3 Common Stock Issued (201) P.29...................................... 100 100 04 Preferred Stock Issued (204) P.29................................................. 0 0 05 Capital Stock Subscribed (202,205)......................................... 0 0 06 Premium on Capital Stock (207) P.29.................................. 411,771,866 411,771,866 0

7 Total........................................................... 411,771,966 411,771,966 0

8 SURPLUS9 Other Paid-In Capital (208-211) P. 30................................ 41,597,121 69,597,121 28,000,000

10 OCI Deficit …………………………………………… 0 0 011 Earned Surplus (215,216) P. 12............................................ 73,261,709 124,811,517 51,549,808

12 Total........................................................... 114,858,830 194,408,638 79,549,808

13 Total Proprietary Capital....................................... 526,630,796 606,180,604 79,549,808

14 LONG TERM DEBT15 Bonds (221) P.31.................................................... 0 0 016 Capital Lease Obligations ........................................ 22,943,250 21,985,336 (957,914)17 Other Long-Term Debt (224) P.31.................................... 317,400,000 384,400,000 67,000,000

18 Total Long-Term Debt............................................................. 340,343,250 406,385,336 66,042,086

19 CURRENT AND ACCRUED LIABILITIES20 Notes Payable (231) P.32............................................ 0 0 021 Accounts Payable (232)......................................... 48,300,387 62,792,713 14,492,32622 Payables to Associated Companies (233,234) P.32.......................... 38,213,487 51,361,887 13,148,40023 Customer Deposits (235)............................................. 3,221,815 3,025,819 (195,996)24 Taxes Accrued (236)............................................... 1,619,133 2,462,196 843,06325 Interest Accrued (237).................................... 830,398 832,877 2,47926 Dividends Declared (238).......................................... 0 0 027 Fuel Purchase Commitments............................. 0 0 028 Capital Leases (240)................................................. 732,359 846,335 113,97629 Tax Collections Payable (241)........................................... 452,908 585,254 132,34630 Misc. Current and Accrued Liabilities (242) P.33................... 91,737,369 32,411,541 (59,325,828)

31 Total Current and Accrued Liabilities........................................... 185,107,856 154,318,622 (30,789,234)

32 DEFERRED CREDITS33 Unamortized Premium on Debt (251) P.26.................................. 0 0 034 Customer Advances for Construction (252) ............................... 7,696 7,496 (200)35 Other Deferred Credits (253) P.33................................... 17,438,114 151,175,890 133,737,776

36 Total Deferred Credits................................................. 17,445,810 151,183,386 133,737,576

37 RESERVES38 Reserves for Depreciation (254-256) P.13........................................ 517,320,592 543,084,770 25,764,17839 Reserves for Amortization (257-259) P.13............................. 219,534,374 226,731,374 7,197,00040 Reserve for Uncollectible Accounts (260)........................... 5,302,943 4,559,159 (743,784)41 Operating Reserves (261-265) P.35................................... 38,131,075 12,171,805 (25,959,270)42 Reserve for Depreciation and Amortization of43 Nonutility Property (266)............................................ 192,134 192,134 0

Reserves for Deferred Federal Income44 Taxes (267,268) P.36................................................... 366,976,617 220,819,763 (146,156,854)

45 Total Reserves............................................................ 1,147,457,735 1,007,559,005 (139,898,730)

46 CONTRIBUTIONS IN AID OF CONSTRUCTION47 Contributions in Aid of Construction (271) P. 36.......................... 6,759,667 7,256,243 496,576

48 Total Liabilities and Other Credits................................... 2,223,745,114 2,332,883,196 109,138,082

10

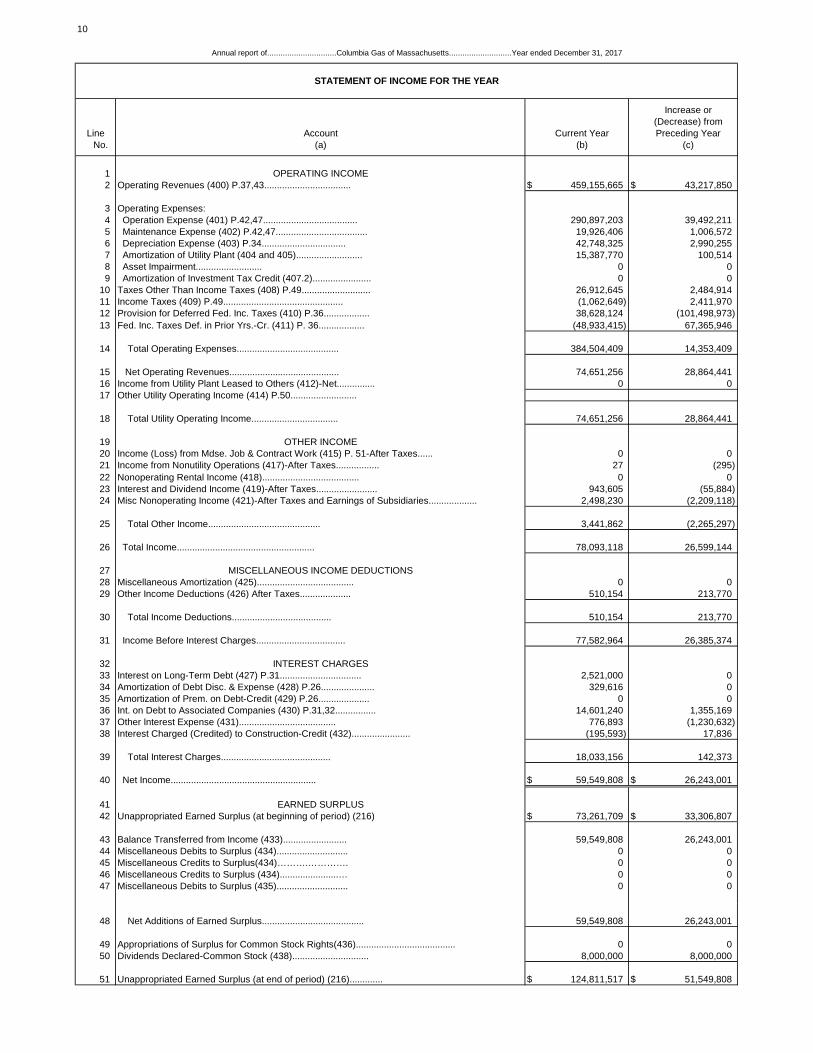

Annual report of...............................Columbia Gas of Massachusetts............................Year ended December 31, 2017

STATEMENT OF INCOME FOR THE YEAR

Increase or(Decrease) from

Line Account Current Year Preceding YearNo. (a) (b) (c)

1 OPERATING INCOME 2 Operating Revenues (400) P.37,43.................................. $ 459,155,665 $ 43,217,850

3 Operating Expenses:4 Operation Expense (401) P.42,47..................................... 290,897,203 39,492,2115 Maintenance Expense (402) P.42,47.................................... 19,926,406 1,006,5726 Depreciation Expense (403) P.34................................. 42,748,325 2,990,2557 Amortization of Utility Plant (404 and 405).......................... 15,387,770 100,5148 Asset Impairment.......................... 0 09 Amortization of Investment Tax Credit (407.2)....................... 0 0

10 Taxes Other Than Income Taxes (408) P.49........................... 26,912,645 2,484,91411 Income Taxes (409) P.49............................................... (1,062,649) 2,411,97012 Provision for Deferred Fed. Inc. Taxes (410) P.36.................. 38,628,124 (101,498,973)13 Fed. Inc. Taxes Def. in Prior Yrs.-Cr. (411) P. 36.................. (48,933,415) 67,365,946

14 Total Operating Expenses........................................ 384,504,409 14,353,409

15 Net Operating Revenues........................................... 74,651,256 28,864,44116 Income from Utility Plant Leased to Others (412)-Net............... 0 017 Other Utility Operating Income (414) P.50..........................

18 Total Utility Operating Income.................................. 74,651,256 28,864,441

19 OTHER INCOME20 Income (Loss) from Mdse. Job & Contract Work (415) P. 51-After Taxes...... 0 021 Income from Nonutility Operations (417)-After Taxes................. 27 (295)22 Nonoperating Rental Income (418)...................................... 0 023 Interest and Dividend Income (419)-After Taxes........................ 943,605 (55,884)24 Misc Nonoperating Income (421)-After Taxes and Earnings of Subsidiaries................... 2,498,230 (2,209,118)

25 Total Other Income............................................ 3,441,862 (2,265,297)

26 Total Income...................................................... 78,093,118 26,599,144

27 MISCELLANEOUS INCOME DEDUCTIONS28 Miscellaneous Amortization (425)...................................... 0 029 Other Income Deductions (426) After Taxes.................... 510,154 213,770

30 Total Income Deductions....................................... 510,154 213,770

31 Income Before Interest Charges................................... 77,582,964 26,385,374

32 INTEREST CHARGES33 Interest on Long-Term Debt (427) P.31................................ 2,521,000 034 Amortization of Debt Disc. & Expense (428) P.26..................... 329,616 035 Amortization of Prem. on Debt-Credit (429) P.26.................... 0 036 Int. on Debt to Associated Companies (430) P.31,32................ 14,601,240 1,355,16937 Other Interest Expense (431)...................................... 776,893 (1,230,632)38 Interest Charged (Credited) to Construction-Credit (432)....................... (195,593) 17,836

39 Total Interest Charges........................................... 18,033,156 142,373

40 Net Income......................................................... $ 59,549,808 $ 26,243,001

41 EARNED SURPLUS42 Unappropriated Earned Surplus (at beginning of period) (216) $ 73,261,709 $ 33,306,807

43 Balance Transferred from Income (433)......................... 59,549,808 26,243,00144 Miscellaneous Debits to Surplus (434)............................ 0 045 Miscellaneous Credits to Surplus(434)……….…………. 0 046 Miscellaneous Credits to Surplus (434).......................… 0 047 Miscellaneous Debits to Surplus (435)............................ 0 0

48 Net Additions of Earned Surplus........................................ 59,549,808 26,243,001

49 Appropriations of Surplus for Common Stock Rights(436)....................................... 0 050 Dividends Declared-Common Stock (438).............................. 8,000,000 8,000,000

51 Unappropriated Earned Surplus (at end of period) (216)............. $ 124,811,517 $ 51,549,808

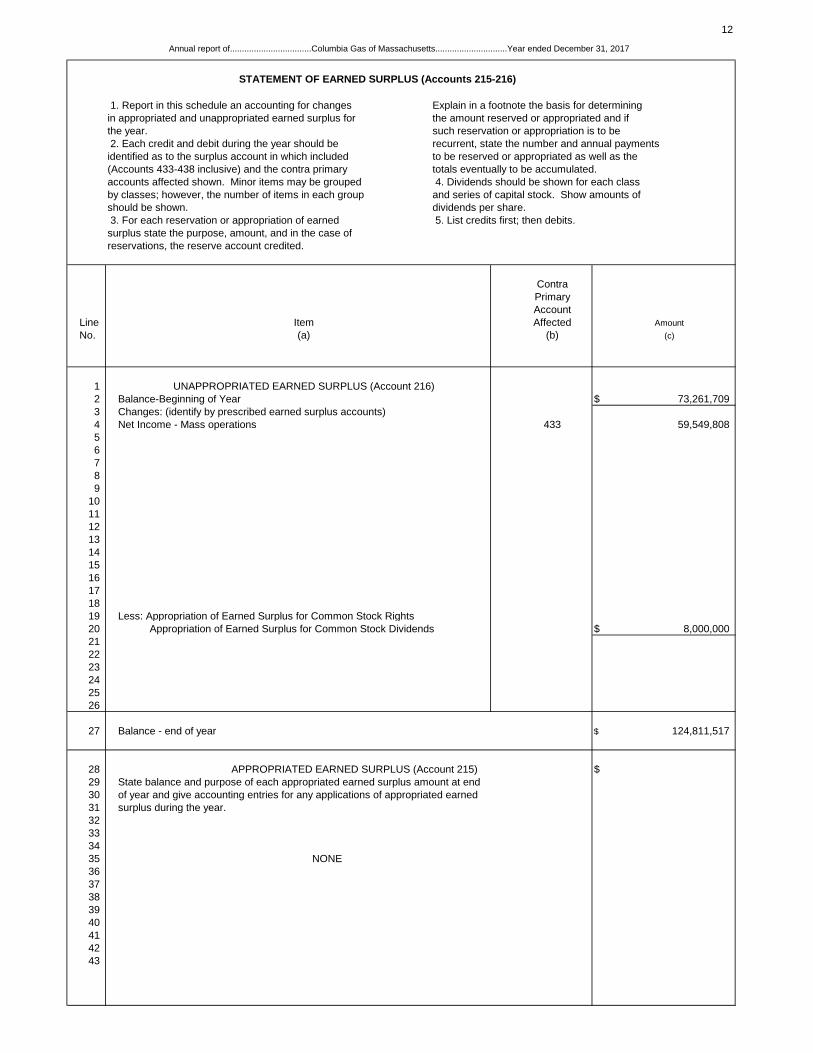

12

Annual report of..................................Columbia Gas of Massachusetts..............................Year ended December 31, 2017

STATEMENT OF EARNED SURPLUS (Accounts 215-216)

1. Report in this schedule an accounting for changes Explain in a footnote the basis for determiningin appropriated and unappropriated earned surplus for the amount reserved or appropriated and ifthe year. such reservation or appropriation is to be 2. Each credit and debit during the year should be recurrent, state the number and annual payments identified as to the surplus account in which included to be reserved or appropriated as well as the(Accounts 433-438 inclusive) and the contra primary totals eventually to be accumulated.accounts affected shown. Minor items may be grouped 4. Dividends should be shown for each classby classes; however, the number of items in each group and series of capital stock. Show amounts ofshould be shown. dividends per share. 3. For each reservation or appropriation of earned 5. List credits first; then debits.surplus state the purpose, amount, and in the case ofreservations, the reserve account credited.

ContraPrimaryAccount

Line Item Affected AmountNo. (a) (b) (c)

1 UNAPPROPRIATED EARNED SURPLUS (Account 216)2 Balance-Beginning of Year $ 73,261,7093 Changes: (identify by prescribed earned surplus accounts)4 Net Income - Mass operations 433 59,549,80856789

10111213141516171819 Less: Appropriation of Earned Surplus for Common Stock Rights20 Appropriation of Earned Surplus for Common Stock Dividends $ 8,000,000212223242526

27 Balance - end of year $ 124,811,517

28 APPROPRIATED EARNED SURPLUS (Account 215) $29 State balance and purpose of each appropriated earned surplus amount at end 30 of year and give accounting entries for any applications of appropriated earned 31 surplus during the year.32333435 NONE3637383940414243

13

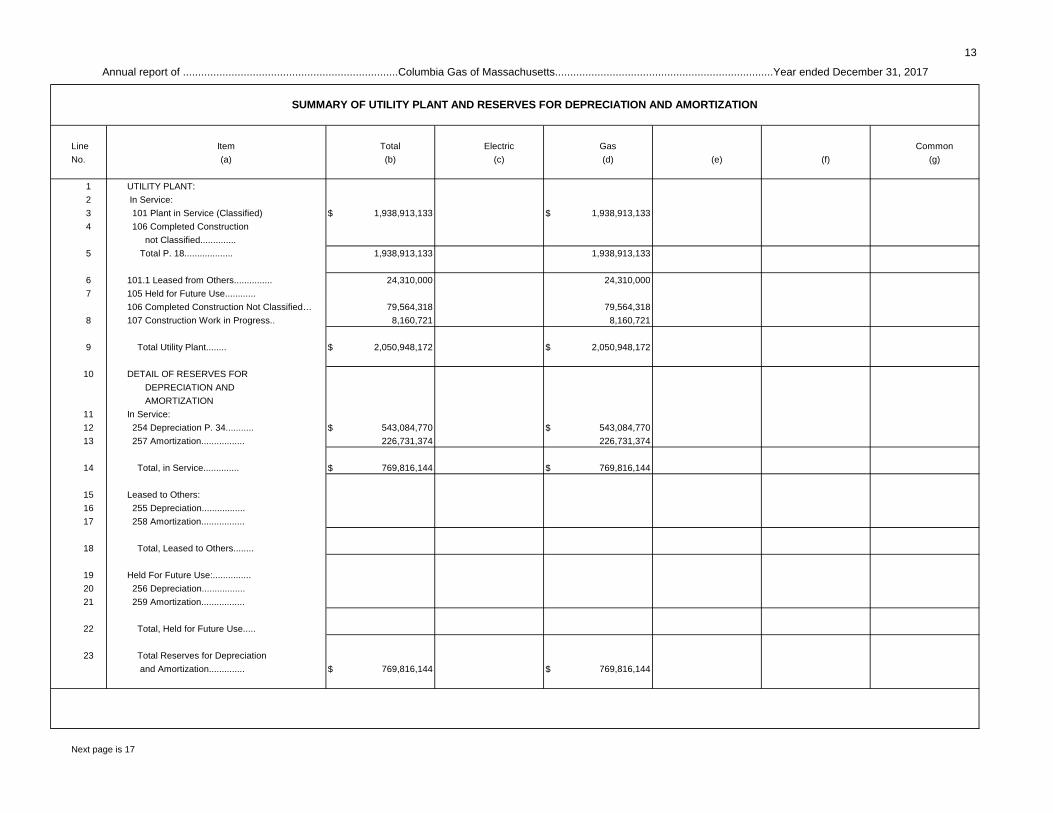

SUMMARY OF UTILITY PLANT AND RESERVES FOR DEPRECIATION AND AMORTIZATION

Line Item Total Electric Gas CommonNo. (a) (b) (c) (d) (e) (f) (g)

1 UTILITY PLANT:2 In Service:3 101 Plant in Service (Classified) $ 1,938,913,133 $ 1,938,913,1334 106 Completed Construction

not Classified..............5 Total P. 18................... 1,938,913,133 1,938,913,133

6 101.1 Leased from Others............... 24,310,000 24,310,0007 105 Held for Future Use............

106 Completed Construction Not Classified… 79,564,318 79,564,3188 107 Construction Work in Progress.. 8,160,721 8,160,721

9 Total Utility Plant........ $ 2,050,948,172 $ 2,050,948,172

10 DETAIL OF RESERVES FOR DEPRECIATION AND AMORTIZATION

11 In Service:12 254 Depreciation P. 34........... $ 543,084,770 $ 543,084,77013 257 Amortization................. 226,731,374 226,731,374

14 Total, in Service.............. $ 769,816,144 $ 769,816,144

15 Leased to Others:16 255 Depreciation.................17 258 Amortization.................

18 Total, Leased to Others........

19 Held For Future Use:...............20 256 Depreciation.................21 259 Amortization.................

22 Total, Held for Future Use.....

23 Total Reserves for Depreciation and Amortization.............. $ 769,816,144 $ 769,816,144

Next page is 17

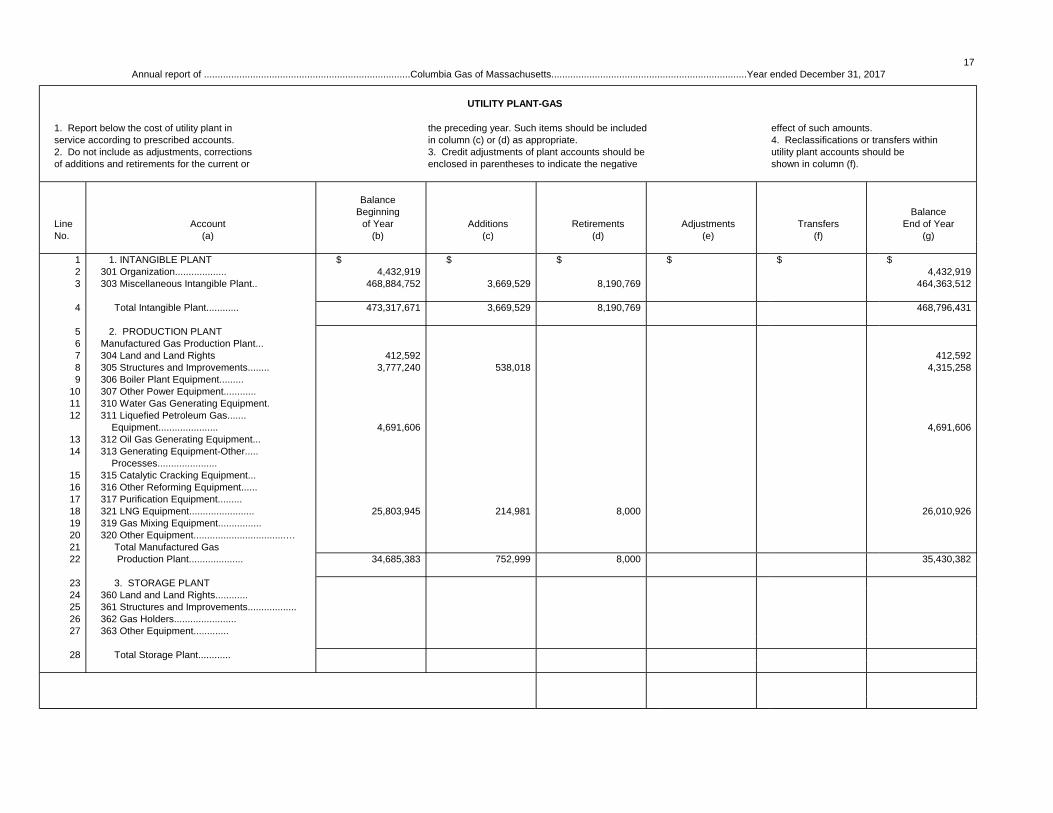

Annual report of .......................................................................Columbia Gas of Massachusetts........................................................................Year ended December 31, 2017

17

UTILITY PLANT-GAS

1. Report below the cost of utility plant in the preceding year. Such items should be included effect of such amounts.service according to prescribed accounts. in column (c) or (d) as appropriate. 4. Reclassifications or transfers within2. Do not include as adjustments, corrections 3. Credit adjustments of plant accounts should be utility plant accounts should beof additions and retirements for the current or enclosed in parentheses to indicate the negative shown in column (f).

BalanceBeginning Balance

Line Account of Year Additions Retirements Adjustments Transfers End of YearNo. (a) (b) (c) (d) (e) (f) (g)

1 1. INTANGIBLE PLANT $ $ $ $ $ $2 301 Organization................... 4,432,919 4,432,9193 303 Miscellaneous Intangible Plant.. 468,884,752 3,669,529 8,190,769 464,363,512

4 Total Intangible Plant............ 473,317,671 3,669,529 8,190,769 468,796,431

5 2. PRODUCTION PLANT6 Manufactured Gas Production Plant...7 304 Land and Land Rights 412,592 412,5928 305 Structures and Improvements........ 3,777,240 538,018 4,315,2589 306 Boiler Plant Equipment.........

10 307 Other Power Equipment............11 310 Water Gas Generating Equipment.12 311 Liquefied Petroleum Gas.......

Equipment...................... 4,691,606 4,691,60613 312 Oil Gas Generating Equipment...14 313 Generating Equipment-Other.....

Processes......................15 315 Catalytic Cracking Equipment...16 316 Other Reforming Equipment......17 317 Purification Equipment.........18 321 LNG Equipment........................ 25,803,945 214,981 8,000 26,010,92619 319 Gas Mixing Equipment................20 320 Other Equipment..................................…21 Total Manufactured Gas22 Production Plant.................... 34,685,383 752,999 8,000 35,430,382

23 3. STORAGE PLANT24 360 Land and Land Rights............25 361 Structures and Improvements..................26 362 Gas Holders.......................27 363 Other Equipment.............

28 Total Storage Plant............

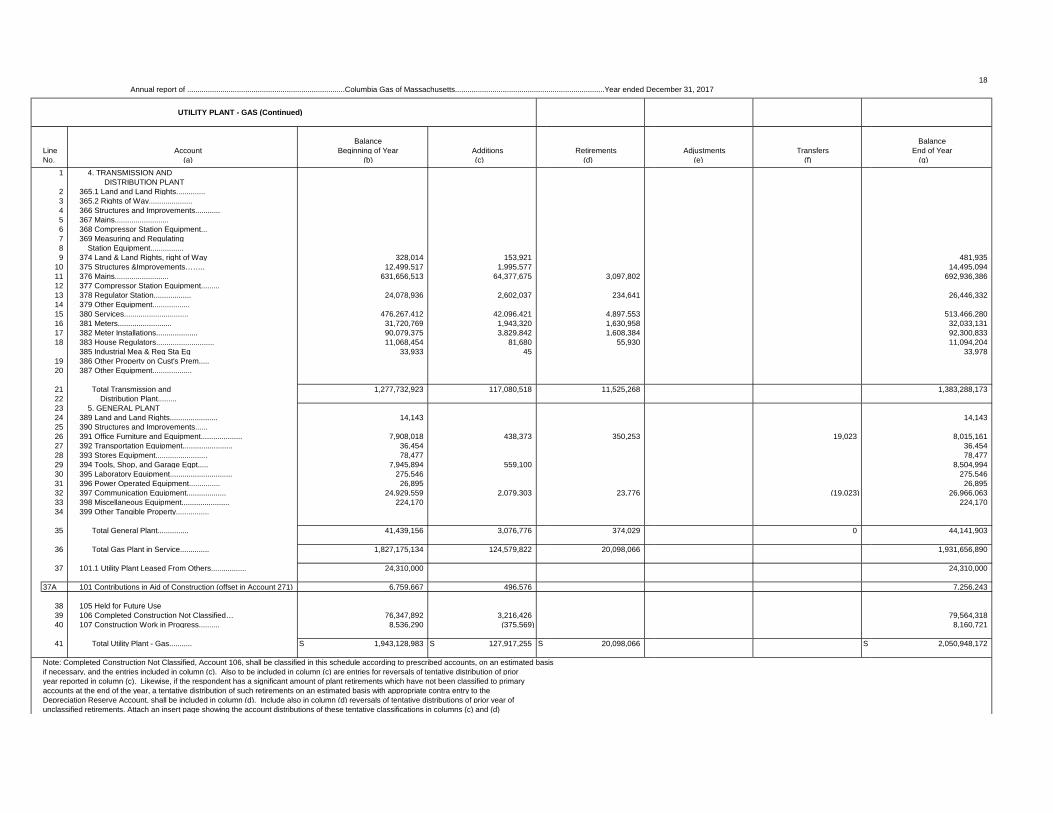

Annual report of ............................................................................Columbia Gas of Massachusetts........................................................................Year ended December 31, 2017

18

UTILITY PLANT - GAS (Continued)

Balance BalanceLine Account Beginning of Year Additions Retirements Adjustments Transfers End of YearNo. (a) (b) (c) (d) (e) (f) (g)

1 4. TRANSMISSION AND DISTRIBUTION PLANT

2 365.1 Land and Land Rights..............3 365.2 Rights of Way.....................4 366 Structures and Improvements............5 367 Mains..........................6 368 Compressor Station Equipment...7 369 Measuring and Regulating8 Station Equipment................9 374 Land & Land Rights, right of Way 328,014 153,921 481,935

10 375 Structures &Improvements…….. 12,499,517 1,995,577 14,495,09411 376 Mains.......................... 631,656,513 64,377,675 3,097,802 692,936,38612 377 Compressor Station Equipment.........13 378 Regulator Station.................. 24,078,936 2,602,037 234,641 26,446,33214 379 Other Equipment..................15 380 Services............................... 476,267,412 42,096,421 4,897,553 513,466,28016 381 Meters.......................... 31,720,769 1,943,320 1,630,958 32,033,13117 382 Meter Installations.................... 90,079,375 3,829,842 1,608,384 92,300,83318 383 House Regulators............................ 11,068,454 81,680 55,930 11,094,204

385 Industrial Mea & Reg Sta Eq 33,933 45 33,97819 386 Other Property on Cust's Prem.....20 387 Other Equipment...................

21 Total Transmission and 1,277,732,923 117,080,518 11,525,268 1,383,288,17322 Distribution Plant.........23 5. GENERAL PLANT24 389 Land and Land Rights....................... 14,143 14,14325 390 Structures and Improvements......26 391 Office Furniture and Equipment.................... 7,908,018 438,373 350,253 19,023 8,015,16127 392 Transportation Equipment........................ 36,454 36,45428 393 Stores Equipment......................... 78,477 78,47729 394 Tools, Shop, and Garage Eqpt..... 7,945,894 559,100 8,504,99430 395 Laboratory Equipment.............................. 275,546 275,54631 396 Power Operated Equipment............... 26,895 26,89532 397 Communication Equipment................... 24,929,559 2,079,303 23,776 (19,023) 26,966,06333 398 Miscellaneous Equipment....................... 224,170 224,17034 399 Other Tangible Property................

35 Total General Plant............... 41,439,156 3,076,776 374,029 0 44,141,903

36 Total Gas Plant in Service.............. 1,827,175,134 124,579,822 20,098,066 1,931,656,890

37 101.1 Utility Plant Leased From Others................. 24,310,000 24,310,000

37A 101 Contributions in Aid of Construction (offset in Account 271) 6,759,667 496,576 7,256,243

38 105 Held for Future Use 39 106 Completed Construction Not Classified… 76,347,892 3,216,426 79,564,31840 107 Construction Work in Progress.......... 8,536,290 (375,569) 8,160,721

41 Total Utility Plant - Gas........... S 1,943,128,983 S 127,917,255 S 20,098,066 S 2,050,948,172

Note: Completed Construction Not Classified, Account 106, shall be classified in this schedule according to prescribed accounts, on an estimated basisif necessary, and the entries included in column (c). Also to be included in column (c) are entries for reversals of tentative distribution of prioryear reported in column (c). Likewise, if the respondent has a significant amount of plant retirements which have not been classified to primary accounts at the end of the year, a tentative distribution of such retirements on an estimated basis with appropriate contra entry to theDepreciation Reserve Account, shall be included in column (d). Include also in column (d) reversals of tentative distributions of prior year of unclassified retirements. Attach an insert page showing the account distributions of these tentative classifications in columns (c) and (d)

Annual report of ............................................................................Columbia Gas of Massachusetts........................................................................Year ended December 31, 2017

I

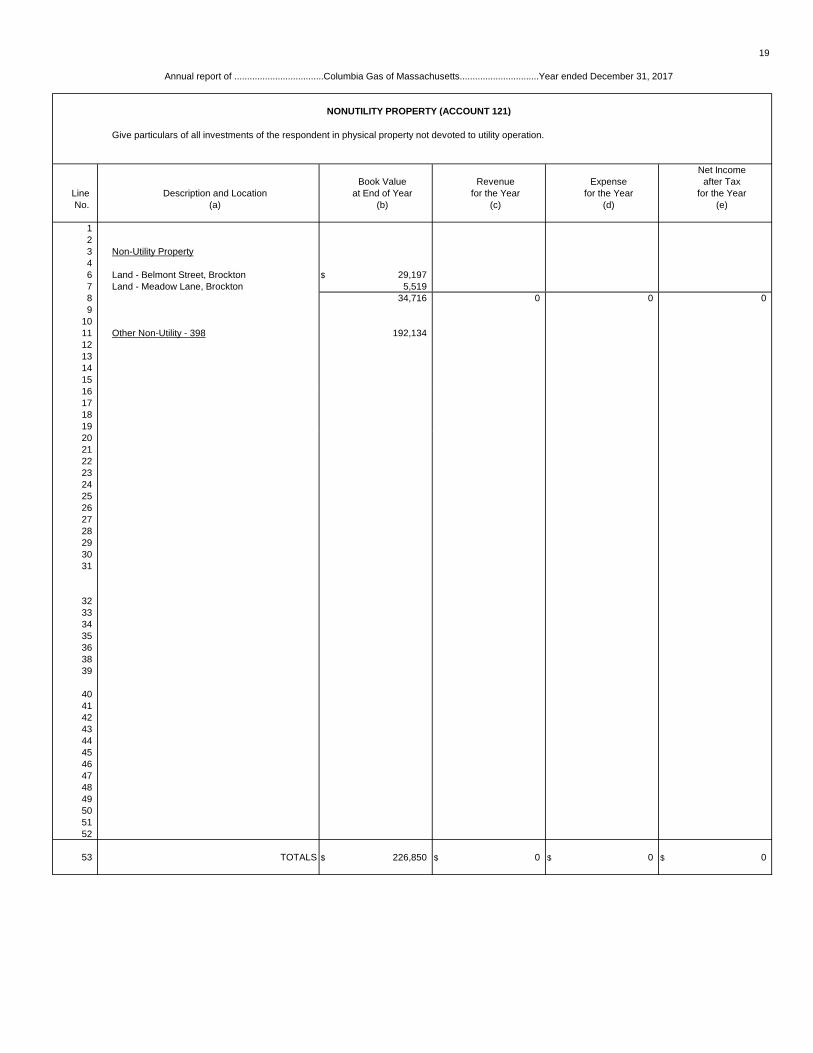

19

NONUTILITY PROPERTY (ACCOUNT 121)

Give particulars of all investments of the respondent in physical property not devoted to utility operation.

Net IncomeBook Value Revenue Expense after Tax

Line Description and Location at End of Year for the Year for the Year for the YearNo. (a) (b) (c) (d) (e)

123 Non-Utility Property46 Land - Belmont Street, Brockton $ 29,1977 Land - Meadow Lane, Brockton 5,5198 34,716 0 0 09

1011 Other Non-Utility - 398 192,1341213141516171819202122232425262728293031

32333435363839

40414243444546474849505152

53 TOTALS $ 226,850 $ 0 $ 0 $ 0

Annual report of ...................................Columbia Gas of Massachusetts...............................Year ended December 31, 2017

20

Annual report of...........................Columbia Gas of Massachusetts...........................Year ended December 31, 2017

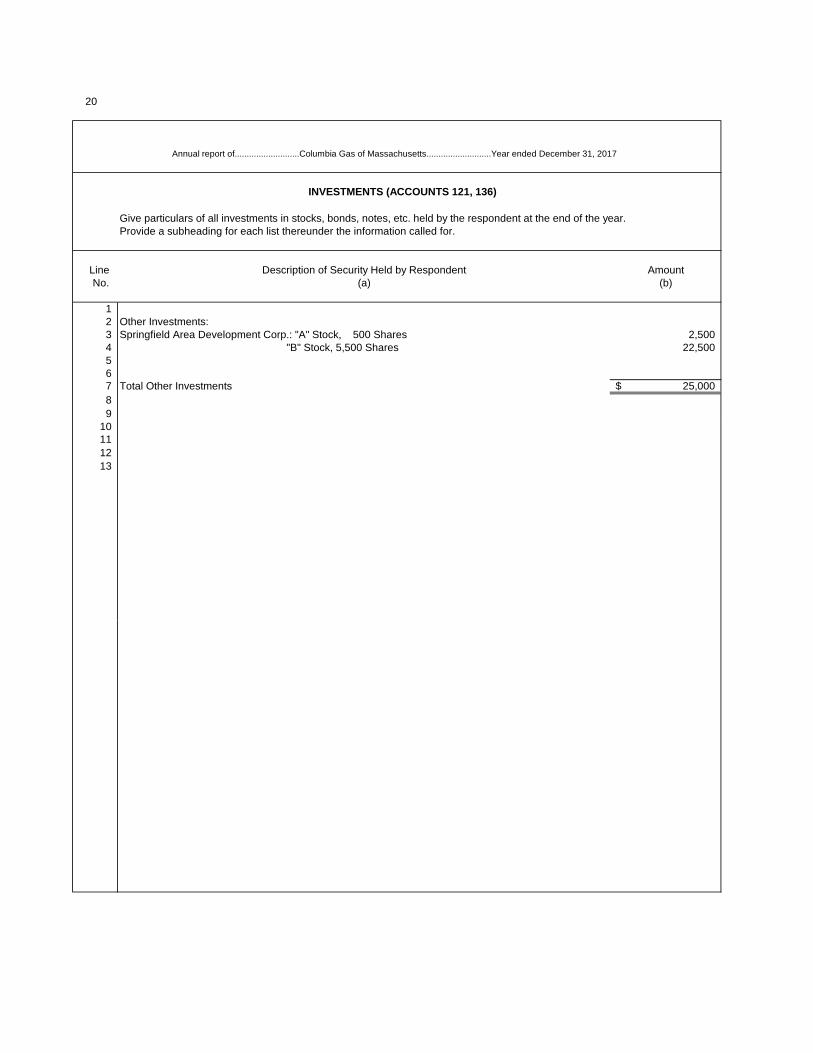

INVESTMENTS (ACCOUNTS 121, 136)

Give particulars of all investments in stocks, bonds, notes, etc. held by the respondent at the end of the year.Provide a subheading for each list thereunder the information called for.

Line Description of Security Held by Respondent AmountNo. (a) (b)

12 Other Investments:3 Springfield Area Development Corp.: "A" Stock, 500 Shares 2,5004 "B" Stock, 5,500 Shares 22,500567 Total Other Investments 25,000$ 89

10111213

21Annual report of.........................Columbia Gas of Massachusetts.........................Year ended December 31, 2017

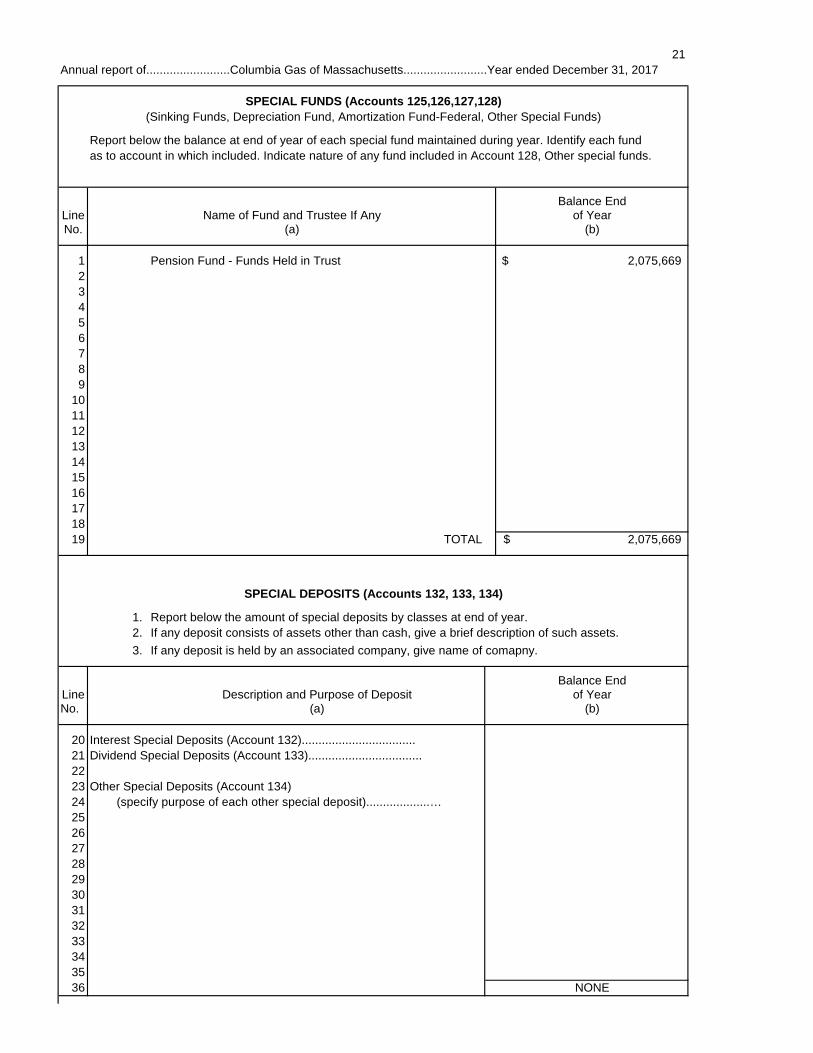

SPECIAL FUNDS (Accounts 125,126,127,128)(Sinking Funds, Depreciation Fund, Amortization Fund-Federal, Other Special Funds)

Report below the balance at end of year of each special fund maintained during year. Identify each fund as to account in which included. Indicate nature of any fund included in Account 128, Other special funds.

Balance EndLine Name of Fund and Trustee If Any of YearNo. (a) (b)

1 Pension Fund - Funds Held in Trust 2,075,669$ 23456789

10111213141516171819 TOTAL 2,075,669$

SPECIAL DEPOSITS (Accounts 132, 133, 134)

1. Report below the amount of special deposits by classes at end of year.2. If any deposit consists of assets other than cash, give a brief description of such assets.3. If any deposit is held by an associated company, give name of comapny.

Balance EndLine Description and Purpose of Deposit of YearNo. (a) (b)

20 Interest Special Deposits (Account 132)..................................21 Dividend Special Deposits (Account 133)..................................2223 Other Special Deposits (Account 134)24 (specify purpose of each other special deposit)...................…252627282930313233343536 NONE

22

Annual report of........................................Columbia Gas of Massachusetts........................................Year ended December 31, 2017

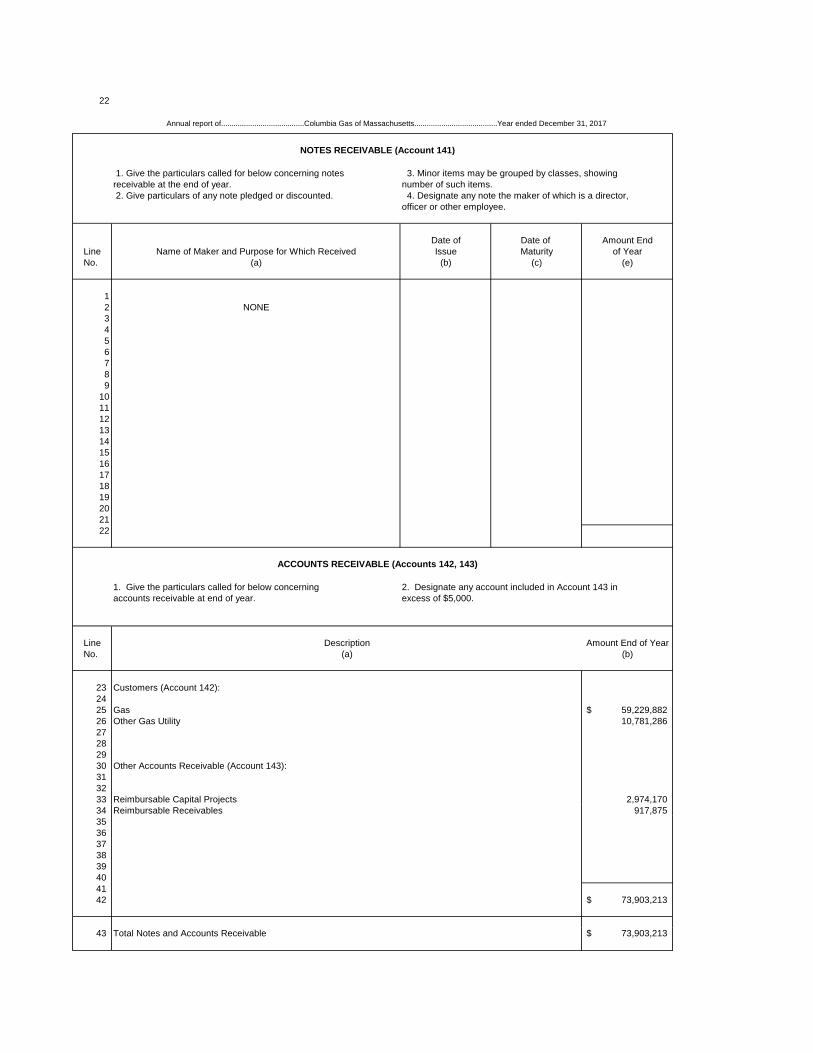

NOTES RECEIVABLE (Account 141)

1. Give the particulars called for below concerning notes 3. Minor items may be grouped by classes, showingreceivable at the end of year. number of such items. 2. Give particulars of any note pledged or discounted. 4. Designate any note the maker of which is a director,

officer or other employee.

Date of Date of Amount EndLine Name of Maker and Purpose for Which Received Issue Maturity of YearNo. (a) (b) (c) (e)

12 NONE3456789

10111213141516171819202122

ACCOUNTS RECEIVABLE (Accounts 142, 143)

1. Give the particulars called for below concerning 2. Designate any account included in Account 143 in accounts receivable at end of year. excess of $5,000.

Line Description Amount End of YearNo. (a) (b)

23 Customers (Account 142):24 25 Gas 59,229,882$ 26 Other Gas Utility 10,781,286 27282930 Other Accounts Receivable (Account 143):313233 Reimbursable Capital Projects 2,974,170 34 Reimbursable Receivables 917,875 3536373839404142 73,903,213$

43 Total Notes and Accounts Receivable 73,903,213$

23

Annual report of........................................Columbia Gas of Massachusetts........................................Year ended December 31, 2017

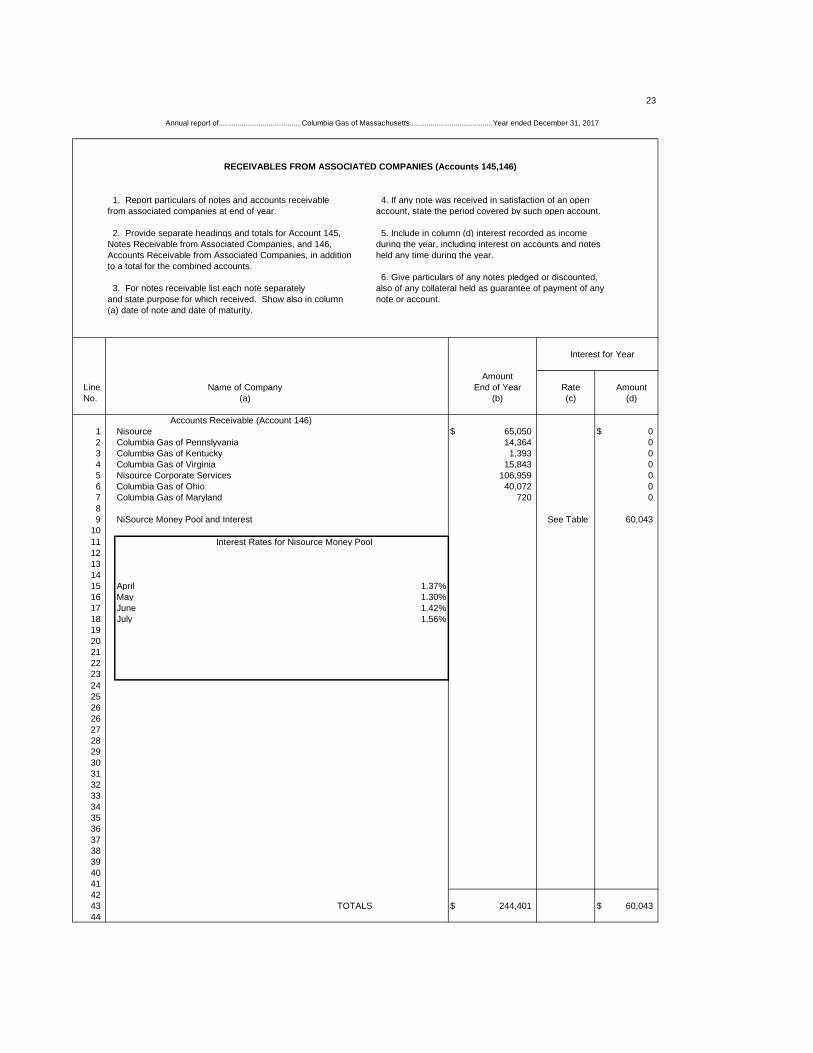

RECEIVABLES FROM ASSOCIATED COMPANIES (Accounts 145,146)

1. Report particulars of notes and accounts receivable 4. If any note was received in satisfaction of an openfrom associated companies at end of year. account, state the period covered by such open account.

2. Provide separate headings and totals for Account 145, 5. Include in column (d) interest recorded as incomeNotes Receivable from Associated Companies, and 146, during the year, including interest on accounts and notesAccounts Receivable from Associated Companies, in addition held any time during the year.to a total for the combined accounts.

6. Give particulars of any notes pledged or discounted, 3. For notes receivable list each note separately also of any collateral held as guarantee of payment of anyand state purpose for which received. Show also in column note or account.(a) date of note and date of maturity.

Interest for Year

AmountLine Name of Company End of Year Rate AmountNo. (a) (b) (c) (d)

Accounts Receivable (Account 146)1 Nisource $ 65,050 $ 02 Columbia Gas of Pennslyvania 14,364 03 Columbia Gas of Kentucky 1,393 04 Columbia Gas of Virginia 15,843 05 Nisource Corporate Services 106,959 06 Columbia Gas of Ohio 40,072 07 Columbia Gas of Maryland 720 089 NiSource Money Pool and Interest See Table 60,043

1011 Interest Rates for Nisource Money Pool12131415 April 1.37%16 May 1.30%17 June 1.42%18 July 1.56%1920212223242526262728293031323334353637383940414243 TOTALS $ 244,401 $ 60,04344

24

Annual report of.............................Columbia Gas of Massachusetts..........................Year ended December 31, 2017

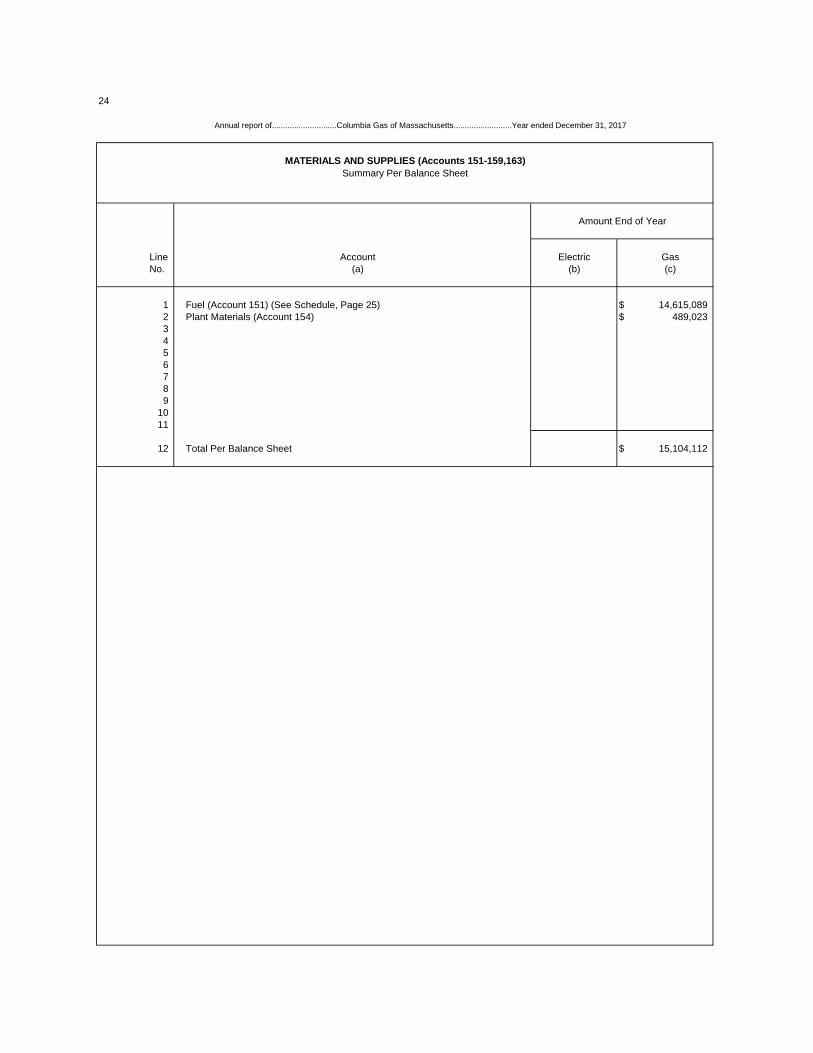

MATERIALS AND SUPPLIES (Accounts 151-159,163)Summary Per Balance Sheet

Amount End of Year

Line Account Electric GasNo. (a) (b) (c)

1 Fuel (Account 151) (See Schedule, Page 25) $ 14,615,0892 Plant Materials (Account 154) $ 489,0233 456 7 8 9

1011

12 Total Per Balance Sheet $ 15,104,112

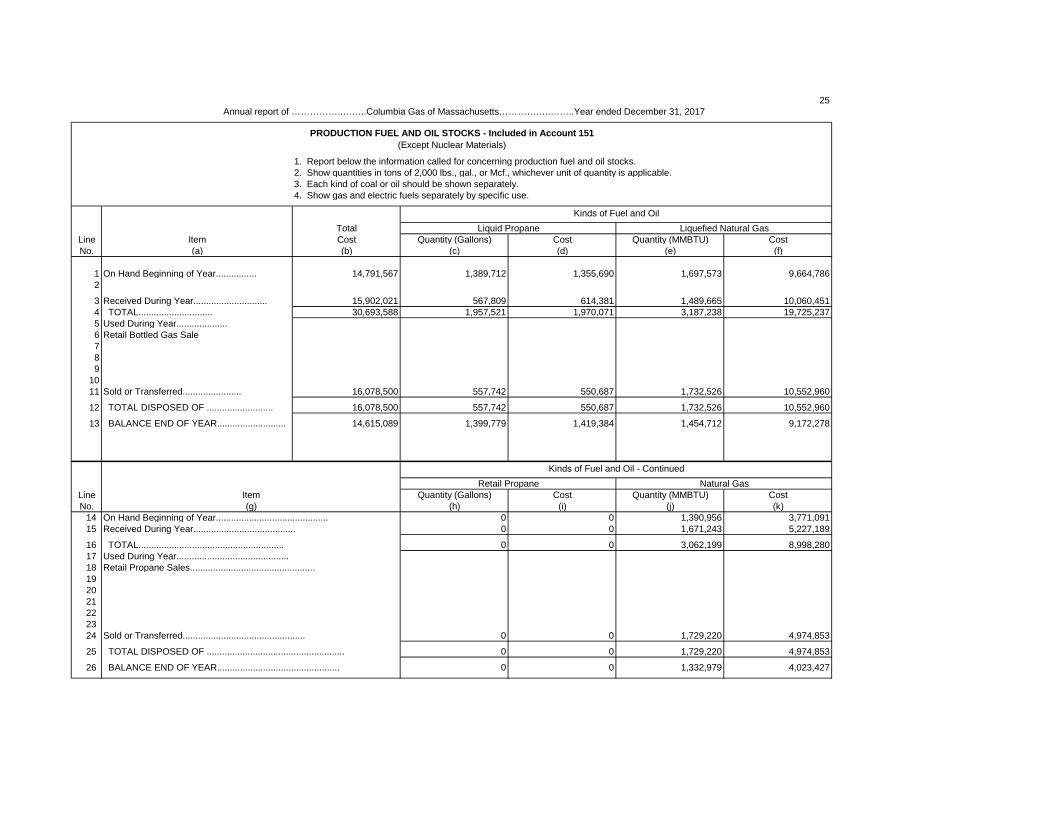

25 Annual report of ……………..……..Columbia Gas of Massachusetts……………..……..Year ended December 31, 2017

PRODUCTION FUEL AND OIL STOCKS - Included in Account 151(Except Nuclear Materials)

1. Report below the information called for concerning production fuel and oil stocks.2. Show quantities in tons of 2,000 lbs., gal., or Mcf., whichever unit of quantity is applicable.3. Each kind of coal or oil should be shown separately.4. Show gas and electric fuels separately by specific use.

Kinds of Fuel and OilTotal Liquid Propane Liquefied Natural Gas

Line Item Cost Quantity (Gallons) Cost Quantity (MMBTU) CostNo. (a) (b) (c) (d) (e) (f)

1 On Hand Beginning of Year................ 14,791,567 1,389,712 1,355,690 1,697,573 9,664,7862

3 Received During Year............................. 15,902,021 567,809 614,381 1,489,665 10,060,4514 TOTAL............................. 30,693,588 1,957,521 1,970,071 3,187,238 19,725,2375 Used During Year....................6 Retail Bottled Gas Sale789

1011 Sold or Transferred....................... 16,078,500 557,742 550,687 1,732,526 10,552,960

12 TOTAL DISPOSED OF .......................... 16,078,500 557,742 550,687 1,732,526 10,552,960

13 BALANCE END OF YEAR........................... 14,615,089 1,399,779 1,419,384 1,454,712 9,172,278

Kinds of Fuel and Oil - ContinuedRetail Propane Natural Gas

Line Item Quantity (Gallons) Cost Quantity (MMBTU) CostNo. (g) (h) (i) (j) (k)

14 On Hand Beginning of Year............................................ 0 0 1,390,956 3,771,09115 Received During Year........................................ 0 0 1,671,243 5,227,189

16 TOTAL......................................................... 0 0 3,062,199 8,998,28017 Used During Year............................................18 Retail Propane Sales.................................................192021222324 Sold or Transferred................................................ 0 0 1,729,220 4,974,853

25 TOTAL DISPOSED OF ...................................................... 0 0 1,729,220 4,974,853

26 BALANCE END OF YEAR................................................ 0 0 1,332,979 4,023,427

26

Annual report of .................……………....................................Columbia Gas of Massachusetts.............………………................Year ended December 31, 2017

UNAMORTIZED DEBT DISCOUNT AND EXPENSE AND UNAMORTIZED PREMIUM ON DEBT (Accounts 181, 251)

1. Report under separate subheadings for Unamor- 4. In column (c) show the discount and expense or 6. Set out separately and identify undisposedtized Debt Discount and Expense and Unamortized premium with respect to the amount of bonds or other amounts applicable to issues which were redeemedPremium on Debt, particularly of discount and expense long-term debt originally issued. in prior years.or premium applicable to each class and series of 5. Furnish particulars regarding the treatment of 7. Explain any debits and credits other than amor-long-term debt. unamortized debt discount and expense or premium, tization debited to Account 428, Amortization of Debt 2. Show premium amounts by enclosure in parentheses. redemption premiums, and redemption expenses asso- Discount or Expense, or credited to Account 429, 3. In column (b) show the principal amount of ciated with issues redeemed during the year, also, date Amortization of Premium on Debt - Credit.bonds or other long-term debt originally issued. of the Department's authorization of treatment other

than as specified by the Uniform System of Accounts.

Principal AmountBalance at the end of Securities toof the reporting year which Discount Total Discount

and Expenses or and Expense or Balance Debits Credits Balance Designation of Long-Term Debt Premium Minus Net Premium Beginning During During End of

Line Expense,Relates (Omit Cents) To of Year Year Year YearNo. (Omit Cents)

(a) (b) (c) (d) (e) (f) (g) (h) (i)

1 6.43% notes, due December 15, 2025 10,000,000 10,000,000 2,148,966 12/15/95 12/15/25 644,652 71,628 573,0242 6.26% notes, due February 15, 2028 30,000,000 30,000,000 5,957,669 12/15/98 2/15/28 2,127,202 191,928 1,935,2743 5.58% notes, due December 20, 2019 35,000,000 35,000,000 14,078 12/20/04 12/20/19 2,808 936 1,8724 5.94% notes, due December 20, 2024 35,000,000 35,000,000 14,079 12/20/04 12/20/24 5,568 696 4,8725 5.36% notes, due December 16, 2041 11,000,000 11,000,000 0 0 0 06 4.97% notes, due November 28, 2042 8,000,000 8,000,000 0 0 0 07 5.57% notes, due September 24, 2043 22,000,000 22,000,000 0 0 0 08 4.98% notes, due March 18, 2043 50,000,000 50,000,000 0 0 0 09 4.62% notes, due November 20, 2044 28,400,000 28,400,000 0 0 0 010 4.99% notes, due June 26, 2045 15,000,000 15,000,000 0 0 0 011 4.70% notes, due December 30, 2045 15,000,000 15,000,000 0 0 0 012 3.86% notes, due June 30, 2046 58,000,000 58,000,000 0 0 0 013 4.16% notes, due June 30, 2047 15,000,000 15,000,000 0 0 0 014 4.11% notes, due September 29, 2047 7,000,000 7,000,000 0 0 0 015 3.89% notes, due December 29, 2047 45,000,000 45,000,000 0 0 0 0

16 Acct 181 TOTALS (Credits tie to 428 account charges) 2,780,230 0 265,188 2,515,042

17 TOTALS 384,400,000 384,400,000 8,134,792

Amortization Period

27

Annual report of ................................Columbia Gas of Massachusetts.......................................Year ended December 31, 2017

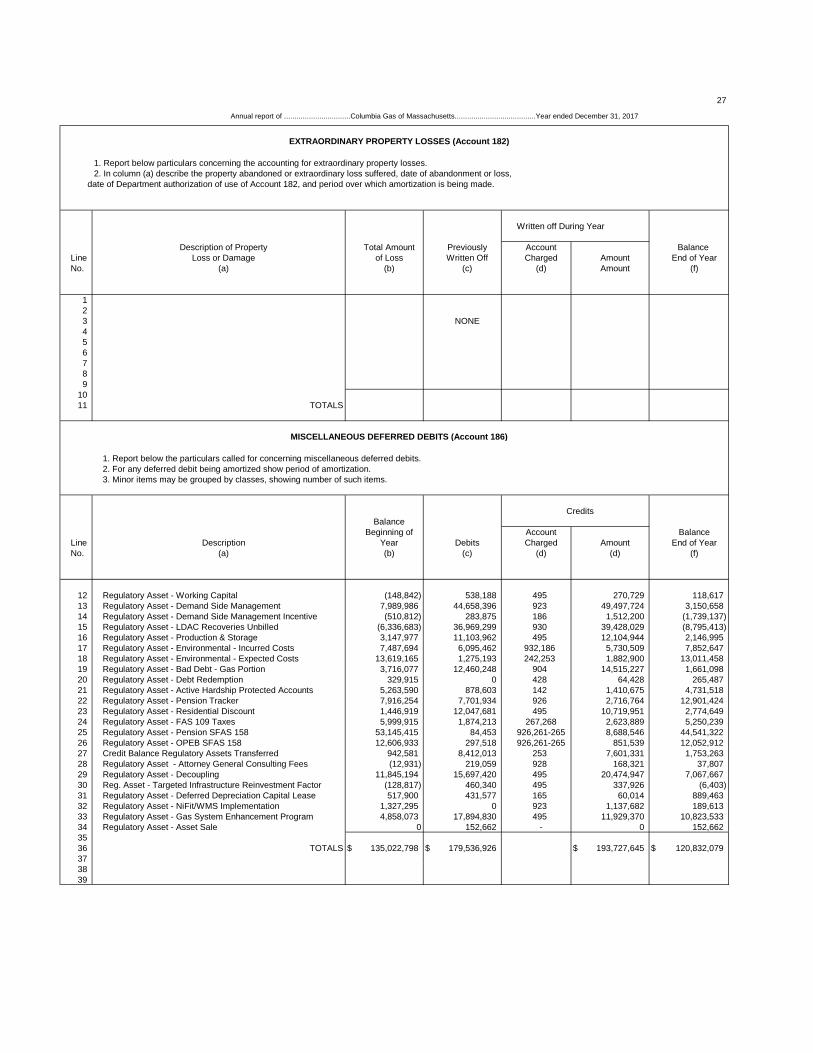

EXTRAORDINARY PROPERTY LOSSES (Account 182)

1. Report below particulars concerning the accounting for extraordinary property losses.2. In column (a) describe the property abandoned or extraordinary loss suffered, date of abandonment or loss,

date of Department authorization of use of Account 182, and period over which amortization is being made.

Written off During Year

Description of Property Total Amount Previously Account Balance Line Loss or Damage of Loss Written Off Charged Amount End of YearNo. (a) (b) (c) (d) Amount (f)

123 NONE456789

1011 TOTALS

MISCELLANEOUS DEFERRED DEBITS (Account 186)

1. Report below the particulars called for concerning miscellaneous deferred debits.2. For any deferred debit being amortized show period of amortization.3. Minor items may be grouped by classes, showing number of such items.

CreditsBalance

Beginning of Account BalanceLine Description Year Debits Charged Amount End of YearNo. (a) (b) (c) (d) (d) (f)

12 Regulatory Asset - Working Capital (148,842) 538,188 495 270,729 118,61713 Regulatory Asset - Demand Side Management 7,989,986 44,658,396 923 49,497,724 3,150,65814 Regulatory Asset - Demand Side Management Incentive (510,812) 283,875 186 1,512,200 (1,739,137)15 Regulatory Asset - LDAC Recoveries Unbilled (6,336,683) 36,969,299 930 39,428,029 (8,795,413)16 Regulatory Asset - Production & Storage 3,147,977 11,103,962 495 12,104,944 2,146,99517 Regulatory Asset - Environmental - Incurred Costs 7,487,694 6,095,462 932,186 5,730,509 7,852,64718 Regulatory Asset - Environmental - Expected Costs 13,619,165 1,275,193 242,253 1,882,900 13,011,45819 Regulatory Asset - Bad Debt - Gas Portion 3,716,077 12,460,248 904 14,515,227 1,661,09820 Regulatory Asset - Debt Redemption 329,915 0 428 64,428 265,48721 Regulatory Asset - Active Hardship Protected Accounts 5,263,590 878,603 142 1,410,675 4,731,51822 Regulatory Asset - Pension Tracker 7,916,254 7,701,934 926 2,716,764 12,901,42423 Regulatory Asset - Residential Discount 1,446,919 12,047,681 495 10,719,951 2,774,64924 Regulatory Asset - FAS 109 Taxes 5,999,915 1,874,213 267,268 2,623,889 5,250,23925 Regulatory Asset - Pension SFAS 158 53,145,415 84,453 926,261-265 8,688,546 44,541,32226 Regulatory Asset - OPEB SFAS 158 12,606,933 297,518 926,261-265 851,539 12,052,91227 Credit Balance Regulatory Assets Transferred 942,581 8,412,013 253 7,601,331 1,753,26328 Regulatory Asset - Attorney General Consulting Fees (12,931) 219,059 928 168,321 37,80729 Regulatory Asset - Decoupling 11,845,194 15,697,420 495 20,474,947 7,067,66730 Reg. Asset - Targeted Infrastructure Reinvestment Factor (128,817) 460,340 495 337,926 (6,403)31 Regulatory Asset - Deferred Depreciation Capital Lease 517,900 431,577 165 60,014 889,46332 Regulatory Asset - NiFit/WMS Implementation 1,327,295 0 923 1,137,682 189,61333 Regulatory Asset - Gas System Enhancement Program 4,858,073 17,894,830 495 11,929,370 10,823,53334 Regulatory Asset - Asset Sale 0 152,662 - 0 152,6623536 TOTALS $ 135,022,798 $ 179,536,926 $ 193,727,645 $ 120,832,079373839

THIS PAGE INTENTIONALLY LEFT BLANK[NEXT PAGE IS 29]

29

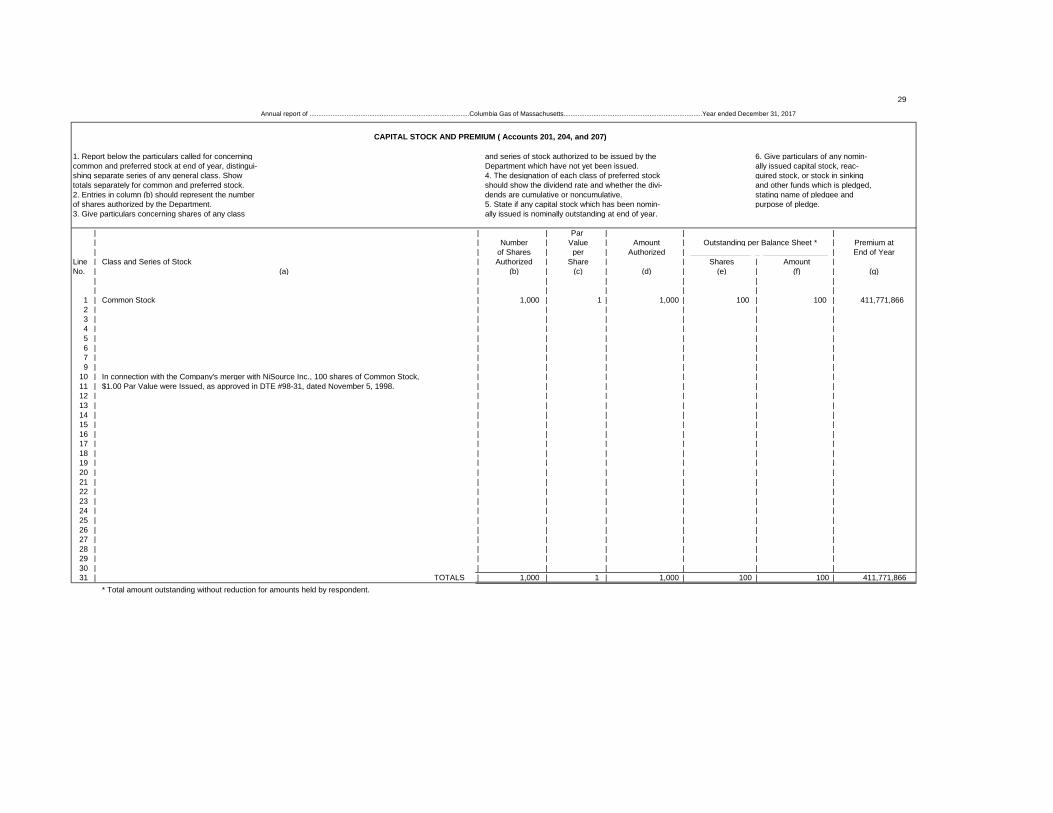

CAPITAL STOCK AND PREMIUM ( Accounts 201, 204, and 207)

1. Report below the particulars called for concerning and series of stock authorized to be issued by the 6. Give particulars of any nomin-common and preferred stock at end of year, distingui- Department which have not yet been issued. ally issued capital stock, reac-shing separate series of any general class. Show 4. The designation of each class of preferred stock quired stock, or stock in sinkingtotals separately for common and preferred stock. should show the dividend rate and whether the divi- and other funds which is pledged,2. Entries in column (b) should represent the number dends are cumulative or noncumulative. stating name of pledgee andof shares authorized by the Department. 5. State if any capital stock which has been nomin- purpose of pledge.3. Give particulars concerning shares of any class ally issued is nominally outstanding at end of year.

| | | Par | | || | Number | Value | Amount | Outstanding per Balance Sheet * | Premium at| | of Shares | per | Authorized | ______________ _ _______________ | End of Year

Line | Class and Series of Stock | Authorized | Share | | Shares | Amount |No. | (a) | (b) | (c) | (d) | (e) | (f) | (g)

| | | | | | |____ | ____________________________________________________________________________________ _ | _____________ | ___________ | _______________ | ______________ | _______________ | _______________ _

1 | Common Stock | 1,000 | 1 | 1,000 | 100 | 100 | 411,771,8662 | | | | | | |3 | | | | | | |4 | | | | | | |5 | | | | | | |6 | | | | | | |7 | | | | | | |9 | | | | | | |

10 | In connection with the Company's merger with NiSource Inc., 100 shares of Common Stock, | | | | | |11 | $1.00 Par Value were Issued, as approved in DTE #98-31, dated November 5, 1998. | | | | | |12 | | | | | | |13 | | | | | | |14 | | | | | | |15 | | | | | | |16 | | | | | | |17 | | | | | | |18 | | | | | | |19 | | | | | | |20 | | | | | | |21 | | | | | | |22 | | | | | | |23 | | | | | | |24 | | | | | | |25 | | | | | | |26 | | | | | | |27 | | | | | | |28 | | | | | | |29 | | | | | | |30 | | | | | | |31 | TOTALS | 1,000 | 1 | 1,000 | 100 | 100 | 411,771,866

* Total amount outstanding without reduction for amounts held by respondent.

Annual report of ...........................................................................................Columbia Gas of Massachusetts...............................................................................Year ended December 31, 2017

30

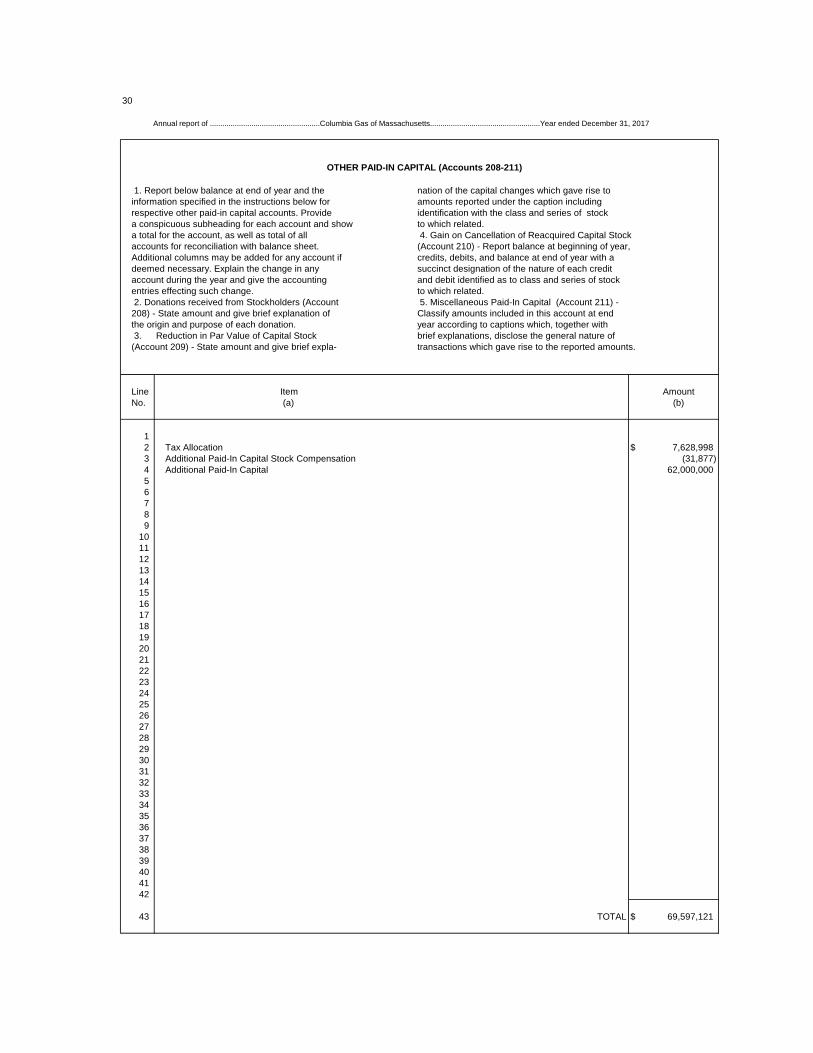

Annual report of .....................................................Columbia Gas of Massachusetts.....................................................Year ended December 31, 2017

OTHER PAID-IN CAPITAL (Accounts 208-211)

1. Report below balance at end of year and the nation of the capital changes which gave rise toinformation specified in the instructions below for amounts reported under the caption includingrespective other paid-in capital accounts. Provide identification with the class and series of stocka conspicuous subheading for each account and show to which related.a total for the account, as well as total of all 4. Gain on Cancellation of Reacquired Capital Stockaccounts for reconciliation with balance sheet. (Account 210) - Report balance at beginning of year,Additional columns may be added for any account if credits, debits, and balance at end of year with a deemed necessary. Explain the change in any succinct designation of the nature of each creditaccount during the year and give the accounting and debit identified as to class and series of stock entries effecting such change. to which related. 2. Donations received from Stockholders (Account 5. Miscellaneous Paid-In Capital (Account 211) - 208) - State amount and give brief explanation of Classify amounts included in this account at end the origin and purpose of each donation. year according to captions which, together with 3. Reduction in Par Value of Capital Stock brief explanations, disclose the general nature of(Account 209) - State amount and give brief expla- transactions which gave rise to the reported amounts.

Line Item AmountNo. (a) (b)

12 Tax Allocation $ 7,628,9983 Additional Paid-In Capital Stock Compensation (31,877)4 Additional Paid-In Capital 62,000,00056789

101112131415161718192021222324252627282930313233343536373839404142

43 TOTAL $ 69,597,121

31

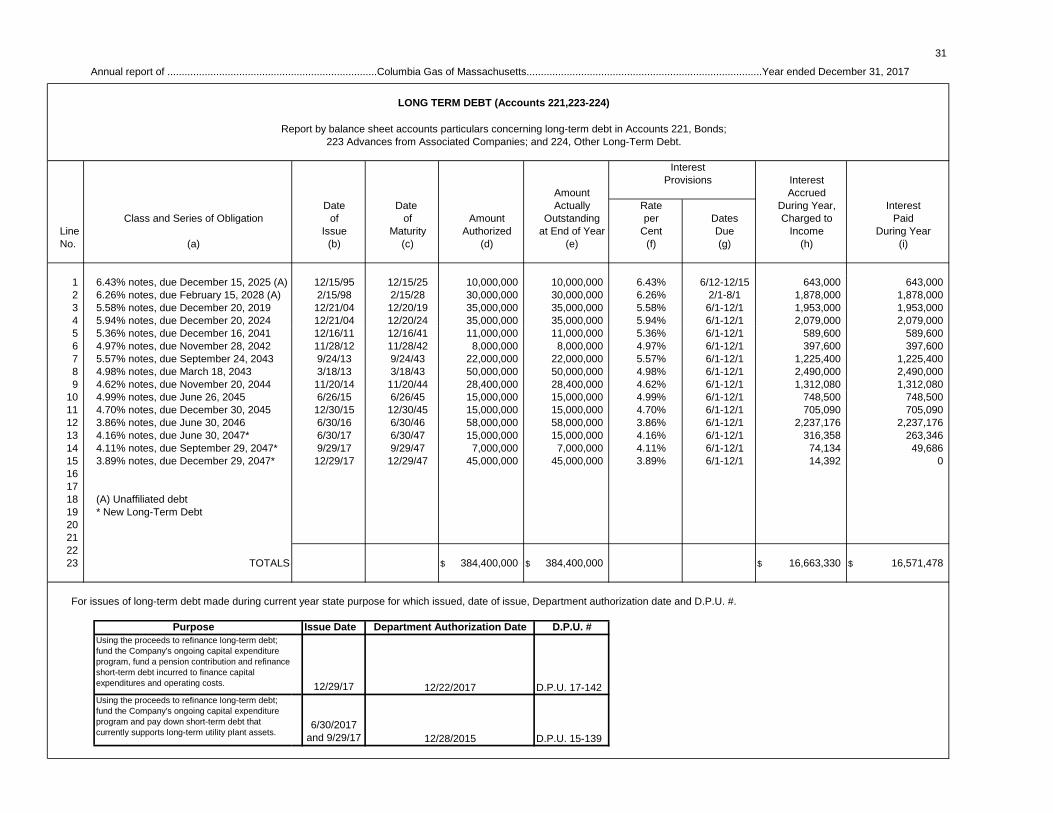

LONG TERM DEBT (Accounts 221,223-224)

Report by balance sheet accounts particulars concerning long-term debt in Accounts 221, Bonds;223 Advances from Associated Companies; and 224, Other Long-Term Debt.

Interest Provisions Interest Amount Accrued

Date Date Actually Rate During Year, InterestClass and Series of Obligation of of Amount Outstanding per Dates Charged to Paid

Line Issue Maturity Authorized at End of Year Cent Due Income During YearNo. (a) (b) (c) (d) (e) (f) (g) (h) (i)

1 6.43% notes, due December 15, 2025 (A) 12/15/95 12/15/25 10,000,000 10,000,000 6.43% 6/12-12/15 643,000 643,0002 6.26% notes, due February 15, 2028 (A) 2/15/98 2/15/28 30,000,000 30,000,000 6.26% 2/1-8/1 1,878,000 1,878,0003 5.58% notes, due December 20, 2019 12/21/04 12/20/19 35,000,000 35,000,000 5.58% 6/1-12/1 1,953,000 1,953,0004 5.94% notes, due December 20, 2024 12/21/04 12/20/24 35,000,000 35,000,000 5.94% 6/1-12/1 2,079,000 2,079,0005 5.36% notes, due December 16, 2041 12/16/11 12/16/41 11,000,000 11,000,000 5.36% 6/1-12/1 589,600 589,6006 4.97% notes, due November 28, 2042 11/28/12 11/28/42 8,000,000 8,000,000 4.97% 6/1-12/1 397,600 397,6007 5.57% notes, due September 24, 2043 9/24/13 9/24/43 22,000,000 22,000,000 5.57% 6/1-12/1 1,225,400 1,225,4008 4.98% notes, due March 18, 2043 3/18/13 3/18/43 50,000,000 50,000,000 4.98% 6/1-12/1 2,490,000 2,490,0009 4.62% notes, due November 20, 2044 11/20/14 11/20/44 28,400,000 28,400,000 4.62% 6/1-12/1 1,312,080 1,312,080

10 4.99% notes, due June 26, 2045 6/26/15 6/26/45 15,000,000 15,000,000 4.99% 6/1-12/1 748,500 748,50011 4.70% notes, due December 30, 2045 12/30/15 12/30/45 15,000,000 15,000,000 4.70% 6/1-12/1 705,090 705,09012 3.86% notes, due June 30, 2046 6/30/16 6/30/46 58,000,000 58,000,000 3.86% 6/1-12/1 2,237,176 2,237,17613 4.16% notes, due June 30, 2047* 6/30/17 6/30/47 15,000,000 15,000,000 4.16% 6/1-12/1 316,358 263,34614 4.11% notes, due September 29, 2047* 9/29/17 9/29/47 7,000,000 7,000,000 4.11% 6/1-12/1 74,134 49,68615 3.89% notes, due December 29, 2047* 12/29/17 12/29/47 45,000,000 45,000,000 3.89% 6/1-12/1 14,392 0161718 (A) Unaffiliated debt 19 * New Long-Term Debt 20212223 TOTALS $ 384,400,000 $ 384,400,000 $ 16,663,330 $ 16,571,478

For issues of long-term debt made during current year state purpose for which issued, date of issue, Department authorization date and D.P.U. #.

Purpose Issue Date D.P.U. #Using the proceeds to refinance long-term debt; fund the Company's ongoing capital expenditure program, fund a pension contribution and refinance short-term debt incurred to finance capital expenditures and operating costs. 12/29/17 D.P.U. 17-142Using the proceeds to refinance long-term debt; fund the Company's ongoing capital expenditure program and pay down short-term debt that currently supports long-term utility plant assets.

6/30/2017 and 9/29/17 D.P.U. 15-139

Department Authorization Date

12/22/2017

12/28/2015

Annual report of .........................................................................Columbia Gas of Massachusetts..................................................................................Year ended December 31, 2017

32

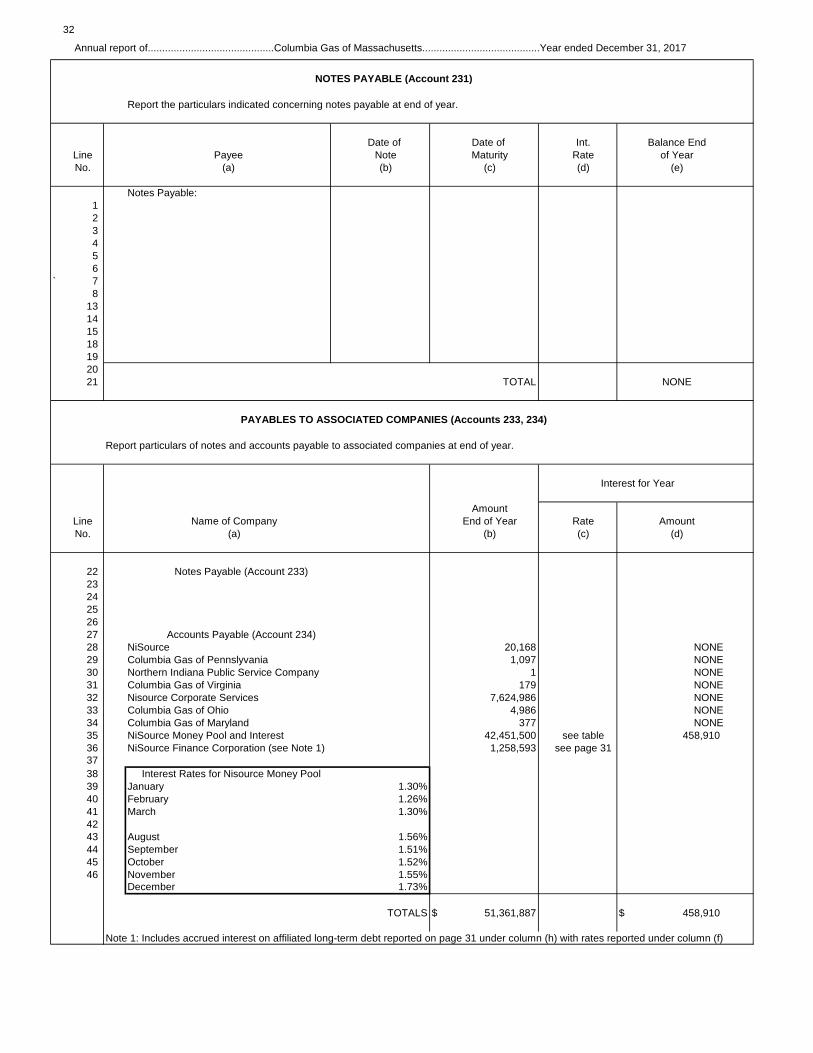

Annual report of............................................Columbia Gas of Massachusetts.........................................Year ended December 31, 2017

NOTES PAYABLE (Account 231)

Report the particulars indicated concerning notes payable at end of year.

Date of Date of Int. Balance EndLine Payee Note Maturity Rate of YearNo. (a) (b) (c) (d) (e)

Notes Payable:123456

` 78

13141518192021 TOTAL NONE

PAYABLES TO ASSOCIATED COMPANIES (Accounts 233, 234)

Report particulars of notes and accounts payable to associated companies at end of year.

Interest for Year

AmountLine Name of Company End of Year Rate AmountNo. (a) (b) (c) (d)

22 Notes Payable (Account 233)2324252627 Accounts Payable (Account 234)28 NiSource 20,168 NONE29 Columbia Gas of Pennslyvania 1,097 NONE30 Northern Indiana Public Service Company 1 NONE31 Columbia Gas of Virginia 179 NONE32 Nisource Corporate Services 7,624,986 NONE33 Columbia Gas of Ohio 4,986 NONE34 Columbia Gas of Maryland 377 NONE35 NiSource Money Pool and Interest 42,451,500 see table 458,91036 NiSource Finance Corporation (see Note 1) 1,258,593 see page 3137 38 Interest Rates for Nisource Money Pool 39 January 1.30% 40 February 1.26%41 March 1.30%4243 August 1.56%44 September 1.51%45 October 1.52%46 November 1.55%

December 1.73%

TOTALS $ 51,361,887 $ 458,910

Note 1: Includes accrued interest on affiliated long-term debt reported on page 31 under column (h) with rates reported under column (f)

33

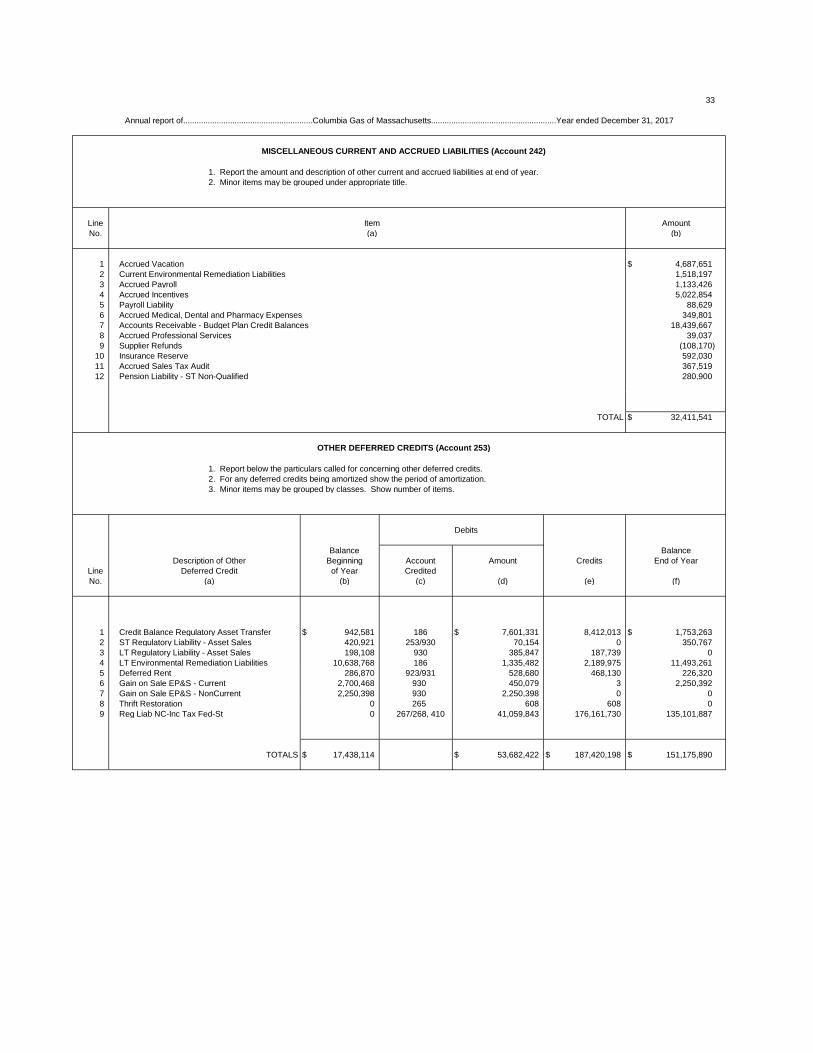

MISCELLANEOUS CURRENT AND ACCRUED LIABILITIES (Account 242)

1. Report the amount and description of other current and accrued liabilities at end of year. 2. Minor items may be grouped under appropriate title.

Line Item AmountNo. (a) (b)

1 Accrued Vacation $ 4,687,6512 Current Environmental Remediation Liabilities 1,518,1973 Accrued Payroll 1,133,4264 Accrued Incentives 5,022,8545 Payroll Liability 88,6296 Accrued Medical, Dental and Pharmacy Expenses 349,8017 Accounts Receivable - Budget Plan Credit Balances 18,439,6678 Accrued Professional Services 39,0379 Supplier Refunds (108,170)