Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Basic Fraud AuditPertemuan IX

Matakuliah : F0184/Audit atas KecuranganTahun : 2007

Bina Nusantara

• Mahasiswa diharapkan mampu mengidentifikasi langkah-langkah dalam melakukan audit atas kecurangan

• Mahasiswa dapat melihat red flag atau symptom atas suatu kejadian didalam setiap transaksi

• Mahasiswa dapat melakukan audit atas kecurangan

Learning Outcomes

3

Bina Nusantara

• Audit Step• Audit Guidance• Audit Plan• Identify fraud scheme and red flag

Outline Materi

4

Skimming DetectionSome detection methods that may be effective in detecting skimming schemes are :– Receipt or Sales Level detection– Check conversion detection– Journal entry review

5Bina Nusantara

Receipt or Sales Level Detection

• Key analytical procedures, such vertical and horizontal analysis of sales account

• Ratio analysis• Detail inventory control procedures

6Bina Nusantara

Check Conversion DetectionRed flag arise when employee attempt to convert a stolen check.– Question of validity of the check– Dual endorsement is not allowed– Canceled checks with dual endorsement should be

cutinized– A forget endorsement is discovered– Employee has opened a bank account with a name similar

to the victim company– An alteration of check payee or endorsement is discovered– etc

7Bina Nusantara

Journal Entry ReviewJournal entry that should be examine:• False credit to inventory to conceal unrecorded or

understated sales• Other write-off of inventory for reason of lost, stolen

or obsolete product• Write-off of account receivable account• Irregular entries to cash account

8Bina Nusantara

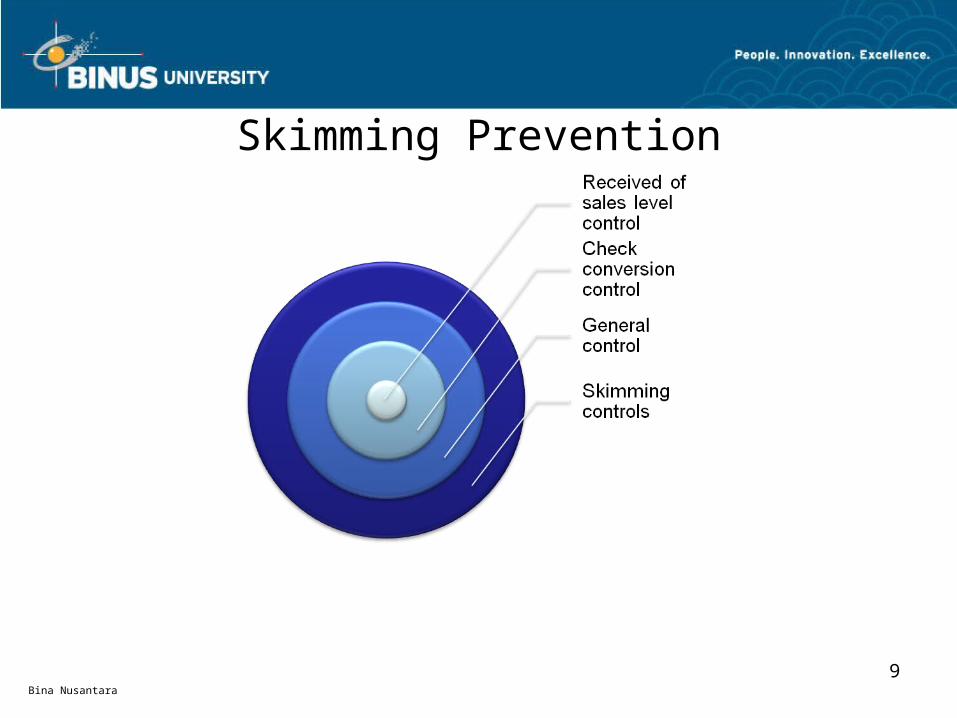

Skimming Prevention

9Bina Nusantara

Received of Sales Level Control

10Bina Nusantara

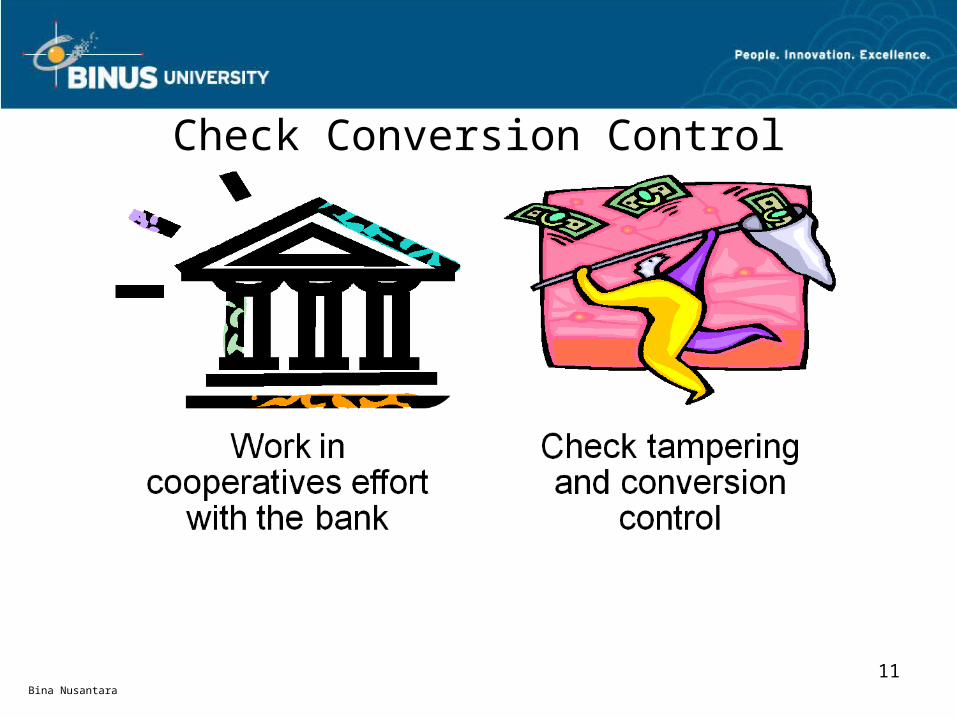

Check Conversion Control

11Bina Nusantara

General Control

Policy and procedures of general control of sales entry and general ledger access will cover:– Appropriate segregation of duties– Transaction must be properly record– Proper safeguard measures– Independent reconciliation

12Bina Nusantara

Skimming ControlsRed Flag for detecting :• Mail open by someone independent• Delivery of unopened business mail

prohibited to employee• Lock box used• Cash receipt pre number• Check reconciliation• Cash receipt deposit daily• Employee who handle receipt bonded

13Bina Nusantara

Cash Larceny

14Bina Nusantara

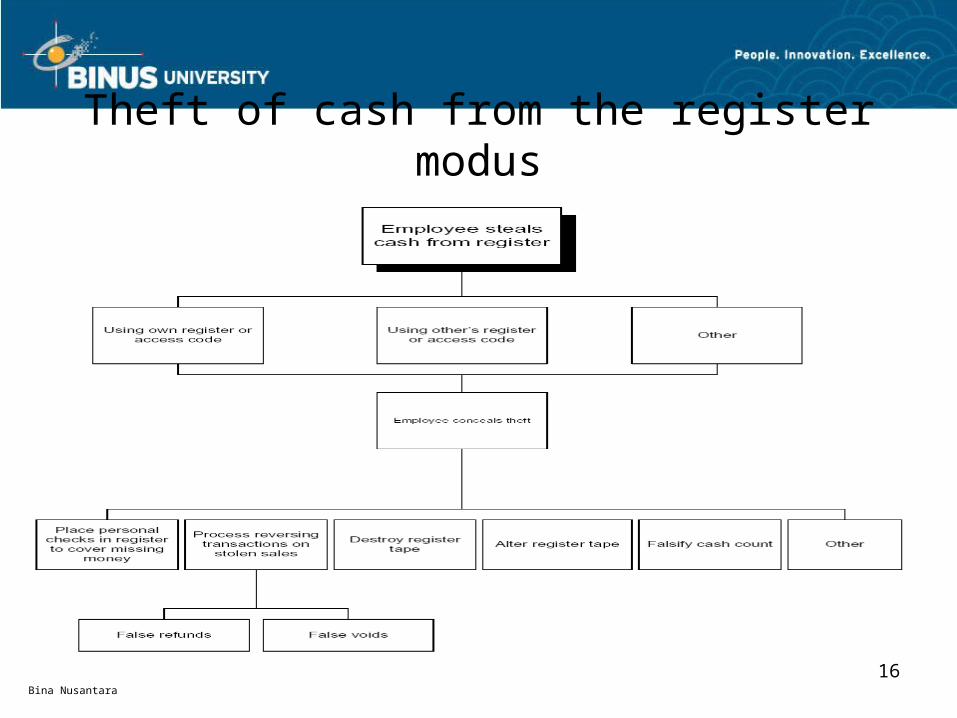

Theft of Cash from the Register

15Bina Nusantara

Theft of cash from the register modus

16Bina Nusantara

Other Larceny of Sales and Receivables

Post all record but stolen the money received and :– Plan to pay the money back– Make unsupported entries– Destroy all the record

17Bina Nusantara

Other Larceny of Sales and Receivables Modus

18Bina Nusantara

Cash Larceny from the Deposit

19Bina Nusantara

Cash Larceny from the Deposit Modus

20Bina Nusantara

Cash Larceny Detection• Receipt recording• Analytical review• Register detection• Cash account analysis

21Bina Nusantara

Receipt RecordingDepth Analysis for :• Mail and register receipt point• Journalizing and recording of receipt• The security of the cash from receipt to deposit

22Bina Nusantara

Analytical Review• Analyzing relationship between sales, cost of

sales and return and allowances can detect inappropriate refunds and discount.

23Bina Nusantara

Register Detection• Access to the register must be closely monitored• Independent person for preparing register count

sheet and aggree them to register total• Popular concealment methods must be watched for.• Complete register documentation and cash• etc

24Bina Nusantara

Cash Account Analysis• Reviewing and analyzing all journal entries made

to account cash

25Bina Nusantara

Cash Larceny Prevention• Segregation of duties• Assigment rotation and mandatory vacation• Surprise cash count and procedures supervision• Phisical security of cash

26Bina Nusantara

Related Documents