Basel II Implementation as a Statutory Requirement of Bangladesh Bank: A Study on Bangladesh Development Bank Limited Internship Report on “Basel II Implementation as a Statutory Requirement of Bangladesh Bank: A Study on Bangladesh Development Bank Limited”

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Basel II Implementation as a Statutory Requirement of Bangladesh Bank: A Study on

Bangladesh Development Bank Limited

Internship Report on

“Basel II Implementation as a Statutory

Requirement of Bangladesh Bank: A Study

on Bangladesh Development Bank Limited”

Basel II Implementation as a Statutory Requirement of Bangladesh Bank: A Study on

Bangladesh Development Bank Limited

Prepared By:

Kazi Khairul Kabir

ID NO. 15050 (BBA), 271 (MBA)

MBA 15th Batch, Section C

Department of Accounting & Information Systems

University of Dhaka

Supervised By:

Amirus Salat

Associate Professor

Department of Accounting & Information Systems

University of Dhaka

Date of Submission: 6th July, 2014

Basel II Implementation as a Statutory Requirement of Bangladesh Bank: A Study on

Bangladesh Development Bank Limited

i

Letter of Transmittal 6th July, 2014

Amirus Salat

Associate Professor

Department of Accounting & Information Systems

University of Dhaka

Subject: Submission of internship report

Dear Sir,

It is a great pleasure for me to submit the report on ― ‘Basel II Implementation as a Statutory

Requirement of Bangladesh Bank: A Study on Bangladesh Development Bank Limited’. I am

submitting this report as part of my internship in Bangladesh Development Bank Limited. The

purpose of the report is based on my working experience in Bangladesh Development Bank

Limited and how the bank has implemented the Basel Accords following the guidelines of

Bangladesh Bank.

I believe the knowledge and experience I gathered during the internship period will be extremely

helpful in my future professional life. I will be grateful to you if you accept the report.

Thanking you.

Sincerely,

___________________

Kazi Khairul Kabir

ID: 271 (MBA)

Basel II Implementation as a Statutory Requirement of Bangladesh Bank: A Study on

Bangladesh Development Bank Limited

ii

Acknowledgement

First of all, I would like to convey my cordial thanks for almighty Allah whose uniqueness,

oneness, and wholeness are unchallenged to guide us in difficult circumstances. All respects are

for his holy prophet Hazrat Muhammad (SM) Peace be upon him, who enable us to recognize

the oneness my creator.

I would like to thank Amirus Salat, my university supervisor, for guiding me in planning and

composing the report. He was always available to provide me with his supervision and guidance

during the entire course. Therefore, I express colossal appreciation for his aid.

I am very grateful to Professor Santi Narayan Ghosh, Chairman Bangladesh Development

Bank Limited, for managing the internship for me and directing me by giving his valuable advice.

I also express my gratitude to Syed Md. Nazrul Islam, Deputy General Manager of Risk

Management Department, for teaching me the critical issues of Basel II.

My most heartfelt gratitude goes to all the employees of Bangladesh Development Bank Limited,

Head office and Kawran Bazar Branch, for making it a good practical and learning experience.

From the early hours of the morning to the sunset of the evening they have guided me through

various operations of the bank and provided me with essential support for my internship report.

I pray to Allah that He be merciful to all of these people.

Last but not the least thanks goes to my parents for bearing the tension, frustration and all the

hard work along with me through the entire BBA program.

Basel II Implementation as a Statutory Requirement of Bangladesh Bank: A Study on

Bangladesh Development Bank Limited

iii

Executive Summery This internship report is based on the three months long internship program that I have

successfully completed in Bangladesh Development Bank Limited under five distinct

departments from April 1, 2014 to June 30, 2014. As a course requirement of MBA program of

the department of Accounting & Information Systems I prepare the report. Although, I worked

in five departments of BDBL, my focal point was the compliance issue regarding Basel II of Risk

management department.

I mainly worked in risk management department which is the responsible wing for implementing

Basel II in BDBL. My faculty advisor and Deputy General Manager of Risk Management

Department helped me choose the topic- “Basel II Implementation as a Statutory Requirement of

Bangladesh Bank: A Study on Bangladesh Development Bank Limited”.

The internship report is mainly divided into two segments. In the very first portion, all the

necessary calculations related with the regulatory requirements of Basel II are calculated (such

as- Capital Adequacy Ratio, Tire 1 Capital, Tire 2 Capital, Tire 3 Capital and Risk Management

Mechanisms). In the later portion, a checklist is prepared to show the compliance issue of Basel

II and a comparison is made between the regulatory compliance reported by BDBL and Sonali

Bank Limited. It is seen that although BDBL complies all the requirements but SBL does not

conform to some of the major requirements of Basel II.

Basel II is a complex yet very important international requirement for banks. The value of the

knowledge attracted me the most. Bangladesh Bank is the governing body of all the commercial

banks in this country. To be in line with the international standard for regulation of banking

industry (Basel Accord), BB has introduced Risk Based Capital Adequacy guideline relating to

Basel II. All banks have to follow this guideline and report to BB effective from 1st January,

2010. The guidelines are structured in three aspects or pillars: (1) banks should have minimum

capital to guard against different kinds of risks (credit, market and operation risk); (2) assessing

capital adequacy with risk profile of the bank and capital growth plan and (3) public disclosure

of bank’s position on risk, capital and management.

The three main risks that a commercial bank faces are: Credit risk, Market risk and Operational

risk. Credit risk is the risk that arises from the probability that the borrowers of the bank will not

pay back. Market risk is the risk that puts the bank in adverse situation when interest rate, foreign

Basel II Implementation as a Statutory Requirement of Bangladesh Bank: A Study on

Bangladesh Development Bank Limited

iv

exchange or equity price move in unfavorable direction. Operational risk stems from the internal

environment, occurring when internal processes, people or system fail. The banks can become

resilient and fend off these risks with adequate capital. This is where the regulatory guidelines

come to play.

BB categorizes capital into three tiers. Tier 1 Capital, also known as the Core Capital, which are

the top quality capital for the bank. The Components include: Paid up capital, general and

statutory reserves, retained earnings, minority interest, non-cumulative preference shares, etc.

Tier 2 Capital, also known as supplementary capital, supports Tier 1 capital. Components

include: general provision; revaluation reserves for Fixed Assets, Securities and equity

investments; other preference shares and subordinated debt. Tier 3 Capital, also known as

additional supplementary capital, whose components include: short term subordinated debt to

solely guard against market risk. There are more specific guidelines for eligibility of the capital

tiers. To measure adequacy; Capital Adequacy Ratio (CAR) is calculated with Risk Weighted

Asset (RWA) on the basis of credit, market and operational risk.

Banks have to follow the regulatory rules; otherwise BB can impose penalty and/or punishment

as per Bank Company Act of 1991.

Bangladesh Development Bank Limited fulfilled all major requirements of Basel II in the three

consecutive years starting from 2010. It has been maintaining a CAR ratio of above 10%

requirement for the last three years of the compliance. In June 2012 Basel II report to BB,

recorded CAR ratio of 27.26% on actual capital. According to the same report, it has a total

eligible capital of nearly BDT 11,025 million and a Total RWA of nearly BDT 40576 million

whose 10% must be kept as capital, i.e. BDT 4057 million. Thus BDBL has a surplus of capital.

Most of its Tier 1 capital is covered by paid up capital which is high quality and major part of its

Tier 2 capital consists of subordinated debt. BDBL can smoothly implement all the pillars of

Basel II further if the impediments are removed. Data and reporting should be centralized;

reasonable time should be given for report submission, unnecessary complex measures can be

neglected to help banks adopt Basel II.

Basel II Implementation as a Statutory Requirement of Bangladesh Bank: A Study on

Bangladesh Development Bank Limited

Table of Contents Letter of Transmittal ...................................................................................................................... i

Acknowledgement ........................................................................................................................ ii

Executive Summery ..................................................................................................................... iii

Chapter 1: Introduction ................................................................................................................. 1

1.1 Introduction ......................................................................................................................... 2

1.2 Problem Statement .............................................................................................................. 2

1.3 Scope of the report .............................................................................................................. 2

1.4 Objective ............................................................................................................................. 3

1.5 Methodology ....................................................................................................................... 3

1.6 Limitations of the Study...................................................................................................... 4

Chapter 2: Overview of BDBL ..................................................................................................... 5

2.1 BDBL at A Glance .............................................................................................................. 7

2.2 Vision of BDBL .................................................................................................................. 9

2.3 Mission of BDBL ................................................................................................................ 9

2.4 Strategic priorities of BDBL ............................................................................................... 9

2.5 Values of BDBL ............................................................................................................... 10

2.6 Management of BDBL ...................................................................................................... 10

2.7 Functions of BDBL ........................................................................................................... 10

2.8 Organizational Structure ................................................................................................... 11

Chapter 3: Literary Review ........................................................................................................ 12

Chapter 4: Basel II Framework .................................................................................................. 15

4.1 Structure of Basel II .......................................................................................................... 17

4.1.1 Pillar 1 – Minimum Capital Requirements ................................................................ 18

4.1.2 Pillar 2 – Supervisory Review Process ...................................................................... 18

4.1.3 Pillar 3 – Market Discipline ....................................................................................... 18

4.2 Scope of Application......................................................................................................... 19

4.3 Pillar I-Minimum Capital Requirements .......................................................................... 19

4.3 Conditions for Maintaining Regulatory Capital ............................................................... 21

4.4 Eligible Regulatory Capital............................................................................................... 21

4.5 Minimum Capital Requirement (MCR) ............................................................................ 22

4.6 Total Risk Weighted Assets (RWA) ................................................................................. 22

Basel II Implementation as a Statutory Requirement of Bangladesh Bank: A Study on

Bangladesh Development Bank Limited

4.7 Capital Charge against Credit Risk ................................................................................... 23

4.8 Capital Charge against Market Risk ................................................................................. 23

Measurement Methodology ................................................................................................. 24

Capital charges for Specific risk ......................................................................................... 24

Capital charge for General Market risk ............................................................................... 24

Capital Charges for Equity Position Risk ........................................................................... 24

Capital Charges for Foreign Exchange Risk ....................................................................... 25

4.9 Capital Charge against Operational Risk .......................................................................... 25

Measurement Methodology ................................................................................................. 25

4.10 Pillar-II Supervisory Review Process ............................................................................. 26

4.11 Internal Capital Adequacy Assessment Process (ICAAP).............................................. 26

4.12 Supervisory Review Evaluation Process (SREP) ........................................................... 27

4.13 Stress Testing .................................................................................................................. 27

4.14 Pillar 3 Market Discipline ............................................................................................... 29

Disclosure Requirements ..................................................................................................... 29

Chapter 5: Mechanisms for Measuring Credit, Market and Operational Risk ........................... 30

5.1 Bangladesh Bank guideline regarding Basel-II ................................................................ 31

5.2 Credit Risk ........................................................................................................................ 31

Standardized approach: ....................................................................................................... 32

5.3 Operational Risk ............................................................................................................... 34

Basic indicator approach or BIA: ........................................................................................ 35

5.4 Market risk ........................................................................................................................ 35

Value at Risk: ...................................................................................................................... 35

Chapter 6: Analysis of Basel II Components in the Annual Report of BDBL ........................... 37

6.1 Tier 1 capital ..................................................................................................................... 39

6.2 Tier 2 Capital .................................................................................................................... 39

6.3 Tier 3 Capital .................................................................................................................... 40

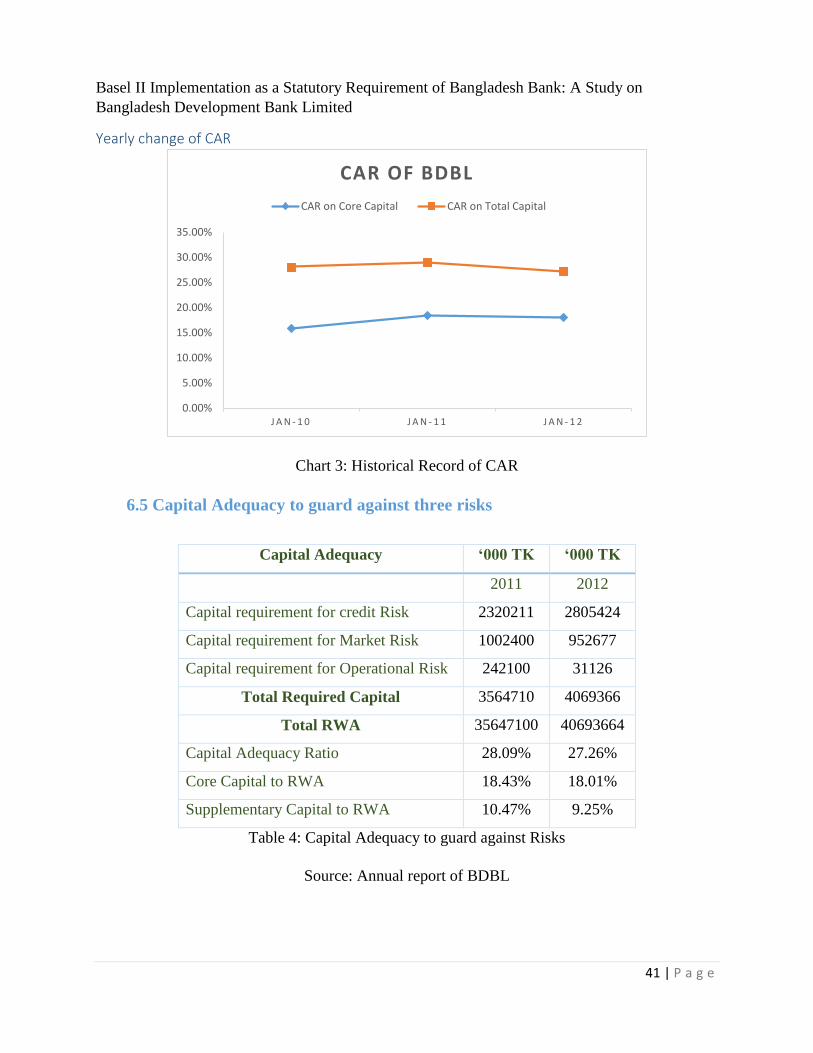

6.4 Capital Adequacy of BDBL .............................................................................................. 40

Yearly change of CAR ........................................................................................................ 41

6.5 Capital Adequacy to guard against three risks .................................................................. 41

Basel II Implementation as a Statutory Requirement of Bangladesh Bank: A Study on

Bangladesh Development Bank Limited

Chapter 7: Compliance of Financial Disclosure with Basel II ................................................... 43

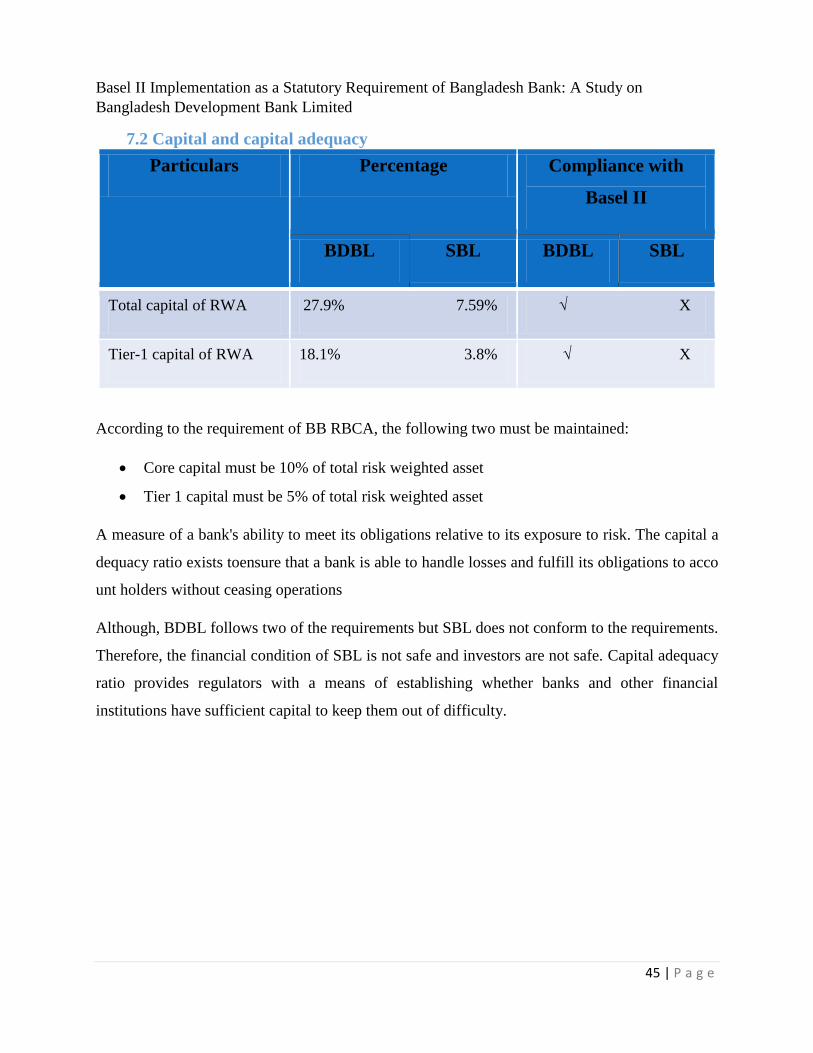

7.1 Regulatory capital ............................................................................................................. 44

7.2 Capital and capital adequacy ............................................................................................ 45

7.3 Mechanism used for risk weights ..................................................................................... 46

7.4 Pillar-2 (Supervisory review) ............................................................................................ 46

7.5 Pillar-3 (Market Disclosure) ............................................................................................. 47

Analysis of Findings ................................................................................................................... 48

Conclusion & Recommendation ................................................................................................. 49

References ................................................................................................................................... iv

Appendix ...................................................................................................................................... v

Basel II Implementation as a Statutory Requirement of Bangladesh Bank: A Study on

Bangladesh Development Bank Limited

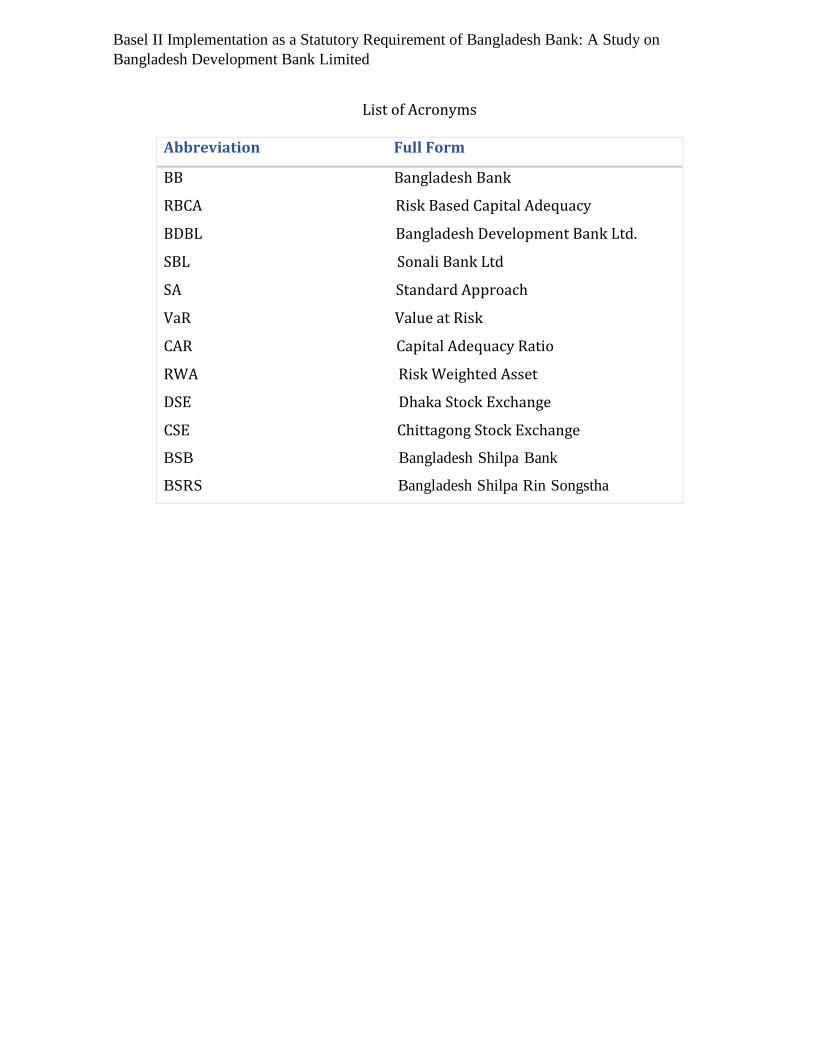

List of Acronyms

Abbreviation Full Form

BB Bangladesh Bank

RBCA Risk Based Capital Adequacy

BDBL Bangladesh Development Bank Ltd.

SBL Sonali Bank Ltd

SA Standard Approach

VaR Value at Risk

CAR Capital Adequacy Ratio

RWA Risk Weighted Asset

DSE Dhaka Stock Exchange

CSE Chittagong Stock Exchange

BSB Bangladesh Shilpa Bank

BSRS Bangladesh Shilpa Rin Songstha

Basel II Implementation as a Statutory Requirement of Bangladesh Bank: A Study on

Bangladesh Development Bank Limited

1 | P a g e

Chapter 1:

Introduction

Basel II Implementation as a Statutory Requirement of Bangladesh Bank: A Study on

Bangladesh Development Bank Limited

2 | P a g e

1.1 Introduction

Bangladesh Bank (BB) is the central bank of Bangladesh and governs all the active performing

commercial banks in the country. Considering the persistent complexity and diversity in the

banking industry and to make the bank’s capital more risk sensitive and shock absorbent,

Bangladesh Bank has introduced Risk Based Capital Adequacy guideline relating to the Basel II

Accord. In compliance to international standards Bangladesh Bank has made the guidelines

statutory for all scheduled banks in Bangladesh from January 01, 2010. These guidelines are

structured on three Pillars namely Pillar 1: Minimum capital requirements to be maintained by a

bank against credit, market, and operational risks, Pillar 2: Process for assessing the overall

capital adequacy aligned with risk profile of a bank as well as capital growth plan, Pillar 3:

Framework of public disclosure on the position of a bank's risk profiles, capital adequacy, and

risk management system. There are three main risks that a commercial bank faces- Credit risk,

Market risk and Operational risk. In the report, I use the Basel II framework for analyzing the

compliance issue of BDBL and compare it with another bank.

1.2 Problem Statement

From January 10, 2010, Bangladesh Bank has made the guidelines to follow the Basel II accord

a statutory requirement for all scheduled banks in Bangladesh. It was instructed by the central

bank to maintain a capital of 10% against its risk weighted assets to guard itself against the risk

of credit, market and operations. This report is done to figure out how Basel II is implemented

by BDBL following the guidelines provided by Bangladesh Bank.

1.3 Scope of the report

This report only talks about Basel II implementation of BDBL. This report has been prepared

using utmost caution, but the complexity of Basel II regulation is very well known. The report

can be a primary reading for anyone who is new to banking industry or wants to know about

regulatory requirement or someone who wants to study Basel II.

Under no circumstances can this report be the sole material or absolute alternative to the original

BB requirement for anyone who wants to know the ins and outs of Basel II or work with Basel

II regulation. For full knowledge of Basel II, the reader must refer back to “Guidelines on Risk

Basel II Implementation as a Statutory Requirement of Bangladesh Bank: A Study on

Bangladesh Development Bank Limited

3 | P a g e

Based Capital Adequacy (Revised Regulatory Capital Framework for banks in line with Basel

II)”, the main text released by BB in December, 2010.

1.4 Objective

The primary objectives of the report are to fulfill the academic requirement of preparing an

internship report during my internship which is required for the completion of MBA degree under

Dhaka University, and to enhance my knowledge base by probing into the details of Basel II

accord and how BDBL sails through the required criteria’s, and how the central bank of

Bangladesh regulates the industry through Basel II. The report goes into explaining the ways

BDBL allocates its credit capital, disclosure of market information and the coordination of Risk.

Some Specific objectives of the report are:

Learning the regulatory requirements of Basel II and having an working experience in the

Risk Management Department of BDBL

Applying the acquired knowledge of Basel II in the preparation of Basel II report of

BDBL which needs to be reported in BB in a regular interval

Knowing the mechanisms of calculating different types of capital (such as-tire 1, tire2

and tire 3) and analyze the financial statement of BDBL

Learning the methodologies of enumerating risks (such as- credit risk, market risk and

operational risk) to analyze the financial report of BDBL

Having a knowledge to calculate risk weighted asset according to Bangladesh Bank

guidelines which is regarded as a basement for calculating Capital Adequacy Ratio

Compare the compliance of Basel II of BDBL with SBL

1.5 Methodology

For my internship report I have collected data from both the Primary sources and the secondary

sources.

Primary data: I got the data or information through the following ways-

Directly from the employees

The head of the departments, and

Basel II Implementation as a Statutory Requirement of Bangladesh Bank: A Study on

Bangladesh Development Bank Limited

4 | P a g e

Basel II Implementation by BDBL following the statutory requirements of Bangladesh

Bank by observing the environmental behavior, facts, record and present condition of the

industry.

Secondary data: I have collected the secondary data through annual reports of BDBL, market

disclosure reports of BDBL, annual reports of SBL, online newspaper articles from The Daily

Star and The Financial Express, various informative websites etc.

1.6 Limitations of the Study

I have dedicated my entire efforts to enrich and complete this report although there are some

limitations which are as follows:

Basel II is a comparatively newer regulation posed on banks compared to the others

regulations from Bangladesh Bank; therefore few employees have sufficient information

about it.

Basel III has not been yet proposed for implementation by Bangladesh Bank.

Bank employees are extremely busy with transactions and other purposed therefore the

time that could be managed from was not enough.

Unfortunately due to the Banks limitations (business secrecy and confidentiality), I was

unable to acquire sufficient information.

Personal barriers such as inability to understand some official terms, office decorum

created a few problems for me.

Time was also a limitation. Gathering such an amount of information by only working

for three months was an extremely difficult job.

Basel II Implementation as a Statutory Requirement of Bangladesh Bank: A Study on

Bangladesh Development Bank Limited

5 | P a g e

Chapter 2:

Overview of BDBL

Basel II Implementation as a Statutory Requirement of Bangladesh Bank: A Study on

Bangladesh Development Bank Limited

6 | P a g e

Non- Bengali entrepreneurs and the public sector nearly monopolized economic activity in

Pakistan era. Of the very few business professionals are active in East Pakistan fewer yet

survived after the war. Post- independence Bangladesh therefore presented a unique set of

opportunities and the problems for the private sector. The good news was that without the

stranglehold of the elite Pakistan business family the field was wide open for the development

of a homegrown Bengali private sector, but that both a capital base and an entirely new

entrepreneurial class would have to be development out of an economic vacuum.

Capital formation rapidly occurred and the newly nationalized banks found themselves with

serious asset management problem because there were few professional entrepreneurial risk

takers with business skills and proven track records to which this capital could be made

available under normal and prudent banking practice.

Under this sort of circumstances, the former Industrial Development Bank of Pakistan (IDBP)

and the Equity Participation Fund (EDF) both of which were established for the industrial

development of Pakistan were converted into singles institution named Bangladesh Shilpa Bank

come to existence on October 31, 1972 by the promulgation of Bangladesh Shilpa Bank order

1972 (president’s order no 129 of 1972). The BSB order, 1972 was amended subsequently

by the parliament to provide more operational autonomy to its management.

BSB & BSRS have played an important role for industrializing the country from 1972 to 31

November 2009. At present in rival banking sector, there is no substitute way without

making versatility in the customer service along with long term loan facilities. It is hoped that by

joining this two institutions via lending activity by making BDBL to achieve Economies of

scale to spread market boundary to increase rivalry & liquid State of money will be

sustainable.

Bangladesh Development Bank Limited has been established to give short term & long term

loan for the development of communication & utility, to develop infrastructural facilities &

to keep role in international business according to t h e company act 1991. It is not only a

development bank but also a commercial bank. So it would execute its activities under the

company’s law &banking companies act.

Basel II Implementation as a Statutory Requirement of Bangladesh Bank: A Study on Bangladesh

Development Bank Limited

7 | P a g e

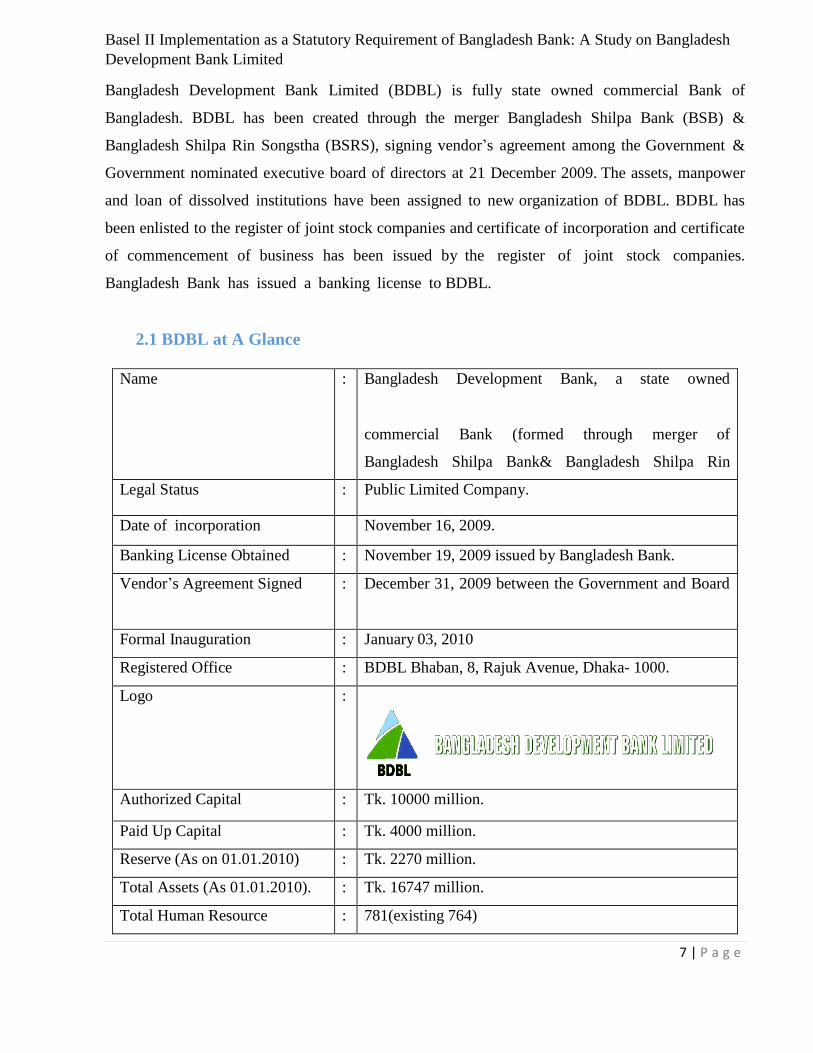

Bangladesh Development Bank Limited (BDBL) is fully state owned commercial Bank of

Bangladesh. BDBL has been created through the merger Bangladesh Shilpa Bank (BSB) &

Bangladesh Shilpa Rin Songstha (BSRS), signing vendor’s agreement among the Government &

Government nominated executive board of directors at 21 December 2009. The assets, manpower

and loan of dissolved institutions have been assigned to new organization of BDBL. BDBL has

been enlisted to the register of joint stock companies and certificate of incorporation and certificate

of commencement of business has been issued by the register of joint stock companies.

Bangladesh Bank has issued a banking license to BDBL.

2.1 BDBL at A Glance

Name : Bangladesh Development Bank, a state owned

commercial Bank (formed through merger of

Bangladesh Shilpa Bank& Bangladesh Shilpa Rin

Sangetha). Legal Status : Public Limited Company.

Date of incorporation November 16, 2009.

Banking License Obtained : November 19, 2009 issued by Bangladesh Bank.

Vendor’s Agreement Signed : December 31, 2009 between the Government and Board

of Directors of BDBL nominated by the Government. Formal Inauguration : January 03, 2010

Registered Office : BDBL Bhaban, 8, Rajuk Avenue, Dhaka- 1000.

Logo :

Authorized Capital : Tk. 10000 million.

Paid Up Capital : Tk. 4000 million.

Reserve (As on 01.01.2010) : Tk. 2270 million.

Total Assets (As 01.01.2010). : Tk. 16747 million.

Total Human Resource : 781(existing 764)

Basel II Implementation as a Statutory Requirement of Bangladesh Bank: A Study on Bangladesh

Development Bank Limited

8 | P a g e

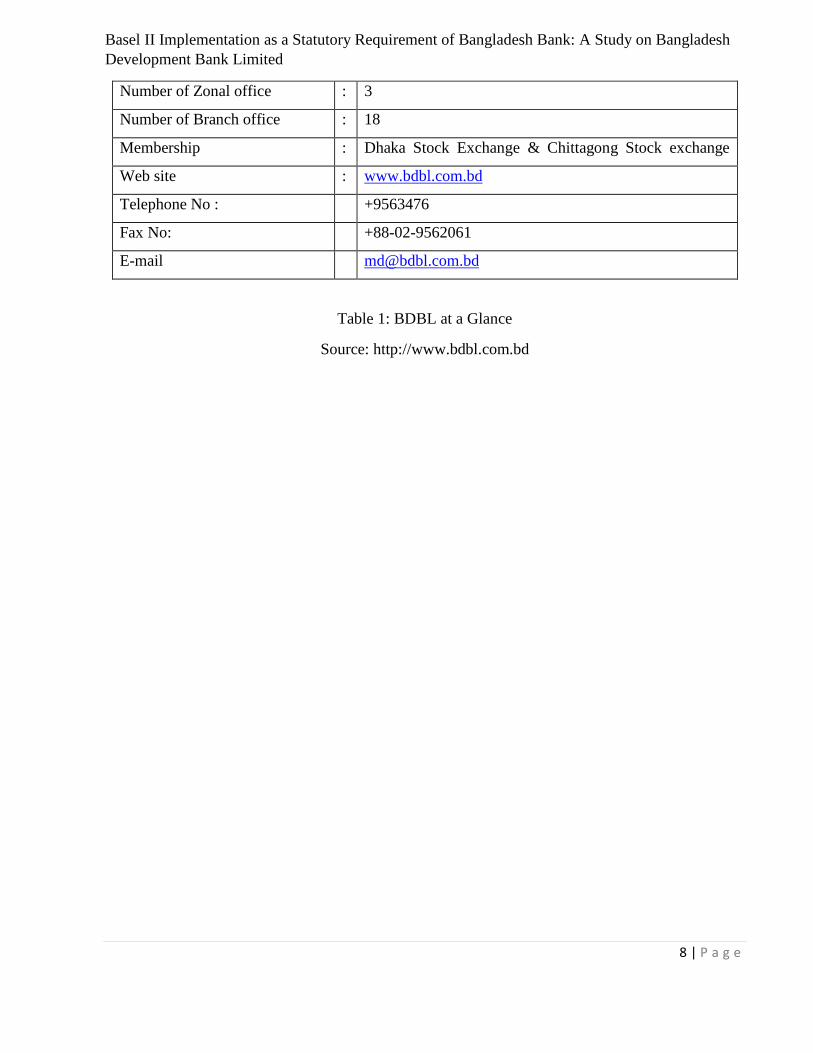

Number of Zonal office : 3

Number of Branch office : 18

Membership : Dhaka Stock Exchange & Chittagong Stock exchange

Ltd.

Web site : www.bdbl.com.bd

Telephone No : +9563476

Fax No: +88-02-9562061

E-mail [email protected]

Table 1: BDBL at a Glance

Source: http://www.bdbl.com.bd

Basel II Implementation as a Statutory Requirement of Bangladesh Bank: A Study on

Bangladesh Development Bank Limited

9 | P a g e

2.2 Vision of BDBL To emerge as the country prime financial institution for supporting private sector industrial

and other projects of great significance to the country’s economic development. Also

be active in commercial banking by introducing new lines of product and providing

excellent services to the customers.

2.3 Mission of BDBL

To be compete with other banks &Financial institutions in rendering services

To contribute to the country’s socio economic development by identifying

new profitable areas for investment.

To mobilize deposit for productive investment.

To expand branch network in commercially & geographically important places.

To employ quality human resources &enhance their capability through motivation

& right type of training at home &abroad.

To delegate maximum authority ensuring proper accountability.

To maintain continuous improvement & up gradation in business polices

& procedures.

To adopt &adapt new technology.

To maximize profit by strong, efficient & prudent financial performance &

To introduce new product lines according to new market needs.

2.4 Strategic priorities of BDBL

Bangladesh Development Bank Limited invest in Eco-friendly industries that help mitigate

environment degradation by lending more for renewable energy and effluent treatment plants

another project that employ energy efficient low-emission technologies including agro- based

industries, small power project, ICT , transport and infrastructure projects.

BDBL select and invest industrial projects where locating advantages like local

availability of raw material, good infrastructural facilities (road construction, road

communication and transport facilities) and utilities (power, gas, water etc.) shall be

available.

Project loans of BDBL are restricted to TK.15 core maximum and TK. 2 core minimum

Basel II Implementation as a Statutory Requirement of Bangladesh Bank: A Study on

Bangladesh Development Bank Limited

10 | P a g e

(for large Project). It arranges and participates in syndicated loan for projects above

TK.15 core.

BDBL identify prospective and potential entrepreneurs and investors or clients and

motivate, guide and help them select profitable industrial ventures for investment.

Economic and research department publish financial disclosures regularly.

It undertakes from time to time SWOT analysis for reviewing bank’s market position

2.5 Values of BDBL

Customer focus- provides smart, efficient, transparent and courteous services.

Social responsibilities- practice corporate social responsibility.

2.6 Management of BDBL

The overall policy formulation and the general direction of Bank’s operation is vested in a

board of directors appointed by the Government. This Board of Directors consists of nine

members including the Chairman and the Managing Director. The Managing Directors is the

Chief Executive Officer (CEO) of the Bank. The General Manager assist the Managing

Director in conducting the overall business of the bank.

2.7 Functions of BDBL BDBL extends term loan facilities in local and foreign currencies to industrial projects (both

new and BMRE) in the private and public sectors. Besides Bank also performs the following

activities:

Provides working capital loans to industrial projects

Provides equity support in the form of underwriting and bridge finance to public

limited companies

Issues guarantees on behalf of borrowers for repayment of loan

Extend commercials banking services along with deposit mobilization

Purchases and sales shares/securities for BDBL and on behalf of customers as member

of DSE Ltd. and CSE Ltd. for capital market development; and

Conducts projects promotional activities along with preparation of various sub-sector

Basel II Implementation as a Statutory Requirement of Bangladesh Bank: A Study on

Bangladesh Development Bank Limited

11 | P a g e

study reports.

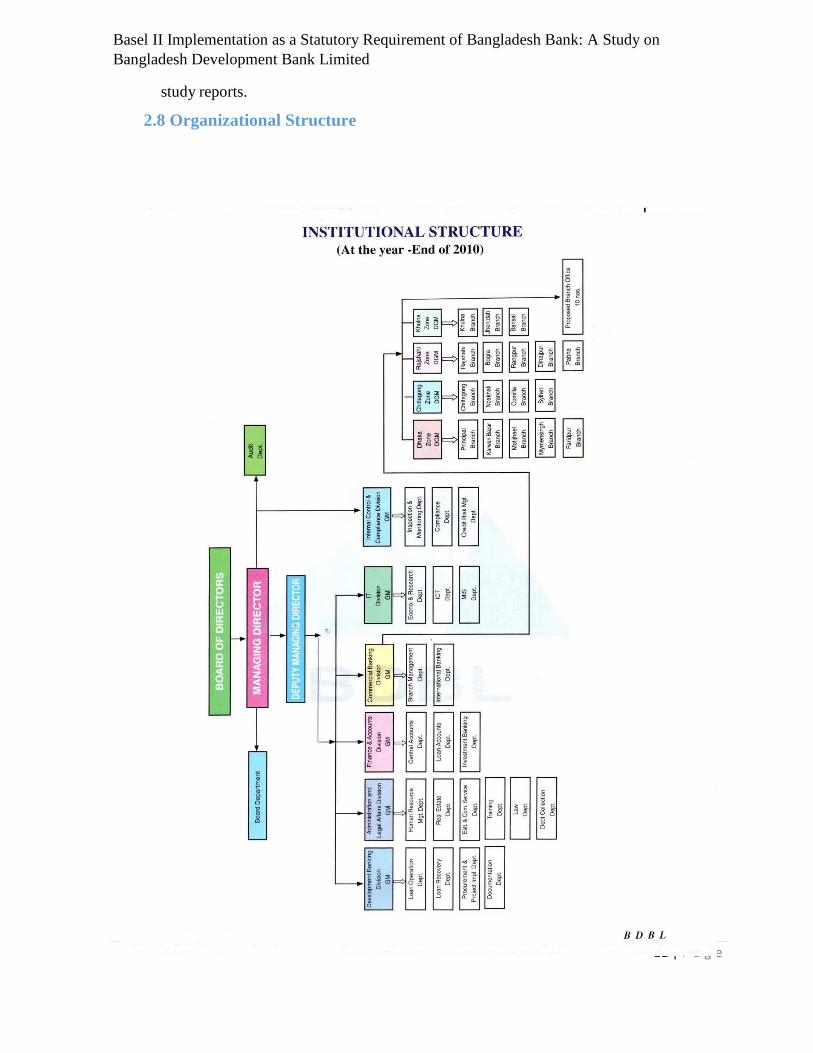

2.8 Organizational Structure

Basel II Implementation as a Statutory Requirement of Bangladesh Bank: A Study on

Bangladesh Development Bank Limited

12 | P a g e

Chapter 3:

Literary Review

Basel II Implementation as a Statutory Requirement of Bangladesh Bank: A Study on

Bangladesh Development Bank Limited

13 | P a g e

In a report titled, ‘Implementation of Basel II and Basel III on Bank Asia Limited Following the

Statutory Requirement of Bangladesh Bank’ Mustaba Risalat Rahman analyzes the compliance of

Basel II and Basel III with the financial report of Bank Asia limited. Historical records of capital

adequacy ratio, risk classification and risk weighted asset calculation is shown in the report.

Capital to guard against three risks is also shown in the report. After analyzing the topic it is

recommended that it is a very complex set of instructions and mathematical terms which demands

a separate department in the bank for its integration purpose and the instructions are very hard to

understand about the global standard regulatory policy or the whole banking industry.

Saif Hossain in the report titled, ‘Basel II Implementation in BRAC Bank Limited: Risk Based

Capital Adequacy Requirement of Bangladesh Bank’ analyze the Pillars of Basel II. He showed

the variations in the historical record to show the variations in keeping capital according to Basel

II accord. The report also discussed some impediments in the compliance with Basel II of BRAC

Bank limited. After analyzing the report the author finds the problems like- Internal data and

reports are not centralized, some of the reporting parts are done by Finance Department and others

are done by the Operational Risk Management (ORM). This issue raises problem in calculation of

various ratios and measures. There is no software specifically modified for Basel II reporting.

Deloitte in the report titled, ‘Understanding the Framework: Adopting the Basel II accord in Asia

Pacific’ shows the regulatory framework of Basel ii. In the report it is shown that although Basel

II is primarily intended for ‘internationally active banks’ among the G–101 countries, many

countries have announced their intention to adopt the Basel II Capital Accord. Bank regulatory

bodies around the world have been studying how Basel II can be incorporated into national

regulations and are developing implementation guidelines and timeframes for compliance. After

analyzing the topic it is shown that Asia Pacific presents a relatively unique situation from a

banking regulation perspective, both in a regional and global context.

In an article by Oracle white paper titled, ‘Key Challenges and Best Practices for Basel II

Implementation’ some major implementation challenges and suggests some of the best practices

Basel II Implementation as a Statutory Requirement of Bangladesh Bank: A Study on

Bangladesh Development Bank Limited

14 | P a g e

that banks can adopt in their pursuit of Basel II compliance and offers recommendations to avoid

the pitfalls. Some major challenges like Multi-jurisdiction Reporting, Data Gap Analysis Study,

Data Quantity Checks and Comprehensive Approach are identified in the report. Basel II

implementation is an opportunity for a bank to improve risk management and ultimately economic

capital management. As stated above, there are many challenges along the way, including

multijurisdictional reporting, data availability and quality, experienced IT resources, solution

completeness, data transparency, solution scalability, flexibility and business intelligence.

Annual disclose of Basel II of some banks like One Bank, DBBL, HSBC and some other banks

show the followings:

Disclosure of three tires of capital

Measurement mechanism of risks

Qualitative and quantitative disclosure of Basel II

Basel II Implementation as a Statutory Requirement of Bangladesh Bank: A Study on

Bangladesh Development Bank Limited

15 | P a g e

Chapter 4:

Basel II Framework

Basel II Implementation as a Statutory Requirement of Bangladesh Bank: A Study on

Bangladesh Development Bank Limited

16 | P a g e

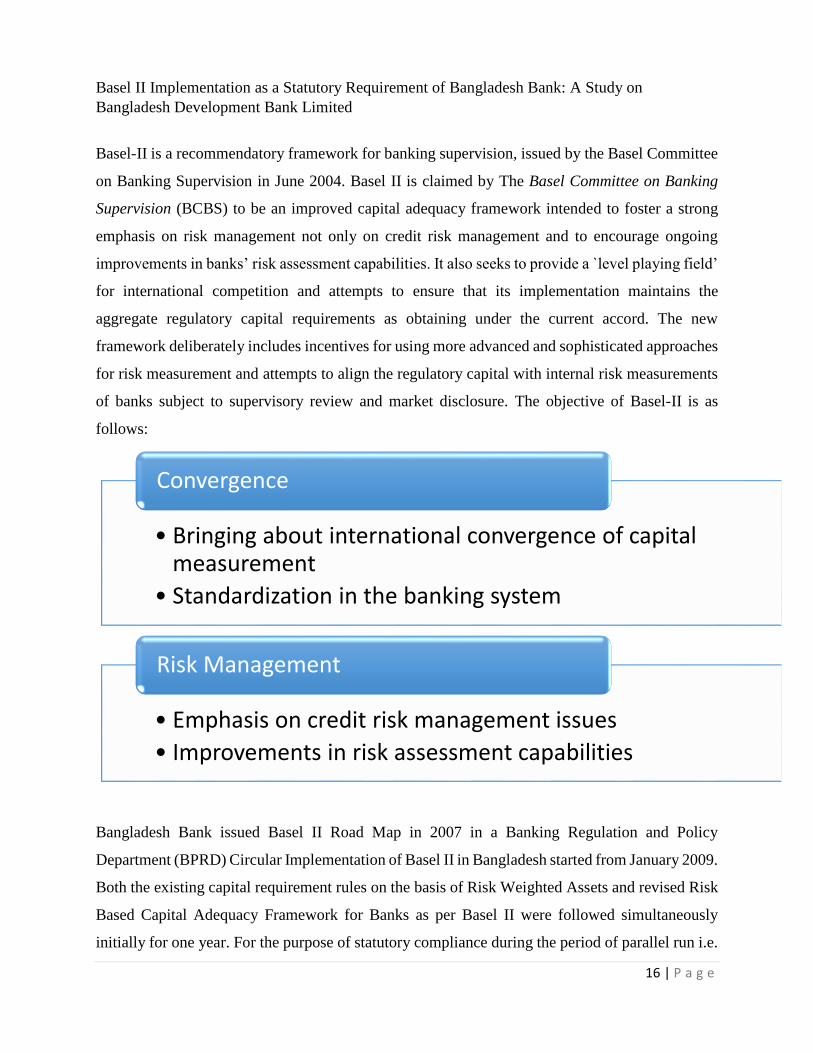

Basel-II is a recommendatory framework for banking supervision, issued by the Basel Committee

on Banking Supervision in June 2004. Basel II is claimed by The Basel Committee on Banking

Supervision (BCBS) to be an improved capital adequacy framework intended to foster a strong

emphasis on risk management not only on credit risk management and to encourage ongoing

improvements in banks’ risk assessment capabilities. It also seeks to provide a `level playing field’

for international competition and attempts to ensure that its implementation maintains the

aggregate regulatory capital requirements as obtaining under the current accord. The new

framework deliberately includes incentives for using more advanced and sophisticated approaches

for risk measurement and attempts to align the regulatory capital with internal risk measurements

of banks subject to supervisory review and market disclosure. The objective of Basel-II is as

follows:

Bangladesh Bank issued Basel II Road Map in 2007 in a Banking Regulation and Policy

Department (BPRD) Circular Implementation of Basel II in Bangladesh started from January 2009.

Both the existing capital requirement rules on the basis of Risk Weighted Assets and revised Risk

Based Capital Adequacy Framework for Banks as per Basel II were followed simultaneously

initially for one year. For the purpose of statutory compliance during the period of parallel run i.e.

• Bringing about international convergence of capital measurement

• Standardization in the banking system

Convergence

• Emphasis on credit risk management issues

• Improvements in risk assessment capabilities

Risk Management

Basel II Implementation as a Statutory Requirement of Bangladesh Bank: A Study on

Bangladesh Development Bank Limited

17 | P a g e

2009, the computation of capital adequacy requirement under existing rules prevailed. On the other

hand, revised Risk Based Capital Adequacy Framework as per Basel II had been practiced by the

banks during 2009 so that Basel II recommendation could effectively be adopted from 2010. From

January 2010, Risk Based Capital Adequacy Framework as per Basel II have been fully practiced

by the banks replacing the previous rules under Basel-I. This has begun an endeavor towards more

improved and risk sensitive capital requirement than the previous regulation.

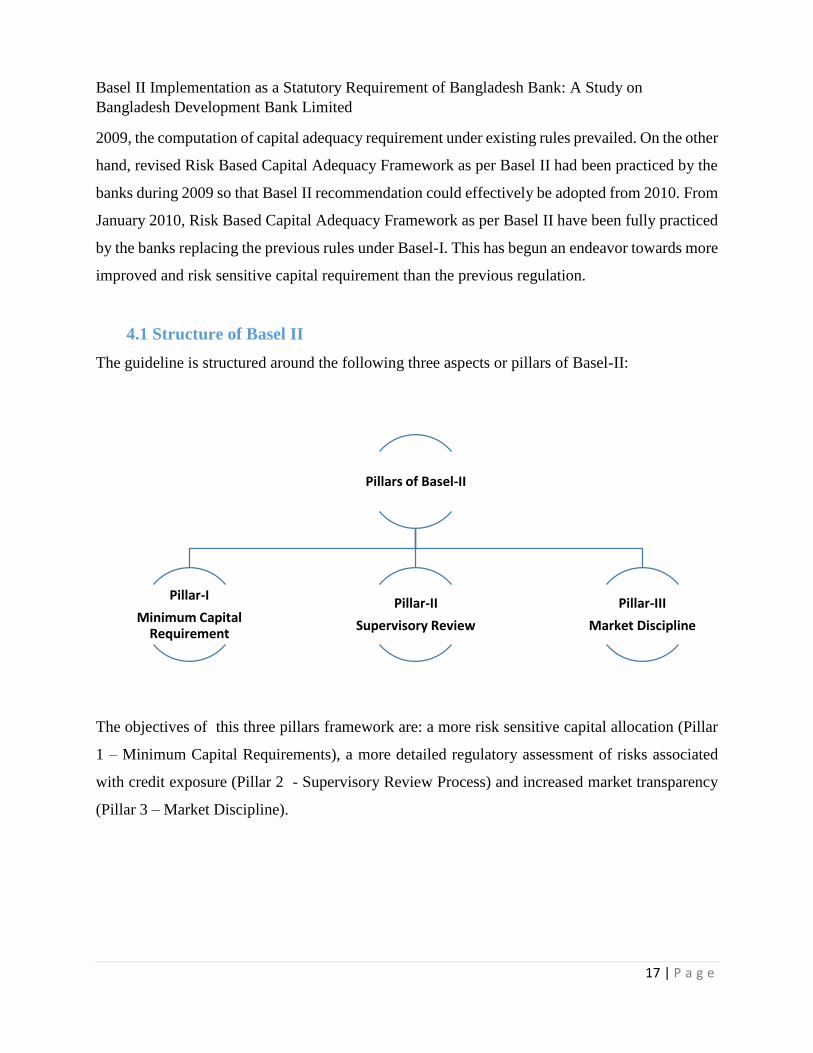

4.1 Structure of Basel II

The guideline is structured around the following three aspects or pillars of Basel-II:

The objectives of this three pillars framework are: a more risk sensitive capital allocation (Pillar

1 – Minimum Capital Requirements), a more detailed regulatory assessment of risks associated

with credit exposure (Pillar 2 - Supervisory Review Process) and increased market transparency

(Pillar 3 – Market Discipline).

Pillars of Basel-II

Pillar-I

Minimum Capital Requirement

Pillar-II

Supervisory Review

Pillar-III

Market Discipline

Basel II Implementation as a Statutory Requirement of Bangladesh Bank: A Study on

Bangladesh Development Bank Limited

18 | P a g e

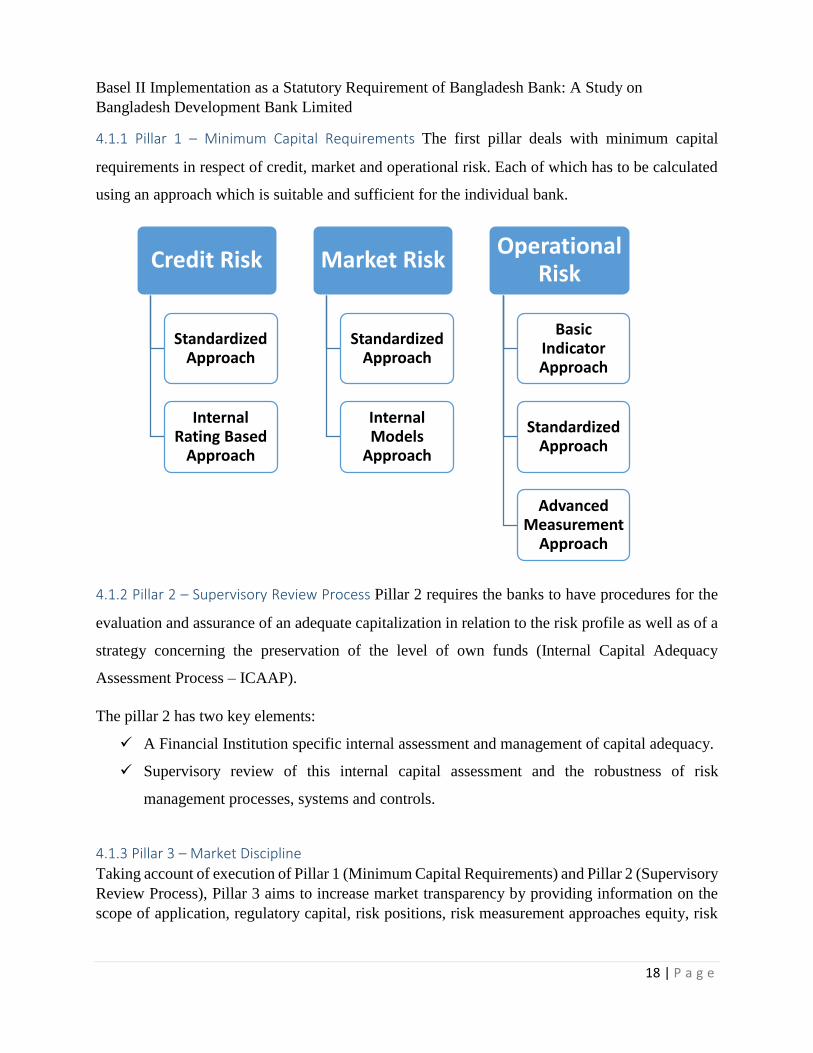

4.1.1 Pillar 1 – Minimum Capital Requirements The first pillar deals with minimum capital

requirements in respect of credit, market and operational risk. Each of which has to be calculated

using an approach which is suitable and sufficient for the individual bank.

4.1.2 Pillar 2 – Supervisory Review Process Pillar 2 requires the banks to have procedures for the

evaluation and assurance of an adequate capitalization in relation to the risk profile as well as of a

strategy concerning the preservation of the level of own funds (Internal Capital Adequacy

Assessment Process – ICAAP).

The pillar 2 has two key elements:

A Financial Institution specific internal assessment and management of capital adequacy.

Supervisory review of this internal capital assessment and the robustness of risk

management processes, systems and controls.

4.1.3 Pillar 3 – Market Discipline

Taking account of execution of Pillar 1 (Minimum Capital Requirements) and Pillar 2 (Supervisory

Review Process), Pillar 3 aims to increase market transparency by providing information on the

scope of application, regulatory capital, risk positions, risk measurement approaches equity, risk

Credit Risk

Standardized Approach

Internal Rating Based

Approach

Market Risk

Standardized Approach

Internal Models

Approach

Operational Risk

Basic Indicator Approach

Standardized Approach

Advanced Measurement

Approach

Basel II Implementation as a Statutory Requirement of Bangladesh Bank: A Study on

Bangladesh Development Bank Limited

19 | P a g e

positions, the IRB (Internal Rating Based)-Approach and as a result the capital requirements of a

bank.

4.2 Scope of Application

This Risk Based Capital Adequacy framework applies to all banks on ‘Solo’ as well as on

‘Consolidated’ basis where- ‘Solo Basis’ refers to all position of the bank and its local and overseas branches/offices.

‘Consolidated Basis’ refers to all position of the bank (including its local and overseas

branches/offices) and its subsidiary company(s) like brokerage firms, discount houses, etc.

(if any).

4.3 Pillar I-Minimum Capital Requirements Basel Committee and Bangladesh Bank agree that some minimum capital must be maintained to

make banks and depository institutions more risk sensitive and shock resilient. Bangladesh Bank

laid out guidelines about the capital that can be and should be counted in calculating Capital

Adequacy Ratio (CAR).

Capital Base

Basel-II accord describes three-tier capital concept with a view to complying with the requirements

which are designed to encourage the banks to strengthen their capital positions considering their

risk, supervisory review process and market discipline. In Basel-II accord, the total capital of a

banking company has been segregated as Tier - I capital, Tier - II capital and Tier - III capital.

Basel II Implementation as a Statutory Requirement of Bangladesh Bank: A Study on

Bangladesh Development Bank Limited

20 | P a g e

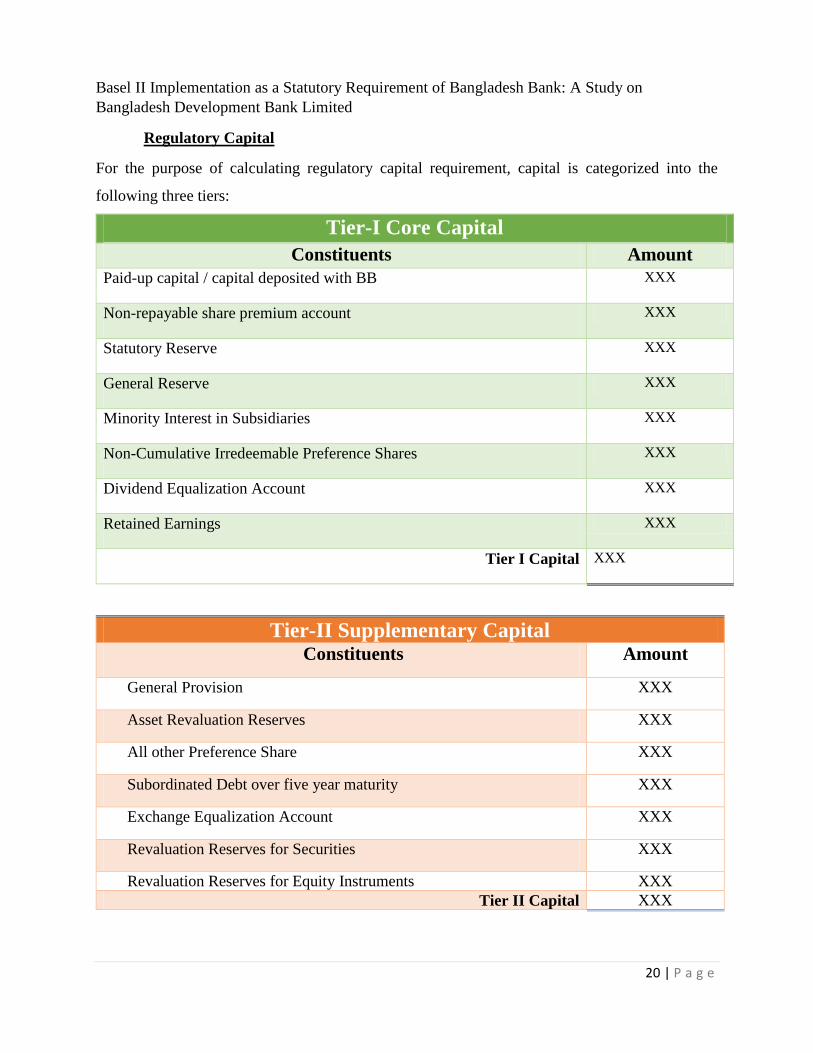

Regulatory Capital

For the purpose of calculating regulatory capital requirement, capital is categorized into the

following three tiers:

Tier-I Core Capital

Constituents Amount

Paid-up capital / capital deposited with BB XXX

Non-repayable share premium account XXX

Statutory Reserve XXX

General Reserve XXX

Minority Interest in Subsidiaries XXX

Non-Cumulative Irredeemable Preference Shares XXX

Dividend Equalization Account XXX

Retained Earnings XXX

Tier I Capital XXX

Tier-II Supplementary Capital Constituents Amount

General Provision XXX

Asset Revaluation Reserves XXX

All other Preference Share XXX

Subordinated Debt over five year maturity XXX

Exchange Equalization Account XXX

Revaluation Reserves for Securities XXX

Revaluation Reserves for Equity Instruments XXX

Tier II Capital XXX

Basel II Implementation as a Statutory Requirement of Bangladesh Bank: A Study on

Bangladesh Development Bank Limited

21 | P a g e

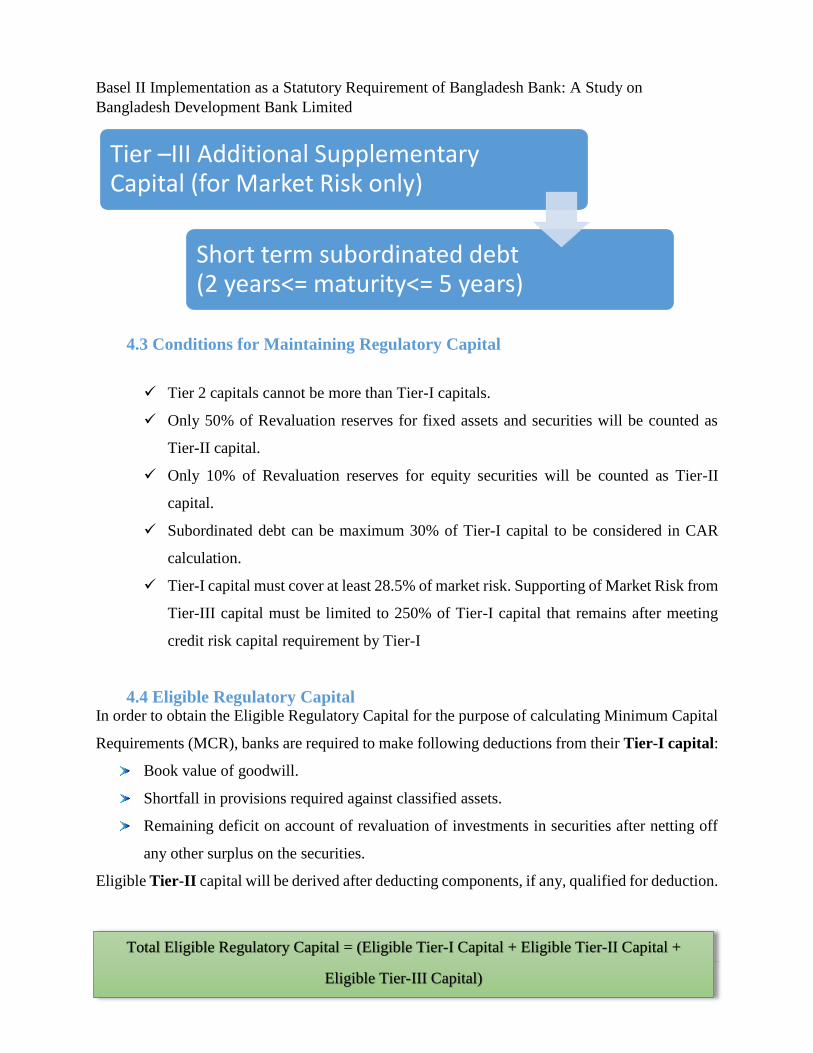

4.3 Conditions for Maintaining Regulatory Capital

Tier 2 capitals cannot be more than Tier-I capitals.

Only 50% of Revaluation reserves for fixed assets and securities will be counted as

Tier-II capital.

Only 10% of Revaluation reserves for equity securities will be counted as Tier-II

capital.

Subordinated debt can be maximum 30% of Tier-I capital to be considered in CAR

calculation.

Tier-I capital must cover at least 28.5% of market risk. Supporting of Market Risk from

Tier-III capital must be limited to 250% of Tier-I capital that remains after meeting

credit risk capital requirement by Tier-I

4.4 Eligible Regulatory Capital In order to obtain the Eligible Regulatory Capital for the purpose of calculating Minimum Capital

Requirements (MCR), banks are required to make following deductions from their Tier-I capital:

Book value of goodwill.

Shortfall in provisions required against classified assets.

Remaining deficit on account of revaluation of investments in securities after netting off

any other surplus on the securities.

Eligible Tier-II capital will be derived after deducting components, if any, qualified for deduction.

Tier –III Additional Supplementary Capital (for Market Risk only)

Short term subordinated debt (2 years<= maturity<= 5 years)

Total Eligible Regulatory Capital = (Eligible Tier-I Capital + Eligible Tier-II Capital +

Eligible Tier-III Capital)

Basel II Implementation as a Statutory Requirement of Bangladesh Bank: A Study on

Bangladesh Development Bank Limited

22 | P a g e

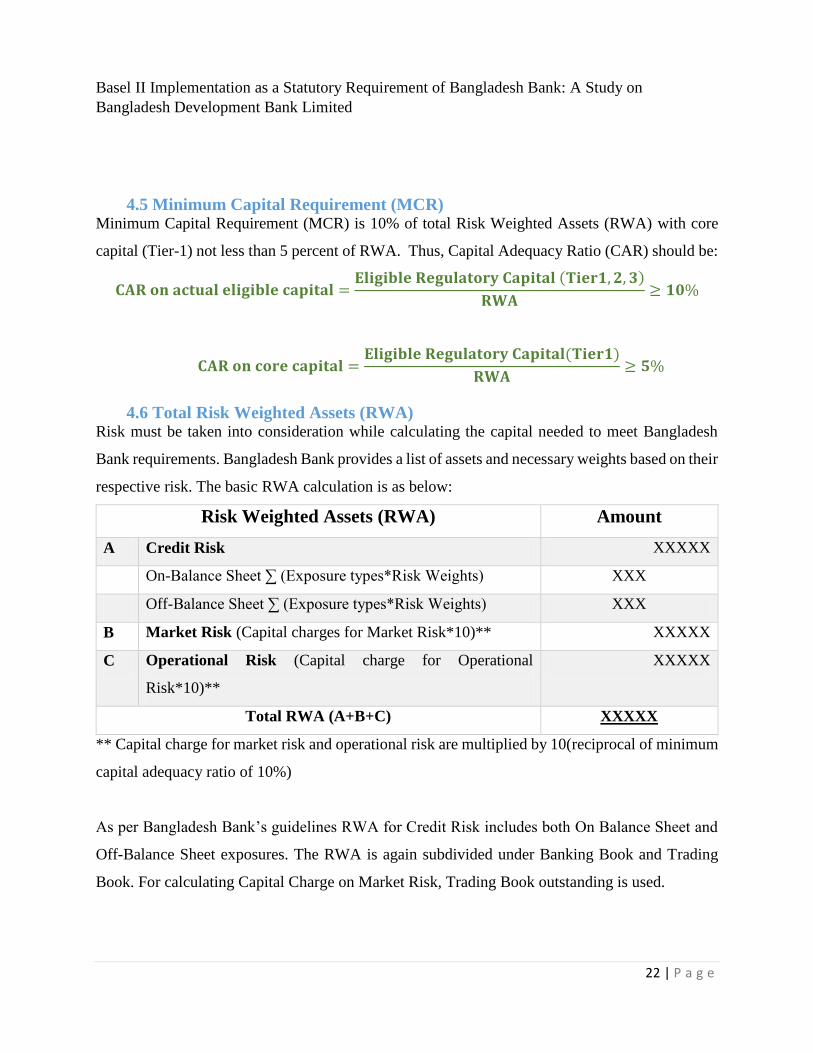

4.5 Minimum Capital Requirement (MCR) Minimum Capital Requirement (MCR) is 10% of total Risk Weighted Assets (RWA) with core

capital (Tier-1) not less than 5 percent of RWA. Thus, Capital Adequacy Ratio (CAR) should be:

𝐂𝐀𝐑 𝐨𝐧 𝐚𝐜𝐭𝐮𝐚𝐥 𝐞𝐥𝐢𝐠𝐢𝐛𝐥𝐞 𝐜𝐚𝐩𝐢𝐭𝐚𝐥 =𝐄𝐥𝐢𝐠𝐢𝐛𝐥𝐞 𝐑𝐞𝐠𝐮𝐥𝐚𝐭𝐨𝐫𝐲 𝐂𝐚𝐩𝐢𝐭𝐚𝐥 (𝐓𝐢𝐞𝐫𝟏, 𝟐, 𝟑)

𝐑𝐖𝐀≥ 𝟏𝟎%

𝐂𝐀𝐑 𝐨𝐧 𝐜𝐨𝐫𝐞 𝐜𝐚𝐩𝐢𝐭𝐚𝐥 =𝐄𝐥𝐢𝐠𝐢𝐛𝐥𝐞 𝐑𝐞𝐠𝐮𝐥𝐚𝐭𝐨𝐫𝐲 𝐂𝐚𝐩𝐢𝐭𝐚𝐥(𝐓𝐢𝐞𝐫𝟏)

𝐑𝐖𝐀≥ 𝟓%

4.6 Total Risk Weighted Assets (RWA) Risk must be taken into consideration while calculating the capital needed to meet Bangladesh

Bank requirements. Bangladesh Bank provides a list of assets and necessary weights based on their

respective risk. The basic RWA calculation is as below:

Risk Weighted Assets (RWA) Amount

A Credit Risk XXXXX

On-Balance Sheet ∑ (Exposure types*Risk Weights) XXX

Off-Balance Sheet ∑ (Exposure types*Risk Weights) XXX

B Market Risk (Capital charges for Market Risk*10)** XXXXX

C Operational Risk (Capital charge for Operational

Risk*10)**

XXXXX

Total RWA (A+B+C) XXXXX

** Capital charge for market risk and operational risk are multiplied by 10(reciprocal of minimum

capital adequacy ratio of 10%)

As per Bangladesh Bank’s guidelines RWA for Credit Risk includes both On Balance Sheet and

Off-Balance Sheet exposures. The RWA is again subdivided under Banking Book and Trading

Book. For calculating Capital Charge on Market Risk, Trading Book outstanding is used.

Basel II Implementation as a Statutory Requirement of Bangladesh Bank: A Study on

Bangladesh Development Bank Limited

23 | P a g e

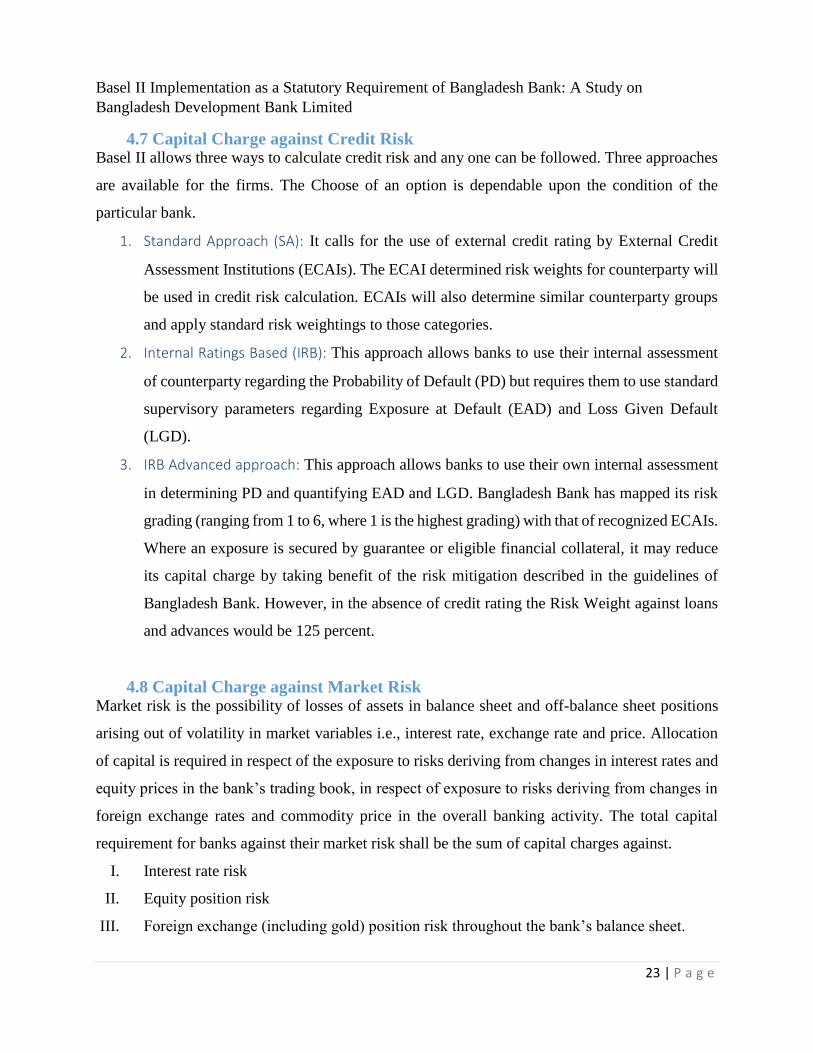

4.7 Capital Charge against Credit Risk Basel II allows three ways to calculate credit risk and any one can be followed. Three approaches

are available for the firms. The Choose of an option is dependable upon the condition of the

particular bank.

1. Standard Approach (SA): It calls for the use of external credit rating by External Credit

Assessment Institutions (ECAIs). The ECAI determined risk weights for counterparty will

be used in credit risk calculation. ECAIs will also determine similar counterparty groups

and apply standard risk weightings to those categories.

2. Internal Ratings Based (IRB): This approach allows banks to use their internal assessment

of counterparty regarding the Probability of Default (PD) but requires them to use standard

supervisory parameters regarding Exposure at Default (EAD) and Loss Given Default

(LGD).

3. IRB Advanced approach: This approach allows banks to use their own internal assessment

in determining PD and quantifying EAD and LGD. Bangladesh Bank has mapped its risk

grading (ranging from 1 to 6, where 1 is the highest grading) with that of recognized ECAIs.

Where an exposure is secured by guarantee or eligible financial collateral, it may reduce

its capital charge by taking benefit of the risk mitigation described in the guidelines of

Bangladesh Bank. However, in the absence of credit rating the Risk Weight against loans

and advances would be 125 percent.

4.8 Capital Charge against Market Risk Market risk is the possibility of losses of assets in balance sheet and off-balance sheet positions

arising out of volatility in market variables i.e., interest rate, exchange rate and price. Allocation

of capital is required in respect of the exposure to risks deriving from changes in interest rates and

equity prices in the bank’s trading book, in respect of exposure to risks deriving from changes in

foreign exchange rates and commodity price in the overall banking activity. The total capital

requirement for banks against their market risk shall be the sum of capital charges against. I. Interest rate risk

II. Equity position risk

III. Foreign exchange (including gold) position risk throughout the bank’s balance sheet.

Basel II Implementation as a Statutory Requirement of Bangladesh Bank: A Study on

Bangladesh Development Bank Limited

24 | P a g e

Measurement Methodology

As banks in Bangladesh are now in a stage of developing risk management models, Bangladesh

Bank suggested the banks for using Standardized Approach for credit risk capital requirement for

banking book and Standardized (rule based) Approach for market risk capital charge in their

trading book. Maturity Method has been prescribed by Bangladesh Bank in determining capital

against market risk. In Standardized (rule based) Approach the capital requirement for various

market risks (interest rate risk, price, and foreign exchange risk) is determined separately. The total

capital requirement in respect of market risk is the sum of capital requirement calculated for each

of these market risk sub-categories. e.g.

a) Capital Charge for Interest Rate Risk = Capital Charge for Specific Risk + Capital Charge

for General Market Risk

b) Capital Charge for Equity Position Risk = Capital Charge for Specific Risk + Capital

Charge for General Market Risk

c) Capital Charge for Foreign Exchange Risk = Capital Charge for General Market Risk

d) Capital Charge for Commodity Position Risk = Capital Charge for General Market Risk

The methodology to calculate capital requirement under Standardized (rule based) Approach for

each of these market risk categories is as follows:

Capital charges for Specific risk

Capital charge for specific risk against interest related instruments is designed to protect against

an adverse movement in the price of an individual security owing to factors related to the individual

issuer.

Capital charge for General Market risk

The capital requirement for general market risk is designed to capture the risk of loss arising from

changes in market interest rates.

Capital Charges for Equity Position Risk

I. As with debt securities, the minimum capital standard for equities is expressed in terms of

two separately calculated charges the “specific risk” and the “general market risk” for the

holdings.

II. The capital charge, for both specific risk and the general market risk charge will be 10

percent.

Basel II Implementation as a Statutory Requirement of Bangladesh Bank: A Study on

Bangladesh Development Bank Limited

25 | P a g e

Capital Charges for Foreign Exchange Risk

The capital charge for foreign exchange risk will be 10 percent of bank’s overall foreign exchange

exposure. The overall foreign exchange exposure is measured by aggregating the sum of the net

short positions or the sum of net long positions; whichever is the greater, regardless of sign. The

capital charge will be 10 percent of the overall net open position.

4.9 Capital Charge against Operational Risk Operational Risk is defined as the risk of losses resulting from inadequate or failed internal

processes, people and systems or from external events. This definition includes legal risk, but

excludes strategic and reputation risk.

Measurement Methodology

Banks operating in Bangladesh shall compute the capital requirements for operational risk under

the Basic Indicator Approach (BIA). Under BIA, the capital charge for operational risk is a fixed

percentage, denoted by · (alpha) of average positive annual gross income of the bank over the past

three years. Figures for any year in which annual gross income is negative or zero, should be

excluded from both the numerator and denominator when calculating the average. The capital

charge may be expressed as follows:

K = [(GI 1 + GI2 + GI3)*α]/n

Where,

K = the capital charge under the Basic Indicator Approach

GI = only positive annual gross income over the previous three years (i.e., negative or zero gross

income if any shall be excluded)

α = 15 percent (as per guideline)

n = number of the previous three years for which gross income is positive.

Total Profit/Loss before tax XX

(+) Total Provision XX

(+) Total Operating Expenses XX

(-) Realized profit/losses from sale of securities XX

(-) Extra ordinary/irregular items XX

(-) Income derived from insurance XX

= Gross Income (GI) XXXX

Basel II Implementation as a Statutory Requirement of Bangladesh Bank: A Study on

Bangladesh Development Bank Limited

26 | P a g e

4.10 Pillar-II Supervisory Review Process The main theme of Pillar 2 is that,

1. Banks have to have a process, a Risk Management Unit (RMU), to assess their own

risk profile and calculate adequate capital

2. They must have a strategy to maintain the level of adequate capital required in the

future.

Banks should also have Supervisory Review Process (SRP) team which will manage all the risks

a bank faces, develop and implement better risk management techniques.

4.11 Internal Capital Adequacy Assessment Process (ICAAP) The supervisory process is a tool for the regulators to ensure adequate capital of banks to guard

against risks. It also delegates responsibility to top management of the institutions to make certain

of the implementation of the laws. The management must analyze their risks internally, make plan

on capital and maintain proper internal control process. Supervisory review process will address:

1. Risk that are not covered by Pillar-I (risks other than credit, market and operation)

2. External risk factors to the bank that are not captured by Pillar-I

Management must take steps to plan for achieving proper capital target and to gradually use

advance process of calculating RWA and CAR. The five main features of effective review process

are:

1. Board and senior management oversight

2. Sound capital assessment

3. Comprehensive assessment of risks

4. Monitoring and reporting

5. Internal control review

The SRP team is responsible for making and applying Internal Capital Adequacy Assessment

Process (ICAAP). The ICAAP is an important part of Pillar 2 because it helps the bank in risk

measurement and capital planning process. It is basically an internally created guideline regarding

risk assessment and reporting process to be followed when considering the amount and type of

capital the bank should maintain to support its business.

Basel II Implementation as a Statutory Requirement of Bangladesh Bank: A Study on

Bangladesh Development Bank Limited

27 | P a g e

4.12 Supervisory Review Evaluation Process (SREP) BB Basel II implementation cell reviews each bank’s supervisory review process. This cell

evaluates the bank’s SRP and then arranges dialogue/ discussion session with that bank’s SRP

team. BB SREP team will analyze bank’s review process. BB expects banks to operate above

minimum capital standards. BB, through SREP, will intervene at an early stage if they feel that the

bank would falter in meeting minimum capital requirement. The frequency of meeting will depend

on bank’s activities and the difference between capital requirement assessed by the bank and BB

team. Usually, the SRP-SREP Dialogue takes place in BB once every year.

4.13 Stress Testing Stress testing is a kind of sensitivity analysis or “what-if-analysis” for banks. The purpose of this

test program is to find out how shock absorbent a bank is. Basically, the test calls for changing a

single variable at a time and observing what the result bring to the bank’s assets, profitability,

liquidity and other measures. The variables are changed to test forward looking scenario a bank

might face. This will measure the vulnerability and exposure to rare, exceptional but potential

events.

The five different risk factors that are used in stress testing are:

1. Interest rate

2. Forced sale value of collateral

3. Non-performing loan (NPL)

4. Share price

5. Foreign exchange rate

Stress test on liquidity must be done separately. The three levels of shocks are: Minor (e.g. only

1% change in interest rate), Moderate (e.g. a 3% change in interest rate) and Major (e.g. 5% or

more change in interest rate).

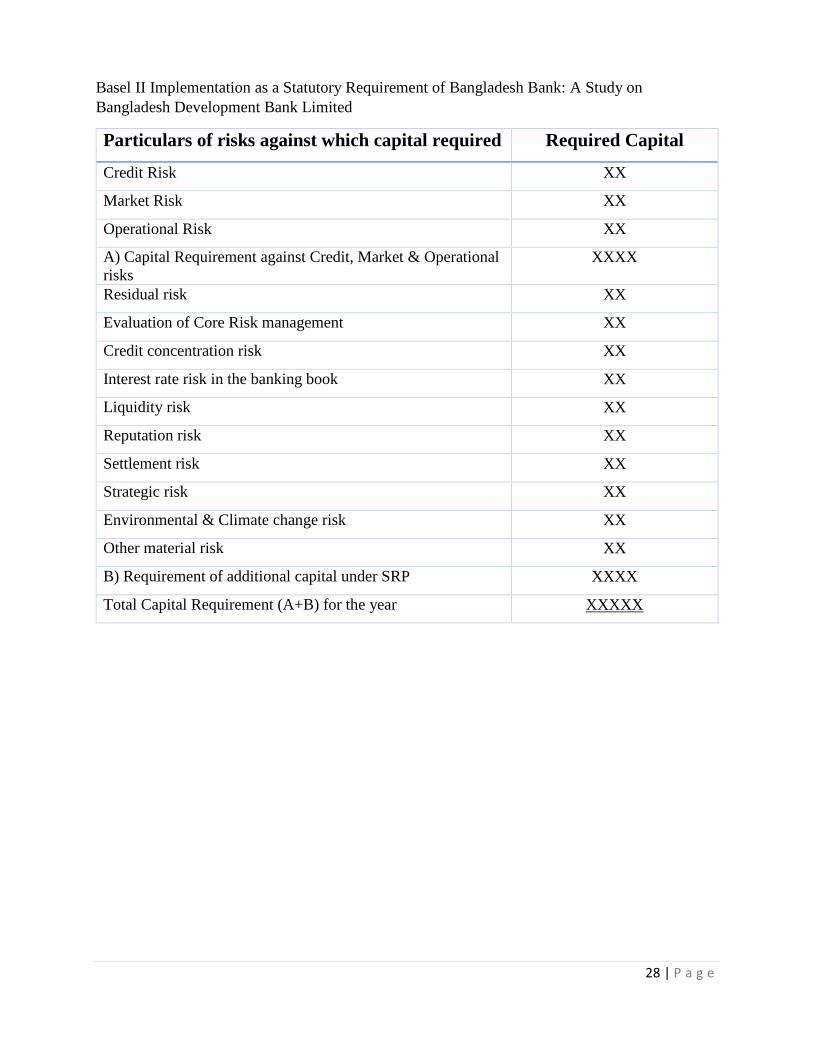

After BB collects information from banks and finishes the dialogue, the bank and BB will set the

total capital requirement for the bank corresponding to the risks they face. The general format of

additional capital is given below:

Basel II Implementation as a Statutory Requirement of Bangladesh Bank: A Study on

Bangladesh Development Bank Limited

28 | P a g e

Particulars of risks against which capital required Required Capital

Credit Risk XX

Market Risk XX

Operational Risk XX

A) Capital Requirement against Credit, Market & Operational

risks

XXXX

Residual risk XX

Evaluation of Core Risk management XX

Credit concentration risk XX

Interest rate risk in the banking book XX

Liquidity risk XX

Reputation risk XX

Settlement risk XX

Strategic risk XX

Environmental & Climate change risk XX

Other material risk XX

B) Requirement of additional capital under SRP XXXX

Total Capital Requirement (A+B) for the year XXXXX

Basel II Implementation as a Statutory Requirement of Bangladesh Bank: A Study on

Bangladesh Development Bank Limited

29 | P a g e

4.14 Pillar 3 Market Discipline This pillar is present in Basel II framework to complement the other two pillars. This pillar requires

the bank to disclose information to public and be more transparent to the financial market and the

participants. Current and potential stockholders, depositors and borrowers will want to know the

bank’s strengths and potential loss of assets.

Disclosure Requirements

Banks must have a formal disclosure framework approved by the Board or CEO of the bank.

The banks must follow the disclosure format provided by BB.

The disclosed information must be consistent to the audited financial statements. The information

must be material and omission of important and relevant data must be avoided. Banks have to

submit the data along with annual financial statements to BB by the end of March every year.

Banks can disclose the Basel II information in their Annual Report and/or on their website. In case

of Annual Report, a separate section must be utilized to report information. In case of website, the

Basel II information must be provided in the home-page. The historical information must be

maintained in the website for 4 years. The components must be disclosed in tabular form and in

quantitative and/or in qualitative form regarding the topics mentioned below:

1. Scope of application

2. Capital structure

3. Capital adequacy

4. Credit Risk

5. Equities: disclosures for banking book positions

6. Interest rate risk in the banking book (IRRBB)

7. Market risk

8. Operational risk

Basel II Implementation as a Statutory Requirement of Bangladesh Bank: A Study on

Bangladesh Development Bank Limited

30 | P a g e

Chapter 5:

Mechanisms for Measuring Credit,

Market and Operational Risk

Basel II Implementation as a Statutory Requirement of Bangladesh Bank: A Study on

Bangladesh Development Bank Limited

31 | P a g e

5.1 Bangladesh Bank guideline regarding Basel-II To cope with the international best practice and to make the bank’s capital more risk sensitive

quantitative and qualitative information are prepared by banks based on the audited financial

position of the Bank under the revised Risk Based Capital Adequacy Guideline (RBCA)

introduced by the central Bank of Bangladesh. Banking Supervision’s (BCBS) capital framework

was published in 1988. Capital Maintenance requirement based on risk weighted assets was set

up. Banks operating in Bangladesh have been maintaining these provisions in line with the Basel

Committee. Bangladesh Bank issued Basel-II guidelines for all scheduled banks on ‘Risk Based

Capital Adequacy (RBCA)’ to report their capital requirements which came fully into effect since

January 01, 2010, in December 2008. It is actually subsequent supplements/revisions replacing

the previous rules under Basel-I. The guidelines have been devised to make the regulatory

requirements more appropriate and also to assist the banks to follow the instructions more

efficiently for smooth implementation of the Basel II framework in the banking sector. The major

highlights of the Bangladesh Bank regulations in this regards are:

To maintain capital adequacy ratio (CAR) at a minimum of 10% (9% for 2010) of Risk

Weighted Assets.

To adopt the Standardized Approach for credit risk for implementing Basel II.

To adopt Standardized (Rule Based) Approach for market risk.

To adopt Basic Indicator Approach for operational risk.

To submit the returns to Bangladesh Bank on a quarterly basis.

5.2 Credit Risk

Credit risk refers to the risk that a borrower will default on any type of debt by failing to make

payments which it is obligated to do. The risk is primarily that of the lender and includes lost

principal and interest, disruption to cash flows, and increased collection costs. Credit default risk,

Concentration risk, Country risk are different types of Credit risk. The loss from credit risk may

be complete or partial and can arise in a number of circumstances. For example:

Basel II Implementation as a Statutory Requirement of Bangladesh Bank: A Study on

Bangladesh Development Bank Limited

32 | P a g e

A consumer may fail to make a payment due on a mortgage loan, credit card, line of credit,

or other loan

A company is unable to repay amounts secured by a fixed or floating charge over the assets

of the company

A business or consumer does not pay a trade invoice when due

A business does not pay an employee's earned wages when due

A business or government bond issuer does not make a payment on a coupon or principal

payment when due

An insolvent insurance company does not pay a policy obligation

An insolvent bank won't return funds to a depositor

A government grants bankruptcy protection to an insolvent consumer or business

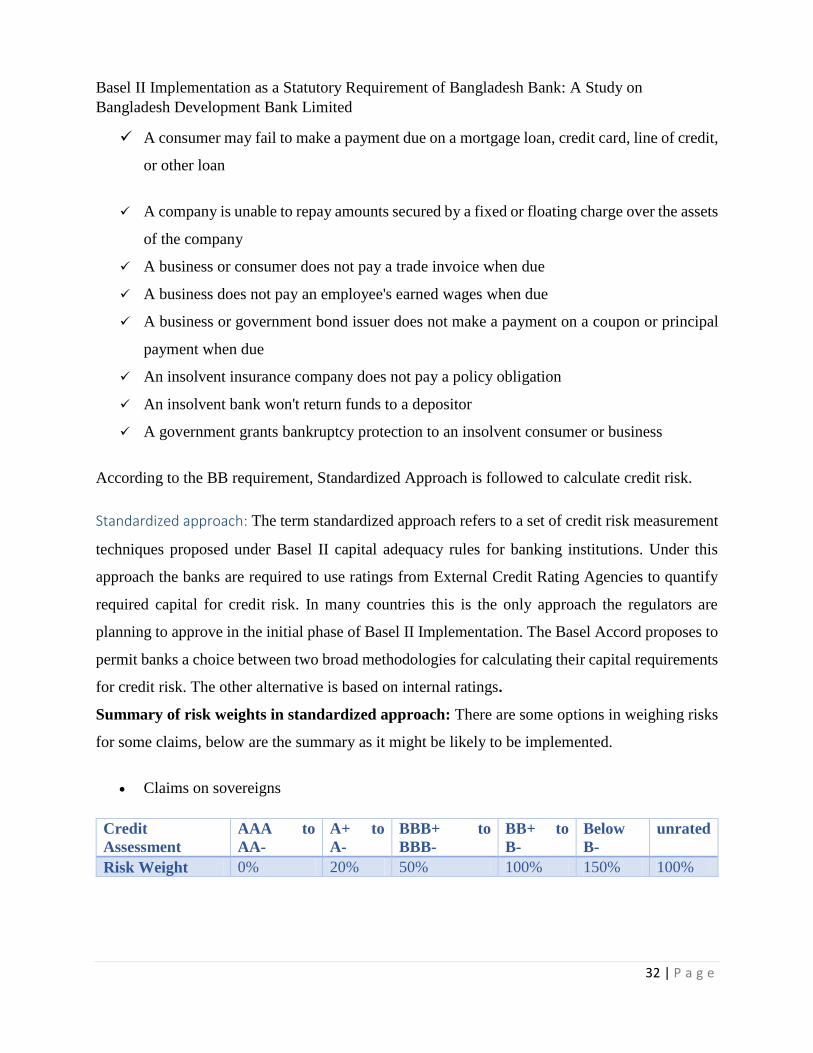

According to the BB requirement, Standardized Approach is followed to calculate credit risk.

Standardized approach: The term standardized approach refers to a set of credit risk measurement

techniques proposed under Basel II capital adequacy rules for banking institutions. Under this

approach the banks are required to use ratings from External Credit Rating Agencies to quantify

required capital for credit risk. In many countries this is the only approach the regulators are

planning to approve in the initial phase of Basel II Implementation. The Basel Accord proposes to

permit banks a choice between two broad methodologies for calculating their capital requirements

for credit risk. The other alternative is based on internal ratings.

Summary of risk weights in standardized approach: There are some options in weighing risks

for some claims, below are the summary as it might be likely to be implemented.

Claims on sovereigns

Credit

Assessment

AAA to

AA-

A+ to

A-

BBB+ to

BBB-

BB+ to

B-

Below

B-

unrated

Risk Weight 0% 20% 50% 100% 150% 100%

Basel II Implementation as a Statutory Requirement of Bangladesh Bank: A Study on

Bangladesh Development Bank Limited

33 | P a g e

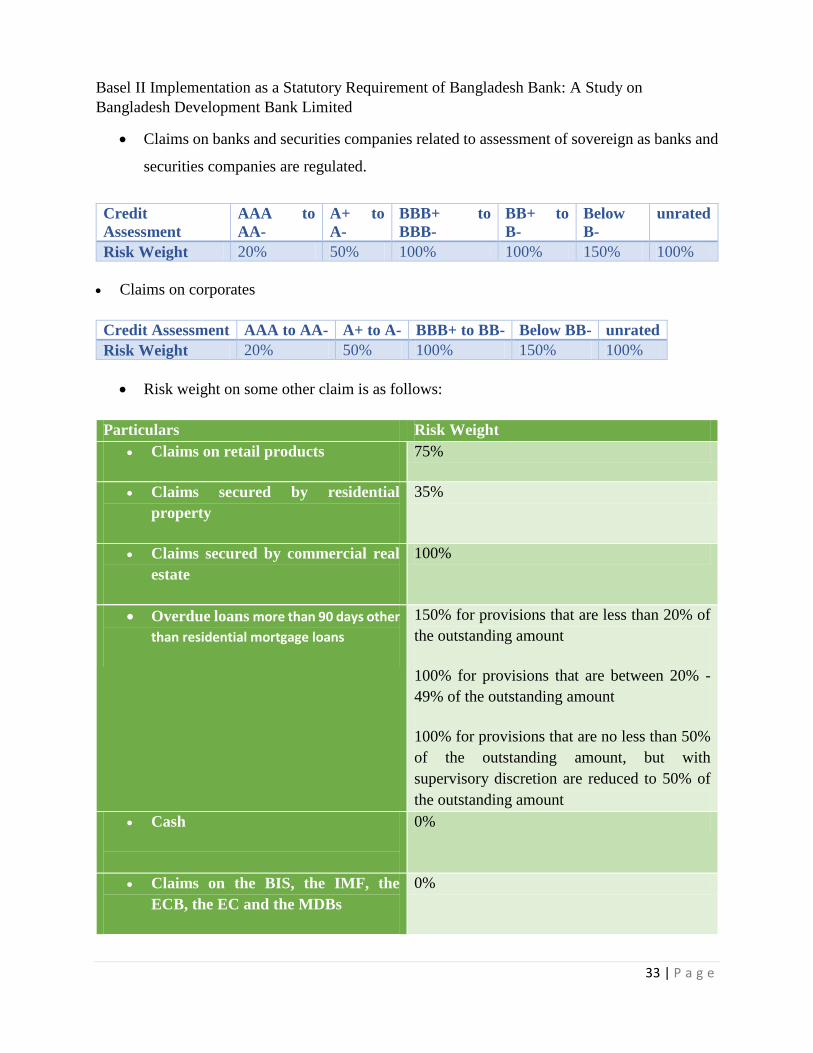

Claims on banks and securities companies related to assessment of sovereign as banks and

securities companies are regulated.

Credit

Assessment

AAA to

AA-

A+ to

A-

BBB+ to

BBB-

BB+ to

B-

Below

B-

unrated

Risk Weight 20% 50% 100% 100% 150% 100%

Claims on corporates

Credit Assessment AAA to AA- A+ to A- BBB+ to BB- Below BB- unrated

Risk Weight 20% 50% 100% 150% 100%

Risk weight on some other claim is as follows:

Particulars Risk Weight

Claims on retail products 75%

Claims secured by residential

property

35%

Claims secured by commercial real

estate

100%

Overdue loans more than 90 days other

than residential mortgage loans

150% for provisions that are less than 20% of

the outstanding amount

100% for provisions that are between 20% -

49% of the outstanding amount

100% for provisions that are no less than 50%

of the outstanding amount, but with

supervisory discretion are reduced to 50% of

the outstanding amount

Cash

0%

Claims on the BIS, the IMF, the

ECB, the EC and the MDBs

0%

Basel II Implementation as a Statutory Requirement of Bangladesh Bank: A Study on

Bangladesh Development Bank Limited

34 | P a g e

NOTE: For some "unrated" risk weights, banks are encouraged to use their own internal-ratings

system based on Foundation IRB and Advanced IRB in Internal-Ratings Based approach with a

set of formulae provided by the Basel-II accord. There exist several alternative weights for some

of the above claim categories published in the original Framework text.

5.3 Operational Risk

The Basel II Committee defines operational risk as: “The risk of loss resulting from inadequate or

failed internal processes, people and systems or from external events. However, the Basel

Committee recognizes that operational risk is a term that has a variety of meanings and therefore,

for internal purposes, banks are permitted to adopt their own definitions of operational risk,

provided that the minimum elements in the Committee's definition are included. The Basel II

definition of operational risk excludes, for example, strategic risk - the risk of a loss arising from

a poor strategic business decision. Other risk terms are seen as potential consequences of

operational risk events. For example, reputational risk (damage to an organization through loss of

its reputation or standing) can arise as a consequence (or impact) of operational failures - as well

as from other events. The following lists the official Basel II defined event types with some

examples for each category:

Internal Fraud - misappropriation of assets, tax evasion, intentional mismarking of

positions, bribery

External Fraud- theft of information, hacking damage, third-party theft and forgery

Employment Practices and Workplace Safety - discrimination, workers compensation,

employee health and safety

Clients, Products, & Business Practice- market manipulation, antitrust, improper trade,

product defects, fiduciary breaches, account churning

Damage to Physical Assets - natural disasters, terrorism, vandalism

Business Disruption & Systems Failures - utility disruptions, software failures, hardware

failures

Execution, Delivery, & Process Management - data entry errors, accounting errors, failed

mandatory reporting, negligent loss of client assets

Basel II Implementation as a Statutory Requirement of Bangladesh Bank: A Study on

Bangladesh Development Bank Limited

35 | P a g e

For operational risk, basic indicator approach is used,

Basic indicator approach or BIA: Regulatory minimal capital requirements for operational risk is

calculated as follows:

Capital charge under the Basic Indicator Approach= average annual gross income over the

previous three years × α

Where, α=15% (set by the Committee based on CISs)

5.4 Market risk Market risk is the risk of losses in positions arising from movements in market prices. Some market

risks include:

Equity risk, the risk that stock or stock indexes (e.g. Euro Stoxx 50, etc.) prices and/or their

implied volatility will change.

Interest rate risk, the risk that interest rates (e.g. Libor, Euribor, etc.) and/or their implied

volatility will change.

Currency risk, the risk that foreign exchange rates (e.g. EUR/USD, EUR/GBP, etc.) and/or

their implied volatility will change.

Commodity risk, the risk that commodity prices (e.g. corn, copper, crude oil, etc.) and/or

their implied volatility will change.

As with other forms of risk, the potential loss amount due to market risk may be measured in a

number of ways or conventions. Traditionally, one convention is to use Value at Risk. The

conventions of using Value at risk are well established and accepted in the short-term risk

management practice.

Value at Risk: In financial mathematics and financial risk management, Value at Risk (VaR) is a

widely used risk measure of the risk of loss on a specific portfolio of financial assets. For a given

portfolio, probability and time horizon, VaR is defined as a threshold value such that the

probability that the mark-to-market loss on the portfolio over the given time horizon exceeds this

value (assuming normal markets and no trading in the portfolio) is the given probability level. For

example, if a portfolio of stocks has a one-day 5% VaR of $1 million, there is a 0.05 probability

Basel II Implementation as a Statutory Requirement of Bangladesh Bank: A Study on

Bangladesh Development Bank Limited

36 | P a g e

that the portfolio will fall in value by more than $1 million over a one day period if there is no

trading. Informally, a loss of $1 million or more on this portfolio is expected on 1 day out of 20

days (because of 5% probability). A loss which exceeds the VaR threshold is termed a “VaR

break.” Thus, VaR is a piece of jargon favored in the financial world for a percentile of the

predictive probability distribution for the size of a future financial loss. In other words if you have

a record of portfolio value over time then the VaR is simply the negative quartile function of those

values. VaR has four main uses in finance- risk management, financial control, financial reporting

and computing regulatory capital. VaR is sometimes used in non-financial applications as well.

Basel II Implementation as a Statutory Requirement of Bangladesh Bank: A Study on

Bangladesh Development Bank Limited

37 | P a g e

Chapter 6:

Analysis of Basel II Components in the Annual Report of BDBL

Basel II Implementation as a Statutory Requirement of Bangladesh Bank: A Study on

Bangladesh Development Bank Limited

38 | P a g e

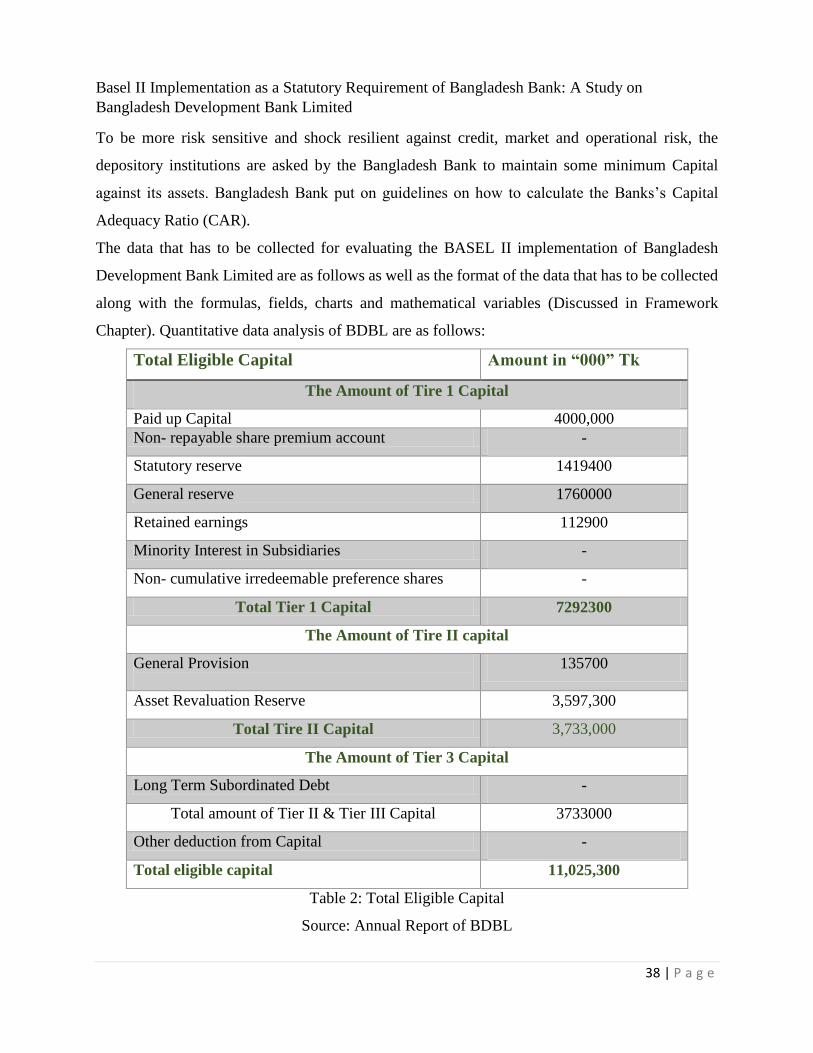

To be more risk sensitive and shock resilient against credit, market and operational risk, the

depository institutions are asked by the Bangladesh Bank to maintain some minimum Capital

against its assets. Bangladesh Bank put on guidelines on how to calculate the Banks’s Capital

Adequacy Ratio (CAR).

The data that has to be collected for evaluating the BASEL II implementation of Bangladesh

Development Bank Limited are as follows as well as the format of the data that has to be collected

along with the formulas, fields, charts and mathematical variables (Discussed in Framework

Chapter). Quantitative data analysis of BDBL are as follows:

Total Eligible Capital Amount in “000” Tk

The Amount of Tire 1 Capital

Paid up Capital 4000,000

Non- repayable share premium account -

Statutory reserve 1419400

General reserve 1760000

Retained earnings 112900

Minority Interest in Subsidiaries -

Non- cumulative irredeemable preference shares -

Total Tier 1 Capital 7292300

The Amount of Tire II capital

General Provision

135700

Asset Revaluation Reserve 3,597,300

Total Tire II Capital 3,733,000

The Amount of Tier 3 Capital

Long Term Subordinated Debt -

Total amount of Tier II & Tier III Capital 3733000

Other deduction from Capital -

Total eligible capital 11,025,300

Table 2: Total Eligible Capital

Source: Annual Report of BDBL

Basel II Implementation as a Statutory Requirement of Bangladesh Bank: A Study on

Bangladesh Development Bank Limited

39 | P a g e

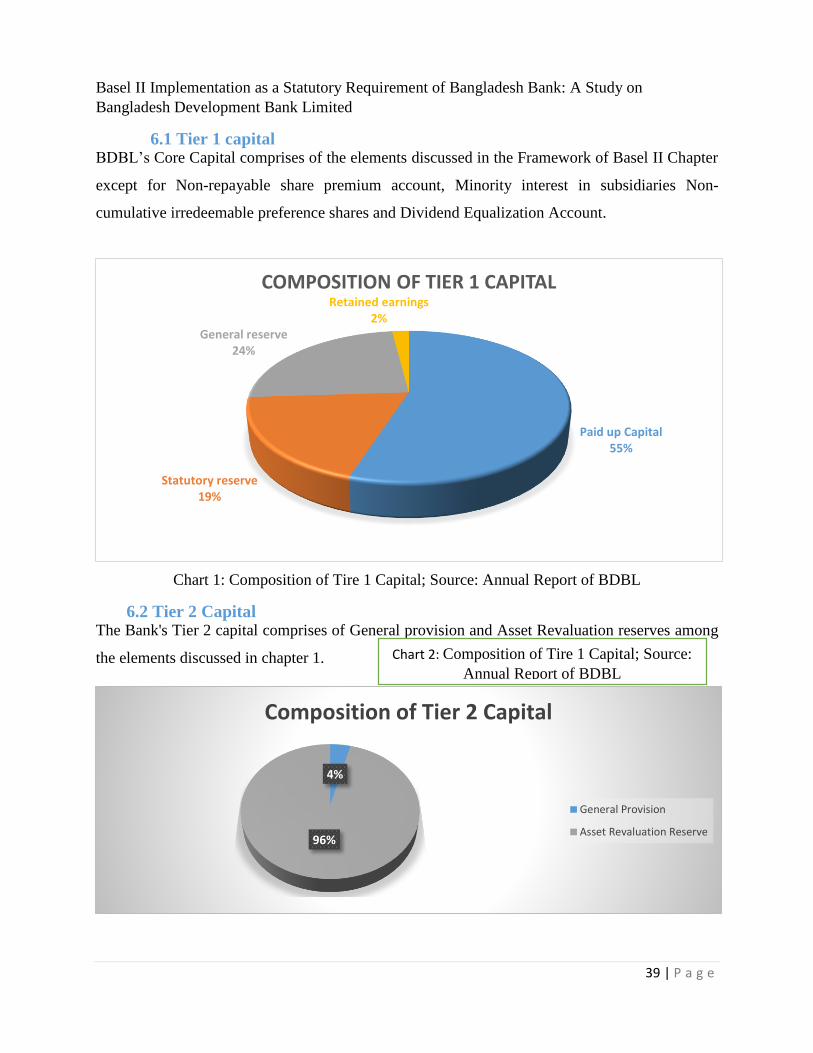

6.1 Tier 1 capital BDBL’s Core Capital comprises of the elements discussed in the Framework of Basel II Chapter

except for Non-repayable share premium account, Minority interest in subsidiaries Non-

cumulative irredeemable preference shares and Dividend Equalization Account.

Chart 1: Composition of Tire 1 Capital; Source: Annual Report of BDBL

6.2 Tier 2 Capital The Bank's Tier 2 capital comprises of General provision and Asset Revaluation reserves among

the elements discussed in chapter 1.

Paid up Capital55%

Statutory reserve19%

General reserve24%

Retained earnings2%

COMPOSITION OF TIER 1 CAPITAL

4%

96%

Composition of Tier 2 Capital

General Provision

Asset Revaluation Reserve

Chart 2: Composition of Tire 1 Capital; Source:

Annual Report of BDBL