BASEL II A NEW GLOBAL MANTRA FOR INDIAN BANKS Performance Measurement Study of ICICI bank By Ms Chand Tandon Sr. Lecturer (Finance) Apeejay School of Management Dwarka sector 8 New Delhi [email protected] Abstract: This study explores the performance of ICICI bank with respect to its policies and impact of BASEL II. The study also deals in detai ls that whether Indian banks are equipped with sufficient technology to combat various clauses proposed in BASEL II particularly ICICI bank. The underlying aim of Basel II is to promote safety and soundness in the financial system by allocating capital in organizations to reflect risk more accurately. This can be attained only by the combination of effective bank-level management, market discipline and supervision. Basel II will impac t the enti re spectr um of banking, incl uding corpor at e fi nance , reta il ban ki ng, asset management, payments and settlements, commercial banking, trading and sales, retail brokerage and agency and custody. Basel II aims to encourage the use of modern risk management techniques; and to encourage banks to ensure that their risk management capabilities are commensurate with the risks of their business. Pre viousl y, regula tor s' main foc us was on credit ri sk and market risk. Basel II takes a more sophisticated approach to credit risk, in that it allows banks to make use of internal ratings based Approach - or "IRB Approach" as they have become known - to calculate their capital requirement for credit risk. It also introduces, in addition to the market risk capital charge, an explicit capital charge for operational risk. The study also outlines the current banking scenario in India and the gain/loss which banks will get as a result of BASEL II implementation. Key words : Minimum Capital requirement Capital adequacy Operational risk Data Base Creation Non performing Assets Corporate penetration Risk adjusted performance Management Regulatory Vs Economic Capital

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

8/6/2019 Basel II a New Global Mantra for Indian Banks

http://slidepdf.com/reader/full/basel-ii-a-new-global-mantra-for-indian-banks 1/15

BASEL II A NEW GLOBAL MANTRA FOR INDIAN BANKS

Performance Measurement Study of ICICI bank

By Ms Chand TandonSr. Lecturer (Finance)

Apeejay School of Management

Dwarka sector 8 New Delhi

Abstract:

This study explores the performance of ICICI bank with respect to its policies and impact of BASEL

II. The study also deals in details that whether Indian banks are equipped with sufficient technologyto combat various clauses proposed in BASEL II particularly ICICI bank.

The underlying aim of Basel II is to promote safety and soundness in the financial system byallocating capital in organizations to reflect risk more accurately. This can be attained only by the

combination of effective bank-level management, market discipline and supervision. Basel II willimpact the entire spectrum of banking, including corporate finance, retail banking, asset

management, payments and settlements, commercial banking, trading and sales, retail brokerage and

agency and custody.

Basel II aims to encourage the use of modern risk management techniques; and to encourage banksto ensure that their risk management capabilities are commensurate with the risks of their business

Previously, regulators' main focus was on credit risk and market risk. Basel II takes a more

sophisticated approach to credit risk, in that it allows banks to make use of internal ratings based

Approach - or "IRB Approach" as they have become known - to calculate their capital requirementfor credit risk. It also introduces, in addition to the market risk capital charge, an explicit capital

charge for operational risk.

The study also outlines the current banking scenario in India and the gain/loss which banks will getas a result of BASEL II implementation.

Key words :

Minimum Capital requirementCapital adequacy

Operational risk Data Base Creation Non performing Assets

Corporate penetration

Risk adjusted performance Management

Regulatory Vs Economic Capital

8/6/2019 Basel II a New Global Mantra for Indian Banks

http://slidepdf.com/reader/full/basel-ii-a-new-global-mantra-for-indian-banks 2/15

BASEL II Introduction

Basel II, also called The New Accord (correct full name is the International Convergence of Capital

Measurement and Capital Standards - A Revised Framework) is the second Basel Accord and

represents recommendations by bank supervisors and central bankers from the 13 countries makingup the Basel Committee on Banking Supervision to revise the international standards for measuring

the adequacy of a bank's capital. It was created to promote greater consistency in the way banks and

banking regulators approach risk management across national borders. The Bank for Internationa

Settlements (often confused with the BCBS) supplies the secretariat for the BCBS and is not itselfthe BCBS.

Basel II promotes the safety and stability of the global financial system and results in greater qualityof and accuracy in obtaining risk information. Basel II requires your institution to identify measure,

validate and report on the risk you assume everyday. For some this will mean a costly and difficult

regulatory headache. For Insightful Financial Solutions customers it means reliable, rigorous resultswith clear reporting and transparent audit trails.

Insightful will help you meet Basel II requirements by providing:

Internal and external data integration

A transparent analytic environment

High-level modeling process flow

A detailed set of pre-programmed risk models

A front-office reporting interface

BASEL II – Are Indian Banks Going to Gain? There are broadly two sets of reasons often given for capital regulation in banks in particular. One is

depositor protection and the second is systemic risk. Banks are often thought to be a source of

systemic risk because of their central role in the payments system and in the allocation of financialresources, combined with the fragility of their financial structure. Banks are highly leveraged with

relatively short-term liabilities, typically in the form of deposits, and relatively illiquid assets

usually loans to firms or households. In that sense banks are said to be "special" and hence subject tospecial regulatory oversight.

Before 1988, many central banks allowed different definitions of capital in order to make their

country's bank appear as solid than they actually were. In order to provide a level playing field the

concept of regulatory capital was standardized in BASEL I. Along with definition of regulatorycapital a basic formula for capital divided by assets was constructed and an arbitrary ratio of 8% was

chosen as minimum capital adequacy. However, there were drawbacks in the BASEL I as it did not

did not discriminate between different levels of risk. As a result a loan to an established corporatewas deemed as risky as a loan to a new business. Also it assigned lower weight age to loans to banks

as a result banks were often keen to lend to other banks.

The BASEL II accord proposes getting rid of the old risk weighted categories that treated allcorporate borrowers the same replacing them with limited number of categories into which

8/6/2019 Basel II a New Global Mantra for Indian Banks

http://slidepdf.com/reader/full/basel-ii-a-new-global-mantra-for-indian-banks 3/15

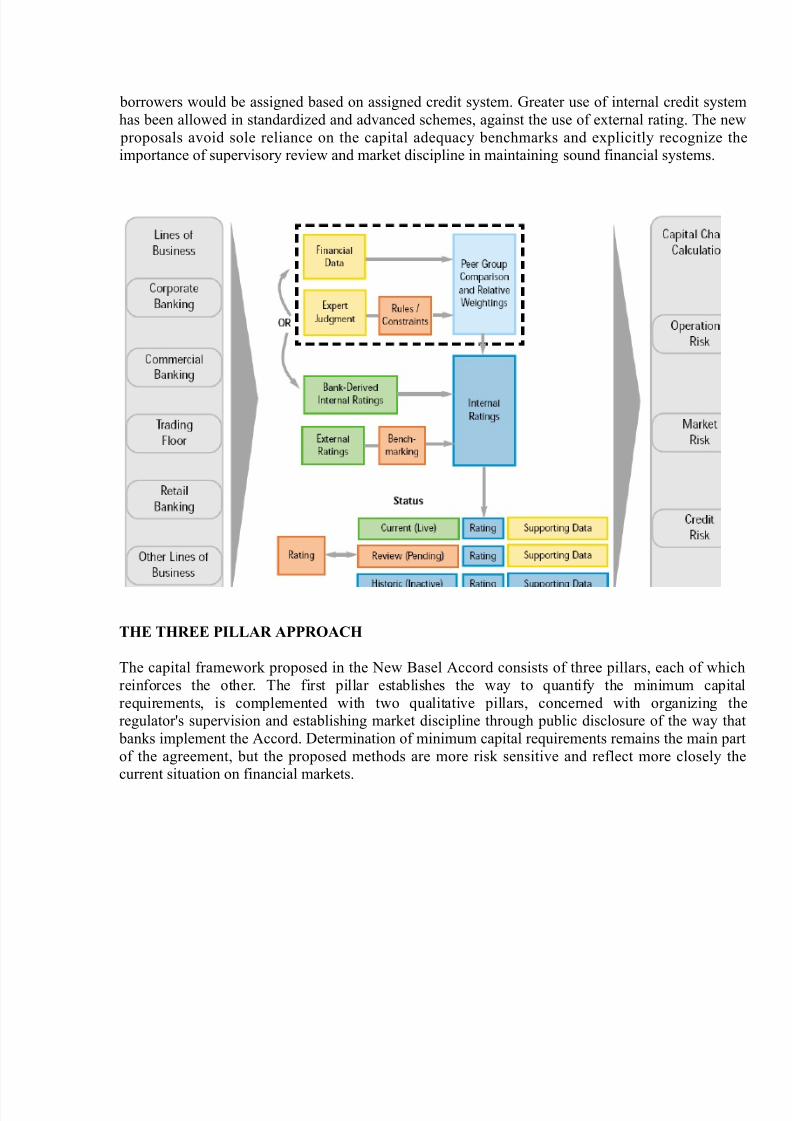

borrowers would be assigned based on assigned credit system. Greater use of internal credit system

has been allowed in standardized and advanced schemes, against the use of external rating. The new

proposals avoid sole reliance on the capital adequacy benchmarks and explicitly recognize theimportance of supervisory review and market discipline in maintaining sound financial systems.

THE THREE PILLAR APPROACH

The capital framework proposed in the New Basel Accord consists of three pillars, each of which

reinforces the other. The first pillar establishes the way to quantify the minimum capital

requirements, is complemented with two qualitative pillars, concerned with organizing theregulator's supervision and establishing market discipline through public disclosure of the way that

banks implement the Accord. Determination of minimum capital requirements remains the main part

of the agreement, but the proposed methods are more risk sensitive and reflect more closely thecurrent situation on financial markets.

8/6/2019 Basel II a New Global Mantra for Indian Banks

http://slidepdf.com/reader/full/basel-ii-a-new-global-mantra-for-indian-banks 4/15

8/6/2019 Basel II a New Global Mantra for Indian Banks

http://slidepdf.com/reader/full/basel-ii-a-new-global-mantra-for-indian-banks 5/15

The Internal Ratings Based Approach (IRB)

Under the IRB approach, distinct analytical frameworks will be provided for different types of loan

exposures. The framework allows for both a foundation method in which a bank estimate the probability of default associated with each borrower, and the supervisors will supply the other inputs

and an advanced IRB approach, in which a bank will be permitted to supply other necessary inputs

as well. Under both the foundation and advanced IRB approaches, the range of risk weights will befar more diverse than those in the standardized approach, resulting in greater risk sensitivity.

2. Operational Risk:

Basel II Accord set a capital requirement for operational risk. It defines operational risk as "the risk

of direct or indirect loss resulting from inadequate or failed internal processes, people and systems or

from external events". Banks will be able to choose between three ways of calculating the capital

charge for operational risk – the Basic

Indicator Approach, the Standardized Approach and the advanced measurement Approaches.

The Second Pillar: Supervisory Review Process

The supervisory review process requires supervisors to ensure that each bank has sound internal

processes in place to assess the adequacy of its capital based on a thorough evaluation of its risks

Supervisors would be responsible for evaluating how well banks are assessing their capital adequacyneeds relative to their risks. This internal process would then be subject to supervisory review and

intervention, where appropriate.

The Third Pillar: Market Discipline

The third pillar of the new framework aims to bolster market discipline through enhanced disclosure

by banks. Effective disclosure is essential to ensure that market participants can better understand banks' risk profiles and the adequacy of their capital positions. The new framework sets ou

disclosure requirements and recommendations in several areas, including the way a bank calculates

its capital adequacy and its risk assessment methods. The core set of disclosure recommendationsapplies to all banks, with more detailed requirements for supervisory recognition of interna

methodologies for credit risk, credit risk mitigation techniques and asset securitization.

RESEARCH METHODOLOGY

For study I had used mainly secondary data which was collected from the various internet sites bank website, various banking journals and some important information regarding latest trend in the

development of Basel II and its implementation process in the bank. And data will also be collected

from officials of the bank regarding the same.

8/6/2019 Basel II a New Global Mantra for Indian Banks

http://slidepdf.com/reader/full/basel-ii-a-new-global-mantra-for-indian-banks 6/15

ANALYSIS AND INTEPETATION

Analysis of Income StatementNet interest income growing strongly…

ICICI Bank reported excellent performance since the past few years. Interest income of the bank

grew at a CAGR of 59.1% during the period 2002-2006 and stood at Rs.137.85bn at the end of Mar

31, 2006. During the same period, interest expense grew at a CAGR of 57.5%. This resulted in netinterest income growing at a CAGR of 63% during the same period. The bank continued this growth

momentum in 2007 to register an impressive year-on-year improvement in financial performance.

Net interest income increased by 47.5% to Rs.41.87bn in FY06 from Rs.28.39bn in FY2005 primarily due to an increase of Rs.553.57bn in the average volume of interest earning assets. Gain on

sell-down of loans (including securitisation of loans and direct assignment of loans) included in

interest income decreased by 12.3% to Rs.4.57bn in FY06 from Rs.5.21bn in FY05. During the year,RBI issued guidelines on accounting for securitisation of standard assets. In accordance with these

guidelines, with effect from February 1, 2006, the Bank accounts for any loss arising on

securitisation immediately at the time of sale and the profit/premium arising on account ofsecuritisation is amortised over the life of the assets. Prior to February 1, 2006, profit arising on

account of securitisation has been recorded at the time of sale.

Operating expenses …

Operating expenses of the bank grew in line with the growth in business. The total operating

expenses grew at a CAGR of 69.1% in the last four years. For the year ended Mar-07, operatingexpenses rose by 35.8% over the previous year and stood at Rs.246.4mn. During the year there was

decline in the operational efficiency as the cost to total operating income after provision increasedfrom 56.6% in FY05 to 59.1% in FY07.

Impressive Earnings Growth…

The bank reported a strong performance in the past four years with net profitability of the

bank recording a CAGR of impressive 77.1%. The year 2007 also turned out to be profitable for the

bank with the bank reporting a net profit of Rs.31.1bn, a rise of 22.45% over FY2006.The improvedearnings have also led to the improvement in the earning per share of the bank, which rose from

Rs.26.6 in FY2004 to Rs.35.7 in FY07. Manpower productivity has fallen over the years as profit

per employee decline from Rs.1.1mn in FY05 to Rs.0.9mn in FY06.

Margins…

ICICI Bank has displayed a steady performance in the last few years in scaling up itsEfficiency levels. The net interest margin in FY07 at 2.4% was at the same level as in FY06.

However, excluding gain from sell-down, net interest margin for FY06 increased to 2.2% in FY06

from 2.0% in FY05. ICICI Bank’s net interest margin is lower than that of other Indian banks due tothe high-cost liabilities of erstwhile ICICI Limited (ICICI) and the maintenance of Statutory

8/6/2019 Basel II a New Global Mantra for Indian Banks

http://slidepdf.com/reader/full/basel-ii-a-new-global-mantra-for-indian-banks 7/15

Liquidity Ratio (SLR) and Cash Reserve Ratio (CRR) on these liabilities, which were not subject to

these ratios prior to the merger. While ICICI Bank’s cost of deposits (5% in FY06) is comparable to

the cost of deposits of other banks in India, ICICI Bank’s total cost of funding (5.8% in FY06) ishigher compared to other banks as a result of these high-cost liabilities. Further, ICICI Bank has to

maintain SLR and CRR on these liabilities, resulting in a negative impact on the spread. ICICI Bank

also reduces direct marketing agency expenses incurred for origination of automobile loans from theinterest income.

Assets growing strongly…

The asset profile of ICICI Bank is spread over a wide array of asset categories similar to the other

commercial banks in India. This has enabled the bank to minimize its risk exposure, yet achieve the

expected returns. Due to the bank’s nature of operations, loan portfolio accounted for a substantial portion of the bank’s assets and it formed 58.14% of the total assets in FY07. Investments portfolio

also accounted for the major portion of the bank’s assets. In 2006, investments portfolio accounted

for 28.46% of the total assets. The total assets of the bank grew at a CAGR of 24.4% in the last five

years and stood at Rs.2,513bn at the end of FY06 representing an increase of 49.9% over FY2005.

Investment Portfolio…

The investment portfolio of the bank constituted around 28.49% of the total asset size of the bank atthe end of FY06. Total investments as of March 31, 2005 increased by 41.7% to Rs715.4bn fromRs504.87bn in the previous year. SLR investments during the period jumped by 48.1% to

Rs.510.74bn from Rs.344.82bn as of March 31, 2005, in line with the growth in the balance sheet.

Other investments (including debentures & bonds) increased by 27.9% to Rs.204.73bn, reflecting

increase in investments in insurance and international subsidiaries, pass-through certificates andcredit-linked notes.

8/6/2019 Basel II a New Global Mantra for Indian Banks

http://slidepdf.com/reader/full/basel-ii-a-new-global-mantra-for-indian-banks 8/15

Funding Structure…

Historically, around 8-9% of the balance sheet was funded by shareholders equity with the restcoming from customers and inter-bank deposits. The bank has been able to expand its deposit base

by rapid expansion in semi-urban and rural areas of the country and by way of introducing number

of innovative products.

Capital Adequacy Ratio…

Despite a subsequent strong growth in assets, the Capital Adequacy Ratio (CAR) at the end of the

year was at 11.69%, above the benchmark requirement of 9% prescribed by the Reserve Bank of

India.

Strength/ Opportunities:The growth for ICICI Bank in the coming years is likely to be fueled by the

Following factors:

Expansion in international operations, increasing retail customer base, debt syndication business and credit linked fees would fuel fee base income for the bank.

Increasing PLR by major banks in the industry would help the bank to maintain its

margins.

Value unlocking in the banks’ subsidiaries could generate cash for further credit growth.

Strong relationship with major corporate house would help bank to sustain its growth

rates.

Strong economic growth would generate higher demand for funds pursuant to highercorporate demand for credit on account of capacity expansion.

Weakness/ Threats:The risks that could ensue to ICICI Bank in time to come are as under:

Stiff competition, especially in the retail segment, could impact retailgrowth of ICICI Bank and hence slowdown in earnings growth.

Contribution of retail credit to total bank credit stood at 69%. Significant

thrust on growing retail book poses higher credit risk to the bank.

Slow down in domestic economy would pose a concern over credit off-take, thereby impacting earnings growth.

CASA contribution to the total deposits is very low. This could result in

higher cost of deposits, thereby impacting margins.

CHALLENGES FOR INDIAN BANKING SYSTEM UNDER BASEL II

A feature, somewhat unique to the Indian financial system is the diversity of its composition. We

have the dominance of Government ownership coupled with significant private shareholding in the

8/6/2019 Basel II a New Global Mantra for Indian Banks

http://slidepdf.com/reader/full/basel-ii-a-new-global-mantra-for-indian-banks 9/15

public sector banks and we also have cooperative banks, Regional Rural Banks and Foreign bank

branches. By and large the regulatory standards for all these banks are uniform.

Costly Database Creation and Maintenance Process:

The most obvious impact of BASEL II is the need for improved risk management and measurement

It aims to give impetus to the use of internal rating system by the international banks. More and

more banks may have to use internal model developed in house and their impact is uncertain. Mostof these models require minimum 5 years bank data which is a tedious and high cost process as most

Indian banks do not have such a database

Additional Capital Requirement:In order to comply with the capital adequacy norms we will see that the overall capital level of the banks will raise a glimpse of which was seen when the RBI raised risk weight ages for mortgages

and home loans in October 2004. Here there is a worrying aspect that some of the banks will not be

able to put up the additional capital to comply with the new regulation and they may be isolated fromthe global banking system.

In ICRA's estimates, Indian banks would need additional capital of up to Rs 120 billion (12,000

crore) to meet the capital charge requirement for operational risk under Basel II. Most of this capitalwould be required by PSBs (Rs 90 billion, or Rs 9,000 crore), followed by the new generation private sector banks (Rs 11 billion, or Rs 1,100 crore), and the old generation private sector bank (Rs

7.5 billion, or Rs 750 crore).

Large Proportion of NPA's:A large number of Indian banks have significant proportion of NPA's in their assets. Along with that

a large proportion of loans of banks are of poor quality. There is a danger that a large number of

banks will not be able to restructure and survive in the new environment. This may lead to forced

mergers of many defunct banks with the existing ones and a loss of capital to the banking system asa whole.

Relative Advantage to Large Banks:The new norms seem to favor the large banks that have better risk management and measurement

expertise. They also have better capital adequacy ratios and geographically diversified portfoliosThe smaller banks are also likely to be hurt by the rise in weightage of inter-bank loans that will

effectively price them out of the market. Thus banks will have to restructure and adopt if they are to

survive in the new environment.

Increased Pro-Cyclically:The appropriate question is not then whether Basel II introduces pro-cyclicality but whether it

increases it. The increased importance to credit ratings under Basel II could actually imply that theminimum requirements could become pro-cyclical as banks are required to raise capital levels forloans in times of economic crises.

Low Degree of Corporate Rating Penetration:India has as few as three established rating agencies and the level of rating penetration is not very

significant as, so far, ratings are restricted to issues and not issuers. While Basel II gives some scopeto extend the rating of issues to issuers, this would only be an approximation and it would be

8/6/2019 Basel II a New Global Mantra for Indian Banks

http://slidepdf.com/reader/full/basel-ii-a-new-global-mantra-for-indian-banks 10/15

necessary for the system to move to ratings of issuers. Encouraging ratings of issuers would be a

challenge.

Cross Border Issues for Foreign Banks:In India, foreign banks are statutorily required to maintain local capital and the following issues are

required to be resolved;

Validation of the internal models approved by their head offices and home countrysupervisor adopted by the Indian branches of foreign banks.

Date history maintained and used by the bank should be distinct for the Indian branches

compared to the global data used by the head office

capital for operational risk should be maintained separately for the Indian branches in India.

Banks need to reorganize within the given timeframe:A 2002 KPMG Survey of 190 banks in 19 countries indicated that data collection was widely

viewed as the main obstacle to implementation. Over 60 percent of the Banks saw the timing ofthe implementation as the main cause for concern. Less than 20 percent had started with the

implementation for Credit Risk, and less than 10 percent for Operational Risk.

Banks will need a new strategy to support data integration between finance, operational and riskmanagement functions. They will need to build a more streamlined and responsive organisation

to take better risk management, performance management and capital allocation decisions.

Banks need to streamline / re-engineer their business processes, primarily

with respect to supervision and controlSupervision will need to be risk-focused and increasingly concerned with validating systems.

Supervisors also need to carefully review the manner in which loss characteristics are estimated.

THE ROAD AHEAD

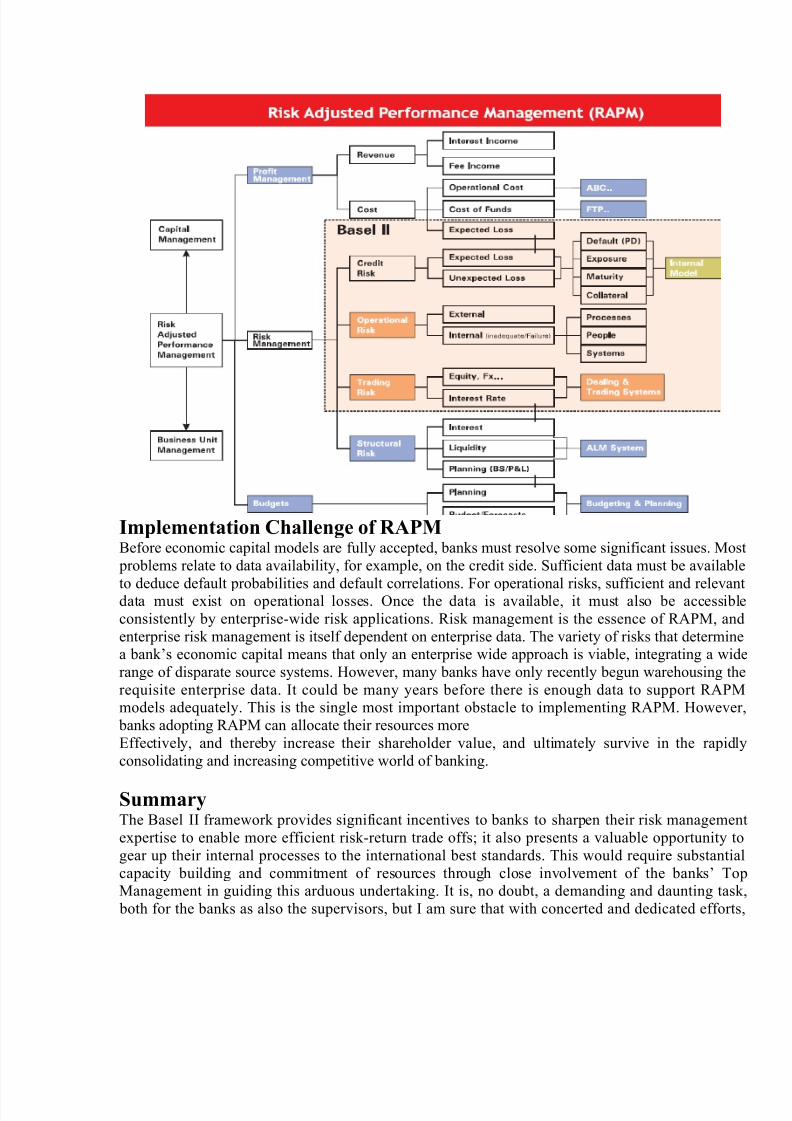

Risk Adjusted Performance Management (RAPM)The emergence of better risk management techniques represents major progress for Banks. Finallyfinancial institutions are analyzing the activities they must do, to obtain

a sufficient risk-adjusted return for shareholders. In this article, we consider why RAPM is so

important and it’s relation to Basel II regulatory capital. Also, we discuss the Challenge ofimplementation. Theoretically, management in any financial institution should aim to maximize

equity investors’ risk-adjusted returns. Faced with this objective,managers can:

increase the return per dollar of equity, or

decrease the equity or capital required per dollar of target return.

Essentially, the target return is driven by market expectations. Exceeding market Expectations

increases shareholder value while missing expectations destroys value.Although it is not ‘rocket science’, until recently, this focus on return was surprisingly absent from

most banks’ boardrooms, particularly in Asia with its closely held Corporations and relatively

passive shareholders. Instead, many institutions chose to focus on asset growth as they wereexacerbated by the wave of deregulation sweeping through the developed economies. Asset growth

(e.g. in the loan portfolio) prioritizes Management, stakeholders, and institutionalizes their agenda

for survival and empire building. It implicitly makes shareholder value a secondary priority. But itdoes more than that.It tends to downplay the risk associated with new business. Short-term growth

8/6/2019 Basel II a New Global Mantra for Indian Banks

http://slidepdf.com/reader/full/basel-ii-a-new-global-mantra-for-indian-banks 11/15

makes loan officers overlook the quality of their loan portfolio – storing up bad debt, which

eventually must be written off, with catastrophic results for the income statement. Only the survivors

learn to focus not just on growth for its own sake, but also on risk-adjusted returns, aligning theorganisational targets with investor preferences. This requires a common language about risk and

return and the tradeoff between the two. Capital, is the

basis for this common language.

Regulatory vs. Economic CapitalOne aspect of the role of capital in a deposit-taking institution is to protect creditors. This is theregulatory perspective, ensuring bank solvency, and thereby, safeguarding the banking system. The

Basel II accord estimates a minimum level of capital required to achieve these objectives. Basel II

does not determine the optimal level of so-called ‘economic’ capital required, given the specific

risks of a particular bank. Economic capital generally does not equal cash capital or book capital orregulatory capital. Economic capital is a buffer against the bank’s future, unidentified losses, up to

some extreme level consistent with investors’ risk preferences. Hence, economic capital must cover

both ‘normal’ or expected losses as well as unexpected losses up to some extreme loss. This reflects

the bank’s target credit rating appropriate for a particular investor segment, or equivalently, aspecific default probability. Theoretically straightforward, determining economic capital is complex

It requires, understanding the extremes of a bank’s future loss distribution, extremes that are rarelyexperienced.

Risk Adjusted Performance MeasurementAll performance measurement frameworks compare returns against capital. Traditionally, these

capital measures (e.g. book capital) are unadjusted for risk. RAPM uses capital measures that reflect

the bank’s risks

8/6/2019 Basel II a New Global Mantra for Indian Banks

http://slidepdf.com/reader/full/basel-ii-a-new-global-mantra-for-indian-banks 12/15

Implementation Challenge of RAPMBefore economic capital models are fully accepted, banks must resolve some significant issues. Most

problems relate to data availability, for example, on the credit side. Sufficient data must be available

to deduce default probabilities and default correlations. For operational risks, sufficient and relevantdata must exist on operational losses. Once the data is available, it must also be accessible

consistently by enterprise-wide risk applications. Risk management is the essence of RAPM, and

enterprise risk management is itself dependent on enterprise data. The variety of risks that determinea bank’s economic capital means that only an enterprise wide approach is viable, integrating a wide

range of disparate source systems. However, many banks have only recently begun warehousing the

requisite enterprise data. It could be many years before there is enough data to support RAPMmodels adequately. This is the single most important obstacle to implementing RAPM. However

banks adopting RAPM can allocate their resources more

Effectively, and thereby increase their shareholder value, and ultimately survive in the rapidly

consolidating and increasing competitive world of banking.

SummaryThe Basel II framework provides significant incentives to banks to sharpen their risk managemen

expertise to enable more efficient risk-return trade offs; it also presents a valuable opportunity to

gear up their internal processes to the international best standards. This would require substantial

capacity building and commitment of resources through close involvement of the banks’ TopManagement in guiding this arduous undertaking. It is, no doubt, a demanding and daunting task

both for the banks as also the supervisors, but I am sure that with concerted and dedicated efforts,

8/6/2019 Basel II a New Global Mantra for Indian Banks

http://slidepdf.com/reader/full/basel-ii-a-new-global-mantra-for-indian-banks 13/15

banks would be able to measure equal to the task and cross yet another important milestone in their

journey of successfully implementing the regulatory reforms in the country.

Basel II represents a long-term opportunity. But with budget issues and operating profits under

pressure, the initial investment that banks must make to comply with the new accord also represents

a short-term challenge. Over time, the improvements in risk management that Basel II is intended todrive, may enhance risk culture, reduce volatility of all risks, lower provision for bad debts, reduce

operational losses, improve the institutions’ external ratings and, thereby, help ensure access to

capital markets and raise Organizational efficiency.

Banks will have to continuously improve the quality of their loss data with Basel II requiring them to

have at least five years of data, including a downturn.

First, Basel II delivers great risk differentiation. Banks that move from sub-prime mortgage lending

or that move from traditional corporate lending into leveraged lending would see a hike in their

capital.

Second, off-balance sheet contractual exposures to Structured Investment Vehicle and conduits

would be brought into the fold and subject to regulatory capital, whatever the accounting treatment.

Third, there will be much more risk-sensitive treatment for securitization exposures. This would

foster more neutral incentives between retaining an exposure on the balance sheet or distributing it in

the market through securitization.

Reference:

Bailey, R (2005), “Basel II and Development Countries: Understanding theImplications”, London School of Economics Working Paper No. 05-71.

Basel Committee on Banking Supervision (1988), “International Convergence of Capital

Measurement and Capital Standards”, available at www.bis.org

Basel Committee on Banking Supervision (2006), “International Convergence of Capital

Measurement and Capital Standards: A Revised Framework”, available at www.bis.org

Financial Stability Institute (2006), “Implementation of the new capital adequacy

framework in non-Basel Committee member countries: Summary of responses to

the 2006 follow-up Questionnaire on Basel II implementation”, Occasional Paper 6, available at www.bis.org

Ghosh, S. and D.M. Nachane (2003), “Are Basel Capital Standards Pro-cyclical? Some

Empirical Evidence from India”, Economic and Political Weekly, 38(8), pp. 777-783

Gill, S. (2005), “An Analysis of Defaults of Long-term Rated Debts”, Vikalpa 30 (1), pp.

8/6/2019 Basel II a New Global Mantra for Indian Banks

http://slidepdf.com/reader/full/basel-ii-a-new-global-mantra-for-indian-banks 14/15

35-50

Griffith-Jones, S., M. Sefoviano and S. Spratt (2002), “Basel II and Developing Countries:

Diversification and Portfolio Effects”, Working Paper of Institute of Development Studies,University of Sussex available at

http://www.ids.ac.uk/ids/global/pdfs/FINALBasel-diversification2.pdf

Gupta, L.C., C P. Gupta and N. Jain (2001), Indian Households’ Investment Preferences:

The Third All-India Survey, Society for Capital Market Research and Development, New

Delhi

Hill, C. (2004), “Regulating the Rating Agencies”, Washington University Law

Quarterly, 82(43), pp. 43-95

Joshi, V. and I.M.D. Little (1996), India's Economic Reforms 1991-2001, Delhi, Oxford

University Press. McKinnon, R.I. (1973), Money and Capital in Economic Development,

Washington D.C, Brookings Institutions.

Leeladhar, V. (2006), “Demystifying Basel II”, Reserve bank of India Bulletin October

2006, pp. 1153-1157

Monfort, B. and C. Mulder (2000), “The Impact of Using Sovereign Ratings by Credit

Rating Agencies on the Capital Requirements for Banks: A Study of Emerging Market

Economies”, IMF Working Paper WP/00/69, March

Nachane, D.M., S. Ghosh and P. Ray (2006), “Basel II and Bank Lending Behaviour:

Some Likely Implications for Monetary Policy”, Economic and Political Weekly,41(11), pp. 1053-1058

Nitsure, R.R. (2005), “Basel II Norms: Emerging Market Perspective with Indian Focus”,

Economic and Political Weekly, 40(12), pp. 1162-1166

Reserve Bank of India (2005a), “Draft Guidelines for Implementation of the New Capital

Adequacy Framework”, RBI Circular DBOD No. BP. 1163/21.04.118/2004-05

Reserve Bank of India (2005b), “Reserve Bank of India Annual Report 2004-05”, available

at www.rbi.org.in

Reserve Bank of India (2006), “Reserve Bank of India Annual Report 2005 -06”, available

at www.rbi.org.in

Reserve Bank of India (2007a), “Revised Draft Guidelines for Implementation of the

New Capital Adequacy Framework”, RBI Circular DBOD No. BP. 1151/21.06.001/2006-

07

8/6/2019 Basel II a New Global Mantra for Indian Banks

http://slidepdf.com/reader/full/basel-ii-a-new-global-mantra-for-indian-banks 15/15

Reserve Bank of India (2007b), “Guidelines for Implementation of the New Capital

Adequacy Framework”, RBI Circular DBOD. No. BP. BC. 90 / 20.06.001/ 2006-07

Related Documents