BASEL I and BASEL II: HISTORY OF AN EVOLUTION Hasan Ersel HSE May 23, 2011

BASEL I and BASEL II: HISTORY OF AN EVOLUTION Hasan Ersel HSE May 23, 2011.

Mar 29, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

BASEL I and BASEL II: HISTORY OF AN EVOLUTION

Hasan ErselHSE

May 23, 2011

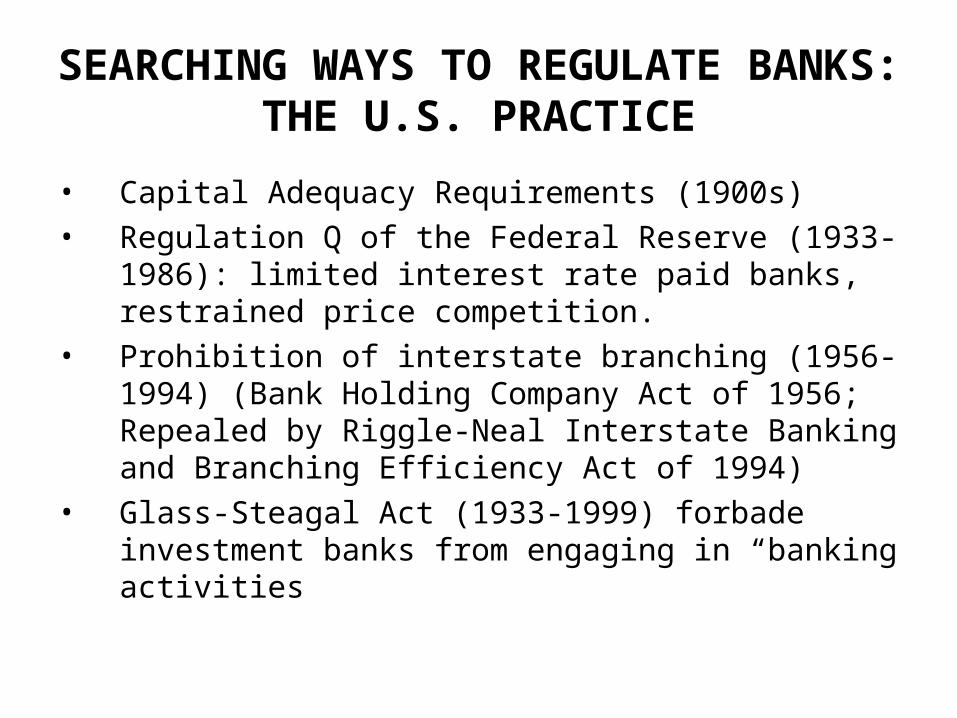

SEARCHING WAYS TO REGULATE BANKS: THE U.S. PRACTICE

• Capital Adequacy Requirements (1900s)• Regulation Q of the Federal Reserve (1933-1986):

limited interest rate paid banks, restrained price competition.

• Prohibition of interstate branching (1956-1994) (Bank Holding Company Act of 1956; Repealed by Riggle-Neal Interstate Banking and Branching Efficiency Act of 1994)

• Glass-Steagal Act (1933-1999) forbade investment banks from engaging in “banking activities

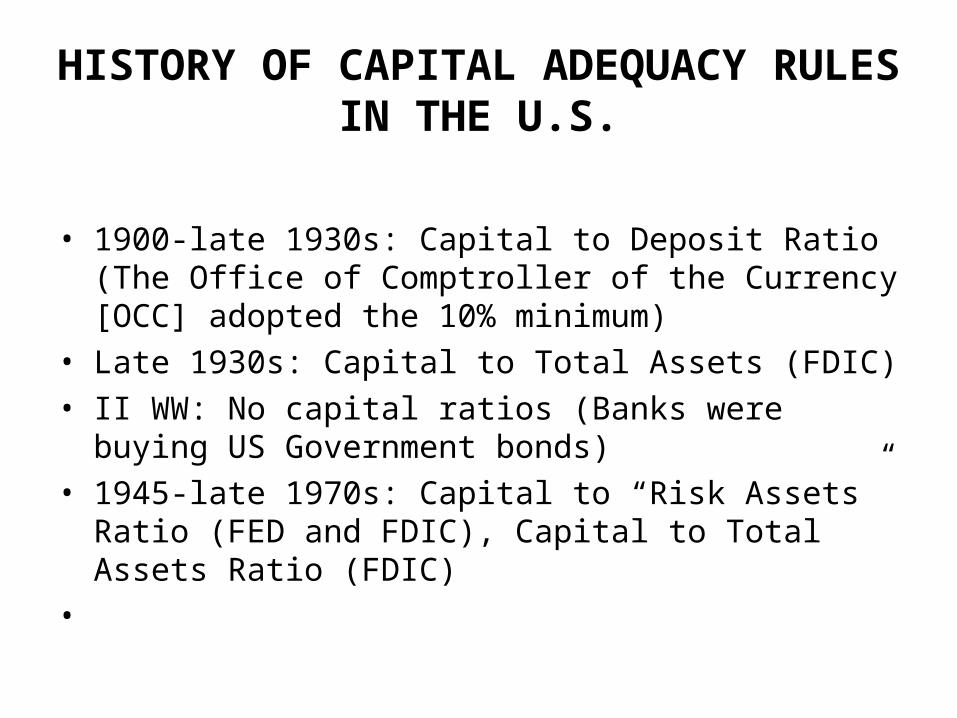

HISTORY OF CAPITAL ADEQUACY RULES IN THE U.S.

• 1900-late 1930s: Capital to Deposit Ratio (The Office of Comptroller of the Currency [OCC] adopted the 10% minimum)

• Late 1930s: Capital to Total Assets (FDIC) • II WW: No capital ratios (Banks were buying US

Government bonds)• 1945-late 1970s: Capital to “Risk Assets” Ratio (FED

and FDIC), Capital to Total Assets Ratio (FDIC)•

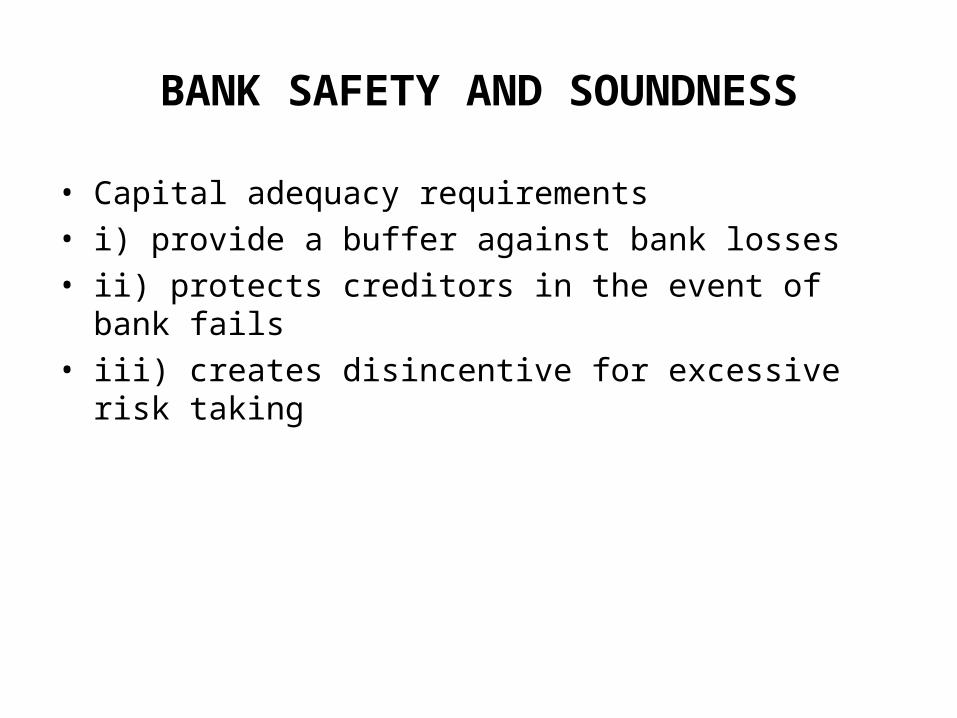

BANK SAFETY AND SOUNDNESS

• Capital adequacy requirements• i) provide a buffer against bank losses• ii) protects creditors in the event of bank fails• iii) creates disincentive for excessive risk taking

INTERNATIONAL REGULATION

• 1988 Basel Accord (Basel-I)• 1993 Proposal: Standard Model• 1996 Modification: Internal Model • New Basel Accord (Basel-II)

THE FIRST BASEL ACCORD

The first Basel Accord (Basel-I) was completed in 1988

WHY BASEL-I WAS NEEDED?

The reason was to create a level playing field for “internationally active banks”

– Banks from different countries competing for the same loans would have to set aside roughly the same amount of capital on the loans

1988 BASEL ACCORD (BASEL-I)

1)The purpose was to prevent international banks from building business volume without adequate capital backing

2) The focus was on credit risk

3) Set minimum capital standards for banks

4) Became effective at the end of 1992

A NEW CONCEPT: RISK BASED CAPITAL

Basel-I was hailed for incorporating risk into the calculation of capital requirements

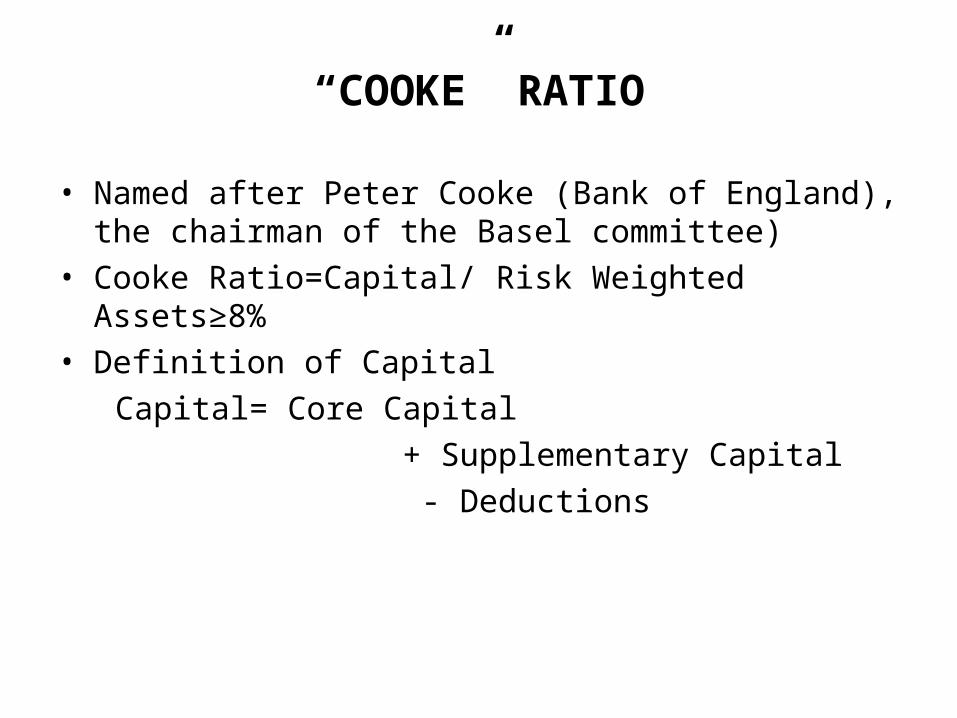

“COOKE” RATIO

• Named after Peter Cooke (Bank of England), the chairman of the Basel committee)

• Cooke Ratio=Capital/ Risk Weighted Assets≥8%• Definition of Capital

Capital= Core Capital

+ Supplementary Capital

- Deductions

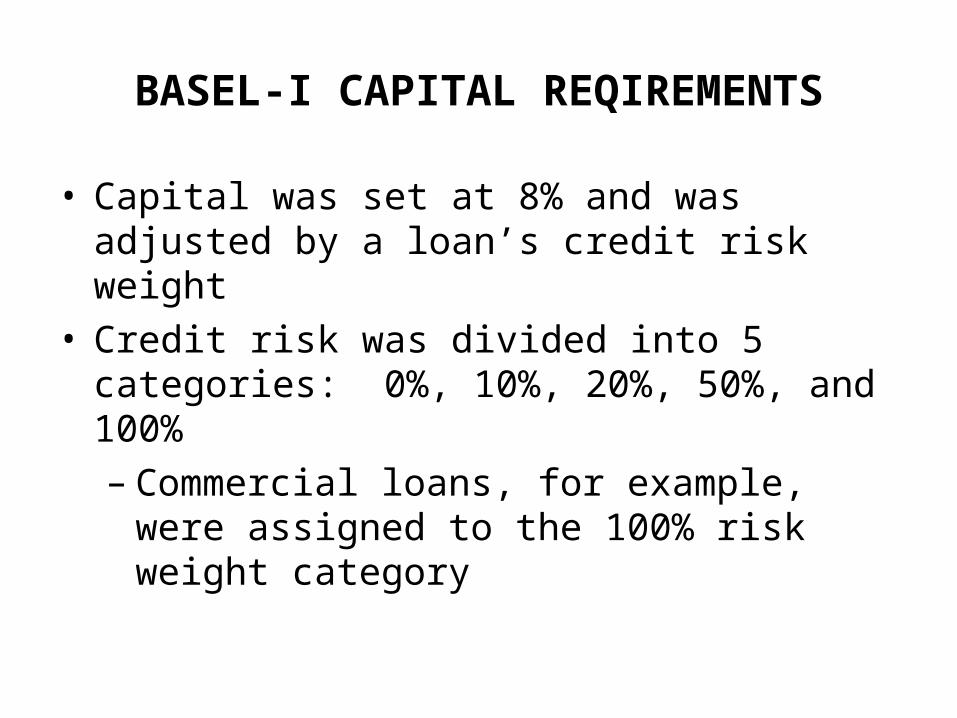

BASEL-I CAPITAL REQIREMENTS

• Capital was set at 8% and was adjusted by a loan’s credit risk weight

• Credit risk was divided into 5 categories: 0%, 10%, 20%, 50%, and 100%– Commercial loans, for example, were

assigned to the 100% risk weight category

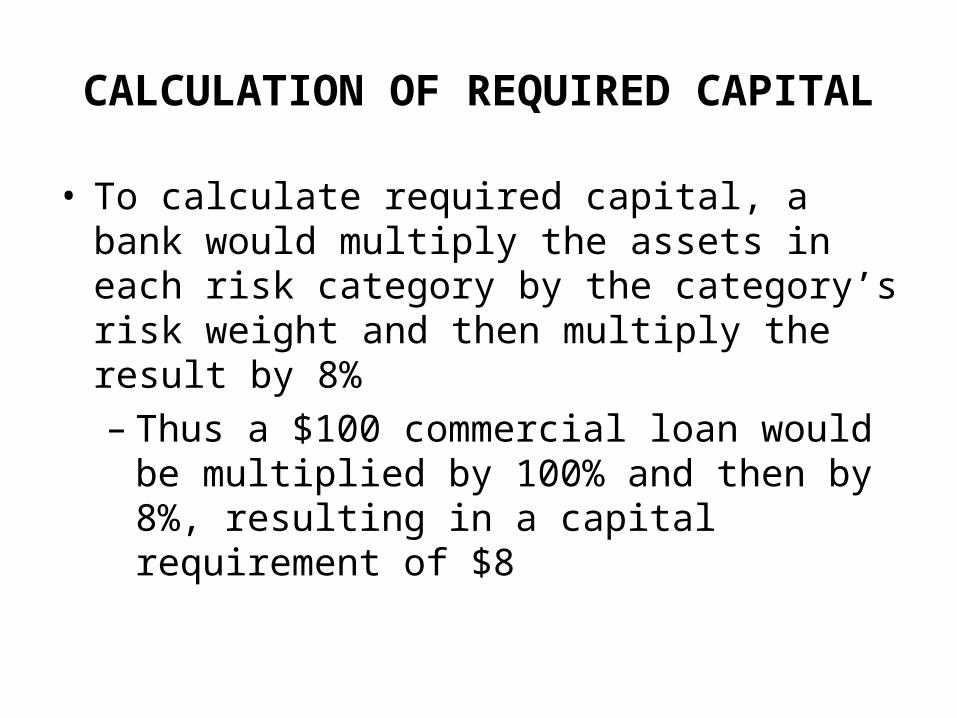

CALCULATION OF REQUIRED CAPITAL

• To calculate required capital, a bank would multiply the assets in each risk category by the category’s risk weight and then multiply the result by 8%– Thus a $100 commercial loan would be

multiplied by 100% and then by 8%, resulting in a capital requirement of $8

CORE & SUPPLEMENTARY CAPITAL

1) Core Capital (Tier I Capital) i) Paid Up Capital

ii) Disclosed Reserves (General and Legal Reserves)

2) Supplementary Capital (Tier II Capital) i) General Loan-loss Provisions

ii) Undisclosed Reserves (other provisions against

probable losses)

iii) Asset Revaluation Reserves

iv) Subordinated Term Debt (5+ years maturity)

v) Hybrid (debt/equity) instruments

DEDUCTIONS FROM THE CAPITAL

• Investments in unconsolidated banking and financial subsidiary companies and investments in the capital of other banks & financial institutions

• Goodwill

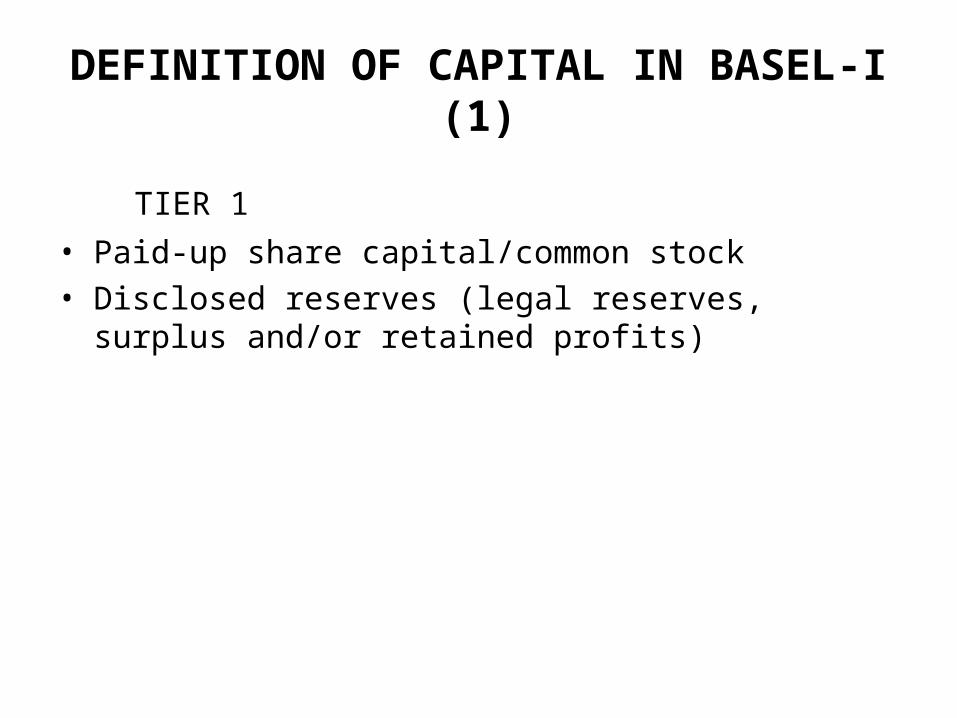

DEFINITION OF CAPITAL IN BASEL-I(1)

TIER 1

• Paid-up share capital/common stock• Disclosed reserves (legal reserves, surplus and/or

retained profits)

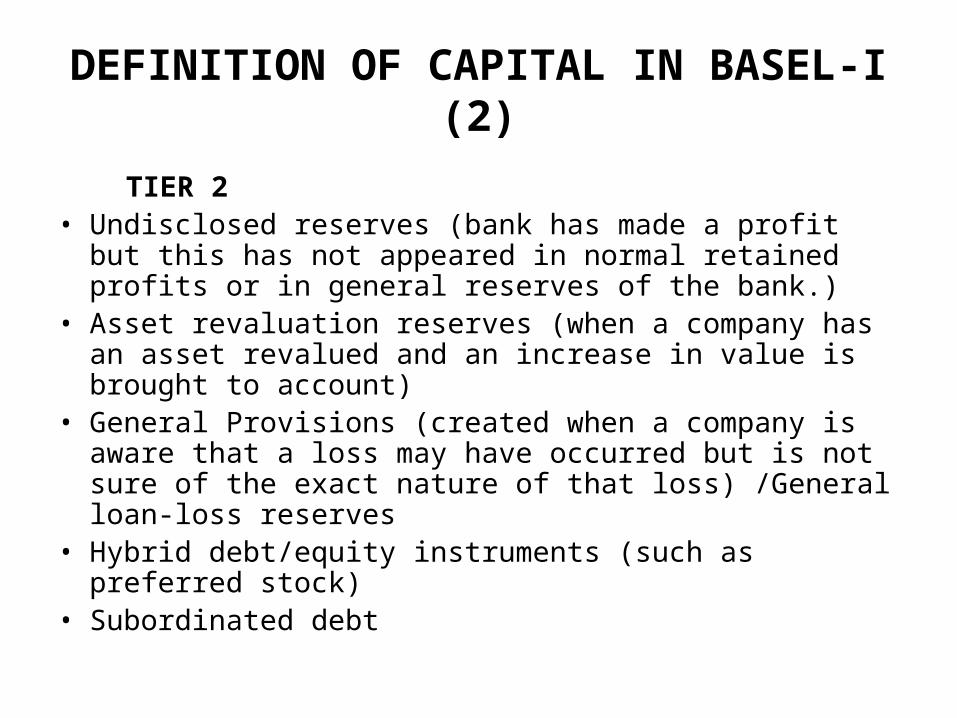

DEFINITION OF CAPITAL IN BASEL-I(2)

TIER 2 • Undisclosed reserves (bank has made a profit but this

has not appeared in normal retained profits or in general reserves of the bank.)

• Asset revaluation reserves (when a company has an asset revalued and an increase in value is brought to account)

• General Provisions (created when a company is aware that a loss may have occurred but is not sure of the exact nature of that loss) /General loan-loss reserves

• Hybrid debt/equity instruments (such as preferred stock)• Subordinated debt

RISK WEIGHT CATEGORIES IN BASEL-I (1)

0% Risk Weight: • Cash, • Claims on central governments and central

banks denominated in national currency and funded in that currency

• Other claims on OECD countries, central governments and central banks

• Claims collateralized by cash of OECD government securities or guaranteed by OECD Governments

RISK WEIGHT CATEGORIES IN BASEL-I (2)

20% Risk Weight• Claims on multilateral development banks and claims

guaranteed or collateralized by securities issued by such banks

• Claims on, or guaranteed by, banks incorporated in the OECD

• Claims on, or guaranteed by, banks incorporated in countries outside the OECD with residual maturity of up to one year

• Claims on non-domestic OECD public-sector entities, excluding central government, and claims on guaranteed securities issued by such entities

• Cash items in the process of collection

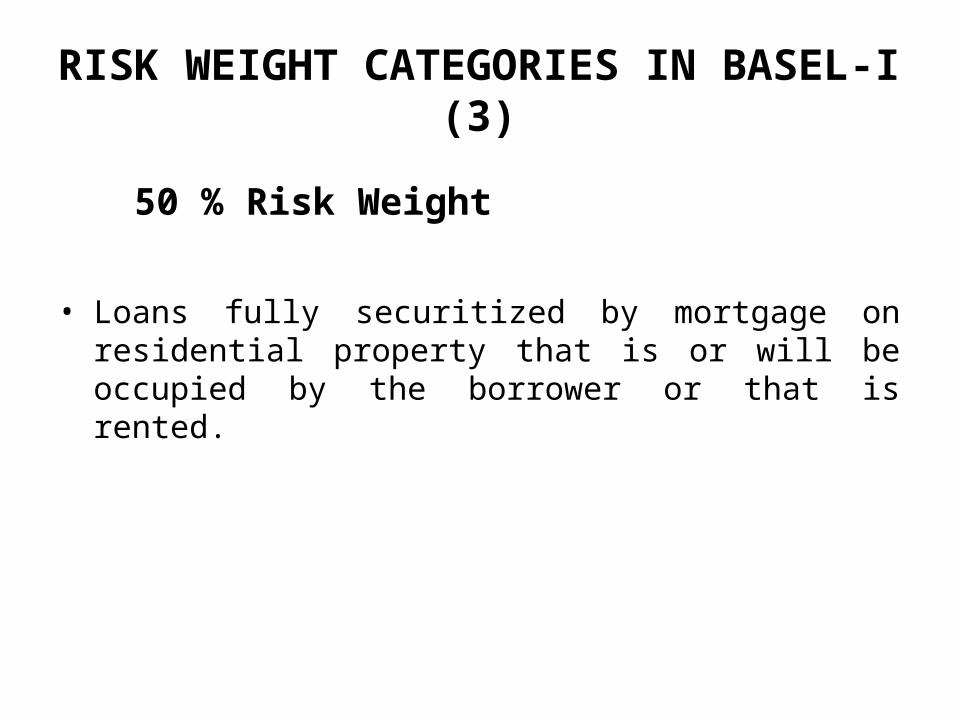

RISK WEIGHT CATEGORIES IN BASEL-I (3)

50 % Risk Weight

• Loans fully securitized by mortgage on residential property that is or will be occupied by the borrower or that is rented.

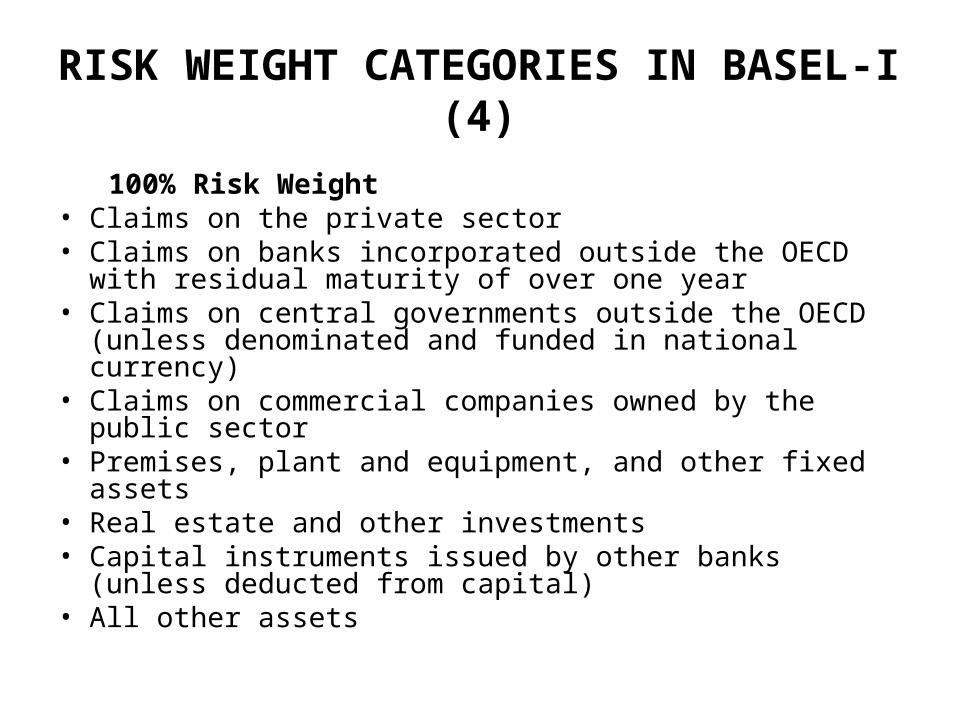

RISK WEIGHT CATEGORIES IN BASEL-I (4)

100% Risk Weight• Claims on the private sector• Claims on banks incorporated outside the OECD with

residual maturity of over one year• Claims on central governments outside the OECD

(unless denominated and funded in national currency)• Claims on commercial companies owned by the public

sector• Premises, plant and equipment, and other fixed assets• Real estate and other investments• Capital instruments issued by other banks (unless

deducted from capital)• All other assets

RISK WEIGHT CATEGORIES IN BASEL-I (5)

At National Discretion (0,10,20 or 50%)

• Claims on domestic public sector entities, excluding central governments, and loans guaranteed by securities issued by such entities

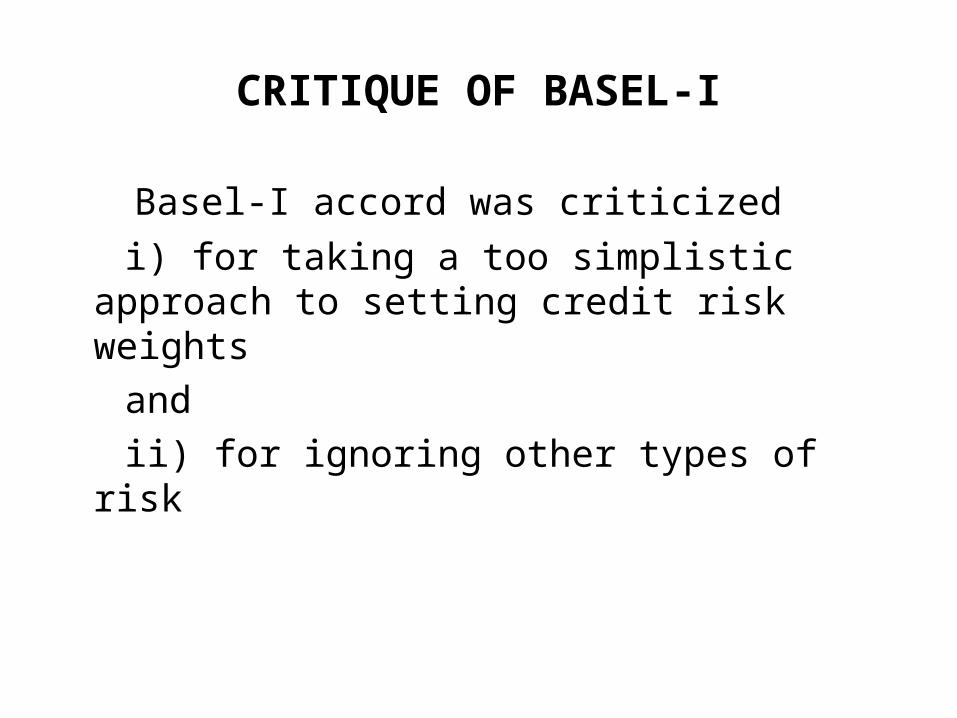

CRITIQUE OF BASEL-I

Basel-I accord was criticized

i) for taking a too simplistic approach to setting credit risk weights

and

ii) for ignoring other types of risk

THE PROBLEM WITH THE RISK

WEIGHTS

• Risk weights were based on what the parties to the Accord negotiated rather than on the actual risk of each asset – Risk weights did not flow from any particular

insolvency probability standard, and were for the most part, arbitrary.

OPERATIONAL AND OTHER RISKS

• The requirements did not explicitly account for operating and other forms of risk that may also be important– Except for trading account activities, the capital

standards did not account for hedging, diversification, and differences in risk management techniques

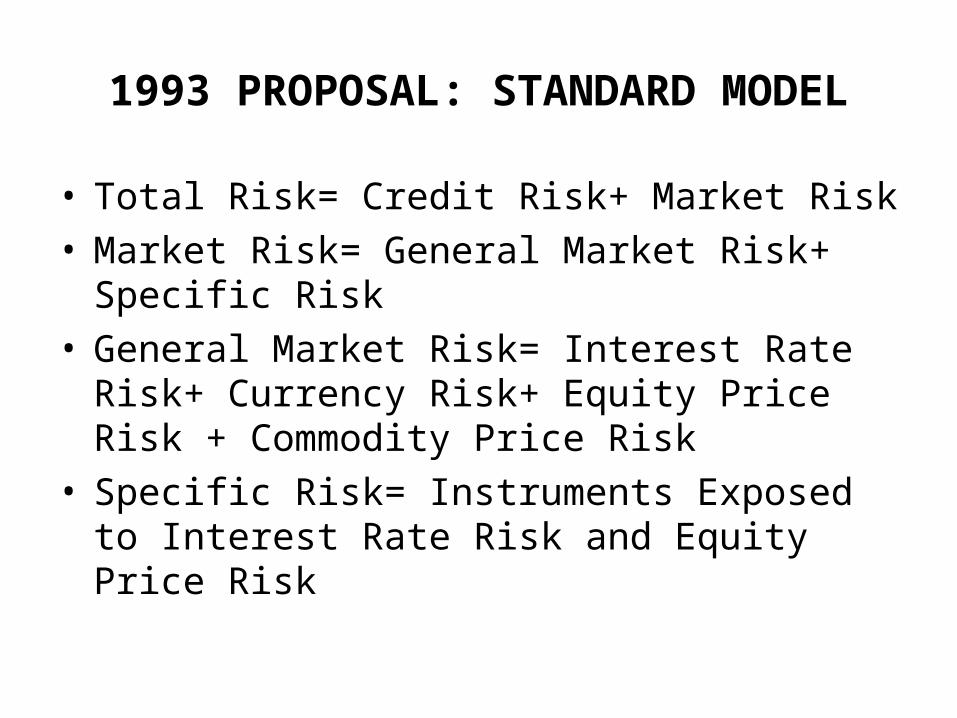

1993 PROPOSAL: STANDARD MODEL

• Total Risk= Credit Risk+ Market Risk• Market Risk= General Market Risk+ Specific

Risk• General Market Risk= Interest Rate Risk+

Currency Risk+ Equity Price Risk + Commodity Price Risk

• Specific Risk= Instruments Exposed to Interest Rate Risk and Equity Price Risk

1996 MODIFICATION: INTERNAL MODEL

• Internal Model → Value at Risk Methodology

• Tier III Capital (Only for Market Risk)

i) Long Term subordinated debt

ii) Option not to pay if minimum required capital is <8%

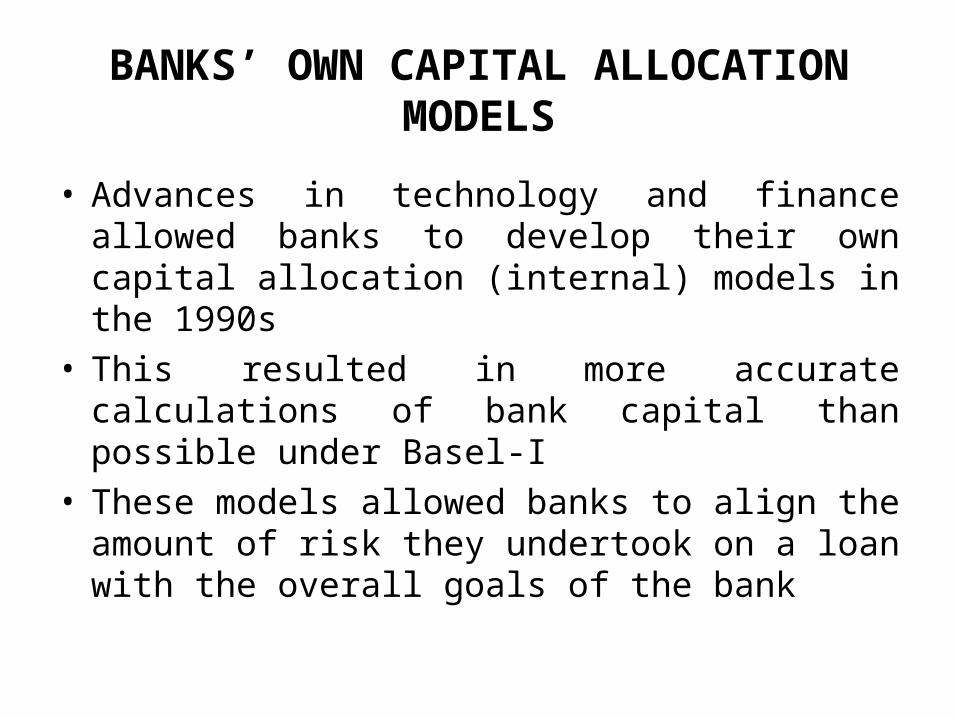

BANKS’ OWN CAPITAL ALLOCATION MODELS

• Advances in technology and finance allowed banks to develop their own capital allocation (internal) models in the 1990s

• This resulted in more accurate calculations of bank capital than possible under Basel-I

• These models allowed banks to align the amount of risk they undertook on a loan with the overall goals of the bank

INTERNAL MODELS AND BASEL I

• Internal models allow banks to more finely differentiate risks of individual loans than is possible under Basel-I– Risk can be differentiated within loan categories and

between loan categories– Allows the application of a “capital charge” to each

loan, rather than each category of loan

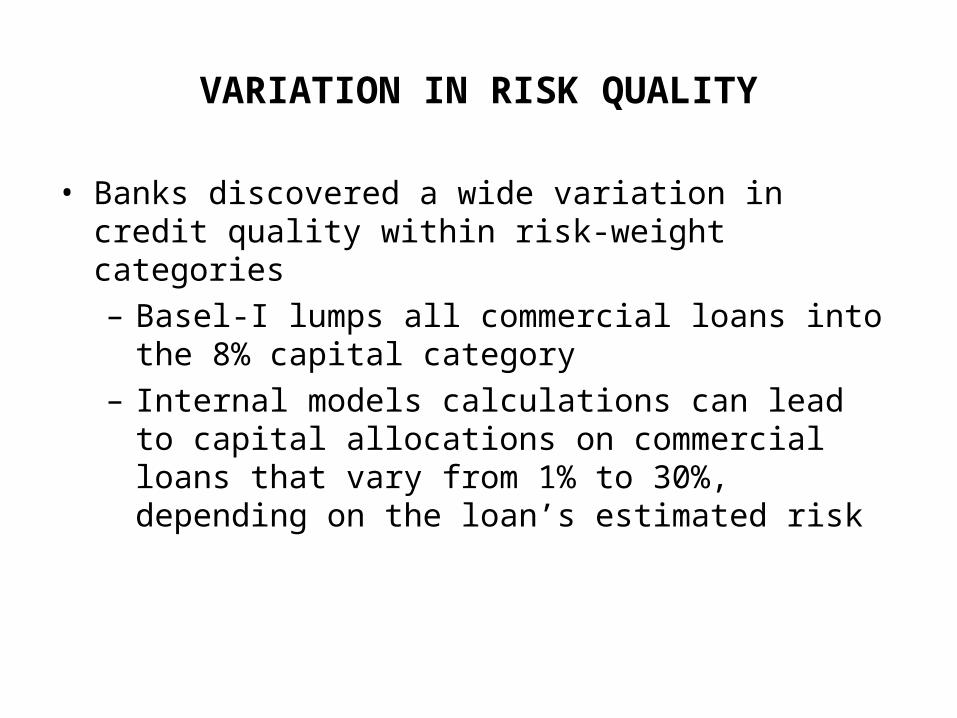

VARIATION IN RISK QUALITY

• Banks discovered a wide variation in credit quality within risk-weight categories– Basel-I lumps all commercial loans into the 8% capital

category– Internal models calculations can lead to capital

allocations on commercial loans that vary from 1% to 30%, depending on the loan’s estimated risk

CAPITAL ARBITRAGE

• If a loan is calculated to have an internal capital charge that is low compared to the 8% standard, the bank has a strong incentive to undertake regulatory capital arbitrage

• Securitization is the main means used especially by U.S. banks to engage in regulatory capital arbitrage

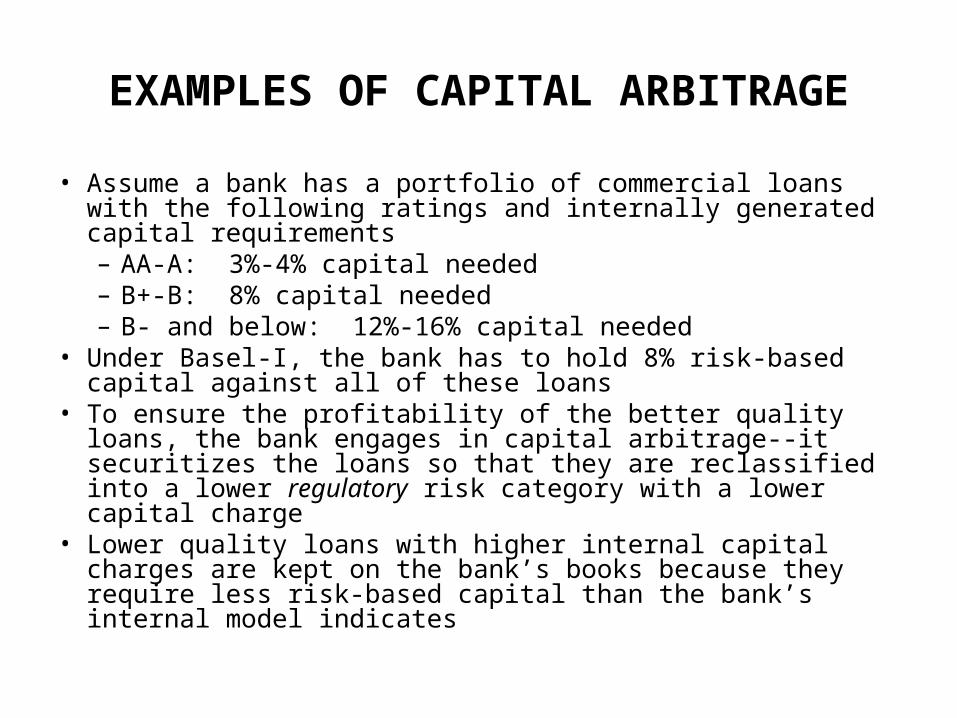

EXAMPLES OF CAPITAL ARBITRAGE

• Assume a bank has a portfolio of commercial loans with the following ratings and internally generated capital requirements– AA-A: 3%-4% capital needed– B+-B: 8% capital needed– B- and below: 12%-16% capital needed

• Under Basel-I, the bank has to hold 8% risk-based capital against all of these loans

• To ensure the profitability of the better quality loans, the bank engages in capital arbitrage--it securitizes the loans so that they are reclassified into a lower regulatory risk category with a lower capital charge

• Lower quality loans with higher internal capital charges are kept on the bank’s books because they require less risk-based capital than the bank’s internal model indicates

NEW APPRACH TO RISK-BASED CAPITAL

• By the late 1990s, growth in the use of regulatory capital arbitrage led the Basel Committee to begin work on a new capital regime (Basel-II)

• Effort focused on using banks’ internal rating models and internal risk models

• June 1999: Committee issued a proposal for a new capital adequacy framework to replace the 1998 Accord

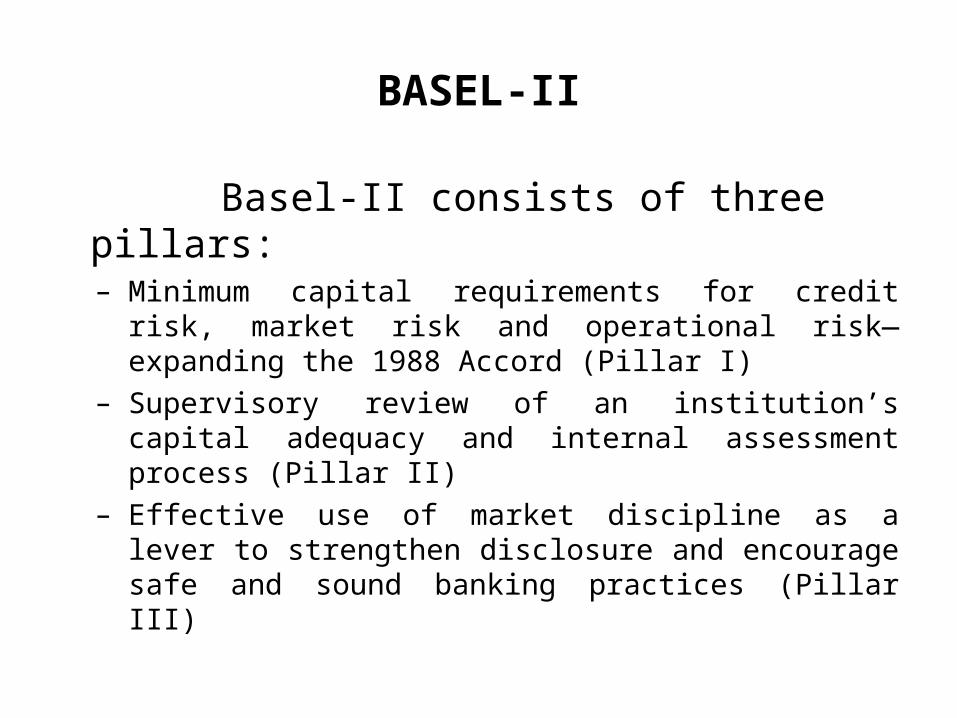

BASEL-II

BASEL-II

Basel-II consists of three pillars:– Minimum capital requirements for credit risk, market

risk and operational risk—expanding the 1988 Accord (Pillar I)

– Supervisory review of an institution’s capital adequacy and internal assessment process (Pillar II)

– Effective use of market discipline as a lever to strengthen disclosure and encourage safe and sound banking practices (Pillar III)

IMPLEMENTATION OF THE BASEL II ACCORD

• Implementation of the Basel II Framework continues to move forward around the globe. A significant number of countries and banks already implemented the standardized and foundation approaches as of the beginning of 2007.

• In many other jurisdictions, the necessary infrastructure (legislation, regulation, supervisory guidance, etc) to implement the Framework is either in place or in process, which will allow a growing number of countries to proceed with implementation of Basel II’s advanced approaches in 2008 and 2009.

• This progress is taking place in both Basel Committee member and non-member countries.

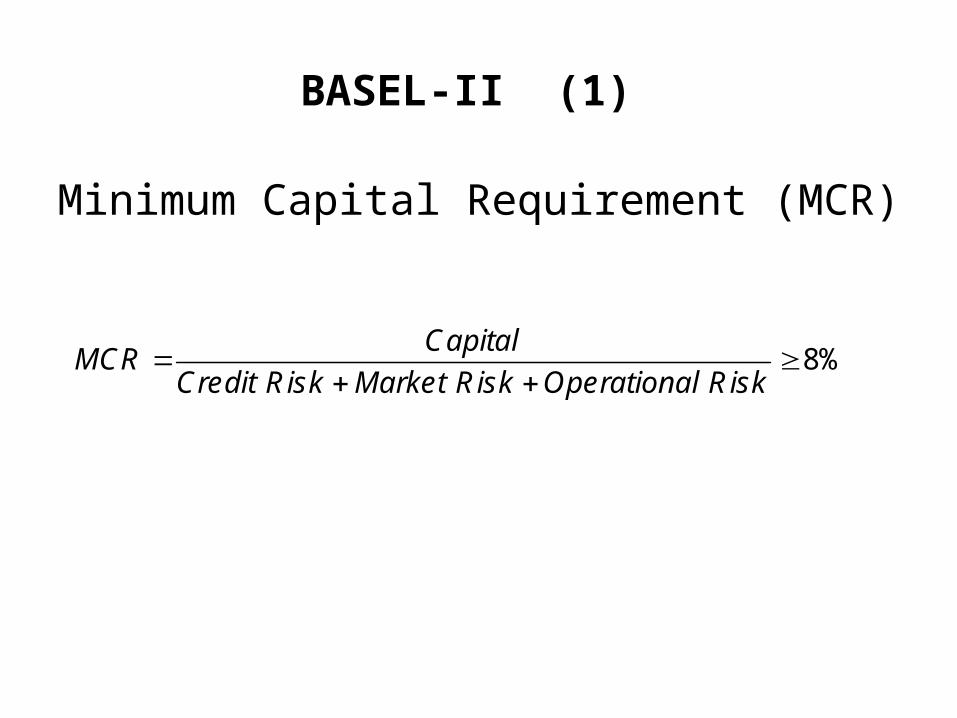

BASEL-II (1)

Minimum Capital Requirement (MCR)

8%Capital

MCRCredit Risk Market Risk Operational Risk

BASEL-II (2)

PILLAR I: Minimum Capital Requirement

1) Capital Measurement: New Methods

2) Market Risk: In Line with 1993 & 1996

3) Operational Risk: Working on new methods

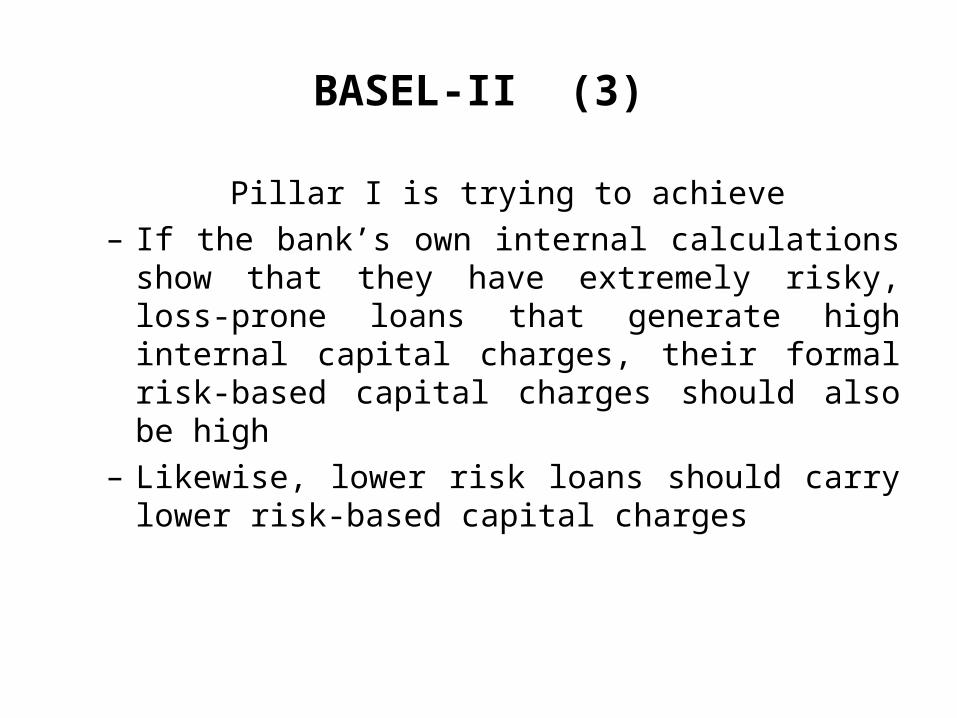

BASEL-II (3)

Pillar I is trying to achieve– If the bank’s own internal calculations show that they

have extremely risky, loss-prone loans that generate high internal capital charges, their formal risk-based capital charges should also be high

– Likewise, lower risk loans should carry lower risk-based capital charges

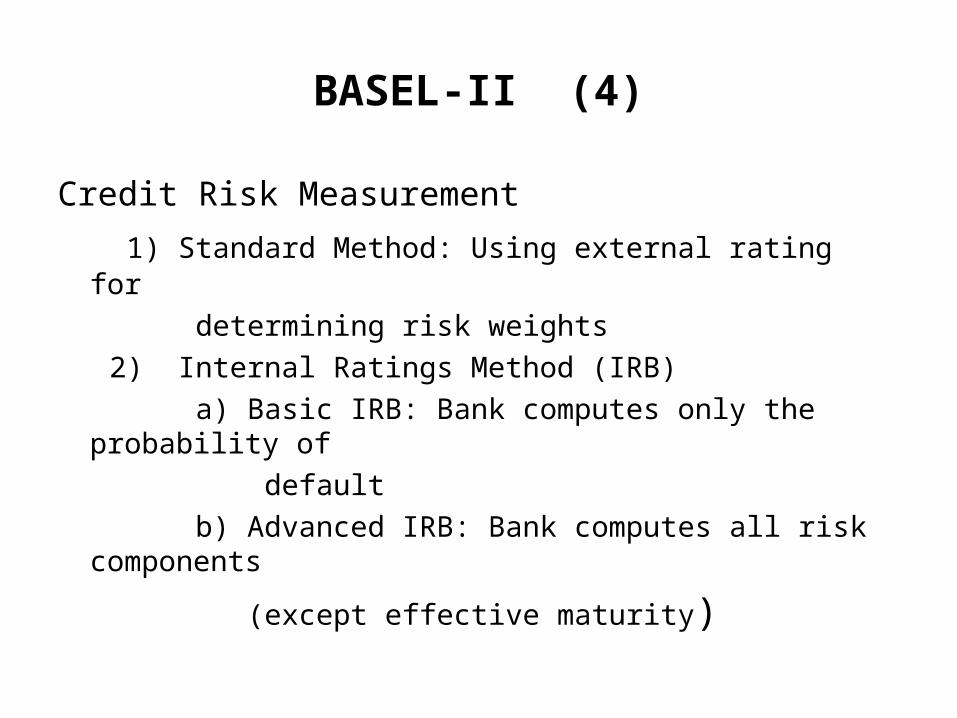

BASEL-II (4)

Credit Risk Measurement

1) Standard Method: Using external rating for

determining risk weights

2) Internal Ratings Method (IRB)

a) Basic IRB: Bank computes only the probability of

default

b) Advanced IRB: Bank computes all risk components

(except effective maturity)

BASEL-II (5)

Operational Risk Measurement

1) Basic Indicator Approach

2) Standard Approach

3) Internal Measurement Approach

BASEL-II (6)

• Pillar I also adds a new capital component for operational risk– Operational risk covers the risk of loss due to system

breakdowns, employee fraud or misconduct, errors in models or natural or man-made catastrophes, among others

BASEL-II (7)

PILLAR 2: Supervisory Review Process

1) Banks are advised to develop an internal capital assessment process and set targets for capital to commensurate with the bank’s risk profile

2) Supervisory authority is responsible for evaluating how well banks are assessing their capital adequacy

BASEL-II (8)

PILLAR 3: Market Discipline

Aims to reinforce market discipline through enhanced disclosure by banks. It is an indirect approach, that assumes sufficient competition within the banking sector.

ASSESSING BASEL-II

• To determine if the proposed rules are likely to yield reasonable risk-based capital requirements within and between countries for banks with similar portfolios, four quantitative impact studies (QIS) have been undertaken

RESULTS OF QUANTITATIVE IMPACT STUDIES (QIS)

• Results of the QIS studies have been troubling– Wide swings in risk-based capital

requirements– Some individual banks show unreasonably

large declines in required capital• As a result, parts of the Basel II Accord have

been revised

IMPLICATIONS OF BASEL-II (1)

• The practices in Basel II represent several important departures from the traditional calculation of bank capital– The very largest banks will operate under a system

that is different than that used by other banks– The implications of this for long-term competition

between these banks is uncertain, but merits further attention

IMPLICATIONS OF BASEL-II (2)

• Basel II’s proposals rely on banks’ own internal risk estimates to set capital requirements– This represents a conceptual leap in determining

adequate regulatory capital• For regulators, evaluating the integrity of bank models is

a significant step beyond the traditional supervisory process

IMPLICATIONS OF BASEL-II (3)

Despite Basel II’s quantitative basis, much will still depend on the judgment

1) of banks in formulating their estimates

and

2) of supervisors in validating the assumptions used by banks in their models

PRO-CYCLICALITY OF THE CAPITAL ADEQUACY REQUIREMENT

• “In a downturn, when a bank’s capital base is likely being eroded by loan losses, its existing (non-defaulted) borrowers will be downgraded by the relevant credit-risk models, forcing the bank to hold more capital against its current loan portfolio. To the extent that it is difficult or costly for the bank to raise fresh external capital in bad times, it will be forced to cut back on its lending activity, thereby contributing to a worsening of the initial downturn.”

Kashyap & Stein (2004, p. 18)

Related Documents