Unlocking investment in Africa’s renewables: what are the binding constraints? First Panel: Planning On-Grid Perspective: Observations from Nigeria Presented by Dr Barry Rawn Thursday 19th January 2017

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Unlocking investment in Africa’s renewables: what are the binding constraints?

First Panel: PlanningOn-Grid Perspective: Observations from NigeriaPresented by Dr Barry Rawn

Thursday 19th January 2017

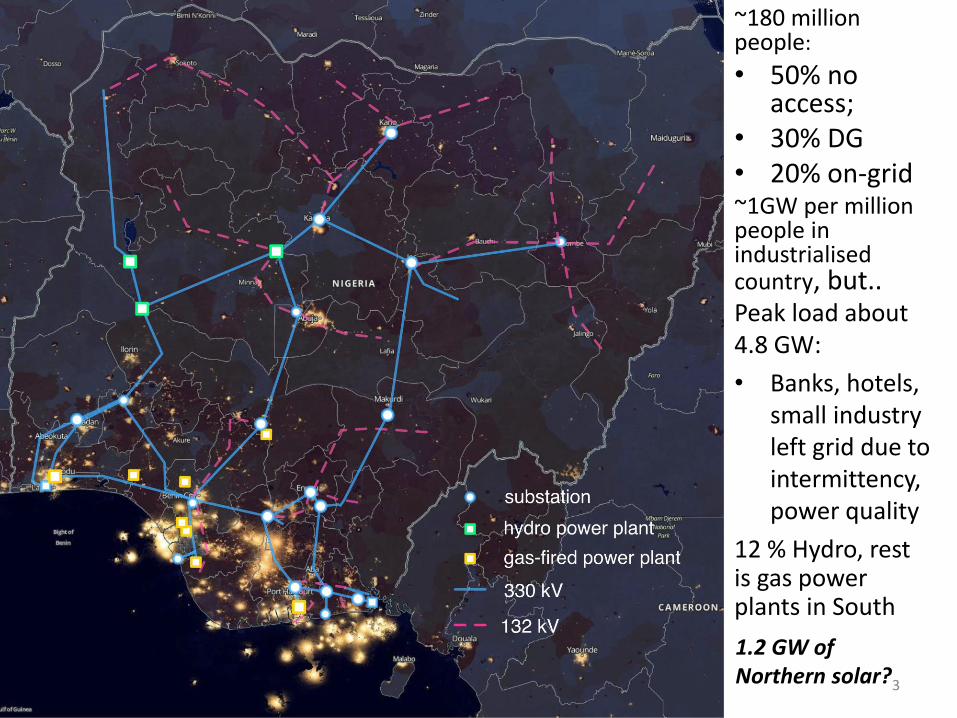

~180 million people:

• 50% no access;

• 30% DG• 20% on-grid~1GW per million people in industrialisedcountry, but..

2

Peak load about 4.8 GW:

• Banks, hotels, small industry left grid due to intermittency, power quality

~180 million people:

• 50% no access;

• 30% DG• 20% on-grid~1GW per million people in industrialisedcountry, but..

12 % Hydro, rest is gas power plants in South

1.2 GW of Northern solar?3

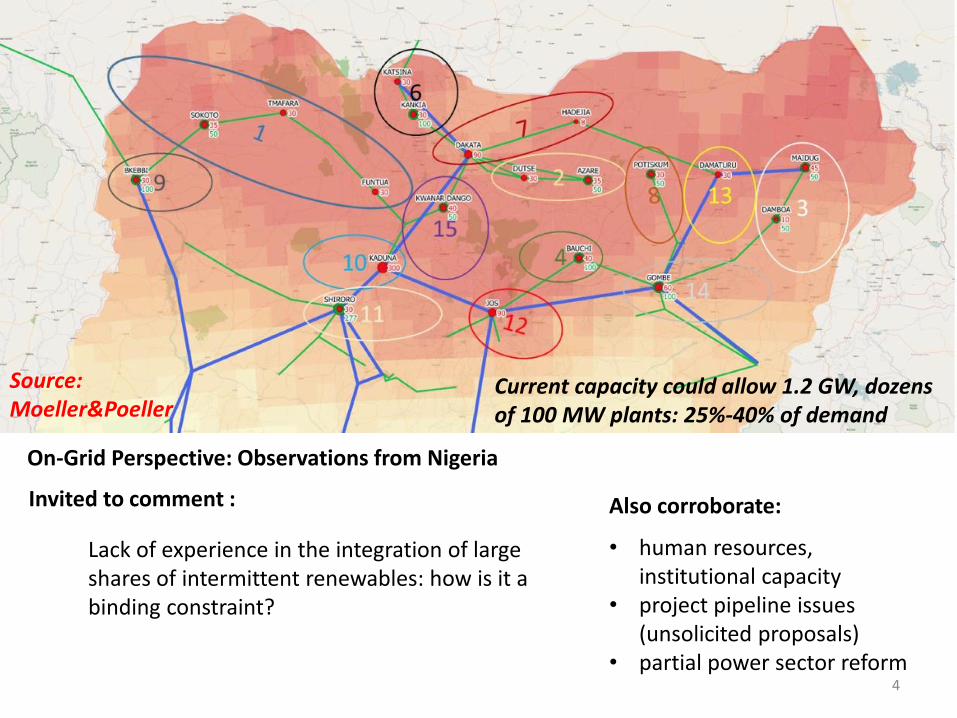

Lack of experience in the integration of large shares of intermittent renewables: how is it a binding constraint?

Invited to comment :

On-Grid Perspective: Observations from Nigeria

Also corroborate:

• human resources, institutional capacity

• project pipeline issues (unsolicited proposals)

• partial power sector reform

Current capacity could allow 1.2 GW, dozens of 100 MW plants: 25%-40% of demand

Source:Moeller&Poeller

4

Investment in training and skills development is a least regret investment that improves planning (A Tale of Two Doctors)

Additional Offering:

On-Grid Perspective: Observations from Nigeria

Investor confidence in utility commercial transactions, operations increases when 3rd party ensures data transparency and auditability. (EPSRC GCRF Proposal)

(1)

(2)

A working power system is much more about people and processes than equipment and calculation.

Key observation:

5

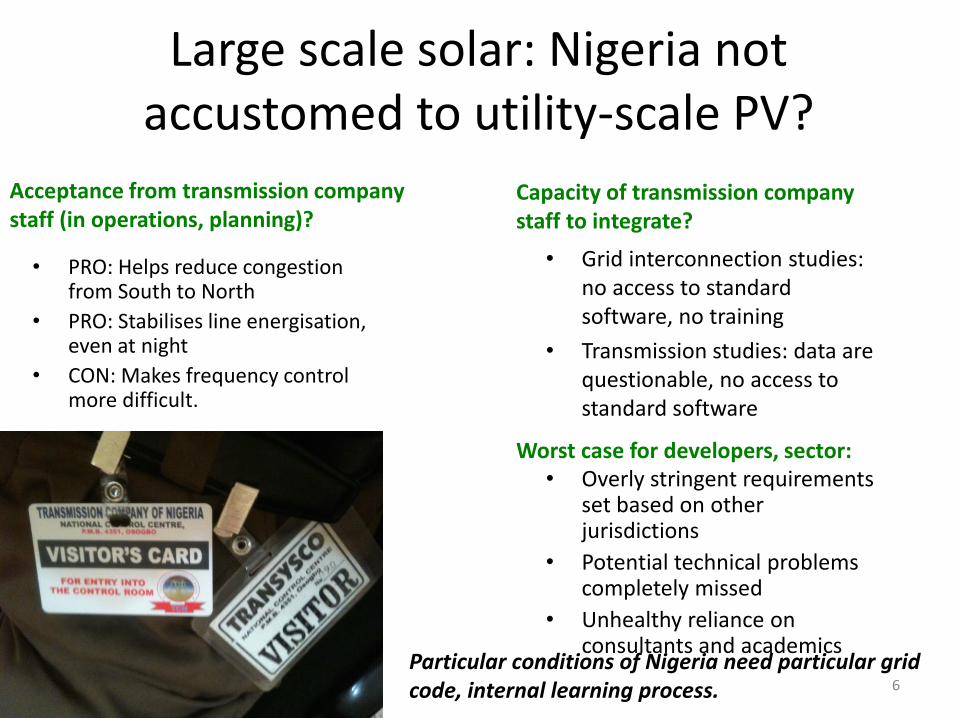

Large scale solar: Nigeria not accustomed to utility-scale PV?

• PRO: Helps reduce congestion from South to North

• PRO: Stabilises line energisation, even at night

• CON: Makes frequency control more difficult.

Acceptance from transmission company staff (in operations, planning)?

Capacity of transmission company staff to integrate?

• Grid interconnection studies: no access to standard software, no training

• Transmission studies: data are questionable, no access to standard software

Particular conditions of Nigeria need particular grid code, internal learning process.

Worst case for developers, sector:• Overly stringent requirements

set based on other jurisdictions

• Potential technical problems completely missed

• Unhealthy reliance on consultants and academics

6

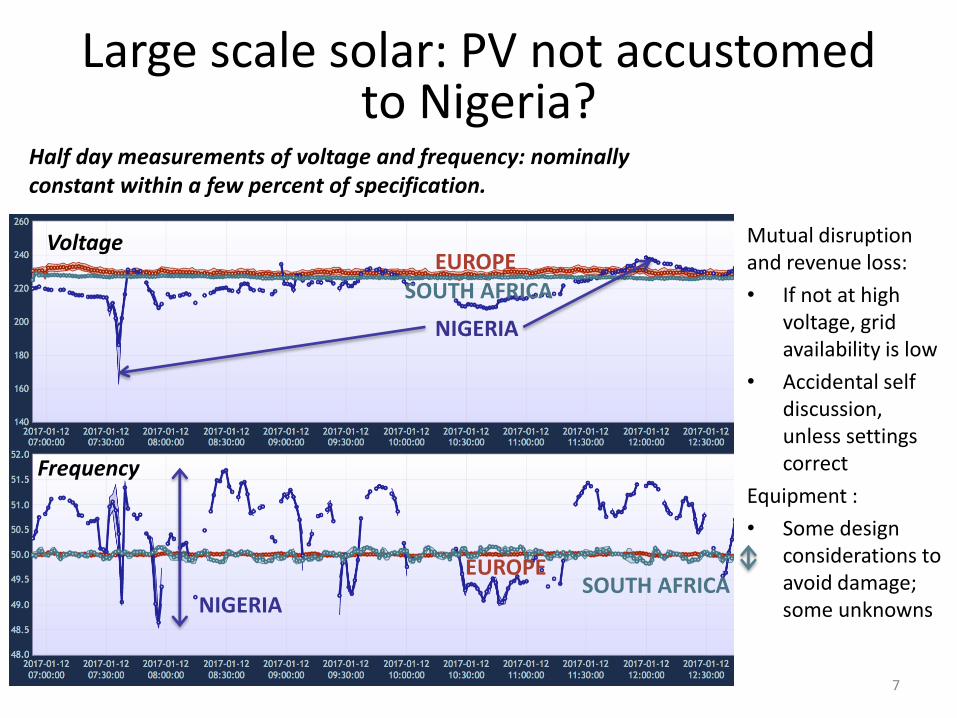

Large scale solar: PV not accustomed to Nigeria?

NIGERIA

SOUTH AFRICAEUROPE

NIGERIASOUTH AFRICA

EUROPE

Mutual disruption and revenue loss:

• If not at high voltage, grid availability is low

• Accidental self discussion, unless settings correct

Equipment :

• Some design considerations to avoid damage; some unknowns

Half day measurements of voltage and frequency: nominally constant within a few percent of specification.

Voltage

Frequency

7

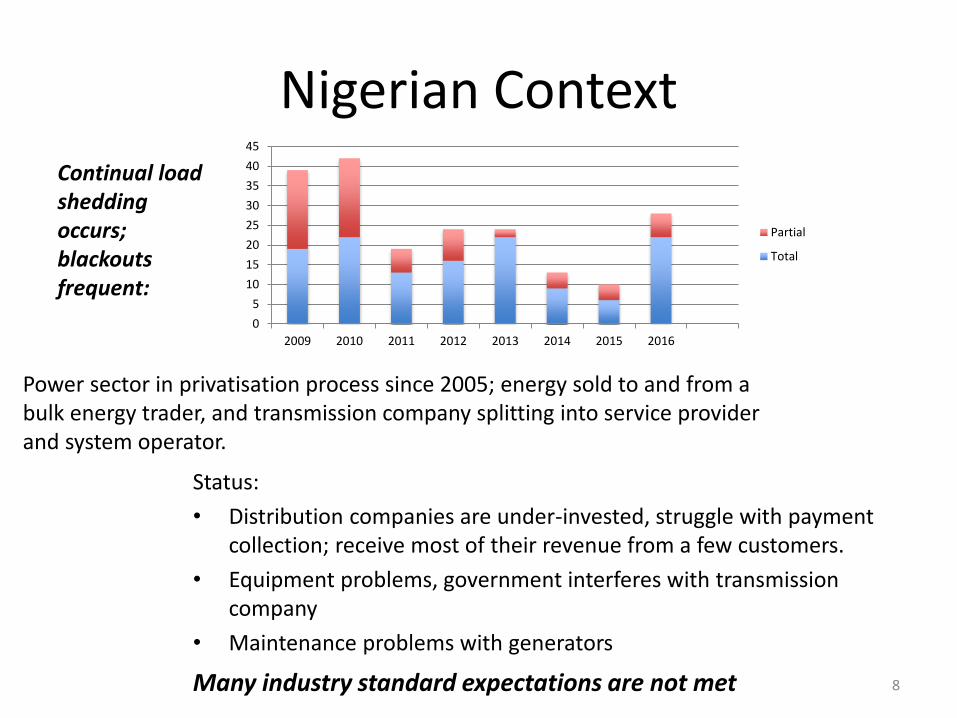

Nigerian Context

Status:

• Distribution companies are under-invested, struggle with payment collection; receive most of their revenue from a few customers.

• Equipment problems, government interferes with transmission company

• Maintenance problems with generators

Power sector in privatisation process since 2005; energy sold to and from a bulk energy trader, and transmission company splitting into service provider and system operator.

Continual load shedding occurs; blackouts frequent:

0

5

10

15

20

25

30

35

40

45

2009 2010 2011 2012 2013 2014 2015 2016

Partial

Total

Many industry standard expectations are not met 8

Transmission PlanningNormal setting:

• Data flawed, analysis capacity limited and experience limited; struggle with pipeline of projects

• Budget moved within government as corruption safeguard, constrained

• Significant Forex risk

• Land Use Act leads to right of way problems

• privatisation layers short term pain on potential transformation

Nigerian context:

• System assets well characterised

• Cost recovery over decades, from balance sheet

• Assume predictable and stable regulated revenue

• Assume stable currency

• Transmission projects experience delay, failure to obtain permits

• Unbundling and privatisationincreases uncertainty, requires stronger regulation, long term energy policy.

Criteria: invest to increase reliability, decrease cost of energy, minimise regret:

Criteria: can be political, donor driven; increase load allocated, reliability

Planning task is relatively crucial: large changes in reliability and viability of sector at stake. 9

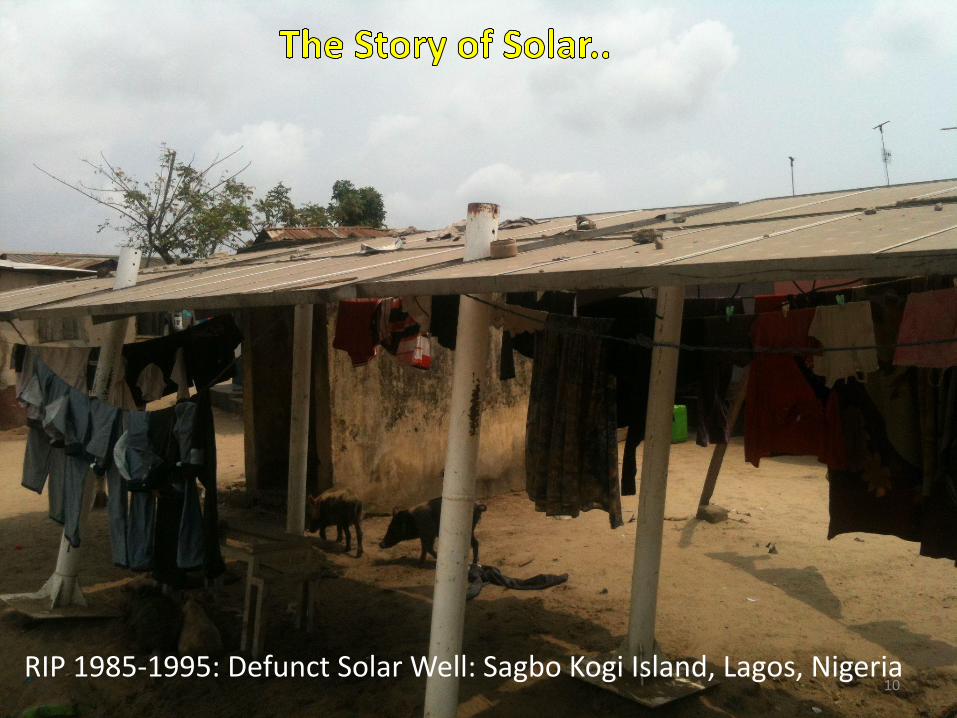

RIP 1985-1995: Defunct Solar Well: Sagbo Kogi Island, Lagos, Nigeria10

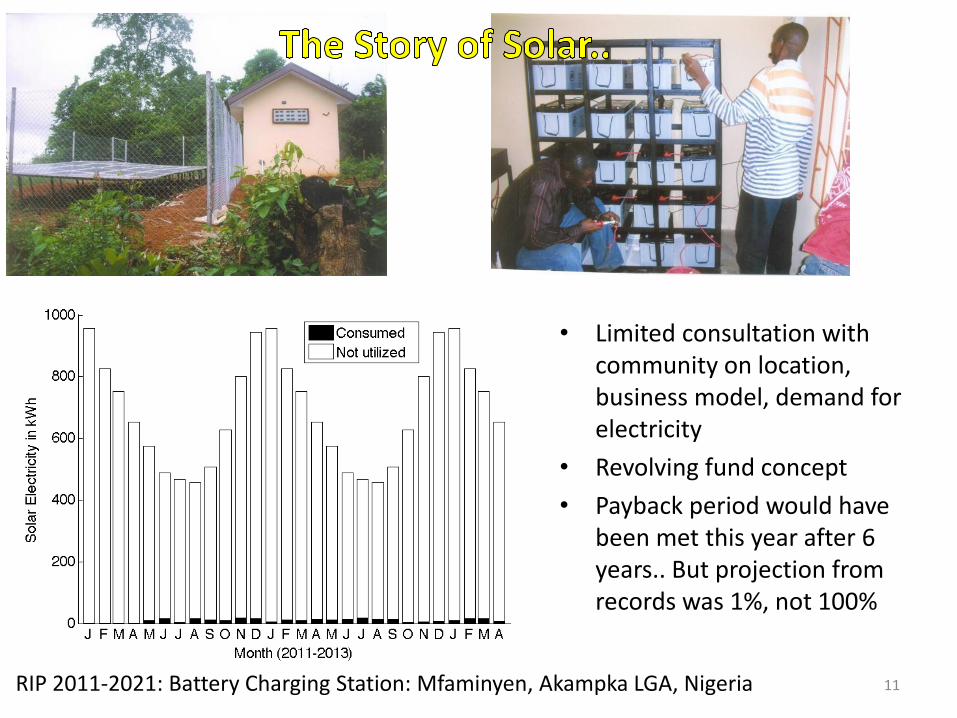

• Limited consultation with community on location, business model, demand for electricity

• Revolving fund concept

• Payback period would have been met this year after 6 years.. But projection from records was 1%, not 100%

RIP 2011-2021: Battery Charging Station: Mfaminyen, Akampka LGA, Nigeria 11

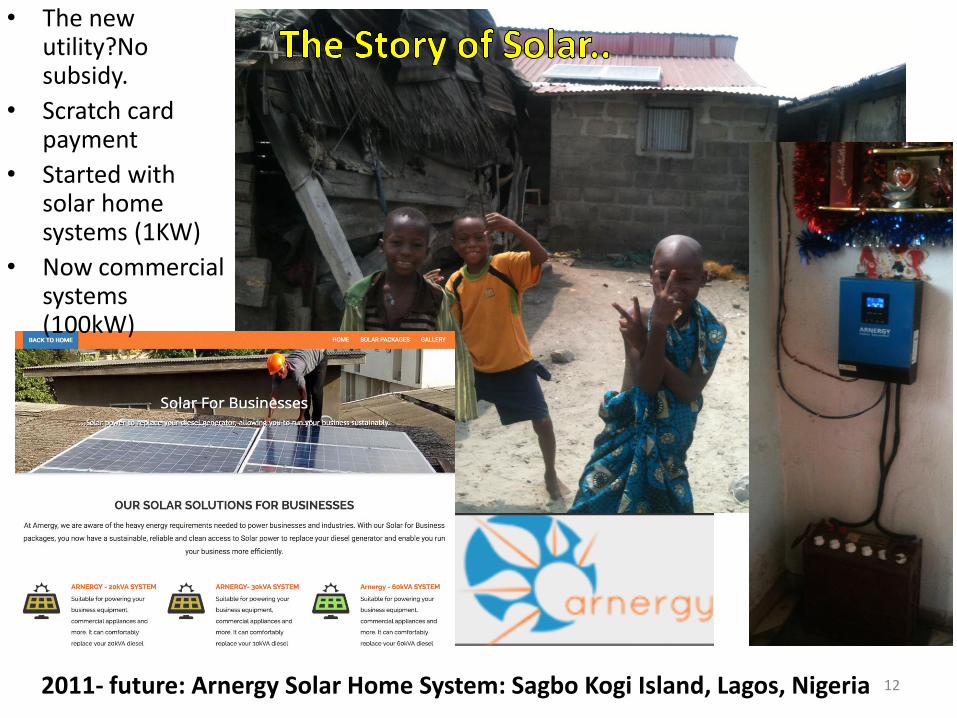

2011- future: Arnergy Solar Home System: Sagbo Kogi Island, Lagos, Nigeria

• The new utility?Nosubsidy.

• Scratch card payment

• Started with solar home systems (1KW)

• Now commercial systems (100kW)

12

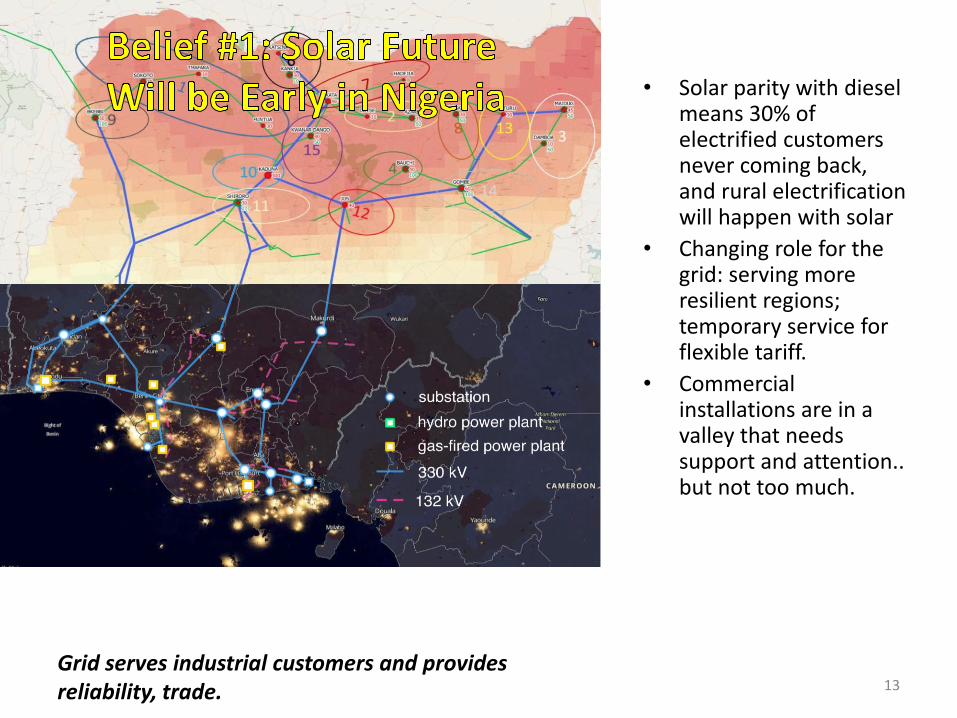

• Solar parity with diesel means 30% of electrified customers never coming back, and rural electrification will happen with solar

• Changing role for the grid: serving more resilient regions; temporary service for flexible tariff.

• Commercial installations are in a valley that needs support and attention.. but not too much.

Grid serves industrial customers and provides reliability, trade. 13

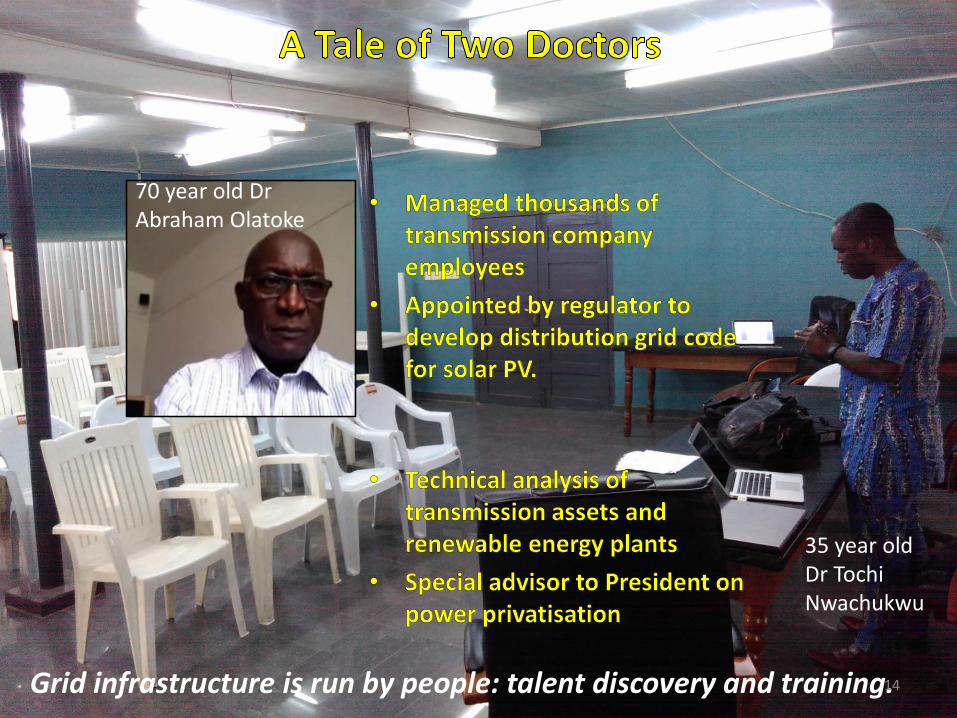

70 year old DrAbraham Olatoke

35 year old Dr TochiNwachukwu

Grid infrastructure is run by people: talent discovery and training.14

Need engineers building skills more than PhDs and consultants

• Summer school with project-driven learning

• Meritocratic selection of participants

• Embedded observers and trainers to enhance

NAPTIN courses

• Well.. maybe a

just a few PhDs

15

Harnessing Energy, Information and Communications Technology for Affordable Electrification of Africa

June 26-30, 2017

Accra,

Ghana

16

Related Documents