2014/2015 School of Business MSc in Global Financial Information Systems (GFIS) Rok Piletic ‘CONTINUOUS ASSESSMENT’ RIPPLE PROTOCOL Module: Global Transaction, Banking and Payment Systems Module Facilitators: Dr. Aidan Duane

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

2014/2015

School of Business

MSc in Global

Financial Information

Systems (GFIS) Rok Piletic

‘CONTINUOUS ASSESSMENT’ RIPPLE PROTOCOL

Module: Global Transaction, Banking and Payment Systems

Module Facilitators: Dr. Aidan Duane

1 | P a g e

STATEMENT OF ORIGINAL AUTHORSHIP

All coursework submitted for assessment must be accompanied by a suitably completed, signed copy of this sheet.

NAME: Rok Piletic

CLASS: Global Transaction, Banking and Payment Systems

STUDENT ID:

TITLE OF ASSIGNMENT:

‘CONTINUOUS ASSESSMENT’ Ripple Protocol

DATE OF SUBMISSION: 8.04.2015

FORMAT: Academic paper - format (19 pages)

I certify that this is my own work and that the use of material from other sources has been properly and fully acknowledged in the text. I understand that the normal consequence of cheating in any element of an examination or assessment, if proven, is that the relevant Faculty Members will be directed to take penalizing action against the student with regards to final marks.

NOTE: You are reminded that you should retain all coursework in your portfolio as it will be required for inspection by Faculty Members at the time of finals.

SIGNED: DATE: Waterford, 08.04.2015

2 | P a g e

CONTENTS

Abstract ................................................................................................................................................................................ 3

1. Introduction .............................................................................................................................................................. 4

2. Literature review .................................................................................................................................................... 5

2.1. Key definitions of virtual currencies - protocols .............................................................................. 7

2.2. Ripple .............................................................................................................................................................. 10

3. Discussion - Comparison of networks and protocols ........................................................................... 14

3.1. SWIFT .............................................................................................................................................................. 14

3.2. BITCOIN.......................................................................................................................................................... 15

3.3. RIPPLE ............................................................................................................................................................ 15

3.4. Benefits and applications of Ripple on Economy .......................................................................... 16

4. Conclusion ............................................................................................................................................................... 17

Bibliography .................................................................................................................................................................... 18

Appendix – Word count table .............................................................................................................................. 19

Figures

Figure 1: XPR network ................................................................................................................................................... 4 Figure 2: Transaction Clearance and Settlement ................................................................................................ 4 Figure 3: Potential impact of innovation domains.............................................................................................. 6 Figure 4: Taxonomy of virtual currencies .............................................................................................................. 8 Figure 5: Relative proportion of national currencies held as reserve currency .................................... 9 Figure 6: Key features and benefits of ripple protocol .................................................................................. 11 Figure 7: Foundation layer of payment system ................................................................................................ 11 Figure 8: Medium of exchange in ripple network ............................................................................................ 12 Figure 9: Security actions of XRP in the network ............................................................................................. 12 Figure 10: Ripple Gateways and Currencies ...................................................................................................... 13 Figure 11: SWIFT network ........................................................................................................................................ 14 Figure 12: Costs of SWIFT network ....................................................................................................................... 14 Figure 13: Bitcoin network transfer ...................................................................................................................... 15 Figure 14: Ripple network ......................................................................................................................................... 15 Figure 15: Summary of different messaging and transaction settlement protocols ........................ 16 Figure 16: How much of digital money is used in today’s society ............................................................. 17

3 | P a g e

Abstract

This Continuous Assessment (CA) is part of module Global Transaction, Banking and Payment Systems (Duane, 2015). The topic chosen for this CA is ‘Ripple protocol’ and its role in developing a banking payment system in regards to other acknowledged systems out there. First there is a literature overview of future of financial systems lead by new guidelines and legislations, as a result of last crisis, environment concern and information communication technology (ICT) influence on finance-banking sector. With explanation of virtual currencies and their terms for better understanding of the Ripple protocol and how it works and who is it made for to use. Second there is discussion on different most used systems (SWIFT, Bitcoin, and Ripple). And third is made a conclusion of the role of Ripple and the systems discussed and overview of literature on financial systems. Key words: Ripple protocol, XRP, transaction network, digital currency, FX.

4 | P a g e

1. Introduction

RIPPLE PROTOCOL

Ripple internet protocol for interbank payments is distributed as open source software and it allows currency exchange and remittance as a payment system. It is a tool for transactions over internet environment. With core cryptocurrency called XPR that enables the FX, Figure 1. Founded in 2012 to power cheapest and fastest payment system enabling transfer of funds (fiat currencies, digital-crypto currencies and other form of value) with tendency to cross international boundaries with easiness as sending e-mails or SMS’s (Ripple, 2015).

FIGURE 1: XPR Network

(Source: Ripple Market Makers (Ripple, 2015))

‘Is Ripple protocol a version of SWIFT 2.0 or better version of Bitcoin cryptocurrency leading a new way of different mobile and web digital-currency system networks.’, as founders of Ripple Labs Inc. claims? This continuous assessment will try to asses’ possibilities this protocol allows to be used by different stakeholder’s trough ICT tools and digital networks. With traditional banking known today or different new features digital-mobile banking is capable of doing with peer-to-peer (p2p) transaction settlements, with decentralized network of computers, see Figure 2. Compared to other protocols and systems that are in the market or used by financial environment, and what that brings to the stakeholders who use this systems daily (governments, businesses, organisations, regulators, people, etc.) for real-time payments and transfer of different currencies (Rapoport, et al., 2014).

FIGURE 2: Transaction Clearance and Settlement

(Source: The Ripple protocol: A deep dive for Finance Professionals (2014) )

5 | P a g e

2. Literature review

What roles do financial information systems hold in the world. Today’s reports on financial system show they should be able to adapt to the systems of tomorrow. Research made by NEF1 for UNEP2 identified five trends, relevant to designing of a ‘Green and inclusive financial system’. For each of these trends there are innovative business models, policies and risk factors (NEF, 2014):

Disintermediation of capital and payments New forms of credit creation Long-term environmental and social impacts Technological innovation Innovations in economics and financial policy

Disintermediation of capital and payments

ICT technology has removed some traditional intermediaries from financial transactions. The biggest innovation is digital currencies with peer-to-peer payments (P2P) and decentralised ledgers (crypto-currencies) in capital sector - crowdfunding and P2P lending. The model of lending switched from few individuals with lots of assets, to a large number of individuals with small amount of capital. Decentralisation of capital control is a big change to the economy and its conduct, as crowds have greater disposal of information of economy, social and environmental transparency. Technology could be used for any other purposes.

New forms of credit creation

Today’s monetary systems are stuck on transferable liabilities (IOUs3). This money supply issued by commercial banks in form of deposits on residual of central banks IOUs. A promise to pay could be done also by non-bank or non-state body functioning as money, if all parties involved agree to take this settlement as payment4. Bitcoin-Ripple are a new technologies of payments (transferring existing purchasing power) and crypto-currency (additional purchasing power), this are two distinct activities (credit creation and payment/capital intermediation). How and with what interest credits are created matters in economy. Crypto-currencies pledges creation of credit for particular purposes.

Long-term environmental and social impacts

Factors savings schemes (pension/insurance industry) are consequently influenced by economic trends (productivity, real-wages, demographic change, debt,…). Restrictions in nature can drive changes in relative prices that impact the economy, same as the climate change.

Technological innovation

Is a driving force of change in any area. Financial sector started with transactions documentation and processes with delivery of new services and corporate models. Latest are increases of dimensions and diversity of data (big data), and linking of everyday devices ICT’s5 to the system networks.

1 New Economics Foundation. 2 United Nations Environment programme. 3 IOUs is in principle what our fiat money is: "I Owe U" - in other words, debt (Anu, 2014). 4 ‘Common tender’ is voluntary, ‘Legal tender’ is imposed by the state. 5 Internet communications technology (PC, Tablet PC, Smart phone, smart watch,...).

6 | P a g e

Innovations in economics and financial policy

Latest economic crisis inclined changes to fundamental economic theories and policy instruments imperative to macroeconomics and financial sector. There were six areas that contribute to the new design of financial system: capital flow management, green credit guidance, strategic quantitative easing, full reserve banking, financial transactions tax (FTT) and the evolution of a global reserve currency.

The six potential trends reviewed here are only a subset of the many instruments that are available to national and international policymakers. They are the latest broader trends in financial system developments of regulations and policies driven by different factors on the financial sector see Figure 3, and how are they influenced by ICT driven innovation (NEF, 2014). FIGURE 3: Potential impact of innovation domains

(Source: www.unep.org (NEF, 2014) )

7 | P a g e

2.1. KEY DEFINITIONS OF VIRTUAL CURRENCIES - PROTOCOLS

There is a lack of common vocabulary of virtual currencies that best describes this sector and be understood by all involved in it (government officials, law enforcements and private sector entities) and ones who develop conceptual of virtual currency operations, there is big risk of AML/CFY6 as found in report of FATF (2014). NPPS Guidance of 2013 did not define ‘digital currency’, ’virtual currency’, ’electronic money’ or it did not distinct internet-based payment systems (e.g., Pay-Pal, Alipay,…) that enable transactions from denominated, real money from digital and not addressing decentralised convertible virtual currencies, by FAFT report (2014):

a) Virtual currency

Is a digital representation 7 of value that could be digitally traded and function as ‘medium of exchange’, ‘unit of account’, and ‘store of value’ with no legal tender status in any jurisdiction (only agreement between members of the user-community and developers of the currency). It is not fiat currency (’real-money’; ‘national-currency’) as coins and papers of a country designated as its legal tender. It is not e-money - this is fiat currency in digital form.

Digital currency can be digital presentation of either virtual currency (non-fiat) or e-money (fiat).

b) Convertible versus non-convertible virtual currency

There are two basic types, convertible (open) or non-convertible (closed) and it does not suggest the ‘ex officio convertibility’ to gold (in case of gold standard), but as an ‘de facto convertibility’ in the existing market not determined by the law.

Convertible - has an equivalent value in real currency and can be back-and-fort exchanged.

Non-convertible – is restricted to basics of certain virtual world or domain. Like online role playing games by the rules leading its use, and cannot be converted to real money. There could emerge a black market where you could exchange non-convertible currencies to any other currencies.

c) Centralised versus non-centralised virtual currencies

Convertible currencies may be centralised or non-centralised as non-convertible are always centralised by definition (issued by central authority that also inflicts the rules).

Centralised virtual currencies - are managed by authority that issues the currency, sets the rules, maintain central ledger figure, and has the right and power to take it out of circulation. Exchange rate could be floated (determent by market) or pegged (fixed by administrator) or other real-store value (fiat, gold, or basket of currencies).

6 Anti-money laundering/Countering the financing of terrorism. 7 ‘DP’ Something in form of digital data – computerised data that behave in continuous manner or represent information using a continuous function, only functioning if linked digitally via internet to virtual currency system network.

8 | P a g e

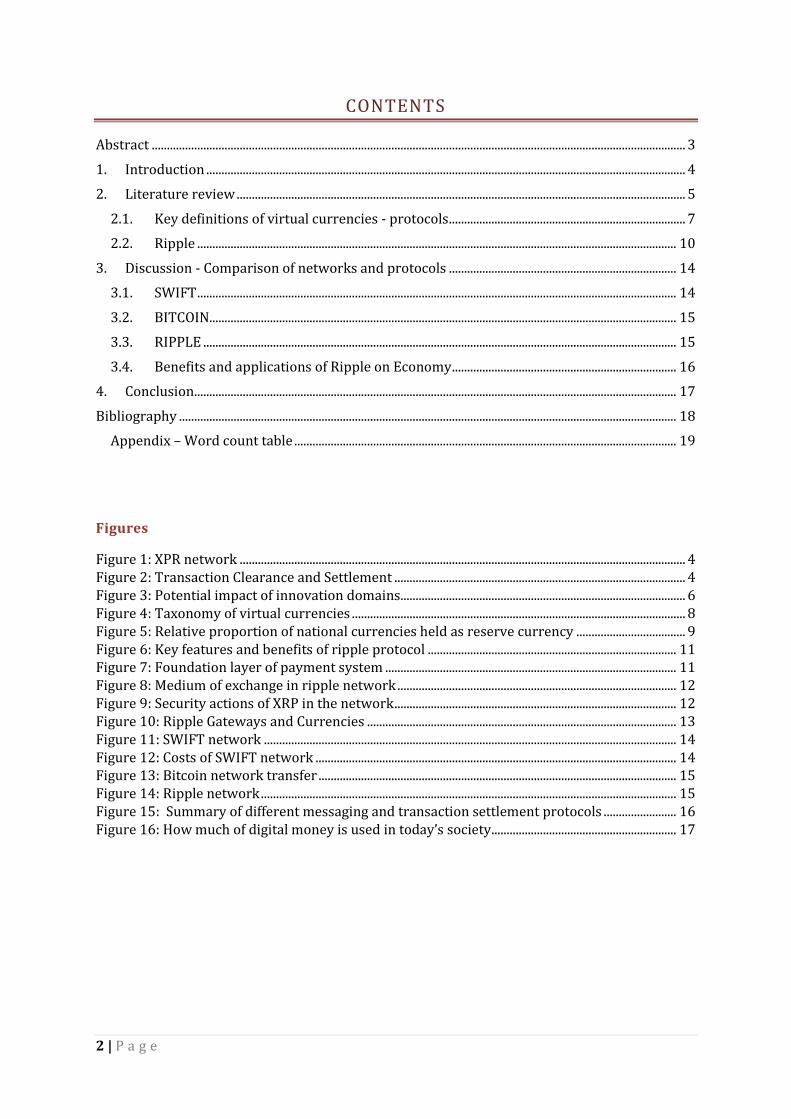

Decentralised virtual currencies (a.k.a. crypto-currencies) - are distributed8, open-source, math-based peer-to-peer (P2P) virtual currencies with no central administration and no central monitoring oversight.

Crypto-currency – decentralised convertible virtual currency using protection

of cryptography. Works on public-private key transferring value from person to person. Bitcoin uses proof-of-work system to authenticate transactions and endure a block-chain. This is now broadly used by many other crypto-currencies; still new development of better method system based on proof-of-stake is being built.

Anonymizer (anonymising tool) - designed to murk the source of a Bitcoin transactions.

Mixer (laundry service, tumbler) - anonymizer that obscures the chain of transactions. Transactions from the same address send together looking like they were sent from another address.

Tor (originally, The Onion Router) - distributed network of computers on the Internet that covers the IP addresses of user.

Dark Wallet - browser-based extension wallet, safeguard for the anonymity of Bitcoin transactions.

Cold Storage - offline wallet not connected to internet, to protect the currency from hacking or theft.

Hot Storage – online wallet, more exposed to theft and hacking. Local Exchange Trading System (LETS) - locally organised economic

organisation in which members exchange goods and services with others. Any crypto currency could be adopted for LETS.

FIGURE 4: Taxonomy of virtual currencies

(Source: www.fatf-gafi.org (FATF, 2014) )

8 Each transaction is distributed among a network of participants who run the algorithm to validate the transaction.

9 | P a g e

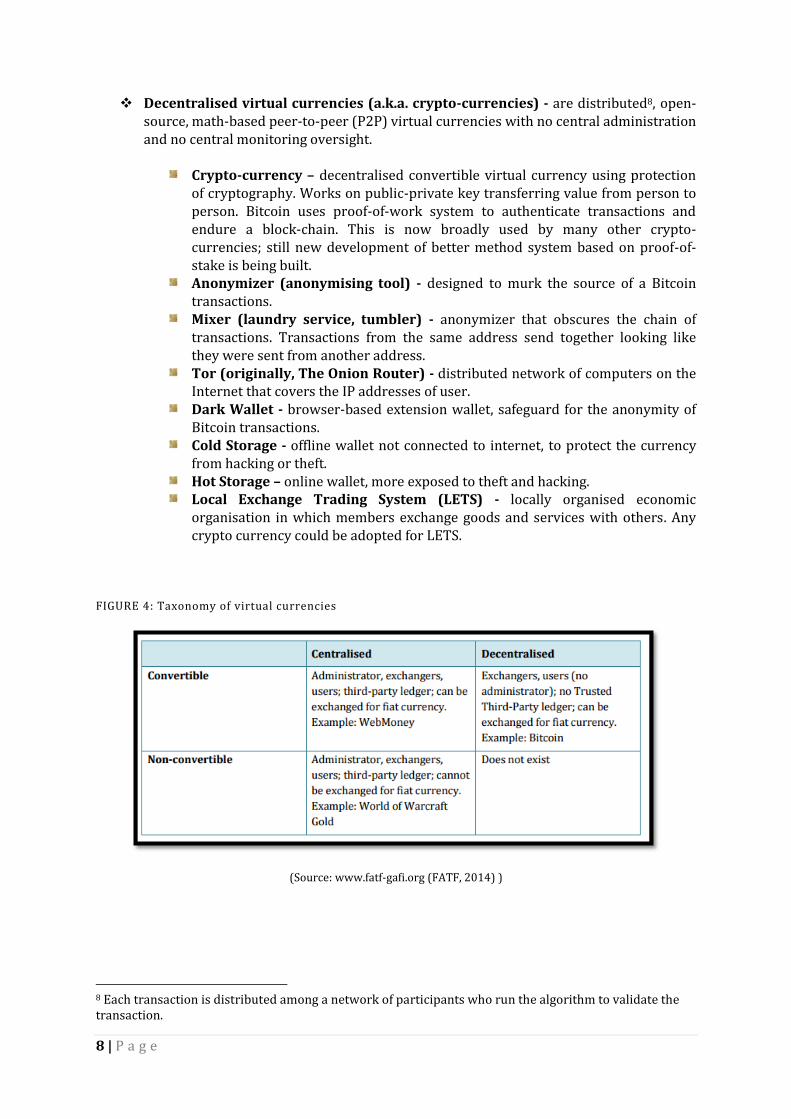

Development of virtual currency technologies and business models bring new terms and threats that pose potential AML/CFT risks also to current world currencies see Figure 5. FIGURE 5: Relative proportion of national currencies held as reserve currency

(Source: www.fatf-gafi.org (FATF, 2014) )

Digital technology is supporting new business models of payments, transfer of value-capital and connecting savers with borrowers of funds. Traditional financial organisations are losing parts of market positions to new companies who are not part of current financial regulatory system. Usually transactions were made by financial institution (exchange an asset for payment or transfer money from A to B) or a bank (credit assessment, aggregation, maturity transformation, and absorbing losses on loans) both intermediations are now being replaced by different systems, organisations and concepts (FATF, 2014):

Transactions (intermediation) Decentralised P2P payment systems Mobile payment systems

Capital (intermediation)

Non-banks providing banking services Crowdfunding and P2P lending

10 | P a g e

2.2. RIPPLE

When looking at Ripple we have to distinguish two main characteristics Ripple Protocol and Ripple Currency (XRP).

2.2.1. RIPPLE KEY CHARACTERISTICS

Ripple protocol

Is decentralised P2P payment system, focusing on clearing transactions with no transaction fees and delays sending money globally in any currency (Bitcoin - store value network). It was developed and maintained by Ripple Labs Inc., that its role is similar of the Red Hat for Linux, but the code itself is an open source for anyone to use freely. First implemented by Ryan Fugger in 2004, developed till 2011, finally being released as open source in 2013. The purpose is to eliminate centralised exchange, usage of less electricity and faster transactions than Bitcoin. It is compared to digital version of Hawala network 9 (non-digital) way of sending money. Both networks have to build up a trust and strong honour system (FATF, 2014). Founder’s idea was to make it advanced LETS 10 with support of arbitrary scalability (Koch, 2014). Ripple, see Figure 6, is a system for value transfer that enables users to exchange money (fiat currencies, digital currencies,…) and items of value (gold,…) globally by easy off sending an email. Core network is run on ‘rippled system’ and users are connected on it by ripple protocol rules that govern communication of computers with each other (like other internet protocols: SMTP–email and HTTP–websites). ‘Ripple Labs does not operate the network, collect fees, or limit access (Rapoport, et al., 2014)’. Two critical functions of protocol (Zagone & Sculley, 2015):

Real-time funds-exchange transaction, clearing and settlement payment system – transferring any currency or item of value with best exchange rate from marketplace, see Figure 7. It gives banks and other payment mainframes to continue their customer experience (determining price, purchases,..) by building gateways to the system and allowing funds enter and exit from the system. Customers don’t need to know how the protocol works (like: ACH11 or SWIFT12), they just use the service.

Shared, Common ledger to connect banks and payment networks – in digital world payments are just updates of the database moving funds, between different accounts. Each institution usually has its own ledger system, so communication between different organisations could be difficult. The ledger connects different networks globally on which developers can build their own payment applications (gateways). Allowing (24/7/365) connection between financial organisations, with real-time clearing (3-6 seconds), netting and monitoring.

9 Is alternative or parallel remittance system (with communications between members of network called dealers), which works outside of traditional banking or financial channels, started in India. Other examples: ‘chop’, ’chit’, ’flying money’ known in China (Jost & Sandhu, 2006). 10 Local Exchange Trading Systems. 11 Automated Clearing House. 12 Society for Worldwide Interbank Financial Telecommunication.

11 | P a g e

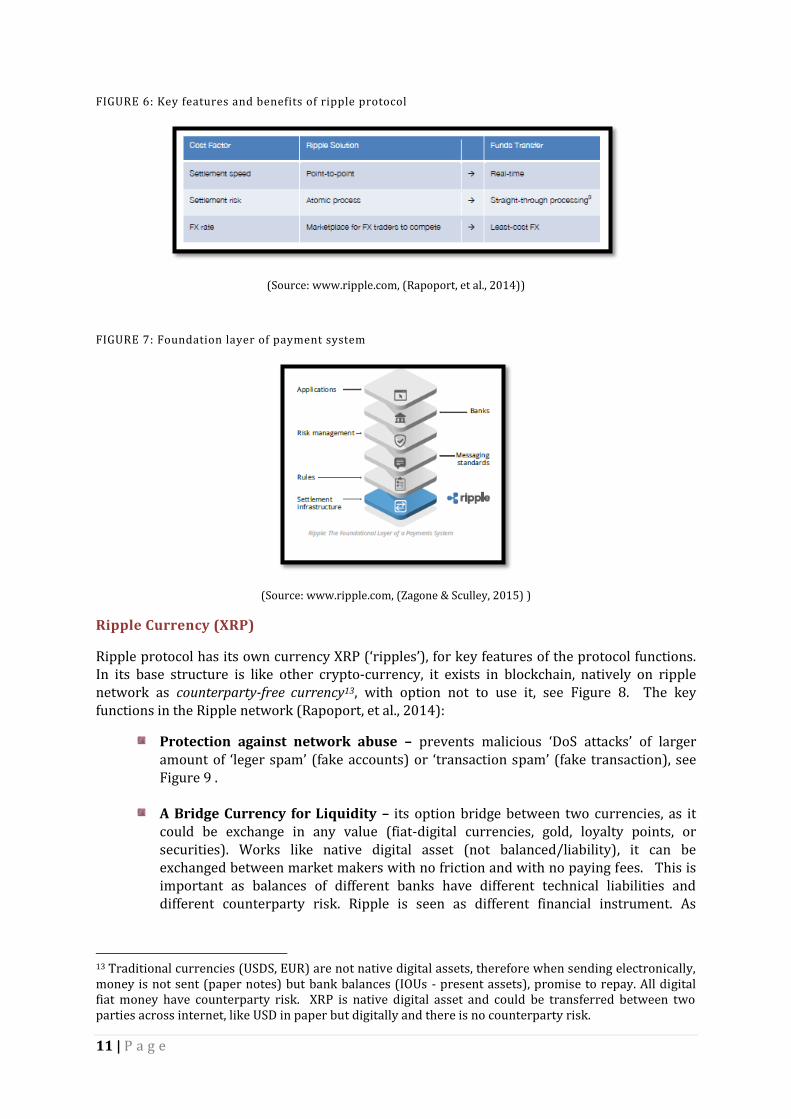

FIGURE 6: Key features and benefits of ripple protocol

(Source: www.ripple.com, (Rapoport, et al., 2014))

FIGURE 7: Foundation layer of payment system

(Source: www.ripple.com, (Zagone & Sculley, 2015) )

Ripple Currency (XRP)

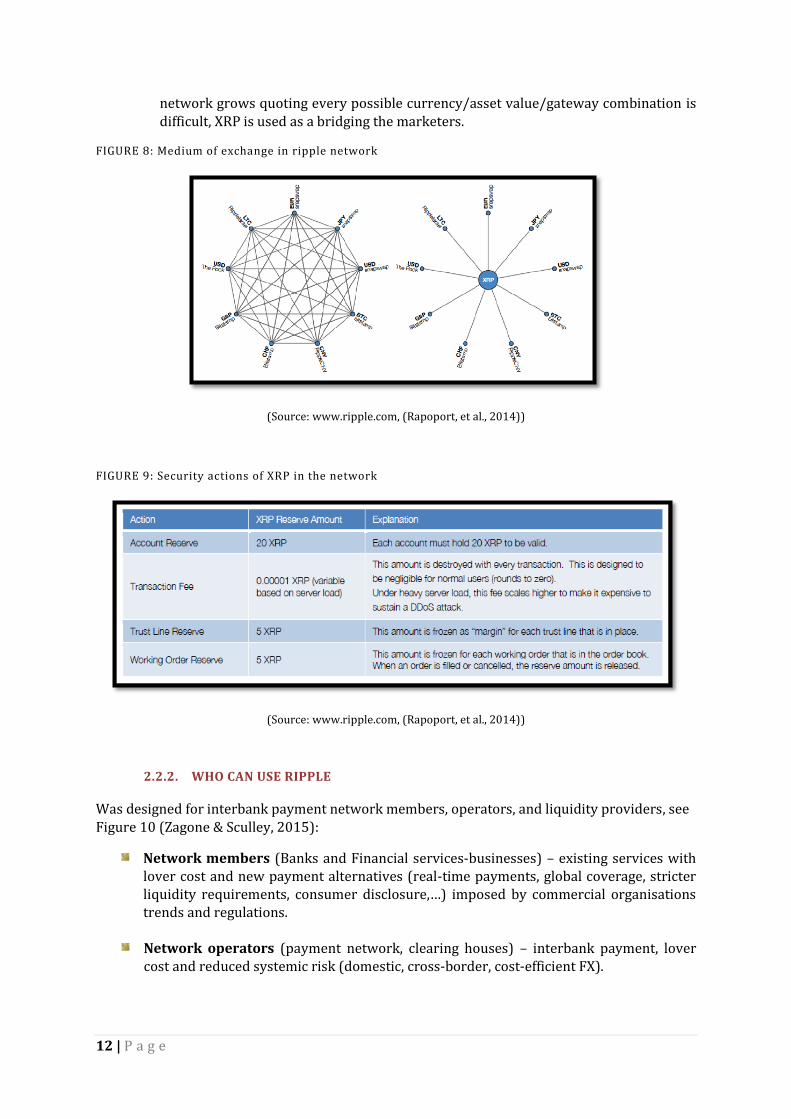

Ripple protocol has its own currency XRP (‘ripples’), for key features of the protocol functions. In its base structure is like other crypto-currency, it exists in blockchain, natively on ripple network as counterparty-free currency13, with option not to use it, see Figure 8. The key functions in the Ripple network (Rapoport, et al., 2014):

Protection against network abuse – prevents malicious ‘DoS attacks’ of larger amount of ‘leger spam’ (fake accounts) or ‘transaction spam’ (fake transaction), see Figure 9 .

A Bridge Currency for Liquidity – its option bridge between two currencies, as it could be exchange in any value (fiat-digital currencies, gold, loyalty points, or securities). Works like native digital asset (not balanced/liability), it can be exchanged between market makers with no friction and with no paying fees. This is important as balances of different banks have different technical liabilities and different counterparty risk. Ripple is seen as different financial instrument. As

13 Traditional currencies (USDS, EUR) are not native digital assets, therefore when sending electronically, money is not sent (paper notes) but bank balances (IOUs - present assets), promise to repay. All digital fiat money have counterparty risk. XRP is native digital asset and could be transferred between two parties across internet, like USD in paper but digitally and there is no counterparty risk.

12 | P a g e

network grows quoting every possible currency/asset value/gateway combination is difficult, XRP is used as a bridging the marketers.

FIGURE 8: Medium of exchange in ripple network

(Source: www.ripple.com, (Rapoport, et al., 2014))

FIGURE 9: Security actions of XRP in the network

(Source: www.ripple.com, (Rapoport, et al., 2014))

2.2.2. WHO CAN USE RIPPLE

Was designed for interbank payment network members, operators, and liquidity providers, see Figure 10 (Zagone & Sculley, 2015):

Network members (Banks and Financial services-businesses) – existing services with lover cost and new payment alternatives (real-time payments, global coverage, stricter liquidity requirements, consumer disclosure,…) imposed by commercial organisations trends and regulations.

Network operators (payment network, clearing houses) – interbank payment, lover cost and reduced systemic risk (domestic, cross-border, cost-efficient FX).

13 | P a g e

Liquidity providers (Central banks, banks, non-bank market-makers) – fund settlements for transactions: same-currency (real-time bilateral exchange) or cross-currency (additional payment volume and markets – retail, commercial, institutional payment…) with range of FX.

FIGURE 10: Ripple Gateways and Currencies

(Source: www.fatf-gafi.org (FATF, 2014) )

14 | P a g e

3. Discussion - Comparison of networks and protocols

How does Ripple protocol work relating with other two big networks on the market Swift and Bitcoin. By words of Chris Larsen (2014), CEO of Ripple Labs Inc. describes Ripple protocol as ‘SWIFT 2.0’ of international payment system. Further there are stated differences between these protocols, see Figure 15 for summary.

3.1. SWIFT

Society for Worldwide Interbank Financial Telecommunication (SWIFT) is a network that provides information of financial transactions across globe in secure and stable environment. It sends messages and does not provide fund settlement. Financial organisations in network still use patchwork of regional rails to do settlements with lots of intermediates see Figure 11 that costs (transaction, exchange, management cost of banks) a lot of money and time, see Figure 12 as there is no direct link from US to EU. There is third-party agreement between sender, receiver and clearing agent seen as double spending problem (Rapoport, et al., 2014).

FIGURE 11: SWIFT network

(Source: www.ripple.com, (Rapoport, et al., 2014))

FIGURE 12: Costs of SWIFT network

(Source: www.ripple.com, (Rapoport, et al., 2014))

15 | P a g e

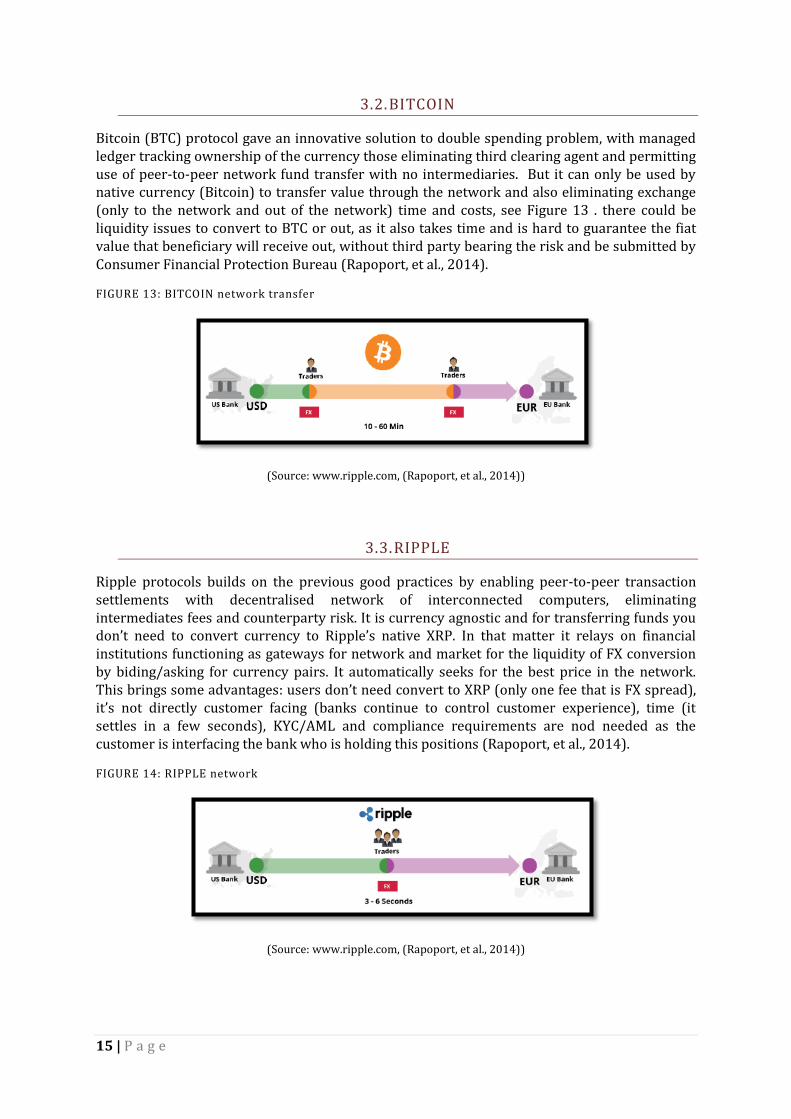

3.2. BITCOIN

Bitcoin (BTC) protocol gave an innovative solution to double spending problem, with managed ledger tracking ownership of the currency those eliminating third clearing agent and permitting use of peer-to-peer network fund transfer with no intermediaries. But it can only be used by native currency (Bitcoin) to transfer value through the network and also eliminating exchange (only to the network and out of the network) time and costs, see Figure 13 . there could be liquidity issues to convert to BTC or out, as it also takes time and is hard to guarantee the fiat value that beneficiary will receive out, without third party bearing the risk and be submitted by Consumer Financial Protection Bureau (Rapoport, et al., 2014).

FIGURE 13: BITCOIN network transfer

(Source: www.ripple.com, (Rapoport, et al., 2014))

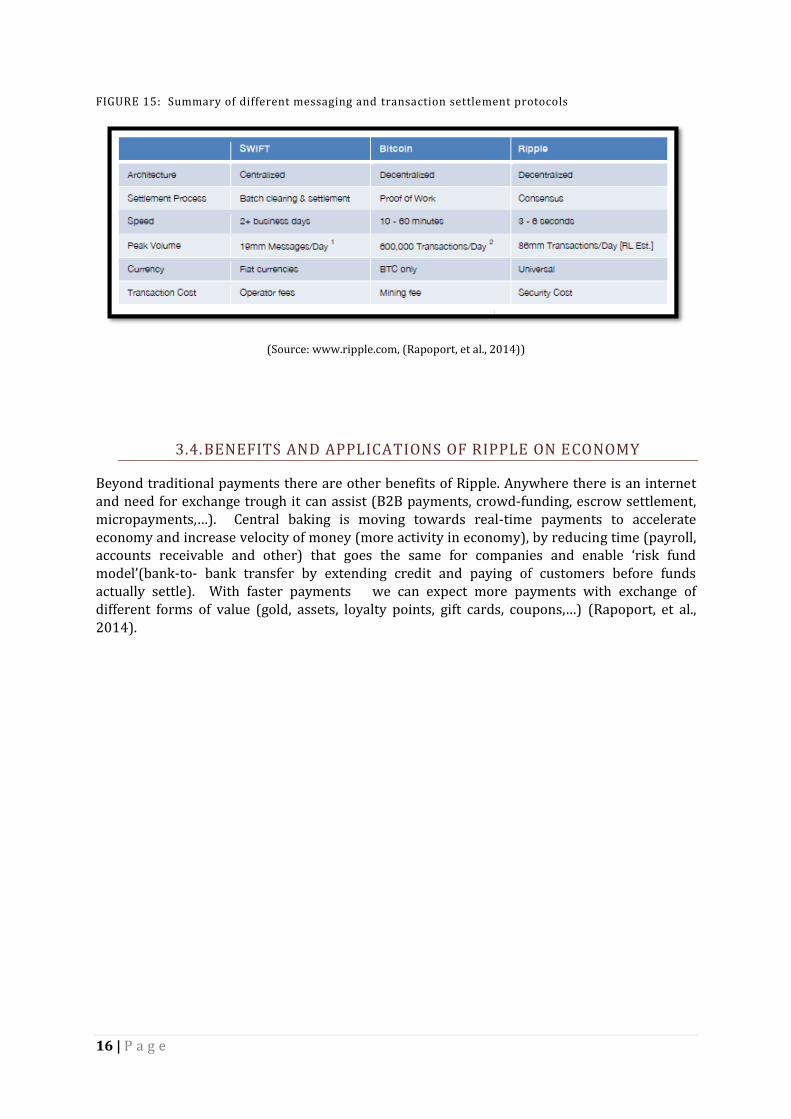

3.3. RIPPLE

Ripple protocols builds on the previous good practices by enabling peer-to-peer transaction settlements with decentralised network of interconnected computers, eliminating intermediates fees and counterparty risk. It is currency agnostic and for transferring funds you don’t need to convert currency to Ripple’s native XRP. In that matter it relays on financial institutions functioning as gateways for network and market for the liquidity of FX conversion by biding/asking for currency pairs. It automatically seeks for the best price in the network. This brings some advantages: users don’t need convert to XRP (only one fee that is FX spread), it’s not directly customer facing (banks continue to control customer experience), time (it settles in a few seconds), KYC/AML and compliance requirements are nod needed as the customer is interfacing the bank who is holding this positions (Rapoport, et al., 2014).

FIGURE 14: RIPPLE network

(Source: www.ripple.com, (Rapoport, et al., 2014))

16 | P a g e

FIGURE 15: Summary of different messaging and transaction settlement protocols

(Source: www.ripple.com, (Rapoport, et al., 2014))

3.4. BENEFITS AND APPLICATIONS OF RIPPLE ON ECONOMY

Beyond traditional payments there are other benefits of Ripple. Anywhere there is an internet and need for exchange trough it can assist (B2B payments, crowd-funding, escrow settlement, micropayments,…). Central baking is moving towards real-time payments to accelerate economy and increase velocity of money (more activity in economy), by reducing time (payroll, accounts receivable and other) that goes the same for companies and enable ‘risk fund model’(bank-to- bank transfer by extending credit and paying of customers before funds actually settle). With faster payments we can expect more payments with exchange of different forms of value (gold, assets, loyalty points, gift cards, coupons,…) (Rapoport, et al., 2014).

17 | P a g e

4. CONCLUSION

Today’s financial sector is changing because of the new technology and the way the economies are connected. Ripple protocol is the latest invention – solution to the problems of globalised economies and digitalisation of financial-banking sector. By research done in the financial systems trends (Disintermediation of capital and payments, New forms of credit creation, Long-term environmental and social impacts, Technological innovation, Innovations in economics and financial policy ) and network systems (SWIFT, Bitcoin), Ripple protocol contains main trends that are relevant for designing of a Green and inclusive financial system that was lead in the research of NEF (2014) on Working paper for the United Nations Environment Programme inquiry. It also possesses the key definitions of Virtual currency (Convertible versus non-convertible virtual currency, Centralised versus non-centralised virtual currencies) that are important to dismiss big risks of AML/CFY (FATF, 2014). Ripple is also helping traditional financial institutions to not be replaced by different systems, organisations and concepts in Capital (intermediation) and Transactions (intermediation) it helps them building gateways to Ripple network. By this the customers and merchants get the best benefit of both world’s old and new coming and good influences on the economy.

Will digitalisation of money take place; see Figure 16, as the technology is here. This answer should be answered before financial sector can say there is a future for Ripple protocol. But at the same time could be concluded that Ripple could survive as it is a better version of SWIFT and Bitcoin network, and it could be used by traditional financial organisations for advanced experience of the current service industry is providing to customers and merchants. The only risk in future there could be are security issues in regards of broader use and interest of the criminals to break in the system, even now the system has a good security measures taken, but with new ICT innovations new problems could emerge. The team behind Ripple Labs Inc. have the goals set in right direction and only time will tell if they were right.

FIGURE 16: How much of digital money is used in today’s society

(Source: www.jwtintelligence.com, (Ayala, 2014) )

18 | P a g e

BIBLIOGRAPHY

Anu, 2014. Zero Reserve. [Online] Available at: https://github.com/zeroreserve/ZeroReserve/wiki [Accessed 15 March 2015].

Ayala, N., 2014. The Future of Paymnets & Currency. [Online] Available at: https://www.jwtintelligence.com/wp-content/uploads/2014/10/F_JWT_The-Future-of-Payments-and-Currency_10.22.14.pdf [Accessed 31 March 2015].

Bradbury, D., 2014. Ripple Courts Developers, Entrepreneurs With New Initiatives. [Online] Available at: http://www.coindesk.com/ripple-courts-developers-entrepreneurs-new-initiatives/ [Accessed 31 March 2015].

Chêne, M., 2008. Hawala remittance system and money laundering. [Online] Available at: file:///C:/Users/20065563/Downloads/expert-helpdesk-170.pdf [Accessed 31 March 2015].

Duane, A., 2015. Continuous Assessment - Guide., Waterford: WIT.

FATF, 2014. Virtual Currencies - Key Definitions and Potential AML/CFT Risks. [Online] Available at: http://www.fatf-gafi.org/media/fatf/documents/reports/virtual-currency-key-definitions-and-potential-aml-cft-risks.pdf [Accessed 30 March 2015].

Jost, P. M. & Sandhu, H. S., 2006. The Hawala Alternative Remittance System and its Role in Money Laundering. [Online] Available at: http://www.treasury.gov/resource-center/terrorist-illicit-finance/Documents/FinCEN-Hawala-rpt.pdf [Accessed 31 March 2015].

Koch, R., 2014. Zero Reserve – A Distributed Exchange Platform. [Online] Available at: file:///C:/Users/20065563/Downloads/zeroreserve.pdf [Accessed 31 March 2015].

NEF, 2014. Financial system impact of disruptive innovation - Working paper for the United Nations Environment Programme inquiry. [Online] Available at: http://www.unep.org/inquiry/Portals/50215/Documents/Disruptive%20Innovation_Inquiry%20Working%20Paper_%20NEF.PDF [Accessed 30 March 2015].

Rapoport, P., Leal, R., Griffin, P. & Sculley, W., 2014. Ripple.com. [Online] Available at: https://ripple.com/files/ripple_deep_dive_for_financial_professionals.pdf [Accessed 4 February 2015].

Rapoport, P., Leal, R., Griffin, P. & Sculley, W., 2014. The Ripple Protocol: A Deep Dive for Finance Professionals. [Online] Available at: https://ripple.com/ripple-deep-dive/ [Accessed 31 March 2015].

19 | P a g e

Ripple Labs Inc., 2014. The Ripple Protocol Primer. [Online] Available at: https://ripple.com/files/ripple_primer.pdf [Accessed 31 March 2015].

Ripple, 2015. Ripple.com. [Online] Available at: https://ripple.com/files/ripple_mm.pdf [Accessed 4 February 2015].

Wheatley, J., 2005. Ancient Banking, Modern Crimes: How HAWALA Secretly Transfers the Finances of Criminals and Thwarts Existing Laws. [Online] Available at: https://www.law.upenn.edu/journals/jil/articles/volume26/issue2/Wheatley26U.Pa.J.Int%27lEcon.L.347%282005%29.pdf [Accessed 31 March 2015].

White, A., 2014. Ripple Investment Guide Version 1.4. [Online] Available at: http://rippleinvestmentguide.com/wp-content/uploads/2014/03/Ripple-Guide.pdf [Accessed 31 March 2015].

Zagone, R. & Sculley, W., 2015. Executive Summary for Financial Institutions. [Online] Available at: https://ripple.com/integrate/executive-summary-for-financial-institutions/ [Accessed 31 March 2015].

APPENDIX – Word count table

HEADINGS WORDS (maximum)

Abstract 149 (200)

Introduction 243 (500)

Literature review

1998 (2000)

Discussion

591 355

------------------------ 946 (750-1000)

Conclusion

TOTAL 3336 (3700)

Related Documents