BANKING OPERATION AND INNOVATION CHAPTER 1 (A) RELATIONSHIP BETWEEN BANKER AND CUSTOMER Introduction: Introduction to Banking Finance is the life blood of trade, commerce and industry. Now-a-days, banking sector acts as the backbone of modern business. Development of any country mainly depends upon the banking system. The term bank is either derived from old Italian word banca or from a French word banque both mean a Bench or money exchange table. In olden days, European money lenders or money changers used to display (show) coins of different countries in big heaps (quantity) on benches or tables for the purpose of lending or exchanging. People earn money to meet their day to day expenses on food, clothing, education of children, having etc. They also need money to meet future expenses on marriage, higher education of children, and housing, building and social functions. These are heavy expenses, which can be met if some money is saved out of the present income. With this practice, savings were available for use whenever needed, but it also involved the risk of loss by theft, robbery and other accidents. Thus, people were in need of a place where money could be saved safely and would be available when required. Banks are such places where people can deposit their savings with the assurance that they will be able to with draw money from the deposits whenever required. Bank is a lawful organization which accepts deposits that can be withdrawn on demand. It also tends money to individuals and business houses that need it. Bank Meaning : A bank is a financial institution which deals with deposits and advances and other related services. It receives money from those who want to save in the form of deposits and it lends money to those who need it. A bank is a financial institution and a financial intermediary that accepts deposits and channels those deposits into lending activities, either directly by loaning or indirectly through capital markets. A bank is the connection between customers that have capital deficits and customers with capital surpluses. Definitions: 1) F.E. Perry: ―The bank is an establishment which deals in money, receiving it on deposit from customers, honoring customer‘s drawings against such deposits on demand, collecting cheques for customs and lending or investing surplus deposits until they are required for repayment. 2) Walter Leaf: ―A banker is an institution or individual who is always ready to receive money on deposits to be returned against the cheques of their depositors. Features of Bank 1. Dealing in Money Bank is a financial institution which deals with other people's money i.e. money given by depositors. 2. Individual / Firm / Company A bank may be a person, firm or a company. A banking company means a company which is in the business of banking.

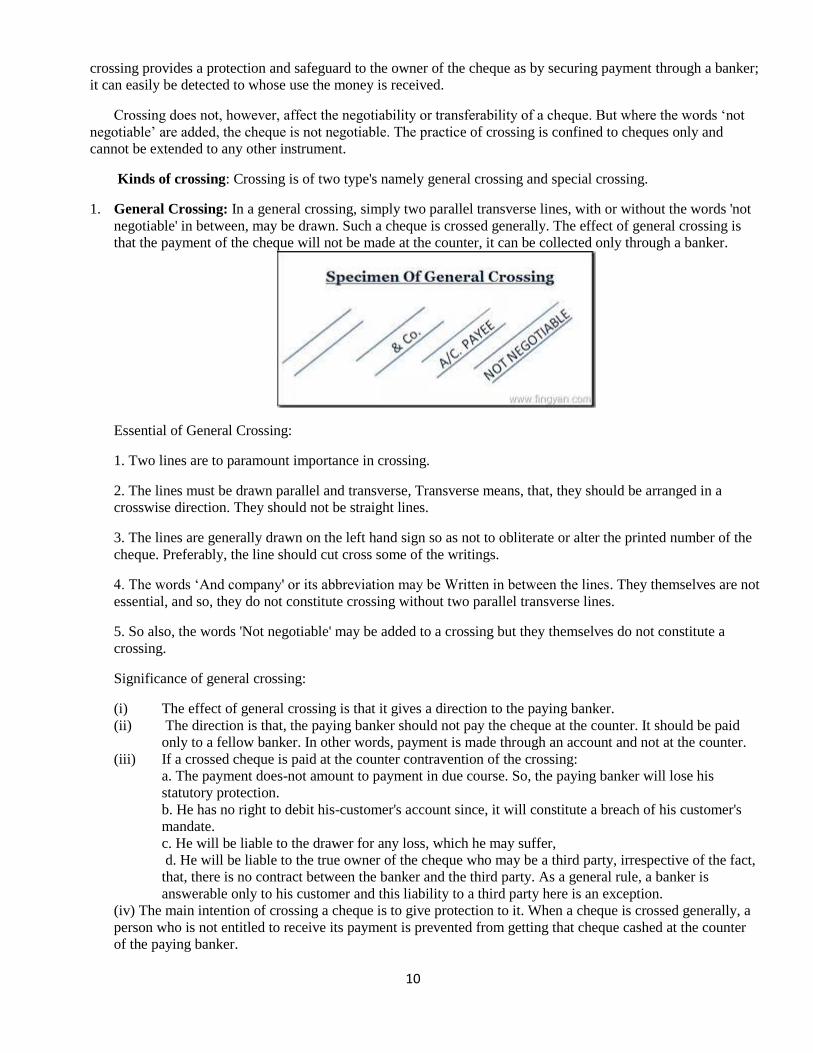

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

BANKING OPERATION AND INNOVATION

CHAPTER 1 (A) RELATIONSHIP BETWEEN BANKER AND CUSTOMER

Introduction:

Introduction to Banking Finance is the life blood of trade, commerce and industry. Now-a-days, banking

sector acts as the backbone of modern business. Development of any country mainly depends upon the

banking system. The term bank is either derived from old Italian word banca or from a French word

banque both mean a Bench or money exchange table. In olden days, European money lenders or money

changers used to display (show) coins of different countries in big heaps (quantity) on benches or tables

for the purpose of lending or exchanging. People earn money to meet their day to day expenses on food,

clothing, education of children, having etc. They also need money to meet future expenses on marriage,

higher education of children, and housing, building and social functions. These are heavy expenses,

which can be met if some money is saved out of the present income. With this practice, savings were

available for use whenever needed, but it also involved the risk of loss by theft, robbery and other

accidents. Thus, people were in need of a place where money could be saved safely and would be

available when required. Banks are such places where people can deposit their savings with the

assurance that they will be able to with draw money from the deposits whenever required. Bank is a

lawful organization which accepts deposits that can be withdrawn on demand. It also tends money to

individuals and business houses that need it.

Bank Meaning : A bank is a financial institution which deals with deposits and advances and other

related services. It receives money from those who want to save in the form of deposits and it lends

money to those who need it. A bank is a financial institution and a financial intermediary that accepts

deposits and channels those deposits into lending activities, either directly by loaning or indirectly

through capital markets. A bank is the connection between customers that have capital deficits and

customers with capital surpluses.

Definitions:

1) F.E. Perry: ―The bank is an establishment which deals in money, receiving it on deposit from

customers, honoring customer‘s drawings against such deposits on demand, collecting cheques for

customs and lending or investing surplus deposits until they are required for repayment.

2) Walter Leaf: ―A banker is an institution or individual who is always ready to receive money on

deposits to be returned against the cheques of their depositors.

Features of Bank

1. Dealing in Money Bank is a financial institution which deals with other people's money i.e. money

given by depositors.

2. Individual / Firm / Company A bank may be a person, firm or a company. A banking company

means a company which is in the business of banking.

3. Acceptance of Deposit A bank accepts money from the people in the form of deposits which are

usually repayable on demand or after the expiry of a fixed period. It gives safety to the deposits of its

customers. It also acts as a custodian of funds of its customers.

4. Giving Advances A bank lends out money in the form of loans to those who require it for different

purposes.

5. Payment and Withdrawal A bank provides easy payment and withdrawal facility to its customers in

the form of cheques and drafts, It also brings bank money in circulation. This money is in the form of

cheques, drafts, etc.

6. Agency and Utility Services A bank provides various banking facilities to its customers. They

include general utility services and agency services.

7. Profit and Service Orientation A bank is a profit seeking institution having service oriented approach.

8. Ever increasing Functions Banking is an evolutionary concept. There is continuous expansion and

diversification as regards the functions, services and activities of a bank.

9. Connecting Link A bank acts as a connecting link between borrowers and lenders of money. Banks

collect money from those who have surplus money and give the same to those who are in need of money

BANKER AND THE CUSTOMER

Banker

Banker is a person doing the banking business is called banker. He must perform following essential

functions such as receiving deposits of various kinds, lending money or creating credit, issuing cheques,

honouring cheques and collecting cheques.

According to Dr.H.C Hart a banker or a bank is a person or company carrying on the business of

receiving money and collecting drafts, for customers subject to the obligation of honoring cheques

drawn upon them from time to time by the customers to the extent of the amounts available in their

current accounts.

Customer

The term "Customer" has not yet been statutorily defined. Generally, the term customer means a person

who has an account with bank. Banking experts and legal judgments in the past, however, used to

qualify this statement by laying emphasis on the period for which such account had actually been

maintained with the bank. Customer is a person who utilizes one or more of the services provided by the

bank. Through customer the bank gets an opportunity to make earnings and banker provides services

A person can become a customer,

(1) If he opens any type of account fixed, current or savings with the bank.

(2) Such account may be frequently operated or not.

(3) The transaction between banker and customer should be of banking nature One cannot be called a

customer if the transaction is of casual nature even of it is continuously done.

DEBOTR AND CREDITOR *BAILEE & BAILOR

*PRINCIPLE & AGENT

*TRUSTEE & BENIFICIARY *HONOUR CUSTOMER *LIE

*CUSTODIAN CHEQUE *

*LESSOR & LESSER *MAINTAINS OF CUSTOMER

SECRECY

Relationship of Debtor and Creditor

When a customer opens an account with a bank and if the account has a credit balance, then the

relationship is that of debtor (banker / bank) and creditor (customer). In case of savings / fixed deposit /

current account (with credit balance), the banker is the debtor, and the customer is the creditor. This is

because the banker owes money to the customer. The customer has the right to demand back his money

whenever he wants it from the banker, and the banker must repay the balance to the customer. In case of

loan / advance accounts, banker is the creditor, and the customer is the debtor because the customer

owes money to the banker. The banker can demand the repayment of loan / advance on the due date, and

the customer has to repay the debt. A customer remains a creditor until there is credit balance in his

account with the banker. A customer (creditor) does not get any charge over the assets of the banker

(debtor). The customer's status is that of an unsecured creditor of the banker.

Relationship of Pledger and Pledgee

The relationship between customer and banker can be that of Pledger and Pledgee. This happens when

customer pledges (promises) certain assets or security with the bank in order to get a loan. In this case,

the customer becomes the Pledger, and the bank becomes the Pledgee. Under this agreement, the assets

or security will remain with the bank until a customer repay the loan

RELATIONSHIP BETWEEN CUSTOMER AND BANKER

GENERAL RELATIONSHIP SPECIAL RELATIONSHIP

PRIMARY RELATIONSHIP SECONDARY RELATIONSHIP

OBLIGATIONS RIGHTS

Relationship of Bailor and Bailee

The relationship between banker and customer can be that of Bailor and Bailee.Bailment is a contract

for delivering goods by one party to another to be held in trust for a specific period and returned when

the purpose is ended. Bailor is the party that delivers property to another. Bailee is the party to whom the

property is delivered. So, when a customer gives a sealed box to the bank for safe keeping, the customer

became the bailor, and the bank became the bailee.

Relationship of Trustee and Beneficiary

A trustee holds property for the beneficiary, and the profit earned from this property belongs to the

beneficiary. If the customer deposits securities or valuables with the banker for safe custody, banker

becomes a trustee of his customer. The customer is the beneficiary so the ownership remains with the

customer.

Relationship of Agent and Principal

The banker acts as an agent of the customer (principal) by providing the following agency services:

Buying and selling securities on his behalf, Collection of cheques, dividends, bills or promissory notes

on his behalf, and Acting as a trustee, attorney, executor, correspondent or representative of a customer.

Banker as an agent performs many other functions such as payment of insurance premium, electricity

and gas bills, handling tax problems, etc.

Relationship of Advisor and Client

When a customer invests in securities, the banker acts as an advisor. The advice can be given officially

or unofficially. While giving advice the banker has to take maximum care and caution. Here, the banker

is an Advisor, and the customer is a Client.

SPECIAL RELATIONSHIP BETWEEN BANKER & CUSTOMER

This is related to the mutual rights and obligation of the customer and banker:

A. Rights of a Banker

1. Banker's right to lien

'Lien' is a term used to identify the right to retain a property belonging to a debtor till such time he

discharges the debt due to the retainer of the property. Lien is simply a right to possess a property. Line

will be lost when the possession of the property is lost. Lien is the right of one person to retain the

property, in his possession, belonging to the other person, until the debt due from the owner of that

property is repaid. In other words, it is the right exercised by the creditor over the property of debtor

until the debt is repaid. The lien may be a particular lien or general lien.

Particular lien: This lien refers, to a particular which is retained by the lender or creditor against the

specific or particular loan. The particular property will be retained until the particular debt is cleared by

the debtor. This lien is enjoyed by people who have sent their labour on such properties and has not yet

recovered their labour charges or service charge from the debtors.

General lien: general lien is enjoyed by banker, mercantile agents (factors), attorneys of High Court and

policy Brokers General lien is a right of the bankers (creditors) to retain an the properties of debtors

(customer's) till the sums due to the bank are recovered. In the absence of any agreement to the contrary,

banker may retain any goods and securities bailed to him as a security for general balance of accounts.

The Indian Contract Act (U/s171) provides, this right and rights is called General lien

2. Right to charge interest, commission, incidental charges, commitment charges.

(i) Interest: The banker has a right to charge interest on customer’s loan account. Normally interest is

calculated at every quarter or half year and debited to the customer’s loan account. The interest on the

first quarter becomes the principal in the next interest charging period and hence interest on interest

(compound interest) is charged. This is a right enjoyed by the banker.

(ii) Commission: the banker has an implied right to charge commission for the service he renders to the

customers.

(iii)Incidental Charges: incidental charges is a levy imposed by the banker on unremunerative current

accounts. Again this is an implied right enjoyed by the banker.

(iv)Commitment charges: this is a charge made by the banker on overdrafts and cash credit accounts.

Besides charging interest on the utilized portion of the overdraft, the commitment charge is charged on

the unutilized portion of the sanctioned limit does not earn any profit to the Banker incorporates

'Commitment Charge Clause' in overdraft and commitment charges agreements.

3. Right to set off: A bankers’ right to set off refers to the right of the banker to adjust the amount due

to him from a customer on one account against the amount due from him to the customer on another

account. It is the right of a banker to combine or adjust the debit and credit balances of two or more

similar accounts held by a customer in the same capacity. The right of set off facilitates the banker to

know the set amount due to him from the customer and ensures the safety of funds.

For instance X has to pay y Rs.10,000 and y has to pay X Rs.4, 000 to X's account, as Y has to a net

balance of Rs 6,000. This adjustment, between the parties is called set- off. The banker, as a debtor has

the right of set- off. This right empowers the banker to the banker to adjust the balance at the credit of

the customer's account towards the amount due to the banker. If a customer holds two accounts in the

same capacity, the account can be adjusted one against one against the other or the accounts can be

combined as per the right of set -off. The right of set-off facilities the banker to know the net amount

due to him from the customer and ensures the safety of funds. When to exercise the right of set-off

(1) By giving a prior notice to the customer

(2) By obtaining a letter of set off from the customer when the customer opens more than one account.

(3) By having the right of automatic set-off under certain circumstances.

The banker gets the right of automatic set off under following circumstances.

(1) On the death of the customer.

(2) On the insolvency of the customer

(3) On the insanity of the customer

(4) On the receipt of a garnishee order attaching the customer’ account. Automatic set off refers to the

right of a banker to adjust the debit and credit balances of two or more accounts held by a customer in

the same name and right or capacity without obtaining any letter of set off from the customer or without

giving him any pervious notice.

Conditions to be satisfied for the exercise of the right of set-off by a banker

(1) The debts must be mutual i.e., must be due between the same parties.

(2) The right of set-off can be exercised only if the mutual debts are determined and certain in amount.

(3) The right of set-off can be exercised if the customer’s account are opened in the same name and

capacity.

(4) The right of set-off can be exercised only in respect of debts which are due and recoverable on the

date of set-off

(5) The right of set-off can be exercised by the banker only in the absence of an agreement to the

contrary.

Right to appropriate Payments: When the customers raises more than one loan account, the question

of appropriation arises. The payments made by the customer may not be sufficient to clear all debts due

by the customer. Similarly, when a customer holds more than one current account and regularly operates

these accounts by depositing funds and making withdrawals simultaneously in all the accounts he holds,

it will be a problem for the banker to appropriate which funds to which account.

Right not to Produce Books of Accounts: The banker need not produce the original books of Accounts

as evidence in the cases in which the banker is not a party. He can issue only the certified copy, of the

required portion of the account. But when a banker is a party to the suit, the court can force the banker to

produce the original records in support of his claim.

Right under Garnishee order:

The term ‘gamishee' is derived from the Latin word ‘gamire’ which means 'to warn’. This order warns

the holders of money of judgments debtor, not to make any payments out of it till the court directs.

Garnishee order is issued by the court at the request of the judgments creditor. A garnishee order is an

order issued by the court, at the instance of judgment creditor to the garnishee first attaching the funds of

the judgment debtor lying with the garnishee and later directing him to pay the same to the judgment

creditor if he does not have any objection to do so. Let us see how a garnishee order can affect the

relationship between the banker and the customer.

Suppose Mr. A is the customer of SBI. He has taken a loan from his friend Mr. B. But Mr. A fails to

repay the loan to Mr. B and as a result Mr. B files a case against Mr. A. Now Mr. B requests the court to

issue an order on the bank of Mr. A directing the banker (SBI) not to make any payment from the

available balance in the account of Mr. A. If the court issues such an order, it is known as ‘Garnishee

Order’. Here, Mr. A (debtor) is known as ‘judgement debtor’, Mr. B (creditor) is known as ‘judgement

creditor’ and the SBI is known as ‘garnishee’. The garnishee order is issued in two phases. First, ‘order

nisi’ is issued directing the garnishee (banker) not to make any payment from the account of the

garnishee debtor. The garnishee is asked to give his reply in the court whether the funds in the account

of the garnishee debtor can be appropriated towards the payment of the particular debt in question. If the

garnishee has no objection then in the second phase the court issues the ‘order absolute’ i.e. the

garnishee order, to make the payment to garnishee creditor to satisfy the debt from the account of the

judgement debtor. Then the banker’s obligation to the customer (garnishee debtor) is discharged to that

extent.

The banker as garnishee has to discharge the following duties on receipt of the garnishee order.

1) He must issue notice to his customer regarding the garnishee order received against his account.

2) The banker should also inform, whether the entire amounts is attached or only a part of it is subjected

to garnishee order.

3) He should advise the customer to open a new account for future operations, as the existing account

cannot be operated because of attachment under garnishee order.

4) Banker has no right to surrender the amount to the court until the ‘order Absolute’ is received.

5) He can ask the customer to raise any objection against the garnishee order.

Conditions to be satisfied for the operation of a garnishee order served on a banker:

The customers’ account must be in credit.

The account should belo0ng to the customer in his own right and should not be held as a trustee

or jointly with another person.

If the garnishee order attaches several accounts held by the customer, then all the accounts must

be held by him in the same right or capacity.

The debt to be attached by a garnishee order must be actually due or accruing due at the time the

order to be served.

The garnishee order must state the name and the address of the customer accurately.

OBLIGATIONS OF A BANKER (DUTIES)

Obligation to honour customer's cheques:

When a current account is opened by a banker in the name if a customer, there is an obligation on the

banker to honour the customer’s cheques as long as there are sufficient funds available in the customer’s

account for meeting the cheques. So whenever the customer demands the repayment of his deposits by

issuing cheques there is a contractual obligation on the banker to honour his customers’ cheques and

repay his deposits. This obligation is provided by stature in section 31 of the Indian Negotiable

Instruments Act of 1881.

Conditions to be satisfied to honour the cheques of the customers:

1. Sufficient funds must be available: The customer should have credit balance in his account which

should be equal to the amount stated in the cheque.

2. Funds must be properly applicable to the payment of the cheque:

(a) The funds available to the credit of the trust account are applicable only for the purposed covered by

the trust.

(b) If the banker has received a notice of the assignment of the customer’s credit balance to a third party

or

(c) If certain funds in the customer’s account are set-aside for some specific purpose. Such funds will

not be available for the payment of the customer’s cheques.

3. Banker must be duly required to pay the cheque: The instrument used for drawing the amount should

be properly written and fulfill all legal obligations. It should be presented within a reasonable time after

its date of issue. In India as per the Banking custom and practice, a cheque must be presented for

payment within 3 months from the date of issue. Otherwise it becomes stale and invalid and such a

cheque need not be honoured If a cheque is not properly drawn then the banker need not honour the

cheque. Similarly if a cheque is presented for payment before the date of payment mentioned in the

cheque (if the cheque is post dated) the banker is not required to pay the cheque. If a cheque is presented

outside business hours the banker is not required to honour the same.

4. There must be no legal ban preventing the payment of cheque: A cheque drawn against an account on

which a garnishee order has been issued by the court need not be honoured by the banker. Similarly if

there is any order issued by the income-tax authorities attaching the customer’s funds in an account,

such a cheque need not be honoured.

5. No obligation to honour cheques drawn against the uncleared cheques or bills: If cheques are drawn

by a customer against uncleared cheques or bills i.e. cheques or bills deposited by the customer for

collection but not yet collected and credited to the customer’s account.

Obligation to maintain secrecy of customers account:

It is a general understanding between the customer and banker that the banker should maintain secrecy

regarding the customer's account. It is believed and the fact is also that if the accounts are enclosed to

others, the image of the customers will be lost or it would affect the customer's business heavily. Hence,

it was the practice of the bankers not to disclose the accounts and banking operations of the customers to

others. The court held that 'the banker must not disclose the state of his customer of his affairs except on

reasonable and proper occasion'. In case, damages for breach of contracts is awarded if it found that

customer's interest has suffered because of the disclosure of the account which is not justified.

Circumstances the banker is justified in disclosure:

1. When there is an express consent of the customer: A banker is justified in disclosing the state of his

customer’s account to a third party when there is an express consent of the customer. For instance when

the customer has given the name of his banker to a third party for the purpose of trade reference, in such

a case as a referee the banker can answer all trade enquiries made by the third party about the customer.

2. When he is compelled by the laws of the country; For instance,

(a) Under the Banker’s Book of Evidence Act of 1891 banker can disclose the state of a customer’s

account to a court.

(b) Under section 285 of the Income Tax Act of 1961 every banker is required to furnish to the income

tax authorities the names, the address and the amounts of interest paid to depositors who get more than

Rs 10,000 as interest during any accounting year.

(c) Under Exchange control Act 1947 a banker can give information relating to a customer’s account to

the exchange control authorities

(d) Under Criminal Procedure Code a banker can disclose the state of a customer’s account to the police

officials for the purpose of investigation.

(e) Under the Companies Act of1956 a banker can give information relating to a company’s account to

the inspectors appointed by the Central Government to investigate the affairs of the company.

(f) Under the Customs Act a banker can give information to the Customs authorities.

(g) Under Gift Tax Act of 1958 information can be given to the gift tax authorities.

(I) Under RBI Act of 1934 the commercial bank has to give credit information of any account to the

RBI.

4. When he is under a public duty to disclose: For instance if a banker comes to know from his

customer’s bank account that his customer is engaged in trading with an enemy country during war or is

engaged in anti-social activity he can disclose the state of the customer’s account to the government in

the interest of the state.

5. When his own interest requires disclosure: For instance when a banker takes legal action against the

customer for the Realisation of the amount due he is permitted to disclose the state of the customer’s

account to his lawyer, the court etc.

6. When an enquiry is received from a fellow banker: When an enquiry is received by a banker from a

fellow banker about the state of the customer’s account the banker can answer that enquiry as a matter of

common courtesy.

Chapter 1 (B) CUSTOMER AND ACCOUNT HOLDERS

TYPES OF CUSTOMER AND ACCOUNTS HOLDERS

Current account:

Current accounts can be opened by individuals, business entities (firms, company), institutions, Government bodies /

departments, societies, liquidators, receivers, trusts, etc.

A current account is a running and active account that may be operated upon any number of times during a working day.

There is no restriction on the number and the amount of withdrawals from a current account.

The other main features of current account are as under: –

Current accounts are non-interest bearing and banks are not allowed to pay any interest or brokerage to the

current account holders.

Overdraft facility for a short period or on a regular basis up to specified limits are permitted in current

accounts

Regular overdraft facility is granted as per prior arrangements made by the account holder with the bank. In

such cases, the bank would honour cheques drawn in excess of the credit balance but not exceeding the

overdraft limit. Prescribed interest is charged on overdraft portion of drawings.

Cheques/ bills collection and purchase facilities may also be granted to the current account holders.

The account holder periodically receives statement of accounts from the Bank.

Normally, banks levy charges for handling such account in the shape of “Ledger Folio charges”. Some

banks make no charge for maintenance of current account provided the balance maintained is sufficient to

compensate the Bank for the work involved.

Third party cheques and cheques with endorsements may be deposited in the current account for collection

and credit.

Savings Account

Savings bank accounts are meant for individuals and a group of persons like Clubs, Trusts, Associations, Self

Help Groups (SHGs) to keep their savings for meeting their future monetary needs and intend to earn income

from their savings. Banks give interest on these accounts with a view to encourage saving habits. Everyone

wants to save for something in the future and their savings should be safe and accessible anytime, anyplace to

help meet their needs. This account helps an individual to plan and save for his future financial requirements. In

this account savings are completely liquid.

Main features of savings bank accounts are as follows:

Withdrawals are permitted to the account-holder on demand, on presentation of cheques or withdrawal

form/letter. However, cash withdrawals in excess of the specified amount per transaction/day (the

amount varies from bank to bank) require prior notice to the bank branch.

Banks put certain restrictions on the number of withdrawals per month/quarter, amount of withdrawal

per day, minimum balance to be maintained in the account on all days, etc. A fee/penalty is levied if

these are violated. These rules differ from bank to bank, as decided by their Boards. The rationale of

these restrictions is that the Savings Bank account should not be used like a current account since it is

primarily intended for attracting and accumulating savings.

The Bank pays interest on the products of balances outstanding on daily basis. Rate of interest is decided

by bank from time to time.

No overdraft in excess of the credit balance in savings bank account is permitted as there cannot be any

debit balance in savings account.

Most banks provide a passbook to the account-holder wherein date-wise debit credit transactions and

credit balances are shown as per the customer’s ledger account maintained by the Bank.

Cheque Book Facility Accounts in which withdrawals are permitted by cheques drawn in favour of self

or other parties. The payees of the cheque can receive payment in cash at the drawee bank branch or

through their bank account via clearing or collection. The account holder may also withdraw cash by

submitting a withdrawal form along with Pass Book, if issued.

Non-cheque Book Facility accounts where account holders are permitted to withdraw only at the drawee

bank branch by submitting a withdrawal form or a letter accompanied with the account passbook

requesting permission for withdrawal. In such cases third parties cannot receive payments.

Almost all banks which provide ATM facility, give ATM cards to their accounts holder, so that they

avail withdrawal facility 24 hours and all days at any place.

Basic Savings Bank Deposit Account With a view to making the basic banking facilities available in a more

uniform manner across banking system, RBI has modified the guidelines on opening of basic banking ‘no-frills’

accounts’. Such accounts are now known as “Basic Savings Bank Deposit” Account which offers the minimum

common facilities as under:

– The account should be considered as a normal banking service available to all;

– No requirement of minimum balance;

– Facilitate deposit and withdrawal of cash at bank branch as well as ATMs;

– Receipt/credit of money through electronic payment channels or by means of cheques/ collection of cheques

drawn by Central/State Government Agencies and departments;

– Account holders are permitted a maximum of four withdrawals in a month including ATM withdrawals;

– Facility of ATM card or ATM-cum Debit Card

– Facilities are free of charge and no charge would be levied for non-operation/activation of in-operative ‘Basic

Savings Bank Deposit Account’;

– Holders of ‘Basic Savings Bank Deposit Account’ are not eligible for opening of any other savings bank

accounts and existing such accounts should be closed down within a period of 30 days from the date of opening

of ‘Basic Savings Bank Deposit Account’.

– Existing ‘no frills’ accounts can be converted to ‘Basic Savings Bank Deposit Account’

Differences between Saving account and Current account: Current account Savings Account

Numbers of transactions Opened for meeting day to day requirements.

No limitation on the number of transactions that can be done in a particular month.

No charge on the amount being transacted.

Opened for deposits/savings from regular income. Limitation on number of transactions in a month.

Limitation on the amount that can be deposited or withdrawn from a savings bank account

Interest paid by Bank Bank does not give any interest on these accounts

Savings Bank offers interest

Facilities offered Overdraft facility is available No overdraft facility

Term Deposits

(a) Recurring Deposits or Cumulative Deposits : In Recurring Deposits accounts, a certain amount of savings

are required to be compulsorily deposited at specified intervals for a specific period. These are intended to

inculcate regular and compulsory savings habit among the low/ middle income group of people for meeting

their specific future needs e.g. higher education or marriage of children, purchase of vehicles etc.

The main features of these deposits are:

The customer deposits a fixed sum in the account at pre-fixed frequency (generally monthly/quarterly)

for a specific period (12 months to 120 months).

The interest rate payable on recurring deposit is normally the applicable rate of fixed deposits for the

same period.

The total amount deposited is repaid along with interest on the date of maturity.

The depositor can take advance against the deposits up to 75% of the balance in the account as on the

date of advance or have the deposits pre-paid before the maturity, for meeting emergent expenses. In

the case of pre-mature withdrawals, the rate of interest would be lower than the contracted rate and

some penalty would also be charged. Similarly, interest is charged on advance against the deposits,

which is normally one or two per cent higher than the applicable rate of interest on deposits.

Monthly-Plus Deposit Scheme / Recurring Deposit Premium account It is a recurring deposit scheme with flexibility of “Step-up and Step-down” options of monthly instalments. The

scheme is available to individuals, institutions, corporate, proprietorship or partnership firms, trusts, HUF, etc.

Under the scheme, the customer selects the “core amount” at the time of opening the account and deposits the

same initially. Minimum core amount may be Rs.100 and maximum Rs.1,00,000. Period of deposit will be pre

decided by the customer himself. The depositor can deposit installment in excess of the minimum core amount

(but not exceeding ten times of the core amount) in the multiples of Rs.100 in any month. Like stepping up the

installment amount, a customer can also reduce the same (Step-down) in any subsequent months but no below

the core amount. The interest on this scheme will be as per the term deposit rate applicable for the fixed period.

Interest will be calculated on the monthly product basis, for the minimum balance between the 10th and the last

day of the month and will be credited quarterly.

Fixed Deposits

Fixed deposits are repayable on the fixed maturity date along with the principal and agreed interest rate for the

period and no operations are allowed to be performed by the customer against the deposit, as is permitted in

demand deposits. The depositor foregoes liquidity on the deposit and the bank can freely deploy such funds for

loans/advances and earn interest. Hence, banks pay higher interest rates on fixed deposits as compared to savings

bank deposits from which he can withdraw, requiring banks to keep some portion of deposits always at the

disposal of the depositors. Another reason for banks paying higher interest on fixed deposits is that the

administrative cost in the maintenance of these accounts is very small as compared to savings bank accounts

where several transactions take place in cash, transfer or clearing, thus increasing the administrative cost.

Main Features of Fixed Deposits are as follows:

o Fixed deposits are accepted for specific periods at specified interest rates as mutually agreed between

the depositor and the banker at the time of opening the account. Since the interest rate on the deposit is

contractual, it cannot be altered even if the interest rate fluctuates - upward or downward - during the

period of the deposit.

o The interest rates on fixed deposits, which were earlier regulated by the RBI, have been deregulated and

banks offer varying interest rates for different maturities as decided by their boards. The maturity- wise

interest rates in a bank will, however, be uniform for all customers subject to two exceptions - high

value deposits above certain cut-off value and deposits of senior citizens (above the specified age

normally 60 years); these may be offered higher interest rate as per specified Basis Points. However,

specific directions are issued by the bank’s board with regard to the differential rate and the authority

vested to allow such differential rate of interest, to prevent discrimination and misuse at branch level.

o Minimum period of fixed deposit is 7 days, as per the directive of the RBI. The maximum term and

band of term maturities are determined by each bank along with the respective interest rates for each

band.

o A deposit receipt is issued by the bank branch accepting the fixed deposit- mentioning the depositor’s

name, principal amount, maturity period and interest rate, dates of the deposit and its maturity etc. The

deposit receipt is not a negotiable instrument, nor is it transferable, like a cheque. However, a term

deposit receipt evidences contract for the deposit on the specified terms.

o On maturity of a deposit, the principal and interest can be renewed for another term at an interest rate

prevalent at that time and a fresh deposit receipt is issued to the customer, evidencing a fresh contract.

Alternatively, the deposit can be paid up by obtaining the discharge of the depositor on the reverse of

the receipt.

o Many banks prepay fixed deposits, at their discretion, to accommodate customers’ request for meeting

emergent expenses. In such cases, interest is paid for the period actually elapsed and at a rate generally

1 per cent lower than that applicable to the period elapsed. Banks also may grant overdraft/ loan against

the security of their fixed deposits to meet emergent liquidity requirements of the customers. The

interest on such facility will be 1 per cent - 2 per cent higher than the interest rate on the fixed deposit.

Special Term Deposits

Special Term Deposit carries all features of Fixed Deposit. In addition to these, interest gets compounded every

quarter resulting higher returns to the depositors. Now-a-days, 80% of the term deposits in banks is under this

scheme. Higher Interest payable to Senior Citizens: Persons who have attained the age of 60 years are “Senior

Citizens” in regard to the payment of higher interest not exceeding 1% over and above the normal rates of term

deposits. Each bank has prepared its own scheme of term deposits for senior citizens.

VARIOUS TYPES OF CUSTOMERS Individuals Accounts of individuals form a major chunk of the deposit accounts in the personal segment of most

banks. Individuals who are major and of sound mind can open a bank account.

Minors:

In case of minor, a banker would open a joint account with the natural guardian. However to encourage the habit

of savings, banks open minor accounts in the name of a minor and allows single operations by the minor himself/

herself. Such accounts are opened subject to certain conditions like

(i) The minor should be of some minimum age say 12 or 13 years or above

(ii) Should be literate

(iii) No overdraft is allowed in such accounts

(iv) Two minors cannot open a joint account.

(v) The father is the natural guardian for opening a minor account, but RBI has authorized mother also to sign as

a guardian (except in case of Muslim minors)

Joint Account Holders:

A joint account is an account by two or more persons. At the time of opening the account all the persons should

sign the account opening documents.

Operating instructions may vary, depending upon the total number of account holders. In case of two persons it

may be

(i) jointly by both account holders

(ii) either or survivor

(iii) former or survivor

(iv) In case no specific instructions is given, then the operations will be by all the account holders

jointly,

The instructions for operations in the account would come to an end in cases of insanity, insolvency,

death of any of the joint holders and operations in the account will be stopped.

Illiterate Persons

Illiterate persons who cannot sign are allowed to open only a savings account (without cheque facility) or fixed

deposit account. They are generally not permitted to open a current account.

The following additional requirements need to be met while opening accounts for such persons:

o The depositor’s thumb impression (in lieu of signature) is obtained on the account opening form in the

presence of preferably two persons who are known to the bank and who have to certify that they know the

depositor.

o The depositor’s photograph is affixed to the ledger account and also to the savings passbook for

identification. Withdrawals can be made from the account when the passbook is furnished, the thumb

impression is verified and a proper identification of the account holder is obtained

Hindu Undivided Family (HUF)

HUF is a unique entity recognized under the Hindu customary law as comprising of a ‘Karta’ (senior-most male

member of the joint family), his sons and grandsons or even great grandsons in a lineal descending order, who

are ‘coparceners’ (who have an undivided share in the estate of the HUF). The right to manage the HUF and its

business vests only in the Karta and he acts on behalf of all the coparceners such that his actions are binding on

each of them to the extent of their shares in the HUF property. The Karta and other coparceners may possess self

acquired properties other than the HUF property but these cannot be clubbed together for the HUF dues. HUF

business is quite distinct from partnership business which is governed by Indian Partnership Act, 1932. In

partnership, all partners are individually and collectively liable to outsiders for the dues of the partnership and all

their individual assets, apart from the assets of the partnership, would be liable for attachment for partnership

dues. Contrarily, in HUF business, the individual properties of the coparceners are spared from attachment for

HUF dues.

The following special requirements are to be fulfilled by the banks for opening and conducting HUF accounts: –

The account is opened in the name of the Karta or in the name of the HUF business.

o A declaration signed by Karta and all coparceners, affirms the composition of the HUF, its Karta and

names and relationship of all the coparceners, including minor sons and their date of birth.

o The account is operated only by the Karta or the authorized coparceners.

o In determining the security of the family property for purposes of borrowing, the self-acquired properties

of the coparceners are excluded.

o On the death of a coparcener, his share may be handed over to his wife, daughters and other female

relatives as per the Hindu Succession Act, 1956. The Hindu Succession Act, 1956 has been amended in

2005. The Amendment Act confers equal rights to daughters in the Mitakshara Coparcenary property.

With this amendment the female coparcener can also act as Karta of the HUF. When any HUF property is

to be mortgaged to the Bank as a security of loan, all the major coparceners (including female

coparceners) will have to execute the documents Firms The concept of ‘Firm’ indicates either a sole

proprietary firm or a partner- ship firm. A sole proprietary firm is wholly owned by a single person,

whereas a partnership firm has two or more partners. The sole-proprietary firm’s account can be opened

in the owner’s name or in the firm’s name.

A partnership is defined under section 4 of the Indian Partnership Act, 1932, as the relationship between

persons who have agreed to share the profits of business carried on by all or any of them acting for all. It can be

created by an oral as well as written agreement among the partners. The Partnership Act does not provide for the

compulsory registration of a firm. While an unregistered firm cannot sue others for any cause relating to the

firm’s business, it can be sued by the outsiders irrespective of its registration.

In view of the features of a partnership firm, bankers have to ensure that the following requirements are complied

with while opening its account:

o The account is opened in the name of the firm and the account opening form is signed by all the partners of

the firm.

o Partnership deed executed by all the partners (whether registered or not) is recorded in the bank’s books,

with suitable notes on ledger heading, along with relevant clauses that affect the operation of the account.

o Partnership letter signed by all the partners is obtained to ensure their several and joint liabilities. The letter

governs the operation of the account and is to be adhered to accordingly. The following precautions should

be taken in the conduct of a partnership account:

o The account has to be signed ‘for and on behalf of the firm’ by all the authorized partners and not in an

individual name.

o A cheques payable to the firm cannot be endorsed by a partner in his name and credited to his personal

account.

o In case the firm is to furnish a guarantee to the bank, all the partners have to sign the document.

o If a partner (who has furnished his individual property as a security for the loan granted to the firm) dies,

no further borrowings would be permitted in the account until an alternative for the deceased partner is

arranged for, as the rule in Clayton’s case operates.

Companies A company is a legal entity, distinct from its shareholders or managers, as it can sue and be sued in its own

name. It is a perpetual entity until dissolved. Its operations are governed by the provisions of the Companies Act,

1956.

A company can be of three types:

o Private Limited company: Having 2 to 51 shareholders.

o Public company: Having 7 or more shareholders.

o Government company: Having at least 51per cent shareholdings of Government (Central or State).

The following requirements are to be met while opening an account in the name of a company:

o The account opening form meant for company accounts should be filled and specimen signatures of the

authorized directors of the company should be obtained.

o Certified up-to-date copies of the Memorandum and Articles of Association should be obtained. The

powers of the directors need to be perused and recorded to guard against ‘ultra vires’ acts of the

company and of the directors in future.

o Certificate of Incorporation (in original) should be perused and its copy retained on record.

o In the case of Public company, certificate of commencement of business should be obtained and a copy

of the same should be recorded. A list of directors duly signed by the Chairman should also be obtained.

o Certified copy of the resolution of the Board of Directors of the company regarding the opening,

execution of the documents and conduct of the account should be obtained and recorded.

Trusts

A trust is a relationship where a person (trustee) holds property for the benefit of another person (beneficiary) or

some object in such a way that the real benefit of the property accrues to the beneficiary or serves the object of

the A trust is generally created by a trust deed and all concerned matters are governed by the Indian Trusts Act,

1882. The trust deed is carefully examined and its relevant provisions, noted. A banker should exercise extreme

care while conducting the trust accounts, to avoid committing breach of trust:

– A trustee cannot delegate his powers to other trustees, nor can all trustees by common consent delegate their

powers to outsiders.

– The funds in the name of the trust cannot be used for crediting in the trustee’s account, nor for liquidating the

debts standing in the name of the trustee.

– The trustee cannot raise loan without the permission of the court, unless permitted by the trust deed.

Clubs Account of a proprietary club can be opened like an individual account. However, clubs that are

collectively owned by several members and are not registered under Societies Registration Act, 1860, or under

any other Act, are treated like an unregistered firm. While opening and conducting the account of such clubs, the

following requirements are to be met:

– Certified copy of the rules of the club is to be submitted.

– Resolution of the managing committee or general body, appointing the bank as their banker and specifying the

mode of operation of the account has to be submitted,

– The person operating the club account should not credit the cheques drawn favouring the club, to his personal

account.

Special Schemes for Non-Resident Indians (NRIs)

Non-resident deposits are mobilized from the persons of Indian nationality, or Indian origin living abroad

(NRIs) and Overseas’ Corporate Bodies (OCBs) predominantly owned by such persons.

1. Non-Resident Indians (NRIs) These fall into two categories:

(a) Indian citizens who stay abroad for employment/business/ vacation or for any other purpose in the

circumstances indicating an intention to stay abroad for an uncertain period. Income Tax Act has prescribed

minimum residence period abroad in a year or block of years for determining income tax liability of such persons

in India.

(b) Persons of Indian Origin (PIOs) other than Pakistan or Bangladesh, who had held Indian Passport at any

time, or whose parents or grand- parents were citizens of India, or the person is a spouse of an Indian citizen.

Ordinary Non-Resident (NRO) NRIs can open Non-Resident Ordinary (NRO) deposit accounts for collecting

their funds from local bona fide transactions. NRO accounts being Rupee accounts, the exchange rate risk on

such deposits is borne by the depositors themselves. When a resident becomes a NRI, his existing Rupee

accounts are designated as NRO.Such accounts also serve the requirements of foreign nationals resident in India.

NRO accounts can be maintained as current, saving, recurring or term deposits. While the principal of NRO

deposits is non-repatriable, current income and interest earning is repatriable. Further NRI/PIO may remit an

amount, not exceeding US $ 1 million per financial year, out of the balances held in NRO accounts/ sale

proceeds of assets /the assets in India acquired by him by way of inheritance/legacy, on production of

documentary evidence in support of acquisition, inheritance or legacy of assets by the remitter, and an

undertaking by the remitter and certificate by a Chartered Accountant in the formats prescribed by the Central

Board of Direct Taxes vide their Circular No. 10/2002 dated October 9, 2002.

Non-Resident (External) (NRE) Accounts The Non-Resident (External) Rupee Account NR(E)RA scheme,

also known as the NRE scheme, was introduced in 1970. Any NRI can open an NRE account with funds remitted

to India through a bank abroad. This is a repatriable account and transfer from another NRE account or FCNR

account is also permitted. A NRE rupee account may be opened as current, savings or term deposit. Local

payments can be freely made from NRE accounts. Since this account is maintained in Rupees, the depositor is

exposed to exchange risk. NRIs / PIOs have the option to credit the current income to their Non-Resident

(External) Rupee accounts, provided the authorized dealer is satisfied that the credit represents current income of

the non-resident account holders and income tax thereon has been deducted / provided for.

FCNR Scheme Non-Resident Indians can open accounts under this scheme. The account should be opened by

the non-resident account holder himself and not by the holder of power of attorney in India.

– These deposits can be maintained in any fully convertible currency.

– These accounts can only be maintained in the form of term deposits for maturities of minimum 1 year to

maximum 5 years.

– These deposits can be opened with funds remitted from abroad in convertible foreign currency through normal

banking channel, which are of repatriable nature in terms of general or special permission granted by Reserve

Bank of India.

– These accounts can be maintained with branches, of banks which are authorized for handling foreign exchange

business/nominated for accepting FCNR deposits.

– Funds for opening accounts under Global Foreign Currency Deposit Scheme or for credit to such accounts

should be received from:

– Remittance from outside India or

– Traveller Cheques/Currency Notes tendered on visit to India. International Postal Orders cannot be accepted

for opening or credit to FCNR accounts.

– Transfer of funds from existing NRE/FCNR accounts.

– Rupee balances in the existing NRE accounts can also be converted into one of the designated currencies at the

prevailing TT selling rate of that currency for opening of account or for credit to such accounts.

Advantages of FCNR Deposits

– Principal along with interest freely repatriable in the currency of the choice of the depositor.

– No Exchange Risk as the deposit is maintained in foreign currency. Loans/overdrafts in rupees can be availed

by NRI depositors or 3rd parties against the security of these deposits. However, loans in foreign currency

against FCNR deposits in India can be availed outside India through correspondent Banks.

– No Wealth Tax & Income Tax is applicable on these deposits.

– Gifts made to close resident relatives are free from Gift Tax.

– Facility for automatic renewal of deposits on maturity and safe custody of Deposit Receipt is also available.

Payment of Interest on FCNR deposits is being paid on the basis of 360 days to a year. However, depositor is

eligible to earn interest applicable for a period of one year if the deposit has completed a period of 365 days. For

deposits up to one year, interest at the applicable rate will be paid without any compounding effect. In respect of

deposits for more than one year, interest can be paid at intervals of 180 days each and thereafter for remaining

actual number of days. However, depositor will have the option to receive the interest on maturity with

compounding effect in case of deposits of over one year.

No bank should:

(i) Accept or renew a deposit over five years;

(ii) Discriminate in the matter of rate of interest paid on the deposits, between one deposit and another accepted

on the same date and for the same maturity, whether such deposits are accepted at the same office or at different

offices of the bank, except on the size group basis.

The permission to offer varying rates of interest based on size of the deposits will be subject to the following

conditions:

(a) Banks should, at their discretion, decide the currency-wise minimum quantum on which differential rates of

interest may be offered. For term deposits below the prescribed quantum with the same maturity, the same rate

should apply.

(b) The differential rates of interest so offered should be subject to the overall ceiling prescribed.

(c) Interest rates paid by the bank should be as per the schedule and not subject to negotiation between the

depositor and the bank.

(iii) Pay brokerage, commission or incentives on deposits mobilized under FCNR Scheme in any form to any

individual, firm, company, association, institution or any other person.

(iv) Employ/ engage any individual, firm, company, association, institution or any other person for collection of

deposit or for selling any other deposit linked products on payment of remuneration or fees or commission in any

form or manner.

(v) Accept interest-free deposit or pay compensation indirectly.

List of documents to be obtained by banks for opening an account

Features to be verified and documents that may be obtained from customers Features Documents

Accounts of individuals

– Legal name and any other names

used

– Correct permanent address

(i) Passport (ii) PAN card (iii) Voter’s Identity Card/ Aadhar Card (iv)

Driving licence (v) Identity card (subject to the bank’s satisfaction) (vi)

Letter from a recognized public authority or public servant verifying the

identity and residence of the customer to the satisfaction of bank (i)

Telephone bill (ii) Bank account statement (iii) Letter from any

recognized public authority (iv) Electricity bill (v) Ration card (vi) Letter

from employer (subject to satisfaction of the bank) (any one document

which provides customer information to the satisfaction of the bank will

suffice)

Accounts of companies

– Name of the company

– Principal place of business

– Mailing address of the company

– Telephone/Fax Number

(i) Certificate of incorporation and Memorandum & Articles of

Association (ii) Resolution of the Board of Directors to open an account

and identification of those who have authority to operate the account (iii)

Power of Attorney granted to its managers, officers or employees to

transact business on its behalf (iv) Copy of PAN allotment letter (v) Copy

of the telephone bill

Accounts of partnership firms

– Legal name

– Address Power of Attorney

granted to a partner or an employee

of the

– Names of all partners and their

addresses

-Telephone numbers of the firm

and the partners

(i) Registration certificate, if registered (ii) Partnership deed (iii) firm to

transact business on its behalf (iv) Any officially valid document

identifying and the persons holding partners the Power of Attorney and

their addresses (v) Telephone bill in the name of firm/partners

1

2. COLLECTING BANKER

NEGOTIABLE INSTRUMENTS Many documents are used in the modem commercial world. But, certain documents

are freely used in commercial transactions which are called negotiable instruments.

‘Negotiable’ means transferable whereas ‘instrument’ means a document, therefore negotiable instruments

means a transferable document. A negotiable instrument is one the legal title of which can be transferred freely from

all defects and the transferee can sue in his own name. But this negotiable instrument is not assignable, but

transferable. Thus, negotiability "easy transferability from one person to another in return for consideration".

Negotiable Instruments Act In India, the negotiable instruments are governed by the Negotiable Instruments

Act of 1881. Sec.13 of the Negotiable Instruments Act simply states that "negotiable means promissory note of

exchange or cheque payable either to order or to bearer ". Thus, Law recognizes three kinds of negotiable instruments,

namely a cheque, a bill of exchange and a promissory note. But, in recent times because of mercantile usage or

custom, certain other documents have been included in the category of Negotiable Instruments there are: dividend

warrants, bearer bonds, bearer scrips debentures payable to bearer, share warrants to bearer and treasury bills.

Definition: A Negotiable Instruments thus plays a key role in the modern business as a document which can

be transferable with ease. Wills defines it as "one property is acquired by anyone who takes it bonafide and for value,

not withstanding any defects of title in the person from whom he took it."

Types of Negotiable Instruments In India law recognizes only three instruments as negotiable and they are:

(i) Promissory note (ii) Bill of Exchange (iii) Cheque.

Meaning of Collecting Banker

A Collecting banker is one who undertakes to collect cheques, drafts, bill, pay order, traveller cheque, letter of

credit, dividend, debenture interest, etc., on behalf of the customer. For undertaking this collection, the collecting

banker will be charging commission. Examples: ICICI Bank, HDFC Bank, SBI Bank etc.

Duties and Responsibilities of a Collecting Banker

The duties and responsibilities of a collecting banker are discussed below:

1. Due Care and carefulness in the Collection of Cheques: The collecting banker is bound to show due care and

carefulness in the collection of cheques presented to him. In case a cheque is entrusted with the banker for collection,

he is expected to show it to the drawee banker within a reasonable time.

2. Serving Notice of Dishonor: When the cheque is dishonoured, the collecting banker is bound to give notice of the

same to his customer within a reasonable time. It may be noted here, when a cheque is returned for confirmation of

endorsement, notice must be sent to his customer.

3. Agent for Collection: In case a cheque is drawn on a place where the banker is not a member of the ‘clearing-

house’, he may employ another banker who is a member of the clearing-house for the purpose of collecting the

cheque. In such a case the banker becomes a substituted agent.

4. Payment of Interest to the Customer: In case a collecting banker has realised the cheque, he should pay the interest

to the customer as per his (customer’s) direction.

5. Collection of Bills of Exchange: There is no legal obligation for a banker to collect the bills of exchange for its

customer. But, generally, bank gives such facility to its customers.

Holder

Definition: Holder is an individual who has lawfully received possession of a Commercial Paper, such as a cheque

and who is entitled for payment on such instrument.

2

Holder for Value

Holder for value is a holder to whom an instrument is issued or transferred in exchange for something of value as a

promise of performance or a negotiable instrument. Example: A banker becomes a holder for value when: The value

of cheque is paid before collection of the cheque.

Holder in Due Course: A holder in due course is the holder of negotiable instruments who has given value in good

faith without notice of any previous dishonour in taking the bill, which appears to be complete and regular. Statutory

protection to Collecting Banks under the negotiable instruments Act The protection provided by Section 131 is not

absolute but qualified.

A collecting banker can claim protection against conversion if the following conditions are fulfilled:

1. Good Faith and Without Negligence Statutory protection is available to a collecting banker when he receives

payment in good faith and without negligence. The phrase in “good faith” means honestly and without notice or

interest of dishonesty or fraud and does necessarily require carefulness. Negligence means failure to exercise

reasonable care. The banker should have exercised reasonable care and deligence.

2. Collection for a Customer Statutory protection is available to a collecting banker if he collects on behalf of his

customer only. If he collects for a stranger or noncustomer, he does not get such protection. A bank cannot get

protection when he collects a cheque as holder for value

3. Acts as an Agent A collecting banker must act as an agent of the customer in order to get protection. He must

receive the payment as an agent of the customer and not as a holder under independent title. The banker as a holder

for value is not competent to claim protection from liability in conversion. In case of forgery, the holder for value is

liable to the true owner of the cheque. Crossed Cheques Statutory protection is available only in case of crossed

cheques. It is not available in case uncrossed or open cheques because there is no need to collect them through a

banker. Cheques, therefore, must be crossed prior to their presentment to the collecting banker for clearance.

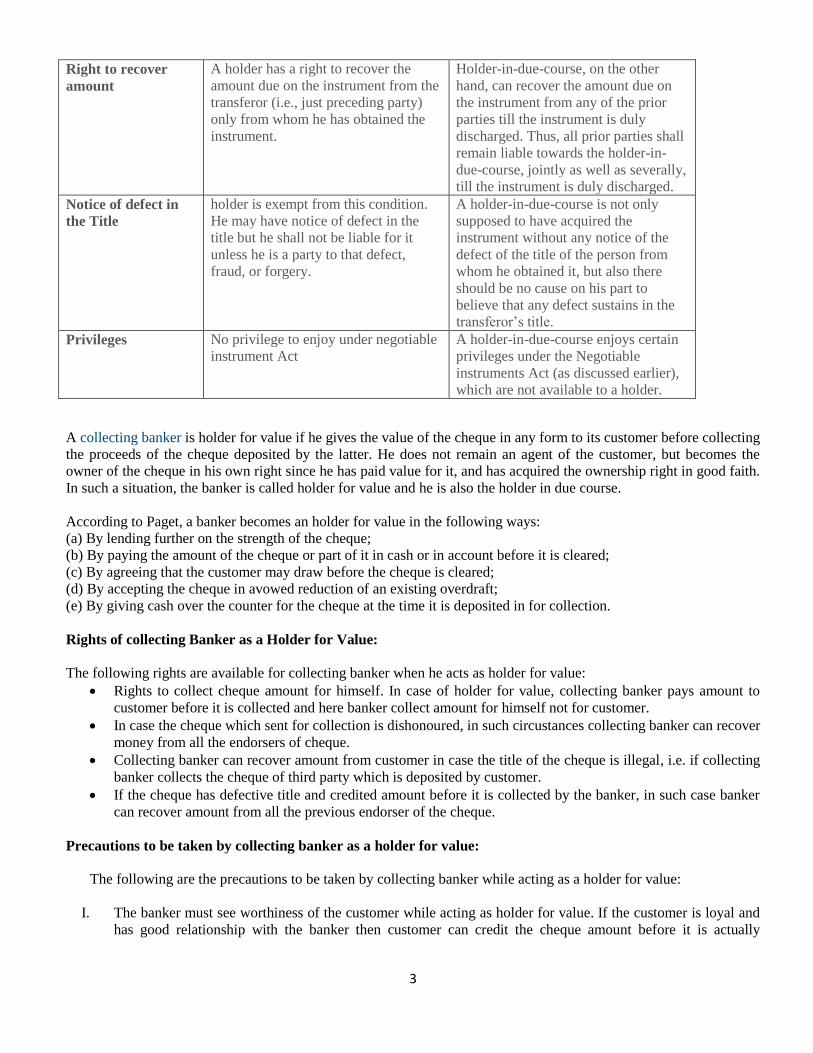

Difference between holder and holder-in-due-course can be explained on the basis of the following

Basis Holder Holder in Due Course

Entitlement Holder is a person who is entitled for

the possession of a negotiable

instrument in his own name. Hence he

shall receive or recover the amount due

thereon

Whereas a Holder-in-due-course is a

person who has obtained the

instrument for consideration and in

good faith and before maturity.

Consideration Consideration is not necessary to

become a holder. The instrument may

also be given by way of a donation or

gift and thus, the done of an instrument

can also become a holder of it.

consideration is a must to become a

holder-in-due-course and thereby the

done of a negotiable instrument can be

a holder but not holder-in-due-course

Maturity A holder may acquire the instrument

even after its maturity

holder-in-due-course must acquire the

instrument before its maturity failing

which he will not enjoy the rights of a

holder-in-due-course.

Title A holder does not acquire a better title

than that of transferor. In simple

words, if the title of any of the prior

party is defective, his title will not be

defect free. Whereas, a holder-in-due-

course derives a good title freed from

all defects.

His title is better than that of the

transferor.

3

Right to recover

amount

A holder has a right to recover the

amount due on the instrument from the

transferor (i.e., just preceding party)

only from whom he has obtained the

instrument.

Holder-in-due-course, on the other

hand, can recover the amount due on

the instrument from any of the prior

parties till the instrument is duly

discharged. Thus, all prior parties shall

remain liable towards the holder-in-

due-course, jointly as well as severally,

till the instrument is duly discharged.

Notice of defect in

the Title

holder is exempt from this condition.

He may have notice of defect in the

title but he shall not be liable for it

unless he is a party to that defect,

fraud, or forgery.

A holder-in-due-course is not only

supposed to have acquired the

instrument without any notice of the

defect of the title of the person from

whom he obtained it, but also there

should be no cause on his part to

believe that any defect sustains in the

transferor’s title.

Privileges No privilege to enjoy under negotiable

instrument Act

A holder-in-due-course enjoys certain

privileges under the Negotiable

instruments Act (as discussed earlier),

which are not available to a holder.

A collecting banker is holder for value if he gives the value of the cheque in any form to its customer before collecting

the proceeds of the cheque deposited by the latter. He does not remain an agent of the customer, but becomes the

owner of the cheque in his own right since he has paid value for it, and has acquired the ownership right in good faith.

In such a situation, the banker is called holder for value and he is also the holder in due course.

According to Paget, a banker becomes an holder for value in the following ways:

(a) By lending further on the strength of the cheque;

(b) By paying the amount of the cheque or part of it in cash or in account before it is cleared;

(c) By agreeing that the customer may draw before the cheque is cleared;

(d) By accepting the cheque in avowed reduction of an existing overdraft;

(e) By giving cash over the counter for the cheque at the time it is deposited in for collection.

Rights of collecting Banker as a Holder for Value:

The following rights are available for collecting banker when he acts as holder for value:

Rights to collect cheque amount for himself. In case of holder for value, collecting banker pays amount to

customer before it is collected and here banker collect amount for himself not for customer.

In case the cheque which sent for collection is dishonoured, in such circustances collecting banker can recover

money from all the endorsers of cheque.

Collecting banker can recover amount from customer in case the title of the cheque is illegal, i.e. if collecting

banker collects the cheque of third party which is deposited by customer.

If the cheque has defective title and credited amount before it is collected by the banker, in such case banker

can recover amount from all the previous endorser of the cheque.

Precautions to be taken by collecting banker as a holder for value:

The following are the precautions to be taken by collecting banker while acting as a holder for value:

I. The banker must see worthiness of the customer while acting as holder for value. If the customer is loyal and

has good relationship with the banker then customer can credit the cheque amount before it is actually

4

collected and even in case of dishonor or the cheque banker can recover amount by the customer if hr is loyal

customer.

II. Acting as holder for value banker should confirm title of cheque. He should ensure that his customer is the

true owner of the cheque to avoid risk.

III. Collecting banker should examine the state of cheque and essential contents of the cheque to avoid dishonor

of the cheque, if everything is right in the cheque the he can go ahead.

IV. Collecting banker should advise customer to repay money or damage caused by the dishonor or defective title

of the cheque.

V. The banker should collect amount from paying banker with in stipulated time or as soon as possible.

As agent for collection:

When the banker undertakes to collect the cheques and credits the account of the customer only on

realization. Thus, in acting as agent for collection, there is no risk for the collection, there is no risk for the collecting

banker whereas in the case of holder for value, the collecting banker has enormous risks, especially when the cheque

is dishonored or payment has been made to the wrongful owner of the cheque.

Liabilities of collecting banker as an agent of customer:

1. Collecting banker should collect the cheque amount with in stipulated time and credit same to the customer

account

2. In case of any dishonor of cheque collecting banker must serve notice to customer regarding dishonor of

cheque with reason of dishonor

3. While collecting cheque banker must function in good faith and without negligence.

4. While collecting customer cheque bank should show his skill and efficiency to collecting cheque as soon as

possible

5. Collecting banker should serve dishonor notice in case dishonor of cheque within reasonable time otherwise

collecting banker is liable for damages causes to customer

6. If any damages cause to customer by the negligence of collection banker while performing function, he will

become liable to customer.

Distinction between Holder for value and Agent of Customer

Holder for value Agent of customer

Collecting banker collects amount for himself but not

for customer in case of holder for value

Collecting banker collects cheque amount for customer

in case of agent of customer

Collecting banker will credit cheque amount to

customer account before it has been collected from

paying banker

Collecting banker will credit cheque amount to

customer account after it has been collected from

paying banker and before that.

Collecting banker will be the owner of cheque not

customer.

The actual owner of the cheque will be the customer

only and he gets the title of cheque.

When Collecting banker acts as holder for value, he

will not get any legal protection.

When Collecting banker acts as agent for value he will

get legal protection of cheque.

Negligence

The word negligence has no particular meaning, it depends on circumstances. Generally negligence refers to

careless of banker while performing its duties. Negligence depends upon the circumstances of each case.

A collecting banker can claim protection against conversion if the following conditions are fulfilled:

1. Good Faith and Without Negligence Statutory protection is available to a collecting banker when he receives

payment in good faith and without negligence. The phrase in “good faith” means honestly and without notice or

5

interest of dishonesty or fraud and does necessarily require carefulness. Negligence means failure to exercise

reasonable care. The banker should have exercised reasonable care and deligence.

2. Collection for a Customer Statutory protection is available to a collecting banker if he collects on behalf of his

customer only. If he collects for a stranger or noncustomer, he does not get such protection. A bank cannot get

protection when he collects a cheque as holder for value

3. Acts as an Agent A collecting banker must act as an agent of the customer in order to get protection. He must

receive the payment as an agent of the customer and not as a holder under independent title. The banker as a holder

for value is not competent to claim protection from liability in conversion. In case of forgery, the holder for value is

liable to the true owner of the cheque.

Crossed Cheques Statutory protection is available only in case of crossed cheques. It is not available in case uncrossed

or open cheques because there is no need to collect them through a banker. Cheques, therefore, must be crossed prior

to their presentment to the collecting banker for clearance. Review

6

3. Paying Banker

Meaning: Paying banker

“The bank on which a cheque is drawn (the bank whose name is printed on the cheque) and which pays the amount

for which the cheque is written and deducted that sum from the customer’s account”

Payment in due course

Analysis of section 10 reveals that the following conditions must be satisfies before a payment of a negotiable

instrument can be called as a payment in due course.

1. Payment in accordance with apparent tenor: When a paying banker receives cheques, he has to carefully go

through the instructions given by the drawer. For example, if the drawer has issued a cheque dated 10th June 2000,

Payment cannot be made before the date. If the cheque is crossed, then the banker cannot make payment across the

counter.