BANKING ECONOMIC EFFICIENCY IN THE DEREGULATION PERIOD: RESULTS FROM HETEROSCEDASTIC STOCHASTIC FRONTIER MODELS* by DIMITRIS K. CHRISTOPOULOS Panteion University, Athens and EFTHYMIOS G. TSIONAS{ Athens University of Economics and Business The paper provides quantitative estimates of technical and allocative ine/ciency measures of the Greek banking sector in the deregulation period. Such estimates are useful tools for bank managers and policy- makers in view of the extensive restructuring of the Greek ¢nancial system in recent years, and participation of Greece in the Euro-zone. The paper generalizes recent approaches based on heteroscedastic stochastic frontier models, and shows how to measure both technical and allocative e/ciency in such models. The method is applied to cost function estimation for the banking sector. It is found that technical ine/ciency is close to 20 per cent, allocative ine/ciency is also a sub- stantial part of costs, averaging 14 per cent, and both components have improved drastically in the deregulation period. This suggests that there is plenty of room for improvement in Greek bank pro¢tability and competitiveness in the new European ¢nancial environment. " Introduction Until the mid-1980s the Greek banking system operated in an environment characterized by selective controls and regulations, which gradually led to ine/ciency and to serious distortions in the functioning of the country’s ¢nancial system. The need for a modern, £exible and market-oriented ¢nancial system and the prospects for participating in the single European market initiated e¡orts towards the deregulation of the ¢nancial system. In recent years banking activity in Greece was decisively a¡ected by the harmonization of national regulations within the EU and especially with the enactment of the Second Banking Directive in 1992. In addition, consistent macroeconomic policies have been adopted in view of the country’s prospects of joining the European Monetary Union which have ß Blackwell Publishers Ltd and The Victoria University of Manchester, 2001. Published by Blackwell Publishers Ltd, 108 Cowley Road, Oxford OX4 1JF, UK, and 350 Main Street, Malden, MA 02148, USA. 656 The Manchester School Vol 69 No. 6 December 2001 1463^6786 656^676 * Manuscript received 17.8.00; ¢nal version received 9.3.01. { The authors wish to thank Sarantis Lolos, our co-author in previous banking research work, and two anonymous referees for useful comments and suggestions.

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

BANKING ECONOMIC EFFICIENCY IN THEDEREGULATION PERIOD: RESULTS FROM

HETEROSCEDASTIC STOCHASTIC FRONTIER MODELS*

byDIMITRIS K. CHRISTOPOULOS

Panteion University, Athensand

EFTHYMIOS G. TSIONAS{Athens University of Economics and Business

The paper provides quantitative estimates of technical and allocativeine¤ciency measures of the Greek banking sector in the deregulationperiod. Such estimates are useful tools for bank managers and policy-makers in view of the extensive restructuring of the Greek ¢nancialsystem in recent years, and participation of Greece in the Euro-zone.The paper generalizes recent approaches based on heteroscedasticstochastic frontier models, and shows how to measure both technicaland allocative e¤ciency in such models. The method is applied to costfunction estimation for the banking sector. It is found that technicaline¤ciency is close to 20 per cent, allocative ine¤ciency is also a sub-stantial part of costs, averaging 14 per cent, and both components haveimproved drastically in the deregulation period. This suggests that thereis plenty of room for improvement in Greek bank pro¢tability andcompetitiveness in the new European ¢nancial environment.

" Introduction

Until the mid-1980s the Greek banking system operated in an environmentcharacterized by selective controls and regulations, which gradually ledto ine¤ciency and to serious distortions in the functioning of the country's¢nancial system. The need for a modern, £exible and market-oriented¢nancial system and the prospects for participating in the single Europeanmarket initiated e¡orts towards the deregulation of the ¢nancial system.In recent years banking activity in Greece was decisively a¡ected by theharmonization of national regulations within the EU and especially withthe enactment of the Second Banking Directive in 1992. In addition,consistent macroeconomic policies have been adopted in view of thecountry's prospects of joining the European Monetary Union which have

ß Blackwell Publishers Ltd and The Victoria University of Manchester, 2001.Published by Blackwell Publishers Ltd, 108 Cowley Road, Oxford OX4 1JF, UK, and 350 Main Street, Malden, MA 02148, USA.

656

The Manchester School Vol 69 No. 6 December 20011463^6786 656^676

*Manuscript received 17.8.00; ¢nal version received 9.3.01.{The authors wish to thank Sarantis Lolos, our co-author in previous banking research work,

and two anonymous referees for useful comments and suggestions.

gradually reduced in£ation and interest rates.1 Currently, the Greekbanking system is faced with increased competition and internationaliza-tion, while banking disintermediation has been in evidence. These factors,together with the fast development of information technology, havetriggered major structural changes in the Greek banking system, which ismaking e¡orts at increasing e¤ciency, reducing costs of bank services anddiversifying in other business areas. More changes are expected in theyears to come.

In recent years, only two empirical works have focused attentionon the rate of productivity growth, scale economies and cost e¤ciency ofthe Greek banking system. In particular, Karafolas and Mantakas(1996) analyse technical change and scale economies over the period1980^89. Their results suggest that scale economies do not exist, andthat the impact of technical change on the performance of Greekcommercial banks has been insigni¢cant. However, when they exclude¢nancial costs from their cost function speci¢cation substantialeconomies of scale emerge. Noulas (1997) using a data envelope analysismethodology to evaluate the relative performance of state againstprivate banks for 1992 concludes that technical e¤ciency decreased forboth private and state banks, and state banks experienced technicalprogress while private banks did not. However, both studies limited theiranalysis to the pre-1993 period when the liberalization of the ¢nancialsystem was initiated.

The present paper relies on the stochastic frontier approach toprovide measures of economic e¤ciency. Stochastic frontier models haveproved to be indispensable tools of applied econometrics because they canbe used to derive estimates of technical ine¤ciency. E¤ciency informationis important not only in its own right but also in the decision-makingprocesses of managers and other units of the enterprise. In cost functionstochastic frontier models the di¡erence between observed cost andminimal cost re£ects total cost ine¤ciency. Total cost ine¤ciency can bedecomposed into technical and allocative ine¤ciency. The latter refers to a¢rm's ability to achieve the optimal input mix, and the former to its abilityto extract the maximum output(s) from a given level of inputs. Severalmodels have been presented in the literature to decompose total costine¤ciency into its components (see for example Kumbhakar, 1987, 1989;Bauer, 1990; Atkinson and Cornwell, 1994). In these models technicale¤ciency is measured by a one-sided term which is present only in the costfunction while allocative e¤ciency is measured by error terms that appearboth in the cost and share equations.

1Since 1993 an ambitious macroeconomic programme (the Greek Convergence Programme)was successfully implemented aiming at achieving the Maastricht criteria by the end ofthe 1990s. For a discussion on this issue, see Tsionas (2000).

Banking Economic E¤ciency 657

ß Blackwell Publishers Ltd and The Victoria University of Manchester, 2001.

However, one serious problem arises in the estimation of the frontierfunctions. This problem is known as Greene's problem (Greene, 1980) andrefers to the exact relationship between the one-sided error term in the costfunction and the two-sided error terms in the cost and share equations.Although some solutions have been suggested in the literature (see Greene,1980, 1993; Bauer, 1990; Ferrier and Lovell, 1990), the implications of aprecise relationship between the one-sided error term in the cost functionand the two-sided error term in the cost and share equations have not beenpresented in the literature. In other words, there is a self-consistency issuethat has not been addressed so far in empirical frontier studies.

This implies that estimates of technical and allocative ine¤ciency thatdo not respect consistency may be seriously misguided, and therefore an issuearises regarding how better estimates can be obtained. One additionalproblem that arises in the estimation of stochastic frontier functions is thepossible correlation between technical and allocative e¤ciency. AlthoughSchmidt and Lovell (1979, 1980) reported that the shape and placement ofthe frontier function was not a¡ected in their samples by whetherindependence was assumed or not, the issue itself has su¤cient economicimportance to merit further examination. To that end, Mensah (1994)suggested a simpli¢cation of the method of cost e¤ciency decompositionproposed by Kopp and Diewert (1982) and Zeischang (1983) which permitsboth issues to be addressed. However, in this solution,Mensah (1994) ignoresthe e¡ect of heteroscedasticity in both technical and allocative e¤ciencymeasures. This issue is of great interest. Caudill and Ford (1993) reportedthat heteroscedasticity in the one-sided error a¡ects parameter estimates in asingle-factor frontier production function materially. Speci¢cally, when themodel is estimated by maximum likelihood, heteroscedasticity leads tooverestimation of the intercept and underestimation of the slope coe¤cients.Thus, they conclude that ine¤ciency measures are a¡ected by heteroscedasti-city. (See also Caudill et al. (1995) for an empirical application ofheteroscedastic frontiers to the US banking industry.)

When estimating stochastic frontiers in the banking sector it is quiteprobable that heteroscedasticity is a feature of the data because banks ofdi¡erent `size' are pooled together. This necessitates the use of hetero-scedastic cost frontiers as in Caudill et al. (1995) and Hadri (1999).However, in the banking industry it is not only necessary to estimate thetechnical e¤ciency of banks but also their allocative e¤ciency, i.e. theirability to combine inputs in an optimal way (see for example Berger andHumphrey, 1991). Previous work in the ¢eld of heteroscedastic frontiershas ignored the issue.

The purpose of the present paper is to show how both technical andallocative e¤ciency can be estimated from a heteroscedastic cost frontierin a self-consistent way, i.e. in a way that respects the fact that costfunction and share equation residuals must be related.

658 The Manchester School

ß Blackwell Publishers Ltd and The Victoria University of Manchester, 2001.

The remainder of the paper is organized as follows. The structureof Greek banking is reviewed in Section 2. The model is presented inSection 3 and the econometric estimation technique is analysed in Section4. The way to measure allocative e¤ciency is explained in Section 5.The data are presented in Section 6. The empirical results are presentedand discussed in Section 7 and the ¢nal section contains some concludingremarks.

á Structure of the Greek Banking System

A major structural feature of the Greek banking system in the past wasits institutional specialization required by law rather than dictated bymarket forces. Towards the late 1980s, there was a process of gradual andextensive liberalization of the market, motivated by international develop-ments and the need for participation in the single European market for¢nancial services. During the 1990s, the process of liberalization andderegulation of the banking system was carried out at an accelerating paceand the provision of the Second Banking Directive concerning theestablishment, operation and supervising of credit institutions was passedby the Greek Parliament in August 1992. Various measures were alsotaken towards the modernization of the capital market.2

Commercial banks have been the dominant group in the Greekbanking system. In 1998, besides the Central Bank, there were 49 creditinstitutions established and operating in the Greek banking market. Thecommercial banking system comprises 18 commercial banks3 and 20branches of foreign banks, of which 12 are EU-based. Also there are sevenspecialized credit institutions, namely two investment banks, three real-estate banks, a saving bank and a speci¢c purpose bank, nine creditcooperatives and 13 cooperative banks.4

A speci¢c structural feature of the Greek ¢nancial credit system,which includes the smallest number of credit institutions in the EU, hasbeen the decisive presence of the state, the dominant role of a few largebanks and the limited share of foreign banks. Also, the relative weight ofbanking in the Greek ¢nancial system is still very high, although the depthof the capital and money markets has increased considerably in recentyears.

2For a detailed discussion on the developments in the regulatory and institutional frameworkof the Greek ¢nancial system see, inter alia, Hondroyiannis et al. (1999), Central Banking(1995^96) and the references cited therein.

3Including the Agricultural Bank, which, although it has been classi¢ed as a commercial banksince 1991, still operates rather as a specialized credit institution.

4For the creation and functioning of credit cooperatives and cooperative banks in Greece,see Karafolas (1997).

Banking Economic E¤ciency 659

ß Blackwell Publishers Ltd and The Victoria University of Manchester, 2001.

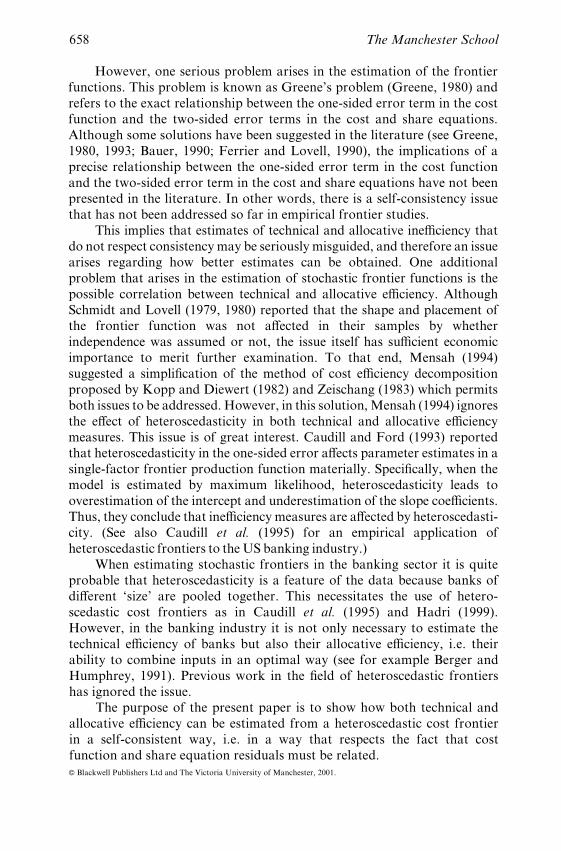

Basic size characteristics of the Greek banking system are depictedin Table 1. Over the period 1993^98, the presence of the large banks interms of assets and branches in the Greek banking system remained high,while most of the smaller banks expanded far more rapidly in relation tolarger ones. On the assets side, loans and advances have been the mostimportant output for all banks, amounting to around 40 per cent of totalassets, while the share of investments in shares is very low with theexception of large banks and the faster growing smaller banks. The shareof bonds (mainly government securities) is fairly signi¢cant for mostbanks, a fact attributed to the obligation (until 1991) of banks to keep ahigh proportion (40 per cent) of their portfolio in government securities.In subsequent years the purchasing of new treasury bills was graduallyreduced but the stock of public debt held by the banking system continued,keeping high interest rate margins between loans and deposits.5 However,the situation was gradually normalized along with the reduction of budgetde¢cits and the liberalization of the banking system.

Table "Characteristics of the Greek Commercial Banking System ("ññâ^ñð)

Bank rankingin terms of

assets Average share (%) in total assets

Bank name

Average totalassets

(billion Dr) 1993 1998 TotalLoans andadvances

Liquidassets Investments

National 8836 1 1 63 24 35 4Commercial 2830 2 3 68 37 26 5Alpha Credit 2579 3 2 42 36 3 3Ionian 1609 4 4 51 27 21 2Ergobank 1128 5 5 40 36 3 1Eurobank 480 9 6 56 34 19 4Macedonia-Thrace 397 8 8 62 44 17 1General 367 6 9 70 45 24 1Kretabank 342 7 11 55 52 1 2Xiosbank 258 10 10 47 38 9 0Piraeus 253 13 7 66 42 16 8Interbank a 149 12 ^ 53 38 15 0Central Greece 135 11 15 62 48 14 1Egnatia 119 17 12 60 54 3 4Attica 116 16 14 55 53 0 2Europaiki 113 19 13 43 29 13 1Athens b 100 15 ^ 67 47 19 1Prime 91 14 17 41 41 0 0Dorian 53 18 16 71 52 16 2

Notes: a 1993^96b 1993^97.

Source: Banks' balance sheets and income statements.

5For a discussion on this point, see Hondroyiannis et al. (1998).

660 The Manchester School

ß Blackwell Publishers Ltd and The Victoria University of Manchester, 2001.

Recently, the Greek ¢nancial and banking landscape has been changingrapidly andmore major changes are expected in the years to come, as a resultof government measures and also as a result of the dynamics of the domesticand the EU ¢nancial and credit markets. In particular, the government hasdecided to reduce the state's presence in a controlled way (four small andmedium-sized banks (Attica, Kretabank, Macedonia-Thrace, CentralGreece) and the third largest bank (Ionian) have been privatized) while aseries of mergers and acquisitions have been undertaken which have changedthe structure of the Greek banking system substantially.

â The Model

Consider the following cost frontier:

log Cit � h�zit; b� � vit � uit � Ait i � 1; . . . ; n; t � 1; . . . ; T �1�where Cit denotes the cost of bank i at date t, zit � �p0it y0it�0 is a k� 1 vectorof explanatory variables which includes the logarithms of input pricesand output quantities, pit is the q� 1 vector of input prices, yit is the s� 1vector of output quantities (notice that k � q� s), b is a k� 1 vector ofparameters, h is a function, vit is a two-sided error term and uit is a one-sided error term representing technical ine¤ciency. Finally, Ait is a non-negative error term that represents allocative ine¤ciency. The shareequations corresponding to the above cost function can be derived usingShephard's lemma, and are given by the following:

Sijt �@ log Cijt

@ log pijt

� m�zit; b� � Zijt j � 1; . . . ; qÿ 1 �2�

where Zijt is a two-sided error term which re£ects allocative ine¤ciency inthe sense that the actual share may be greater than or less than its optimalcounterpart. Denote by git the �qÿ 1� � 1 vector of the Zjt. For moredetails, see Greene (1980), Kumbhakar (1987, 1989) and Ferrier andLovell (1990). Greene raised the issue of the connection that must existbetween A and the Zj. Other approaches which ignore the connection (e.g.set A � 0) and rely on a multivariate normal distribution for g and anindependent convolution for v and u include Kalirajan (1990), Greene(1980), Kumbhakar (1987, 1989) and Seale (1990).

In this paper, we make the following assumptions:

(i) vit � IN�0; s2v�;

(ii) uit � IN�0; s2u;it�; uit � 0;

(iii) s2u;it � exp�w0ith� where wit is a g� 1 vector of explanatory variables

of the variance of the one-sided error term, and h is a g� 1 vector ofparameters;

(iv) vit and uit are mutually independent as well as independent of zit.

Banking Economic E¤ciency 661

ß Blackwell Publishers Ltd and The Victoria University of Manchester, 2001.

These assumptions are standard except for (iii) which states that the one-sided error term is heteroscedastic and the logarithm of its variancedepends on predetermined variables wit.

ã Estimation Technique

Because of the presence of the one-sided error uit and in particular the factthat this term is heteroscedastic, popular estimation methods such asZellner's seemingly unrelated regression (SUR) cannot be used.6 Part ofthe problem is that least squares estimation of a single-equation frontierwith heteroscedasticity leads to inconsistent estimates (Caudill and Ford,1993), so the same must be true for SUR estimation which ignores hetero-scedasticity. A feasible technique is to estimate the cost function and shareequations separately. Since the cost function and share equations haveparameters in common by construction, this may involve some loss ofe¤ciency but estimates are still consistent. Joint estimation is very di¤cultin this context. The likelihood function is given by a product of con-volutions of the multivariate normal distribution for the cost function^share equation errors with the heteroscedastic normal one-sided errorterm. This likelihood function is prone to numerical failures7 so we preferto stick with a simpler, operational estimator.

Under the assumption of a multivariate normal distribution for git,estimation of the share equations is straightforward. Estimating the costfunction is more involved and has to be done using maximum likelihood.The common practice before proceeding to estimation is to identify aparametric form of the cost frontier in equation (1). To keep the analysissimple, we adopt the Cobb^Douglas cost function. Thus, our cost functioncan be written as follows:

ln Cit � a0 �Xm

k�1bk ln Pitk �

XL

l�1Yitl �

XT

t�2jtDt � vit � uit � Ait �3�

where Pitk is the k th input price �k � 1; 2; . . . ;m� of the i th bank�i � 1; 2; . . . ; n� in time period t �t � 1; 2; . . . ; T �, Yitl is the l th output�l � 1; 2; . . . ; L � of the i th bank in time period t and Dt are time-speci¢cdummies �t � 2; 3; . . . ; T �. The coe¤cients jt are parameters to beestimated and capture technical progress in a general way.

6This entails estimating the system of cost function and share equations by SUR andestimating ine¤ciency by the formula of Jondrow et al. (1982).

7Part of the problem is that the covariance matrix of the cost function^share equation errorterms cannot be concentrated out of the likelihood function so unrestricted estimation ofthis matrix is not guaranteed to yield positive de¢nite estimates. If constrained to bepositive de¢nite by use of Cholesky parameterization, the likelihood function is highlynon-linear and intractable. These problems do not arise in the simpler heteroscedasticcost frontier because this does not involve the added complexity of simultaneousestimation with the share equations.

662 The Manchester School

ß Blackwell Publishers Ltd and The Victoria University of Manchester, 2001.

Since in the presence of non-constant returns to scale allocativeine¤ciency values will be a hash of the allocative ine¤ciency and thedi¡erence between the scale of the bank and the e¤ciency scale, weallow for the possibility of constant returns to scale by restricting

Pbk

to equal 1.8

The method of maximum likelihood involves ignoring the term Ait

and following the estimation method of Caudill et al. (1995). Thisapproach does not imply that we totally ignore allocative e¤ciency,however, because it can still be estimated in a self-consistent way, as weshall see later. If eit � vit � uit, the density function of the composed errorterm of the cost frontier is

p�eit� �2sit

feit

sit

� �F

liteit

sit

� ��4�

where f and F denote the probability distribution function and cumulativedistribution function, respectively, of the standard normal distribution,s2

it � s2v � s2

u;it, and lit � su;it=sv. The log-likelihood function9 can bewritten as

L �b; h; sv; data� �Xn

i�1

XT

t�1log p�eit� �5�

Following Jondrow et al. (1982), the conditional expected value of uit

given eit is

E�uit j eit� � sit

eitlit

sit

� feitlit

sit

� �F

eitlit

sit

� �ÿ1" #�6�

where sit � svsu;it=sit.The important property of this procedure is that allocative e¤ciency

can still be estimated in a consistent way (in the sense that the dependencebetween A and git is respected) by using the approach presented in the nextsection.

ä Estimating Allocative Inefficiency

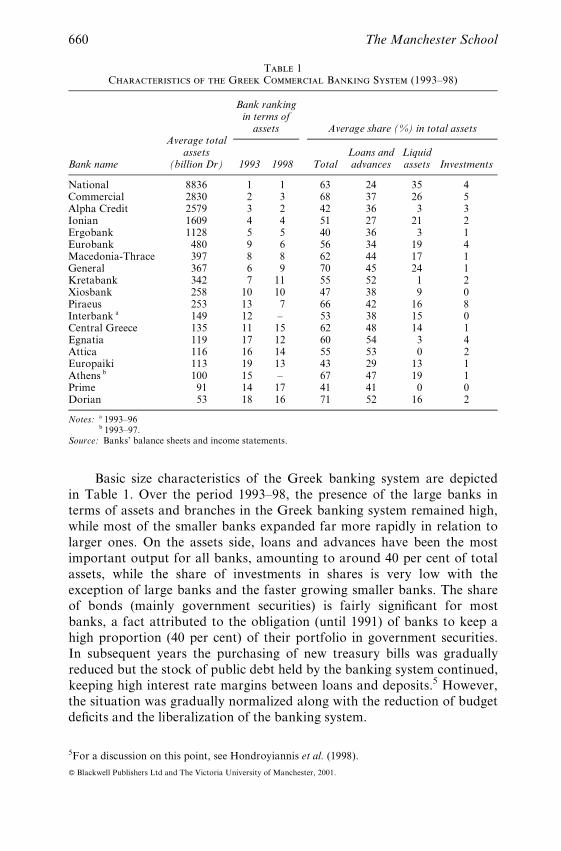

A promising approach to measuring allocative ine¤ciency was suggestedby Kopp and Diewert (1982). In Fig. 1, consider the isoquant at �y and letxA be the actual input choice and xB the technically e¤cient choice relative

8This observation was pointed out to us by an anonymous referee. Later on, we do test therestriction to ¢nd that it is not rejected by our data.

9It should be noted that ordinary least squares (OLS) estimation of stochastic frontierswithout heteroscedasticity provides consistent (albeit ine¤cient) estimates of allparameters except for the intercept term. With heteroscedasticity, OLS estimates arebiased and inconsistent because the frontier is not simply displaced but `twisted' (seeCaudill and Ford, 1993).

Banking Economic E¤ciency 663

ß Blackwell Publishers Ltd and The Victoria University of Manchester, 2001.

to xA. The economically e¤cient choice is xE given the price vector pA.The measure of allocative e¤ciency is k xC k=k xB k. To obtain point xC,Kopp and Diewert (1982) suggested obtaining an estimate of the minimumcost function C�y; pA�. Let CA

� be the implied minimum cost of productionof �y at prices pA. The components of xC can be deduced as follows. First,the input mix of xA and xC must be the same which implies

xCi

xCn

� xAi

xAn

i � 1; . . . ; nÿ 1 �7�

Second, the total cost of production at xC and xE is the same whichimplies

pA 0xC � CA� �8�

The components of vector xB can be obtained by using the fact thatthere exists a price vector pB for which xB is allocative e¤cient. Relativeprices and xB can be obtained as follows. First, the input mix at xB and xA

must be the same which implies

xBi

xBn

� xAi

xAn

i � 1; . . . ; nÿ 1 �9�

Second, the demand system implied by Shephard's lemma is

xBi �

@C�y; pB�@pi

i � 1; . . . ; n �10�

Fig. 1

x2

xA

xB

xC

xE

y

x1

664 The Manchester School

ß Blackwell Publishers Ltd and The Victoria University of Manchester, 2001.

This provides a set of nÿ 1 linear and n non-linear equations (see alsoZeischang, 1983). The iterative solution of such systems is no small matter.Mensah (1994) derived a simpli¢cation of the Kopp and Diewert (1982)procedure and showed that the components of pB satisfy

pBi �

m� pB; y�Si

pAi i � 1; . . . ; n �11�

where m� pB; y� is the optimal cost share and Si is the observed share. Thisoptimal share function involves parameters that have been consistentlyestimated in the application of the maximum likelihood method to the costfrontier in (5). Therefore, the logarithmic cost function may be written as

ln C � hm� pB; y�

Si

pAi ; y

� ��12�

A further approximation, which Mensah (1994) has found to workwell, is to replace m� pB; y� with m� pA; y�, i.e. the observed prices. If wede¢ne

p�i �m� pA; y�

Si

pAi i � 1; . . . ; n �13�

the logarithmic cost function becomes

ln C � h� p�; y� �14�and the measure of allocative ine¤ciency is

AI � h� p�; y� ÿ h� p; y� �15�For our Cobb^Douglas function expression (15) reduces to a simplefunction of logarithms of ¢tted input shares, actual input shares and theparameters to be estimated.10 Moreover, for the Cobb^Douglas costfunction, Mensah's approach is exact. More complicated cost functions donot yield exact solutions, and require numerical methods to obtain pB.

å Data

The empirical investigation has been carried out using annual data fromthe balance sheet accounts and income statements of the Greek bankingsystem. Our sample covers all Greek commercial banks operating inGreece over the period 1993^98; thus we have panel data. Thus, 19 banksare included in our sample for the period 1993^96, 18 banks in the year1997 since one bank (Interbank) ceased operating independently, and 17

10This issue was brought to our attention by an anonymous referee.

Banking Economic E¤ciency 665

ß Blackwell Publishers Ltd and The Victoria University of Manchester, 2001.

banks in 1998 since yet another bank (Bank of Athens) ceased independentoperation; both have been absorbed by Eurobank.

The estimated cost function employs three inputs and three outputs,the choice of which was determined by the availability of data and fromour view on the way that banks operate. All variables are de¢nedaccording to the Consolidated Banking Accounting System.

The three output variables YL (loans) YI (investments) and YA (liquidassets) are de¢ned in real terms as follows:

YL value of loans and advances: includes short-term and long-term loansand advances to non-bank and credit institutions and customers (notexcluding provisions)

YI value of investments: includes shares and other variable-incomesecurities and participation in a¤liated and non-a¤liated companies

YA value of liquid assets: liquid assets include all investments in ¢xedincome securities including government securities

The three input variables L (labour), K (capital) and D (deposits) are asfollows:

L labour: total number of full-time employeesK capital: ¢xed assets which include tangible ¢xed assets (land, lots,

buildings and installations, furniture, o¤ce equipment etc., less de-preciation), as well as intangible ¢xed assets (goodwill, software,restructuring expenses, research and development expenses, minorityinterests, formation expenses, underwriting expenses etc.)

D deposits: total deposits that include bank bonds and sight, saving,time and restricted deposits private and public in drachmae and inforeign exchange

Finally, the unit prices of the three respective inputs (PL;PK and PD)are de¢ned as follows:

PL unit price of labour: ratio of personnel expenses to total labour (L );personnel expenses include wages and salaries, social security con-tributions, contributions to pension funds and other related expenses

PK unit price of capital: ratio of capital expenses to ¢xed assets (K);capital expenses refer to depreciation expenses on a historical cost-basis balance sheet

PD unit price of deposits: ratio of interest expenses to total deposits (D);interest expenses include interest paid on deposits and commissionexpenses and payments under Law 128/75.11

11Law 128/75 refers to obligations of commercial banks to ¢nance priority sectors atpreferential interest rates. Note that these are payments to the Bank of Greece, but theyare also included in the interest income as revenues.

666 The Manchester School

ß Blackwell Publishers Ltd and The Victoria University of Manchester, 2001.

æ Empirical Results

7.1 E¤ciency Measurement

The parameters of equation (3) were estimated by maximum likelihood.Estimation was accomplished using the algorithm described by Berndt etal. (1974) as implemented in TSP. To allow for heteroscedasticity in theone-sided error term several variables were included in the vector Z.However, only total deposits was found to permit convergence of theiterative procedure, although we tried a great number of combinations ofother variables and several sets of initial conditions. Therefore, we usetotal deposits as a determinant of bank e¤ciency heteroscedasticity.

The regression coe¤cients and the variance parameters are reportedin Table 2. All price coe¤cients have the expected signs, and the majorityof them are statistically signi¢cant at conventional signi¢cance levels.Turning our attention to variance parameters we can conclude that ourresults provide strong evidence for the existence of a heteroscedastic costfrontier. The slope coe¤cient �Z1� is statistically signi¢cant. Finally, to testfor the presence of constant returns to scale, a Wald test was used. Thecomputed w2�1� is 3.25 while the 5 per cent critical value is 3.84. Thus, ourresults are consistent with the hypothesis that constant returns to scaleprevail in the Greek banking industry.

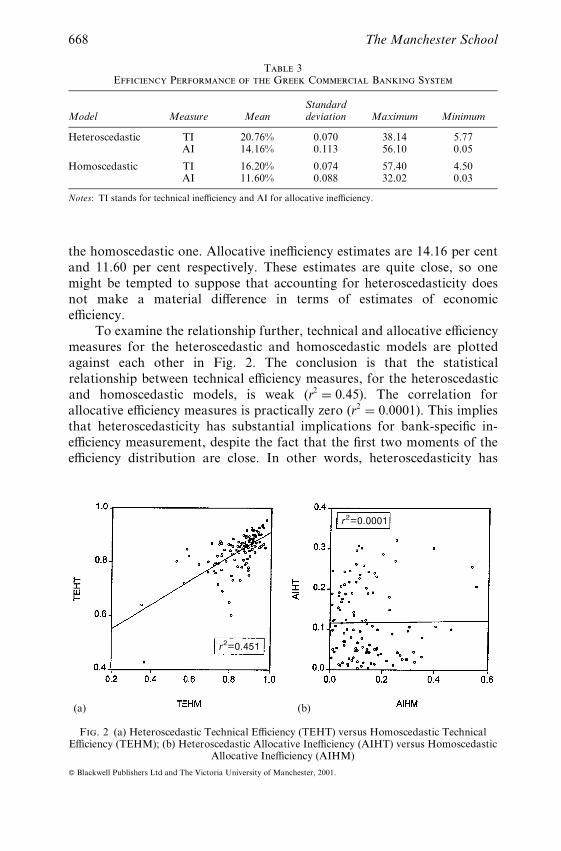

Table 3 contains summary results of e¤ciency analysis withhomoscedastic and heteroscedastic frontiers. Average technical e¤ciencyis about 80 per cent for the heteroscedastic model and over 83 per cent for

Table áMaximum Likelihood Estimated Cost Parameters

Parameter Estimate Standard error

a0 1.05*** 0.54aL 1.04*** 0.05aI 0.04* 0.01aA 0.02 0.03bD 0.85*** 0.07bL 0.03 0.11j94 0.05 0.09j95 ÿ0.07 0.09j96 ÿ0.18*** 0.10j97 ÿ0.25 0.12j98 ÿ0.30* 0.13

Variance parameter estimatesZ0 ÿ2.26*** 0.86Z1 0.23*** 0.06sV 0.14** 0.07

Notes: The signs ***, ** and * indicate statistical signi¢cance at the 1, 5 and 10per cent levels of signi¢cance respectively.

Banking Economic E¤ciency 667

ß Blackwell Publishers Ltd and The Victoria University of Manchester, 2001.

the homoscedastic one. Allocative ine¤ciency estimates are 14.16 per centand 11.60 per cent respectively. These estimates are quite close, so onemight be tempted to suppose that accounting for heteroscedasticity doesnot make a material di¡erence in terms of estimates of economice¤ciency.

To examine the relationship further, technical and allocative e¤ciencymeasures for the heteroscedastic and homoscedastic models are plottedagainst each other in Fig. 2. The conclusion is that the statisticalrelationship between technical e¤ciency measures, for the heteroscedasticand homoscedastic models, is weak �r2 � 0:45�. The correlation forallocative e¤ciency measures is practically zero �r2 � 0:0001�. This impliesthat heteroscedasticity has substantial implications for bank-speci¢c in-e¤ciency measurement, despite the fact that the ¢rst two moments of thee¤ciency distribution are close. In other words, heteroscedasticity has

Table âEfficiency Performance of the Greek Commercial Banking System

Model Measure MeanStandarddeviation Maximum Minimum

Heteroscedastic TI 20.76% 0.070 38.14 5.77AI 14.16% 0.113 56.10 0.05

Homoscedastic TI 16.20% 0.074 57.40 4.50AI 11.60% 0.088 32.02 0.03

Notes: TI stands for technical ine¤ciency and AI for allocative ine¤ciency.

(a) (b)

Fig. 2 (a) Heteroscedastic Technical E¤ciency (TEHT) versus Homoscedastic TechnicalE¤ciency (TEHM); (b) Heteroscedastic Allocative Ine¤ciency (AIHT) versus Homoscedastic

Allocative Ine¤ciency (AIHM)

r2=0.0001

r2=0.451

668 The Manchester School

ß Blackwell Publishers Ltd and The Victoria University of Manchester, 2001.

a¡ected bank-speci¢c e¤ciency measures signi¢cantly without greatlya¡ecting the mean or the variance of the overall e¤ciency distribution.

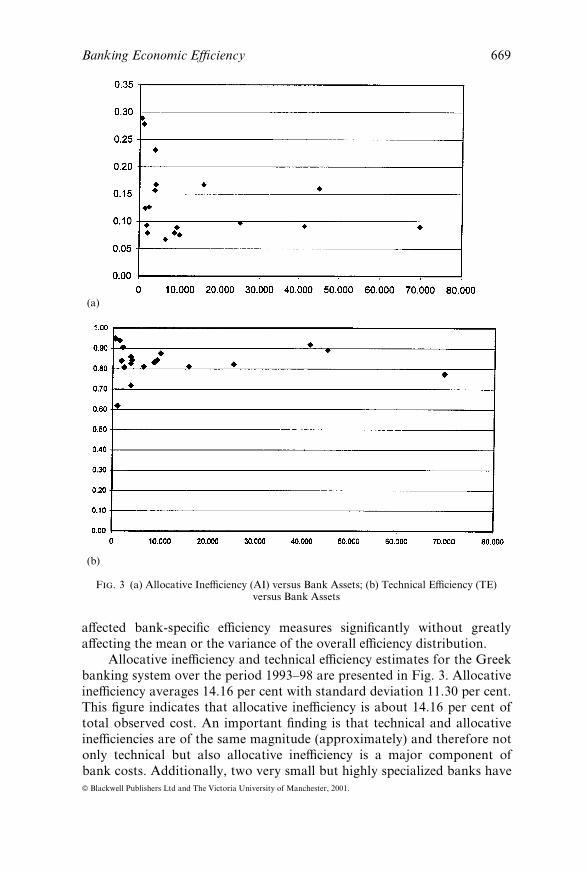

Allocative ine¤ciency and technical e¤ciency estimates for the Greekbanking system over the period 1993^98 are presented in Fig. 3. Allocativeine¤ciency averages 14.16 per cent with standard deviation 11.30 per cent.This ¢gure indicates that allocative ine¤ciency is about 14.16 per cent oftotal observed cost. An important ¢nding is that technical and allocativeine¤ciencies are of the same magnitude (approximately) and therefore notonly technical but also allocative ine¤ciency is a major component ofbank costs. Additionally, two very small but highly specialized banks have

(a)

(b)

Fig. 3 (a) Allocative Ine¤ciency (AI) versus Bank Assets; (b) Technical E¤ciency (TE)versus Bank Assets

Banking Economic E¤ciency 669

ß Blackwell Publishers Ltd and The Victoria University of Manchester, 2001.

high allocative ine¤ciency scores, in excess of 25 per cent. However, bothbanks were sold to other ¢nancial institutions in 1999. Our ¢nding thatboth technical and allocative ine¤ciencies are high is in line with allocativeine¤ciency estimates reported by Aly et al. (1990) for a sample of UScommercial banks and Vivas-Lozano (1998) for the Spanish bankingindustry.

Technical e¤ciency results indicate that, for the great majority ofbanks, e¤ciency ranges from 80.78 to 94.30 per cent and most of thevariation comes from banks of smaller size. When size exceeds a certainlimit, e¤ciency measures tend to be of similar magnitudes (see Fig. 3(b)).These ¢ndings are in line with banking industry results in other countries.Thus, high technical e¤ciency scores are also reported by Aly et al. (1990),Ferrier and Lovell (1990) and Elyasiani and Mehdian (1995) for samplesof US commercial banks, Vivas-Lozano (1998) for the Spanish bankingindustry, and Favero and Papi (1995) for Italian banks.

These results imply that if a bank were to use its inputs as technicallye¤ciently as possible, it could reduce its production cost by roughly 6^20per cent depending on its size. For larger banks the cost reduction wouldbe close to 20 per cent. The average small bank is also as e¤cient as largerbanks (although the variation in technical e¤ciency within the set of smallbanks is substantialösee Fig. 3). These estimates indicate that there issubstantial room for improvement for both small and large bankinginstitutions in Greece. Greece's accession to the Euro-zone and the re-structuring of the European banking system make it imperative for Greekcommercial banks to drastically reduce their costs and become morecompetitive in the European environment. Primary candidates for costreductions include ine¤ciencies of the technical and allocative variety,since currently the combined e¡ect of economic ine¤ciencies averages 35per cent of total costs.

7.2 Temporal Behaviour of Economic E¤ciency

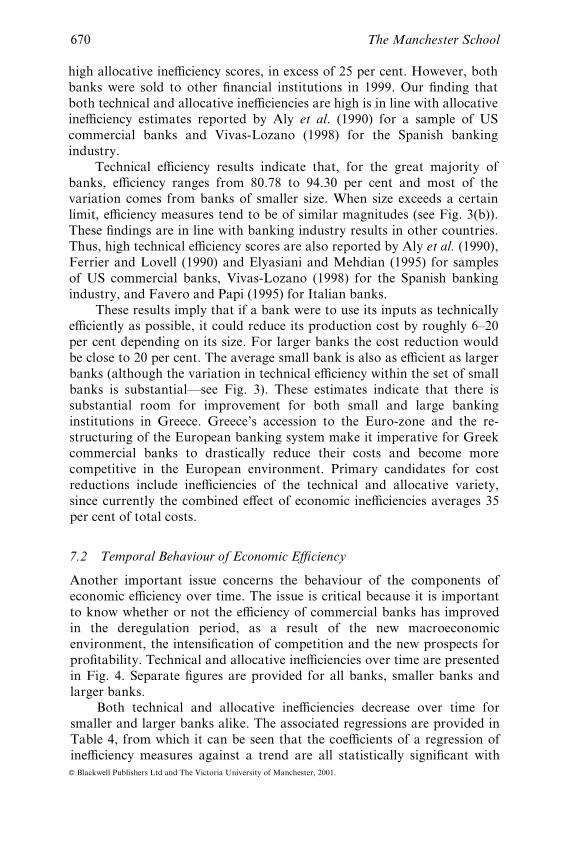

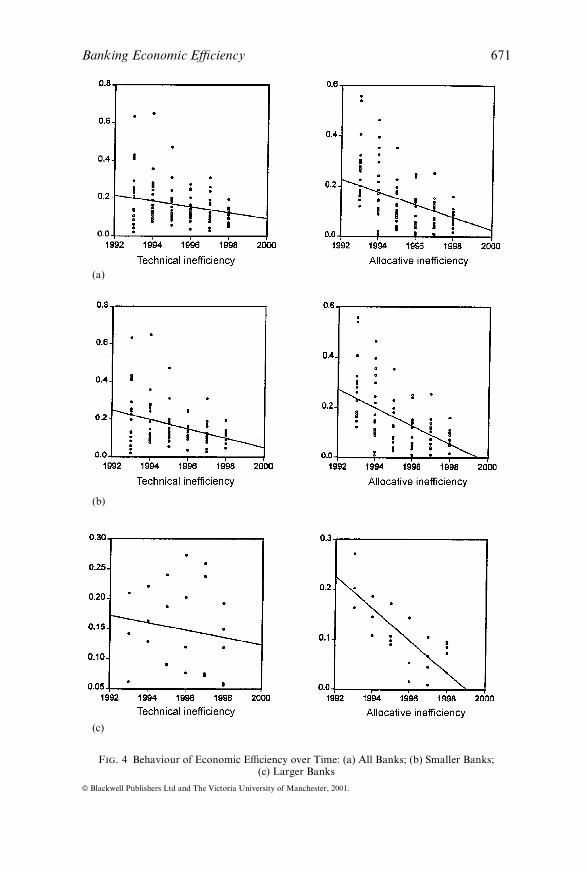

Another important issue concerns the behaviour of the components ofeconomic e¤ciency over time. The issue is critical because it is importantto know whether or not the e¤ciency of commercial banks has improvedin the deregulation period, as a result of the new macroeconomicenvironment, the intensi¢cation of competition and the new prospects forpro¢tability. Technical and allocative ine¤ciencies over time are presentedin Fig. 4. Separate ¢gures are provided for all banks, smaller banks andlarger banks.

Both technical and allocative ine¤ciencies decrease over time forsmaller and larger banks alike. The associated regressions are provided inTable 4, from which it can be seen that the coe¤cients of a regression ofine¤ciency measures against a trend are all statistically signi¢cant with

670 The Manchester School

ß Blackwell Publishers Ltd and The Victoria University of Manchester, 2001.

(a)

(b)

(c)

Fig. 4 Behaviour of Economic E¤ciency over Time: (a) All Banks; (b) Smaller Banks;(c) Larger Banks

Banking Economic E¤ciency 671

ß Blackwell Publishers Ltd and The Victoria University of Manchester, 2001.

the exception of technical ine¤ciency for smaller banks. However, aWhite's correction of standard errors gave a highly signi¢cant coe¤cientin this case as well. Therefore, for smaller banks we see an improvement intechnical ine¤ciency as well as in allocative ine¤ciencyöwhich is ratherremarkable (39.1 per cent per annum). For larger banks, technicaline¤ciency improves by 10.4 per cent and allocative ine¤ciency improvesat the rate of 21.1 per cent per annum. For smaller banks this would implya vanishing of allocative ine¤ciency within 2.5 years. For larger banks thiswould imply a vanishing of both types of ine¤ciency during the de-regulation period. Although these predictions are highly optimistic they doimply something important, namely that economic e¤ciency of both largerand smaller banks has improved dramatically during the deregulationperiod.

The improvement of allocative ine¤ciency is due to the restructuringof bank portfolios that took place as a result of removals of variousconstraints regarding bank positions in the market for government bonds.For all commercial banks, this made funds available which were invested inpro¢t-maximizing activities. To put things di¡erently, commercial banksfound themselves in a position to manage better their deposit accountsyielding a drastic reduction in costs. On the other hand, technical change inthe banking sector (credit cards, ATMs etc.) has been mostly associatedwith larger banks while the bene¢ts of technical change are greater forlarger banks. This is the dominant reason why the technical e¤ciency ofsmaller banks has not improved drastically in the deregulation period.

ð Concluding Remarks

In this study we have estimated the economic e¤ciency of the Greekbanking system using a sample of commercial banks over the deregulationperiod 1993^98. We ¢nd that heteroscedasticity is an important factor inthe determination of technical and allocative e¤ciency, and that grossbiases arise when heteroscedasticity is not accounted for in the estimationof bank-speci¢c e¤ciency measures.

Table ãEfficiency Regressions

Smaller banks Larger banks

log�TI� log�AI� log�TI� log�AI�Constant 392.21 (1.76) 779.3 (3.73) 205.1 (3.54) 419.4 (3.88)Trend ÿ0.197 (1.76) ÿ0.391 (3.71) ÿ0.104 (3.57) ÿ0.211 (3.90)R2 0.115 0.368 0.133 0.155

Notes: TI stands for technical ine¤ciency and AI for allocative ine¤ciency. Absolute values of t statisticsappear in parentheses.

672 The Manchester School

ß Blackwell Publishers Ltd and The Victoria University of Manchester, 2001.

For the great majority of the banks technical e¤ciency ranges from80 to 94 per cent while average allocative ine¤ciency is about 14 per cent.E¤ciency measures show some variability within smaller banks but aresimilar for larger banks. It appears that over the deregulation periodGreek banks enjoyed fairly low cost e¤ciency. The intensi¢cation of cross-country competition from the rapidly changing international environmentwill put pressures on bank pro¢tability forcing them to improve ine¤ciency even further. Our estimates suggest that there is plenty of roomfor improvement since for the larger banks total economic ine¤ciency israther high.

Over the second half of the 1990s, Greek banks started to reconsidertheir strategies and extensive restructuring in terms of mergers andacquisitions took place, in view of Greece entering the Euro-zone in 2001.As a result the average bank size increased considerably, although it stillremains low compared to the EU average. The observed mergers andacquisitions may be attributed to two main factors. The ¢rst is related to awave of privatization initiated by direct government action, in line withEU agreements. The second factor directing acquisitions has been marketdiscipline, i.e. to obtain cost and e¤ciency gains, and they took place inthe sector of smaller banks. The expected cost reduction impact of thisrestructuring of the Greek banking system will occur in the future.12

Since larger banks are as e¤cient as the small ones on average, it ispuzzling to ¢nd them engaged in mergers and acquisitions as buyers.However, Resti (1998) who analysed 67 bank mergers in Italy obtained thesame result. To explain this result, it should be noted that di¡erences ine¤ciency constitute the most important pre-merger cost incentive foracquiring another bank. According to Berger and Humphrey (1992) if theacquiring bank is more cost e¤cient than the acquired bank, there is anincentive for merger, since transferring management skills to the acquiredbank can create additional pro¢t. Indeed, the crucial phrase is `onaverage'. Since there is greater variability of e¤ciency measures withinsmaller banks and some of them are less e¤cient compared to largerbanks, it follows that they constitute prime candidates for acquisition. Forwhat we consider less e¤cient small banks according to our empiricalresults, recent historical experience justi¢es this statement.

Moreover, we ¢nd that technical and allocative ine¤ciencies dropdrastically during the deregulation period. For larger and smaller banksalike we ¢nd a strong negative trend for both components of e¤ciency.This is due to the nature of deregulation which gave commercial banks the

12Note that most o¤cials of banks involved are expecting substantial cost reductions by2000. For example, Eurobank o¤cials estimate that the uni¢cation with the acquiredbanks will lead to a cost reduction of the order of 10 per cent of total assets (To Vima,1999).

Banking Economic E¤ciency 673

ß Blackwell Publishers Ltd and The Victoria University of Manchester, 2001.

opportunity to withdraw funds from obligatory purchase of governmentbonds and restructure their portfolios in order to engage in pro¢t-maximizing activities. On the other hand technical progress in the form ofthe introduction of credit cards and ATMs as well as the awareness ofbank managers that they have to compete in the new Europeanenvironment contributed to sizable improvements in technical e¤ciency.

In the years to come a new round of mergers, acquisitions, con-glomeration and strategic alliances is expected in the Greek bankingmarket (`mega' mergers by Greek standards).13 Our ¢nding that technicaline¤ciency in banks of smaller size is persistent, making them primecandidates for further mergers and acquisitions, reinforces this.

Greek banks will be aiming at repositioning in the European MonetaryUnion markets and achieving the necessary large-scale operations (i.e. thecritical mass) with regard to break-even volumes. Incentives for large-scaleoperations arise from the increasing necessity to share the high informationtechnology development costs in order to reap economies of scale, sincethere are economies of scale in automated processes as opposed to paper-based and labour-intensive methods. Another incentive is the ¢nding of thispaper that economic ine¤ciency in Greek banking averages 35 per cent oftotal costs for larger commercial banks.

De¢nitely, it is not ruled out for smaller Greek banks to exploitmarket segments (within the EU) or to provide services to local or regionalclients (e.g. in the Balkans), but they will be less able to achieve a moree¤cient use of resources owing to their small size of business.

References

Aly, H. Y., Grabowski, R., Pasurka, C. and Rangan, N. (1990). `Technical Scaleand Allocative E¤ciencies in US Banking: an Empirical Investigation', Reviewof Economics and Statistics, May, pp. 211^218.

Atkinson, E. S. and Cornwell, C. (1994). `Parametric Estimation of Technical andAllocative Ine¤ciency with Panel Data', International Economic Review,Vol. 35, No. 10, pp. 231^243.

Bauer, P. W. (1990). `Recent Developments in the Econometric Estimation ofFrontiers', Journal of Econometrics, Vol. 46, No. 1^2, pp. 39^56.

Berger, A. N. and Humphrey, D. B. (1991). `The Dominance of Ine¤ciencies overScale and Product Mix Economies in Banking', Journal of MonetaryEconomics, Vol. 28, No. 1, pp. 117^148.

Berger, N. A. and Humphrey, D. B. (1992). `Megamergers in Banking and theUse of Cost E¤ciency as an Antitrust Device', Antitrust Bulletin, Vol. 37,No. 1, pp. 541^600.

13Indicative of future developments and prospects in the Greek banking system is the recentcooperation agreement between the largest private bank, the largest state-controlledbank and the national telecommunications organization in an e¡ort to use e¡ectively themost up-to-date information technology.

674 The Manchester School

ß Blackwell Publishers Ltd and The Victoria University of Manchester, 2001.

Berndt, E. R., Hall, B. H., Hall, R. E. and Hausman, J. A. (1974). `Estimationand Inference in Non-linear Structure Models', Annals of Economic and SocialMeasurement, Vol. 4, No. 1, pp. 653^665.

Caudill, S. B. and Ford, J. M. (1993). `Biases in Frontier Estimation due toHeteroscedasticity', Economics Letters, Vol. 41, No. 1, pp. 17^20.

Caudill, S. B., Ford, J. M. and Gropper, D. M. (1995). `Frontier Estimationand Firm-speci¢c Ine¤ciency Measures in the Presence of Hetero-scedasticity', Journal of Business and Economic Statistics, Vol. 13, pp.105^111.

Elyasiani, E. and Mehdian, S. (1995). `The Comparative E¤ciency Performanceof Small and Large US Commercial Banks in the Pre and Post DeregulationEras', Applied Economics, Vol. 27, No. 11, pp. 1069^1079.

Favero, C. A. and Papi, L. (1995). `Technical E¤ciency and Scale E¤ciency inthe Italian Banking Sector: a Non-parametric Approach', Applied Economics,Vol. 27, No. 4, pp. 385^395.

Ferrier, D. G. and Lovell, K. A. C. (1990). `Measuring Cost E¤ciency in Banking',Journal of Econometrics, Vol. 46, No. 1^2, pp. 229^245.

Greene, W. (1980). `On the Estimation of a Flexible Frontier Production Model',Journal of Econometrics, Vol. 13, No. 1, pp. 101^115.

Greene, W. H. (1993). `The Econometric Approach to E¤ciency Analysis', inH. O. Fried, C. A. K. Lovell and S. S. Schmidt (eds), The Measurement ofProductive E¤ciency: Techniques and Applications, Oxford, Oxford UniversityPress.

Hadri, K. (1999). `Estimation of a Doubly Heteroscedastic Stochastic FrontierCost Function', Journal of Business and Economic Statistics, Vol. 17, No. 3,pp. 359^363.

Hondroyiannis, G., Lolos, S. E. and Papapetrou, E. (1998). `Market Structureand Performance in the Greek Banking System', in J. J. Choi and J. A.Doukas (eds), Emerging Capital Markets: Financial and Investment Issues,London, Quorum Books, pp. 179^191.

Hondroyiannis, G., Lolos, S. E. and Papapetrou, E. (1999). `Assessing CompetitiveConditions in the Greek Banking System', Journal of International FinancialMarkets, Institutions and Money, Vol. 9, No. 1, pp. 377^391.

Jondrow, J., Lovell, C. A. K., Materov, I. and Schmidt, P. (1982). `On theEstimation of Technical Ine¤ciency in the Stochastic Frontier ProductionModel', Journal of Econometrics, Vol. 19, No. 2^3, pp. 233^238.

Kalirajan, K. (1990). `On Measuring Economic E¤ciency', Journal of AppliedEconometrics, Vol. 5, No. 1, pp. 75^86.

Karafolas, S. (1997). `Le Credit Cooperatif en Grece', Revue des EtudesCooperatives Mutualistes et Associatives, No. 264, pp. 38^74.

Karafolas, S. and Mantakas, G. (1996). `A Note on Cost Structure and Economiesof Scale in Greek Banking', Journal of Banking and Finance, Vol. 20, No. 2,pp. 377^387.

Kopp, R. and Diewert, W. (1982). `The Decomposition of Frontier Cost FunctionDeviations into Measures of Technical and Allocative E¤ciency', Journal ofEconometrics, Vol. 19, No. 2^3, pp. 319^332.

Kumbhakar, S. (1987). `The Speci¢cation of Technical and Allocative Ine¤ciencyin Stochastic Production and Pro¢t Functions', Journal of Econometrics,Vol. 34, No. 1, pp. 335^348.

Kumbhakar, S. (1989). `Modeling Technical and Allocative Ine¤ciency inTranslog Production Functions', Economics Letters, Vol. 31, pp. 119^124.

Banking Economic E¤ciency 675

ß Blackwell Publishers Ltd and The Victoria University of Manchester, 2001.

Mensah, Y. M. (1994). `A Simpli¢cation of the Kopp^Diewert Method ofDecomposing Cost E¤ciency and Some Implications', Journal of Econometrics,Vol. 60, No. 1^2, pp. 133^144.

Noulas, A. (1997). `Productivity Growth in the Greek Banking Industry: Stateversus Private Banks', Applied Financial Economics, Vol. 7, No. 3, pp.223^228.

Resti, A. (1998). `Regulation Can Foster Mergers. Can Mergers Foster E¤ciency?The Italian Case', Journal of Economics and Business, Vol. 50, No. 2, pp.157^169.

Schmidt, P. and Lovell, C. A. K. (1979). `Estimating Technical and AllocativeIne¤ciency Relative to Stochastic Production and Cost Frontiers', Journal ofEconometrics, Vol. 9, No. 3, pp. 343^366.

Schmidt, P. and Lovell, C. A. K. (1980). `Estimating Stochastic Production andCost Frontiers when Technical and Allocative Ine¤ciency are Correlated',Journal of Econometrics, Vol. 13, No. 1, pp. 83^100.

Seale, J. (1990). `Estimating Stochastic Frontier Systems with Unbalanced PanelData: the Case of Floor Tile Manufactures in Egypt', Journal of AppliedEconometrics, Vol. 5, No. 1, pp. 59^74.

Tsionas, E. G. (2000). `P-STAR Analysis in a Converging Economy: the Case ofGreece', Economic Modeling, Vol. 18, No. 2, pp. 46^60.

Vivas-Lozano, A. (1998). `E¤ciency and Technical Change for Spanish Banks',Applied Financial Economics, Vol. 8, No. 3, pp. 289^300.

Zeischang, K. (1983). `A Note on the Decomposition of Cost E¤ciency intoTechnical and Allocative Components', Journal of Econometrics, Vol. 23,No. 1, pp. 401^405.

676 The Manchester School

ß Blackwell Publishers Ltd and The Victoria University of Manchester, 2001.

Related Documents