Bankability in Highway PPP Projects

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Bankability in Highway PPP Projects

Contents

1. Overview of PPIAF

2. Understanding bankability

3. The lender’s perspective – understanding project finance and credit risk – Mitigating credit risk through the borrower

– Mitigating credit risk through the government

– Mitigating credit risk through the supply chain

4. A worked example: Sheffield Highways Maintenance PFI

5. Recommendations for India

Overview of PPIAF Mission and Strategy

Who are we?

4

Vision: To be the center of excellence in enabling the public sector to attract private sector participation and investment in infrastructure by supporting institution development, building capacity and accelerating PPP programs at a regional, national and sub-national level.

Mission: To help eliminate poverty and achieve sustainable development in developing countries by facilitating private sector involvement in infrastructure

PPIAF Mission and Strategy

3 Year Strategy and Business Plan – FY15-17

http://www.ppiaf.org/sites/ppiaf.org/files/documents/PPIAF_Strategy_Final.pdf http://www.ppiaf.org/sites/ppiaf.org/files/documents/PPIAF_3yrBusinessPlan_Final.pdf

Understanding Bankability

Understanding Bankability

• Bankability is a narrow concept that is widely misrepresented and misunderstood and widely confused with value for money (vfm)

• Bankability narrowly is really just a ‘state’ where a project is sufficiently attractive to raise private finance

• However – bankability is not a zero sum game – just because a project is attractive to private financiers does not mean that it is necessarily optimal (or value for money) for the government

• We can define vfm as when there is confluence between bankability, risk transfer and affordability…see the important venn diagram overleaf!

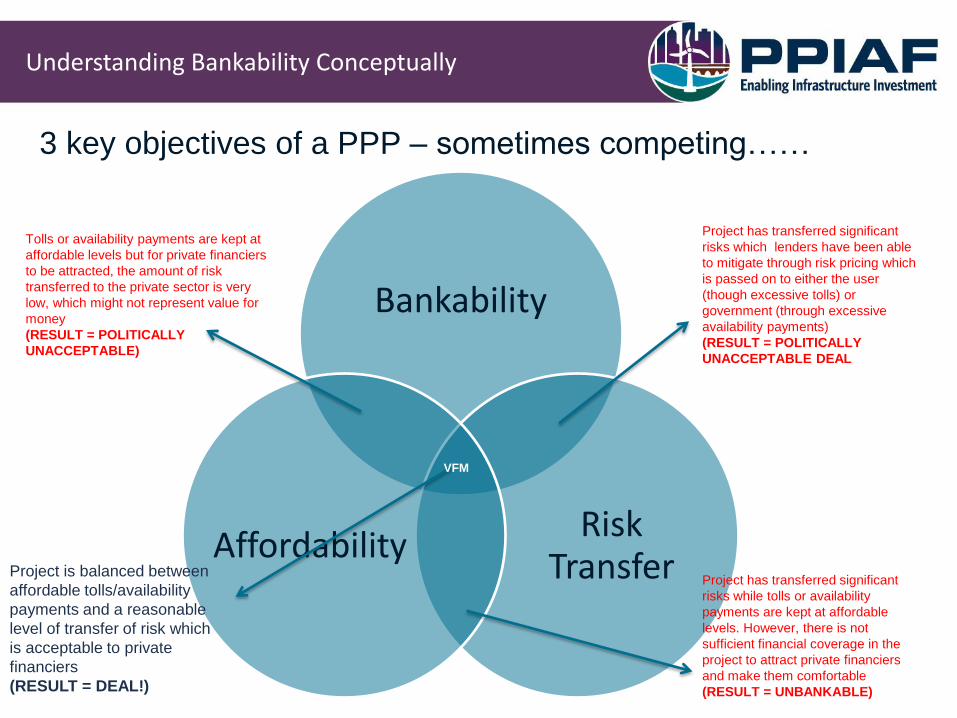

VFM

Understanding Bankability Conceptually

Bankability

Risk Transfer

Affordability

Project has transferred significant

risks which lenders have been able

to mitigate through risk pricing which

is passed on to either the user

(though excessive tolls) or

government (through excessive

availability payments)

(RESULT = POLITICALLY

UNACCEPTABLE DEAL

Project has transferred significant

risks while tolls or availability

payments are kept at affordable

levels. However, there is not

sufficient financial coverage in the

project to attract private financiers

and make them comfortable

(RESULT = UNBANKABLE)

Tolls or availability payments are kept at

affordable levels but for private financiers

to be attracted, the amount of risk

transferred to the private sector is very

low, which might not represent value for

money

(RESULT = POLITICALLY

UNACCEPTABLE)

Project is balanced between

affordable tolls/availability

payments and a reasonable

level of transfer of risk which

is acceptable to private

financiers

(RESULT = DEAL!)

VFM

3 key objectives of a PPP – sometimes competing……

Understanding Bankability (3)

• So bankability should not be seen in isolation by governments – PPPs should not (obviously) attract private finance at all costs!

• Instead, governments have to prepare robust projects that ensure key project risks are transferred to the private sector party but not fully at the expense of undermining the interest of financiers and/or burdening users or government with excessive fees/cost

• But how will a lender eventually get to this point where it is happy with the project’s fundamentals and happy to participate?

• To understand this requires us to delve into some of the fundamentals of asset-based lending (so-called project finance)

The Lender’s Perspective – Understanding Project Finance and

Credit Risk

The Lenders Perspective

• PPPs are typically funded through a certain type of lending called project finance:

• What is project finance? - Non recourse: only recourse is to the contract or project asset and therefore the cashflow

it creates– not the balance sheet of the borrower - Lending against (mostly known) project risks and not a range of corporate risks (e.g.

bankruptcy) - Limited room for manoeuvre for management – not a credit line

• Why project finance? - The projects are of such scale that the liabilities may be too large for a borrower to provide

a credit line for/not enough balance sheet capacity – too capital intensive - Not the borrower’s asset in the first place – it is conceded so the borrower does not

typically provide the security directly - Its clean. Lenders do not necessarily want to be exposed to the various risks of a

corporate’s balance sheet – this is why you have Project Companys (with big management restrictions) and allows a project to be geared up

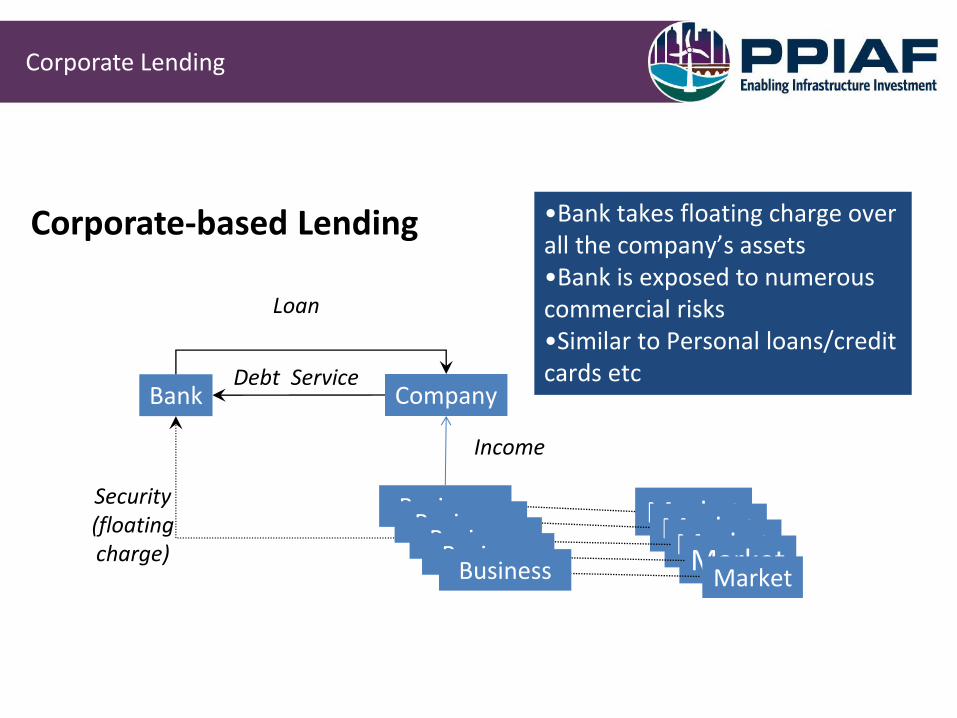

Corporate Lending

Corporate-based Lending •Bank takes floating charge over all the company’s assets •Bank is exposed to numerous commercial risks •Similar to Personal loans/credit cards etc

Bank Company

Loan

Market

Debt Service

Market Market Market

Market

Business Business

Business Business

Business

Income

Security (floating charge)

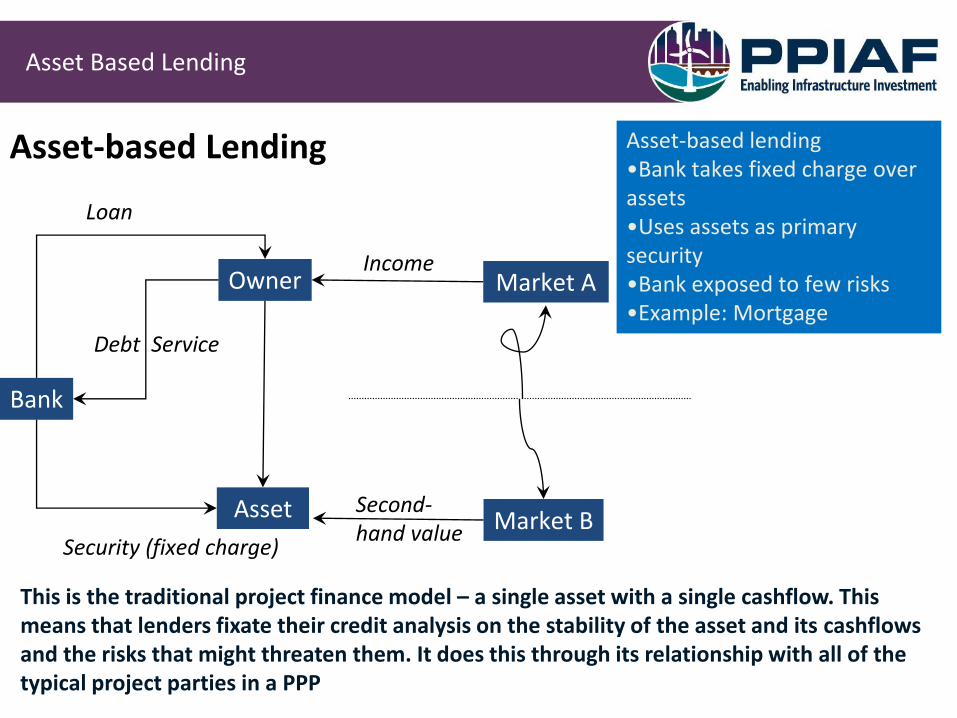

Asset-based Lending

Asset

Bank

Owner

Loan

Security (fixed charge)

Market A Income

Market B Second- hand value

Debt Service

Asset-based lending •Bank takes fixed charge over assets •Uses assets as primary security •Bank exposed to few risks •Example: Mortgage

Asset Based Lending

This is the traditional project finance model – a single asset with a single cashflow. This means that lenders fixate their credit analysis on the stability of the asset and its cashflows and the risks that might threaten them. It does this through its relationship with all of the typical project parties in a PPP

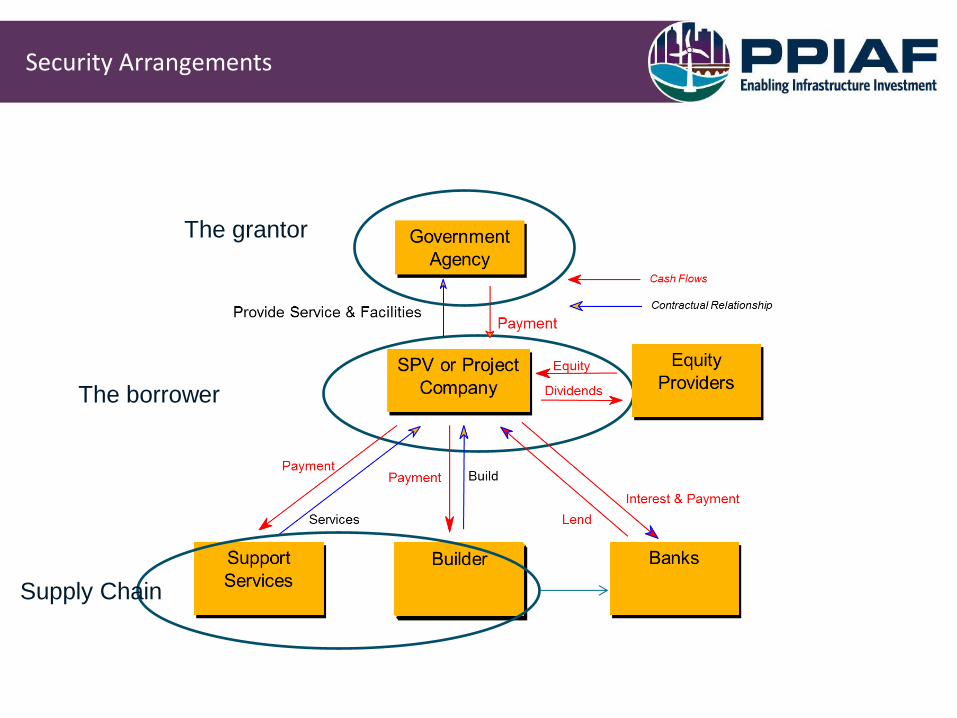

Security Arrangements

The grantor

The borrower

Supply Chain

Mitigating credit risk through the borrower

Mitigating Credit Risk through the Borrower

• In a typical project financing, the borrower is a special company with one asset – the project. To ensure risk protection the loan is riddled with obligations – so called debt covenants. Key covenants include:

• Gearing restrictions

• Debt service coverage ratios

• Reserve accounts (e.g. DSRA, MRA, CILA)

• Hedging against key risks (e.g. interest rate swaps, inflation swaps)

• Insurance

The imposition of each of the above either increases the cost of finance or it simply reduces the viability of a project by reducing potential equity returns

Mitigating Credit Risk through the Borrower

Typical Project Cashflows

25 years

Revenue

Cash to Equity

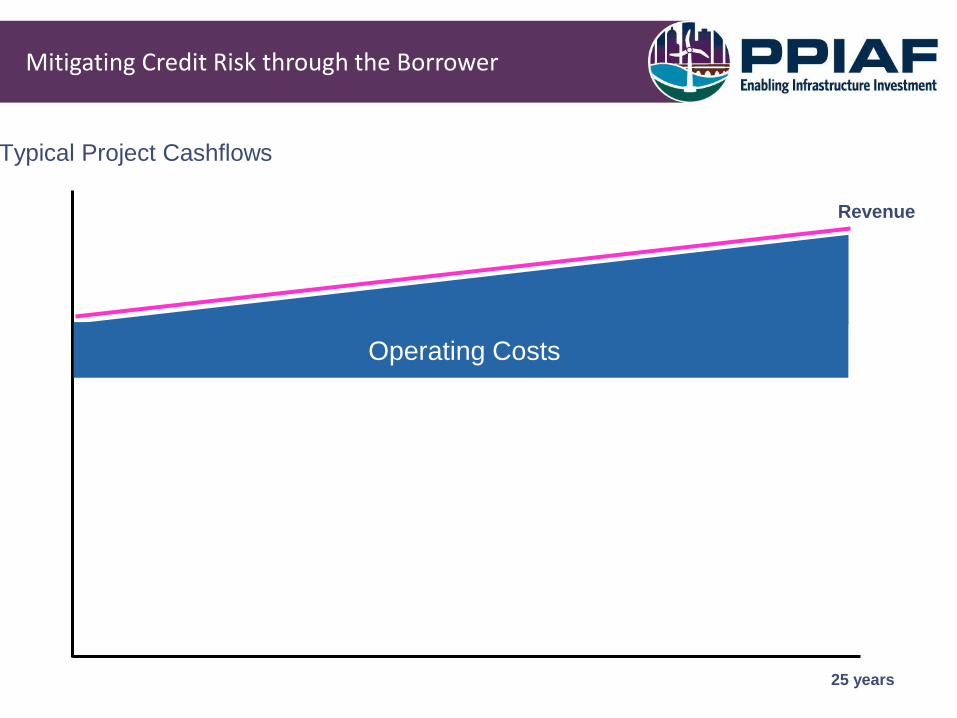

Mitigating Credit Risk through the Borrower

Typical Project Cashflows

25 years

Revenue

Operating Costs

Cash to Equity

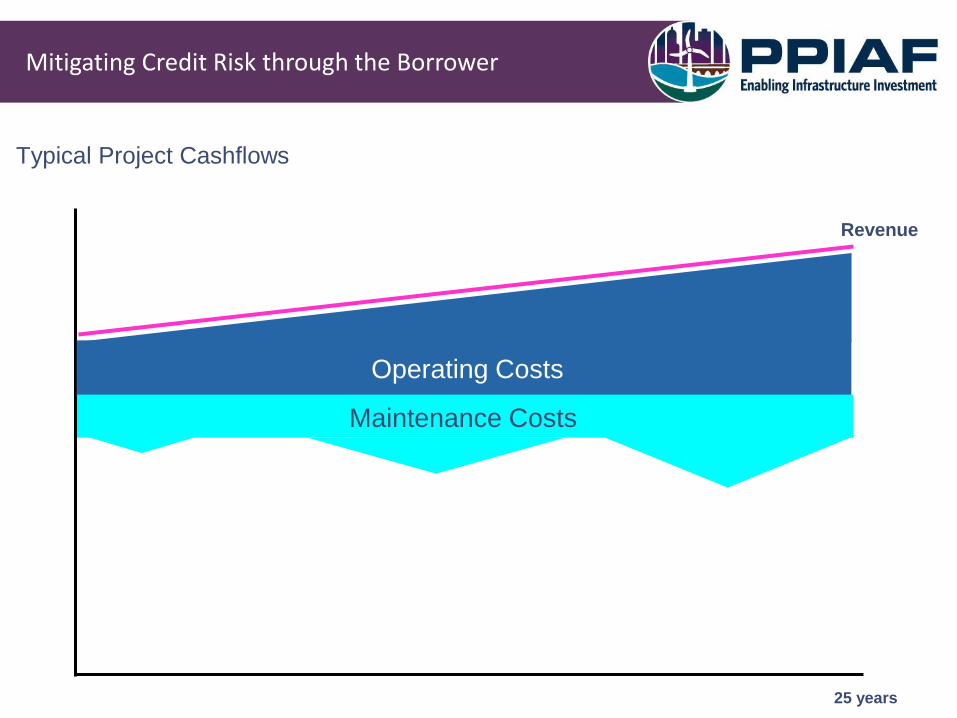

Mitigating Credit Risk through the Borrower

Typical Project Cashflows

25 years

Revenue

Operating Costs

Maintenance Costs

Cash to Equity

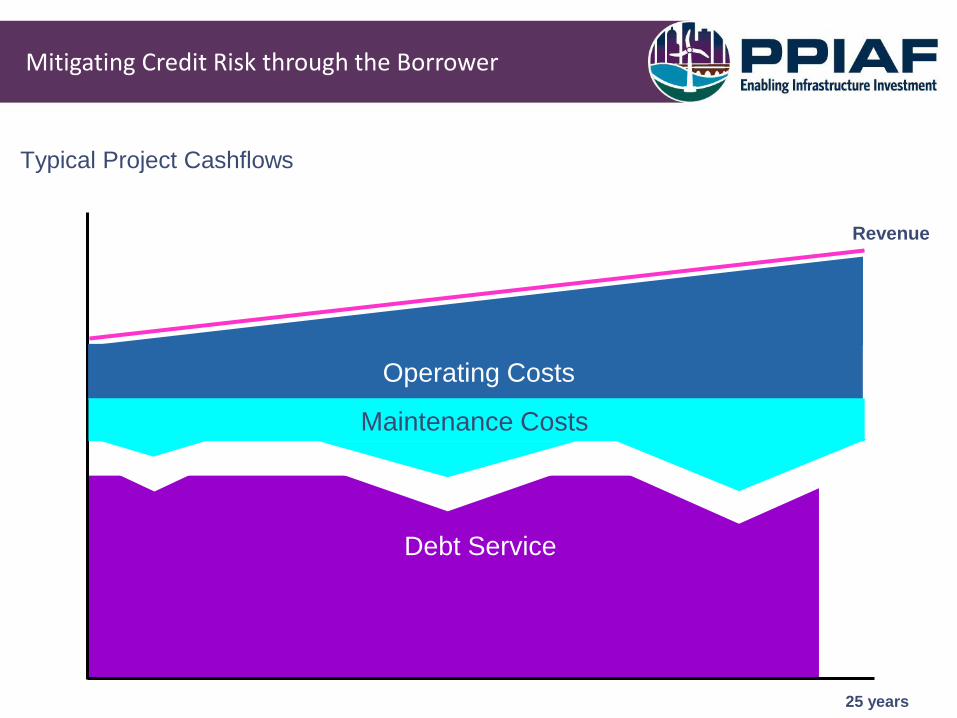

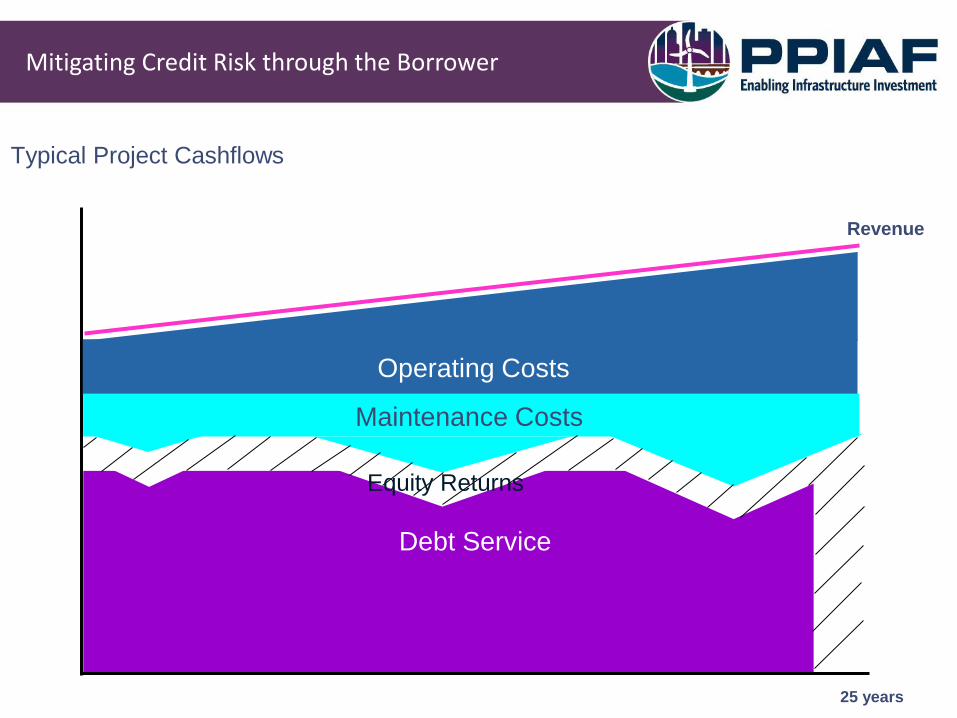

Mitigating Credit Risk through the Borrower

Typical Project Cashflows

Debt Service

25 years

Revenue

Operating Costs

Maintenance Costs

Cash to Equity

Mitigating Credit Risk through the Borrower

Typical Project Cashflows

Debt Service

25 years

Revenue

Operating Costs

Maintenance Costs

Cash to Equity

Equity Returns

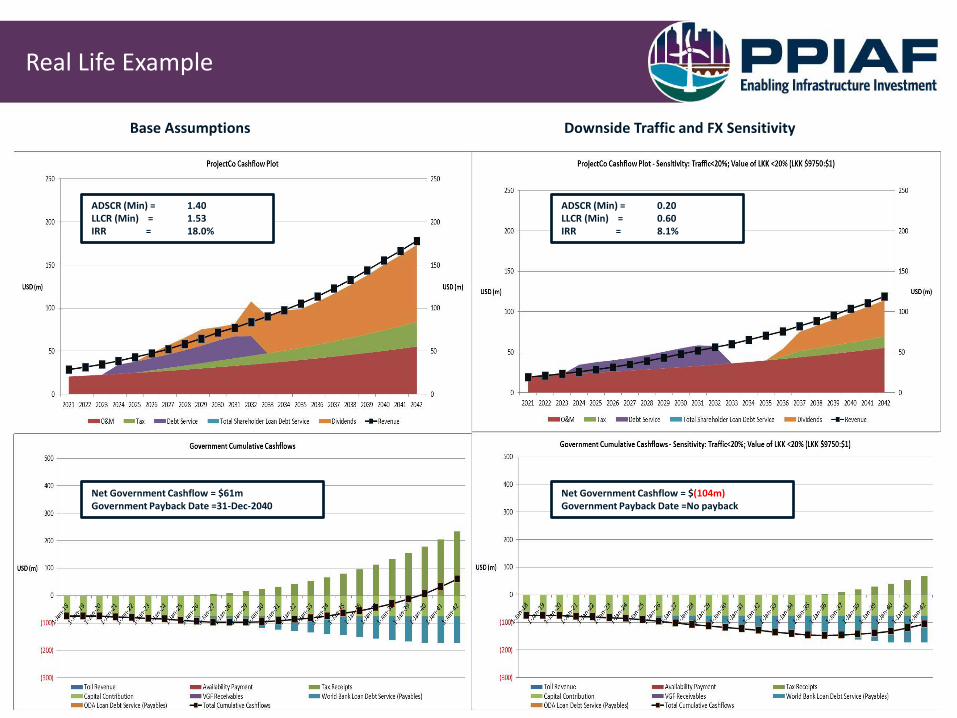

Real Life Example

ADSCR (Min) = 0.20 LLCR (Min) = 0.60 IRR = 8.1%

Net Government Cashflow = $(104m) Government Payback Date =No payback

ADSCR (Min) = 1.40 LLCR (Min) = 1.53 IRR = 18.0%

Net Government Cashflow = $61m Government Payback Date =31-Dec-2040

Base Assumptions Downside Traffic and FX Sensitivity

Covenants in the current financial market

• Since the financial crisis – debt covenants have become increasingly more severe

• Limited liquidity and damage to bank balance sheets has led to: – Heightened credit risk perception

– Market-making rather than market-taking – lending is on their terms

• The security requirements over the borrower are real – they increase cost of capital here and now. This increased cost of capital is passed on to either or all of the following parties: – Government – may need to pay increased subsidies to safeguard equity

returns

– Users – may need to pay higher tariffs/tolls to safeguard equity

– Equity – themselves may have to take a hit on their project returns

Mitigating credit risk through the government

The Role of the Project Agreement

• Lenders also seek protection through the contract between the Project Company (borrower) and the government

• These protections are effectively the lenders ‘red-lines’ which afford the lender adequate protection from actions of both the government and the Project Company (borrower)

• Unlike debt covenants – these commercial ‘red-lines’ do not have such a direct impact on project cost but can significantly increase contingent liabilities for the government

• Since financial crisis – these requirements have become more strict and reduces the value for money of PPPs to government

Typical Lender ‘Red Lines’ in Project Agreements

• Step-in rights: Prior to terminating the contract of the Project Company – the lender has the right to replace the Project Company or operate the asset themselves and collect the cashflow

• Compensation-on-termination: Lenders increasingly require compensation if the contract is finally terminated. This allows some recovery of outstanding debt and exists as an incentive to stop ‘hair-trigger’ termination

• Compensation Events: Lenders will not accept certain risks being transferred to the Project Company. Thus compensation is contractually stipulated in certain events – (e.g. acts-of-god, change in law, delay caused by government)

• Guarantees: Lenders may require certain guarantees on project revenue and other risks (e.g. political risks such as nationalization)

• Collateral: Lenders may also require “real” security in the event of termination of the Project Company. This is often security over the project land which has a re-sale market value

Mitigating credit risk through the supply chain

Supply Chain Security Packages

• Typical structures pass key project risks (e.g. construction risk and operating risks) to sub-contractors on a ‘back-to-back’ basis

• Lenders need to be sure that these sub-contractors can absorb these risks because if they crystallize then failure to keep the Project Company whole will financially damage the Project Company and affect its ability to service senior debt

• As such senior lenders typically require a range of financial and promissory guarantees that the sub-contractor will keep the Project Company whole – these include:

– Liquidated Damages – a contractual promise to pay specified damages in certain events (e.g. construction delay)

– Performance Bond – a liquid security that can be called by lenders on certain events (e.g. constructions)

– Parent Company Guarantees – a promissory that the parent company of the sub-contractor will ‘wrap’ some of the obligations of the sub-contractor

– Letters of credit – a further ‘liquid’ wrap normally secured against the balance sheet of the parent company to guarantee the sub-contractor’s obligations

A Worked Example: Sheffield Highways PFI (UK)

Worked Example: Sheffield Highways PFI (UK)

Worked Example: Sheffield Highways PFI

The 25-year maintenance PFI contract includes the renovation and repairing of the entire Sheffield city’s road network, covering 1,900km of roads including over 350 bridges, 3,300km of footway, 36,000 highway trees, 500 traffic signals, 68,000 street lights, over 18,000 items of street furniture and 12,700 street name plates. The contract will also include services such as street cleaning, winter gritting and landscape maintenance. Refurbishment and repairs will be carried out in the first five years and maintenance in the remaining 20 years.

Worked Example – Lenders Perspective

• UK had a long history of ‘greenfield’ highway PPP projects which had been consistently banked (e.g. A1/M1, M6 Toll, M80 etc)

• There had not been a history of ‘brownfield’ renovation and maintain projects – these projects were asking the private sector and its financiers to take a series of long-term risks for which they had not previously been so exposed (e.g. long-term condition of existing assets – so called latent defects)

• The private sector partner (Project Company) would be paid an availability payment/annuity over 25 years for keeping a network of city-wide road assets up to an agreed condition standard

• Sheffield City Council was also launching the project in difficult financial market conditions – many senior lenders had left the UK/PFI project finance market, liquidity and credit conditions were tight

• Financial close was reached in 2012 with Amey Ventures (large European contractor) appointed as the sponsor.

• How did the ‘club’ of senior lenders (Lloyds, NordLB, KfW, SMBC) reach a point where they were satisfied with the risks and could commit lending?

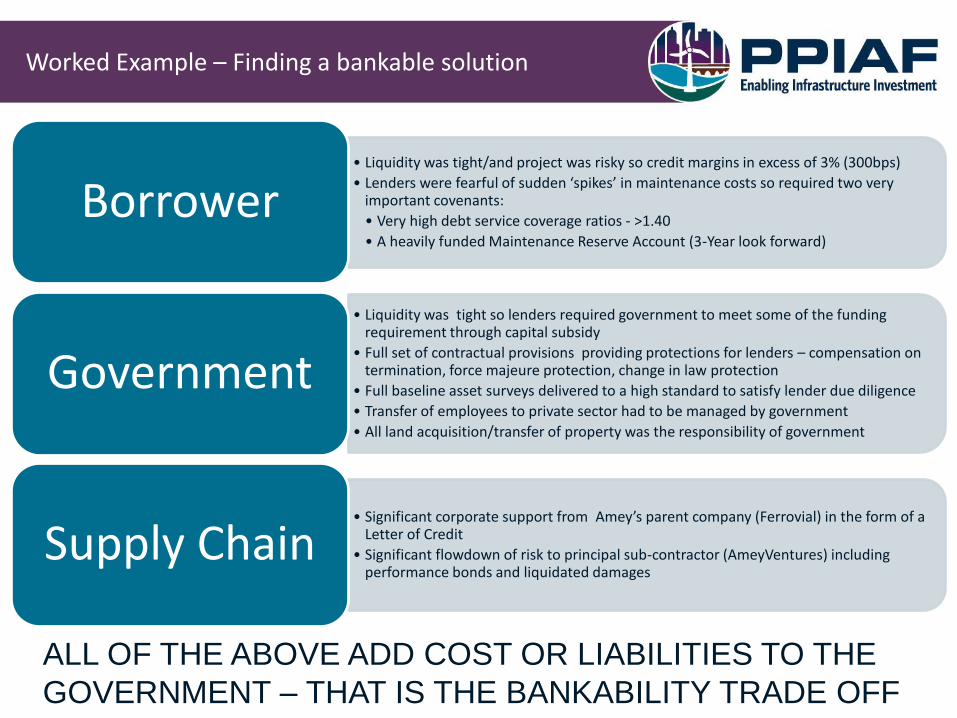

Worked Example – Finding a bankable solution

• Liquidity was tight/and project was risky so credit margins in excess of 3% (300bps)

• Lenders were fearful of sudden ‘spikes’ in maintenance costs so required two very important covenants:

• Very high debt service coverage ratios - >1.40

• A heavily funded Maintenance Reserve Account (3-Year look forward)

Borrower

• Liquidity was tight so lenders required government to meet some of the funding requirement through capital subsidy

• Full set of contractual provisions providing protections for lenders – compensation on termination, force majeure protection, change in law protection

• Full baseline asset surveys delivered to a high standard to satisfy lender due diligence

• Transfer of employees to private sector had to be managed by government

• All land acquisition/transfer of property was the responsibility of government

Government

• Significant corporate support from Amey’s parent company (Ferrovial) in the form of a Letter of Credit

• Significant flowdown of risk to principal sub-contractor (AmeyVentures) including performance bonds and liquidated damages

Supply Chain

ALL OF THE ABOVE ADD COST OR LIABILITIES TO THE

GOVERNMENT – THAT IS THE BANKABILITY TRADE OFF

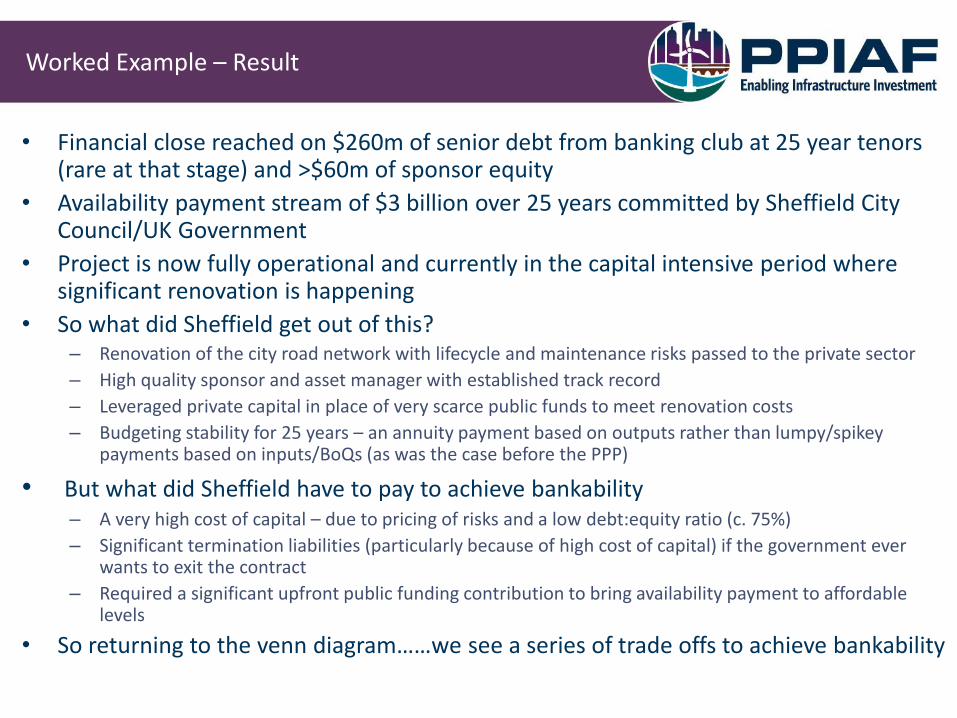

Worked Example – Result

• Financial close reached on $260m of senior debt from banking club at 25 year tenors (rare at that stage) and >$60m of sponsor equity

• Availability payment stream of $3 billion over 25 years committed by Sheffield City Council/UK Government

• Project is now fully operational and currently in the capital intensive period where significant renovation is happening

• So what did Sheffield get out of this? – Renovation of the city road network with lifecycle and maintenance risks passed to the private sector

– High quality sponsor and asset manager with established track record

– Leveraged private capital in place of very scarce public funds to meet renovation costs

– Budgeting stability for 25 years – an annuity payment based on outputs rather than lumpy/spikey payments based on inputs/BoQs (as was the case before the PPP)

• But what did Sheffield have to pay to achieve bankability – A very high cost of capital – due to pricing of risks and a low debt:equity ratio (c. 75%)

– Significant termination liabilities (particularly because of high cost of capital) if the government ever wants to exit the contract

– Required a significant upfront public funding contribution to bring availability payment to affordable levels

• So returning to the venn diagram……we see a series of trade offs to achieve bankability

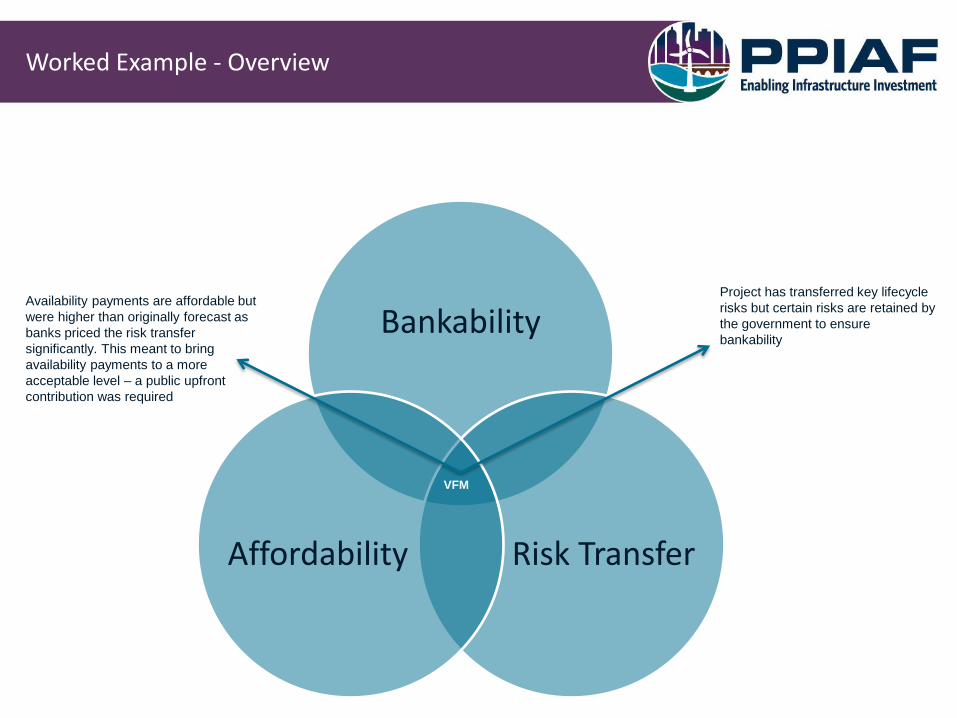

Worked Example - Overview

Bankability

Risk Transfer Affordability

Project has transferred key lifecycle

risks but certain risks are retained by

the government to ensure

bankability

VFM

Availability payments are affordable but

were higher than originally forecast as

banks priced the risk transfer

significantly. This meant to bring

availability payments to a more

acceptable level – a public upfront

contribution was required

Recommendations for India

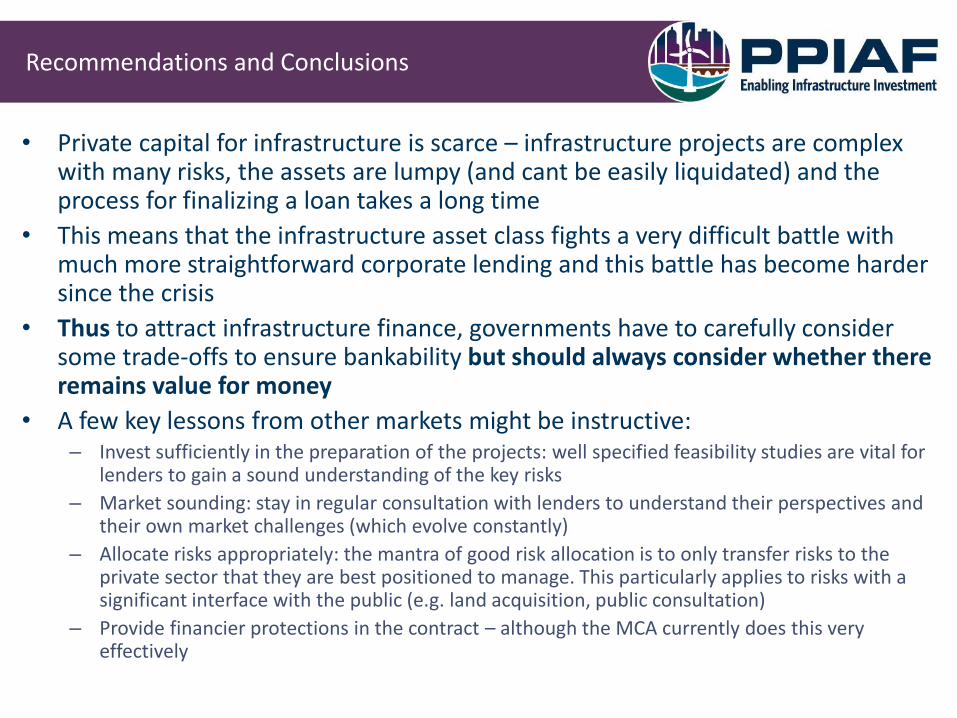

Recommendations and Conclusions

• Private capital for infrastructure is scarce – infrastructure projects are complex with many risks, the assets are lumpy (and cant be easily liquidated) and the process for finalizing a loan takes a long time

• This means that the infrastructure asset class fights a very difficult battle with much more straightforward corporate lending and this battle has become harder since the crisis

• Thus to attract infrastructure finance, governments have to carefully consider some trade-offs to ensure bankability but should always consider whether there remains value for money

• A few key lessons from other markets might be instructive: – Invest sufficiently in the preparation of the projects: well specified feasibility studies are vital for

lenders to gain a sound understanding of the key risks

– Market sounding: stay in regular consultation with lenders to understand their perspectives and their own market challenges (which evolve constantly)

– Allocate risks appropriately: the mantra of good risk allocation is to only transfer risks to the private sector that they are best positioned to manage. This particularly applies to risks with a significant interface with the public (e.g. land acquisition, public consultation)

– Provide financier protections in the contract – although the MCA currently does this very effectively

Public Private Infrastructure Advisory Facility

Contact:

Matt Bull, Senior Infrastructure Finance Specialist; [email protected]

Juliana Bedoya Carmona (PPIAF South Asia Coordinator); [email protected]

Website : www.ppiaf.org

Related Documents