Bank : We can define bank as a financial intermediary accepting deposits and granting loans ; widest menu of services of any financial institution banks.

Dec 25, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Bank : We can define bank as a financial intermediary accepting deposits and granting loans ; widest menu of services of any financial institution banks are considered the most important financial institution in the economy. Banks are the principal source of loan able funds for anyone who wants funds. Banks are replenish short-term working capital as well as long-term working capital for millions of individuals and organization. Even banks are being the leading buyers of bonds and notes issued by governments to finance the government . In this ways banks are playing a vital role in whole economy.

Services offer by banks : •Exchange of currency•Discounting commercial notes and bills •Offering savings deposits •Making Business Loans/Consumer loans•Offering Current/Checking accounts•Trust services (locker service)•Supporting government activities•Financial advising •Cash management • Offering Equipment leasing• Making ventures capital loans • Insurance services• Online Banking • Offering Mutual funds and Annuities• Merchant Banking Services and so on.

Above Services offered and the service delivery channels used by financial institution like banks, add up a great convenience for the customer. So, we can define bank as a financial department store Where a customer can get any financial services in a single place.

Islami Bank Bangladesh LimitedCorporate Profile :Is Islamic Bank Bangladesh Limited is a multinational Joint ventures public limited company engaged in commercial banking business based on Islamic shari’ah with 58% foreign share holding having largest branch network with 176 branches among the private sector banks in Bangladesh. It was in corporate as the first shariah based interest-free bank in south-east Asia on the 13th march 1983. It is listed with Dhaka stock exchange ltd. And Chittagong stock exchange ltd. Paid up capital was 3456 million number of shareholders was 20,960 and number of employees are 7,459 in 2006.

Mission : The mission of Islamic Bank Bangladesh Ltd. Is to establish Islamic banking through the introduction of a welfare oriented banking system and also ensure equity and justice in the field of all economic activities, achieve balanced growth through diversified investment operations particularity in the priority sectors and less developed area of the country .Vision : Vision of the bank is to always strive to achieve superior performance, be considered a leading Islamic by reputation and through performance. Ultimate goal of Islamic Bank Bangladesh Ltd. Is to establish and maintain modern banking techniques, to ensure the soundness and development and to become the strong and efficient organization through satisfying customers.

Special features : •All activities are conducted on interest-free system according to Islamic shariah principles.•Investment is made through different modes as per Islamic Shariah.•Aims to introduce a welfare-oriented banking system and also established and justice in the all economic operations.•Plays a vital in human resources development and employment-generation particularly among the unemployed youths.•Investment Income of the bank is shared with the mudaraba depositors according to an agreed upon ratio.

Capital: The Authorized capital of the bank is taka 5000 million and paid up capital of the bank raised 3456 million from 2768 in 2006. And way of issuing bonus share 1:4 (one bonus share for existing 4 Share. The price equation of share o the bank in the stock exchange was as taka 1000 The first Rights of Share was issued in 1989. 2nd rights of share was issued in 1996. 3rd was issued in 2000, and rights of share was issued in 2003.Deposits : 2006 was the another successful year for mobilization of deposit total deposit stood at tk. 132,419 million and deposit increased at the rate of 22.86% . The number of depositors of IBBL from 3,207,131 as on 31st December,2006 form 2,705,180 and increased rate 18.56%.S

Investment : Investment of the bank increased to tk. 113,575 million as on 31.12.2006 from 93,644 million as on the proceeding Year. Increased rate was 21.28%. The share of Investment of IBBL in banking sector as on the 31.12.2005.Investment in Industrial Sector: As per Investment policy of the Bank to priority has been given towards the Industrial sector is substantially higher compared with that of other commercial banks. Total investment for projects finance as well as of working capital stood at tk. 62,642.10 million in 2006 and growing level was 36% compare that of proceeding Year.

Foreign Exchange business: Total Foreign Exchange business handled during the year 2006 was in 2006 Tk. 201,822 million and growing rate o 37.00% compared to 31.09% in 2005. There were 38 Authorized dealer branches , branches having license to handle import and remittance business in 2006. Comparative figures of import was 48%, export was 25.34% and remittance 26.66% in 2006.

Social welfare Activities : IBBL has established the following projects and programs up to 2006. •6 modern islami bank hospitals.•6 Islami bank community hospitals•Five vocational training Institutes•Five service Centers.•Islami bank Physiotherapy and disabled rehabilitation center.•Islami bank International school and college.•Scholarship.•Islami bank Model school and College.•Bangladesh Sangskritic Kendra and so on.Islami bank is concern about social welfare and they are trying continuously to do better for the society as whole.

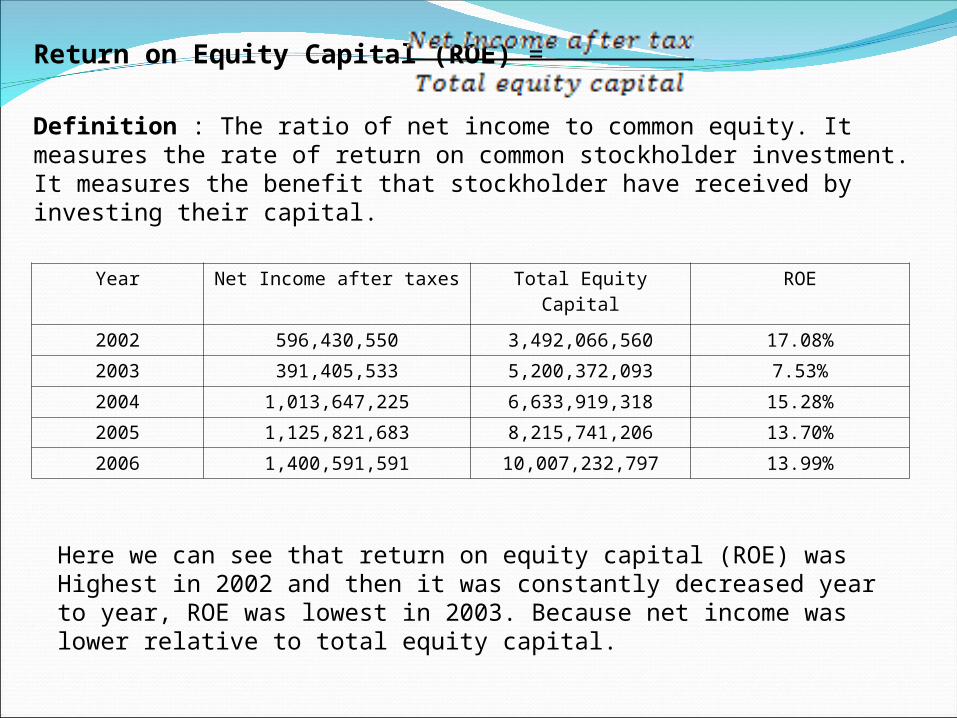

Year Net Income after taxes Total Equity Capital ROE

2002 596,430,550 3,492,066,560 17.08%

2003 391,405,533 5,200,372,093 7.53%

2004 1,013,647,225 6,633,919,318 15.28%

2005 1,125,821,683 8,215,741,206 13.70%

2006 1,400,591,591 10,007,232,797 13.99%

Return on Equity Capital (ROE) =

Definition : The ratio of net income to common equity. It measures the rate of return on common stockholder investment. It measures the benefit that stockholder have received by investing their capital.

Here we can see that return on equity capital (ROE) was Highest in 2002 and then it was constantly decreased year to year, ROE was lowest in 2003. Because net income was lower relative to total equity capital.

Year Net Income After Taxes Total Assets ROA2002 596,430,550 65,080,700,199 0.97%2003 391,405,533 81,704,745,989 0.48%2004 1,013,647,225 102,149,282,158 1.00%2005 1,125,821,683 122,880,348,222 0.92%2006 1,400,591,591 150,252,820,801 0.93%

Return on Assets (ROA) =

Definition : The ratio of net income to total asset. It measures the capacity of a bank to convert the Institute asset into the net earning . It is an indicator of management efficiency.

Here we can see that Return on Assets (ROA) was highest in 2004 with 1%. And it was decreased in 2005 and 2006. But it does not indicate that bank is under threat. Because in proportion to assets, net income was very good.

Year Net Interest Income Total Assets 2002 1,620,339,347 65,080,700,199 2.49%2003 2,210,018,117 81,704,745,989 2.70%2004 20042,848,665,832 102,149,282,158 2.8%2005 2,558,928,209 122,880,348,222 2.09%2006 3,138,721,051 150,252,820,801 2.09%

Net Interest Margin =

Definition: The ratio of the net interest income divided by a banks total asset. It measures how large a spread between interest revenues and interest costs management has been able to achieve by close control over the banks earning assets and the pursuit of cheapest source of funding.

Net interest margin was better in 2004 with 2.8%. It refers that management was able to gain funds from cheapest sources.

Year Net Non Interest Income Total Assets NNIM2002 (99724118) 65080700199 (0.15%)2003 (235511427) 81704745989 (0.29%)2004 (197116288) 102149282158 (0.19%)2005 309936725 122880348222 0.25%2006 176576037 150252820801 0.12%

Net Non Interest Margin =

Definition : The ratio of the net non interest income divided by a banks total assets. It measures the amount of non interest revenues from deposit service and other service against the non interest expenses , bank has been able to collect. For most bank , the non interest margin is negative. Now bank service fee income is increasing constantly.

For most banks non interest income is negative. Here we can see that net non interest margin was negative in three consecutive year. In 2005 and 2006 it was much better relative to past three years. No doubt about this bank is going very strongly.

Year Total operating revenues

total operating expenses

Total Assets

2002 (2,520,248,618-999,633,389) 65,080,700,199 2.34%

2003 (3,270,600,384-1,296,093,694) 81,704,745,989 2.42%

2004 (4,249,551,341-1,598,001,797) 102,149,282,158 2.59%

2005 (4,702,057,535-1,833,192,601 122,880,348,222 2.33%

2006 (6,018,967,069-2,703,669,981) 150,252,820,801 2.20%

Net Bank Operating margin =

Definition : Net bank operating margin is use to measure the efficiency and profitability of a bank. It gives analysts an idea of how much a bank makes from each dollar of loans, before interest and taxes.

Here we can see that net bank operating margin was better in 2004 and lowest in 2006. Overall it was stable.

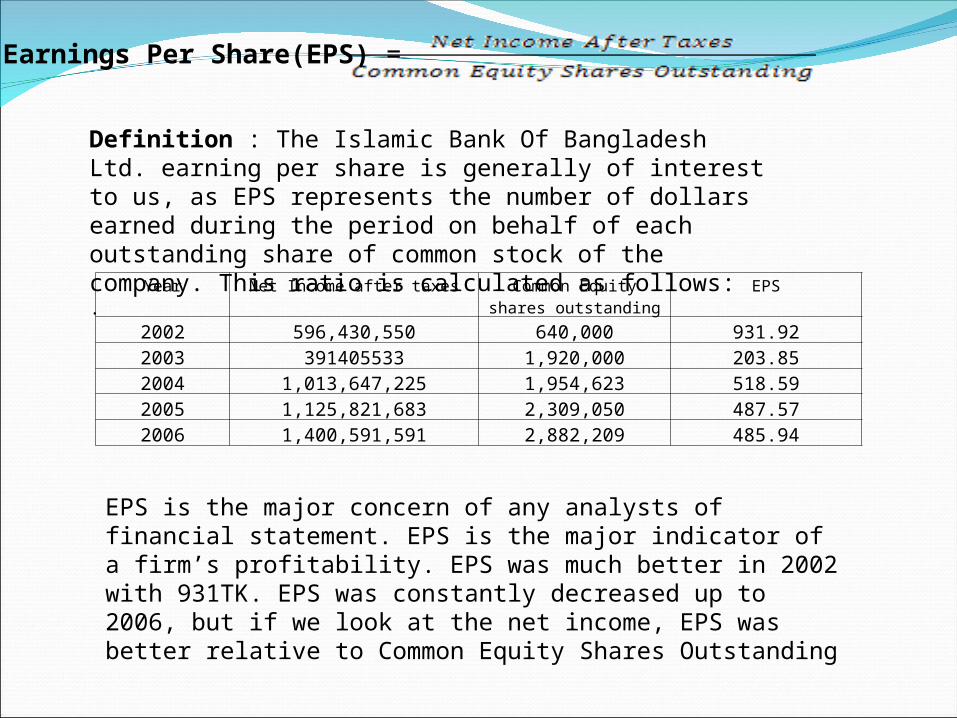

Year Net Income after taxes Common Equity shares outstanding

EPS

2002 596,430,550 640,000 931.922003 391405533 1,920,000 203.852004 1,013,647,225 1,954,623 518.592005 1,125,821,683 2,309,050 487.572006 1,400,591,591 2,882,209 485.94

Definition : The Islamic Bank Of Bangladesh Ltd. earning per share is generally of interest to us, as EPS represents the number of dollars earned during the period on behalf of each outstanding share of common stock of the company. This ratio is calculated as follows:.

EPS is the major concern of any analysts of financial statement. EPS is the major indicator of a firm’s profitability. EPS was much better in 2002 with 931TK. EPS was constantly decreased up to 2006, but if we look at the net income, EPS was better relative to Common Equity Shares Outstanding

Earnings Per Share(EPS) =

Findings : After studying the five years annual report of Islami Bank of Bangladesh and analyzing the respective ratio, we have found some negative and positive information relative to bank’s performance.•Islami Bank Of Bangladesh Ltd’s net income is constantly increasing year by year.•Total Assets and equity capital is also increasing •Net Non Interest Income was positive in 2005 and 2006.•Bank was large enough to gain funds from cheapest sources.•Bank was able to control their operating expenses.•Their contribution to social welfare is remarkable.•According to Earning per share (EPS) Bank was better in 2002.•According to ROA, Net Interest Margin and ROE, Bank was better in 2004.•Bank has huge channel to delivery service.• Overall performance was better in 2006.• Online Banking Service of IBBL is not up to the mark.• Number of ATM Booth is very few.

At least we can say that Islami Bank Bangladesh Limited is one of the biggest financial Institution of Bangladesh in term of profitability and efficiency of Management. We have no doubt that bank is going strongly and their performance is up to the mark.

Recommendations : Finally we think that it is high time to recommend future courses of action for our selected bank. •Though profitability and Efficiency was better, but bank has to increase their profitability and Efficiency, because profitability was much better in preceding years.•Bank has to introduce new services for their customer to capture customer satisfaction and value. Because competition is rising rapidly.•Bank has to concentrate on their online banking.•Bank has must increase their ATM Booth. •They should increase efficiency of employees.•Consumer loans service is major source of income, so they should invest in proper place.

CONCLUSIONAfter having completed the project, we want to say that Islami Bank Bangladesh Ltd. has the best overall position in terms of Efficiency, activity, and profitability. On the other hand . Recommendations have been given as to what the company can do to in order to enhance corporate image and maximize value.

Related Documents