43 Gerald P. Dwyer, Jr. and R. Alton Gilbert Gerald P. Dwyer, Jr., a professor of economics at Clemson University, is a visiting scholar and R. Alton Gilbert is an assistant vice president at the Federal Reserve Bank of St. Louis. Erik A. Hess and Kevin L. Kliesen provided research assistance. Bank Runs and Private Remedies URRENT banking regulation in the United States is based in part on the notion that both the banking system and the economy must be protected from the adverse effects of bank runs. An example often cited as typical is the string of bank runs from 1930 to 1933, which conventional wisdom holds responsible for thousands of bank failures and the Banking Holiday of 1933 when all banks closed. The runs on savings associations in Ohio and Mary- land in 1985 are more recent examples. This conventional view is reflected in a recent comment on the “Panic of 1907” in the Wall Street Journal (1989): Long lines of depositors outside the closed doors of their banks signaled yet another financial crisis, an all-too familiar event around the turn of the century. Research in the last few years on bank runs indicates that the conventional view is mistaken. Runs on the banking system were not common- place events, and their impact on depositors and the economy easily can be overstated. Prior to the formation of the Federal Reserve System in 1914, banks responded to runs in %vays that lessened their impact. These private remedies did not solve the problem of runs, but they did mitigate the effects of the runs on the banks and the economy. In this article, we explain the private remedies for runs and provide some evidence on the frequency and severity of runs on the banking system. BANK RUN’S: THE THEORY Before examining the history of bank runs, it is useful to consider why banks at-c vulnerable to runs. This examination establishes a frame- work for determining the kinds of observations that would be consistent with their occurrence. Runs on Individual Banks In a run, depositors attempt to withdraw cur- rency from a bank because they think the bank will not continue to honor its commitment to pay on demand a dollar of currency for a dollar of deposits.’ One aspect of the contract banks make with their customers is central to under- standing why depositors would run on their bank. Banks make contractual promises that they cannot always honor: exchange of gold or ‘Salant (1983) provides a general analysis of the break- down of such arrangements as bank redemption of its liabilities at par. The mapping from speculative attacks into bank runs is discussed by Flood and Garber (1982). MAY/JUNE 1SBE

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

43

Gerald P. Dwyer, Jr.and R. Alton Gilbert

Gerald P. Dwyer, Jr., a professor of economics at ClemsonUniversity, is a visiting scholar and R. Alton Gilbert is anassistant vice president at the Federal Reserve Bank of St.Louis. Erik A. Hess and Kevin L. Kliesen provided researchassistance.

Bank Runs and PrivateRemedies

URRENT banking regulation in the UnitedStates is based in part on the notion that boththe banking system and the economy must beprotected from the adverse effects of bankruns. An example often cited as typical is thestring of bank runs from 1930 to 1933, whichconventional wisdom holds responsible forthousands of bank failures and the BankingHoliday of 1933 when all banks closed. Theruns on savings associations in Ohio and Mary-land in 1985 are more recent examples.

This conventional view is reflected in a recentcomment on the “Panic of 1907” in the WallStreet Journal (1989):

Long lines of depositors outside the closed doorsof their banks signaled yet another financial crisis,an all-too familiar event around the turn of thecentury.

Research in the last few years on bank runsindicates that the conventional view is mistaken.Runs on the banking system were not common-place events, and their impact on depositors andthe economy easily can be overstated. Prior tothe formation of the Federal Reserve System in1914, banks responded to runs in %vays that

lessened their impact. These private remediesdid not solve the problem of runs, but they didmitigate the effects of the runs on the banksand the economy. In this article, we explain theprivate remedies for runs and provide someevidence on the frequency and severity of runson the banking system.

BANK RUN’S: THE THEORY

Before examining the history of bank runs, itis useful to consider why banks at-c vulnerableto runs. This examination establishes a frame-work for determining the kinds of observationsthat would be consistent with their occurrence.

Runs on Individual Banks

In a run, depositors attempt to withdraw cur-rency from a bank because they think the bankwill not continue to honor its commitment topay on demand a dollar of currency for a dollarof deposits.’ One aspect of the contract banksmake with their customers is central to under-standing why depositors would run on theirbank. Banks make contractual promises thatthey cannot always honor: exchange of gold or

‘Salant (1983) provides a general analysis of the break-down of such arrangements as bank redemption of its

liabilities at par. The mapping from speculative attacks intobank runs is discussed by Flood and Garber (1982).

MAY/JUNE 1SBE

44

currency at par value for bank liabilities.’ Whenbanks issued notes as a form of currency, thepromise was a contractual agreement to deliverspecie (gold or silver) in exchange for the bank’snotes at par value. Banks currently promise todeliver U.S. currency to depositors on demandat par value. Because banks hold reserves thatare only a fraction of their liabilities payable ondemand, they cannot honor this promise if allof their depositors try to convert deposits intocurrency at the same time.

Fractional-reserve banking by itself is not suf-ficient to make it impossible for banks to honortheir promises to deliver currency in exchangefor deposits on demand. Banks always couldhonor a promise to pay currency at a variableexchange rate of currency for deposits. If alldepositors want to exchange their deposits forcurrency at the same time, banks do not havesufficient currency (or’ other reserves that canbe transformed into currency on a dollar-for-dollar basis instantaneously) to meet that de-mand for currency at a price of one dollar ofcurrency for one dollar of deposits.’

in the normal course of affairs, the inabilityof all depositors to exchange their deposits forcurrency is irrelevant. As some depositors with-draw currency from a bank, others deposit it.The low probability of every depositor closinghis or her account at the same time is thereason a bank usually can operate with frac-tional reserves and pay currency on a dollar-for-dollar basis.

A low probability is not the same as a zeroprobability though. Information or rumorswhich suggest a capital loss by a bank may in-duce its depositors to attempt to convert theirdeposits to currency.4 The mere expectationthat other depositors will attempt the same con-version also can cause a run on a hank. A runon a single bank is unlikely, however, to havesubstantial effects on the economy. The primaryeffect of a single bank closing is that the bankwinds up its affairs and no longer operates.

The effects of a run by depositors on onebank can be illustrated by an example. Table 1shows the balance sheet of a hypothetical na-tional bank in New York City in the nationalbanking period (1863 to 1914). Its liabilities in-clude deposits and national bank notes backedby securities deposited with the Treasury. Inthe event of the bank’s failure, the notes wereguaranteed by the U.S. Treasury, whether ornot the deposited bonds were sufficient backingfor the notes. Apparently as a result of thisguarantee, runs on banks in the national bank-ing era were runs by depositors, not by noteholders.’

During tlus period, national banks in NewYork City were required to maintain reserves ofspecie and legal tender equal to 25 percent ormore of deposits, with the required ratio ofreserves to deposits lower for national banks inother cities. Banks generally held excess re-serves as a buffer stock to meet deposit with-drawals, but we use a reserve ratio of 25 per-cent to keep the numerical example simple. ‘l’hesecond part of table I shows the initial loss ofreserves upon withdrawal of $2 million ofdeposits, while the last part indicates the reac-tion of the bank to the decrease in deposits. Anindividual bank can replenish its reserves byselling assets; in the example, the bank returnsits reserve ratio to 25 pci-cent by selling $1.5million in assets. At least part of the reservesare from other banks, thereby transmitting thereserve loss to other banks.

In a i-un on a single bank, the specie and legaltender withdrawn from the bank are likely tobe largely deposited in other banks. As a result,a run on a single bank is not likely to drainreserves from the banking system or increasecurrency held by the public. If the currencywithdrawn is deposited in other banks, the neteffect on the bank’s balance sheet is that shownin table 1, and the deposit and reserve loss atthis bank is matched by a similar’ increase indeposits and reserves at other banks.

‘Whether this promise is a result of market forces orgovernment regulation is an open question. Davis (1910)summarizes the laws in the United States in the 19th cen-tury, and Schweikart (1987) provides the historical devel-opment of these laws in the South in the 19th century.

‘Promises that cannot be kept in all states of the world arehardly unique to banking. For instance, firms often cannotmake payments on debt if there is a large decrease in thedemand for their products. The common legal word forfailure to honor contractual commitments is “default.”

While default generally is not the expected outcome of acontract, it does happen.

4Among others, Diamond and Dybvig (1983) and Gorton(1985a) present models of runs.

5In banking panics prior to the national banking era,customers of banks attempted to redeem their bank notesfor specie. For details on the backing for notes in the na-tional banking era, see Friedman and Schwartz (1963), pp.20-23, 781-82.

FEDERAL RESERVE BANK OF St LLU-tS

45

N’ ,,, ‘

Tabiel ,, N

BaI~à$beet*1 a t4~tIonaIBank In New York CityWith a Large

Nw8thdtawai of*wo (mi1Iion~of dollars)1uthAl~BAIAN* ~HEE?

Assets N LisF~dtt1es

5 DØ)~OSS *09tsØsf$rtd*) Nota I 0

,n*ssn~itig~a$S~ “I~te , ,N~t~vorth , \zsSsásets~ “s” “ Totstiiabthtes’ $36

‘~~MMS!S~. tfl$aRA~~$2~tUOMS\p~,

NN Assets N -\ ~“ N N “N N V

~‘N\~tGtVSt\ ~N\ ,~ N’ , ~poS $80N N,, N’,N Sti~s

‘‘N N$wt’,N N N Tawlla~lnttes

N Afl~NEsTOSXtK*’ÔP RESE~W~!$AT1o‘ton ~ACENT N

N N ~N :“ N UIbilttes

4fl D~posi$N Notes

N\M$rN ~$SSN t4wfl 25

N N \‘N tIS T1a~brfrtt~S $14 N

Runs on the Banking System

Runs on a single bank can develop into runson the banking system.6 An important, if seem-ingly obvious, aspect of banking is that the like-lihood of a bank’s default on its deposit agree-ment is not known with certainty by depositors.Instead, depositors estimate this likelihood asbest they can with available information. Onetype of information that can be useful inestimating the value of a bank’s assets is infor-mation on the value of assets at other banks.News about the failure of one bank can causedepositors at other banks to raise their estimateof the probability that their bank will default.Contagious bank runs can be defined as runswhich spread from one bank or group of banksto other banks.

A term sometimes used for a period of a r’unon the banking system is a “banking panic,” a

term that has a connotation of unreasoning fearor hysteria. Contagious runs, however, can bebased on the optimal use of all information byall agents. As a simple example, suppose thattwo banks are identical in all respects knownby depositors, and one of the two fails becauseof loan losses. Because of the first failure, de-positors will increase their estimate of the pro-bability that the second bank will fail. If thisestimate increases sufficiently, depositors willrun on the second bank, even though no otherinformation has appeared. This use of informa-tion is quite consistent with rational behavior.Depositors use the information available, andone part of that information is the condition ofother banks.

Simultaneous runs on many banks need notbe contagious runs though. For example, an ex-ogenous event can increase simultaneously de-

6Gorton (1985a) and Waldo (1985) provide models ofaspects of the process which we discuss in this section.

MAY/JUN.E 1989

46

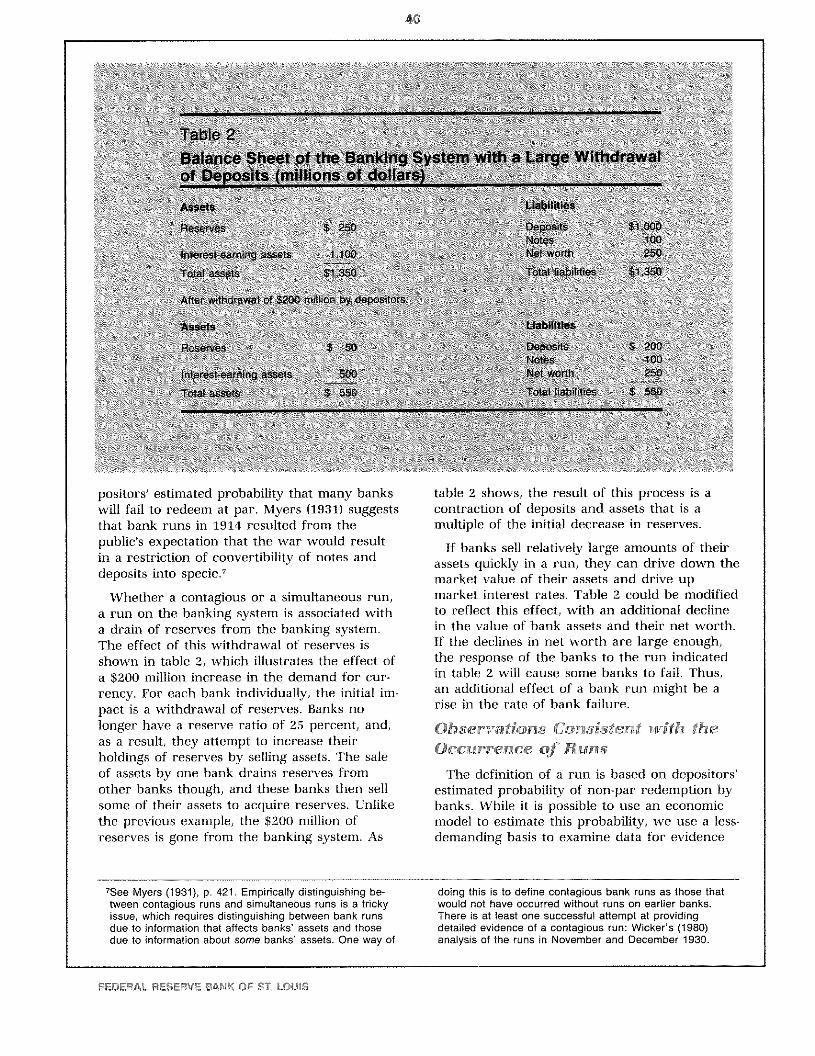

positors’ estimated probability that many bankswill fail to redeem at par. Myers (1931) suggeststhat bank runs in 1914 resulted from thepublic’s expectation that the war would resultin a restriction of convertibility of notes anddeposits into specie.’

Whether a contagious or a simultaneous run,a run on the banking system is associated witha drain of reserves from the banking system.The effect of this withdrawal of reserves isshown in table 2, which illustrates the effect ofa $200 million increase in the demand for cur-rency. For each bank individually, the initial im-pact is a withdrawal of reserves. Banks nolonger have a reserve ratio of 25 percent, and,as a result, they attempt to increase theirholdings of reserves by selling assets. The saleof assets by one bank drains reserves fromother banks though, and these banks then sellsome of their assets to acquire reserves. Unlikethe previous example, the $200 million ofreserves is gone from the banking system. As

If banks sell relatively large amounts of theirassets quickly in a run, they can drive down themarket value of their assets and drive upmarket interest rates. Table 2 could be modifiedto reflect this effect, with an additional declinein the value of bank assets and their net worth.If the declines in net worth are large enough,the response of the banks to the run indicatedin table 2 will cause some banks to fail. Thus,an additional effect of a bank run might be arise in the rate of bank failure.

Observations Consistent with theOccurrence of Runs

The definition of a run is based on depositors’estimated probability of non-par redemption bybanks. While it is possible to use an economicmodel to estimate this probability, we use a less-demanding basis to examine data for’ evidence

‘See Myers (1931), p. 421. Empirically distinguishing be-tween contagious runs and simultaneous runs is a trickyissue, which requires distinguishing between bank runsdue to information that affects banks’ assets and thosedue to information about some banks’ assets. One way of

doing this is to define contagious bank runs as those thatwould not have occurred without runs on earlier banks.There is at least one successful attempt at providingdetailed evidence of a contagious run: Wicker’s (1980)analysis of the runs in November and December 1930.

table 2 shows, the result of this process is acontraction of deposits and assets that is amultiple of the initial decrease in reserves.

FEDE RAL RESERVE BANK OF St LOUIS

47

of runs: we examine the data for consequencesof runs.’

A leading example of an event consistent witha run on the banking system is a joint restric-tion of convertibility by banks. Without an of-ficial central bank, banks can limit the effects ofa run by jointly agreeing to restrict currencypayments to depositors.° The effects of such arestriction can be illustrated by referring totable 2. Suppose that, after depositors withdraw$50 million in currency, the banks agree to stopmaking currency payments. In this illustration,deposits decline by only $200 million, to $800million. The demand for more currency bydepositors will not cause a further decline indeposits because some or all of that demand isrefused by the banks.

Hence, one observation that provides clearevidence of a run on a banking system is arestriction of currency payments by banks inthe system. An individual bank resorts to arestriction of currency payments if it cannotmeet its commitment to pay currency to deposi-tors on demand. Banks will resort to this actionjointly if they face a common problem of cur-rency withdrawals.

If the restriction of payments results in signifi-cant restrictions on depositors’ ability to trans-form deposits into currency, a market for trans-forming currency into deposits may develop. Ifthere is such a market, there will be a premiumfor currency in terms of deposits.bn

A bank run need not result in restrictionthough. The following developments also wouldbe consistent with the occurrence of a run on abanking system, although they are not inevi-table effects of runs and they can occur in the

absence of a run. Perhaps most importantly forour purposes, these indicators of runs can belessened by a restriction of payments to deposi-tors. They are:

1. a decline in the ratio of reserves to deposits.2. a rise in the ratio of currency to deposits.3. for a given monetary base, a decline in the

money supply (because the decline in de-posits is a multiple of the decline in bankreserves).

RESTRICTION OF

CONVERTIBILITY

The view that the banking system is vulner-able to runs may be based primarily on the ex-perience of the early 1930s, but the most rele-vant period to examine for evidence of runs isbefore the operation of the Federal ReserveSystem. Prior to late 1914, the United Stateshad no official central bank.11 We focus on thebanking system beginning with the 1850s. Whileevents in earlier years also are of interest, 1853marks the beginning of a weekly data set onreserves and deposits in banks in New York Ci-ty which is very useful. In addition, by the1850s, New York City was the most importantfinancial center in the United States. Manybanks in other parts of the country held cor-respondent balances in New York City banks,and pressures affecting banks in the rest of thecountry affected New York City banks throughthese balances.”

Restrictions on Payments

As table 3 indicates, banks in New YorkCity restricted payments on five occasions

°Gorton(1988) does estimate a particular model for runsand finds them generally consistent with our analysis. Healso defines runs on the banking system, or in his terms“banking panics,” as periods when convertibility wasrestricted in New York City, clearing house loan cer-tificates were authorized by the New York Clearing Houseor both (1988, pp. 222-23). We prefer not to identifyperiods with runs based on a single criteria. If we were topick a single criteria, it would be restriction of paymentsby banks. With any penalties on nonpar payments, bankswill not do this unless they at least believe that they can-not continue payments at par indefinitely. For the use of amultiple set of criteria along our lines, see Bordo (1986).

9The names “restriction of cash payments” or “restrictionof convertibility of deposits into currency” are suggestedby Friedman and Schwartz (1963, p. 110, fn. 32) ratherthan the traditional name of “suspension of currencypayments.” Following this suggestion avoids confusion of“suspension of currency payments” with “suspension ofoperations” and is more consistent with the fact that

banks commonly did not completely stop convertingdeposits into currency. Currency payments were non-pricerationed, not suspended. Evidence for the post-Civil-Warperiod that payments generally were restricted, notsuspended, is presented by Sprague (1910), pp. 63-65,121-24, 171-78, 286-90, and Andrew (1908), pp. 501-02.A more general and precise, but also quite pedantic, namefor restrictions would be “restriction of convertibility at parof bank liabilities with promised par redemption on de-mand.”

‘oAs we show below, banks remained open for deposits.Hence, a discount on currency could not persist.

11Friedman and Schwartz (1963) and, in more detail,Timberlake (1978) discuss the central banking activities bythe Treasury in the national banking period. As arguedforcefully by Dewald (1972), the New York Clearing Houseacted as a central bank at times.

‘25ee Myers (1931) and Sprague (1910).

MAY/JUNE 1888

48

ab N

o 0 tteneral Restriction otS len 4kwVar I toIflN

N ~ 4Me Ending tie

ast N

em 28 Apt $i~2JT*S ~4 N N

N ‘Se$embar2— N ~ a be~enter28~fl N Mar“r’’’,~”’’—

slaNt øs

between the iSSOs and 1914.” In the episodesfrom 1857 to 1907, banks across much of thecountry restricted currency payments, but therestrictions were not universal.’~The last suchrestriction was the banking holiday of March1933. In the banking holiday of 1933, the fed-eral government closed all banks in the countryand gradually reopened those that regulatorsjudged to be in satisfactory financial condition.In the earlier restrictions, in contrast, banks re-mained open and processed transfers of depos-its for their customers.

Other than for the restriction of payments in1907, it is difficult to obtain precise estimates ofhow widespread or binding these restrictionswere. Shortly after the panic of 1907, A. PiattAndrew surveyed banks in 147 cities in theUnited States with populations greater than25,000. Andrew (1908) found that, of the 145cities for which he had responses, 53 had norestriction of payments or emergency response.Of the remaining 92, the only restriction ofpayments in 20 cities was a request by thebanks that larger depositors mark their checksas “payable only through the clearing house.” Inthe remaining 72 cities, limits on withdrawalswere often discretionary. Even in the 36 citieswhere there was joint agreement between thebanks in the city to limit withdrawals, therewas substantial variations across them. For cx-

ample, in Atlanta, depositors could withdraw upto $50 per day and $100 per week from theirbanks. At the same time, depositors in two ofthese 36 cities, South Bend, tndiana, and Youngs-town, Ohio, could withdraw nothing from theirchecking accounts.

The Relative Price of Currencyand Deposits

During the periods of restrictions of currencypayments in the national banking era, marketsdeveloped in New York City for the exchange ofcurrency for certified checks. Holders of cer-tified checks marked “payable through theclearing house” could obtain currency in thismarket if they were willing to accept less thanthe face amount of the certified checks. FigureI shows the premiums on currency quoted inthese markets in the three periods of restric-tions in New York City in the national bankingera. These markets operated for about fourmonths in this period. The maximum premiumson currency are about 4 percent to 5 percent,but for most of the days in which these mar-kets operated, the premiums are much smaller.Nonetheless, the important issue is whether thepremiums are nonzero, which they are.

Clearinghouses and Restriction

During these restrictions of payments, banksremained open for much of their regular busi-ness and processed checks for their customersas they usually did. In some parts of the coun-try, banks in a local area processed checksbilaterally, but in other areas, banks used clear-inghouses to process checks. From 1857 to1914, these clearinghouses developed an emer-gency currency used during restrictions forclearing checks.

Clearinghouses for banks — In the secondhalf of the nineteenth century, banks in manycities established clearinghouses to decrease theresources used in clearing checks and exchang-ing gold and currency with other banks.”Rather than sending checks received to the of-fices of each bank for collection, members of aclearinghouse sent checks drawn on other mem-ber banks to the clearinghouse. Those with net

13A data appendix, available on request from the authors,gives the sources of these dates and the other data in thispaper.

14For a discussion of 1873 and 1893, see Sprague (1910),pp. 63-74, 168-69. Andrew (1908) presents the results of asurvey for 1907.

‘6Descriptions of clearinghouses are provided by Cannon(1910), Myers (1931), pp. 94-97, and Redlich (1968),ch. XVII.

FEDERAL RESERVE BANK OF St LOUiS

18 L C 2 C C ~0

CDo ,

—

-CD 2 a. 0 w a 0 C, -p 0 a. CD -. CD (4

0 C, CO

t (D C, 0

(Do

V —-I

CD-‘

30

0.

0)0

1<

C, ‘-4. 0 a-C

DC

D~

——

-‘0

-J (4

n-l

i

-I’

-‘

0k

‘C -I CD 3 C 3 C)) a. C (a CD (I)

-I 0 0 U) 0 -l

a to

0 CD

~00’

50

November and December 1907Percent

outflows of deposits at the clearinghouse paidthose with net inflows in gold and currency or,more conveniently, with clearinghouse certifi-cates. These certificates were receipts for banksdeposits of gold and legal tender at the clearing-house.

Clearinghouse loan certjficates — In someperiods, clearinghouses issued additional certifi-cates called clearinghouse loan certificates thatcould be used to clear checks. These certificateswere a commonly used expedient in runs from1860 until the creation of the Federal Reserve.’6

The precursor of these loan certificates wasan extraordinary issue of clearinghouse cer-tificates in the run on banks in 1857. Fearsabout the solvency of banks resulted in a drainof specie and ultimately a run on the banks inNew York City in 1857.” At this time, banksissued notes that were used as currency, andthe banks redeemed them in gold or silver ondemand. if a bank failed though, holders of the

notes could wind up with less than the prom-ised amount of specie. In 1857, holders of bank-notes were concerned about the likelihood thatbanks in various parts of the country would beable to continue converting their notes intospecie at par. As a result of the continuingredemption of their notes, these banks con-verted their correspondent balances in NewYork City banks into specie for redeeming theirOWfl notes. Thus, specie balances in New YorkCity banks dwindled and this drain of reservesculminated in a run on banks in New York City.On October 13, banks in New York City re-stricted specie payments, with restriction inmany other pares of the United States following.

In part, the effect of this specie drain onbanks in New York City was alleviated by ajoint agreement of the banks in the New YorkClearing House on November 7. New York statebanks that were not redeeming their notesagreed to pay 6 percent interest on them, andthe clearinghouse agreed that the notes of the

16Th~ssection owes much to the analyses in Timberlake(1984) and Gorton (1985b).

17Th~saccount is based on Gibbons (1859), oh. XIX; Myers

(1931), pp. 97-99, 141-44; Cabmiris and Schweikart(1988), pp. 31-56.

Percent5

4

3

2

0

FEDERAL RESERVE BANK OF ST. LOWS

51

banks could be used as backing for clearing-house certificates. Until they were graduallyretired, these certificates were used for clearingchecks just as if they were clearinghouse certi-ficates backed by deposits of specie.

Clearinghouse loan certificates were firstissued in 1860. In anticipation of war, Southern-ers converted their deposit balances in Northernbanks into specie and, just as in 1857, banks inNew York City were confronted with a drain oftheir specie reserves.18 After the election ofAbraham Lincoln in November, the banks in theNew York Clearing House responded to thedrain by jointly agreeing to allow bonds issuedby the federal government and the state of NewYork to be used as backing for certificates, call-ed “clearinghouse loan certificates,’ which couldbe used for clearing checks.

The procedure adopted in 1860 was basicallythe same as in every later instance when suchcertificates were issued. A loan committee wasestablished which examined collateral and is-sued certificates based on the collateral. Uponusing a loan certificate, a bank was required topay interest, at a rate fixed by the clearing-house, to any bank that held its loan certifi-cates.t9 The members of the clearinghouse,however1 were jointly liable for any loss atten-dant on holding a loan certificate. In addition,the clearinghouse agreements specified a date atwhich loan certificates would no longer be ac-ceptable for settling balances at the clear-inghouse.

Several features of the practices of clear-inghouses indicate that, in issuing loan cer-tificates, members of a clearinghouse were pool-ing their resources to deal with a common pro-blem of withdrawals, Clearinghouse memberspledged to absorb any losses on loan certificatesas a group, with Tosses allocated according toeach bank’s capital. Losses were not likely,however, because the borrowing banks pledgedassets with the clearinghouse, receiving loancertificates for a fraction of the value of theassets. In some panics, clearinghouse membersstopped the weekly publication of their individ-

ual balance sheets and published combinedbalance sheets of their members, thus withhold-ing information on the relative weakness of in-dividual members.20

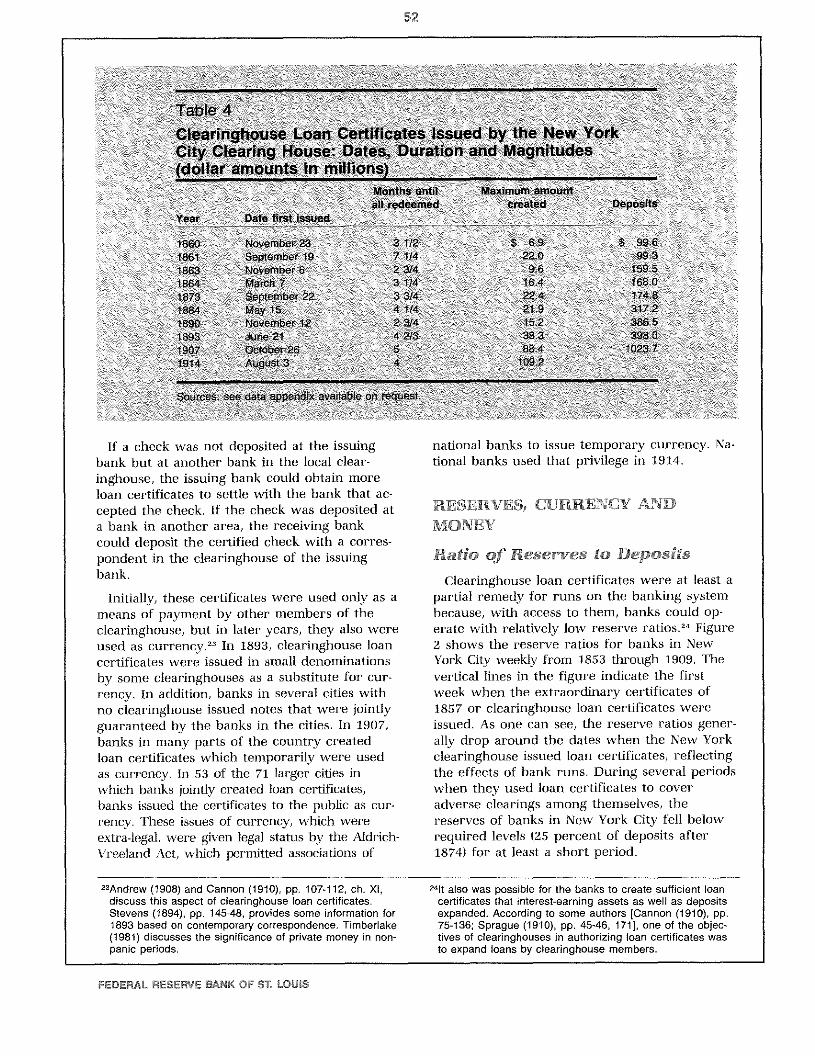

Clearinghouse loan certificates were createdseveral times in the 55 years from 1860 to1914. Table 4 shows the dates when these cer-tificates were issued by the New York ClearingHouse.21 As a quick comparison of tables 3 and4 shows, clearinghouse loan certificates wereissued whenever convertibility of deposits intocurrency was restricted. This is no coincidence,because clearinghouse loan certificates were animportant part of banks strategy for stayingopen after a run on the banking system.

Although first issued in 1860 in New YorkCity only, the use of clearinghouse loan certifi-cates became widespread over time (Stevens1894; Andrew 1908; Cannon 1910). In 1873, theclearinghouses in New York City, Boston, Cincin-nati, New Orleans, Philadelphia and St. Louisissued them. In 1884, New York City again wasthe only clearinghouse to issue loan certificates,but in 1890 it was joined by Boston and Phila-delphia. In 1893, clearinghouses in at least 12cities issued loan certificates, and in 1907, banksin 42 of 145 cities in the United States withmore than 25,000 people used such certificates.

Loan certificates and restrictions — Evenwith access to clearinghouse loan certificates,banks could provide currency in a run only un-til they exhausted their inventories of specieand legal tenderY During restrictions, banks ra-tioned currency, meeting the requests by somecustomers for their customary withdrawals ofcurrency and denying requests by others. Banksthat were members of the clearinghouse con-tinued to accept checks drawn on other clear-inghouse members when deposited by theircustomers. As a result, depositors could makepayments by writing checks drawn on their ac-counts or with certified checks issued by theirbanks. The major limitation was that the checksgenerally could not be exchanged for specie orcurrency by the recipient of the check.

‘8Swanson (1908) provides a detailed account of thisepisode.

‘9The annual rates were 7 percent in 1860 and 1873 and 6percent in every other instance when they were ssued,Comptroller of the Currency (1915, voL 1), p. 103.

20Members of the New York City Clearing House agreed topool reserves n the panic of 1873 but not in the following

panics. Sprague (1910), pp. 46, 120; Myers (1931), pp.408-20.

21The New York Cleanng House authorized but did notSue loan cerUficates ri December 1895 and August 1896.Gorton (1985b), p.280, fri. 11.

22This section draws heavily on Sprague (1910).

MAY/JUNE 1989

52

Table 4Clearinghouse Loan Certificates Issued by the New YorkCity Clearing House: Dates, Duration and Magnitudes(dollar amounts in millions)

Months until Maximum amountall redeemed created Deposits

Year Date tirst issued

1860 November23 3 1/2 $ 69 $ 99.61861 September 19 7 1/4 22.0 99.31863 November 6 23/4 96 15951864 March 7 3 1/4 16.4 168.01873 September22 33/4 22.4 174.81884 May15 41/4 21.9 31721890 November 12 23/4 152 38651893 June21 4213 383 39E301907 October26 5 88.4 1023 71914 August3 4 1092

Sources see data appendix available on request

If a check was not deposited at the issuingbank but at another bank in the local clear-inghouse, the issuing bank could obtain moreloan certificates to settle with the bank that ac-cepted the check. If the check was deposited ata bank in another area, the receiving bankcould deposit the certified check with a corres-pondent in the clearinghouse of the issuingbank.

Initially, these certificates were used only as ameans of payment by other members of theclearinghouse, but in later years, they also wereused as currency.23 In 1893, clearinghouse loancertificates were issued in small denominationsby some clearinghouses as a substitute for cur-rency. In addition, banks in several cities withno clearinghouse issued notes that were jointlyguaranteed by the banks in the cities. In 1907,banks in many parts of the country createdloan certificates which temporarily were usedas currency. lii 53 of the 71 larger cities inwhich banks jointly created loan certificates,banks issued the certificates to the public as cur-rency. These issues of currency, which wereextra-legal, were given legal status by the Aldrich-~~reeJand Act, which permitted associations of

national banks to issue temporary currency. Na~tional banks used that privilege in 1914.

RESERVES2 CURRENCY ANDMONEY

Ratio of Reserves to Deposits

Clearinghouse loan certificates were at least apartial remedy for runs on the banking systembecause) with access to them, banks could op-erate with relatively low reserve ratios.2~Figure2 shows the reserve ratios for banks in NewYork City weekly from 1853 through 1909. Thevertical lines in the figure indicate the firstweek when the extraordinary certificates of1857 or clearinghouse loan certificates wereissued. As one can see, the reserve ratios gener-ally drop around the dates when the New Yorkclearinghouse issued loan certificates, reflectingthe effects of bank runs. During several periodswhen they used loan certificates to coveradverse clearings among themselves, thereserves of banks in New York City fell belowrequired levels (25 percent of deposfts after1874) for at least a short period.

23Andrew (1908) and Cannon (1910), pp. 107-112, ch. XI, 241t also was possthle for the banks to create sufficient loandiscuss this aspect of dearinghouse loan certificates, certificates that interest-earning assets as well as depositsStevens (1894), pp. 145-48, provWes some information for expanded. According to some authors [Cannon (1910), pp.1893 based on contemporary correspondence. Timberlake 75-136; Sprague (1910), pp. 45-46, 1711, one of the objeo-(1981) discusses the significance of pñvate money in non- tives of cieadnghouses in authorizing loan certificates waspanic periods, to expand loans by cleannghouse members.

FEDERAL RESERVE BANK OF St LOWS

53

In 1873, 1893 and 1907, the banks in the NewYork City clearinghouse restricted convertibilityshortly after they had begun borrowing clear-inghouse loan certificates. The reserve ratiorose sharply after the banks restricted pay.rnents, and they built up substantial excess re-serve positions before resuming payments todepositors. The New York City banks also builtup their excess reserves substantially after theycreated these certificates in 1860 and 1884, andafter the creation of the extraordinary cer-tificates of 1857.

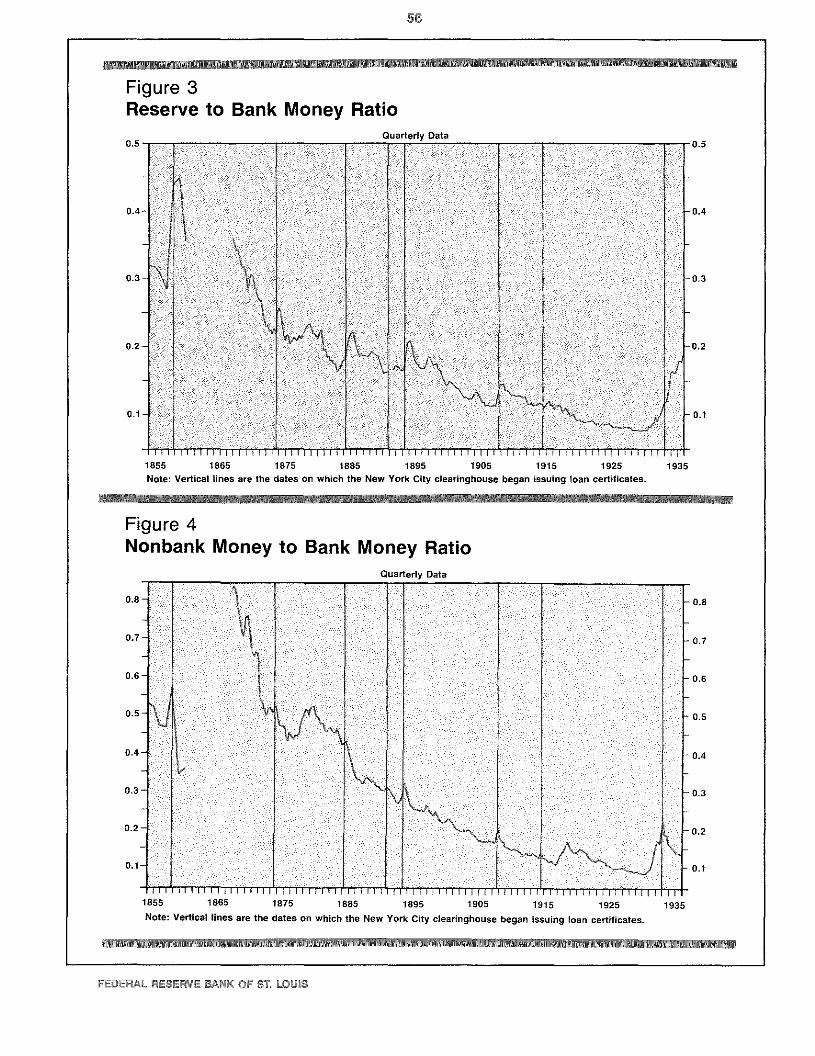

The decreases in reserve ratios at the time ofruns were short-lived. Indeed, the quarterlydata in figure 3 for all banks in the UnitedStates from 1853 to 1935 do not show thesesharp declines in the reserve ratio. They doshow, though, the increases in the ratio afterbanks restricted convertibility.

Ratio of Currency to Deposits

We would expect a rise in the ratio of non-bank money held by the nonbank public tobank money in a run on the banking system, atleast until banks limited the reserve outflow byrestricting payments. The year-end data for1856 and 1857 show some indication of an ef-fect of withdrawals in the panic of 1857, whichoccurred in the fall of that year. The ratio ofspecie held by the public relative to bank notesand deposits rose from 47 percent in December1856 to 57 percent in December 1857. Figure 4shows these data and quarterjy data on thecurrency-to-deposit ratio for the U.S. bankingsystem from 1867 to 1935. This ratio generallyincreases around the dates when banks in NewYork City issued clearinghouse loan certificatesor restricted currency payments.

The most extreme rise in the currency ratioin figure 4 occurs in the early 1930s. Friedmanand Schwartz (1963) argue that the rise in thecurrency ratio was more exftetne in the early1930s than before the operation of the FederalReserve System because, rather than restrictingcurrency payments, the banks expected the Fedto provide reserves. In the event, the FederalReserve failed to provide sufficient reserves.25

Monet’ Growth

As the example in table 2 illustrates, a bankrun results in a decrease in the money stock fora given monetary base. Table 5 shows the quar-ters with relatively large decreases in themoney stock from 1867 to 1933 and zero orpositive growth of the monetary base. Everyquarter with a decrease in the money stock atgreater than a 2 percent annual rate and non-negative growth of the monetary base is includ.ed in the table.

Of the six periods in table 5, only one — 1877to 1878 — is not associated with a restriction ofconvertibility or the creation of clearinghouseloan certificates in New York City. The de-creases in the money supply in 1877 and 1878occur during the Treasury’s retirement ofgreenbacks prior to resumption of dollar con-vertibility into gold on January TI., 1879.z6 All ofthe dates of general restriction — 1873, 1893,1907 and 1933 — are periods in which themoney stock fell and the base increased for atleast one quarter. The year 1884 has somecharacteristics of bank runs: banks in New YorkCity created clearinghouse loan certificates, butconversion of deposits into currency was notrestricted. As the table indicates, the highestrates of decrease in the money stock occurredfrom 1931 to 1933, after the Federal Reservewas established.

EFFECTS OF BANK RUNS

While the previous section presents evidencethat there were several episodes of runs on theU.S. banking system before the Federal Reservewas formed, it provides little indication of theimportance of their effects. ‘I’h~ssection pro-vides some perspective on the impact of thoseruns.

Losses by DepositorsThe premiums on currency provide one mea-

sure of the cost of runs to bank depositors. Interms of currency, depositors suffered a loss ontheir deposits during these periods. Thepremiums indicate that, immediately after runson the banking system, some people were will-ing to exchange currency for certified checks at96 cents or more on the dollar and3 within a

25See Friedman and Schwartz (1963), pp. 167-72, 308-12. outside New York City. Friedman and Schwartz (1963), pp.56-58, 82.26Friedman and Schwartz (1963), ch. 2, discuss this period

in detaU. They attribute these movements to runs on banks

MAYIJtJNE 1989

54

Figure 2Reserve Ratio

month, the currency premiums were Tess than 2percent.27

Depositors also suffered losses when banksclosed. The total losses borne by depositors inclosed banks from 1865 through 1933 were atan annual rate of .21 percent of total deposits.Before the Great Depression, the general trendof these loss rates was downward. The lossrates were .19 percent in 1865-80, .12 percentin 1881-1900, .04 percent in 1901-20, and roseto a peak of .34 percent in 1921-33.

These figures are for all years and understatethe loss rates in years with runs. Depositors’losses on total deposits exceed .25 percent in 12years: 1873, 1875-78, 1884, 1891, 1893 and

1930-33. The average loss rate in these 12 yearsis .78 percent of total deposits. In all but two ofthese periods, either convertibility of depositswas restricted or clearinghouse loan certificateswere issued in New York City. In only one yearwas convertibility of deposits into currencyrestricted, loan certificates issued, and the lossrate less than .25 percent: 1907.28

In the 1930s, for which data on individualyears are available, it is possible to get reason-ably accurate estimates of Toss rates borne bythe depositors in closed banks. The losses werenot borne evenly across the population: anaverage loss rate per dollar of total deposits of.47 percent of total deposits in 1930 does not

~It is worth noting that these losses by depositors werecounter-balanced at least in part by gains by holders ofcurrency. The bid-ask spread would be a measure of thedirect real resource cost of nonpar trades.

28Unfortunately, the data before 1920 are provided only asaverages for periods of sever& years; we know that theloss rates in 1907 and 1908 were not as high as .25 per-cent, but we do not know more about them.

Weekly Data0.5

O~4

0.3

0.2

0.1

0.0

0.3

1853 1860 1970 1880Note: Vertical lines are the dates on which the New York City clearinghouse began issuing loan certificates.

FEDERAL RESERVE BANK OF St LOWS

55

0.5

0.4

0.3

0.2

0.1

0.0

1880

convey the losses borne by individual depositorsin individual banks. The average loss rates fordepositors in banks that failed are about 28 per-cent in 1930 and 15 percent in 1933.29

In sum, two things seem to be clear fromthese data. First, some holders of bank liabilitiesdid bear significant losses during periods withruns. These losses were not necessarily causedby the runs themselves. The runs and the lossesboth may have been triggered by events outsidethe banking system. It is possible, though, that

the runs increased the losses from what theymight have been under different institutionalarrangements.

Second, before the creation of the FederalReserve, depositors’ loss rate from failed bankswere declining over time. In this regard, it isworth noting that depositors’ loss rate in 1907was not as high as in as many previous periods,even though the panic of 1907 was the appar-ent impetus for the creation of the FederalReserve System.

29The loss rates in closed banks for every year from 1921through 1929 are higher than from 1930 to 1933. Thisdecrease in depositors loss rate in banks c’osed n yearswith runs s not necessarily surprising because runs canforce banks to liquidate with posifive net worth or networth less negative than ft might be otherwise. This latterobservation is consistent with the FDIC’s observation that

loss rates are ess after the 12 crisis years” than ri othernon.crisis years. FOIC (1940), pp. 65, 69.The loss rates for the national banking period are substan-tially, but not always, lower than some of the loss ratesestimated by King (1983) and Roloick and Weber (1988)for the earlier free banking period (1838 to 1863).

Weekly Data0.5

0.4

0.3

0.2

0.1

1890 1900 1909Note: Vertical lines are the dates on which the New York City clearinghouse began issuing loan certificates.

0.0

MAY/JUNE 1989

Figure 3Reserve to Bank Money Ratio

56

Note: Vertical lines are the dates on which the New York City clearinghouse began issuing loan certificates.

Figure 4Nonbank Money to Bank Money Ratio

II I I I I Ill I [ I I] I I F F

1855 1865 1875 1885

Quarterly Data

I [ II ] I FI I 1fF II II liii’ ii 1T1895 1905 1915 1925 1935

Note: Vertical lines are the dates on which the New York City clearinghouse began issuing loan certificates.

FEDERAL RESERVE BANK OF St LOtUS

1855 1865 1875 1885 1895 1905 1915 1925 1935

0.8-

0_i

0.6-

0.5 -

0.4 -

O.3

0.2-

0.1— 1...._ —

- 0.8

- 0.7

0.6

-0.5

- 0.4

- 0.3

- 0.2

- 0.1

57

Losses by Bank Shareholders:

Bank Failures

During restrictions, two things happened.Banks were able to stop the drain of reservesand possibly the sale of assets at distress prices.In addition, they were able to take stock anddetermine which banks might survive the panic.

Table 5 The importance of this effect perhaps is most

Growth Rates of the Money Supply clearly indicated by a comparison of Illinois andWisconsin banks just before the Civil War.Banks in Illinois did not restrict specie paymentsWhich the Money Supply Declined and, ultimately, 93 out of 112 of the banks

at . . closed. With similar portfolios of assets, banks

in Wisconsin did restrict specie payments andfewer of them, 50 out of 107 banks, ultimatelyclosed.30

(annual growth rates of quarterlyAnother way of getting an idea of the costs todata, seasonally adjusted) banks is to compare failure rates in banking

Money Monetary panics before 1933 with the failure rate insupply base 1933. At the onset of the Depression, banks did

not issue clearinghouse loan certificates orrestrict currency payments. While the FederalReserve increased the monetary base) the basewas not increased sufficiently to prevent re-peated runs until the restriction of payments inthe Banking Holiday. As a result) 1933 providesa contrasting indicator of how serious banking

panics can be.1893- Figure 5 shows that banking panics can in-

deed be associated with relatively large num~

1907: 3 . 8.0 00 bers of banks failing. Nonetheless, it is notewor-1908 thy that, before 1933, the only year with

restriction and a large increase in the failure

1929. 1 3.1 1 ~ rate is 1893.

1931: 2 ~11.2 12.53 --147 11.2 Wacroeconorn~c Effects3l4 -308 13.3 Figure 6 shows the monthly average call loan

1932 2 - 136 13.9 rate for 1857 through 1935. Call loans are over-

~ night loans with stock as collateral that are1933 1 —39.9 20.7 callable without notice. Because call loans were

a part of their assets that they were not con-Sources see data appendix available on request. tractually obligated to continue for longer per-

iods, banks in New York City reduced their callloans when they wished to convert part of theirassets into reserves. In figure 8, vertical linesdenote the periods when banks in New York Ci-ty restricted convertibility or had large drains

~°SeeDowrie (1913), Krueger (1933) and Economopoulos (1983), Bordo (1986), Gorton (1988), Kaufman (1988),(1988). Taliman (1988) and Grossman (1989).

31For other discussions of the macroeconomic effects ofbank runs, see Friedman and Schwartz (1963), Bernanke

MAY/JUNE 1989

58

Figure 5Bank Suspension and Failure RatePercent Annual Data21 -

Figure 6Call RatePercent70

1933

60

50

40

30

20

10

0

18571860 1870 1880 1890 1900 1910 1920 1930 1935Note: Vertical lines are the dates on which the New York City clearinghouse began issuing loan certificates,

60

50

40

30

20

10

0

Percent21

Is

15

12

9

6

a

a1864 1870 1880 1890 1900 1910 1920

Note: Vertical lines are the dates on which the New York City cteadnghouse began issuing loan certificates.

Monthly Data Percent70

FEDERAL RESERVE BANK OF St LOthS

59

of reserves to which they responded by issuingclearinghouse loan certificates. While the in.creases in the call loan rate associated withrestrictions and drains are not unique, some areextraordinary.

Evidence that would support the view thatbank runs had adverse effects on the economywould be as follows: bank runs occurred justprior to the onset of recessions, and moresevere recessions followed banking panics.Table 6 provides information on the timing andseverity of recessions and the timing of bankruns. The data do not support a simple conclu-sion on the macroeconomic effects of bankruns. Other than the episode in 1873, bankscreated clearinghouse loan certificates andrestricted currency payments several months

after the beginning of the recessions. Whilesome of the more severe recessions occurredwhen banks restricted currency payments, thisis consistent with two very different conclu-sions: restrictions led to severe recessions3 orsevere recessions led to restrictions.

Table 6 also indicates that several recessionsoccurred without runs on the banking system.These observations provide information aboutthe stability of the U.S. banking system withouta federal safety net. Several recessions, withdeclines in real output and losses to businesses,occurred apparently without undermining theconfidence of the public in the safety of bankdeposits to the point of starting runs on thebanking system.

MAY/JUNE 19-59

60

CONCLUSION

The federal safety net for the banking systemincludes the Federal Reserve as the lender oflast resort, federal deposit insurance, and banksupervision and regulation designed to limit therisk assumed by banks. The rationale for thissafety net is that, in its absence, the bankingsystem would be vulnerable to the kind of runon the banking system that occurred in the ear-ly 1930s. The run in the early 1930s, however,was, perhaps, the most extreme run on thebanking system in U.S. history.

While several runs on the banking systemtook place before the formation of the FederalReserve System in 1914, banks took actions thatlimited their effects. By issuing clearinghouseloan certificates that other banks accepted toclear checks, banks operated temporarily withrelatively low reserve ratios. In the more severeruns, bankers jointly restricted payments butcontinued operating. Moreover, even prior tothe creation of the federal safety net in theUnited States, runs on the banking system wereinfrequent. The banking system can operate formany years without runs on the bankingsystem, even in recessions.

REFERENCES

Andrew, A. Plait. Substitutes for Cash n the Panic of1907;’ Quarterly Journal of Economics (August 1908), pp.497-516.

Bernanke, Ben. ‘Nonmonetary Effects of the Anancial Crisisin the Propagation of the Great Depression,” AmericanEconomic Review (June 1983), pp. 257-76.

Bordo, Michael D. “Financial Crises, Banking Crises, StockMarket Crashes and the Money Supply: Some InternationalEvidence, 1870-1933,” in Forrest Capie and Geoffrey E.Wood, eds., Financial Crises and the World Banking System(St. Martin’s Press, 1986), pp. 190-248.

Calomiñs, Charles W., and Larry Schweikart. ‘Was theSouth Backward?: North-South Differences n AntebellumBanking during Normalcy and Crisis[ unpublished paper,Northwestern tiniversfly, August 1988.

Cannon, James G. Clearing Houses, U.S. National MonetaryCommission, Senate Document No. 491, 61 Cong., 2ndSess. (U.S. Government Printing Office, 1910).

Comptroller of the Currency. Report (U.S. Department of theTreasury, 1915).

Davis, Andrew M. The Origin of the National Ranking Sys-tem, U.S. National Monetary Cornm~ssion,Senate Docu-ment No. 582, 61 Cong., 2nd Sess. (U.S. Government Prin-ting Office, 1910).

Dewald, William G. The National Monetary Commission: ALook Back,” Journal of Money, Credit and Banking(November 1972), pp. 930-56.

Diamond, Douglas W., and Philip H. Dybvig. ‘Bank Runs,Deposfl Insurance, and Liquidity,” Journal of PoliticalEconomy (June 1983), pp. 401-19.

Dowrie, George W. The Development of Banking in Illinois,1817-1865. Vo’ume 11, No. 4 of the Series, University of II-Unois Studies in the Social Sciences (University of Illinois,December 1913).

Economapoulos, Andrew J. “Illinois Free Banking Exper-ience:’ Journal of Money, Credit, and Banking (May 1988),pp. 249-64.

Federal Deposit Insurance Corporation. Annual Report,(Federal Deposit Insurance Corporation, 1940).

Flood, Robert R, and Peter M. Garber. ‘Bubbles, Runs, andGold MoneUzation,” in Paul Wachtel, ed. Crises in theEconomic and Financial Structure (Lexington Books, 1982).

Friedman, Milton, and Anna J. Schwartz. A Monetary Historyof the United States, 1867-1960 (Princeton University Press,1963).

Gibbons, J.S. The Banks of New York, their Dealers, theClearing House, and the Panic of 185Z Original publication,1859. (Reprint edition, Greenwood Press Publishers, 1968).

Gorton, Gary. ‘Bank Suspension of Convertibility,” Journa’of Monetary Economics (March 1985a), pp. 177-93.

‘Clearinghouses and the Origin of CentralBanking in the United States,” Journal of Economic History(June 1985b), pp. 277-83.

Banking Panics and Business Cycles,” OxfordEconomic Papers (December 1988), pp. 751-81.

Grossman, Richard S. The Macroeconomic Consequencesof Bank FaHures Under the National Banking System,” U.S.Department of State. Bureau of Economic and Business Af-fairs, Planning and Economic Analysis Staff, WorkingPaper 14, April 1989.

Kaufman, George G. The Truth About Bank Runs:’ nCatherine Eng’and and Thomas F. Huertas, eds. TheFinancial Services Revolution: Poiicy Directions for theFuture (Kiuwer Academic Publishers, 1988), pp. 9-40.

King, Robert G. On the Economics of Private Money,”Journal of Monetary Economics (July 1983), pp. 127-5&

Krueger, Leonard. History of Commercial Banking inWisconsin (University of Wisconsin, 1933).

Myers, Margaret G. The New York Money Market, Vol. I,Origins and Development (Columbia University Press,1931).

FEDERAL RESERVE BANK OF ST. LOthS

61

Redlich, Fritz. The Molding of American Banking, 2nd S. T~mberlake,Jr., Richard H. The Origins of Central Banking in(Johnson Repñnt Corporation, 1968). the United States (Harvard Unh’ersity Press, 1978).

Rolnick, Arthur J., and Warren E. Weber. Explaining theDemand for Free Bank Notes,” Journal of MonetaryEconomics (January 1988), pp. 47-71. . The Significance of Unaccounted Currencies,”

Journal of Economic Histo~(December 1981), pp. 553-66.Salant, Stephen W. The Vulnerability of Price Stab~ItzationSchemes to Speculative Attack,” Journal of PoliticalEconomy (February 1983), pp. 1-38.

_______ The Central Banking Role of ClearinghouseSchw&kart, Larry. Banking in the American South from the Associations,” Journal of Money, Credit and Banking

Age of Jackson to Reconstruction (Louisiana State Universi- (February 1984), pp. 1-15.ty Press, 1987).

Sprague, 0. M. W. History of Crises under the NationalBanking System, U.S. National Monetary Commission, Waldo, Douglas G. “Bank Runs, the Deposit-Currency RatioSenate Document No. 538, 61 Cong., 2 Sess. (GPO, 1910). and the Interest Rate,” Journal of Monetary Economics

Stevens, Albert C. “Analysis of the Phenomena of the Panic (May 1985), pp. 269-77.in the United States in 1893,” Quarterly Journal ofEconomics (January 1894), pp. 117.48, 252-60. Wall Street Journal. “Panic Button Finally Thggers Reform,

Swanson, William Walker. “The Crisis of 1860 and the First i907’ February 16, 1989.Issue of Ctear~ng-HouseCertificates,’ Journal of PoliticalEconomy (April 1908), pp. 212~26.

Taliman, Ellis. ‘Some Unanswered Questions about Bank Wicker, Elmus. “A Reconsideration of the Causes of thePanics,” Federal Reserve Bank of Atlanta Economic Review Banking Panic of 1930,” Journal of Economic History(November/December 1988), pp. 2-21. (September 1980), pp. 571-83.

FEDERAL RESERVE BANK OF ST. LOWS

Related Documents