SHARING OF FINANCIAL WISDOM Others may quote and refer to the contents on this website provided that they have the author's consent and proper reference is made to investingbythebooks.com. Bank Primer Thank you to Swedbank and Kepler Cheuvreux Swedbank for releasing the material What we will cover This text was originally published September 30, 2016 as a thematic piece in Swedbank’s quarterly smalland midcap product called The Companion. It is, with slight cosmetic alterations, republished by InvestingByTheBooks thanks to Swedbank’s and Kepler Cheuvreux Swedbank’s kind permission. Note that this altered text is solely the responsibility of the author and not of the above mentioned firms. Mats Larsson, September 29, 2018 Contents 8.1 Introduction 8.2 The Spread Business 8.3 Investment Banking 8.4 The Other Stuff 8.5 Financial Statements 8.6 Banking on Troubles 8.7 Risk Management 8.8 Regulation 8.9 Fintech 8.10 Bank Valuation 8.11 Investing in Banks 8.1 Introduction Financials is one of the really big global sectors in equity markets. In fact, measured in market capitalization it’s the largest one. It’s also a more diverse sector than many perhaps realize hosting a number of different business models. In the GICS framework the sector is made up of four industry groups, namely banks, diversified financials, insurance and real estate. Each industry group in turn contains between one and three so-called industries as pictured by the boxes in the picture below. One common theme is that the businesses in the financial sector are interest rate sensitive.

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

SHARING OF FINANCIAL WISDOM

Others may quote and refer to the contents on this website provided that they have the author's consent and proper reference is made to investingbythebooks.com.

Bank Primer

Thank you to Swedbank and Kepler Cheuvreux Swedbank for releasing the material What we will cover

This text was originally published September 30, 2016 as a thematic piece in Swedbank’s quarterly small-‐and mid-‐cap product called The Companion. It is, with slight cosmetic alterations, republished by InvestingByTheBooks thanks to Swedbank’s and Kepler Cheuvreux Swedbank’s kind permission. Note that this altered text is solely the responsibility of the author and not of the above-‐mentioned firms. Mats Larsson, September 29, 2018

Contents § 8.1 Introduction § 8.2 The Spread Business § 8.3 Investment Banking § 8.4 The Other Stuff § 8.5 Financial Statements § 8.6 Banking on Troubles § 8.7 Risk Management § 8.8 Regulation § 8.9 Fintech § 8.10 Bank Valuation § 8.11 Investing in Banks

8.1 Introduction Financials is one of the really big global sectors in equity markets. In fact, measured in market capitalization it’s the largest one. It’s also a more diverse sector than many perhaps realize hosting a number of different business models. In the GICS framework the sector is made up of four industry groups, namely banks, diversified financials, insurance and real estate. Each industry group in turn contains between one and three so-called industries as pictured by the boxes in the picture below. One common theme is that the businesses in the financial sector are interest rate sensitive.

SHARING OF FINANCIAL WISDOM

Others may quote and refer to the contents on this website provided that they have the author's consent and proper reference is made to investingbythebooks.com.

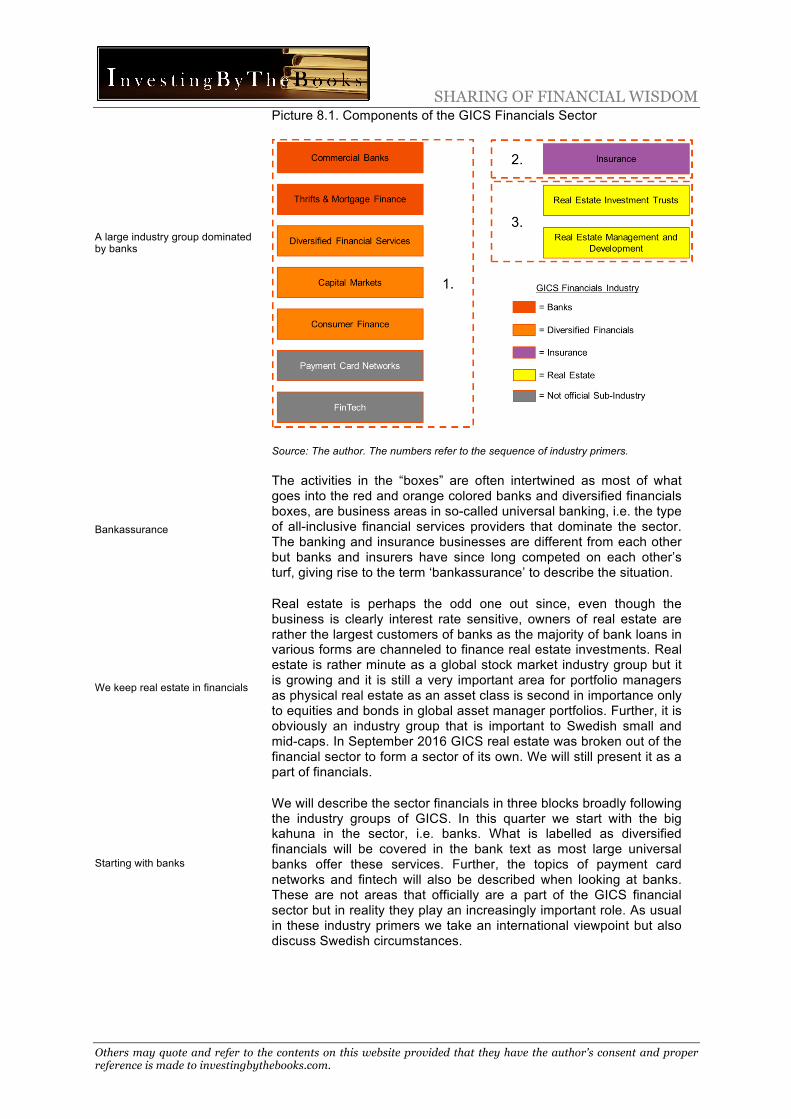

A large industry group dominated by banks

Bankassurance

We keep real estate in financials

Starting with banks

Picture 8.1. Components of the GICS Financials Sector

Source: The author. The numbers refer to the sequence of industry primers.

The activities in the “boxes” are often intertwined as most of what goes into the red and orange colored banks and diversified financials boxes, are business areas in so-called universal banking, i.e. the type of all-inclusive financial services providers that dominate the sector. The banking and insurance businesses are different from each other but banks and insurers have since long competed on each other’s turf, giving rise to the term ‘bankassurance’ to describe the situation.

Real estate is perhaps the odd one out since, even though the business is clearly interest rate sensitive, owners of real estate are rather the largest customers of banks as the majority of bank loans in various forms are channeled to finance real estate investments. Real estate is rather minute as a global stock market industry group but it is growing and it is still a very important area for portfolio managers as physical real estate as an asset class is second in importance only to equities and bonds in global asset manager portfolios. Further, it is obviously an industry group that is important to Swedish small and mid-caps. In September 2016 GICS real estate was broken out of the financial sector to form a sector of its own. We will still present it as a part of financials.

We will describe the sector financials in three blocks broadly following the industry groups of GICS. In this quarter we start with the big kahuna in the sector, i.e. banks. What is labelled as diversified financials will be covered in the bank text as most large universal banks offer these services. Further, the topics of payment card networks and fintech will also be described when looking at banks. These are not areas that officially are a part of the GICS financial sector but in reality they play an increasingly important role. As usual in these industry primers we take an international viewpoint but also discuss Swedish circumstances.

SHARING OF FINANCIAL WISDOM

Others may quote and refer to the contents on this website provided that they have the author's consent and proper reference is made to investingbythebooks.com.

ROE pre and post 2008…

…today they are lower

What are banks for?

A market place for money…

Let’s start with some background. Financials as a global sector – dominated by the large banks in the western world - has seen some ups and downs. From early 1980’s to mid-1990’s ROE declined due to pressure on profit margins. Then followed a marked and long lasting trend of improving ROE up until 2008 (albeit with a bump in the road during the crisis 2002/03). Leverage levels that had stayed fairly constant from the early 1980’s, in the late 1990’s started to edge up and the levels between 2002 and 2008 was clearly higher than historical precedents. Hence, the first part of the secular ROE improvement was driven by profitability improvements and the second part by a higher risk taking. Especially US banks saw uncharacteristically high ROE prior to the GFC. As a share of the total market capitalization in the US (as measured by MSCI) the financial sector rose from 8% early 1990 to 23% late 2006 and back to the current 15%.

The global ROE that up to 2008 had averaged above 11% nosedived to negative levels in the financial crisis to subsequently stabilize at a lower than historic average level in later years while the leverage gradually has returned to the 1980’s and 1990’s level. The lower ROE is in part driven by reduced risk taking but mainly by higher capital requirements. The leverage in the US is now at historically relatively low levels while banks in other regions probably still will shrink balance sheets further. New capital requirements are enforced and the massively delayed US Volcker-rule to curb banks’ proprietary trading will be implemented. The global post-crisis loan growth has with time become quite decent but the main part of the growth comes from emerging markets, not least China. The last two years US loan growth has picked up as well.

Which functions do banks perform? Which customer needs are met? The basic function of a bank is to transfer money from those who have an excess and want to save for a later date to those who have a shortage and want to invest now (or consume for that matter). The former often deposit money with the bank and the latter borrow from the bank. By this the customers of the bank can allocate their usage of funds over time. The spread between the interest of the party who wants to save and the interest of the one who wants to borrow is generally the main earnings in a bank. This spread is a function of that the bank through its diversification over a large number of financiers and customers are more credit worthy than the customers borrowing the money.

Thus, to some extent a bank is a market square where those that supply money meet those who demand money, i.e. it’s a matching service. In addition to acting as the meeting place, the bank’s service is to change the risk profile of the customer’s transactions by pooling the money from a large number of lenders and borrowers and by this changing the counterparty risk. For example the credit risk of the depositor is largely diversified away. The pooling of money also allows lenders and borrowers with different maturity/liquidity expectations to meet. Generally those who deposit money want immediate access to their money and those who borrow want the option to keep the funds for as long as they would want. The pooling of many deposits further allows banks to make larger individual loans.

SHARING OF FINANCIAL WISDOM

Others may quote and refer to the contents on this website provided that they have the author's consent and proper reference is made to investingbythebooks.com.

…and more

But there are alternatives

Retail banking…

…is a mature business in the western world…

…and investment banking is seeing some troubles

Banking license

Additionally, the bank is also the party that executes the transactions made on the square, i.e. handles payments, the record keeper who keeps track of all the transactions and a safe storage of money in-between transactions.

Apart from using bank lending the two alternatives to matching savers and borrowers are direct lending or capital markets. Direct lending has been very cumbersome historically, as finding a counterparty that matches the size of the sum someone wants to borrow/lend and also matches the same expectation on the maturity of the transaction is hard. On top of this, direct lending that lacks the diversification, places a cost on the two parties to gather the information to handle the counterparty risk, i.e. the risk that the other will not fulfil his obligations. With the aid of improved technology direct lending in the form of peer-to-peer lending is emerging as a more viable alternative. We will cover this area further below. The capital market alternative for the one who wants to borrow is to issue an interest bearing security. This way to raise funds is however seldom an alternative for anyone apart from large or medium sized corporations.

Global retail banking revenues in 2015 grew 3% to USD 1.59tr. The Americas stood for 37% of the revenues, Asia-Pacific 30% and Western Europe 25%.

Picture 8.2. Growth in Retail Banking Revenues

Source: Boston Consulting Group. The 2015-19 numbers are BCG estimates.

Further, banks offer a host of services and investment banking services, where banks facilitate securities market intermediation, are important revenue generators. According to BCG global investment banking revenues fell by 5% in 2015.

However, the core of a bank is still to be able to offer deposits subject to withdrawal on demand and making loans. To be able to legally be recognized as a bank the organization needs to have a banking license. Licenses are issued by national financial services authorities (FSAs) and applicants must meet a number of requirements on capital, regarding the directors etc. With a banking license a bank can perform banking activities of which some are often exclusive to banks, typically taking deposits from the public.

-2%0%2%4%6%8%10%12%14%

2006-2010 2010-2015 2015-2019

SHARING OF FINANCIAL WISDOM

Others may quote and refer to the contents on this website provided that they have the author's consent and proper reference is made to investingbythebooks.com.

Banks create more money than…

…central banks

The money multiplier…

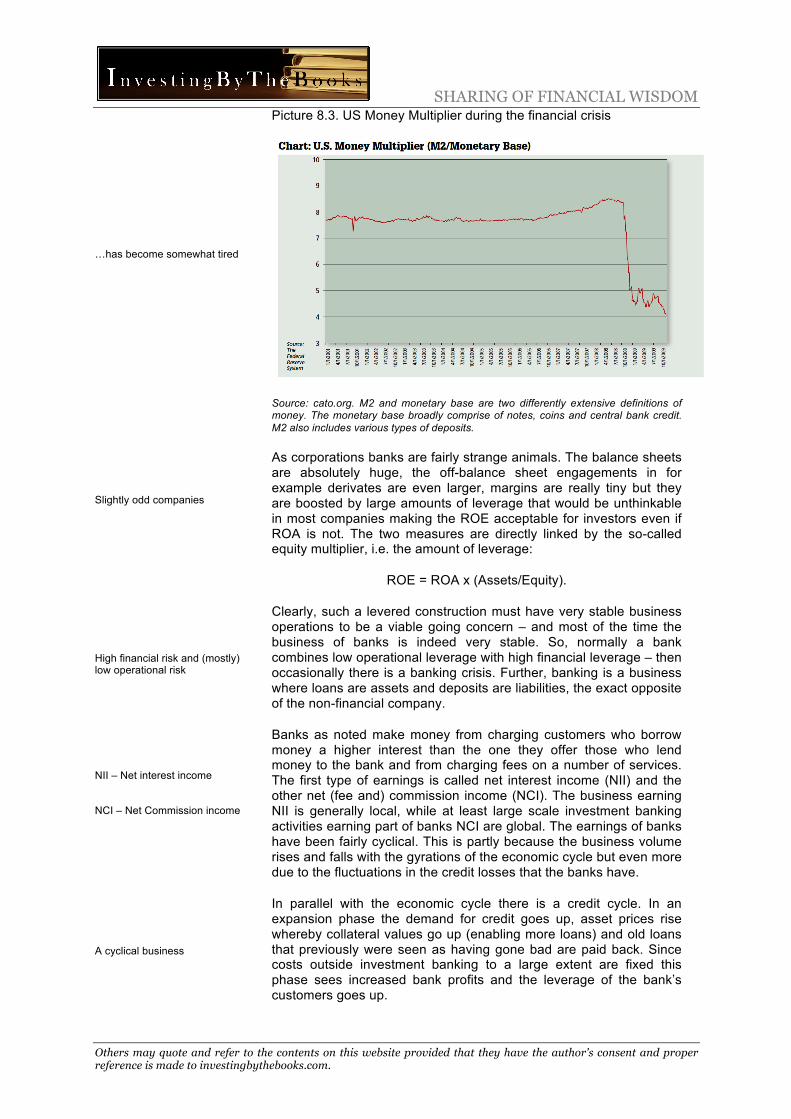

On a societal level banks aid central banks in creating money. What money is, is however no easy thing to pin down. Your economics textbook will traditionally say something along the line that money is a social good that a) acts like a medium of exchange by which buyers and sellers can pay and receive payment for goods and services, b) store value over time and c) works as a unit of account for pricing, accounting etc. This in a modern society obviously applies to notes and coins, but also to bank deposits and central bank reserves that are largely virtual and, some would argue, to crypto-currencies like Bitcoin.

Central banks only create a minority of countries monetary base through their physical or digital printing press. Banks create money through leverage and extending credit. The process is often called fractional reserve banking and the tool used is called the money multiplier. If someone comes by $ 1,000 and deposits them at a bank, then the bank can turn around and lend that money to someone else. Hence, the depositor still has his money left but the borrower also has new money to spend. Note that the bank has capital requirements placed on itself from a regulator (and financiers) which means that it cannot lend the full $1,000 (hence the name fractional reserve banking). Say that 10% has to be retained then obviously the borrower only gets his hand on $900. Both the passive side and the active side of the bank’s balance sheet will expand as a consequence.

Now, say that the new debtor doesn’t need to spend the money immediately but instead again deposits them in the bank. The bank can now lend a further $810 to someone else and so on. In theory $1,000 will in the end turn into $ 10,000 ($1,000/10%). This is the effect of the money multiplier.

Theoretical money multiplier, m = 1/reserve requirement

The lower/higher the reserve requirements on the bank the more/less money the banking system will create. The central bank directly affects this process by injecting or subtracting money into the banking system, by influencing the interest rates banks charge and sometimes by regulating the amount of reserves that has to be retained in the banks. As the aftermath of the 2008 financial crisis clearly showed the willingness and ability of banks to part with money (as opposed to repair their balance sheet) and the demand from customers to borrow will obviously also affect the effect of the multiplier by adding more or less friction into the process.

SHARING OF FINANCIAL WISDOM

Others may quote and refer to the contents on this website provided that they have the author's consent and proper reference is made to investingbythebooks.com.

…has become somewhat tired

Slightly odd companies

High financial risk and (mostly) low operational risk

NII – Net interest income

NCI – Net Commission income

A cyclical business

Picture 8.3. US Money Multiplier during the financial crisis

Source: cato.org. M2 and monetary base are two differently extensive definitions of money. The monetary base broadly comprise of notes, coins and central bank credit. M2 also includes various types of deposits.

As corporations banks are fairly strange animals. The balance sheets are absolutely huge, the off-balance sheet engagements in for example derivates are even larger, margins are really tiny but they are boosted by large amounts of leverage that would be unthinkable in most companies making the ROE acceptable for investors even if ROA is not. The two measures are directly linked by the so-called equity multiplier, i.e. the amount of leverage:

ROE = ROA x (Assets/Equity).

Clearly, such a levered construction must have very stable business operations to be a viable going concern – and most of the time the business of banks is indeed very stable. So, normally a bank combines low operational leverage with high financial leverage – then occasionally there is a banking crisis. Further, banking is a business where loans are assets and deposits are liabilities, the exact opposite of the non-financial company.

Banks as noted make money from charging customers who borrow money a higher interest than the one they offer those who lend money to the bank and from charging fees on a number of services. The first type of earnings is called net interest income (NII) and the other net (fee and) commission income (NCI). The business earning NII is generally local, while at least large scale investment banking activities earning part of banks NCI are global. The earnings of banks have been fairly cyclical. This is partly because the business volume rises and falls with the gyrations of the economic cycle but even more due to the fluctuations in the credit losses that the banks have.

In parallel with the economic cycle there is a credit cycle. In an expansion phase the demand for credit goes up, asset prices rise whereby collateral values go up (enabling more loans) and old loans that previously were seen as having gone bad are paid back. Since costs outside investment banking to a large extent are fixed this phase sees increased bank profits and the leverage of the bank’s customers goes up.

SHARING OF FINANCIAL WISDOM

Others may quote and refer to the contents on this website provided that they have the author's consent and proper reference is made to investingbythebooks.com.

Mark Twain has a quote for everything!

But there are structural changes as well

A department store

Money-flows through a bank

The rest of the text

GFC – Global financial crisis

At some point the cycle turns whereby credit demand dries up, credit supply dries up, credit losses increase and potentially assets have to be written down - all dragging down the banks’ profits. The fact that banks in unison tend to tighten lending requirements when the economic going gets tough has given rise to the well-known Mark Twain quote, “A banker is a fellow who lends you his umbrella when the sun is shining, but wants it back the minute it begins to rain”.

Although both NII and NCI increase with a buoyant economy the latter usually increases faster. Hence, the business mix says something about where in the cycle we are. For example, over time NII has been a larger contributor to the total profits of SEB than has the NCI, but both in 2000 and in 2006/07 NCI surpassed NII. These points in time were obviously the peaks of those economic cycles.

One feature of a modern universal bank is that it’s like a department store or supermarket for multiple financial services, increasing the complexity of the organizations. Several of these services are separate business areas and have different business models.

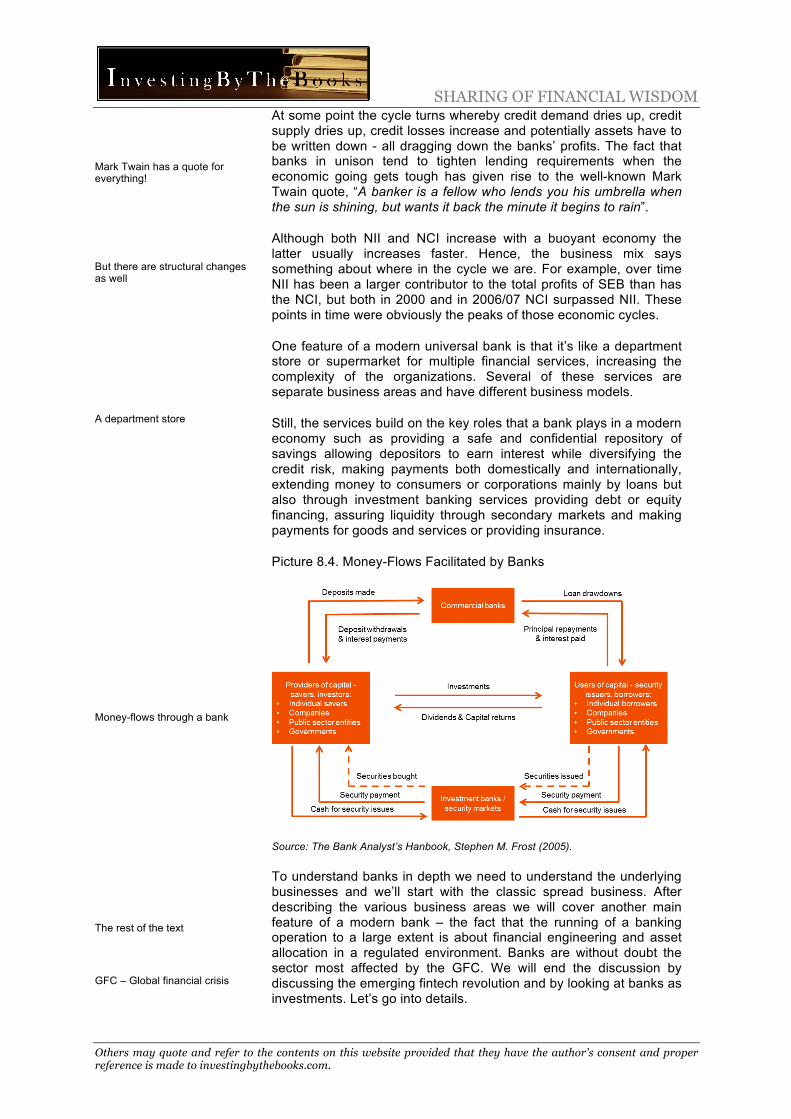

Still, the services build on the key roles that a bank plays in a modern economy such as providing a safe and confidential repository of savings allowing depositors to earn interest while diversifying the credit risk, making payments both domestically and internationally, extending money to consumers or corporations mainly by loans but also through investment banking services providing debt or equity financing, assuring liquidity through secondary markets and making payments for goods and services or providing insurance.

Picture 8.4. Money-Flows Facilitated by Banks

Source: The Bank Analyst’s Hanbook, Stephen M. Frost (2005).

To understand banks in depth we need to understand the underlying businesses and we’ll start with the classic spread business. After describing the various business areas we will cover another main feature of a modern bank – the fact that the running of a banking operation to a large extent is about financial engineering and asset allocation in a regulated environment. Banks are without doubt the sector most affected by the GFC. We will end the discussion by discussing the emerging fintech revolution and by looking at banks as investments. Let’s go into details.

SHARING OF FINANCIAL WISDOM

Others may quote and refer to the contents on this website provided that they have the author's consent and proper reference is made to investingbythebooks.com.

+ Interest income

- Interest expenses

= Net interest income

NII = asset margin + liability margin

NIM – Net interest margin

Transformations

Steepening yield curves…

8.2 The Spread Business The main business of commercial banks is to match savers and borrowers so that the majority of bank profits is created by the spread between interest earned on assets (mainly loans and securities) and interest paid on liabilities (mainly deposits and so-called wholesale funding). The interest earned on assets is called – surprise – interest income, the interest paid on liabilities is called interest expense and if we deduct interest expenses from interest income we get net interest income (NII).

NII is driven by asset volume times the spread that banks earn on assets over funding costs. NII can be further broken down by into an asset margin and a liability margin by using some intermediary interest rate factor (like for example a two year government bond yield) to separate the two sides. NII divided by the interest bearing assets (or sometimes alternatively average assets) is called net interest margin (NIM) and is a key profitability metric for banks.

The capital that has been made available to the bank is pooled as it is recognized on the balance sheet. This allows a number of transformations to take place. Some are simple, like for example taking funds from deposits with a varying interest rate and lending to a corporation at a fixed rate or taking many small deposits and lending a larger amount to a party.

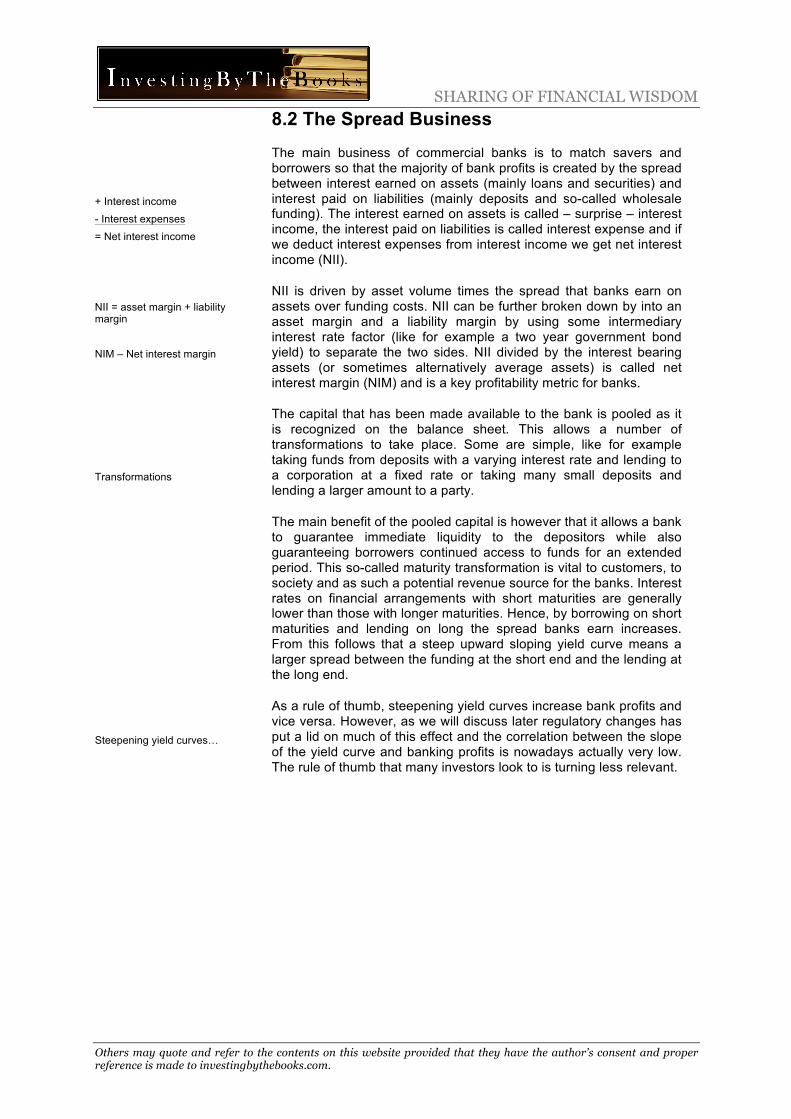

The main benefit of the pooled capital is however that it allows a bank to guarantee immediate liquidity to the depositors while also guaranteeing borrowers continued access to funds for an extended period. This so-called maturity transformation is vital to customers, to society and as such a potential revenue source for the banks. Interest rates on financial arrangements with short maturities are generally lower than those with longer maturities. Hence, by borrowing on short maturities and lending on long the spread banks earn increases. From this follows that a steep upward sloping yield curve means a larger spread between the funding at the short end and the lending at the long end.

As a rule of thumb, steepening yield curves increase bank profits and vice versa. However, as we will discuss later regulatory changes has put a lid on much of this effect and the correlation between the slope of the yield curve and banking profits is nowadays actually very low. The rule of thumb that many investors look to is turning less relevant.

SHARING OF FINANCIAL WISDOM

Others may quote and refer to the contents on this website provided that they have the author's consent and proper reference is made to investingbythebooks.com.

…are generally profitable

Maturity gap

Picture 8.5. What the Bank Pays and What the Bank Charges

Source: The author

Banks disclose the maturity profile of their assets and liabilities by presenting the sums owned and owed in different maturity buckets. If you’ve read textbooks on banking they will say that using so-called maturity gap analysis investors and analysts can see how much assets and liabilities re-price at different maturities and by this they can estimate the bank’s interest rate sensitivity. In this analysis the assets in each maturity bucket are divided by the liabilities with the same maturity.

An interest rate sensitivity below one means more liabilities than assets. Hence, the liability heavy short end of maturities will have interest rate sensitivity below one and the asset heavy long end will come in above one. As noted above, steepening yield curves increase bank profits and vice versa. The sensitivities can then, in a way we will not cover, be summed up to give a total understanding of how changes in interest rates affect the NII.

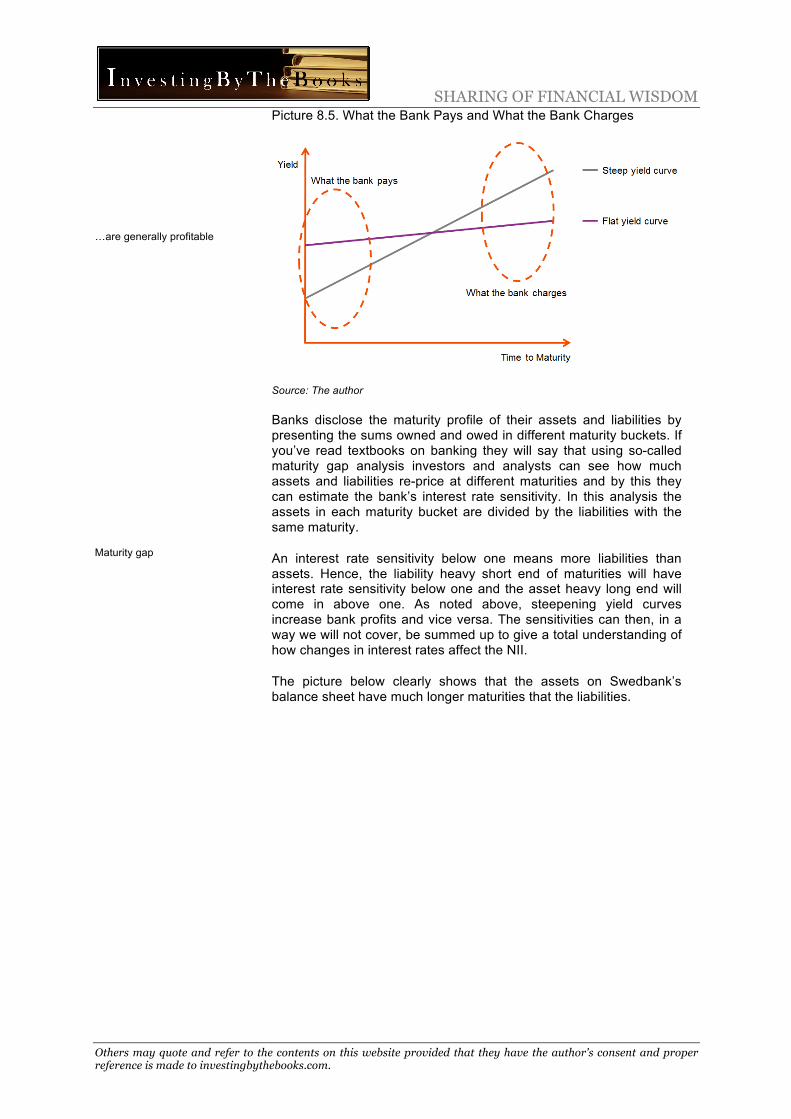

The picture below clearly shows that the assets on Swedbank’s balance sheet have much longer maturities that the liabilities.

SHARING OF FINANCIAL WISDOM

Others may quote and refer to the contents on this website provided that they have the author's consent and proper reference is made to investingbythebooks.com.

Swedbank’s maturities

Maturity mismatch -> potential interest rate risk & potential liquidity risk

Derivates

Swedbank’s interest rate sensitivity

Picture 8.6. Maturity 2015-12-31 of Swedbank’s Assets and Liabilities

Source: Swedbank 2015 Annual Report.

The problem with gap analysis is that regulations and the modern day use of off-balance sheet derivatives have rendered it practically useless. A maturity mismatch will bring two risks to the table. First, it will be a major contributor to interest rate risk as movements in interest rates will affect the value of assets and liabilities differently. Secondly, if liabilities have shorter maturities than the assets the bank faces a liquidity risk since for example depositors can withdraw the banks funding on short notice but the bank will have a hard time recalling the mortgage loans they have made.

Changes in regulation have meant that banks no longer can profit from maturity transformation to the same extent and the banks’ treasury departments actively manage the day-to-day maturity profiles mainly by taking positions in interest rate swaps and forwards. The real interest rate exposure is nowhere to be found on the balance sheet and even though some banks also report their asset-liability maturity profile adjusted for derivative exposures, that exposure could look materially different the day after the reporting date. The outsider to some extent fumbles in the dark when it comes to understanding the effects of banks’ interest rate exposures.

According to the Q4’15 Swedbank Factbook the net interest income impact of interest rates rising one percentage point was estimated to be SEK 4,887m, while the impact of interest rates declining one percentage point was estimated to be SEK -4,573m or -7,471m. The first figure assumes a 0% deposit rate floor for private individuals while the other extends this assumption to all depositors. Since the floor is so far valid for retail customers and SMEs but not large corporates the truth probably lies somewhere in-between the two figures. Hence, the asymmetry in the effects between rising and falling interest rates comes from the fact that some proportion of liabilities don’t reprice below 0%. The numbers include on- and off balance sheet assets and liabilities by the end of 2015.

SHARING OF FINANCIAL WISDOM

Others may quote and refer to the contents on this website provided that they have the author's consent and proper reference is made to investingbythebooks.com.

Assets earn interest

Charges for risks

Corporate lending

Self-reinforcing loops

The Asset Side of the Balance Sheet Earning Interest

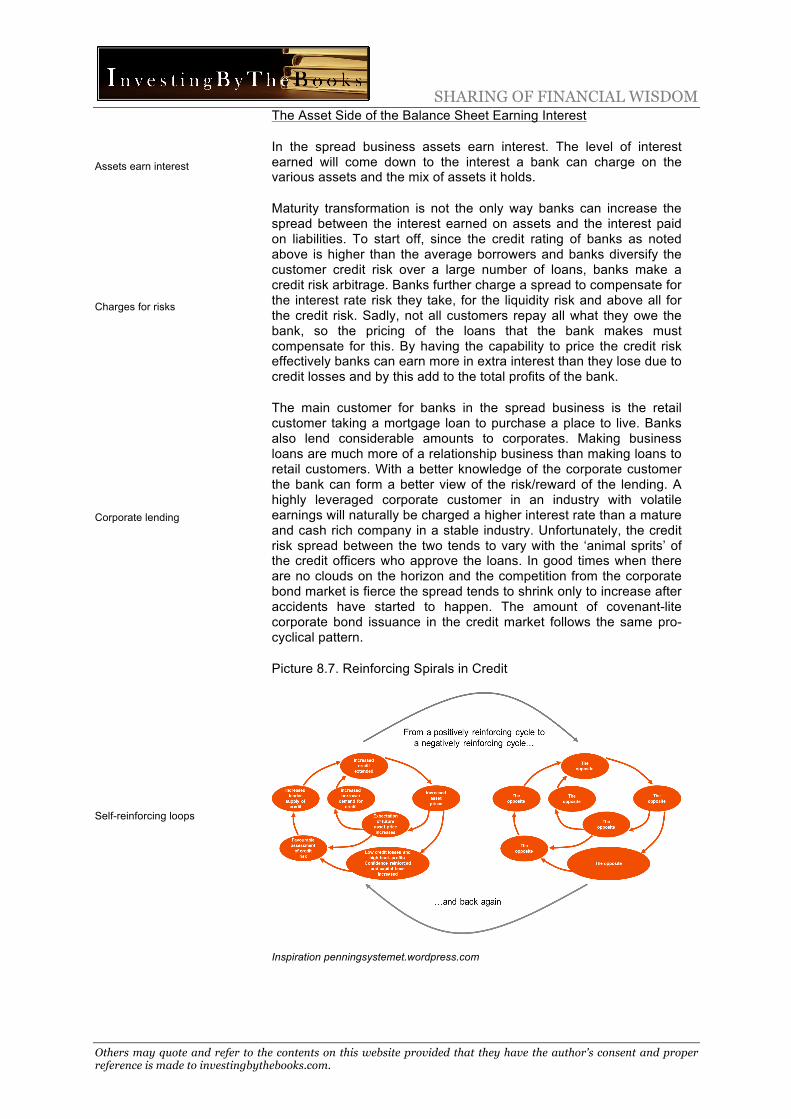

In the spread business assets earn interest. The level of interest earned will come down to the interest a bank can charge on the various assets and the mix of assets it holds.

Maturity transformation is not the only way banks can increase the spread between the interest earned on assets and the interest paid on liabilities. To start off, since the credit rating of banks as noted above is higher than the average borrowers and banks diversify the customer credit risk over a large number of loans, banks make a credit risk arbitrage. Banks further charge a spread to compensate for the interest rate risk they take, for the liquidity risk and above all for the credit risk. Sadly, not all customers repay all what they owe the bank, so the pricing of the loans that the bank makes must compensate for this. By having the capability to price the credit risk effectively banks can earn more in extra interest than they lose due to credit losses and by this add to the total profits of the bank.

The main customer for banks in the spread business is the retail customer taking a mortgage loan to purchase a place to live. Banks also lend considerable amounts to corporates. Making business loans are much more of a relationship business than making loans to retail customers. With a better knowledge of the corporate customer the bank can form a better view of the risk/reward of the lending. A highly leveraged corporate customer in an industry with volatile earnings will naturally be charged a higher interest rate than a mature and cash rich company in a stable industry. Unfortunately, the credit risk spread between the two tends to vary with the ‘animal sprits’ of the credit officers who approve the loans. In good times when there are no clouds on the horizon and the competition from the corporate bond market is fierce the spread tends to shrink only to increase after accidents have started to happen. The amount of covenant-lite corporate bond issuance in the credit market follows the same pro-cyclical pattern.

Picture 8.7. Reinforcing Spirals in Credit

Inspiration penningsystemet.wordpress.com

SHARING OF FINANCIAL WISDOM

Others may quote and refer to the contents on this website provided that they have the author's consent and proper reference is made to investingbythebooks.com.

Good times feed on themselves

Penetration – bank lending/GDP

Taking on more and more debt that costs less and less

Securities…

Clearly, banks’ loan volume growth depends on both supply and demand. Supply increases in good economic times when banks are in good financial shape, they have plenty of funds to lend and since customers are equally prosperous the prospects for them to repay the loans are deemed satisfactory. Demand also increases in good economic times as companies see good business opportunities which create investment needs and finally real estate prices rise bringing the needed size of mortgage loans up with them in a self-fulfilling spiral. Unfortunately the spiral at times spins in the opposite direction.

The correlation between GDP growth and bank lending growth is very high and there is also some correlation between GDP/capita and household loans/GDP, i.e. wealthier people borrow more in relative terms. However, there are also secular trends in loan penetration (i.e. in the loan volume in relation to GDP) as economies de-lever and re-lever. If loan growth far outstrips GDP growth, so-called increasing penetration, this can be a warning signal of a coming credit bubble. Prior to the financial crisis 2007/08 Spain and Ireland saw significantly increasing loan penetration.

The debt to income levels have increased significantly in Sweden since 1995 while the declining interest rate levels simultaneously has made the burden of these growing loans continuously lighter to carry.

Picture 8.8. Left: Household debt-to-income ratio. Right: Household interest expenditure

The data is for Sweden. The dotted lines are the Riksbank’s forecasts. Source: Financial Stability Report 2016:1, Riksbanken.

As an alternative to making loans the bank can invest the available money in securities earning interest or receiving dividends. Making loans are generally more profitable but holding securities gives the bank required liquidity. The accounting of the securities owned is a tricky issue since securities are valued differently according to management’s stated intention of how long they will own them. Securities kept for the short term are called trading securities (which is only an accounting label and doesn’t mean that the bank intends to use them for the proprietary trading business) and must be recorded at fair value, i.e. current market value. Securities held for the mid-term are called available-for-sale securities and they are also to be recorded at fair value. Finally, bonds held for the longer term are called held-to-maturity investments and they are recorded at historical cost or book value. The held-to-maturity assets are often called the banking book while the other assets are called the trading book.

SHARING OF FINANCIAL WISDOM

Others may quote and refer to the contents on this website provided that they have the author's consent and proper reference is made to investingbythebooks.com.

…vary in accounting treatment

Liabilities costing interest

Deposits…

Any change in the value of securities held for trading is shown in the income statement while changes in the value of securities available-for-sale is recognized to the equity through the other comprehensive income statement as long as they aren’t sold and obviously securities held-to-maturity show no change in accounting value as long as they are kept. There are two issues here. First, if there isn’t a reliable market value then management has the choice to use theoretical models to establish fair value. Models like this introduce subjectivity in the valuation. Secondly, the intended investment horizon is a choice made by the holder of a security. Not in theory but in practice this opens up for switching the intended horizon depending on which gives the highest asset value. This was a feature among US banks in 2008/09 when plenty of troubled bonds suddenly became “investments” and by this could be recognized at historical cost.

The Liability Side of the Balance Sheet Costing Interest

It stands to reason that the spread between the interest earned on assets and the interest paid on liabilities isn’t only determined by the pricing and mix of the assets but also by the pricing and the mix of the liabilities. In today’s low interest rate environment it might not be obvious, and banks naturally want to point to their other advantages such as for example excellent customer service, but there is a competitive market for attracting deposits and some of this competition comes down to pricing, i.e. the interest offered on deposits.

Most think of deposits as a way to save and receive interest but for banks deposits are loans made to the bank that allow them to be in business. Banks compete for deposits because normally this is the cheapest form of financing and banks can in theory make money simply by having inflows of money from deposits and investing them in the overnight interbank market or with the central bank. However, it’s not only deposits that compete for the customers’ money. There are numerous other investment alternatives available. In for example Sweden an unusually large part of the retail customers’ money is invested in mutual funds making Swedish banks relatively dependent on funding sources other than deposits. Then again, the banks themselves have a large part of the mutual fund market earning them nice fees.

SHARING OF FINANCIAL WISDOM

Others may quote and refer to the contents on this website provided that they have the author's consent and proper reference is made to investingbythebooks.com.

…have competition

Current accounts or demand deposits

Term deposits

Cheap funding

Retail deposit rates still not below 0%

Corporate deposits

Picture 8.9. Fund managers competing with bank deposits

Source: Google Images

Deposits are of two primary types. On the one hand there are current accounts or demand deposits where savers even in normal interest rate environments receive close to zero interest but can access their funds whenever they like. On the other hand there are term deposits that comes with some type of liquidity condition such as the obligation to give notice for example three month prior to a withdrawal or deposits that are locked for a fixed period. Term deposits give the customers higher interest and for the bank they are clearly more expensive but on the other hand their longer duration makes the bank less interest rate sensitive.

Access to cheaper funding from deposits was an important driver of bank profitability when interest rates were higher. Also, variations in interest rate levels added to the profitability as banks usually were slightly quicker to adjust market interest increases on loans than they were on deposits, while interest rate declines always were promptly visible in deposit rates.

With all interest rates so close to zero today the value of deposits has decreased from an earnings point of view. In theory, the interest on the interbank market could, as some central banks’ policy rates, turn negative while banks so far have refrained from negative interest rates on deposits for retail customers to curb cash outflows. For the cynical reader negative interest rates could be interpreted as one reason why banks are so keen on the digitalization of money. With no physical bills and coins left outstanding people cannot withdraw their money out of the financial system and place their money in the mattress in case of negative interest rates charged on deposits.

Corporate deposits are considered less valuable than retail deposits as corporations demand higher interest and often have deposits at several banks which make it easy for them to quickly leave the bank in times of trouble. Still, even in the case of highly liquid demand deposits most customers – retail or corporate - don’t normally withdraw their money on a daily basis. The true average maturity of deposits is several years but it varies over time and averages don’t matter much in times of stress.

SHARING OF FINANCIAL WISDOM

Others may quote and refer to the contents on this website provided that they have the author's consent and proper reference is made to investingbythebooks.com.

Loan-to-deposit ratio

TED is an acronym formed from T-bill and ED, the ticker symbol for the Eurodollar futures contract

Other funding

Secured and unsecured loans

Covered bonds

Mortgage bonds

Considering how money is created through the above-described money multiplier and that the asset side and the liability side of a balance sheet must balance it should surprise few that deposit growth and asset growth tend to move in tandem. However, since banks have other means of funding themselves the liability mix changes over time. A common ratio that illuminates this mix is the loan-to-deposit ratio that at least to some extent is a measure of banks’ loan capacity.

Alternative, generally more expensive, sources of funds for banks are borrowing from other banks with excess liquidity in the interbank market or borrowing from the central bank. These loans tend to have short maturity. The interest rate differential between loans made on the U.S interbank market and short term government bills are called the TED-spread.

As a corporation a bank can also issue various types of interest bearing securities to provide funding. Swedish banks have larger non-deposit funding than most other banks since Swedes tend to favor mutual funds over deposits. These securities can be secured or unsecured, they can be senior or junior and they vary in maturities.

Secured loans are those that are protected by an asset or collateral of some sort, like a mortgage or an auto loan. Unsecured loans offer no such protection and examples include credit cards, student loans and personal loans. If there are several loans taken by a bank the question arises which lender will be paid first if the bank ends up in economic difficulties. A senior loan will have the legal claim to the bank’s assets prior to a junior (or subordinated) loan. This is a relative game so a loan can be senior to one other loan but junior to a second. Even though it’s not a security, deposits are seen as unsecured subordinated debt, albeit with a government guarantee up to a certain amount.

Banks can issue unsecured bonds and they can be senior and subordinated. So-called covered bonds are secured and provide the bondholder with collateral protection in a pool of loans and as secured they are a reasonably low-cost funding for banks. The pools of loans are generally mortgages that are legally segregated from the bank but stay on the balance sheet. The bank issues the loans to the public with the mortgage loans as collateral and the loans of course in their turn have collateral in the underlying real estate. The cash flow from the mortgages back up the interest rate payments to the bondholders and the bonds trade on a relatively liquid secondary market.

There are often regulatory restrictions on the loan-to-value ratio of the mortgages that can be pooled for covered bonds. Also in most cases banks, in all secured types of lending, will seek to ensure that the value of the collateral is at least 20-30% higher than the loan principal. In case of a bank failure the bondholder receives the pool of loans, as it will be ejected from the bank. The only way for the bondholder to lose money is if the bank first defaults and runs out of equity, the mortgage loan then defaults and the price of the collateralized real estate has finally dropped so low that the loan-to-value exceeds 100%.

SHARING OF FINANCIAL WISDOM

Others may quote and refer to the contents on this website provided that they have the author's consent and proper reference is made to investingbythebooks.com.

U.S. securitization

MBS – Mortgage-backed security

RMBS – Residential mortgage-backed security

Market-risk anyone?

Fannie and Freddie in the subprime crisis

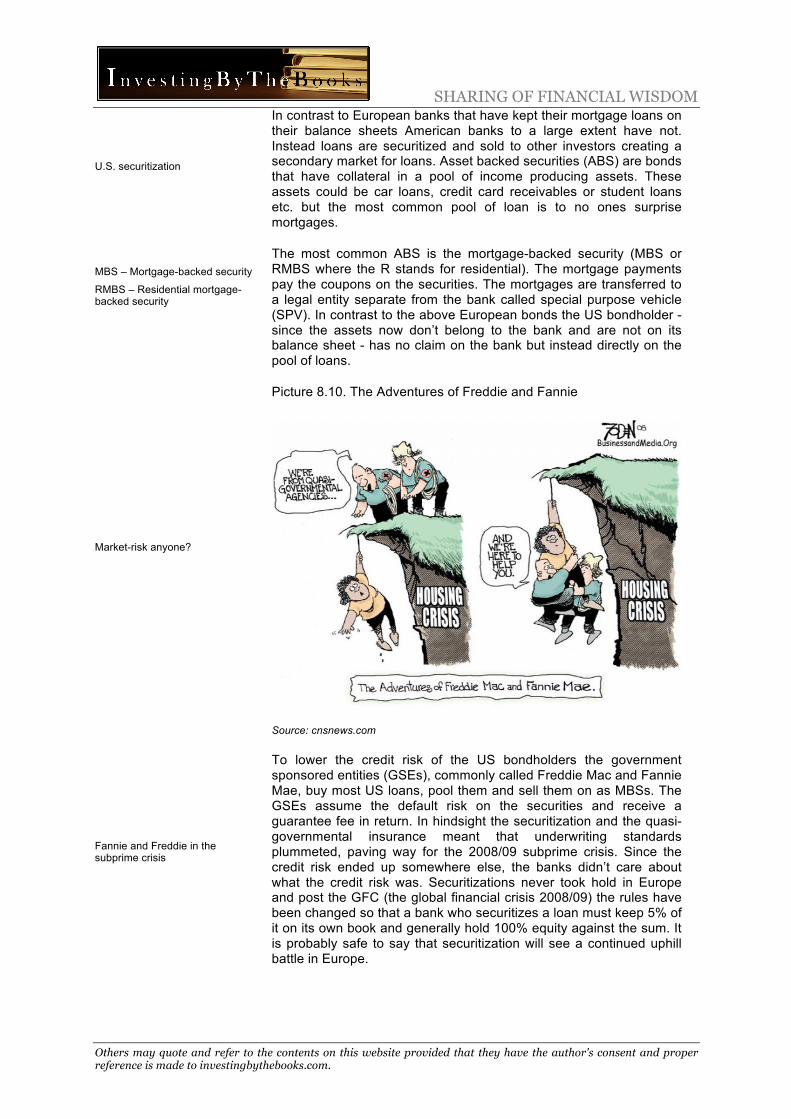

In contrast to European banks that have kept their mortgage loans on their balance sheets American banks to a large extent have not. Instead loans are securitized and sold to other investors creating a secondary market for loans. Asset backed securities (ABS) are bonds that have collateral in a pool of income producing assets. These assets could be car loans, credit card receivables or student loans etc. but the most common pool of loan is to no ones surprise mortgages.

The most common ABS is the mortgage-backed security (MBS or RMBS where the R stands for residential). The mortgage payments pay the coupons on the securities. The mortgages are transferred to a legal entity separate from the bank called special purpose vehicle (SPV). In contrast to the above European bonds the US bondholder - since the assets now don’t belong to the bank and are not on its balance sheet - has no claim on the bank but instead directly on the pool of loans.

Picture 8.10. The Adventures of Freddie and Fannie

Source: cnsnews.com

To lower the credit risk of the US bondholders the government sponsored entities (GSEs), commonly called Freddie Mac and Fannie Mae, buy most US loans, pool them and sell them on as MBSs. The GSEs assume the default risk on the securities and receive a guarantee fee in return. In hindsight the securitization and the quasi-governmental insurance meant that underwriting standards plummeted, paving way for the 2008/09 subprime crisis. Since the credit risk ended up somewhere else, the banks didn’t care about what the credit risk was. Securitizations never took hold in Europe and post the GFC (the global financial crisis 2008/09) the rules have been changed so that a bank who securitizes a loan must keep 5% of it on its own book and generally hold 100% equity against the sum. It is probably safe to say that securitization will see a continued uphill battle in Europe.

SHARING OF FINANCIAL WISDOM

Others may quote and refer to the contents on this website provided that they have the author's consent and proper reference is made to investingbythebooks.com.

CP – Commercial paper

CD – Certificates of Deposit

Deals on primary and secondary markets

Some of what investment banks do

U.S. dominants

Commercial paper (CP) and Certificates of Deposit (CD) are short-term unsecured wholesale funding. Securities with shorter maturities offer banks cheaper funding than those with longer and prior to the global financial crisis this was a growing part of the bank liabilities. New liquidity rules and stress tests that assume that this funding cannot be renewed in a negative scenario have made the instruments much less attractive.

Unsecured debt in banks has historically been cheaper than for companies in general as investors – rightly - were counting on governments to bail out banks in case of trouble. The new bail-in rules post the crisis are trying to pass the buck back to the banks, which is changing the status of senior and junior unsecured debt in banks. We will come back to this below.

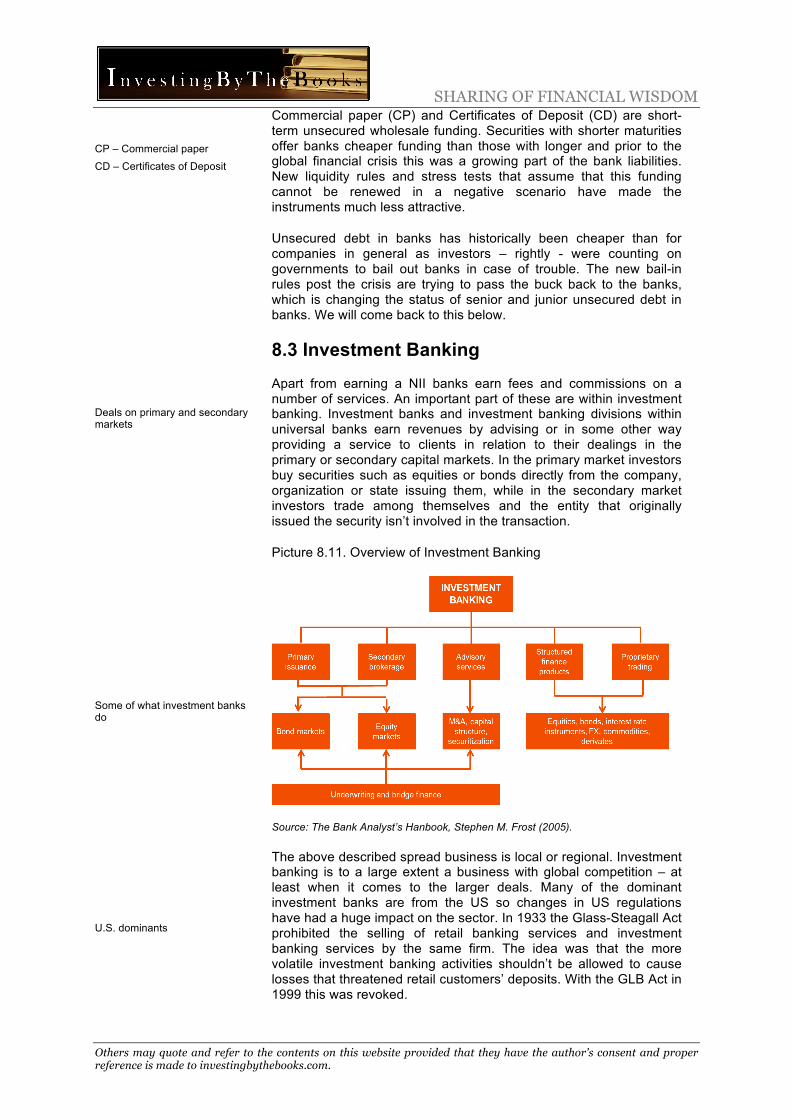

8.3 Investment Banking Apart from earning a NII banks earn fees and commissions on a number of services. An important part of these are within investment banking. Investment banks and investment banking divisions within universal banks earn revenues by advising or in some other way providing a service to clients in relation to their dealings in the primary or secondary capital markets. In the primary market investors buy securities such as equities or bonds directly from the company, organization or state issuing them, while in the secondary market investors trade among themselves and the entity that originally issued the security isn’t involved in the transaction.

Picture 8.11. Overview of Investment Banking

Source: The Bank Analyst’s Hanbook, Stephen M. Frost (2005).

The above described spread business is local or regional. Investment banking is to a large extent a business with global competition – at least when it comes to the larger deals. Many of the dominant investment banks are from the US so changes in US regulations have had a huge impact on the sector. In 1933 the Glass-Steagall Act prohibited the selling of retail banking services and investment banking services by the same firm. The idea was that the more volatile investment banking activities shouldn’t be allowed to cause losses that threatened retail customers’ deposits. With the GLB Act in 1999 this was revoked.

SHARING OF FINANCIAL WISDOM

Others may quote and refer to the contents on this website provided that they have the author's consent and proper reference is made to investingbythebooks.com.

IB turned UB

M&A – Mergers & Acquisitions

ECM – Equity Capital Markets

DCM – Debt Capital Markets

USD 61 billion

Corporate finance

Love the suspenders!

Pro-cyclical M&A

Post the financial crisis and despite the recent IPO-boom the revenues from investment banking have been lower than previously. Given the changing rules and turmoil in the crisis that threatened many IB-firms, many of the largest investment banks are today parts of universal banks. The only big investment banks that still generate more than half their sales from investment banking are Goldman Sachs and Credit Suisse.

Primary Markets

In the primary market banks earn revenues through fees mainly within M&A, ECM and DCM. The revenue line in the income statement often says “advisory and origination fees” where the former relates to M&A and the latter to ECM and DCM. Since such revenues are quite high profile and require relatively low levels of bank capital to support them, they are highly sought after and competition is fierce. The competition is however not on prices as fee levels have been relatively stable over the last decade.

The leaders of the advisory and origination business are large US and European banks. According to Dealogic the global market amounted to USD 61.1bn in 2014 and the top ten companies held slightly more than half of the global market shares.

In academia the term corporate finance is an area within finance that according to Wikipedia deals “with the sources of funding and the capital structure of corporations and the actions that managers take to increase the value of the firm to shareholders”. The corporate finance department in banks is an advisory business in the corporate finance discipline that mainly deals with M&A and ECM. In their characteristically modest fashion the employees of corporate finance departments simply call themselves “bankers”. With private equity’s (PE) rise to economic power, corporate finance professionals have seen increased competition. PE is involved in a growing amount of interesting deals and the PE professionals often have the skill to handle many of the previous corporate finance tasks internally.

Picture 8.12. Legendary Bankers

Felix Rohathyn, Lazard, Steve Rattner, Lazard, Bob Greenhill, Smith Barney, Bruce Wasserstein, Wasserstein Perella & Co, Joe Perella, Wasserstein Perella & Co and Ken Wilson, Goldman Sachs. Source: Google Images

The highly cyclical M&A practice is the embodiment of a relationship business as it deals with advice on major corporate events like acquisitions, mergers, restructurings and takeover defense strategies. The M&A banker has to nurture a wide network of corporate executives and board directors. You might think that companies would take the opportunity to do these deals in weak economic environments when asset prices are low but it is rather the opposite as greater trust in the economic outlook and filled war

SHARING OF FINANCIAL WISDOM

Others may quote and refer to the contents on this website provided that they have the author's consent and proper reference is made to investingbythebooks.com.

IPO – Initial Public Offering

Pitching power and placing power

Remuneration systems

Issuing bonds have been…

…a good business

chests give managers greater confidence to carry out the deals. In fairness they at times also pay for the acquisitions with their equally inflated own stock. The payment to the bank for M&A services is generally a fee comprising of a certain percentage of the transaction value.

ECM is a service provided to corporations related to raising equity capital including deals such as private placements, IPOs, rights issuances and so on. The term origination simply means that the ECM team creates the deal. The ECM team will help companies execute equity transactions in the primary market by structuring and syndication of the deal, handling regulatory demands and by marketing and distributing the deal. For this service they charge a fee that is also a certain percentage of the transaction value.

The main ECM business is IPOs. In both ECM and DCM it’s easier for the bank to market and distribute the deal if they have a large distribution platform and a leading secondary market capability with highly regarded security analysts. Leading research on the secondary market is both vital when pitching for deals and when marketing them to institutional clients. Since the sellers of shares on the primary market want to sell at high prices, the ECM business tends to vary with the stock market valuation level. Expensive and non-volatile stock markets are prosperous IPO environments. IPO fees vary with deal size and with the risk profile of the company (the smaller and riskier company the higher percentage fee) but according to Dealogic they averaged 2.4% in Europe 2014.

Corporate finance departments often also supply ancillary services to corporations like for example structuring of management remuneration systems. These services are often seen as less flashy but provide stable income in less buoyant market environments.

DCM is the debt equivalent of the ECM function of corporate finance departments. Contrary to the US where corporations for a long time have used the capital markets for funding through issuance of corporate bonds, banks have been the primary and often only corporate funding vehicles in Europe. After the financial crisis the banks on the one hand have been forced to shrink their balance sheets making the supply of bank lending scarcer and on the other hand the corporate lenders themselves saw the benefit of a diversified supply to capital as banks were unwilling to make loans mid-crisis. Luckily then banks have the debt capital market (DCM) departments whose job it is to help companies issue corporate bonds.

In parallel European insurance regulation has created a need among insurance companies to shift some of their portfolio assets from equities to fixed income, creating a demand for corporate bonds. Consequently the European corporate bond market has seen good growth the last few years - although the tepid economic cycle has made the growth somewhat less impressive than some DCM-officers may have hoped for a few years back since bank loans still offer more flexibility.

SHARING OF FINANCIAL WISDOM

Others may quote and refer to the contents on this website provided that they have the author's consent and proper reference is made to investingbythebooks.com.

Commission, price spread and prop trading

FICC – Fixed Income, Currencies and Commodities

Declining inventory

The issuance of corporate debt is divided between the investment grade market where issuers have (or at least should have) lower credit risk and the high yield market with higher credit risk. The fees in European DCM vary mainly with the level of credit risk and in 2014 they were 0.4% according to Dealogic. The larger size of the investment grade issues skews this average number to the downside.

Secondary Markets

The secondary markets provide liquidity to existing owners of securities. Equities that are perpetual securities have a active secondary market with good liquidity at least for the larger companies. Corporate bonds are to a higher degree bought at issuance and kept for their full maturities. The weighted average maturity of a corporate bond portfolio is usually around 5-7 years. In secondary markets 1) bank employed brokers trade clients’ securities earning a commission, 2) banks act as market makers earning a spread from the price paid for a security when buying it from one customer and the price received when selling it to another or 3) banks trade in the market with their own money aiming to earn investment income – so called proprietary trading, or prop trading.

Starting in the 1990s up until the financial crisis 2007/08 trading revenue increased very sharply as a percent of banks’ risk weighted assets. Banks added assets with low regulatory risk weights to trading books, a form of regulatory arbitrage and an unintended consequence of capital rules that were meant to keep risks at bay. Today the trend is the opposite and according to Boston Consulting Group global investment banking revenues declined 5% to USD 228bn in 2015 and the investment banking ROE fell to a 6% post crisis low. Apart from relatively high costs the reason was mainly a decline in secondary trading. Fixed Income, Currencies and Commodities (FICC) profitability fell from 70% of the investment banking profit pool three years ago to 44% in 2015.

FICC is a mixture of operations trading in various assets either on the behalf of a client or on the behalf of the bank itself. Rates have been the biggest FICC revenue generator for banks and include government bond trading, interest rate derivatives such as interest rate swaps, money market instruments and municipal finance. This is still a manual telephone market to a large extent. Banks take a small spread between the seller (bid) and the buyer (ask) when executing a client’s deal. To facilitate the trades banks as market makers often hold a small inventory of securities. Most products have low risk but the volumes are large.

In credit, investment grade and high yield corporate bonds are traded as well as other types of tradable loans. As noted above the liquidity is at times relatively low and this is a telephone-based market. The lower the liquidity the higher the bid-ask spread. Since regulators have raised the capital requirements for a bank’s holding of securities the market making inventories of corporate bonds have been lowered further threatening the liquidity of the market. Given the popularity of packaged corporate bond products like corporate bond funds, high yield ETFs, emerging market credit ETFs and so on, it could turn ugly if too many retail investors want to exit at the same time.

SHARING OF FINANCIAL WISDOM

Others may quote and refer to the contents on this website provided that they have the author's consent and proper reference is made to investingbythebooks.com.

FX – Foreign exchange

Small stable spreads

DMA – Direct market access

Brokers

§ Sales

§ Sales traders

§ Traders

Yours…

Foreign exchange (FX) includes cash transactions plus a number of delta one and delta two derivatives. Banks again take a small spread between the seller (bid) and the buyer (ask). Electronic trading increasingly drives this market - the margins are low but the volumes massive. In the US and some European countries trading of securitized products is a large segment. Finally there is the commodities segment with spot and derivatives trading in for example oil, metals or agricultural products. This is usually a small part of FICC.

From one point of view revenues earned from a bid-ask spread in market making for clients is a trading income as the bank owns the securities it has bought until it sells them. However, the spreads are relatively stable and are more dependent on trading volumes so the character is more similar to the commissions earned in equities. The bid-ask spread on highly liquid securities like 5-year rate swaps has varied between 0.5 bps and 1.5 bps the last decade. The FX spread on USDEUR has varied between 1 and 2 bps. To support the FICC business there are a number of commodity, fixed income and FX research analysts and a few economists. The chief economist of a bank is often a high profile position that comes with plenty of media coverage.

Moving on, the equity segment generates revenues from cash equities, equity derivatives and from prime services. In cash equities banks trade in equities earning commissions on trades executed or investment income on prop trading. The business also includes block trades and revenues from giving customers direct market access (DMA) to execute their own trades. The buying and selling of cash equities is fully computerized since many years which has increased customer transparency and significantly lowered commission levels. This has also spilled over on the funds available for equity research. According to the Economist, quoting Frost Consulting, the global equity-research budgets have dropped from USD 8.2bn in 2007 to an expected USD 3.4bn in 2017 – that equates to an annual decline of 8.4%.

The cash equity department is generally where the equity research department is located. General media often name those who execute the deals “brokers” but due to varying roles the internal lingo is more nuanced. The sales staff that market both the bank’s equity research and its transaction capabilities to institutional investors are simply called “sales”, the brokers executing the transactions that institutional investors make are called “sales traders” and those who trade equities with the bank’s own money are generally just called “traders”.

Picture 8.13. Just Another Day at the Job For the Brokers?

Source: Google Images

SHARING OF FINANCIAL WISDOM

Others may quote and refer to the contents on this website provided that they have the author's consent and proper reference is made to investingbythebooks.com.

CSA – Commission sharing agreements

OTC – Over the counter

Securities exchanges…

…have digitalized

When equity sales traders execute a transaction on behalf of an institutional investor the bank never owns the securities but only facilitates the matching between an external buyer and an external seller and by this earns a commission amounting to a certain percent of the transaction value. This commission pays for both the execution handled by the sales trader, the marketing of the sales representative and the advice of the research analyst. Within short this bundling of equity research and execution services will not be allowed towards mutual funds in the EU, who will then have to pay for the two services separately in an arrangement called commission sharing agreements (CSA). For the immediate future other institutional investors like pension funds and insurance companies can still pay for the bundled service through commissions.

Banks also trade in equity derivatives such as options, futures, forwards and swaps plus in convertible bonds and structured products. The bulk of these derivates have been so-called over the counter (OTC) that is it’s a transaction done directly between two parties without the usage of an exchange. Here it could be harder to track the business model from the outside. Some derivatives and structured products offered to clients could see the bank take the other side of the trade and hold the exposure (or it may instead sell the exposure to the market). In prime services banks help hedge fund clients with the financing of trades and with clearing and reporting. They also help in raising capital and stock lending. Revenues come from financing revenues and fees related to borrowing, stock lending, capital raisings etc.

The bank sales traders and proprietary traders execute their transactions on securities exchanges. There are separate exchanges for the various types of securities. The exchanges make money by charging a small fee on the transaction volume but also by fees charged when companies list their shares on the exchange, fees as payment for market data, technology services, co-location of servers, risk management services etc.

Historically some of the bank employees would have to be physically present at the exchange to participate in the manual open outcry process in trading pits like the one to the left in the picture below. Over time the markets have in general seen a digitalization or at least moved to be performed over the phone (meaning bank staff now stays on their own premises like the UBS trading floor to the right in the picture). To a large extent an exchange today is a virtual feature only present on a server. Exchanges have seen their fair amount of issues the last decade. A narrowing of bid-ask spreads and lowering of commission levels, a fragmentation over several competing exchanges has meant lower liquidity on any one of them separately.

SHARING OF FINANCIAL WISDOM

Others may quote and refer to the contents on this website provided that they have the author's consent and proper reference is made to investingbythebooks.com.

Some of the drama is gone

Derivates

Digitalizing the corporate bond trading?

Agency vs prop trading

Chinese walls

Picture 8.14. Traders have Moved From the Pit

Source: Google Images

Derivates are trades in several of the above described asset classes. The markets for OTC swaps and forwards are absolutely huge. OTC instruments have as noted above never been traded on an exchange. Instead the traders execute the deals through their own personal networks with other banks’ traders in the market. With some OTC instruments playing lead roles in the GFC and due to the low transparency of the markets there has been a push to move more of the OTC market towards being cleared by clearinghouses. A clearinghouse provides stability by taking an intermediary role in all deals removing the direct counterparty risk between those performing the transaction. The move to cleared securities improves customer visibility and has tended to pressure bank profits.

As electronic trading has taken over in equities, FX and parts of the derivatives markets the question sometimes arises if the telephone based corporate bond markets also will turn electronic and if this would threaten the profitability. It’s probably no doubt that the increased transparency would lower the profitability if it would happen as it has in for example equities. However, the risk to banks is probably low in the immediate future. The corporate bond market is wide but not very deep. That is, there are often dozens of bonds issued by a company with very different terms and conditions that all trade separately but very rarely. Compare this to common stocks where all have the same rights and the trading volume generally is sufficiently deep. Time will tell.

The fact that a market-making sales trader acts like a buyer, then a temporary owner and finally a seller when executing a deal (and on top of that owns an inventory of securities to facilitate this role) makes the line between the agency trading for clients and the prop trading for the bank by the trader very hard to draw. In both cases the bank is on one side of every trade and an external investor is on the other and both take risk in the market. The demarcation line is more a matter of who initiated the deal.

Engaging in the combination of client facilitation and prop trading offer the risk of conflicting interests as the prop trader can gain advantages from knowing about the client flows. To hinder the trader from front running the sales trader’s deals, making a profit on the bank’s clients’ behalf, regulation requires that the sales traders and the traders at banks have to be separated. There has to be so-called Chinese walls with regards to physical location and information.

SHARING OF FINANCIAL WISDOM

Others may quote and refer to the contents on this website provided that they have the author's consent and proper reference is made to investingbythebooks.com.

Volcker rule

More on the shelf

Asset management and wealth management

Who would you nominate as the 10th investor?

AuM – Assets under management

Big size portfolios

Mainly due to the ethical aspects of the risk for trading losses and the solvency consequences of these, but also because of the conflict of interest the US Volcker rule has meant that US prop trading has been spun off from the investment banks (but market making remains). In Europe prop trading is still allowed but with changing rules, the capital that the bank has to hold against the trading assets has increased making the new asset-heavier business significantly less attractive as it cannot be levered as high as before.

8.4 The Other Stuff The financial department store has more products on its shelf earning additional fees and commissions. Some of the more prevalent services are asset and wealth management, payment services, card issuance, cash management for companies, custody services, insurance and sometimes real estate brokerage.

Asset management refers to providing investment products such as for example mutual funds or ETFs to retail clients and institutional investors. Wealth management is a hybrid between asset management and retail banking and refers to specialized and individually tailored services provided to meet the wealth-planning, investing & financial management needs of wealthy individuals. Those individuals are often segmented according to their wealth. The descriptive labels include affluent, wealthy, high net worth and ultra-high net worth.

Picture 8.15. Some Legendary (Equity) Investors

Upper left to right: Philip Fisher, Warren Buffett, Ben Graham, Peter Lynch, Ed Thorpe, Jim Simmons, Seth Klarman, George Soros and Julian Robertson. Source: Google Pictures.

Fees are generally set as a certain percentage point of managed assets. Both asset and wealth management are highly attractive to banks since they generate recurring fees without requiring much capital and the client relationships are relatively sticky. After a certain scale of assets under management (AuM) is reached the profit margins can be very attractive. Global wealth management is dominated by the big investment banks like for example UBS, Merrill Lynch, Morgan Stanley, Credit Suisse and Royal Bank of Canada.

On the other hand, and even though the investment banks are major players, the global asset management industry is dominated by non-banks like for example Blackrock, Vanguard, Fidelity, Capital and PIMCO. These rival the pension funds, the insurance companies and the sovereign wealth funds for the top spots as the world’s largest asset portfolio managers.

SHARING OF FINANCIAL WISDOM

Others may quote and refer to the contents on this website provided that they have the author's consent and proper reference is made to investingbythebooks.com.

A good business getting tougher

Alternatives…

…and passive investments taking share

BCG – Boston Consulting Group

Asset and wealth management services are savings alternatives to placing money on deposit accounts. Despite fee pressure and a mix shift towards index based savings products the combination of rising asset values and to some extent inflows into the portfolios means that the combined global investment management industry has seen slow but okay growth the last few years.

2015 was tougher for the asset management sector with both stalling asset prices and asset inflows plus continued fee pressure. Fees have been in a slow decline for quite some time. According to a report from Morningstar European equity fond fees averaged 1.27%, down from 1.43% three years earlier. Sweden had the third lowest fees where the average fee was 0.94%, down from 1.09% three years earlier.

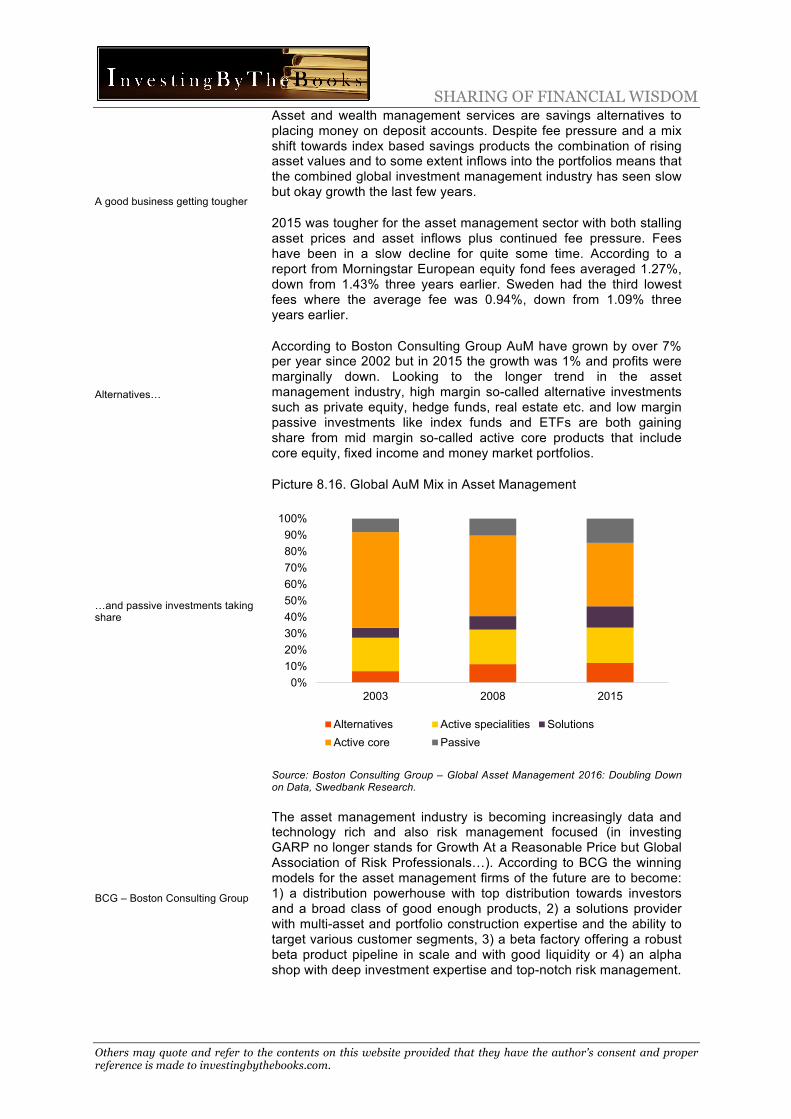

According to Boston Consulting Group AuM have grown by over 7% per year since 2002 but in 2015 the growth was 1% and profits were marginally down. Looking to the longer trend in the asset management industry, high margin so-called alternative investments such as private equity, hedge funds, real estate etc. and low margin passive investments like index funds and ETFs are both gaining share from mid margin so-called active core products that include core equity, fixed income and money market portfolios.

Picture 8.16. Global AuM Mix in Asset Management

Source: Boston Consulting Group – Global Asset Management 2016: Doubling Down on Data, Swedbank Research.

The asset management industry is becoming increasingly data and technology rich and also risk management focused (in investing GARP no longer stands for Growth At a Reasonable Price but Global Association of Risk Professionals…). According to BCG the winning models for the asset management firms of the future are to become: 1) a distribution powerhouse with top distribution towards investors and a broad class of good enough products, 2) a solutions provider with multi-asset and portfolio construction expertise and the ability to target various customer segments, 3) a beta factory offering a robust beta product pipeline in scale and with good liquidity or 4) an alpha shop with deep investment expertise and top-notch risk management.

0%10%20%30%40%50%60%70%80%90%

100%

2003 2008 2015

Alternatives Active specialities SolutionsActive core Passive

SHARING OF FINANCIAL WISDOM

Others may quote and refer to the contents on this website provided that they have the author's consent and proper reference is made to investingbythebooks.com.

Trusts

Payments

Overdraft fees

Card payments

Corporate banking

Trade finance

Trust services is a related service similar to wealth management where banks manage the property held by trusts. This is often securities portfolios but could also involve real estate, land etc.

We now move on to payments. Since banks provide the accounts that individuals and corporations use to deposit their funds in it is also natural that they have come to provide the payment service for when money should be moved between deposit accounts as payment for goods and services. From the society’s point of view this is one of the more vital functions performed by banks and it’s one that is generally paid for by fees on the transaction. The payment fee income is sometimes specified in the financial accounts of banks and sometimes not, but it is usually a big part of total fee income.

Another important fee income is overdraft fees charged when a customer makes a payment but have non-sufficient funds on his account. Banks then allow the transaction but charge an overdraft fee. Less common today but still existent are monthly deposit fees, i.e. a fee for providing the client the service of having a deposit account to start with. The argument for such a fee is that there is a customer value related to the service of safe storage of money.

Related, but still separate, are fees from payment card payments. A payment card transaction involves a number of players who all split the fee that is deducted from the price that the consumer pays for the product or service. Generally the bank that issued the payment card to the consumer gets about 2/3rds of the fee and the bulk of the rest is shared between the network companies like VISA and Mastercard and the so-called merchant acquirers. This split is motivated by the fact that the banks shoulder the credit risks of the transaction. Fraudulent use of payment cards is a growing problem. We will take a closer look at the payments market in the segment fintech below.

Further, banks provide corporate clients with cash management, working capital financing and trade finance. Over 80% of global trade is reliant of the latter service. Trade financing reconciles the divergent needs of an exporter and an importer lowering the friction of transactions where the parties often don’t have intimate knowledge of each other. An exporter would prefer to be paid upfront by the importer for an export shipment. The risk to the importer is then that the exporter may simply pocket the payment and refuse shipment. Conversely, if the exporter extends credit to the importer, the latter may refuse to make payment or delay it inordinately.

The most common form of trade finance is letters of credit where the bank guarantees payment to the seller as long as delivery conditions have been met. If the buyer defaults and the seller risk a credit loss the bank will cover the cost. This is similar to selling insurance and similar to insurance the bank seldom has to shoulder its responsibility but when it happens it can prove costly. The bank could also buy the receivables (or the exposure of the receivables) from the seller at a discount to the cash value of the transaction.

SHARING OF FINANCIAL WISDOM

Others may quote and refer to the contents on this website provided that they have the author's consent and proper reference is made to investingbythebooks.com.

NCI on the decline

Swedbank’s 2015 statements

Loans to the public

70% real estate

Retail dominated

Cash and balances with central banks

Overall, net commission income (NCI), i.e. the total fee income from various products – in investment banking or other – rose as a percent of total income from the early 1980s up until the financial crisis. In many well-known banks it accounted for more than half of income. After the crisis many banks have refocused on the more mundane net interest income.

8.5 Financial Statements It is obviously critical to understand the business operations of banks. But to understand a bank it’s also beneficial to understand the financial statements. In banking the balance sheet is to a large extent a part of the operations and as such drives the income statement. We will exemplify the financial statements of a bank by looking at the 2015 balance sheet and income statement of a prestigious Swedish bank – Swedbank. In this we are only using public sources: the 2015 annual report, the 2015 risk management and capital adequacy report and the Q4, 2015 fact book (all in all 455 pages…).

The Balance Sheet

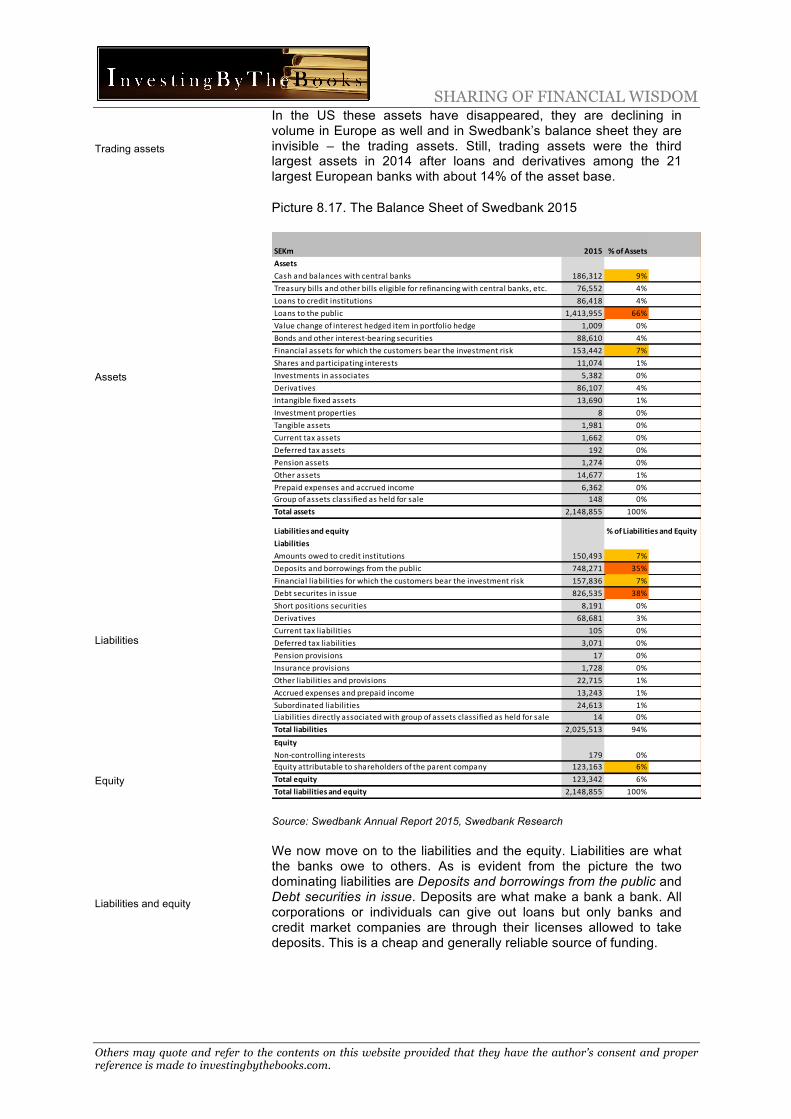

Assets are what are owed to the bank by others. In principle (if not in the accounting) they are loan receivables, securities that are on the balance sheet and derivatives that are mainly off the balance sheet. The assets for Swedbank consist of a long number of line items. Three of them make up 82% of the balance sheet and Loans to the public itself accounts for 66% of the balance sheet or SEK 1.4tr – equivalent to more of a third of Swedish GDP that year. Out of the sum, 84% was lent in Sweden and the rest abroad – mainly the Baltics. The largest and fastest growing part of the loans was made to private customers who accounted for 58% of the loans (private mortgages 49% and the remaining 9% was mainly lending to private tenant associations). The second largest part of the loans was to corporate customers that accounted for 33%. Out of this property management stood for 14%, agriculture, forestry, fishing 5%, manufacturing 3% and lending to corporations in other sectors 11%.

Apart from lending to private customers and corporations 9% of the lending is to financial institutions such as other banks. In 2015 70% of the loans (and 49% of total assets, not counting mortgage bonds that add another 2%) was related to real estate in some form and this is slightly up from 66% in 2014 and 67% in 2013.

For a bank loans should be seen as a sold product that will produce income in the future. Loans are shown on a net basis, i.e. net of loan loss reserves. Swedbank is a universal bank but it is, as most medium sized European banks, still relatively retail dominated as can be seen from the relative size of the loans in the asset mix. Among the 21 largest European banks loans accounted for 49% of assets 2014.

Since loans are illiquid and deposits and other funding are liquid banks need to keep a certain portion of liquid assets as a hedge against outflows. Looking at the picture of the balance sheet below, the second largest asset after the dominating loans is Cash and balances with central banks that accounts for 9% of the asset base. This is held in part for business related liquidity reasons and increasingly in part for regulatory related liquidity reasons.

SHARING OF FINANCIAL WISDOM

Others may quote and refer to the contents on this website provided that they have the author's consent and proper reference is made to investingbythebooks.com.

Investments

Insurance assets

Derivates

A huge gross amount…

…but smaller net