BANK INDONESIA POLICY ROLE TO ACCELERATE ACCESS TO FINANCE FOR MSMEs Financial Access and SME Development Department 2014 Eni V. Panggabean, Ph.D Executive Director The views expressed in this presentation are the views of the author and do not necessarily reflect the views or policies of the Asian Development Bank Institute (ADBI), the Asian Development Bank (ADB), its Board of Directors, or the governments they represent. ADBI does not guarantee the accuracy of the data included in this paper and accepts no responsibility for any consequences of their use. Terminology used may not necessarily be consistent with ADB official terms.

Bank Indonesia Policy Role to Accelerate Access to Finance for MSMEs

Dec 11, 2015

This presentation was given at the Policy Dialogue: Financing SMEs: Sharing Ideas for Effective Policies which was held in Jakarta, Indonesia on 15-16 October 2014.

Read more about the event: http://bit.ly/1VZsLcb

Read more about the event: http://bit.ly/1VZsLcb

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

BANK INDONESIA POLICY ROLE TO ACCELERATE ACCESS TO FINANCE FOR MSMEs

Financial Access and SME Development Department

2014

Eni V. Panggabean, Ph.D Executive Director

The views expressed in this presentation are the views of the author and do not necessarily reflect the views or policies of the Asian Development Bank Institute (ADBI), the Asian Development Bank (ADB), its Board of Directors, or the governments they represent. ADBI does not guarantee the accuracy of the data included in this paper and accepts no responsibility for any consequences of their use. Terminology used may not necessarily be consistent with ADB official terms.

OUTLINE BACKGROUND

MSME CHALLENGES

REGULATION TO ACCELERATE MSME FINANCING

BI INITIATIVES TO PROMOTE MSME FINANCING

THE WAY FORWARD

2

I

III

II

IV

V

3

The strong resilience of the Indonesia economy among other is due to the strong domestic demand, which is supported by the pivotal role of MSME

I. BACKGROUND

Source : Ministry of Cooperatives and SME

99.9% of 55 million business

units

absorb around 97,2% of total

labor force.

contribution around 57,48%

to the GDP

contribution around 14.06% to export (non

oil and gas)

Indonesia’s economy resilience

A. THE ROLE OF MSMES

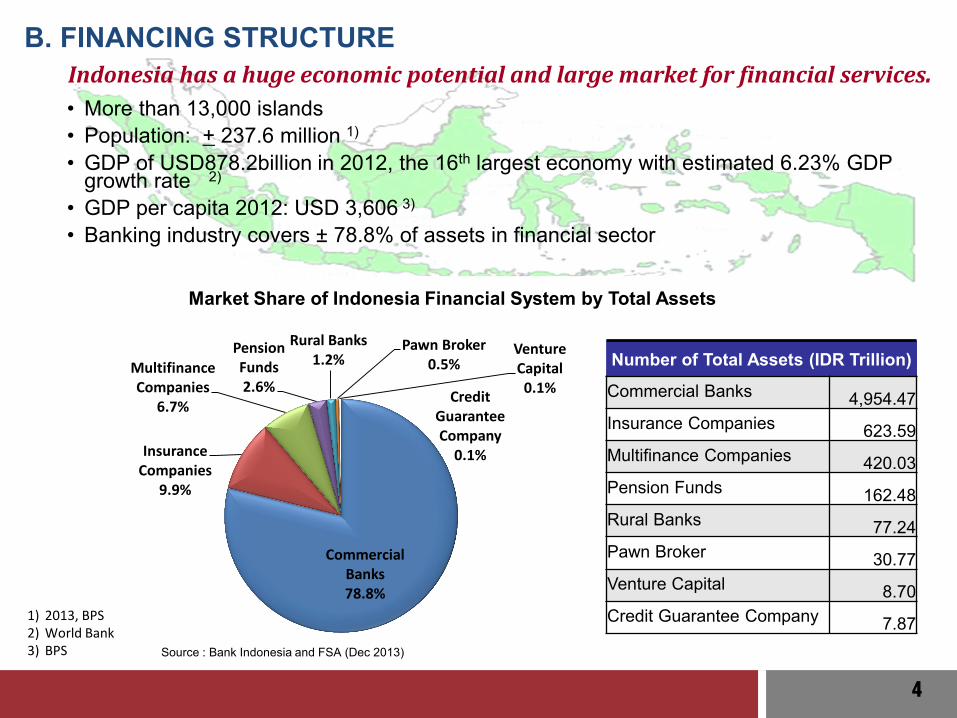

Number of Total Assets (IDR Trillion)

Commercial Banks 4,954.47

Insurance Companies 623.59

Multifinance Companies 420.03

Pension Funds 162.48

Rural Banks 77.24

Pawn Broker 30.77

Venture Capital 8.70

Credit Guarantee Company 7.87

• More than 13,000 islands • Population: + 237.6 million 1) • GDP of USD878.2billion in 2012, the 16th largest economy with estimated 6.23% GDP

growth rate 2) • GDP per capita 2012: USD 3,606 3)

• Banking industry covers ± 78.8% of assets in financial sector

Market Share of Indonesia Financial System by Total Assets

Source : Bank Indonesia and FSA (Dec 2013)

Indonesia has a huge economic potential and large market for financial services.

1) 2013, BPS 2) World Bank 3) BPS

4

B. FINANCING STRUCTURE

Commercial Banks 78.8%

Insurance Companies

9.9%

Multifinance Companies

6.7%

Pension Funds 2.6%

Rural Banks 1.2%

Pawn Broker 0.5%

Venture Capital 0.1% Credit

Guarantee Company

0.1%

Share of MSME loans to total loans in August 2014 reached 19.5%.

Share of MSME accounts to banking accounts in August 2014 is 24.36%.

The portion of MSME loan is largely distributed to the trade sector (52.55%).

C. OUTSTANDING OF MSME LOAN MSME Loan Outstanding

MSME Loan by Sector MSME Loan Accounts

5

A. Survey by ADB, 2010

B. Survey by Bank Indonesia, 2010

Lack of collateral is considered as the common barrier to financial access of MSME

II. MSME CHALLENGES A. BARRIERS TO FINANCIAL ACCESS

6

Financing 35%

Marketing 35% Fuel/Energy

4%

Transportation 3%

Skill 1%

Wage of Labour

1%

Materials 11%

Others 10%

Financing and Marketing aspects are the main challenges of the MSME Source : National Economic Census 2006

B. WEAKNESS OF MSME

7

Act No. 20/2008 on MSME

Micro Small Medium Assets ≤ IDR50-million

(≈USD4,167) ≤IDR500-million

(≈USD41,667) ≤ IDR10-billion (≈USD833,833)

Annual Sales

≤ IDR300-million (≈USD25,000)

≤IDR2,5-billion (≈USD208,333)

IDR50-billion (≈USD4,2 million)

8

III. REGULATION TO ACCELERATE MSME FINANCING

A. MSME ACT – DEFINITION OF MSME

Assumed: USD 1 equal to IDR12.000

Bank Indonesia Regulation No. 14/22/PBI of 2012

B. REGULATION ON MSME FINANCING (1)

Mandates that 20% of banks portfolios should be lent to MSME segment by 2018 2015 : 5% 2016 : 10% 2017 : 15% To meet this requirement,

Banks are allowed to directly lend to MSME or through linkage and on-lending programs.

Bank Indonesia provides Technical Assistance to increase capacities of FI and MSME in the form of research, training, provision of information, and facilitation.

Penalty for the failure to achieve target of MSME lending: Bank has to allocate certain budget for provision of training to MSME.

9

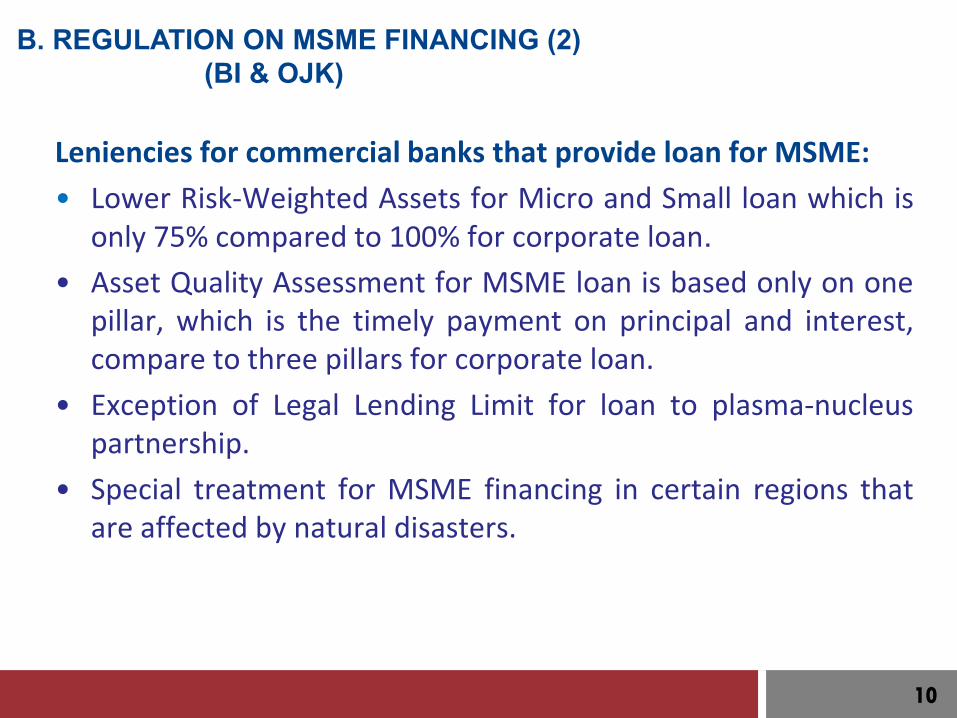

Leniencies for commercial banks that provide loan for MSME: • Lower Risk-Weighted Assets for Micro and Small loan which is

only 75% compared to 100% for corporate loan. • Asset Quality Assessment for MSME loan is based only on one

pillar, which is the timely payment on principal and interest, compare to three pillars for corporate loan.

• Exception of Legal Lending Limit for loan to plasma-nucleus partnership.

• Special treatment for MSME financing in certain regions that are affected by natural disasters.

B. REGULATION ON MSME FINANCING (2) (BI & OJK)

10

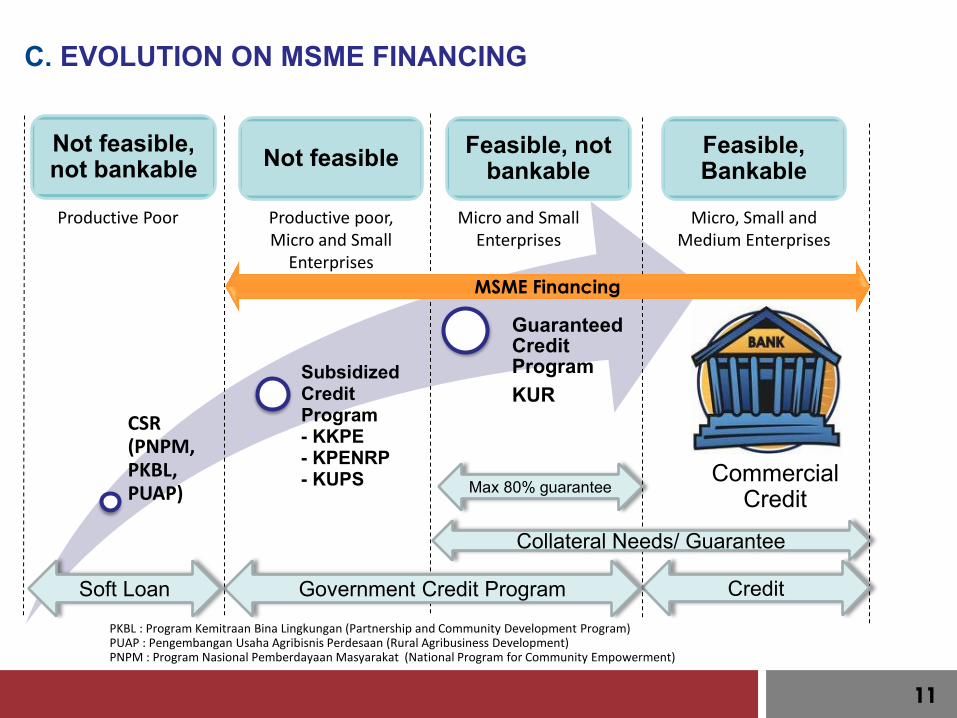

Not feasible, not bankable Not feasible Feasible, not

bankable

CSR (PNPM, PKBL, PUAP)

Subsidized Credit Program - KKPE - KPENRP - KUPS

Guaranteed Credit Program KUR

Feasible, Bankable

Commercial Credit

Credit Government Credit Program Soft Loan

Collateral Needs/ Guarantee

PKBL : Program Kemitraan Bina Lingkungan (Partnership and Community Development Program) PUAP : Pengembangan Usaha Agribisnis Perdesaan (Rural Agribusiness Development) PNPM : Program Nasional Pemberdayaan Masyarakat (National Program for Community Empowerment)

Productive Poor Productive poor, Micro and Small

Enterprises

Micro and Small Enterprises

Micro, Small and Medium Enterprises

MSME Financing

Max 80% guarantee

C. EVOLUTION ON MSME FINANCING

11

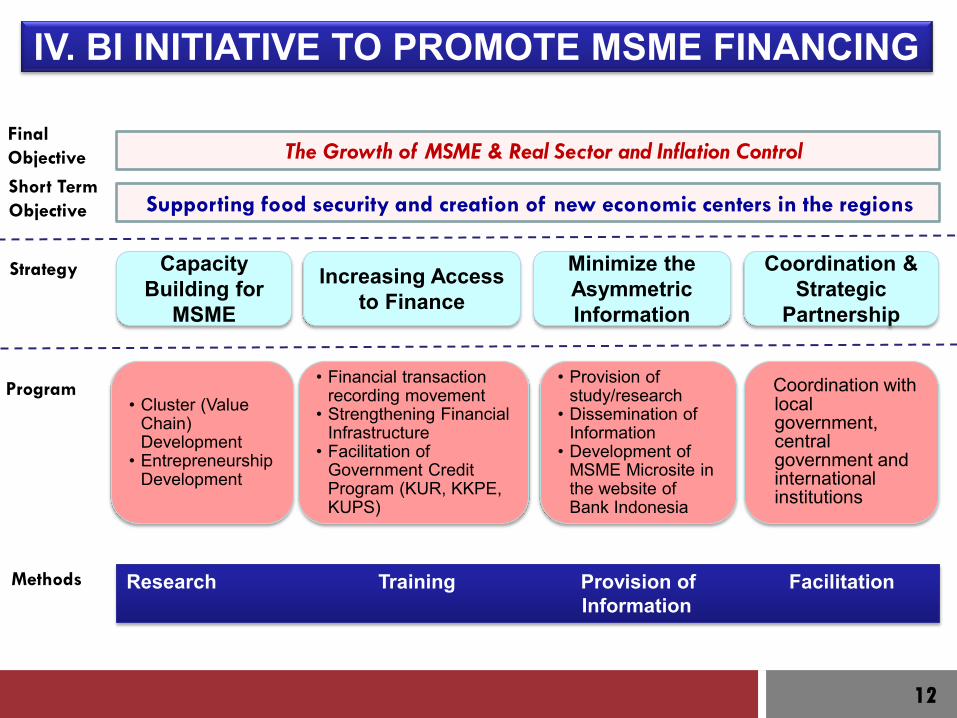

Supporting food security and creation of new economic centers in the regions

Final Objective The Growth of MSME & Real Sector and Inflation Control Short Term Objective

Strategy Capacity Building for

MSME

Increasing Access to Finance

Minimize the Asymmetric Information

Coordination & Strategic

Partnership

Program • Cluster (Value

Chain) Development

• Entrepreneurship Development

• Financial transaction recording movement

• Strengthening Financial Infrastructure

• Facilitation of Government Credit Program (KUR, KKPE, KUPS)

• Provision of study/research

• Dissemination of Information

• Development of MSME Microsite in the website of Bank Indonesia

Coordination with local government, central government and international institutions

Methods Research Training Provision of Facilitation Information

IV. BI INITIATIVE TO PROMOTE MSME FINANCING

12

Clusters Development

Provision technical assistance to improve MSME competitiveness in following aspects: • Marketing, • Production, • Finance, • Human Resources/Social

Capital.

To create new entrepreneur by providing technical assistance and business coaching

Entrepreneurship Development

A. MSME CAPACITY BUILDING

13

B. INCREASING ACCESS TO FINANCE

14

Regional Credit Guarantee Agency

• To address lack of

collateral faced by MSME in the region.

• Initiated by joint cooperation among government ministries and Bank Indonesia

SME Credit Rating

•To overcome

asymmetric information between SME and banks.

•Pilot Project as a cooperation between Bank Indonesia, OJK, banks and rating agencies.

The Utilization of Land Certificate

• To encourage the

use of land certificates to improve access to finance for MSME.

• Joint cooperation among related Ministries, National Land Agency, and Bank Indonesia.

Cattle Insurance

• To address the risks

inherent in the cattle farm business.

• Joint cooperation among Bank Indonesia, Ministries of Agriculture and insurance companies.

Financial Infrastructure Institutions Financial Infrastructure Instruments

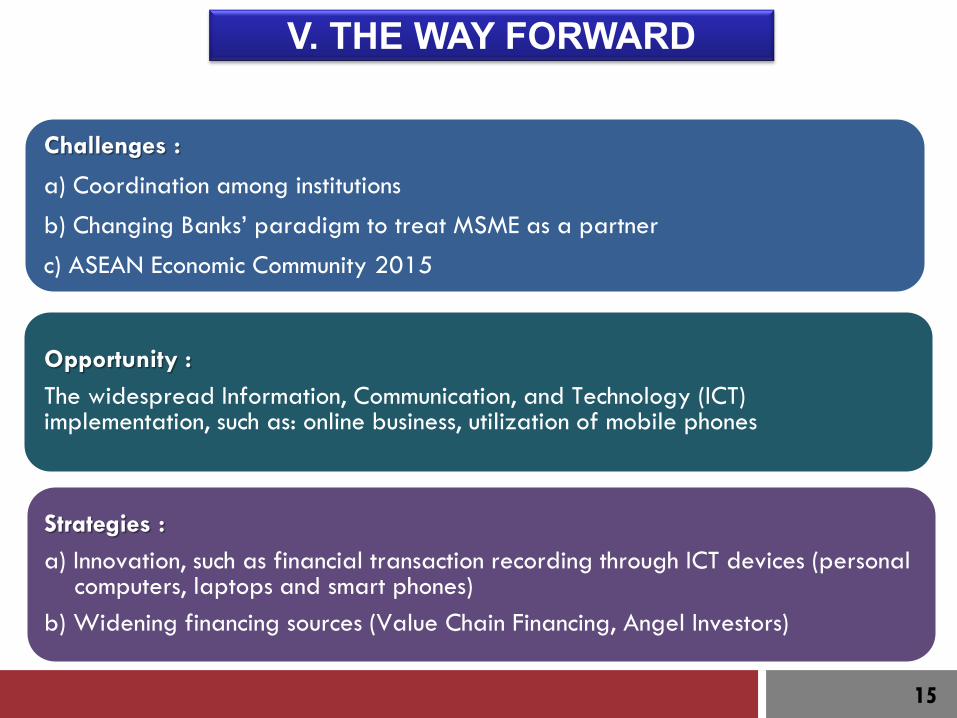

Challenges :

a) Coordination among institutions

b) Changing Banks’ paradigm to treat MSME as a partner

c) ASEAN Economic Community 2015

Opportunity : The widespread Information, Communication, and Technology (ICT) implementation, such as: online business, utilization of mobile phones

Strategies : a) Innovation, such as financial transaction recording through ICT devices (personal

computers, laptops and smart phones) b) Widening financing sources (Value Chain Financing, Angel Investors)

V. THE WAY FORWARD

15

Related Documents