For Community-Driven Development, Mobilization Matters The impact of mobilization messages on Self-Help Group performance in a community-driven development intervention in rural India Robindra Nath Banerji Department of Economics Haverford College 30 April 2015 Abstract As the rate of investment in community-driven development (CDD) increases (totalling $85 billion as of 2013 from the World Bank alone), it is increasingly important to understand the causes of its successes and failures. This project examines the role of mobilizers: specifically, how does a mobilizer encourage active buy-in from potential beneficiaries? Using cross-sectional survey data from Jeevika, a women’s empowerment, anti-poverty, and rural livelihoods intervention in Bihar, India, I find that CRPs (Community Resource Persons)—poor, female leaders in Jeevika—are the most effective in encouraging participation among potential beneficiaries, due to their high levels of social capital. I additionally find that imposing abstract positive messages such as “Jeevika will help you get out of poverty” and “Jeevika will bring you together as one” on potential beneficiaries crowds out intrinsic motivation stemming from social capital and reduces participation. JEL Classifications: D71, O12, O43, R51, R58, Z13

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

For Community-Driven Development, Mobilization Matters

The impact of mobilization messages on Self-Help Group performance in a

community-driven development intervention in rural India

Robindra Nath Banerji

Department of Economics

Haverford College

30 April 2015

Abstract

As the rate of investment in community-driven development (CDD) increases (totalling $85

billion as of 2013 from the World Bank alone), it is increasingly important to understand the causes

of its successes and failures. This project examines the role of mobilizers: specifically, how does a

mobilizer encourage active buy-in from potential beneficiaries? Using cross-sectional survey data

from Jeevika, a women’s empowerment, anti-poverty, and rural livelihoods intervention in Bihar,

India, I find that CRPs (Community Resource Persons)—poor, female leaders in Jeevika—are the

most effective in encouraging participation among potential beneficiaries, due to their high levels

of social capital. I additionally find that imposing abstract positive messages such as “Jeevika will

help you get out of poverty” and “Jeevika will bring you together as one” on potential beneficiaries

crowds out intrinsic motivation stemming from social capital and reduces participation.

JEL Classifications: D71, O12, O43, R51, R58, Z13

For the women of Lakshmi and Maa Kali SHGs in Rupauli, Bihar, in the hope that the fervor of

your empowerment will spread to every corner of the state of Bihar.

Acknowledgments

The realization of this project would not have been possible without the help and advice of my

thesis advisor, David Owens, or my research supervisors at The World Bank, Shruti Majumdar,

Vijayendra Rao, and Upamanyu Dutta. I am very grateful to the Center for Peace and

Global Citizenship at Haverford College, as well as The World Bank, for their gracious funding

of components of this project.

iii

Contents

1 Introduction 1

2 Previous literature 3

2.1 Scaling up . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 3

2.2 Evaluation . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 4

2.3 Social capital . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 5

2.3.1 Implications of social capital theory . . . . . . . . . . . . . . . . . . . . . . . 5

2.3.2 Measuring social capital . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 6

2.4 Models of aid and development . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 7

3 Context and methodology 8

3.1 Organizational context . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 9

3.1.1 Jeevika structure . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 9

3.1.2 The mobilization process . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 10

3.2 Methodology . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 12

3.2.1 Sampling strategy . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 12

3.2.2 Survey strategy . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 13

3.2.3 Analytical methods . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 14

4 Data 15

4.1 Dependent variables . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 15

4.2 Independent variables . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 16

4.2.1 Messaging dummies . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 16

4.2.2 Mobilizer dummies . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 19

4.3 Control variables . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 20

4.3.1 Group demographic controls . . . . . . . . . . . . . . . . . . . . . . . . . . . . 20

4.3.2 Geographic controls . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 23

v

5 Analysis 23

5.1 Effect of mobilizers on Jeevika participation . . . . . . . . . . . . . . . . . . . . . . . 24

5.2 Effect of messaging on Jeevika participation . . . . . . . . . . . . . . . . . . . . . . . 26

6 Discussion 27

6.1 Implications for social capital theory . . . . . . . . . . . . . . . . . . . . . . . . . . . 27

6.2 Why positive messages can lead to less participation . . . . . . . . . . . . . . . . . . 28

6.3 Implications for the great aid debate: Is localization worth it? . . . . . . . . . . . . . 29

7 Conclusion: Policy Implications and Further Research 29

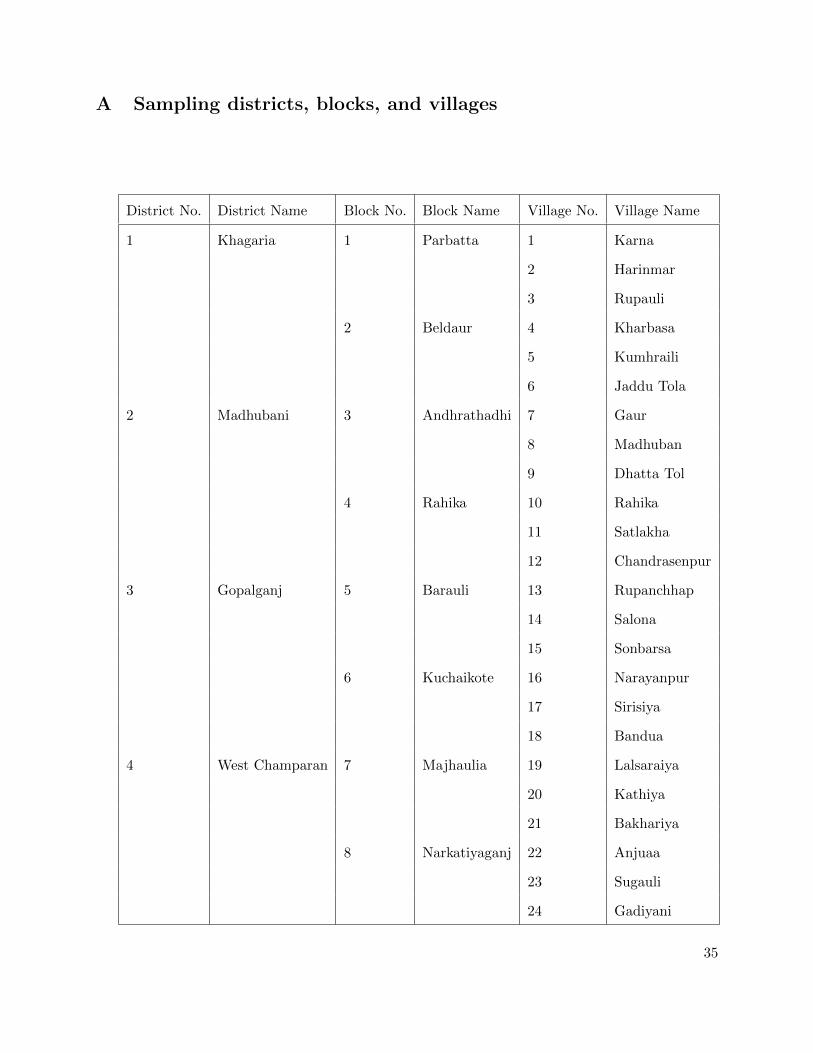

A Sampling districts, blocks, and villages 35

B Jeevika’s Panchasutra 36

C Regression tables 36

vi

List of Figures

1 Plots of three measures of participation in Jeevika—average number of loans taken

per member, average amount (Rs.) of loan taken, and average savings—over time

(days since group formation), controlling for the passage of time. . . . . . . . . . . . 2

2 3 × 3 matrix of potential mobilizers and their respective attributes. With regard to

the “origin” of the mobilizer, ‘outside’ and ‘inside’ refer to the social position of the

potential mobilizer vis-a-vis the village. . . . . . . . . . . . . . . . . . . . . . . . . . 10

3 Map of Bihar with the four districts in which surveys were conducted highlighted. . 12

4 Averages of the dependent variables across the four districts studied: number of

loans taken by the average SHG member, lifetime amount of money borrowed by the

average SHG member, and lifetime savings of the average SHG member. . . . . . . . 16

5 Prevalence of messages delivered in each district. . . . . . . . . . . . . . . . . . . . . 18

6 Proportion of groups with each mobilizer present at the time of mobilization, by

district. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 20

7 Averages of the dependent variables across the four districts studied: number of

loans taken by the average SHG member, lifetime amount of money borrowed by the

average SHG member, and lifetime savings of the average SHG member. . . . . . . . 21

8 Time since formation of each group (in days), with a normal distribution function

with corresponding mean and standard deviation superimposed. . . . . . . . . . . . 21

9 Distribution of group size, in number of members. . . . . . . . . . . . . . . . . . . . 22

List of Tables

1 Correlation between dependent variables, control variables, and independent vari-

ables, excluding message variables. . . . . . . . . . . . . . . . . . . . . . . . . . . . . 15

2 Regressions of the mobilizer variables on each different message extracted from group

interview transcripts. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 19

3 Results of regression of mobilizers’ presence on the likelihood that a CM will be

present. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 25

4 Regression results of mobilizers on average per member number of loans taken. . . . 37

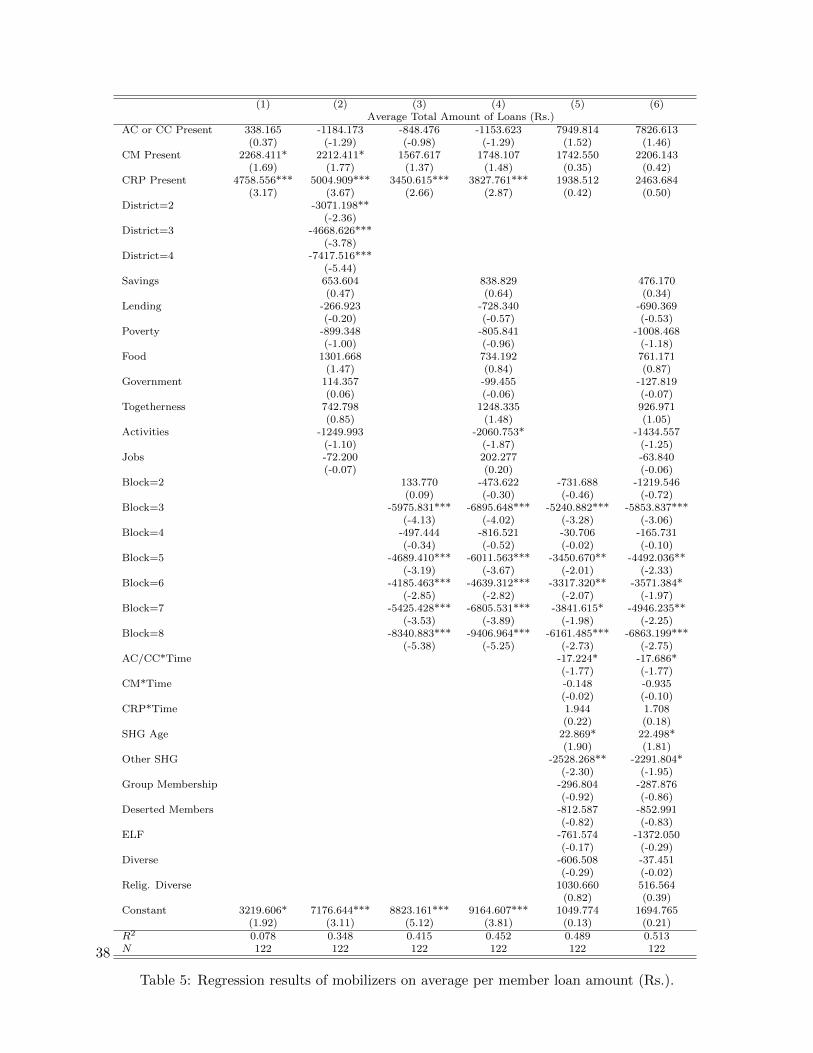

5 Regression results of mobilizers on average per member loan amount (Rs.). . . . . . 38

6 Regression results of mobilizers on average per member savings. . . . . . . . . . . . . 39

vii

7 Regression results of messages on average per member number of loans taken. . . . . 40

8 Regression results of messages on average per member loan amount (Rs.). . . . . . . 41

9 Regression results of messages on average per member savings. . . . . . . . . . . . . 42

viii

Glossary

Area Coordinator (AC) A paid, trained Jeevika staff member who AC oversees a cluster of

three CCs, thus responsible for approximately 600 SHGs.

Community Coordinator (CC) A paid, trained Jeevika staff member who oversees SHGs and

VOs in a number of villages; CCs are generally responsible for approximately 200 SHGs.

community-driven development (CDD) A model of economic development in which “com-

munities have direct control over key project decisions, including management of investment

funds” Mansuri and Rao (2004, 2).

Community Mobilizer (CM) A literate member of a Jeevika community who maintains records

and performs administrative tasks for the SHG.

Community Resource Person (CRP) CRPs are always SHG members. CRPs form SHGs and

serve as a general representatives of Jeevika and its ideals. CRPs also go on “CRP drives”

in which a team of five women—1 PRA CRP, 2 SHG-forming CRPs, a Master Trainer CRP,

and a CM—visit a non-Jeevika village and recruit them to Jeevika.

ethnolinguistic fractionalization (ELF) A measure of diversity and heterogeneity calculated

using the Herfindahl formula.

Initial Capitalization Fund (ICF) A revolving pot of money held by the VO to fund business

activities. Before 2014, an ICF consisted of a Rs. 50,000 loan at 2 percent interest; since 2014

it has been increased to a Rs. 60,000 loan with an extra Rs. 15,000 of revolving fund money

that permanently stays with the SHG.

participatory rural appraisal (PRA) One of the first steps in the process of a village starting

SHGs. The mission of a PRA is to get a reliable picture of the village to assess the social

and economic state of the village in order to set a target for the number of women should be

mobilized into SHGs..

self-help group (SHG) A saving and lending group comprised of between ten and fifteen bene-

ficiary women.

ix

1 Introduction

Community-driven development (CDD) falls under the umbrella of participatory development,

a movement in development theory and practice calling for the consideration of the needs and wants

of beneficiaries and the use of local knowledge to determine the contextual factors that should af-

fect a program’s design. In CDD programs, this framework is realized through active beneficiary

participation in the design, implementation, and management of the project; Mansuri and Rao

(2004, 2) emphasize that in CDD, “communities have direct control over key project decisions,

including management of investment funds.” CDD and its related philosophy, community-based

development, have long been considered a breakthrough innovation in the methodology of interna-

tional development, especially in the realm of anti-poverty, health, and sanitation initiatives. This

is reflected in the current boom in interest in participatory and community development; the World

Bank alone has invested over $85 billion in participatory programs (Mansuri and Rao, 2013, 15).

Due to the local and contextual nature of CDD programs, they generally begin in small-scale

pilot tests of the program, closely monitored by evaluators and implementers. Because of this situa-

tion, CDD programs face unique challenges in expansion and ‘scaling-up’ compared to development

programs operating under different models, especially top-down or technocratic development mod-

els. In particular, it is often difficult to use standard methods of recruitment (or “mobilization,” in

the language of community organizing), since the methods that work in one community may prove

unhelpful in another. This leads from the understanding that communities are “fluid, dynamic,

and differentiated, rather than static and homogenous” (Mathie and Cunningham, 2005, 175).

Currently, published studies on the successes and failures of the scaling-up process focus on

the institutional and organizational factors that lead CDD programs to either scale up effectively

or stagnate. However, this approach fails to consider what may be the most important factor in

deciding the extent of a CDD program’s success or failure: the decisions of potential beneficiaries

to join or not, and the related question of the locus of their motivations in joining the program.

A beneficiary with intrinsic motivation can be expected to participate considerably more and thus

achieve more successes, both tangible and intangible, than a beneficiary driven only by external

1

Figure 1: Plots of three measures of participation in Jeevika—average number of loans taken permember, average amount (Rs.) of loan taken, and average savings—over time (days since group

formation), controlling for the passage of time.

motives such as receiving food staples or cheap credit1 (Vansteenkiste et al., 2004). The challenge

faced by CDD programs struggling to expand is that, as documented by several works, the target

demographic of most CDD programs—the poorest of the poor—are most likely to join a program

only if induced with external incentives, with no subsequent likelihood that they will participate2

(Mansuri and Rao, 2013; Mosse, 2004; Botes and Van Rensburg, 2000).

This raises an important question: how can CDD programs scale up in an engaging manner,

maintaining high participation in the program through spurring beneficiaries’ intrinsic motivation?

This question forms the core inquiry of this paper, with a specific focus on the mechanism through

which the scaling-up process takes place: mobilization. In this study, I use a mixed-methods

analysis of the mobilization in the scaling-up process of Jeevika, a CDD organization in Bihar,

India, and find that over the time period studied, participation in Jeevika by saving money has

risen modestly participation by taking out loans has stagnated, participation by increasing the

amount of money borrowed has fallen (see Figure 1). Apart from the effect of time, my analysis

indicates that being mobilized by a person with similar characteristics to the potential beneficiary

is associated with higher participation, all other things equal.

1Moreover, it has been documented and experimentally shown that the provision of external rewards to sparkmotivation can significantly diminish intrinsic motivation through depletion of one’s perceived autonomy or througha motivational “crowding out” mechanism (Eisenberger et al., 1999; Frey and Jegen, 2001)

2Note here that the definition of “participation” holds no connotation of democratic discourse or self-governance,as it is commonly used in works such as Mansuri and Rao (2012). In this paper, the term simply connotes a potentialbeneficiary’s active psychic and material “buying into” a CDD program, observably shown through the investmentof time and money.

2

2 Previous literature

2.1 Scaling up

Previous studies on the challenges facing community-driven development projects while scaling

up have largely focused on the organizational and structural issues that may arise in the context of

community development, and have in doing so taken out of the equation the beneficiary’s agency

to choose her own level of participation.

For instance, in his analysis of the scaling-up processes of two CDD projects headed respectively

by Indian and Nepali NGOs, the National Agricultural Bank for Agriculture and Rural Development

(NABARD) and the Nirdhan Uttthan Bank Limited (NUBL), Sharma (2004) demonstrates that the

projects would not have been able to expand without the aid of the federal and state governments.

The paper comments that one of the most helpful factors to effectively expanding the projects and

reaching a larger beneficiary base was the support of the governments of India and Nepal in the

form of subsidized, “priority-sector” lines of credit.

The paper also comments that the two projects differed in that NUBL provided banking services

directly to beneficiaries and NABARD used third-party financial organizations to provide banking

services. Thus, “in the case of NABARD, the dynamics of group formation and the quality of

the group’s interaction with the financial institution is greatly conditional on the type of NGO

and bank selected to service the group” (Sharma, 2004). However, the author claims that both

NUBL and NABARD benefited from having standard rules of conduct and basic service delivery

mechanisms. Commenting on NUBL, especially, Sharma speaks of “methodologically-imposed lim-

itations,” such as the labor-intensive practice of visiting each village to recruit, rather than opening

central branches serving several villages. While these findings are useful from a high-level policy

perspective, they stem from the unreliable assumption that all beneficiaries will join the program

if given the opportunity—which sometimes turns out not to be the case.

Many papers evaluating the overall successes and failures of CDD projects cite the critical

importance of many different contextual variables contributing the ability of a project to function,

3

let alone achieve its intended impact on the community in which it works. Wolff (2013) echoes

Binswanger and Aiyar (2003) and Mansuri and Rao (2004) in positing, “the most important aspect

of a community development project is that it fits the local context as best as possible.” Mansuri

and Rao (2012) also elaborate on this point, citing “inequality, history, geography, the nature of

social interactions, networks, and political systems” as contextual features that can lead to the

success or failure of a CDD project.

2.2 Evaluation

Scholarly authors and works disagree on how a project involving women’s self-help groups

(SHGs) should be evaluated. Mansuri and Rao (2012) call for contextualization and customization

of the monitoring and evaluation components of different groups and encourage innovation among

evaluation teams, giving the example of the emerging availability of SMS project updates and other

mobile technologies that can be employed to effectively track various the indicators chosen by the

monitoring and evaluation team.

In their study of women’s SHGs in Andhra Pradesh, India, Galab and Rao (2003) name the

two parameters of evaluation as poverty alleviation and women empowerment. Within women

empowerment, there are three dimensions of outcomes: the first, “power to,” includes basic abilities

to perform necessary and desired roles and functions. The second, “power with,” includes the power

of collective action with other women members of the community to negotiate their status. Finally,

“power within” includes what (Galab and Rao, 2003, 1274) call “strategic gender awareness”, or

questioning at a deep level the structure of power among genders. A successful women’s SHG

project, the authors claim, will empower women among all of these dimensions, as well as lift them

out of poverty in terms of their income or consumption.

To Sanyal (2009), women’s empowerment is intrinsically linked to escaping the strict bonds of

the patriarchal culture of rural India, which includes limits on women’s vocations, mobility, choice of

social networks, and ability to make household decisions. In the case of Sanyal (2009), empowerment

not only involves engaging in individual social, economic, and political action (studied in other works

4

such as Hashemi et al. (1996)), but collective action as well. In a sociological interview study of

400 women in 59 microfinance groups (organizationally similar to SHGs), she found that the simple

act of having regular meetings of a microfinance group led one third of the study participants to

organize collective action.

2.3 Social capital

Social capital is a piece of theoretical technology that has emerged into the development lit-

erature in the past fifteen years. The definition employed by Woolcock (1998, 153), summarizing

generalizations and definitions from social scientists from the early 1990s, begins from the premise

that social capital constitutes “the information, trust, and norms of reciprocity inhering in one’s

social networks.” This definition clearly implies that the main detrimental consequence of low lev-

els of social capital is the inability to cohere in groups to perform actions that would collectively

benefit the members of the groups.

2.3.1 Implications of social capital theory

Quoting Robert Putnam’s seminal work (Putnam, 1995), Woolcock elaborates that the conse-

quences of using pre–social theory models to develop models of economic development are “propos-

als for strengthening market economies and democratic institutions [in developing and transitional

countries that] center almost exclusively on deficiencies in financial and human capital (thus calling

for loans and technical assistance)” (Woolcock, 1998, 154). Applying this generalization to the

analysis of development programs is crucial because without social capital, it would be expected

that any community would be able to solve all of its economic development challenges with the

simple injection of money and training on how to use the money—which, time and again, has

proven not the case (Woolcock, 2002; Narayan, 1999).

As pointed out by Narayan (1999) and Woolcock (1998), social capital has the ability to hinder

economic development as well as help. Rigid social structures that produce in-group/out-group

dynamics—one potential outcome of a society with high overall social capital—can generate polar-

ized outcomes between elites and the underclass. Social norms excluding members of society on the

5

basis of gender, caste, tribe, or ethnicity can significantly impede the flow of economic, physical,

and human capital (Narayan, 1999). Coleman (1988) examines the effect that different rates of

social capital can have on the formation of human capital: specifically, he finds that high-schoolers

with low levels of social capital have a significantly higher likelihood of dropping out. This effect is

compounded by social structures in which norms prevent women, for instance, from even attending

school at all.

Despite the possible negative implications of high social capital, issues of low social capital

present significant roadblocks to the expansion of CDD programs. A main hypothesis put forth

in this paper is that low levels of social capital among beneficiaries and mobilizers during the

mobilization process forms a main constraint affecting the participation of beneficiaries in Jeevika.

2.3.2 Measuring social capital

A common proxy for the level of social capital is the level of participation in formal institutions

of civil society3. By default, participation in Jeevika is participation in a formal grassroots, civil

society organization. Thus, measuring social capital by participation in civil society institutions in

this study involves a circular argument about social capital—that high social capital is reflected in

high participation in institutions like Jeevika, and that if we observe high participation, it shows

that there is high social capital.

This paper additionally examines the concept of ethnolinguistic fractionalization (ELF), a mea-

sure of diversity and heterogeneity. ELF is a measure of diversity among groups in a particular

population. Here, ELF is calculated using the Herfindahl formula, modified for the purposes of this

study. That is, the statistic takes the form

ELF =n∑

i=1

(Ni

N)2

where an SHG with N members includes castes4 i = 1, 2, · · · , n, each caste having a share NiN in

3For more on the link between formal institutions and social capital, see (among others) Glaeser et al. (2002),Knack and Keefer (1997a), and Grootaert and van Bastelaer (2002).

4It is important to note here that other groups, as well as official government caste groupings, are included in the

6

the SHG on whole.

As a macroeconomic concept, ELF is now understood to be a critical determinant of growth,

and is used in all notable cross-country models of economic growth and development (Easterly et al.,

2006). Although the index—especially the country-level estimates calculated during the emergence

of the statistic’s use—is only a rough estimation of the actual social situation of a particular region

or country5, the calculation in this study is at the SHG level, allowing for a granularity of analysis

that lends it additional explanatory power.

2.4 Models of aid and development

An important contribution of this paper is the development of new tools and strategies—for

instance, documenting the messages imparted by mobilizers—in order to gauge the effectiveness of

the CDD model. As discussed above, CDD operates under the premise that local knowledge and

beneficiary participation can yield the most effective results for the personal, social, economic, and

political development of a community.

This view contrasts sharply to models of economic development that focus solely on provid-

ing economic and human capital to communities based on their needs, like the model pursued

in the Millennium Villages Project headed by Jeffrey Sachs (Murphy, 2014; Easterly, 2014). In

several demonstration villages, mainly in East Africa, Sachs proposed that each impoverished in-

habitants receive roughly $100 per year while concurrently receiving state-of-the-art improvements

to sanitation, power, education, roads, and other infrastructure systems. The main element of

these projects, as commented on by scholar and journalist Sam Rich (2007) below, is the immense

scrutiny provided to every minute need of the villages and the wealth of economic capital available.

Inside a concrete compound at the headquarters of the Millennium Villages Project,

development experts sat at computer monitors in glass-walled offices. As I entered,

the receptionist at the front desk was on the phone: “You need notebooks?. . . How

calculation of ELF in this paper, including one group of Scheduled Tribes (Adivasis) and seven internal groupings ofMuslims.

5For a more in-depth analysis of the shortcomings of ELF as a determinant of growth, see Posner (2004)

7

many?. . . Three hundred, is that all? Right, I’ll order them for you tomorrow. You’ll

get them in a few days.”

I’ve spent the last five years in Africa, where I’ve worked with outfits ranging from big

international nongovernmental organizations to tiny one-man-band agencies, but I’ve

never seen an order made as breezily as this. At most NGOs, the procurement even of

stationery entails filling out forms in triplicate and long delays. (Rich, 2007)

A main criticism of the Millennium Villages Project, as well as Jeffrey Sachs’ program of “shock

therapy” is its emphasis on the provision of economic or human capital for the solution of problems

that may have a much more knotty underlying cause than a simple lack of money or expertise

(Easterly, 2014). Another is the prediction that interventions that rely heavily on the raising

and disbursing of enormous aid funds to small villages with evolving needs is not a sustainable

or scalable model of development (Rosen, 2014). This study comments on this generalization by

further uncovering the factors that allow for flexibility in the scale-up process in a program that

relies more heavily on local capital and expertise than on an external aid fund.

3 Context and methodology

New data for this project came from a mixed qualitative/quantitative survey administered to

members of 122 SHGs in four districts in Bihar, India. All participants were members or former

members of SHGs formed and run as part of Jeevika, the main program run by the Bihar Rural

Livelihoods Promotion Society, an independent agency of the Ministry of Rural Development of

the Government of India. These data were analyzed using a number of qualitative and econometric

methods.

8

3.1 Organizational context

3.1.1 Jeevika structure

Bihar, located in India’s northeastern Ganges plain, is the poorest state in India with a per-

capita GNP of Rs. 24,681 ($389.356) (IndiaStat, 2012). A largely rural state, only slightly over

1 in 10 people in Bihar lives in a city (IndiaStat, 2001), although migration to national urban

centers in North India and Bengal, such as Delhi, Mumbai, and Kolkata, is widespread. Due to

the lack of basic amenities and widespread poverty in many parts of the state, Bihar is a hotbed

of concerted action on the parts of the Government of India, multilateral development agencies

such as the World Bank, DFID, and the World Health Organization, and private non-governmental

organizations in humanitarian and anti-poverty interventions.

Initially funded by the World Bank and implemented jointly between the World Bank and

the Government of Bihar, Jeevika (officially stylized JEEViKA), or the Bihar Rural Livelihoods

Promotion Society, was founded in 2006 to empower poor, rural women and aid them in lifting

themselves out of poverty (Khan et al., 2013)7. The basic unit of Jeevika is the SHG, a saving

and lending group comprised of between ten and fifteen beneficiary women. Jeevika’s SHGs meet

weekly and collect savings of Rs. 10 ($0.16) from each member. The funds of the SHG are used

in inter-loaning, a process through which a member of the SHG can obtain a microloan from the

SHG at a rate of 2 percent interest. In inter-loaning, the amount and terms of the loan are decided

upon through a democratic process involving the group members and the group’s Community

Mobilizer (CM), who maintains the SHG’s records. Other opportunities available to SHGs are

bank linkages, through which the SHG gains a Rs. 60,000 ($946.52) line of credit from a local

bank, and the provision of an Initial Capitalization Fund (ICF), a grant of Rs. 50,000–Rs. 75,000

($788.77–$1,183.34) from Jeevika to be subsequently used for the group’s rotating fund.

6In this paper, I use the exchange rate between the Indian Rupee (ISO code: INR) and the U.S. Dollar (ISO code:USD) as of the date of this paper’s publication, 30 April 2015. Note that the exchange rate has varied greatly in thepast decade and a half, and not all conversions will reflect the dollar value of the figure in question.

7Khan et al. (2013, 10) quote the exact mission statement of the National Rural Livelihoods Mission, of whichJeevika is a part, as: “reduce poverty by enabling the poor households to access gainful self-employment and skilledwage employment opportunities, resulting in appreciable improvement in their livelihoods on a sustainable basis,through building strong grassroots institutions of the poor.”

9

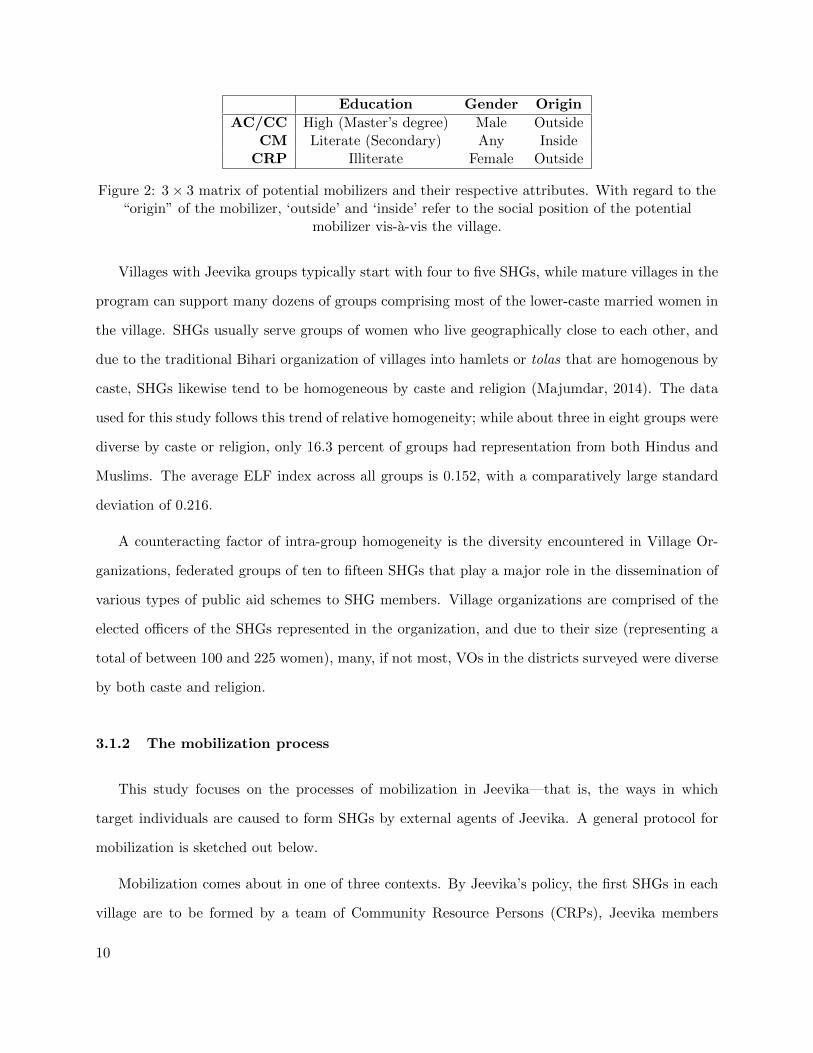

Education Gender Origin

AC/CC High (Master’s degree) Male OutsideCM Literate (Secondary) Any Inside

CRP Illiterate Female Outside

Figure 2: 3 × 3 matrix of potential mobilizers and their respective attributes. With regard to the“origin” of the mobilizer, ‘outside’ and ‘inside’ refer to the social position of the potential

mobilizer vis-a-vis the village.

Villages with Jeevika groups typically start with four to five SHGs, while mature villages in the

program can support many dozens of groups comprising most of the lower-caste married women in

the village. SHGs usually serve groups of women who live geographically close to each other, and

due to the traditional Bihari organization of villages into hamlets or tolas that are homogenous by

caste, SHGs likewise tend to be homogeneous by caste and religion (Majumdar, 2014). The data

used for this study follows this trend of relative homogeneity; while about three in eight groups were

diverse by caste or religion, only 16.3 percent of groups had representation from both Hindus and

Muslims. The average ELF index across all groups is 0.152, with a comparatively large standard

deviation of 0.216.

A counteracting factor of intra-group homogeneity is the diversity encountered in Village Or-

ganizations, federated groups of ten to fifteen SHGs that play a major role in the dissemination of

various types of public aid schemes to SHG members. Village organizations are comprised of the

elected officers of the SHGs represented in the organization, and due to their size (representing a

total of between 100 and 225 women), many, if not most, VOs in the districts surveyed were diverse

by both caste and religion.

3.1.2 The mobilization process

This study focuses on the processes of mobilization in Jeevika—that is, the ways in which

target individuals are caused to form SHGs by external agents of Jeevika. A general protocol for

mobilization is sketched out below.

Mobilization comes about in one of three contexts. By Jeevika’s policy, the first SHGs in each

village are to be formed by a team of Community Resource Persons (CRPs), Jeevika members

10

from another village who are paid to spend 45 days in each village, conducting a participatory

rural appraisal (PRA) including identification of the poorest of the poor, forming SHGs through

motivational speaking and the sharing of stories and songs, and training the SHG members in three

modules of training explaining the social causes of poverty and the SHG model.

Following the formation of the first groups by the CRPs, other groups come to be formed in the

village through the efforts of Jeevika staff organizers, such as Community Coordinators (CCs) and

Area Coordinators (ACs). While CCs are responsible for managing approximately 200 groups, ACs

are responsible for managing three CCs, or 600 SHGs, in a contiguous geographical area. CMs,

literate, non-beneficiary members of the village community who are charged with maintaining the

record books of 5–11 SHGs in the same village. CMs also often act as representatives or coordinators

of the Village Organizations in their locale.

In practice, groups may be mobilized by CRPs, ACs, CCs, or CMs. While it is most directly the

task of CRPs to form new groups and mobilize women to join Jeevika, ACs and CCs often either

accompany CRPs to their target villages or form groups independently of CRPs, responding to

pressure to meet mandatory targets for group saturation set by block- and district-level authorities.

CMs form groups when petitioned by potential beneficiaries who wish to join Jeevika, as well as

for their own benefit, since CMs receive higher stipends for overseeing 1–5, 6–10, and more than 10

groups.

Additionally, the mobilization process does not always involve the educational and empower-

ment messages put forth by official Jeevika mobilization trainings: mobilizers sometimes use tactics

they believe will entice the maximum number of potential beneficiaries to join SHGs. When asked

what messages spurred them to join Jeevika, many respondents to the survey in this study men-

tioned material benefits that they were told they could expect for free or at a subsidized cost,

including food staples (wheat; rice; salt; oil), household necessities (soap; cloth; toilets), or finan-

cial benefits (cheap, easy-to-access credit; cash transfers). In fact, Jeevika does not provide any

of the above material benefits to its beneficiaries, apart from loans. These incentives are used to

encourage potential members, especially the poorest of the poor, to join Jeevika. However, these

incentives backfire, as they do not cause intrinsic motivation for the members to join and actively

11

Figure 3: Map of Bihar with the four districts in which surveys were conducted highlighted.

participate in their Self-Help Group.

3.2 Methodology

3.2.1 Sampling strategy

In August 2014, I led a team of three independent surveyors funded by the World Bank in col-

lecting data from beneficiaries of Jeevika SHGs formed between 5 September 2012 and 27 November

2013 by CRPs, Jeevika staff (ACs and CCs), and CMs. Of the eight districts with Jeevika activity

at the time of formation, four were selected by random; within each district, two blocks were se-

lected at random, and three villages were selected at random from these blocks in which to conduct

data collection8.

It is important to note that sub-national administrative levels in India differ significantly from

their counterparts in other countries, largely due to India’s geography and tremendous population

density. A district is a division of a state, geographically analogous to a county in the United

States. However, in terms of population, districts are much larger—for instance, the district of

Madhubani is slightly smaller than the US state of Louisiana. There are 37 districts in Bihar. Each

8See Appendix A for the list of locations surveyed and the numbers corresponding to each location used in thisstudy.

12

district is comprised of a number of blocks, each with dozens of villages; the number of blocks in

the four districts studied ranges from 21 (Madhubani) to 7 (Khagaria).

The four districts chosen contrast in interesting ways that are significant for the analysis of

the data collected. For instance, while all of the blocks in this study were entered less than to

years ago, certain blocks in Khagaria and Madhubani (Districts 1 and 2, respectively) comprised

part of of the original four districts where Jeevika was piloted by the World Bank between six

and eight years before this study. In contrast, the first blocks in West Champaran and Gopalganj

(Districts 3 and 4, respectively) were entered in the latest round of mobilization, beginning in 2013.

West Champaran and Gopalganj are also located in the far northwest of the state of Bihar, an

impoverished area ravaged over the past decades by the violent activities of the Naxalite Maoist

rebels. On whole, the contrast between Districts 1 and 2 and Districts 3 and 4, and geographical

idiosyncrasies on whole, plays a large role in explaining variation in program outcomes.

3.2.2 Survey strategy

Within each village, one or more CMs were requested to arrange meetings of between 7 and

15 SHG members, with whom a surveyor conducted a focus group discussion. Following this,

the same surveyor conducted two one-on-one interviews: one each with a semi-randomly chosen

office-bearer and non-office-bearer. While the interviews were conducted using questionnaires in

Hindi, interviewers and interviewees also used local languages such as Bhojpuri and Maithili. In

addition to paper and digital notation of responses, the interviewers also used audio recordings to

capture the responses in individual interviews and focus group discussions. Rosters were collected

for each SHG with each member’s name and caste as well as her total savings amount, total amount

withdrawn as a loan, and number of loans taken.

Questions on the questionnaires focused on collecting two types of data: information on the

methods of mobilization and the messages employed by the mobilizers to recruit the interviewees

to Jeevika, and questions designed to gauge the effectiveness of Jeevika. Both in groups and

individually, respondents were asked to recall what messages the mobilizer shared to convince

the respondent to join Jeevika, and they were also asked who the mobilizer was in relation to

13

them. In order to understand how Jeevika may have affected the respondents’ levels of social

capital and mobility in her community, respondents were asked to consider a number of scenarios

of economic issues she might confront such as lack of money to buy food, political issues such as

an extended closing of the village’s government ration shop, or social issues such as domestic abuse

or alcoholism. The respondents were also asked who they regularly confided in and looked to for

help; many respondents cited women they had met through Jeevika.

3.2.3 Analytical methods

Using Microsoft Excel and NVivo, a software package for qualitative analysis, I analyzed the field

notes collected from individual and group interviews for the messages that the interview participants

recalled being shared with them by their mobilizers. These messages were then organized into eight

themes by broad topic, as described in Section 4.2.1 below. Each instance of a theme’s mention

was recorded as a value of “1” for the corresponding dummy variable, with the variable taking a

value of “0” otherwise.

Factor analysis was used to condense message variables into more concise, highly explanatory

motivational incentives, but ultimately failed, because the message variables were already in their

most concise form—no hidden, underlying variable was found to be inducing covariance between

variables. In testing the suitability of the data for factor analysis, Bartlett’s test of sphericity yielded

a significant result (p < 0.0001). However, using the Kaiser-Meyer-Olkin Measure of Sampling

Adequacy, the message variables are shown to be already expressed in their most concise form,

with no underlying variables able to explain correlational or covariance matrices (KMO = 0.523,

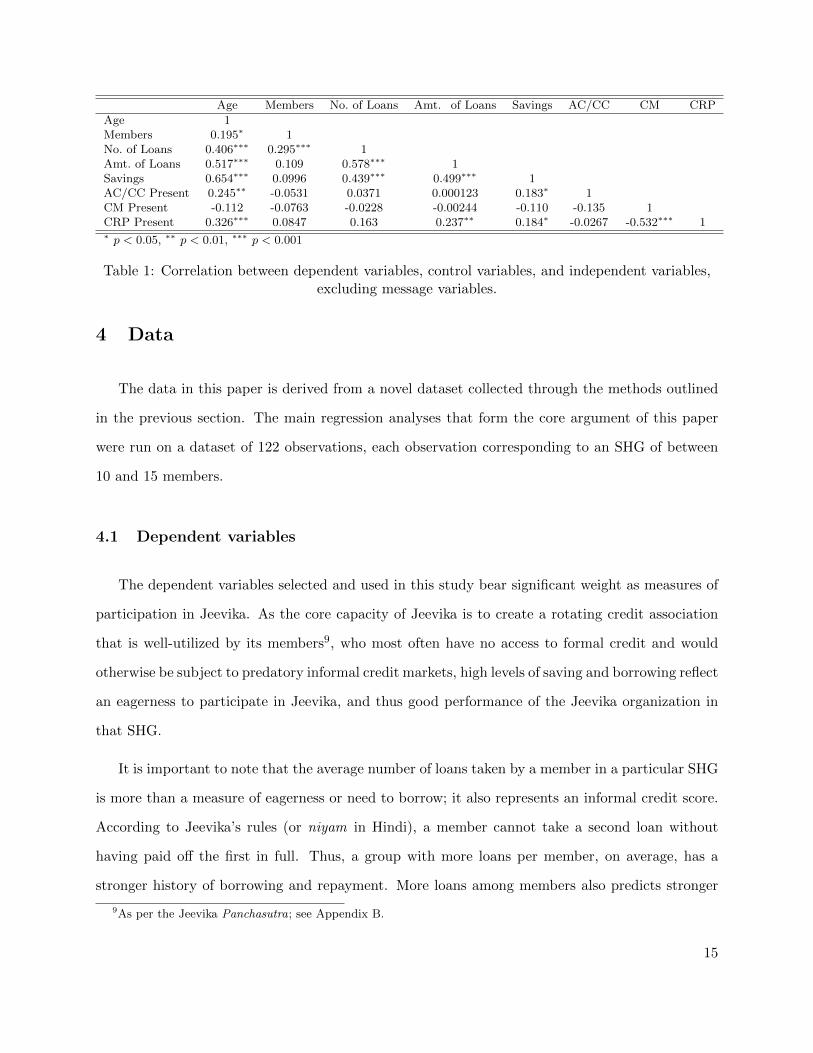

slightly above the threshold of acceptability). The correlation between the dependent variables,

controls, and independent variables not used in factor analysis is shown in Table 1.

The association between outcomes, messages, mobilizers, and group characteristics was estab-

lished through OLS regression analysis of the latter three groups of variables on the outcome vari-

ables, and OLS regressions were also run to determine the relative tendencies of different mobilizers

to deliver certain messages. The results of these regressions is discussed in Section 4.2.1.

14

Age Members No. of Loans Amt. of Loans Savings AC/CC CM CRP

Age 1Members 0.195∗ 1No. of Loans 0.406∗∗∗ 0.295∗∗∗ 1Amt. of Loans 0.517∗∗∗ 0.109 0.578∗∗∗ 1Savings 0.654∗∗∗ 0.0996 0.439∗∗∗ 0.499∗∗∗ 1AC/CC Present 0.245∗∗ -0.0531 0.0371 0.000123 0.183∗ 1CM Present -0.112 -0.0763 -0.0228 -0.00244 -0.110 -0.135 1CRP Present 0.326∗∗∗ 0.0847 0.163 0.237∗∗ 0.184∗ -0.0267 -0.532∗∗∗ 1∗ p < 0.05, ∗∗ p < 0.01, ∗∗∗ p < 0.001

Table 1: Correlation between dependent variables, control variables, and independent variables,excluding message variables.

4 Data

The data in this paper is derived from a novel dataset collected through the methods outlined

in the previous section. The main regression analyses that form the core argument of this paper

were run on a dataset of 122 observations, each observation corresponding to an SHG of between

10 and 15 members.

4.1 Dependent variables

The dependent variables selected and used in this study bear significant weight as measures of

participation in Jeevika. As the core capacity of Jeevika is to create a rotating credit association

that is well-utilized by its members9, who most often have no access to formal credit and would

otherwise be subject to predatory informal credit markets, high levels of saving and borrowing reflect

an eagerness to participate in Jeevika, and thus good performance of the Jeevika organization in

that SHG.

It is important to note that the average number of loans taken by a member in a particular SHG

is more than a measure of eagerness or need to borrow; it also represents an informal credit score.

According to Jeevika’s rules (or niyam in Hindi), a member cannot take a second loan without

having paid off the first in full. Thus, a group with more loans per member, on average, has a

stronger history of borrowing and repayment. More loans among members also predicts stronger

9As per the Jeevika Panchasutra; see Appendix B.

15

Figure 4: Averages of the dependent variables across the four districts studied: number of loanstaken by the average SHG member, lifetime amount of money borrowed by the average SHG

member, and lifetime savings of the average SHG member.

future participation: as borrowers pay interest on loans, repayment with interest increases the

amount that SHG members can borrow in the future.

Understandably, the three outcome variables are significantly positively correlated with each

other, with r-values ranging from 0.44 (between savings and number of times a loan was withdrawn)

to 0.58 (between number of times a loan was withdrawn and the total amount in rupees of loans).

Across districts, the outcome variables are somewhat uniform (see Figure 4).

4.2 Independent variables

4.2.1 Messaging dummies

Eight variables relating to the message delivered by the mobilizer during the mobilization of

the SHG under study were derived and quantified from group and individual interview transcripts,

encoded respectively as savings, lending, poverty, food, govt, together, activities, and work.

If a message or related theme was mentioned in an interview, the value of the variable for that

observation (SHG) was set to “1”, “0” otherwise.

Savings and lending are perhaps the most straightforwardly understood messages, and also the

most common: if the interview participants recalled the mobilizer mentioning the incentive of saving

or lending through Jeevika—as they did in 88.5 and 87.7 percent of the time, respectively—the

message was understood as the mobilizer intended. Food is a related variable, but different in one

important way: in most cases, the participant recalled receiving a message such as “through Jeevika,

16

you will receive wheat” (Hindi: Jeevika se gehoon milegi). While some Village Organizations do

participate in wheat- and rice-buying operations, the perception that food will be “received” by

the potential Jeevika beneficiaries is inaccurate—the assumption being that it will be received free

of cost. The prevalence of this message (39.3 percent of interview participants reported hearing it)

shows clear misalignment between the incentives of the mobilizers and potential beneficiaries.

Government and work are other sites of potential disingenuity. Like food, these was most

often recalled in the formulation Jeevika se rozgaar/sarkaari sahayta milegi—“you will receive a

job/government help.” Government message was recalled much less frequently; only about 1 in 13

participants recalled it, whereas 1 in 5 participants recalled a message about jobs or work.

The second-most-prevalent message recalled was poverty, which usually was associated with a

message such as Jeevika se garibi ka samasya door ho jayenge—“though Jeevika, the problems of

poverty will be relieved.”

Finally, many participants recalled receiving messages about the Jeevika lifestyle, expressed in

the variables together and activities. Together captures a number of different sentiments recalled

as incentivizing messages from the mobilizers: examples include “you will come together as one”

(ekta ho jayengi), “you will sit together as an SHG” (samooh se milke baithayenge), and “you will

have a weekly meeting together” (sare sapta, aap logon milke ek baithak karenge); more than 2

in 5 participants recalled this message. Activities encompasses empowerment exercises performed

weekly by the SHGs, including singing songs together and introducing oneself to other members of

the SHG.

As shown in Figure 5, there is significant level of variation in the distribution of messages

delivered across districts. On whole, survey respondents in District 1, Khagaria, recalled a much

more diverse set of messages than in any other district. For instance, respondents in District

1, Khagaria, recalled significantly more mobilizers mentioning government help (p < 0.0510) and

group activities (p < 0.05). Respondents in District 4, West Champaran, recalled significantly

more mobilizers mentioning employment opportunities, and respondents in Khagaria mentioned

10The p-values listed in this paragraph are derived from χ2-tests of independence between the district variable andthe relevant messaging variable.

17

Figure 5: Prevalence of messages delivered in each district.

this variable significantly less (p < 0.001).

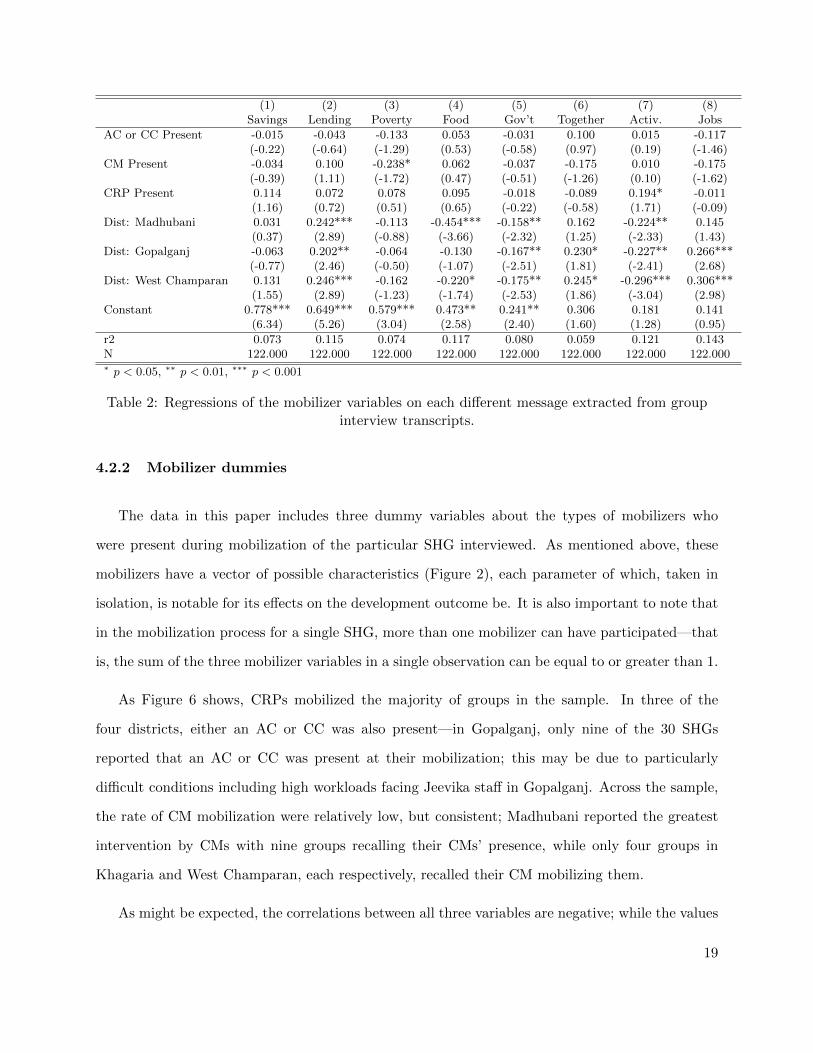

A regression calculating the propensity of different kinds of mobilizers to give different kinds of

messages (Table 2) shows little significant explanation of why particular messages are recalled by

survey respondents. Two interesting effects revealed by these regressions is that CMs, or having

a CM present during mobilization, is associated with 23.8% less delivery of messages relating to

poverty. This may be because when CMs mobilize new groups, they are sometimes formed at the

request of the potential beneficiaries, who would not need more information or incentive about Jee-

vika in order to join. Having a CRP present increases the probability that a message about Jeevika

activities conducted in SHGs by 19.4%; this is an intuitive result, because in general, CRPs narrate

their own experiences with Jeevika, which would naturally include the activities they participated

in at the beginning of every SHG meeting, like praying together and introducing themselves.

However, it should be noted that these results do not persist with a more granular geographic

control. When control variables at the block level are included in place of those at the district

level, the geographic control variables are the only variables with significant coefficients at the 10%

confidence level. For these regressions, the R2 value is also higher, ranging between 0.083 and 0.198,

in contrast to the R2 values shown in Table 2.

18

(1) (2) (3) (4) (5) (6) (7) (8)Savings Lending Poverty Food Gov’t Together Activ. Jobs

AC or CC Present -0.015 -0.043 -0.133 0.053 -0.031 0.100 0.015 -0.117(-0.22) (-0.64) (-1.29) (0.53) (-0.58) (0.97) (0.19) (-1.46)

CM Present -0.034 0.100 -0.238* 0.062 -0.037 -0.175 0.010 -0.175(-0.39) (1.11) (-1.72) (0.47) (-0.51) (-1.26) (0.10) (-1.62)

CRP Present 0.114 0.072 0.078 0.095 -0.018 -0.089 0.194* -0.011(1.16) (0.72) (0.51) (0.65) (-0.22) (-0.58) (1.71) (-0.09)

Dist: Madhubani 0.031 0.242*** -0.113 -0.454*** -0.158** 0.162 -0.224** 0.145(0.37) (2.89) (-0.88) (-3.66) (-2.32) (1.25) (-2.33) (1.43)

Dist: Gopalganj -0.063 0.202** -0.064 -0.130 -0.167** 0.230* -0.227** 0.266***(-0.77) (2.46) (-0.50) (-1.07) (-2.51) (1.81) (-2.41) (2.68)

Dist: West Champaran 0.131 0.246*** -0.162 -0.220* -0.175** 0.245* -0.296*** 0.306***(1.55) (2.89) (-1.23) (-1.74) (-2.53) (1.86) (-3.04) (2.98)

Constant 0.778*** 0.649*** 0.579*** 0.473** 0.241** 0.306 0.181 0.141(6.34) (5.26) (3.04) (2.58) (2.40) (1.60) (1.28) (0.95)

r2 0.073 0.115 0.074 0.117 0.080 0.059 0.121 0.143N 122.000 122.000 122.000 122.000 122.000 122.000 122.000 122.000∗ p < 0.05, ∗∗ p < 0.01, ∗∗∗ p < 0.001

Table 2: Regressions of the mobilizer variables on each different message extracted from groupinterview transcripts.

4.2.2 Mobilizer dummies

The data in this paper includes three dummy variables about the types of mobilizers who

were present during mobilization of the particular SHG interviewed. As mentioned above, these

mobilizers have a vector of possible characteristics (Figure 2), each parameter of which, taken in

isolation, is notable for its effects on the development outcome be. It is also important to note that

in the mobilization process for a single SHG, more than one mobilizer can have participated—that

is, the sum of the three mobilizer variables in a single observation can be equal to or greater than 1.

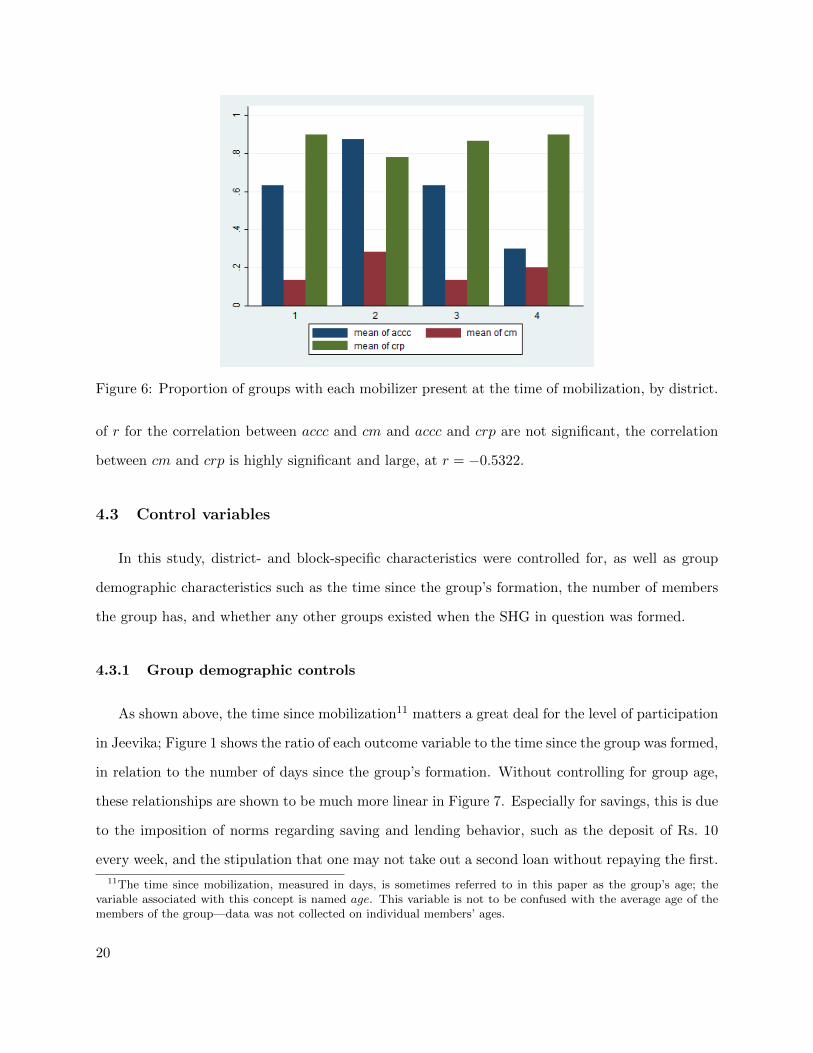

As Figure 6 shows, CRPs mobilized the majority of groups in the sample. In three of the

four districts, either an AC or CC was also present—in Gopalganj, only nine of the 30 SHGs

reported that an AC or CC was present at their mobilization; this may be due to particularly

difficult conditions including high workloads facing Jeevika staff in Gopalganj. Across the sample,

the rate of CM mobilization were relatively low, but consistent; Madhubani reported the greatest

intervention by CMs with nine groups recalling their CMs’ presence, while only four groups in

Khagaria and West Champaran, each respectively, recalled their CM mobilizing them.

As might be expected, the correlations between all three variables are negative; while the values

19

Figure 6: Proportion of groups with each mobilizer present at the time of mobilization, by district.

of r for the correlation between accc and cm and accc and crp are not significant, the correlation

between cm and crp is highly significant and large, at r = −0.5322.

4.3 Control variables

In this study, district- and block-specific characteristics were controlled for, as well as group

demographic characteristics such as the time since the group’s formation, the number of members

the group has, and whether any other groups existed when the SHG in question was formed.

4.3.1 Group demographic controls

As shown above, the time since mobilization11 matters a great deal for the level of participation

in Jeevika; Figure 1 shows the ratio of each outcome variable to the time since the group was formed,

in relation to the number of days since the group’s formation. Without controlling for group age,

these relationships are shown to be much more linear in Figure 7. Especially for savings, this is due

to the imposition of norms regarding saving and lending behavior, such as the deposit of Rs. 10

every week, and the stipulation that one may not take out a second loan without repaying the first.

11The time since mobilization, measured in days, is sometimes referred to in this paper as the group’s age; thevariable associated with this concept is named age. This variable is not to be confused with the average age of themembers of the group—data was not collected on individual members’ ages.

20

Figure 7: Averages of the dependent variables across the four districts studied: number of loanstaken by the average SHG member, lifetime amount of money borrowed by the average SHG

member, and lifetime savings of the average SHG member.

Figure 8: Time since formation of each group (in days), with a normal distribution function withcorresponding mean and standard deviation superimposed.

The age of groups in the sample is roughly normally distributed, as seen in 8, and has a minimum

of 267 days for Bhawani Jeevika SHG in the village of Madhuban in Andhrathadhi, Madhubani,

or slightly less than nine months since the mobilization of the group. The largest value for age

is 887 days, from Mithila Jeevika SHG, which was the first SHG formed in the village of Gaur,

Andhrathadhi, Madhubani, as it was formed at the beginning of April, 2012. The mean age of

groups, at 535 days (approximately one and one half years) was slightly less than the median of

549.5 days.

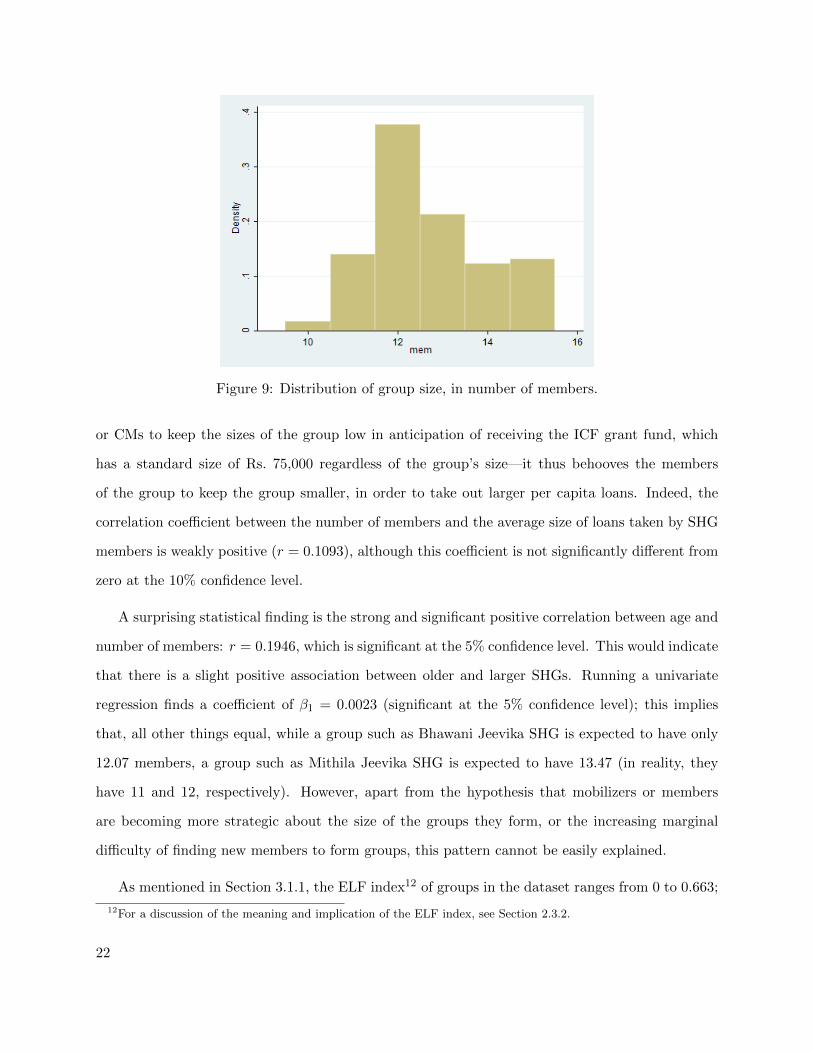

The groups in the sample all lie in the required range of 10-15 members, with the plurality (37.7

percent) having 12 members (see Figure 9). This may be in response to pressure from beneficiaries

21

Figure 9: Distribution of group size, in number of members.

or CMs to keep the sizes of the group low in anticipation of receiving the ICF grant fund, which

has a standard size of Rs. 75,000 regardless of the group’s size—it thus behooves the members

of the group to keep the group smaller, in order to take out larger per capita loans. Indeed, the

correlation coefficient between the number of members and the average size of loans taken by SHG

members is weakly positive (r = 0.1093), although this coefficient is not significantly different from

zero at the 10% confidence level.

A surprising statistical finding is the strong and significant positive correlation between age and

number of members: r = 0.1946, which is significant at the 5% confidence level. This would indicate

that there is a slight positive association between older and larger SHGs. Running a univariate

regression finds a coefficient of β1 = 0.0023 (significant at the 5% confidence level); this implies

that, all other things equal, while a group such as Bhawani Jeevika SHG is expected to have only

12.07 members, a group such as Mithila Jeevika SHG is expected to have 13.47 (in reality, they

have 11 and 12, respectively). However, apart from the hypothesis that mobilizers or members

are becoming more strategic about the size of the groups they form, or the increasing marginal

difficulty of finding new members to form groups, this pattern cannot be easily explained.

As mentioned in Section 3.1.1, the ELF index12 of groups in the dataset ranges from 0 to 0.663;

12For a discussion of the meaning and implication of the ELF index, see Section 2.3.2.

22

the mean index is 0.152 due to a large number—63.1 percent of all groups—having no diversity

whatsoever, and thus an ELF of zero. 16.4 percent of all groups have at least one member from the

non-majority religion in the group (as recorded by the variable reldiv), indicating a high rate of

groups that are entirely homogeneous by religion13. This may also be because a disproportionately

low proportion of respondents in the sample are Muslim; while the overall proportion in Bihar is

about 1 in 5, only about 8.6 percent of members surveyed were Muslim. This gap was most severely

pronounced for Khagaria, in which fewer than 1 in 20 respondents were Muslim.

4.3.2 Geographic controls

Inter-group variation that could not be explained through any of the independent or control

variables above were often accounted for by dummy variables indexed to the SHG’s district or block

(see Figure 4 for a breakdown of outcome variables by district). These variables were coded “1” if

an SHG fell into a particular district or block and “0” otherwise; in regressions, the first variable

in each set was omitted to avoid issues pertaining to multicollinearity.

5 Analysis

In this section, OLS regression analysis of the data shows the following effect:

The OLS regressions yielding the results in Tables 4–9 all take the general form:

Y = β0 +

i∑β1(X1)i +

j∑β2(X2)j +

k∑β3(X3)k +

l∑β4(X4)l + ε

Where: Y is the dependent variable, one of the three participation outcomes, (X1)i is a set of

messaging dummy variables, (X2)j is a set of mobilizer dummy variables, (X3)k is a set of group-

level control variables, (X4)l is a set of geographic control variables, β0 is the constant regression

13Formally, reldiv = 1 when at least one member of the group is not Hindu and one member of the group is notMuslim. The Diverse variable, represented by div, takes a value of 1 when at least two members of the group do notshare the same value of caste.

23

coefficient,∑β1 · · ·

∑β4 is a set of the sums of the regression coefficients on X1 · · ·X4, and ε is an

error term, assumed to be i.i.d.

5.1 Effect of mobilizers on Jeevika participation

Simple regressions of the three mobilizer variables on each participation measure variable (Tables

4, 5, and 6, Column 1) show the importance of CRPs’ presence in the mobilization process to

subsequent participation. The coefficient on the CRP variable is always significant (p < 0.1),

and the effect is shown to have a huge effect on both savings and lending: all other things equal,

having a CRP present during mobilization will cause an average member to withdraw approximately

Rs. 4,750 ($74.77) more, and save about Rs. 100 ($1.57) more—equivalent to ten weeks’ saving.

Additionally, in these regressions, CMs are predicted to positively affect borrowing amounts and

ACs and CCs are predicted to positively affect savings.

However, these effects becomes murkier with the addition of more potentially explanatory vari-

ables. For instance, in Table 4, Column 2 shows that the effect of CRPs on number of loans taken

does not change when geographical controls are taken into account. However, Columns 3 and 4

demonstrate that the effect is overshadowed by the explanatory effect of the control variables, es-

pecially the variable of whether another SHG was present during mobilization: if one was, then,

all other things equal, members are predicted to take 0.8 fewer loans.

Similarly, Columns 2, 3, and 4 of Table 5 show that while the effect of CRPs on the amount of

money a member borrows is not diminished by the inclusion of messages or geographical controls—

either at the district or block level—it is diminished by the inclusion of the othershg variable, the

coefficient on which is significant and negative. Additionally, the table shows that older groups

borrow more than younger groups, all other things equal, and that the older groups that were

mobilized by ACs and CCs participate less than younger groups that were mobilized in the same

way.

The results of mobilizers on savings are perhaps the most interesting: without controlling for

geographic idiosyncrasies, or when controlling for geographic idiosyncrasies at the district level,

24

(1) (2)CM Present

AC or CC Present -0.137* -0.507***(-1.95) (-2.97)

CRP Present -0.602*** -0.873***(-6.60) (-6.02)

Block=2 0.056 0.051(0.45) (0.42)

Block=3 0.084 0.080(0.70) (0.68)

Block=4 0.192 0.174(1.61) (1.49)

Block=5 0.030 -0.012(0.25) (-0.10)

Block=6 -0.014 -0.052(-0.11) (-0.43)

Block=7 0.167 0.158(1.32) (1.28)

Block=8 -0.069 -0.084(-0.54) (-0.67)

AC/CC and CRP Present 0.426**(2.37)

Constant 0.734*** 0.987***(5.89) (6.08)

R2 0.351 0.382N 122.000 122.000

Table 3: Results of regression of mobilizers’ presence on the likelihood that a CM will be present.

savings seem to be affected most by the CRPs out of all three kinds of mobilizers. However,

when controlling for more granular geographic effects at the block level, CMs show an increasingly

significant effect as more variables are added. The effect is in the negative direction, such that a

group that was mobilized with a CM present will save Rs. 384 ($6.04) less than one without a CM

present at mobilization, all other things equal. In terms of saving, this is equivalent to a 46 percent

reduction in participation.

An interesting additional note to this observation is the low chance that a CM will be present

if any other kind of mobilizer is present (results shown in Table 3). If an AC or CC is present

without a CRP, the data predicts that a CM is half as likely to be present, and if a CRP is present

without an AC or CC, the data predicts that a CM will be almost one-tenth as likely to be present.

Interestingly, if both an AC/CC and a CRP are present, a CM is in fact 42.6 percent more likely

to have joined them.

Other results from the regressions showing the effects of mobilizers on savings include the

relevance of time: an SHG that was formed a week earlier will save Rs. 3.98 ($0.06) more. The

25

effect of one standard deviation in formation date is thus a whopping Rs. 62.43 ($0.98) in per-capita

savings, even holding all other factors constant. Table 6 also shows that for groups formed later,

CMs encourage more and more participation, such that holding other factors constant, having a

CM form a group a week later is associated with the group’s members saving Rs. 4.35 ($0.07) more.

Finally, savings are also affected by the identities of the members of the group: a religiously diverse

group will save Rs. 71.35 ($1.12) more, all other things equal.

5.2 Effect of messaging on Jeevika participation

Overall, mobilization messages are shown to give relatively little explanation of the variation in

participation outcomes in Jeevika compared to locale-specific, group-demographic, and mobilizer

variation. In fact, in a simple regression of messages on the number of times a Jeevika member

takes out a loan yields no significant right-hand-side variables other than the constant term, a point

estimate—in other words, the regression predicts that, on the basis of the messages given, all Jeevika

beneficiaries will borrow exactly 2.65 times. This is true regardless of the inclusion of mobilizers

(Table 7, Column 3) or block-specific controls (Column 5) in the regression or not; Column 6

elaborates that this effect (or lack thereof) persists when other controls are added to geographic

controls. On the other hand, Columns 2 and 4 show that one message, poverty, becomes significant

with the inclusion of group-demographic controls. This effect persists in the largest regression in

Column 7. The coefficient on poverty is negative; it indicates that the act of sharing a message

such as “Jeevika will get you out of poverty” is associated with borrowing 0.385 of one time less.

In a regression of all available explanatory variables except geographical controls on the average

per capita amount of money withdrawn by a Jeevika member (Table 8, Column 1), no message is

shown to have a significant effect; the same is true for a regression that includes block-level controls

(Column 4). Interestingly, the message activities is significant and negative when it its regressed on

the average total amount of loans along with block-level controls and mobilizer variables. This may

be a chance product of the omitted variables age and othershg, which are significantly correlated

with activities (r = 0.22; p ≈ 0.01 for both correlations, respectively).

In predicting the effects of messages on savings behavior among Jeevika members (Table 9),

26

two messages stand out: together and work, represented in Table 9 as “Togetherness” and “Jobs”.

Both variables have significant, relatively large, and negative regression coefficients14. The clear

result in this case is that messages such as “you will come together as one” and “you will receive

employment opportunities” hurt potential beneficiaries’ future participation levels.

6 Discussion

So far, this paper has found that while the the role and identity of a particular mobilizer

matters considerably to the level of participation found among beneficiaries, messages thought to

be positive, such as poverty, together, and work can actually lead to less participation. This section

brings some insights and theories from the literature to bear to find why these findings may have

arisen.

6.1 Implications for social capital theory

Like physical, human, or political capital, social capital exists because of the investment a

particular person contributes to it (Collier, 2002; Knack and Keefer, 1997b). Glaeser et al. (2002)

defines social capital for their own purposes as “. . . a person’s social characteristics—including social

skills, charisma, and the size of his Rolodex—which enables him to reap market and non-market

returns from interactions with others. As such, individual social capital might be seen as the social

component of human capital.” This definition heavily implies that besides tangible investments

in social capital one can make—such as a large Rolodex—one can also invest in intangible social

assets, like the relationships represented in the Rolodex. An individual is also endowed with a

stock of innate, idiosyncratic social capital (e.g. charisma, which cannot be honed and practiced

like “social skills”).

This is crucial for the current-day setting of Jeevika. Testimony from respondents to the survey

conducted for this study indicates that the current amount of time spent in a village by a mobilizing

14A skeptic may claim here that these coefficients could not be individually negatively correlated with positivesavings—however, in fact, the significant regression coefficients derived from univariate regression of together andwork on avgsavings are indeed negative, and larger than those in the regressions shown in Table 9

27

team is far from the recommended 45 days—in fact, most respondents in Madhubani recalled CRPs

spending no more than three days with each group before leaving the members to their own devices.

Most likely, this is a paired effect of the pressure from supervisors to create as many groups as

possible, and the desire to work as little as possible in order to receive the CRP stipend, which is

paid as a lump sum for 45 days’ work15.

In situations like the mobilization process, which may involve as little as three days in order to

establish relationships and build social capital, the contribution of investment social capital to an

overall level of social capital can be far out-shadowed by an individual’s personal prior endowment

of social capital. As seen in Section 5.1 above, an important aspect of this prior endowment is the

identity and role an individual carries. As a poor, typically illiterate, married, lower-caste woman

with command of the sociolinguistically relevant local dialect, a CRP is much more likely to be

able to foment participation and intrinsic motivation than a CM, AC, or CC.

6.2 Why positive messages can lead to less participation

It is difficult to tell why certain messages—poverty, activities, and together among them—

lead to reduced rates of participation rather than increasing them. A possible theory proposed

by Vansteenkiste et al. (2004) is the notion of “crowding out” motivation: that given too many

overt, extrinsic motives, an individual may lose sight of intrinsically important motives, and lose

motivation overall.

It is also possible that, as alluded to by Mansuri and Rao (2013), Mosse (2004), and Botes

and Van Rensburg (2000), the poorest of the poor may not respond as readily to non-material

incentives as material incentives, and without the granting of material incentives—food, work, or

money—the potential beneficiaries would choose to spend their time away from Jeevika meetings.

Additional evidence for this hypothesis comes from Table 2, which shows that CMs, with their more

intimate knowledge of the community being mobilized, use less of the poverty message. However,

15In fact, while a rationally acting individual fully expecting to be paid the stipend may adopt the same course ofaction, CRPs are often wary that the stipend will not be paid at all, further diminishing their motivation to work forlonger.

28

this explanation lacks considerable support, and shows ample room for improvement in future

qualitative and mixed-methods studies.

6.3 Implications for the great aid debate: Is localization worth it?

This paper presents a nuanced case study to the literature on overarching theories of aid and

development. Jeevika has not had universal success in scaling up—in the groups with the lowest

levels of participation, the group had only apportioned four loans among 12 members, loans totaled

only Rs. 125 ($1.96), and savings amounted to Rs. 130 ($2.04) per member. However, the program

has also achieved enormous successes, including one group that has an average borrowing rate of

Rs. 33,367 ($524.76) per member.

Other groups have made great strides in social empowerment: whereas before, members may

have been victims of domestic violence, denied agency in the household, and physically and socially

immobile, many survey respondents reported feeling liberated through increased solidarity with the

members of their SHGs. When asked what they would want to do further with Jeevika (Hindi:

Jeevika ke bare me aur kya hona chahiye? ), about one in five groups in this study wanted to

expand Jeevika by enlarging loans, one group thought that the savings rates were too low, and

many wanted to build education programs through Jeevika and meeting-houses for the SHGs and

Village Organizations.

The conclusion overall, then, is that yes: localization is worth it. By continuing the mobilization

process and perfecting the messages and the building of social capital between mobilizers and

potential beneficiaries, Jeevika is, in fact, making much larger strides toward sustainable, grassroots

economic and social empowerment than the Millennium Villages Project or any “shock-therapy”

program.

7 Conclusion: Policy Implications and Further Research

This research and analysis draws the following conclusions:

29

1. Among all mobilizers, CRPs most effectively encourage participation in Jeevika in the form

of savings;

2. For other measures of participation, the effect of mobilizers is washed out by group- and

area-specific features;

3. Groups mobilized by CMs tend to show less participation than average in the form of savings;

4. CMs are most likely to mobilize a group only in two situations: entirely alone, or as a small

part of CRPs, ACs and CCs;

5. Groups formed further in the past participate more in Jeevika, with an effect noticeable even

in data limited to a span of one year;

6. While the effects of mobilization messages on participation are minimal, certain messages—

poverty, together, and work, for example—lead to less participation than average, holding

other factors constant.

There are four main, direct implications of these findings for CDD programs such as Jeevika.

First, for the greatest level of participation during scale-up, the organization should actively pursue

a strategy of “the poor recruiting the poor” through a CRP drive rather than a model of using

professional Program Resource Persons as represented in Khan et al. (2013). Second, as far as

possible, CRPs should have more than adequate knowledge of the area of mobilization, or should

be allowed ample time—upwards of one month—to become acquainted with the local context

of mobilization and build interpersonal social capital before they begin the mobilization process.

Third, while it may be tempting to allow groups to form independently of the CRP process through

CMs, these groups may not have adequate information and cohesive social capital to effectively

enforce the Panchasutra (see Appendix B). Finally, CRPs should be careful to allow prospective

beneficiaries to come to their own conclusions about whether to join or not—those who do will

have high levels of intrinsic motivation, and may become strongly empowered by the program.

While this study opens the way for further research on the role promised incentives and individ-

ual decisions interact in the sphere of development, much remains to be explored. Further research

30

may use more heavily qualitative methods or theoretical economic methods to determine the struc-

ture and tradeoffs involved in the decision of whether or not to participate in a CDD organization,

and if so, how much. Other directions include the interpersonal strategies CRPs use to build social

capital during the mobilization process, that may be transferred to CMs, ACs, and CCs; behavioral

economic experimentation to determine which incentives function in which ways in the laboratory

setting; dynamic network analysis using qualitative and quantitative methods to determine how

social capital lubricates economic empowerment on the micro scale; and cross-organizational em-

pirical study to find whether other strategies of scale-up, such as the use of PRPs, may, in fact,

benefit . Finally, this preliminary investigation provides significant rationale for a larger study with

an increased sample size, employing the textual/qualitative and quantitative analyses used in this

paper, to better understand the decision at the moment of mobilization.

31

References

Binswanger, H. P. and S. S. Aiyar (2003). Scaling up community-driven development: theoretical