Bajaj Electricals - A Multi-Year Compounding Machine at Reasonable Valuations Our key objective is to pick stocks which can compound sustainably at a healthy rate for the next 3-5 years and create wealth. We like to select companies with strong competitive advantages and are quoting at a discount to their intrinsic value.

Bajaj electricals a compounding machine !

Sep 13, 2014

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Bajaj Electricals - A Multi-Year Compounding Machine at Reasonable Valuations

Our key objective is to pick stocks which can compound sustainably at a healthy

rate for the next 3-5 years and create wealth. We like to select companies with strong

competitive advantages and are quoting at a discount to their intrinsic value.

Content Index

• Bajaj Electricals – Investment Snapshot :- Slide #3 • Industry Opportunity – An Overview:- Slide #6 • Bajaj Electricals – Business Overview :- Slide #14 • Investment Rationale :- Slide #23 • Bajaj Electricals – Financials:- Slide #30 • Concerns & Reasoning :- Slide #32 • Conclusion :- Slide #35

“ Specialists in discovering Multibagger stocks “

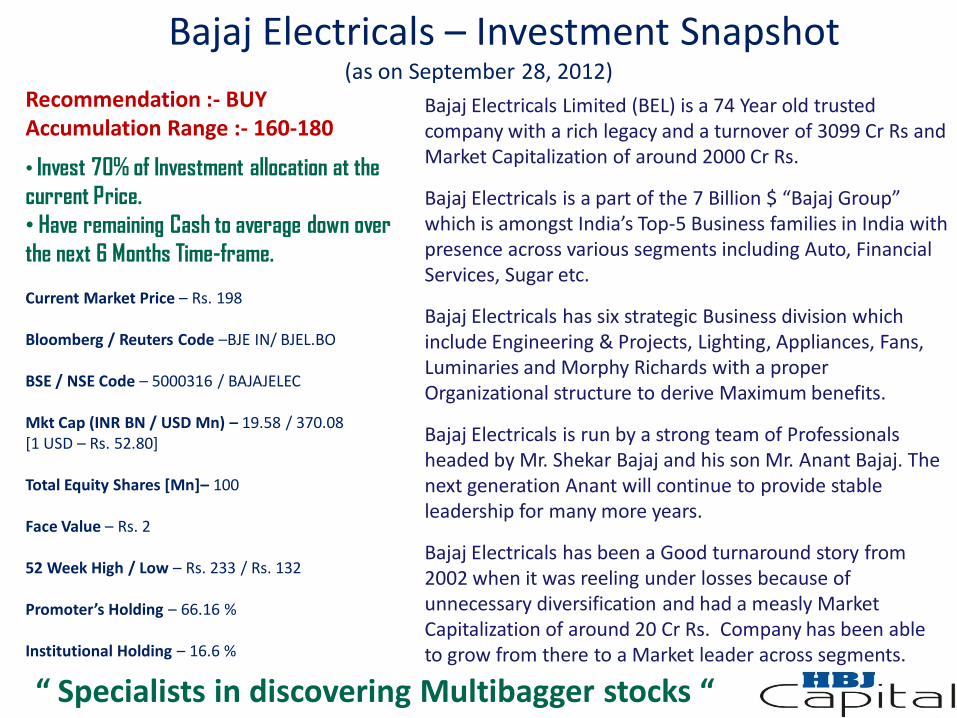

Bajaj Electricals – Investment Snapshot (as on September 28, 2012)

Recommendation :- BUY Accumulation Range :- 160-180

• Invest 70% of Investment allocation at the

current Price.

• Have remaining Cash to average down over

the next 6 Months Time-frame. Current Market Price – Rs. 198 Bloomberg / Reuters Code –BJE IN/ BJEL.BO BSE / NSE Code – 5000316 / BAJAJELEC Mkt Cap (INR BN / USD Mn) – 19.58 / 370.08 [1 USD – Rs. 52.80] Total Equity Shares [Mn]– 100 Face Value – Rs. 2 52 Week High / Low – Rs. 233 / Rs. 132 Promoter’s Holding – 66.16 % Institutional Holding – 16.6 %

Bajaj Electricals Limited (BEL) is a 74 Year old trusted company with a rich legacy and a turnover of 3099 Cr Rs and Market Capitalization of around 2000 Cr Rs.

Bajaj Electricals is a part of the 7 Billion $ “Bajaj Group” which is amongst India’s Top-5 Business families in India with presence across various segments including Auto, Financial Services, Sugar etc.

Bajaj Electricals has six strategic Business division which include Engineering & Projects, Lighting, Appliances, Fans, Luminaries and Morphy Richards with a proper Organizational structure to derive Maximum benefits.

Bajaj Electricals is run by a strong team of Professionals headed by Mr. Shekar Bajaj and his son Mr. Anant Bajaj. The next generation Anant will continue to provide stable leadership for many more years.

Bajaj Electricals has been a Good turnaround story from 2002 when it was reeling under losses because of unnecessary diversification and had a measly Market Capitalization of around 20 Cr Rs. Company has been able to grow from there to a Market leader across segments.

“ Specialists in discovering Multibagger stocks “

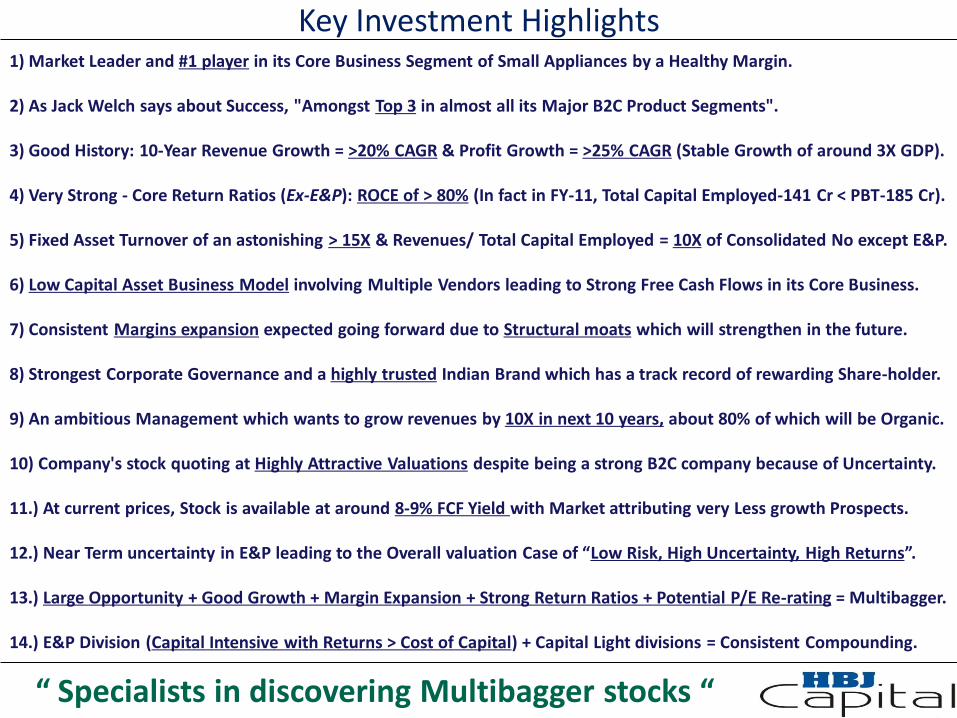

Key Investment Highlights 1) Market Leader and #1 player in its Core Business Segment of Small Appliances by a Healthy Margin.

2) As Jack Welch says about Success, "Amongst Top 3 in almost all its Major B2C Product Segments". 3) Good History: 10-Year Revenue Growth = >20% CAGR & Profit Growth = >25% CAGR (Stable Growth of around 3X GDP). 4) Very Strong - Core Return Ratios (Ex-E&P): ROCE of > 80% (In fact in FY-11, Total Capital Employed-141 Cr < PBT-185 Cr). 5) Fixed Asset Turnover of an astonishing > 15X & Revenues/ Total Capital Employed = 10X of Consolidated No except E&P. 6) Low Capital Asset Business Model involving Multiple Vendors leading to Strong Free Cash Flows in its Core Business. 7) Consistent Margins expansion expected going forward due to Structural moats which will strengthen in the future. 8) Strongest Corporate Governance and a highly trusted Indian Brand which has a track record of rewarding Share-holder. 9) An ambitious Management which wants to grow revenues by 10X in next 10 years, about 80% of which will be Organic. 10) Company's stock quoting at Highly Attractive Valuations despite being a strong B2C company because of Uncertainty. 11.) At current prices, Stock is available at around 8-9% FCF Yield with Market attributing very Less growth Prospects. 12.) Near Term uncertainty in E&P leading to the Overall valuation Case of “Low Risk, High Uncertainty, High Returns”. 13.) Large Opportunity + Good Growth + Margin Expansion + Strong Return Ratios + Potential P/E Re-rating = Multibagger. 14.) E&P Division (Capital Intensive with Returns > Cost of Capital) + Capital Light divisions = Consistent Compounding.

“ Specialists in discovering Multibagger stocks “

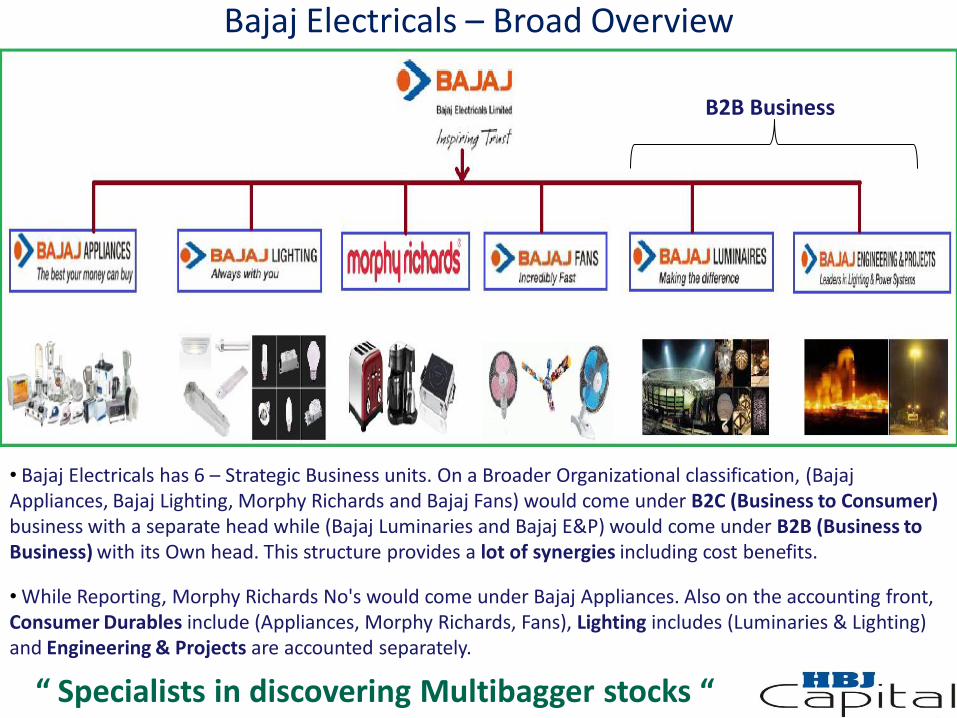

Bajaj Electricals – Broad Overview

• Bajaj Electricals has 6 – Strategic Business units. On a Broader Organizational classification, (Bajaj Appliances, Bajaj Lighting, Morphy Richards and Bajaj Fans) would come under B2C (Business to Consumer) business with a separate head while (Bajaj Luminaries and Bajaj E&P) would come under B2B (Business to Business) with its Own head. This structure provides a lot of synergies including cost benefits.

• While Reporting, Morphy Richards No's would come under Bajaj Appliances. Also on the accounting front, Consumer Durables include (Appliances, Morphy Richards, Fans), Lighting includes (Luminaries & Lighting) and Engineering & Projects are accounted separately.

“ Specialists in discovering Multibagger stocks “

B2B Business

Industry Opportunity & Potential - An Overview

“ Specialists in discovering Multibagger stocks “

Appliances Segment

“ Specialists in discovering Multibagger stocks “

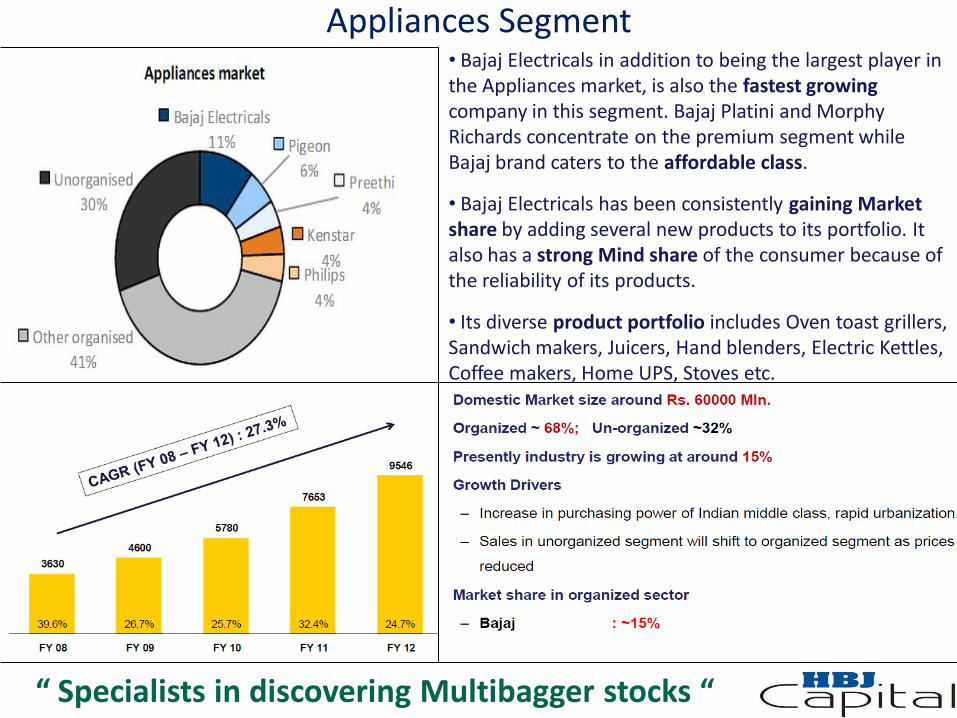

• Bajaj Electricals in addition to being the largest player in the Appliances market, is also the fastest growing company in this segment. Bajaj Platini and Morphy Richards concentrate on the premium segment while Bajaj brand caters to the affordable class.

• Bajaj Electricals has been consistently gaining Market share by adding several new products to its portfolio. It also has a strong Mind share of the consumer because of the reliability of its products.

• Its diverse product portfolio includes Oven toast grillers, Sandwich makers, Juicers, Hand blenders, Electric Kettles, Coffee makers, Home UPS, Stoves etc.

Fans Segment

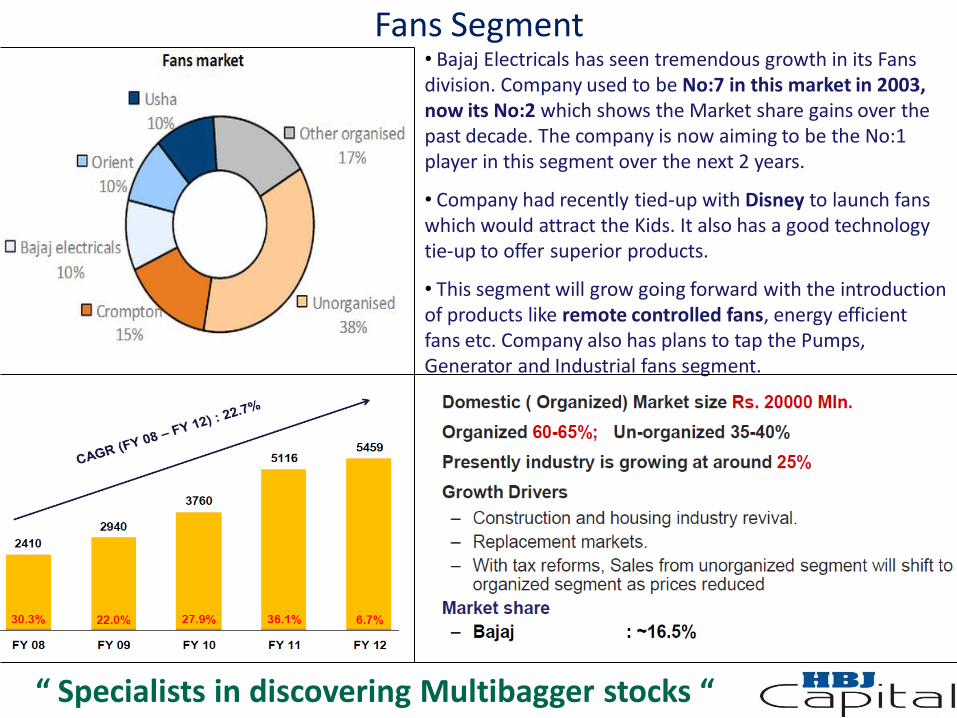

• Bajaj Electricals has seen tremendous growth in its Fans division. Company used to be No:7 in this market in 2003, now its No:2 which shows the Market share gains over the past decade. The company is now aiming to be the No:1 player in this segment over the next 2 years.

• Company had recently tied-up with Disney to launch fans which would attract the Kids. It also has a good technology tie-up to offer superior products.

• This segment will grow going forward with the introduction of products like remote controlled fans, energy efficient fans etc. Company also has plans to tap the Pumps, Generator and Industrial fans segment.

“ Specialists in discovering Multibagger stocks “

Lighting Segment

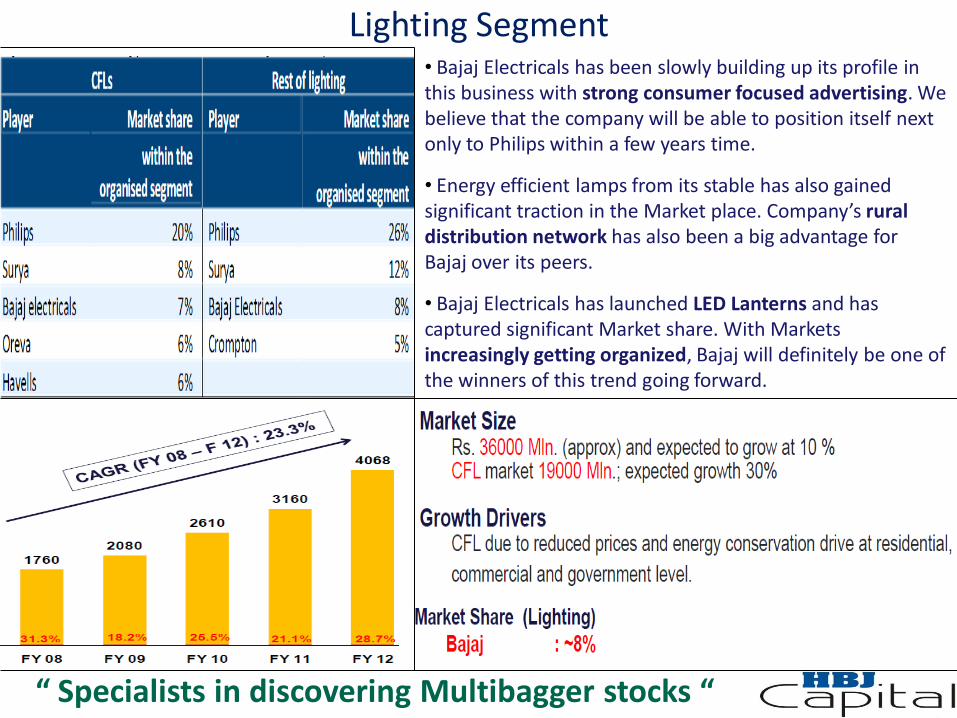

• Bajaj Electricals has been slowly building up its profile in this business with strong consumer focused advertising. We believe that the company will be able to position itself next only to Philips within a few years time.

• Energy efficient lamps from its stable has also gained significant traction in the Market place. Company’s rural distribution network has also been a big advantage for Bajaj over its peers.

• Bajaj Electricals has launched LED Lanterns and has captured significant Market share. With Markets increasingly getting organized, Bajaj will definitely be one of the winners of this trend going forward.

“ Specialists in discovering Multibagger stocks “

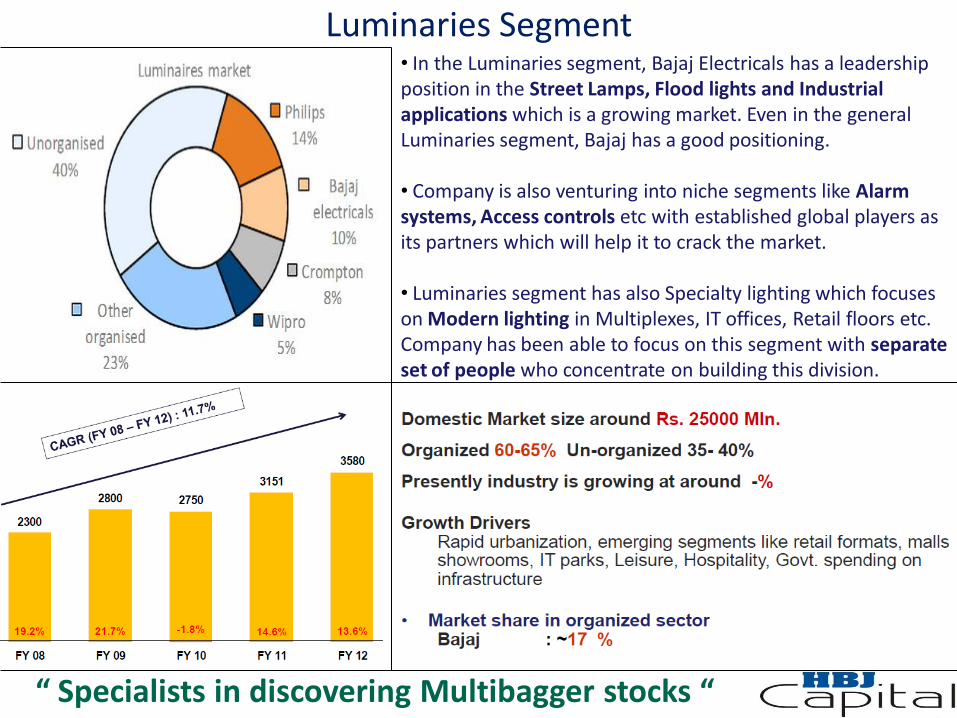

Luminaries Segment

• In the Luminaries segment, Bajaj Electricals has a leadership position in the Street Lamps, Flood lights and Industrial applications which is a growing market. Even in the general Luminaries segment, Bajaj has a good positioning. • Company is also venturing into niche segments like Alarm systems, Access controls etc with established global players as its partners which will help it to crack the market. • Luminaries segment has also Specialty lighting which focuses on Modern lighting in Multiplexes, IT offices, Retail floors etc. Company has been able to focus on this segment with separate set of people who concentrate on building this division.

“ Specialists in discovering Multibagger stocks “

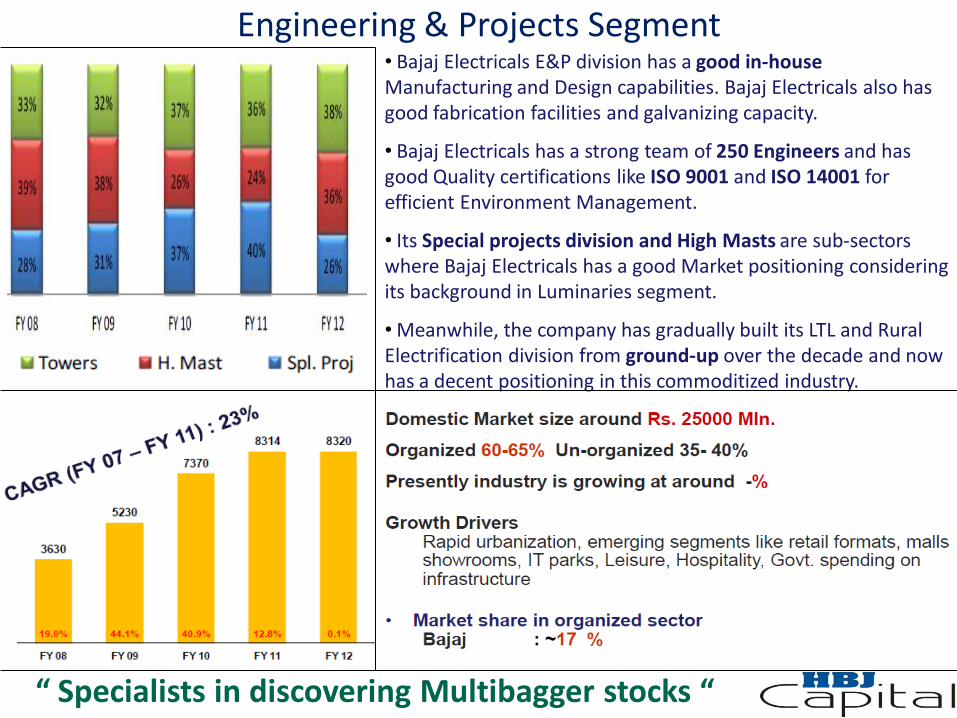

Engineering & Projects Segment

• Bajaj Electricals E&P division has a good in-house Manufacturing and Design capabilities. Bajaj Electricals also has good fabrication facilities and galvanizing capacity.

• Bajaj Electricals has a strong team of 250 Engineers and has good Quality certifications like ISO 9001 and ISO 14001 for efficient Environment Management.

• Its Special projects division and High Masts are sub-sectors where Bajaj Electricals has a good Market positioning considering its background in Luminaries segment.

• Meanwhile, the company has gradually built its LTL and Rural Electrification division from ground-up over the decade and now has a decent positioning in this commoditized industry.

“ Specialists in discovering Multibagger stocks “

Engineering & Projects Opportunity

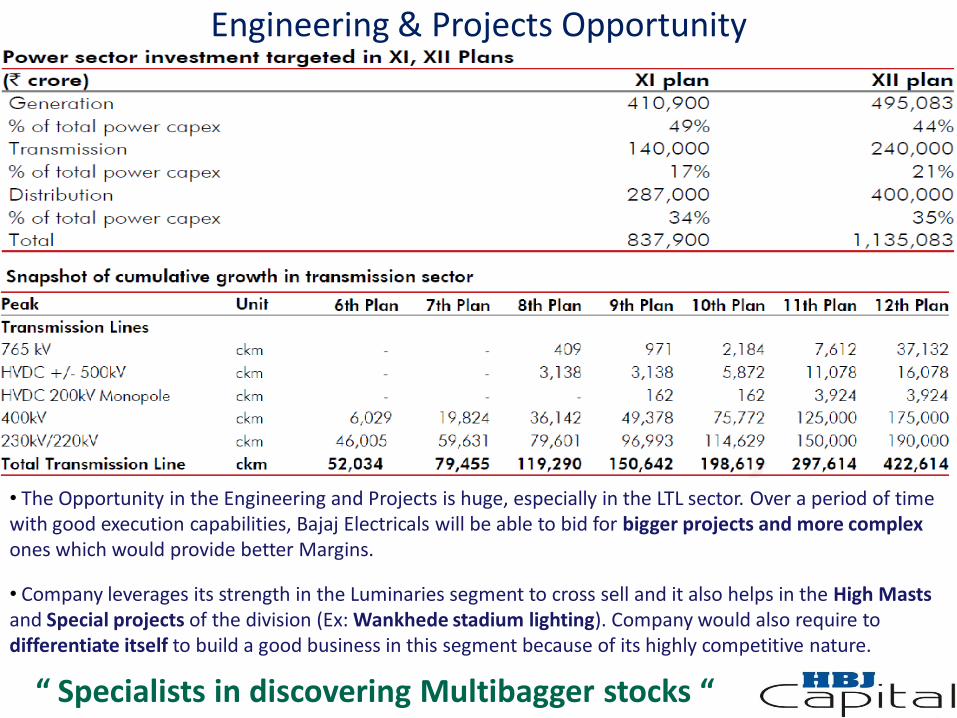

• The Opportunity in the Engineering and Projects is huge, especially in the LTL sector. Over a period of time with good execution capabilities, Bajaj Electricals will be able to bid for bigger projects and more complex ones which would provide better Margins.

• Company leverages its strength in the Luminaries segment to cross sell and it also helps in the High Masts and Special projects of the division (Ex: Wankhede stadium lighting). Company would also require to differentiate itself to build a good business in this segment because of its highly competitive nature.

“ Specialists in discovering Multibagger stocks “

Segmental Snapshot

“ Specialists in discovering Multibagger stocks “

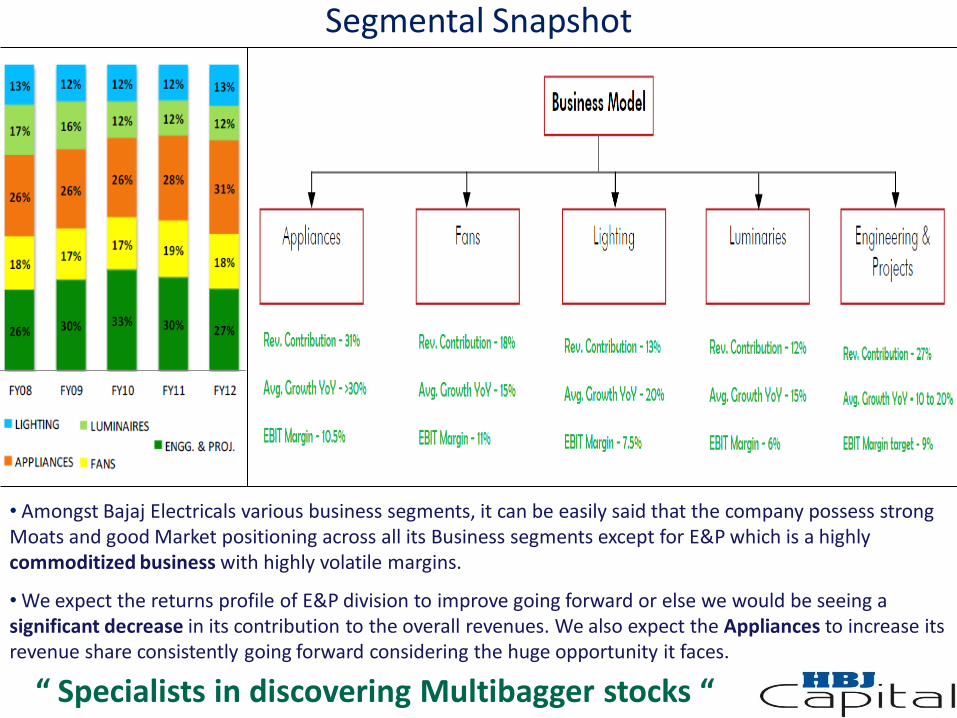

• Amongst Bajaj Electricals various business segments, it can be easily said that the company possess strong Moats and good Market positioning across all its Business segments except for E&P which is a highly commoditized business with highly volatile margins.

• We expect the returns profile of E&P division to improve going forward or else we would be seeing a significant decrease in its contribution to the overall revenues. We also expect the Appliances to increase its revenue share consistently going forward considering the huge opportunity it faces.

Bajaj Electricals – Business Overview

“ Specialists in discovering Multibagger stocks “

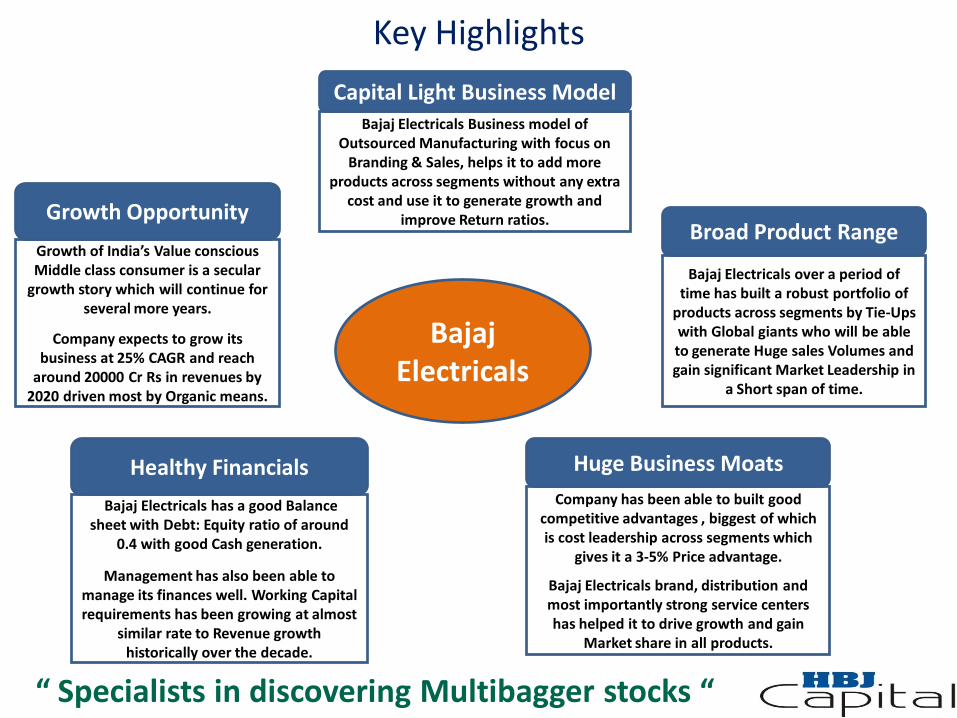

Key Highlights

Bajaj Electricals Business model of Outsourced Manufacturing with focus on

Branding & Sales, helps it to add more products across segments without any extra

cost and use it to generate growth and improve Return ratios.

Capital Light Business Model

Bajaj Electricals over a period of time has built a robust portfolio of

products across segments by Tie-Ups with Global giants who will be able to generate Huge sales Volumes and gain significant Market Leadership in

a Short span of time.

Broad Product Range

Company has been able to built good competitive advantages , biggest of which is cost leadership across segments which

gives it a 3-5% Price advantage.

Bajaj Electricals brand, distribution and most importantly strong service centers has helped it to drive growth and gain

Market share in all products.

Huge Business Moats

Bajaj Electricals has a good Balance sheet with Debt: Equity ratio of around

0.4 with good Cash generation.

Management has also been able to manage its finances well. Working Capital requirements has been growing at almost

similar rate to Revenue growth historically over the decade.

Healthy Financials

Growth of India’s Value conscious Middle class consumer is a secular

growth story which will continue for several more years.

Company expects to grow its business at 25% CAGR and reach

around 20000 Cr Rs in revenues by 2020 driven most by Organic means.

Growth Opportunity

Bajaj Electricals

“ Specialists in discovering Multibagger stocks “

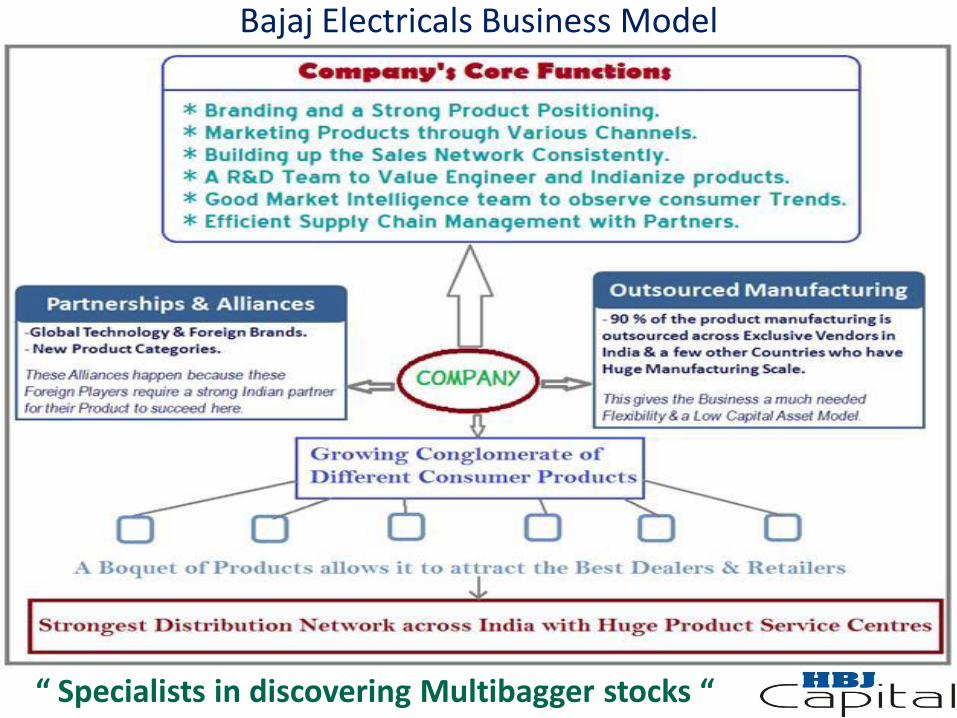

Bajaj Electricals Business Model

“ Specialists in discovering Multibagger stocks “

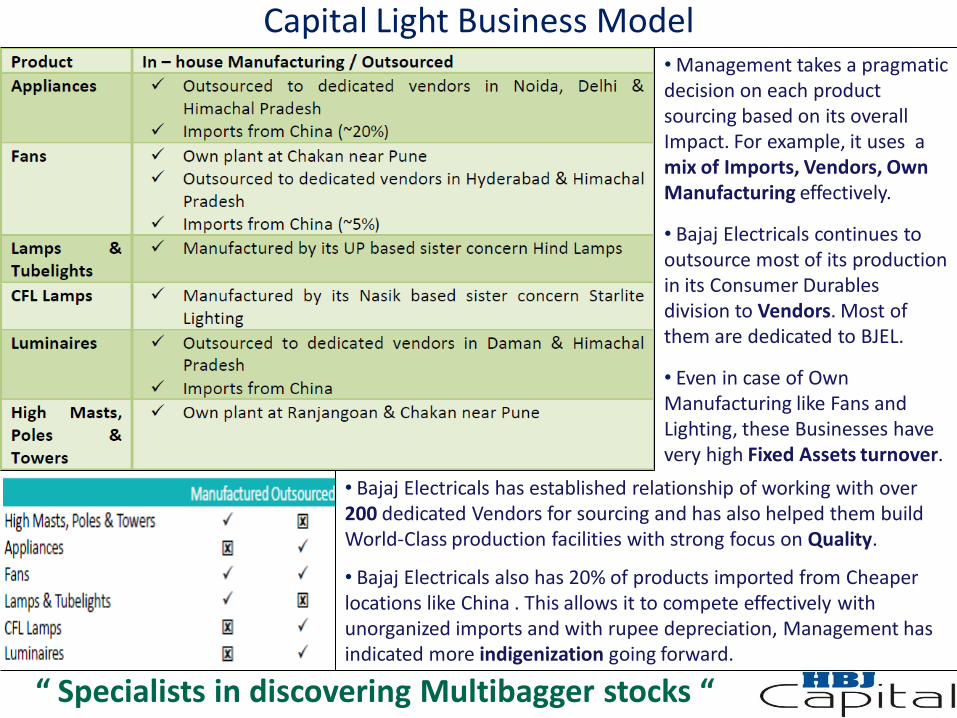

Capital Light Business Model

“ Specialists in discovering Multibagger stocks “

• Management takes a pragmatic decision on each product sourcing based on its overall Impact. For example, it uses a mix of Imports, Vendors, Own Manufacturing effectively.

• Bajaj Electricals continues to outsource most of its production in its Consumer Durables division to Vendors. Most of them are dedicated to BJEL.

• Even in case of Own Manufacturing like Fans and Lighting, these Businesses have very high Fixed Assets turnover. • Bajaj Electricals has established relationship of working with over

200 dedicated Vendors for sourcing and has also helped them build World-Class production facilities with strong focus on Quality.

• Bajaj Electricals also has 20% of products imported from Cheaper locations like China . This allows it to compete effectively with unorganized imports and with rupee depreciation, Management has indicated more indigenization going forward.

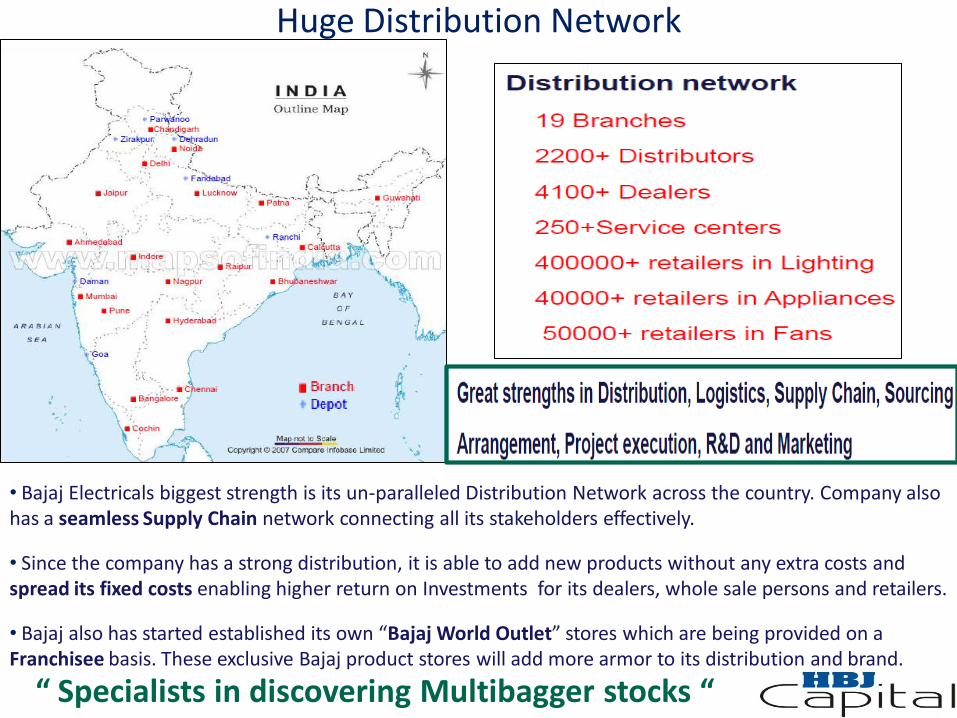

Huge Distribution Network

• Bajaj Electricals biggest strength is its un-paralleled Distribution Network across the country. Company also has a seamless Supply Chain network connecting all its stakeholders effectively.

• Since the company has a strong distribution, it is able to add new products without any extra costs and spread its fixed costs enabling higher return on Investments for its dealers, whole sale persons and retailers.

• Bajaj also has started established its own “Bajaj World Outlet” stores which are being provided on a Franchisee basis. These exclusive Bajaj product stores will add more armor to its distribution and brand.

“ Specialists in discovering Multibagger stocks “

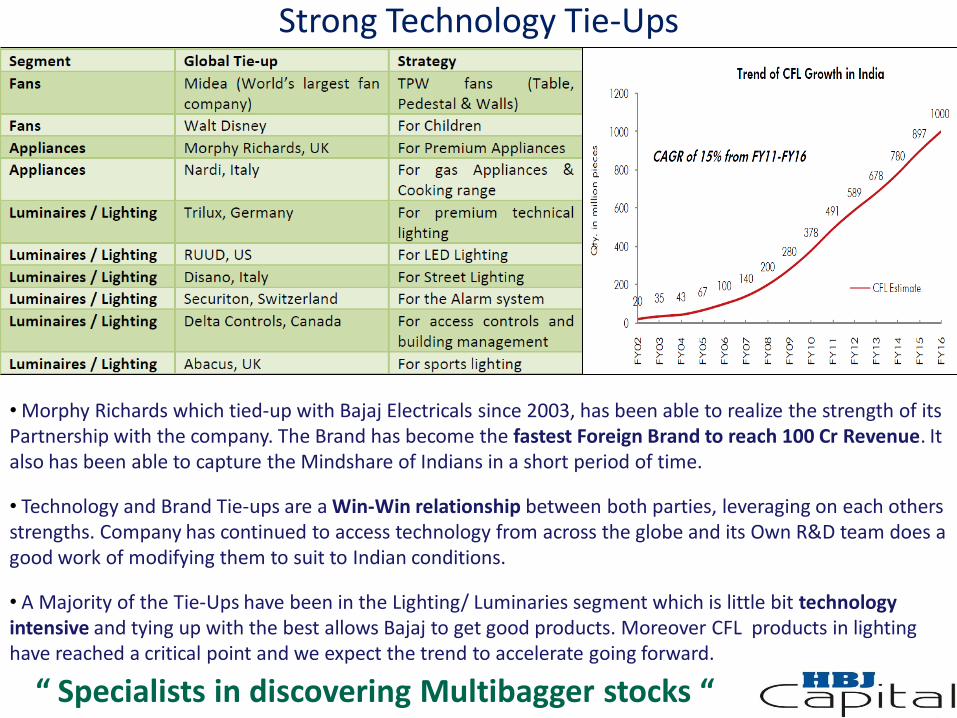

Strong Technology Tie-Ups

“ Specialists in discovering Multibagger stocks “

• Morphy Richards which tied-up with Bajaj Electricals since 2003, has been able to realize the strength of its Partnership with the company. The Brand has become the fastest Foreign Brand to reach 100 Cr Revenue. It also has been able to capture the Mindshare of Indians in a short period of time.

• Technology and Brand Tie-ups are a Win-Win relationship between both parties, leveraging on each others strengths. Company has continued to access technology from across the globe and its Own R&D team does a good work of modifying them to suit to Indian conditions.

• A Majority of the Tie-Ups have been in the Lighting/ Luminaries segment which is little bit technology intensive and tying up with the best allows Bajaj to get good products. Moreover CFL products in lighting have reached a critical point and we expect the trend to accelerate going forward.

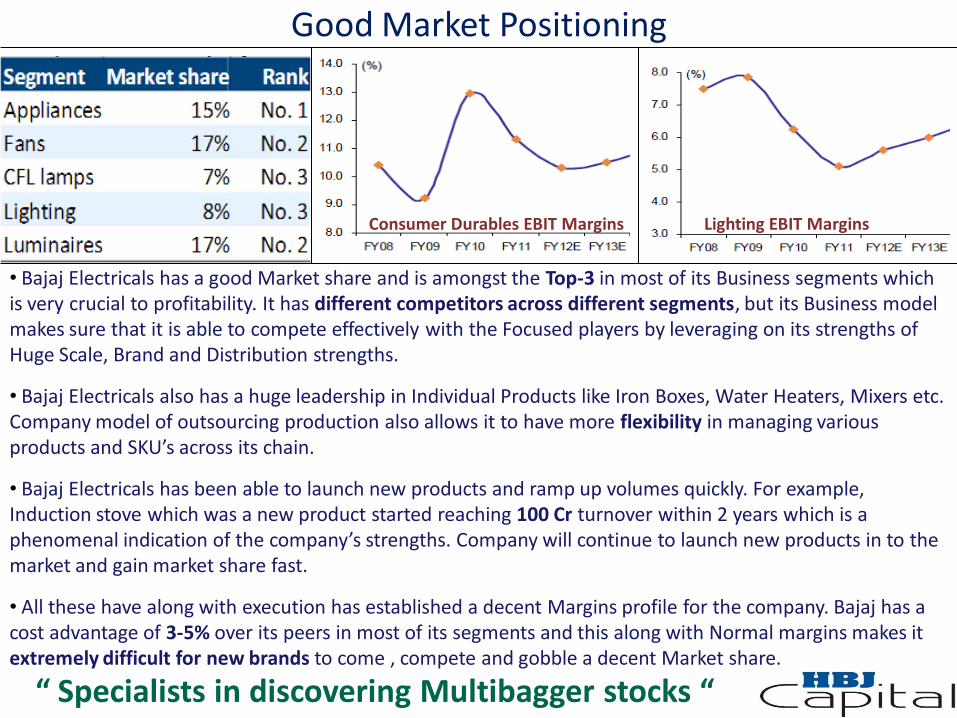

Good Market Positioning

• Bajaj Electricals has a good Market share and is amongst the Top-3 in most of its Business segments which is very crucial to profitability. It has different competitors across different segments, but its Business model makes sure that it is able to compete effectively with the Focused players by leveraging on its strengths of Huge Scale, Brand and Distribution strengths.

• Bajaj Electricals also has a huge leadership in Individual Products like Iron Boxes, Water Heaters, Mixers etc. Company model of outsourcing production also allows it to have more flexibility in managing various products and SKU’s across its chain.

• Bajaj Electricals has been able to launch new products and ramp up volumes quickly. For example, Induction stove which was a new product started reaching 100 Cr turnover within 2 years which is a phenomenal indication of the company’s strengths. Company will continue to launch new products in to the market and gain market share fast.

• All these have along with execution has established a decent Margins profile for the company. Bajaj has a cost advantage of 3-5% over its peers in most of its segments and this along with Normal margins makes it extremely difficult for new brands to come , compete and gobble a decent Market share. “ Specialists in discovering Multibagger stocks “

Lighting EBIT Margins Consumer Durables EBIT Margins

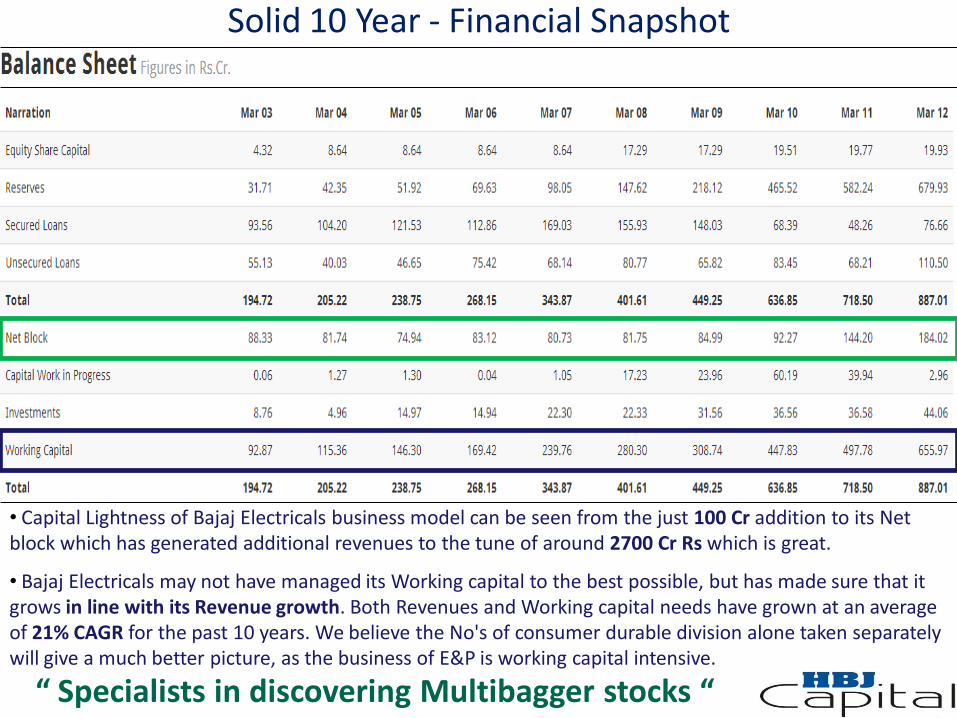

Solid 10 Year - Financial Snapshot

“ Specialists in discovering Multibagger stocks “

• Capital Lightness of Bajaj Electricals business model can be seen from the just 100 Cr addition to its Net block which has generated additional revenues to the tune of around 2700 Cr Rs which is great.

• Bajaj Electricals may not have managed its Working capital to the best possible, but has made sure that it grows in line with its Revenue growth. Both Revenues and Working capital needs have grown at an average of 21% CAGR for the past 10 years. We believe the No's of consumer durable division alone taken separately will give a much better picture, as the business of E&P is working capital intensive.

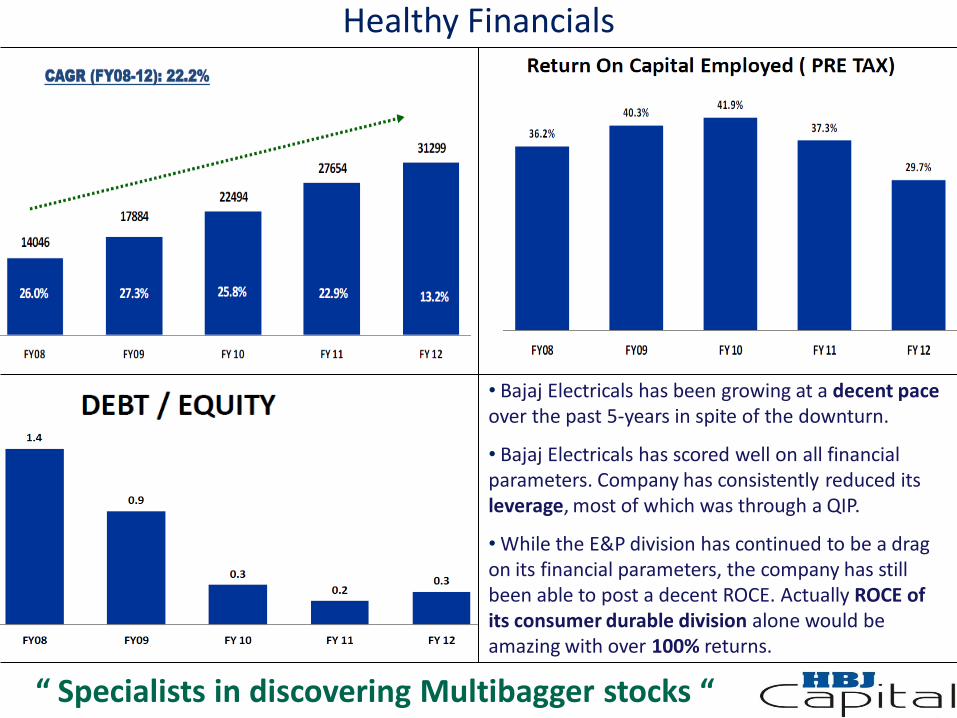

Healthy Financials

“ Specialists in discovering Multibagger stocks “

• Bajaj Electricals has been growing at a decent pace over the past 5-years in spite of the downturn.

• Bajaj Electricals has scored well on all financial parameters. Company has consistently reduced its leverage, most of which was through a QIP.

• While the E&P division has continued to be a drag on its financial parameters, the company has still been able to post a decent ROCE. Actually ROCE of its consumer durable division alone would be amazing with over 100% returns.

Investment Rationale

“ Specialists in discovering Multibagger stocks “

Profitable Growth Opportunity

“ Specialists in discovering Multibagger stocks “

Bajaj Electricals with strong competitive advantages over its peers in the Consumer Durables division is well positioned to capitalize on the secular trend of Middle-Class consumer boom over the next many years. Bajaj Electricals has several operational levers to grow profitably at a healthy pace. We think a mix of several initiatives will help Bajaj Electricals (Consumer Durables & Lighting) divisions to grow at 20% consistently.

Incremental Sales :-

* Continued Thrust on Network Expansion will generate 5% Incremental Sales. * Focus on New Products and New Price Points will generate 5% Incremental Sales. * Focus on Rural Markets with strong Product positioning will generate 3% Incremental Sales. * Placing Products aggressively in Modern Format Retail will generate 3% Incremental Sales.

Fast Growth :-

* Bajaj Electricals Management has indicated that they can use 1000 Cr for Acquisitions of Niche Brands.

* Company has established Leadership in new product categories like Induction Stoves, Toasters, Grills etc which have little penetration in India and Potential Growth is very high.

* Bajaj with expanding Service centers will continue to consolidate its position amongst the traditional Value Conscious Indian consumer who uses Products for a much longer time frame than in other countries.

Maintaining Margins :-

* Bajaj Electricals can also continue to maintain its margins through a lot of Value Engineering Initiatives from its R&D centers which will help save costs, especially during inflationary commodity prices.

* Bajaj also has been able to obtain good Market Share in the Premium Segment with its, “Bajaj Platini” and “Morphy Richards” brands. These products have Higher margins and better Product Mix will also help it to improve its overall EBIT Margins.

Short Term Uncertainty

“ Specialists in discovering Multibagger stocks “

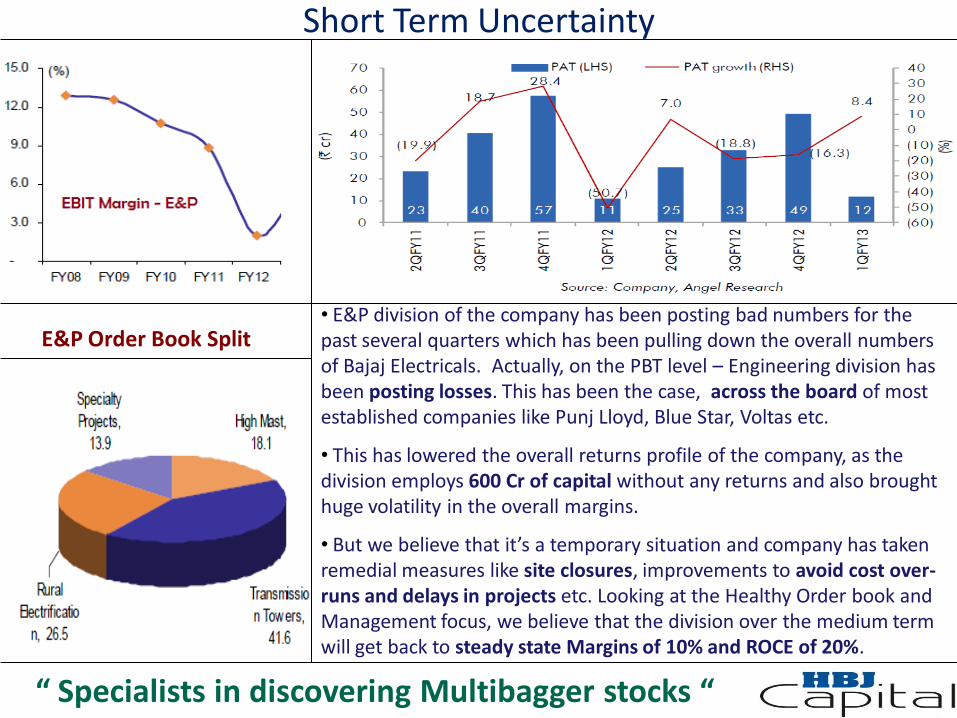

• E&P division of the company has been posting bad numbers for the past several quarters which has been pulling down the overall numbers of Bajaj Electricals. Actually, on the PBT level – Engineering division has been posting losses. This has been the case, across the board of most established companies like Punj Lloyd, Blue Star, Voltas etc.

• This has lowered the overall returns profile of the company, as the division employs 600 Cr of capital without any returns and also brought huge volatility in the overall margins.

• But we believe that it’s a temporary situation and company has taken remedial measures like site closures, improvements to avoid cost over-runs and delays in projects etc. Looking at the Healthy Order book and Management focus, we believe that the division over the medium term will get back to steady state Margins of 10% and ROCE of 20%.

E&P Order Book Split

Management Team

“ Specialists in discovering Multibagger stocks “

• Bajaj Electricals has also implemented a program called, “Theory of Constraints” which is expected to streamline its Supply chain further and help in reducing the Working Capital costs. It will also make sure that the Inventory is managed better which was an issue last year when the Inventory of Consumer Durables division (Esp: Fans) shot up very sharply.

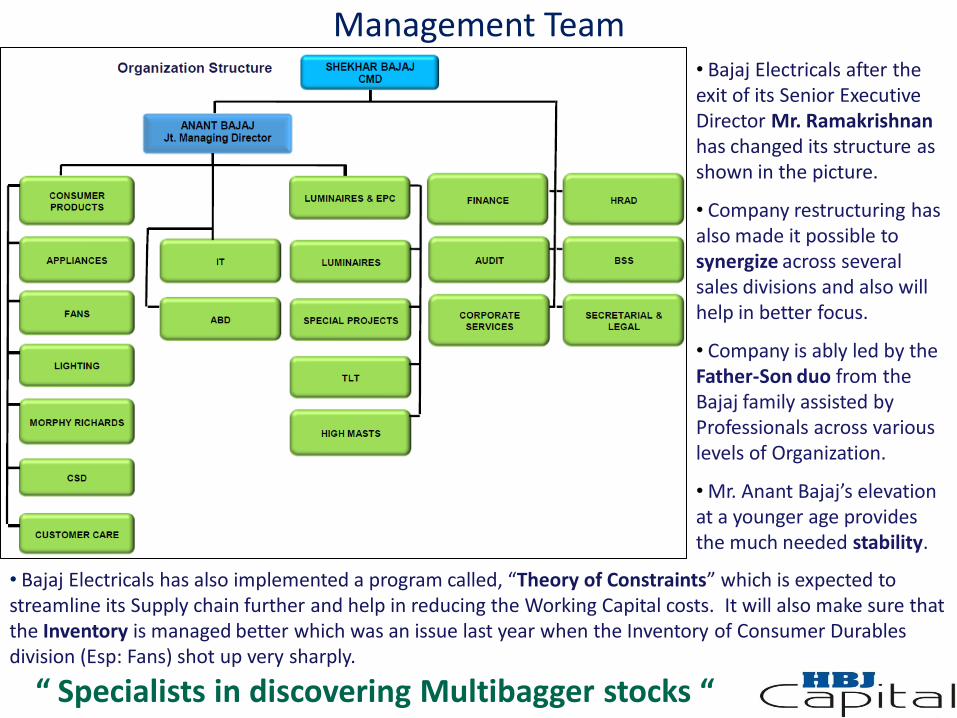

• Bajaj Electricals after the exit of its Senior Executive Director Mr. Ramakrishnan has changed its structure as shown in the picture.

• Company restructuring has also made it possible to synergize across several sales divisions and also will help in better focus.

• Company is ably led by the Father-Son duo from the Bajaj family assisted by Professionals across various levels of Organization.

• Mr. Anant Bajaj’s elevation at a younger age provides the much needed stability.

10 Years – Consistent Growth & Value Creation

“ Specialists in discovering Multibagger stocks “

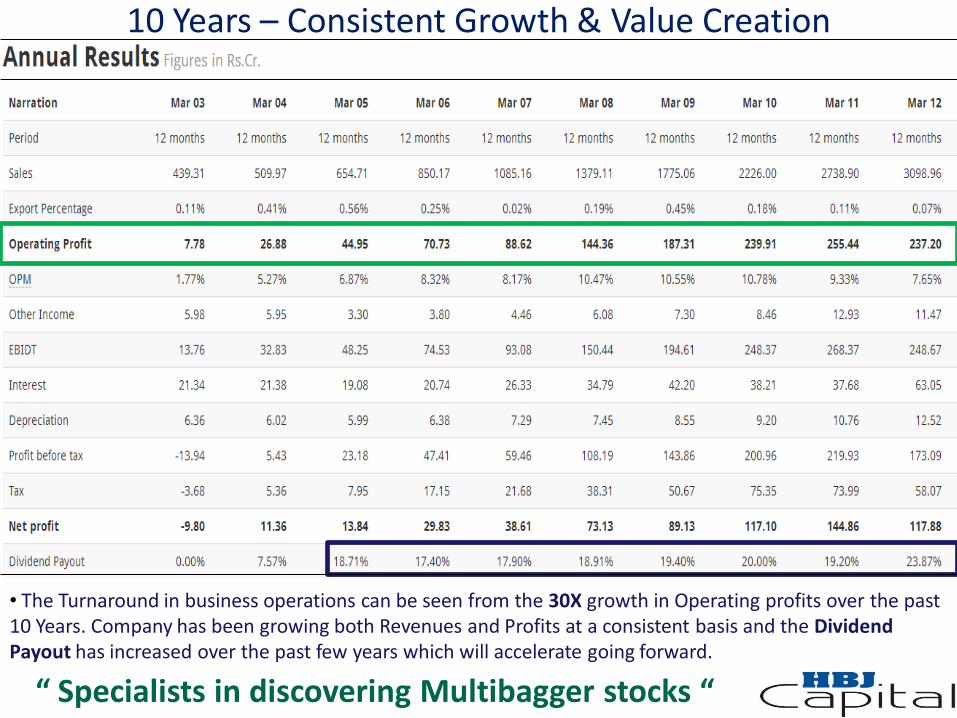

• The Turnaround in business operations can be seen from the 30X growth in Operating profits over the past 10 Years. Company has been growing both Revenues and Profits at a consistent basis and the Dividend Payout has increased over the past few years which will accelerate going forward.

High Return Businesses

“ Specialists in discovering Multibagger stocks “

Segment wise Capital Employed

Segment wise PBT Segment wise Revenues

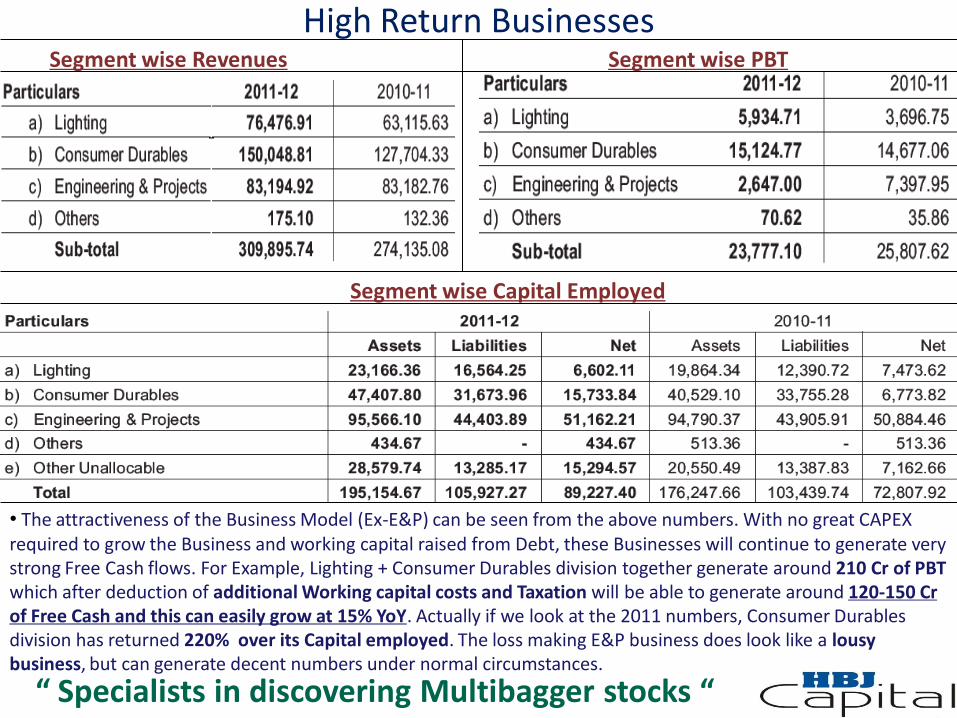

• The attractiveness of the Business Model (Ex-E&P) can be seen from the above numbers. With no great CAPEX required to grow the Business and working capital raised from Debt, these Businesses will continue to generate very strong Free Cash flows. For Example, Lighting + Consumer Durables division together generate around 210 Cr of PBT which after deduction of additional Working capital costs and Taxation will be able to generate around 120-150 Cr of Free Cash and this can easily grow at 15% YoY. Actually if we look at the 2011 numbers, Consumer Durables division has returned 220% over its Capital employed. The loss making E&P business does look like a lousy business, but can generate decent numbers under normal circumstances.

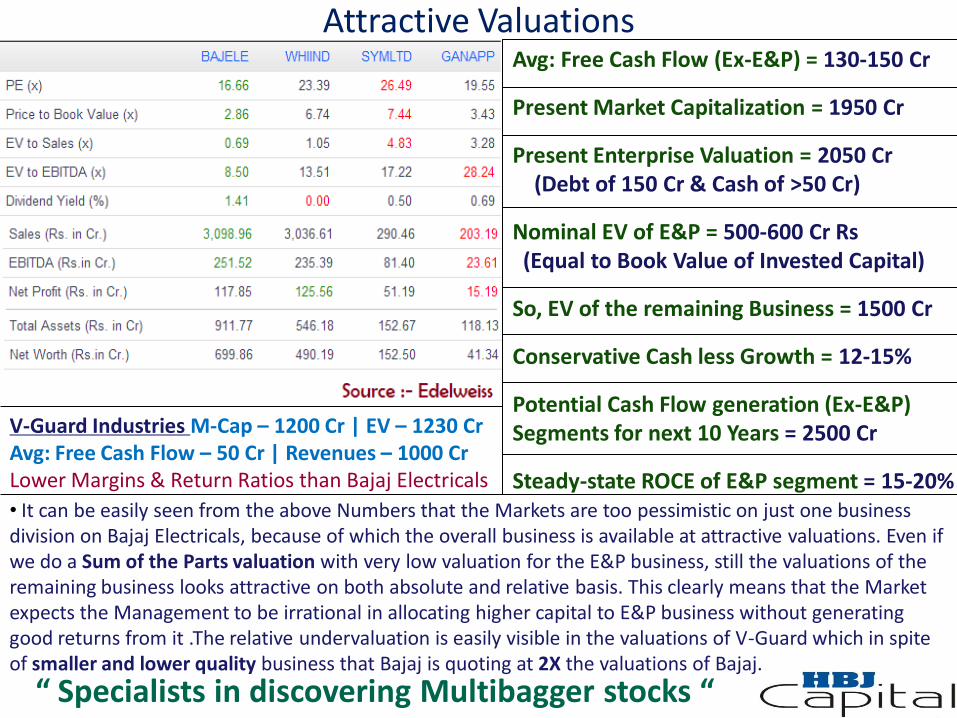

Attractive Valuations

“ Specialists in discovering Multibagger stocks “

• It can be easily seen from the above Numbers that the Markets are too pessimistic on just one business division on Bajaj Electricals, because of which the overall business is available at attractive valuations. Even if we do a Sum of the Parts valuation with very low valuation for the E&P business, still the valuations of the remaining business looks attractive on both absolute and relative basis. This clearly means that the Market expects the Management to be irrational in allocating higher capital to E&P business without generating good returns from it .The relative undervaluation is easily visible in the valuations of V-Guard which in spite of smaller and lower quality business that Bajaj is quoting at 2X the valuations of Bajaj.

Avg: Free Cash Flow (Ex-E&P) = 130-150 Cr

Present Market Capitalization = 1950 Cr

Present Enterprise Valuation = 2050 Cr (Debt of 150 Cr & Cash of >50 Cr)

Nominal EV of E&P = 500-600 Cr Rs (Equal to Book Value of Invested Capital)

So, EV of the remaining Business = 1500 Cr

Conservative Cash less Growth = 12-15%

Potential Cash Flow generation (Ex-E&P) Segments for next 10 Years = 2500 Cr

Steady-state ROCE of E&P segment = 15-20%

V-Guard Industries M-Cap – 1200 Cr | EV – 1230 Cr Avg: Free Cash Flow – 50 Cr | Revenues – 1000 Cr Lower Margins & Return Ratios than Bajaj Electricals

Financials

“ Specialists in discovering Multibagger stocks “

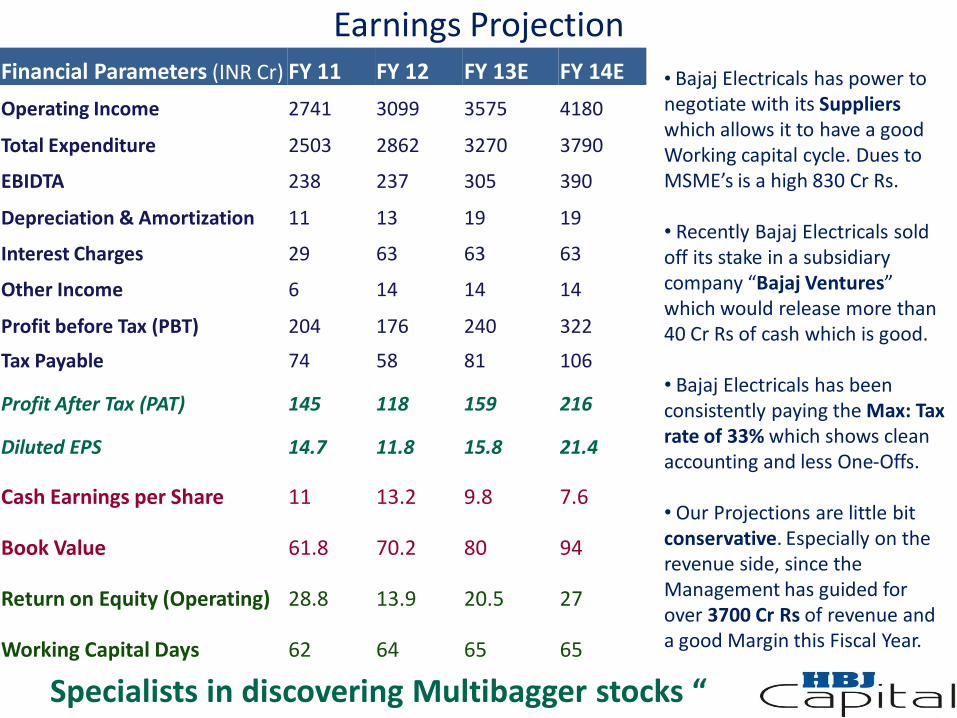

Earnings Projection Financial Parameters (INR Cr) FY 11 FY 12 FY 13E FY 14E

Operating Income 2741 3099 3575 4180

Total Expenditure 2503 2862 3270 3790

EBIDTA 238 237 305 390

Depreciation & Amortization 11 13 19 19

Interest Charges 29 63 63 63

Other Income 6 14 14 14

Profit before Tax (PBT) 204 176 240 322

Tax Payable 74 58 81 106

Profit After Tax (PAT) 145 118 159 216

Diluted EPS 14.7 11.8 15.8 21.4

Cash Earnings per Share 11 13.2 9.8 7.6

Book Value 61.8 70.2 80 94

Return on Equity (Operating) 28.8 13.9 20.5 27

Working Capital Days 62 64 65 65

• Bajaj Electricals has power to negotiate with its Suppliers which allows it to have a good Working capital cycle. Dues to MSME’s is a high 830 Cr Rs. • Recently Bajaj Electricals sold off its stake in a subsidiary company “Bajaj Ventures” which would release more than 40 Cr Rs of cash which is good. • Bajaj Electricals has been consistently paying the Max: Tax rate of 33% which shows clean accounting and less One-Offs. • Our Projections are little bit conservative. Especially on the revenue side, since the Management has guided for over 3700 Cr Rs of revenue and a good Margin this Fiscal Year.

Specialists in discovering Multibagger stocks “

Concerns & Reasoning

“ Specialists in discovering Multibagger stocks “

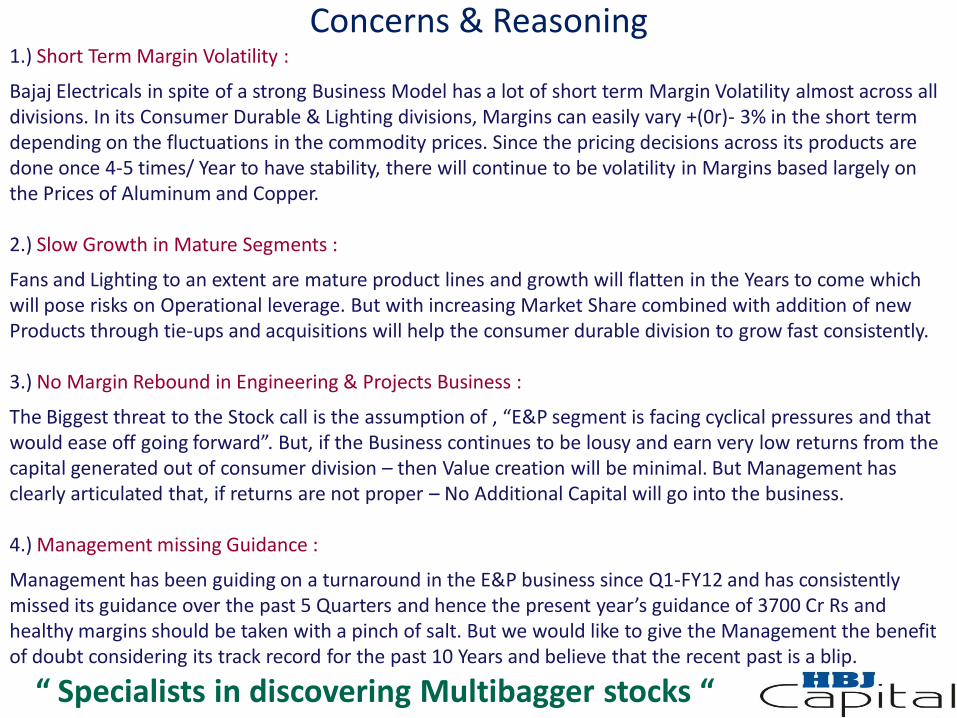

1.) Short Term Margin Volatility :

Bajaj Electricals in spite of a strong Business Model has a lot of short term Margin Volatility almost across all divisions. In its Consumer Durable & Lighting divisions, Margins can easily vary +(0r)- 3% in the short term depending on the fluctuations in the commodity prices. Since the pricing decisions across its products are done once 4-5 times/ Year to have stability, there will continue to be volatility in Margins based largely on the Prices of Aluminum and Copper. 2.) Slow Growth in Mature Segments :

Fans and Lighting to an extent are mature product lines and growth will flatten in the Years to come which will pose risks on Operational leverage. But with increasing Market Share combined with addition of new Products through tie-ups and acquisitions will help the consumer durable division to grow fast consistently. 3.) No Margin Rebound in Engineering & Projects Business :

The Biggest threat to the Stock call is the assumption of , “E&P segment is facing cyclical pressures and that would ease off going forward”. But, if the Business continues to be lousy and earn very low returns from the capital generated out of consumer division – then Value creation will be minimal. But Management has clearly articulated that, if returns are not proper – No Additional Capital will go into the business. 4.) Management missing Guidance :

Management has been guiding on a turnaround in the E&P business since Q1-FY12 and has consistently missed its guidance over the past 5 Quarters and hence the present year’s guidance of 3700 Cr Rs and healthy margins should be taken with a pinch of salt. But we would like to give the Management the benefit of doubt considering its track record for the past 10 Years and believe that the recent past is a blip.

Conclusion

“ Specialists in discovering Multibagger stocks “

Price Chart

• Bajaj Electricals stock has been in a correction phase since the start of 2010. There has been a substantial Value erosion over the past 2 years.

• If we look at a longer time frame, Stock has delivered phenomenal returns over the past decade. Stock is actually up by about 100X since its 2003 lows.

• Promoters have a substantial shareholding and have in fact bought additional shares over the past 2 Quarters, while the Institutional Investors have been reducing their exposure which gives us a good opportunity to accumulate the shares at attractive prices.

“ Specialists in discovering Multibagger stocks “

Share Holding %

June 2012

Mar 2012

Dec 2011

Sept 2011

Promoters 66.16 65.98 65.60 65.61

FII 9.40 5.47 6.86 6.49

DII 7.20 10.06 9.44 10.10

Decent Correction in Share Price

Conclusion As Investment Legend Warren Buffet used to say, “Great business is one which can grow without Huge Capital requirements”. Actually one of his best Investment bets was – Sees Candy which helped in earn huge amounts of Free Cash every year and when so much of cash was available with the best Capital Allocator, the kind of value creation which happened with that One Investment decision is just enormous. While Bajaj Electricals management may not be such a wonderful Capital Allocator, but the company surely has a business which can throw up Huge Free cash flow consistently YoY along with a decent growth.

We believe over the Medium to Long term, Bajaj’s Consumer Durables and Lighting division will continue to generate cash which would be used by the E&P division to grow at a healthy pace. We also continue to think that the E&P division can have a decent returns profile of 15-20% in normal conditions. This will generate good Share-Holder value for all Investors. We also believe Market is too much pessimistic on E&P division and continues to believe that it will suck in a lot of cash in the future with little returns.

Even after considering a valuation of less than Book for its E&P business, we can easily see that the Valuations are highly attractive. Actually our Reverse DCF Calculations on its Consumer Durables and Lighting business shows us that the Market is considering a No-Growth scenario for these business which shows the amount of pessimism in the current stock price. Considering the Business Quality, Returns Profile and Improvements expected, we think that the stock is a Value buy at the current levels.

Bajaj Electricals will surely qualify as an Alpha stock where the Risk adjusted Returns are very high. We look at buying the stock as, “Investing in a Fundamentally sound company which is available at reasonable valuations, due to Short term Uncertainty”. We believe a few positive surprises will help the stock to get the sentiment back making it eligible for a Valuations Re-rating. As we have said, this stock over the longer term definitely can give Multibagger returns, considering an unique combination of “Large Opportunity + Good Growth + Margin Expansion + Strong Return Ratios + Potential P/E Re-rating.

“ Specialists in discovering Multibagger stocks “

THANK YOU

“ Specialists in discovering Multibagger stocks “

Related Documents