MINISTRY OF EDUCATION AND SCIENCE OF THE REPUBLIC OF KAZAKHSTAN KAZAKH-BRITISH TECHNICAL UNIVERSITY FINANCE & ECONOMICS FACULTY Department of Finance and Accounting APPROVED BY Dean of Finance &Economics Faculty, Doctor in Economics, Associate Professor _____________ G.T. Abdrakhmanova BACHELOR’S DIPLOMA THESIS Thesis title: «Global financial crisis and its influence on Kazakhstan» Major: 5B050900 «Finance» Developed by A.K.Pstebayeva Bachelor Thesis Supervisor (MSc, Senior Lecturer of Finance & Accounting Department) A.N.Mamyrbayev Chair of «Finance and Accounting Department», Doctor in Economics, Associate Professor G.T. Abdrakhmanova Аlmaty 2012

Bachelors Diploma Thesis

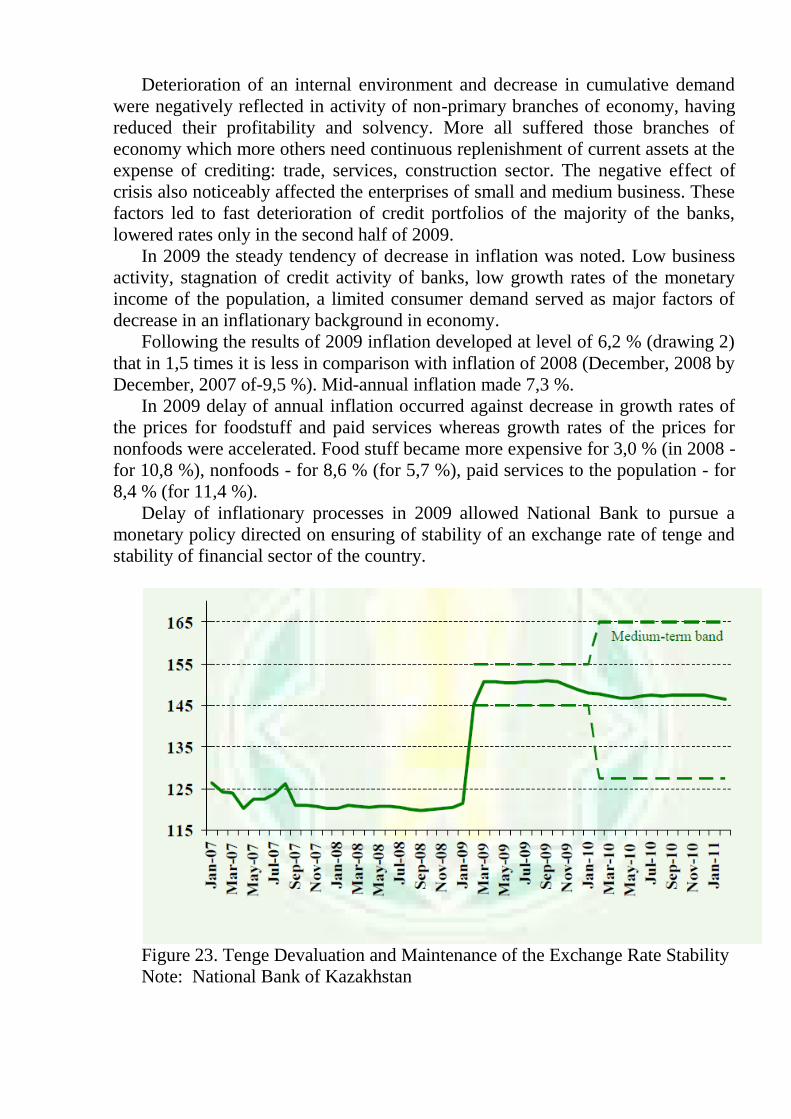

Oct 24, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

MINISTRY OF EDUCATION AND SCIENCE

OF THE REPUBLIC OF KAZAKHSTAN

KAZAKH-BRITISH TECHNICAL UNIVERSITY

FINANCE & ECONOMICS FACULTY

Department of Finance and Accounting

APPROVED BY

Dean of Finance &Economics Faculty,

Doctor in Economics, Associate Professor

_____________ G.T. Abdrakhmanova

BACHELOR’S DIPLOMA THESIS

Thesis title: «Global financial crisis and its influence on

Kazakhstan»

Major: 5B050900 «Finance»

Developed by A.K.Pstebayeva

Bachelor Thesis Supervisor

(MSc, Senior Lecturer of

Finance & Accounting Department) A.N.Mamyrbayev

Chair of «Finance and Accounting Department»,

Doctor in Economics, Associate Professor G.T. Abdrakhmanova

Аlmaty 2012

TABLE OF CONTENT

INTRODUCTION………………………………………………………………...3

PART I GLOBAL FINANCIAL CRISIS AND ITS PECULARITIES

1.1 Theoretical framework for the analysis of global financial crisis:

Defining and identifying financial crisis…………………………………....5

1.2 The world financial crisis during 2007-2012: causes and consequences…..11

PART II FINANCIAL CRISIS IN KAZAKHSTAN

2.1 Influence of global financial crisis on Kazakh economy…………………...21

2.2 Anti-crisis measures conducted by National Bank of Kazakhstan during the

crisis………………………………………………………………………....35

PART III CRISIS MANAGEMENT AS A NEW MANAGEMENT PARADIG

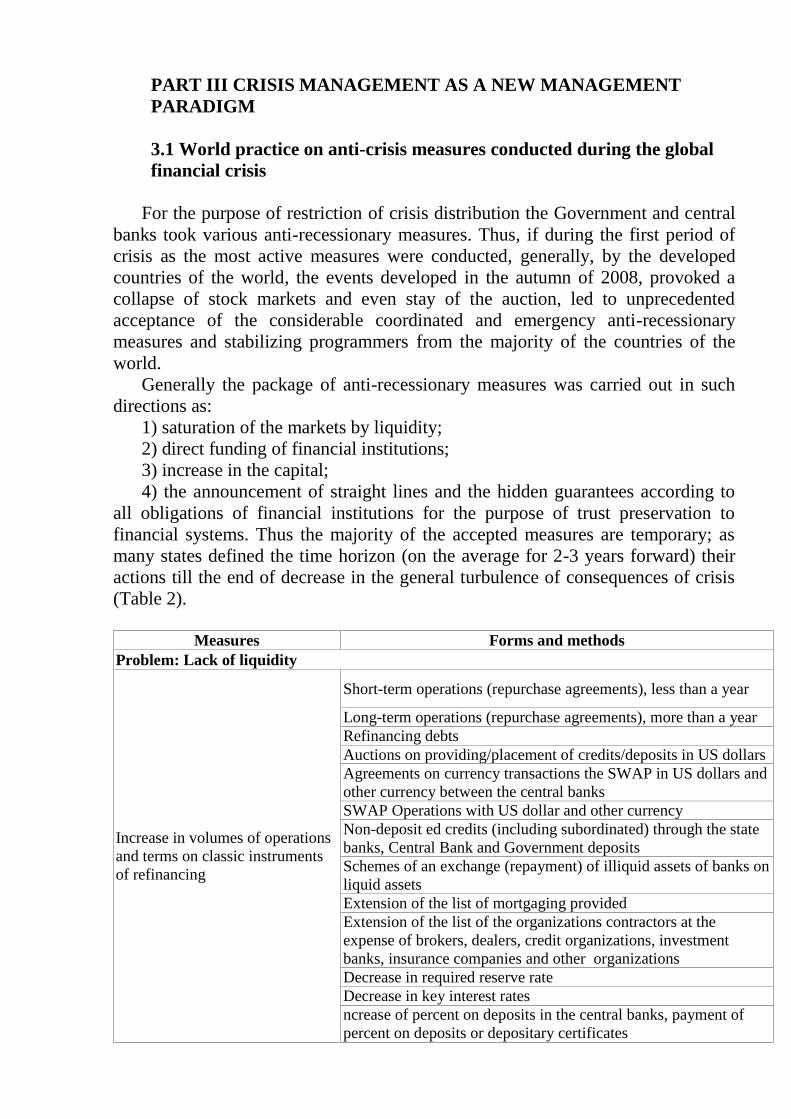

3.1 World practice on anti-crisis measures conducted during the global financial

crisis……………………………………………………………………………….49

3.2 Ways of improvement of anti-crisis packages conducted by central banks…..54

CONCLUSION………………………………………………………………………………......62

BIBLIOGRAPHY………………………………………………………………………………..64

APPENDICES

INTRODUCTION

Global Financial Crisis of 2007-2012 has been the worst since the Great

Depression in the 1930s. The financial crisis has had a profound effect, much more

than that anticipated by many. The national borders have been breached and the

ramifications are still being felt far from the epicenter. Although the global

economy is recovering, the confidence in the markets is still weak as market

participants are looking for a direction which is by no means straight forward.

The financial crisis was the event which was not supposed to happen, but it did.

Few economists thought that the U.S. economy would ever experience a systemic

financial crisis again or that it would turn into a global crisis. But, the crisis, which

began in August of 2007, developed into the worst crisis. It has been

unprecedented in its depth and scope. The recession in the United States spread

around the world. It appeared for a time that a new Great Depression was going to

occur, but central banks engaged in extraordinary efforts to stabilize the economy.

As is the common perception, government regulations follow the crisis. Regulatory

bodies analyze the events specific to the crisis and try to bring down formal

regulations which would avoid a similar crisis in the future. After witnessing

trillions of dollars of losses, high unemployment rates and company bankruptcies,

national governments are pressurized and are expected to take immediate and

concrete actions that restore the market confidence. But often, regulatory bodies

come out with regulations which are not the optimal solution. These regulations

can be more than required or sometimes, under political pressure emphasize on

matters that are not the actual causes of the debacle.

The aim of this Bachelor Thesis is to understand the financial crisis, its causes

and the regulatory policies that have come up to avoid a next financial crisis in

Kazakhstan. There has been lot of discussion on the miscreants that spawned the

crisis. This thesis tries to understand the new regulations that have come up in the

world. Also, it tries to identify the similarities and differences in the approaches of

regulatory bodies in different regions. During the research following tasks were

defined:

Developing an understanding of the world financial crisis (understanding the

views of different authors);

Identifying main factors behind the crisis;

Analyzing the impact of financial crisis on world economy, in particular,

Kazakh economy;

Understanding the regulatory changes during the world financial crisis;

Comparison and analysis of regulatory changes;

Providing views on the effectiveness of regulations in improving the current

situation.

This work uses a lot of information available from various books on financial

crisis, conferences and panel discussions, blogs and newspaper articles, statistical

data, websites of central banks and various regulatory bodies.

The Thesis is structured as follows:

Part I provides a theoretical framework for the analysis of world financial crisis

and describes origins of the contemporary financial crisis, disputes reasons and

tries to find out explanations of some questions, such as causality of the crisis, role

and regulation of the systemic risk, etc.

Part II is devoted to the analysis of negative effects on Kazakh economy

including national economy, industrial sector and banking system. The chapter

contains also description of the most important regulatory changes in Kazakhstan.

Part III concludes the Thesis with some after-crisis-to-do and proposals.

PART I GLOBAL FINANCIAL CRISIS AND ITS PECULARITIES

1.1 Theoretical framework for the analysis of global financial crisis:

Defining and identifying financial crisis

The crises in the world economy are supposed to be logical, inevitable, and

periodic. By the way the most are almost always unexpected, in spite of the

warning signs and prevention of persistent analysts and economists. That is what

happened with the current global financial and economic crisis.

When selecting a particular object of study, the authors try to reveal the

traditional notion of a phenomenon on the basis of its internal contents. According

to the glossary crisis − a sharp abrupt fracture, dislocation of the economic life,

which leads to a reduction in the production of goods, increased unemployment,

deterioration of the situation of workers. In a large economic dictionary noted that

"the financial crisis − the deep frustration of the state financial system, followed by

inflation, the volatility of the securities exchange, manifested in the sharp disparity

of income to the expenditure budget, instability and collapse of the exchange rate

of the national currency, mutual non-payments of economic entities, currency

mismatch in circulation requirements of the law of money circulation ".

Philosophical Dictionary interprets "financial crisis" as "the emergence of

conflicts and their resolution, and at the same time, the emergence of new

contradictions", it should be noted that every crisis is a necessary aspect and stage

of development, when the contradictions of the system deteriorated sharply to the

brink of collapse, which allows to detect and in their awareness of their historical

subjects of action, this collapse, and clears the way for updating or eliminating

system for the jump, achieving a new quality system or the transition to a

qualitatively new system, thus accelerating the movement of history, the pace of

historical development. Referred to the financial crisis is quite a variety of

situations in which some financial companies or assets (for example, shares or

bonds) dramatically lose a substantial part of its value. It is clear that the financial

crisis first hit the financial sector. However, due to the fact that the real sector is

closely related to finance, in the end such crises are reflected in all sectors of the

economy and lead to a decline in production, increased unemployment, lower

living standards, etc.

More common definition on financial crisis used in literature is a situation in

which the value of financial institutions or assets drops rapidly. A financial crisis is

often associated with a panic or a run on the banks, in which investors sell off

assets or withdraw money from savings accounts with the expectation that the

value of those assets will drop if they remain at a financial institution. A financial

crisis can come as a result of institutions or assets being overvalued, and can be

exacerbated by investor behavior. A rapid string of sell offs can further result in

lower asset prices or more savings withdrawals. If left unchecked, the crisis can

cause the economy to go into a recession or depression.

According to definition proposed by Frederic S. Mishkin, “A financial crisis is

a disruption to financial markets in which adverse selection and moral hazard

problems become much worse, so that financial markets are unable to efficiently

channel funds to those who have the most productive investment opportunities. A

financial crisis thus results in the inability of financial markets to function

efficiently, which leads to a sharp contraction in economic activity”.

By the way, up until recently, views of financial crises in the literature have

split into two polar camps, those associated with monetarists versus a more eclectic

view put forward by Charles Kindleberger and Hyman Minsky. Monetarists

beginning with Friedman and Schwartz (1963) have linked financial crises with

banking panics. They stress the importance of banking panics because they view

them as a major source of contractions in the money supply which, in turn, have

lead to severe contractions in aggregate economic activity in the United States.

Monetarists do not view as real financial crises events in which, despite a sharp

decline in asset prices and a rise in business failures, there is no potential for a

banking panic and a resulting sharp decline in the money supply. Indeed, Schwartz

(1986) characterizes these situations as "pseudo financial crises". Government

intervention in a pseudo-financial crisis is unnecessary and can indeed be harmful

since it leads to a decrease in economic efficiency because firms that deserve to

fail are bailed out or because it results in excessive money growth that stimulates

inflation.

An opposite view of financial crises is outlined by Kindleberger (1978) and

Minsky (1972) who have a much broader definition of what constitutes a real

financial crisis than monetarists. In their view, financial crises either involve sharp

declines in asset prices, failures of large financial and nonfinancial firms,

deflations or disinflations, disruptions in foreign exchange markets, or some

combination of all of these. Since they perceive any of these disturbances as

having potential serious consequences for the aggregate economy, they advocate a

much expanded role for government intervention when a financial crisis, broadly

defined, occurs. One problem with the Kindleberger-Minsky view of financial

crises is that it does not supply a rigorous theory of what characterizes a financial

crisis, and it thus lends itself to being used too broadly as a justification for

government interventions that might not be beneficial for the economy. Indeed,

this is the basis of Schwartz's (1986) attack on the Kindleberger-Minsky view. On

the other hand, the monetarist view of financial crises is extremely narrow because

it only focuses on bank panics and their affect on the money supply.

The President of the European Central Bank− Mr. Jean Claude Trichet opines

that “financial crises share some commonalities. In particular, crises are associated

with the emergence of euphoria and complacency in financial markets, typically

supported by rapid credit growth and a growing belief that new concepts like

financial innovation or technological advances have rendered old limits on

economic performance obsolete”.

At the same time Trichet acknowledges the fact that each crisis is also unique.

Every crisis has its own characteristics, which make it different from the previous

ones. In order to avoid the next crisis it is essential to understand the causes and

mechanisms behind the current crisis. Every crisis takes its own course in the

financial system and affects specific sectors more than others.

Crisis, being the moment of dialectic development represents process, and as

that, passes some stages of development, namely:

- Stage of formation of crisis;

- Stage of development of crisis till a full maturity;

- Stage of a full maturity of crisis;

- Stage of permission of crisis.

For emergence of crisis the special aggravation of contradictions - not initial,

initial for this system, and not maximum is necessary. Definition of degree of this

aggravation is connected with the concept a measure of relative independence of

the parties of a contradiction, that is that limit of an aggravation of contradictions

behind which crisis begins.

This degree of an aggravation of contradictions is reached at a stage of

formation of crisis. This stage covers the period from emergence of the first

sporadic crisis moments in development of the phenomenon, process and system to

such level of an aggravation of contradictions when there is a possibility of a

quantum leap in the presence of especially favorable circumstances, conditions. In

dialectics necessary and casual accident even more strongly than need, however,

the new reality is already possible, and, means, crisis became, is the fact and a

development.

At the second stage they become crisis develops before complete maturing,

there is a process of further isolation of contrasts, aggravations of dialectic

contradictions, need declares everything itself more persistently, generating more

and more the corresponding accidents, transformation of possibility into reality

becomes more and more necessary.

The third stage - a stage of a full maturity of crisis. The unity of finally stood

apart parties of a contradiction is supported violently, the antagonism reached

extreme development, the old qualitative condition practically reached the top

border of the quantitative measure (the internal limit of system is almost reached),

transition to new quality is objectively possible at any time in the presence of a

maturity of a subjective factor, transformation of possibility of a quantum leap into

reality became crucial need of development.

The fourth stage - a stage of permission of crisis or the negative destructive

side of the crisis. In crisis as its last stage, enters not jump as a whole which

includes not only destruction old, but also creation new but only the negative

destructive part of jump.

It is often said that those who do not remember the past are doomed to repeat

it. With economics it's no different, considering the world has experienced dozens

of crashes and recessions, undoubtedly caused by acquisitive traders and

lawmakers with few memories of the past. So its important review past

crashes−hopefully new management won't repeat them. But during the assessment

of views of crises and their reasons it is necessary to note that they changed in time

together with change of the most social and economic reality. Taking into account

it the point of view of a number of the Russian economists who allocate three

stages in change of views of recurrence in the crisis phenomena is worthy.

The first stage covers the period since the beginning of the XVIII century to the

middle of the 30th of the XX century when judgments prevailed that economic

crises or in general are impossible under capitalism (J. S.Mill, D. Ricardo), or they

carry, only casual character and system of free competition is capable to overcome

independently them (Sismondi, R. Rodbertus, K.Kautsky).

The second stage covers the period from the middle of the 30th to the middle

of the 60th of the XX century. Allocation of this period is connected with Keynes

and first of all with his conclusion that economic crises (the depression is more

exact, stagnation) are inevitable in the conditions of classical capitalism and follow

from the nature of the market inherent in it. Keynes among the western economists

directly declared to one of the first that the capitalist market includes various

manifestations of monopolist and why the price and a salary are nonflexible. As

essentially necessary means of smoothing of problems of crisis and unemployment

Keynes put forward idea of ensuring the state intervention in economy with a view

of stimulation of effective cumulative demand. In research of a factor of recurrence

it is necessary to carry to his merits also the theory of the animator developed by it

which in the subsequent began to be used widely in the analysis of the reasons of

recurrence.

The third stage in research of the reasons of crises is the period from the

middle of the 60th so far. During this period, first, it began to be given particular

attention to differentiation of the internal and external reasons of recurrence of

market economy, and to internal factors it began to be paid primary attention.

Secondly, the position of a number of experts according to which the state in

the developed countries not always aspires to anti-recessionary regulation, to

smoothing of cyclic fluctuations and to stabilization of economic balance was

defined, and carries out quite often so-called about cyclic policy, i.e. provokes and

supports recurrence.

Researches of the nature of crisis in the conditions of state regulation of

economy generated a number of new views and concepts on this problem. Among

them: concepts of «an equilibrium business cycle» and «a political business cycle».

The first reflects development of ideas of monetarism. According to this

concept the state along with many functions inherent in it carries out a role of a

peculiar generator of monetary "shocks" which deduce economic system from an

equilibrium state and thus sustain cyclic fluctuations in public reproduction.

In 70 — the 80th this concept was actively developed by representatives of the

theory of rational expectations. If monetarists consider that the state can provoke a

cycle, using insufficient awareness of people on the true contents and the purposes

of the various directions of state economic policy, supporters of the theory of

rational expectations proceed in the matter from opposite reasons. They consider

that businessmen and the population learned to estimate and distinguish true

motives of decisions of state authorities thanks to occurring information revolution

and can react in due time every time to them in compliance with the benefit. As a

result of the purpose of a state policy remain unrealized, and recession or lifting

accepts more strongly pronounced character.

The second concept (“a political business cycle”) is based that dependence

between an unemployment rate and a rate of inflation is defined by Phillips Curve,

i.e. there is an inverse relationship between two variables: with the low rate of

unemployment, the prices rise rapidly. His supporters believe that the economic

situation within the country essentially influences popularity of ruling party. As the

main economic indicators to which the population reacts, rates of inflation and

standard of unemployment are allocated: than below their levels, other things being

equal more voices will be submitted by that on upcoming elections for ruling party

or the president.

The literature has used different criteria to identify crisis episodes, many of

which fit directly or indirectly in parts of the definition proposed above. A full and

uncontroversial identification is difficult, since it involves a counter-factual

exercise: what would have happened in each particular episode if the financial

sector had remained intact throughout? Instead, literature has identified episodes in

which there are signs of disruption in the financial system, in financial variables, in

macroeconomic variables or in some combination of these without a stronger

causal claim. For example, a direct sign of a large-scale disruption in financial

markets is the presence of widespread bank runs, bank failures or bank

insolvencies. While it is easy to determine whether there was a bank run or a bank

failure, insolvencies are much harder to spot. For this reason, the identification of

banking crises often relies on the assessments of specialists (Caprio and

Klingebiel, 1999; Laeven and Valencia 2008).

Another way to detect disruptions in financial markets is to look at the

behavior of financial flows and stocks. An important example of this strategy is

Calvo (1991), who looks for sudden stops in the inflow of foreign capital.

Mendoza and Terrones (2008) focus instead on credit booms, defined as large

departures of credit to the private sector from its long-term trend. As it turns out,

the peak of these booms oft en coincides with financial crises, especially when

they happen in less developed countries. A third approach is to look for loss in the

value of important classes of assets such as government debt (Reinhart and Rogoff,

2010), stocks and housing (Bordo and Jeanne, 2002). These are assets that

represent an important part of the balance sheet of households and firms, so that a

drop in their value may lead to an interruption in the flow of finance as lenders fear

for the value of the collateral that the borrowers have to offer.

Exchange rate crises can trigger or amplify a financial crisis if financial

institutions have liabilities in foreign currency (Diaz-Alejandro 1984; Calvo and

Talvi 2008). However, not all exchange rate crises turn into financial crisis. For

instance, while the collapse of the European Exchange Rate Mechanism in the

early 90’s was something policy makers at the time did not desire, in most cases

there was no spill over to the broader financial system. In this respect, Kaminsky

and Reinhart (2000) propose that it is useful to focus on episodes in which an

exchange rate and a banking crisis take place simultaneously.

The combination of criteria filters out episodes such as the ERM crisis as well

as episodes in which banking crises did not have any real effect. Lastly, Kehoe and

Prescott (2007) define episodes that they call “Great Depressions of the 20th

Century”. These are occasions in which a country has suffered a precipitous and

persistent output drop. Their definition lacks any reference to disruptions in the

financial sector but, as it turns out, there is a substantial degree of overlap with

financial crises identified in other studies. In spite of the different definitions, there

is a striking amount of agreement on the relevant events. Apart from the Great

Depression, most studies include observations from the Latin American sovereign

debt crisis in the early 80s, the Scandinavian collapse in the early 90s, Japan

throughout the 90s, the Asian crisis in the late 90s and Argentina in 1998-2001.

This coincidence strengthens the presumption that financial crisis represent a

reasonably well-defined economic problem, which is amenable to data collection

and systematic research.

Before discussing what happens during a crisis, it is important to understand

the period preceding a crisis. As the literature shows, this proves to be crucial in

designing and implementing the right set of policies. The identification of clear

antecedent patterns can provide a warning signal to policy makers and suggest

corrections to be taken in order to avoid the worse. While there are several factors

that led to the crisis, the most notable pattern is a period of “boom” in economic

and financial activity that gave rise to stock market and housing bubbles.

A stylized account of the “typical” boom can be reconstructed from the

findings of different papers in the literature. There are regulatory changes, which

allow banks to lend more freely and take more risk (Kaminsky and Reinhart, 2000;

Tornell and Westermann, 2002). What follows is an increase in the supply of credit

by banks, as they lend more relative to their assets and to their capital (Mendoza

and Terrones, 2008). To this increased supply of credit there is a matching increase

in the demand as firms increase their leverage and the government borrows more

heavily (Rogoff and Reinhart, 2010). At the aggregate level, these trends are

apparent in an increase in domestic credit (Mendoza and Terrones, 2008) and in

capital infl ows from abroad

(Rogoff and Reinhart, 2010). Prices of key assets react as house and equity

prices increase (Bordo and Jeanne, 2002; Rogoff and Reinhart 2010) and as the

exchange rate appreciates (Tornell and Westermann, 2002). All the while there is a

boom in economic activity, with an increase in output and investment. As the real

economy starts to lose steam, these trends revert abruptly, and the boom turns into

a crisis (Kaminsky and Reinhart, 2002; Mendoza and Terrones 2008). Two main

strands of the literature on crises attempt to account for the boom preceding the

bust. The first view states that the boom-bust cycle is evidence of excessive

investment and risk taking. In the second view, asset price boom increases liquidity

and facilitates investment. In particular, the boom in asset prices may stem from

self-fulfilling expectations about their value, rendering the boom fragile.

Examining both these strands of economic literature provides a more balanced

view of boom periods.

However, it should be noted that both strands of the literature point out that

booms eventually lead to busts. Despite the fact that there were many signals

reflecting the crisis, economists significantly underestimated the severity of the

downturns. Many economists, Nouriel Roubini among them, argue that some of

the optimism is built into the very machinery, the mathematics, of modern

economic theory. Econometric models typically rely on the assumption that the

near future is likely to be similar to the recent past, and thus it is rare that the

models anticipate breaks in the economy. And if the models can’t foresee a

relatively minor break like a recession, they have even more trouble modeling and

predicting a major rupture like a full-blown financial crisis. Only a handful of

20th-century economists have even bothered to study financial panics. (The most

notable example is probably the late economist Hyman Minksy, of whom Roubini

is an avid reader). As Roubini stated, today “we’re in uncharted territory where

standard economic theory isn’t helpful”.

Finally, literature review showed that economic science did not cause the

crisis. However, many of its theories did offer an intellectual background or some

sort of academic legitimacy to both policy and the markets, and, in the case of the

recent crisis, there was not only a failure of the dominant form of economic

thought but, above all (neoclassicist school, dominant until now, and Keynesian). It

should be noted that there is a problem of selective use of economic theories when

it comes to practical economics and that, in order to be useful, economics ought to

utilize knowledge from other disciplines and take more account of

interdependencies between political and social phenomena.

1.2 The world financial crisis during 2007-2012: causes and consequences

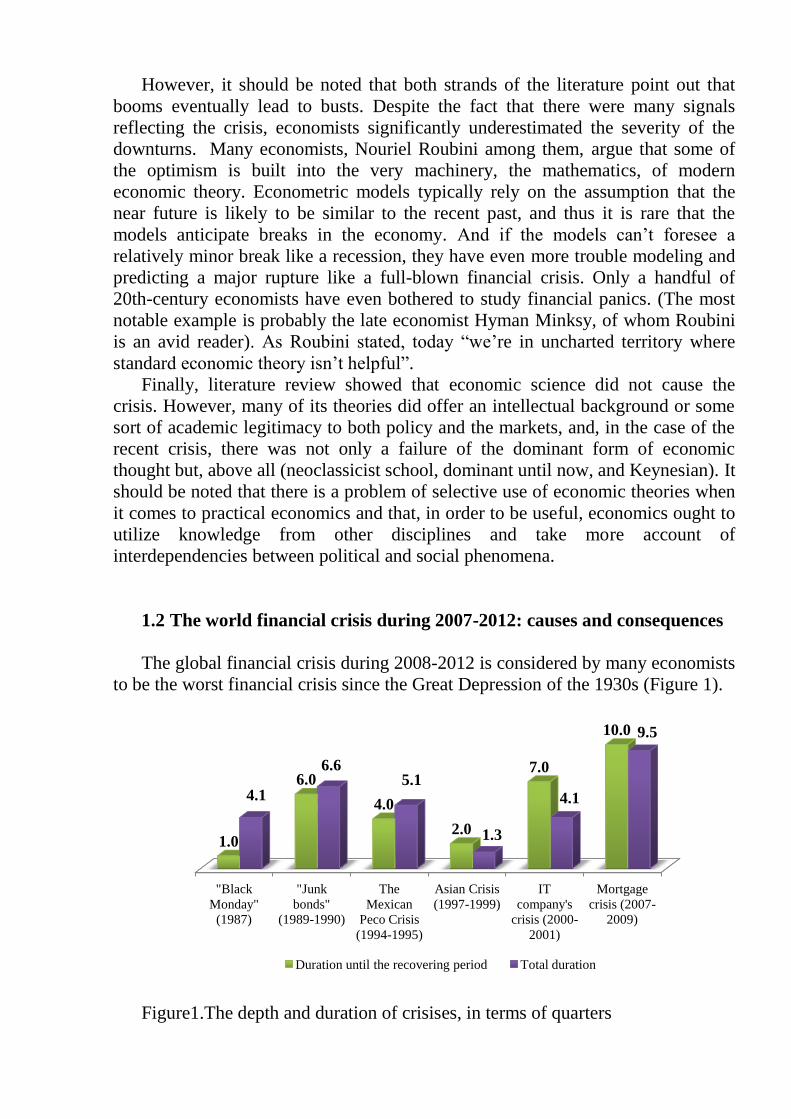

The global financial crisis during 2008-2012 is considered by many economists

to be the worst financial crisis since the Great Depression of the 1930s (Figure 1).

Figure1.The depth and duration of crisises, in terms of quarters

"Black

Monday"

(1987)

"Junk

bonds"

(1989-1990)

The

Mexican

Peco Crisis

(1994-1995)

Asian Crisis

(1997-1999)

IT

company's

crisis (2000-

2001)

Mortgage

crisis (2007-

2009)

1.0

6.0

4.0

2.0

7.0

10.0

4.1

6.6 5.1

1.3

4.1

9.5

Duration until the recovering period Total duration

Note: created by author based on The Global Europe Anticipation Bulletin

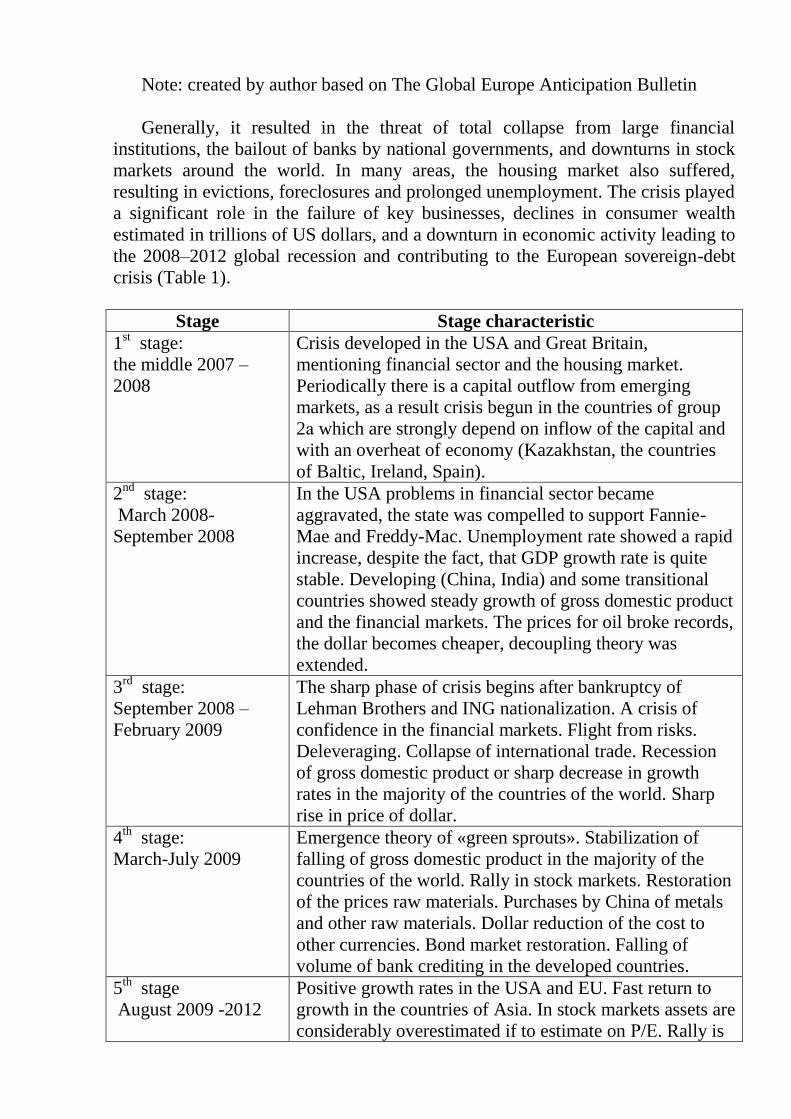

Generally, it resulted in the threat of total collapse from large financial

institutions, the bailout of banks by national governments, and downturns in stock

markets around the world. In many areas, the housing market also suffered,

resulting in evictions, foreclosures and prolonged unemployment. The crisis played

a significant role in the failure of key businesses, declines in consumer wealth

estimated in trillions of US dollars, and a downturn in economic activity leading to

the 2008–2012 global recession and contributing to the European sovereign-debt

crisis (Table 1).

Stage Stage characteristic

1st stage:

the middle 2007 –

2008

Crisis developed in the USA and Great Britain,

mentioning financial sector and the housing market.

Periodically there is a capital outflow from emerging

markets, as a result crisis begun in the countries of group

2а which are strongly depend on inflow of the capital and

with an overheat of economy (Kazakhstan, the countries

of Baltic, Ireland, Spain).

2nd

stage:

March 2008-

September 2008

In the USA problems in financial sector became

aggravated, the state was compelled to support Fannie-

Mae and Freddy-Mac. Unemployment rate showed a rapid

increase, despite the fact, that GDP growth rate is quite

stable. Developing (China, India) and some transitional

countries showed steady growth of gross domestic product

and the financial markets. The prices for oil broke records,

the dollar becomes cheaper, decoupling theory was

extended.

3rd

stage:

September 2008 –

February 2009

The sharp phase of crisis begins after bankruptcy of

Lehman Brothers and ING nationalization. A crisis of

confidence in the financial markets. Flight from risks.

Deleveraging. Collapse of international trade. Recession

of gross domestic product or sharp decrease in growth

rates in the majority of the countries of the world. Sharp

rise in price of dollar.

4th

stage:

March-July 2009

Emergence theory of «green sprouts». Stabilization of

falling of gross domestic product in the majority of the

countries of the world. Rally in stock markets. Restoration

of the prices raw materials. Purchases by China of metals

and other raw materials. Dollar reduction of the cost to

other currencies. Bond market restoration. Falling of

volume of bank crediting in the developed countries.

5th

stage

August 2009 -2012

Positive growth rates in the USA and EU. Fast return to

growth in the countries of Asia. In stock markets assets are

considerably overestimated if to estimate on Р/Е. Rally is

slowed down. The markets become unstable waiting for

sovereign or sub-sovereign defaults: restructuring of a

duty of Dubai-world, decrease in a rating of Greece and

etc. Some of the countries are compelled to turn off

support and to cut down the public expenses. The dollar

rises in price again, though isn't so strong, as year before

though isn't so strong, as year before. Greece gets a

€110bn (£93bn) bail-out from other countries using the

euro, and the International Monetary Fund. Euro

continues to fall and the public debt of other members of

EU starts to attract attention (Ireland). EU and IMF

agreed on 85 billion euro bail-out for the Irish Republic.

By the way Portugal recognizes that can’t cope with

problems and asks help from EU. Three countries mostly

affected by the crisis (Greece, Ireland and Portugal)

accumulated 6 percent of Eurozone GDP. However, Fitch

Ratings assumes that Greece finally declares a default.

The Swiss economy appeared on the verge of technical

recession. Low rate of probability that world economy will

recover in 2012-2013.

Table 1. Global financial crisis stages

Note: developed by the author based on BBC News, Bloomberg, The

Economist, Telegraph

To understand what happened in details it is important to be clear about what

has to be explained.

First, the subprime mortgage shock which triggered the crisis was not large.

The crisis was connected to subprime mortgages, a relatively new kind of

mortgage that was designed to make home ownership available to lower‐income

people, but which depended on house prices rising for its efficacy. (Gorton 2010).

When house prices stopped rising, there were expected losses on these mortgages,

many of which had been securitized. But, subprime was not large enough to

explain the crisis. At the time of the crisis there was about $1.2 trillion of subprime

mortgages outstanding, about 80 percent of which had been securitized. Even if

every single one of those mortgages defaulted with no recovery at all, it would not

explain the magnitude of the crisis. Furthermore, the losses on subprime mortgages

have not, in fact, been large. Park (2011) examines trustee reports on February

2010 for 88.6 percent of the notional amount of subprime bonds issued between

2004 and 2007. She calculates the realized principal losses on the $1.9 trillion of

originally AAA/Aaa‐rated subprime bonds issued between 2004 and 2007 to be 17

basis points as of February 2011. The same point is by the Financial Crisis Inquiry

Commission (FCIC) Report (2011: 228‐29) by looking at the ratings on

subprime mortgages.

The FCIC notes that: ”Overall, for 2005 to 2007 vintage tranches of

mortgage‐backed securities originally rated triple‐A, despite the mass downgrades,

only about 10% of Alt‐A and 4% of subprime securities had been ’materially

impaired’‐meaning that losses were imminent or had already been suffered‐by the

end of 2009.” So, if the shock was not large, how did we get a crisis?

Second, at the onset of the crisis all bond prices fell (spreads rose), not just

subprime‐related bonds. In particular, the prices of all manner of asset‐backed

securities fell. Why did the prices of, say, AAA/Aaa credit card asset‐backed

securities nose‐dive when this asset class has nothing to do with subprime

mortgages, and did not experience losses? Moreover, the prices of other securities

falling closely tracked measures of the deterioration of bank counterparty risk,

rather than track prices of subprime mortgages. Financial institutions’ counterparty

risk is usually measured by looking at LIBOR (the London Interbank Offered

Rate), the rate at which large financial institutions lend to each other, minus the

rate on the overnight index swap (OIS), which is taken as the riskless rate. So,

LIBOR minus OIS (LIB‐OIS) measures the risk premium in the interbank market.

Spreads on subprime did not follow this pattern, but rose continuously from

January 2007 (Gorton and Metrick 2012). The measure of interbank counterparty

risk and the spreads on non‐subprime bonds moved together, but they did not move

with subprime spreads.

Finally, any explanation of the financial crisis confronts another issue, namely,

the question of whether the crisis of 2007‐2009 was special, an unlucky

convergence of a number of unique factors. Or, was it at root fundamentally

similar to all the financial crises that have repeatedly occurred throughout the

history of market economies internationally? This question is especially important

for policy considerations.

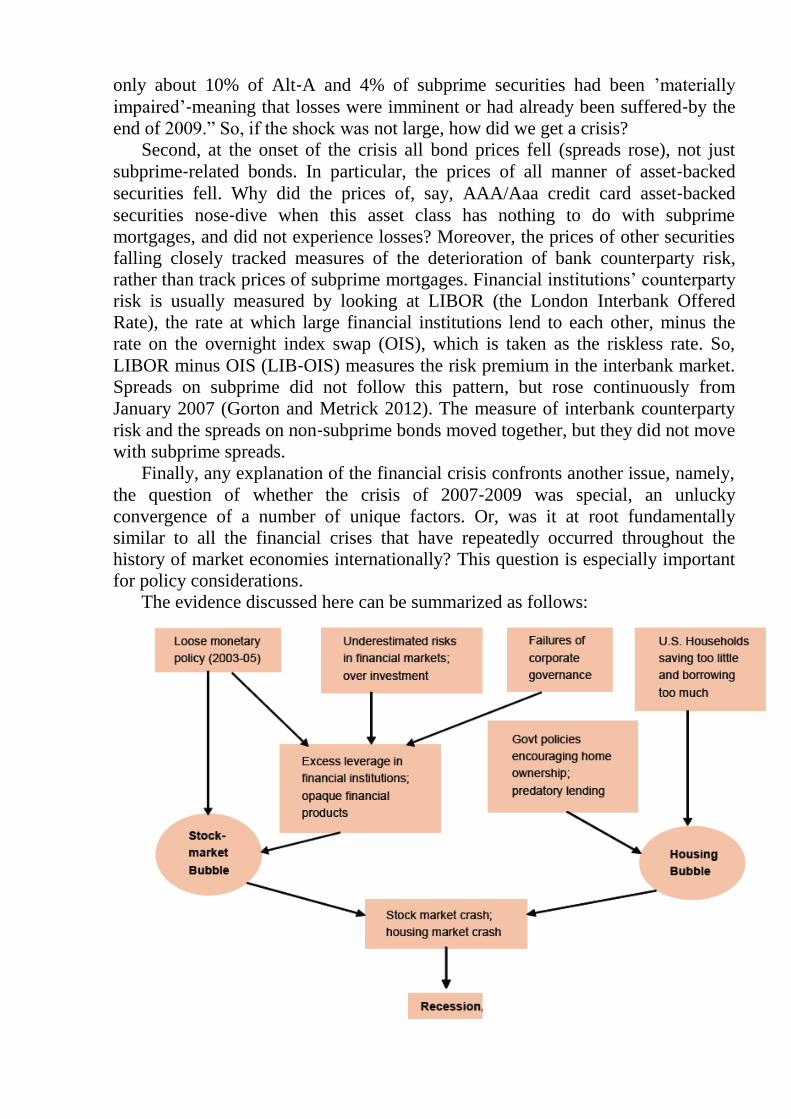

The evidence discussed here can be summarized as follows:

Figure 3.Origins of world financial crisis

Note: International Institute for Labor Studies

So, the main causes of the global financial recession:

problems with selected by the U.S. model of economic advancement;

extensive development of derivative financial instruments;

prices at commodity exchanges;

inefficient investments risk assessment system, investing in risky

assets - the crisis in subprime.

In 2007 in the United States has badly hit by the burst of the property bubble

and panic spread over the country. Although the economy of United States grew by

0.6 per cent in the last quarter of 2007, down from 4.9 percent in the previous

quarter, day by day worsening scenarios emerge, from escalating oil prices, to a

depreciating dollar and financial institutions’ bailout by the Federal Reserve. Many

economists and policy makers share the view that a subprime‐led recession – i.e.

two consecutive quarters with negative growth – is inevitable and will be much

deeper and longer than the 2001 dot‐com downturn. United States recession will

undoubtedly have an important impact on the world economy.

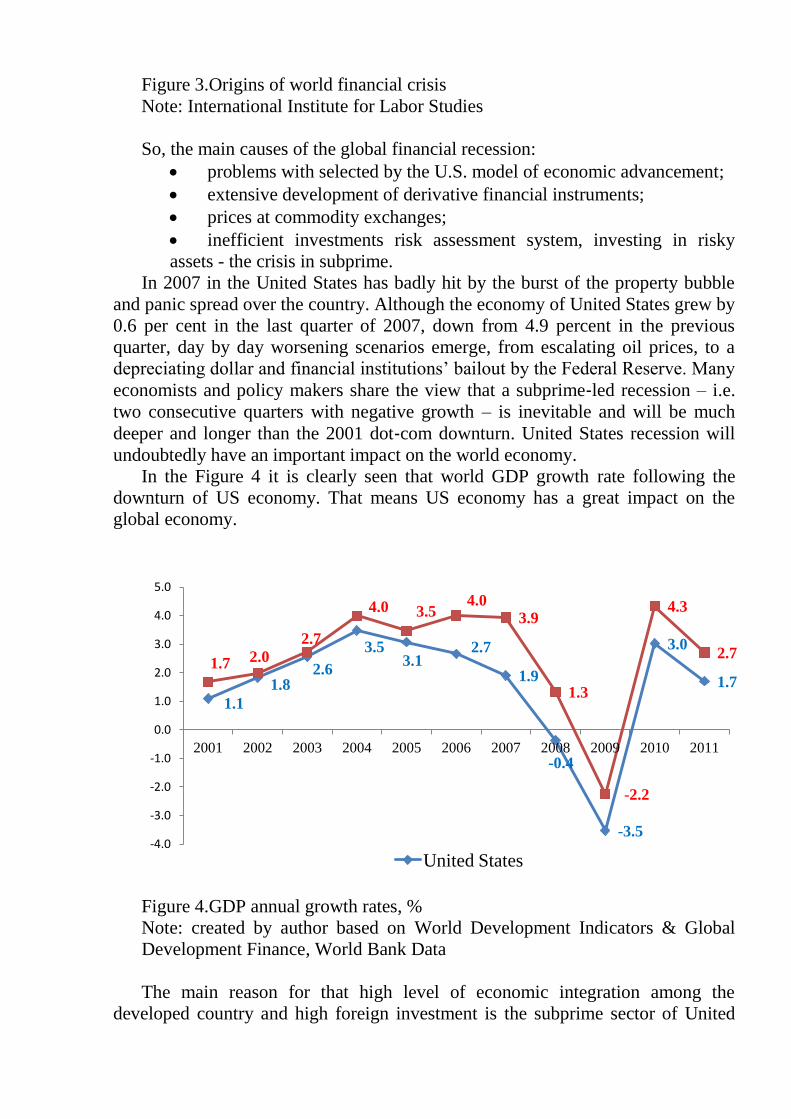

In the Figure 4 it is clearly seen that world GDP growth rate following the

downturn of US economy. That means US economy has a great impact on the

global economy.

Figure 4.GDP annual growth rates, %

Note: created by author based on World Development Indicators & Global

Development Finance, World Bank Data

The main reason for that high level of economic integration among the

developed country and high foreign investment is the subprime sector of United

1.1

1.8 2.6

3.5 3.1

2.7

1.9

-0.4

-3.5

3.0

1.7

1.7 2.0

2.7

4.0 3.5 4.0

3.9

1.3

-2.2

4.3

2.7

-4.0

-3.0

-2.0

-1.0

0.0

1.0

2.0

3.0

4.0

5.0

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

United States

States. Except few exception like India, China most of the countries around the

world badly hit by this financial meltdown. In this paper impact of financial crisis

over the major economies of the world revisited to find out the recovery policy and

their effects. During this financial crisis, global economy has suffered, but the

degree of regression varied. After second half of 2009, the global recession

triggered by financial crisis was nearing completion, and economic recovery began

to appear, but the situation of recovery was different in various countries. January

2010 the report of IMF "World Economic Outlook" noted that developed countries

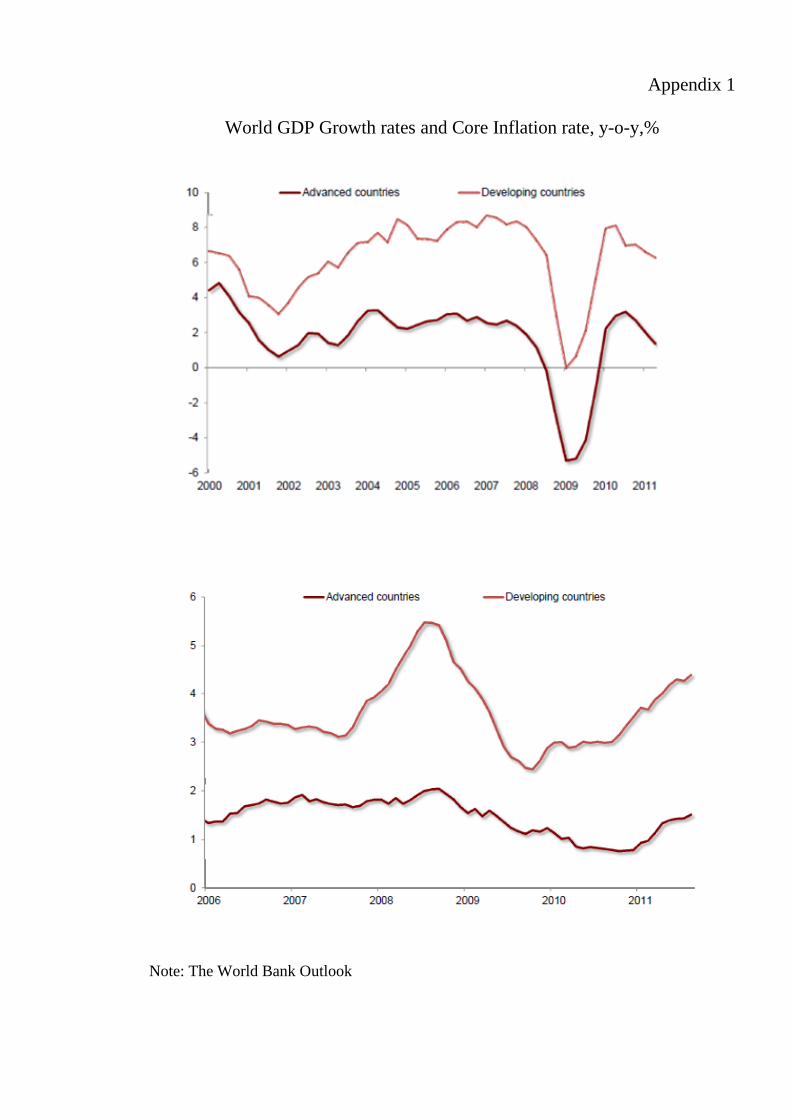

experienced a growth with 3.2% in 2009; after the recession, the economic growth

was expected in 2010 only 2.1%; yet this was in sharp contrast to the emerging

economies, whose growth as a whole in 2010 would reach 6.0% (Appendix 1).

According to "World Economic Outlook" report of 2011, the real economic growth

rate of emerging and developing economies in 2010 has reached 7.1%.

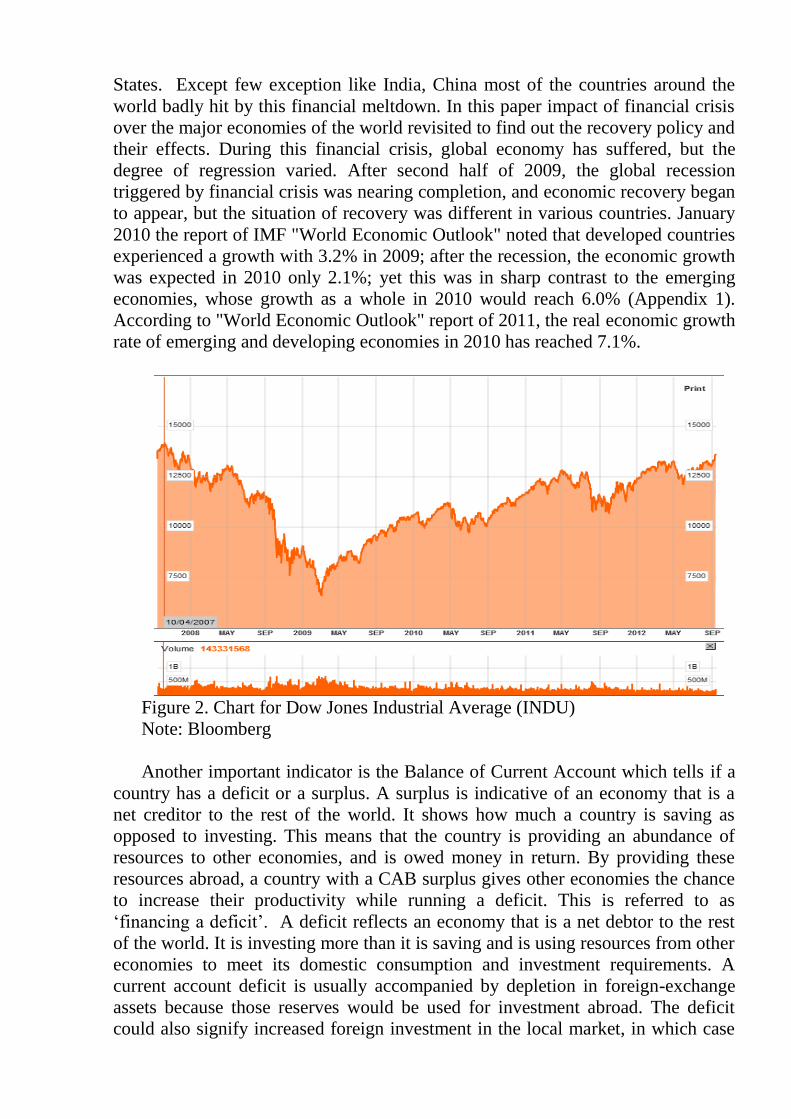

Figure 2. Chart for Dow Jones Industrial Average (INDU)

Note: Bloomberg

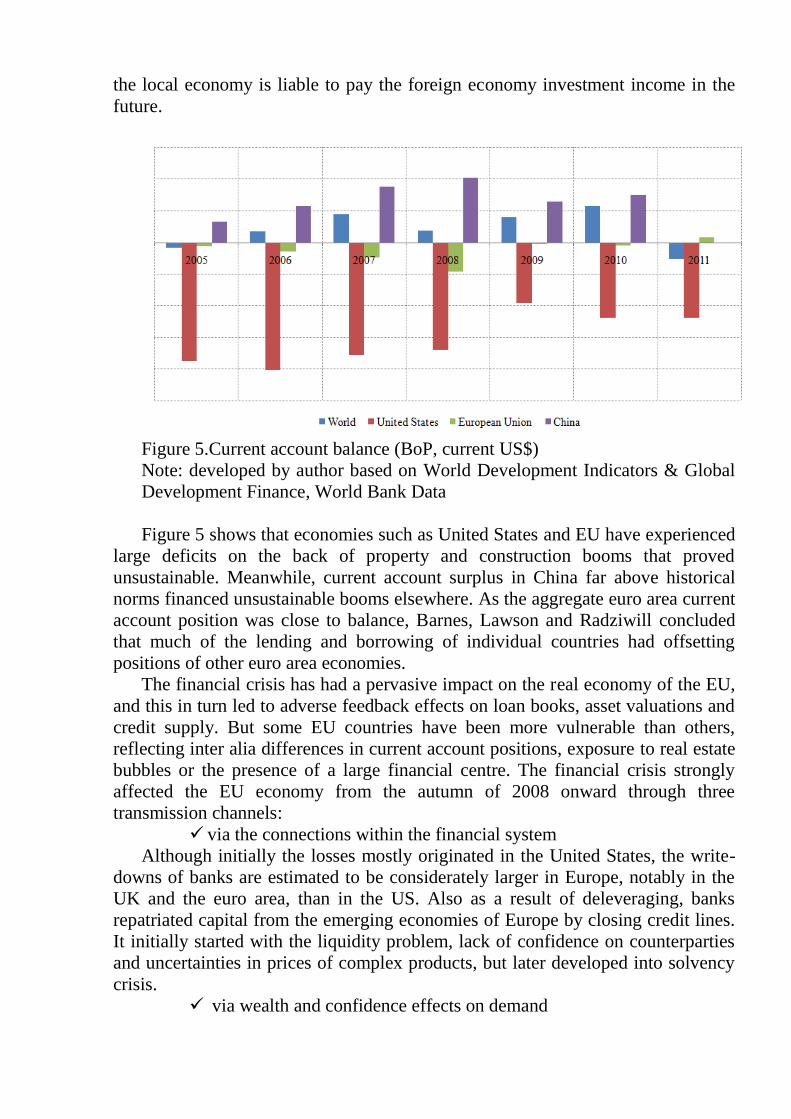

Another important indicator is the Balance of Current Account which tells if a

country has a deficit or a surplus. A surplus is indicative of an economy that is a

net creditor to the rest of the world. It shows how much a country is saving as

opposed to investing. This means that the country is providing an abundance of

resources to other economies, and is owed money in return. By providing these

resources abroad, a country with a CAB surplus gives other economies the chance

to increase their productivity while running a deficit. This is referred to as

‘financing a deficit’. A deficit reflects an economy that is a net debtor to the rest

of the world. It is investing more than it is saving and is using resources from other

economies to meet its domestic consumption and investment requirements. A

current account deficit is usually accompanied by depletion in foreign-exchange

assets because those reserves would be used for investment abroad. The deficit

could also signify increased foreign investment in the local market, in which case

the local economy is liable to pay the foreign economy investment income in the

future.

Figure 5.Current account balance (BoP, current US$)

Note: developed by author based on World Development Indicators & Global

Development Finance, World Bank Data

Figure 5 shows that economies such as United States and EU have experienced

large deficits on the back of property and construction booms that proved

unsustainable. Meanwhile, current account surplus in China far above historical

norms financed unsustainable booms elsewhere. As the aggregate euro area current

account position was close to balance, Barnes, Lawson and Radziwill concluded

that much of the lending and borrowing of individual countries had offsetting

positions of other euro area economies.

The financial crisis has had a pervasive impact on the real economy of the EU,

and this in turn led to adverse feedback effects on loan books, asset valuations and

credit supply. But some EU countries have been more vulnerable than others,

reflecting inter alia differences in current account positions, exposure to real estate

bubbles or the presence of a large financial centre. The financial crisis strongly

affected the EU economy from the autumn of 2008 onward through three

transmission channels:

via the connections within the financial system

Although initially the losses mostly originated in the United States, the write-

downs of banks are estimated to be considerately larger in Europe, notably in the

UK and the euro area, than in the US. Also as a result of deleveraging, banks

repatriated capital from the emerging economies of Europe by closing credit lines.

It initially started with the liquidity problem, lack of confidence on counterparties

and uncertainties in prices of complex products, but later developed into solvency

crisis.

via wealth and confidence effects on demand

As the housing prices dropped, households experienced stiffening of lending

standards. Saving increased and the demand for consumer goods decreased. Easy

credit was no more available. Also there was little confidence on the bank

portfolios. These portfolios found no buyers, as investors flocked to safe havens

(government bonds).

via global trade

Business investment and demand for consumer durables - both strongly credit

dependent and trade intensive - had plummeted, due to the unavailability of trade

finance and a faster impact of activity on trade as a result of globalization and the

prevalence of global supply chains.

The world financial crisis - starting from the US subprime mortgage crisis -

spread in all major economies. “UBS quantified their expected recession durations:

the Eurozone's would last two quarters, the United States' would last three quarters,

and the United Kingdom's would last four quarters.” Many experts suggest

systematic money injection in the financial market to pull the global economy. The

main idea was not to break established system very rapidly. Just bring the

confidence of the stakeholders of the market. Developing countries show a mixed

impact from the crisis. Some economies fall from very high growth rate like

Cambodia and Kenya. On the other hand India shows a very good economic

projection with around double digit economic growth. One of the major

economies, China also shows more than double digit economic growth. Arab world

also badly affected by the crisis. They lose around $3 trillion due to crisis.

Unemployment also hit very badly. Worst scenario was reduction in foreign

investment. Due to lack of foreign investment Arabs are failed to continue their

development project create huge layoffs. Euro crisis, 2010 added a new dimension

of the existing financial crisis. Some euro countries are suffering from very high

amount of external debt. Recently a long desired package received by the Greece

government. Some other euro nations are also contracted for mutual financial

assistance which is approved by the euro central bank.

IMF was forecasted in January, 2010 the advanced economies will be exit from

the current recession from middle of 2010. Conversely these countries shows

average GDP growth rate of about 2% in the third quarter of 2009. And emerging

economies accelerated at around 8%. Besides global productions and trade deals

increase indicating recovery. Most of the researcher forecasted continuation of this

recovery in 2010. But the central question is the strength of the recovery as very

high level of unemployment and huge external debt exist in the major economies.

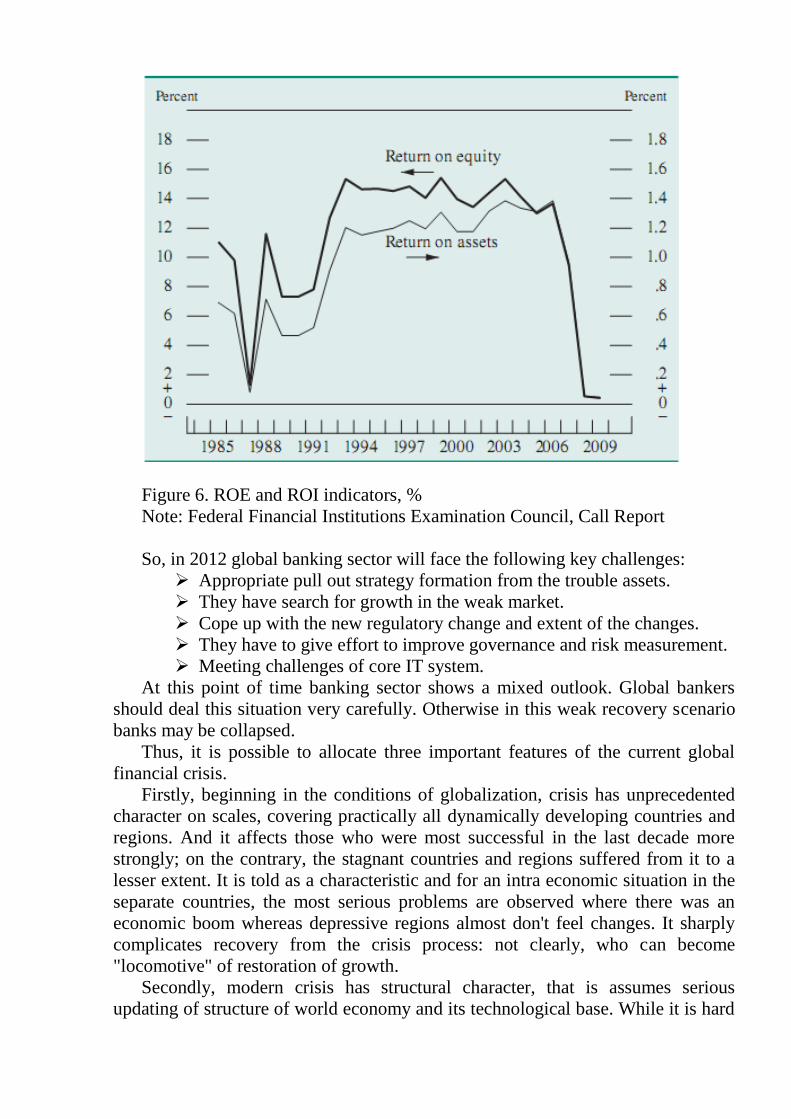

Banking sector was seriously affected by the financial crisis. Profitability was hit at

the bottom. This sector is coming out from the recession but very slowly. The write

down of bad debt is lower than the expected earlier. United States and European

banks recapitalization is progressing while financial instability is the major risk.

Governments should not stop the measures taken in the recession period. And they

have to cautiously plan the exit strategy of intervention.

Figure 6. ROE and ROI indicators, %

Note: Federal Financial Institutions Examination Council, Call Report

So, in 2012 global banking sector will face the following key challenges:

Appropriate pull out strategy formation from the trouble assets.

They have search for growth in the weak market.

Cope up with the new regulatory change and extent of the changes.

They have to give effort to improve governance and risk measurement.

Meeting challenges of core IT system.

At this point of time banking sector shows a mixed outlook. Global bankers

should deal this situation very carefully. Otherwise in this weak recovery scenario

banks may be collapsed.

Thus, it is possible to allocate three important features of the current global

financial crisis.

Firstly, beginning in the conditions of globalization, crisis has unprecedented

character on scales, covering practically all dynamically developing countries and

regions. And it affects those who were most successful in the last decade more

strongly; on the contrary, the stagnant countries and regions suffered from it to a

lesser extent. It is told as a characteristic and for an intra economic situation in the

separate countries, the most serious problems are observed where there was an

economic boom whereas depressive regions almost don't feel changes. It sharply

complicates recovery from the crisis process: not clearly, who can become

"locomotive" of restoration of growth.

Secondly, modern crisis has structural character, that is assumes serious

updating of structure of world economy and its technological base. While it is hard

to say, what structural changes will occur, however redistribution of forces in

branch and regional aspects will be their result.

Thirdly, crisis has innovative character. In recent years it was much told about

importance of innovations, transfer of economy to an innovative way of

development; it also occurred in the financial and economic sphere. Here arose and

quickly financial innovations — new tools of the financial market which as then it

seemed, can create conditions for infinite growth extended. But, as it becomes

clear now, many leaders of the financial world had of them very vague idea that

brought to a double sort to consequences.

Finally, the global financial recession that began in 2007 and covered almost

every country, could be prognosticated. If its consequences and growth were

predicted, its negative and destructive influence on the world and national

economics could be partly neutralized. As any crisis, the financial recession of

2007 had its own preconditions and indicators, showing disproportions in the

global economics and the U.S. financial system’s condition, that the world's rating

agencies and leading economic analysts were not paying attention or were believed

in U.S. indestructibility and firmness. Still, the recession occurred, maybe a little

earlier or later than it should, it’s an occasion for dispute.

PART II FINANCIAL CRISIS IN KAZAKHSTAN

2.1 Influence of global financial crisis on Kazakh economy

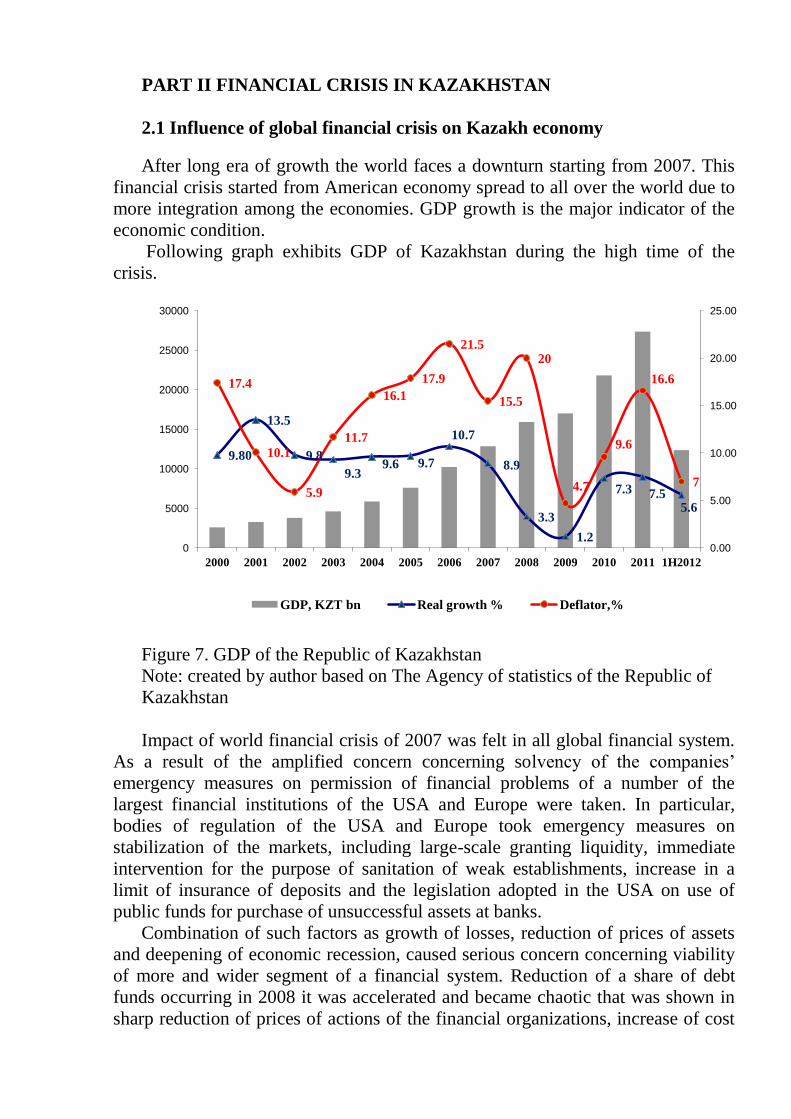

After long era of growth the world faces a downturn starting from 2007. This

financial crisis started from American economy spread to all over the world due to

more integration among the economies. GDP growth is the major indicator of the

economic condition.

Following graph exhibits GDP of Kazakhstan during the high time of the

crisis.

Figure 7. GDP of the Republic of Kazakhstan

Note: created by author based on The Agency of statistics of the Republic of

Kazakhstan

Impact of world financial crisis of 2007 was felt in all global financial system.

As a result of the amplified concern concerning solvency of the companies’

emergency measures on permission of financial problems of a number of the

largest financial institutions of the USA and Europe were taken. In particular,

bodies of regulation of the USA and Europe took emergency measures on

stabilization of the markets, including large-scale granting liquidity, immediate

intervention for the purpose of sanitation of weak establishments, increase in a

limit of insurance of deposits and the legislation adopted in the USA on use of

public funds for purchase of unsuccessful assets at banks.

Combination of such factors as growth of losses, reduction of prices of assets

and deepening of economic recession, caused serious concern concerning viability

of more and wider segment of a financial system. Reduction of a share of debt

funds occurring in 2008 it was accelerated and became chaotic that was shown in

sharp reduction of prices of actions of the financial organizations, increase of cost

9.80

13.5

9.8

9.3 9.6 9.7

10.7

8.9

3.3

1.2

7.3 7.5 5.6

17.4

10.1

5.9

11.7

16.1

17.9

21.5

15.5

20

4.7

9.6

16.6

7

0.00

5.00

10.00

15.00

20.00

25.00

0

5000

10000

15000

20000

25000

30000

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 1H2012

GDP, KZT bn Real growth % Deflator,%

of financing and the expenses connected with protection against a default, and also

falling of the prices for assets.

Separate attempts to overcome intensity with liquidity and to solve problems of

the organizations experiencing financial difficulties, didn't allow restoring trust of

participants of the market as these measures couldn't solve widely extended deep

problems.

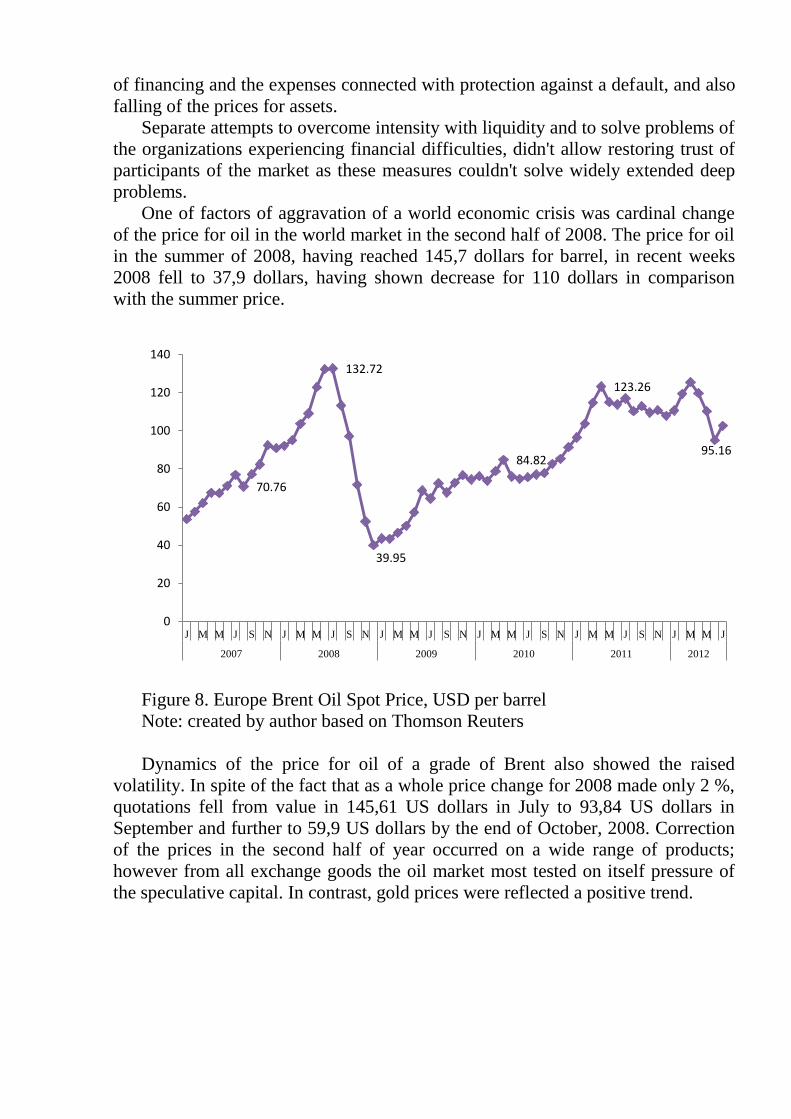

One of factors of aggravation of a world economic crisis was cardinal change

of the price for oil in the world market in the second half of 2008. The price for oil

in the summer of 2008, having reached 145,7 dollars for barrel, in recent weeks

2008 fell to 37,9 dollars, having shown decrease for 110 dollars in comparison

with the summer price.

Figure 8. Europe Brent Oil Spot Price, USD per barrel

Note: created by author based on Thomson Reuters

Dynamics of the price for oil of a grade of Brent also showed the raised

volatility. In spite of the fact that as a whole price change for 2008 made only 2 %,

quotations fell from value in 145,61 US dollars in July to 93,84 US dollars in

September and further to 59,9 US dollars by the end of October, 2008. Correction

of the prices in the second half of year occurred on a wide range of products;

however from all exchange goods the oil market most tested on itself pressure of

the speculative capital. In contrast, gold prices were reflected a positive trend.

70.76

132.72

39.95

84.82

123.26

95.16

0

20

40

60

80

100

120

140

J M M J S N J M M J S N J M M J S N J M M J S N J M M J S N J M M J

2007 2008 2009 2010 2011 2012

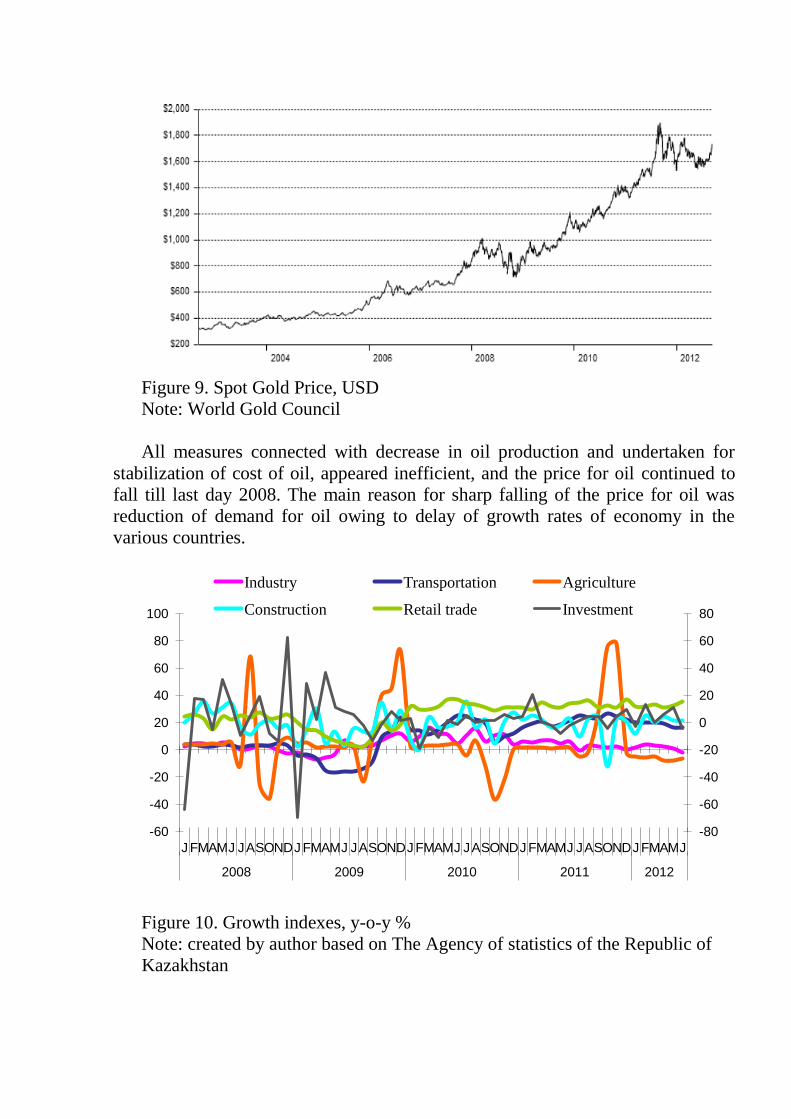

Figure 9. Spot Gold Price, USD

Note: World Gold Council

All measures connected with decrease in oil production and undertaken for

stabilization of cost of oil, appeared inefficient, and the price for oil continued to

fall till last day 2008. The main reason for sharp falling of the price for oil was

reduction of demand for oil owing to delay of growth rates of economy in the

various countries.

Figure 10. Growth indexes, y-o-y %

Note: created by author based on The Agency of statistics of the Republic of

Kazakhstan

-80

-60

-40

-20

0

20

40

60

80

-60

-40

-20

0

20

40

60

80

100

J F M A M J J A S O N D J F M A M J J A S O N D J F M A M J J A S O N D J F M A M J J A S O N D J F M A M J

2008 2009 2010 2011 2012

Industry Transportation Agriculture

Construction Retail trade Investment

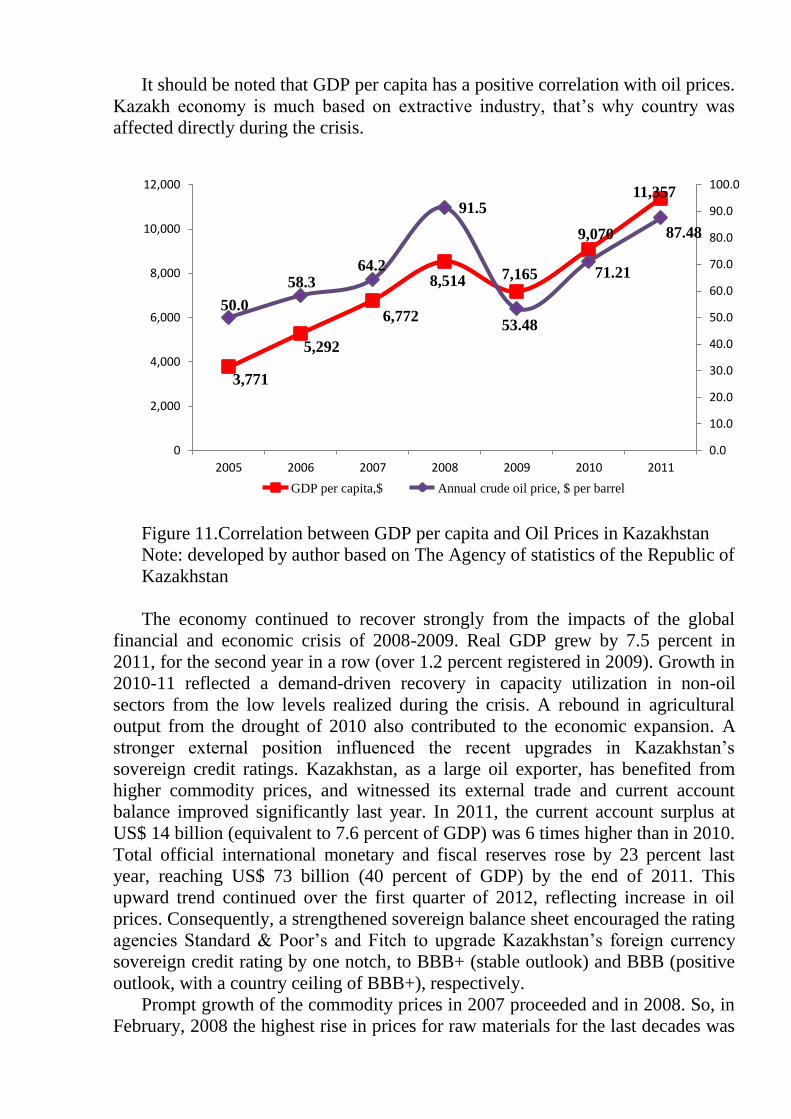

It should be noted that GDP per capita has a positive correlation with oil prices.

Kazakh economy is much based on extractive industry, that’s why country was

affected directly during the crisis.

Figure 11.Correlation between GDP per capita and Oil Prices in Kazakhstan

Note: developed by author based on The Agency of statistics of the Republic of

Kazakhstan

The economy continued to recover strongly from the impacts of the global

financial and economic crisis of 2008-2009. Real GDP grew by 7.5 percent in

2011, for the second year in a row (over 1.2 percent registered in 2009). Growth in

2010-11 reflected a demand-driven recovery in capacity utilization in non-oil

sectors from the low levels realized during the crisis. A rebound in agricultural

output from the drought of 2010 also contributed to the economic expansion. A

stronger external position influenced the recent upgrades in Kazakhstan’s

sovereign credit ratings. Kazakhstan, as a large oil exporter, has benefited from

higher commodity prices, and witnessed its external trade and current account

balance improved significantly last year. In 2011, the current account surplus at

US$ 14 billion (equivalent to 7.6 percent of GDP) was 6 times higher than in 2010.

Total official international monetary and fiscal reserves rose by 23 percent last

year, reaching US$ 73 billion (40 percent of GDP) by the end of 2011. This

upward trend continued over the first quarter of 2012, reflecting increase in oil

prices. Consequently, a strengthened sovereign balance sheet encouraged the rating

agencies Standard & Poor’s and Fitch to upgrade Kazakhstan’s foreign currency

sovereign credit rating by one notch, to BBB+ (stable outlook) and BBB (positive

outlook, with a country ceiling of BBB+), respectively.

Prompt growth of the commodity prices in 2007 proceeded and in 2008. So, in

February, 2008 the highest rise in prices for raw materials for the last decades was

3,771

5,292

6,772

8,514 7,165

9,070

11,357

50.0

58.3 64.2

91.5

53.48

71.21

87.48

0.0

10.0

20.0

30.0

40.0

50.0

60.0

70.0

80.0

90.0

100.0

0

2,000

4,000

6,000

8,000

10,000

12,000

2005 2006 2007 2008 2009 2010 2011

GDP per capita,$ Annual crude oil price, $ per barrel

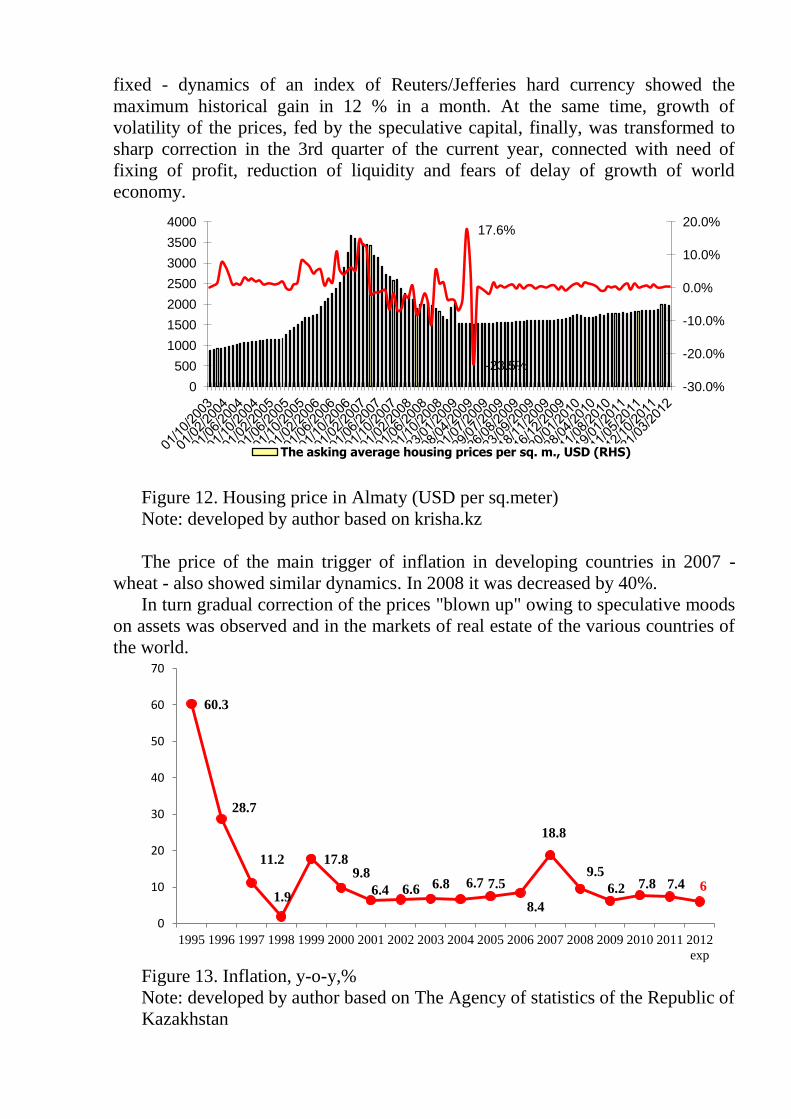

fixed - dynamics of an index of Reuters/Jefferies hard currency showed the

maximum historical gain in 12 % in a month. At the same time, growth of

volatility of the prices, fed by the speculative capital, finally, was transformed to

sharp correction in the 3rd quarter of the current year, connected with need of

fixing of profit, reduction of liquidity and fears of delay of growth of world

economy.

Figure 12. Housing price in Almaty (USD per sq.meter)

Note: developed by author based on krisha.kz

The price of the main trigger of inflation in developing countries in 2007 -

wheat - also showed similar dynamics. In 2008 it was decreased by 40%.

In turn gradual correction of the prices "blown up" owing to speculative moods

on assets was observed and in the markets of real estate of the various countries of

the world.

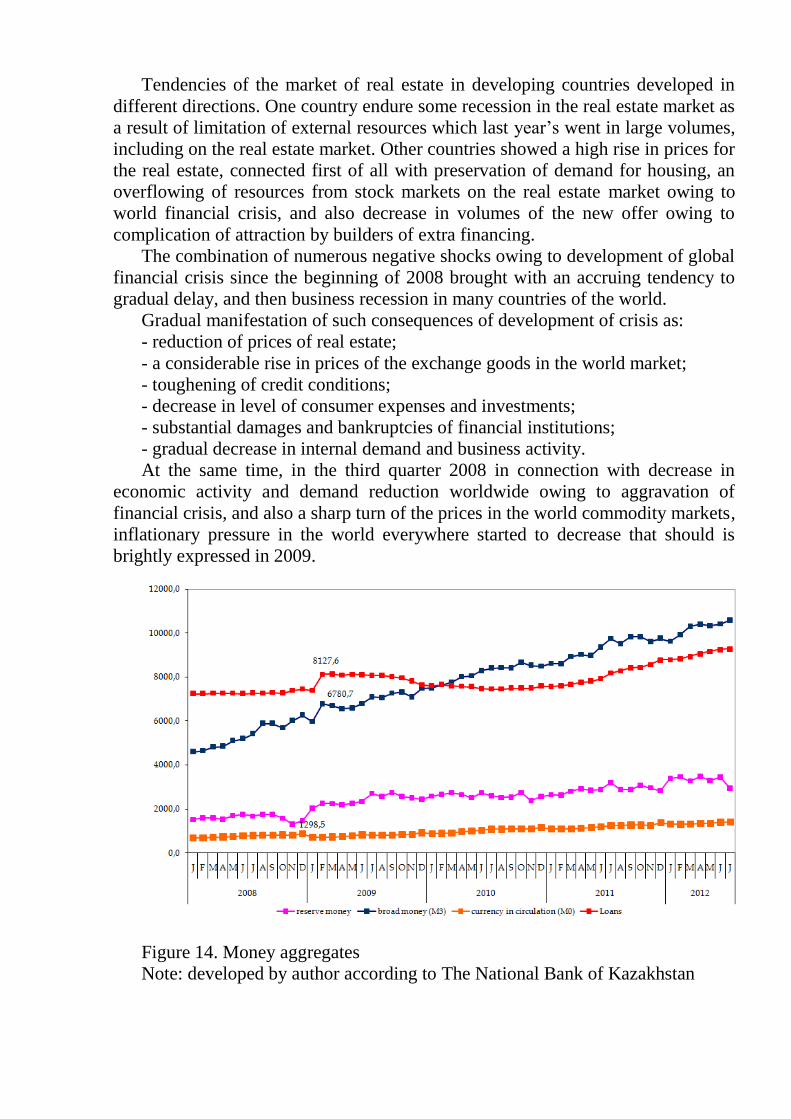

Figure 13. Inflation, y-o-y,%

Note: developed by author based on The Agency of statistics of the Republic of

Kazakhstan

17.6%

-23.5%

-30.0%

-20.0%

-10.0%

0.0%

10.0%

20.0%

0

500

1000

1500

2000

2500

3000

3500

4000

The asking average housing prices per sq. m., USD (RHS)

60.3

28.7

11.2

1.9

17.8 9.8

6.4 6.6 6.8 6.7 7.5

8.4

18.8

9.5

6.2 7.8 7.4 6

0

10

20

30

40

50

60

70

1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

exp

Tendencies of the market of real estate in developing countries developed in

different directions. One country endure some recession in the real estate market as

a result of limitation of external resources which last year’s went in large volumes,

including on the real estate market. Other countries showed a high rise in prices for

the real estate, connected first of all with preservation of demand for housing, an

overflowing of resources from stock markets on the real estate market owing to

world financial crisis, and also decrease in volumes of the new offer owing to

complication of attraction by builders of extra financing.

The combination of numerous negative shocks owing to development of global

financial crisis since the beginning of 2008 brought with an accruing tendency to

gradual delay, and then business recession in many countries of the world.

Gradual manifestation of such consequences of development of crisis as:

- reduction of prices of real estate;

- a considerable rise in prices of the exchange goods in the world market;

- toughening of credit conditions;

- decrease in level of consumer expenses and investments;

- substantial damages and bankruptcies of financial institutions;

- gradual decrease in internal demand and business activity.

At the same time, in the third quarter 2008 in connection with decrease in

economic activity and demand reduction worldwide owing to aggravation of

financial crisis, and also a sharp turn of the prices in the world commodity markets,

inflationary pressure in the world everywhere started to decrease that should is

brightly expressed in 2009.

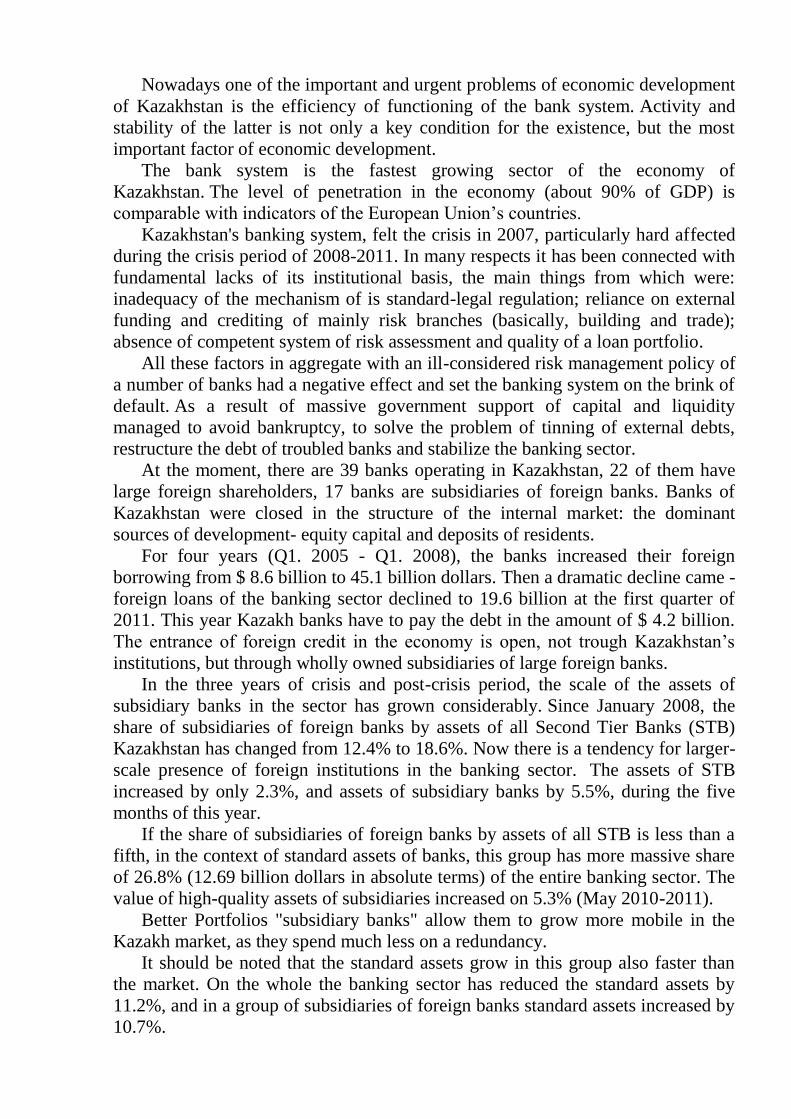

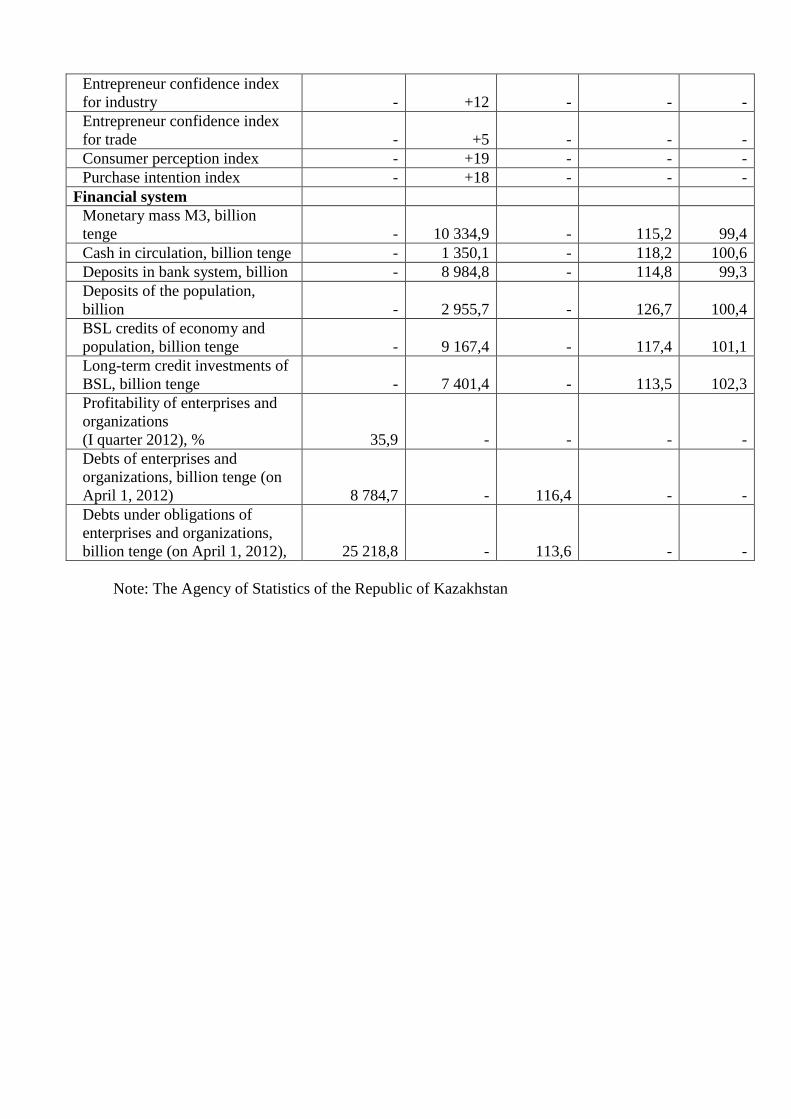

Figure 14. Money aggregates

Note: developed by author according to The National Bank of Kazakhstan

Nowadays one of the important and urgent problems of economic development

of Kazakhstan is the efficiency of functioning of the bank system. Activity and

stability of the latter is not only a key condition for the existence, but the most

important factor of economic development.

The bank system is the fastest growing sector of the economy of

Kazakhstan. The level of penetration in the economy (about 90% of GDP) is

comparable with indicators of the European Union’s countries.

Kazakhstan's banking system, felt the crisis in 2007, particularly hard affected

during the crisis period of 2008-2011. In many respects it has been connected with

fundamental lacks of its institutional basis, the main things from which were:

inadequacy of the mechanism of is standard-legal regulation; reliance on external

funding and crediting of mainly risk branches (basically, building and trade);

absence of competent system of risk assessment and quality of a loan portfolio.

All these factors in aggregate with an ill-considered risk management policy of

a number of banks had a negative effect and set the banking system on the brink of

default. As a result of massive government support of capital and liquidity

managed to avoid bankruptcy, to solve the problem of tinning of external debts,

restructure the debt of troubled banks and stabilize the banking sector.

At the moment, there are 39 banks operating in Kazakhstan, 22 of them have

large foreign shareholders, 17 banks are subsidiaries of foreign banks. Banks of

Kazakhstan were closed in the structure of the internal market: the dominant

sources of development- equity capital and deposits of residents.

For four years (Q1. 2005 - Q1. 2008), the banks increased their foreign

borrowing from $ 8.6 billion to 45.1 billion dollars. Then a dramatic decline came -

foreign loans of the banking sector declined to 19.6 billion at the first quarter of

2011. This year Kazakh banks have to pay the debt in the amount of $ 4.2 billion.

The entrance of foreign credit in the economy is open, not trough Kazakhstan’s

institutions, but through wholly owned subsidiaries of large foreign banks.

In the three years of crisis and post-crisis period, the scale of the assets of

subsidiary banks in the sector has grown considerably. Since January 2008, the

share of subsidiaries of foreign banks by assets of all Second Tier Banks (STB)

Kazakhstan has changed from 12.4% to 18.6%. Now there is a tendency for larger-

scale presence of foreign institutions in the banking sector. The assets of STB

increased by only 2.3%, and assets of subsidiary banks by 5.5%, during the five

months of this year.

If the share of subsidiaries of foreign banks by assets of all STB is less than a

fifth, in the context of standard assets of banks, this group has more massive share

of 26.8% (12.69 billion dollars in absolute terms) of the entire banking sector. The

value of high-quality assets of subsidiaries increased on 5.3% (May 2010-2011).

Better Portfolios "subsidiary banks" allow them to grow more mobile in the

Kazakh market, as they spend much less on a redundancy.

It should be noted that the standard assets grow in this group also faster than

the market. On the whole the banking sector has reduced the standard assets by

11.2%, and in a group of subsidiaries of foreign banks standard assets increased by

10.7%.

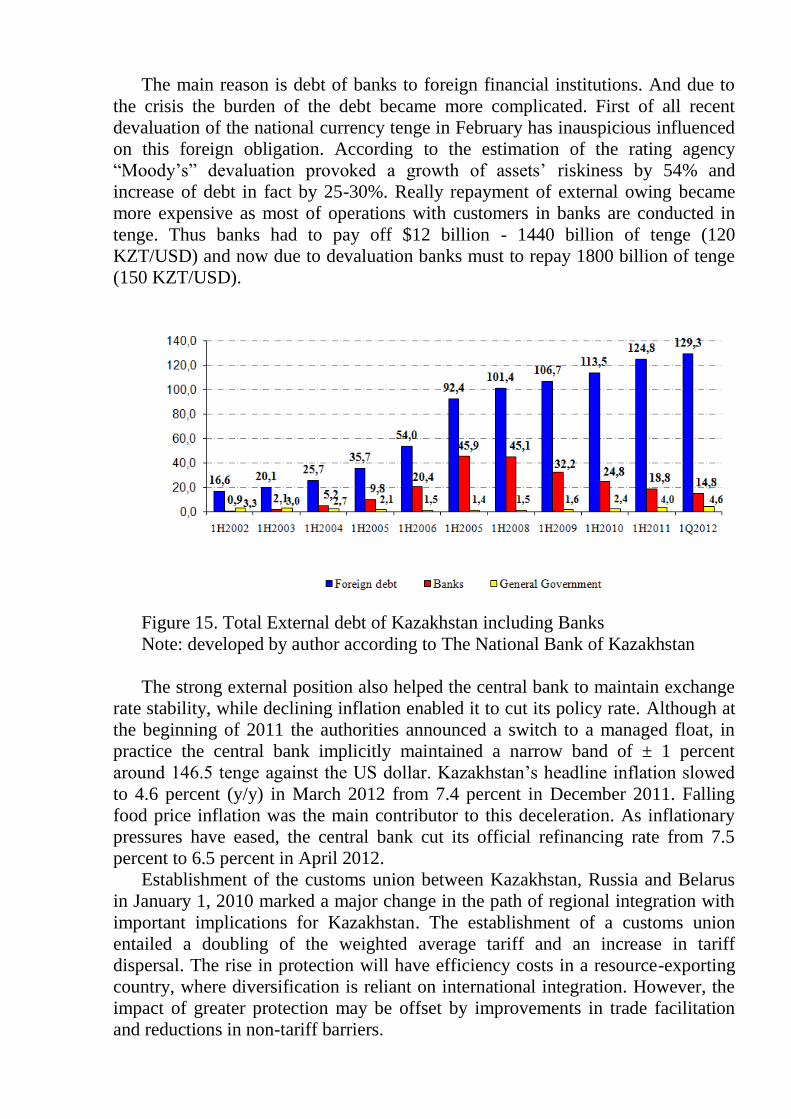

The main reason is debt of banks to foreign financial institutions. And due to

the crisis the burden of the debt became more complicated. First of all recent

devaluation of the national currency tenge in February has inauspicious influenced

on this foreign obligation. According to the estimation of the rating agency

“Moody’s” devaluation provoked a growth of assets’ riskiness by 54% and

increase of debt in fact by 25-30%. Really repayment of external owing became

more expensive as most of operations with customers in banks are conducted in

tenge. Thus banks had to pay off $12 billion - 1440 billion of tenge (120

KZT/USD) and now due to devaluation banks must to repay 1800 billion of tenge

(150 KZT/USD).

Figure 15. Total External debt of Kazakhstan including Banks

Note: developed by author according to The National Bank of Kazakhstan

The strong external position also helped the central bank to maintain exchange

rate stability, while declining inflation enabled it to cut its policy rate. Although at

the beginning of 2011 the authorities announced a switch to a managed float, in

practice the central bank implicitly maintained a narrow band of ± 1 percent

around 146.5 tenge against the US dollar. Kazakhstan’s headline inflation slowed

to 4.6 percent (y/y) in March 2012 from 7.4 percent in December 2011. Falling

food price inflation was the main contributor to this deceleration. As inflationary

pressures have eased, the central bank cut its official refinancing rate from 7.5

percent to 6.5 percent in April 2012.

Establishment of the customs union between Kazakhstan, Russia and Belarus

in January 1, 2010 marked a major change in the path of regional integration with

important implications for Kazakhstan. The establishment of a customs union

entailed a doubling of the weighted average tariff and an increase in tariff

dispersal. The rise in protection will have efficiency costs in a resource-exporting

country, where diversification is reliant on international integration. However, the

impact of greater protection may be offset by improvements in trade facilitation

and reductions in non-tariff barriers.

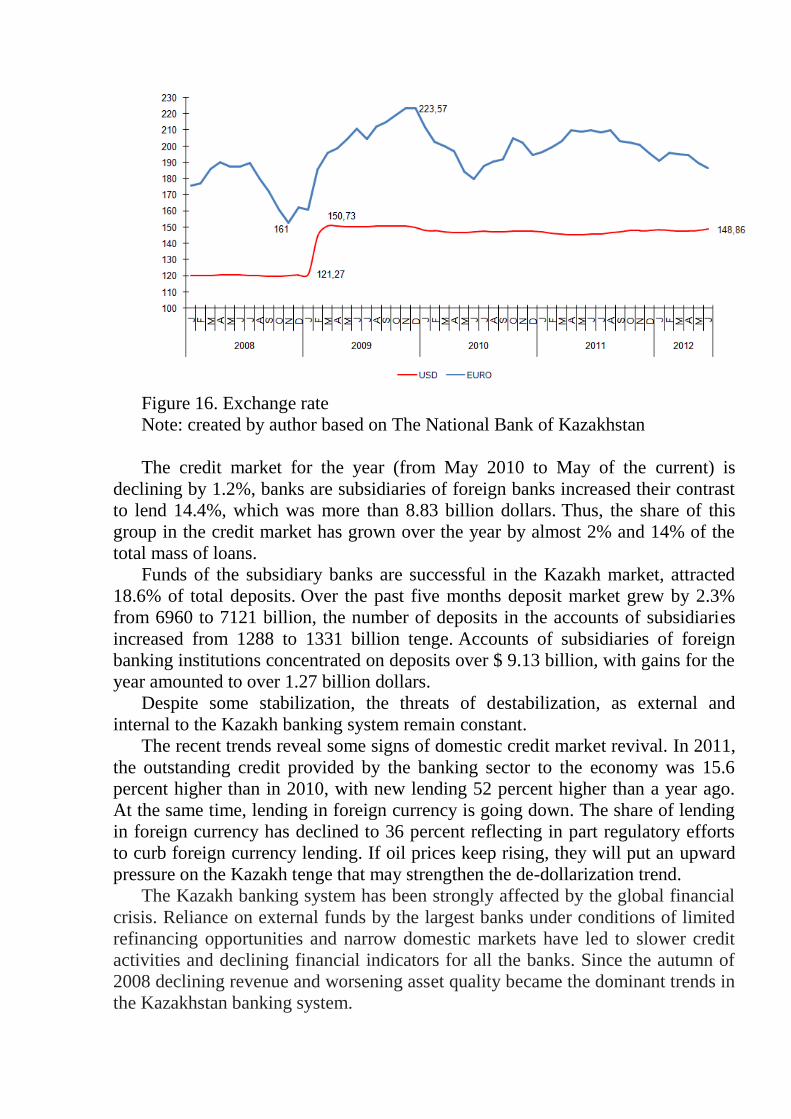

Figure 16. Exchange rate

Note: created by author based on The National Bank of Kazakhstan

The credit market for the year (from May 2010 to May of the current) is

declining by 1.2%, banks are subsidiaries of foreign banks increased their contrast

to lend 14.4%, which was more than 8.83 billion dollars. Thus, the share of this

group in the credit market has grown over the year by almost 2% and 14% of the

total mass of loans.

Funds of the subsidiary banks are successful in the Kazakh market, attracted

18.6% of total deposits. Over the past five months deposit market grew by 2.3%

from 6960 to 7121 billion, the number of deposits in the accounts of subsidiaries

increased from 1288 to 1331 billion tenge. Accounts of subsidiaries of foreign

banking institutions concentrated on deposits over $ 9.13 billion, with gains for the

year amounted to over 1.27 billion dollars.

Despite some stabilization, the threats of destabilization, as external and

internal to the Kazakh banking system remain constant.

The recent trends reveal some signs of domestic credit market revival. In 2011,

the outstanding credit provided by the banking sector to the economy was 15.6

percent higher than in 2010, with new lending 52 percent higher than a year ago.

At the same time, lending in foreign currency is going down. The share of lending

in foreign currency has declined to 36 percent reflecting in part regulatory efforts

to curb foreign currency lending. If oil prices keep rising, they will put an upward

pressure on the Kazakh tenge that may strengthen the de-dollarization trend.

The Kazakh banking system has been strongly affected by the global financial

crisis. Reliance on external funds by the largest banks under conditions of limited

refinancing opportunities and narrow domestic markets have led to slower credit

activities and declining financial indicators for all the banks. Since the autumn of

2008 declining revenue and worsening asset quality became the dominant trends in

the Kazakhstan banking system.

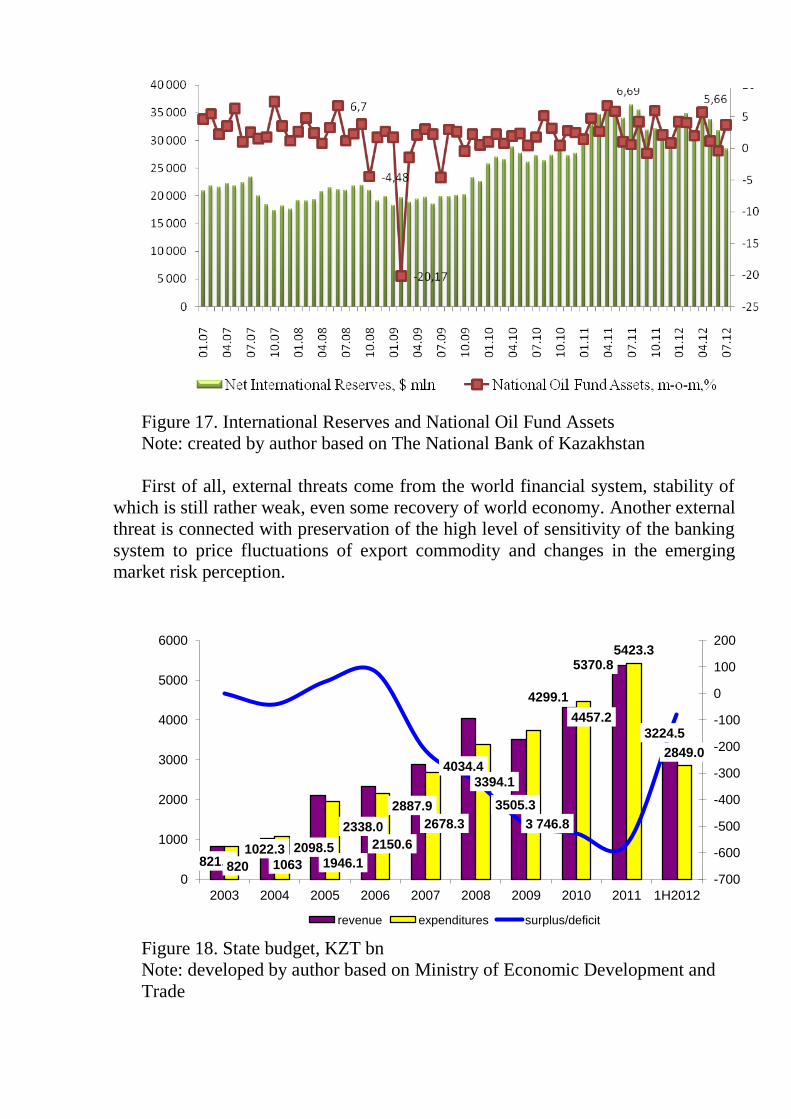

Figure 17. International Reserves and National Oil Fund Assets

Note: created by author based on The National Bank of Kazakhstan

First of all, external threats come from the world financial system, stability of

which is still rather weak, even some recovery of world economy. Another external

threat is connected with preservation of the high level of sensitivity of the banking

system to price fluctuations of export commodity and changes in the emerging

market risk perception.

Figure 18. State budget, KZT bn

Note: developed by author based on Ministry of Economic Development and

Trade

821.2 1022.3 2098.5

2338.0

2887.9

4034.4

3505.3

4299.1

5370.8

3224.5

820 1063 1946.1

2150.6

2678.3

3394.1

3 746.8

4457.2

5423.3

2849.0

-700

-600

-500

-400

-300

-200

-100

0

100

200

0

1000

2000

3000

4000

5000

6000

2003 2004 2005 2006 2007 2008 2009 2010 2011 1H2012

revenue expenditures surplus/deficit

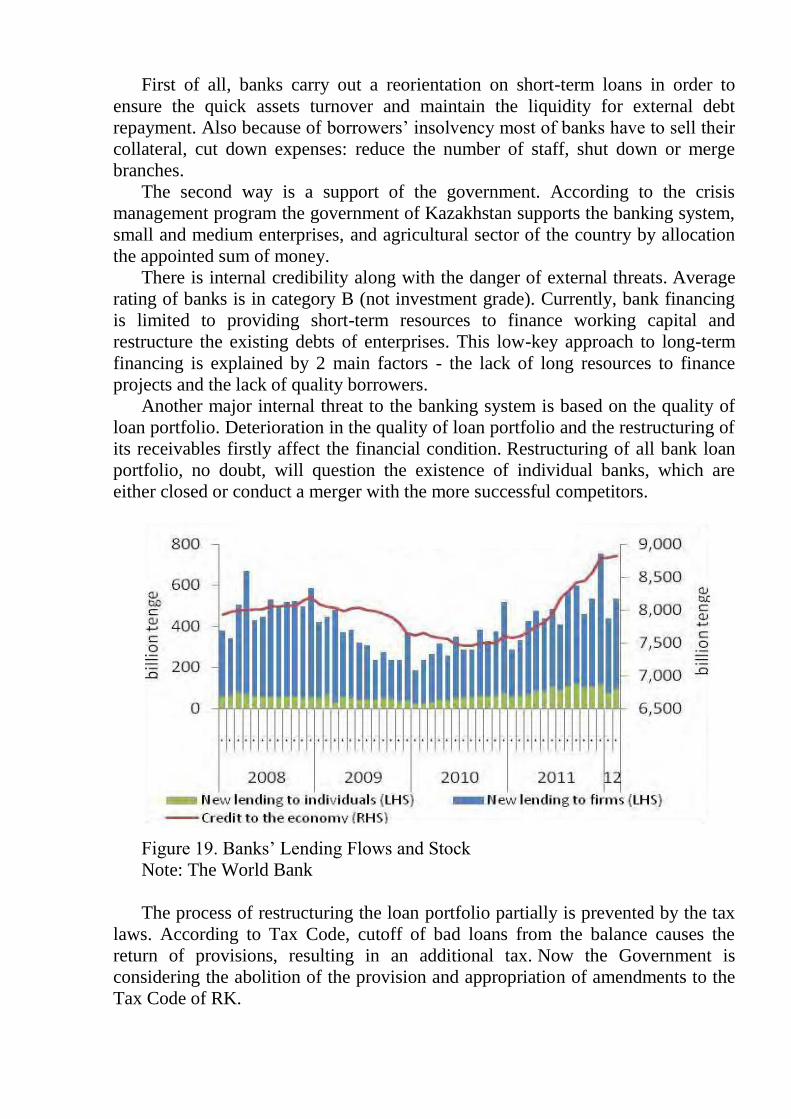

First of all, banks carry out a reorientation on short-term loans in order to

ensure the quick assets turnover and maintain the liquidity for external debt

repayment. Also because of borrowers’ insolvency most of banks have to sell their

collateral, cut down expenses: reduce the number of staff, shut down or merge

branches.

The second way is a support of the government. According to the crisis

management program the government of Kazakhstan supports the banking system,

small and medium enterprises, and agricultural sector of the country by allocation

the appointed sum of money.

There is internal credibility along with the danger of external threats. Average

rating of banks is in category B (not investment grade). Currently, bank financing

is limited to providing short-term resources to finance working capital and

restructure the existing debts of enterprises. This low-key approach to long-term

financing is explained by 2 main factors - the lack of long resources to finance

projects and the lack of quality borrowers.

Another major internal threat to the banking system is based on the quality of

loan portfolio. Deterioration in the quality of loan portfolio and the restructuring of

its receivables firstly affect the financial condition. Restructuring of all bank loan

portfolio, no doubt, will question the existence of individual banks, which are

either closed or conduct a merger with the more successful competitors.

Figure 19. Banks’ Lending Flows and Stock

Note: The World Bank

The process of restructuring the loan portfolio partially is prevented by the tax

laws. According to Tax Code, cutoff of bad loans from the balance causes the

return of provisions, resulting in an additional tax. Now the Government is

considering the abolition of the provision and appropriation of amendments to the

Tax Code of RK.

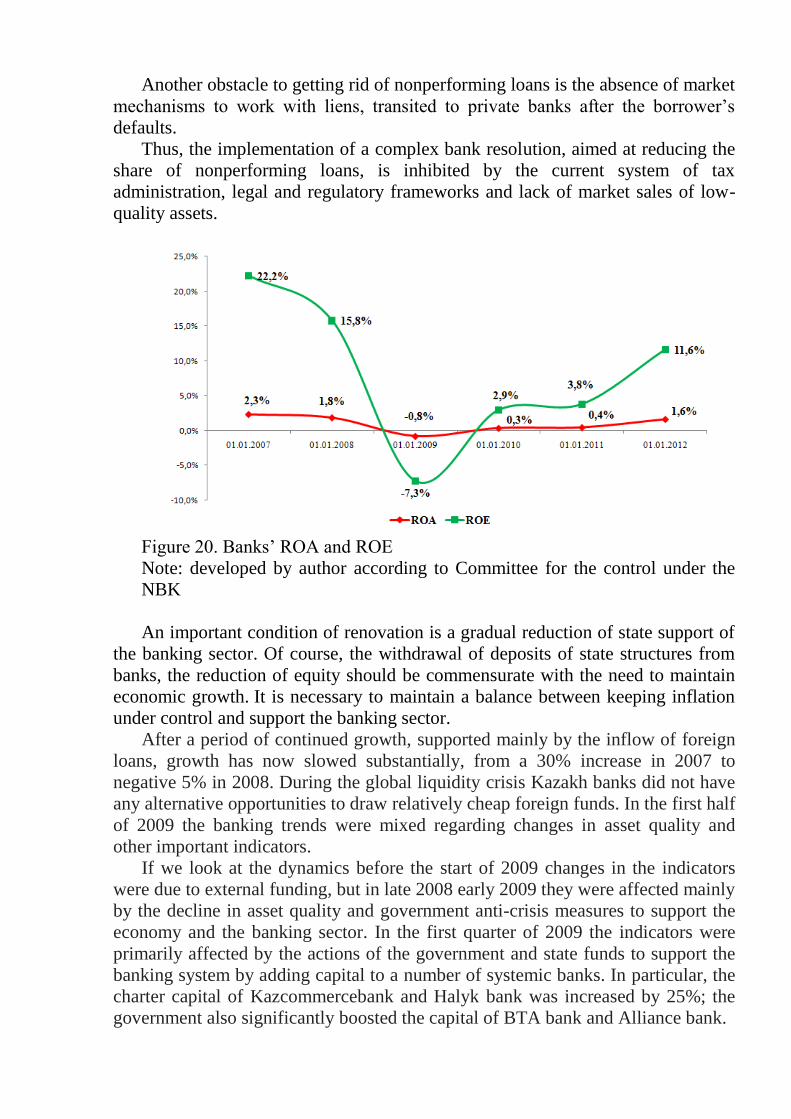

Another obstacle to getting rid of nonperforming loans is the absence of market

mechanisms to work with liens, transited to private banks after the borrower’s

defaults.

Thus, the implementation of a complex bank resolution, aimed at reducing the

share of nonperforming loans, is inhibited by the current system of tax

administration, legal and regulatory frameworks and lack of market sales of low-

quality assets.

Figure 20. Banks’ ROA and ROE

Note: developed by author according to Committee for the control under the

NBK

An important condition of renovation is a gradual reduction of state support of

the banking sector. Of course, the withdrawal of deposits of state structures from

banks, the reduction of equity should be commensurate with the need to maintain

economic growth. It is necessary to maintain a balance between keeping inflation

under control and support the banking sector.

After a period of continued growth, supported mainly by the inflow of foreign

loans, growth has now slowed substantially, from a 30% increase in 2007 to

negative 5% in 2008. During the global liquidity crisis Kazakh banks did not have

any alternative opportunities to draw relatively cheap foreign funds. In the first half

of 2009 the banking trends were mixed regarding changes in asset quality and

other important indicators.

If we look at the dynamics before the start of 2009 changes in the indicators

were due to external funding, but in late 2008 early 2009 they were affected mainly

by the decline in asset quality and government anti-crisis measures to support the

economy and the banking sector. In the first quarter of 2009 the indicators were

primarily affected by the actions of the government and state funds to support the

banking system by adding capital to a number of systemic banks. In particular, the

charter capital of Kazcommercebank and Halyk bank was increased by 25%; the

government also significantly boosted the capital of BTA bank and Alliance bank.

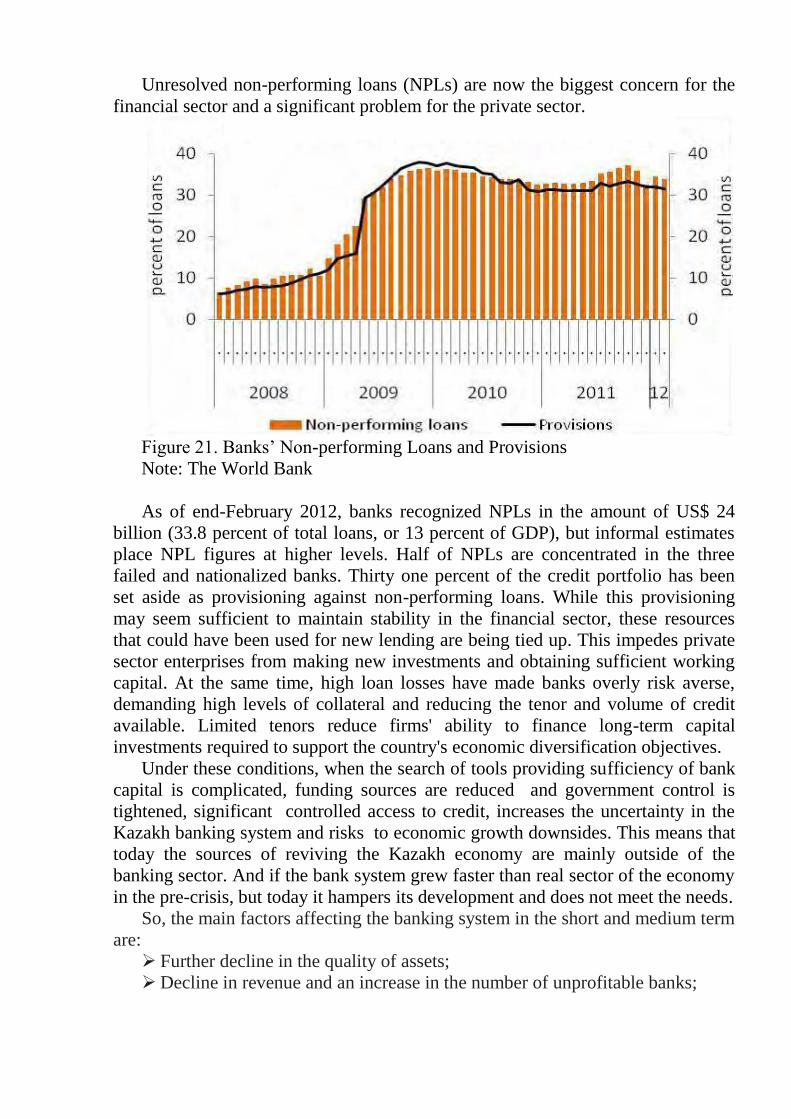

Unresolved non-performing loans (NPLs) are now the biggest concern for the

financial sector and a significant problem for the private sector.

Figure 21. Banks’ Non-performing Loans and Provisions

Note: The World Bank

As of end-February 2012, banks recognized NPLs in the amount of US$ 24

billion (33.8 percent of total loans, or 13 percent of GDP), but informal estimates

place NPL figures at higher levels. Half of NPLs are concentrated in the three

failed and nationalized banks. Thirty one percent of the credit portfolio has been

set aside as provisioning against non-performing loans. While this provisioning

may seem sufficient to maintain stability in the financial sector, these resources

that could have been used for new lending are being tied up. This impedes private

sector enterprises from making new investments and obtaining sufficient working

capital. At the same time, high loan losses have made banks overly risk averse,

demanding high levels of collateral and reducing the tenor and volume of credit

available. Limited tenors reduce firms' ability to finance long-term capital

investments required to support the country's economic diversification objectives.

Under these conditions, when the search of tools providing sufficiency of bank

capital is complicated, funding sources are reduced and government control is

tightened, significant controlled access to credit, increases the uncertainty in the

Kazakh banking system and risks to economic growth downsides. This means that

today the sources of reviving the Kazakh economy are mainly outside of the

banking sector. And if the bank system grew faster than real sector of the economy

in the pre-crisis, but today it hampers its development and does not meet the needs.

So, the main factors affecting the banking system in the short and medium term

are:

Further decline in the quality of assets;

Decline in revenue and an increase in the number of unprofitable banks;

Less interest from foreign investors in Kazakhstan’s banking system due to

the fact that a number of banks stopped making payments on external liabilities

and started restructuring;

Growth of risks due to noneconomic regulation of the banking system from

the government.

To counter the phenomena of bank stagnation must change their business

model and follow reforming directions:

Conducting upgrade (modernization, renovation, re-evaluation) of the

business model of banking activities. Adaptation principles should be established

in business model, continuously evaluating in compliance with the new economic

conditions.

Development of new strategies to reach markets. Optimization requires the

presence in the markets of different banking products and (or) services, expanding

their range and increase market supply, including at regional level.

Optimization of operational flexibility. Necessary to increase the efficiency

of banking due to the flexibility of the structure and optimal use of resources, the

use of LIN-approach (lean production, the philosophy of "lean production") to

create a new operating system.

Improving the quality of risk management process. It should change the

quality of implementation of the regulatory requirements set market risk

assessment and develop a robust integrated system of internal control and

planning.

Optimizing access to sources of funding and location. The growing