B428 Real Estate B428 Real Estate Day 5 Day 5 Leases, Income Tax, 1031 Leases, Income Tax, 1031 Exchanges, Lending and Exchanges, Lending and Borrowing Borrowing

B428 Real Estate Day 5 Leases, Income Tax, 1031 Exchanges, Lending and Borrowing.

Dec 28, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

B428 Real EstateB428 Real Estate

Day 5Day 5Leases, Income Tax, 1031 Leases, Income Tax, 1031 Exchanges, Lending and Exchanges, Lending and

BorrowingBorrowing

Environmental WarningEnvironmental Warning

Responsible parties liable:Responsible parties liable:Parties who arranged disposalParties who arranged disposal

Parties who transportedParties who transported

Prior ownerPrior owner

Current ownerCurrent owner

LiabilityLiabilityAll costs of removal, restorationAll costs of removal, restoration

costs of private partiescosts of private parties

damagesdamages

health costs related to contamination health costs related to contamination

Mechanics LiensMechanics Liens

Who?Who?

How?How?

Duration?Duration?

Income Tax IssuesIncome Tax Issues

Purchase and Sale of PropertyPurchase and Sale of Property• Capital asset?Capital asset?• Gain or loss?Gain or loss?

Income Tax continuedIncome Tax continued

OwnershipOwnership• DepreciationDepreciation• Passive incomePassive income• Passive lossPassive loss

Review of Income Tax AspectsReview of Income Tax Aspects

Real estate must qualify as a capital Real estate must qualify as a capital asset to get capital gains treatment.asset to get capital gains treatment.

Sales by dealers do not get capital Sales by dealers do not get capital gains treatment.gains treatment.• Inventory and real estate used in Inventory and real estate used in

taxpayer’s trade or business aren’t taxpayer’s trade or business aren’t capital assetcapital asset

• Possible tests: frequency of sales, Possible tests: frequency of sales, subdividing, promotional activitiessubdividing, promotional activities

Holding period is one year.Holding period is one year.

Intro to LeasesIntro to Leases

Lease Durations: How long do they Lease Durations: How long do they last?last?• Houses and apartments, month to month, Houses and apartments, month to month,

annualannual• Office space, 3 – 5 years (What about Office space, 3 – 5 years (What about

renewals)renewals)• Retail, small- 1-2 years, malls 10 to 20 Retail, small- 1-2 years, malls 10 to 20

yearsyears• Industrial, 3 -5 yearsIndustrial, 3 -5 years• Ground LeasesGround Leases

Income Tax MattersIncome Tax Matters

Taxable IncomeTaxable Income

NOI-Interest-DepreciationNOI-Interest-Depreciation

Cash Flow does not equal Taxable Cash Flow does not equal Taxable IncomeIncome

Sale of PropertySale of Property

Sales PriceSales Price

LESSLESS

Adjusted Basis =Adjusted Basis =

Taxable GainTaxable Gain

Passive Loss LimitationsPassive Loss Limitations

Taxpayer may not offset passive losses Taxpayer may not offset passive losses

against other income.against other income.

Exceptions for RE InvestorsExceptions for RE Investors

Individual rental property ownersIndividual rental property owners

RE professionals, material RE professionals, material involvementinvolvement

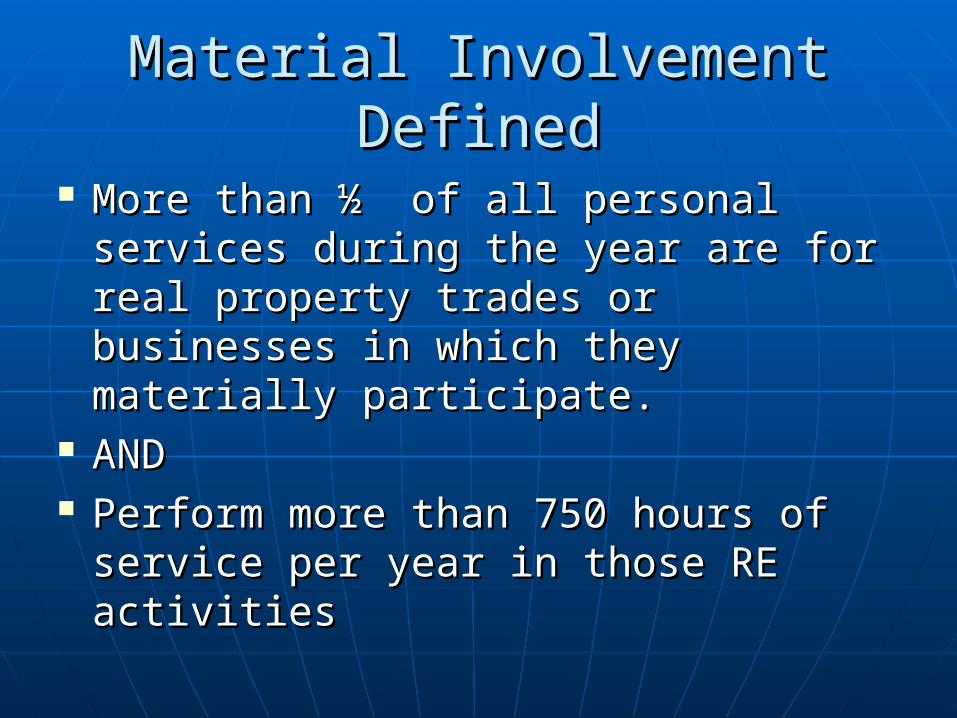

Material Involvement DefinedMaterial Involvement Defined

More than ½ of all personal services More than ½ of all personal services during the year are for real property during the year are for real property trades or businesses in which they trades or businesses in which they materially participate.materially participate.

ANDAND Perform more than 750 hours of Perform more than 750 hours of

service per year in those RE activitiesservice per year in those RE activities

Tenant DepositsTenant Deposits

RENTRENT

OROR

SECURITYSECURITY

Common Area ChargesCommon Area Charges

Charged for the use of space “in Charged for the use of space “in common” with otherscommon” with others

Examples: Hallways, parking, Examples: Hallways, parking, recreation, landscaping, reception recreation, landscaping, reception areasareas

Lease ProvisionsLease Provisions

Base RentBase Rent Step-up ProvisionsStep-up Provisions

• Increase in costs (management, Increase in costs (management, maintenance…)maintenance…)

• Specific IndexSpecific Index

Most commonly, the CPI (Consumer Price Most commonly, the CPI (Consumer Price Index)Index)

Lease Provisions Continued…Lease Provisions Continued…

Percentage RentsPercentage Rents Net LeaseNet Lease Limitations on Assignment and SublettingLimitations on Assignment and Subletting Destruction of PremisesDestruction of Premises Insurance of Premises and ContentsInsurance of Premises and Contents Options to renewOptions to renew Options to purchaseOptions to purchase

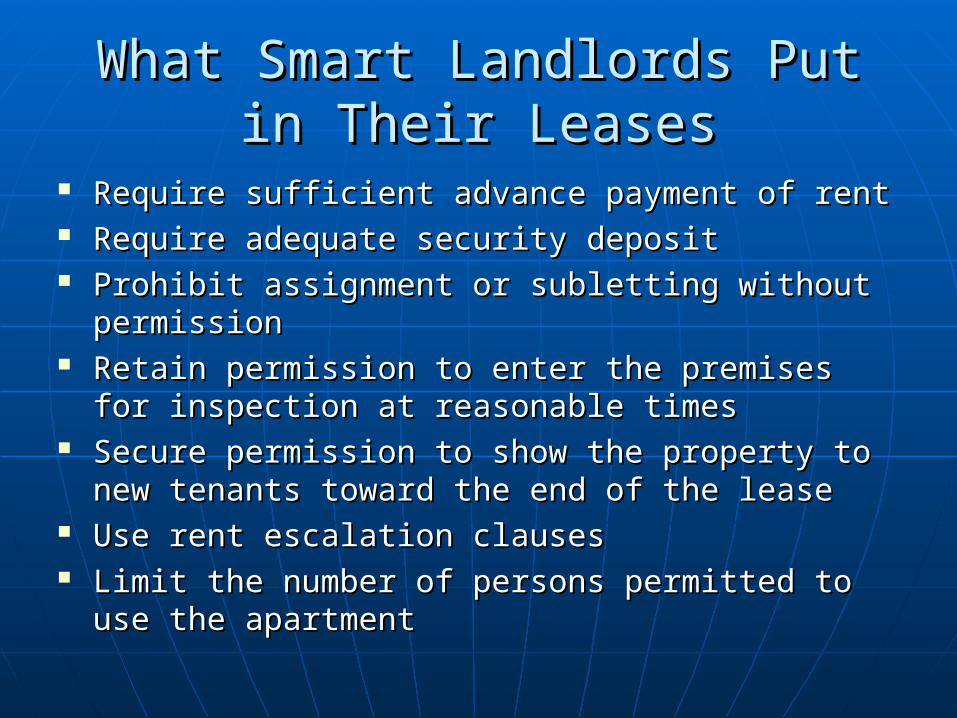

What Smart Landlords Put in Their What Smart Landlords Put in Their LeasesLeases

Require sufficient advance payment of rentRequire sufficient advance payment of rent Require adequate security depositRequire adequate security deposit Prohibit assignment or subletting without Prohibit assignment or subletting without

permissionpermission Retain permission to enter the premises for Retain permission to enter the premises for

inspection at reasonable timesinspection at reasonable times Secure permission to show the property to new Secure permission to show the property to new

tenants toward the end of the leasetenants toward the end of the lease Use rent escalation clausesUse rent escalation clauses Limit the number of persons permitted to use the Limit the number of persons permitted to use the

apartmentapartment

Smart Landlords continued…Smart Landlords continued…

• Use percentage leases on commercial Use percentage leases on commercial property to permit participation in profits property to permit participation in profits of the tenantof the tenant

• Require the tenant to make repairs and do Require the tenant to make repairs and do maintenancemaintenance

• Have regulations or rules for the benefit of Have regulations or rules for the benefit of all tenantsall tenants

• Avoid exclusion clauses which limit the L’s Avoid exclusion clauses which limit the L’s ability to lease remainder of the propertyability to lease remainder of the property

Termination of LeasesTermination of Leases

Expiration of LeaseExpiration of Lease Mutual AgreementMutual Agreement Breach of the Lease (Default)Breach of the Lease (Default) Eviction (Unlawful Detainer)Eviction (Unlawful Detainer) Constructive EvictionConstructive Eviction

• Is there a statute?Is there a statute?• Rent abatementRent abatement

Unlawful DetainerUnlawful Detainer

The BasicsThe Basics DefinitionDefinition ProcedureProcedure

• Three day noticeThree day notice• Service of noticeService of notice• Action for possessionAction for possession• EnforcementEnforcement

Tax Deferred ExchangeTax Deferred Exchange

Section 1031 IRCSection 1031 IRC• Both properties (relinquished and acquired) must be Both properties (relinquished and acquired) must be

held for business or investment purposes.held for business or investment purposes.• Must be like-kind.Must be like-kind.• Exchange must actually occur.Exchange must actually occur.• Basis in acquired property equal to basis in relinquished Basis in acquired property equal to basis in relinquished

property plus any “boot.”property plus any “boot.”

BOOTBOOT

Boot is a general term for property in Boot is a general term for property in an exchange which is not like-kind.an exchange which is not like-kind.

• Boot is taxableBoot is taxable

• Boot is not limited to cashBoot is not limited to cash

Two VariationsTwo Variations

Three Party ExchangesThree Party Exchanges

Delayed ExchangesDelayed Exchanges• Owner of relinquished property identifies replacement Owner of relinquished property identifies replacement

property within 45 days of transfer.property within 45 days of transfer.

• Exchange is completed using a third party specialist within Exchange is completed using a third party specialist within 180 days or due date of tax return, whichever sooner180 days or due date of tax return, whichever sooner

• Owner of relinquished property must not receive the Owner of relinquished property must not receive the proceeds from the relinquished property.proceeds from the relinquished property.

The Final TestThe Final Test

IssueIssue

Rule Rule

AnalysisAnalysis

ConclusionConclusion

Related Documents