GULF COAST FOOD & FUEL EXPO BEAU RIVAGE RESORT & CASINO BILOXI, MISSISSIPPI MARCH 11-12, 2015

B EAU R IVAGE R ESORT & C ASINO B ILOXI, M ISSISSIPPI M ARCH 11-12, 2015.

Dec 17, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

GULF COAST FOOD & FUEL EXPO

BEAU RIVAGE RESORT & CASINOBILOXI, MISSISSIPPI

MARCH 11-12, 2015

Credit Card Proceeds – Are They Yours Or May They Be Levied By The

IRS?

Alphonse M. Alfano, EsquireBassman, Mitchell & Alfano, Chartered

March 11, 2015

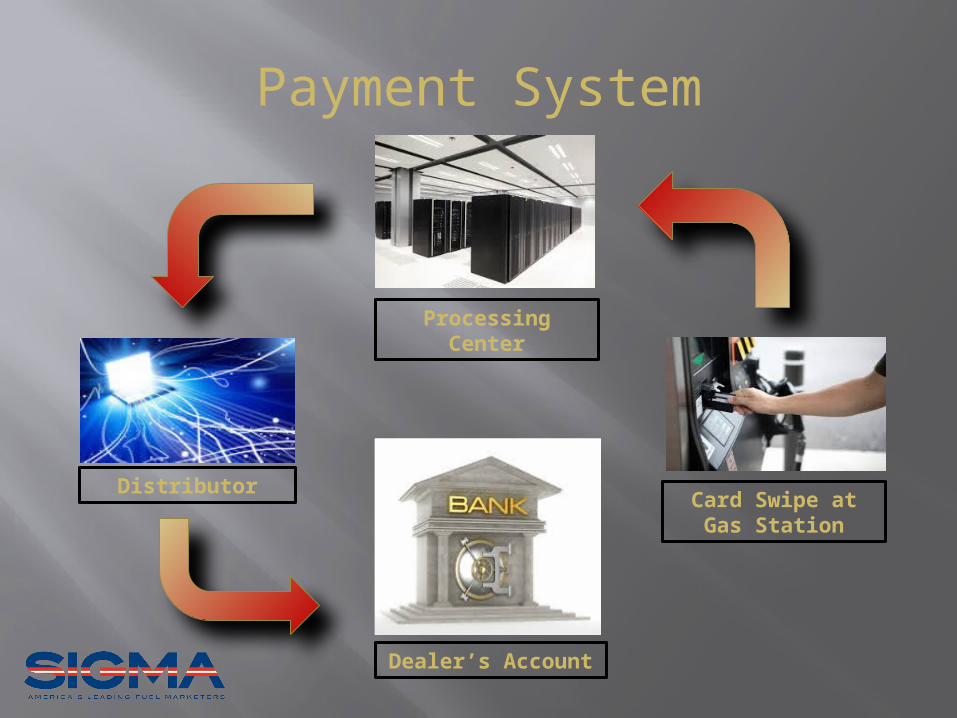

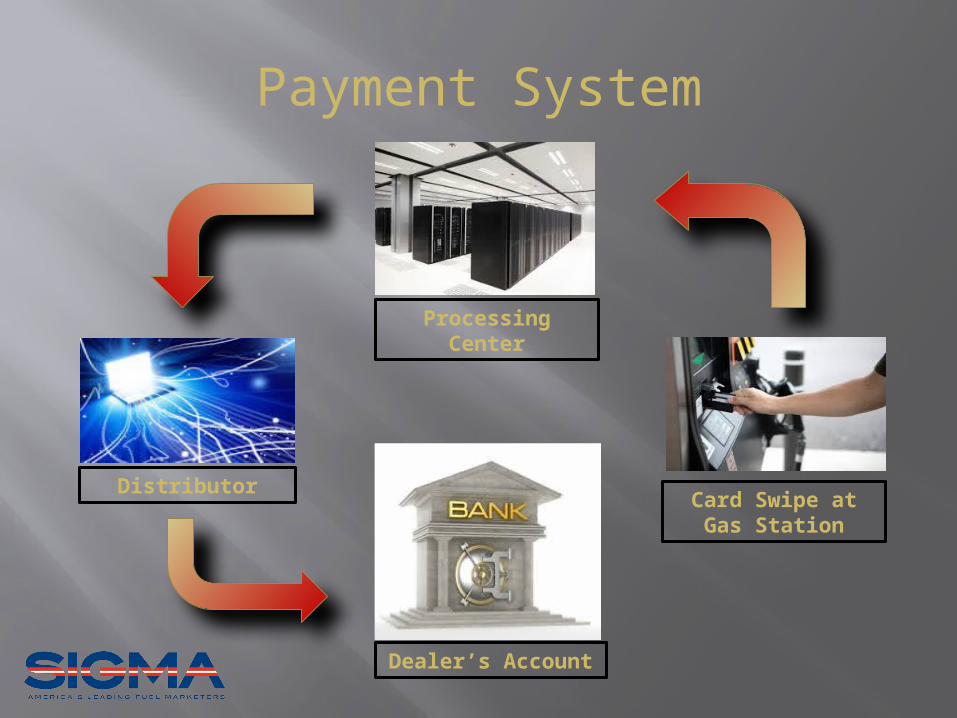

Processing Center

Distributor

Dealer’s Account

Card Swipe at Gas Station

Payment System

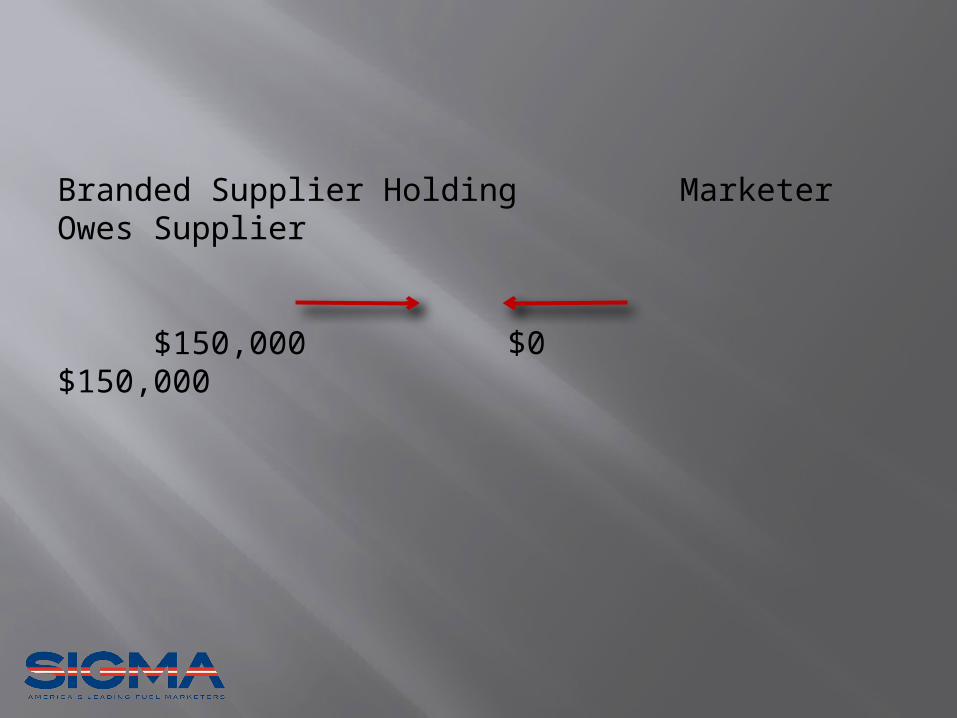

Branded Supplier Holding Marketer Owes Supplier

$150,000 $0 $150,000

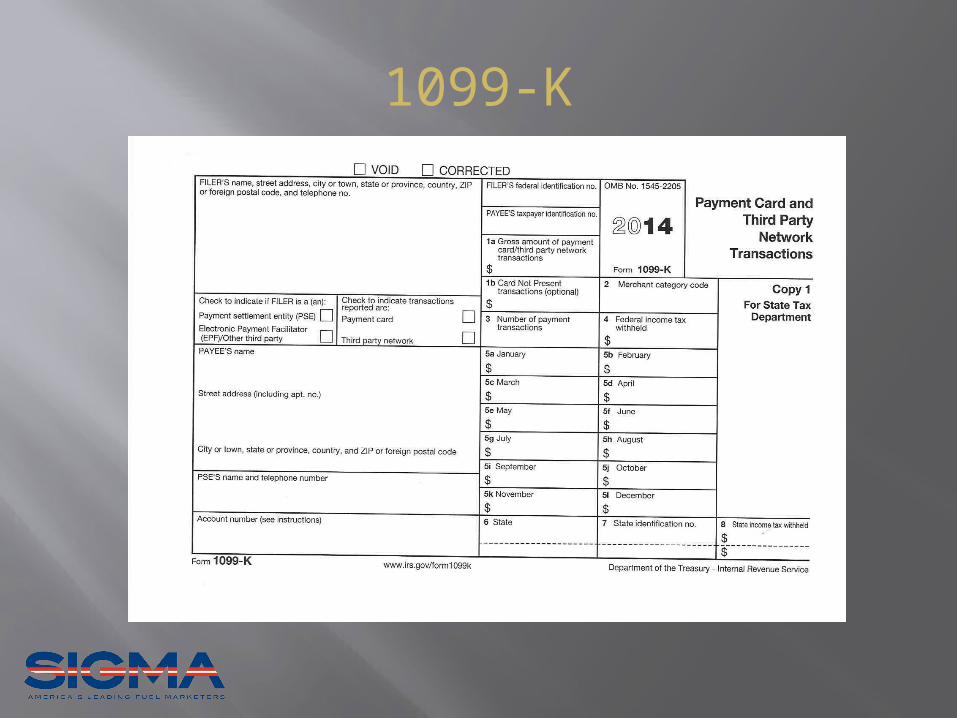

1099-K

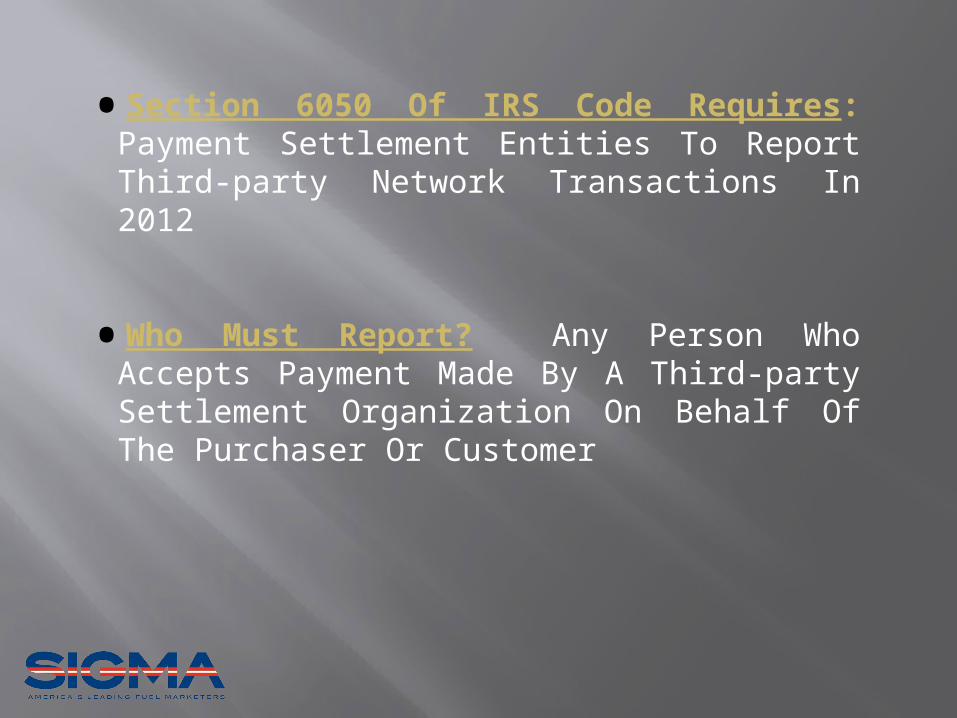

• Section 6050 Of IRS Code Requires: Payment Settlement Entities To Report Third-party Network Transactions In 2012

• Who Must Report? Any Person Who Accepts Payment Made By A Third-party Settlement Organization On Behalf Of The Purchaser Or Customer

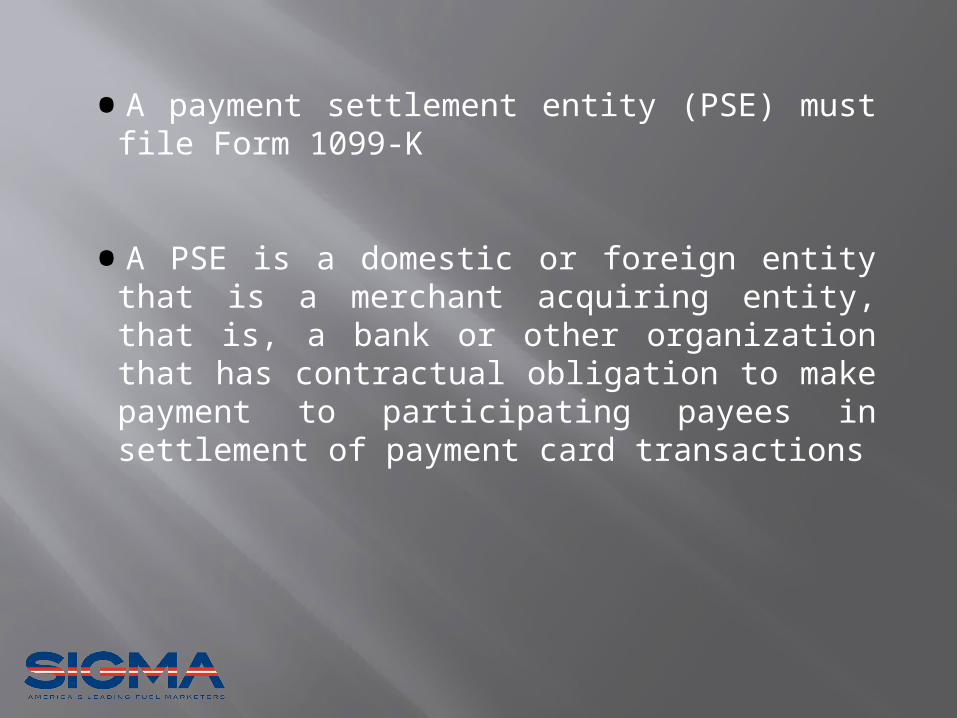

• A payment settlement entity (PSE) must file Form 1099-K

• A PSE is a domestic or foreign entity that is a merchant acquiring entity, that is, a bank or other organization that has contractual obligation to make payment to participating payees in settlement of payment card transactions

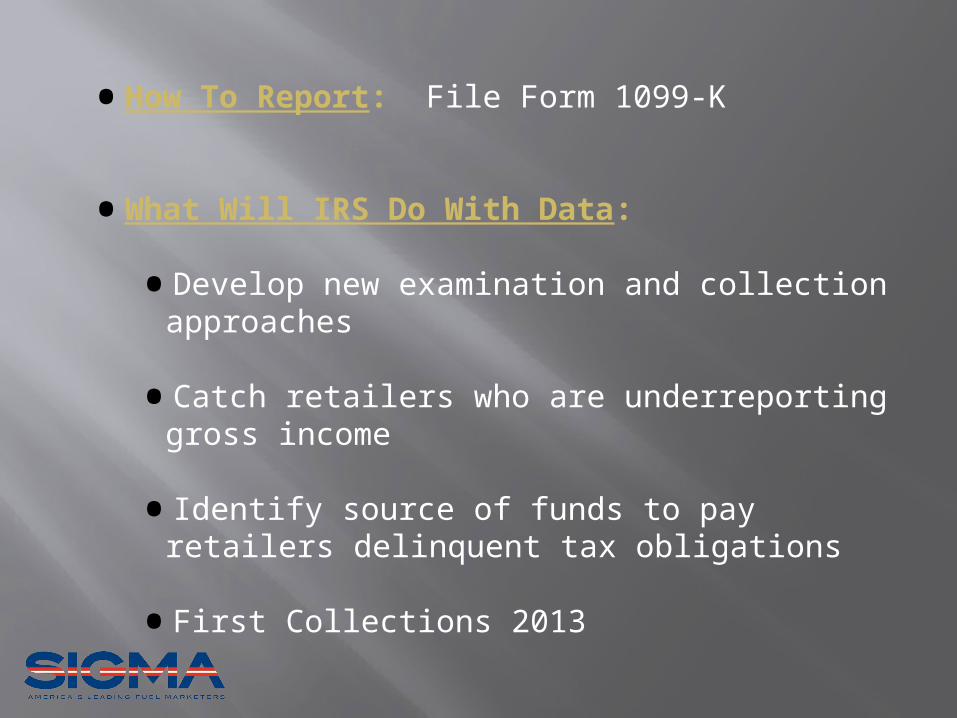

• How To Report: File Form 1099-K

• What Will IRS Do With Data:

• Develop new examination and collection approaches

• Catch retailers who are underreporting gross income

• Identify source of funds to pay retailers delinquent tax obligations

• First Collections 2013

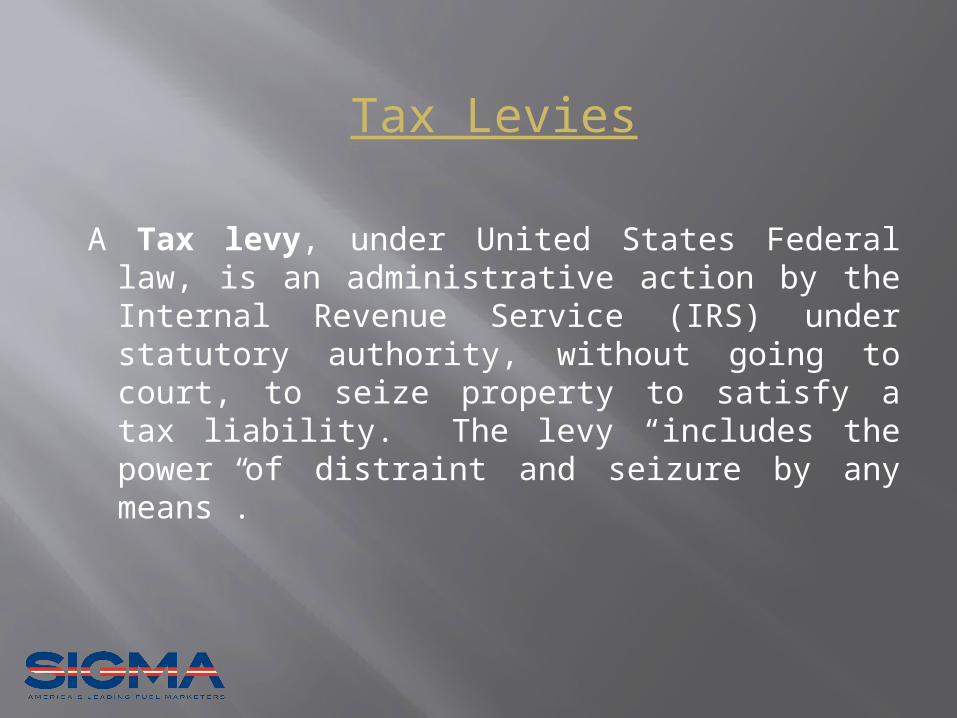

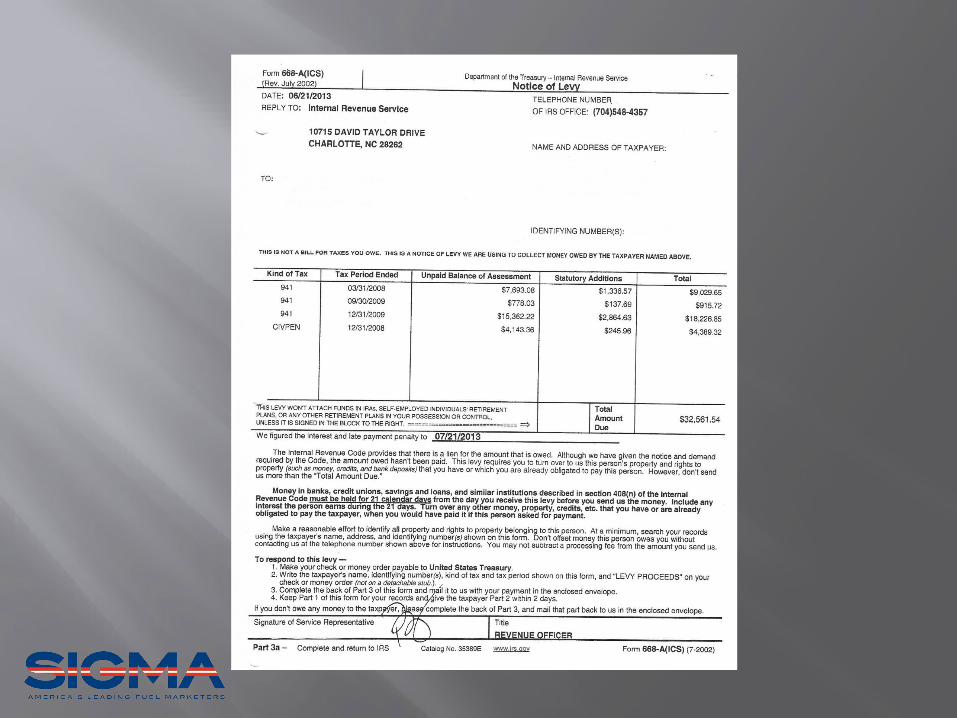

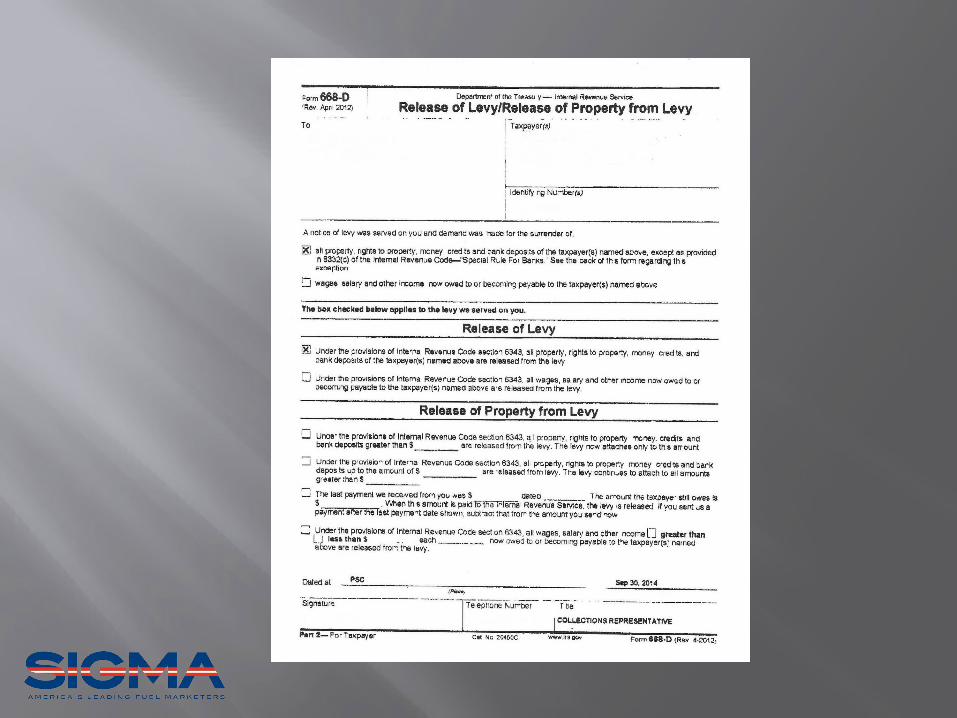

Tax Levies

A Tax levy, under United States Federal law, is an administrative action by the Internal Revenue Service (IRS) under statutory authority, without going to court, to seize property to satisfy a tax liability. The levy “includes the power of distraint and seizure by any means”.

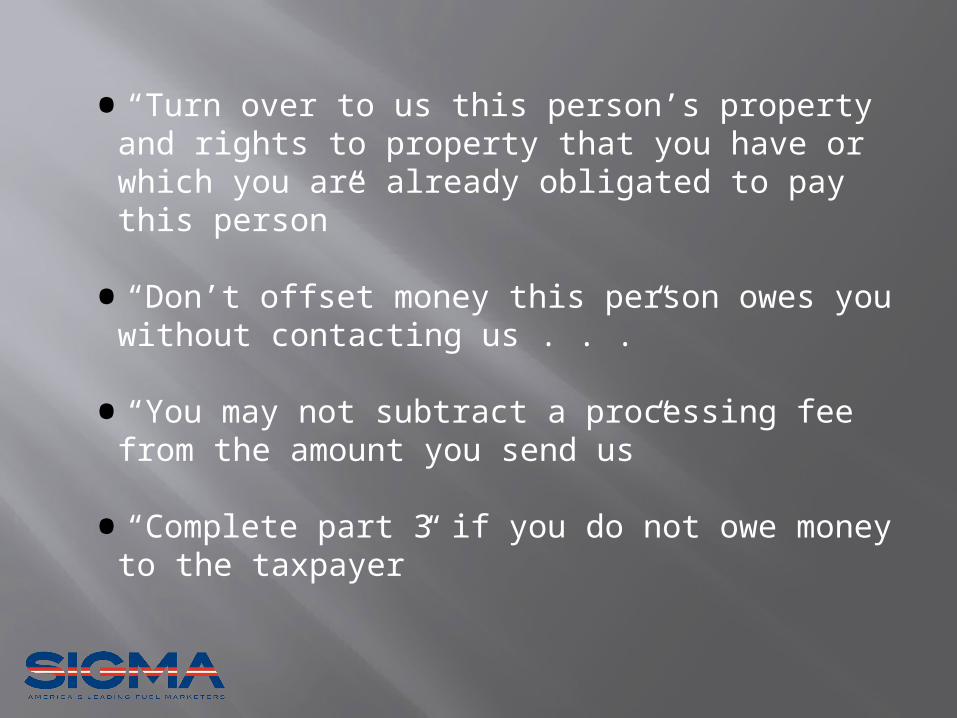

• “Turn over to us this person’s property and rights to property that you have or which you are already obligated to pay this person”

• “Don’t offset money this person owes you without contacting us . . .”

• “You may not subtract a processing fee from the amount you send us”

• “Complete part 3 if you do not owe money to the taxpayer”

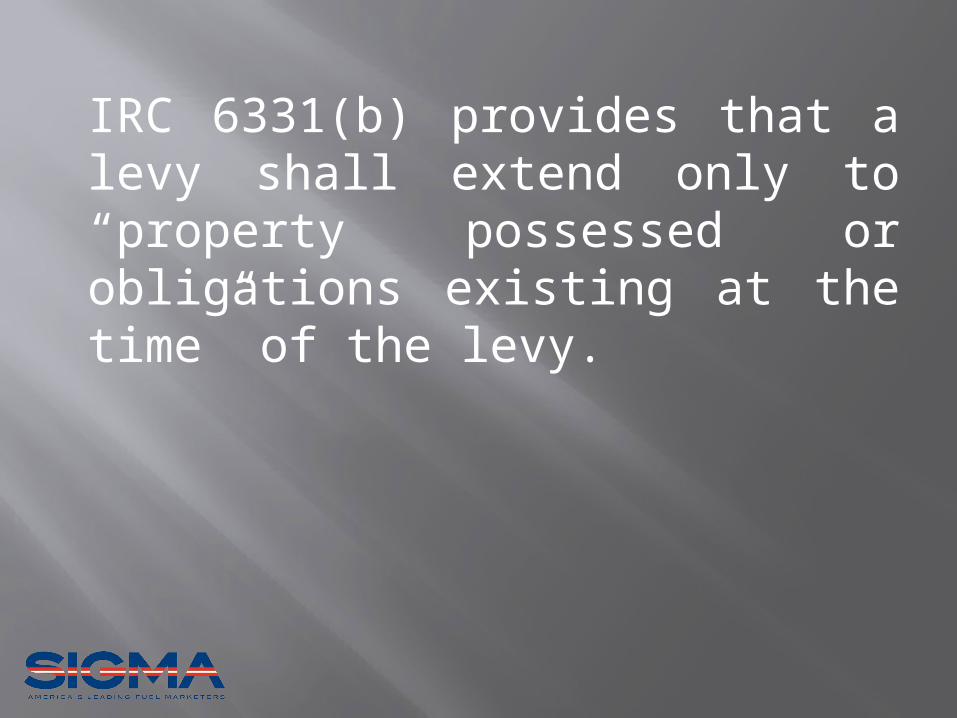

IRC 6331(b) provides that a levy shall extend only to “property possessed or obligations existing at the time” of the levy.

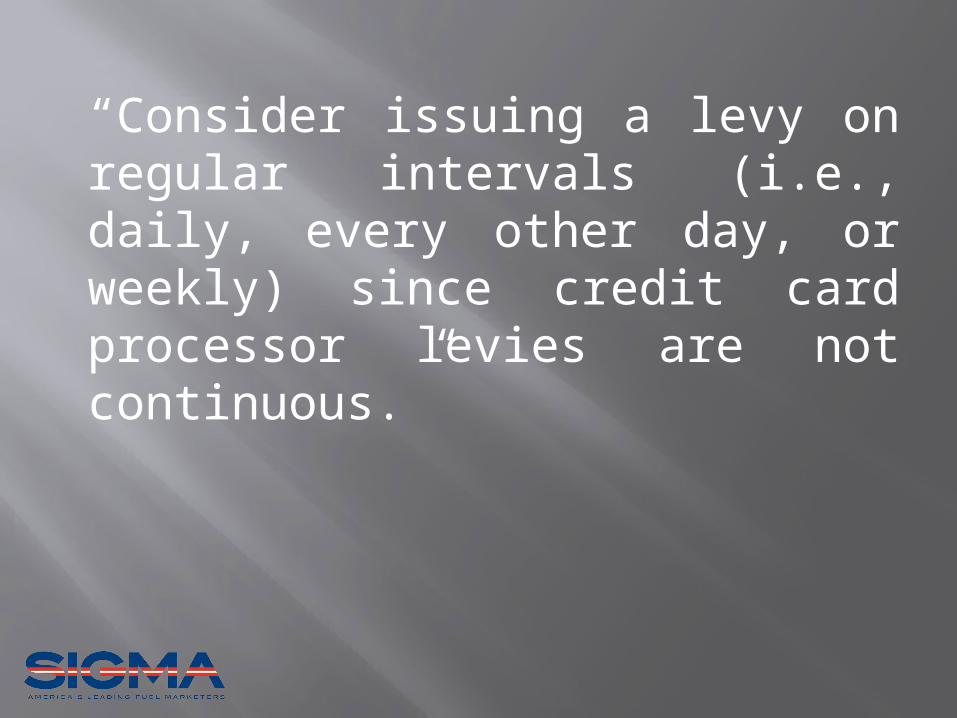

“Consider issuing a levy on regular intervals (i.e., daily, every other day, or weekly) since credit card processor levies are not continuous.”

•The funds held by processors and acquiring bank are not deposits within the meaning of IRC 6332(c), and the 21-day holding period does not apply to these funds.

•Payment is required when marketer would otherwise make payment

Levy Premised On

• Settlement Monies Are The Property Of The Dealer

Or

• Marketer Has A Contractual Obligation To Make Payment To The Dealer

• Set-off Before Receiving Levy Notice

Major Problem If Set Off Has Not Occurred

• Levy Notice Received November 11

• Dealer Owes For Two Loads ($60,000)

• Marketer Holding $40,000 In Settlement Monies

• $40,000 Paid To IRS

• Dealer Lacks Cash To Pay The Account Balance

Processing Center

Distributor

Dealer’s Account

Card Swipe at Gas Station

Payment System

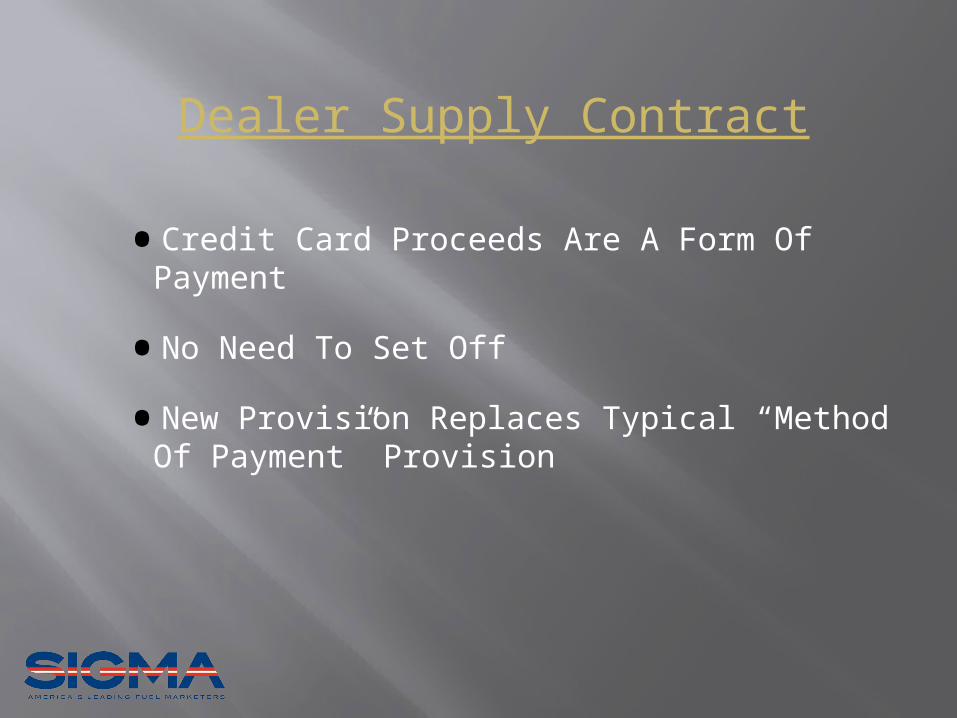

Dealer Supply Contract

• Credit Card Proceeds Are A Form Of Payment

• No Need To Set Off

• New Provision Replaces Typical “Method Of Payment” Provision

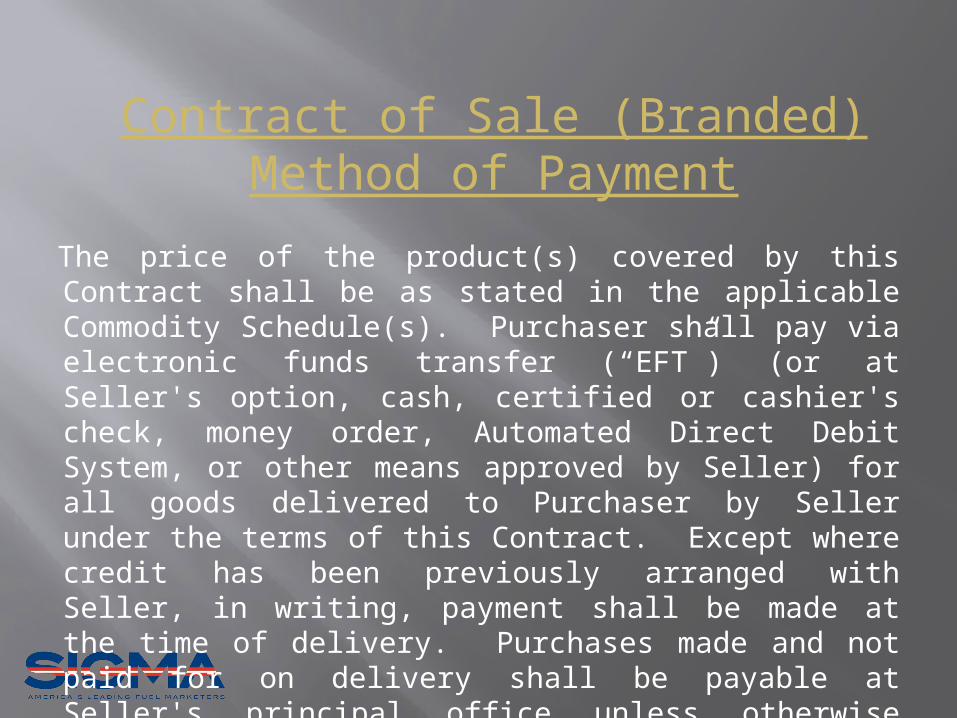

Contract of Sale (Branded)Method of Payment

The price of the product(s) covered by this Contract shall be as stated in the applicable Commodity Schedule(s). Purchaser shall pay via electronic funds transfer (“EFT”) (or at Seller's option, cash, certified or cashier's check, money order, Automated Direct Debit System, or other means approved by Seller) for all goods delivered to Purchaser by Seller under the terms of this Contract. Except where credit has been previously arranged with Seller, in writing, payment shall be made at the time of delivery. Purchases made and not paid for on delivery shall be payable at Seller's principal office unless otherwise specified by Seller.

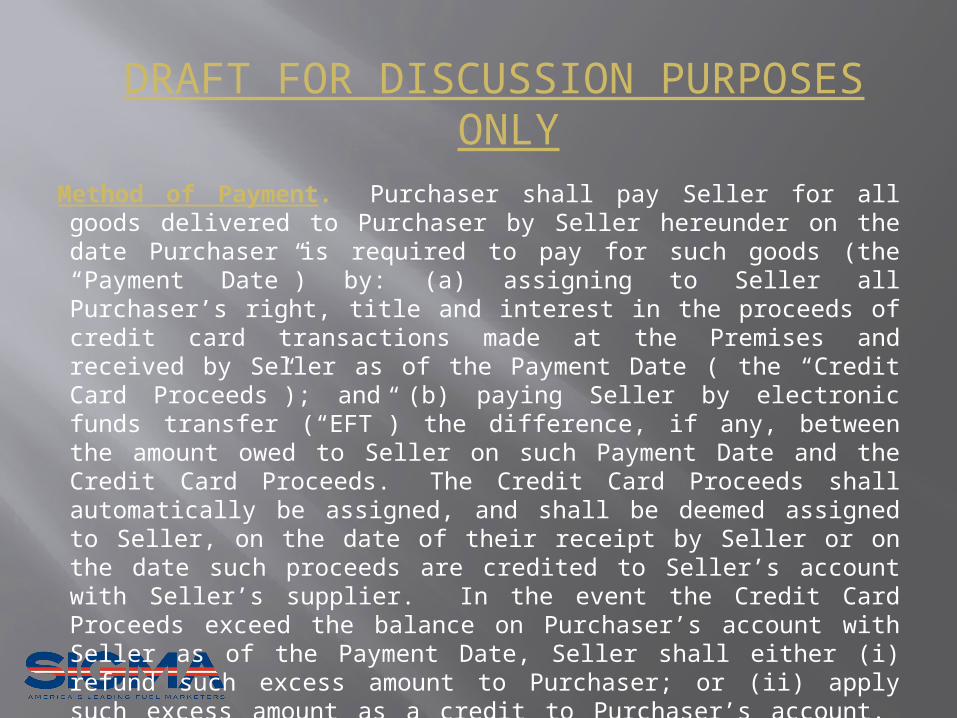

DRAFT FOR DISCUSSION PURPOSES ONLY

Method of Payment. Purchaser shall pay Seller for all goods delivered to Purchaser by Seller hereunder on the date Purchaser is required to pay for such goods (the “Payment Date”) by: (a) assigning to Seller all Purchaser’s right, title and interest in the proceeds of credit card transactions made at the Premises and received by Seller as of the Payment Date ( the “Credit Card Proceeds”); and (b) paying Seller by electronic funds transfer (“EFT”) the difference, if any, between the amount owed to Seller on such Payment Date and the Credit Card Proceeds. The Credit Card Proceeds shall automatically be assigned, and shall be deemed assigned to Seller, on the date of their receipt by Seller or on the date such proceeds are credited to Seller’s account with Seller’s supplier. In the event the Credit Card Proceeds exceed the balance on Purchaser’s account with Seller as of the Payment Date, Seller shall either (i) refund such excess amount to Purchaser; or (ii) apply such excess amount as a credit to Purchaser’s account. For the avoidance of doubt, the assignment of the Credit Card Proceeds shall be a form of payment for the goods sold hereunder and shall be the property of Seller, provided that Seller shall be obligated to reimburse Purchaser for any amount by which the Credit Card Proceeds exceed Purchaser’s account balance on any Payment Date.

Related Documents