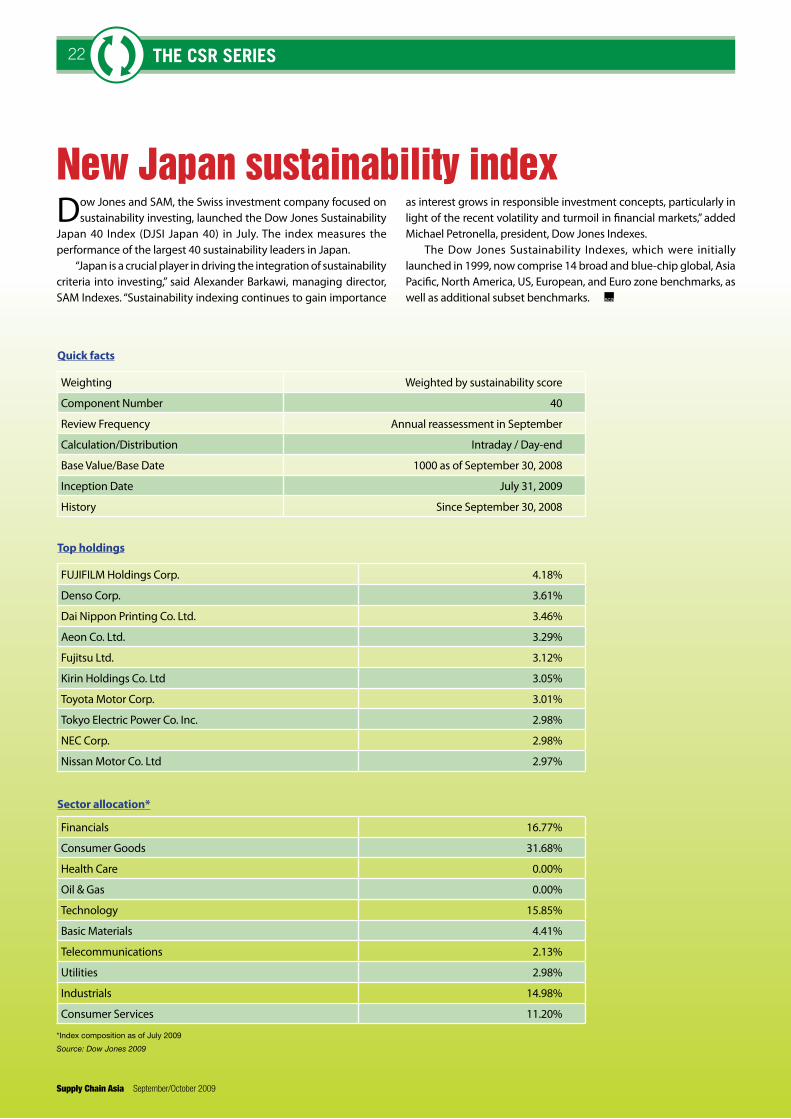

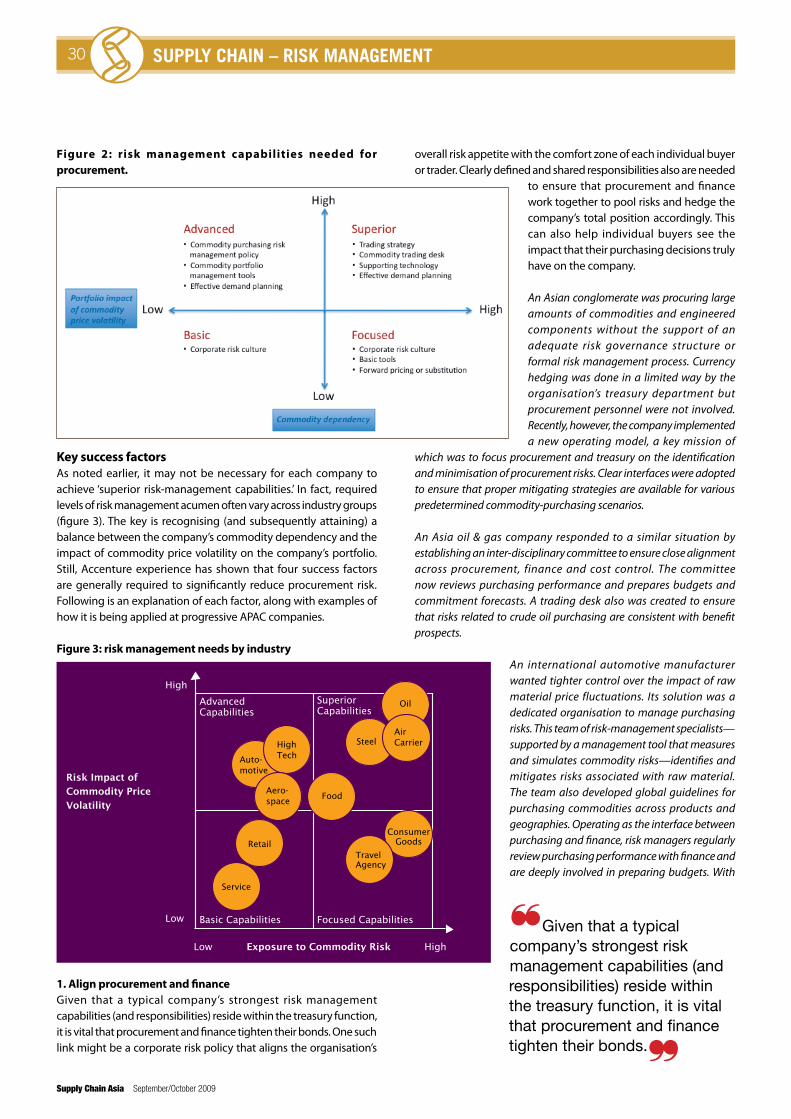

Supply Chain Asia Magazine September/October 2009 MICA(P) 036/02/2009 | SEP/OCT 2009 SUPPLY CHAIN ASIA magazine www.supplychainasia.com Connect • Communicate • Collaborate Awards 2009, The List of Finalists Procurement Tactics for volatile market conditions Air Cargo Beijing ups the ante in the north Asia hub game ISSN 1793 5377 SPEND anagement m sustainable $avings for Maritime Shippers choose ocean over TransSiberian Plus… Exposing the conflicts in service supply chains

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Supply Cha

in Asia

Magazine

Septem

ber/O

ctober 2

00

9

Mica(P) 036/02/2009 | SEP/OCT 2009

SupplY Chain aSiam

ag

azin

e

www.supplychainasia.comConnect • Communicate • Collaborate

Awards 2009, The List of Finalists

Procurement Tactics for volatile market conditions

Air Cargo Beijing ups the ante in the north Asia hub game

ISSN 1793 5377

SPendanagementm sustainable$avings

for

Maritime Shippers choose ocean

over TransSiberian

Plus…Exposing the conflicts in

service supply chains

SCAsiaContents

Editor’s View02 Time to rebalance

President’s Address04 Supply Chain Asia City

Dialogues

Developments6 Regional and global

supply chain news update

Air Cargo 8 Beijing ups the ante in

north Asia hub game

Maritime9 Shippers choose ocean

over TransSiberian

10 Work in progress — Shanghai’s ambitious targets

The CSR Series18 Structural change:

greener supply chain buildings

September/October 2009

521810

14On the Cover

Spend management for sustainable savings

36Chinese Section

Risk Management28 Tactics for procurement in

volatile market conditions

32 A uniform approach to global supply chain risk management

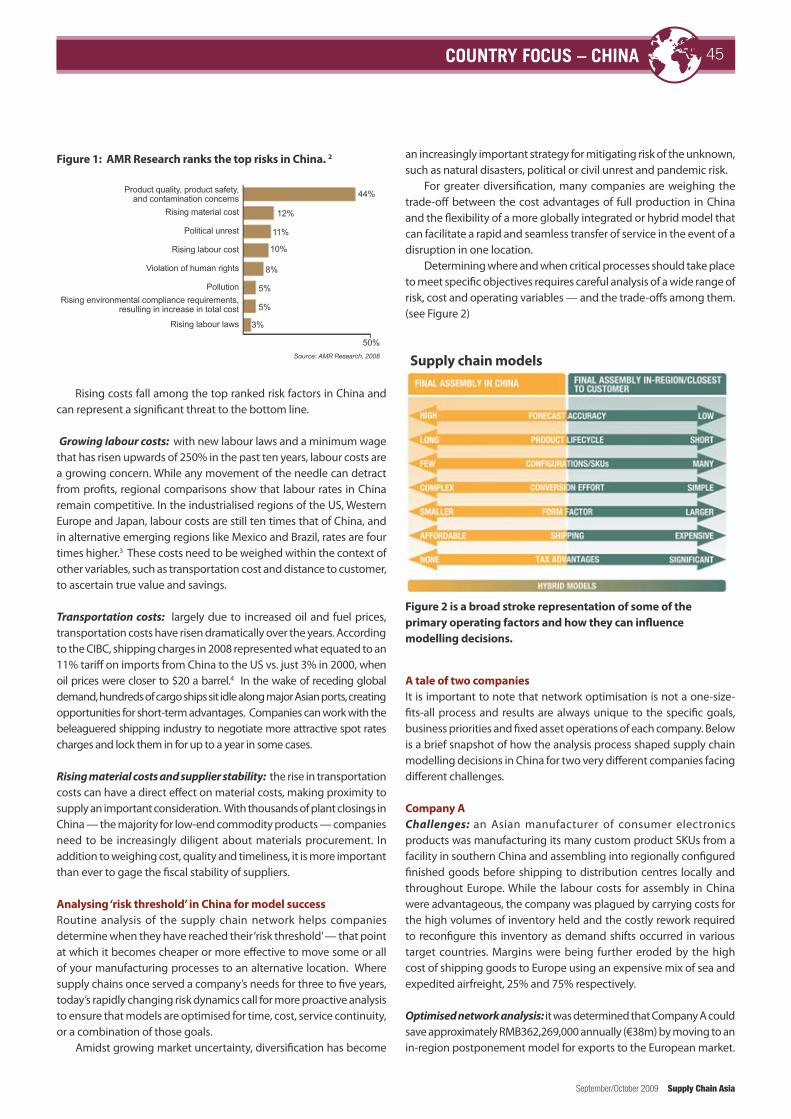

Country Focus – China44 Changing market

conditions bring new challenges for manufacturers

Reverse Supply Chains48 Creating sustainable high

performance service supply chains

Opinion52 The importance of supply

chain research to industry and society

56 What does ECR really stand for?

Regulars24 Awards 2009: the

finalists60 Lao Tze — when less

than 100% is good enough

62 Supply Chain Indicators

64 Blogs

14

To welcome your next supply chain opportunity, contact Craig Rawlings, [email protected].

Opportunity awaits

greenDot-Ads-door-190x60-draft3.indd 1 21/8/2009 10:15:50 AM

management team & support team

advisory CounCil members of supply Chain asia

editor’sview

Dr robert Yap (Founding Chairman)Chairman & CEO, YCH Group

Mr paul braDleY (Vice Chairman)Member, Global Advisory Board, Arshiya International

CounCil MeMbers

Mr MahenDra agarwalManaging Director & CEO, GATI

Mr neeraj bhargavaRegional Logistics Procurement Director,

Johnson & Johnson Asia Pacific

Mr vittorio FavatiPresident, Asia Pacific, CEVA Logistics

Mr allen FukaDaRegional Solutions Leader, Asia Pacific,

Supply Chain Management Services, IBM Business Process Delivery

associate proFessor Mark gohDirector, Industry Research,

The Logistics Institute Asia Pacific

Mr harrY lagaDIndependent

Mr richarD lorettoExecutive Director, Fashion and Home Asia Pacific Supply Chain,

AVON

Mr Mark MillarManaging Director, M Power Associates

Mr turloch MooneYManaging Director, SC Asia Publications

Mr peter o’ brienHead, Asia Pacific Supply Chain Practice,

Russell Reynolds Associates

Mr Michael proFFittStrategic Advisor/Consultant, Dubai Logistics City

Mr vivek sooDManaging Director, Global Supply Chain Group

Mr Mark wettasingheVice President, Value Added/Tech Services, DHL

publisherSC ASIA PuBLICATIONS PTE [email protected]

Managing direCtor, editorialTuRLOCH MOONEY

Managing direCtor, CoMMerCialFRANk PAuL

ContributorsPARI ANNAMALAI, RICHARD BRuBAkER, SAM CHAMBERS,

CHEW WAI YEE, OWEN CLEAVER, BARRY ELLIOTT, DR JOHN GATTORNA, PATRICIA GRACE, RYAN HuMPHREY,

PAuL LIM, CRAIG RAWLINGS, JEFFREY RuSSELL, CRYSTAL YAN

design & produCtionDESIGN WORkz

printingREGENT PRINTING (S) PTE LTD

Time to ‘rebalance’

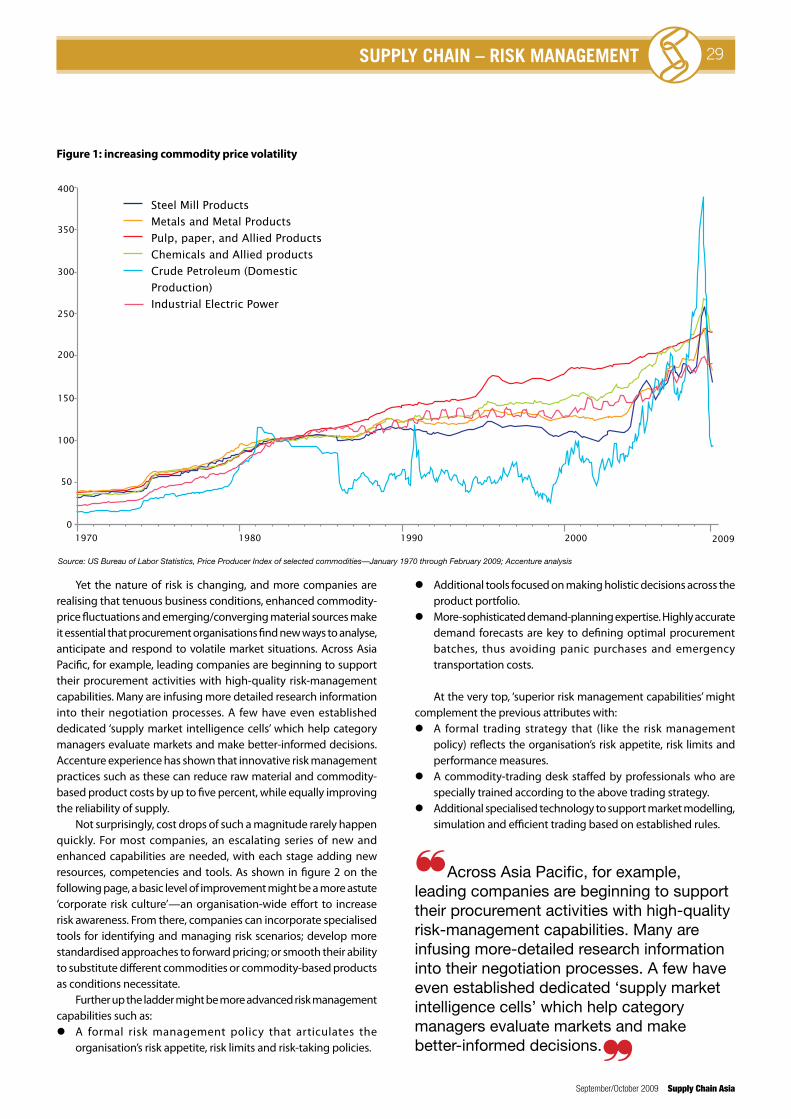

Over the course of this recession we have frequently looked at the potential of using supply chain management to drive positive change in organisations and business models. We have discussed how improved supply chain risk and security management systems, better supplier relations and sourcing and procurement strategies; even complete redesign of organisations and business operations around supply chain functions, can create healthier, higher performing companies and organisations. “Fix your supply chains and you fix the company” was the self-explanatory title of the contribution to our May/June issue from supply chain thought-leader Dr John Gattorna. In this issue – as part of a call for better research and understanding of the contribution of supply chain management and logistics to industry and society – he extends the idea from companies to national economies to regions.

The central and increasingly recognised role of supply chain and logistics systems and processes in the emergence of Asia, in terms of the transformation of its organisations and national economies, and integration of those with each other and with other parts of the global economy, is the rationale behind the set up and existence of Supply Chain Asia Magazine and its parent the Supply Chain Asia Community. As such, as we move through the second half of 2009 we have a sense of optimism, not only because more signs of recovery have been emerging, but because of the probability that this recession has helped to drive home the importance of the discipline of supply chain management and all its constituent parts to the health of organisations and national economies, and to the emergence of Asia. The frequent identification over the past year of supply chain management as a very effective channel to create more sustainable organisastions and economies is one good example.

Another good example comes from the new urgency on the part of the Chinese government to rebalance its economy (perhaps the most significant economic challenge to emerge from the recession on a regional level). As outlined in the Beijing government’s new logistics rejuvenation plan – released as part of the response to the recession – this is a task heavily dependant on getting a good basic logistics system in place throughout the country and ultimately ensuring the creation of efficient supply chain systems and processes to support the domestic economy.

This is a task we will be covering in detail in coming issues of Supply Chain Asia Magazine. In the meantime, we will also be carrying out some rebalancing of our own. Over the coming twelve months, the Supply Chain Asia Dialogues will be rolled out across the region (see President’s Message, overleaf). The goal of the dialogues is to extend the function of informing and supporting the development of the industry to individual Asian cities. At the same time, Supply Chain Asia Magazine will be gradually converted to a subscription-based publication. This is in line with growing demand for supply chain intelligence, analysis and thought-leadership among private companies, universities, government and consultants as the industry gains influence and importance.

We look forward to expanding our role as providers of the highest quality information on the development of the industry in Asia, and to continuing to provide front row seats to watch its emergence.

Turloch Mooney

Editor-in-Chief, Supply Chain Asia MagazineManaging Director, EditorialSC Asia Publications

agilitylogistics.com

WESTERN DIGITAL HAS FREDERICK ANTONY. Facing a surge in worldwide demand for their hard-drives, Western Digital asked Agility’s Frederick Antony to ramp up inventory velocity. With little lead time, he planned and executed a substantial expansion of their Malaysian distribution center that increased capacity, improved pallet position, and added the efficiencies of advanced tracking software. In doubling their output, Frederick showed the high-tech leader that he shares their passion for storage and speed.

WESTERN DIGITAL HAS AGILITY.

Frederick Antony Sr. Logistics Manager

Agility, Malaysia

Pub __________________________________Size: __________________________________Insertion: ______________________________

Agility Western Digital Ad r2

Prepared By Green Street AdsContact: John Espinoza626-644-8094

Supply Chain Asia210mm x 297mm Full Pg TrimAug 20, 2009

AGL-WDIG_ad_SupplyChainAsia.090820.indd 1 8/20/09 12:16:24 PM

supporting organisations

Corporate endorsers

Dear friends and readers,

On September 1 2009, we celebrate the fourth anniversary of Supply Chain Asia. Since the community was founded in 2005, we have been able to experience high growth and support and we want to thank each and every one of you for making this possible. Without you, there would be no Supply Chain Asia as there would be no community to serve.

As a community, our focus was never about the minute details of forming a formal structure comprised of by-laws and constitutions. However, we realised we could not function as an effective framework for the community without bringing like-minded people together to provide direction and support. The Advisory Council and Executive Committee were formed in early 2006 with this sole purpose in mind.

To date, we continue to maintain an informal structure with no formal election or campaigns that would distract us from our work in bringing connectivity and knowledge to community members. While this approach has many benefits, we are also aware of its shortcomings in terms of our ability to maintain a consistent and coordinated structure.

During our last annual EXCO meeting held the day before Supply Chain Asia Forum 2009, the Council and Executive Committee members deliberated over the work we have done for the past four years. It was felt strongly that the capacity to reach out to a wider physical audience through activities in other major cities in Asia would be an excellent complement to our already strong reach in both print and Internet media.

Taking the cue from the results of our discussions, the Council and Executive Committee members residing in each country have decided to take on the responsibility of hosting talks and dialogues in their cities of origins. In the next 12 months, we are targeting to host half-day talks and dialogues in major cities in Asia, including Kuala Lumpur (Malaysia), Surabaya (Indonesia), Mumbai (India), Shanghai (China), Tianjin (China), Taipei (Taiwan), Hong Kong, Sydney (Australia) and Bangkok (Thailand). More news on these dialogues and talks will be posted on our website.

Singapore will remain the host country for the annual Supply Chain Asia Forum and the next event will take place from August 24-27, 2010.

Again, we want to express our heartfelt gratitude for all your support in making Supply Chain Asia a viable entity today. We will continue our small work in bringing knowledge and connectivity through our platform in this magazine, the Internet, and through our talks, dialogues, forums and training initiatives.

Paul LimPresident, Supply Chain Asia

president’sADDReSS

Asosiasi Logistik Indonesia (ALI)

Chartered Institute of Logistics & Transport Singapore (CILT)

China Federation of Logistics & Purchasing (CFLP)

Singapore Economic Development Board (EDB)

Federation of Malaysian Manufacturers (FMM)

Global Logistics Council of Taiwan (GLCT)

International Enterprise Singapore (IE Singapore)

Kainan University of Taiwan (KUT)

Korea International Logistics Council (KILC)

Logistics Association of Australia (LAA)

Logistics and Supply Chain Management Society (LSCMS)

Philippines Institute of Supply Management (PISM)

Supply Chain & Logistics Group of the Middle East (SCLG)

Thai Logistics and Production Society (TLAPS)

list of appointment holders

ExEcutivE committEE mEmbErs

eXeCutiVe teaMFounder/president

Mr Paul Lim, Regional BD Manager, TNT

vice president, international relationsMr Mark Millar, Managing Director, M Power Associates

vice president, training & DevelopmentMr Raymond Heman, Supply Chain Manager,

Eastman Chemicals

vice president, Young professionalsMr Joshua Wu, Supply Chain Manager, INTEL

vice president, Memberships & community DevelopmentMr Ang Tian Teck, Director, StickySpy

aCadeMY board MeMbersMr David Chew, Managing Director, SC Asia Consulting

Mr Raymond Heman, Supply Chain Manager, Eastman Chemicals

Ms Nathalie Ricaud, Director, TAD LogsiticsMr Pari Annamalai, CEO, Planvisage

Mr koh Jin kiat, Regional Operations Director, Reader’s DigestMr Ang Tian Teck, Director, StickySpy

Mr Harry Lagad, IndependentMs Gwendy krijger, Director, ConnectingtheLink

A/P Mark Goh, Director, Industry Research, TLI-APMs Christina Lim, Executive Director, SC Asia Academy

Corporate relationsMr Frank Paul, Managing Director, SC Asia Publications

Mr Darryl Judd, Director, Logistics Recruitment

Young proFessionals adVisorsMr Joshua Wu, Supply Chain Manager, INTEL

Ms Christine Lee, General Manager, FlextronicsMr koh Jin kiat, Regional Operations Director, Reader’s Digest

Mr Ang Tian Teck, Director, StickySpyMr Phil Vaudin, Asst to Chairman, Best Logistics

CountrY representatiVesMr Neil Morrison, Partner, Noble International (Hong kong)

Mr Babhui Lee, Independent (Shenzhen, China)Mr Mark Millar, Managing Director, M Power Associates (Hong kong)

Mr Teoh kok Siang, Site Manager, INTEL (Shanghai, China)Mr Sanjay Goel, Chairman, GTC Inc. (Mumbai, India)

Ms Ayda Sulianti, Vice President, MIF (Surabaya, Indonesia)Mr Nigel Moore, Managing Director, Logistics Recruitment (Dubai)

Mr Sheikh Abdul Hai, Director, Logistics, Abdulla Fouad (Saudi Arabia)Mr Daniel Lu, Consultant, CBS Technology (Malaysia)

Mr Durairaj Veeraiyah, Director, Service Management, BASF (Malaysia)Mr Antonio kent Valderrama, Director, Macrolite Corporation

(Philippines)Mr Pari Annamalai, CEO, Planvisage (Singapore)

Mr Phil Vaudin, Asst to Chairman, Best Logistics (Taiwan)Ms Amanda Rasmussen, Commercial Manager, Maersk Vietnam

(Vietnam)

CoMMittee MeMbersMr Low Mun kong, Independent

Prof Jim Wu, Professor, National Sun Yat Sen university

Young proFessionals eXCopresident

Mr Derrick kim, Asst Manager, British American Tobacco

vice presidentsMr Jacky Soh, Student, Republic Polytechnic

Ms karen Quek, Student, Singapore Management universityMr Marcus Ho, Senior Executive, Lufthansa CargoMr koh Wee Gek, Officer, Singapore Armed Forces

Ms Justina Tay, Student, Temasek PolytechnicMr Aaron Tay, Student, Singapore Management university

Mr Christopher Lo, Student, Singapore Management universityMr khor Yeng Hock, Executive, Panalpina

Mr James Loh, Student, Singapore Management universityMs Natasha koo, Student, university of Melbourne

Supply Chain Asia Magazine (MICA (P) 036/02/2009) is published by SC Asia Publications, a unit of the Supply Chain Asia industry community. All rights reserved. No part of the publication may be reproduced without prior permission from the publisher. For subscription and other enquiries, please visit www.supplychainasia.com

Regional Headquarter:Schaefer Systems International Pte Ltd73, Tuas Avenue 1 Singapore 639512 Phone +65/ 6863 0168Fax +65/ 6863 0288eMail [email protected] www.ssi-schaefer-asia.com

Efficient space utilisation, especially in high-cost cold storage environment is of paramount importance.

SCHAEFER’s mobile racking system is a cost-effective and efficient storage system that can effectively increase pallet capacity by up to 100%! Equipped with the latest technology, with the current EN safety features, the mobile racking system can be customised to specific requirements.

Interested to find out more?

Call us today, or visit us at www.ssi-schaefer-asia.com

“The system maximises both volume capacity and product selectivity, in the space of 2200 m2 at the temperature of -25 ◦C.”

Mr. Kevin LimIntegrated Cold Chain

Logistics Sdn Bhd

Mobile Racking SystemCost-effective, Semi-Automated, Safe

SCA 216x303 bleed Ad_Mobile_Reg.indd 1 8/15/2008 4:42:07 PM

Supply Chain Asia September/October 2009

infrastructure update6 developments

•

•

•

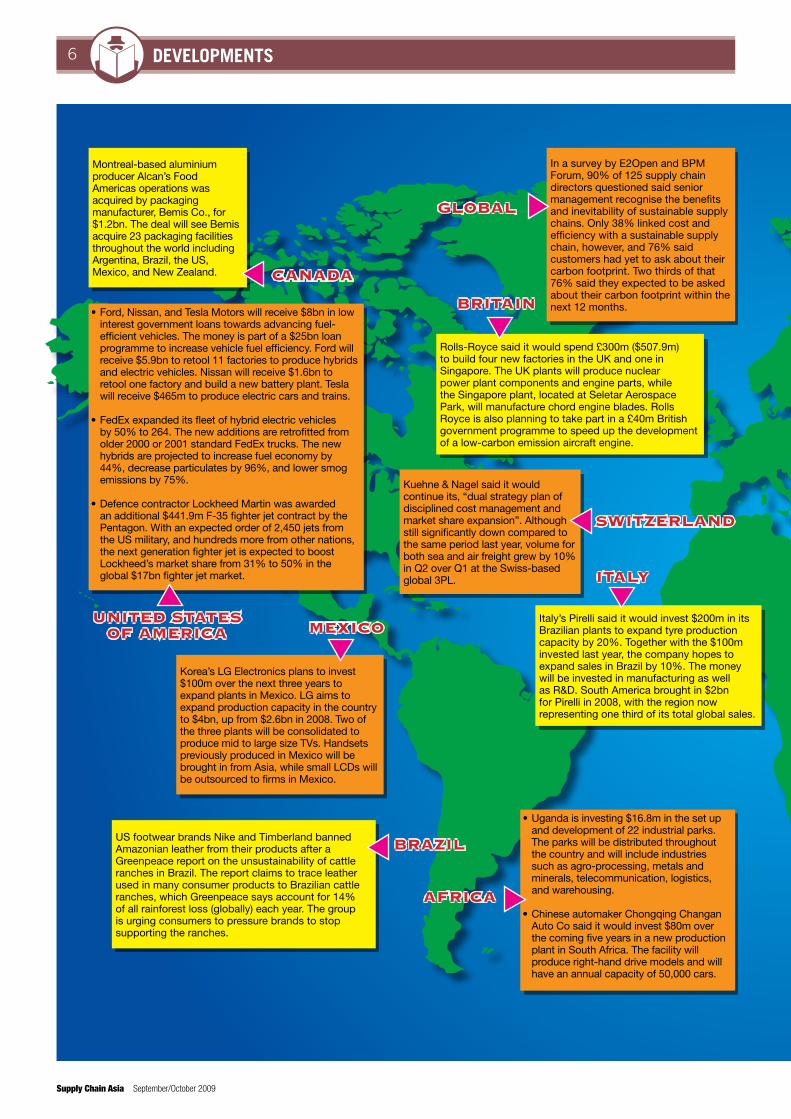

Ford, Nissan, and Tesla Motors will receive $8bn in low interest government loans towards advancing fuel-efficient vehicles. The money is part of a $25bn loan programme to increase vehicle fuel efficiency. Ford will receive $5.9bn to retool 11 factories to produce hybrids and electric vehicles. Nissan will receive $1.6bn to retool one factory and build a new battery plant. Tesla will receive $465m to produce electric cars and trains.

FedEx expanded its fleet of hybrid electric vehicles by 50% to 264. The new additions are retrofitted from older 2000 or 2001 standard FedEx trucks. The new hybrids are projected to increase fuel economy by 44%, decrease particulates by 96%, and lower smog emissions by 75%.

Defence contractor Lockheed Martin was awarded an additional $441.9m F-35 fighter jet contract by the Pentagon. With an expected order of 2,450 jets from the US military, and hundreds more from other nations, the next generation fighter jet is expected to boost Lockheed’s market share from 31% to 50% in the global $17bn fighter jet market.

UNITED STATES OF AMERICA

BRAzIl

MExICO

In a survey by E2Open and BPM Forum, 90% of 125 supply chain directors questioned said senior management recognise the benefits and inevitability of sustainable supply chains. Only 38% linked cost and efficiency with a sustainable supply chain, however, and 76% said customers had yet to ask about their carbon footprint. Two thirds of that 76% said they expected to be asked about their carbon footprint within the next 12 months.

US footwear brands Nike and Timberland banned Amazonian leather from their products after a Greenpeace report on the unsustainability of cattle ranches in Brazil. The report claims to trace leather used in many consumer products to Brazilian cattle ranches, which Greenpeace says account for 14% of all rainforest loss (globally) each year. The group is urging consumers to pressure brands to stop supporting the ranches.

Kuehne & Nagel said it would continue its, “dual strategy plan of disciplined cost management and market share expansion”. Although still significantly down compared to the same period last year, volume for both sea and air freight grew by 10% in Q2 over Q1 at the Swiss-based global 3PL.

Italy’s Pirelli said it would invest $200m in its Brazilian plants to expand tyre production capacity by 20%. Together with the $100m invested last year, the company hopes to expand sales in Brazil by 10%. The money will be invested in manufacturing as well as R&D. South America brought in $2bn for Pirelli in 2008, with the region now representing one third of its total global sales.

ITAly

GlOBAl

Montreal-based aluminium producer Alcan’s Food Americas operations was acquired by packaging manufacturer, Bemis Co., for $1.2bn. The deal will see Bemis acquire 23 packaging facilities throughout the world including Argentina, Brazil, the US, Mexico, and New Zealand.

Korea’s LG Electronics plans to invest $100m over the next three years to expand plants in Mexico. LG aims to expand production capacity in the country to $4bn, up from $2.6bn in 2008. Two of the three plants will be consolidated to produce mid to large size TVs. Handsets previously produced in Mexico will be brought in from Asia, while small LCDs will be outsourced to firms in Mexico.

CANADA

SwITzERlAND

Rolls-Royce said it would spend £300m ($507.9m) to build four new factories in the UK and one in Singapore. The UK plants will produce nuclear power plant components and engine parts, while the Singapore plant, located at Seletar Aerospace Park, will manufacture chord engine blades. Rolls Royce is also planning to take part in a £40m British government programme to speed up the development of a low-carbon emission aircraft engine.

BRITAIN

•

•

Uganda is investing $16.8m in the set up and development of 22 industrial parks. The parks will be distributed throughout the country and will include industries such as agro-processing, metals and minerals, telecommunication, logistics, and warehousing.

Chinese automaker Chongqing Changan Auto Co said it would invest $80m over the coming five years in a new production plant in South Africa. The facility will produce right-hand drive models and will have an annual capacity of 50,000 cars.

AFRICA

September/October 2009 Supply Chain Asia

infrastructure update 7developments

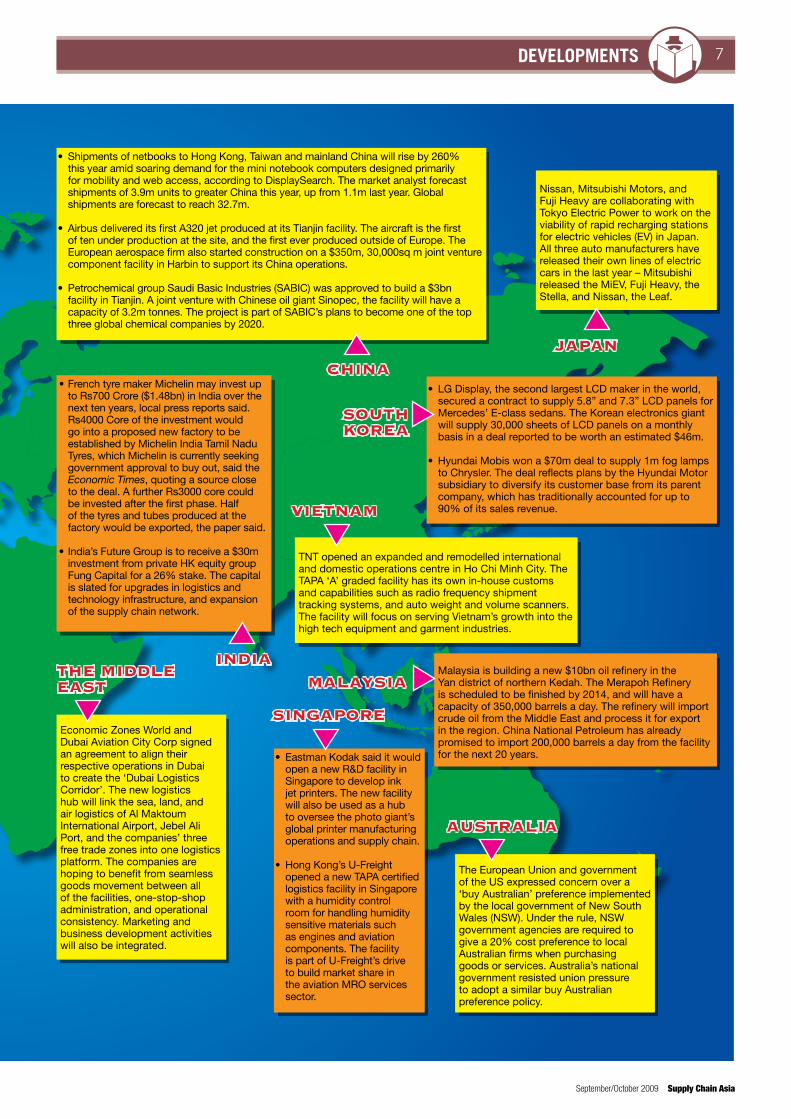

•

•

French tyre maker Michelin may invest up to Rs700 Crore ($1.48bn) in India over the next ten years, local press reports said. Rs4000 Core of the investment would go into a proposed new factory to be established by Michelin India Tamil Nadu Tyres, which Michelin is currently seeking government approval to buy out, said the Economic Times, quoting a source close to the deal. A further Rs3000 core could be invested after the first phase. Half of the tyres and tubes produced at the factory would be exported, the paper said.

India’s Future Group is to receive a $30m investment from private HK equity group Fung Capital for a 26% stake. The capital is slated for upgrades in logistics and technology infrastructure, and expansion of the supply chain network.

Nissan, Mitsubishi Motors, and Fuji Heavy are collaborating with Tokyo Electric Power to work on the viability of rapid recharging stations for electric vehicles (EV) in Japan. All three auto manufacturers have released their own lines of electric cars in the last year – Mitsubishi released the MiEV, Fuji Heavy, the Stella, and Nissan, the Leaf.

Malaysia is building a new $10bn oil refinery in the Yan district of northern Kedah. The Merapoh Refinery is scheduled to be finished by 2014, and will have a capacity of 350,000 barrels a day. The refinery will import crude oil from the Middle East and process it for export in the region. China National Petroleum has already promised to import 200,000 barrels a day from the facility for the next 20 years.

VIETNAM

SOUTh KOREA

INDIAThE MIDDlE EAST

AUSTRAlIA

MAlAySIA

JApAN

•

•

Eastman Kodak said it would open a new R&D facility in Singapore to develop ink jet printers. The new facility will also be used as a hub to oversee the photo giant’s global printer manufacturing operations and supply chain.

Hong Kong’s U-Freight opened a new TAPA certified logistics facility in Singapore with a humidity control room for handling humidity sensitive materials such as engines and aviation components. The facility is part of U-Freight’s drive to build market share in the aviation MRO services sector.

•

•

LG Display, the second largest LCD maker in the world, secured a contract to supply 5.8” and 7.3” LCD panels for Mercedes’ E-class sedans. The Korean electronics giant will supply 30,000 sheets of LCD panels on a monthly basis in a deal reported to be worth an estimated $46m.

Hyundai Mobis won a $70m deal to supply 1m fog lamps to Chrysler. The deal reflects plans by the Hyundai Motor subsidiary to diversify its customer base from its parent company, which has traditionally accounted for up to 90% of its sales revenue.

•

•

•

Shipments of netbooks to Hong Kong, Taiwan and mainland China will rise by 260% this year amid soaring demand for the mini notebook computers designed primarily for mobility and web access, according to DisplaySearch. The market analyst forecast shipments of 3.9m units to greater China this year, up from 1.1m last year. Global shipments are forecast to reach 32.7m.

Airbus delivered its first A320 jet produced at its Tianjin facility. The aircraft is the first of ten under production at the site, and the first ever produced outside of Europe. The European aerospace firm also started construction on a $350m, 30,000sq m joint venture component facility in Harbin to support its China operations.

Petrochemical group Saudi Basic Industries (SABIC) was approved to build a $3bn facility in Tianjin. A joint venture with Chinese oil giant Sinopec, the facility will have a capacity of 3.2m tonnes. The project is part of SABIC’s plans to become one of the top three global chemical companies by 2020.

ChINA

TNT opened an expanded and remodelled international and domestic operations centre in Ho Chi Minh City. The TAPA ‘A’ graded facility has its own in-house customs and capabilities such as radio frequency shipment tracking systems, and auto weight and volume scanners. The facility will focus on serving Vietnam’s growth into the high tech equipment and garment industries.

SINGApORE

The European Union and government of the US expressed concern over a ‘buy Australian’ preference implemented by the local government of New South Wales (NSW). Under the rule, NSW government agencies are required to give a 20% cost preference to local Australian firms when purchasing goods or services. Australia’s national government resisted union pressure to adopt a similar buy Australian preference policy.

Economic Zones World and Dubai Aviation City Corp signed an agreement to align their respective operations in Dubai to create the ‘Dubai Logistics Corridor’. The new logistics hub will link the sea, land, and air logistics of Al Maktoum International Airport, Jebel Ali Port, and the companies’ three free trade zones into one logistics platform. The companies are hoping to benefit from seamless goods movement between all of the facilities, one-stop-shop administration, and operational consistency. Marketing and business development activities will also be integrated.

Supply Chain Asia September/October 2009

infrastructure update8 transporters – air cargo

Beijing ups the ante in the north Asia hub gameBeijing is capitalising on the vibrancy of its post-Olympics infrastructure and city spirit with a big push to become a serious northeast Asia air logistics and supply chain hub. In October of this year, the Beijing Airport City Logistics Park (ACLP) will be fully operational at Beijing Capital International Airport — China’s busiest civil airport — marking a huge leap in efficiency and layout of support infrastructure for major air cargo operations in the Chinese capital.

“It’s the first time we’ll have ground handling, customs, quarantine and inspec-tion all located together next to the runway,” said Ellen Hu, vice president of corporate strategy with ACL, the developer and op-erator of the logistics park.

The 3.4m sq m development, built at a cost of RMB4bn ($585m), offers clients new infrastructure, services and the regulatory environment for a range of different business functions, from cargo handling and bonded logistics, to trading, R&D and reverse supply chain operations.

According to ACL, logistics companies currently operating at the old cargo handling area of Beijing Capital Airport are required to move to the new park. DTW, Rockwood and Kerry EAS have already moved into the ACLP, with UPS, DHL, FedEx and TNT

Airport cargo traffic, 2008

Rank City (Airport) Total Cargo % Change1 MEMPHIS TN (MEM) 3 695 438 (3.8)2 HONG KONG (HKG) 3 660 901 (3.0)3 SHANGHAI (PVG) 2 602 916 1.74 INCHEON (ICN) 2 423 717 (5.2)5 ANCHORAGE AK (ANC)* 2 339 831 (17.2)6 PARIS (CDG) 2 280 050 (0.8)7 FRANKFURT (FRA) 2 111 031 (2.7)8 TOKYO (NRT) 2 100 448 (6.8)9 LOUISVILLE KY (SDF) 1 974 276 (5.0)10 SINGAPORE (SIN) 1 883 894 (1.8)11 DUBAI (DXB) 1 824 992 9.412 MIAMI FL (MIA) 1 806 770 (6.0)13 LOS ANGELES CA (LAX) 1 629 525 (11.9)14 AMSTERDAM (AMS) 1 602 585 (3.0)15 TAIPEI (TPE) 1 493 120 (7.0)16 LONDON (LHR) 1 486 260 6.517 NEW YORK NY (JFK) 1 450 605 (9.8)18 BEIJING (PEK) 1 365 768 14.519 CHICAGO IL (ORD) 1 332 123 (13.1)20 BANGKOK (BKK) 1 173 084 (3.9)Total Cargo: loaded and unloaded freight and mail in metric tonnes*ANC data includes transit freight

431,000 flight arrivals and departures in 2008, serving 98 domestic and 85 international flight routes.

Along with the CBD and financial centre, the airport district is one of six areas of the city targeted by the municipal government for development. The ACLP is located in the Beijing Tianzhu Free Trade Zone — the first FTZ in the country to have an airport within its confines — which is directly under the guidance of the municipal government.

“The location of the logistics park within the FTZ is a big advantage in attracing companies. [They] can get tax rebates when they locate here; operations like customs are more efficient; and they can do other supply chain functions such as trading and after-service work,” said Hu.

A major marketing push has been undertaken to promote the ACLP. Earlier this year, ACL hired Ogilvy PR to promote the park ahead of the Airport Cities World Conference & Exhibition taking place in Beijing in 2010. Advertising campaigns, industry conferences and summits, and invitations to site inspections for potential clients are also taking place.

expected to relocate there once it is fully operational in October. ACL, which is a joint venture between Beijing Capital Airport Holdings and the Beijing Shunyi District People’s Government, is expecting a doubling of air cargo volumes through Beijing within the next five years. The airport currently handles over 1.35m tonnes of cargo on an annual basis. “The efficiency of the cargo facilities in the past was low, and you had a lot of goods destined for north China going through either Shanghai or Incheon [South Korea]. It will be much easier for those goods to come directly to Beijing,” said Hu.

The Airports Council International ranked Beijing Capital Airport 18th in the world in cargo throughput volume in 2008, when it handled 1.365m tonnes. Shanghai (Pudong) was ranked 3rd with 2.602m tonnes; Incheon 4th with 2.423m, and Tokyo (Narita) 8th with 2.1m (see table below).Beijing’s position as the busiest civil airport in China is a considerable advantage in its drive to boost cargo volumes. Capital Airport handled some

Date: 14/7/09 Op: SGRevise: 21/7/09 6th Op: dm Size: 120x85mm AH: NK (5515)

Deliveries around the world. Logistics solutions.• Guaranteed door-to-door service for your international small

package shipments• International transportation for ocean, air and ground freight• Logistics services for a controlled, reliable and economic

distribution of your shipments• Complete visibility of your shipments through our website

24 hours a day• Customs clearance

*UPS Supply Chain Solutions local office

COUNTRY: ASIA

CLASSIFICATION:

COURIER

SERVICES

CLIENT: UPS

DIRECTORY:

SUPPLY CHAIN

ASIA

www.ups.com

Singapore(65) 67383388(65) 63028000*

Hong Kong(852) 27353535(852) 31668989*

Vietnam(848) 38112888(848) 38118728*

Taiwan(886) 228833868(886) 227724232*

Malaysia(60) 377841233(60) 380231333*

Indonesia(62) 8071877877(62) 215265353*

Korea(82-2) 15886886(82-2) 20003800*

Japan(81) 3 54845834(81) 3 67020300*

Thailand(66) 27623300(66) 23188400*

Philippines(63) 28533333(63) 28511023*

UPS Asia 120x85 21/7/09 11:06 Page 1

Source: Airports Council International

9transporters – maritime

September/October 2009 Supply Chain Asia

Shippers skip the TransSiberian despite big savings on transit timesRussia’s privately held equivalent of China’s Sinotrans, FESCO Transportation Group, has concluded a study showing how depressed ocean freight rates are affecting shippers’ decisions on how best to shift cargoes from China to the Russian capital.

Transporting cargo from Shanghai to Moscow via ship tends to go via Rotterdam and St Petersburg before going overland to Moscow, with current costs in the region of $3,000 per teu, the study shows. The rail option, meanwhile, sees cargoes shipped from Shanghai to Vladivostok before boarding the TransSiberian to Moscow. Costs on this route are now running at $5,500 per teu.

“The difference is big and has become a lot bigger lately,” FESCO director Stanislav Vartanyan told Supply Chain Asia Magazine. The survey of shippers found that if the gap is down to $1,000 to $1,200, the client will often accept the higher price and ship by rail as transit times are so superior — typically 19 days rather than 40 by ship. “When the gap becomes more than that, the shipper switches to ocean,” said Vartanyan.

Were the TransSiberian to be working perfectly, cargoes could transit from Vladivostok to Moscow in eight days, but the infrastructure is still too unpredictable, resulting in shipments taking twice as long.

With 16,000 rail cars, FESCO is the second largest private rail car owner in Russia. Traditionally, the company has been best known as a shipping line — Far Eastern Shipping Co — out of Vladivostok, but it is rebranding with a focus on all of its core businesses — shipping, rail, ports and terminals, and logistics. “We are trying to rebrand as FESCO,” explains Vartanyan. “We’re really trying to be like a DHL. We want to be an integrated logistics provider.”

FESCO, which happens to be Russia’s biggest ocean container carrier, reported in late July that 2008 revenues surged 40% year-on-year from the previous year but net income plunged 80%, thanks in part to the plunging rouble.

FESCO took delivery of its biggest box ship, the 3,091 teu Fesco Diomid from Poland’s Stocznia shipyard earlier this year,

and immediately chartered the vessel to Mediterranean Shipping Co. The ship will eventually be deployed on FESCO’s own container routes between the Russian Far East, China, Korea and Japan.

The company is looking at reducing

its asset base, particularly its shipping fleet. “The strategic development of the company,” according to Vartanyan, “is not to increase our asset base for the sake of it… We want to offer solutions, not a trade.”

Hard-pressed container lines will be relieved by the latest figures from Shanghai port, revealed exclusively by Supply Chain Asia Magazine. The port, the largest in the world overall and number two on the box front, is widely perceived as a bellwether for container fortunes.

A solid July has revived the port: “We feel the trend of decreasing has slowed,” said Lu Haihu, chairman of Shanghai International Port (Group). Together with recent rises in manufacturing indices, the news lends credence to a general feeling in the industry that ex-China container volumes have bottomed.

Shanghai container throughput was 15.5% down year-on-year in the first half, but an improved July, down just 200,000 teu year-on-year, at 2.15m teu, means the year to date is down 14.5%.

Chairman Lu anticipates full year box figures of 24.5m teu, a big gap from earlier goals of cracking 30m this year. Having been operating at up to 33% over its operating capacity just four years ago, chairman Lu said that with Phase IIIB of Yangshan port up and running since December, Shanghai port is, “suffering from an oversupply of box facilities”.

Plans for further phases of development have been put on hold. Yangshan, comprised of two islands to the southeast of Shanghai, opened in November 2005. Thus far all phases of development have focused on the northern, smaller island, which is now full bar some lower draught shoreline on the west of the island that in years to come will be developed for barge use. Development of the southern larger island has been put on hold during the container recession.

Bellwether port brings good news

BUSAN

BERLIN

MOSCOW

10 transporters – maritime

Supply Chain Asia September/October 2009

Shanghai is already the world’s largest port. Only Singapore, 3,800 km to the south, lies ahead of China’s financial

metropolis in terms of container volumes, and this last hurdle could soon be overcome.

Shanghai’s container terminals have undeniably come a long way, and done so in double-quick time. In years gone by, even the most senior Shanghai government politicians severely underestimated the potential for growth in exports and container volumes from the city. “Container capacity (in 2010) will reach 8m to 10m teu,” said Xu Kuangdi, then mayor of Shanghai, at the Marintec conference in 1995. Shanghai handled 1.52m teu over its docks that year. Last year it handled 28m teu.

Such breakneck speed of growth, however, means that there are still big kinks in the supply chain infrastructure supporting the port, from both a software and hardware point of view.

The need for transhipment servicesOne man well placed to pass comment is Thomas Knudsen from Maersk Line, the world’s largest container shipping line. Maersk recently restructured its China operations so that Beijing is no longer country headquarters, and divided its business into three administrative regions:

Qingdao, Shanghai and Hong Kong. The Shanghai cluster, which Knudsen moved to head up six months ago, stretches from Xiamen to Shanghai and takes in much of the Yangzte river delta. Knudsen’s background with Maersk has seen him work in two port cities that Shanghai would no doubt like to emulate — Singapore and Dubai.

“One of the strengths of both Dubai and Singapore is transhipment,” Knudsen says. For foreign container lines in China, this thorny issue is still a no go area, due to cabotage rules. There are regular rumours from Beijing that cabotage will be eased but thus far Beijing has only eased the ruling for empty boxes. “We want to be able to do (transhipment),” says Knudsen, who believes this is what “will take Shanghai to the next level.”

Maersk Line currently employs some 375 people in Shanghai alone.

Knudsen said Beijing’s promise to ensure Shanghai becomes a genuine international finance centre by 2020 is vital for the local shipping sector. He also believes that as the dragon’s head of the Yangtze River Delta, exponential hinterland growth will be a major contributor to the growth of volumes through the port.

Aside from restricted transhipment operations as a result of cabotage, Knudsen has a few other gripes about doing shipping

business in China’s second city. Electronic data interchange (EDI) and the general links between carriers and the port could be improved and simplified, he notes: “A simplification in general for customs and getting the units of the port community working closer together with more coherence is important.” Operations and communications in Singapore and Dubai are still more coherent, he adds.

Erxin Yao, China managing director at Orient Overseas Container Line (OOCL), looks after more than 1,000 staff in Shanghai involved in shipping, logistics and other functions of the Hong Kong headquartered group. He is delighted with the State Council’s decision to make Shanghai an international shipping centre: “The development of another global shipping centre will offer the industry more options and competitive services, which in turn will facilitate trade growth.” That said, he is quick to stress that Shanghai’s rise will not come at the expense of Hong Kong, for so long the international maritime centre for Greater China.

“Hong Kong and south China ports will continue to be the key gateways for south China. We believe Hong Kong port’s role will continue to be complementary, due to the geographical differences and distance between the two cities.”

❝Shanghai’s container terminals have undeniably come a long way, and done so in double-quick time. In years gone by, even the most senior Shanghai leaders severely underestimated the potential for growth in exports and container volumes from the city. “Container capacity (in 2010) will reach 8m to 10m teu,” said Xu Kuangdi, then mayor of Shanghai, at the Marintec conference in 1995. Shanghai handled 1.52m teu over its docks that year. Last year it handled 28m teu. ❞

Work in progressEarlier this year, China’s State Council said Shanghai would become an international financial and maritime centre by 2020. Foreign boxlines tell Sam Chambers that while the huge potential of the city as a container hub is undeniable, there is still plenty of work to be done ahead of achieving the goal

11transporters – maritime

September/October 2009 Supply Chain Asia

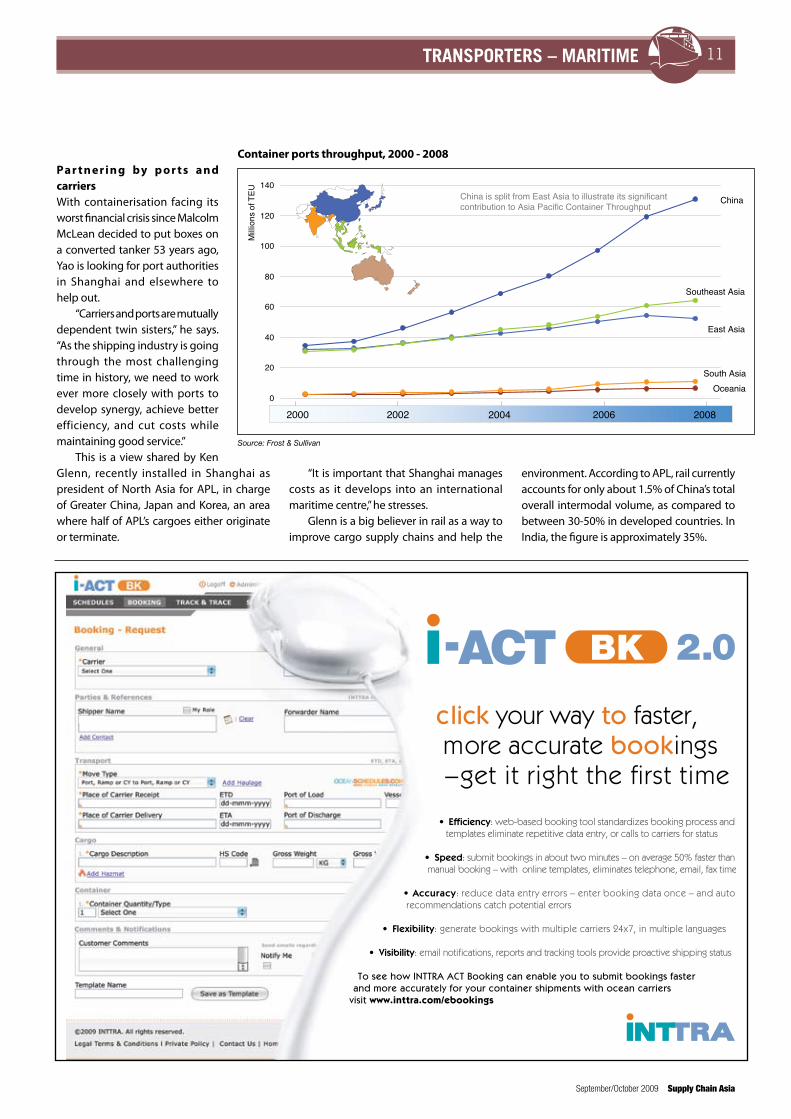

Container Ports: Container Ports Throughput, 2000 - 2008

0

20

40

60

80

100

120

140

Mill

ions

of T

EU

20082006200420022000

China

Southeast Asia

East Asia

South AsiaOceania

China is split from East Asia to illustrate its significant contribution to Asia Pacific Container Throughput

Pa r t n e r i n g by p o r t s a n d carriers With containerisation facing its worst financial crisis since Malcolm McLean decided to put boxes on a converted tanker 53 years ago, Yao is looking for port authorities in Shanghai and elsewhere to help out.

“Carriers and ports are mutually dependent twin sisters,” he says. “As the shipping industry is going through the most challenging time in history, we need to work ever more closely with ports to develop synergy, achieve better efficiency, and cut costs while maintaining good service.”

This is a view shared by Ken Glenn, recently installed in Shanghai as president of North Asia for APL, in charge of Greater China, Japan and Korea, an area where half of APL’s cargoes either originate or terminate.

“It is important that Shanghai manages costs as it develops into an international maritime centre,” he stresses.

Glenn is a big believer in rail as a way to improve cargo supply chains and help the

Container ports throughput, 2000 - 2008

Source: Frost & Sullivan

environment. According to APL, rail currently accounts for only about 1.5% of China’s total overall intermodal volume, as compared to between 30-50% in developed countries. In India, the figure is approximately 35%.

12 transporters – maritime

Supply Chain Asia September/October 2009

“In our experience as a terminal operator,” he says, “rail transportation is the most efficient mode when rail schedules are synchronised with a vessel’s arrival and departures — especially when handling very large container ships. Neither Waigaoqiao or Yangshan are currently equipped to handle shipments by rail.” For Yangshan, the headache will be adding a rail option along the 32.5km bridge connecting the port to the mainland.

APL’s Shanghai office has more than 500 employees. As a newcomer to the city, Glenn is in awe of the purpose with which authorities are going about their mission to become a shipping hub. “The Yangshan project is just one example of Shanghai’s strong will and ability to turn the city into a world-class maritime centre.”

“Yangshan is an improvement on older Waigaoqiao,” concurs John Wang, president of CMA CGM in China, but it is by no means perfect, he adds.

“Yangshan is relatively deeper than Waigaoqiao so it can take bigger ships. Customers, though, don’t like Yangshan because of the additional trucking required.” Wang points out that despite being a pair of islands out at sea, Yangshan still has its own draft restrictions: “14,000 teu ships on a second or third port of call cannot call here; it has to be their first port of call. Ningbo is much better as a natural deepwater port with a draft of 17 to 18 mts.”

Shanghai is the largest port in China for CMA CGM’s weekly volumes, followed by Shenzhen and then Ningbo. CMA CGM has 64 branches in China with some 1,300 staff. The

French line founded its Shanghai operations in 1992 and Wang has been in charge from day one. Hong Kong is still headquarters for the Far East but the line now has 310 staff in Shanghai and is investing in Yangshan.

Getting back to the issue of costs, something his peers at OOCL and APL also mentioned, Wang says while stevedoring in Shanghai is much cheaper than most other countries, other service items such as tug fees and pilotage are relatively expensive compared to other ports around the world. There are also hidden costs, he adds.

“China has been carrying an open door policy but it is still not as easy as Hong Kong and Singapore to get visas or move around. This is still a restriction to being a shipping centre. However, Shanghai is the dragon’s head of the Yangtze river — this is a cargo gathering centre, something Singapore and Hong Kong are not.”

Looking out at the stunning skyline from his lofty, luxurious perch high up on the 39th floor of the Bund Centre in Puxi, Wang says proudly of his home city: “We are becoming a great shipping centre”.

❝In our experience as a terminal operator, rail transportation is the most efficient mode when rail schedules are synchronised with a vessel’s arrival and departures — especially when handling very large container ships. Neither Waigaoqiao or Yangshan are currently equipped to handle shipments by rail. ❞

Ken Glenn, president, North Asia, APL

Container port throughput (in ‘000 TEU)Rank Country Name of Port 2007 2008 %

21 Vietnam Saigon 2,940 3,253 11%22 Philippines Manila 2,945 3,043 3%23 China Lianyungang 2,001 3,001 50%24 Japan Nagoya 2,895 2,816 -3%25 China Suzhou 1,881 2,569 37%26 Japan Kobe 2,472 2,557 3%27 Australia Melbourne 2,139 2,250 5%28 Indonesia Tanjung Perak 2,109 2,185 4%29 Taiwan Keelung 2,215 2,055 -7%30 China Yingkou 1,371 2,030 48%31 Japan Osaka 1,973 1,950 -1%32 Australia Sydney 1,696 1,858 10%33 South Korea Gwangyang 1,723 1,810 5%34 South Korea Incheon 1,664 1,703 2%35 China Yantai 1,250 1,530 22%36 Thailand Bangkok 1,582 1,377 -13%37 China Nanjing 1,060 1,292 22%38 Taiwan Taichung 1,248 1,239 -1%39 China Quanzhou 1,020 1,207 18%40 Pakistan Karachi 1,149 1,200 4%

Rank Country Name of Port 2007 2008 %1 Singapore Singapore 27,932 29,918 7%2 China Shanghai 26,150 28,006 7%3 China Hong Kong 23,990 24,494 2%4 China Shenzen 21,099 21,400 1%5 South Korea Busan 13,261 13,426 1%6 China Ningbo 9,360 11,226 20%7 China Guangzhou 9,259 11,001 19%8 China Qingado 9,462 10,320 9%9 Taiwan Kaohsiung 10,257 9,677 -6%

10 China Tianjin 7,103 8,503 20%11 Malaysia Klang 7,119 7,974 12%12 Malaysia Tanjung Pelepas 5,465 5,594 2%13 Thailand Laem Chabang 4,848 5,126 6%14 China Xiamen 4,627 5,035 9%15 China Dalian 3,810 4,503 18%16 Japan Tokyo 4,124 4,135 0%17 Indonesia Tanjung Priok 3,689 3,984 8%18 India Jawaharlal Nehru 4,060 3,953 -3%19 Sri Lanka Colombo 3,381 3,687 9%20 Japan Yokohama 3,428 3,481 2%

Source: Frost & Sullivan

www.supplychainasia.comwww.supplychainasia.com

Supply Chain Asia MagazineReaching over 40,000 key industry executives*

A sample of our reader database

DP World Senior VP FedEx Corp Chief EconomistFinancial Times China Correspondent Eastman Chemical Director, Supply Chain Solutions Eastman Kodak Director, Demand and PlanningEmirates Shipping Line President & CEOEmirates SkyCargo Senior VP, CargoEpson CFOFlextronics DirectorFujitsu PC Asia Pacific Head of Supply ChainFord Motor Co Director, Service Parts PurchasingGeneral Motors ODC MDGoodyear Tire Supply Chain/Logistics Drector,Global Sourcing OfficeHong Kong Air Cargo Terminals MDHong Kong Shippers CouncilExecutive DirectorHewlett Packard APJ Manager, Strategic Planning and Modeling Hipro Electronics Executive VPIBM VP, Global LogisticsInha University, South Korea Professor, Maritime & LogisticsIntel APAC/Japan SCS ManagerINTTRA CEOInvest Hong Kong Head of Transportation Jones Lange LaSalle Head of Industrial Practice, ChinaKenwood Electronics Singapore Finance ManagerKorea Trade Center Strategic Research DirectorKuehne + Nagel MDLenovo Executive DirectorLG Electronics Finance ManagerLufthansa Cargo Regional Manager, Asia PacificMaersk CEO, ChinaMattel Global Procurement VP

McKinsey Senior ConsultantMicrosoft Operations Logistics Manager ModusLink Senior VPMotorola Inc Global Lead, Transportation and FulfillmentNestle VPNokia Logistics Director, Asia PacificOracle Corp Senior DirectorPhilips Electronics Director, Air & CourierProLogis VPProctor & Gamble Country ManagerRabobank VPRW Baird Research DirectorSamsung Asia Manager, Supply Chain ManagementSara Lee VP, Operations Shanghai Airport Authority VPShanghai International Port Group ChairmanSinotrans DirectorSony Electronics Divisional MDSony Ericsson Mobile Communications Senior Manager, Asia PacificStarbucks Supply Chain DirectorTaipei Computer Association DirectorToshiba Data Dynamics Finance ControllerTNT SVPUnilever Senior SC Planning ManagerVisteon Global Purchasing DirectorWal-Mart SVP and COOWestern Digital President & CEOXerox CorporationDirector of Supply Chain & LogisticsYCH Group Chairman

Accenture MD, Supply Chain Asia PacificAgility CEO, Asia PacificAir China Cargo PresidentAirbus DirectorAmway Senior Distribution ManagerAramex CEOArshiya InternationalPresidentAudi Executive Director, ChinaAvon Executive Director, StrategyBASF Senior Manager, Supply Chain ConsultingBayer Material Science Logistics Procurement ManagerBenQ VPBHP Billiton VPBooz Allen Hamilton Senior ConsultantCarrefour Country ManagerCarrier UTC Director of LogisticsCathay Pacific Director and GM, CargoCH Robinson MDCoca Cola National Transport ManagerComputer Associates VP, Global Supply Chain & LogisticsCaterpillar VPChina Federation of Logistics & Purchasing PresidentCisco Senior DirectorCompal Electronics VPCon-way DirectorCosco Container Lines MDDaewoo International VPDelphi Automotive Systems Logistics Manager, Asia PacificDeloitte Consulting DirectorDHL CIO/Senior VPDow Chemical Logistics Supply Manager, Asia Pacific

*For full details of distribution, download the magazine Media Kit at www.supplychainasia.com/magazine

Supply Chain Asia September/October 2009

infrastructure update14 supply chain – strateGy

Industr y is facing unprecedented cost challenges. The global economy is suffering from deep recession and

consumers have reduced their spend drastically. Add to this other challenges such as commodity price variability, supplier financial uncertainty and global sourcing risks such as the recent and well-publicised food safety risks. Companies are dealing with an unenviable combination of potentially

Sourcing optimisation for sustainable savings

By Craig Rawlings, director, Supply Chain, Deloitte

Consulting, Southeast Asia

In today’s environment, the challenge is not convincing the supply market to reduce their costs, but ensuring the negotiated savings find their way to the bottom line

declining revenues, continuing rising costs and quality issues.

Against this backdrop, most companies have recognised that external spend is a large component of their cost structure — typically 40-70% and growing with increased outsourcing. Many organisations in Asia are now looking to procurement as the mechanism to both reduce costs and lock in favourable terms as consumer

demand recovers in the medium term. For mainly regional and local organisations new to procurement-driven cost reduction, conducting strategic sourcing initiatives will be a significant challenge given the constraints around organisational structures, availability of procurement spend information, and the skills of procurement practitioners.

Other organisations though, primarily

September/October 2009 Supply Chain Asia

infrastructure update 15supply chain – strateGy

sustainable savings that track to bottom line impacts on cost of goods sold (COGS) or selling, general and administrative (SG&A) expenses. Too often, long term savings are not adopted, and the costs quickly creep back.

The questions businesses are askingWhat causes this phenomenon? Part of the problem stems from the seemingly perfect logic that organisations should take a ‘show-me-the-money’ approach and focus on renegotiating their largest contracts. However, by focusing on what is immediately obvious, organisations have tended not to develop sustainable management processes to truly control costs. Another challenge is that supplier costs are impacted by employees across the organisation, yet external spend reduction has too often become the responsibility of the procurement function which then must ‘market’ its services back to internal customers.

are developing a new discipline of spend management.

Spend management seeks three core objectives:

C o m p r e h e n s i v e : p r o v i d e a comprehensive view, addressing all relevant processes across all the organisation’s external spend categories

Continuous: focus on continuous process improvement and renewable cost savings

Control: provide greater control over spending and risks right across the organisation

Spend management is not structured around initiatives but rather around on-going management processes for spend categories, for which objectives, stakeholders, roles, responsibilities, and new processes are developed. All external spend categories including strategic indirect, operating indirect, direct materials and capital expenditures are in scope.

Furthermore, as organisations grow, complexity increases with multiple systems, increased product lines, business units and geographies, thus making it difficult to manage spend in traditional ways. Take for instance a typical challenge for MNC’s who can be required to manage supplier spend for multiple categories in a large number of countries, dealing with fiercely autonomous business units. The magnitude of the challenge becomes apparent.

However, top organisations increasingly realise they have a significant opportunity to further reduce and control external spend. They are transitioning away from a procurement initiative-based approach and

❝For the past decade and a half, many companies have completed successive waves of initiatives to reduce spend. Strategic sourcing was followed by e-procurement, B2B exchanges and reverse auctions. These companies now face a different challenge. Although most of these initiatives have resulted in large potential costs savings (often called identified savings), executives are frequently thwarted in their ability to transform these opportunities into sustainable savings that track to bottom line impacts on cost of goods sold (COGS) or selling, general and administrative (SG&A) expenses. Too often, long term savings are not adopted, and the costs quickly creep back.

❞ Spend management goes beyond the sourcing/procurement function. Leadership from business units, finance and functions with large spend are aligned around key spend categories. Spend management focuses on a broader set of business issues and incorporates an expansive set of management processes that include ‘levers’ to manage tax, intellectual property, risk, demand, assets, compliance, specifications, and more.

The case for changeLarge organisations usually have numerous initiatives underway to manage external costs. If viewed from a spend management

multinational companies, have already aggressively tackled these costs. For the past decade and a half, many of these companies have completed successive waves of initiatives to reduce spend. Strategic sourcing was followed by e-procurement, B2B exchanges and reverse auctions. These companies now face a different challenge. Although most of these initiatives have resulted in large potential costs savings (often called identified savings), executives are frequently thwarted in their ability to transform these opportunities into

Current approaches versus spend management

Current approach Spend management

Initiative based Management process based

Sourcing and procurement focus Broad business focus

Selected spend categories All spend categories

One cost reduction lever applied across many spend categories

Many or all levers applied across each category

One-time cost savings Continuous cost savings

Focus on projects Focus on controls

Numerous disconnected stakeholders Clear roles and responsibilities

Potential savings Realised savings

Supply Chain Asia September/October 2009

infrastructure update16 supply chain – strateGy

perspective, however, these activities are typically managed in a sub-optimal manner, which manifests itself in one of two ways: incomplete and disconnected.

Most companies take an incomplete and disconnected approach to managing costs. Rather than attacking costs through a coherent category-specific programme, levers are often poorly applied. Far too few stakeholders are aware of or onboard with new strategies, and roles and responsibilities are not defined or understood across the category. There is an absence of ‘ownership’ for the category, and incentives across stakeholders are often misaligned. This is not for a lack of capable people, rather a lack of integrated processes. Business schools and major software solutions have historically focused on budgeting, sourcing and purchase-to-pay as separate processes, and only recently has an integrated ‘spend management’ process emerged.

Initiative focusOften, cost management efforts are driven by a focus on initiatives. It is common for companies to report that “we are implementing sourcing tools”, or “we are standardising our contracts”, or “we are standardising our specifications”. The problem is when the initiative-driven mentality blinds organisations to the unique aspects of the individual categories.

❝Most companies take an incomplete and disconnected approach to managing costs. Rather than attacking costs through a coherent category-specific programme, levers are often poorly applied. Far too few stakeholders are aware of or onboard with new strategies and roles and responsibilities are not defined or understood across the category. There is an absence of ‘ownership’ for the category, and incentives across stakeholders are often misaligned. ❞

As an example, best practices and key requirements for services procurement are subordinated or completely overlooked i n m a ny e - p r o c u r e m e n t p r o j e c t s . Similarly, the requirements for managing advertising spend are completely different for commodity products, yet too often processes are not effectively designed to account for these differences. When initiatives are managed ‘down’, the matrix and objectives are structured for successful project completion rather than the successful management of major spend categories, the result can only be described as, “the sourcing activity was a success, but the category is still out of control.”

This is frequently seen with a sourcing initiative that ends with the announcement of the savings, a declaration of victory, and a new contract that is quickly filed away. The required execution of the strategy, process changes, compliance, and supplier management are only partially deployed, and the realised savings differ dramatically from the announcement.

There is the additional problem of accounting for the savings. Finance, procurement and the operating business units seldom agree on how to calculate and distribute savings. Considerable time is spent second-guessing the true success of initiatives rather than developing a management process for calculating and

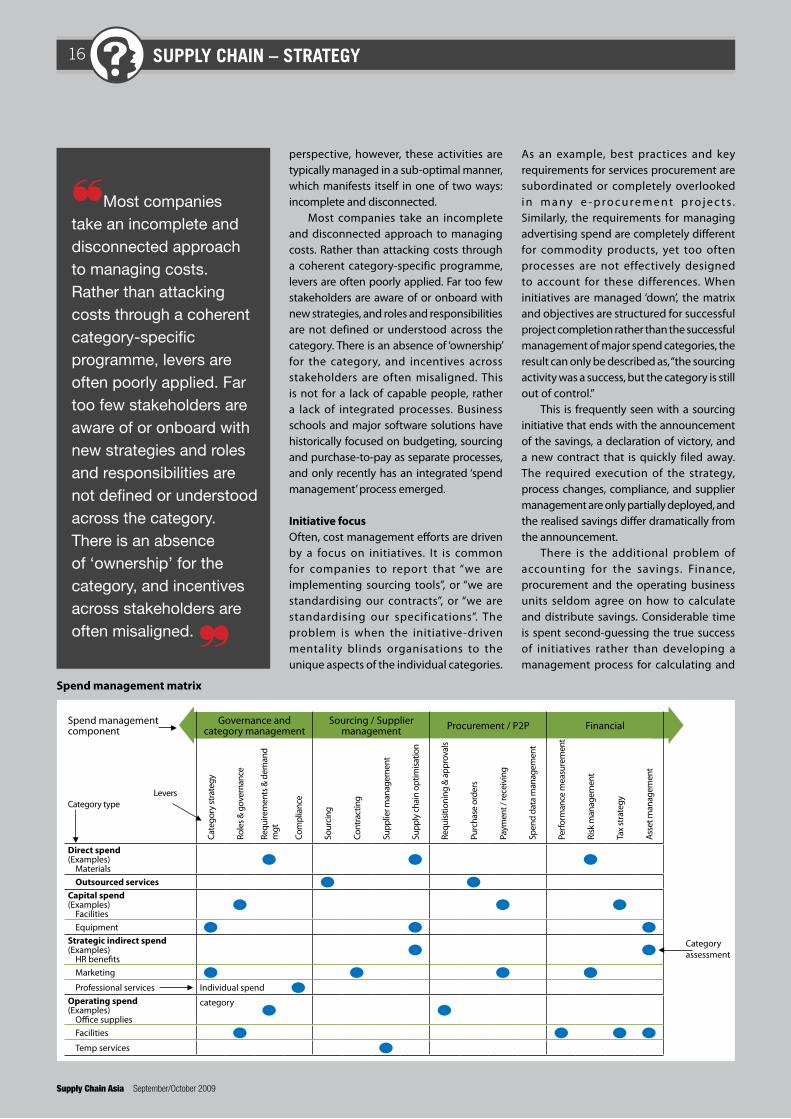

Spend management matrix

Spend managementcomponent

Governance andcategory management

Sourcing / Suppliermanagement Procurement / P2P Financial

LeversCategory type

Cate

gory

stra

tegy

Role

s & g

over

nanc

e

Requ

irem

ents

& d

eman

d m

gt

Com

plia

nce

Sour

cing

Cont

ract

ing

Supp

lier m

anag

emen

t

Supp

ly c

hain

opt

imisa

tion

Requ

isitio

ning

& a

ppro

vals

Purc

hase

ord

ers

Paym

ent /

rece

ivin

g

Spen

d da

ta m

anag

emen

t

Perfo

rman

ce m

easu

rem

ent

Risk

man

agem

ent

Tax

stra

tegy

Asse

t man

agem

ent

Direct spend(Examples)

Materials

Outsourced services Capital spend(Examples)

Facilities

Equipment Strategic indirect spend(Examples)

HR benefits

Marketing Professional services Individual spend

Operating spend(Examples)

Office supplies

category

Facilities Temp services

Categoryassessment

September/October 2009 Supply Chain Asia

infrastructure update 17supply chain – strateGy

assigning performance metrics. To overcome these and other characteristic challenges, a new spend management discipline is needed.

Building spend management disciplinesBuilding a spend management discipline requires a comprehensive programme, including changes in leadership, organisation, process, technology, and performance management. Both a fact-based business case and active leadership of change are required for success. A systematic approach contains five key steps, as in the table below.

Spend management strategies are at two levels:

Enterprise level: for some organisations with declining revenue, cost containment —and thus spend management — becomes the key strategy. During the strategy development step, high-level goals and objectives should be reviewed and updated based on the assessment. Strategies to achieve goals can then be developed.

Category level: category specific strategies are developed to align stakeholders with the spend management objectives for each key category. Category specific strategies should include: Category description and scope Category value drivers Stakeholder impact assessment Performance metrics D e f i n e d r e s p o n s i b i l i t i e s a n d

accountabilities

For most companies, establishing a sustainable and scaleable spend management programme requires a fundamental transformation in cross-organisational teamwork and the adoption of new processes. To transition from an initiative-base approach to an ongoing management process, a project/transition management team should be staffed and roles for managing the rollout and ongoing coordination should be designated.

Because spend management is not an established process within most organisations, but rather a new discipline, there is no base-level understanding or experience about how the overall process should work. As a result, spend management programmes raise predictable challenges from various stakeholders. Understanding these challenges in advance can help leaders prepare and respond in a manner that moves the programme forward. Typical challenges include: Natural friction between business unit

leaders who are highly motivated to sus-tain production/operations at the highest levels, and finance/procurement leaders who challenge the extra costs associated with frequent ‘emergency’ purchases

Functional leaders who don’t see value in other stakeholders without ‘sufficient domain expertise’ reviewing and/or challenging their practices

Stakeholders who believe that spend management will impair the current organisational culture and reduce productivity

Suspicion that the spend management team is not a broad-based team of stakeholders, but rather a small team that will make ‘reckless’ decisions that trade off supplier quality and services levels to demonstrate short-term results

The transition team should manage these ‘softer’, more intangible variables in order to impact leadership and culture, while driving ‘harder’, more tangible improvements in organisation, process and technology changes.

To do so, a well designed change management programme is required — one that proactively uses a variety of frameworks and tools to manage risk and guide the organisation through the transition, such as: Communications Guiding coalit ions and decision

structures Cases for change Commitment mechanisms Stakeholder assessment Change impact assessment Performance goals and monitoring Education and training

By addressing these issues, organisations can move from an initiative focused approach, where success is based on identified savings; to a spend management approach, where the negotiated savings are realised through improvements in bottom line profitability.

Spend management discipline

Build foundation Establish baseline Assess opportunities Develop strategy Execute and manage

Key steps

Build leadership team. Develop category structure.

Analyse spend and usage data.

• Develop enterprise spend management strategy.

• Staff project management team.

•

•

•

•

Establish roles and governance.

Understand current initiatives and background.

Conduct enterprise level benchmarking.

Develop high level goals and objectives and business case.

•

•

•

Collect spend data.

Review current initiatives, roles and process for each category

Develop hypotheses for improvement concepts.

•

•

•

•

Conduct category internal and external benchmarking/best practices review.

Assess category improvements for each lever.

Assess technology enablers.

Quantify opportunities/costs.

•

•

•

•

•

Develop category strategies.

Redesign organisation(s).

Redesign key processes.

Redesign technology.

Set specific performance targets.

•

•

•

Develop implementation roadmap and execution plans.

Develop communication and change management plans.

Measure and track benefits.

infrastructure update18 the csr series

Supply Chain Asia September/October 2009

Energy is at the core of many debates surrounding global warming and efficient economies. Over the past

years, realities about the limitations of fossil fuels to meet global energy needs have reached a wider audience and permeated deeper into individual and corporate consciences. As firms such as GE began to invest in wind turbine technology, Suntech in solar panels, and Vinod Khosla in algae fuels, the investment community began to think technology would bring the solutions.

For many firms struggling to understand their environmental impact and make positive changes, the problem with the energy debate has been that many of the solutions available in the marketplace require investments that are seemingly not market competitive. While more fortunate firms have been able to access clean energy from their energy providers; or managed to convince their board that putting up a solar panel array would increase brand value, many have had to centre efforts to reduce energy consumption or increase efficiency on improving processes or purchasing new equipment. It is few that to date have taken an holistic look at their supply chains to look for efficiency gains.

In such an exercise, physical structures would figure strongly, as buildings are the largest ‘user’ of energy and the largest ‘waster’ of energy as well. If firms take a step back and study their physical supply chain infrastructure and the environments in which they exist, they would come to understand that through a process of designing, constructing, operating, and maintaining buildings with an understanding of how each of these actions impacts the environment, large efficiency and cost gains can be found for both their own businesses and the environment.

Debating the benefitsWhen a firm begins the process of developing more efficient and ultimately more environmentally friendly structures, the first major hurdle to be cleared is budget. Due to higher upfront costs, better designs and materials are often seen as additional ‘icing on the cake’ benefits. The additional costs would not be a problem if those in the boardroom could see the gains more clearly, including gains from things like the positive press that comes from investing in environment friendly structures. But short-term projections and

Structural changeBuildings are the largest users and wasters of energy in supply chains. as part of the Supply Chain Asia Magazine CSR Series, Richard Brubaker demonstrates that by studying physical supply chain structures and the environments in which they exist, companies can make large efficiency and cost gains for both their businesses and the environment

infrastructure update 19the csr series

September/October 2009 Supply Chain Asia

cash flow statements are normally not built to include such gains.

Nevertheless, rising costs of traditional materials and sources of energy over the past two years have resulted in a tidal shift in investment by manufacturers and users in more efficient building designs, processes and materials. Staple building products such as cement, dry wall, and tiling, for instance, are seeing significant advances in efficiency and are being produced from recycled materials. The newer versions of these products offer managers long-term positive returns on investment. At the same time, new energy and process efficiency machinery and technologies that minimise solid wastes, VOC emissions, and sludge, can also now be viable investment options.

Site selectionBeginning with site selection and building design, perhaps one of the biggest drivers of change has been market awareness of LEED and other local building certification programmes that rank buildings using various constraints.

For firms that have the luxury of starting with a blank slate, or are planning a move to a new location, accessibility is one of the first considerations that need to be made. This consideration involves a host of different questions: how close will the building be to suppliers, customers and staff? How close is it to supporting infrastructure (road, rail, seaport and airport); and whether or not the supporting infrastructure is the most

appropriate (export-focused organisations should be near international sea and airports, while organisations focused on selling to the domestic market should be near rail or road networks).

O n c e t h e g e o g r a p h i c location is selected, the process of d e t e r m i n i n g w h e t h e r a n existing site or Greenfield site is most appropriate can begin. While

❝Pepsi, the world’s second largest beverage producer, recently opened its

greenest plant to date in chongqing, china. It is a plant that has been designed

architecturally and operationally to significantly reduce water and energy

consumption. the new plant uses 22% less water and 23% less energy than the

average Pepsico plant in china. at the same time, Pepsi’s site saves water by utilising a high-pressure cleaning system, water-free

conveyor belt lubricant, water-saving fixtures, and systems to reuse water from the factory

in the surrounding landscape.

❞

both choices offer options for ‘greening’ the supply chain, each will offer a different set of challenges and a different set of opportunities. Greenfield sites can be

You deliver the cargo

We deliver your message

RTG Communications Room 1603 Beverly House, 93-107 Lockhart Road, Wanchai, Hong Kong

Tel: 2858-7176 Fax: 2893-3486 Email: [email protected] Website: www.rtgcommunications.com

infrastructure update20 the csr series

Supply Chain Asia September/October 2009

designed 100% from scratch and therefore offer a lot more flexibility in terms of design, materials used, and so on; while an existing site may already possess structural hurdles that limit the potential green characteristics of the building. Yet using an existing site also presents the opportunity of conversion, and thereby improvement of the existing stock on the market.

Example: for investors looking to enter China through a Greenfield build, the Tianjin Eco-City is one example of where firms will soon have options. Built on 110 hectares of land, the Eco-City, a partnership with the government of Singapore, will offer manufacturing, commercial, and residential properties with all necessary amenities. The park’s green credentials will include renewable energy options, the latest in water treatment, green spaces, and public transportation (light rail and bus) in a single package.

Building designThrough the process of site selection and design, it is also important for managers to split the ‘sustainability’ of the building into different areas. Solutions that will reduce the energy needs of buildings may include how the building is insulated and passive solar application; while improving the ‘green’ environment can include creating green spaces inside and outside the structure; use of recycling systems, and use of systems that mitigate and use waste and filter waste water.

Laying out the floors to maximise natural light is one of the easiest ways to reduce the energy demand of a building, and through design it is possible to ensure that everyone has access to natural light (i.e. not only the offices of senior managers). This means significantly reduced electricity loads during daylight hours, and a number of studies have shown that layouts with natural light improve productivity.

Allowing managers in each office to personally control their own temperatures will result in inefficiencies and waste, while planning for centralised control does not.

Better floor layout and smart use of open spaces can improve circulation and reduce HVAC loads.

Example: Pepsi, the world’s second largest beverage producer, recently opened their greenest plant to date in Chongqing China. It is a plant that has been designed architecturally

and operationally to significantly reduce water and energy consumption. The new plant uses 22% less water and 23% less energy than the average PepsiCo plant in China. At the same time, Pepsi’s site saves water by utilising a high-pressure cleaning system, water-free conveyor belt lubricant, water-saving fixtures, and systems to reuse water from the factory in the surrounding landscape.

MaterialsDue in large part to the direct visible relationship between costs and product quality, the liveliest debates surrounding the construction of a building will occur as a firm begins to look at materials and equipment. Important because of the direct correlation between product quality and building quality, in the past this process has typically rarely involved environmental considerations outside of what it took to meet a local standard. However, over the past two years, through the introduction of certifications such as LEED as well as market education, lower prices, and incentive programmes, many firms are starting to look at what alternative materials and equipment is available to them.

Starting with capital equipment, investing in efficient HVAC and lighting systems are of prime importance, given the amount

of energy expended by each. Investment in better insulation and double-glazed windows can also go a long way to reduce the amount of energy required to run the building on a day-to-day basis. Passive and active solar systems may offset some of the environmental impact, but even more effective could be the installation of rainwater collection and wastewater treatment systems.

Selection of the right materials is a process that should go well beyond investment in capital equipment. Cement using fly ash can be specified; tiling and carpeting systems can be ordered from producers like Interface, who develop products and services to support firms looking to reduce their environmental footprint while maintaining a high quality look. Installing two flush toilet systems; removing paper towels, and providing an on-site recycling centre, are all ways to reduce the numerous environmental footprints that a building and its occupants create.

Example: Plantronic’s in Suzhou, a few hours west of Shanghai, commissioned a building in 2003 that would become one of China’s LEED buildings. Designed by Bechtel, the building’s design incorporated not only water collection and natural cooling, but also actively incorporated products that could be sourced locally (60%) and remove VOC emissions inside the building.

❝as firms such as GE began to invest in wind turbine technology, Suntech in solar panels, and Vinod Khosla

in algae fuels, the investment community began to think technology would bring the solutions.

❞

infrastructure update 21the csr series

September/October 2009 Supply Chain Asia

Operation and maintenance Once the building is constructed and equipment is installed, managers will need to develop a process that will measure how it is operated and maintained to ensure that reductions are fully achieved and further gains are realised. It is the ongoing, everyday, management of the site: identifying areas where efficiencies can be made; ensuring equipment is running as it should, and looking for further improvements through adjustments; that will bear the full fruits of the investment. In a manufacturing environment, where large amounts of energy and utilities are used, variances in performance and efficiencies can be reduced through an effective management system. Gains in corporate offices can be extended through smart use of centralised air conditioning and education of employees to turn off the lights in unused conference rooms, and so on.

ConclusionsWith all the announcements and discussion surrounding the benefits of solar panels and carbon offsets in the marketplace, it is important to remember that the structures themselves are part of the problem. It is also important to remember that the environmental inefficiencies of buildings can be reduced with minimal improvements.