Contents Indian Automotive Sector ........................................................................................................................................2 Overview .............................................................................................................................................................2 Value Chain of automobile industry .....................................................................................................................5 Industry Dynamics ...............................................................................................................................................7 Market Segments ............................................................................................................................................7 Macro-Factors Affecting the auto-industry.......................................................................................................9 Government Policies and Regulations................................................................................................................ 10 Outlook ............................................................................................................................................................. 12 Auto Ancilliary ....................................................................................................................................................... 13 An Overview...................................................................................................................................................... 13 Investments................................................................................................................................................... 14 Exports .......................................................................................................................................................... 15 Auto Components Industry Value Chain.............................................................................................................16 Industry Dynamic s ............................................................................................................................................. 17 Market Segments .......................................................................................................................................... 17 Macro-F actors Affecting Industry ................................................................................................................... 21 Government Policy and Regulations .................................................................................................................. 21 Outlook ............................................................................................................................................................. 23 Business Model ................................................................................................................................................. 25

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

8/6/2019 Auto Auto Ancilliary

http://slidepdf.com/reader/full/auto-auto-ancilliary 1/40

Contents

Indian Automotive Sector ......................................................................................................................................Overview ...........................................................................................................................................................

Value Chain of automobile industry ...................................................................................................................

Industry Dynamics .............................................................................................................................................

Market Segments ..........................................................................................................................................

Macro-Factors Affecting the auto-industry.....................................................................................................

Government Policies and Regulations ................................................................................................................

Outlook ............................................................................................................................................................. Auto Ancilliary .......................................................................................................................................................

An Overview ......................................................................................................................................................

Investments ...................................................................................................................................................

Exports ..........................................................................................................................................................

Auto Components Industry Value Chain .............................................................................................................

Industry Dynamics .............................................................................................................................................

Market Segments ..........................................................................................................................................

Macro-Factors Affecting Industry ...................................................................................................................

Government Policy and Regulations ..................................................................................................................

Outlook .............................................................................................................................................................

Business Model .................................................................................................................................................

8/6/2019 Auto Auto Ancilliary

http://slidepdf.com/reader/full/auto-auto-ancilliary 2/40

Indian Automotive Sector

Overview

The automotive Industry in India is now working in terms of the dynamics of an open market. Many joint venture

have been set up in India with foreign collaboration, both technical and financial with leading global

manufacturers. Also a very large number of joint ventures have been set up in the auto-components sector andthe pace is expected to pick up even further. The Government of India is keen to provide a suitable economic, an

business environment conducive to the success of the established and prospective foreign partnership ventures.

The Indian auto sector was the place to be in for global OEMs right from the early 2000s. At a penetration of less

than ten cars per 1000 persons, the upside was enormous. While many manufacturers were not making huge

profits, they did not want to miss out on what could eventually be amongst the top five markets by volume. As th

middle class India started to buy to its potential and as the roads became better, the anxiety in companies was n

around ‘will we sell’. It was more around ‘do we have the capacity and brand position to convert opportunity int

revenues’.

8/6/2019 Auto Auto Ancilliary

http://slidepdf.com/reader/full/auto-auto-ancilliary 3/40

8/6/2019 Auto Auto Ancilliary

http://slidepdf.com/reader/full/auto-auto-ancilliary 4/40

8/6/2019 Auto Auto Ancilliary

http://slidepdf.com/reader/full/auto-auto-ancilliary 5/40

Value Chain of automobile industry

The value chain in most cases consists of following :

Tier3 suppliers:- these are basically small workshops that provide small or may be recycled components or may bconsumables to TIER2 Supplier. The company usually does not deals directly with them but could if some

regulatory requirements are to be fulfilled.

TIER2 Supplier:- they provide much sophisticated products to TIER1 like metal rods or fabrics that go on produci

the axle rods or carpets. The quality of component they produce could affect the quality of the vehicle.

TIER1 Suppliers:- These are the biggest in operations as compared to the rest and supply the product directly to

the OEM for manufacturing. The company takes a stock of the quality of component supplied. Components could

be gear boxes, pistons or unmachined blocks which the company could process further depending on its

requirement, hence it could not be the final product.

OEMs:- the OEMs actually coordinate with the suppliers for part development and only deal with designing and

assembly of parts. They are the centralized agencies in the overall process.

The processes followed are

1. Procurement of Steel

2. Blanking

3. Welding

4. Painting

5. Assembly ( components are assembled during these operations)

a. Of engineb. Of vehicle

6. Quality Check

7. Stocking

8. Delivery

Dealer:- After the product is made it is supplied to the dealer by the OEM depending upon his request who acts a

an interface between the OEM and the customer

Finance and insurance:- increasing the OEMs are entering into this field due to

• Shrinking margins in the core business

• More returns from this business

Besides this the company can aid in the procurement of the vehicle and increase its sales.

2ndhand retailers:- They procure the used vehicle from the customers and sell them in the 2nd hand car market.

Increasingly this market is also expanding and many OEMs have opened shop in this sector also

8/6/2019 Auto Auto Ancilliary

http://slidepdf.com/reader/full/auto-auto-ancilliary 6/40

8/6/2019 Auto Auto Ancilliary

http://slidepdf.com/reader/full/auto-auto-ancilliary 7/40

Industry Dynamics

Market Segments

The industry is categorized in the broadly in the following segments

1.Passenger Vehicles ( PVs )Passenger Cars

UVs

MPVs

2.Commercial Vehicles (CVs)

M&HCVs

Passenger Carriers

Goods Carriers

LCVs

Passenger Carriers

Goods Carriers

3.Three WheelersPassenger Carrier

Goods Carrier

4.Two wheelers

Scooter/Scooterettee

Motor cycles/Step- Throughs

Mopeds

Electric Two Wheelers

5.Agriculture Machinery

However these can further be divided on the basis of length, engine capacity, tonnage, seating capacity and like

Eg:- the Passenger vehicle market is segmented on the basis of length of the vehicle as the government has some

restrictions based on the overall length of the vehicle and the taxes are varied based on this criteria

A : Passenger Cars - No. of seats including driver not exceeding 6(differentiation based on seating capacity)

A1: Mini - (Upto 3400 mm)

A3: Mid-size (4001-4500 mm)

A4: Executive (4501-4700 mm)

A5: Premium (4701-5000 mm)

B: Max.Mass upto 3.5 tonnes

B1: No. of seats including driver not exceeding 7

B2: No. of seats including driver exceeding 7 but not exceeding 9 (7+1 & 8+1)

Differentiation based length of

the vehicle.

8/6/2019 Auto Auto Ancilliary

http://slidepdf.com/reader/full/auto-auto-ancilliary 8/40

Similarly the Commercial Vehicles are segmented on the basis of Tonnage and seating capacity

Eg

M3 Category:More than 8+1 seats & Max. Mass exceeding 5 tonnes (Passenger Carrier)A: Max. Mass exceeding 5 tonnes but not exceeding 7.5 tonnes

B: Max. Mass exceeding 7.5 tonnes but not exceeding 12 tonnes

C: Max. Mass exceeding 12 tonnes but not exceeding 16.2 tonnes

D: No. of seats including driver exceeding 13 and Max. Mass exceeding 16.2 tonnes

2 –Wheeler market is segmented on the basis of big wheel size and engine capacity

Eg

A: Scooter/Scooterettee : Wheel size less than or equal to 12''

A1: Engine Capacity less than 75 cc

A2: Engine Capacity 75 cc and above but less than 125 cc

A3: Engine Capacity 125 cc and above but less than 250 cc

B: Motorcycle/Step- Through : Big Wheel size more than 12''

B2: Engine Capacity 75 cc and above but less than 125 cc

B3: Engine Capacity 125 cc and above but less than 250 cc

B4: Engine Capacity 250 cc and above

8/6/2019 Auto Auto Ancilliary

http://slidepdf.com/reader/full/auto-auto-ancilliary 9/40

Macro-Factors Affecting the auto-industry

• Economic Policies.

a. Entry of new competitors because of low trade barriers

b. FTAs or agreements with nations to reduce the trade barriers

c. Petrol Pricing

d. Monetary policies which promote low / high interest rates depending upon parameters like

inflation etc.

e. Exchange Rates

• Agreements and partnerships amongst automobile majors

• Ecological and physical forces

1. Environmental care

a. Emission Norms

b. Fuel Efficiency Norms

2. Infrastructure in Cities/ Trains/ Planes

a. Improvement of automobile infrastructure (roads, parking lots and

complementary public transportation.• Socio Cultural effects and Consumer behavior

1. Age distribution

a. Age of ownership of a car has dropped from 39 to 32 years indicating more preference o

vehicles with unique designs and features

2. Family plans

3. Consumer Behaviour/ Spending culture / Budget

4. Social expectations

8/6/2019 Auto Auto Ancilliary

http://slidepdf.com/reader/full/auto-auto-ancilliary 10/40

Government Policies and Regulations

Safety and Emission

• Implementation of Bharat Stage norms- requiring manufacturers to tweak or build new engines a

Petroleum producers to improve the quality leading to price hikes

• Setting up of state of the art testing facilities across India by National Automotive Testing and R&

Infrastructure Project (NATRIP) and increased safety norms.

• Move to the international model of leving higher road tax on older vehicles in order to discourage their

use

• In order to facilitate faster upgradation of environmental quality, the Govt. will consider having a termin

life policy for commercial vehicles alongwith incentives for replacement for such vehicles.

• Use of ethanol blended petroleum would require the OEMs to change or tweak the engines accordingly

• Government to notify fuel efficiency standards for vehicles under the Energy Conservation Act of 2002 b

2011

Taxes and Rebates

• R&D policy decision to promote in-house R&D might be reflected in fiscal policy as tax-break to firms f

their expenditure on R&D. weighted tax deduction of more than 125% was decided for R&D activities

vehicle and component manufacturing

• Approval of foreign equity investment upto 100% for the manufacture of automobiles and aut

components.

• Policy proposed to fix the import tariffs in a way that the actual production within the country a

facilitated over mere assembly hence develop India as hub for small Cars

• Excise Duties :-

o The recommendation of promoting passenger cars of length upto 3.8 meters through exci

benefits

o Decision to hike up excise duty by 2%

• Vehicle manufacturers will also be considered for a rebate on the applicable excise duty for every 1%

the gross turnover of the company expended during the year on Research and Development carried eith

in-house under a distinct dedicated entity

• Freeing up of petrol prices and the subsequent rise in petro prices could impact the sales.

• Government decisions to reduce the import barriers of certain auto-components would help the OEM

shore up their production volumes

• In order to facilitate faster upgradation of environmental quality, the Govt. will consider having a termin

life policy for commercial vehicles alongwith incentives for replacement for such vehicles.

8/6/2019 Auto Auto Ancilliary

http://slidepdf.com/reader/full/auto-auto-ancilliary 11/40

• A number of tax incentives have been provided to benefit the investments in the country

• FTAs with ASEAN nation could lead to some OEMs moving to countries like Thailand for production whe

the costs are lower than in India thus impacting the local OEMs.

Govt.Spendings on different sectors

• Increased allocation on infrastructure development of the country will help in the sales of automobi

o Road Development

o Rail Development

o Port Infrastructure

o Power

Improvements in the above infrastructures would also help in the exports

• Policies like NREGA and others to distribute the wealth and develop rural india would increase thsales in the rural market.

8/6/2019 Auto Auto Ancilliary

http://slidepdf.com/reader/full/auto-auto-ancilliary 12/40

Outlook

Short Run

1. Demand to increase on back of good monsoons and onset of festival season.

2. Capacity constraints at Auto ancilliary units could impact the sales and production besides Maruti Suzu

also faces the production constraints which are improbable to be removed till 2012 when the new placomes up.

3. Introduction of new models by Toyota and Honda in A2 segment and by Volkwagen in A3 could boost t

sales

4. Withdrawl of Cash- for Clunkers scheme operating in Euro region could further impact the exports

Maruti and Hyundai which have led them to look for African and Latin nations

5. Shortage of skilled manpower could prove a detriment to the companies trying to increase the

production.

Long Run

1. Development of new factories would ease the capacity crunch currently faced by OEMs.

2. Forecasts of a double Dip recession could impact the sales

3. Stress on R&D by major automobiles giants will lead to products specifically designed for Indi

Consumers.

4. Development of Delhi – Mumbai corridor and other infrastructural programmes would boost the expo

and help in easy transport of vehicles.

5. With companies like TATA and M&M increasing looking for export markets as production bases throu

acquisitions of others companies the sales of these companies is bound to increase

6. Increased entry by car majors could erode the profitability and margins in the industry where the margi

are already very low.

7. Global OEMs could leverage their tie- ship with local suppliers to source components for their glob

operation from India and with global scenario improving this trend would be visible across.

8. Govt. decision to spend $ 1 trillion on infrastructure sector would benefit the majors operating in thHCV/LCV segment.

9. Still a high level of inflation could indirectly affect the sales due to tightening of monetory policies.

10. Prices of raw materials and petrol would play a significant role on how the sector shapes up as the

demand would increase with the economies moving out of recession.

11. With increasing stress on exports by CV majors the outlook seems to be positive.

8/6/2019 Auto Auto Ancilliary

http://slidepdf.com/reader/full/auto-auto-ancilliary 13/40

Auto Ancilliary

An Overview

The Indian auto component industry is one of India's sunrise industries with tremendous growth prospects. From

low-key supplier providing components to the domestic market alone, the industry has emerged as one of the ke

auto components centres in Asia and is today seen as a significant player in the global automotive supply chain.

India offers the advantage of low manufacturing costs due to economies of scale, low design, research and labou

costs and local sourcing of tools and components.

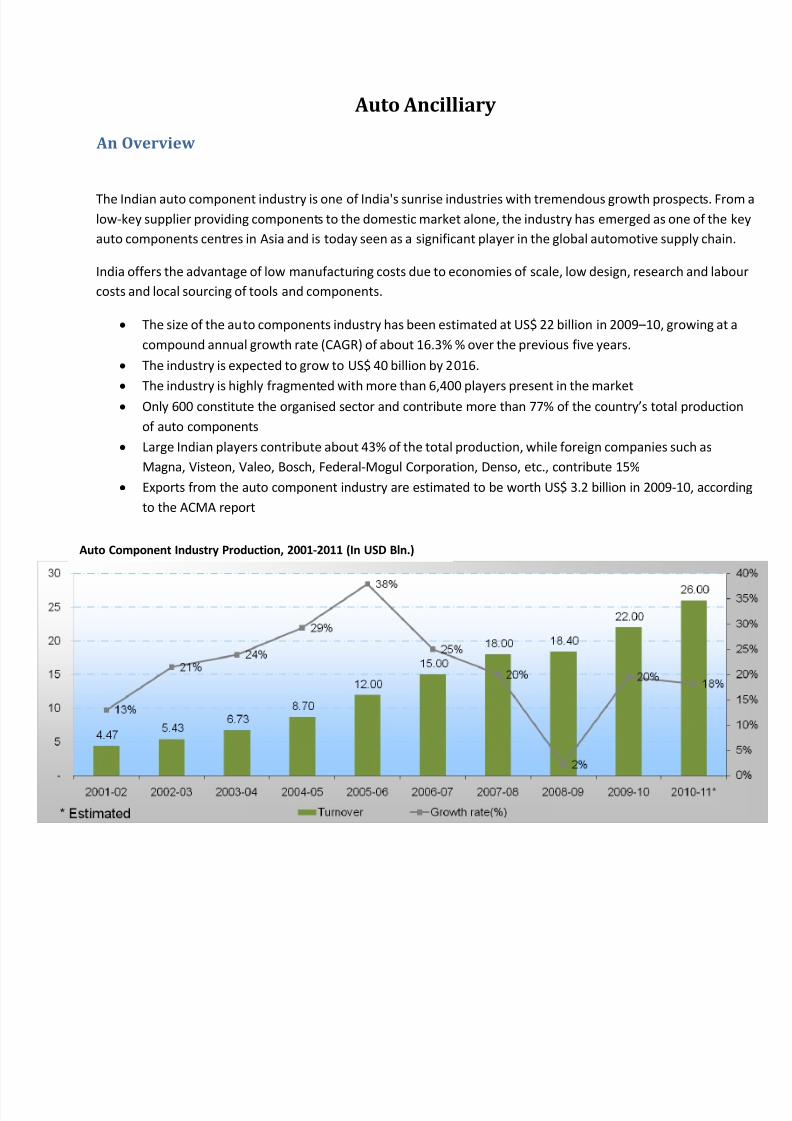

• The size of the auto components industry has been estimated at US$ 22 billion in 2009–10, growing at a

compound annual growth rate (CAGR) of about 16.3% % over the previous five years.

• The industry is expected to grow to US$ 40 billion by 2016.

• The industry is highly fragmented with more than 6,400 players present in the market

• Only 600 constitute the organised sector and contribute more than 77% of the country’s total production

of auto components

• Large Indian players contribute about 43% of the total production, while foreign companies such as

Magna, Visteon, Valeo, Bosch, Federal-Mogul Corporation, Denso, etc., contribute 15%

• Exports from the auto component industry are estimated to be worth US$ 3.2 billion in 2009-10, accordi

to the ACMA report

Auto Component Industry Production, 2001-2011 (In USD Bln.)

8/6/2019 Auto Auto Ancilliary

http://slidepdf.com/reader/full/auto-auto-ancilliary 14/40

Investments

• Investments in the auto component industry are estimated at US$ 9.0 billion in 2009-10, according to

ACMA

• The investments have increased steadily over the past 10 year period, increasing from USD 2.3 billion in

2001-02 to USD 9.0 billion in 2009-10

Auto Component Industry Investment, 2001-2010 (In USD Bln)

8/6/2019 Auto Auto Ancilliary

http://slidepdf.com/reader/full/auto-auto-ancilliary 15/40

Exports

• There has been a geographical market shift i.e. from supplying components to markets in developing

countries to exporting them to developed markets

o Europe accounted for 40.4 % of India's auto components exports in 2009-10, followed by Asia w

23.8 % and North America with 22.6 %.• The industry has witnessed a shift in the composition of exports over the years, with the original

equipment manufacturer (OEM/TIER 1) segment accounting for 80 % of exports in 2009-10

o The share of the aftermarket segment in auto component exports stood at 20% in the same year

Auto Component Exports, 2009-2010, by Geography

100%= USD 3.2 Bln

Auto Component Exports-Imports, 2003-2010, by Value (USD Bln)

8/6/2019 Auto Auto Ancilliary

http://slidepdf.com/reader/full/auto-auto-ancilliary 16/40

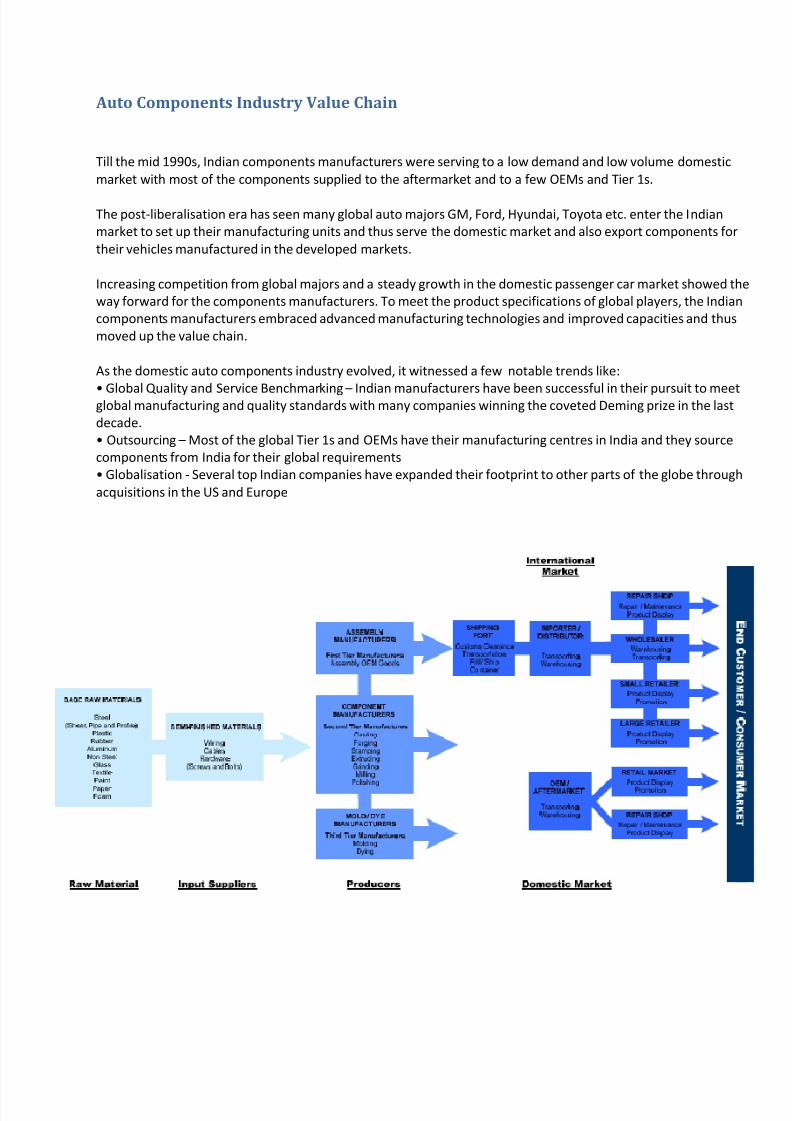

Auto Components Industry Value Chain

Till the mid 1990s, Indian components manufacturers were serving to a low demand and low volume domestic

market with most of the components supplied to the aftermarket and to a few OEMs and Tier 1s.

The post-liberalisation era has seen many global auto majors GM, Ford, Hyundai, Toyota etc. enter the Indian

market to set up their manufacturing units and thus serve the domestic market and also export components for

their vehicles manufactured in the developed markets.

Increasing competition from global majors and a steady growth in the domestic passenger car market showed th

way forward for the components manufacturers. To meet the product specifications of global players, the Indian

components manufacturers embraced advanced manufacturing technologies and improved capacities and thus

moved up the value chain.

As the domestic auto components industry evolved, it witnessed a few notable trends like:

• Global Quality and Service Benchmarking – Indian manufacturers have been successful in their pursuit to meetglobal manufacturing and quality standards with many companies winning the coveted Deming prize in the last

decade.

• Outsourcing – Most of the global Tier 1s and OEMs have their manufacturing centres in India and they source

components from India for their global requirements

• Globalisation - Several top Indian companies have expanded their footprint to other parts of the globe through

acquisitions in the US and Europe

8/6/2019 Auto Auto Ancilliary

http://slidepdf.com/reader/full/auto-auto-ancilliary 17/40

Industry Dynamics

Market Segments

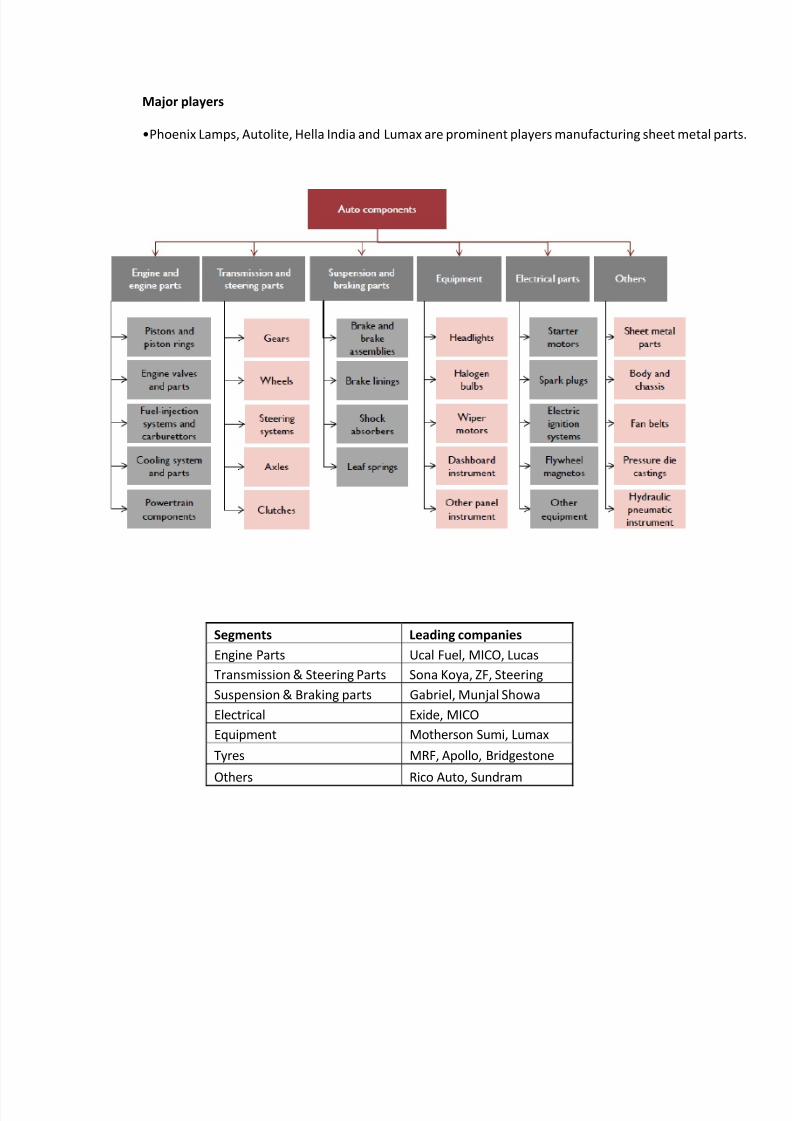

1. Engine parts comprise the largest product segment of the auto components industry with a 31 % production

share.

• The sub-segments include pistons, piston rings, engine valves, carburettors, fuel-delivery and cooling

systems and powertrain components.

Major players

•The four major players in the pistons sub-segment include Goetze, Shriram Pistons & Rings, India Piston

and SamkrgPistons, while RaneEngine Valves, KAR Mobiles and Shriram Pistons & Rings lead the engine

valves sub-segment.

•Ucal Fuel Systems and Spaco Carburettors & Escorts Auto Components are prominent players that

manufacture carburetors. In diesel-based fuel injection systems, Mico, Delphi, TVS Diesel System and Tat

Cummins are the major players.

2. Transmission and steering parts comprise the second-largest product segment in the Indian auto components

industry, with a 19 % production share.

•The sub-segment comprises gears, wheels, steering systems, axles and clutches.

Major players

•Sona Koyo Steering Systems, Rane Madras and Rane TRW Systems are the key players in steering

systems.

•Bharat Gears, Gajra Bevel Gears and Eicher are some of the major players in the gears sub-segment. Tw

international companies, GrazianoTrasmissioni and SlAP Gears India, have set up their base in India.

•Clutch Auto, Ceekay Daikin, Amalgamations Repco and Luk Clutches are the major players in the clutch

sub-segment. RaneBrake Lining and Rico Auto are the key players manufacturing clutch-facings.

•GKN Driveshafts (India) and Delphi cater to the drive shaft requirements of passenger cars and SonaKoySteering Systems services to the commercial vehicle segment.

3. Suspension and braking parts is the third-largest product segment with a 12 % production share.

•The primary sub-segments comprise brakes, brake assemblies, brake linings, shock absorbers and leaf

springs.

8/6/2019 Auto Auto Ancilliary

http://slidepdf.com/reader/full/auto-auto-ancilliary 18/40

•The demand share of the replacement market in this segment varies from 30 to 70 %, depending on the

product.

Major players

•Brakes India, KalyaniBrakes and Automotive Axles are the three major brake system suppliers in the

country.

•Rane Brake Lining, SundaramBrake Lining, Hindustan Composites and Allied Nippon dominate the brake

linings sub-segment.

•Jamna Auto and Jai Parabolic are the major manufacturers of leaf springs.

•Gabriel India, Delphi and Munjal Showa are the key manufacturers of shock absorbers.

4. Equipment is the fourth-largest product segment with a 10 % production share.

•The primary sub-segments include headlights, halogen bulbs, wiper motors, dashboard instruments,

switches, electric horns and other panel instruments.

•The demand share of the replacement market in this segment varies from 30 to 70 %.

Major players

•Lumax, Autoliteand Phoenix Lamps are the key players in the headlights sub-segment.

•Premiere Instruments and Controls is the leading player in the dashboard sub -segment.

•Jay Bharat Maruti, OmaxAuto and JBM Tools are the major players in the sheet metal parts sub-segmen

5. Electrical Parts is the fifth-largest product segment in the auto components industry, with a 9 % production shar

•The primary sub-segments comprise starter motors, generators, distributors, spark plugs, ignition coils,

flywheel magnetos, voltage regulators and electric ignition systems (EIS).

•The demand share of the replacement and export markets is low at about 25 %, while that of the OEM

segment is about 75 %.

Major players

•Lucas TVS, Denso, Delco Remy Electricals and Nippon Electricals are the key players in this segment.

6. Others (segment) is one of the fastest growing within the automotive components industry, with a 19 %

production share.

•The segment includes components such as sheet metal parts, pressure die castings, plastic moulded

components, fan belts and hydraulic pneumatic equipment.

8/6/2019 Auto Auto Ancilliary

http://slidepdf.com/reader/full/auto-auto-ancilliary 19/40

Major players

•Phoenix Lamps, Autolite, Hella India and Lumax are prominent players manufacturing sheet metal parts

Segments Leading companies

Engine Parts Ucal Fuel, MICO, Lucas

Transmission & Steering Parts Sona Koya, ZF, Steering

Suspension & Braking parts Gabriel, Munjal Showa

Electrical Exide, MICO

Equipment Motherson Sumi, Lumax

Tyres MRF, Apollo, Bridgestone

Others Rico Auto, Sundram

8/6/2019 Auto Auto Ancilliary

http://slidepdf.com/reader/full/auto-auto-ancilliary 20/40

Auto Component Industry Revenue Split, 2009-2010, by Component Group

8/6/2019 Auto Auto Ancilliary

http://slidepdf.com/reader/full/auto-auto-ancilliary 21/40

Macro-Factors Affecting Industry

Since the components industry is mostly dependant on the Auto industry for its demand, the macro-economic

factors affecting the industry are similar to that already discussed in the Auto section of the report.

Government Policy and Regulations

The increased commitment towards road infrastructure development is expected to increase the network of

highways and interstate roads. For personal segments such as cars and two-wheelers, it is expected to increase

connectivity in rural and upcountry area which will help generate more demand in these regions. Further, the

roads and highway development will be conducive to inter-city cargo movement, a key enabler for CV demand.

1. The National Strategy for Manufacturing

The policy drawn up by the National Manufacturing Competitiveness Council (NMCC), has identified the

automobile and auto components sector as one of the key areas for priority action. The government has

undertaken a number of initiatives to promote growth in this sector such as:

a) Auto Policy 2002

• The policy emphasizes on low emission fuel auto technologies and availability of appropriate auto

fuels to take auto manufacturing to a self-sustaining level.

• Foreign equity investment up to 100 % for manufacturing of auto components is permitted through

the automatic route. Manufacturing and imports in this sector are free from licencing and approvals

b) Automotive Mission Plan (AMP) 2006–2016

•The AMP 2006 –2016 aims to make India a preferred destination for designing and manufacturing

automobile and automotive components.

•It proposes to increase the output to US$ 145 billion and account for more than 10 % of the country’s

GDP.

• The plan envisages additional employment for 25 million people by 2016.

c) National Automotive Testing and R&D Infrastructure Project (NATRiP)

• The government has set up NATRiP at a total cost of US$ 388.5 million, to enable the industry to adopt

and implement global standards of vehicular safety, emission and performance standards.

• NATRiP will focus on enhancing the industry’s competitiveness by providing low-cost manufacturing an

product development.

8/6/2019 Auto Auto Ancilliary

http://slidepdf.com/reader/full/auto-auto-ancilliary 22/40

2. Department of Heavy Industries and Public Enterprise

• Initiatives such as increase of the deduction limit for Research and Development (R&D) in the sector from 15

200%, increased budgetary allocation for R&D activities and lowering of the duty regime have been

undertaken to further strengthen the capability of the sector.

• The department has also suggested the creation of a fund, worth US$ 0.2 billion (INR 10 billion), to

modernisethe auto components industry by providing an interest subsidy on loans and the purchase of new

plants and equipment.

3. De-reservation of items for small scale sector

• This will include extension of deemed export benefits to intermediate suppliers of auto components against

the duty free replenishment (DFR) scheme in the government’s EXIM Policy for 2004–05 .

• It is aimed at benefiting all auto component manufacturers to enable them to avail of duty drawbacks, refun

of terminal excise duties and an advance licence for duty free import of input.

4. Other incentives

• These include reduction of excise duty on smaller passenger vehicles and reduction in the duty levied on raw

material to 5 to 7.5 % from the earlier 10 %.

• Emission norms and environmental standards, in line with those of developed world, and enforcement of Eu

IV and Bharat Stage IV emission norms, have fostered the growth of the Indian auto components industry.

• By lowering Customs duty on some critical parts or sub-assemblies of electric vehicles, the Minister isencouraging the vehicle manufacturers working in this area to promote clean technology.

8/6/2019 Auto Auto Ancilliary

http://slidepdf.com/reader/full/auto-auto-ancilliary 23/40

Outlook

According to the ACMA-EY Vision 2020 study, India is expected to witness strong growth in vehicle productio

across all segments by 2020.

• Passenger vehicles - projected to be 5 million units by 2015 and over 9 million by 2020 driven by domest

demand and as a global hub for exports of small cars

• Commercial vehicles – volumes of over 1.4 million by 2015 and over 2.2 million by 2020. Small Commerc

Vehicles (SCV), a relatively new segment, expected to grow 28% annually over the next few years

• Two and three wheelers – expected to double to 22 million units by 2015 and reach 30 million by 2020 drive

by low penetration levels, expanding rural sales and growth in exports

• Tractors – projected to be over 0.7 million by 2015 and over 1 million by 2020 with steady growth expected

domestic and export volumes

• Construction equipment – likely to grow 2.5 times to 0.1million units by 2015 and almost double to 0.18 milli

by 2020 driven by the infrastructure sector

The Indian auto component industry can potentially grow to over USD 110 billion by the year 2020 driven in

tandem with the surge in vehicle production in the country. Of this, the domestic turnover can grow to USD 80

billion and exports scale up to another USD 29 billion.

The auto component industry can thus be an engine of India’s economic and manufacturing sector growth,

potentially contributing 3.6% of GDP by 2020, up from the current 2.1%. To achieve this potential the auto

component industry would require investments of over USD 35 billion during the period. It will also create

employment opportunity for over 1 million skilled people.

Increasing cost pressures is driving OEMs towards low cost country (LCC) sourcing. In order for the Indian

component manufacturers to stay competitive, among other things, they will have to move up the value chain.

Many different regions around the world are fast becoming centres for LCC sourcing; India will have to be wary o

these.

The Indian component industry must raise capital – strengthen balance sheets; scale capacities – manage costs

and flexibility of new assets; build R&D competence - product development, design and frugal engineering

capabilities; and build robust organizations - to manage significantly increased complexities and risks associated

with growth

8/6/2019 Auto Auto Ancilliary

http://slidepdf.com/reader/full/auto-auto-ancilliary 24/40

8/6/2019 Auto Auto Ancilliary

http://slidepdf.com/reader/full/auto-auto-ancilliary 25/40

Business Model

Ashok Leyland Ltd

ALL is the second-largest commercial vehicle manufacturer in India. The Hinduja Group holds 51% stake in the

company through a holding company Hinduja Automotive, UK. ALL has six manufacturing plants at four locations

in India: Ennore (Tamil Nadu), Hosur (Tamil Nadu), Alwar (Rajasthan) and Bhandara (Maharashtra). The companyfocused on the M&HCV segment and has a significant presence in the bus segment.

Quarterly Outlook

1) Being the second largest

player in commercial vehicle segment, Ashok Leyland is well positioned among the players. Going forwar

the company is expected to post good numbers due to positive factors like the increase in the freightrates, huge spending on infrastructure space and availability of finance

2) Ashok Leyland will able to cater to the northern market more effectively with its new plant in

Uttarakhand. The company has already started production from this plant, where it is also enjoying the

benefits on excise duty and income tax

3) Ashok Leyland was missing in LCV segment, but with the JVwith Nissan, it will be able to get the traction

the LCV segment. The company will introduce three models in LCV segment by 2HFY11

100% = Rs 8,035 Cr

Ashok Leyland Sales Break-up, by Value, FY 2010

Ashok Leyland CV Volume Break-up, by type, FY 2010

100% = 64,075 Units

Ashok Leyland CV Volume Break-up, by geography, FY 2010

100% = 64,075 Units

8/6/2019 Auto Auto Ancilliary

http://slidepdf.com/reader/full/auto-auto-ancilliary 26/40

Bharat Forge Ltd

Bharat Forge Ltd., the flagship company of the US $ 2.4 billion Kalyani Group, is a leading global ‘Full Service

Supplier’ of forged and machined - engine & chassis components. It is the largest exporter of auto components

from India and leading chassis component manufacturer in the world. Its manufacturing facilities are spread acro

11 locations and 5 countries - four in India, three in Germany, one each in Sweden, USA and two in China.

Quarterly Outlook

1. The strong growth in the domestic automotive segment along with the rising demand in the export mark

has been a strong supporter for the company’s growth. In FY10, the company had spent Rs 85 crore in th

restructuring of its subsidiaries. This has started to show positive results with all its major subsidiariesincluding FAW China contributing positively to the bottomline of the company. The operations in the US

market have seen completion of the restocking cycle. Going forward, this would signal a further demand

pick-up and rise in production.

2. The management has a strong growth outlook for the coming quarters with the machining mix envisage

to improve by around 50% from the present levels along with further improvement in topline contributio

from the non-automotive segment from the present 33% levels.

3. The management has also guided on the order visibility for its JV with Alstom from Q3FY10 onwards. The

facility being developed would have a high degree of indigenisation providing additional leverage to

handle competitors.

4. The company is also in talks with various OEMs domestically and internationally to promote the REVOLO

product developed in a JV with KPIT Cummins towards better emission controls and high fuel efficiency a

a cost effective price

00% = Rs 1,940 Cr

Bharat Forge Sales Break-up, by Value, FY 2010 Bharat Forge Sales Value Break-up, by Geography, FY 2010

100% = Rs 1,940 Cr

8/6/2019 Auto Auto Ancilliary

http://slidepdf.com/reader/full/auto-auto-ancilliary 27/40

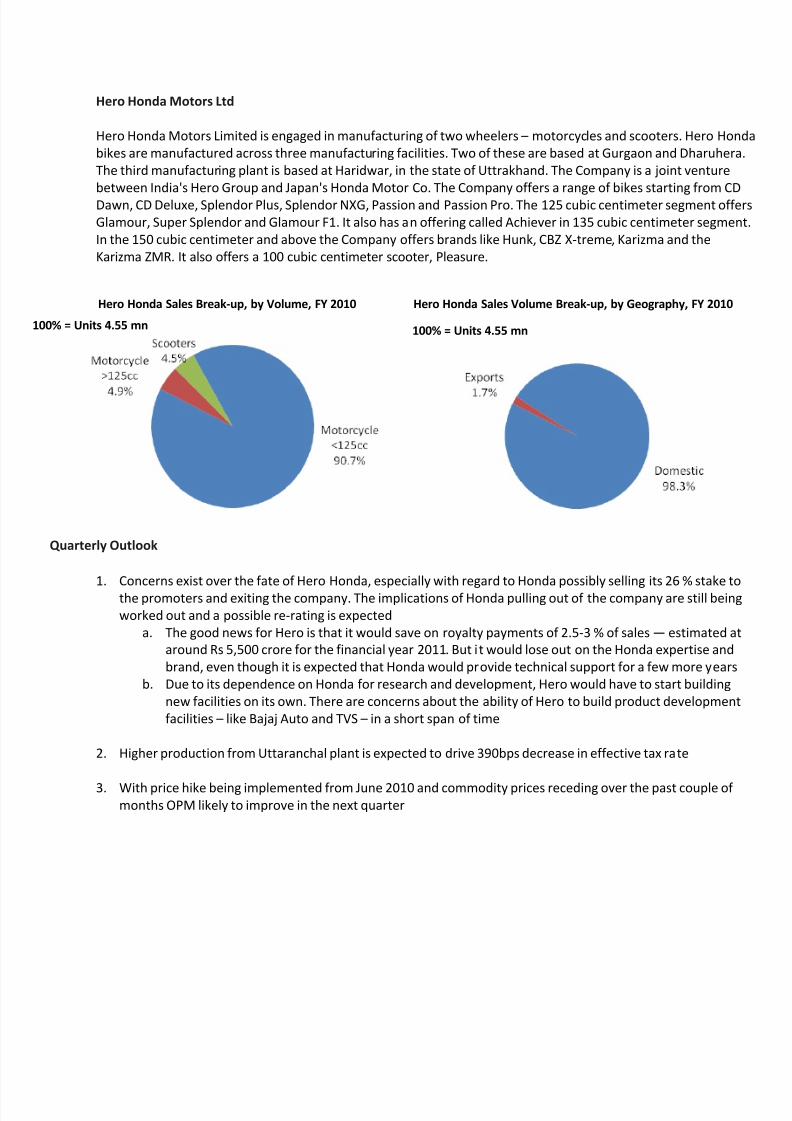

Hero Honda Motors Ltd

Hero Honda Motors Limited is engaged in manufacturing of two wheelers – motorcycles and scooters. Hero Hon

bikes are manufactured across three manufacturing facilities. Two of these are based at Gurgaon and Dharuhera

The third manufacturing plant is based at Haridwar, in the state of Uttrakhand. The Company is a joint venture

between India's Hero Group and Japan's Honda Motor Co. The Company offers a range of bikes starting from CD

Dawn, CD Deluxe, Splendor Plus, Splendor NXG, Passion and Passion Pro. The 125 cubic centimeter segment offe

Glamour, Super Splendor and Glamour F1. It also has an offering called Achiever in 135 cubic centimeter segmen

In the 150 cubic centimeter and above the Company offers brands like Hunk, CBZ X-treme, Karizma and the

Karizma ZMR. It also offers a 100 cubic centimeter scooter, Pleasure.

Quarterly Outlook

1. Concerns exist over the fate of Hero Honda, especially with regard to Honda possibly selling its 26 % stake to

the promoters and exiting the company. The implications of Honda pulling out of the company are still being

worked out and a possible re-rating is expected

a. The good news for Hero is that it would save on royalty payments of 2.5-3 % of sales — estimated at

around Rs 5,500 crore for the financial year 2011. But it would lose out on the Honda expertise and

brand, even though it is expected that Honda would provide technical support for a few more years

b. Due to its dependence on Honda for research and development, Hero would have to start building

new facilities on its own. There are concerns about the ability of Hero to build product development

facilities – like Bajaj Auto and TVS – in a short span of time

2. Higher production from Uttaranchal plant is expected to drive 390bps decrease in effective tax rate

3. With price hike being implemented from June 2010 and commodity prices receding over the past couple of months OPM likely to improve in the next quarter

Hero Honda Sales Break-up, by Volume, FY 2010 Hero Honda Sales Volume Break-up, by Geography, FY 2010

100% = Units 4.55 mn 100% = Units 4.55 mn

8/6/2019 Auto Auto Ancilliary

http://slidepdf.com/reader/full/auto-auto-ancilliary 28/40

8/6/2019 Auto Auto Ancilliary

http://slidepdf.com/reader/full/auto-auto-ancilliary 29/40

Escorts

Subsidiary

Escorts automotive ltd

Escorts construction equipement ltdEscorts agrimachinery USA

Escort asset management

Farmtrac tractors Europe

Farmtrac North America

Beaver Creak Holding

Revenue Break UP

year ended 30.09.2009 year ended 30.09.2008

Agri Machinery 1953.83 1968.92

Auto Ancilliary 86.63 89.04Railway Equipement 199.47 143.36

Construction Equipment 417.76 587.31

Others 39.97 43.69

Unallocated 6.94 6.13

Agri Machinery year ended 30.09.2009 year ended 30.09.2008

Domestic 3,47,010 3,46,501

Exports 38,214 43,553

8/6/2019 Auto Auto Ancilliary

http://slidepdf.com/reader/full/auto-auto-ancilliary 30/40

Company Outlook

• Good monsoon would lead to good sales in near future. Good presence in UP where good harvest of

sugarcane could lead to positive effect on sales

• Order from Tanzania , operations in morocco

• To launch 3 new models in the next 6 months in range(25-40 Hp which constitutes the bulk of tractor

market)

• Railway equipement segment not performing well and has impacted the revenue growth due to delays i

approval of orders

Railway just managed to break even –EBIT=1 ( 3rd quarter)

• An expected 3rd price rise in the quarter could affect the demand of the tractors as Mahindra is planning

raise the production output by 60% which could enable M&M to sell the tractors at lower price.

• Agri-business contributed around 75% of the revenues . Any impact on this part could affect the profit

margins as other segments are already underperforming

• Currently the plants run at 50% productivity level , so no problem of increasing the production levels due

to capacity constraints.

• Increase in demand of 2 and 4 wheelers and the capacity constraints of component supplier could benef

escort in the auto –component business in the quarter(capacity used<50%)

• Increased spending in the infra-space could help boost the sales of construction equipements.

• Currently the company is in construction currently material handling but now plans to manufacture

earthmoving equipment where volumes are high.

• Railways:-

New orders from govt

Diversifying into metro business

Looking at foreign markets(west European countries)

8/6/2019 Auto Auto Ancilliary

http://slidepdf.com/reader/full/auto-auto-ancilliary 31/40

TATA MOTORS

Revenue Breakdown from different companies

Key Subsidiaries

Net Revenue

FY09 FY10

JLR (GBP Mn) 4,974.00 6,555.00

Tata Daewoo CV Ltd., Korea (Rs. Mn) 26,437.00 26,789.00

Tata Technologies Ltd Consolidated (Rs. Mn) 12,024.30 10,703.80

HV Transmissions Ltd (Rs. Mn) 1,422.00 2,099.00

HV Axles Ltd (Rs. Mn) 1,546.00 2,401.00

Tata Motors Finance Ltd (Rs. Mn) 7,879.00 11,320.00

Businesses And Operations

Jaguar and Land Rover Business:

The company bought JLR operation from Ford Motors and the division is run as a separate entity from the ma

TATA motors. The company deals with luxury segment with Jaguar and SUV/MUV segement with Landrover a

RangeRover.

Area of sales-

Outlook

• European crisis will not have an immediate impact on JLR sales as it has a healthy Order Book. Howev

the order traffic has somewhat slowed down in Europe

• Economic recovery in the US and China is expected to offset the slowing European demand to som

extent. JLR has sold 25,000 units in China in FY2010. To broaden its foothold in China, JLR has set up

8/6/2019 Auto Auto Ancilliary

http://slidepdf.com/reader/full/auto-auto-ancilliary 32/40

National sales company in the region. The company has also seen revival in demand from Russia in the la

two months.

• Dependency for Supply of engines from Ford motors could impact the production of the vehicles

• Tata would integrate the networks at JLR to help achieve economies of scale and hence reduce operati

costs. Also Integration of design processes would help reduce the developmental costs for TATA besid

more initiative to source from low cost countries

• New and improved version of popular platforms to be launched and The company would also look

smaller entry-level cars under the Jaguar and Land Rover brand for higher volumes

Tata motors (Indian Operations)

Sources of Revenues

As seen around 85% of revenues come from the sale of vehicles both in domestic and export marketTata motors operates in the following segments in Indian auto sector

I Passenger Vehicles ( PVs )

A: Passenger Cars

B: Utility Vehicles(UVs)

C: Multi Purpose Vehicles (MPVs),Van type

II Commercial Vehicles (CVs)

M&HCVs

A: Passenger Carriers

B: Goods CarriersLCVs

A: Passenger Carriers

B: Goods Carriers

Sales segment Wise:-

8/6/2019 Auto Auto Ancilliary

http://slidepdf.com/reader/full/auto-auto-ancilliary 33/40

Category 2009-10 2008-09 % change

M&HCV 155,161 113,697 36.47LCVs* 218,681 151,676 44.18

Total CVs 373,842 265,373 40.87

Small Car (mini + compact) 158,093 115,160 37.28

Midsize Car 68,420 53,057 28.96

Utility Vehicle/SUV 33,507 39,295 -14.73

Total PVs 260,020 207,512 25.30

SEGMENTS:-

M&HCV

Outlook

• Investments in infra space and giving licenses to more coal mining operation and an overall improvi

industrial activity would increase the sales of trucks with higher tonnage

• Entry of foreign players like Japanese players—Isuzu and Hino—and two Chinese firms—FAW and Fot

would lead to an increase in competition and impacting the sales

• Tata Motors signs pact with Saudi bus operator. The company has signed an agreement with Saudi Arab

based Hafil Transport to supply 1,000 air-conditioned school buses. The order is valued at about $

million.

• Expanding capacity at our Dharwad bus plant and eyeing exports to Latin America, Egypt and Nigeria

• 1900 buses for CWG to provided by TATA

LCVs

Outlook

• The company plans to launch a new mini truck in this segment named “ Project Dolphin” and a new

carrier in this segment would help increase the sales. Introduction of Magic Iris and the micro-truck A

Zip.

• Investments to increase the productions of ACE to cater to the ASEAN and south asian markets

8/6/2019 Auto Auto Ancilliary

http://slidepdf.com/reader/full/auto-auto-ancilliary 34/40

• The company also has plans to start production of its mini-truck 'ACE' at its Dharwad plant which wou

help the company meet the increasing demands from LCV segment

Passenger Vehicles

Outlook

• New launch of cross over Aria and multi-purpose vehicle, Venture would help in the sales.

• Assistance from JLR in manufacturing of PVs would help in better quality cars and improving the bra

image which has been the major concern for TATA on satisfaction indexes.

• A continuous spate of fire incidents in NANO could affect the sales of NANO . Also a possible increase

prices of NANO could also impact the sales.

• Sales of PV segment would improve due to monsoon and festival season.

• Plans to reopen the bookings for NANO which could be bought directly without waitlist

8/6/2019 Auto Auto Ancilliary

http://slidepdf.com/reader/full/auto-auto-ancilliary 35/40

Apollo tyres

Apollo, Vredestein and Dunlop (in 30 countries in the African continent) are the three key brands. Others are Regal and Kaiz

(truckbus tyres), Maloya (passenger car) DuraTyres (retreaded tyres),

DuraTread (retreading material) and Acelere Wheelz (alloy wheels for passenger cars).

Apollo’s largest unit is in Limda, in the western Indian state of Gujarat. Two other units are located in the southern Indirubber-producing state of Kerala. These three together have a combined production of around 850 tonnes a day.

In South Africa, the Ladysmith and Durban plants account for a combined capacity of around 180 tonnes, and the Ensche

plant in the Netherlands adds another 150 tonnes a day.

Business Model

Apollo currently has three brands

1. Apollo

2. Vredestein

3. Dunlop

Revenue Segmentation

1. Apollo

The brand Apollo ie the main brand under the company caters to the Indian Market specifically

The breakdown of sales is given below

8/6/2019 Auto Auto Ancilliary

http://slidepdf.com/reader/full/auto-auto-ancilliary 36/40

The Apollo brand operates in 5 segments catering to PVs and CVs segment

Revenue from different products

Type

Revenues

2009-10 2008-09

Automobile Tyres 48,311 40,606

Automobile Tubes 4,648 3,816

Automobile Flaps 1,038 841

Alloy wheels 24 9

Pre-cured tread Rubber 236 224

8/6/2019 Auto Auto Ancilliary

http://slidepdf.com/reader/full/auto-auto-ancilliary 37/40

2. Apollo Vredestein BV

Brands

• Vredestein – premium brand

• Maloya – high value brand

Business Model

Caters basically to the European market with a minimal exports in Americas(US and Canada)

The brand caters mostly to the Replacement market but has 8% revenues from OEM with likes of Mercedes, Porsch

3. Dunlop Brand- African Market(SA)

The brand deals in 4 segments

• Passenger Car

• UV/ SUVs

• Trucks

• Earthmovers

Segmenting the Revenues

Revenue Segmentation by Market % Share

RM 81

OEM 1

Exports 18

Segment % Share

Passenger 36

Farm & OTR 51

Trucks 34

Light Trucks 24

Others 1

8/6/2019 Auto Auto Ancilliary

http://slidepdf.com/reader/full/auto-auto-ancilliary 38/40

Quarter Outlook

• Opening of Chennai plant(started operation in July 2010) would help in meeting excess demand

• Regarding truck radial tyres Apollo is a beginner in the market whereas JK tyres has a considerable presence in t

segment and is further investing to raise output to cater to increasing sales which could pose a challenge to Apollo

• 2nd

phase of capacity expansion had started in Jan2010 and is expected to materialize by this year and allow Apollo

expand its market.

• Currently caters to RM(71%) , which is a more volatile market than OEM even though the margins are higher in R

as there is no order booking in RM

• With the restriction on import of radial truck tyres lifted, imported tyres could flood the market affecting the loc

suppliers like Apollo. However further cuts have been ruled out(currently – 20%)

• With increase in demand of radial tyres OEMs are demanding lifting of duty on imported tires that may affect t

local suppliers if the decision is taken in the quarter.

• Supply of rubber would improve from October in Indian market after the monsoon that could ease the rubb

prices(monsoon affects the tapping process) , Increase in imports by Apollo of rubber would help balance of t

rubber prices in near term. Also with govt relaxing the import duty on rubber, it would further bring down the rubb

prices.

• Apollo is a supplier to Vehicle like VW Polo, GM Beat, Ford Figo whose sales could increase as OEMs launch ne

variants ( VW Venta) and Beat(CNG).

• 70-day long lock out at the Perambra unit of Apollo Tyres, near Thrissur, was withdrawn and plans to raise outp

from 308 to 340 tonnes per day which would prove beneficial in the sales

• With Scrappage policy over in most of EURO region cars sales have dropped which would affect the demand of ty

from Vredestein Banden BV

• With winter season approaching in Europe sales of specialty Winter tyres, could peak benefitting the Vredeste

Banden BV which is famous for winter tyres.

8/6/2019 Auto Auto Ancilliary

http://slidepdf.com/reader/full/auto-auto-ancilliary 39/40

Rico

Rico is a world-class engineering company supplying a wide range of high precision fully machined aluminum and ferrous

components and assemblies to automotive OEMs across the globe. Rico Auto operates mainly in the auto-components

business. Rico supplies aluminum and ferrous machined components and assemblies to original equipment manufacturers

(OEMs) across the globe.

JVs

FCC Rico

F.C.C. RICO is a joint venture company of F.C.C. Co. Ltd Japan and Rico Auto Industries Ltd. India established in February 199

with 50:50 share equity.

The company is exclusively into manufacturing & supplying of automobile clutch assemblies to O.E.M's of Two Wheelers and

Four Wheeler.

MAGNA Powertrain RICO

Oil & Water Pump (with Aluminum Housings) for Automotive Engines – India & Europe

RICO JINFEI

Aluminum Alloy Wheels for Two Wheelers

CONTINENTAL RICO

Products : Hydraulic Brake Products and Services for Vehicles of all Classes for OEMs in India

Sub Products

• Brake Calipers for Front and Rear Axles : 2 Million Units

• Drum Brakes : 1.5 Million Units

• Master Cylinders : 1 Million Units

• Actuation Units & Brake Boosters : 1 Million Units

• LSPV Load Sensing Proportioning Valves : 0.5 Million Units

Subsidiaries

Rico Auto Industries Inc. USA

This Company is engaged in the business of trading of Auto Components in the North American and Brazil

Rico Auto Industries (UK) Limited, U.K.

This Company is engaged in the business of trading of Auto Components for the European Markets.

Sources of revenues

8/6/2019 Auto Auto Ancilliary

http://slidepdf.com/reader/full/auto-auto-ancilliary 40/40

Company Revenues(2008-09)

Rico Auto Industries Limited 765.7

Rico Auto Industries Inc., USA 106.1

Rico Auto Industries (UK) Limited, UK 39.6

FCC Rico Limited 180.5

Continental Rico Hydraulic Brakes India Private Limited 1.4

Magna Rico Powertrain Private Limited 0.2

Segmentation of revenues

Product Sales(2008-09) Sales(2007-08)

AUTO PARTS 788.67 786.86

Mould & Dies 35.67 20.43

Others 3.28 2.76

Outlook

• Ramp of the Tata Nano (to which Rico is one of the key component suppliers) would also be a key revenue driver

going forward

• Hero Honda (46% of consolidated turnover), Maruti Suzuki (12%) are the key OEMs whose sales will increase leadin

to increase in sales of RICO

• It has a number of JVs in other countries and the recovery of global markets would help in sales increase

• However the company already operates at high level of productivity so increase in demand could lead to company

facing capacit constraints in the ne t q arter

Related Documents