Home / Individuals and families / Tax return / Deductions / Medical expenses / List of allowable medical expenses / Authorized medical practitioners by province or territory for the purposes of claiming medical expenses Canada Revenue Agency Authorized medical practitioners by province or territory for the purposes of claiming medical expenses The following list summarizes publicly available provincial and territorial information identifying those health care professionals authorized to practice as medical practitioners. This is not an all inclusive list of every profession that is authorized by each province or territory. For the most up to date information, see the provincial or territorial website that applies to you. Medical practitioners: A to E Medical practitioners: H to O Medical practitioners: P to T Medical practitioners: A to E Profession AB BC MB NB NL NS NT NU ON PE QC SK YT Acupuncturist ✔ ✔ ✔ ✔ ✔ Audiologist ✔ ✔ ✔ ✔ ✔ ✔ ✔ ✔ Chiropodist ✔ ✔ ✔ Chiropractor ✔ ✔ ✔ ✔ ✔ ✔ ✔ ✔ ✔ ✔ ✔ Combined lab and x-ray technologist ✔ Counselling therapist ✔ Dental assistant ✔ ✔ ✔ ✔ ✔ ✔ ✔ Dental hygienist ✔ ✔ ✔ ✔ ✔ ✔ ✔ ✔ ✔ ✔ ✔ ✔ ✔

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Home / Individuals and families / Tax return / Deductions / Medical expenses / List of allowable medical expenses / Authorized medical practitioners by province or territory for the purposes of claiming medical

expenses

Canada Revenue Agency

Authorized medical practitioners byprovince or territory for the purposes ofclaiming medical expensesThe following list summarizes publicly available provincial and territorial information identifyingthose health care professionals authorized to practice as medical practitioners. This is not anall inclusive list of every profession that is authorized by each province or territory.

For the most up to date information, see the provincial or territorial website that applies to you.

Medical practitioners: A to EMedical practitioners: H to OMedical practitioners: P to T

Medical practitioners: A to E

Profession AB BC MB NB NL NS NT NU ON PE QC SK YT

Acupuncturist ✔ ✔ ✔ ✔ ✔

Audiologist ✔ ✔ ✔ ✔ ✔ ✔ ✔ ✔

Chiropodist ✔ ✔ ✔

Chiropractor ✔ ✔ ✔ ✔ ✔ ✔ ✔ ✔ ✔ ✔ ✔

Combined lab andx-ray technologist

✔

Counsellingtherapist

✔

Dental assistant ✔ ✔ ✔ ✔ ✔ ✔ ✔

Dental hygienist ✔ ✔ ✔ ✔ ✔ ✔ ✔ ✔ ✔ ✔ ✔ ✔ ✔

elliottstone

Highlight

elliottstone

Highlight

elliottstone

Highlight

elliottstone

Highlight

elliottstone

Highlight

elliottstone

Highlight

elliottstone

Highlight

elliottstone

Highlight

elliottstone

Highlight

elliottstone

Highlight

elliottstone

Highlight

Dental nurse ✔

Dental technician ortechnologist

✔ ✔ ✔ ✔ ✔ ✔ ✔ ✔ ✔

Dental therapist ✔ ✔ ✔ ✔ ✔

Dentist ✔ ✔ ✔ ✔ ✔ ✔ ✔ ✔ ✔ ✔ ✔ ✔ ✔

Denturist, dentalmechanic,denturologist

✔ ✔ ✔ ✔ ✔ ✔ ✔ ✔ ✔ ✔ ✔ ✔ ✔

Dietician ✔ ✔ ✔ ✔ ✔ ✔ ✔ ✔ ✔ ✔

Emergency medicaltechnician

✔ ✔ ✔ ✔

Medical practitioners: H to O

Profession AB BC MB NB NL NS NT NU ON PE QC SK YT

Hearing aidpractitioner

✔ ✔ ✔ ✔ ✔

Kinesiologist ✔

Licensed orregistered practicalnurse

✔ ✔ ✔ ✔ ✔ ✔ ✔ ✔ ✔ ✔ ✔ ✔ ✔

Marriage and familytherapist

✔

Medical laboratorytechnologist

✔ ✔ ✔ ✔ ✔ ✔ ✔ ✔

Medical radiation

technologist

✔ ✔ ✔ ✔ ✔ ✔

Midwife ✔ ✔ ✔ ✔ ✔ ✔ ✔ ✔ ✔ ✔

Naturopath ✔ ✔ ✔ ✔ ✔ ✔

elliottstone

Highlight

elliottstone

Highlight

elliottstone

Highlight

elliottstone

Highlight

elliottstone

Highlight

elliottstone

Highlight

elliottstone

Highlight

elliottstone

Highlight

elliottstone

Highlight

elliottstone

Highlight

elliottstone

Highlight

elliottstone

Highlight

elliottstone

Highlight

elliottstone

Highlight

elliottstone

Highlight

elliottstone

Highlight

elliottstone

Highlight

elliottstone

Highlight

elliottstone

Highlight

elliottstone

Highlight

Naturopath ✔ ✔ ✔ ✔ ✔ ✔

Occupationaltherapist

✔ ✔ ✔ ✔ ✔ ✔ ✔ ✔ ✔ ✔

Ophthalmic medicalassistant

✔ ✔

Optician ✔ ✔ ✔ ✔ ✔ ✔ ✔ ✔ ✔ ✔

Optometrist ✔ ✔ ✔ ✔ ✔ ✔ ✔ ✔ ✔ ✔ ✔ ✔ ✔

Medical practitioners: P to T

Profession AB BC MB NB NL NS NT NU ON PE QC SK YT

Pharmacist ✔ ✔ ✔ ✔ ✔ ✔ ✔ ✔ ✔ ✔ ✔ ✔ ✔

Physician ✔ ✔ ✔ ✔ ✔ ✔ ✔ ✔ ✔ ✔ ✔ ✔ ✔

Physiotherapist orphysical therapist

✔ ✔ ✔ ✔ ✔ ✔ ✔ ✔ ✔ ✔ ✔

Podiatrist ✔ ✔ ✔ ✔ ✔ ✔ ✔

Professionaltechnologist inorthoses/prostheses

✔

Psychologicalassociate

✔ ✔ ✔

Psychologist ✔ ✔ ✔ ✔ ✔ ✔ ✔ ✔ ✔ ✔ ✔ ✔

Registered massagetherapist ormassage therapist

✔ ✔ ✔ ✔

Registered nurse

(including nursepractitioner)

✔ ✔ ✔ ✔ ✔ ✔ ✔ ✔ ✔ ✔ ✔ ✔ ✔

Registered nursingassistant

✔ ✔ ✔

elliottstone

Highlight

elliottstone

Highlight

elliottstone

Highlight

elliottstone

Highlight

elliottstone

Highlight

elliottstone

Highlight

elliottstone

Highlight

elliottstone

Highlight

elliottstone

Highlight

elliottstone

Highlight

elliottstone

Highlight

elliottstone

Highlight

elliottstone

Highlight

elliottstone

Highlight

elliottstone

Highlight

elliottstone

Highlight

elliottstone

Highlight

elliottstone

Highlight

elliottstone

Highlight

elliottstone

Highlight

elliottstone

Highlight

elliottstone

Highlight

elliottstone

Highlight

elliottstone

Highlight

assistant

Registerednutritionist

✔ ✔ ✔ ✔

Registeredpsychiatric nurse

✔ ✔ ✔ ✔ ✔

Respiratorytherapist

✔ ✔ ✔ ✔ ✔ ✔ ✔ ✔

Sexologist ✔

Social worker ✔ ✔ ✔ ✔ ✔ ✔ ✔ ✔ ✔ ✔

Speech languagepathologist

✔ ✔ ✔ ✔ ✔ ✔ ✔ ✔

Surgeon ✔ ✔ ✔ ✔ ✔ ✔ ✔ ✔ ✔ ✔ ✔ ✔ ✔

Traditional chinesemedicinepractitioner

✔ ✔

Date modified:2015-02-04

elliottstone

Highlight

elliottstone

Highlight

elliottstone

Highlight

elliottstone

Highlight

elliottstone

Highlight

elliottstone

Highlight

elliottstone

Highlight

elliottstone

Highlight

elliottstone

Highlight

elliottstone

Highlight

elliottstone

Highlight

Medical Expense Credit Quick Reference Table

M-1 Overview (Medical Expense Credit Quick Reference Table)

The Medical Expense Credit Quick Reference Table (M-2) lists and describes over 350 itemized expenses, stating if they do or do not qualify for the medical expense tax credit under section 118.2 of the Income Tax Act, and identifying the authority, including sections of the Income Tax Act and Income Tax Regulations, case law, CRA Views Documents, Interpretation Bulletins, Folio Views, Guides, and other relevant CRA publications. The table has been updated to include references to every paragraph of new Folio View S1-F1-C1: Medical Expense Tax Credit, which replaced IT-519R2. The table is intended to serve as a guideline only. Section 118.2 of the Act and the Income Tax Regulations should be consulted for precise wording, exceptions and restrictions.

At the end of the Medical Expense Credit Quick Reference Table is a summary of claimable attendant care or care in an establishment expenses reproduced from CRA Guide RC4064 (M-3), and a list of authorized medical practitioners by province or territory, reproduced from the CRA website (M-4).

M-2 – Itemized Expense List (Medical Expense Credit Quick Reference Table)

Last updated: December 2013

Item Qualifies Description of Medical Expense/Conditions for Qualification

Reference

Acne treatment Depends Cosmetic procedures to treat common acne would generally not qualify; however, cosmetic procedures to treat acne that is severe, persistent and disfiguring would be considered to have a medical or reconstructive purpose, and may qualify if the conditions in 118.2(2)(a) are met. See also “Cosmetic surgery”

118.2(2)(a), 118.2(2.1), 2011-0412591E5, S1-F1-C1 (paras 1.143-1.146)

Acoustic coupler Yes Amount paid for an acoustic coupler (prescription not required)

118.2(2)(i), CRA Guide RC4064

Acupuncturist Yes Amount paid to an acupuncturist licensed to practise under the laws of the province or territory as a medical practitioner. The CRA's view is that a person is authorized by the laws a jurisdiction to act as a medical practitioner if there is specific legislation that enables, permits or empowers a person to perform medical services and generally, such specific legislation provides for the licensing or certification of the practitioner as well as for the establishment of a governing body (eg, a college or board) with the authority to determine competency, enforce discipline and set basic standards of conduct. In Couture, an acupuncturist in Ontario was held not to be a “medical practitioner” as “authorized to practice”

118.2(2)(a), S1-F1-C1 (paras 1.20-1.23, 1.131),

2009-0337771E5, Couture, [2009] 2 C.T.C. 80 (FCA,

reversing the TCC), Murphy, [2010] 6 C.T.C. 2341 (TCC), Power, 2012 CarswellNat 977 (TCC),

2009-0337771E5

Item Qualifies Description of Medical Expense/Conditions for Qualification

Reference

means specifically authorized by legislation, not simply permitted. As well, in Power, acupuncture services performed by an unlicensed practitioner in Ontario were not eligible. However, in Murphy, an acupuncturist was held to be a “medical practitioner” in 2007 because Ontario had passed the Traditional Chinese Medicine Act (Couture was distinguished from Murphy by virtue of the enactment of the TCMA). The CRA looks for specific legislation that enables, permits or empowers a person to perform medical services

Air conditioner (prescribed)

Yes Amount paid for an air conditioner to cope with an individual's severe chronic ailment, disease or disorder qualify if prescribed by a medical practitioner. The claimable portion of the expense is limited to the lesser of: 1) $1,000 and 2) 50% of the amount paid for the air conditioner. The cost of electricity used to operate an air conditioner that qualifies for the medical expense credit is not eligible for the medical expense credit. A central air conditioner may qualify under this provision; 2009-0314751E5 (document numbers provided throughout this table refer to CRA Views Documents, available in TaxnetPro and TaxPartner)

118.2(2)(m), Reg 5700(c.3), 2007-

0251291I7, S1-F1-C1 (para 1.122)

Air filter, cleaner, or purifier (prescribed)

Yes Amount paid for an air filter, cleaner, or purifier for use by an individual who is suffering from a severe chronic respiratory ailment or a severe chronic immune system disregulation to cope with or overcome that ailment or disregulation qualify (prescription required). If an air exchanger and an air purifier are separate units such that each may be purchased separately (ie, the functions of purifying and exchanging the air are not engineered to work together inextricably as one unit), the CRA's view is that only the cost of the air purifier may qualify as a medical expense under 118.2(2)(m) and 5700(c.1). If the device acts as an air exchanger in addition to an air purifier, this fact will not generally preclude it from qualifying for the medical expense credit

118.2(2)(m), Reg 5700(c.1), 2002-0140205, 2010-0379331E5, S1-F1-

C1 (para 1.122)

No

Altered auditory feedback device (prescribed)

Yes Amount paid for an altered auditory feedback device designed to be used by an individual who has a speech impairment (prescription required)

118.2(2)(m), Reg 5700(z.1), S1-F1-C1 (para

1.122)

Item Qualifies Description of Medical Expense/Conditions for Qualification

Reference

Alternative medicine No The medications for which the medical tax credit is available must be prescribed by a medical practitioner

118.2(2)(n), Banman v. R., [2001] 2 C.T.C. 2111

(TCC) Ambulance service fees

Yes Amount paid for ambulance service fees for transportation to or from a public or licensed private hospital

118.2(2)(f), S1-F1-C1 (para 1.64)

Amount claimed under section 64 (disability supports deduction)

No An amount claimed under section 64 cannot be deducted under section 118.2. Section 64 allows a deduction for various eligible expenditures paid in the year by a disabled individual for services, devices, or supports that enable the individual to perform the duties of an office or employment, carry on a business, attend a designated educational institution or secondary school, or carry on research or similar work for which a grant was received. A section 64 deduction is generally limited to the amount of disability support costs paid in the year to enable a disabled individual to earn certain sources of income less reimbursements and other forms of assistance the disabled individual received in respect of the disability support cost. Individuals do not have to be eligible for the disability tax credit to claim a deduction under section 64 (except in the case of the deduction of part-time attendant care costs). Also, the disability tax credit can be claimed in addition to a deduction under section 64

64(a)A(iv), S1-F1-C3, S1-F1-C1 (para 1.148)

Anaesthetist fees (prescribed)

Yes Amount paid in respect of anaesthetist fees not covered by provincial health insurance (prescription required)

118.2(2)(o), S1-F1-C1 (para 1.130)

Animals (specially trained to assist impaired person)

Yes The cost of an animal specially trained to assist a patient who is blind or profoundly deaf or has severe autism, severe epilepsy or a severe and prolonged impairment that markedly restricts the use of the patient's arms or legs may qualify for the credit. The animal must be provided by a person or organization one of whose main purposes is such training of animals. Eligible expenses include amounts paid for the care and maintenance of such an animal, including food and veterinary care; for reasonable travel expenses of the patient incurred for the purpose of attending a school, institution or other facility that trains, in the handling of such animals, individuals who are so impaired; and for reasonable board and lodging expenses of the patient incurred for the purpose of the patient's

118.2(2)(l), S1-F1-C1 (para 1.92); 2010-0378461E5

Item Qualifies Description of Medical Expense/Conditions for Qualification

Reference

full-time attendance at a school, institution or other facility just described. A certificate from a medical practitioner that the animal is required by the patient is not required

Antiseptic No Amount paid for antiseptic 2009-0332141E5 Appointment cancellation fee

No A fee paid in respect of a missed appointment with a medical practitioner

118.2(2)(a), Zaffino, [2007] 5 C.T.C. 2560 (TCC)

Artecoll injections Depends For expenses incurred after March 4, 2010, expenses incurred for purely cosmetic procedures no longer qualify for the credit (unless required for medical or reconstructive purposes). See also “Cosmetic surgery”

118.2(2.1), CRA 2004-0078231I7, S1-F1-C1 (paras 1.143-1.146)

Artificial eye Yes Including expenses in respect of (prescription not required)

118.2(2)(i), S1-F1-C1 (paras 1.73-1.74)

Artificial kidney machine

Yes Amount paid for a kidney machine, including the cost of repairs, maintenance, and supplies; additions, renovations, or alterations to a home (the hospital official who installed the machine must certify in writing that the additions, renovations, or alterations were necessary for installation); the portion of the operating costs of the home that relate to the machine (excluding mortgage interest and CCA); a telephone extension in the dialysis room and all calls to a hospital for advice or to obtain repairs; and necessary and unavoidable costs to transport supplies. A prescription is not required

118.2(2)(i), CRA Guide RC4064, S1-F1-C1 (paras

1.73-1.74, 1.82-1.86)

Artificial limbs Yes Amount paid for an artificial limb, including the cost of repairs and parts and other expenses in respect of (prescription not required)

118.2(2)(i), S1-F1-C1 (paras. 1.73-1.74)

Assessment, medical Yes Costs for a medical assessment qualify if the fee is paid to a medical practitioner. If the fee is not paid to a medical practitioner, it may qualify if it is for diagnostic purposes (2011-0427011E5).

118.2(2)(a), (o), 2011-0427011E5

Associations Yes Payments made to partnerships, societies and associations for medical services rendered by their employees or partners qualify for the credit as long as the person who provided the service is a medical practitioner, dentist or nurse authorized to practice as a medical practitioner (for example, the Victorian Order of Nurses and The Canadian Red Cross Society Home Maker Services). The CRA has stated that “payments qualify only to the extent that they are for the period when the patient is at home. Payments for a period when the nurse is simply looking after a home and

118.2(2)(a), S1-F1-C1 (para 1.28)

Item Qualifies Description of Medical Expense/Conditions for Qualification

Reference

children when the patient is in hospital or otherwise away from home do not qualify since these would be personal or living expenses. In some instances, such as that of the Canadian Mothercraft Society, the visiting worker instead of the society may give the receipts but, if the worker can be regarded as a practical nurse, those receipts will be accepted.”

Athletic or fitness club fees

No Amounts paid for athletic or fitness club membership

CRA Guide RC4064, 2011-0402881E5, 2010-

0361011E5, Roberts, 2012 CarswellNat 3320

Attendant care (patient qualifies for the disability credit)

Yes Amount paid as remuneration for one full-time attendant for a patient who qualifies for the disability credit, or the cost of full-time care in a nursing home for such a patient, may qualify for the credit. At the time the remuneration is paid, the full-time attendant cannot be under 18 years of age or be the individual's spouse or common-law partner. It is the CRA's view that a taxpayer's private home would not be considered a “nursing home” for purposes of 118.2(2)(b). The CRA accepts that a particular place need not be a licensed nursing home but is of the view that it must have the equivalent features and characteristics of a nursing home (see 2007-0253621E5). If a patient claims the medical expense credit under 118.2(2)(b), the patient cannot claim the disability tax credit. See also under “Nursing home (full-time care)” and 2011-0418081E5, 2009-0346431E5, 2008-0285321C6, 2005-0142361E5. See also the summary of claimable attendant care expenses in Chapter 8

118.2(2)(b), CRA Guide RC4064, S1-F1-C1 (paras

1.31-1.39)

Attendant care at a retirement home, home for seniors, or other institution

Yes Amounts paid for attendant care at a retirement home, home for seniors, or other institution as remuneration for a full-time attendant may quality. A disability tax credit certificate is required. Also, the CRA requires a detailed statement from the establishment showing the amount paid for staff salaries that apply to attendant care services. Qualifying costs include: food preparation; housekeeping services for a resident's personal living space; laundry services for a resident's personal items; health care (registered nurse, practical nurse, certified health care aide, personal support worker); activities (social programmer); salon services (hairdresser, barber, manicurist, pedicurist), if included in the

118.2(2)(b), CRA Guide RC4064, S1-F1-C1 (paras

1.31-1.39), 2009-0346431E5

Item Qualifies Description of Medical Expense/Conditions for Qualification

Reference

monthly fee; transportation (driver); and security for a secured unit. Ineligible costs include: rent; food; cleaning supplies; other operating costs (such as the maintenance of common areas and outside grounds); and salaries and wages paid to the following employees: administrators; receptionists; groundskeepers; and janitors or maintenance staff. If a claim is made under 118.2(2)(b) rather than 118.2(2)(b.1) (limited to $10,000; see below), the disability tax credit cannot be claimed. See also the summary of claimable attendant care expenses in Chapter 8

Attendant care (part-time)

Yes Amounts paid as remuneration for part-time attendant care may qualify for the credit, The attendant cannot be the patients spouse or common-law partner and must be over 17 years of age when the amounts were paid. The care must be provided in Canada and a disability tax credit certificate (Form T2201) is required. Where amounts are paid to an establishment, the CRA requires a detailed statement from the establishment showing the amount paid for staff salaries that apply to attendant care services (all amounts paid to a nursing home generally qualify). The claim is limited to $10,000 (or $20,000 if the individual dies in the year). While most claims under 118.2(2)(b.1) will be for a part-time attendant, the CRA acknowledges that expenses for a full-time attendant may also be claimed under 118.2(2)(b.1). The $10,000 limit applies to each person paying for attendant care. A person can claim the disability credit and make a claim under 118.2(2)(b.1); however, where a claim is made under 118.2(2)(b.1), no part of the remuneration can be included in computing a deduction claimed in respect of the patient under section 63 or 64 or 118.2(2)(b), (b.2), (c), (d) or (e) for any taxation year. See under “Attendant care at a retirement home, home for seniors, or other institution” regarding qualifying costs (see also 2004-0101081E5)

118.2(2)(b.1), CRA Guide RC4064, S1-F1-C1 (paras

1.31-1.36, 1.40-1.43), 2006-0172181I7

Attendant care provided at a group home in Canada

Yes Amounts paid as remuneration for an individual's care or supervision provided in a group home in Canada maintained and operated exclusively for the benefit of individuals who have a severe and prolonged impairment may qualify. A disability tax credit certificate (Form T2201) is required. Also, the CRA requires a detailed statement from

118.2(2)(b.2), CRA Guide RC4064, S1-F1-C1 (paras

1.31-1.36, 1.44-1.46)

Item Qualifies Description of Medical Expense/Conditions for Qualification

Reference

the establishment showing the amount paid for staff salaries that apply to attendant care services. A claim under 118.2(2)(b.2) does not preclude a person from claiming the disability credit; however, where a claim is made under 118.2(2)(b.2), no part of the remuneration can be included in computing a deduction claimed in respect of the patient under section 63 or 64 or 118.2(2)(b), (b.1), (c), (d) or (e) for any taxation year. See also the summary of claimable attendant care expenses in Chapter 8

Attendant care in a self-contained domestic establishment (full-time)

Yes Amounts paid as remuneration for a full-time attendant at a person's personal residence may qualify for the credit. The attendant cannot be the patients spouse or common-law partner and must be over 17 years of age when the amounts were paid. Additionally, ether: 1) a disability tax credit certificate (Form T2201) is required or 2) a letter from a medical practitioner has to certify that the patient is likely to continue to be dependent on others for his or her personal needs and care for the long-term and needs a full-time attendant because of an impairment in mental or physical functions. Fees claimed must be for salaries and wages paid for attendant care services. If an individual issues the receipt for attendant care services, the receipt must include the attendant's social insurance number. Several attendants can qualify as one full-time attendant as long as there is only one attendant for any given period of time (2007-0253621E5). If a claim is made under 118.2(2)(c) rather than 118.2(2)(b.1) (limited to $10,000), the disability tax credit cannot be claimed. See also the summary of claimable attendant care expenses in Chapter 8

118.2(2)(c), CRA Guide RC4064, S1-F1-C1 (paras

1.31-1.36, 1.47-1.50)

Attendant care (full-time at a nursing home; patient lacks normal mental capacity)

Yes The cost of receiving full-time care in a nursing home is an eligible medical expense not only in respect of a patient with a severe and prolonged mental or physical impairment (see 118.2(2)(b)), but also in respect of a patient who is and will in the foreseeable future continue to be dependent on others for his/her personal needs and care because of a lack of normal mental capacity. Such a condition must be certified by a medical practitioner in either a letter or by completing Form T2201. An individual can generally claim the entire amount paid for full-time care in a nursing home. The care does not have to be

118.2(2)(d), CRA Guide RC4064, S1-F1-C1 (paras

1.31-1.36, 1.51-1.55), 2005-0149621E5, 2007-

0253621E5

Item Qualifies Description of Medical Expense/Conditions for Qualification

Reference

provided in Canada. Where a claim is made under 118.2(2)(d), the disability tax credit cannot be claimed (see para 118.3(1)(c)). Though the term “nursing home” in paragraph 118.2(2)(b) does not include a retirement residence even if it provides 24-hour nursing care (see Miles Estate v. R., [2000] 2 C.T.C. 2165), the CRA accepts that where a portion of retirement home costs is identified as being paid for attendant care, it will qualify under paragraph 118.2(2)(b.1) (2005-0142361E5). A taxpayer's home also does not qualify as a nursing home. See also the summary of claimable attendant care expenses in Chapter 8

Audible signal device Yes Amount paid for an audible signal device (prescription not required)

118.2(2)(i), CRA Guide RC4064, S1-F-C1 (paras

1.73-1.74, 1.80) Autistic child day care, school, institution or other place

Depends For an institute to qualify, the CRA's view is that certification would need to clearly indicate that the centre has specialized equipment, facilities, or trained personnel to provide care, or care and training, of a person with an autistic disorder

118.2(2)(e), 2010-0403181E5, 2004-

0065621E5, S1-F1-C1 (paras 1.31-1.36, 1.56-1.63)

Baby formula (prescribed)

No Amounts paid for baby formula, even if prescribed by a medical practitioner, do not qualify if it is also available over-the-counter (see also “Over-the-counter medications”).

118.2(2)(n), 2011-0399851E5

Baby wipes/moist wipes

No It is CRA's view that the reference to “other products” in 118.2(2)(i.1) is restricted to the same class of products as diapers, disposable briefs, etc. and would not include baby wipes or moist wipes

118.2(2)(i.1), 2010-0356391E5, 2012-

0437351E5, S1-F1-C1 (para 1.87)

Baby's cry signal device

See “Infants”

Balance disorder (prescribed device)

Yes Amount paid for a pressure pulse therapy device designed to be used by an individual who has a balance disorder (prescription required)

118.2(2)(m), Reg 5700(z.4), S1-F1-C1 (para

1.122) Bathroom aids See “Device or equipment (bathtub or shower)” Bicycle, battery-powered

No The CRA's view is that a battery powered two-wheeled bicycle cannot be considered a wheelchair

2009-0323571E5

Bicycle, motorized stationary

No The CRA’s view is that a motorized stationary bicycle (designed for people with medical conditions such as Parkinson’s disease, muscular dystrophy and arthritis) cannot be considered a device

2012-0440931E5

Birth control devices Depends The CRA has stated that birth control pills which a medical practitioner has prescribed are considered to qualify under 118.2(2)(n) if a

118.2(2)(n), S1-F1-C1 (para 1.127)

Item Qualifies Description of Medical Expense/Conditions for Qualification

Reference

pharmacist has recorded the prescription Bite-activated nipples for sippy-cup

No Amount paid for bite-activated nipples for sippy-cup

2009-0332141E5

Blind individuals (braille note-taker; prescribed)

Yes Amount paid for a braille note-taker designed to be used by a blind individual to allow them to take notes (that can be read back to them or printed or displayed in Braille) with the help of a keyboard and that is for the individual's use as prescribed by a medical practitioner (prescription required)

118.2(2)(m), Reg 5700(y), S1-F1-C1 (para 1.122)

Blind individuals (guide dog)

Yes The purchase of a guide dog for a blind individual from an institution that trains such dogs, as well as related expenses (for a list of qualifying expenses, see under “Animals”)

118.2(2)(l), S1-F1-C1 (para 1.92)

Blind individuals (intervening services)

Yes Amount paid for deaf-blind intervening services used by a person who is both blind and profoundly deaf and paid to someone in the business of providing such services

118.2(2)(l.44), S1-F1-C1 (para 1.106)

Blind individuals (optical scanner; prescribed)

Yes Amount paid for an optical scanner (or similar device) designed to be used by a blind individual to enable him to read print (prescription required)

118.2(2)(m), Reg 5700(l), S1-F1-C1 (para 1.122)

Blind individuals (reading software; prescribed)

Yes Amount paid for a device or software designed to be used to enable the individual to read print and that is for the individual's use as prescribed by a medical practitioner (prescription required)

118.2(2)(m), Reg 5700(l.1), S1-F1-C1 (para 1.122)

Blind individuals (special computer devices; prescribed)

Yes Amount paid for a device or equipment, including a synthetic speech system, Braille printer and large print-on-screen device, designed exclusively to be used by a person who is blind in the operation of a computer (prescription required)

118.2(2)(m), Reg 5700(o), CRA Guide RC4064, S1-

F1-C1 (para 1.122)

Bliss symbol board or similar device (prescribed)

Yes Amount paid for a bliss symbol board or similar device designed to be used to help an individual who has a speech impairment communicate by selecting the symbols or spelling out words (prescription required). The purchase of an iPad to assist certain special needs children would not qualify for the medical expense credit, nor would a digital camera used to make Bliss symbol boards (Henschel, 2010 CarswellNat 1783 (TCC))

118.2(2)(m), Reg 5700(x), 2010-0383021E5, S1-F1-

C1 (para 1.122)

Block fees Yes Block fee paid to a medical centre to cover the cost of certain ancillary or incidental uninsured medical services

118.2(2)(a), 2007-0255741I7, S1-F1-C1 (para

1.29) Blood coagulation monitors (prescribed)

Yes Prescribed blood coagulation monitor for individuals who require anti-coagulation therapy, including associated disposable peripherals such as pricking devices, lancets and test strips

118.2(2)(m); Reg 5700(s.1), S1-F1-C1 (para

1.122)

Item Qualifies Description of Medical Expense/Conditions for Qualification

Reference

Blood pressure monitors

No Purchase of a blood pressure monitor CRA Guide RC4064

Blood transfusion (prescribed)

Yes Amount paid for a blood transfusion (prescription required)

CRA Guide RC4064, 118.2(2)(a)

Bone conduction receiver

Yes Purchase of a bone conduction receiver (prescription not required). See also “Hearing aid”

118.2(2)(i), CRA Guide RC4064, S1-F1-C1 (para

1.80) Bone marrow transplant

Yes Reasonable amounts paid to locate a compatible donor, to arrange the transplant including legal fees and insurance premiums, and reasonable travelling costs including board and lodging for the patient, the donor, and their respective companions

118.2(2)(l.1), S1-F1-C1 (paras 1.93, 1.147)

Boots (Orthopaedic) See “Brace (including related costs)” and “Orthopaedic shoe or boot (and an insert for a shoe or boot)”

Botox injections Depends For expenses incurred after March 4, 2010, expenses incurred for purely cosmetic procedures no longer qualify for the credit (unless required for medical or reconstructive purposes). See also “Cosmetic surgery”

118.2(2.1), 2004-0078231I7, S1-F1-C1 (paras 1.143-1.146)

Brace (for a limb) Yes Amounts paid for braces for a limb, including woven or elasticized stockings made to measure, qualify for the credit (prescription not required). The CRA has stated that “a “brace for a limb” does not necessarily have to be something of a rigid nature, although at least one of the functions of the brace must be to impart some degree of rigidity to the limb which is being braced. Accordingly, that phrase is considered to include woven or elasticized stockings where these are of a kind that are carefully fitted to measurement or are made to measure. When a brace for a limb is necessarily built into a boot or shoe in order to permit a person to walk, the brace will be considered to include the boot or shoe. A rehabilitative splinting system to stretch the tissue in the elbow would likely qualify as a “brace for a limb” (2011-0429871E5).

118.2(2)(i), CRA Guide RC4064, S1-F1-C1 (paras

1.73-1.74, 1.77)

Brace (spinal) Yes Amount paid for a spinal brace (prescription not required)

118.2(2)(i), S1-F1-C1 (paras 1.73-1.74)

Braille note-taker See “Blind individuals” Braille printer See “Blind individuals” Breast prosthesis See “External breast prosthesis” Breast pump No Purchase of a breast pump 2007-0248701E5 Buzzer See “Hearing aid”

Item Qualifies Description of Medical Expense/Conditions for Qualification

Reference

Canadian Red Cross Society Home Maker Services

See “Associations”

Cancellation fee See “Appointment cancellation fee” Cancer treatment Yes Cost of cancer treatments provided by a medical

practitioner, including treatment received outside Canada for drugs not approved in Canada.

118.2(2)(a), CRA Guide RC4064

Car seat No An infant car seat, even if specially designed for a disabled child

2003-0046145

Cardiograph (prescribed)

Yes Amount paid in respect of cardiograph tests not covered by provincial health insurance (prescription required)

118.2(2)(o), CRA Guide RC4064

Care or care and training at institutions or other places

Yes Amounts paid for care at an institution or other place may qualify for the credit. An “appropriately qualified person” (normally a medical practitioner; preferably who does not work for the institution) has to certify in writing that the person has an impairment in mental or physical functions and confirm the person “requires” the equipment, facilities, or personnel available at the establishment. A private home adapted to the needs of its owner/occupant would not qualify as an “other place” for purposes of 118.2(2)(e) (2007-0253621E5). A retirement home was found to qualify in McKinley, [2004] 2 C.T.C. 2672 (TCC), but not in Lister, [2007] 1 C.T.C. 137 (FCA) or in Shultis, [2007] 1 C.T.C. 2182 (TCC). The expense of renting an accommodation near the school or institution would not qualify; however, transportation expenses to and from the school may qualify under 118.2(2)(g) (2009-0349551E5).

118.2(2)(e), CRA Guide RC4064, S1-F1-C1 (paras

1.31-1.36, 1.56-1.63)

Care or care and training at special schools

Yes Amounts paid for care or training at a school may qualify for the credit. An “appropriately qualified person” (normally a medical practitioner; preferably who does not work for the school) has to certify in writing that the person has an impairment in mental or physical functions and confirm the person “requires” the equipment, facilities, or personnel available at the establishment. Under former 110(1)(c)(vi), private school fees incurred for a child with behavioral problems were held to be ineligible (see Somers v. MNR, [1979] C.T.C. 2001 (TRB)) since there was no evidence of mental or physical handicap and the school in question was not an institution of the type specified. Also, in Flower

118.2(2)(e), CRA Guide RC4064, S1-F1-C1 (paras

1.31-1.36, 1.56-1.63), 2006-0213231E5, Scott,

[2009] 1 C.T.C. 224 (FCA)

Item Qualifies Description of Medical Expense/Conditions for Qualification

Reference

v. R., [2005] 2 C.T.C. 2730 (TCC), fees to anAcademy for children with learning disabilities did not qualify. However, in Rannelli v. MNR, [1991] 2 C.T.C. 2040, the Court concluded that fees paid to a school for dyslexic children qualified under former 110(1)(c)(vi). Fees paid to a disciplinary school for children with attention disorders were found to qualify in Marshall, [2003] 4 C.T.C. 2794 (TCC). Fees paid to the Calgary Academy qualified in Karn, 2013 CarswellNat 1382, since the school was only for students with learning disabilities; however, tuition fees paid did not qualify in Bauskin, 2013 CarswellNat 342, because there was no evidence of special equipment, facilities or personnel in the school’s mainstream program.

Caregiver training Yes An amount paid for reasonable expenses (other than amounts paid to a person who was at the time of the payment the individual's spouse or common-law partner or a person under 18 years of age) to train the individual (or a person related to the individual) if the training relates to the mental or physical infirmity of a person who is related to the individual and is a member of the individual's household (or is dependent on the individual for support)

118.2(2)(l.8), S1-F1-C1 (paras 1.113-1.114)

Catheters and catheter trays

Yes Amounts paid for catheters and catheter trays required by the patient by reason of incontinence caused by illness, injury or affliction (including catheter trays, tubing, or other products required for incontinence caused by illness, injury, or affliction); a prescription is not required

118.2(2)(i.1), CRA Guide RC4064, S1-F1-C1 (para

1.87)

Certificates Yes Amount paid to a medical practitioner for completing and providing additional information in regard to Form T2201 and other certificates

118.2(2)(a), CRA Guide RC4064

Chair (power-operated)

See “Power-operated guided chair”, “wheelchair”, and “Scooter”

Chiropodist (or podiatrist)

Yes Amount paid to a chiropodist (or podiatrist) licensed to practise under the laws of the province or territory as a medical practitioner

118.2(2)(a), S1-F1-C1 (paras 1.20-1.23)

Chiropractor Yes Amount paid to a chiropractor licensed to practise under the laws of the province or territory as a medical practitioner

118.2(2)(a), S1-F1-C1 (paras 1.20-1.23)

Christian Science practitioner

No Payments to a Christian Science practitioner where the practitioner is not otherwise a medical doctor or a nurse acting within the scope of his or her profession (none of the provinces or territories

118.2(2)(a), 2006-0180991M4, 2005-0126931E5, 2006-0180991M4, 2007-

Item Qualifies Description of Medical Expense/Conditions for Qualification

Reference

license Christian Science practitioners as being medical practitioners). Amounts paid to a Christian Science nurse authorized to practise as a nurse according to the relevant laws referred to in subsection 118.4(2) would qualify. The CRA's view is that a person is authorized by the laws of a jurisdiction to act as a medical practitioner if there is specific legislation that enables, permits or empowers a person to perform medical services and generally, such specific legislation provides for the licensing or certification of the practitioner as well as for the establishment of a governing body (eg, a college or board) with the authority to determine competency, enforce discipline and set basic standards of conduct

0224311E5, 2009-0337771E5, S1-F1-C1

(paras 1.20-1.23)

Circumcision procedure

Depends Cost of infant male circumcision would generally qualify if it can be shown that it is not done purely for cosmetic purposes

118.2(1), 118.2(2.1), 2011-0411641E5, S1-F1-C1

(paras 1.143-1.146) Clinic or corporation (amount paid for medical services)

Yes Amounts paid to a clinic or corporation for medical services provided by or supervised by a medical practitioner

118.2(2)(a), Mudry, 2008 CarswellNat 715 (TCC), 2003-0045561E5, 2010-0361011E5, S1-F1-C1

(para 1.28) Clinical counsellor See “Counsellor” Cochlear implant Yes Amount paid for a cochlear implant (prescription

not required) 118.2(2)(i), CRA Guide RC4064, S1-F1-C1 (para

1.80) Colostomy and ileostomy pads

Yes Amount paid for colostomy and ileostomy pads, including pouches and adhesives (prescription not required)

118.2(2)(i), CRA Guide RC4064, S1-F1-C1 (paras

1.73-1.74, 1.78) Commodes See “Device or equipment (bathtub, shower or

toilet)” Compression stockings

Depends Cost of compression stockings required to be worn after treatment for varicose veins would qualify if fitted to measurement or made to measure

118.2(2)(i), S1-F1-C1 (para 1.77), 2011-0411181E5

Contact lenses (prescribed)

Yes Amount paid for contact lenses (prescription required from a medical practitioner or optometrist)

118.2(2)(j), CRA Guide RC4064, S1-F1-C1 (para

1.89) Cosmetic surgery (purely cosmetic procedures)

No After March 4, 2010, expenses incurred for purely cosmetic procedures no longer qualify for the credit. This generally includes surgical and non-surgical procedures purely aimed at enhancing one's appearance, such as the following: augmentations (such as chin, cheek, lips); body modifications (such as tongue splits); body

118.2(2.1) 2004-0078231I7, 2006-

0180991M4, 2010-0362981M4, 2010-0365801E5, 2011-0429431E5, 2012-

0448691E5, S1-F1-C1

Item Qualifies Description of Medical Expense/Conditions for Qualification

Reference

shaping, contouring or lifts (such as breasts, buttocks, face and stomach); botulinum injections; chemical peels; implants (such as jewellery implanted into an eye or a tooth, or microdermal, transdermal, and subdermal cosmetic implants); filler injections for removal of wrinkles; hair removal and replacement procedures; laser treatments (such as skin resurfacing and removal of age spots); liposuction; reshaping procedures (such as rhinoplasty and otoplasty); rib removal; tattoo removal; and teeth whitening, contouring or reshaping. A cosmetic procedure will continue to qualify if required for medical or reconstructive purposes (see directly below). The CRA's former position was that an amount paid to a medical practitioner for surgery of any kind, whether cosmetic or elective, generally qualified as a medical expense.

(paras 1.143-1.146)

Cosmetic surgery (for medical or reconstructive purposes)

Yes After March 4, 2010, expenses incurred for purely cosmetic procedures no longer qualify for the credit. A cosmetic procedure will continue to qualify if required for medical or reconstructive purposes (for example, those that would ameliorate a deformity arising from, or directly related to, a congenital abnormality, a personal injury resulting from an accident or trauma, or a disfiguring disease), including the following: breast implant and related procedures for reconstructive purposes after a mastectomy; breast reduction to reduce back and shoulder pain; dental braces, if required to correct a misaligned bite; dental veneers to correct decayed or misaligned teeth; gastric bypass surgery, gastric sleeve surgery or gastric stapling; laser eye surgery; removal of excess skin after rapid weight loss due to a risk of infection; and the treatment of melasma that is severe, persistent and disfiguring. The cost of sex reassignment surgery and related surgeries would likely qualify (2012-0463201E5). The CRA's former position was that and amount paid to a medical practitioner for surgery of any kind, whether cosmetic or elective, generally qualified as a medical expense.

118.2(2.1) 2004-0078231I7, 2010-

0362981M4, 2010-0365801E5, 2010-0378051E5, 2012-0439481E5, 2013-

0480831E5, S1-F1-C1 (paras 1.143-1.146)

Counsellor Depends The CRA has stated that counselling services are considered to qualify if: 1) the counsellor is working in a recognized mental health clinic, community agency or hospital; 2) the counsellor

2002-0171795, 2005-0153591E5, 2006-

0213231E5

Item Qualifies Description of Medical Expense/Conditions for Qualification

Reference

is a member of an association governing their profession; and 3) the treatment is at the request of, or in association with, a medical practitioner

Courses, pain management

Yes Expenses related to pain management courses if incurred for diagnosis, therapy or rehabilitation purposes in relation to a pre-existing medical problem and paid to a certified medical practitioner or public or private hospital.

2011-0397731E5

Crutches Yes Amount paid for crutches, including related costs (prescription not required)

118.2(2)(i), S1-F1-C1 (paras 1.73-1.74)

Cushion (wheelchair or bath

Depends Amount paid for a wheelchair cushion would qualify as a medical expense, but amount paid for a bath cushion would not

118.2(2)(i), S1-F1-C1 (paras 1.73-1.74), 2010-

0361221E5 Cycle monitoring fees (prescribed)

Yes Amount paid in respect of cycle monitoring fees not covered by provincial health insurance (prescription required), including diagnostic procedures relating to cycle monitoring fees

118.2(2)(o), S1-F1-C1 (para 1.130), 2011-

0401711E5

Deaf individual (intervening services)

Yes Amount paid for deaf-blind intervening services used by a person who is both blind and profoundly deaf and paid to someone in the business of providing such services

118.2(2)(l.44), S1-F1-C1 (para 1.106)

Deaf individual (teletypewriter; prescribed)

Yes Amount paid for a teletypewriter or similar device, including a telephone ringing indicator, that enables a deaf or mute individual to make and receive telephone calls (prescription required)

118.2(2)(m), Reg 5700(k), S1-F1-C1 (para 1.122)

Dental appliance (used to treat sleep apnea)

Yes Amount paid for a dental appliance would qualify as a medical expense if the individual is suffering from a “severe chronic respiratory ailment” and the dental appliance was “designed exclusively for use by” the individual for that ailment.

118.2(2)(m), Reg 5700(c), 2011-0429541E5, S1-F1-

C1 (para 1.122)

Dental crowns Yes Amount paid to a dentist or medical practitioner for dental crowns

118.2(2)(a), 2010-0362981M4

Dental hygienist Yes Amount paid to a dental hygienist licensed to practise under the laws of the province or territory as a medical practitioner

118.2(2)(a), S1-F1-C1 (paras 1.20-1.23)

Dental implants Yes Amount paid to a dentist or medical practitioner for dental implants

118.2(2)(a), 2006-0218021E5, 2011-

0397151E5 Dentist Yes Amount paid for dental services 118.2(2)(a), S1-F1-C1

(paras 1.20-1.23) Dentures Yes Amount paid to a person authorized under the

laws of a province to carry on the business of a dental mechanic for the making or repairing of an upper or lower denture, or for the taking of

118.2(2)(p), S1-F1-C1 (para 1.132)

Item Qualifies Description of Medical Expense/Conditions for Qualification

Reference

impressions, bite registrations and insertions in respect of the making, producing, constructing and furnishing of an upper or lower denture (prescription not required)

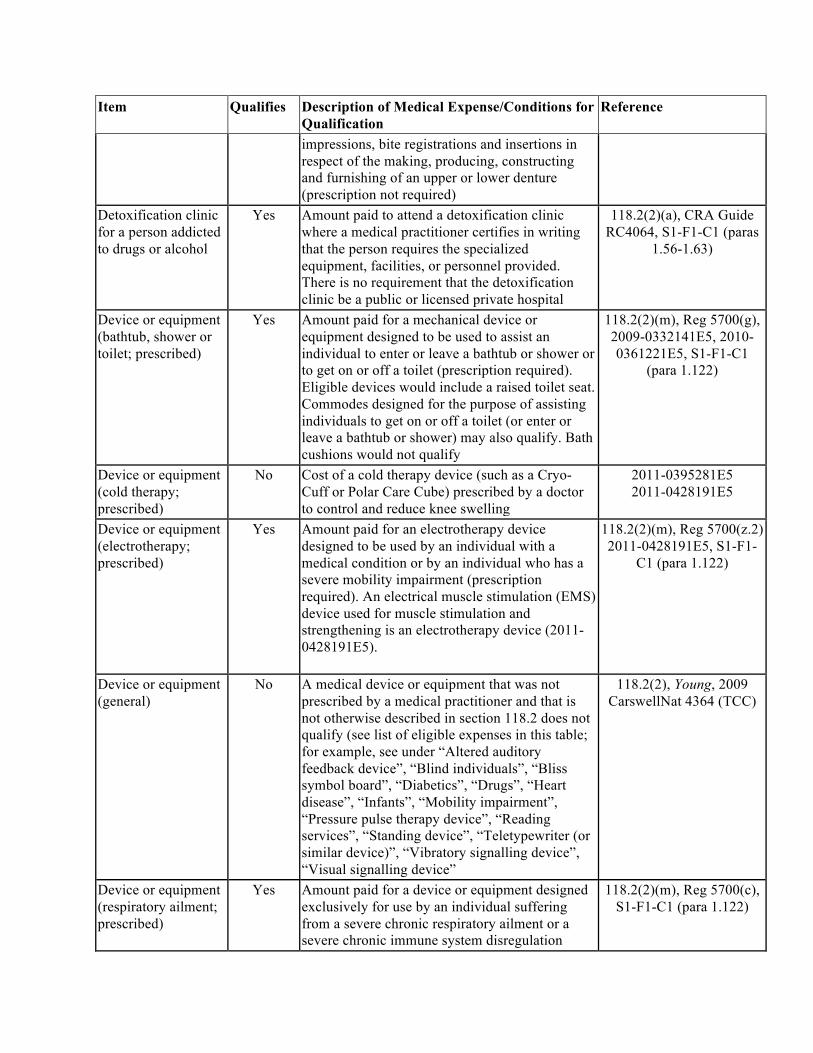

Detoxification clinic for a person addicted to drugs or alcohol

Yes Amount paid to attend a detoxification clinic where a medical practitioner certifies in writing that the person requires the specialized equipment, facilities, or personnel provided. There is no requirement that the detoxification clinic be a public or licensed private hospital

118.2(2)(a), CRA Guide RC4064, S1-F1-C1 (paras

1.56-1.63)

Device or equipment (bathtub, shower or toilet; prescribed)

Yes Amount paid for a mechanical device or equipment designed to be used to assist an individual to enter or leave a bathtub or shower or to get on or off a toilet (prescription required). Eligible devices would include a raised toilet seat. Commodes designed for the purpose of assisting individuals to get on or off a toilet (or enter or leave a bathtub or shower) may also qualify. Bath cushions would not qualify

118.2(2)(m), Reg 5700(g), 2009-0332141E5, 2010-0361221E5, S1-F1-C1

(para 1.122)

Device or equipment (cold therapy; prescribed)

No Cost of a cold therapy device (such as a Cryo-Cuff or Polar Care Cube) prescribed by a doctor to control and reduce knee swelling

2011-0395281E5 2011-0428191E5

Device or equipment (electrotherapy; prescribed)

Yes Amount paid for an electrotherapy device designed to be used by an individual with a medical condition or by an individual who has a severe mobility impairment (prescription required). An electrical muscle stimulation (EMS) device used for muscle stimulation and strengthening is an electrotherapy device (2011-0428191E5).

118.2(2)(m), Reg 5700(z.2) 2011-0428191E5, S1-F1-

C1 (para 1.122)

Device or equipment (general)

No A medical device or equipment that was not prescribed by a medical practitioner and that is not otherwise described in section 118.2 does not qualify (see list of eligible expenses in this table; for example, see under “Altered auditory feedback device”, “Blind individuals”, “Bliss symbol board”, “Diabetics”, “Drugs”, “Heart disease”, “Infants”, “Mobility impairment”, “Pressure pulse therapy device”, “Reading services”, “Standing device”, “Teletypewriter (or similar device)”, “Vibratory signalling device”, “Visual signalling device”

118.2(2), Young, 2009 CarswellNat 4364 (TCC)

Device or equipment (respiratory ailment; prescribed)

Yes Amount paid for a device or equipment designed exclusively for use by an individual suffering from a severe chronic respiratory ailment or a severe chronic immune system disregulation

118.2(2)(m), Reg 5700(c), S1-F1-C1 (para 1.122)

Item Qualifies Description of Medical Expense/Conditions for Qualification

Reference

(prescription required). An air conditioner, humidifier, dehumidifier, heat pump or heat or air exchanger specifically does not qualify under Regulation 5700(c)

Diabetics (blood sugar measure; prescribed)

Yes Amount paid for a device designed to enable individual to measure blood sugar level (prescription required)

118.2(2)(m), Reg 5700(s), S1-F1-C1 (para 1.122)

Diabetics (infusion pump; prescribed)

Yes Infusion pump (including disposable peripherals) for the treatment of diabetes (prescription required)

118.2(2)(m), Reg 5700(s), S1-F1-C1 (para 1.122)

Diabetics (insulin) Yes The cost of insulin or substitutes, as prescribed by a medical practitioner, purchased by a person suffering from diabetes qualifies. The CRA has stated that when such a person has to take sugar-content tests using test-tapes or test tablets and a medical practitioner has prescribed this diagnostic procedure, the tapes or tablets qualify as devices or equipment under 118.2(2)(m) and Part LVII of the Regulations

118.2(2)(k), (n), S1-F1-C1 (paras 1.90-1.91)

Diabetics (scales) No The cost of various kinds of scales, which diabetics frequently use for weighing themselves or their food

S1-F1-C1 (paras 1.91, 1.131)

Diapers Yes Diapers required by the patient by reason of incontinence caused by illness, injury or affliction qualify; a prescription is not required. Amounts paid to a diaper service do not qualify

118.2(2)(i.1), CRA Guide RC4064, S1-F1-C1 (para

1.87)

Diathermy Yes Amount paid to a medical practitioner or a licensed private hospital

118.2(2)(a), CRA Guide RC4064

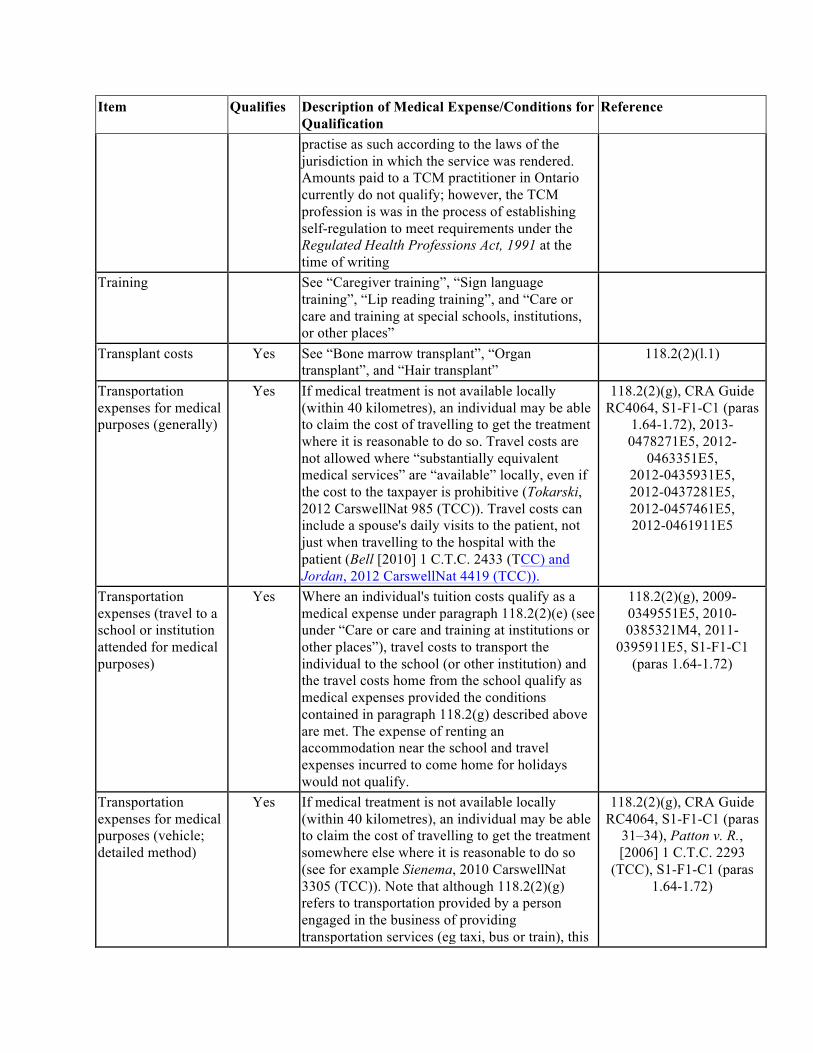

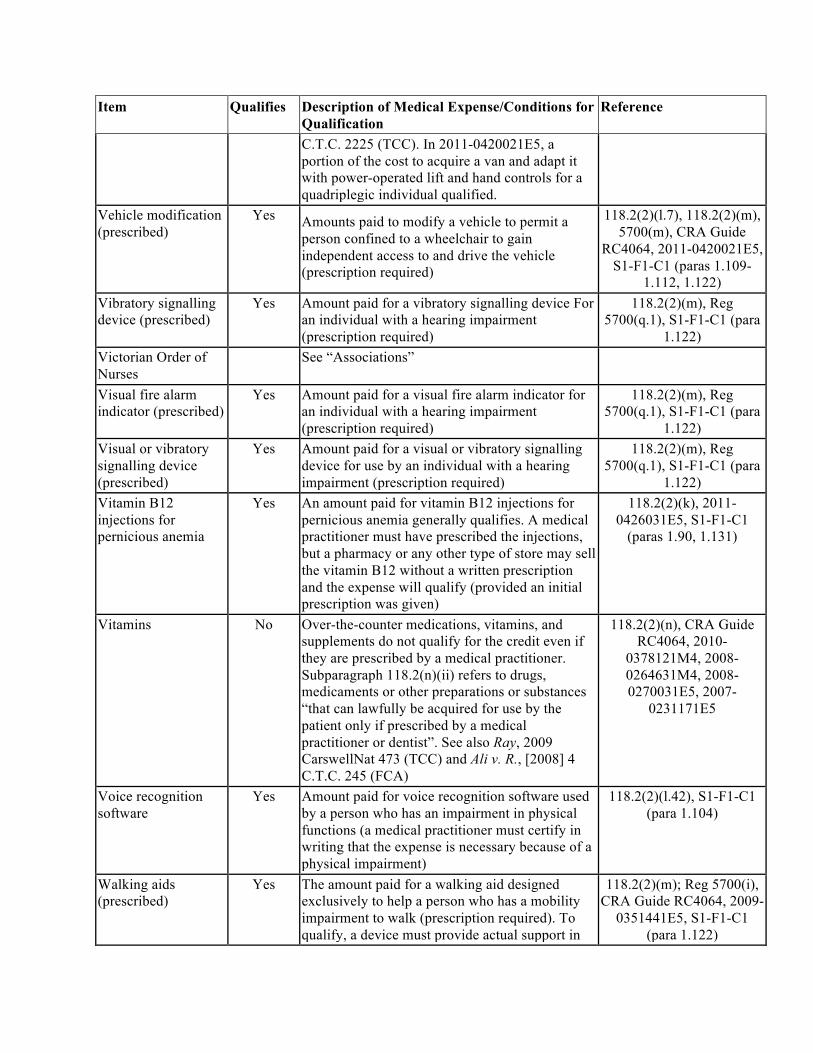

Dietician Yes Payments to a dietician would not qualify as eligible medical expenses unless the amounts were paid for “medical services” performed by a medical practitioner authorized to practise as such according to the laws of the jurisdiction in which the service was rendered (the CRA's view is that a person is authorized by the laws of a jurisdiction to act as a medical practitioner if there is specific legislation that enables, permits or empowers a person to perform medical services and generally, such specific legislation provides for the licensing or certification of the practitioner as well as for the establishment of a governing body (eg, a college or board) with the authority to determine competency, enforce discipline and set basic standards of conduct)

118.2(2)(a), 2009-0337771E5, S1-F1-C1

(paras 1.20-1.23)

Disposable briefs Yes Amounts paid for disposable briefs required by the patient by reason of incontinence caused by

118.2(2)(i.1), S1-F1-C1 (para 1.87)

Item Qualifies Description of Medical Expense/Conditions for Qualification

Reference

illness, injury or affliction; a prescription is not required

Doctor Yes Amounts paid to a medical practitioner (meaning discussed in CRA Guide RC4064 and S1-F1-C1 (paras 20-23) for medical services

118.2(2)(a)

Dogs (guide) See “Guide dogs” Driveway alterations Yes Reasonable amounts paid to alter the driveway of

the main residence of a person who has a severe and prolonged mobility impairment to allow easier access to a bus qualify. Also, the CRA has stated that “reasonable expenses relating to alterations to the driveway would also qualify under this provision if they facilitate access to whatever mode of transportation, bus or otherwise, that is ordinarily used by the patient.” However, the cost of installing a walkway would generally not qualify as an eligible medical expense (see 2011-0404911E5).

118.2(2)(l.6), 2011-0404911E5, S1-F1-C1

(para 1.108)

Driving lessons for disabled person

No The cost of tuition fees and exams for driver training for a disabled individual

2007-0244411E5

Drugs bought under Health Canada's Special Access Program

Yes Drugs and medical devices bought under Health Canada's Special Access Program (ie, amounts paid for drugs and medical devices that have not been approved for use in Canada if they were purchased under this program). Visit Health Canada's Web site at www.mdall.ca

118.2(2)(s), (t), S1-F1-C1 (para 1.137)

Drugs, medicaments or other preparations or substances (over-the-counter)

No Over-the-counter medications, vitamins, and supplements, even if prescribed by a medical practitioner. Subparagraph 118.2(n)(ii) refers to drugs, medicaments or other preparations or substances “that can lawfully be acquired for use by the patient only if prescribed by a medical practitioner or dentist”. See also 2010-0362941E5, 2008-0264631M4, 2008-0270031E5 and 2007-0231171E5

CRA Guide RC4064, 118.2(2)(n), S1-F1-C1

(paras 1.123-1.125)

Drugs, medicaments or other preparations or substances (prescribed)

Yes Amounts paid for drugs, medicaments or other preparations or substances that are manufactured, sold or represented for use in the diagnosis, treatment or prevention of a disease, disorder or abnormal physical state, or its symptoms, or in restoring, correcting or modifying an organic function qualify for the credit if a medical practitioner or dentist prescribed the medication and the medication is purchased from a pharmacist who recorded the prescription in a prescription record. Additionally, such amounts also qualify where they are available without a

118.2(2)(n), S1-F1-C1 (paras 1.123-1.127), Reg

5701

Item Qualifies Description of Medical Expense/Conditions for Qualification

Reference

prescription and a medical practitioner or dentist has prescribed the medication for the patient and the medication is only available with the intervention of a medical practitioner (eg a pharmacist)

Elastic support hose (prescribed)

Yes Amount paid for elastic support hose designed exclusively to relieve swelling caused by chronic lymphedema (prescription required)

118.2(2)(m), Reg 5700(u), S1-F1-C1 (para 1.122)

Elective medical procedures performed by a medical practitioner

Depends For expenses incurred after March 4, 2010, expenses incurred for purely cosmetic procedures no longer qualify for the credit (unless required for medical or reconstructive purposes). See also “Cosmetic surgery”

2006-0180991M4, 118.2(2.1), S1-F1-C1 (paras 1.143-1.146)

Electric breast pump No Purchase of an electric breast pump 2007-0248701E5 Electric shock treatments (prescribed)

Yes Amount paid for electric shock treatments (prescription required)

CRA Guide RC4064, 118.2(2)(a)

Electrocardiograms (prescribed)

Yes Amount paid in respect of electrocardiogram tests not covered by provincial health insurance (prescription required)

118.2(2)(o), CRA Guide RC4064

Electrolysis Depends Amounts paid to a medical practitioner for electrolysis

CRA Guide RC4064, S1-F1-C1 (paras 1.143-1.146)

Electronic bone healing device (prescribed)

Yes Amount paid for electronic bone healing device (prescription required)

118.2(2)(m), Reg 5700(z.2), CRA Guide

RC4064, S1-F1-C1 (para 1.122)

Electronic speech synthesizer (prescribed)

Yes Amount paid for a speech synthesizer (electronic) that enables a mute individual to communicate by use of a portable keyboard (prescription required)

118.2(2)(m), Reg 5700(p), S1-F1-C1 (para 1.122)

Electrotherapy device (prescribed)

Yes Amount paid for an electrotherapy device designed to be used by an individual with a medical condition or by an individual who has a severe mobility impairment (prescription required)

118.2(2)(m), Reg 5700(z.2), S1-F1-C1 (para

1.122)

Elevators or lifts (power-operated) (prescribed)

Yes Amount paid for elevators or lifts designed exclusively for use by a person with an impairment to allow them to access different levels of a building, enter or leave a vehicle, or place a wheelchair on or in a vehicle (prescription required)

118.2(2)(m), Reg 5700(m), CRA Guide RC4064, S1-

F1-C1 (para 1.122)

Environmental control system (electronic or computerized) (prescribed)

Yes Amount paid for environmental control system designed exclusively for the use of an individual with a severe and prolonged mobility restriction (prescription required) (including the basic computer system used by a person with a mobility impairment)

118.2(2)(m), Reg 5700(t), CRA Guide RC4064, S1-

F1-C1 (para 1.122)

Item Qualifies Description of Medical Expense/Conditions for Qualification

Reference

Exercise equipment (prescribed)

No Amount paid for exercise equipment that was prescribed by a licensed medical practitioner

2010-0385911E5, 2011-0402881E5

External breast prosthesis (prescribed)

Yes Amount paid for an external breast prosthesis prescribed by a medical practitioner and that is required because of a mastectomy (prescription required). However, the cost of undergarments used to hold the prosthesis in place would not qualify (2012-0436991E5).

118.2(2)(m), Reg 5700(j), S1-F1-C1 (para 1.122)

Extremity pump (prescribed)

Yes Amount paid for an extremity pump designed exclusively to relieve swelling caused by chronic lymphedema (prescription required)

118.2(2)(m), Reg 5700(u), S1-F1-C1 (para 1.122)

Eyeglasses (prescribed)

Yes The cost of eyeglasses qualifies as a medical expense under 118.2(2)(j), including the cost of both the frames and lenses (prescription required from a medical practitioner or optometrist). The CRA has expressed the view that sunglasses prescribed by an optometrist to treat photosensitivity, which causes an individual to suffer from headaches caused by the sun or bright lighting, would not qualify for the credit (2003-0046081E5). The sunglasses in the particular situation were purchased from a retail story and were not prescription sunglasses

118.2(2)(j), S1-F1-C1 (para 1.89)

Eyelid surgery Depends For expenses incurred after March 4, 2010, expenses incurred for purely cosmetic procedures no longer qualify for the credit (unless required for medical or reconstructive purposes). See also “Cosmetic surgery”

118.2(2.1), 2004-0078231I7, S1-F1-C1 (paras 1.143-1.146)

Feeding tube No Feeding tube insertion and an accompanying apparatus

2007-0220531E5

Fertility treatments Yes The cost of fertility treatments, including artificial insemination and fertility medications, qualifies as a medical expense.

118.2(2)(a), (n), 2010-0381401E5, S1-F1-C1

(para 1.130) Fitness club fees See “Athletic or fitness club fees” Full-time attendant care

See “Attendant care in a self-contained domestic establishment (full-time)”, “Attendant care (full-time at a nursing home; patient lacks normal mental capacity)”, “Attendant care (patient qualifies for the disability credit)”, and “Attendant care at a retirement home, home for seniors, or other institution”

Furnace Yes Electric or sealed combustion furnace acquired to replace a furnace that is neither of these types of furnace where the replacement is necessary solely because of a severe chronic respiratory ailment or

118.2(2)(m), Reg 5700(c.2), S1-F1-C1 (para

1.122)

Item Qualifies Description of Medical Expense/Conditions for Qualification

Reference

a severe chronic immune system disregulation and the replacement is prescribed by a medical practitioner

Glasses (prescribed) See “Eyeglasses” Gluten-free food Yes For a patient who has celiac disease, the

incremental cost of acquiring gluten-free food products as compared to the cost of comparable non-gluten-free food products generally qualifies. Such costs qualify if the patient has been certified in writing by a medical practitioner to be a person who, because of that disease, requires a gluten-free diet. For a list of qualifying expenses, see http://www.cra-arc.gc.ca/tx/ndvdls/tpcs/clc-eng.html

118.2(2)(r), 2010-0403181E5, 2011-

0427621E5, S1-F1-C1 (para 1.136)

Group home See “Attendant care provided at a group home in Canada”

Guide dogs Yes The purchase of a guide dog for a blind individual from an institution that trains such dogs, as well as related expenses (for a list of qualifying expenses, see under “Animals”)

118.2(2)(l), S1-F1-C1 (para 1.92)

Hair transplant surgery

Depends For expenses incurred after March 4, 2010, expenses incurred for purely cosmetic procedures no longer qualify for the credit (unless required for medical or reconstructive purposes). See under “Cosmetic procedures”

118.2(2.1), CRA Guide RC4064, S1-F1-C1 (paras

1.143-1.146)

Hardwood floors Depends The CRA’s view is that hardwood flooring would not generally be an eligible medical expense because it would typically be expected to increase the value of a home, or because it would normally be incurred by persons without a severe and prolonged mobility impairment (S1-F1-C1 para. 1.97). However, see Sotski, 2013 CarswellNat 3360 (TCC), where the taxpayer was successful in claiming the cost of laminate flooring as a medical expense, since the court found that the new flooring did not necessarily increase the value of the home, and was installed specifically for the purpose of easing the taxpayer’s spouse’s difficulty with walking on carpeting. In this case, the taxpayer’s spouse suffered from Parkinson’s disease, arthritis, and postural problems, which made walking on carpeting difficult and unsafe (see also under “Home alterations”).

118.2(l.2), (l.21), 2009-0326721I7, 2011-

0422991E5, Hendricks, 2008 CarswellNat 3091

(TCC), Sotski, 2013 CarswellNat 3360 (TCC),

S1-F1-C1 (para 1.97)

Health Line Services No Amount paid for a personal response system CRA Guide RC4064, Mattinson, 2008

CarswellNat 84 (TCC)

Item Qualifies Description of Medical Expense/Conditions for Qualification

Reference

Health plan premiums

Yes See “Premiums paid to private health services plans (PHSP)” and www.cra.gc.ca/medical

118.2(2)(q) 2013-0480711M4, S1-F1-

C1 (paras 1.133-1.135) Health plan premiums paid by employer

Depends Health plan premiums paid by an employer and not included in employment income do not qualify; however, such amounts can qualify if included in computing employment income

118.2(3)(b), CRA Guide RC4064, S1-F1-C1 (paras

1.133-1.135)

Health programs No Cost of general health programs CRA Guide RC4064 Hearing aid (general) Yes Amount paid for a hearing aid, including the cost

of repairs, batteries, parts, moulds, creams, rental costs, and other expenses in respect of the hearing aid qualify for the credit (prescription not required). The CRA has stated that in addition to the more usual hearing aid devices, an “aid to hearing” includes: a device that produces extra-loud audible signals such as a bell, horn or buzzer; a device to permit the volume adjustment of telephone equipment above normal levels; a bone-conduction telephone receiver; and a “Cochlear” implant. When a hearing aid is incorporated into the frame of a pair of eyeglasses, both the hearing aid and the eyeglass frame qualify under 118.2(2)(i). A listening device that is acquired to alleviate a hearing impairment by eliminating or reducing sound distortions for the purpose of listening to television programs, movies, concerts, business conferences or similar events, is also considered to qualify as an “aid to hearing” under 118.2(2)(i). See also see “Vibratory signalling device” and “Visual fire alarm indicator”

118.2(2)(i), CRA Guide RC4064, 2009-0332141E5, S1-F1-C1 (paras 1.73-1.74,

1.80-1.81))

Hearing aid (service contract)

Yes Amount paid for a service contract for a cochlear implant

118.2(2)(i), 2003-0001495, S1-F1-C1 (paras 1.73-1.74)

Hearing aid (volume control feature)

Yes Amount paid for a volume control feature (additional) used by a person who has a hearing impairment (prescription required)

118.2(2)(i), CRA Guide RC4064, S1-F1-C1 (para

1.80) Hearing aid (warranty)

Yes Cost of an extended warranty for a hearing aid 118.2(2)(i), 2007-0247031E5, S1-F1-C1

(paras 1.73-1.74) Heart monitor (prescribed)

Yes Amount paid for a heart monitor including the cost of repairs and batteries (prescription required)

118.2(2)(m), Reg 5700(d), CRA Guide RC4064, S1-

F1-C1 (para 1.122) Herbal medicines See “Homeopathic medicines” and “Over-the-

counter medications” Hernia truss Yes Amount paid for a hernia truss (prescription not

required) 118.2(2)(i), S1-F1-C1

(paras 1.73-1.74)

Item Qualifies Description of Medical Expense/Conditions for Qualification

Reference

Home alterations (addition of bathroom)

No An amount paid to add a bathroom to a home is not a qualifying home renovation cost where the addition of the bathroom increases the value of the home. In Chobotar, 2009 CarswellNat 1308 (TCC), the credit was denied in respect of a specially designed bathroom for a person in a wheelchair because the bathroom increased the value of the home

Chobotar, 2009 CarswellNat 1308 (TCC),

S1-F1-C1 (paras 1.94-1.100)

Home alterations (pedestal sink)

No An amount paid for a pedestal sink 118.2(2)(l.2), (l.21), Young, 2009 CarswellNat

4364 (TCC), S1-F1-C1 (paras 1.94-1.100)

Home alterations (qualifying expenses)

Yes Amounts paid to make changes to give a person who has a severe and prolonged mobility impairment or who lacks normal physical development access to (or greater mobility or functioning within) the person's home may qualify. The costs may be incurred in building the principal residence of the person, or in renovating or altering an existing home (an RV that is used as a place of residence could be considered a home for this purpose; 2005-0133691I7). Renovation or construction expenses do not qualify unless: 1) they would not typically be expected to increase the value of the home; and 2) they would not normally be incurred by people without a severe and prolonged mobility impairment (ie, items such as hot tubs, swimming pools, and hardwood floors do not generally qualify; although, see Sotski, 2013 CarswellNat 3360 (TCC), where the taxpayer was successful in claiming the cost of laminate flooring as a medical expense, since the court found that the new flooring did not necessarily increase the value of the home, and was installed specifically for the purpose of easing the taxpayer’s spouse’s difficulty with walking on carpeting). Eligible expenses could include, for example: buying and installing outdoor or indoor ramps where stairways impede the person's mobility; enlarging halls and doorways to give the person access to the various rooms of his or her dwelling; lowering kitchen or bathroom cabinets to give the person access to them; power flush toilets; or the cost of installing a stair lift. See also 2007-0251071E5, 2009-0342581E5, 2005-0163161E5, 2007-0251071E5, 2010-0379331E5, 2011-0422991E5, Hendricks, 2008 CarswellNat 3091

118.2(2)(l.2), (l.21), CRA Guide RC4064, S1-F1-C1 (paras 1.94-1.100), Hillier

v The Queen, [2000] 3 C.T.C. 2367 (TCC)

Item Qualifies Description of Medical Expense/Conditions for Qualification

Reference

(TCC), Totten, [2005] 3 C.T.C. 2061 (TCC), Henschel, 2010 CarswellNat 1783 (TCC) and Savoy, 2011 CarswellNat 193 (TCC).

Home care services (provided by a nurse)

Yes Amount paid to a licensed nurse for home care services (ie, for private nursing care)

118.2(2)(a), CRA Guide RC4064, 2009-0332141E5

Home construction costs

See “Home Alterations”

Homeopathic services

Depends Amount paid to a medical practitioner for homeopathic services qualifies. The CRA's view is that a person is authorized by the laws of a jurisdiction to act as a medical practitioner if there is specific legislation that enables, permits or empowers a person to perform medical services and generally, such specific legislation provides for the licensing or certification of the practitioner as well as for the establishment of a governing body (eg, a college or board) with the authority to determine competency, enforce discipline and set basic standards of conduct. Homeopaths are not authorized as medical practitioners in New Brunswick (2010-0407341E5).

118.2(2)(a), CRA Guide RC4064, Herzig, [2004] 3 C.T.C. 2496 (TCC), 2009-

0337771E5, S1-F1-C1 (paras 1.20-1.23)

Homeopathic medicines

No The cost of vitamins, herbs, organic and natural foods, natural health products and bottled water not recorded by a pharmacist, even if they are prescribed by a medical practitioner (see under “Over-the-counter medications”)

118.2(2)(n), 2011-0391961E5, Ray, 2009

CarswellNat 473 (TCC), S1-F1-C1 (para 1.125)

Hospital bed Yes Amount paid for a hospital bed for an individual's use as prescribed by a medical practitioner qualifies (including such attachments thereto as may have been included in a prescription therefor). A ceragem massager bed does not qualify (Reid, 2008 CarswellNat 2069 (TCC)). Nor does a RIK Fluid Overlay mattress (2009-0318231E5) or a Sleep Country adjustable bed (Young, 2009 CarswellNat 4364 (TCC)). A Slumberland adjustable bed qualifies (Crockart, [1999] 2 C.T.C. 2409 (TCC)). Also, the cost of redesigning a bed to be a hospital bed qualifies; Vucurevich, [2000] 1 C.T.C. 3044 (TCC). The cost of an over-bed rolling table does not qualify. Also, a massage chair would not qualify; 2009-0341601E5 (See also under “Mattress”)

118.2(2)(m), Reg 5700(h), 2009-0332141E5, S1-F1-

C1 (para 1.122)

Hospitals Yes Amount paid to a public or private hospital that is designated as a hospital by the province or territory where the hospital is located

118.2(2)(a), CRA Guide RC4064 S1-F1-C1 (paras

1.24-1.30) Hot tub See “Whirlpool bath”

Item Qualifies Description of Medical Expense/Conditions for Qualification

Reference

House cleaning services

No Amounts paid for house cleaning services do not qualify. See however under “Attendant care at a retirement home, home for seniors, or other institution”. Also, see Zaffino, [2007] 5 C.T.C. 2560 (TCC) (cleaning costs allowed under paragraph 118.2(2)(b.1) (part-time attendant costs))

2009-0332141E5

Hydrotherapy Depends Amounts paid to a medical practitioner for hydrotherapy qualify. The CRA's view is that a person is authorized by the laws of a jurisdiction to act as a medical practitioner if there is specific legislation that enables, permits or empowers a person to perform medical services and generally, such specific legislation provides for the licensing or certification of the practitioner as well as for the establishment of a governing body (eg, a college or board) with the authority to determine competency, enforce discipline and set basic standards of conduct

118.2(2)(a), CRA Guide RC4064, 2009-0337771E5

Iliostomy pads Yes Amount paid for iliostomy pads (prescription not required)

118.2(2)(i), S1-F1-C1 (paras 1.73-1.74, 1.78)

Immune system disregulation or respiratory ailment (air or water filter; prescribed)

Yes Air or water filter or purifier for use by an individual who is suffering from a severe chronic respiratory ailment or a severe chronic immune system disregulation to cope with or overcome that ailment or disregulation (prescription required)

118.2(2)(m), Reg 5700(c.1), S1-F1-C1 (para

1.122)

Immune system disregulation or respiratory ailment (electric or sealed combustion furnace)

Yes Electric or sealed combustion furnace acquired to replace a furnace that is neither an electric furnace nor a sealed combustion furnace where the replacement is necessary solely because of a severe chronic respiratory ailment or a severe chronic immune system disregulation and the replacement is prescribed by a medical practitioner

118.2(2)(m), Reg 5700(c.2), S1-F1-C1 (para

1.122)

Incontinence Yes Amounts paid for catheters and catheter trays required by the patient by reason of incontinence caused by illness, injury or affliction (including catheter trays, tubing, or other products required for incontinence caused by illness, injury, or affliction); a prescription is not required. Bed clothing, disposable gloves for caregivers and body ointments do not qualify for the credit.

118.2(2)(i.1), 2010-0359861E5, S1-F1-C1

(paras 1.87-1.88)

Inductive coupling osteogenesis stimulator (prescribed)

Yes Amount paid for an inductive coupling osteogenesis stimulator for treating non-union of fractures or aiding in bone fusion (prescription required)

118.2(2)(m), Reg 5700(v), S1-F1-C1 (para 1.122)

Item Qualifies Description of Medical Expense/Conditions for Qualification

Reference

Infants (SIDS device) Yes Amount paid for a device designed to be attached to infants diagnosed as being prone to sudden infant death syndrome in order to sound an alarm if the infant ceases to breathe and that is for the infant's use as prescribed by a medical practitioner (a medical practitioner must certify in writing that the infant is prone to sudden infant death syndrome)

118.2(2)(m), Reg 5700(r), S1-F1-C1 (para 1.122)

Infusion pump (prescribed)

Yes Amount paid for an Infusion pump, including the cost of disposable peripherals used in the treatment of diabetes (prescription required). See also “Diabetics”

118.2(2)(m), Reg 5700(s), S1-F1-C1 (para 1.122)

Insulin Yes An amount paid for insulin and insulin substitutes generally qualifies. A medical practitioner must have prescribed the insulin, but a pharmacy or any other type of store may sell the insulin without a written prescription and the expense will qualify (ie, provided an initial prescription was given). See also “Diabetics”

118.2(2)(k), S1-F1-C1 (paras 1.90-1.91, 1.126)

Insurance See “Travel medical insurance” Interest (on bank loan)

No Interest expense on a bank loan obtained to finance a medical or dental procedure does not qualify because it is paid to a bank instead of a medical practitioner, dentist, nurse, public hospital, or licensed private hospital

2011-0416651I7

In-vitro fertilization procedure (prescribed)

Yes Amount paid in respect of in-vitro fertilization procedure not covered by provincial health insurance (prescription required). Qualifying amounts include daily ultrasound and blood tests once the in-vitro procedure has begun, sperm freezing and egg freezing and storage, but do not include amounts paid to cover the donor's costs. Travel costs incurred for an IVF procedure outside of Canada will likely qualify (2011-0396951E5).

S1-F1-C1 (para 1.130), CRA Guide RC4064, 118.2(2)(a), (o), 2011-

0396951E5, 2011-0415601E5, 2011-0416451E5, 2011-0396951E5, 2009-

0311051E5

Iontophoresis device (prescribed)

Yes Costs for an iontophoresis device that has been prescribed by a doctor for the treatment of hyperhidrosis (excessive sweating)

118.2(2)(m), Reg 5700 (z.2), 2011-0391861E5, S1-

F1-C1 (para 1.122) Iron lung Yes Cost of an iron lung, including the cost of repairs,

a portable chest respirator that performs the same function, a continuous positive airway pressure machine, and parts and other expenses in respect of (prescription not required)

118.2(2)(i), CRA Guide RC4064, S1-F1-C1 (paras

1.73-1.75)

Kidney machine (artificial)

Yes Amount paid for a kidney machine, including the cost of repairs, maintenance, and supplies; additions, renovations, or alterations to a home

118.2(2)(i), CRA Guide RC4064, S1-F1-C1 (paras

1.73-1.74, 1.82-1.86)

Item Qualifies Description of Medical Expense/Conditions for Qualification

Reference